of www. pans.co.id www. post.co.id 1 14 Coal Mining & Contracting Sector FAJAR INDRA [email protected] +62215153055 Prepared by December 2014

Panin Sekuritas Coal Sector Outlook 2015-edited

Aug 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ofwww. pans.co.id www. post.co.id 1 14

Coal Mining & Contracting Sector

FAJAR [email protected]

+62215153055

Prepared by

December 2014

ofwww. pans.co.id www. post.co.id 2 31

Global Economic Outlook 2015 – Recoveries

Viany Indah

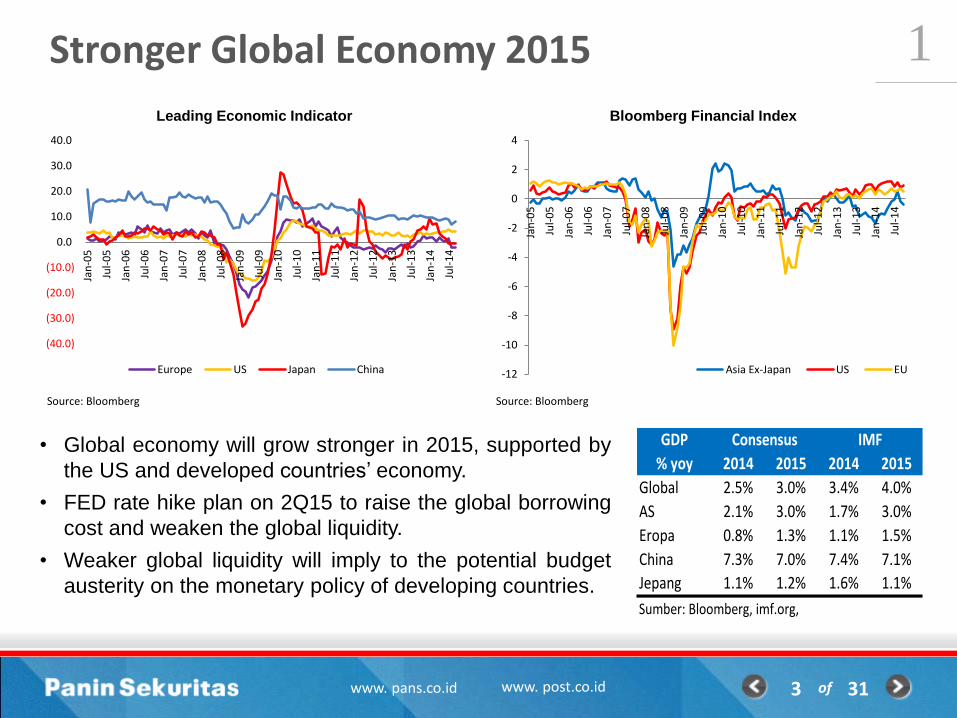

Stronger Global Economy 2015

ofwww. pans.co.id www. post.co.id

1

3 31

Source: Bloomberg

• Global economy will grow stronger in 2015, supported by

the US and developed countries’ economy.

• FED rate hike plan on 2Q15 to raise the global borrowing

cost and weaken the global liquidity.

• Weaker global liquidity will imply to the potential budget

austerity on the monetary policy of developing countries.

Source: Bloomberg

GDP

% yoy 2014 2015 2014 2015

Global 2.5% 3.0% 3.4% 4.0%

AS 2.1% 3.0% 1.7% 3.0%

Eropa 0.8% 1.3% 1.1% 1.5%

China 7.3% 7.0% 7.4% 7.1%

Jepang 1.1% 1.2% 1.6% 1.1%

Sumber: Bloomberg, imf.org,

Consensus IMF

-12

-10

-8

-6

-4

-2

0

2

4

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Bloomberg Financial Index

Asia Ex-Japan US EU

(40.0)

(30.0)

(20.0)

(10.0)

0.0

10.0

20.0

30.0

40.0

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Leading Economic Indicator

Europe US Japan China

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Mar

-05

Oct

-05

May

-06

Dec

-06

Jul-

07

Feb

-08

Sep

-08

Ap

r-0

9

No

v-0

9

Jun

-10

Jan

-11

Au

g-1

1

Mar

-12

Oct

-12

May

-13

Dec

-13

Jul-

14

Chinese GDP Growth & Inflation

GDP Growth (yoy) Inflation

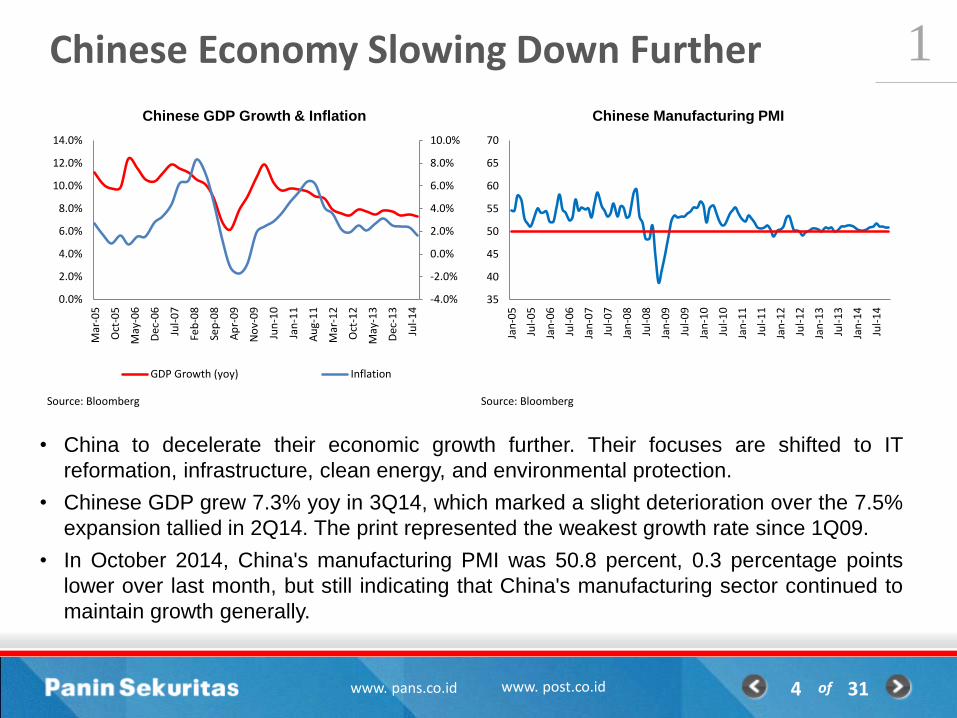

Chinese Economy Slowing Down Further

ofwww. pans.co.id www. post.co.id

1

4 31

Source: Bloomberg

• China to decelerate their economic growth further. Their focuses are shifted to IT

reformation, infrastructure, clean energy, and environmental protection.

• Chinese GDP grew 7.3% yoy in 3Q14, which marked a slight deterioration over the 7.5%

expansion tallied in 2Q14. The print represented the weakest growth rate since 1Q09.

• In October 2014, China's manufacturing PMI was 50.8 percent, 0.3 percentage points

lower over last month, but still indicating that China's manufacturing sector continued to

maintain growth generally.

Source: Bloomberg

35

40

45

50

55

60

65

70

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Chinese Manufacturing PMI

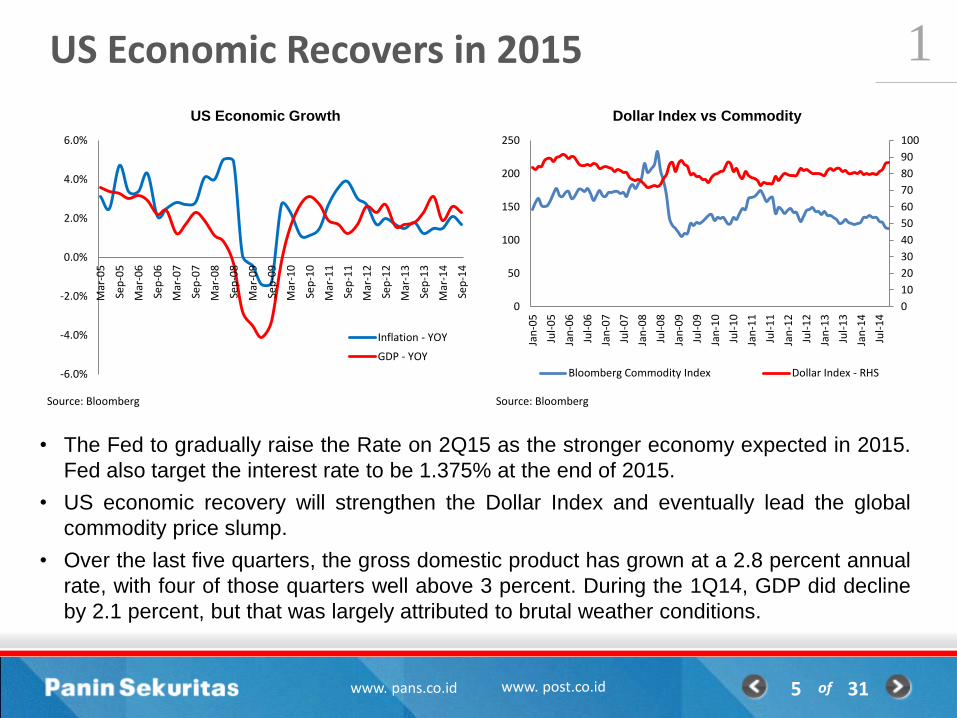

US Economic Recovers in 2015

ofwww. pans.co.id www. post.co.id

1

5 31

Source: Bloomberg

• The Fed to gradually raise the Rate on 2Q15 as the stronger economy expected in 2015.

Fed also target the interest rate to be 1.375% at the end of 2015.

• US economic recovery will strengthen the Dollar Index and eventually lead the global

commodity price slump.

• Over the last five quarters, the gross domestic product has grown at a 2.8 percent annual

rate, with four of those quarters well above 3 percent. During the 1Q14, GDP did decline

by 2.1 percent, but that was largely attributed to brutal weather conditions.

Source: Bloomberg

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

Mar

-05

Sep

-05

Mar

-06

Sep

-06

Mar

-07

Sep

-07

Mar

-08

Sep

-08

Mar

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

Sep

-13

Mar

-14

Sep

-14

US Economic Growth

Inflation - YOY

GDP - YOY

0

10

20

30

40

50

60

70

80

90

100

0

50

100

150

200

250

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Dollar Index vs Commodity

Bloomberg Commodity Index Dollar Index - RHS

ofwww. pans.co.id www. post.co.id 6 31

Coal Market Outlook 2015 - No Turnaround Story

Fajar IndraTechnical Perspective by Purwoko Sartono

Thermal Coal Global Balance: Oversupply

ofwww. pans.co.id www. post.co.id

2

7 31

Source: BREE, McKloskey, SXCoal, Peabody, Bloomberg, ITMG, ADRO, PANS Estimates

(mio tonnes) Additional

Input/OutputRemarks

Supply

Indonesia +10.0 Production Cap, Stronger Domestic Demand, DMO, Tax Levels

Australia +10.0 Chinese Import Tax, AUD Depreciation, Diminishing Exploration

Russia +4.5 Divert Coal To Export Due To Lower Domestic Demand

Columbia +5.0 Production Target Lifting, Cerrejon & Drummond Expansions

South Africa +1.5 Limited Rail Capacity, Uncertain Expansion

US -5.0 Arbitrage for Exports Closing, Continued Domestic Retraction

Others -2.0 Small Coal Producers Witn Higher Cash Cost

Global +28.0

Demand

China -15.0 Weaker Economic Growth, Protectionism Policy

Japan +2.0 High Reliance on Thermal Generator, Some Nuclear Reactors Are Reactivated

Europe -5.0 High Inventory, Power Plants Retirement Continues

India +20.0 Facing Coal Shortage, Increased Power Demand

Others +5.0 Other Asian & South Americas Drive Demand Growth

Global +7.0

• The market is still plagued by oversupply. The supply glut that’s driven coal to the lowest

since 2009 will more than double next year.

• Demand will increase at a modest rate and prices will remain near the level of marginal

production costs.

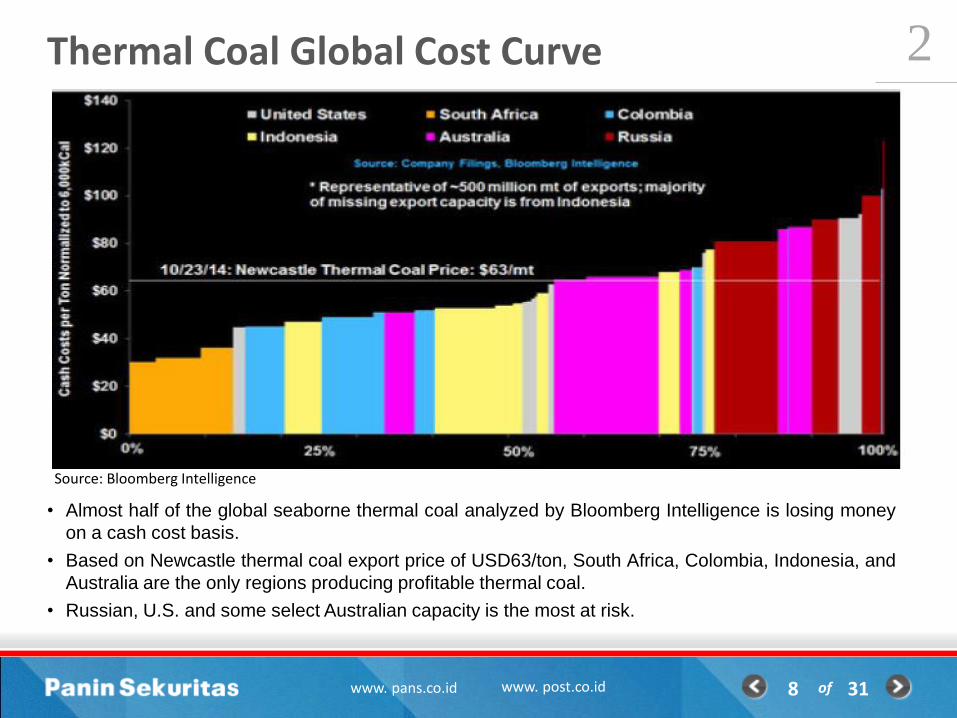

Thermal Coal Global Cost Curve

ofwww. pans.co.id www. post.co.id

2

8 31

Source: Bloomberg Intelligence

• Almost half of the global seaborne thermal coal analyzed by Bloomberg Intelligence is losing money

on a cash cost basis.

• Based on Newcastle thermal coal export price of USD63/ton, South Africa, Colombia, Indonesia, and

Australia are the only regions producing profitable thermal coal.

• Russian, U.S. and some select Australian capacity is the most at risk.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Chinese Coal Import, Including Brown Coal (miotonnes)

0.0

100.0

200.0

300.0

400.0

500.0

600.0

Chinese Electricity Output (bio KWh)

Hydro Nuclear Thermal

China: Weak Demand Continues in 2015

ofwww. pans.co.id www. post.co.id

2

9 31

Source: Bloomberg Source: Bloomberg

• Chinese seaborne coal demand until 10M14 is not living up the expectation. Coal imports fall 4.8%

yoy to 243.8 mio tonnes, supported by the significant import decline from Indonesia (27.7% yoy).

• Growth in imports has been moderated by slower economic activity, increased utilisation of

hydropower and relatively low domestic prices which reduced the competitiveness of imports.

• The thermal electricity output growth until 10M14 is steady by growing 0.4% yoy to 3160 bio KWh.

• The coal import will likely weaken further in 2015 as China to set higher standards on coal quality.

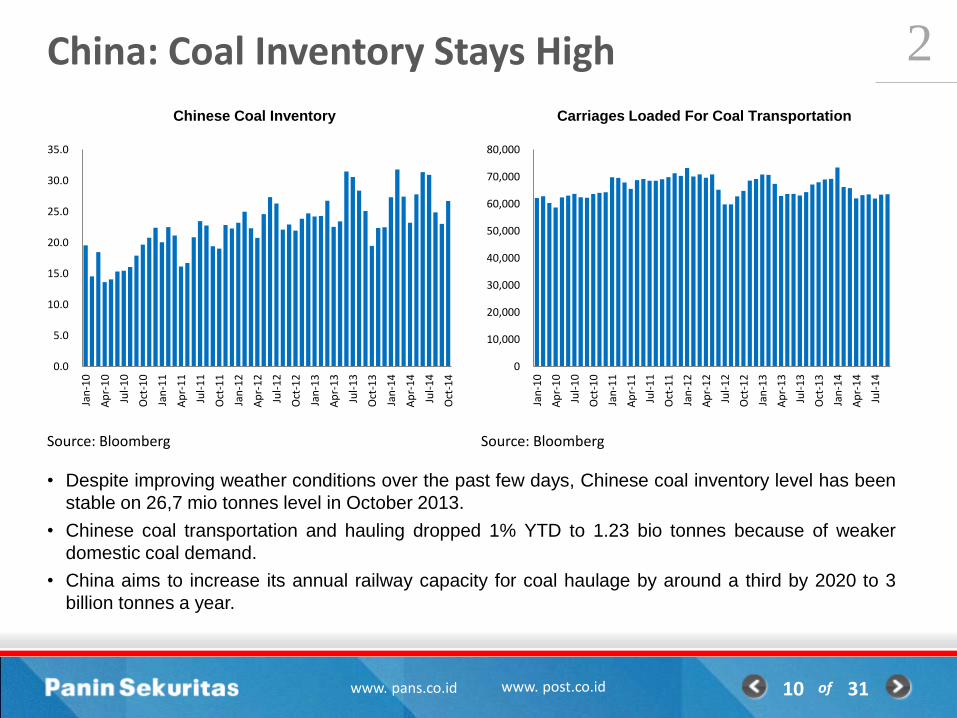

China: Coal Inventory Stays High

ofwww. pans.co.id www. post.co.id

2

10 31

Source: Bloomberg Source: Bloomberg

• Despite improving weather conditions over the past few days, Chinese coal inventory level has been

stable on 26,7 mio tonnes level in October 2013.

• Chinese coal transportation and hauling dropped 1% YTD to 1.23 bio tonnes because of weaker

domestic coal demand.

• China aims to increase its annual railway capacity for coal haulage by around a third by 2020 to 3

billion tonnes a year.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Chinese Coal Inventory

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Carriages Loaded For Coal Transportation

Development in Chinese Energy Policy

ofwww. pans.co.id www. post.co.id

2

11 31

• China has announced that it will restrict

consumption of thermal coal with high ash and

sulphur content from 1 January 2015.

• China has introduced a 3% import tax for both

anthracite and coking coal and 6% for

bituminous imports starting 15 October 2014 to

protect its domestic coal producers.

• China has announced that it will replace its tax

on coal production with a tax on coal sales

from 1 December 2014.

• China has mandated that power utilities reduce

their coal imports by a combined 50 mio

tonnes in 2014.

• China has announced an action plan to

improve the operating efficiency of coal-fired

power plants between 2014 and 2020. It is

targeted that plants will reduce their thermal

coal use to between 300–310g/kWh by 2020.

• China to punish coal mines operating above

approved capacity. Companies that exceed

production limits will be fined and have their

license suspended.

Australia31%

Indonesia17%Russia

9%Mongolia

6%

North Korea5%

Others32%

Chinese Seaborne Coal Import

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

Jan

-12

Mar

-12

May

-12

Jul-

12

Sep

-12

No

v-1

2

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-1

3

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

Chinese Domestic Coal Production

Source: Bloomberg

Source: Bloomberg

India: Facing Coal Shortages

ofwww. pans.co.id www. post.co.id

2

12 31

Source: BREE, Coal Ministry of India Source: Central Electricity Authority of India

• India’s electricity demand is expected to rise substantially over the projection period as household

income increases, the middle class expands and the government improves electrification. India is

halfway though building another 65 GW Powerplant until 2017.

• The coal producers are projected to be unable to fulfill the whole Indian coal consumption because of

the infrastructure bottleneck.

• Coal-fired power is a major component of India’s existing electricity generation capacity and this role

is expected to expand with more than 100 GW of new coal-fired capacity under construction.

118 124 132 143 148

159 174

200

223

246 260

272 288

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014F2015F2016F2017F

Indian Power Plant Capacity

21.7 25.2 33.3

40.8

58.3

71.8

98.2

123.0 130.0

145.0 155.0

160.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E 2015F 2016F

Indian Coal Import Volume

Japan: Still Relies On Thermal Power, But May Decline

ofwww. pans.co.id www. post.co.id

2

13 31

Source: BREE, ABARES Source: Federal Electrical Companies of Japan

• Japan has relied heavily on thermal power (oil, gas and coal) since the end of 2013 when all of its

nuclear capacity was closed.

• Japanese coal demand may decline if authorities move forward with the reactivation of nuclear

reactors in a bid to reduce reliance on foreign energy sources.

• As older coal-fired capacity is closed, Japan’s coal imports are projected to decline at an average

annual rate of 2.2% from 142 mio tonnes in 2014 to 127 mio tonnes in 2019.

128.8 126.7

111.4

127.7 121.5

131.6

141.8 142.0 140.0

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

2007 2008 2009 2010 2011 2012 2013 2014E 2015F

Japanese Coal Import

8%

78%

13%

1%

Japanese Power Generator 2013

Hydroelectric Thermal Nuclear Others

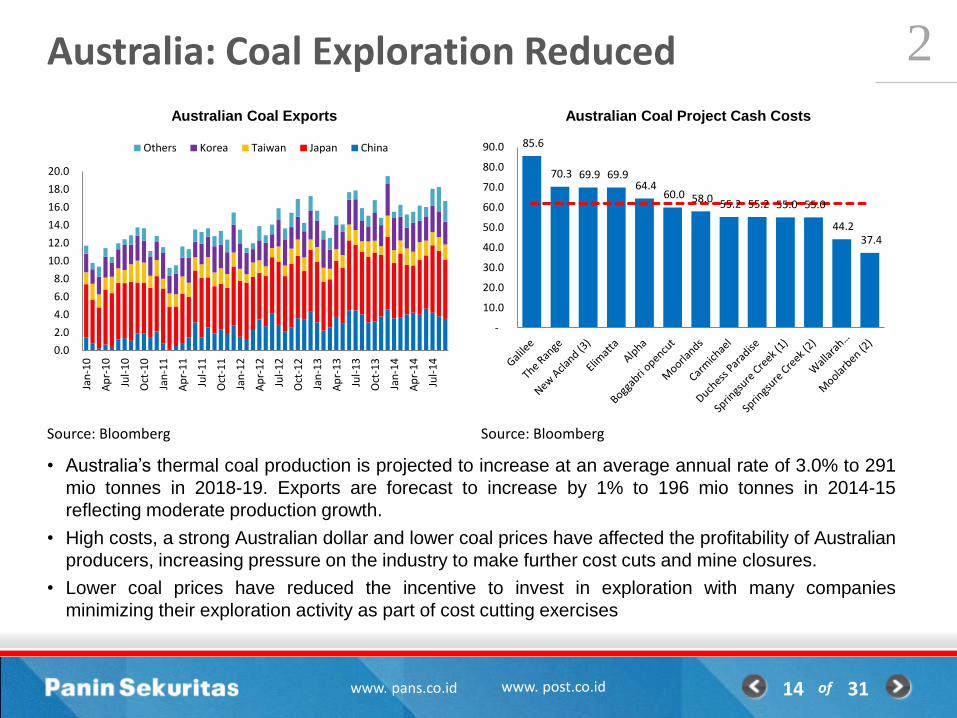

Australia: Coal Exploration Reduced

ofwww. pans.co.id www. post.co.id

2

14 31

Source: Bloomberg Source: Bloomberg

• Australia’s thermal coal production is projected to increase at an average annual rate of 3.0% to 291

mio tonnes in 2018-19. Exports are forecast to increase by 1% to 196 mio tonnes in 2014-15

reflecting moderate production growth.

• High costs, a strong Australian dollar and lower coal prices have affected the profitability of Australian

producers, increasing pressure on the industry to make further cost cuts and mine closures.

• Lower coal prices have reduced the incentive to invest in exploration with many companies

minimizing their exploration activity as part of cost cutting exercises

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Australian Coal Exports

Others Korea Taiwan Japan China 85.6

70.3 69.9 69.9 64.4

60.0 58.0 55.2 55.2 55.0 55.0

44.2 37.4

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Australian Coal Project Cash Costs

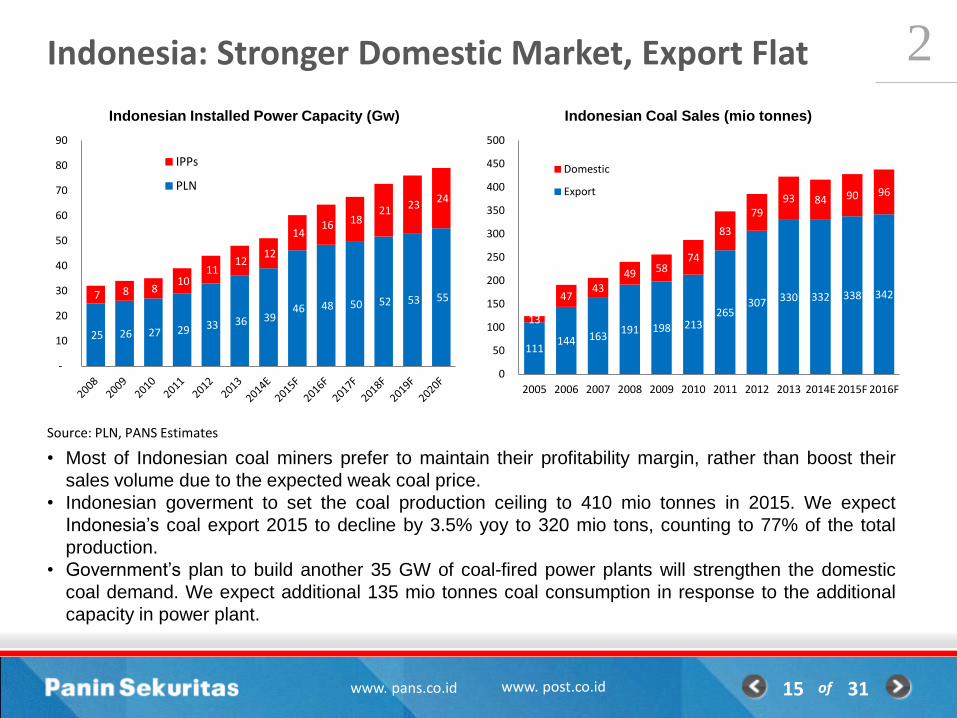

Indonesia: Stronger Domestic Market, Export Flat

ofwww. pans.co.id www. post.co.id

2

15 31

Source: PLN, PANS Estimates

• Most of Indonesian coal miners prefer to maintain their profitability margin, rather than boost their

sales volume due to the expected weak coal price.

• Indonesian goverment to set the coal production ceiling to 410 mio tonnes in 2015. We expect

Indonesia’s coal export 2015 to decline by 3.5% yoy to 320 mio tons, counting to 77% of the total

production.

• Government’s plan to build another 35 GW of coal-fired power plants will strengthen the domestic

coal demand. We expect additional 135 mio tonnes coal consumption in response to the additional

capacity in power plant.

111 144 163

191 198 213 265

307 330 332 338 342

13

47 43

49 58 74

83

79 93 84 90 96

0

50

100

150

200

250

300

350

400

450

500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E 2015F 2016F

Indonesian Coal Sales (mio tonnes)

Domestic

Export

25 26 27 29 33 36 39 46 48 50 52 53 55 7 8 8

10 11

12 12

14 16 18

21 23 24

-

10

20

30

40

50

60

70

80

90

Indonesian Installed Power Capacity (Gw)

IPPs

PLN

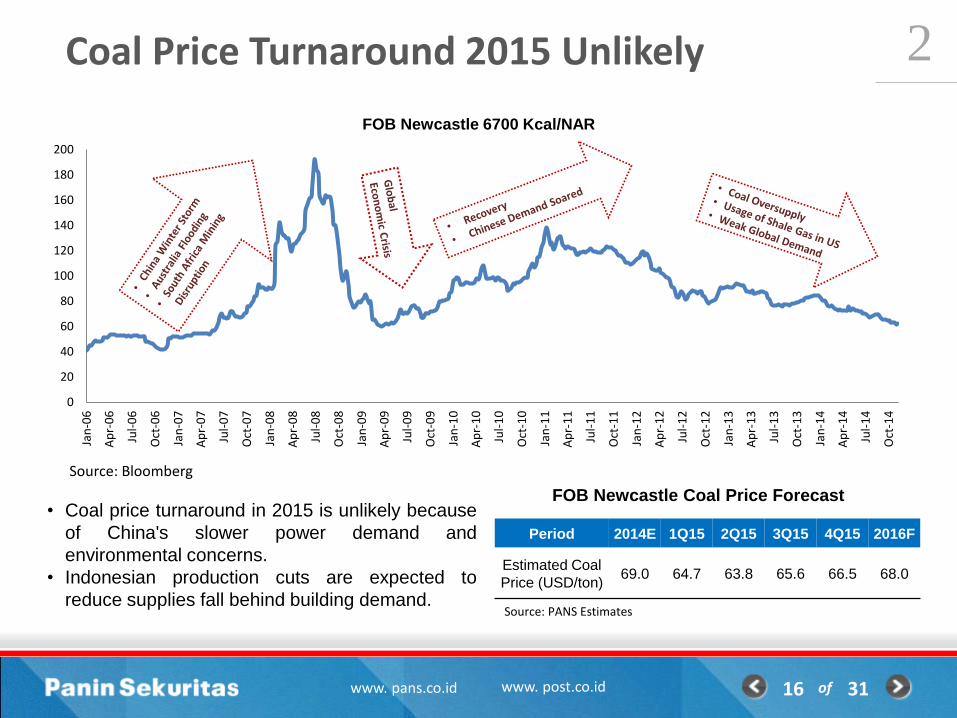

Coal Price Turnaround 2015 Unlikely

ofwww. pans.co.id www. post.co.id

2

16 31

Source: Bloomberg

• Coal price turnaround in 2015 is unlikely because

of China's slower power demand and

environmental concerns.

• Indonesian production cuts are expected to

reduce supplies fall behind building demand.

FOB Newcastle Coal Price Forecast

Period 2014E 1Q15 2Q15 3Q15 4Q15 2016F

Estimated Coal

Price (USD/ton)69.0 64.7 63.8 65.6 66.5 68.0

Source: PANS Estimates

0

20

40

60

80

100

120

140

160

180

200

Jan

-06

Ap

r-0

6

Jul-

06

Oct

-06

Jan

-07

Ap

r-0

7

Jul-

07

Oct

-07

Jan

-08

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

FOB Newcastle 6700 Kcal/NAR

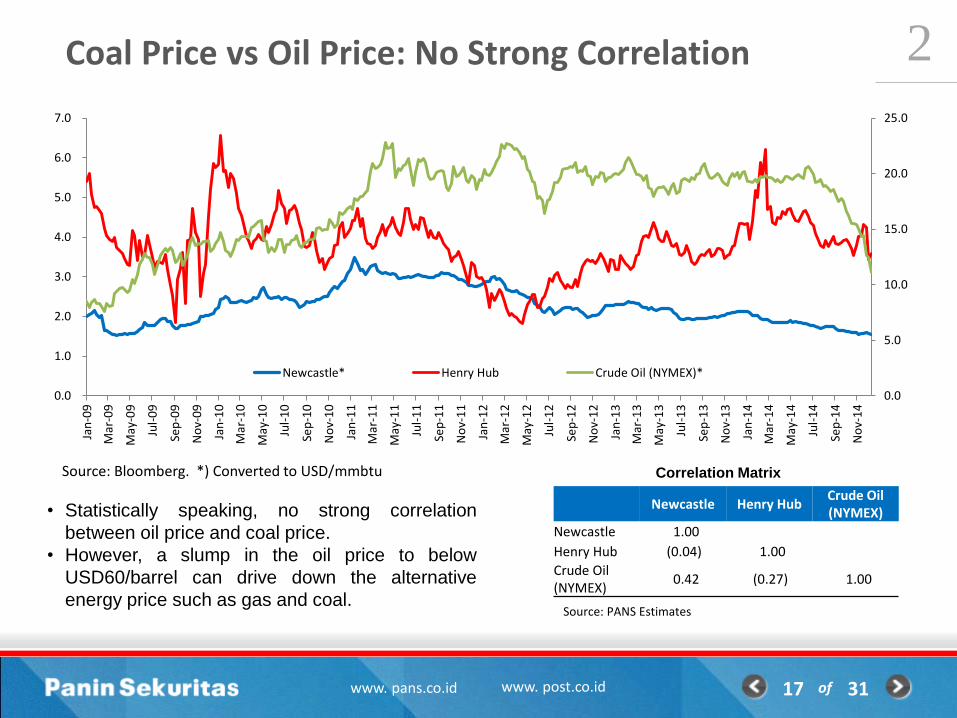

Coal Price vs Oil Price: No Strong Correlation

ofwww. pans.co.id www. post.co.id

2

17 31

• Statistically speaking, no strong correlation

between oil price and coal price.

• However, a slump in the oil price to below

USD60/barrel can drive down the alternative

energy price such as gas and coal.

0.0

5.0

10.0

15.0

20.0

25.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Jan

-09

Mar

-09

May

-09

Jul-

09

Sep

-09

No

v-0

9

Jan

-10

Mar

-10

May

-10

Jul-

10

Sep

-10

No

v-1

0

Jan

-11

Mar

-11

May

-11

Jul-

11

Sep

-11

No

v-1

1

Jan

-12

Mar

-12

May

-12

Jul-

12

Sep

-12

No

v-1

2

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-1

3

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-1

4

Newcastle* Henry Hub Crude Oil (NYMEX)*

Source: Bloomberg. *) Converted to USD/mmbtu

Newcastle Henry HubCrude Oil (NYMEX)

Newcastle 1.00

Henry Hub (0.04) 1.00

Crude Oil (NYMEX)

0.42 (0.27) 1.00

Correlation Matrix

Source: PANS Estimates

Coal Price: Technical Perspective

ofwww. pans.co.id www. post.co.id

2

18 31

The Newcastle coal price is still running on the bearish region as depicted on the chart above. The

coal price is forming the wave 5 with the Fibonacci Projection target150% to USD58,2/ton, implied

to 9,9% downside. However, that Elliot Wave scenario can be denied if the coal price rebounds to

wave 4 in USD69,5/ton.

ofwww. pans.co.id www. post.co.id 19 31

Indonesian Coal 2015 – Entering The Downstream

Fajar Indra

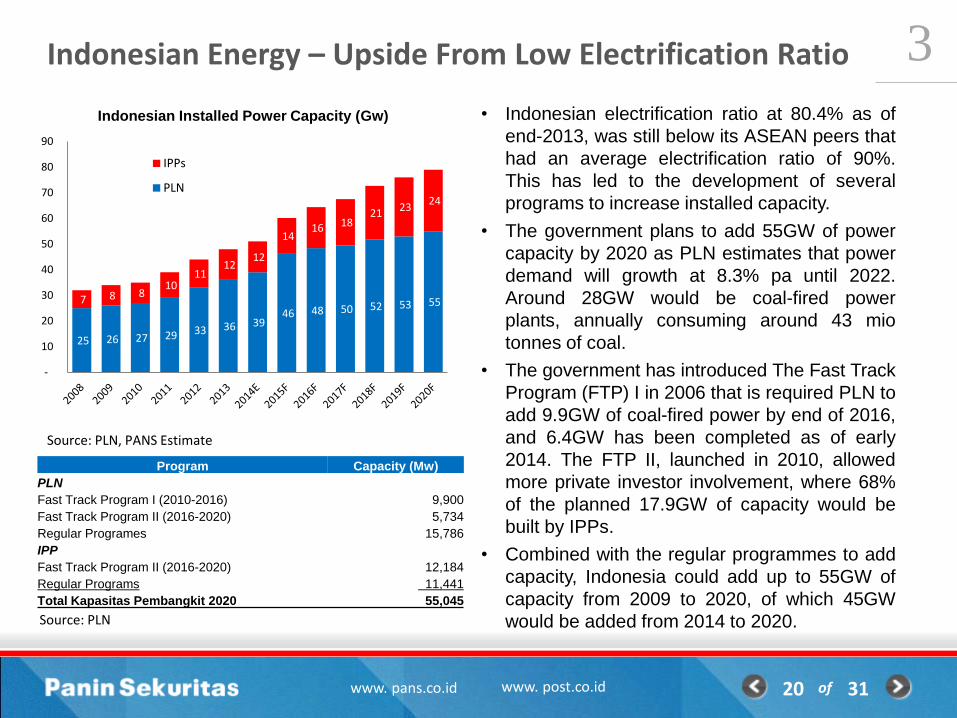

Indonesian Energy – Upside From Low Electrification Ratio

ofwww. pans.co.id www. post.co.id

3

20 31

Source: PLN, PANS Estimate

Source: PLN

• Indonesian electrification ratio at 80.4% as of

end-2013, was still below its ASEAN peers that

had an average electrification ratio of 90%.

This has led to the development of several

programs to increase installed capacity.

• The government plans to add 55GW of power

capacity by 2020 as PLN estimates that power

demand will growth at 8.3% pa until 2022.

Around 28GW would be coal-fired power

plants, annually consuming around 43 mio

tonnes of coal.

• The government has introduced The Fast Track

Program (FTP) I in 2006 that is required PLN to

add 9.9GW of coal-fired power by end of 2016,

and 6.4GW has been completed as of early

2014. The FTP II, launched in 2010, allowed

more private investor involvement, where 68%

of the planned 17.9GW of capacity would be

built by IPPs.

• Combined with the regular programmes to add

capacity, Indonesia could add up to 55GW of

capacity from 2009 to 2020, of which 45GW

would be added from 2014 to 2020.

25 26 27 29 33 36 39 46 48 50 52 53 55 7 8 8

10 11

12 12

14 16 18

21 23 24

-

10

20

30

40

50

60

70

80

90

Indonesian Installed Power Capacity (Gw)

IPPs

PLN

Program Capacity (Mw)

PLN

Fast Track Program I (2010-2016) 9,900

Fast Track Program II (2016-2020) 5,734

Regular Programes 15,786

IPP

Fast Track Program II (2016-2020) 12,184

Regular Programs 11,441

Total Kapasitas Pembangkit 2020 55,045

Indonesian Energy – Replacing Diesel to Coal

ofwww. pans.co.id www. post.co.id

3

21 31

Source: PLN, PANS Estimate Source: PLN

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009 2010 2011 2012 2013 2014E 2015F

Indonesian Power Generation

Others Diesel Hydro Natural Gas Coal

• Indonesia has 46GW of installed power generation capacity as of end-2013. Around 45% is fuelled

by coal, while 30% is either gas powered or coal fired power plants.

• Diesel’s share of overall power generation has declined over the past 5 years and been replaced by

coal and natural gas power generation. The fuel cost for diesel power generation is almost 8x higher

than that of coal and 3x higher than that of natural gas power generation.

• Around 18GW of coal power capacity has already been assigned in the FTP II and IPP programmes,

while geothermal would add 7.3GW.

66%

26%

8%

PLN’s Fast Track Program II

Coal Geothermal Others

Higher Expectation on Domestic Coal Demand

ofwww. pans.co.id www. post.co.id

3

22 31

Source: ESDM, PANS Estimate Source: PLN, PANS Estimates

• We believe the additional 28 Gw power capacity for coal-fired powerplant over the next 5-6 years will

be translated to the rising of domestic coal consumption.

• While the consumption is expected to grow, production is expected to shrink as the thermal coal price

is getting weaker.

• However, Indonesian coal exports may decline following the new regulation that requires licenses as

registered exporters to export the coal. It can stimulate the coal trading shifting to the domestic

market.

-

5

10

15

20

25

30

35

40

2008 2009 2010 2011 2012 2013 2014E 2015F 2016F 2017F

Indonesian Coal-Fired Installed Capacity (Gw)

IPPs

PLN

13

47 43

49

58

74

83 79

93 84

90 96

105

0

20

40

60

80

100

120

Indonesian Coal Consumption

Production Flat as The Coal Price Weaker

ofwww. pans.co.id www. post.co.id

3

23 31

Source: ESDM, PANS Estimate Source: PLN, PANS Estimates

• Indonesian government has imposed the annual coal production ceiling at 420 mio tonnes in 2014 as

the coal price getting weaker.

• Most of Indonesian mining companies focus on maintaining the operational cost rather than ramping up

the production. Some of them have even suspended the mining operation.

• Most of mining companies strip ratios will be flat in 2015, indicated their initiatives to reduce the cost

and hold the expansion.

114 153 157 167

198 219 244 255 271 275 276 275

10

38 49 73

58 68

104 130

151 141 152 155

0

50

100

150

200

250

300

350

400

450

500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E 2015F 2016F

Indonesian Coal Production

Mining Licenses CCOW

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Kideco BUMI ADRO PTBA ITMG HRUM

Strip Ratio of Major Coal Companies

2013 2014E 2015F

Indonesian Coal Miners – The Best Among The Worst

ofwww. pans.co.id www. post.co.id

3

24 31

• We prefer PTBA & ADRO to be our “best among the worst” for the coal sector. PTBA has the highest

exposure to domestic coal sales within our coverage universe. Besides, PTBA also promises potential

growth, driven by its volume growth.

• In the long run, ADRO will also be attractive if its downstream projects such as 2x1000 Mw Batang

powerplant and 2x300 Mw mine-mouth powerplant are completed. ADRO also promises highers

potential earning growth on small number basis.

• ITMG has its own reputation as a high dividend payer. With lower capex, we believe ITMG will

maintain its dividend on 80-90% of their annual earnings, implied to 7-9% dividend yield.

• UNTR will face a difficult period over the next few years as many coal producers will maintain their

production on the low strip ratio level. Besides, lower capex will hit the heavy equipment sales on the

mining sectors.

• We do not prefer on HRUM due to its lack coal reserves and no significant cost efficiency initiatives.

• IDR depreciation will benefit UNTR and PTBA as they state their financial statements in IDR. UNTR

and PTBA are the USD earners with around half IDR cash cost.

Stock RatingTarget

PricePE-15 PBV-15 ROE-15

Dividend

Yield

EPS Growth

- 15

PTBA NEUTRAL 11.600 13.5x 1.2x 20.4% 3.6% -2.2%

ADRO NEUTRAL 1.100 13.0x 1.0x 6.3% 1.5% 28.1%

UNTR NEUTRAL 19.750 13.5x 1.9x 13.2% 3.0% -6.8%

ITMG NEUTRAL 18.200 9.6x 1.8x 18.8% 9.0% -16.6%

HRUM SELL 1.000 15.0x 0.7x 6.2% 5.5% -16.2%

Head Office :Indonesia Stock Exchange Tower II Suite 1705

Jl. Jend Sudirman kav. 52-53, Jakarta Selatan - 12190Telp: (021) 515 3055, Faks: (021) 515 3061

Email: [email protected] Website: www.pans.co.id

Online Trading: www.post.co.id

PT PANIN SEKURITAS Tbk

Branch Offices :Kelapa Gading - North Jakarta : (021) 2938 5767Pluit Village - North Jakarta : (021) 6667 0268Pluit Sakti - North Jakarta : (021) 666 00302 Pondok Indah - South Jakarta : (021) 722 4420Puri Kencana - West Jakarta : (021) 582 3868Tanah Abang - Central Jakarta : (021) 2357 1177Tangerang - Alam Sutera : (021) 2921 1518

Denpasar-Bali : (0361) 7152 999Medan-Dipenogoro : (061) 451 9267Medan-Iskandar Muda : (061) 453 0123Medan-Pemuda : (061) 457 6996Padang : (0751) 811 322Palembang : (0711) 370 235Pekanbaru : (0761) 27827Pontianak : (0561) 748 888Semarang : (024) 850 2300Solo : (0271) 727888Surabaya : (031) 561 3388

ofwww. pans.co.id www. post.co.id 25 31

Bandung – Batununggal : (022) 87301954Bandung – Sunda : (022) 732 1434Bandung – Dago : (022) 426 8127, 426 8129Batam : (0778) 459 222Bukit Tinggi : (0752) 33998

Related Documents