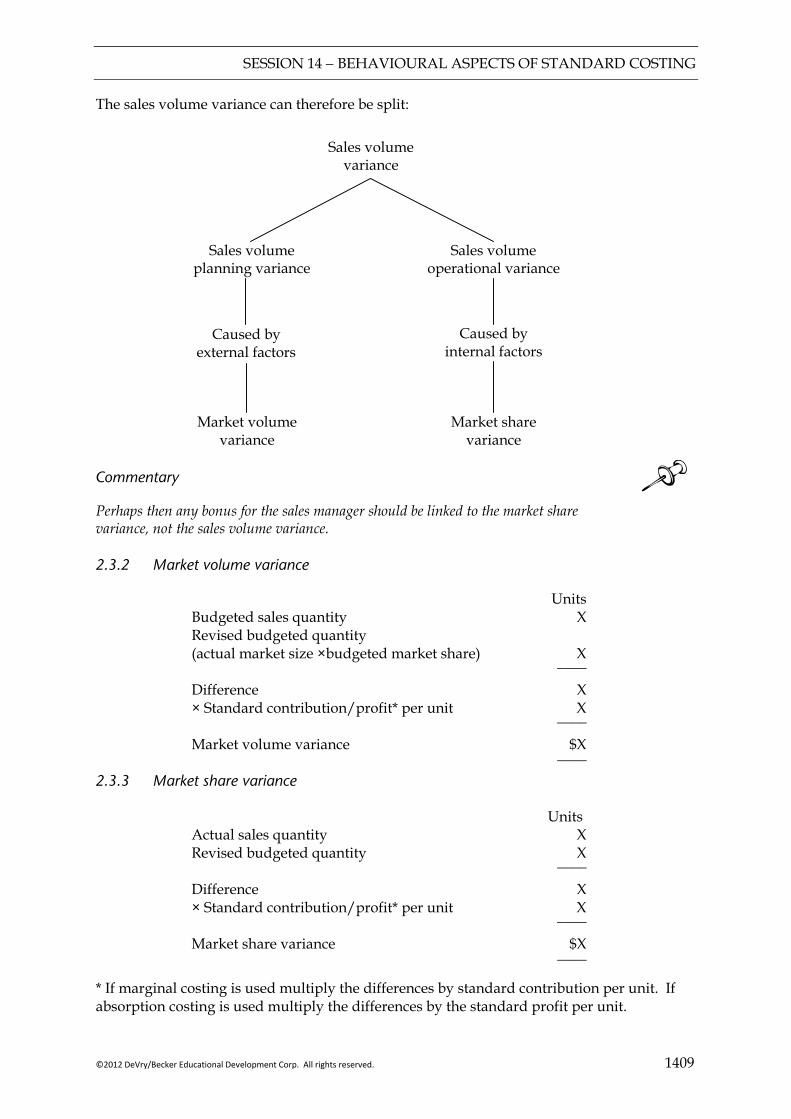

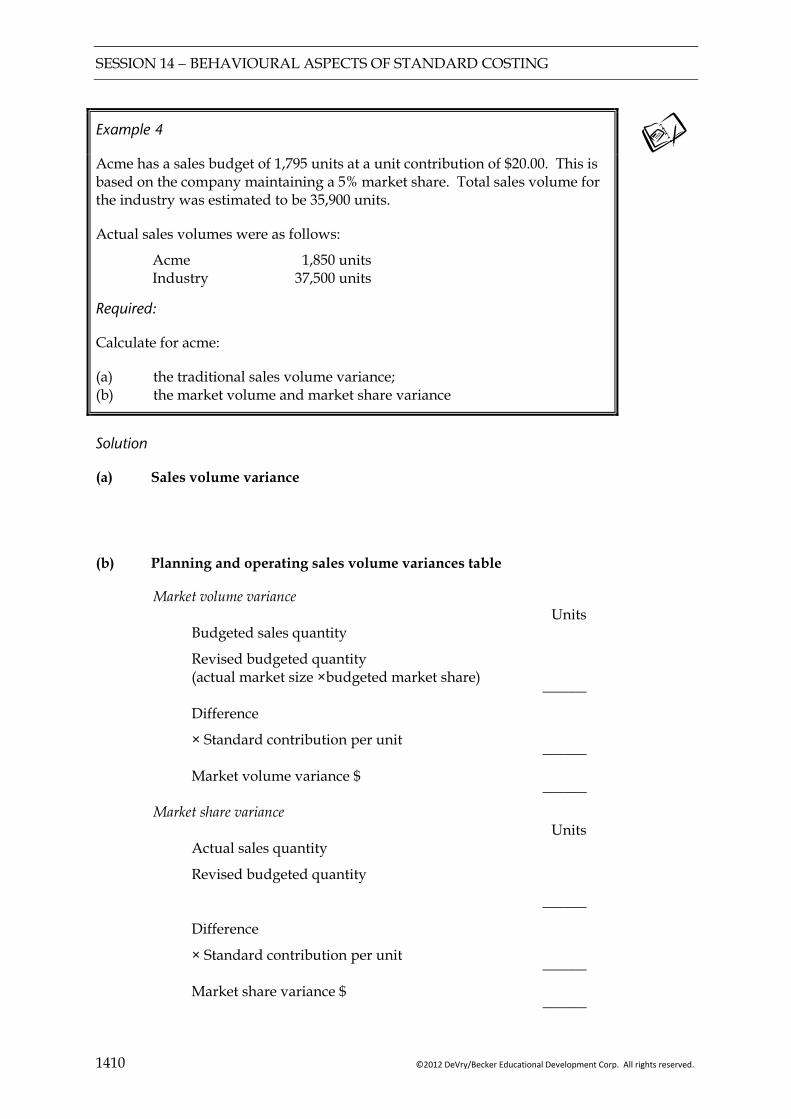

2012 EDITION | Study System ® ATC International became a part of Becker Professional Education in 2011. ATC International has 20 years of experience providing lectures and learning tools for ACCA Professional Qualifications. Together, Becker Professional Education and ATC International offer ACCA candidates high quality study materials to maximize their chances of success. ACCA Paper F5 | PERFORMANCE MANAGEMENT

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2012 EDITION | Study System

®

®

ATC International became a part of Becker

Professional Education in 2011. ATC International

has 20 years of experience providing lectures

and learning tools for ACCA Professional

Qualifications. Together, Becker Professional

Education and ATC International offer ACCA

candidates high quality study materials to maximize

their chances of success.

ACCA Paper F5 | PERFORMANCE MANAGEMENT

In 2011 Becker Professional Education, a global leader in professional education, acquired ATC

International. ATC International has been developing study materials for ACCA for 20 years, and

thousands of candidates studying for the ACCA Qualification have succeeded in their professional

examinations through its Platinum and Gold ALP training centers in Central and Eastern Europe and

Central Asia.*

Becker Professional Education-ATC International has also been awarded ACCA Approved Learning

Partner-content Gold Status for materials for the Diploma in International Financial Reporting (DipIFR).

Nearly half a million professionals have advanced their careers through Becker Professional Education's

courses. Throughout its more than 50 year history, Becker has earned a strong track record of student

success through world-class teaching, curriculum and learning tools.

Together with ATC International, we provide a single destination for individuals and companies in need of

global accounting certifications and continuing professional education.

*Platinum – Moscow, Russia and Kiev, Ukraine. Gold – Almaty, Kazakhstan

BECKER PROFESSIONAL EDUCATION’S ACCA STUDY MATERIALS

All of Becker’s materials are authored by experienced ACCA lecturers and are used in the delivery of

classroom courses.

Study System*: Provides comprehensive coverage of the core syllabus areas and is designed to be

used both as a reference text and as part of integrated study to provide you with the knowledge, skill and

confidence to succeed in your ACCA examinations. It also includes a bank of practice questions relating

to each topic covered.

Revision Question Bank*: Exam style and standard questions with model answers to give guidance in

final preparation.

Revision Essentials: A condensed, easy-to-use aid to revision containing essential technical content,

examiners' insights and exam guidance.

* ACCA Gold Approved Learning Partner – content

®

LICENSE AGREEMENT DO NOT USE ANY OF THESE MATERIALS UNTIL YOU HAVE READ THIS AGREEMENT CAREFULLY. IF YOU USE ANY OF THE MATERIALS, YOU ARE AGREEING AND CONSENTING TO BE BOUND BY AND ARE BECOMING A PARTY TO THIS AGREEMENT. These materials are NOT for sale and are not being sold to you. You may NOT transfer these materials to any other person or permit any other person to use these materials. You may only acquire a license to use these materials and only upon the terms and conditions set forth in this license agreement. Read this agreement carefully before using these materials. Do not use these materials unless you agree with all terms of this agreement. NOTE: You may already be a party to this agreement if you are registered for a Becker Professional Education® ACCA course. (the "Course"), or if you placed an order for these materials on-line or using a printed form that included this license agreement. Please review the termination section regarding your rights to terminate this license agreement and receive a refund of your payment. Grant: Upon your acceptance of the terms of this agreement, in a manner set forth above, DeVry/Becker Educational Development Corp. ("Becker") hereby grants to you a non-exclusive, revocable, non-transferable, non-sublicensable, limited license to use the materials, including eBooks ("Materials"), as defined below, and any Materials to which you are granted access as a result of your license to use the Materials and/or in connection with the Course on the following terms: You may: • use the Materials for the Course, for preparation for one or more parts of the ACCA exam (the "Exam"), and/or for your studies relating to the

subject matter covered by the Course and/or the Exam; and • take electronic and/or handwritten notes during the Program; provided, however, that all notes taken by you during the Course that relate to the

subject matter of the Course are and shall remain Materials subject to the terms of this agreement. You may not: • use the Materials for any purpose other than as expressly permitted above; • make copies of all or any part of the Materials; • rent, lease, license, lend, or otherwise transfer or provide (by gift, sale, or otherwise) all or any part of the Materials to anyone; • permit the use of all or any part of the Materials by anyone other than you; or • create derivative works of the Materials. Materials: Materials means and includes any and all written and electronic materials provided to you in connection with the Course and/or otherwise provided to you and/or to which you are otherwise granted access by Becker (directly or indirectly) in connection with your license of the accompanying materials and/or the Course, and shall include notes you take (by hand, electronically, digitally, or otherwise) during the Course relating to the subject matter of the Course. Materials may include, but are not limited to, one or more hardcover workbooks and/or eBooks (books in electronic format) for each of the subject matter areas of the Exam. Title: Becker is and will remain the owner of all title, ownership rights, intellectual property, and all other rights and interests in and to the Materials and all other Materials that are subject to the terms of this agreement. The Materials are protected by the copyright laws of the United States and international copyright laws and treaties. Termination: This license shall terminate the earlier of: (i) ten (10) business days after notice to you of non-payment of or default on any payment due Becker which has not been cured within such 10 day period; or (ii) immediately if you fail to comply with any of the limitations described above. On termination of this license in its entirety, you must destroy all copies of the Materials, including, but not limited to, any archival copies you may have made. On termination of this license with respect to a particular Material, you must destroy such Material, including, but not limited to, any archival copies you may have made. Your Limited Right to Terminate this License and Receive a Refund: You may terminate this license in accordance with Becker's refund policy as provided at www.beckeratci.com No Warranty: BECKER MAKES NO WARRANTIES, EXPRESS OR IMPLIED, WITH RESPECT TO THE PRINTED MATERIALS, THEIR MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE AND NO WARRANTY OF NONINFRINGEMENT OF THIRD PARTIES' RIGHTS. NO DEALER, AGENT OR EMPLOYEE OF BECKER IS AUTHORIZED TO MAKE ANY MODIFICATIONS, EXTENSIONS OR ADDITIONS TO THIS NO WARRANTY. Exclusion of Damages: UNDER NO CIRCUMSTANCES AND UNDER NO LEGAL THEORY, TORT, CONTRACT, OR OTHERWISE, SHALL BECKER OR ITS DIRECTORS, OFFICERS, EMPLOYEES OR AGENTS, BE LIABLE TO YOU OR ANY OTHER PERSON FOR ANY CONSEQUENTIAL, INCIDENTAL, INDIRECT, PUNITIVE, EXEMPLARY OR SPECIAL DAMAGES OF ANY CHARACTER, INCLUDING, WITHOUT LIMITATION, DAMAGES FOR LOSS OF GOODWILL, WORK STOPPAGE, COMPUTER FAILURE OR MALFUNCTION OR ANY AND ALL OTHER DAMAGES OR LOSSES, OR FOR ANY DAMAGES IN EXCESS OF BECKER'S LIST PRICE FOR A LICENSE TO THE MATERIALS, EVEN IF BECKER SHALL HAVE BEEN INFORMED OF THE POSSIBILITY OF SUCH DAMAGES, OR FOR ANY CLAIM BY ANY OTHER PARTY. Indemnification and Remedies: You agree to indemnify and hold Becker and its employees, representatives, agents, attorneys, affiliates, directors, officers, members, managers and shareholders harmless from and against any and all claims, demands, losses, damages, penalties, costs or expenses (including reasonable attorneys' and expert witness' fees and costs) of any kind or nature, arising from or relating to any violation, breach or nonfulfillment by you of any provision of this license. If you are obligated to provide indemnification pursuant to this provision, Becker may, in its sole and absolute discretion, control the disposition of any indemnified action at your sole cost and expense. Without limiting the foregoing, you may not settle, compromise or in any other manner dispose of any indemnified action without the consent of Becker. If you breach any material term of this license, Becker shall be entitled to equitable relief by way of temporary and permanent injunction and such other and further relief as any court with jurisdiction may deem just and proper. Severability of Terms: If any term or provision of this license is held invalid or unenforceable by a court of competent jurisdiction, such invalidity shall not affect the validity or operation of any other term or provision and such invalid term or provision shall be deemed to be severed from the license. This license agreement may only be modified by written agreement signed by both parties. Governing Law: This license agreement shall be governed and construed according to the laws of the state of Illinois, save for any choice of law provisions. Any legal action regarding this Agreement shall be brought only in the U.S. District Court for the Northern District of Illinois, or another court of competent jurisdiction in DuPage County, Illinois, and all parties hereto consent to jurisdiction and venue in DuPage County, Illinois. ACCA and Chartered Certified Accountants are registered trademarks of The Association of Chartered Certified Accountants and may not be used without their express, written permission. Becker Professional Education is a registered trademark of DeVry/Becker Educational Development Corp. and may not be used without its express, written permission.

©2012 DeVry/Becker Educational Development Corp. All rights reserved.

ACCA

PAPER F5

PERFORMANCE MANAGEMENT

STUDY SYSTEM

JUNE 2012

®

©2012 DeVry/Becker Educational Development Corp. All rights reserved.

No responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication can be accepted by the author, editor or publisher.

This training material has been published and prepared by Accountancy Tuition Centre (International Holdings) Limited

16 Elmtree Road Teddington TW11 8ST United Kingdom.

Copyright ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

No part of this training material may be translated, reprinted or reproduced or utilised in any form either in whole or in part or by any electronic, mechanical or other means, now known or hereafter invented, including photocopying and recording, or in any information storage and retrieval system. Request for permission or further information should be addressed to the Permissions Department, DeVry/Becker Educational Development Corp.

.

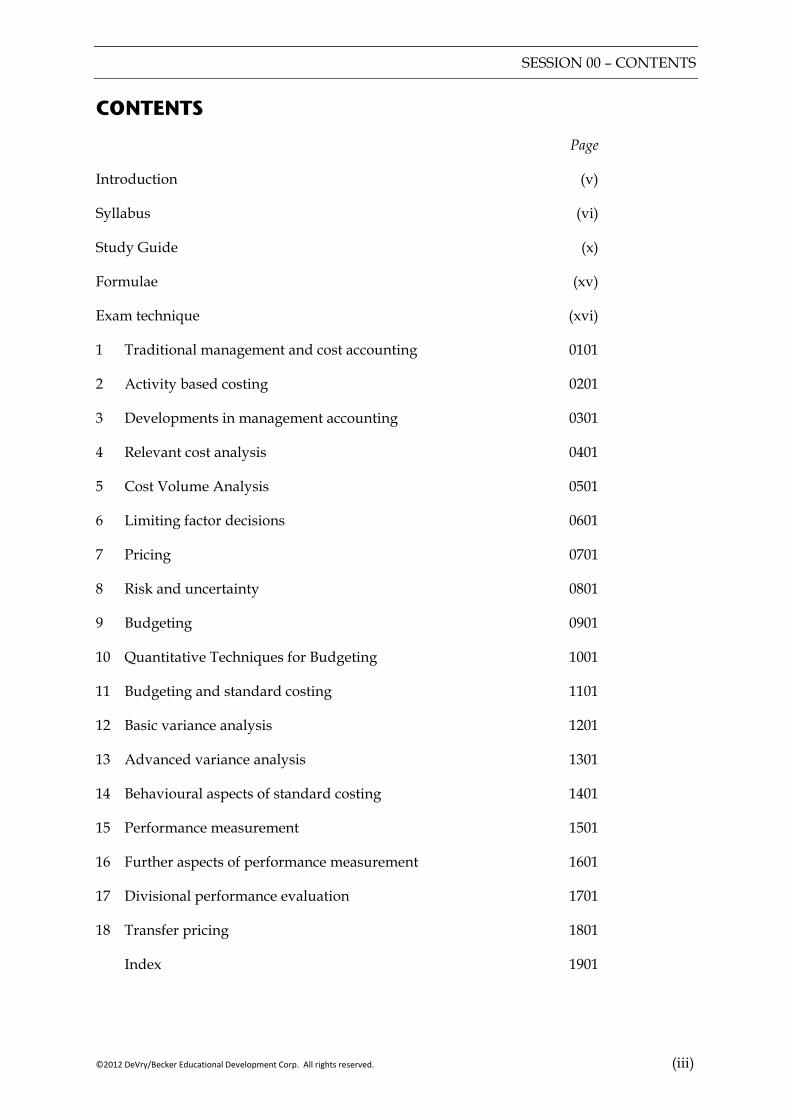

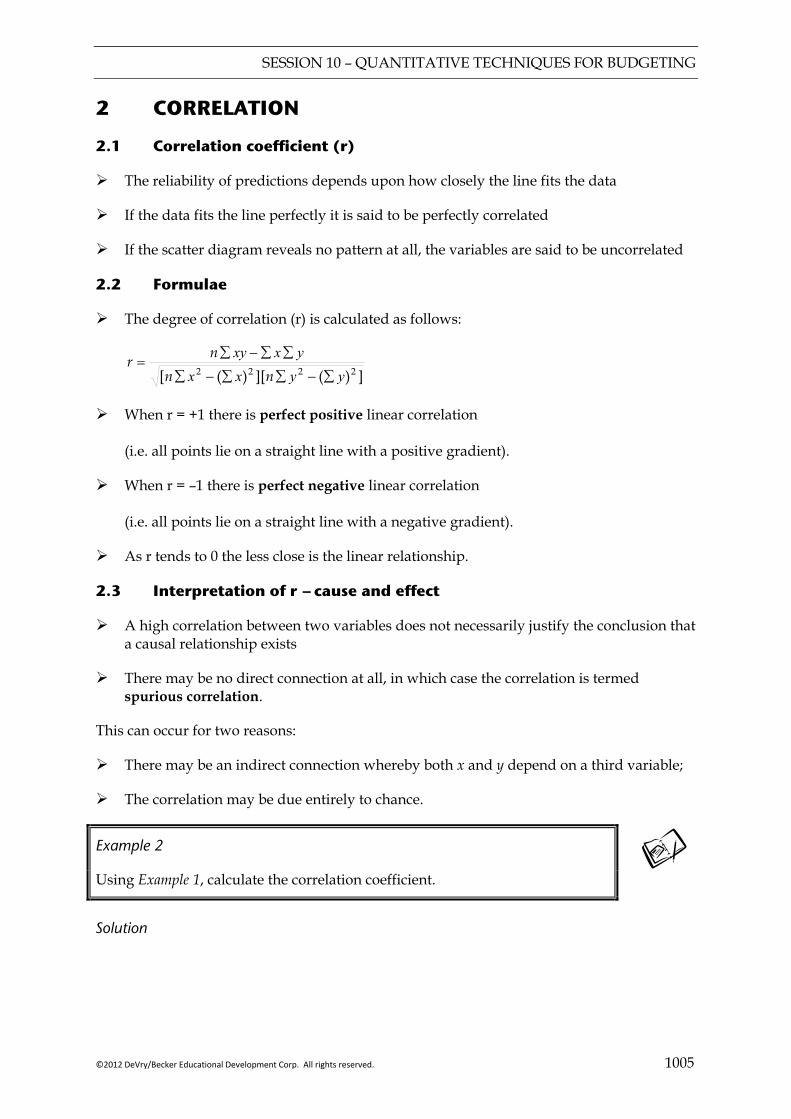

SESSION 00 – CONTENTS

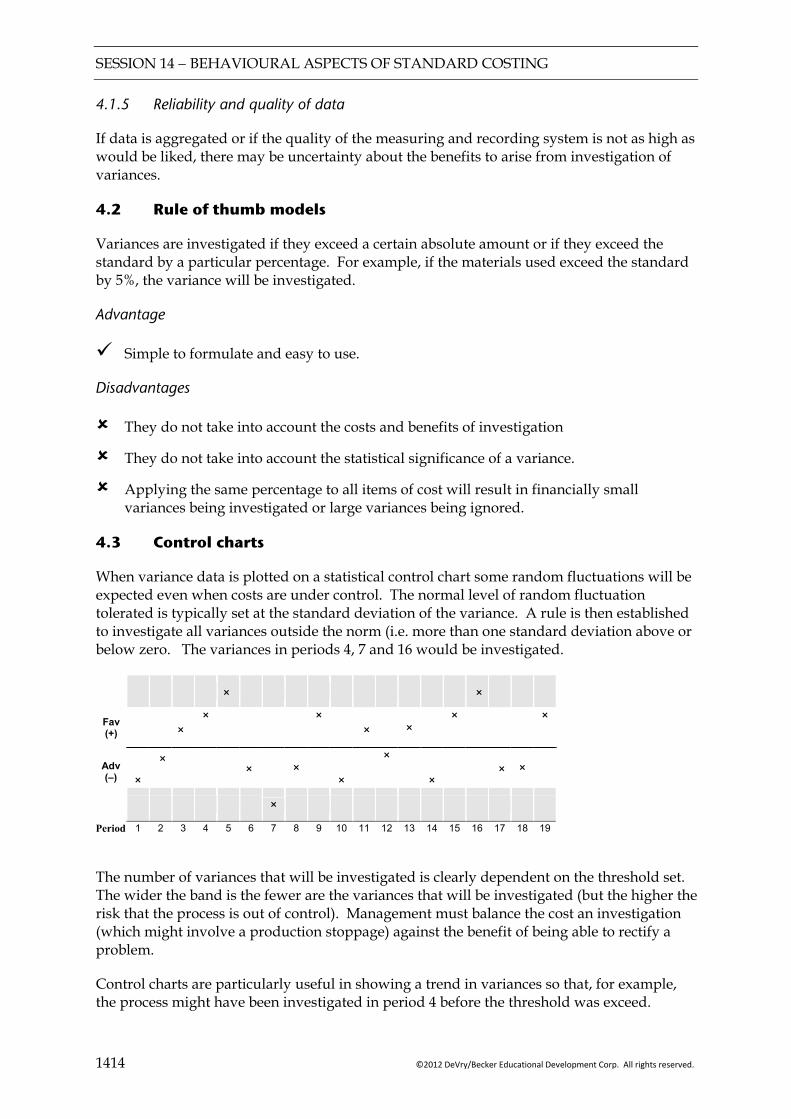

©2012 DeVry/Becker Educational Development Corp. All rights reserved. (iii)

CONTENTS

Page

Introduction (v)

Syllabus (vi)

Study Guide (x)

Formulae (xv)

Exam technique (xvi)

1 Traditional management and cost accounting 0101

2 Activity based costing 0201

3 Developments in management accounting 0301

4 Relevant cost analysis 0401

5 Cost Volume Analysis 0501

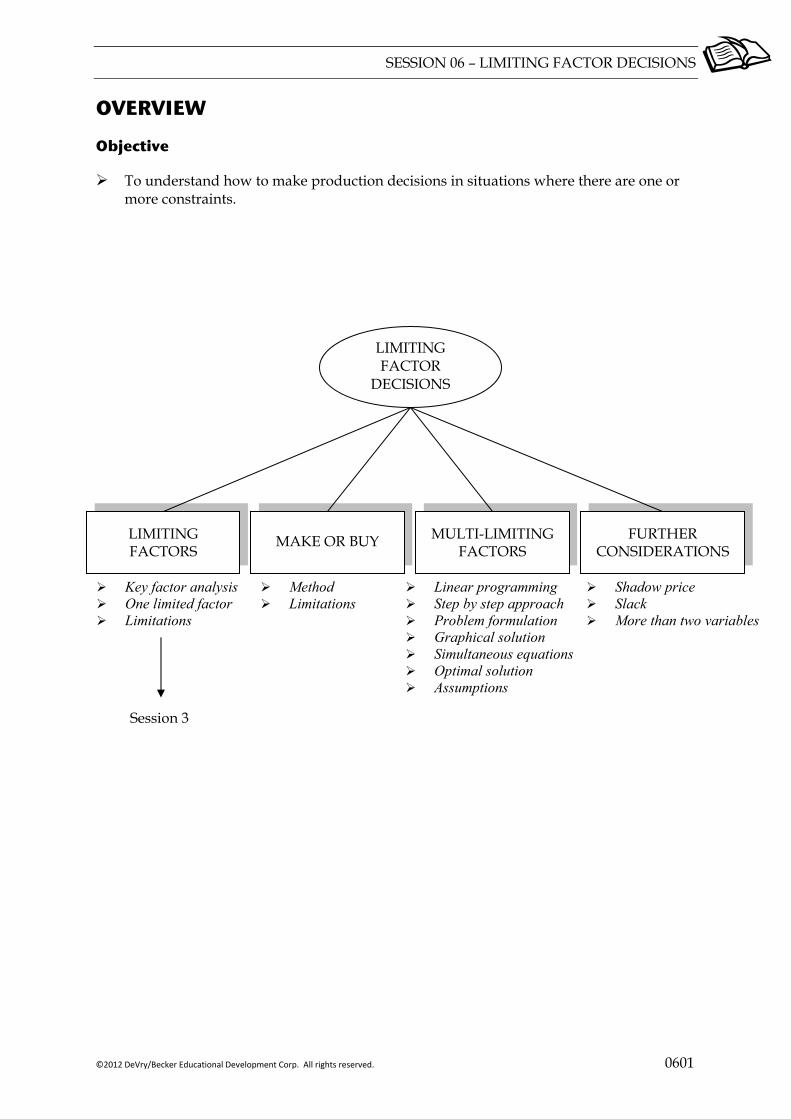

6 Limiting factor decisions 0601

7 Pricing 0701

8 Risk and uncertainty 0801

9 Budgeting 0901

10 Quantitative Techniques for Budgeting 1001

11 Budgeting and standard costing 1101

12 Basic variance analysis 1201

13 Advanced variance analysis 1301

14 Behavioural aspects of standard costing 1401

15 Performance measurement 1501

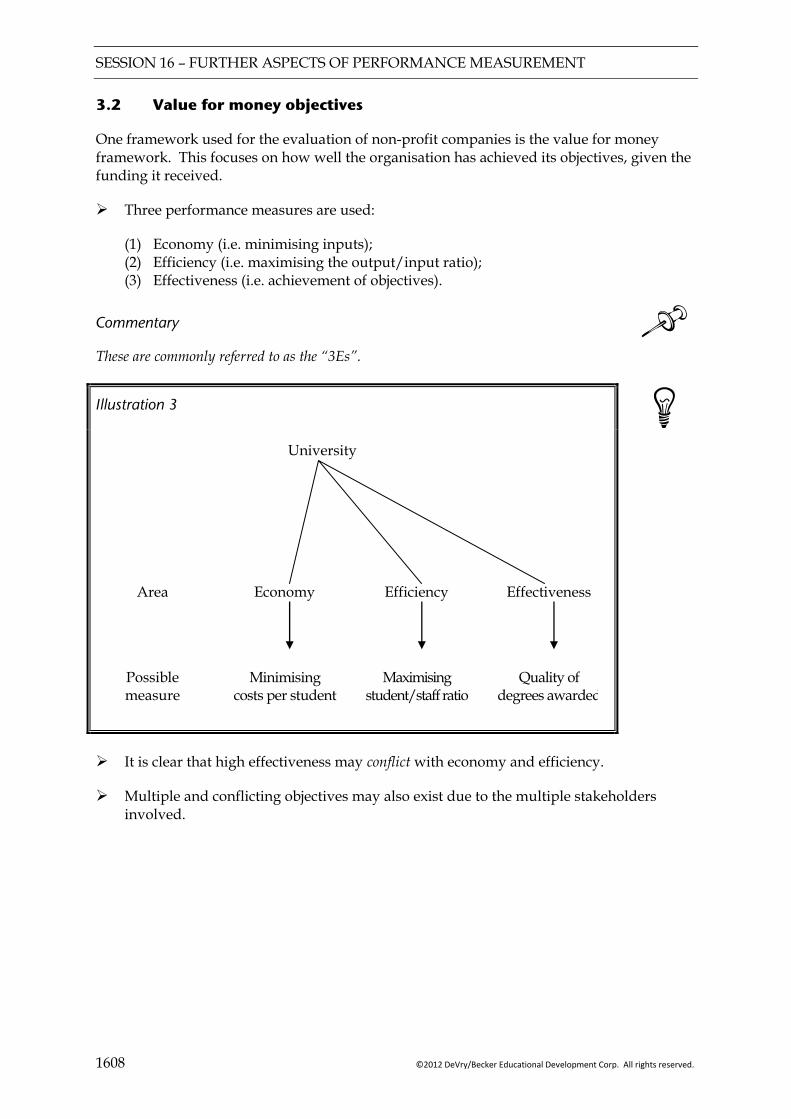

16 Further aspects of performance measurement 1601

17 Divisional performance evaluation 1701

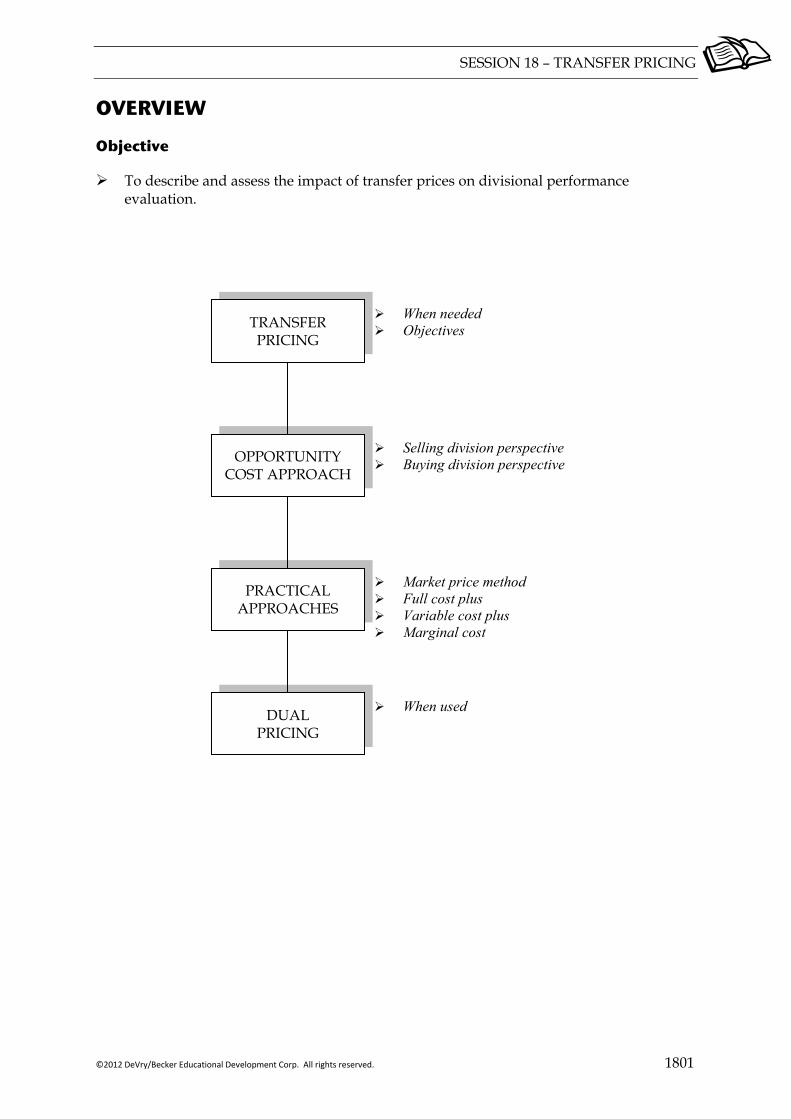

18 Transfer pricing 1801

Index 1901

SESSION 00 – CONTENTS

(iv) ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

SESSION 00 – INTRODUCTION

©2012 DeVry/Becker Educational Development Corp. All rights reserved. (v)

Introduction

This Study System has been specifically written for the Association of Chartered Certified Accountants fundamentals level examination, Paper F5 Performance Management.

It provides comprehensive coverage of the core syllabus areas and is designed to be used both as a reference text and interactively with the ATC Learning System to provide you with the knowledge, skill and confidence to succeed in your ACCA studies.

About the author: Nick Ryan is ATC International’s lead tutor in performance management and has more than 10 years’ experience in delivering ACCA exam-based training.

How to use this Study System

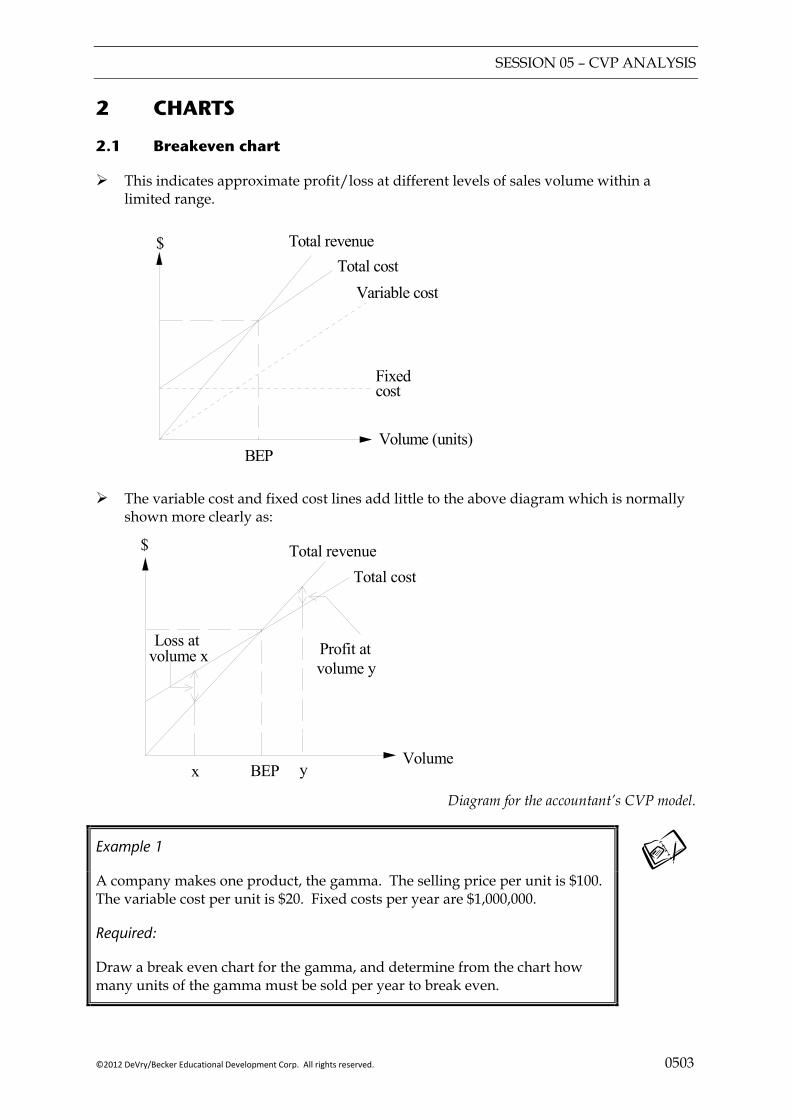

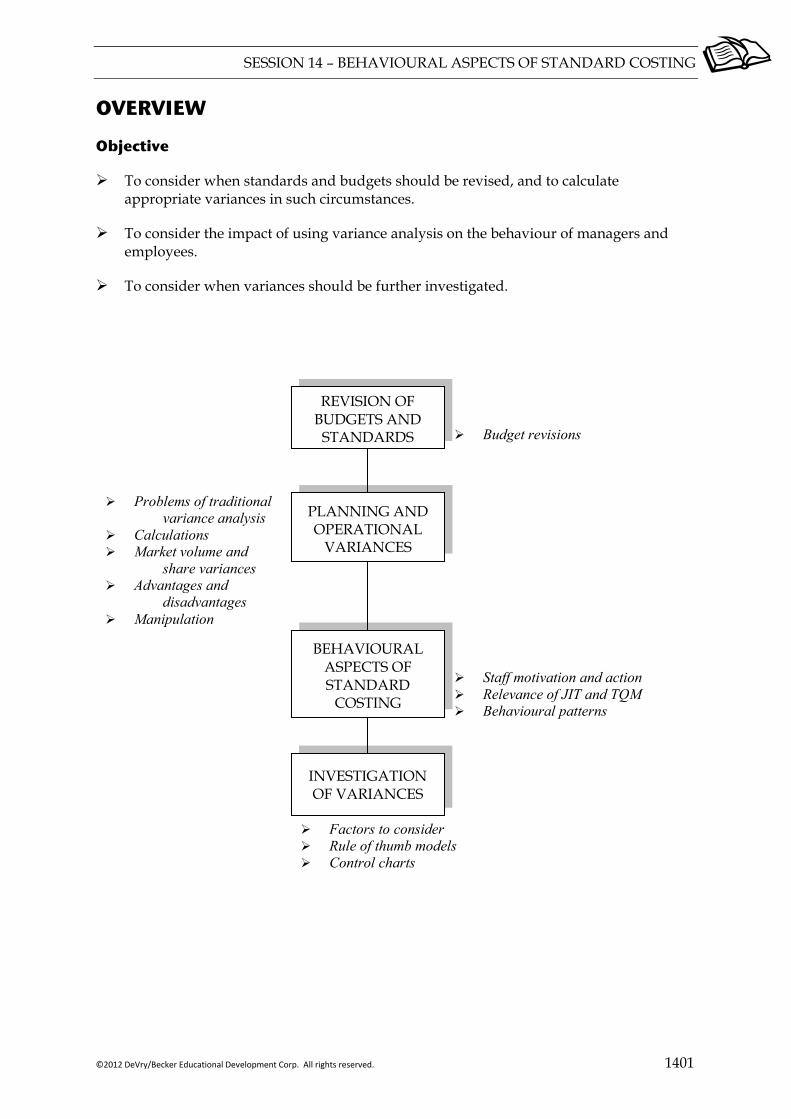

You should first read through the syllabus, study guide and approach to examining the syllabus provided in this session to familiarise you with the content of this paper. The sessions which follow include:

An overview diagram at the beginning of each session. This provides a visual summary of the topics covered in each Session and how they are related

The body of knowledge which underpins the syllabus. Features of the text include:

Definitions Terms are defined as they are introduced.

Illustrations These are to be read as part of the text. Any solutions

to numerical illustrations follow on immediately.

Examples These should be attempted using the proforma solution provided (where applicable).

Key points Attention is drawn to fundamental rules and

underlying concepts and principles.

Commentaries These provide additional information.

Focus These are the learning outcomes relevant to the

session, as published in ACCA’s Study Guide.

Example solutions are presented at the end of each session.

A bank of practice questions is contained in the Study Question Bank provided. These are linked to the topics of each session and should be attempted after studying each session.

SESSION 00 – SYLLABUS

(vi) ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

SYLLABUS

Aim

To develop knowledge and skills in the application of management accounting techniques to quantitative and qualitative information for planning, decision-making, performance evaluation, and control

Main capabilities

On successful completion of this paper candidates should be able to:

A Explain, apply, and evaluate cost accounting techniques.

B Select and appropriately apply decision-making techniques to evaluate business choices and promote efficient and effective use of scarce business resources, appreciating the risks and uncertainty inherent in business and controlling those risks.

C Apply budgeting techniques and evaluate alternative methods of budgeting, planning and control.

D Use standard costing systems to measure and control business performance and to identify remedial action.

E Assess the performance of a business from both a financial and non-financial viewpoint, appreciating the problems of controlling divisionalised businesses and the importance of allowing for external aspects.

Rationale

The syllabus for Paper F5, Performance Management, builds on the knowledge gained in Paper F2, Management Accounting. It also prepares candidates for more specialist capabilities which are covered in P5 Advanced Performance Management.

The syllabus begins by introducing more specialised management accounting topics. There is some knowledge assumed from Paper F2 – primarily overhead treatments. The objective here is to ensure candidates have a broader background in management accounting techniques.

The syllabus then considers decision-making. Candidates need to appreciate the problems surrounding scarce resource, pricing and make-or-buy decisions, and how this relates to the assessment of performance. Risk and uncertainty are a factor of real-life decisions and candidates need to understand risk and be able to apply some basic methods to help resolve the risks inherent in decision-making.

Budgeting is an important aspect of many accountants’ lives. The syllabus explores different budgeting techniques and the problems inherent in them. The behavioural aspects of budgeting are important for accountants to understand, and the syllabus includes consideration of the way individuals react to a budget.

SESSION 00 – SYLLABUS

©2012 DeVry/Becker Educational Development Corp. All rights reserved. (vii)

Standard costing and variances are then built on. All the variances examined in Paper F2 are examinable here. The new topics are mix and yield variances, and planning and operational variances. Again, the link is made to performance management. It is important for accountants to be able to interpret the numbers that they calculate and ask what they mean in the context of performance.

The syllabus concludes with performance measurement and control. This is a major area of the syllabus. Accountants need to understand how a business should be managed and controlled. They should appreciate the importance of both financial and non-financial performance measures in management. Accountants should also appreciate the difficulties in assessing performance in divisionalised businesses and the problems caused by failing to consider external influences on performance. This section leads directly to Paper P5.

Relational diagram of main capabilities

Specialist cost and management accounting

techniques (A)

Decision-making techniques (B)

Budgeting (C)

Standard costing and variance analysis (D)

Performance measurement and

control (E)

Syllabus structure

APM (P5)

PM (F5)

MA (F2)

SESSION 00 – SYLLABUS

(viii) ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

Detailed syllabus

A Specialist cost and management accounting techniques

1. Activity-based costing

2. Target costing

3. Life-cycle costing

4. Throughput accounting

5. Environmental Accounting

B Decision-making techniques

1. Relevant cost analysis

2. Cost volume profit analysis

3. Limiting factors

4. Pricing decisions

5. Make or buy and other short term decisions

6. Dealing with risk and uncertainty in decision-making

C Budgeting

1. Objectives

2. Budgetary systems

3. Types of budget

4. Quantitative analysis in budgeting

5. Behavioural aspects of budgeting

D Standard costing and variances analysis

1. Budgeting and standard costing

2. Basic variances and operating statements

3. Material mix and yield variances

4. Sales mix and quantity variances

5. Planning and operational variances

6. Behavioural aspects of standard costing

E Performance measurement and control

1. The scope of performance measurement

2. Divisional performance and transfer pricing

3. Performance analysis in not-for-profit organisations and the public sector

4. External considerations and behavioural aspects

SESSION 00 – SYLLABUS

©2012 DeVry/Becker Educational Development Corp. All rights reserved. (ix)

Approach to examining the syllabus

Paper F5, Performance Management, seeks to examine candidates’ understanding of how to manage the performance of a business.

The paper builds on the knowledge acquired in Paper F2, Management Accounting, and prepares those candidates who choose to study Paper P5, Advanced Performance Management, at the Professional level.

The syllabus is assessed by a three-hour paper-based examination. The examination contains five compulsory 20-mark questions. There will be calculation and discursive elements to the paper with the balance being broadly in line with the pilot paper. The pilot paper contains questions from four of the five syllabus sections. Generally, the paper will seek to draw questions from as many of the syllabus sections as possible.

ACCA Support

For examiner’s reports, guidance and technical articles relevant to this paper see http://www2.accaglobal.com/students/acca/exams/f5/

The ACCA’s Study Guide which follows is referenced to the Sessions in this Study System.

SESSION 00 – STUDY GUIDE

(x) ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

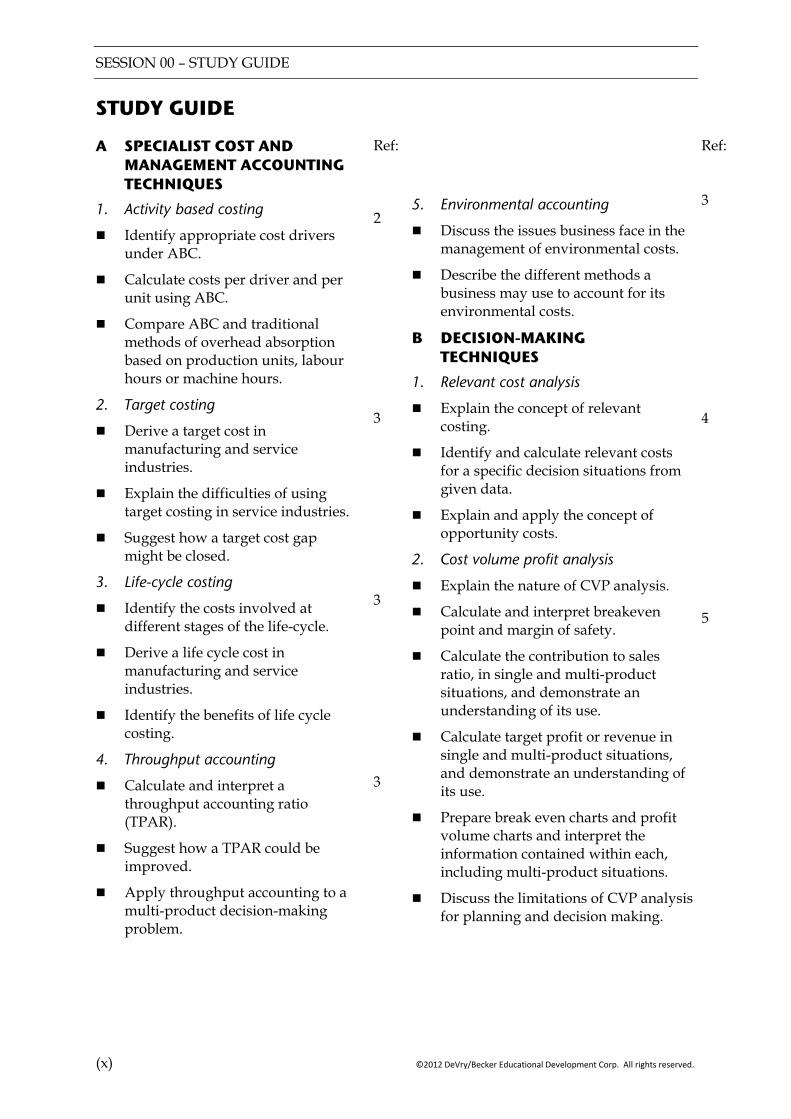

STUDY GUIDE

A SPECIALIST COST AND MANAGEMENT ACCOUNTING TECHNIQUES

1. Activity based costing

Identify appropriate cost drivers under ABC.

Calculate costs per driver and per unit using ABC.

Compare ABC and traditional methods of overhead absorption based on production units, labour hours or machine hours.

2. Target costing

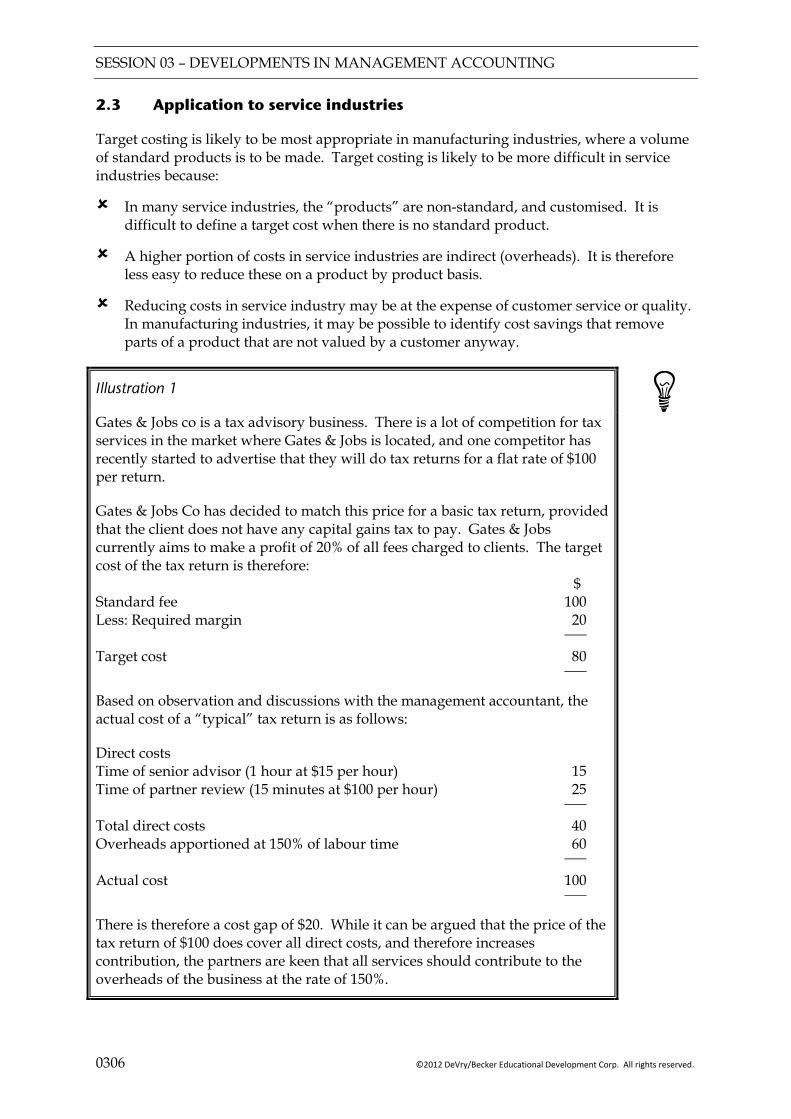

Derive a target cost in manufacturing and service industries.

Explain the difficulties of using target costing in service industries.

Suggest how a target cost gap might be closed.

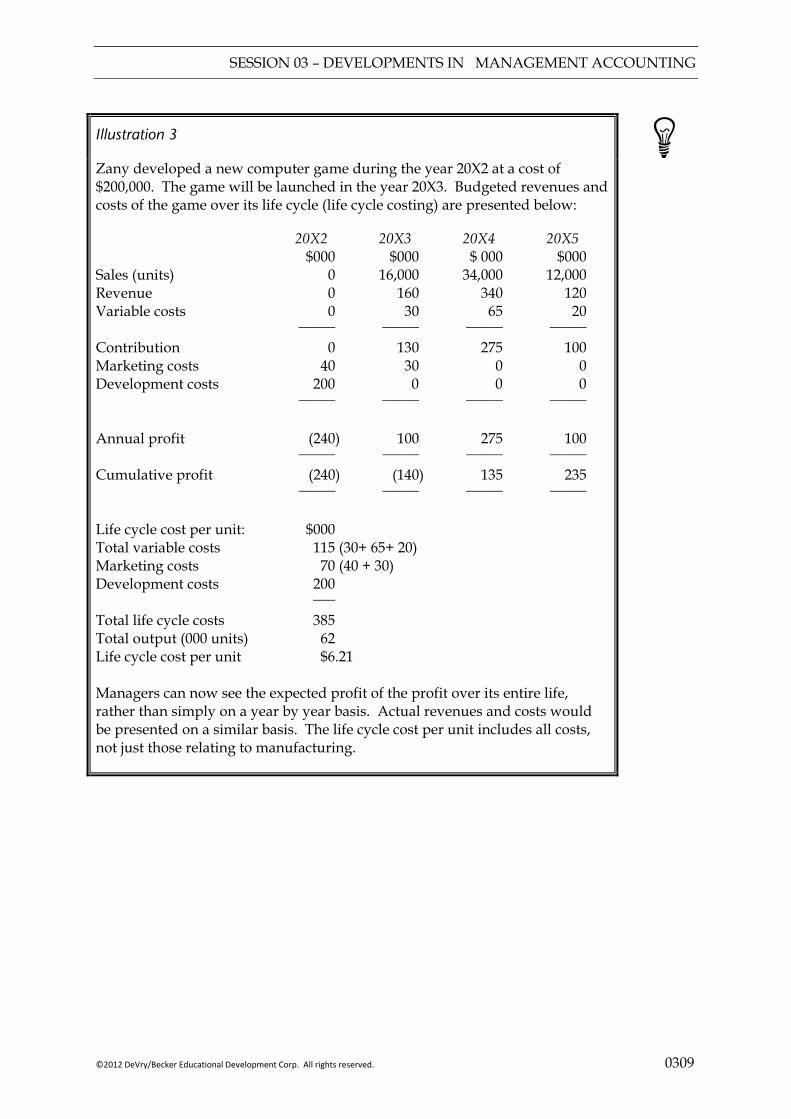

3. Life-cycle costing

Identify the costs involved at different stages of the life-cycle.

Derive a life cycle cost in manufacturing and service industries.

Identify the benefits of life cycle costing.

4. Throughput accounting

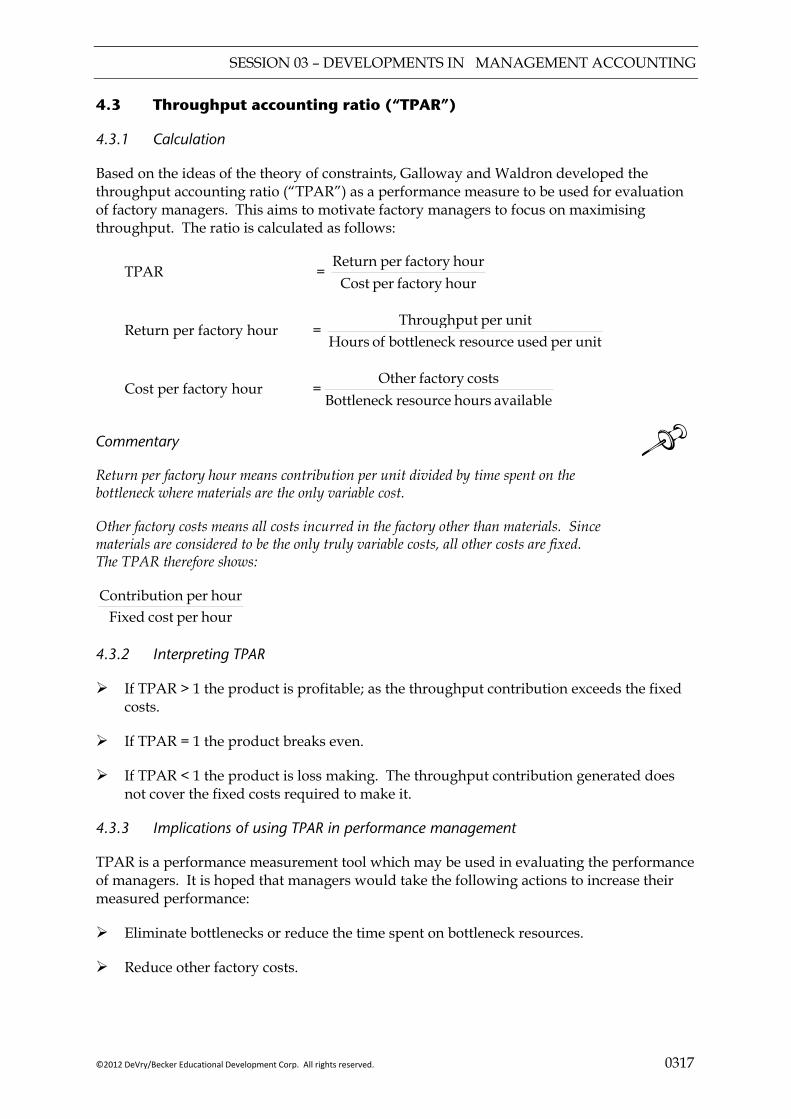

Calculate and interpret a throughput accounting ratio (TPAR).

Suggest how a TPAR could be improved.

Apply throughput accounting to a multi-product decision-making problem.

Ref: 2 3 3 3

5. Environmental accounting

Discuss the issues business face in the management of environmental costs.

Describe the different methods a business may use to account for its environmental costs.

B DECISION-MAKING TECHNIQUES

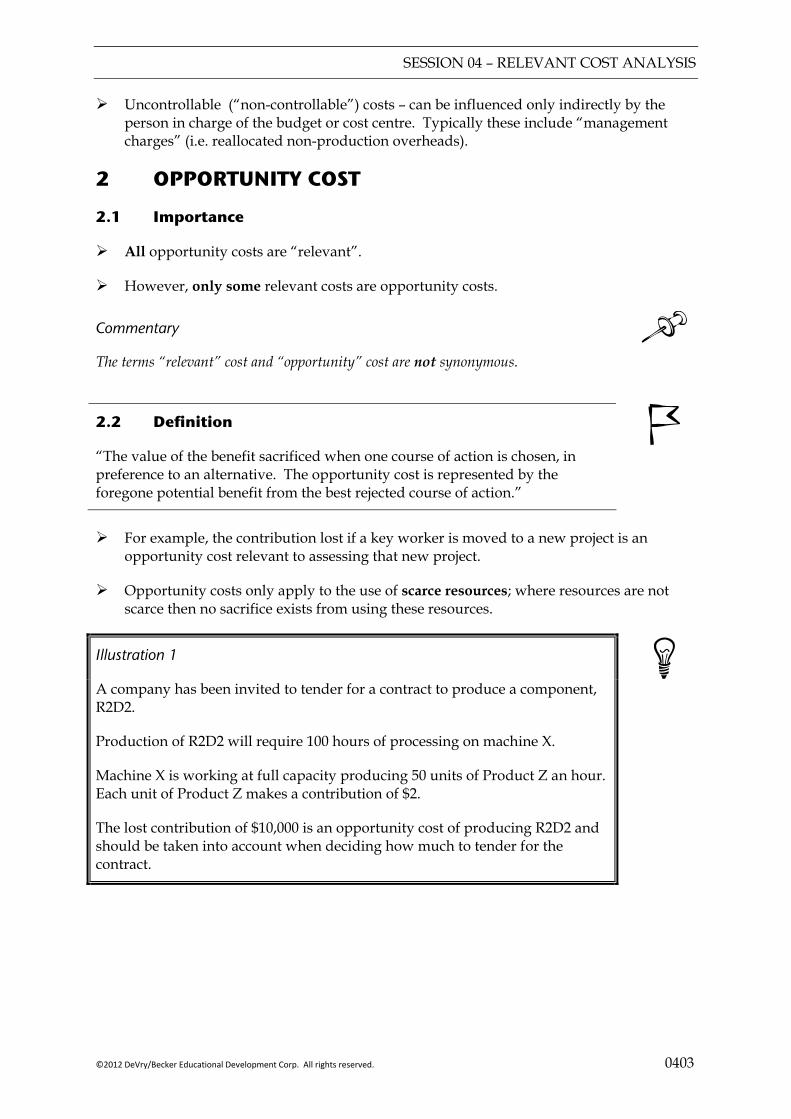

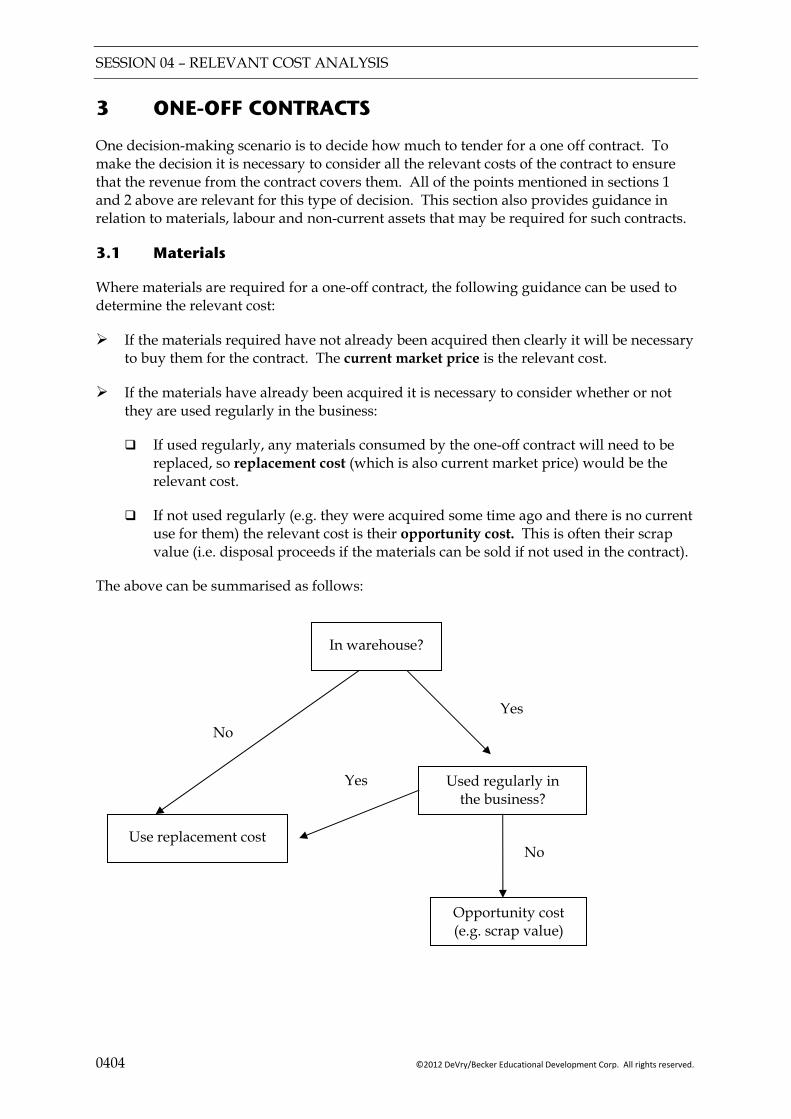

1. Relevant cost analysis

Explain the concept of relevant costing.

Identify and calculate relevant costs for a specific decision situations from given data.

Explain and apply the concept of opportunity costs.

2. Cost volume profit analysis

Explain the nature of CVP analysis.

Calculate and interpret breakeven point and margin of safety.

Calculate the contribution to sales ratio, in single and multi-product situations, and demonstrate an understanding of its use.

Calculate target profit or revenue in single and multi-product situations, and demonstrate an understanding of its use.

Prepare break even charts and profit volume charts and interpret the information contained within each, including multi-product situations.

Discuss the limitations of CVP analysis for planning and decision making.

Ref: 3 4 5

SESSION 00 – STUDY GUIDE

©2012 DeVry/Becker Educational Development Corp. All rights reserved. (xi)

3. Limiting factors

Identify limiting factors in a scarce resource situation and select an appropriate technique.

Determine the optimal production plan where an organisation is restricted by a single limiting factor, including within the context of “make” or “buy” decisions.

Formulate and solve multiple scarce resource problem both graphically and using simultaneous equations as appropriate.

Explain and calculate shadow prices (dual prices) and discuss their implications on decision-making and performance management.

Calculate slack and explain the implications of the existence of slack for decision-making and performance management. (Excluding simplex and sensitivity to changes in objective functions)

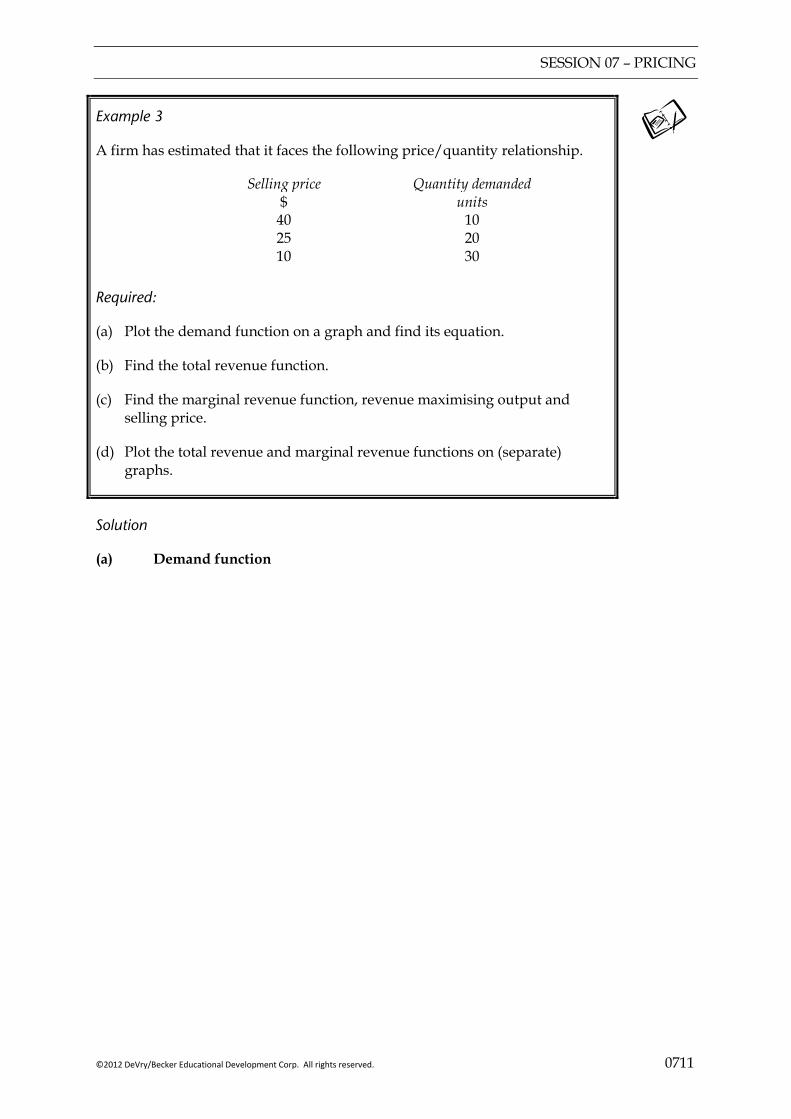

4. Pricing decisions

Explain the factors that influence the pricing of a product or service.

Explain the price elasticity of demand.

Derive and manipulate a straight line demand equation. Derive an equation for the total cost function (including volume-based discounts).

Calculate the optimum selling price and quantity for an organisation, equating marginal cost and marginal revenue

Evaluate a decision to increase production and sales levels, considering incremental costs, incremental revenues and other factors.

Ref: 6 7

Determine prices and output levels for profit maximisation using the demand based approach to pricing (both tabular and algebraic methods).

Explain different price strategies, including:

− All forms of cost-plus − Skimming − Penetration − Complementary product − Product-line − Volume discounting − Discrimination − Relevant cost

Calculate a price from a given

strategy using cost-plus and relevant cost.

5. Make-or-buy and other short-term decisions

Explain the issues surrounding make vs buy and outsourcing decisions.

Calculate and compare make costs with “buy-in” costs.

Compare in-house costs and outsource costs of completing tasks and consider other issues surrounding this decision.

Apply relevant costing principles in situations involving shut down, one-off contracts and the further processing of joint products.

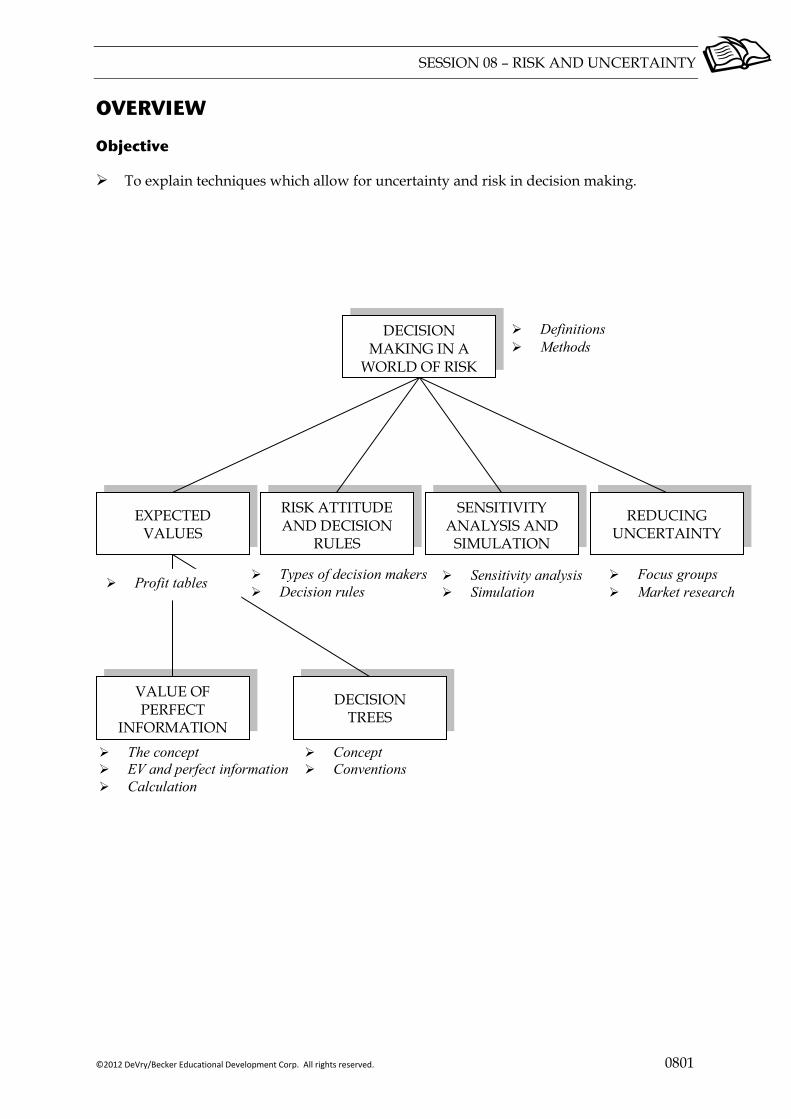

6. Dealing with risk and uncertainty in decision-making

Suggest research techniques to reduce uncertainty (e.g. focus groups, market research).

Explain the use of simulation, expected values and sensitivity.

Ref: 6 8

SESSION 00 – STUDY GUIDE

(xii) ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

Apply expected values and sensitivity to decision-making problems.

Apply the techniques of maximax, maximin, and minimax regret to decision-making problems including the production of profit tables.

Draw a decision tree and use it to solve a multi-stage decision problem

Calculate the value of perfect information.

C BUDGETING

1. Objectives

Outline the objectives of a budgetary control system.

Explain how corporate and divisional objectives may differ and can be reconciled.

Identify and resolve conflicting objectives and explain implications.

2. Budgetary systems

Explain how budgetary systems fit within the performance hierarchy.

Select and explain appropriate budgetary systems for an organisation, including top-down, bottom-up, rolling, zero-base, activity-base, incremental and feed-forward control.

Describe the information used in budget systems and the sources of the information needed.

Explain the difficulties of changing a budgetary system.

Explain how budget systems can deal with uncertainty in the environment.

Ref: 9 9

3. Types of Budget

Indicate the usefulness and problems with different budget types (zero-base, activity-based, incremental, master, functional and flexible).

Explain the difficulties of changing the type of budget used.

4. Quantitative analysis in budgeting

Analyse fixed and variable cost elements from total cost data using high/low and regression methods.

Explain the use of forecasting techniques, including time series, simple average growth models and estimates based on judgement and experience. Predict a future value from provided time series analysis data using both additive and proportional data.

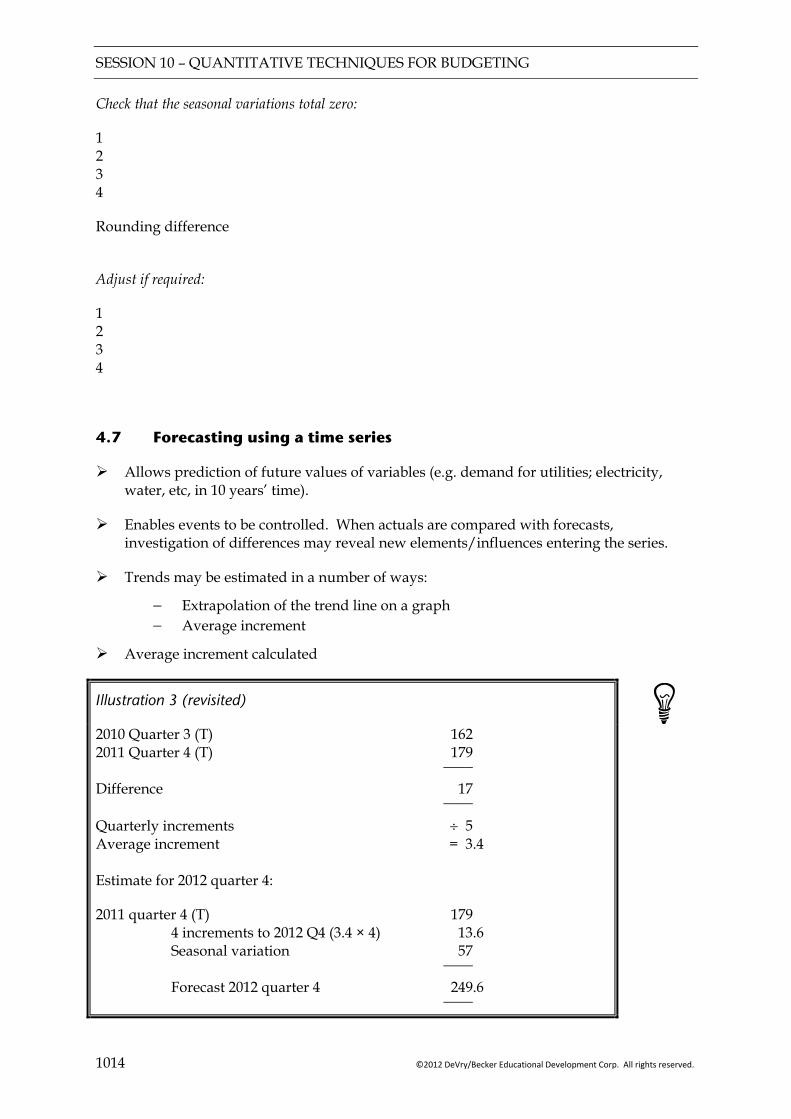

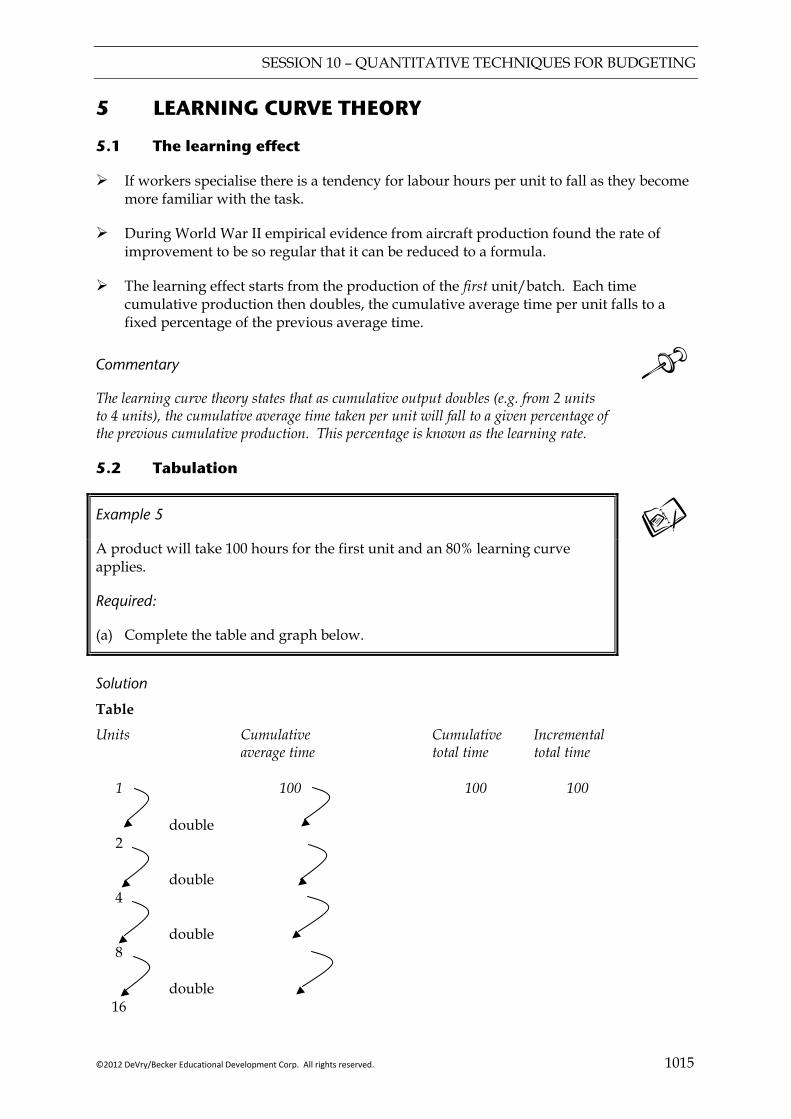

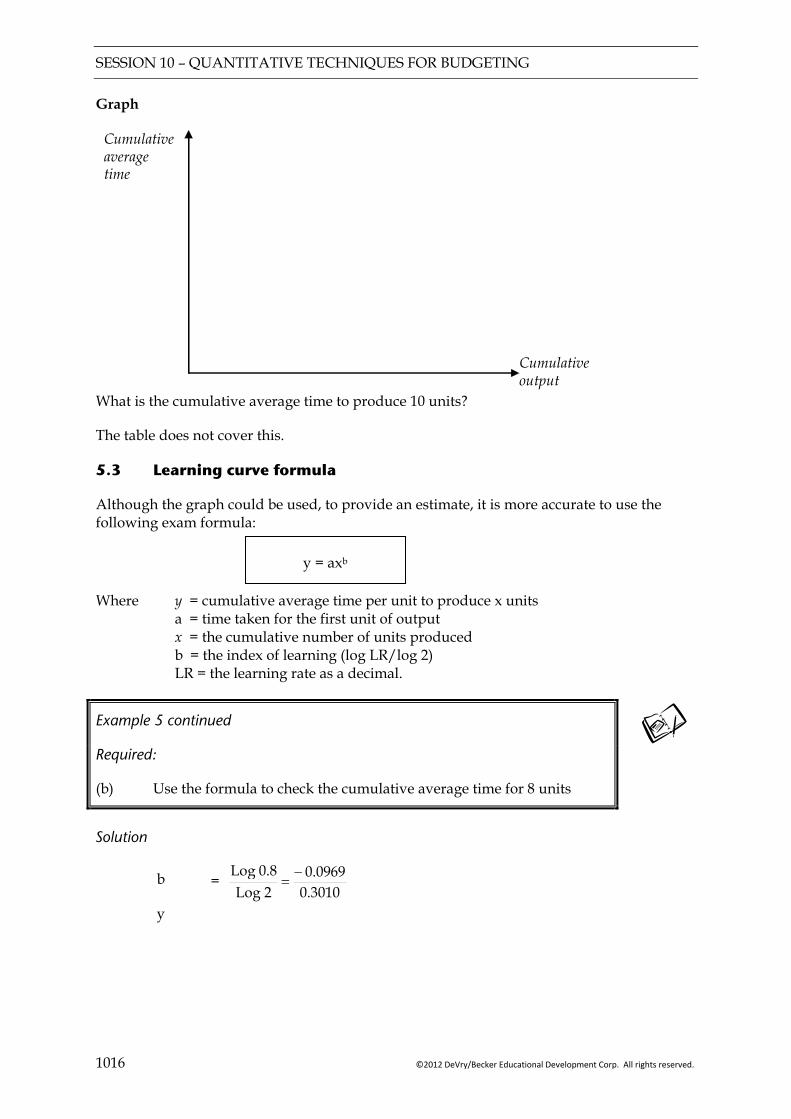

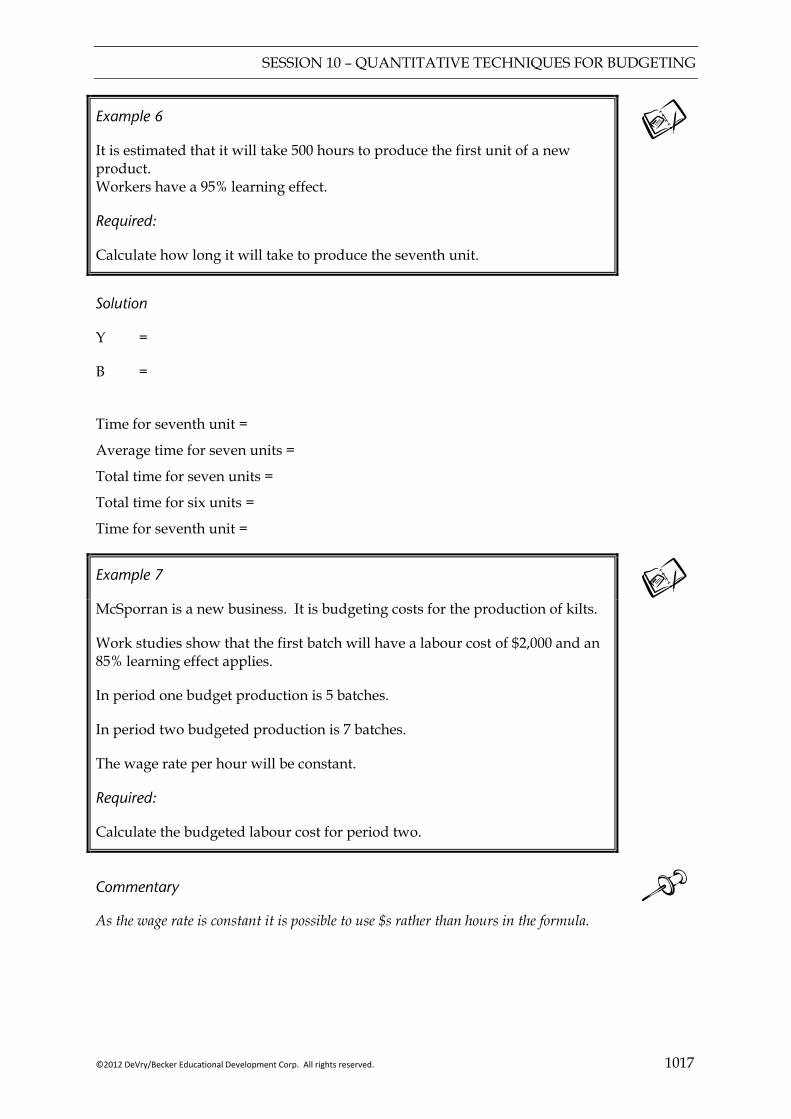

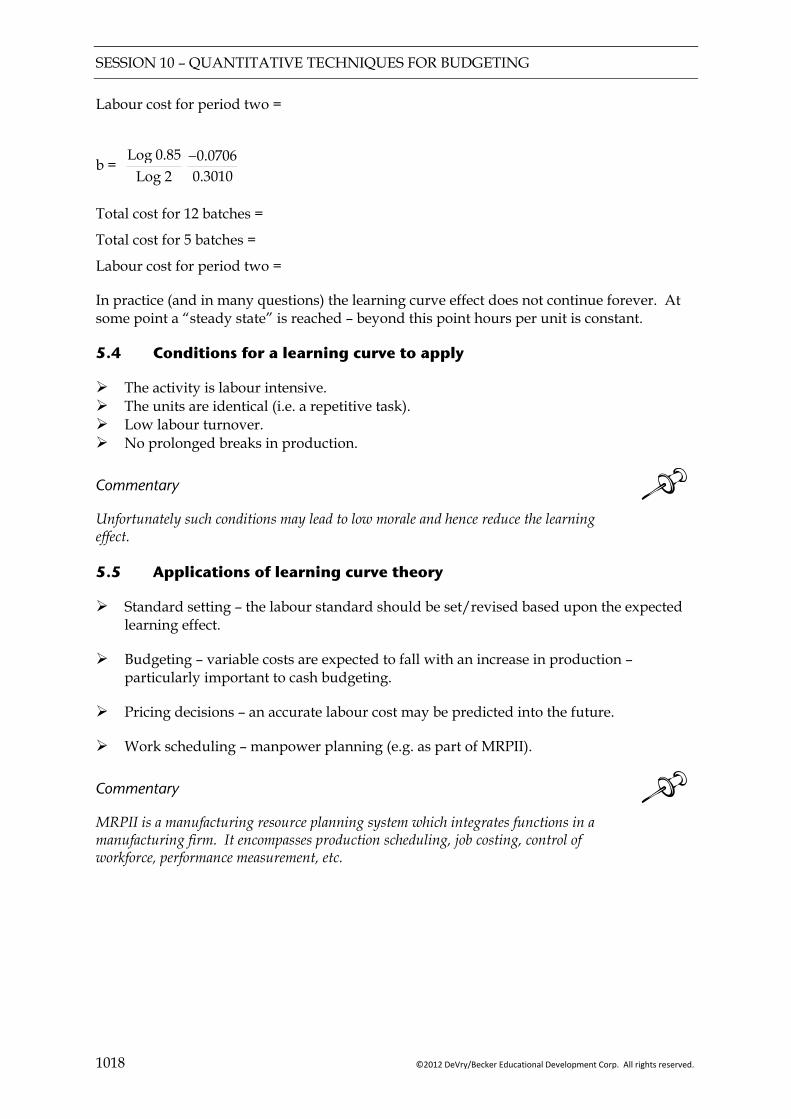

Estimate the learning effect and apply the learning curve to a budgetary problem, including calculations on steady states.

Discuss the reservations with the learning curve.

Apply expected values and explain the problems and benefits.

Explain the benefits and dangers inherent in using spreadsheets in budgeting.

5. Behavioural aspects of budgeting

Identify the factors which influence behaviour.

Discuss the issues surrounding setting the difficulty level for a budget.

Explain the benefits and difficulties of the participation of employees in the negotiation of targets.

Ref: 9 10 9

SESSION 00 – STUDY GUIDE

©2012 DeVry/Becker Educational Development Corp. All rights reserved. (xiii)

D STANDARD COSTING AND VARIANCES ANALYSIS

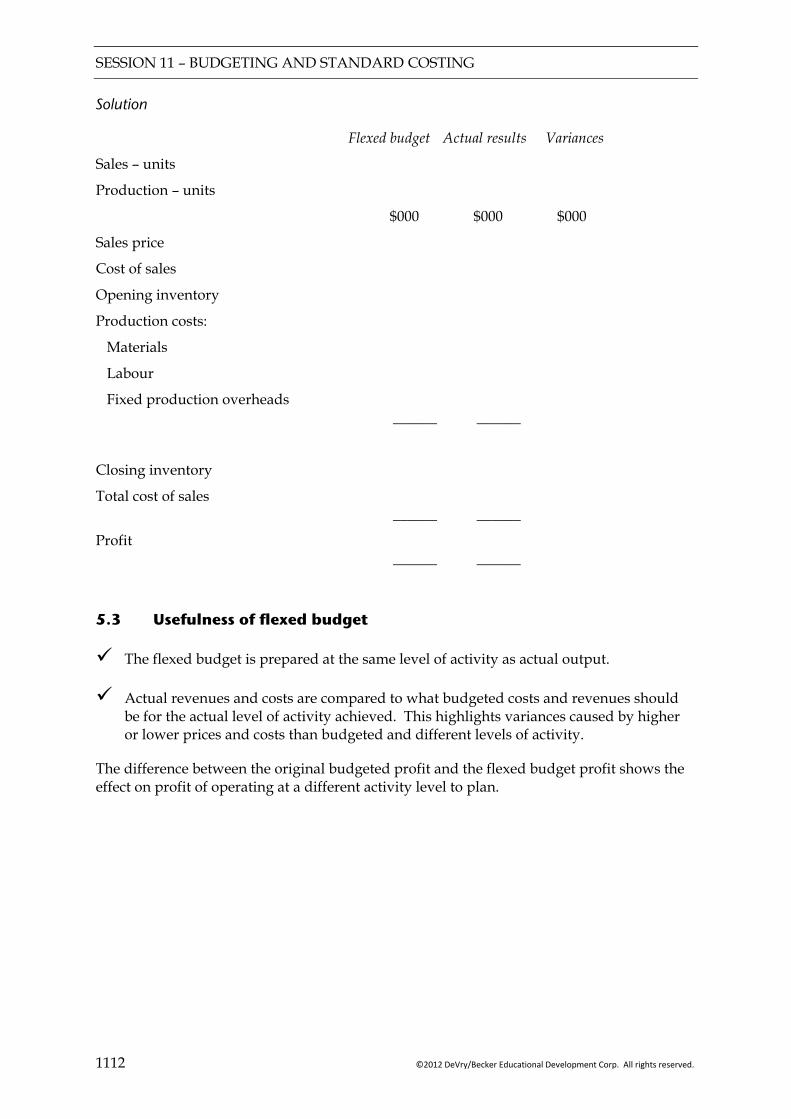

1. Budgeting and standard costing

Explain the use of standard costs.

Outline the methods used to derive standard costs and discuss the different types of cost possible.

Explain the importance of flexing budgets in performance management.

Prepare budgets and standards that allow for waste and idle time.

Explain and apply the principle of controllability in the performance management system.

Prepare a flexed budget and comment on its usefulness.

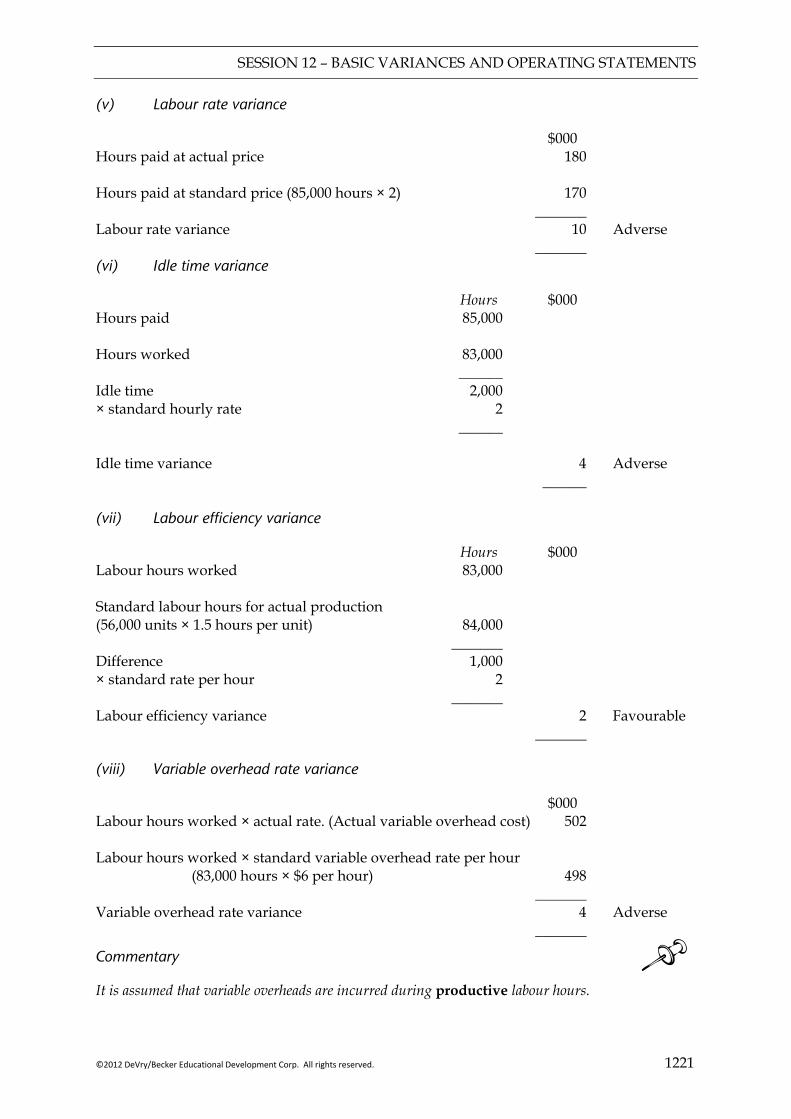

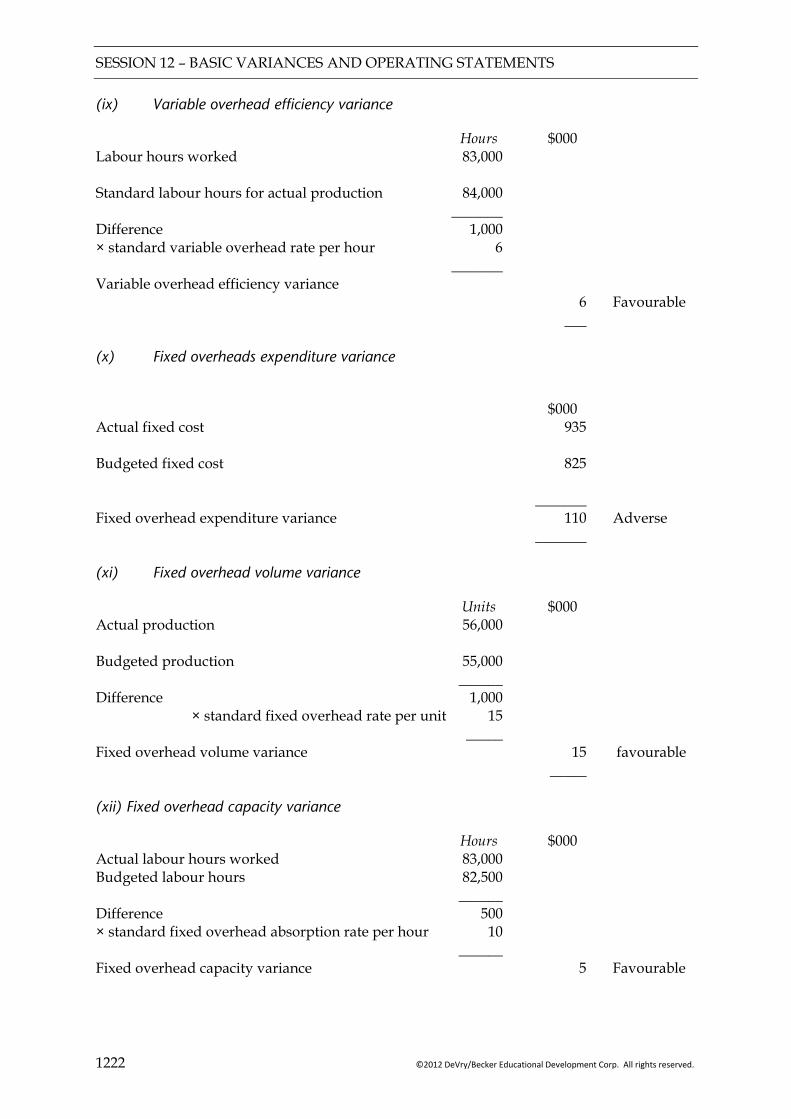

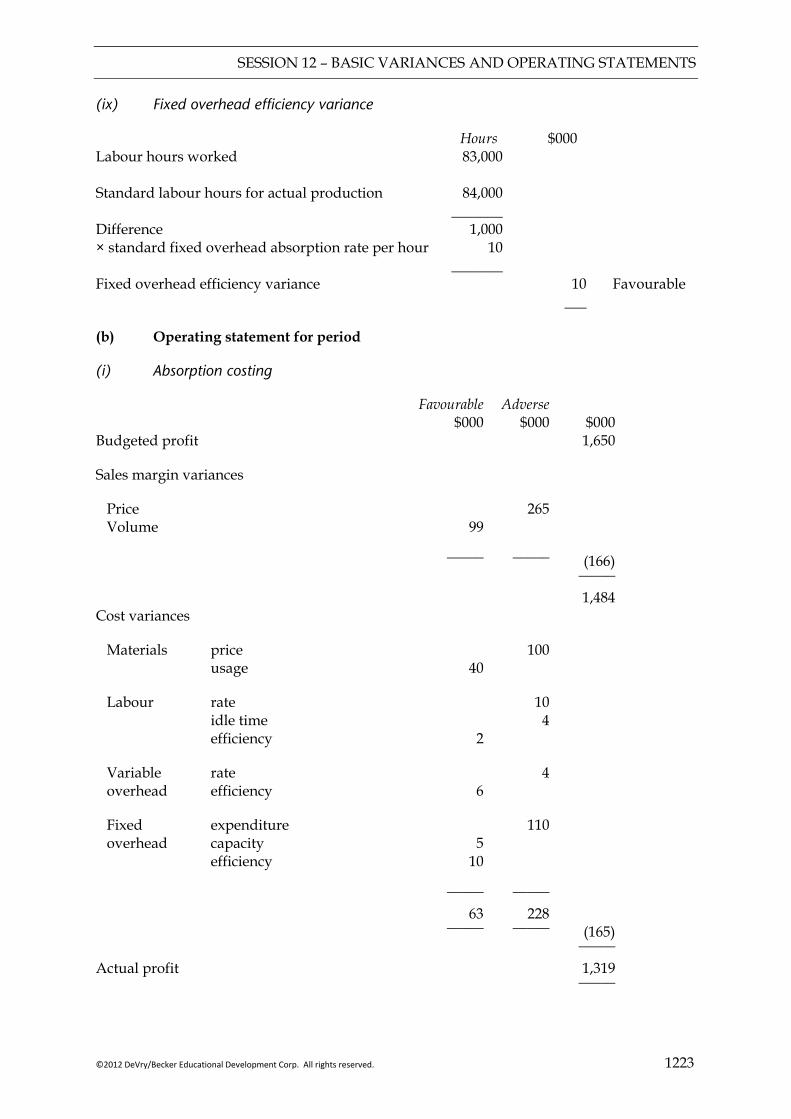

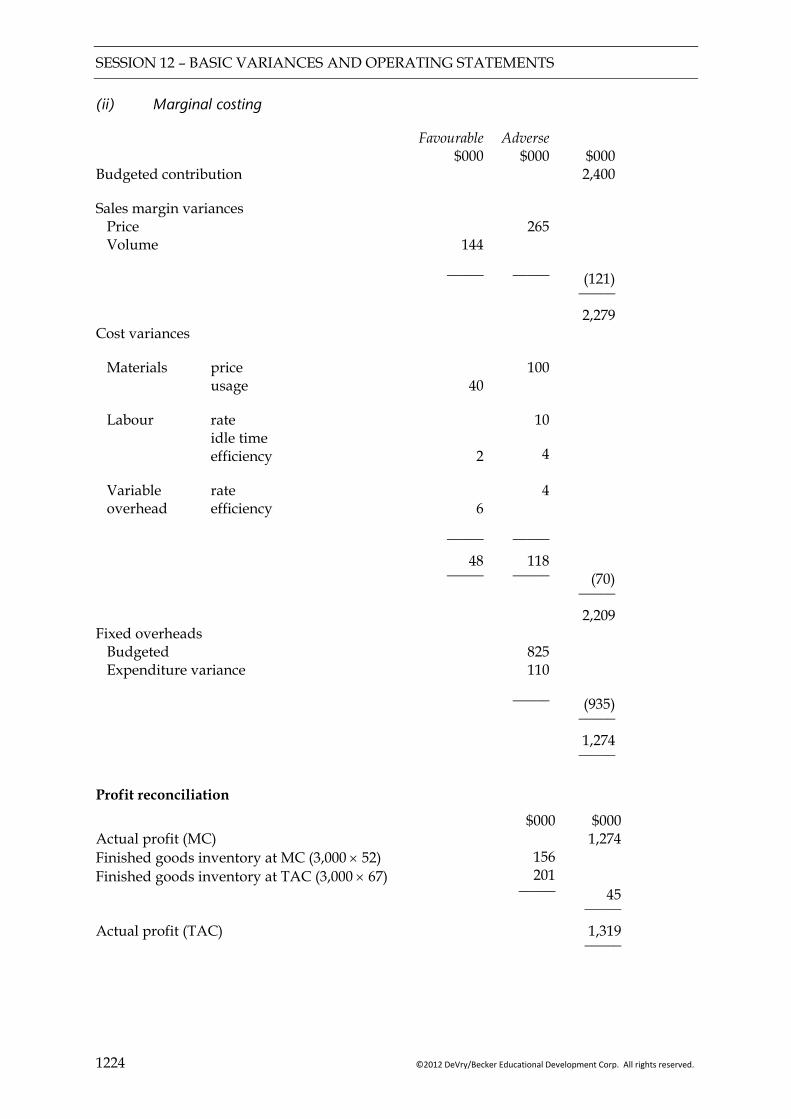

2. Basic variances and operating statements

Calculate, identify the cause of and interpret basic variances:

− Sales price and volume − Materials total, price and usage − Labour total, rate and efficiency − Variable overhead total,

expenditure and efficiency − Fixed overhead total,

expenditure and, where appropriate, volume, capacity and efficiency.

Explain the effect on labour variances where the learning curve has been used in the budget process.

Produce full operating statements in both a marginal cost and full absorption costing environment, reconciling actual profit to budgeted profit.

Calculate the effect of idle time and waste on variances including where idle time has been budgeted for.

Ref: 11 12 13 12 13

Explain the possible causes of idle

time and waste and suggest methods of control.

Calculate, using a simple situation, ABC-based variances.

Explain the different methods available for deciding whether or not too investigate a variance cause.

3. Material mix and yield variances

Calculate, identify the cause of, and explain material mix and yield variances.

Explain the wider issues involved in changing material mix (e.g. cost, quality and performance measurement issues).

Identify and explain the relationship of the material price variance with the material mix and yield variances.

Suggest and justify alternative methods of controlling production processes.

4. Sales mix and quantity variances

Calculate, identify the cause of, and explain sales mix and quantity variances.

Identify and explain the relationship of the sales volume variances with the sales mix and quantity variances.

5. Planning and operational variances

Calculate a revised budget.

Identify and explain those factors that could and could not be allowed to revise an original budget.

Calculate planning and operational variances for sales, including market size and market share, materials and labour.

Explain and discuss the manipulation issues involved in revising budgets.

Ref: 13 13 13 13

SESSION 00 – STUDY GUIDE

(xiv) ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

6. Behavioural aspects of standard costing

Describe the dysfunctional nature of some variances in the modern environment of JIT and TQM.

Discuss the behavioural problems resulting from using standard costs in rapidly changing environments.

Discuss the effect that variances have on staff motivation and action.

E PERFORMANCE MEASUREMENT AND CONTROL

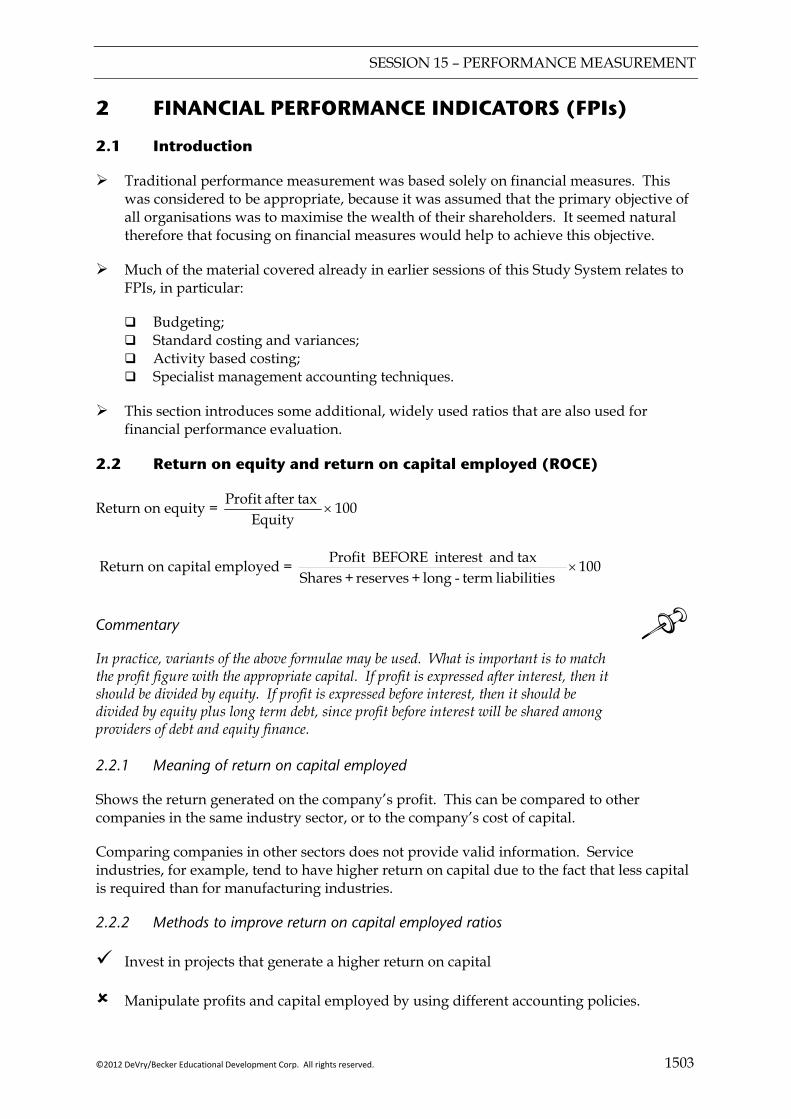

1. The scope of performance measurement

Describe, calculate and interpret financial performance indicators (FPIs) for profitability, liquidity and risk in both manufacturing and service businesses. Suggest methods to improve these measures.

Describe, calculate and interpret non-financial performance indicators (NFPIs) and suggest method to improve the performance indicated.

Explain the causes and problems created by short-termism and financial manipulation of results and suggest methods to encourage a long term view.

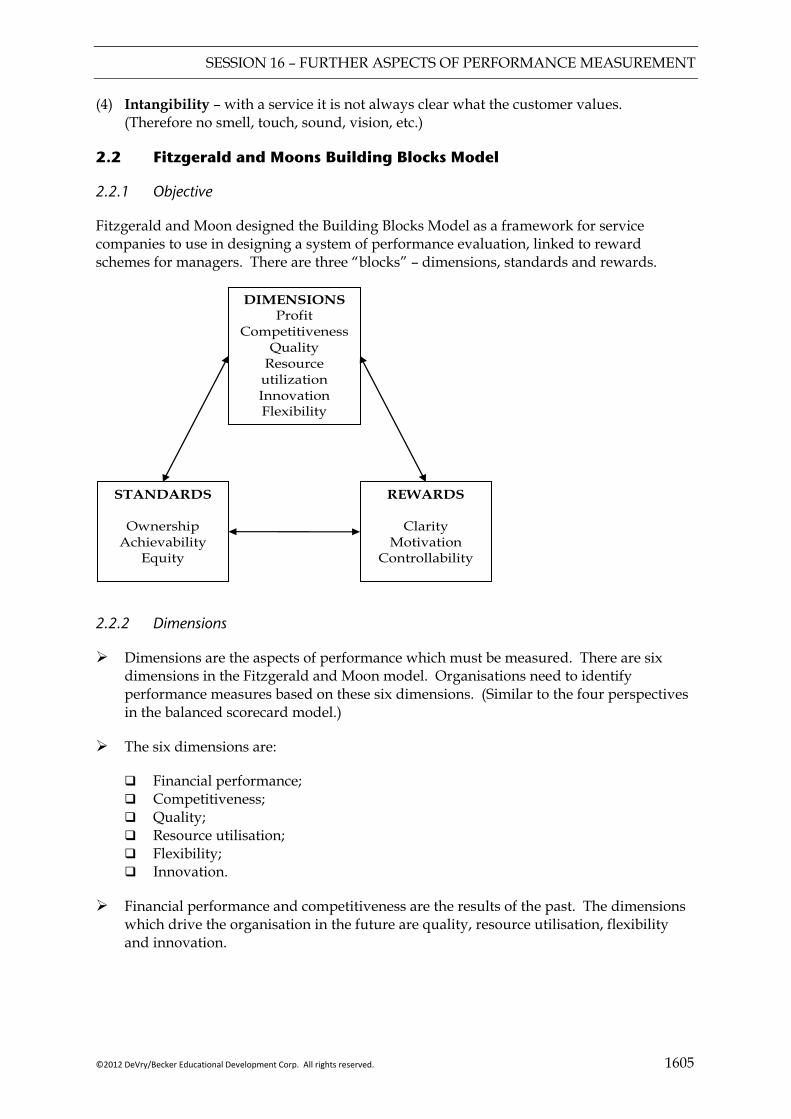

Explain and interpret the Balanced Scorecard, and the Building Block model proposed by Fitzgerald and Moon.

Discuss the difficulties of target setting in qualitative areas.

Ref:

14 15 16

2. Divisional performance and transfer pricing

Explain and illustrate the basis for setting a transfer price using variable cost, full cost and the principles behind allowing for intermediate markets.

Explain how transfer prices can distort the performance assessment of divisions and decisions made.

Explain the meaning of, and calculate, Return on Investment (ROI) and Residual Income (RI), and discuss their shortcomings.

Compare divisional performance and recognise the problems of doing so.

3. Performance analysis in not for profit organisations and the public sector

Comment on the problems of having non-quantifiable objectives in performance management.

Explain how performance could be measured in this sector.

Comment on the problems of having multiple objectives in this sector.

Outline Value for Money (VFM) as a public sector objective)

4. External considerations and behavioural aspects

Explain the need to allow for external considerations in performance management, including stakeholders, market conditions and allowance for competitors.

Suggest ways in which external considerations could be allowed for in performance management.

Interpret performance in the light of external considerations.

Identify and explain the behaviour aspects of performance management.

Ref: 18 18 17 17 16 16

SESSION 00 – FORMULAE

©2012 DeVry/Becker Educational Development Corp. All rights reserved. (xv)

Formulae Sheet

Learning curve

Y = axb

Where Y = cumulative average time per unit to produce x units a = time taken for the first unit of output x = total number of units produced b = the index of learning (log LR/log 2) LR = the learning rate as a decimal

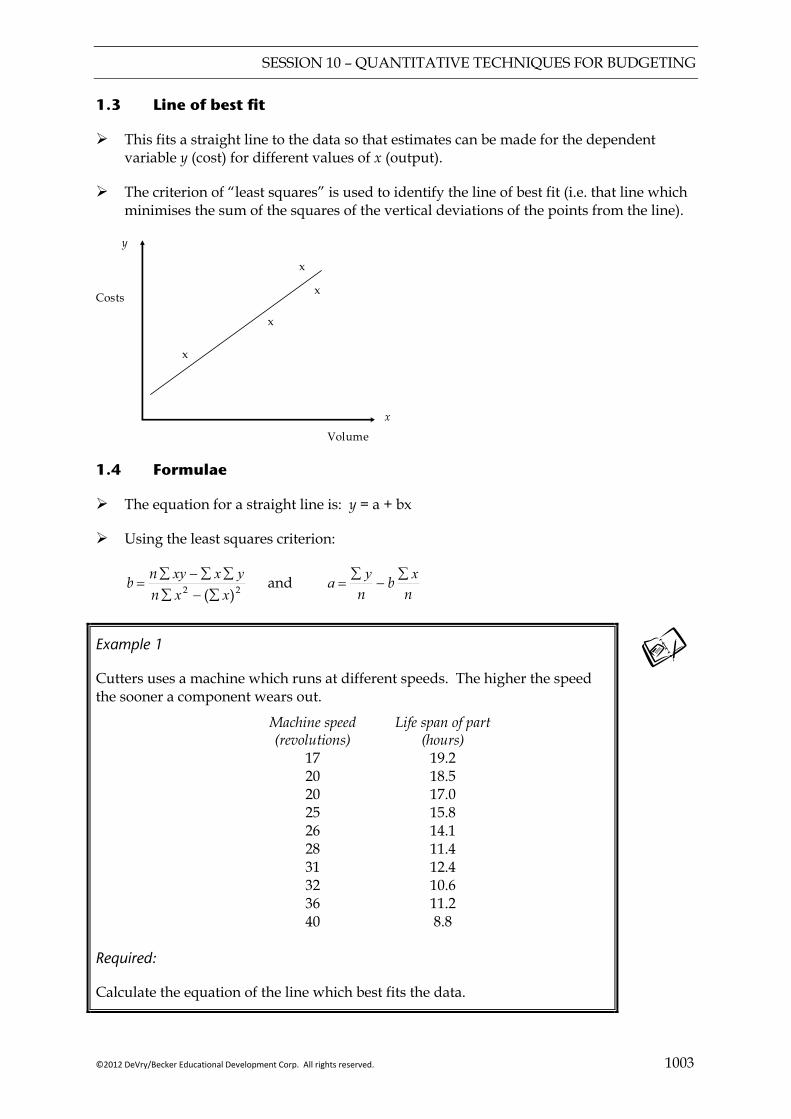

Regression analysis

y = a + bx

b = 22 )(∑∑∑ ∑∑−

−

xxnyxxyn

a = nxb

ny ∑∑ −

r = ( )( ) ( )( )2222 ∑∑∑∑∑ ∑ ∑

−−

−

yynxxn

yxxyn

Demand curve

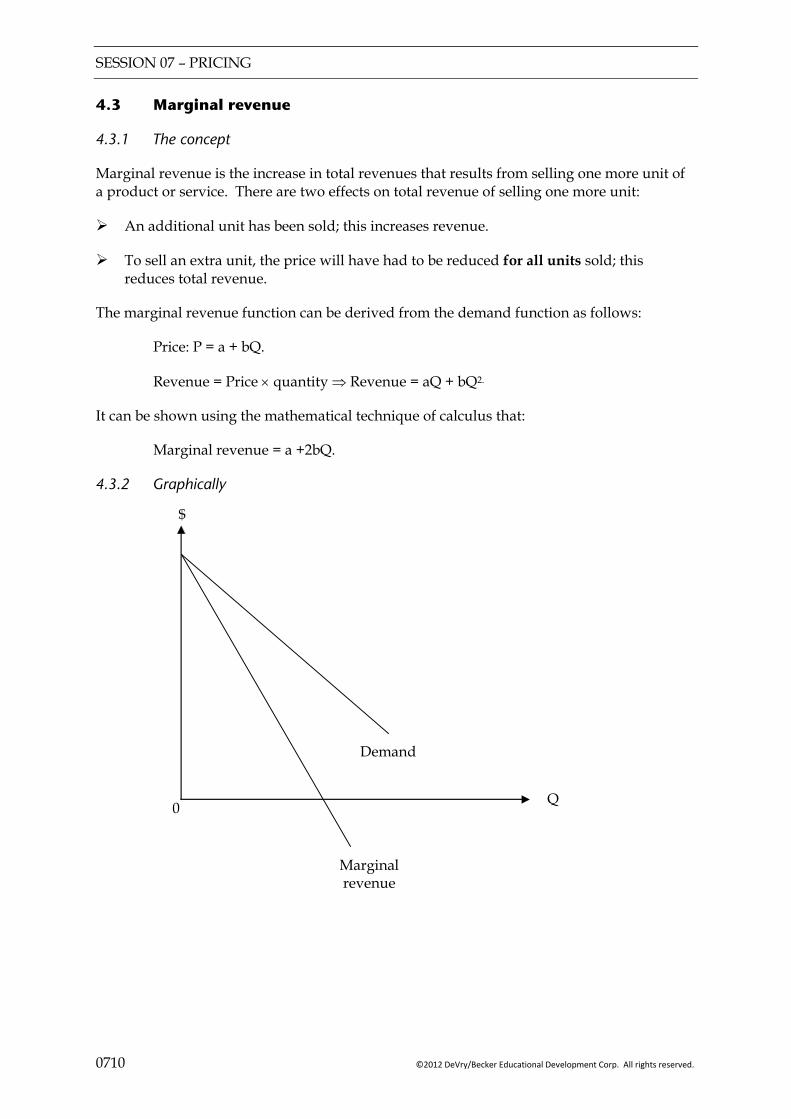

P = a – bQ

b = qualityin changepricein change

a = price when Q = 0

MR = a – 2bQ

SESSION 00 – EXAM TECHNIQUE

(xvi) ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

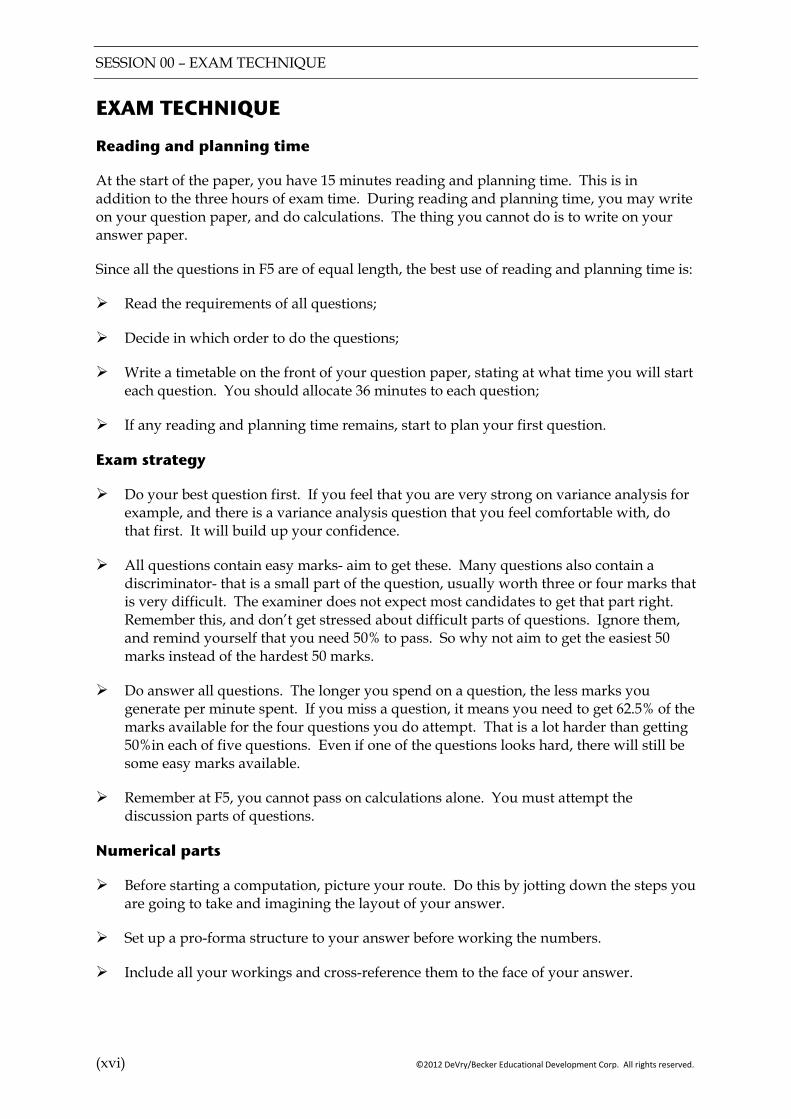

EXAM TECHNIQUE

Reading and planning time

At the start of the paper, you have 15 minutes reading and planning time. This is in addition to the three hours of exam time. During reading and planning time, you may write on your question paper, and do calculations. The thing you cannot do is to write on your answer paper.

Since all the questions in F5 are of equal length, the best use of reading and planning time is:

Read the requirements of all questions;

Decide in which order to do the questions;

Write a timetable on the front of your question paper, stating at what time you will start each question. You should allocate 36 minutes to each question;

If any reading and planning time remains, start to plan your first question.

Exam strategy

Do your best question first. If you feel that you are very strong on variance analysis for example, and there is a variance analysis question that you feel comfortable with, do that first. It will build up your confidence.

All questions contain easy marks- aim to get these. Many questions also contain a discriminator- that is a small part of the question, usually worth three or four marks that is very difficult. The examiner does not expect most candidates to get that part right. Remember this, and don’t get stressed about difficult parts of questions. Ignore them, and remind yourself that you need 50% to pass. So why not aim to get the easiest 50 marks instead of the hardest 50 marks.

Do answer all questions. The longer you spend on a question, the less marks you generate per minute spent. If you miss a question, it means you need to get 62.5% of the marks available for the four questions you do attempt. That is a lot harder than getting 50%in each of five questions. Even if one of the questions looks hard, there will still be some easy marks available.

Remember at F5, you cannot pass on calculations alone. You must attempt the discussion parts of questions.

Numerical parts

Before starting a computation, picture your route. Do this by jotting down the steps you are going to take and imagining the layout of your answer.

Set up a pro-forma structure to your answer before working the numbers.

Include all your workings and cross-reference them to the face of your answer.

SESSION 00 – FORMULAE

©2012 DeVry/Becker Educational Development Corp. All rights reserved. (xvii)

A clear approach and workings will help earn marks even if you make an arithmetic mistake.

If you do spot a mistake in your answer, it is not worthwhile spending time amending the consequent effects of it. The marker of your script will not punish you for errors caused by an earlier mistake.

Don’t ignore marks for written recommendations or comments based upon your computation. These are easy marks to gain.

If you could not complete the calculations required for comment then assume an answer to the calculations. As long as your comments are consistent with your assumed answer you can still pick up all the marks for the comments.

Written questions

Planning

Read the requirements carefully at least twice to identify exactly how many points you are being asked to address. Focus on the key work in the requirement- for example, explain, describe, outline. The meaning of these terms is explained in an article by the F5 examiner Ann Irons, “Approaching Written Questions” which can be downloaded from the ACCA web site.

Jot down relevant thoughts on your plan- use the scenario for clues, plus your technical knowledge.

Give your plan a structure which you will follow when you write up the answer. Take into account the marking guide.

Presentation

Use short paragraphs for each point that you are making.

Separate paragraphs by leaving at least one line of space between each one.

Style

Long philosophical debate does not impress markers. Concise, easily understood language scores marks.

Imagine that you are a marker; you would like to see a short, concise answer which clearly addresses the requirement.

SESSION 00 – EXAM TECHNIQUE

(xviii) ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

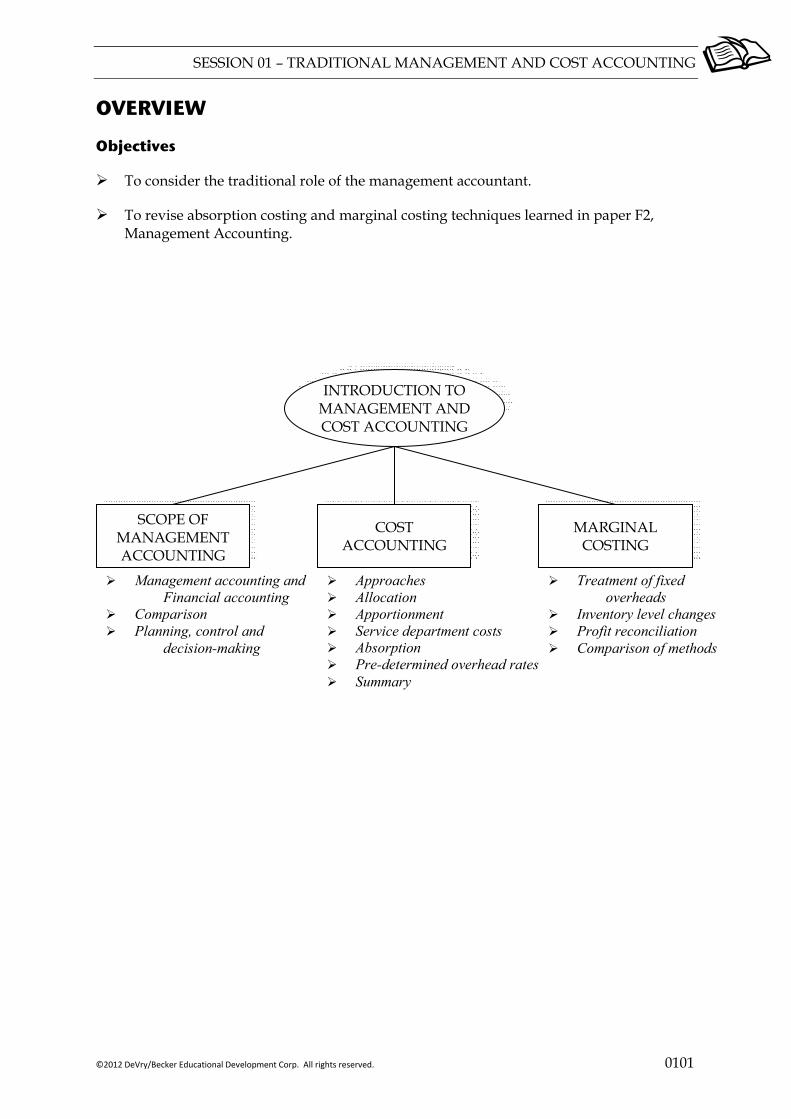

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0101

OVERVIEW

Objectives

To consider the traditional role of the management accountant.

To revise absorption costing and marginal costing techniques learned in paper F2, Management Accounting.

COST ACCOUNTING

SCOPE OF MANAGEMENT ACCOUNTING

INTRODUCTION TO MANAGEMENT AND COST ACCOUNTING

MARGINAL COSTING

Management accounting and Financial accounting

Comparison Planning, control and

decision-making

Approaches Allocation Apportionment Service department costs Absorption Pre-determined overhead rates Summary

Treatment of fixed overheads

Inventory level changes Profit reconciliation Comparison of methods

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

0102 ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

1 SCOPE OF TRADITIONAL MANAGEMENT ACCOUNTING

Commentary The material in this session is background information, and is not likely to feature largely in the F5 exam. However, an understanding of absorption costing is necessary to understand activity based costing which is covered in session 2. It is likely that exam questions will require candidates to compare and contrast traditional absorption costing with activity based costing.

1.1 Management accounting and financial accounting

Management accounting is concerned with the preparation and presentation of accounting information to management to help them plan, control and make decisions about the operations of the business.

Financial accounting is concerned with the preparation and presentation of accounting information on the performance and financial position of the business.

1.2 Comparison

Management accounting Financial accounting

Users of information

Management Shareholders, banks, lenders and suppliers, potential investors, tax authorities, and governments

Format of information

Can take any form Presentation regulated by law and by the profession through Accounting Standards (e.g. IFRS)

Purpose of information

Useful to plan, control and make decisions

Stewardship and investment decisions

Bases of valuation

Relevant costs Historical costs

1.3 Planning, control and decision-making

1.3.1 Planning

Encompasses establishing objectives and evaluating policies and actions required to achieve them.

Planning is the setting of goals and selecting the means of achieving them.

As businesses become large, these procedures will need to be formalised.

Short-term plans such as the annual budget show in detail the intended results for the forthcoming year (see Session 8).

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0103

Long-term plans (also called “strategic” plans) are usually documents showing the long-term objectives of the business.

1.3.2 Control

Control means checking that an organisation is on track to meet its long and short term objectives, and taking action to correct any deviations from these.

Long term control includes strategic performance evaluation, which aims to measure how the organisation is performing against its strategic objectives

Short term control focuses on comparing the budgeted results with actual results.

This usually takes the form of an operating statement which breaks down the difference into its component parts (variances). (See Sessions 10 & 11.)

1.3.3 Decision-making

Decision-making usually involves using the information provided by the costing system to make decisions (see Sessions 3 to 7).

2 COST ACCOUNTING

2.1 Approaches

Costs are recorded and accumulated in cost accounting systems using one of three main approaches:

absorption costing; marginal costing; Activity based costing (see Session 2).

Under absorption costing system overhead costs must be allocated, apportioned and then absorbed.

2.2 Allocation

This is where costs that relate to a single cost centre are allocated to that cost centre.

2.3 Apportionment

Apportionment is where an overhead is common to more than one cost centre and therefore needs to be shared out amongst the relevant cost centres using an appropriate method of apportionment.

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

0104 ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

Illustration 1

Cost Basis of apportionment Rent, rates, heat − Floor area Supervision, canteen costs − Number of employees Depreciation, plant insurance − Book value of plant

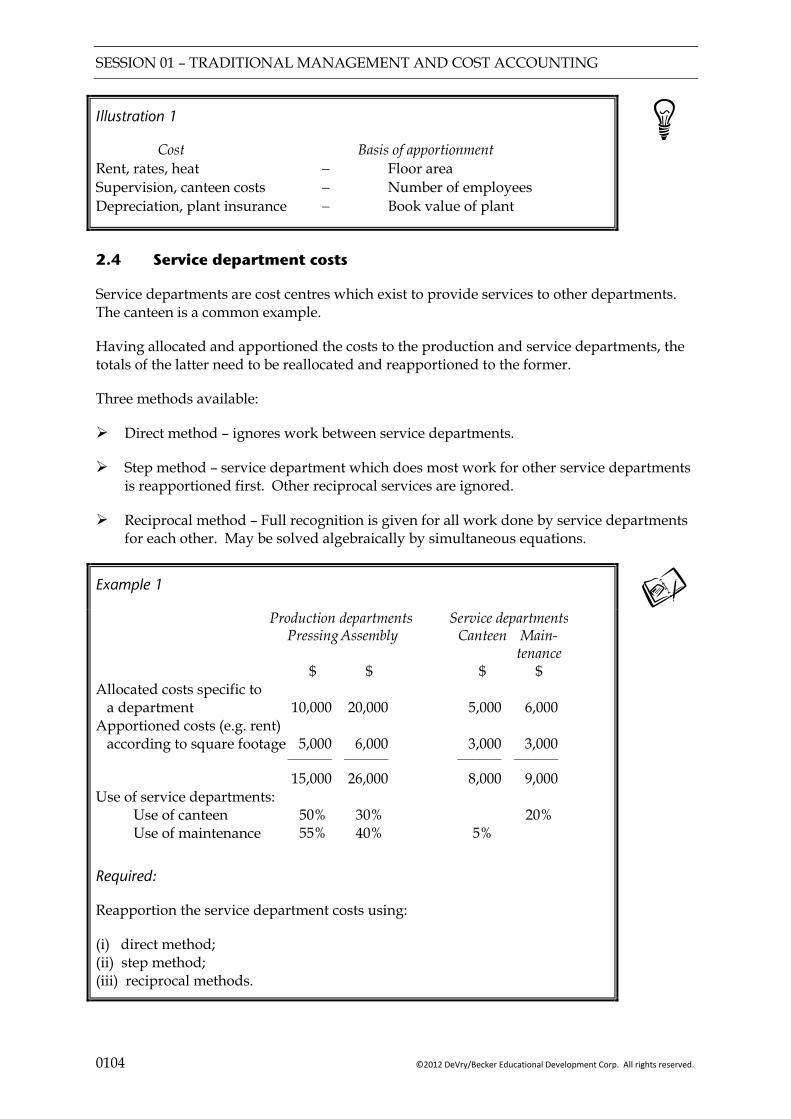

2.4 Service department costs

Service departments are cost centres which exist to provide services to other departments. The canteen is a common example.

Having allocated and apportioned the costs to the production and service departments, the totals of the latter need to be reallocated and reapportioned to the former.

Three methods available:

Direct method – ignores work between service departments.

Step method – service department which does most work for other service departments is reapportioned first. Other reciprocal services are ignored.

Reciprocal method – Full recognition is given for all work done by service departments for each other. May be solved algebraically by simultaneous equations.

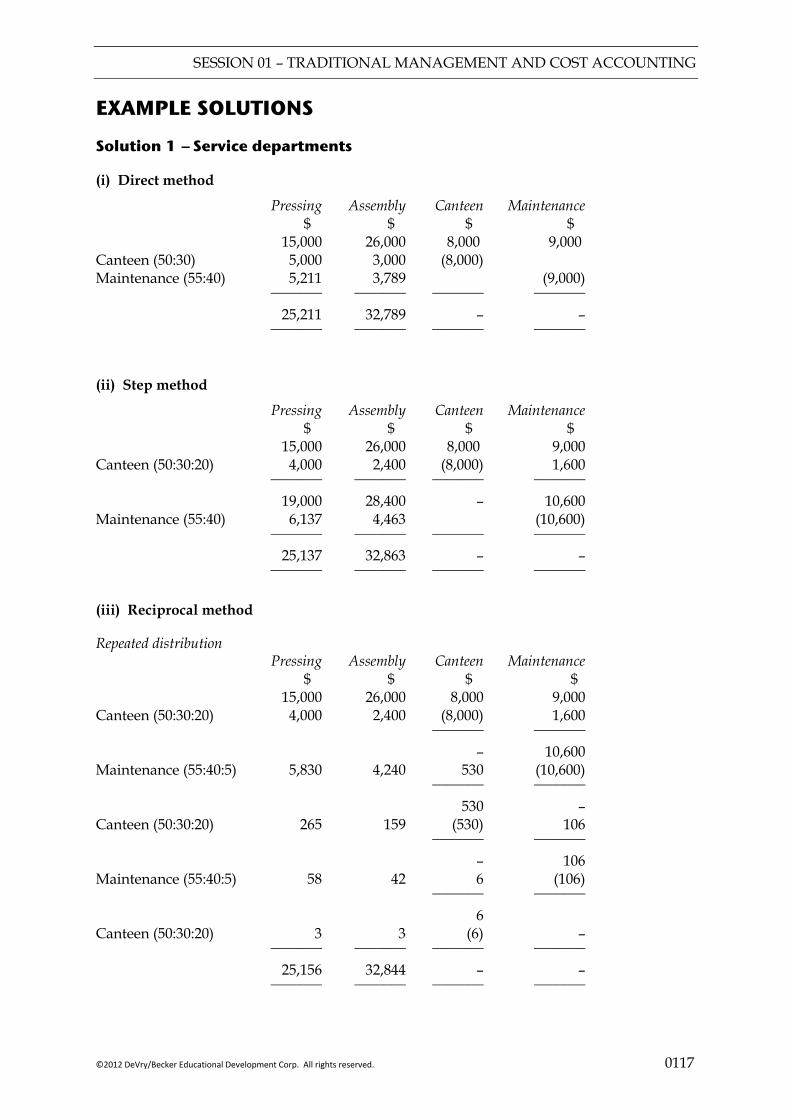

Example 1

Production departments Service departments Pressing Assembly Canteen Main- tenance $ $ $ $ Allocated costs specific to a department 10,000 20,000 5,000 6,000 Apportioned costs (e.g. rent) according to square footage 5,000 6,000 3,000 3,000 ______ ______ ______ ______ 15,000 26,000 8,000 9,000 Use of service departments: Use of canteen 50% 30% 20% Use of maintenance 55% 40% 5%

Required:

Reapportion the service department costs using:

(i) direct method; (ii) step method; (iii) reciprocal methods.

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0105

Solution

(i) Direct method

Pressing Assembly Canteen Maintenance $ $ $ $ Canteen (50:30)

Maintenance (55:40)

15,000

26,000

8,000

9,000

______ ______

______ ______

______ ______

______ ______

(ii) Step (down) method

Pressing Assembly Canteen Maintenance $ $ $ $ Canteen (50:30:20)

15,000

26,000

8,000

9,000

______ ______ ______ ______

Maintenance (55:40)

______ ______

______ ______

______ ______

______ ______

(iii) Reciprocal method

Repeated distribution also Pressing Assembly Canteen Maintenance $ $ $ $ Canteen (50:30:20)

15,000

26,000

8,000

9,000

_______ _______ Maintenance (55:40:5)

_______ _______ Canteen (50:30:20)

_______ _______ Maintenance (55:40:5)

_______ _______ Canteen (50:30:20)

_______ _______

_______ _______

_______ _______

_______ _______

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

0106 ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

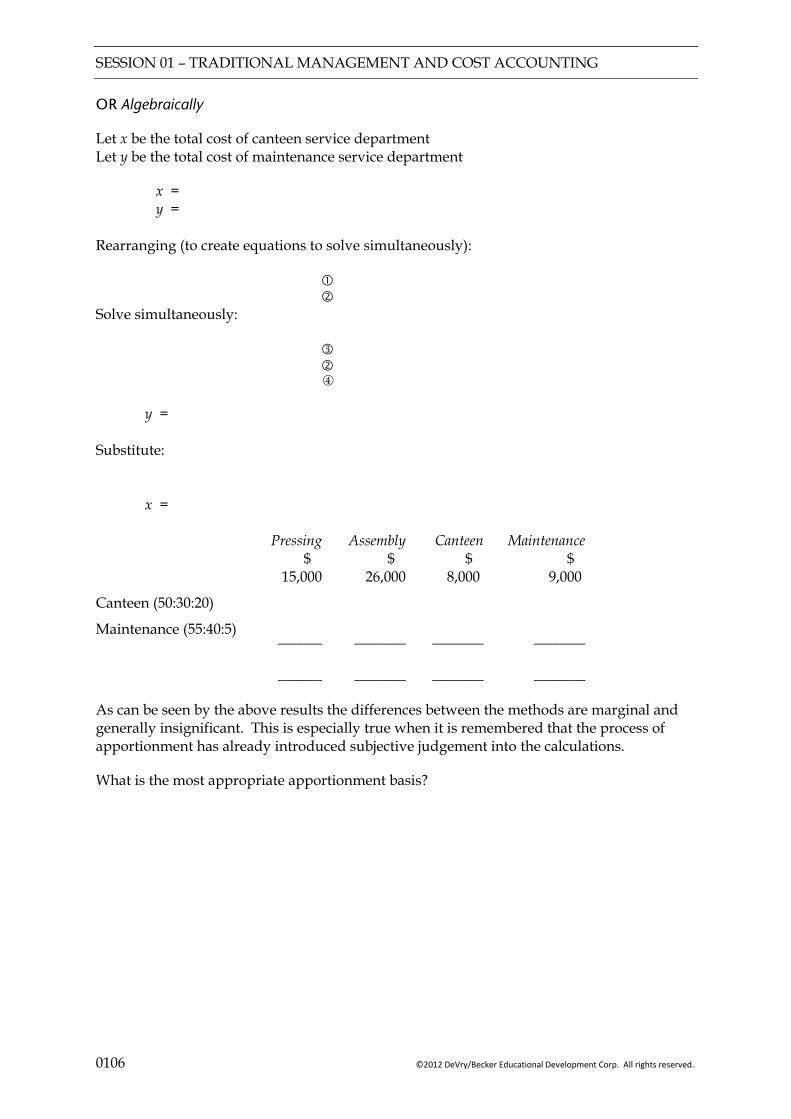

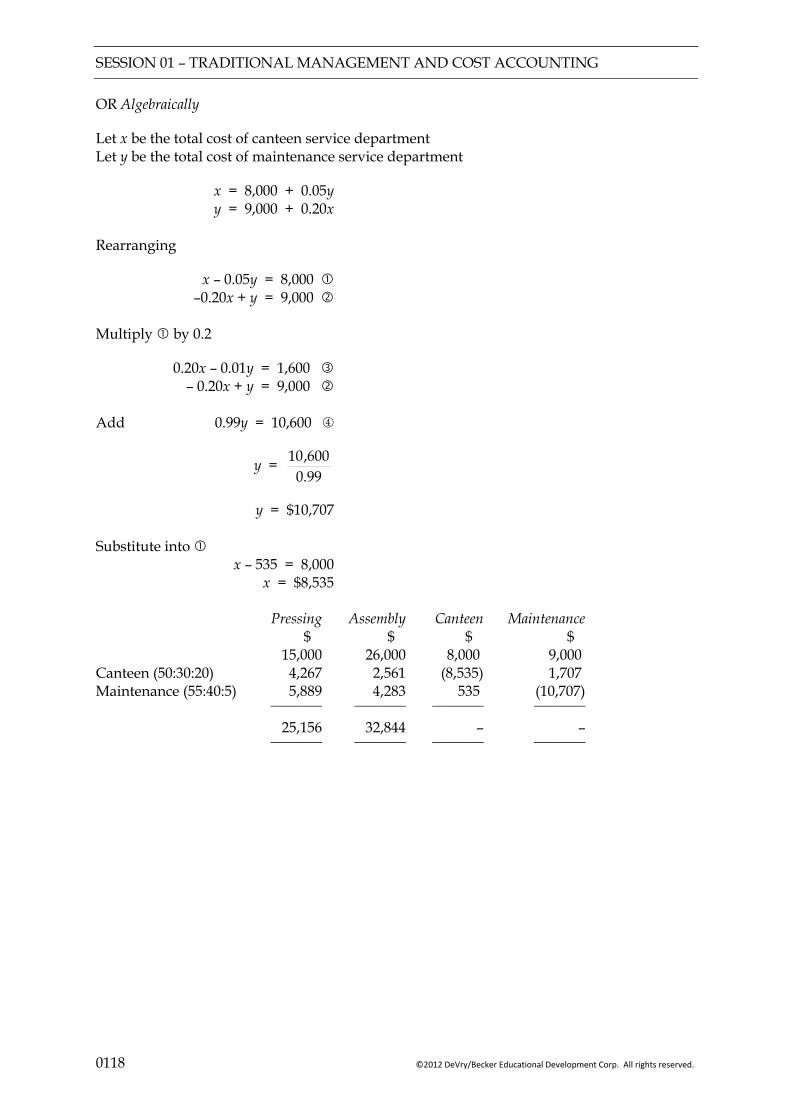

OR Algebraically

Let x be the total cost of canteen service department Let y be the total cost of maintenance service department

x = y =

Rearranging (to create equations to solve simultaneously):

Solve simultaneously:

y = Substitute:

x =

Pressing Assembly Canteen Maintenance $ $ $ $

Canteen (50:30:20)

Maintenance (55:40:5)

15,000

26,000

8,000

9,000

______ ______

_______ _______

_______ _______

_______ _______

As can be seen by the above results the differences between the methods are marginal and generally insignificant. This is especially true when it is remembered that the process of apportionment has already introduced subjective judgement into the calculations.

What is the most appropriate apportionment basis?

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0107

2.5 Absorption

The total of the overheads in each production department must now be absorbed into the units of production.

This is achieved using one of the following methods:

direct labour hour rate; direct material cost rate; direct labour cost rate; prime cost percentage rate; machine hour rate; unit of output rate.

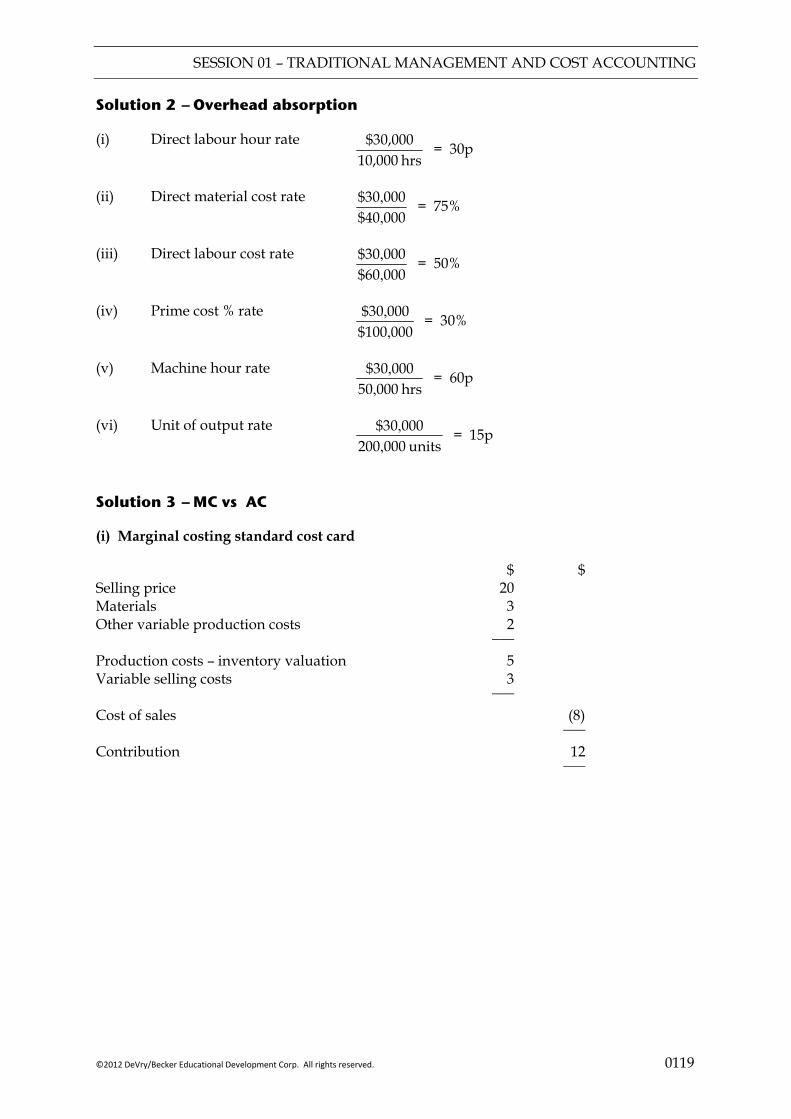

Example 2

X Ltd estimates that its factory costs for the coming year will be as follows:

$ Direct material 40,000 Direct wages 60,000 _______ PRIME COST 100,000 Factory overhead 30,000 _______ Total factory cost 130,000 _______ During the year there will be 100,000 direct labour hours, 50,000 machine hours and 200,000 units will be produced.

Required:

Work out the absorption rate using the following methods:

(i) direct labour hour rate; (ii) direct material cost rate; (iii) direct labour cost rate; (iv) prime cost % rate; (v) machine hour rate; (vi) unit of output rate.

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

0108 ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

Solution

(i) Direct labour hour rate

(ii) Direct material cost rate

(iii) Direct labour cost rate

(iv) Prime cost % rate

(v) Machine hour rate

(vi) Unit of output rate

2.6 Pre-determined overhead rates

As the above figures have been calculated using estimates of costs for the coming year, it is known as a pre-determined overhead absorption rate (POAR). This is then used to apportion the overheads to the products. This rate is generally derived from the budgeted overhead and the normal level of production figures, in order to avoid distortion caused by seasonal fluctuations and to provide a consistent basis for measuring costs.

Finally there are three relevant figures relating to overheads:

originally budgeted overhead; actual overhead spent; overhead absorbed (POAR × Actual activity level).

The difference between (2) and (3) is the under or over absorption which will be adjusted for in the income statement for the period.

> = under-absorption – debit to income statement > = over-absorption – credit to income statement

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0109

2.7 Summary

The diagram below shows the process described above:

PRODUCTION OVERHEADS

PRODUCTION COST

PRODUCTION DEPARTMENT B

SERVICE DEPARTMENT

DIRECT COSTS

Allocation Apportionment Reapportionment Absorption Charging of direct costs

PRODUCTION DEPARTMENT B

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

0110 ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

3 MARGINAL COSTING

3.1 Treatment of fixed overheads

Under marginal costing, fixed overheads are not included in unit costs, but treated as a period cost (i.e. written off in full in the income statement in the period in which they occur).

Inventory valuation includes only the variable costs of production.

Example 3

Budgeted sales and production are 10,000 items.

Standard/Budgeted figures

Selling price = $20 per unit Materials = $3 per unit Other variable production costs = $2 per unit Variable selling costs = $3 per unit Fixed production costs = $40,000 Fixed selling costs = $20,000

Actual figures

Opening inventory = 1,000 units Sales = 9,000 units Production = 11,000 units

Required:

Produce

(i) a marginal costing standard cost card; (ii) an absorption costing standard cost card; (iii) a marginal costing income statement; (iv) an absorption costing income statement.

(Produce income statements assuming that revenues and costs are as originally budgeted.)

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0111

Solution

(i) Marginal costing standard cost card $ $ Selling price

Materials

Other variable production costs

____ Production costs – inventory valuation

Variable selling costs

____ Cost of sales

Contribution

____ ____

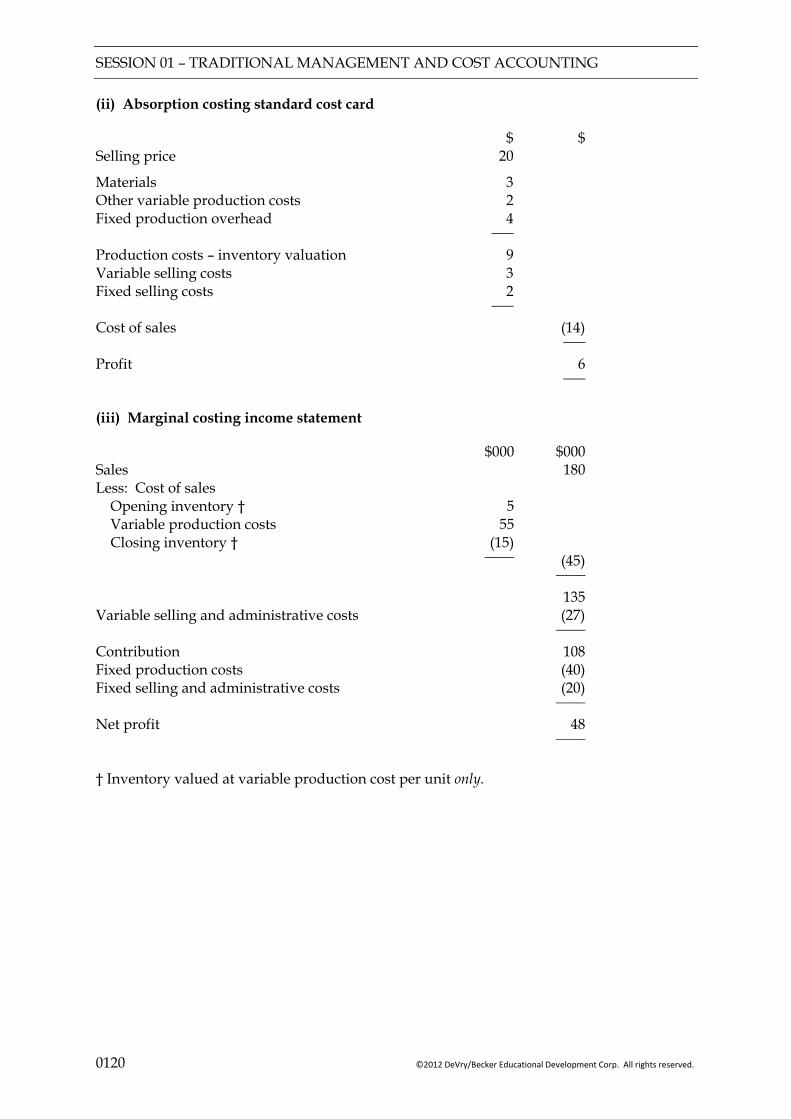

(ii) Absorption costing standard cost card $ $ Selling price

Materials

Other variable production costs

Fixed production overhead

____ Production costs – inventory valuation

Variable selling costs

Fixed selling costs

____ Cost of sales

Profit

____ ____

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

0112 ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

(iii) Marginal costing income statement $000 $000 Sales

Less: Cost of sales

Opening inventory †

Variable production costs

Closing inventory †

____ ____ Variable selling and administrative costs

____ Contribution

Fixed production costs

Fixed selling and administrative costs

Net profit

____ ____

† Inventory valued at variable production cost per unit only.

(iv) Absorption costing income statement $000 $000 Sales

Less: Cost of sales

Opening inventory*

Variable production costs

Fixed production costs

Closing inventory*

____ ____ Gross profit

Fixed selling and administrative costs

Variable selling and administrative costs

Net profit

____ ____

* Inventory valued at variable production cost plus fixed production cost per unit.

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0113

An alternative layout of the absorption costing income statement, which clearly shows the over or under-absorption of overheads, would be as follows:

$000 $000

Sales

Opening inventory

Total production costs Closing inventory

____ ____

Under/over absorption

Overhead absorbed Overhead spent

____

Over absorption

____

Gross profit

Fixed selling and administrative costs

Variable selling and administrative costs

Net profit

____ ____

Example 4

$ Direct variable costs 7 Fixed production overheads 5 __ Total cost 12 __

Selling price 20

Opening inventory 1,000 units

Production 8,000 units per month

Sales Month 1 6,000 units Month 2 8,500 units Month 3 8,000 units

Required:

Produce income statements for months 1–3 using:

(a) total absorption costing; (b) marginal costing.

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

0114 ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

Solution

(a) Absorption costing

Month 1 Month 2 Month 3 $ $ $ $ $ $ Sales

Opening inventory

Variable production costs

Fixed production costs

Closing inventory

_______ _______ _______

Cost of goods sold

Gross profit

_______ _______

_______ _______

_______ _______

(b) Marginal costing

Month 1 Month 2 Month 3 $ $ $ $ $ $ Sales

Opening inventory

Variable production costs

Closing inventory

_______ _______ _______

Cost of goods sold

_______ _______ _______

CONTRIBUTION

Fixed production costs

Gross profit

_______ _______

_______ _______

_______ _______

3.2 Inventory level changes

Change in inventory Effect on profit

(1) (2) (3)

Closing inventory > Opening inventory Closing inventory = Opening inventory Closing inventory < Opening inventory

TAC profit > MC profit TAC profit = MC profit TAC profit < MC profit

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0115

3.3 Profit reconciliation

Using Example 4 figures: Month 1 Month 2 Month3 $ $ $ Marginal cost profit 38,000 70,500 64,000 Difference in profit (Change in stock level × Fixed prodn o/h per unit) 2,000 × $5 500 × $5 10,000 (2,500) − ______ ______ ______ Absorption cost profit 48,000 68,000 64,000 ______ ______ ______

The above profit reconciliation assumes that the fixed overhead absorption rate per unit remains constant. If this were to change, the reconciling difference would become the difference between fixed production costs:

(i) b/f in opening inventory; and (ii) c/f in closing inventory.

3.4 Comparison of methods

Total absorption costing Marginal costing

Inventory valuation Conforms to accounting standards

Prudent valuation

Profits Depends on sales and production (manipulate it by over-inventorying)

Depends on sales

Costing procedures Avoids splitting semi-variable costs

Avoids allocation, apportionment and absorption

Decision-making Pricing More useful and relevant

Cost control Focuses on all costs Focuses on controllable costs

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

0116 ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

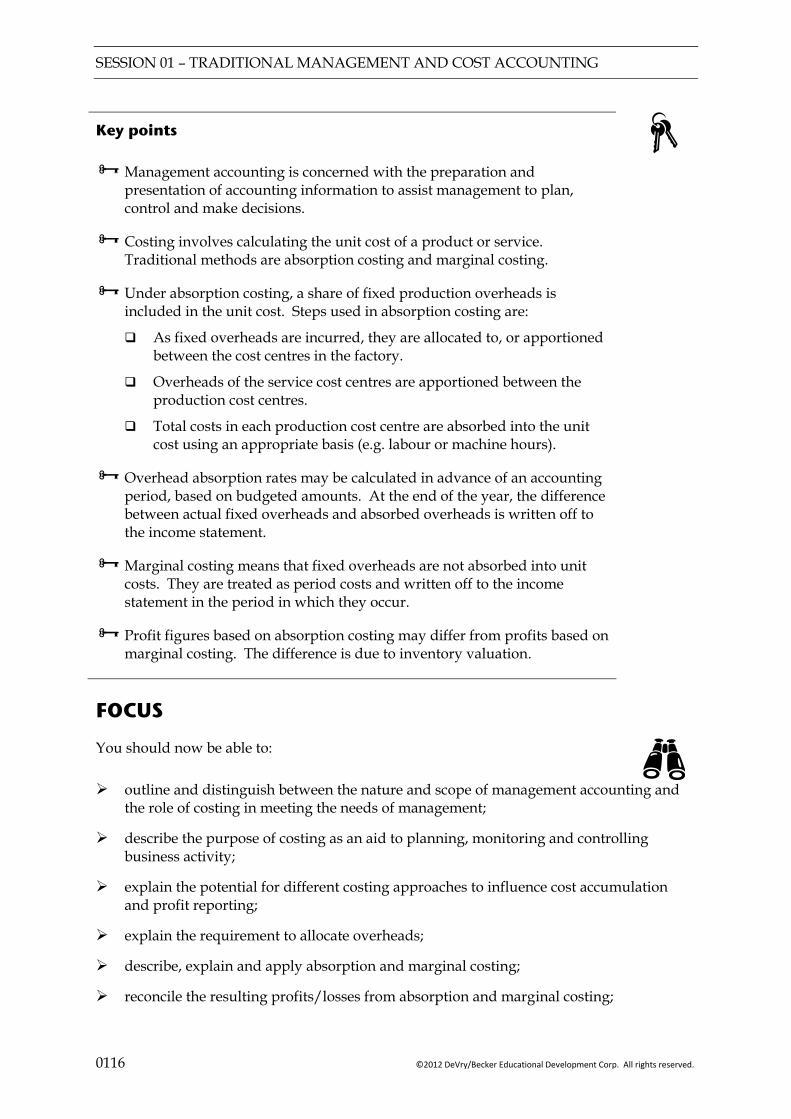

Key points

Management accounting is concerned with the preparation and presentation of accounting information to assist management to plan, control and make decisions.

Costing involves calculating the unit cost of a product or service. Traditional methods are absorption costing and marginal costing.

Under absorption costing, a share of fixed production overheads is included in the unit cost. Steps used in absorption costing are:

As fixed overheads are incurred, they are allocated to, or apportioned between the cost centres in the factory.

Overheads of the service cost centres are apportioned between the production cost centres.

Total costs in each production cost centre are absorbed into the unit cost using an appropriate basis (e.g. labour or machine hours).

Overhead absorption rates may be calculated in advance of an accounting period, based on budgeted amounts. At the end of the year, the difference between actual fixed overheads and absorbed overheads is written off to the income statement.

Marginal costing means that fixed overheads are not absorbed into unit costs. They are treated as period costs and written off to the income statement in the period in which they occur.

Profit figures based on absorption costing may differ from profits based on marginal costing. The difference is due to inventory valuation.

FOCUS

You should now be able to:

outline and distinguish between the nature and scope of management accounting and

the role of costing in meeting the needs of management;

describe the purpose of costing as an aid to planning, monitoring and controlling business activity;

explain the potential for different costing approaches to influence cost accumulation and profit reporting;

explain the requirement to allocate overheads;

describe, explain and apply absorption and marginal costing;

reconcile the resulting profits/losses from absorption and marginal costing;

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0117

EXAMPLE SOLUTIONS

Solution 1 — Service departments

(i) Direct method

Pressing Assembly Canteen Maintenance $ $ $ $ Canteen (50:30) Maintenance (55:40)

15,000 5,000 5,211

26,000 3,000 3,789

8,000 (8,000)

9,000

(9,000) _______

25,211 _______

_______ 32,789 _______

_______ – _______

_______ – _______

(ii) Step method

Pressing Assembly Canteen Maintenance $ $ $ $ Canteen (50:30:20)

15,000 4,000

26,000 2,400

8,000 (8,000)

9,000 1,600

_______ _______ _______ _______ 19,000 28,400 – 10,600 Maintenance (55:40) 6,137 4,463 (10,600) _______

25,137 _______

_______ 32,863 _______

_______ – _______

_______ – _______

(iii) Reciprocal method

Repeated distribution Pressing Assembly Canteen Maintenance $ $ $ $ Canteen (50:30:20)

15,000 4,000

26,000 2,400

8,000 (8,000)

9,000 1,600

_______ _______ Maintenance (55:40:5)

5,830

4,240

– 530

10,600 (10,600)

_______ _______ Canteen (50:30:20)

265

159

530 (530)

– 106

_______ _______ Maintenance (55:40:5)

58

42

– 6

106 (106)

_______ _______ Canteen (50:30:20)

3

3

6 (6)

–

_______ 25,156 _______

_______ 32,844 _______

_______ – _______

_______ – _______

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

0118 ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

OR Algebraically

Let x be the total cost of canteen service department Let y be the total cost of maintenance service department

x = 8,000 + 0.05y y = 9,000 + 0.20x

Rearranging

x – 0.05y = 8,000 –0.20x + y = 9,000

Multiply by 0.2

0.20x – 0.01y = 1,600 – 0.20x + y = 9,000

Add 0.99y = 10,600

y = 99.0600,10

y = $10,707 Substitute into x – 535 = 8,000

x = $8,535

Pressing Assembly Canteen Maintenance $ $ $ $ Canteen (50:30:20) Maintenance (55:40:5)

15,000 4,267 5,889

26,000 2,561 4,283

8,000 (8,535)

535

9,000 1,707

(10,707) _______

25,156 _______

_______ 32,844 _______

_______ – _______

_______ – _______

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0119

Solution 2 — Overhead absorption

(i) Direct labour hour rate hrs 10,000

$30,000 = 30p

(ii) Direct material cost rate 00040$00030$

,, = 75%

(iii) Direct labour cost rate 00060$00030$

,, = 50%

(iv) Prime cost % rate 000100$

00030$,, = 30%

(v) Machine hour rate hrs 00050

00030$,

, = 60p

(vi) Unit of output rate units 000200

000$30,

, = 15p

Solution 3 — MC vs AC

(i) Marginal costing standard cost card

$ $ Selling price 20 Materials Other variable production costs

3 2

___ Production costs – inventory valuation Variable selling costs

5 3

___ Cost of sales (8) Contribution

___ 12 ___

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

0120 ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

(ii) Absorption costing standard cost card

$ $ Selling price 20

Materials Other variable production costs Fixed production overhead

3 2 4

___ Production costs – inventory valuation Variable selling costs Fixed selling costs

9 3 2

___ Cost of sales (14) Profit

___ 6 ___

(iii) Marginal costing income statement

$000 $000 Sales 180 Less: Cost of sales Opening inventory † Variable production costs Closing inventory †

5 55

(15)

____ (45) ____ 135 Variable selling and administrative costs (27) ____ Contribution Fixed production costs Fixed selling and administrative costs

108 (40) (20)

Net profit

____ 48 ____

† Inventory valued at variable production cost per unit only.

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0121

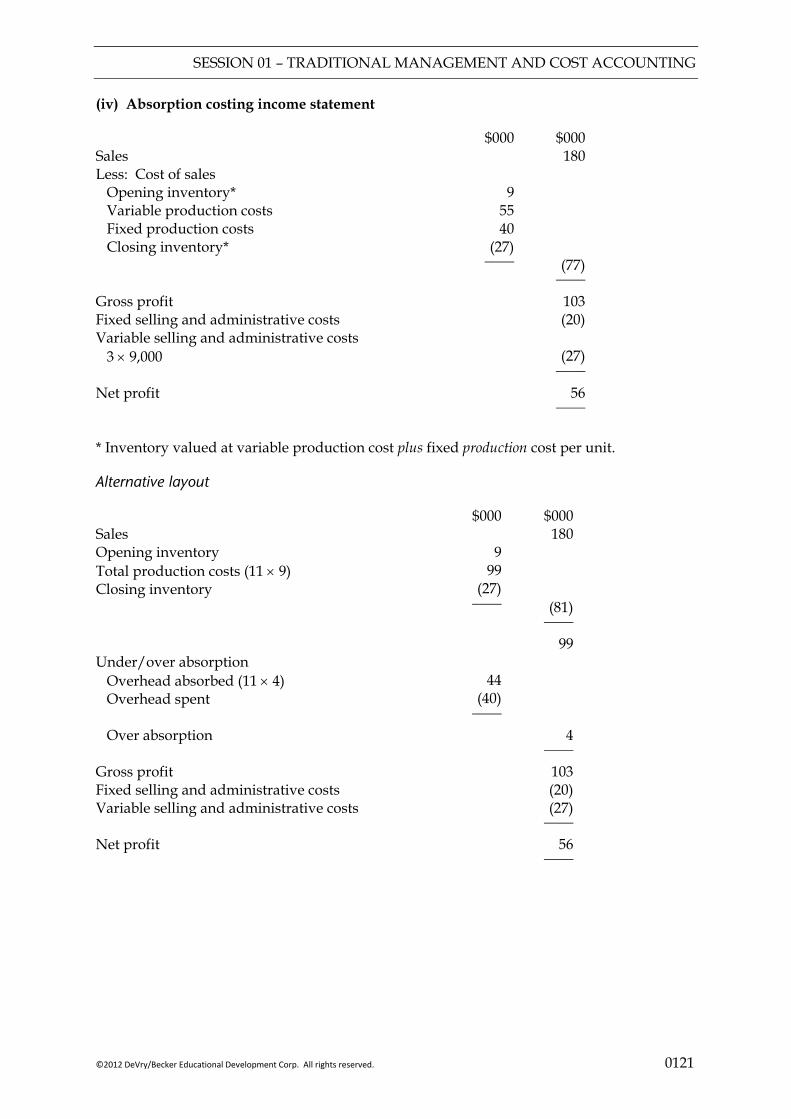

(iv) Absorption costing income statement

$000 $000 Sales 180 Less: Cost of sales Opening inventory* Variable production costs Fixed production costs Closing inventory*

9 55 40

(27)

____ (77) ____ Gross profit Fixed selling and administrative costs Variable selling and administrative costs 3 × 9,000

103 (20)

(27)

Net profit

____ 56 ____

* Inventory valued at variable production cost plus fixed production cost per unit.

Alternative layout

$000 $000 Sales Opening inventory Total production costs (11 × 9) Closing inventory

9

99 (27)

180

____ (81) ____ 99 Under/over absorption Overhead absorbed (11 × 4) Overhead spent

44 (40)

____ Over absorption 4 ____ Gross profit Fixed selling and administrative costs Variable selling and administrative costs

103 (20) (27)

Net profit

____ 56 ____

SESSION 01 – TRADITIONAL MANAGEMENT AND COST ACCOUNTING

0122 ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

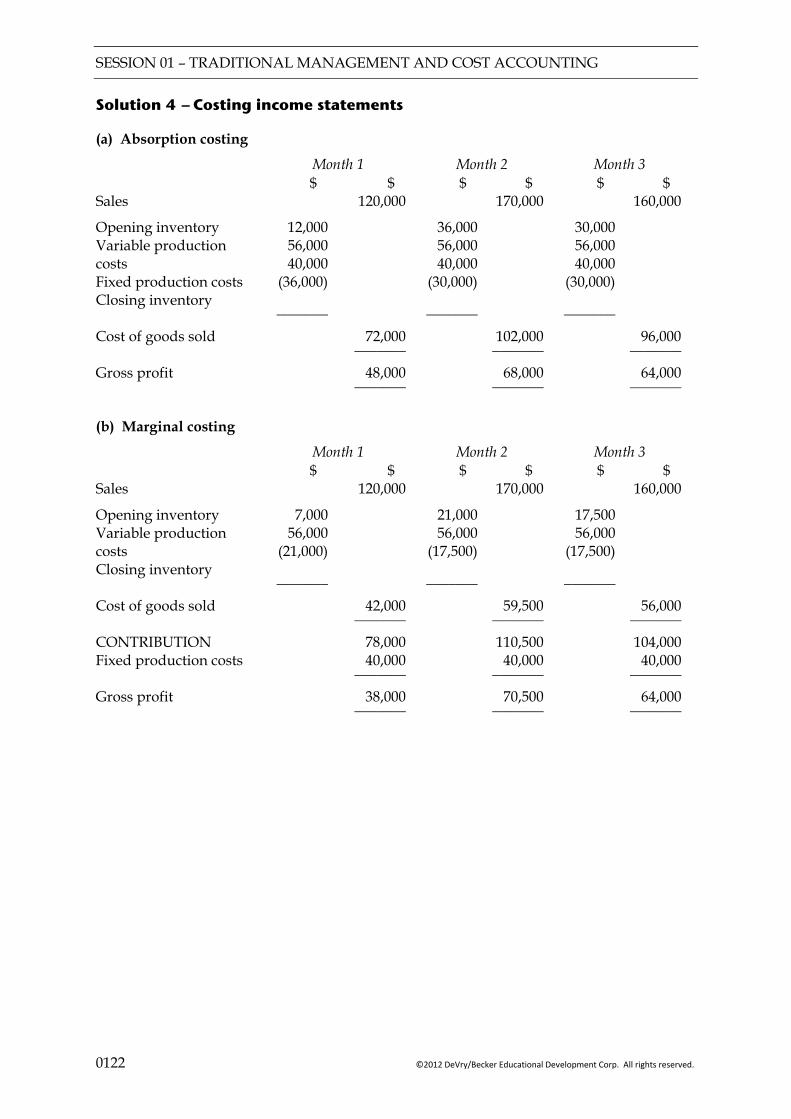

Solution 4 — Costing income statements

(a) Absorption costing

Month 1 Month 2 Month 3 $ $ $ $ $ $ Sales 120,000 170,000 160,000

Opening inventory Variable production costs Fixed production costs Closing inventory

12,000 56,000 40,000

(36,000)

36,000 56,000 40,000

(30,000)

30,000 56,000 40,000

(30,000)

_______ _______ _______ Cost of goods sold 72,000 102,000 96,000 Gross profit

_______ 48,000 _______

_______ 68,000 _______

_______ 64,000 _______

(b) Marginal costing

Month 1 Month 2 Month 3 $ $ $ $ $ $ Sales 120,000 170,000 160,000

Opening inventory Variable production costs Closing inventory

7,000 56,000

(21,000)

21,000 56,000

(17,500)

17,500 56,000

(17,500)

_______ _______ _______ Cost of goods sold 42,000 59,500 56,000 _______ _______ _______ CONTRIBUTION Fixed production costs

78,000 40,000

110,500 40,000

104,000 40,000

Gross profit

_______ 38,000 _______

_______ 70,500 _______

_______ 64,000 _______

SESSION 02 – ACTIVITY BASED COSTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0201

OVERVIEW

Objective

To consider the differences between traditional costing systems and activity based costing.

ACTIVITY BASED COSTING

PRODUCT COST

COST DRIVERS

ANALYSIS

Definition Steps

Definition Advantages Disadvantage

Calculation

SESSION 02 – ACTIVITY BASED COSTING

0202 ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

1 ACTIVITY BASED COSTING

Definition

Activity-based costing (ABC) is an approach to costing and activity monitoring which assigns resources consumed to activities and activities to cost objects (based on estimated consumption). Cost drivers are used to apportion activity costs to output.

Commentary “ABC” as a costing method is not to be confused with ABC inventory systems.

This approach for calculating product costs was developed by Cooper and Kaplan.

It recognises that traditional ideas of fixed and variable cost categorisations are not always appropriate and that, as the proportion of overhead costs in manufacture has increased, there is a need for a more accurate method of absorbing these costs into cost units.

It looks for a clearer picture of cost behaviour and a better understanding of what determines the level of costs (i.e. “cost drivers”).

1.1 Steps

To find total product costs, overheads are traced to individual production departments, as usual, with common costs being apportioned using suitable bases.

SESSION 02 – ACTIVITY BASED COSTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0203

Then

Identify major activities within each

department which create cost

Determine what causes the cost of each activity – the “cost

driver”

Create a cost centre/cost pool

for each activity – the “activity cost pool”

Step 1

Step 2

Step 3

Step 4

Examples (1) Production scheduling (2) Machining (3) Despatching of orders (4) Inspections (1) Number of batch set-ups for production

scheduling (2) Machine hours for machining (3) Number of despatch orders for

despatching (4) Number of inspections Cost pool for: (1) all production scheduling costs (2) all machining costs (3) all despatching costs (4) all inspection costs Cost per (1) batch set up (2) machine hour (3) despatch order (4) inspection E.g. Product Z (1) No of batch set ups for Product Z × Cost per batch set up x (2) No of machine hours for Product Z × Cost per machine hour x (3) No of despatch orders for Product Z × Cost per despatch order x (4) No of inspections for Product Z × Cost per inspection x ___ y ___ E.g. Product Z

Overhead cost per unit = produced Zs of Noy

Calculate an absorption rate

for each “cost driver”

Calculate the total overhead cost

for manufacturing each product

Calculate overhead

cost per unit

Step 5

Step 6

Having discovered the cost drivers within the business, the original production departments may be re-organised to take advantage of potential cost savings.

SESSION 02 – ACTIVITY BASED COSTING

0204 ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

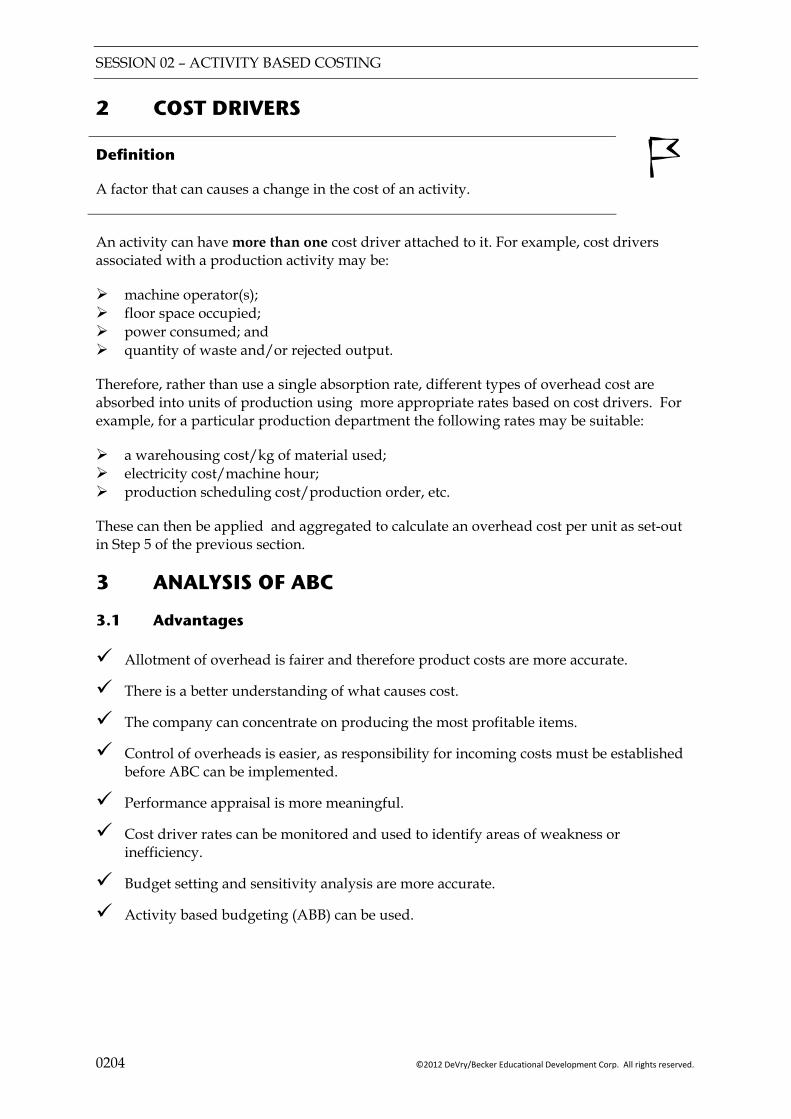

2 COST DRIVERS

Definition

A factor that can causes a change in the cost of an activity.

An activity can have more than one cost driver attached to it. For example, cost drivers associated with a production activity may be:

machine operator(s); floor space occupied; power consumed; and quantity of waste and/or rejected output.

Therefore, rather than use a single absorption rate, different types of overhead cost are absorbed into units of production using more appropriate rates based on cost drivers. For example, for a particular production department the following rates may be suitable:

a warehousing cost/kg of material used; electricity cost/machine hour; production scheduling cost/production order, etc.

These can then be applied and aggregated to calculate an overhead cost per unit as set-out in Step 5 of the previous section.

3 ANALYSIS OF ABC

3.1 Advantages

Allotment of overhead is fairer and therefore product costs are more accurate.

There is a better understanding of what causes cost.

The company can concentrate on producing the most profitable items.

Control of overheads is easier, as responsibility for incoming costs must be established before ABC can be implemented.

Performance appraisal is more meaningful.

Cost driver rates can be monitored and used to identify areas of weakness or inefficiency.

Budget setting and sensitivity analysis are more accurate.

Activity based budgeting (ABB) can be used.

SESSION 02 – ACTIVITY BASED COSTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0205

Definition

Activity-based budgeting (ABB) is a budgeting method based on an activity framework which uses cost driver data in the processes of budget-setting and variance feedback.

New products can be designed to utilise efficient cost drivers. Cost can be designed out

of products.

When cost plus methods of pricing are used, prices based on ABC are likely to reflect more accurately the true cost of producing a product.

3.2 Disadvantages

ABC may be based on historic information but could be used for future strategic decisions.

Selection of cost drivers may not be easy.

Additional time and cost of setting up and administering the system.

Cost measurement may not be easy.

Exclusion of non-production overheads can be difficult.

Assessing the degree of completion of work in progress with respect to each cost driver is difficult.

Variance analysis is complicated.

Many judgemental decisions still required in the construction of an ABC system.

SESSION 02 – ACTIVITY BASED COSTING

0206 ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

4 PRODUCT COST

4.1 Calculation

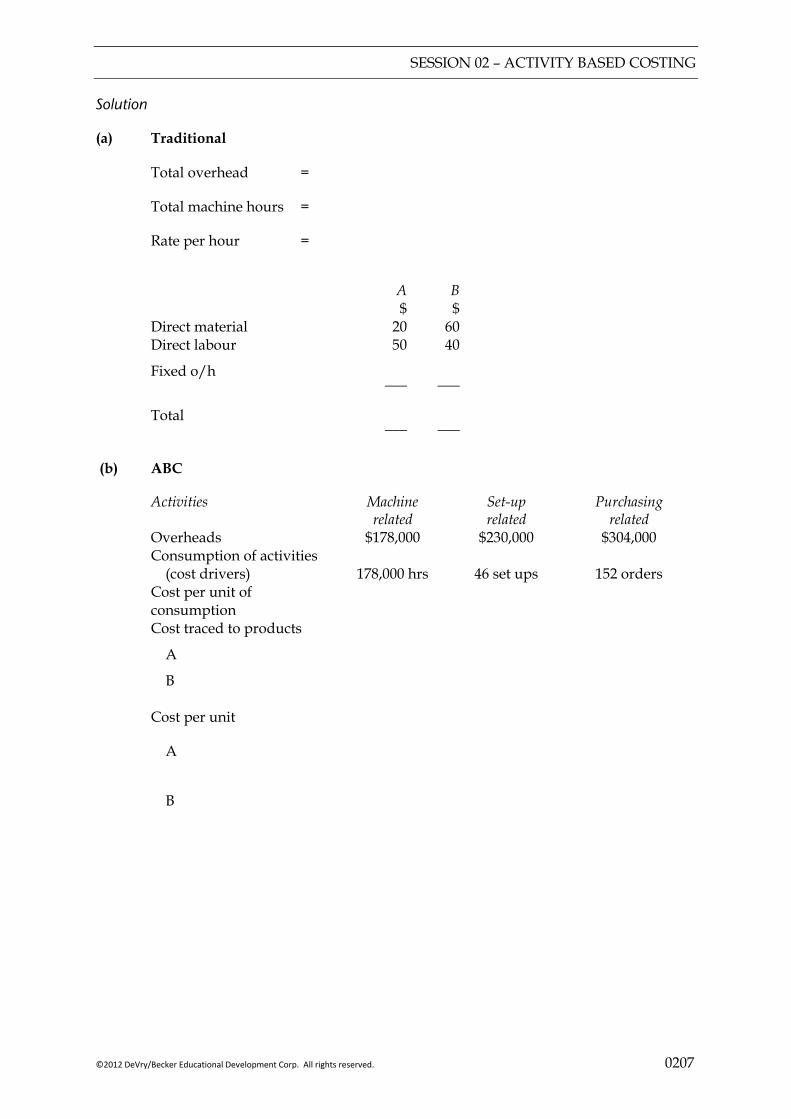

Example 1

Total budgeted fixed overheads for a firm are $712,000. These have traditionally been absorbed on a machine hour basis. The firm makes two products, A and B.

A B

Direct material cost $20 $60 Direct labour cost $50 $40 Machine time 3 hrs 4 hrs Annual output 6,000 40,000

Required:

(a) Calculate the total cost for each product on the assumption that the firm continues to absorb overheads on a machine hours’ basis.

(b) The firm is considering changing to an activity based costing system and has identified the following information:

Machine Annual Total Number of Number of hours/unit output machine hours set ups purchase orders Product A 3 6,000 18,000 16 52 Product B 4 40,000 160,000 30 100

_______ _______ _______ _______ 46,000 178,000 46 152

_______ _______ _______ _______ Cost pools: Cost driver: $ Machine related 178,000 Machine hours Set-up related 230,000 Set-ups Purchasing related 304,000 Purchase orders

_______ Total overheads 712,000

_______ Required:

Calculate the cost per unit using the ABC system.

SESSION 02 – ACTIVITY BASED COSTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0207

Solution

(a) Traditional

Total overhead =

Total machine hours =

Rate per hour =

A $

B $

Direct material Direct labour

20 50

60 40

Fixed o/h

___ ___ Total

___ ___ (b) ABC

Activities Machine related

Set-up related

Purchasing related

Overheads $178,000 $230,000 $304,000 Consumption of activities

(cost drivers)

178,000 hrs

46 set ups

152 orders Cost per unit of

consumption

Cost traced to products A

B

Cost per unit

A

B

SESSION 02 – ACTIVITY BASED COSTING

0208 ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

A

$ B $

Direct material Direct labour

Fixed overhead

20.00 50.00

60.00 40.00

______ ______

Total

______ ______

Key points

Activity based costing aims to provide a more reliable calculation of the cost of a product, by relating the cost to the activities used in producing it.

Steps in ABC:

Identify the activities which cause costs to be incurred.

Identify the drivers related to each activity (a driver is a factor that causes the cost of the activity to rise).

Costs are allocated and apportioned between “activity pools” – where each pool represents an activity.

The absorption rate per unit of driver is calculated.

The product cost is calculated using absorption rates based on the drivers.

The main advantage of ABC is that it focusses on “more accurate” costs.

The main disadvantage is its complexity, which makes it inappropriate for many organisations.

FOCUS

You should now be able to:

identify appropriate cost drivers under ABC;

calculate costs per driver and per unit using ABC;

compare ABC and traditional methods of overhead absorption based on production units, labour hours or machine hours.

SESSION 02 – ACTIVITY BASED COSTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0209

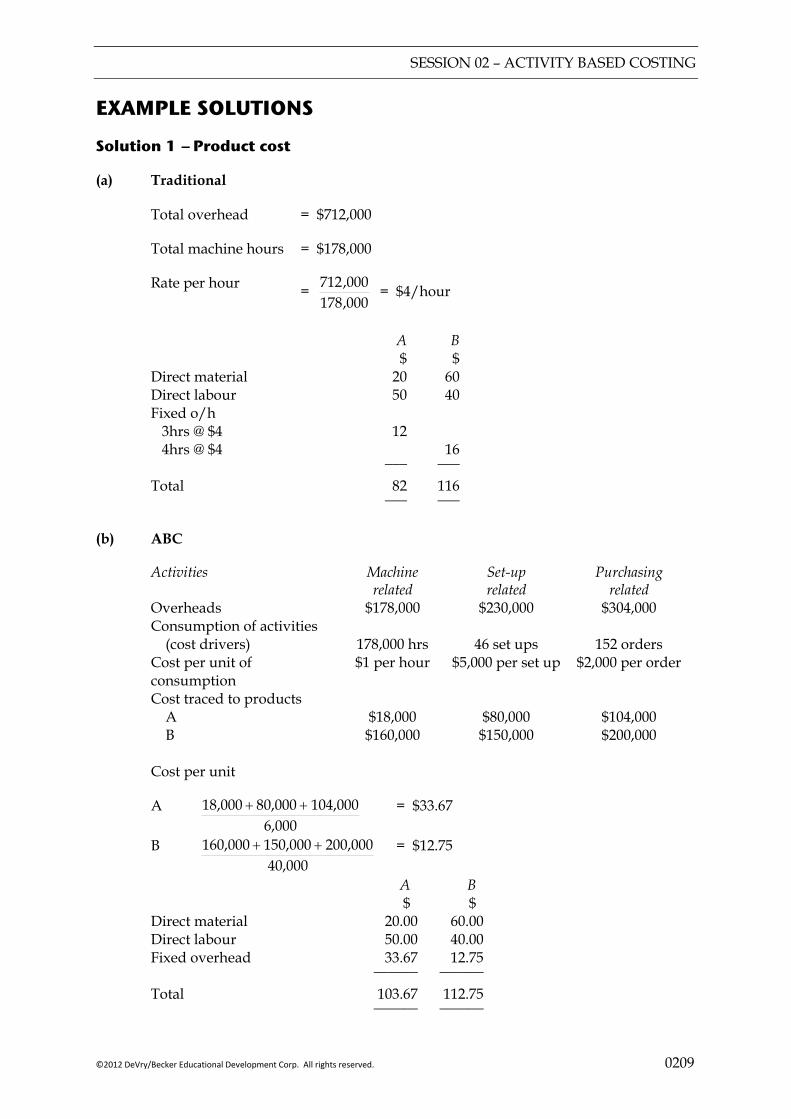

EXAMPLE SOLUTIONS

Solution 1 — Product cost

(a) Traditional

Total overhead = $712,000

Total machine hours = $178,000

Rate per hour = 000,178000,712 = $4/hour

A

$ B $

Direct material Direct labour

20 50

60 40

Fixed o/h 3hrs @ $4

4hrs @ $4 12

16 ___ ___ Total 82 116 ___ ___ (b) ABC

Activities Machine related

Set-up related

Purchasing related

Overheads $178,000 $230,000 $304,000 Consumption of activities

(cost drivers)

178,000 hrs

46 set ups

152 orders Cost per unit of

consumption $1 per hour $5,000 per set up $2,000 per order

Cost traced to products A

B $18,000 $160,000

$80,000 $150,000

$104,000 $200,000

Cost per unit

A 6,000

104,000 80,000 18,000 ++ = $33.67

B 40,000

200,000 150,000 160,000 ++ = $12.75

A $

B $

Direct material Direct labour Fixed overhead

20.00 50.00 33.67

60.00 40.00 12.75

______ ______

Total 103.67 112.75 ______ ______

SESSION 02 – ACTIVITY BASED COSTING

0210 ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

SESSION 03 – DEVELOPMENTS IN MANAGEMENT ACCOUNTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0301

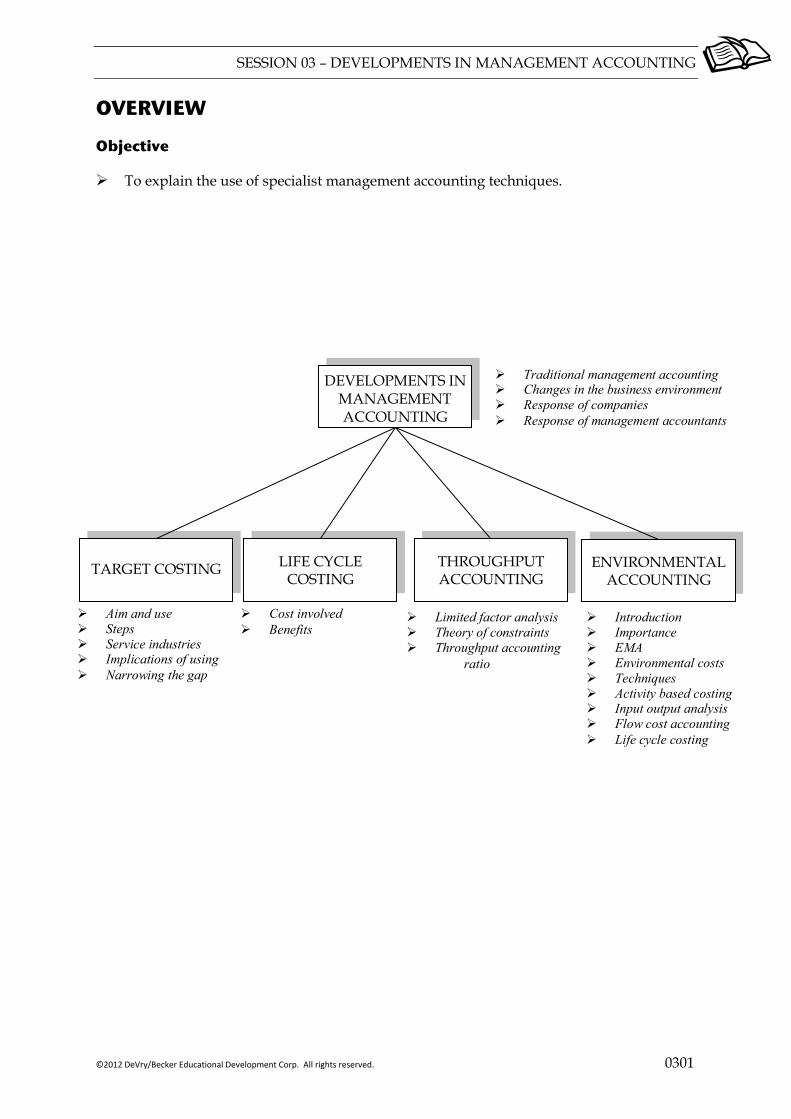

OVERVIEW

Objective

To explain the use of specialist management accounting techniques.

TARGET COSTING

Traditional management accounting Changes in the business environment Response of companies Response of management accountants

THROUGHPUT ACCOUNTING

DEVELOPMENTS IN MANAGEMENT ACCOUNTING

Aim and use Steps Service industries Implications of using Narrowing the gap

LIFE CYCLE COSTING

Limited factor analysis Theory of constraints Throughput accounting

ratio

Cost involved Benefits

ENVIRONMENTAL ACCOUNTING

Introduction Importance EMA Environmental costs Techniques Activity based costing Input output analysis Flow cost accounting Life cycle costing

SESSION 03 – DEVELOPMENTS IN MANAGEMENT ACCOUNTING

0302 ©2012 DeVry/Becker Educational Development Corp. All rights reserved.

1 DEVELOPMENTS IN MANAGEMENT ACCOUNTING

1.1 Traditional management accounting

Traditional management accounting was inward looking, focusing on controlling costs. You are already familiar with many of the techniques used in traditional management accounting from earlier papers. The most important of these are:

Costing systems (marginal and absorption costing); Budgeting systems; Standard costing and variance analysis; Working capital management

1.2 Changes in the business environment

During the 1950s and 1960s, the Western industrialised nations enjoyed strong positions in international markets. There was little competition either on price or quality. Businesses could continue to be successful by just continuing to do what they had always done. During the 1970s however, this stable business world began to disappear:

Less protection in home markets and increased globalisation led to increased competition from newly emerging industrialised nations (particularly Japan).

Introduction of computerised manufacturing systems led to the opportunity to reduce manufacturing costs while increasing quality of products.

Products’ life cycles began to fall so there was increased demand for new products from consumers.

The growth of service industries.

Business combinations resulted in larger multi-national organisations with diverse operations.

Change in the structure of business with more decentralised decision making.

1.3 Response of companies

Two developments in the commercial world are worth specific mention:

1.3.1 Total Quality Management (TQM)

Definition

Total quality management consists of continuous improvement in activities involving everyone in the organisation, managers and workers, in a totally integrated effort towards improving performance at every level.

Commentary TQM is a philosophy of getting it right first time. It is recognised that the costs of bad quality may exceed the costs of good quality. Quality is considered in more detail in a later session.

SESSION 03 – DEVELOPMENTS IN MANAGEMENT ACCOUNTING

©2012 DeVry/Becker Educational Development Corp. All rights reserved. 0303

1.3.2 Weaknesses of traditional western approach

The traditional western approach to manufacturing was to produce maximum capacity. Production was driven by internal plans rather than external demand. This led to:

Excessive holding of inventory with the associated costs of storage and obsolescence;

Delays between customer ordering products and the delivery of the products;