ANNUAL REPORT 2013 Panoro Energy

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

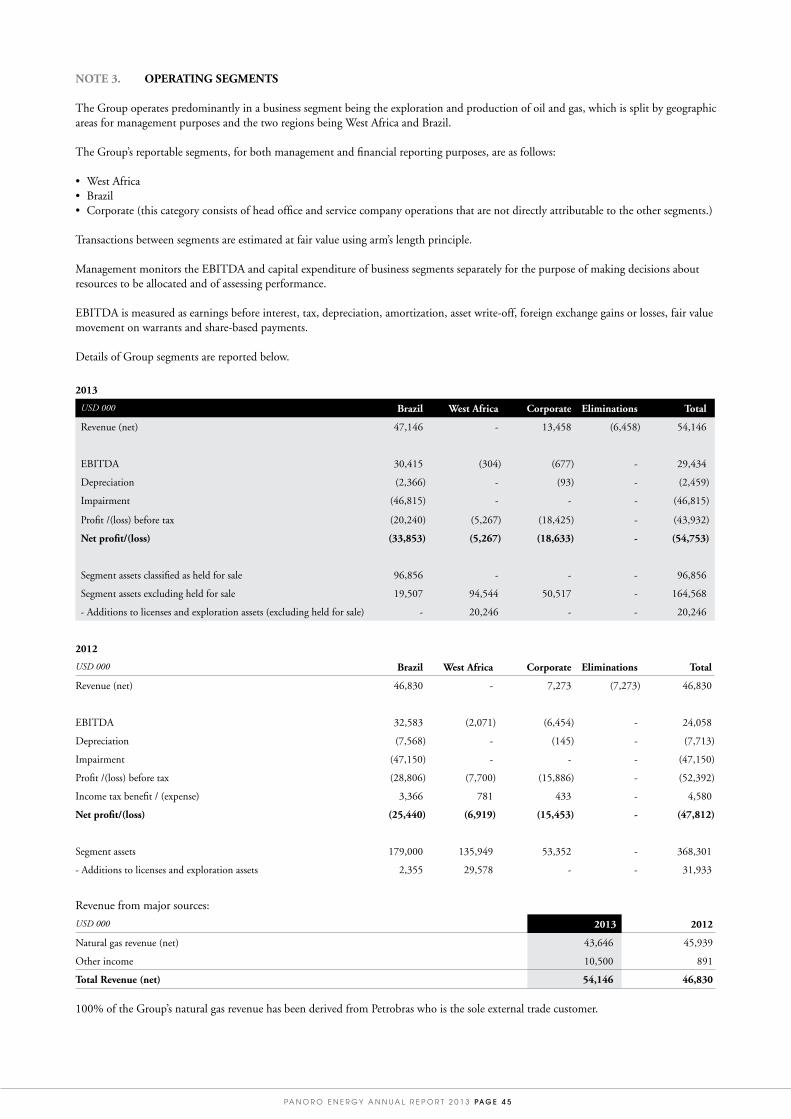

Transcript

PA

NO

RO

EN

ER

GY

AN

NU

AL

RE

PO

RT

20

13

A N N U A L R E P O R T 2 0 1 3

P a n o r o E n e r g y

C O M PA N Y O V E R V I E W

Panoro Energy ASA is an independent E&P company with assets

in the South Atlantic region. The Company has offices in Oslo,

London and Rio de Janeiro. The Company is listed on the Oslo Stock

Exchange with ticker “PEN”.

PA G E 2 PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3

FINANCIAL CALENDAR

May 15, 2014First quarter 2014 results and Annual General Meeting

August 14, 2014Second quarter 2014 results

November 6, 2014Third quarter 2014 results

CONTENTS

Company Overview 2

Assets 4

CEO letter 6

Company Operations 8

Reserves and Contingent Resources 12

Directors’ Report 2013 16

Board of Directors 24

Senior Management 26

Consolidated Statement of Comprehensive Income 28

Notes to the Consolidated Financial Statements 32

Panoro Energy ASA Parent Company Income Statement 68

Panoro Energy ASA Notes to the Financial Statements 71

Auditor’s Report 84

Statement on Corporate Governance in Panoro Energy ASA 86

Corporate Social Responsibility/ Ethical Code of Conduct 92

Glossary and Definitions 94

PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3 PA G E 3

C O M PA N Y O V E R V I E W

KEY FIGURES 2013

Net revenues (USD million) 54.1

EBITDA (USD million) 29.4

EBIT (USD million) (21.8)

Net profit/loss (USD million) (54.8)

2P Reserves (MMBOE) 10.0

2C Contingent Resources (MMBOE) 65.5

2013 Production of gas and condensate (BOE/day) 3,822

Share price December 31, 2013 (NOK) 3.05

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2011 20132012

BOE/day

2

3

4PanoroNOK/share

January 2013 December 2013

OSEBX

SHARE PRICE DEVELOPMENTMANATI NET PRODUCTION

HIGHLIGHTS AND EVENTS

• EBITDA of USD 29.4 million• Group production of 3,822 BOE/day (gas plus condensate)• Drilled a discovery well in Gabon• Entered into agreement to sell the Brazilian subsidiary Rio das

Contas for USD 140 million plus a contingent earn out of up to USD 20 million

• Divested the Mengo-Kundji-Bindi asset, onshore Republic of Congo (Brazzaville)

• Impairment charge of USD 46.2 million on BS-3 assets and USD 0.6 million on Round 9 assets in Brazil

• Concluded on the strategic review process and decided to put the Company up for sale

2013 HIGHLIGHTS

PA G E 4 PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3

GABON

• 33.33% interest (30% post back in right exercise) in Dussafu Marin permit, offshore

NIGERIA

• 6.502% participating interest (12.19% revenue interest and 16.255% paying interest) in OML 113 Aje field, offshore

BRAZIL

• 10% interest Manati gas field (BCAM-40 block), pipeline, gas plant and production platform, Camamu-Almada Basin (divested in 2014)

• 10% interest Camarão Norte discovery (BCAM-40 block), Camamu-Almada Basin (divested in 2014)

• 65% interest Estrela do Mar field, Santos Basin (relinquishment process)

• 50% interest Cavalo Marinho field, Santos Basin (relinquishment process)

A S S E T S

PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3 PA G E 5

Offices

Panoro License area

Panoro Offices

PA G E 6 PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3

C E O L E T T E R

Dear Shareholders,2013 was an eventful year for Panoro Energy during which our main focus was to execute on the announced divestment strategy, reduce G&A cost and reshape the Company. This was necessary in order to position the Company as an attractive investment opportunity. A strategic review process in close dialog with our shareholders was undertaken which concluded that the preferred way forward would be to divest the Company. This process is currently ongoing.

In May 2013, Panoro entered into a Sales and Purchase Agreement with GeoPark to sell the Brazilian subsidiary Rio das Contas which holds the 10% interest in the Manati field. The transaction with GeoPark was concluded in March 2014 and Panoro received the settlement of USD 140 million. The majority of the funds were used to repay the outstanding bond debt which resulted in a debt free company. The sale of Rio das Contas was part of the strategic decision to exit Brazil.

In June 2013, the Company entered into an agreement to divest our interest in the OML 113 asset in Nigeria to Lekoil. However, Lekoil decided to terminate the Sale and Purchase Agreement and as a result paid Panoro USD 7 million in break-fee compensation.

In July 2013, we successfully divested our 20% working interest in the onshore MKB asset in Congo to the Congolese national oil company Societe Nationale des Petroles du Congo (SNPC).

The production from the Manati field continued to be strong throughout the year and the periodic five year shutdown was successfully completed as planned with no significant findings. Panoro will continue to have an indirect interest in Manati going forward through the agreement for an earn-out payment linked to the future production of the field which can add up to USD 20 million.Divesting the asset allowed us to repay all our debt and market ourselves as a pure play West African focused company. Panoro has two near term production assets in Nigeria and Gabon. Both assets have the potential to become “company makers”.

In Gabon, the Tortue exploration campaign was completed in February 2013 and resulted in an oil discovery in the offshore wildcat well Dussafu Tortue Marin. Hydrocarbons were discovered in both the pre-salt Gamba reservoir and the Dentale reservoir. Together with the previous discoveries made in the Dussafu permit the field is believed to have sufficient recoverable reserves to allow for a field development. The partners are preparing for a fast-track cluster development of Tortue, Ruche and Walt Whitman with first oil being targeted in 2016. We are excited about the development of this asset.

In the last quarter of 2013, a 3D seismic acquisition program was executed covering the outboard area of the permit previously only covered by 2D, as well as overshooting the Tortue and Ruche

discoveries. The interpretation of the new seismic is expected to be completed in the second half of 2014 and we hope this will provide improved data that could upgrade some very significant size leads into drillable prospects.

In Nigeria, the Joint Venture partners in the OML113 license are moving forward with the plan to commercialize the Aje field. In Q1 2014 the Joint Venture partners received approval of the Field Development Plan (FDP) from the Nigerian authorities. The FDP is primarily focused on the development of the Cenomanian Oil reservoir and includes two subsea production wells, tied back to a leased FPSO. The FDP envisages first oil commencing in Q4 2015. The Aje Joint Venture will take a Final Investment Decision in the next few months. Future phases of the project will likely target additional Cenomanian wells and a later Turonian/Albian gas condensate project is currently considered as a separate development in the future.

The Coral asset in Brazil was relinquished in 2013 and ANP sent a notice requesting relinquishment of the two remaining BS-3 assets Cavalo Marinho and Estrela do Mar based on the assertion that the consortia had not met the development requirements set by the ANP. These requirements included the drilling of one ADR (Advanced Data Recovery) well to test the B-1 zone on each of the concessions. These wells were not part of the original development plan and the requirements would force the concession holders to conduct potentially uneconomic development activities. As a result, the partners decided to initiate a joint farm out process which included offering operatorship of all the BS-3 blocks, however, due to lack of interest from potential buyers the process was terminated in Q1 2014 and the Company took actions to exit the licenses. Consequently, the Company impaired the remaining two licenses in BS-3; Cavalo Marinho and Estrela do Mar at year end.

2013 has been a transformational year for Panoro and the Company is now well positioned ahead of the sale process that has been initiated. We have made solid progress in our plan to reduce core G&A costs throughout the year to align the size of the organization with the activity level. Following the closing of the divestment of Rio das Contas in the first quarter of 2014 the Company had 10 employees compared with 30 at the end of 2012. We have cleaned up our balance sheet and we have a solid financial platform that will ensure that we can meet all financial commitments. We have two exciting assets that are located in two highly attractive hydrocarbon rich areas.

The Company is now positioned to take the next step and demonstrate value creation to our shareholders. I would like to thank shareholders for their feedback, support and continued commitment.

Jan Kielland CEO, Panoro Energy ASA

PA G E 8 PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3

C O M PA N Y O P E R A T I O N S

Panoro Energy currently has assets in West-Africa and Brazil. In West Africa, the Company is

engaged in projects in Gabon and Nigeria, having divested its interest In Congo Brazzaville during

2013. The Company has announced that it will exit Brazil, but at year end 2013 the Company still

had interests in three projects in Brazil of which one is a producing field.

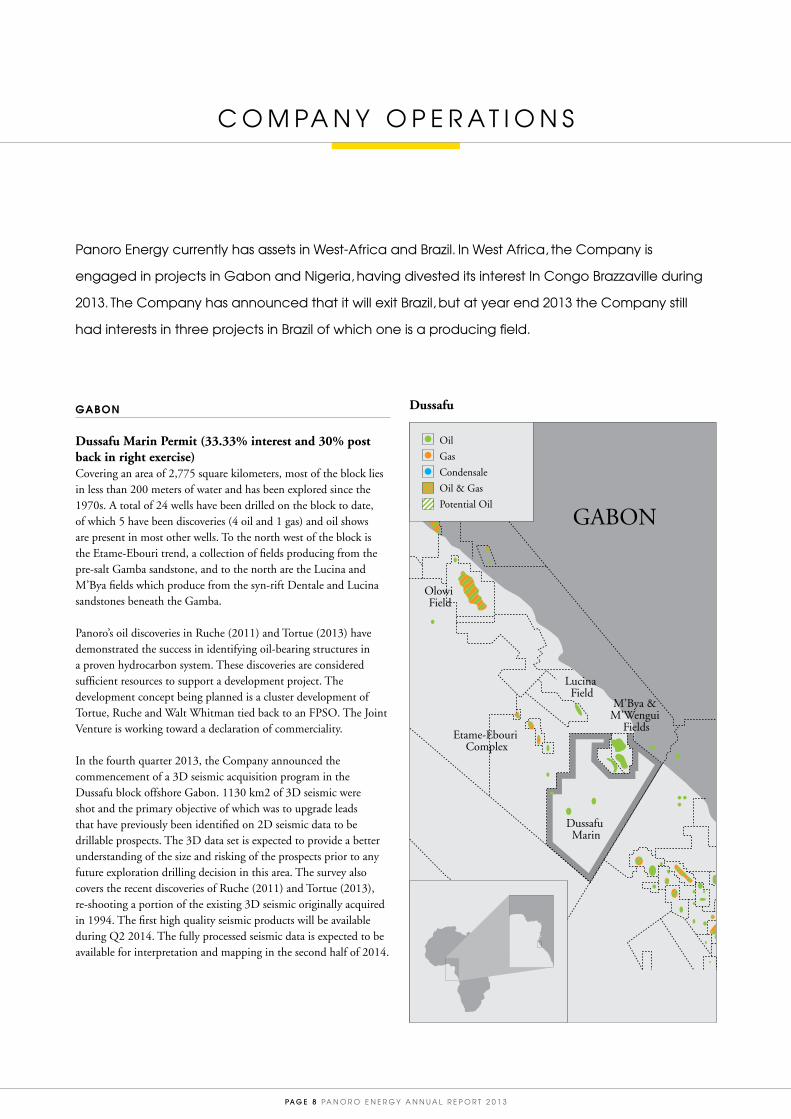

GABON

Dussafu Marin Permit (33.33% interest and 30% post back in right exercise)Covering an area of 2,775 square kilometers, most of the block lies in less than 200 meters of water and has been explored since the 1970s. A total of 24 wells have been drilled on the block to date, of which 5 have been discoveries (4 oil and 1 gas) and oil shows are present in most other wells. To the north west of the block is the Etame-Ebouri trend, a collection of fields producing from the pre-salt Gamba sandstone, and to the north are the Lucina and M’Bya fields which produce from the syn-rift Dentale and Lucina sandstones beneath the Gamba.

Panoro’s oil discoveries in Ruche (2011) and Tortue (2013) have demonstrated the success in identifying oil-bearing structures in a proven hydrocarbon system. These discoveries are considered sufficient resources to support a development project. The development concept being planned is a cluster development of Tortue, Ruche and Walt Whitman tied back to an FPSO. The Joint Venture is working toward a declaration of commerciality.

In the fourth quarter 2013, the Company announced the commencement of a 3D seismic acquisition program in the Dussafu block offshore Gabon. 1130 km2 of 3D seismic were shot and the primary objective of which was to upgrade leads that have previously been identified on 2D seismic data to be drillable prospects. The 3D data set is expected to provide a better understanding of the size and risking of the prospects prior to any future exploration drilling decision in this area. The survey also covers the recent discoveries of Ruche (2011) and Tortue (2013), re-shooting a portion of the existing 3D seismic originally acquired in 1994. The first high quality seismic products will be available during Q2 2014. The fully processed seismic data is expected to be available for interpretation and mapping in the second half of 2014.

Olowi Field

Lucina Field

Etame-Ebouri Complex

Dussafu Marin

M’Bya & M’Wengui

Fields

GABON

Dussafu

Oil

Gas

Condensale

Oil & Gas

Potential Oil

PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3 PA G E 9

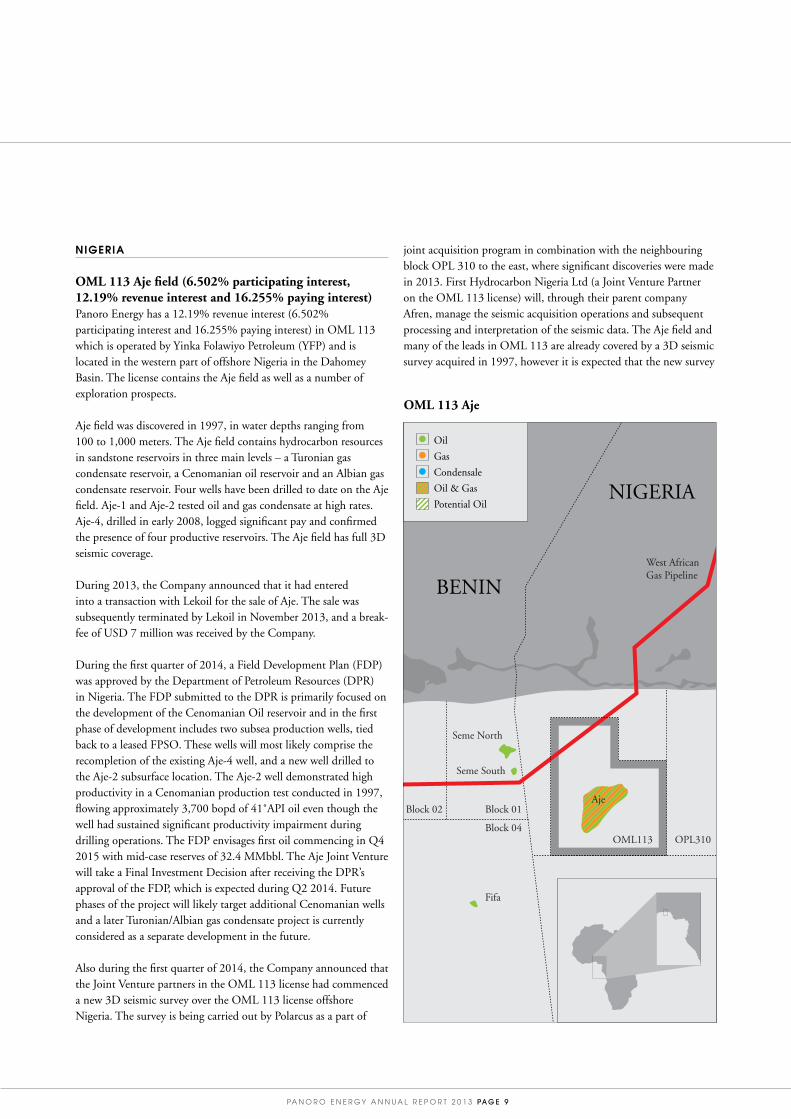

NIGERIA

OML 113 Aje field (6.502% participating interest, 12.19% revenue interest and 16.255% paying interest)Panoro Energy has a 12.19% revenue interest (6.502% participating interest and 16.255% paying interest) in OML 113 which is operated by Yinka Folawiyo Petroleum (YFP) and is located in the western part of offshore Nigeria in the Dahomey Basin. The license contains the Aje field as well as a number of exploration prospects.

Aje field was discovered in 1997, in water depths ranging from 100 to 1,000 meters. The Aje field contains hydrocarbon resources in sandstone reservoirs in three main levels – a Turonian gas condensate reservoir, a Cenomanian oil reservoir and an Albian gas condensate reservoir. Four wells have been drilled to date on the Aje field. Aje-1 and Aje-2 tested oil and gas condensate at high rates. Aje-4, drilled in early 2008, logged significant pay and confirmed the presence of four productive reservoirs. The Aje field has full 3D seismic coverage.

During 2013, the Company announced that it had entered into a transaction with Lekoil for the sale of Aje. The sale was subsequently terminated by Lekoil in November 2013, and a break-fee of USD 7 million was received by the Company.

During the first quarter of 2014, a Field Development Plan (FDP) was approved by the Department of Petroleum Resources (DPR) in Nigeria. The FDP submitted to the DPR is primarily focused on the development of the Cenomanian Oil reservoir and in the first phase of development includes two subsea production wells, tied back to a leased FPSO. These wells will most likely comprise the recompletion of the existing Aje-4 well, and a new well drilled to the Aje-2 subsurface location. The Aje-2 well demonstrated high productivity in a Cenomanian production test conducted in 1997, flowing approximately 3,700 bopd of 41˚API oil even though the well had sustained significant productivity impairment during drilling operations. The FDP envisages first oil commencing in Q4 2015 with mid-case reserves of 32.4 MMbbl. The Aje Joint Venture will take a Final Investment Decision after receiving the DPR’s approval of the FDP, which is expected during Q2 2014. Future phases of the project will likely target additional Cenomanian wells and a later Turonian/Albian gas condensate project is currently considered as a separate development in the future.

Also during the first quarter of 2014, the Company announced that the Joint Venture partners in the OML 113 license had commenced a new 3D seismic survey over the OML 113 license offshore Nigeria. The survey is being carried out by Polarcus as a part of

joint acquisition program in combination with the neighbouring block OPL 310 to the east, where significant discoveries were made in 2013. First Hydrocarbon Nigeria Ltd (a Joint Venture Partner on the OML 113 license) will, through their parent company Afren, manage the seismic acquisition operations and subsequent processing and interpretation of the seismic data. The Aje field and many of the leads in OML 113 are already covered by a 3D seismic survey acquired in 1997, however it is expected that the new survey

Seme North

Block 02

West AfricanGas Pipeline

Block 01

Block 04OML113 OPL310

Aje

Fifa

Seme South

NIGERIA

BENIN

OML 113 Aje

Oil

Gas

Condensale

Oil & Gas

Potential Oil

PA G E 1 0 PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3

will provide a considerable improvement in data quality over the existing 3D data. It is envisaged that the data will enable better development planning for the second phase of development drilling on Aje and provide improved data to fully evaluate the exploration potential over the whole of the OML 113 license, including the exciting synrift exploration play that was significantly de-risked though the discovery made in OPL 310. The survey is expected to be completed by end of May 2014.

BRAZIL

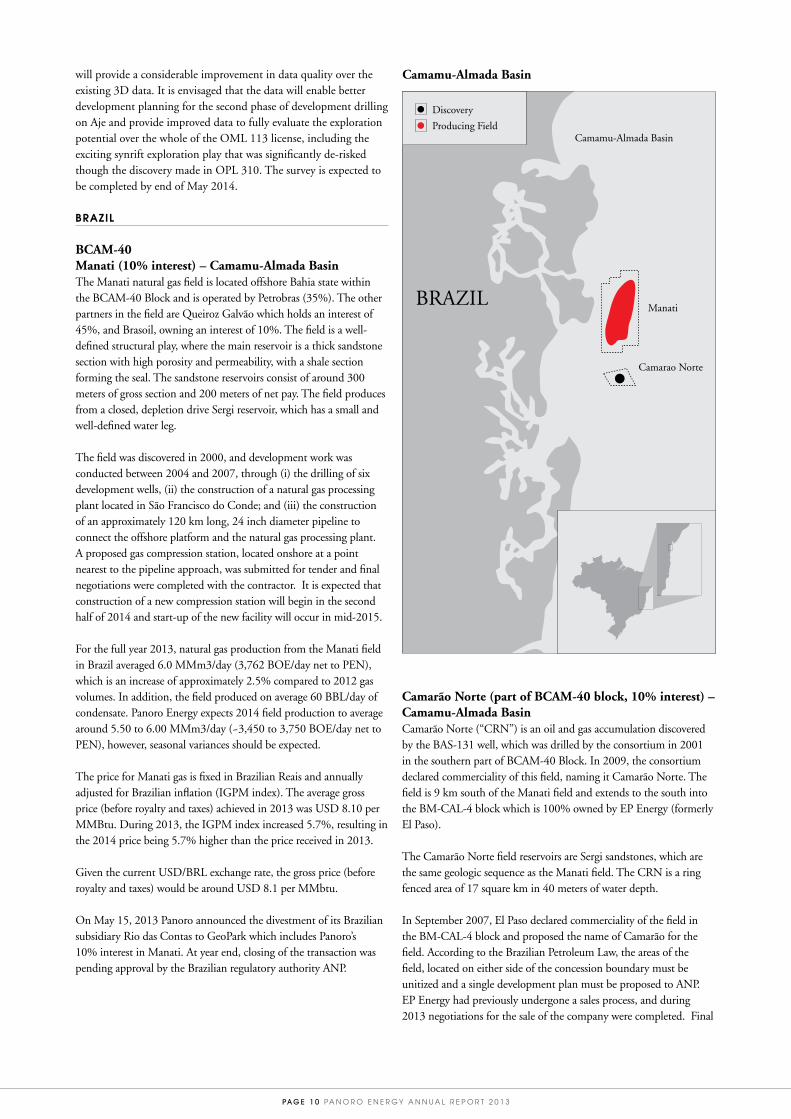

BCAM-40Manati (10% interest) – Camamu-Almada BasinThe Manati natural gas field is located offshore Bahia state within the BCAM-40 Block and is operated by Petrobras (35%). The other partners in the field are Queiroz Galvão which holds an interest of 45%, and Brasoil, owning an interest of 10%. The field is a well-defined structural play, where the main reservoir is a thick sandstone section with high porosity and permeability, with a shale section forming the seal. The sandstone reservoirs consist of around 300 meters of gross section and 200 meters of net pay. The field produces from a closed, depletion drive Sergi reservoir, which has a small and well-defined water leg.

The field was discovered in 2000, and development work was conducted between 2004 and 2007, through (i) the drilling of six development wells, (ii) the construction of a natural gas processing plant located in São Francisco do Conde; and (iii) the construction of an approximately 120 km long, 24 inch diameter pipeline to connect the offshore platform and the natural gas processing plant. A proposed gas compression station, located onshore at a point nearest to the pipeline approach, was submitted for tender and final negotiations were completed with the contractor. It is expected that construction of a new compression station will begin in the second half of 2014 and start-up of the new facility will occur in mid-2015.

For the full year 2013, natural gas production from the Manati field in Brazil averaged 6.0 MMm3/day (3,762 BOE/day net to PEN), which is an increase of approximately 2.5% compared to 2012 gas volumes. In addition, the field produced on average 60 BBL/day of condensate. Panoro Energy expects 2014 field production to average around 5.50 to 6.00 MMm3/day (~3,450 to 3,750 BOE/day net to PEN), however, seasonal variances should be expected.

The price for Manati gas is fixed in Brazilian Reais and annually adjusted for Brazilian inflation (IGPM index). The average gross price (before royalty and taxes) achieved in 2013 was USD 8.10 per MMBtu. During 2013, the IGPM index increased 5.7%, resulting in the 2014 price being 5.7% higher than the price received in 2013.

Given the current USD/BRL exchange rate, the gross price (before royalty and taxes) would be around USD 8.1 per MMbtu.

On May 15, 2013 Panoro announced the divestment of its Brazilian subsidiary Rio das Contas to GeoPark which includes Panoro’s 10% interest in Manati. At year end, closing of the transaction was pending approval by the Brazilian regulatory authority ANP.

Camarão Norte (part of BCAM-40 block, 10% interest) – Camamu-Almada BasinCamarão Norte (“CRN”) is an oil and gas accumulation discovered by the BAS-131 well, which was drilled by the consortium in 2001 in the southern part of BCAM-40 Block. In 2009, the consortium declared commerciality of this field, naming it Camarão Norte. The field is 9 km south of the Manati field and extends to the south into the BM-CAL-4 block which is 100% owned by EP Energy (formerly El Paso).

The Camarão Norte field reservoirs are Sergi sandstones, which are the same geologic sequence as the Manati field. The CRN is a ring fenced area of 17 square km in 40 meters of water depth.

In September 2007, El Paso declared commerciality of the field in the BM-CAL-4 block and proposed the name of Camarão for the field. According to the Brazilian Petroleum Law, the areas of the field, located on either side of the concession boundary must be unitized and a single development plan must be proposed to ANP. EP Energy had previously undergone a sales process, and during 2013 negotiations for the sale of the company were completed. Final

Manati

Camamu-Almada Basin

Camarao Norte

BRAZIL

Camamu-Almada Basin

Discovery

Producing Field

PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3 PA G E 1 1

closing of the sale of EP Energy is contingent on final approval by the ANP, after which it is expected that unitization discussions and plans for development will be brought forward by the purchasing party. Panoro’s 10 % interest in CRN will be divested along with Rio das Contas.

BS-3BS-3 Project – Cavalo Marinho (50% interest) and Estrela do Mar (65% interest) – Santos BasinPanoro acquired interests in the BS-3 area in a series of negotiations conducted between 2001 and 2006, resulting in the interests shown above as of the end of 2013. As of year-end 2013, Panoro continued its participation in Petrobras operated partnerships in the Cavalo Marinho and Estrela do Mar fields, which are among several shallow water offshore Guaruja carbonate oilfields located in the South Santos Basin of Brazil. Cavalo Marinho and Estrela do Mar have never been produced, however two adjacent fields in the trend, Caravela (100% Petrobras) and Coral (35% Panoro in partnership with Petrobras, Brasoil and QGEP), cumulatively produced over 32 mmbo between 1993 and 2008. Technical data indicates that all of these fields have very good quality 40 degree API oil, with most of the reservoirs having excellent producing characteristics.

During 2012 and 2013, Panoro continued to work with the consortium to configure development plans that would lead to economic exploitation of the fields. The technical work performed by both Panoro and the operator, Petrobras, led to the submissions of development plans to the National Petroleum Agency (ANP). Despite technical arguments presented in technical reports and presented in multiple technical meetings, the ANP would not relent on two key points: 1) The development plan must include drilling wells to test the low-permeability B-1 zone in every field, including long-term production testing and contingent pilot injection, and 2) The development plan must include a gas offtake plan to comply with regulations put in place after the Caravela and Coral fields were produced.

The combination of the requirements for B1 tests and a gas solution add substantial cost to the project, and therefore have a significantly negative impact on the economics. While the economic analysis of a project including B1 tests and a gas solution indicates a positive net present value these factors significantly reduce the attractiveness of the project. The most recent economic evaluations show that the project is only marginally economic. During the latter part of 2013, Panoro and its partners Petrobras and Brasoil embarked on a process to attempt to farmout the BS-3 assets, in an attempt to monetize the asset and to test the perceived value of this project within the industry. During the process, over 30 companies were contacted, but a limited number of these companies elected to conduct an evaluation, and of these no company was willing to demonstrate strong interest by submitting an Indicative Offer or a Letter of Interest.

Given the difficulties in defining an economically attractive development plan and the general perception of limited value remaining in the BS-3 blocks, the decision was made to surrender the blocks during early 2014. Note that as of year-end 2012 the reserves associated with the remaining BS-3 fields were re-categorized as contingent resources.

Coral field, 35% interestThe Coral license was relinquished back to the Brazilian regulatory authorities ANP during 2013.

BM-S-63, BM-S-71 & BM-S-72 exploration blocks (15% interest) – Santos BasinAll three blocks were relinquished back to the Brazilian regulatory authorities ANP during 2013 after evaluation showed that the discoveries were considered sub-commercial for a standalone development project by Panoro.

CONGO-BRAZZAVILLE

Mengo-Kundji-Bindi (20% interest)In July 2013 the Company completed the sale of its 20% interest in the MKB permit to Société Nationale des Pétroles du Congo (“SNPC”) the operator of the MKB Permit in the Republic of Congo.

Santos Basin

Piracuca

SidonTiroTubarao

Estrela do Mar

Coral

CaravelaCaravela Sul

Cavalo Marinho

1-BSS.070

BM-S-63

BM-S-71

BM-S-72

Oil

Gas

Condensale

Oil & Gas

Potential Oil

PA G E 1 2 PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3

R E S E R V E S A N D C O N T I N G E N T R E S O U R C E S

Panoro’s classification of reserves and resources complies with the guidelines established by the Oslo Stock Exchange and are based on the definitions set by the Petroleum Resources Management System (PRMS-2007), sponsored by the Society of Petroleum Engineers/World Petroleum Council/ American Association of Petroleum Geologists/ Society of Petroleum Evaluation Engineers (SPE/WPC/AAPG/SPEE) as issued in March 2007.

Reserves are the volume of hydrocarbons that are expected to be produced from known accumulations:

• In production• Under development • With development committed

Reserves are also classified according to the associated risks and probability that the reserves will be actually produced.

1P Proven reserves represent volumes that will be recovered with 90% probability

2P Proven + Probable represent volumes that will be recovered with 50% probability

3P Proven + Probable + Possible volumes that will be recovered with 10% probability

Contingent resources are the volume of hydrocarbons that is expected to be produced from known accumulations:

• In planning phase• Where development is likely• Where development is unlikely with present basic assumptions• Under evaluation Contingent resources are reported as 1C, 2C and 3C reflecting similar probabilities as reserves.

Panoro Energy’s reserve report per end 2013 is summarized in the table below:

Contingent resources are reported as 1C, 2C and 3C reflecting similar probabilities as reserves. Panoro Energy’s reserve report per end 2013 is summarized in the table below:

Asset1P reserves

MMBOE2P reserves

MMBOE

Manati 9.3 10.0

Panoro total 9.3 10.0

2C Contingent resources summary (MMBOE)

Asset

Dussafu* 11.0

Aje 26.6

Cavalo Marinho 11.0

Estrela do Mar 15.6

Caravela Sul 0.4

Camarão Norte 0.9

Panoro total 65.5

* Dussafu working interst share.

As of year-end 2013, Panoro was producing reserves from one asset, being the Manati gas field in Brazil.

In addition, Panoro had six assets with contingent resources.

A summary description of each asset with status as of year-end 2013 is included below. In addition we refer to the company web-site for background information on each asset.

2013 2C RESOURCES BY FIELD (MMBOE) - TOTAL 65.5 MMBOE2013 2P RESERVES (MMBOE) - TOTAL 10.0 MMBOE

10

n Manati

1111

0.4

26.6

15.6

0.9

n Cavalo Marinhon Estrela do Marn Caravela Suln Ajen Dussafun Camarao Norte

PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3 PA G E 1 3

Unless otherwise specified, all numbers quoted below are net to Panoro’s interest.

DUSSAFU: OFFSHORE GABON, OPERATOR HARVEST NATURAL RESOURCES, PANORO 33.33%

Dussafu is a large exploration block with several small oil fields, the most recent being the Ruche and Tortue discoveries. The 2C Contingent Resources reported by the operator are 49 MMbbl oil in the Ruche, Tortue, Moubenga and Walt Whitman fields. This figure does not include the GMC-1X gas field which has 2C resources of 142 bcf gas and 5 MMbbl oil.

The recent GCA certified (3rd party) potentially recoverable 2C contingent Resources are 33.4 MMbbl, based on a commercial evaluation of a development scenario, which is being considered as the basis for the declaration of commerciality. This evaluation yields 2C potentially recoverable resources net to Panoro of 11.0 MMbbls of oil. These 2C Contingent Resources are Panoro’s Working Interest fraction of the Gross Field Resources; they do not represent Panoro’s actual Net Entitlement under the terms of the PSC that governs the asset, which would likely be lower.

Studies to evaluate Dussafu development options continue. The conceptual plan is to aggregate the established accumulations with shared infrastructure. The JV is moving towards a Declaration of Commerciality and submission of a Field Development Plan for Dussafu in 2014.

AJE: OFFSHORE NIGERIA, OPERATOR YINKA FOLAWIYO PETROLEUM (YFP), PANORO 12.1913%

The Aje discovery, close to the border with Benin, is predominantly a gas discovery with significant condensate, but also contains a separate oil leg.

As of year-end a Field Development Plan (FDP) was pending to be submitted to the Department of Petroleum Resources during the first quarter of 2014. The FDP focuses on a two-well development of the Cenomanian oil reservoir only, with mid-case reserves of 32.4 MMbbls. Panoro’s entitlement of this is equal to 4.4 MMbbls. Aje volumes for all reservoirs as reported by TRACS in December 2013 are included as contingent resources with a best estimate – 2C of 26.6 MMBOE net to Panoro’s share.

MANATI: GAS FIELD OFFSHORE BRAZIL, OPERATOR PETROBRAS, PANORO 10%

The original development plan for Manati called for seven producing wells, but based on initial production experience and reservoir understanding, the Operator concluded that six wells could potentially suffice to drain the reservoirs. The consortium consequently has decided to postpone the decision to drill the seventh well.

With the exception of a scheduled maintenance shut-down for three week period in April, production remained at high levels throughout 2013.

Total production for the field during the year 2013 was 218.287 MMm3 gas and 3,510 m3 of condensate, which is 1.395 MMBOE when stated in equivalent units, compared to 1.436 MMBOE in 2012.

As of year-end 2013 the Manati field had cumulative gas production (100%) of 13.24 Bm3. Compression is now planned to be operational beginning in mid-2015.

The Manati reserves report for year end 2013 reflects a reserves adjustment made by GCA during 2013, based on updated Manati reservoir pressure data and the resulting update to the simulation model, as reported by the operator. As a result of this adjustment, the ultimate 1P recovery was increased by 0.9 MMBOE, while 2P ultimate recovery was reduced slightly.

As of the publication date of this report, this asset has now been sold, along with interest in the Camarão Norte field.

CAMARÃO NORTE: OFFSHORE BRAZIL, OPERATOR PETROBRAS, PANORO 10%

Camarão/Camarão Norte is a discovery extending into the area previously designated as the BCAM-40 (Manati) block. It straddles the block boundary with the neighboring block to the south (BM-CAL-4, 100% owned and operated by a third party). Camarão Norte was declared commercial in July 2009. Five wells have been drilled on the structure (four in block BM-CAL-4), proving the presence of both oil and gas.

A Unitization process will be required and volumes are included as Contingent Resources, best estimate - 2C - of 0.9 MMBOE. This includes both oil and gas volumes considered inside the BCAM-40 ring fence with a 50-50 resource estimate scenario between the blocks. As of the publication date of this report, this asset has now been sold, along with interest in the Manati field.

PA G E 1 4 PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3

BS-3: OFFSHORE BRAZIL, OPERATOR PETROBRAS, PANORO 50-65%

The BS-3 area offshore in the southern part of the Santos basin holds two Panoro assets: the Cavalo Marinho, and Estrela-do-Mar oil fields. The Coral field was relinquished during 2013.

Generally, in all the BS3 fields, hydrocarbons are present in up to four separate, vertically stacked carbonate reservoir zones (B1-B4), where commercial production so far has been associated with the lower three. The uppermost zone (referred to as B1), holds significant hydrocarbon volumes in place but has low permeability and has not been proven to be commercially producible with conventional technology.

Planning for development of these fields has been complicated by the ANP requirements for testing of the low permeability B1 zone and by the requirement for a gas solution. The consortia have worked together to attempt to resolve these complicating issues for several years, but have not been able to configure a commercial solution to develop the fields.

As of year-end, Panoro was involved in a farmout process for the BS-3 assets, and this process had attracted some interest from several qualified companies. The farmout process was ongoing as of the end of the year 2013, with confidentiality agreements having been signed, and data rooms had been either held or scheduled, however no company demonstrated interest in entering into serious negotiations. As of the date of publication of this reserves report, faced with increasing pressure from the ANP, all partners have agreed to relinquish the BS-3 blocks. It is expected that this relinquishment will proceed without any major obstacles.

MANAGEMENT DISCUSSION AND ANALYSIS

Panoro uses the services of Gaffney, Cline & Associates (GCA) for 3rd party verifications of its reserves.

All evaluations are based on standard industry practice and methodology for production decline analysis and reservoir modelling based on geological and geophysical analysis.

The following discussions are a comparison of the volumes reported in previous reports, along with a discussion of the consequences for the year-end 2013 ASR:

• Dussafu: The block has made significant progress towards a future development sanction. The joint venture has now agreed that the discoveries can result in a commercial development and discussions are ongoing with the Direction Generale des Hydrocarbures in Gabon to pass though the Declaration of Commerciality milestone defined under the Production Sharing Contract. There is now increased confidence that a Field Development Plan will be approved by the Government in the future and these Contingent Resources will be reclassified as Reserves.

• Aje: The block has undergone some partnership changes which have resulted in significant re-alignment of the Joint Venture

group. With the Cenomanian Oil Development plan now submitted to the Department of Petroleum Resources in Nigeria for approval, tangible progress toward a field development has been made. These factors, improve the likelihood of a future re-classification of the Resource Volumes as Reserves.

• Manati: Reserves are carried forward from a slight upward revision performed by Gaffney Cline during 2013, after the publication of the Year End 2012 reserve report. The 2013 Gaffney Cline revision was based on the Operator’s revised technical assessment, using updated production data and newly acquired reservoir pressure data. As of the publication date of this report, this asset has now been sold, along with interest in the Camarão Norte field.

• BS3: Estrela do Mar and Cavalo Marinho Contingent Resources are unchanged, as Panoro is continued during 2013 to seek solutions through interaction with all major stakeholders, as well as pursuing a farmout. The major issues that affected development of the fields are: 1) Gas export solution, and 2) Plan to assess the B1 zone through a pilot program, with the aim being eventual development. As of the date of publication of this reserves report, faced with increasing pressure from the ANP, all partners have agreed to relinquish the BS-3 blocks. It is expected that this relinquishment will proceed without any major obstacles.

ASSET ACQUISITIONS/DISPOSALS DURING 2013

The BM-S-63, BM-S-71 and BM-S-72 blocks and the Coral field were relinquished in 2013. Additionally, the MKB asset was sold during 2013.

ASSUMPTIONS

The commerciality and economic tests for the December 31, 2013 Manati reserves volumes were based on condensate and gas sales prices as shown in the following table. Gas price is fixed in Brazilian Reais according to the sales contract, allowing annual escalation with the domestic market inflation. GCA estimates that the balance between that escalation and the exchange ratio to the US Dollar would give a net escalation close to 1% per year. Condensate price was based on GCA’s future scenario for Brent crude oil price with a USD 2.07/Bbl location discount and a USD 0.07/Bbl quality premium.

Both gas and condensate prices were grossed up for taxes, which are 21.25% for gas (PIS, PASEP, COFINS and ICMS taxes) and 9.25% for condensate (PIS and COFINS taxes).

YearCondensate

US$/BblGas

US$/MMBtu

2014 111.28 8.76

2015 106.69 9.02

2016 104.19 9.29

2017 107.67 9.57

2018 109.76 9.86

Thereafter +2% per year +3% per year

PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3 PA G E 1 5

Converting gas volumes to oil-equivalents is done using a conversion factor of 6.29 bbl/m3.

Panoro’s total 1P reserves at end of 2013 amount to 9.26 MMBOE.

This reflects adjusting for 2013 production, a reduction to account for the sale of the MKB asset and an interim 2013 adjustment for the Manati field, conducted by Gaffney Cline & Associates, to reflect updated pressure data and revisions to the 3D simulation model as performed by the operator.

Panoro’s 2P reserves after similar adjustment is 10.0 MMBOE.

Panoro’s Contingent Resource base includes discoveries of varying degrees of maturity towards development decisions. By end of 2013, Panoro’s assets contain a total 2C volume of 65.5 MMBOE.

Oslo, April 2014

Jan KiellandCEO

PA G E 1 6 PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3

D I R E C T O R S ’ R E P O R T 2 0 1 3

Panoro Energy ASA (“Panoro” or the “Company”) is an independent E&P company with assets

offshore West-Africa and offshore Brazil. The Company’s business activities comprise exploration and

production of oil and natural gas in Gabon, Nigeria and Brazil. The Company has offices in Oslo,

Norway, London, United Kingdom and Rio de Janeiro, Brazil. Panoro Energy is listed on the Oslo Stock

Exchange (OSE) under the ticker symbol “PEN”.

As of year-end 2013, Panoro had one asset classified with reserves and six with contingent resources. Proved and probable (2P) reserves as of year-end 2013 were 10.0 MMBOE and best estimate (2C) contingent resources as of year-end 2013 were 65.5 MMBOE. Of this 27 MMBOE were (2C) contingent resources related to BS-3. At the end of 2013, the Company impaired the Company’s assets in the BS-3 area in the Southern Santos Basin offshore Brazil. Refer to the “Reserves and contingent resources” section of the report for further information.

OPERATIONS

Operations in GabonCovering an area of 2,775 square kilometers, most of the block lies in less than 200 meters of water and has been explored since the 1970s. A total of 24 wells have been drilled on the block to date, of which 5 have been discoveries (4 oil and 1 gas) and oil shows are present in most other wells. To the north west of the block is the Etame-Ebouri trend, a collection of fields producing from the pre-salt Gamba sandstone, and to the north are the Lucina and M’Bya fields which produce from the syn-rift Dentale and Lucina sandstones beneath the Gamba.

Panoro’s oil discoveries in Ruche (2011) and Tortue (2013) have demonstrated the success in identifying oil-bearing structures in a proven hydrocarbon system. These discoveries are considered sufficient resources to support a development project. The development concept being planned is a cluster development of Tortue, Ruche and Walt Whitman tied back to an FPSO. The Joint venture is working toward a declaration of commerciality.

In the fourth quarter 2013, the Company announced the commencement of a 3D seismic acquisition program in the Dussafu block offshore Gabon. 1,130 km2 of 3D seismic were shot and the primary objective of which was to upgrade leads that have previously been identified on 2D seismic data to be drillable prospects. The 3D data set is expected to provide a better

understanding of the size and risking of the prospects prior to any future exploration drilling decision in this area. The survey also covers the recent discoveries of Ruche (2011) and Tortue (2013), re-shooting a portion of the existing 3D seismic originally acquired in 1994. The first high quality seismic products are expected to be available during Q2 2014. The fully processed seismic data is expected to be available for interpretation and mapping in the second half of 2014.

Net 2C contingent resources for this field as per GCA report were 11.0 MMbbls per year-end 2013. However, the operator’s number was 16,5 MMBOE.

Operations in NigeriaPanoro Energy has a 12.19% revenue interest (6.502% participating interest and 16.255% paying interest) in OML 113 which is operated by Yinka Folawiyo Petroleum (YFP) and is located in the western part of offshore Nigeria in the Dahomey Basin. The license contains the Aje field as well as a number of exploration prospects.

Aje field was discovered in 1997, in water depths ranging from 100 to 1,000 meters. The Aje field contains hydrocarbon resources in sandstone reservoirs in three main levels – a Turonian gas condensate reservoir, a Cenomanian oil reservoir and an Albian gas condensate reservoir. Four wells have been drilled to date on the Aje field. Aje-1 and Aje-2 tested oil and gas condensate at high rates. Aje-4, drilled in early 2008, logged significant pay and confirmed the presence of four productive reservoirs. The Aje field has full 3D seismic coverage.

During 2013, the Company announced that it had entered into a transaction with Lekoil for the sale of Aje. The sale was subsequently terminated by Lekoil in November 2013, and a break-fee of USD 7 million was received by the Company.

During the first quarter of 2014, a Field Development Plan (FDP)

PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3 PA G E 1 7

was submitted to the Department of Petroleum Resources (DPR) in Nigeria. The FDP submitted to the DPR is primarily focused on the development of the Cenomanian Oil reservoir and in the first phase of development includes two subsea production wells, tied back to a leased FPSO. These wells will most likely comprise the recompletion of the existing Aje-4 well, and a new well drilled to the Aje-2 subsurface location. The Aje-2 well demonstrated high productivity in a Cenomanian production test conducted in 1997, flowing approximately 3,700 bopd of 41˚API oil even though the well had sustained significant productivity impairment during drilling operations. The FDP envisages first oil commencing in Q4 2015 with mid-case reserves of 32.4 MMbbl. The Aje Joint Venture will take a Final Investment Decision after receiving the DPR’s approval of the FDP, which is expected during Q2 2014. Future phases of the project will likely target additional Cenomanian wells and a later Turonian/Albian gas condensate project is currently considered as a separate development in the future.

Also during the first quarter of 2014 the Company announced that the Joint Venture partners in the OML 113 license had commenced a new 3D seismic survey over the OML 113 license offshore Nigeria. The survey is being carried out by Polarcus as a part of joint acquisition program in combination with the neighbouring block OPL 310 to the east, where significant discoveries were made in 2013. First Hydrocarbon Nigeria Ltd (a Joint Venture Partner on the OML 113 license) will, through their parent company Afren, manage the seismic acquisition operations and subsequent processing and interpretation of the seismic data. The Aje field and many of the leads in OML 113 are already covered by a 3D seismic survey acquired in 1997, however it is expected that the new survey will provide a considerable improvement in data quality over the existing 3D data. It is envisaged that the data will enable better development planning for the second phase of development drilling on Aje and provide improved data to fully evaluate the exploration potential over the whole of the OML 113 license, including the exciting synrift exploration play that was significantly de-risked though the discovery made in OPL 310. The survey is expected to be completed by end of May 2014.

2C contingent resources related to the OML 113 license stood at 26.6 MMbbls per year-end 2013.

Operations in Congo-BrazzavillePanoro Energy held a 20% working interest in Mengo-Kundji-Bindi (“MKB”) in Congo-Brazzaville, which was sold to SNPC.

Operations in BrazilPanoro had three licenses in Brazil at the end of 2013, of which two are located in the Santos Basin and one in the Camamu-Almada Basin. Four blocks were relinquished to the ANP in 2013. After completion of a three-well exploration program on blocks BM-S-63, BM-S-71 and BM-S-72 the discoveries were considered sub commercial for a stand-alone development project by the partners. The Coral license was also relinquished back to ANP.

Panoro Energy’s production is from the Manati field in Brazil in the BCAM-40 block in the Camamu-Almada basin, where the Company holds a 10% interest. The field commenced production in 2007 and daily natural gas production averaged 6.0 MMm3 per

day in 2013 (3,762 boe per day net to Panoro), representing an increase of approximately 2.5% from 2012. Panoro‘s 2P reserves on Manati were 10.0 MMBOE per the end of 2013.

The Company also has a 10% interest in the Camarão Norte discovery, which is located 9 km south of the Manati field in the same block. This field was discovered in 2001. Camarão Norte extends southwards into the BM-CAL-4 block, which is 100% owned by EP Energy (formerly El Paso). Unitization discussions and plans for this field are pending discussions with EP Energy. Panoro Energy’s 2C contingent resources in this field amounted to 0.9 MMBOE per year-end 2013.

In May 2013, Panoro announced the divestment of its Brazilian subsidiary Rio das Contas to GeoPark which includes Panoro’s 10% interest in the BCAM-40 block. At year end the closing of the transaction was pending approval from the Brazilian Regulatory authorities ANP. This transaction was completed in 2014.

In the Santos Basin, the Company has ownership in two discoveries in the BS-3 area; Cavalo Marinho (50% interest) and Estrela do Mar (65% interest). Panoro Energy and its partners initiated a farmout process for their interests in the fields in the BS-3 area without success and as a result made a decision after year end to discontinue the farmout process. The operator will submit an abandonment plan for the BS-3 to ANP during 2014. As a result of the decision to withdraw from the BS-3 licenses, Panoro Energy charged the Income Statement for 2013 with a write-down of USD 46.2 million, leaving the remaining book value related to these assets at USD nil at the end of 2013.

As described above, the Company and its partners relinquished the BM-S-63, BM-S-71 and BM-S-72 licenses to ANP in 2013. Following the transfer of operatorship and a 35% working interest to Vanco, Panoro Energy held a 15% working interest in the three exploration licenses. Vanco carried Panoro’s cost of drilling for the three exploration wells in 2012. As a result of the unsuccessful drilling in the three blocks, Panoro Energy charged the Income Statement for 2013 with a write-down of the assets of USD 0.6 million, and recognized no remaining value related to these assets in the statement of financial position per the end of 2013.

Above divestment, relinquishments and exit from BS-3 leaves the Company with no further assets in Brazil.

The Company has through its subsidiary Rio das Contas an ongoing Research and Development project with the Federal University of Bahia (UFBA) using sequence stratigraphical methods to re-evaluate the hydrocarbon bearing layers in the Reconcavo basin.

THE ACCOUNTS

The Board of Directors confirms that the annual financial statements have been prepared pursuant to the going concern assumption, in accordance with §3-3a of the Norwegian Accounting Act, and that this assumption was realistic at the time the accounts were approved. The going concern assumption

PA G E 1 8 PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3

is based upon the financial position of the Company and the development plans currently in place. In the Board of Directors’ view, the annual accounts give a true and fair view of the group’s assets and liabilities, financial position and results. The Board of Directors is not aware of any factors that materially affect the assessment of the group’s position as of December 31, 2013, or the loss for 2013, other than those presented in the Directors’ Report or that otherwise follow from the financial statements.

Panoro Energy ASA prepares its financial statements in accordance with the International Financial Reporting Standards (IFRS), as provided for by the EU and the Norwegian Accounting Act.

The financial statements reflect the activities in 2013, and the Company’s financial position is considered to be sound. The consolidated accounts are presented in US dollars.

The below analysis compares 2013 with 2012 figures:

FINANCIAL PERFORMANCE AND ACTIVITIES

Condensed Consolidated Income Statement (Amounts in USD 000) 2013 2012

Total revenues (net revenues) 54,146 46,830

Operating expenses

Production costs (10,877) (5,557)

Exploration related costs (922) (903)

General and administrative costs (10,723) (16,312)

Strategic review costs (2,190) -

Total operating expenses (24,712) (22,772)

Earnings before interest, tax, depreciation and amortisation (EBITDA) 29,434 24,058

Depreciation (2,459) (7,713)

Asset write-off and impairment (46,815) (47,150)

Loss on disposal of assets (1,681) (75)

Share based payments (235) (1,150)

Earnings before interest and tax (EBIT) (21,756) (32,030)

Net financial items (22,176) (20,362)

Loss before taxes (43,932) (52,392)

Income tax benefit / (expense) (10,821) 4,580

Net loss for the year (54,753) (47,812)

Income statementTotal revenues amounted to USD 54.1 million in 2013 compared to USD 46.8 million in 2013. This includes other income of USD 10.5 million in 2013 representing USD 7 million earned from termination of sale agreement with Lekoil and USD 3.5 millionreversal of milestone liabilities against BS-3 licences that are no longer payable with the imminent relinquishment of the licences. In comparison other income in 2012 was USD 0.9 million.

The remaining amount of revenue is driven from oil and gas sales that amounted to USD 43.6 million in 2013, a decrease of 5% revenues from USD 45.9 million in 2012, with gas sales volumes declining 2.8% to 3,592 boe/day. The decrease relates to lower production at the Manati field, which was subdued in 2013 due to planned maintenance and repair work conducted in April 2013. The gas sale price is fixed in BRL and therefore subject to currency movements on translation to USD for reporting purposes. Measured in USD, the average gas price declined from USD 8.25/MMbtu in 2012 to USD 8.10/MMbtu in 2013.

Production cost for the full year was USD 10.9 million in 2013. This was an increase from USD 5.6 million in 2012 which was driven by scheduled maintenance in April 2013 and decommissioning costs incurred on BAS-128 well in the BCAM-40 licence area.

Exploration related costs remained consistent at USD 0.9 million for both years.

General and administration costs (G&A) declined to USD 10.7 million in 2013 from USD 16.3 million in 2012. The cost reduction has been achieved through implementation of Group’s aggressive plans of cost control.

Strategic review costs in 2013 amounted to USD 2.2 million, representing identifiable overheads incurred on the ongoing divestment program. Parts of these costs are incremental selling costs, which will be reclassified to the gain/loss on disposal upon completion of the Rio das Contas sale. These costs are of a one-off nature and will discontinue once these processes are concluded. There were no strategic review costs in 2012.

Earnings before interest, taxes, depreciation and amortisation (EBITDA) hence amounted to USD 29.4 million in 2013, up from USD 24.1 million in 2012. The increase mainly reflects higher income from other sources including USD 7 million termination fee and USD 3.5 million reversal of liabilities no longer payable offset by a higher production cost in 2013.

Depreciation amounted to USD 2.5 million in 2013, down from USD 7.7 million in 2012. This reflects that the depreciation of production assets and equipment has been suspended after classification of Rio das Contas as a held for sale investment with effect from April 1, 2013.

Panoro Energy recognized impairment charges of USD 46.8 million related to the operations in Brazil in 2013. This mainly relates to write-down of BS-3 licenses (Cavalo Marinho and Estrela do Mar) and small expenditure on Round-9 blocks and Coral prior to relinquishment. In November 2013, consortium partners were advised by ANP to meet the requirement of ADR wells in the development plan or risk forced relinquishment. Since then, the JV partners have attempted a farm-out of the licences which did not bring any success. As a result, it is imminent that the licences will be surrendered due to the non-commercial restrictions of ADR wells imposed by ANP and henceforth Panoro’s interest in the BS-3 area has been fully impaired and the carrying value of BS-3 licences as of December 31, 2013 is nil.

PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3 PA G E 1 9

Impairment charge of USD 47.2 million in 2012, represents write-down of BS-3 and Round-9 licences respectively by USD 42 million and USD 5.2 million.

Loss on disposal of the Company’s MKB permit in Republic of Congo was USD 1.7 million, which was recognised during 2013.

Share based payment charges were USD 0.2 million in the current year, compared to USD 1.2 million in 2012. The decline is mainly due to leavers and a declining balance of unvested options compared to prior year.

Earnings before interest and taxes (EBIT) were hence a negative USD 21.8 million for the full year 2013, compared to a negative USD 32 million in the previous year. The improvement is a result of lower G&A and depreciation and higher other income in 2013.

Net financial items amounted to a negative USD 22.2 million for the current year, including net interest costs of USD 13.0 million, net other financial costs of USD 1.2 million, a net foreign exchange gain of USD 0.7 million, and a USD 8.7 million charge to recognise reassessment of bond liability under IAS 39. The latter represents a discounted value of bond liability assuming a maximum of three month redemption assumption and is expected to coincide with the closing of the sale transaction of Rio das Contas to GeoPark. The outstanding bond liability was fully repaid subsequent to year end, after closing of Manati sale transaction to GeoPark.

This compared to net financial items of a negative USD 20.4 million in 2012, including net interest costs of USD 11.9 million, net other financial costs of USD 3.5 million, and a net foreign exchange loss of USD 4.9 million.

The net loss before tax was hence USD 43.9 million in 2013, compared to a net loss before tax of USD 52.4 million in 2012. The change mainly reflects reversal of deferred tax assets, which are less likely to be available for utilisation after completion of Rio das Contas sale.

The Group reflected an income tax charge of USD 10.8 million in 2013, compared to a tax benefit of USD 4.6 million in 2012. This mainly reflects recognition of deferred tax assets arising on tax losses in Brazil in 2012.

The reported net loss was thus USD 54.8 million in 2013, compared to a net loss of USD 47.8 million in 2012.

Other comprehensive loss was USD 19.1 million in 2013, reflecting a non-cash loss arising on the translation of Brazilian subsidiaries from BRL to USD for reporting purposes. BRL (Brazilian Reais) weakened 14.6% against the USD during the year. In 2012, other comprehensive loss was USD 18.4 million.

Total comprehensive loss was USD 73.9 million for 2013, compared to USD 66.2 million for 2012. All of the comprehensive loss was attributable to shareholders of the parent company.

Statement of financial positionThe Group’s total assets of USD 261.4 million at the end of 2013 correspond to a decline of USD 106.9 million from USD 368.3 million at the end of 2012. The Brazilian operations including held for sale items accounted for USD 116.4 million of total assets (2012: USD 179.0 million) and the West Africa operations for USD 94.5 million (2012: USD 135.9 million), with the remaining USD 50.5 million in corporate entities (2012: USD 53.4 million).

The decline in total assets partially reflects the negative effect of USD 46.8 million impairments of licenses and exploration assets in Brazil, USD 8.2 million decline in deferred tax assets, USD 19.1 million exchange loss arising on currency translations from BRL to USD and a reduction in cash balances due to repayment of bond loan and related interest.

Total non-current assets declined to USD 106.8 million (2012: USD 275.8 million) due to write-down of BS-3 asset and divestment of MKB. Total current assets stood at USD 57.7 million at the end of 2013 (2012: USD 92.5 million). The decline mainly reflects a reduction of the holding of cash and cash equivalents to USD 56.8 million including restricted cash (2012: USD 73.5 million). Trade and other receivables stood at USD 1.0 million at December 31, 2103 (2012: 19.0 million) with the decline representing reclassification of Rio das Contas related receivables as held for sale items.

During the year, the Group entered into an agreement with GeoPark to sell the entire shareholding in its subsidiary Rio das Contas for a cash consideration of USD 140 million. The transaction is effective from April 1, 2013 and as such all balances related to Rio das Contas have been classified as assets held for sale which stood at USD 96.9 million at the end of 2013. This classification is in accordance with IFRS 5.

Equity declined to USD 118.4 million (2012: USD 192.1 million), reflecting mainly the net loss for the year and a negative movement in currency translation reserve. There were no changes in the share capital during the year. The equity ratio declined to 45% (2012: 52%), reflecting both lower equity and a reduced total asset base.

Non-current liabilities were USD 4.4 million, a decline of USD 126.2 million from USD 130.6 million at the end of 2012. The decrease mainly reflects reclassification of interest-bearing debt to current liabilities and reclassification of Rio das Contas related liabilities as held for sale items. Current liabilities amounted to USD 124.2 million (2012: USD 45.6 million), with the increase mainly due to reclassification of bond liability as current partly offset by settlement of MKB related outstanding liabilities on disposal.

Total interest bearing debt (net of issue costs) totalled USD 118.9 million at the end of 2013 (2012: USD 126.3 million), which includes a USD 8.7 million of re-measurement effect incorporating a 6% early redemption premium. The decrease in liability can mainly be attributed to repayment of principal amount in November 2013, minor currency movements on the NOK tranche, and amortisation of debt issue costs offset by the re-measurement

PA G E 2 0 PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3

effects. The entire bond liability was repaid subsequent to year end on completion on Manati sale in April 2014.

Liabilities directly associated with assets classified as held for sale amounted to USD 14.4 million (2012: USD nil) and represents reclassifications of divested balances in relation to Rio das Contas (Manati) in accordance with the requirements of IFRS 5.

Cash flowsNet cash flow from operating activities amounted to USD 18.3 million in 2013, compared to USD 19.8 million in 2012. The decline is primarily explained by higher production costs incurred in 2013.

Net cash flow from investing activities was an inflow of USD 3.0 million in 2013, compared to an outflow of USD 21.8 million in 2012. The cash inflow in 2013 mainly relate to part divestment of West African portfolio and termination fee received from Lekoil offset by expenditure on drilling activity in Dussafu in Gabon and reclassification of USD 17.0 million of cash equivalents as held for sale.

Net cash flow from financing activities represented a cash outflow of USD 29.0 million in 2013, mainly comprising paid net financial charges of USD 15.4 million and bond repayments of USD 13.9 million. This compares to a cash outflow from financing activities of USD 33.1 million in 2012, including USD 19.1 million in net financial charges and USD 14.1 million of bond repayment.

Foreign exchange impact on cash balances was a negative USD 8.7 million in 2013 and a negative USD 2.3 million in 2012.

Cash and cash equivalents thus declined to USD 54.2 million (2012: USD 70.6 million), not including restricted cash balances of USD 2.6 million (2012: USD 2.9 million).

ALLOCATION OF PROFITS AND LOSSES

Parent company financial information

(Amounts in USD 000) 2013 2012

Total revenues 101 529

Operating expenses

Depreciation (6) (22)

General and administrative costs (3,670) (4,512)

Intercompany recharges (3,434) (3,508)

Share based payments (99) (230)

Loss on disposal of tangible assets - (75)

Impairment of investment in subsidiary (111,660) (23,425)

Write-down of capitalised exploration costs (512) -

Total operating expenses (119,381) (31,772)

Earnings before interest and tax (EBIT) (119,280) (31,243)

Net interest and financial items (16,069) (10,161)

Loss before taxes (135,349) (41,404)

Income tax benefit / (expense) - -

Net loss (135,349) (41,404)

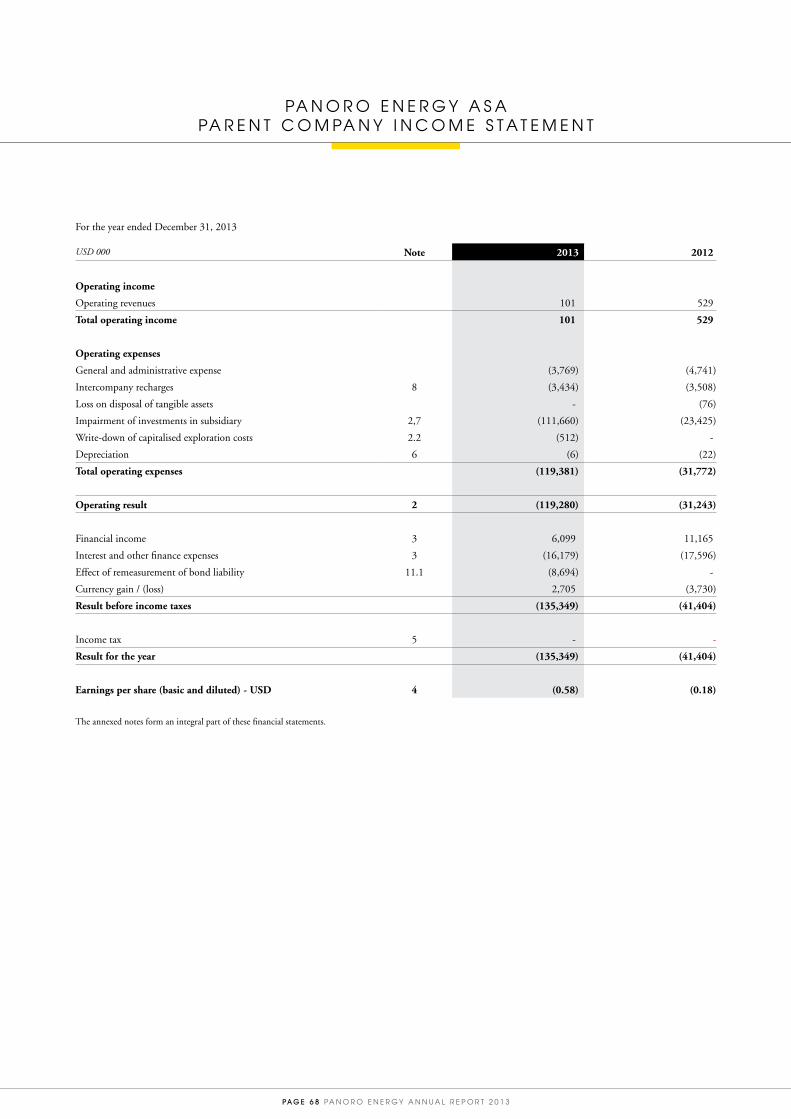

The total comprehensive loss of USD 135.3 million for 2013 was in its entirety attributable to the shareholders of the parent company.

The parent company Panoro Energy ASA had a net result of USD 135.3 million loss in 2013 (2012: USD 41.4 million loss). The Board of Directors propose that the net loss is allocated to other equity. Distributable equity in Panoro Energy ASA as per December 31, 2013 was nil. The Board of Directors does not propose an ordinary dividend for 2013.

Revenue in the parent company amounted to USD 0.1 million in 2013 (2012: USD 0.5 million), reflecting primarily management fee income from subsidiaries. EBIT was a negative USD 119.3 million (2012: negative USD 31.2 million), comprising general and administrative costs of USD 3.7 million (2012: USD 4.5 million), USD 111.7 million in impairment of investment in subsidiaries (2012: USD 23.4 million), USD 0.5 million of exploration costs write-downs (2012: USD nil) and USD 3.4 million in intercompany charges (2012: USD 3.5 million).

Net financial items were a negative USD 16.1 million (2012: USD negative 10.2 million) mainly representing bond interest expenses partially offset by finance income. The 2013 charge also includes USD 8.7 million non-cash effect of re-measurement of bond liability to include an anticipated 6% early redemption premium. There was no such adjustment in 2012.

The parent company had total assets of USD 298.8 million per December 31, 2013 (2012: USD 442.0 million), representing mainly investments and loans to subsidiaries of USD 247.7 million (2012: USD 389.0 million), cash balances of USD 48.9 million (2012: USD 50.4 million), and other assets of USD 2.2 million (2012: USD 2.6 million). Investments and intercompany receivables have declined, mainly reflecting impairment during the year. The decline in the cash balance mainly reflects funding of investments in Africa and servicing of bond commitments offset by proceeds from collection of intercompany loans.

Total liabilities in the parent company amounted to USD 125.1 million (2012: USD 133.2 million), comprising USD 118.9 million of bond loans (2012: USD 126.3 million) and USD 6.2 million relating to accounts and other payables (2012: USD 6.9 million).

Equity amounted to USD 173.7 million at December 31, 2013 (2012: USD 308.8 million) which has primarily declined due to loss for the year.

PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3 PA G E 2 1

FUNDING

The Company had focus on cash preservation and asset divestments during 2013. With challenging markets and a time consuming divestment process for the West Africa portfolio, the Company had focus on balancing its cash preservation with carefully honouring its investment commitments. During the year the Company’s cash position was mainly reduced due to investments in Dussafu and Manati. The cumulative cash balance as of December 31, 2013 was USD 56.8 million which excludes USD 17.0 million that has been classified as held for sale. This compared to USD 73.5 million of cash resources as of December 31, 2012. On an overall basis the cash position remained consistent since the close of 2012.

Panoro regards itself as being in a healthy financial situation due to its cash position and with the sale of Rio das Contas fully completed with bond repayment in April 2014, the Company is debt free with sufficient cash resources to fund its commitments.

RISK FACTORS

The development of oil and gas fields in which the Company is involved is associated with technical risk, alignment in consortiums with regards to development plans, and on obtaining necessary licenses and approvals from the authorities. Disruptions of operations might lead to cost overruns and production shortfall, or delays compared to the schedules laid out by the operator of the fields. As a non-operator, the Company has limited influence on operational risks related to exploration and development of the licenses and fields in which it has interests.

As the Company is exiting Brazil there are potential tax liabilities related among others to the divestment of Rio das Contas. In addition there are uncertainties related to the abandonment costs of BS-3 licenses.

The Company’s ability to successfully bid on and acquire additional property rights, to discover reserves, to participate in drilling opportunities and to identify and enter into commercial arrangements with customers will be dependent upon developing and maintaining close working relationships with industry partners, joint operators and authorities, as well as its ability to select and evaluate suitable properties, and complete transactions in a highly competitive environment.

Financial risk factorsFinancial risk is managed by the finance department in close co-operation with the business units, under policies approved by the Board of Directors. The overall risk management program seeks to minimize the potential adverse effects of unpredictable fluctuations in financial and commodity markets on financial performance, i.e., risks associated with currency exposures, debt servicing and oil and gas prices. Financial instruments such as derivatives, forward contracts and currency swaps are continuously being evaluated for the hedging of such risk exposures.

The Company has no interest rate risk exposure on its long-term borrowings, which exclusively consists of fixed-rate debt

arrangements. The Company’s cash holdings and bank balances are held in various currencies in different countries, and are subject to interest rate risk and credit risk.

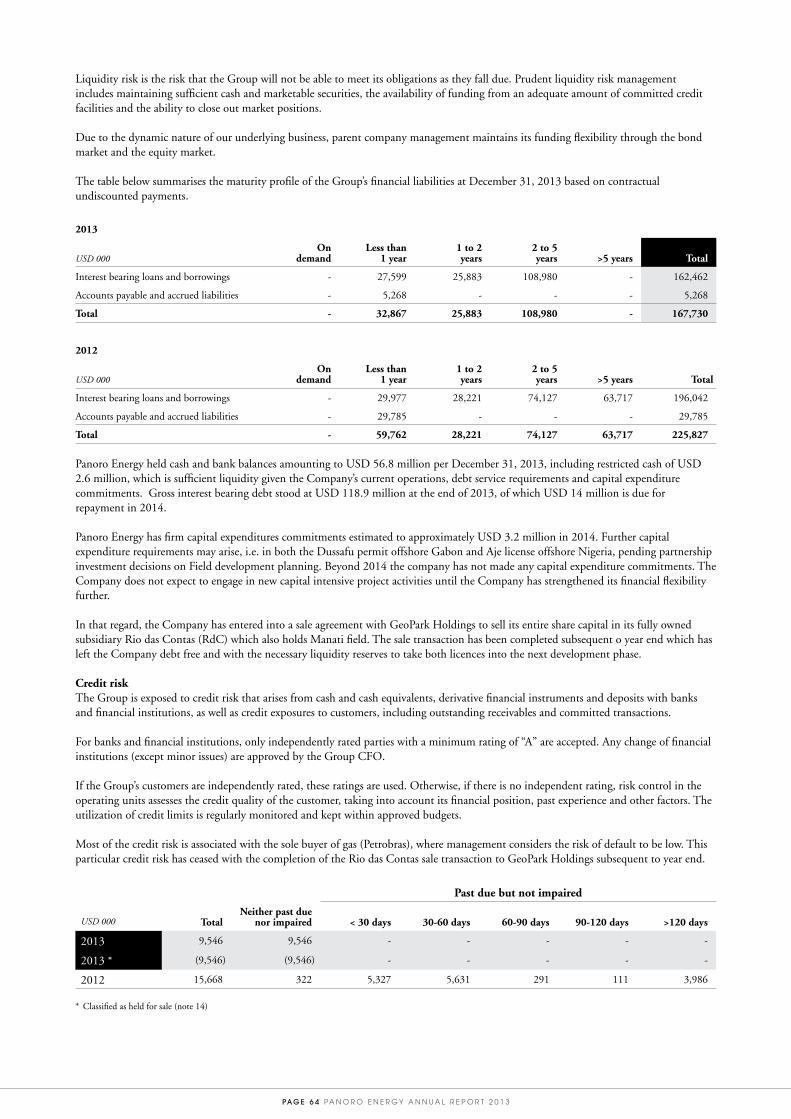

Panoro Energy held cash and bank balances amounting to USD 56.8 million per December 31, 2013, including restricted cash of USD 2.6 million, which is sufficient liquidity given the Company’s current operations, debt service requirements and capital expenditure commitments. Gross interest bearing debt stood at USD 118.9 million at the end of 2013, of which USD 14 million is due for repayment in 2014.

Panoro Energy had an estimated USD 3.2 million of contractual commitments as of December 31, 2013. Further capital expenditure requirements may arise, i.e. in both the Dussafu permit offshore Gabon and Aje licence offshore Nigeria, pending partnership investment decisions on Field Development planning. Beyond 2014, the Company has not made any capital expenditure commitments.

ORGANIZATION AND HEALTH, SAFETY AND ENVIRONMENT (HSE)

The management of the Company is led by CEO Jan Kielland. Mr. Kielland holds a MSc in Petroleum Engineering and more than 30 years of experience working with oil and gas companies. He is supported by CFO and Country Manager Brazil Anders Kapstad working out of Rio de Janeiro and COO Nishant Dighe working out of London.

At the end of 2013, Panoro Energy employed 23 persons (including part-time employees), 2 in Norway, 6 in UK and 15 in Brazil. This was a decline from 30 people at the end of 2012. As of January 1, 2014, Panoro Energy employed 19 persons, 1 in Norway, 6 in UK and 12 in Brazil. The workforce has been reduced to 10 full time employees following the divestment of Rio das Contas as a result of the ongoing efforts to reduce G&A costs.

The Company emphasizes the importance of a good working environment both for the individual employee and for the work to achieve Company goals and objectives. The objective is to create a constructive working environment characterized by a spirit where ideas and initiatives are welcome, founded on mutual trust between employees, management and the Board of Directors.

Panoro Energy’s vision for Health, Safety and Environment (HSE) is to avoid accidents and incidents and minimize the impact of its activities on the environment. Panoro performs all its activities with focus on and respect for people and the environment. The Board believes this is a key condition for creating value in a very demanding business. The Company’s vision for health, environment, safety and quality (HSEQ) is zero accidents and zero unwanted incidents in all activities. The Company strives towards performing all its activities with no harm to people or the environment. Panoro experienced no major accidents, injuries, incidents or any environmental claims during the year.

Company time lost due to employee illness or accidents was less than 1 per cent of total hours worked during the year. Employee

PA G E 2 2 PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3

safety is of the highest priority, and company policies imply continuous work towards identifying and employing administrative and technical solutions that ensure a safe and efficient work-place.

The Company has established a set of operational guidelines building on its principles of Corporate Governance, covering critical operational aspects ranging from ethical issues and practical travel advice to delegation of authority matrices.

The asset bases in South America and West Africa means frequent travel, and the Company seeks to ensure adequate safety levels for employees travelling. An emergency preparedness organization has been established, in which membership in International SOS is a key factor. International SOS provides updated risk assessments, medical support and evacuation services worldwide.

As a non-operator, Panoro is dependent on the efforts of the operators with respect to achieving physical results in the field. However, the Company has chosen to take an active role in all license committees with the conviction that high safety standards are the best means to achieve successful operations. Through this involvement, the Company can influence the choice of technical solutions, vendors and quality of applied procedures and practices.

The Company’s operations have been conducted by the operators on behalf of the licensees, at acceptable HSE standards. No accidents that resulted in loss of human lives or serious damage to people or property have been reported.

Panoro Energy is committed to work towards minimizing waste and pollution as a consequence of its activities. Operations at the main offices in Rio de Janeiro and London do not pollute the environment. A video-conferencing system has been installed to reduce travel requirements, reducing both operational costs and carbon footprint.

As described above, all operating activities are being conducted by operators on behalf of the Company, and to the best of the Company’s knowledge, all operations have been conducted within the limits set by approved environmental regulatory authorities.

CORPORATE GOVERNANCE

The main objective for Panoro Energy ASA’s Corporate Governance is to develop a strong, sustainable and competitive company in the best interest of the shareholders, employees and society at large, within the laws and regulations of the respective country. The Board and management aim for a controlled and profitable development and long-term creation of growth through well-founded governance principles and risk management.

Panoro Energy acknowledges that successful value-added business is profoundly dependent upon transparency and internal and external confidence and trust. Panoro Energy believes that this is achieved by building a solid reputation based on our financial performance, our values and by fulfilling our promises. Thus, good corporate governance combined with Panoro Energy’s Code of Conduct is an important tool in helping the Board to ensure that we properly discharge our duty.

The composition of the Board ensures that the Board represents the common interests of all shareholders and meets the Company’s need for expertise, capacity and diversity. The members of the Board represent a wide range of experience including shipping, offshore, energy, banking and investment. The composition of the Board ensures that it can operate independently of any special interests. Members of the Board are elected for a period of two years. Recruitment of members of the Board will be phased so that the entire Board is not replaced at the same time. The Chairman of the Board of Directors is elected by the General Meeting.

Any acquisition of own shares will be at market price, and the Company will not deviate from the principle of equal treatment of all shareholders. Any decision to deviate from the principle of equal treatment by waiving the pre-emption rights of existing shareholders to subscribe for shares in the event of an increase in share capital will be justified. Such deviation will be made only if in the common interest of the shareholders and the Company.

The Board may be given a power of attorney by the General Meeting to acquire the Company’s own shares. If the Board of Directors resolves to carry out an increase in share capital on the basis of a mandate granted to the Board, the justification for waiving pre-emption rights of existing shareholders will be disclosed in the stock exchange announcement of the increase in share capital.

In the event that the Company carries out any transactions in its own shares, these will be carried out through a regulated marketplace at market price. If there is limited liquidity in the Company’s shares at the time of such transaction, the Company will consider other ways to ensure equal treatment of all shareholders.

The Company has not granted any loans or guarantees to anyone in the management or any of the directors.

The Board acknowledges the Norwegian Code of Practice for Corporate Governance of October 23, 2012 and the principle of comply or explain. Panoro Energy has implemented the Code and will use its guidelines as the basis for the Board’s governance duties. A summary of the corporate governance policy is incorporated in a separate section of this report and a lengthier version of the policy is posted on the Company’s website at www.panoroenergy.com.

The Company has implemented a policy for Ethical Code of Conduct and work diligently to comply with these guidelines. The full policy is enclosed in this annual report (see section Ethical Code of Conduct

DISCRIMINATION AND EQUAL EMPLOYMENT OPPORTUNITIES

Panoro Energy is an equal opportunity employer, with an equality concept integrated in its human resources policies. A diversified working environment is embraced, and the Company’s personnel policies promote equal opportunities and rights and prevent discrimination based on gender, ethnicity, colour, language, religion or belief. All employees are governed by Panoro Energy’s Code of

PA N O R O E N E R G Y A N N U A L R E P O R T 2 0 1 3 PA G E 2 3

Conduct, to ensure uniformity in behaviour across a workforce representing 8 different nationalities.

Panoro Energy is a knowledge-based company in which a majority of the workforce has earned college or university level educations, or has obtained industry-recognized skills and qualifications specific to their job requirements. Employees are remunerated exclusively based upon skill level, performance and position.

57% of the employees were men and 43% women (67% and 33%, respectively in Q4-2012). There are currently no women in Panoro Energy’s senior management.

DIRECTORS AND SHAREHOLDERS

According to its articles of association, the Company shall have a minimum of three and a maximum of eight directors on its Board. The number of Board members was five at year end 2013 (reduced to four in January 2014), all non-executive directors. The members have varied backgrounds and experience, offering the Company valuable perspectives on industrial, operational and financial issues. Two of the four current Board members are female. The Board held 13 meetings during the year.

OUTLOOK

Panoro Energy has been narrowing its geographical focus during 2013 with core focus on Gabon and Nigeria in West Africa as the Company is in the process of exiting Brazil. The Company’s main asset, the Manati field was divested by the end of Q1 2014.

Panoro Energy has had discussions with the operator and Brazilian authorities (ANP) with regards to the BS-3 licenses in the Santos Basin, but as the farm out attempt did not yield results the Company has decided to relinquish these assets. Commercialising the fields faces significant challenges including the need to deal with the associated gas as well as the obligation that the ANP imposed on the joint ventures to the drill multiple high cost B1 wells.