Panel on Accounting for Income Taxes: Rate-regulated Utilities FAS 71 Exceptions to FAS 109 David J. Yankee Deloitte Tax LLP April 23, 2007

Panel on Accounting for Income Taxes: Rate-regulated Utilities FAS 71 Exceptions to FAS 109 David J. Yankee Deloitte Tax LLP April 23, 2007.

Dec 23, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Panel on Accounting for Income Taxes:Rate-regulated Utilities

FAS 71 Exceptionsto FAS 109

David J. YankeeDeloitte Tax LLPApril 23, 2007

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Caveats

• The views expressed do not necessarily represent Deloitte & Touche LLP or Deloitte Tax LLP policy.

• The outcome of any specific matter depends upon the specific facts and circumstances in which the matter arises.

• The views expressed cannot be relied upon as accounting or tax advice.

2

3Copyright © 2007 Deloitte Development LLC. All rights reserved.

Agenda*

•Effective Tax Rate Items

•Income Taxes and Ratemaking

•Normalization v. Flow-through Accounting

•Changes in Tax Rates – Excess Deferred Income Taxes

•Allowance for Funds Used During Construction

•Investment Tax Credit

*Normalization requirements to be addressed in a separate session

4Copyright © 2007 Deloitte Development LLC. All rights reserved.

Effective Tax Rate Items

• Permanent differences

• Credits

• Temporary differences with:

– Flow-through accounting

– Historical tax rates

– After-tax accounting

5Copyright © 2007 Deloitte Development LLC. All rights reserved.

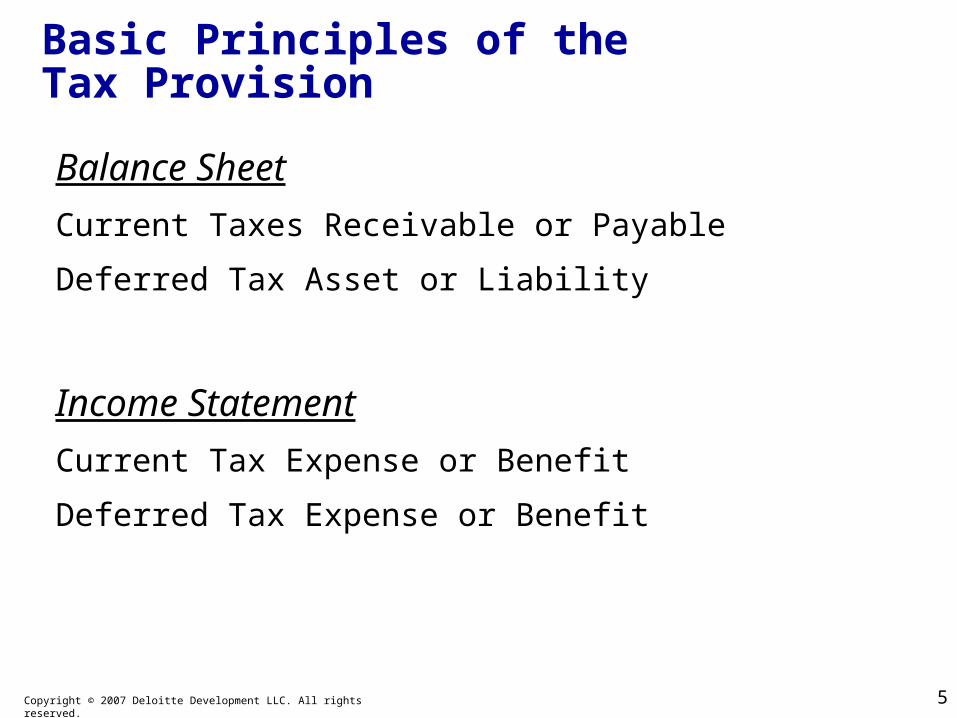

Basic Principles of theTax Provision

Balance Sheet

Current Taxes Receivable or Payable

Deferred Tax Asset or Liability

Income Statement

Current Tax Expense or Benefit

Deferred Tax Expense or Benefit

6Copyright © 2007 Deloitte Development LLC. All rights reserved.

Basic Principles of theTax Provision – Regulated Utilities

Balance SheetCurrent Taxes Receivable or Payable

Deferred Tax Asset or Liability

Regulatory Assets Related to Income Taxes

Regulatory Liabilities Related to Income Taxes

Deferred Investment Tax Credits

Income StatementCurrent Tax Expense or Benefit

Deferred Tax Expense

Amortization of Investment Tax Credits

7Copyright © 2007 Deloitte Development LLC. All rights reserved.

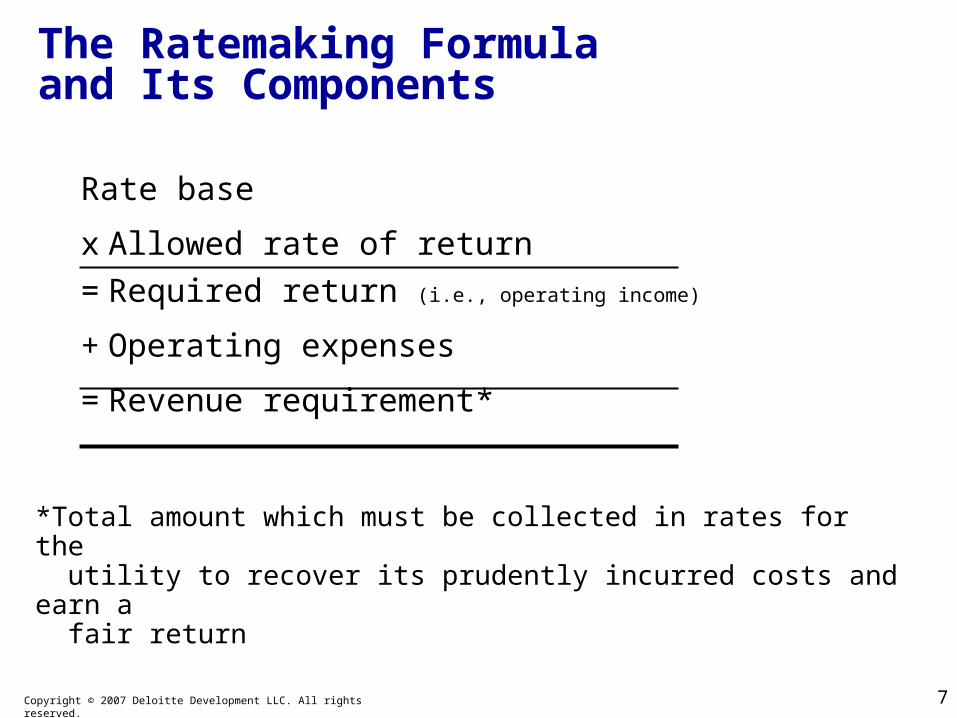

The Ratemaking Formula and Its Components

Rate base

x Allowed rate of return

=Required return (i.e., operating income)

+Operating expenses

=Revenue requirement*

*Total amount which must be collected in rates for the utility to recover its prudently incurred costs and earn a fair return

8Copyright © 2007 Deloitte Development LLC. All rights reserved.

Tax-on-tax Gross-up Formula –Federal Items and Allowed Equity Return

• Required revenue is the total amount which must be collected from customers in rates in order for the utility to recover its costs, including the allowed equity return.

• Allowed equity return must be grossed-up for taxes:

Equity Return Gross-up for Equity 1 – Tax Rate* = Return and Taxes

*Based on combined statutory federal/state tax rates

• Example:

Allowed Equity Return = $3,000,000

$3,000,000 / (1 – 40%) = $5,000,000

Note – Adjustments to income tax expense (e.g., flow-through, flow-backs, ITC amortization) must also beconsidered.

9Copyright © 2007 Deloitte Development LLC. All rights reserved.

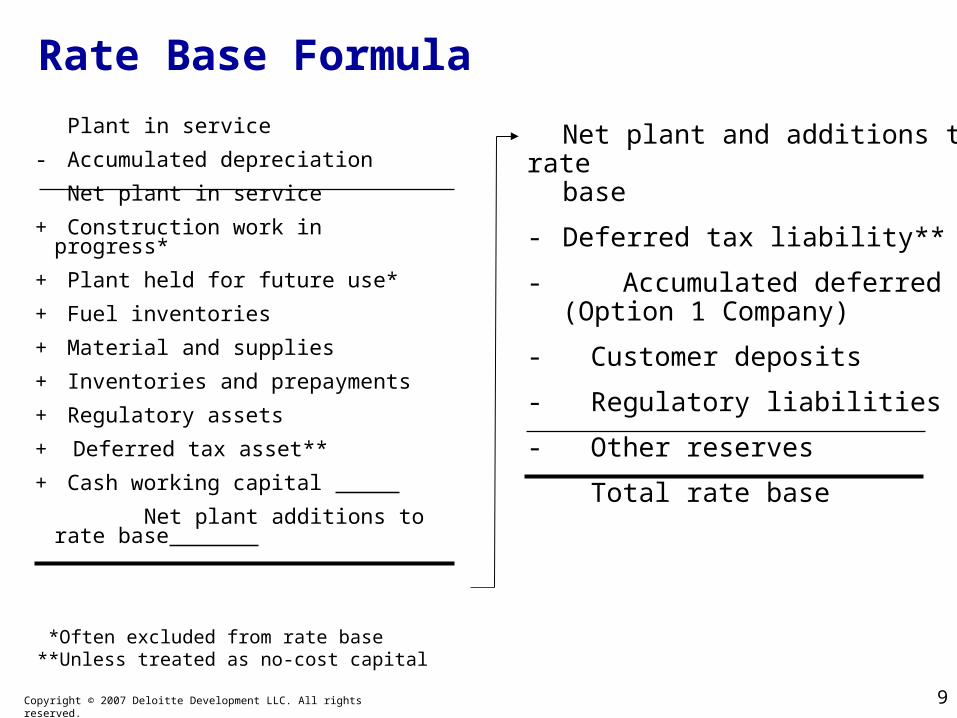

Plant in service

- Accumulated depreciation

Net plant in service

+ Construction work in progress*

+ Plant held for future use*

+ Fuel inventories

+ Material and supplies

+ Inventories and prepayments

+ Regulatory assets

+ Deferred tax asset**

+ Cash working capital

Net plant additions to rate base

Net plant and additions to rate base

- Deferred tax liability**

- Accumulated deferred ITC (Option 1 Company)

- Customer deposits

- Regulatory liabilities

- Other reserves

Total rate base

Rate Base Formula

*Often excluded from rate base**Unless treated as no-cost capital

10Copyright © 2007 Deloitte Development LLC. All rights reserved.

Rate Base Components –Income Taxes

• Accumulated Deferred Federal Income Taxes – represents the deferred federal income taxes resulting from tax normalization and is considered a source of interest-free funds (i.e., cost-free capital) provided by the U.S. Treasury to the utility

– ADFIT balances deducted from rate base, or

– ADFIT balances included in the capital structure of the utility at zero cost when computing the rate of return

11Copyright © 2007 Deloitte Development LLC. All rights reserved.

Rate Base Components –Income Taxes

• Accumulated Deferred Investment Tax Credit

– The accounting and ratemaking treatment for ITC is largely dictated by former Internal Revenue Code (IRC) Sections 46(f)(1) and 46(f)(2)

– The IRC permits sharing of ITC benefits between utility investors and customers either

Option 1 - As ADITC rate base reduction, with no amortization through operating expenses (i.e., income tax expense), or

Option 2 - Through amortization of ITC “above-the-line” as a reduction in operating expenses (i.e., income tax expense). No rate base reduction. Option 2 deferred ITC should earn at least the overall cost of capital if included in the capital structure

12Copyright © 2007 Deloitte Development LLC. All rights reserved.

Normalization v. Flow-through

• Normalization – the reflection in ratemaking of a tax benefit commensurate with the level of depreciation expense being recovered from ratepayers

– Accrual-basis accounting for interperiod tax allocation (i.e., deferred taxes)

Current and deferred provisions and liabilities

• Flow-through – the reflection in ratemaking of a tax benefit commensurate with the level of depreciation expense being deducted on the tax return

– Cash-basis accounting for interperiod tax allocation

Current tax provision/payable only

– Exception to comprehensive interperiod tax allocation

13Copyright © 2007 Deloitte Development LLC. All rights reserved.

Normalization v. Flow-throughCharacteristics and Impacts

• Over the life of an asset, the amount of income tax expense and the amount of rate recovery are the same

• The methods differ on an annual basis as to the amount of tax expense included in rates and, thus, the amount recognized in the income statement

• Sharing of tax benefits

– Between utilities and ratepayers

– Between generations of ratepayers

• Regulatory promise for future rate recovery

14Copyright © 2007 Deloitte Development LLC. All rights reserved.

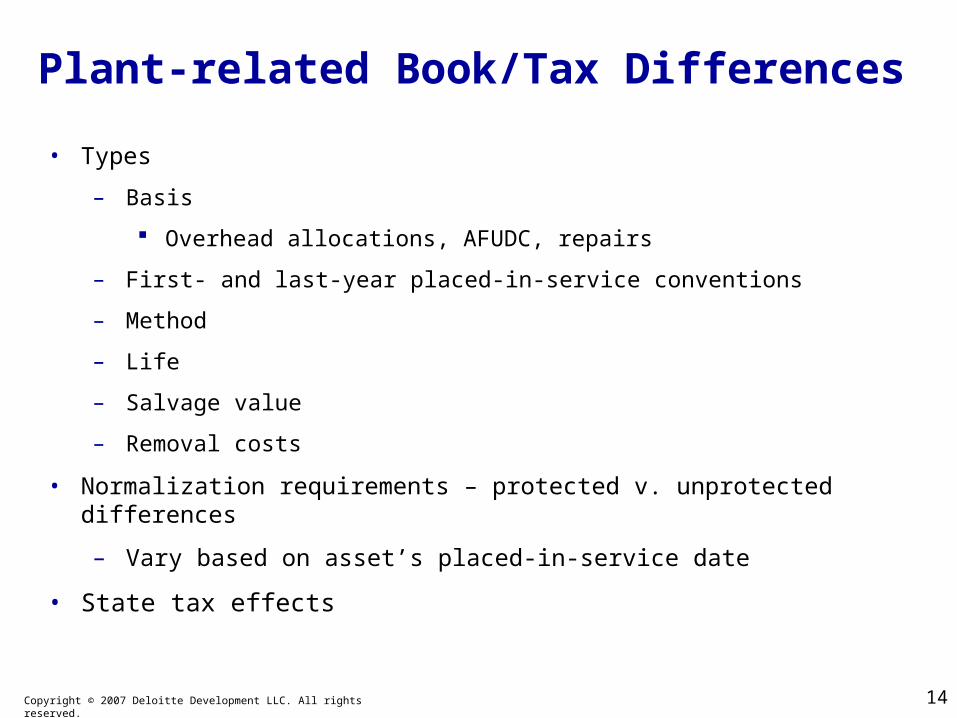

Plant-related Book/Tax Differences

• Types

– Basis

Overhead allocations, AFUDC, repairs

– First- and last-year placed-in-service conventions

– Method

– Life

– Salvage value

– Removal costs

• Normalization requirements – protected v. unprotected differences

– Vary based on asset’s placed-in-service date

• State tax effects

15Copyright © 2007 Deloitte Development LLC. All rights reserved.

Flow-through ItemsRegulatory Asset Calculation

Temporary difference flowed through

x Enacted tax rate

x Gross-up (tax-on-tax) factor

Regulatory asset

Dr. Regulatory Asset

Cr. Deferred Tax Liability

16Copyright © 2007 Deloitte Development LLC. All rights reserved.

Prior Flow-through

• Book/tax differences for which deferred taxes were not originally provided (or recovered in rates)

– Interest-free government loan from government to taxpayer is in the hands of ratepayers until it is repaid (i.e., when the future liability becomes due)

• Scope and extent varies on a company-by-company, commission-by-commission basis

• Change from state to FERC regulation

• Resulted in lower revenue requirement and lower effective tax rate as favorable book/tax differences originated

• Results in higher revenue requirement and higher effective tax rate as book/tax differences reverse

• Prior to adoption of SFAS No. 109 – resulted in understated deferred tax liabilities

• Adoption of SFAS No. 109 – recognition of deferred tax liabilities and regulatory asset as well as tax-on-tax gross-up

17Copyright © 2007 Deloitte Development LLC. All rights reserved.

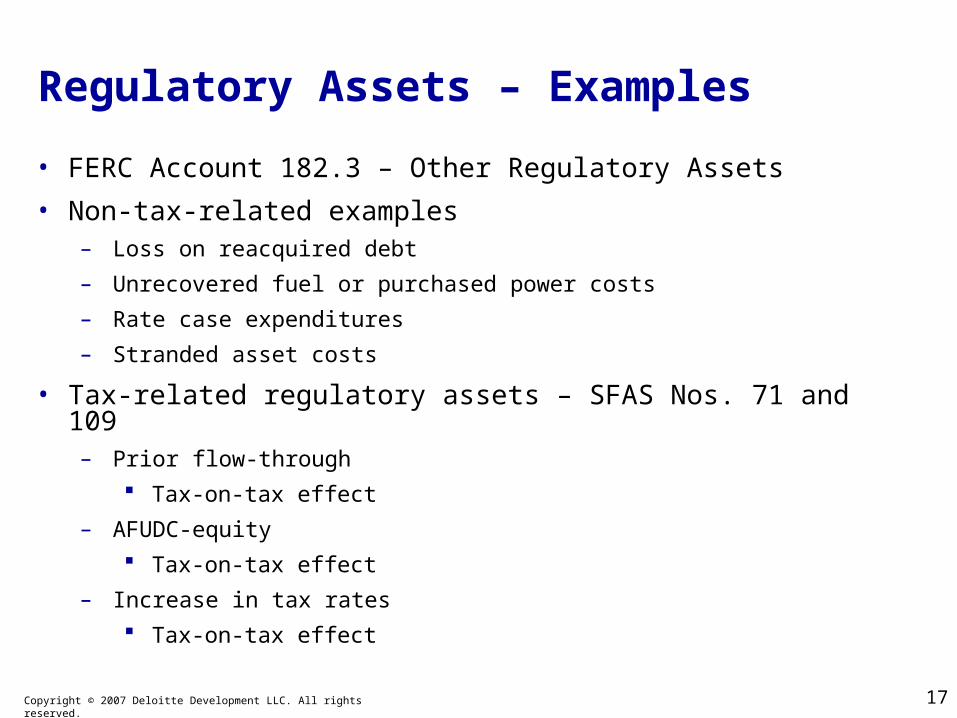

Regulatory Assets – Examples

• FERC Account 182.3 – Other Regulatory Assets

• Non-tax-related examples– Loss on reacquired debt

– Unrecovered fuel or purchased power costs

– Rate case expenditures

– Stranded asset costs

• Tax-related regulatory assets – SFAS Nos. 71 and 109– Prior flow-through

Tax-on-tax effect

– AFUDC-equity Tax-on-tax effect

– Increase in tax rates Tax-on-tax effect

18Copyright © 2007 Deloitte Development LLC. All rights reserved.

Flow-back of Prior Flow-through

• Basis differences reverse over the book lives of an asset

• Measure the reversing (temporary) basis difference as the difference between:

– Book depreciation (i.e., book basis, book life, book method)

– Tax straight-line depreciation (i.e., tax basis, book life, book method)

• Remaining book/tax depreciation difference is normalized:

– Tax straight-line depreciation

– Tax depreciation (i.e., tax basis, tax life, tax method)

19Copyright © 2007 Deloitte Development LLC. All rights reserved.

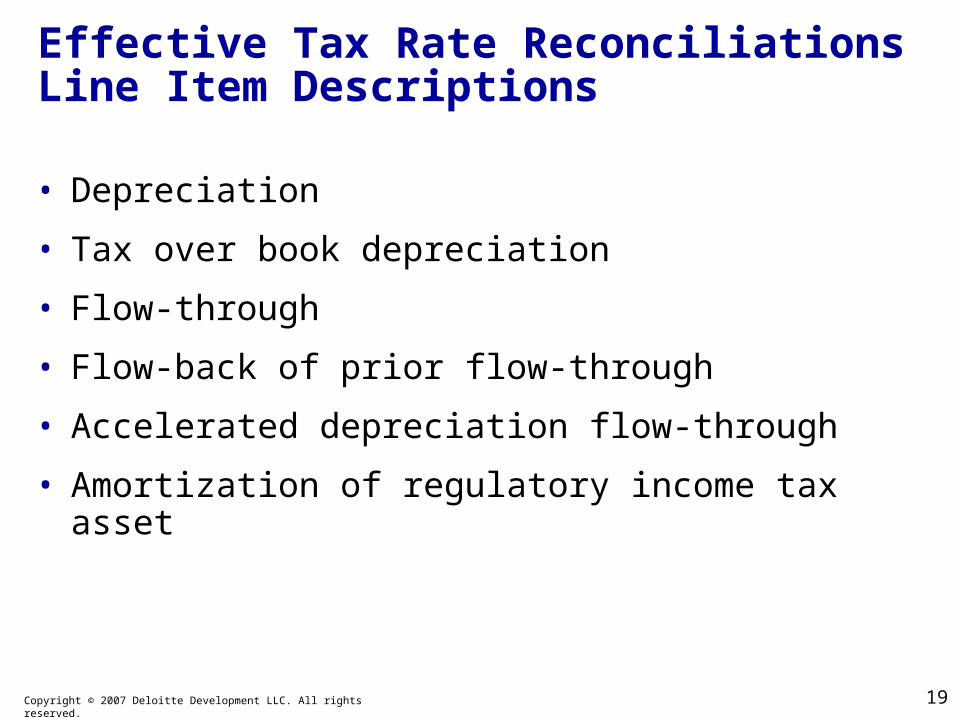

Effective Tax Rate ReconciliationsLine Item Descriptions

• Depreciation

• Tax over book depreciation

• Flow-through

• Flow-back of prior flow-through

• Accelerated depreciation flow-through

• Amortization of regulatory income tax asset

20Copyright © 2007 Deloitte Development LLC. All rights reserved.

Flow-through Effective Tax Rate – Case Study #1

Assumptions

Tax-related regulatory asset = $1,000

Tax rate = 40%

Gross-up factor = 1.67 (rounded)

What is the amount of temporary differences for which deferred taxes have not been recovered through rates?

Divided by enacted tax rate ÷ 40%

Plant-related book/tax difference $1,500

Regulatory asset $1,000

Divided by gross-up factor ÷ 1.67

Plant-related deferred tax liability 600

21Copyright © 2007 Deloitte Development LLC. All rights reserved.

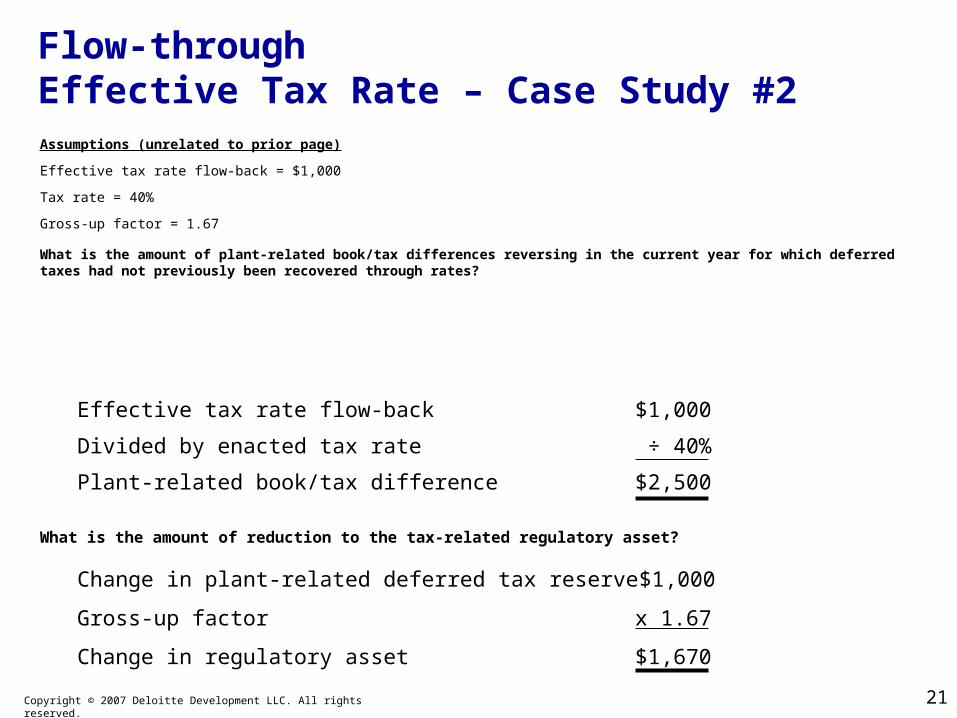

Flow-through Effective Tax Rate – Case Study #2Assumptions (unrelated to prior page)

Effective tax rate flow-back = $1,000

Tax rate = 40%

Gross-up factor = 1.67

What is the amount of plant-related book/tax differences reversing in the current year for which deferred taxes had not previously been recovered through rates?

Effective tax rate flow-back $1,000

Divided by enacted tax rate ÷ 40%

Plant-related book/tax difference $2,500

Change in plant-related deferred tax reserve $1,000

Gross-up factor x 1.67

Change in regulatory asset $1,670

What is the amount of reduction to the tax-related regulatory asset?

22Copyright © 2007 Deloitte Development LLC. All rights reserved.

Tax Rate Changes Overview

• SFAS No. 109 requires use of enacted tax rates

• Other factors

– Normalization requirements

– Regulators

• Federal rate changes

• State rate changes

23Copyright © 2007 Deloitte Development LLC. All rights reserved.

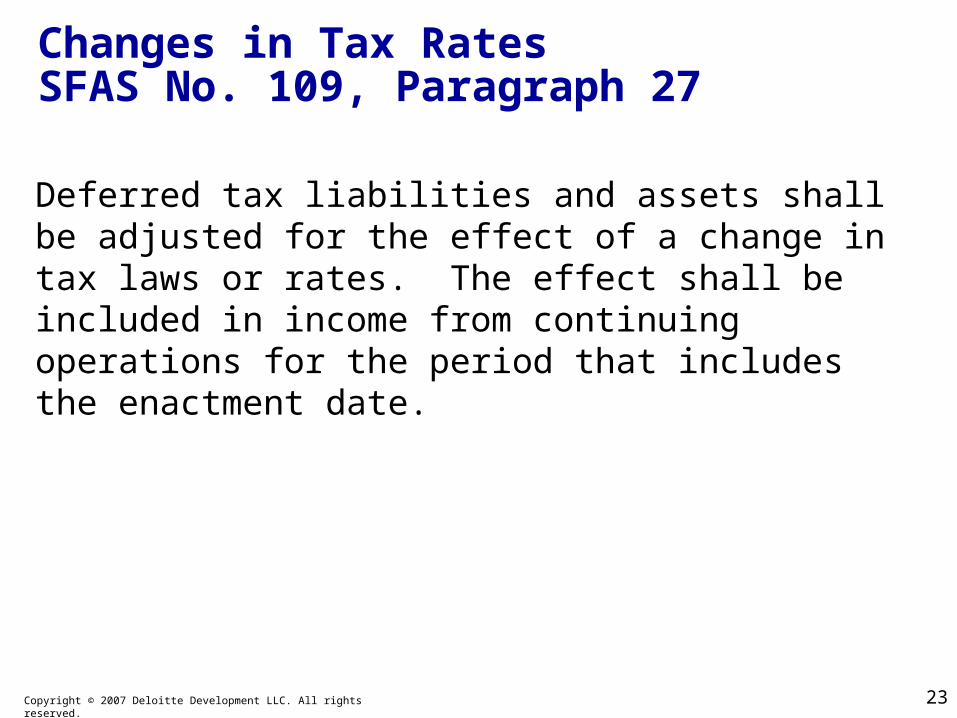

Changes in Tax RatesSFAS No. 109, Paragraph 27

Deferred tax liabilities and assets shall be adjusted for the effect of a change in tax laws or rates. The effect shall be included in income from continuing operations for the period that includes the enactment date.

24Copyright © 2007 Deloitte Development LLC. All rights reserved.

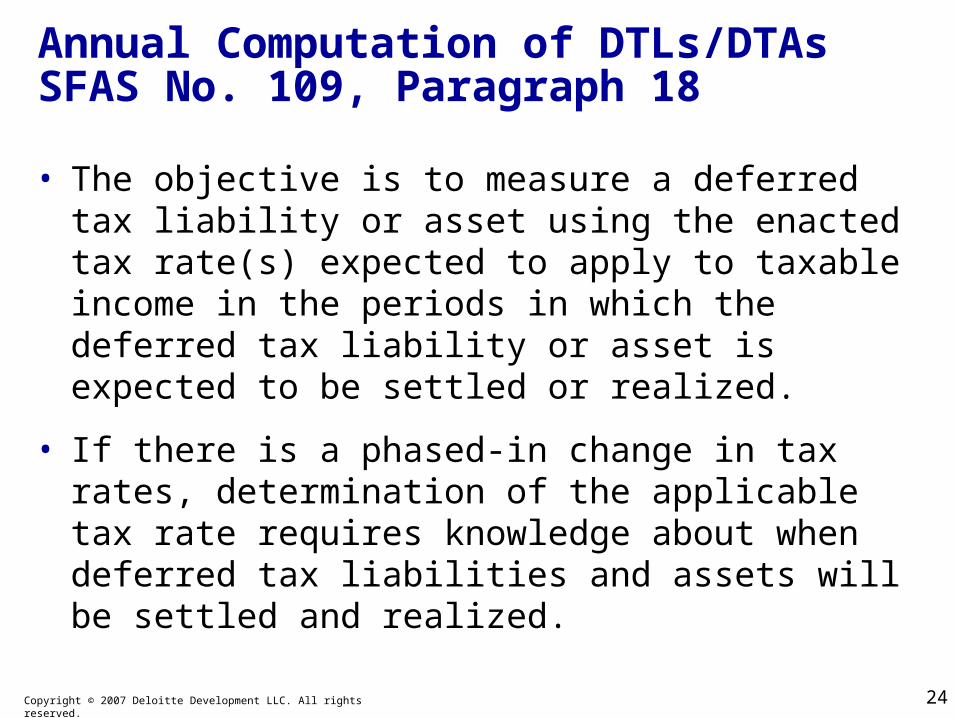

Annual Computation of DTLs/DTAsSFAS No. 109, Paragraph 18

• The objective is to measure a deferred tax liability or asset using the enacted tax rate(s) expected to apply to taxable income in the periods in which the deferred tax liability or asset is expected to be settled or realized.

• If there is a phased-in change in tax rates, determination of the applicable tax rate requires knowledge about when deferred tax liabilities and assets will be settled and realized.

25Copyright © 2007 Deloitte Development LLC. All rights reserved.

Excess Deferred Federal Income Taxes (EDFIT) - Overview• Deferred taxes provided at tax rates in excess of the current statutory

tax rate– Pre-1979 48%– 1979-1986 46%– 1987 40%– 1987-93 34%– Post-1993 35%

• Reduction in rates charged to ratepayers (as a reduction of ratemaking income tax expense) as the book/tax depreciation differences giving rise to the deferred tax liability reverse– Average rate assumption method - Act Section 203(e) of TRA of 1986– Reverse South Georgia method - Rev. Proc. 88-12

• Impact of turnaround on effective tax rate (decrease)

• Adoption of SFAS No. 109– Regulatory liability

26Copyright © 2007 Deloitte Development LLC. All rights reserved.

Reduction in Tax RatesRegulatory Liability Calculation – Part I

Previously recorded DTL

<Temporary differences at new tax rate>

“Excess” deferred taxes

27Copyright © 2007 Deloitte Development LLC. All rights reserved.

Reduction in Tax RatesRegulatory Liability Calculation – Part II

Excess deferred taxes

x Gross-up (tax-on-tax) factor

Regulatory liability

Dr. Deferred Tax Liability (Reduction due to Rate Reduction)

Dr. Deferred Tax Asset (on Regulatory Liability)

Cr. Regulatory Liability – Excess Deferred Taxes

28Copyright © 2007 Deloitte Development LLC. All rights reserved.

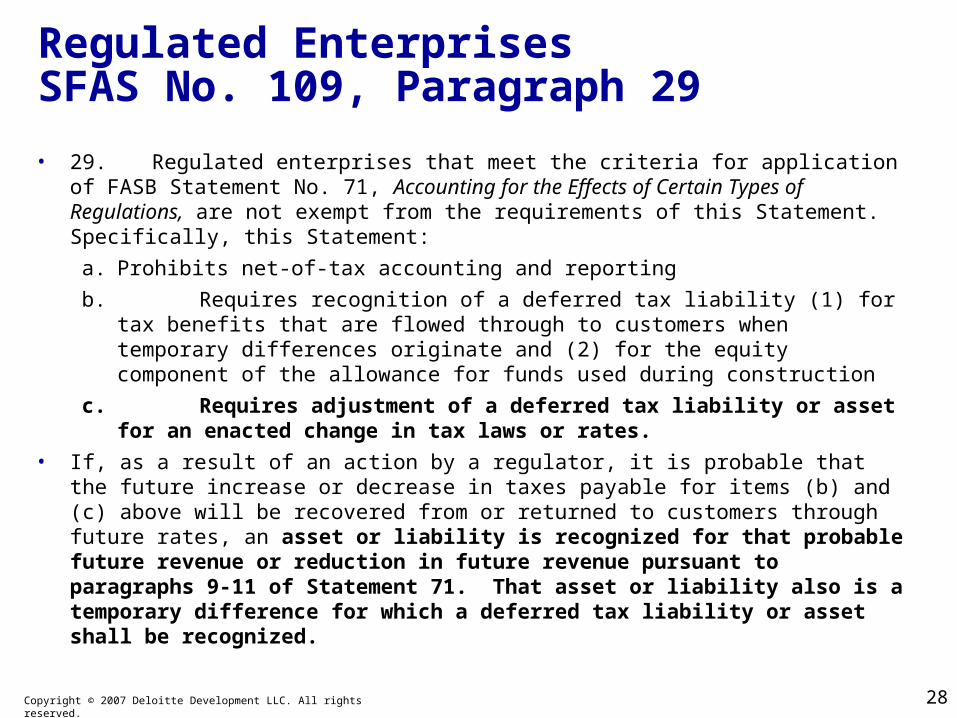

Regulated EnterprisesSFAS No. 109, Paragraph 29

• 29. Regulated enterprises that meet the criteria for application of FASB Statement No. 71, Accounting for the Effects of Certain Types of Regulations, are not exempt from the requirements of this Statement. Specifically, this Statement:

a. Prohibits net-of-tax accounting and reporting

b. Requires recognition of a deferred tax liability (1) for tax benefits that are flowed through to customers when temporary differences originate and (2) for the equity component of the allowance for funds used during construction

c. Requires adjustment of a deferred tax liability or asset for an enacted change in tax laws or rates.

• If, as a result of an action by a regulator, it is probable that the future increase or decrease in taxes payable for items (b) and (c) above will be recovered from or returned to customers through future rates, an asset or liability is recognized for that probable future revenue or reduction in future revenue pursuant to paragraphs 9-11 of Statement 71. That asset or liability also is a temporary difference for which a deferred tax liability or asset shall be recognized.

29Copyright © 2007 Deloitte Development LLC. All rights reserved.

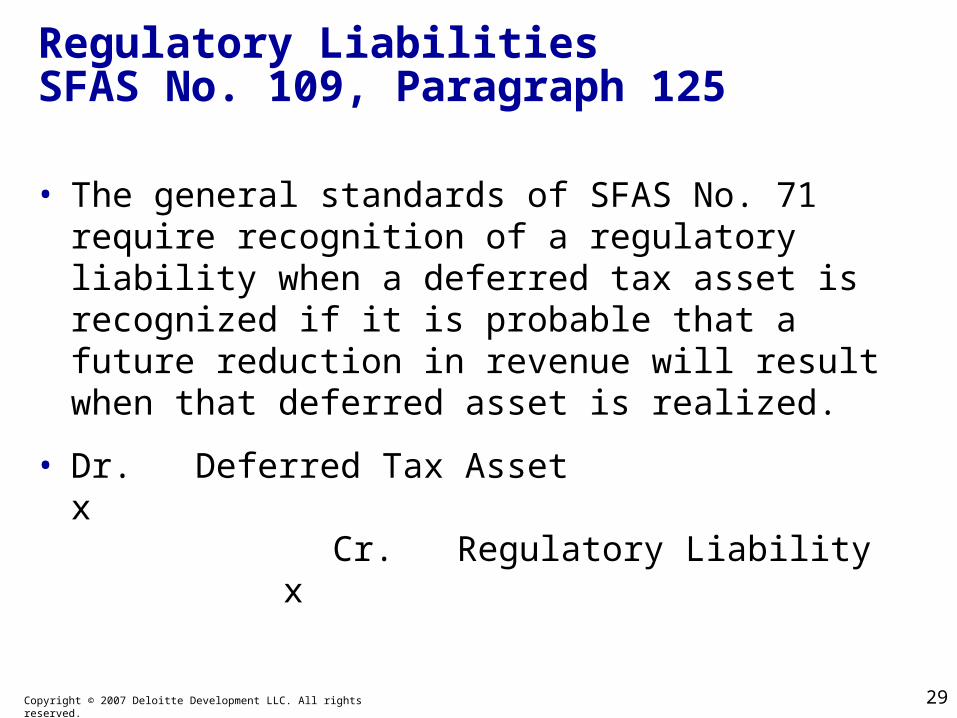

Regulatory LiabilitiesSFAS No. 109, Paragraph 125

• The general standards of SFAS No. 71 require recognition of a regulatory liability when a deferred tax asset is recognized if it is probable that a future reduction in revenue will result when that deferred asset is realized.

• Dr. Deferred Tax Asset x Cr. Regulatory Liability x

30Copyright © 2007 Deloitte Development LLC. All rights reserved.

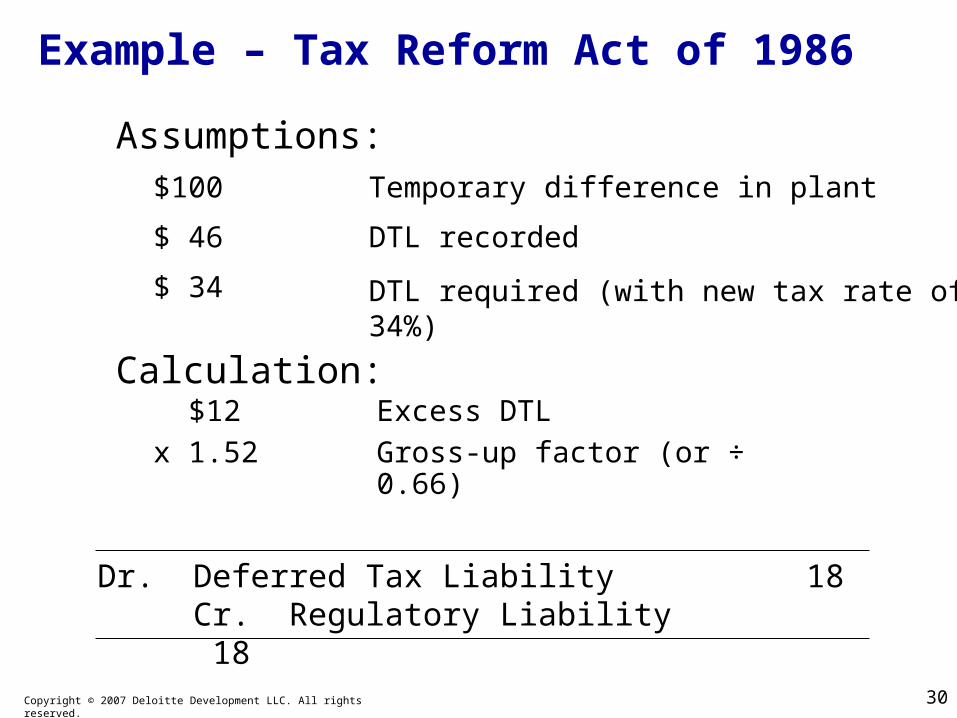

Example – Tax Reform Act of 1986

Assumptions:

Calculation:

$100

$ 46

$ 34

Temporary difference in plant

DTL recorded

DTL required (with new tax rate of34%)

$12 Excess DTLx 1.52 Gross-up factor (or ÷ 0.66)

Dr. Deferred Tax Liability 18 Cr. Regulatory Liability 18

31Copyright © 2007 Deloitte Development LLC. All rights reserved.

Example – Tax Reform Act of 1986

28

46

$28*

Net $ 82

x 34%

18

Assets $100

Reg. Liability (18)

Temporary DifferencesDTL

*Deferred tax liability of $34 for $100 depreciation temporary difference less deferred tax benefit of $6 for settling $18 regulatory liability with ratepayers.

32Copyright © 2007 Deloitte Development LLC. All rights reserved.

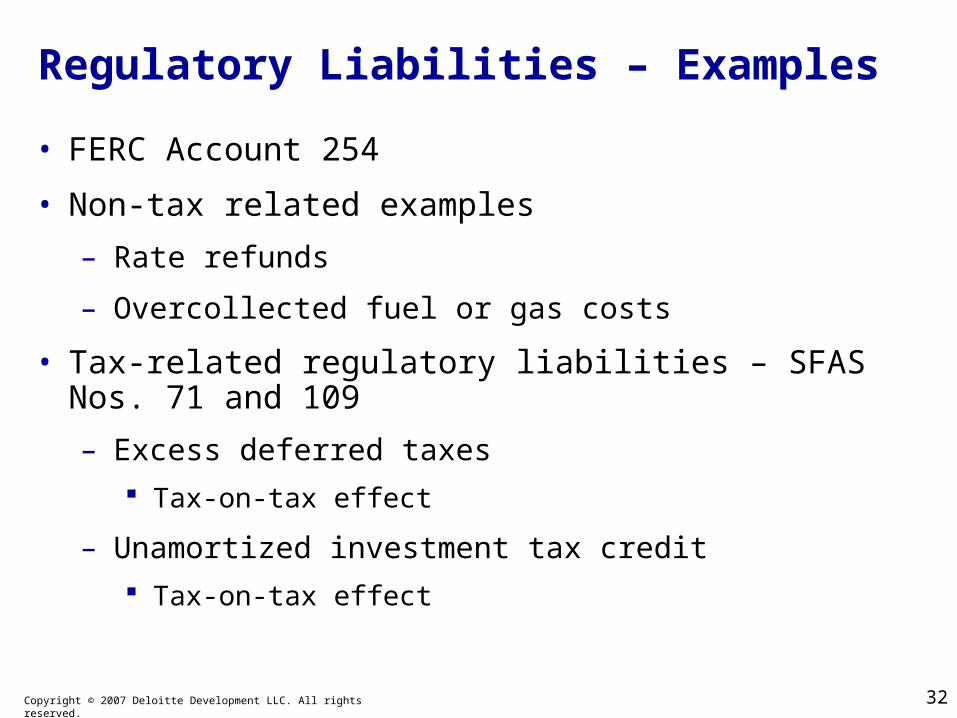

Regulatory Liabilities – Examples

• FERC Account 254

• Non-tax related examples

– Rate refunds

– Overcollected fuel or gas costs

• Tax-related regulatory liabilities – SFAS Nos. 71 and 109

– Excess deferred taxes Tax-on-tax effect

– Unamortized investment tax credit Tax-on-tax effect

33Copyright © 2007 Deloitte Development LLC. All rights reserved.

Changes in State Tax Rates

• Increases in tax rates for regulated utilities with net deferred tax liabilities may result in regulatory assets.

• Decreases in tax rates for regulated utilities with net deferred tax liabilities may result in regulatory liabilities.

• Changes in apportionment factors

– Statutory formula

– Facts

• Impact on tax-on-tax gross-up factors

– Federal items

– State items

34Copyright © 2007 Deloitte Development LLC. All rights reserved.

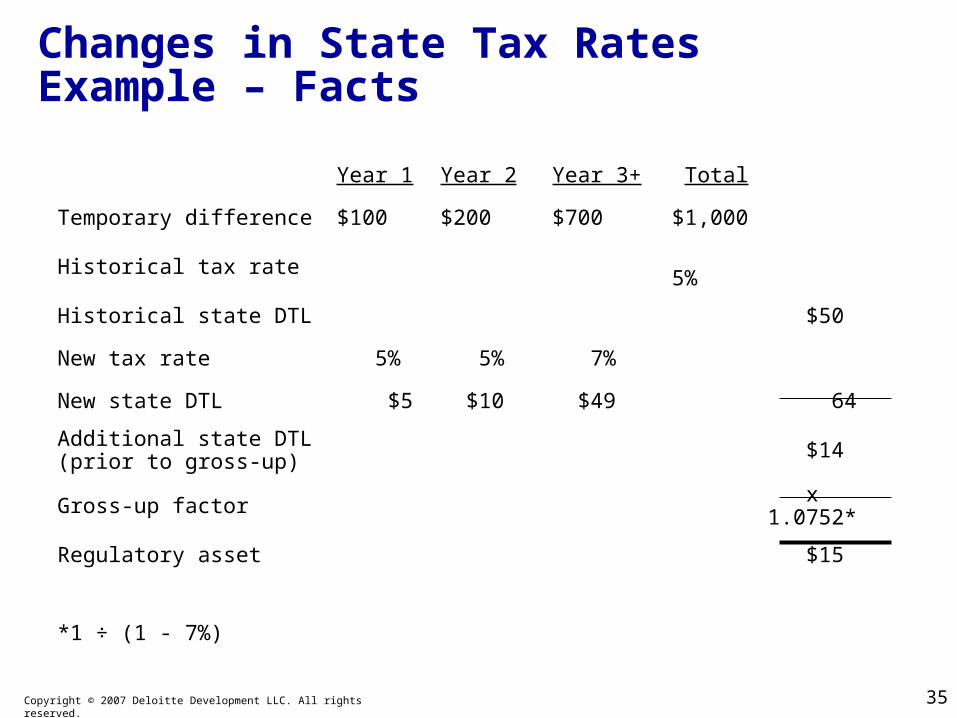

Changes in State Tax RatesExample – Facts

• Company has 100 percent apportionment in State A.

• During Year 1, State A raises its tax rate from 5 percent to 7 percent.

• The rate increase is effective at the beginning of Year 3.

• Company has $1,000 of taxable temporary differences at the end of the Year 1 quarter during which the tax law is amended.

• Company expects $100 of these temporary differences to reverse in Year 1 and $200 to reverse in Year 2.

• The federal income tax note is 35 percent.

35Copyright © 2007 Deloitte Development LLC. All rights reserved.

Changes in State Tax RatesExample – Facts

Year 1 Year 2 Year 3+ Total

Temporary difference $100 $200 $700 $1,000

Historical tax rate 5%

Historical state DTL $50

New tax rate 5% 5% 7%

New state DTL $5 $10 $49 64

Additional state DTL (prior to gross-up) $14

Gross-up factor x 1.0752*

Regulatory asset $15

*1 ÷ (1 - 7%)

36Copyright © 2007 Deloitte Development LLC. All rights reserved.

Change in State Tax RatesExample – Scenario #1

It is uncertain whether the PUC will allow Company to recover the shortfall in its state DTL in its next rate case.

Dr. Deferred State Tax Expense 14.00

Cr. DTL – State 14.00

Dr. DTA – Federal 4.90

Cr. Deferred Tax Benefit 4.90

Immediate impact on the income statement = $ 9.10

37Copyright © 2007 Deloitte Development LLC. All rights reserved.

Change in State Tax RatesExample – Scenario #2

The PUC has indicated that it will allow Company to recover the shortfall in its state DTL in its next rate case. (Assume that the entries on the previous page have not been recorded.)

Dr. Regulatory Asset 15

Cr. DTL – State 15

Dr. DTA – Federal (on State DTL) 5.25

Cr. DTL – Federal (on Reg. Asset)5.25

Immediate impact on the income statement = $0

38Copyright © 2007 Deloitte Development LLC. All rights reserved.

Allowance for Funds Used During Construction (“AFUDC”)

• When utilities are not allowed to recover in current rates a return necessary to finance construction projects during the construction period, they will generally be allowed to capitalize the financing costs for future recovery from ratepayers.

– AFUDC represents capitalized interest and equity costs, which will ultimately be included in rate base as a component of plant in service, thereby earning a return and being recovered through depreciation allowances.

39Copyright © 2007 Deloitte Development LLC. All rights reserved.

Allowance for Funds Used During Construction

• Employed when construction work in progress is not included in rate base

• Non-cash income item representing composite interest cost of debt and a return on equity funds used to finance construction. The allowance is capitalized in the property accounts and included in GAAP income.

• Results in additional GAAP depreciable basis in plant that is not recognized for tax purposes

• AFUDC–Equity represents an estimate of the after-tax equity costs associated with construction.

• Journal Entry

Dr. Plant (CWIP) 100Cr. Interest expense (debt portion) 60Cr. Other income (equity portion) 40

40Copyright © 2007 Deloitte Development LLC. All rights reserved.

Allowance for Funds Used During Construction

• SFAS No. 109 prohibits net-of-tax and after-tax accounting

• SFAS No. 109 requires recognition of a deferred tax liability for the equity component recorded in plant

• AFUDC-Equity results in a decrease to the effective rate in the year recognized (if recorded on an after-tax basis)

• AFUDC-Equity recorded on an after-tax basis results in an increase to the effective rate in the years that the asset is depreciated (i.e., reversal of the basis difference)

41Copyright © 2007 Deloitte Development LLC. All rights reserved.

AFUDC-EquityRegulatory Asset Calculation

AFUDC-Equity capitalized*

x Enacted tax rate

x Gross-up (tax-on-tax) factor

Regulatory asset

*In CWIP or plant in service

Dr. Regulatory Asset

Cr. Deferred Tax Liability

42Copyright © 2007 Deloitte Development LLC. All rights reserved.

AFUDC-EquityExample - Facts

Facts:• Pre-tax income from operations is $1,000,000• Tax rate is 40%• Assume the only potential effective tax rate reconciling item is AFUDC-Equity• $1,000,000 construction project

– Started in January 2006– Placed into service on January 1, 2007– Useful life is 20 years– Assume no difference between book and tax depreciation method and

lives.• AFUDC-Equity:

– On a after-tax basis, AFUDC-Equity is $75,000 (7.5% after-tax rate)– On a pre-tax basis, AFUDC-Equity would be $115,385 (11.5385%)

43Copyright © 2007 Deloitte Development LLC. All rights reserved.

AFUDC-Equity – Example Income Statement

Income Statement

Pre-tax Income from Operations $1,000,000

Income Taxes (35%) (350,000)

Income from Operations $ 650,000

Other Income – AFUDC-Equity 75,000

Tax on AFUDC-Equity 0

Book Income $ 725,000

*Net of tax of $40,385 ($115,385 - $40,385 = $75,000)

*

44Copyright © 2007 Deloitte Development LLC. All rights reserved.

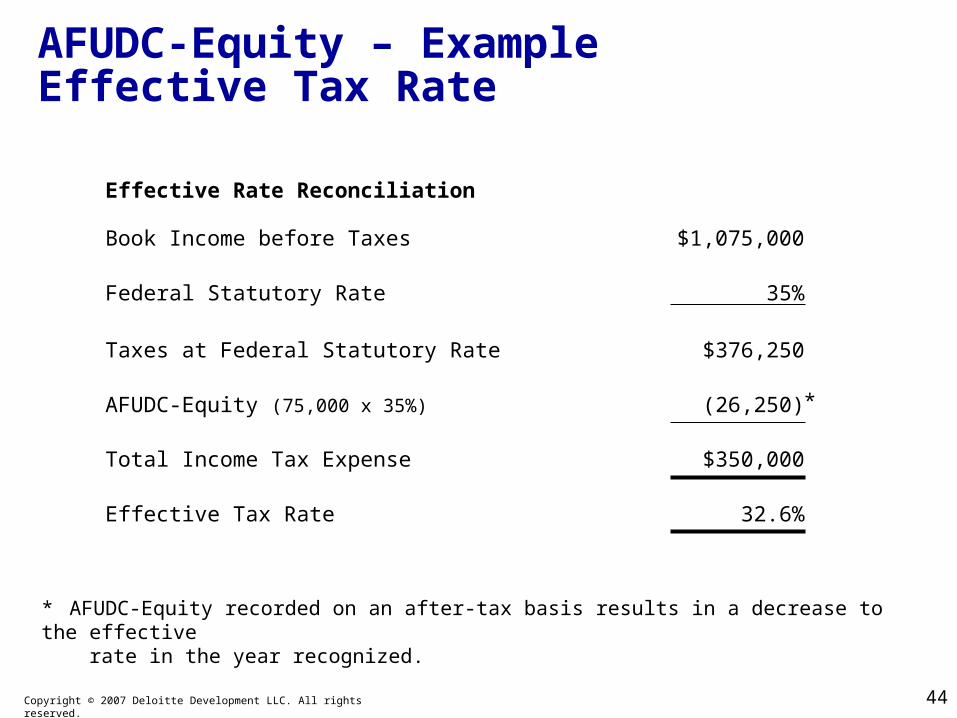

AFUDC-Equity – Example Effective Tax Rate

Effective Rate Reconciliation

Book Income before Taxes $1,075,000

Federal Statutory Rate 35%

Taxes at Federal Statutory Rate $376,250

AFUDC-Equity (75,000 x 35%) (26,250)

Total Income Tax Expense $350,000

Effective Tax Rate 32.6%

* AFUDC-Equity recorded on an after-tax basis results in a decrease to the effective rate in the year recognized.

*

45Copyright © 2007 Deloitte Development LLC. All rights reserved.

AFUDC-Equity – Example Subsequent Year

• AFUDC-Equity recorded on an after-tax basis results in an increase to the effective rate in the years that the asset is depreciated (i.e., reversal of the basis difference).

46Copyright © 2007 Deloitte Development LLC. All rights reserved.

Investment Tax Credit (ITC) – Federal

• Credit for investment in qualified property for the tax year in which the property was placed in service

– Enacted, repealed, re-enacted, etc., in the 1960s-1980s

– Generally tangible personal property and certain real property (excluding buildings or their structural components)

– In the later years, taxpayer could elect to receive a reduced credit to avoid a reduction in depreciable basis

– Credit was subject to full or partial recapture if the property was prematurely disposed

• Repealed by the Tax Reform Act of 1986

– General transition rules applied for property placed in service through December 31, 1990

Mandatory reduction in depreciable basis

• Alternative energy investment tax credits

47Copyright © 2007 Deloitte Development LLC. All rights reserved.

SFAS No. 109Investment Tax Credit 5. This Statement does not address:

a. The basic methods of accounting for the U.S. federal investment tax credit (ITC) and for foreign, state, and local investment tax credits or grants. (The deferral and flow-through methods as set forth in APB Opinions No. 2 and No. 4, Accounting for the "Investment Credit," continue to be acceptable methods to account for the U.S. federal ITC.)

116. The requirements for accounting for investment tax credits are contained in Opinions 2 and 4. In Opinion 2, the Accounting Principles Board (APB) concluded that:

a. The investment tax credit reduces the cost of the related asset, and for that reason, it should be deferred and amortized over the productive life of the related asset.

b. Display of the deferral in the statement of financial position as a reduction of the cost of the asset ordinarily is preferable.

c. Display of the deferral as deferred income is also permitted provided that the investment tax credit is accounted for as a reduction of the cost of the asset, that is, amortized over the productive life of the asset.

In Opinion 4, the APB concluded that:

(1) The essential nature of the investment tax credit is that it reduces the cost of the related asset, and the method of accounting for it in Opinion 2 is preferable.

(2) The flow-through method to account for the investment tax credit is also acceptable.

48Copyright © 2007 Deloitte Development LLC. All rights reserved.

SFAS No. 109Investment Tax Credit

117. Accounting for an investment tax credit as required by Opinion 2 reduces the cost of the asset to less than its tax basis. The excess of tax basis over cost for financial reporting will be deductible in future years when the asset is recovered. Deferred tax accounting for that temporary difference does not change the accounting for the investment tax credit required by Opinion 2. The entire amount of the investment tax credit is still deferred at the outset and subsequently amortized over the life of the asset. The Board concluded that accounting for this temporary difference (a) is consistent with the basic principles of the Board's asset and liability approach to accounting for deferred income taxes and (b) is not a change in the deferred method of accounting for investment tax credits under Opinion 2.

49Copyright © 2007 Deloitte Development LLC. All rights reserved.

ITC Normalization Requirements

• Normalization provisions require ITC benefits to be shared:

– Between utilities and ratepayers

– Between generations of ratepayers

• ITC benefit is spread over the regulatory life of property

• Two main options are available for ratemaking

50Copyright © 2007 Deloitte Development LLC. All rights reserved.

Unamortized ITCRegulatory Liability Calculation

Unamortized ITC

x Enacted tax rate

x Gross-up (tax-on-tax) factor

Regulatory liability

Dr. Deferred Tax Asset

Cr. Regulatory Liability

51Copyright © 2007 Deloitte Development LLC. All rights reserved.

State ITC

• Investment tax credit is still available in some states

• Considerations

– Consistent application of the GAAP rules under APB Nos. 2 and 4

– Application of the normalization requirements

• Book/tax difference tax-on-tax gross-up factor

52Copyright © 2007 Deloitte Development LLC. All rights reserved.

TerminologySummary

• Normalization

• Flowthrough

• Protected v. unprotected

• Prior flowthrough

• Flowback of prior flowthrough

• ARAM v. Reverse South Georgia Method

53Copyright © 2007 Deloitte Development LLC. All rights reserved.

Regulated Utility Effective Tax Rate ItemsSummary

• Flow-through

– Flow-back of prior flow-through – straight-line or variable based on amount of temporary difference reversal

– Originating differences (if applicable) – amount varies with current capital expenditures and amount of originating temporary differences

• Allowance for Funds Used During Construction (Equity)

– Current amount capitalized – amount varies with current equity rate and capital expenditures

– Depreciation of existing balance in plant – straight-line, but decreasing as vintages become fully amortized

54Copyright © 2007 Deloitte Development LLC. All rights reserved.

Regulated Utility Effective Tax Rate ItemsSummary

• Excess deferred income taxes

– ARAM method – increasing benefit late in asset lives as tax depreciation ends and temporary difference reversal increases

– South Georgia method - straight-line

• Change in state tax rates

• Investment tax credit – straight-line, but decreasing as vintages become fully amortized

55Copyright © 2007 Deloitte Development LLC. All rights reserved.

FAS 71 Exceptions to FAS 109

Circular 230 Statement

Any tax advice included in this written or electronic communication was not intended or written to be used, and it cannot be used by the taxpayer, for the purpose of avoiding any penalties that may be imposed on the taxpayer by any governmental taxing authority or agency.

Limitation on Use

The information contained in this publication is for general purposes only and is not intended, and should not be construed, as legal, accounting, or tax advice or opinion provided by Deloitte & Touche LLP or Deloitte Tax LLP to the reader. This material may not be applicable or suitable for the reader’s specific circumstances of needs. Therefore, the information should not be used as a substitute for consultation with professional accounting, tax, or other competent advisors. Please contact a local Deloitte & Touche LLP or Deloitte Tax LLP professional before taking any action based upon this information.

56Copyright © 2007 Deloitte Development LLC. All rights reserved.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu, a Swiss Verein, its member firms and their respective subsidiaries and affiliates. Deloitte Touche Tohmatsu is an organization of member firms around the world devoted to excellence in providing professional services and advice, focused on client service through a global strategy executed locally in nearly 150 countries. With access to the deep intellectual capital of 120,000 people worldwide, Deloitte delivers services in four professional areas, audit, tax, consulting and financial advisory services, and serves more than one-half of the world’s largest companies, as well as large national enterprises, public institutions, locally important clients, and successful, fast-growing global growth companies. Services are not provided by the Deloitte Touche Tohmatsu Verein and, for regulatory and other reasons, certain member firms do not provide services in all four professional areas.

As a Swiss Verein (association), neither Deloitte Touche Tohmatsu nor any of its member firms has any liability for each other’s acts or omissions. Each of the member firms is a separate and independent legal entity operating under the names “Deloitte,” “Deloitte & Touche,” “Deloitte Touche Tohmatsu,” or other related names.

In the US, Deloitte & Touche USA LLP is the US member firm of Deloitte Touche Tohmatsu and services are provided by the subsidiaries of Deloitte & Touche USA LLP (Deloitte & Touche LLP, Deloitte Consulting LLP, Deloitte Financial Advisory Services LLP, Deloitte Tax LLP and their subsidiaries), and not by Deloitte & Touche USA LLP. The subsidiaries of the US member firm are among the nation's leading professional services firms, providing audit, tax, consulting and financial advisory services through nearly 30,000 people in more than 80 cities. Known as employers of choice for innovative human resources programs, they are dedicated to helping their clients and their people excel. For more information, please visit the US member firm’s web site at www.deloitte.com/us.

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Related Documents