Copyr ight©2007 A KD Securities Limited. A ll rights res erved. The information provided on this document is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrar y to law or r egulation or whic h would s ubject AKD Secur ities or its affiliates to any regis tration requirement within such jurisdiction or country. Neither the information, nor any opinion contained in this document constitutes a solicitation or offer by AKD Securities or its affiliates to buy or sell any securities or provide any investment advic e or service. AKD Securities does not warrant the accuracy of the information provided herein. Pakistan Market: 2007-2008 AKD SECURITIES Member: Karachi Stock Exchange Find AKD research on Bloomberg (AKDS<GO>), firstcall.com and Reuters Knowledge www.akdsecurities.net Equity Research / Pakistan January 2008 AKD Research Team [email protected] Priced on January 04, 2008 KSE-100 Index 14,259.60 KSE Market Cap PkR4,352.89bn (US$69,982mn) KSE-100 Mkt Cap as % of Total Mkt Cap. 86% 1 Year KSE-100 High/Low 14,814/10,040 12m KSE-100 Avg. Traded Value PkR26,268mn (US$406.25mn) KSE-30 Mkt Cap. as % of Total Mkt Cap. 17% YTD KSE-30 High/Low 18,083/11,301 AKD Universe 71% of KSE-100 Market Cap. AKD Research's take on the Numbers 2008 has begun with clouds of political uncertainty hanging on the Pakistan stock market. With the political risk premium having risen after the ghastly assassination of Benazir Bhutto the shocked nation is groping for hope. Announcement of election date as February 18, 2008 and a mature stance by PPP's new leadership as well as PML(N) to participate in the elections have provided investors a degree of comfort regarding the transition to a democratically elected government. Yet, investors remain cautious keeping in mind that there's "many a slip betwixt the cup and the lips". The Central Bank’s latest quarterly review (for quarter ended Sep 2007) indicates that political uncertainty has created a drag on the economy and this was before BB's assassination and consequent law & order crisis. While the law & order situation has been brought under control, investors will be keeping a wary eye on the political scene leading up to the election in six week's time. As such, 1QCY2008 is expected to witness high market volatility driven by news flow from the political front. That said, our oft repeated point regarding stronger market resilience than in the past was again demonstrated last week when the KSE-100 Index staged a smart recovery in the second half of the week and closed 4% down from its most recent peak. In the first half of the week the Index had been down 10% from its peak. By most valuation measures the Pakistan market is arguably the cheapest in the Asian (ex Japan) region. The question investors have to address is whether the Pakistan market could be a value trap in 2008 if longer term political risk premium has significantly increased? That risk cannot be discounted at this point. However, we need to keep in mind that much more is at stake in Pakistan than merely the stock market. The geo-political dynamic of this region has meant that what happens in Pakistan is not simply a domestic issue. It has significant regional and global implications. That is why we believe the powers that be - both internal and external, are likely to leave no stone unturned to focus on: (i) medium term socio-political stability; (ii) a new concerted and sustained campaign against terrorism & extremism post the elections; (iii) ensuring sufficient economic growth to keep the domestic political constituencies aligned to the first two objectives. In the above context, we believe that less risk averse investors will likely find significant potential for outperformance in Pakistan in 2008. In this report we have focused primarily on numbers. Both fundamental sector and company performance in 2007 and forecasts for 2008 are provided, as well as market and valuation data. We believe that this comprehensive databank of AKD covered universe should prove useful for investors as they mull over their near term and longer term investment exposure to Pakistan. . AKD Uni verse - Val uation Multiples FY07A/F FY0 8F FY09F EPS (%) 0.6 6 2 0.44 11 .23 PER (x) 12 .7 10.5 9.5 P/BVS (x) 3.0 8 2.64 2 .29 Dividend Yield (%) 4.4 4.9 5.5 ROE (%) 24.2 5 2 5.02 2 4.1 KSE-100 Index 9,500 10,600 11,700 12,800 13,900 15,000 Dec-06 Apr-07 Jun-07 Sep-07 Jan-08 Index - 100 200 300 400 500 600 Shares (mn) Volume(mn) KSE-100 Index Readers are recommended to also keep in mind risk factors (please see page 63) when investing in equities.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Copyr ight©2007 AKD Securities Limited. All rights reserved. The information provided on this document is not intendedfor distribution to, or use by, any person or entity in any jur isdiction or country where such dis tr ibution or use wouldbe contrary to law or regulation or which would subject AKD Secur ities or its affi liates to any regis tration requirementwithin such jurisdiction or country. Neither the information, nor any opinion contained in this document constitutes asolicitation or offer by AKD Securities or its affiliates to buy or sell any securities or provide any investment advice or service.AKD Securities does not warrant the accuracy of the information provided herein.

Pakistan Market: 2007-2008

AKD SECURITIESMember: Karachi Stock Exchange

Find AKD research on Bloomberg(AKDS<GO>), firs tcall.com and Reuters Knowledge

w w w .akd s ec u ri t i es . n et

Equity Research / Pakistan January 2008

AKD Research [email protected]

Priced on January 04, 2008

KSE-100 Index

14,259.60

KSE Market Cap

PkR4,352.89bn (US$69,982mn)

KSE-100 Mkt Cap as % of Total Mkt Cap.

86%

1 Year KSE-100 High/Low

14,814/10,040

12m KSE-100 Avg. Traded Value

PkR26,268mn (US$406.25mn)

KSE-30 Mkt Cap. as % of Total Mkt Cap.

17%

YTD KSE-30 High/Low

18,083/11,301

AKD Universe

71% of KSE-100 Market Cap.

AKD Research's take on the Numbers2008 has begun with clouds of political uncertainty hanging on the Pakistanstock market. With the political risk premium having risen after the ghastlyassassination of Benazir Bhutto the shocked nation is groping for hope.Announcement of election date as February 18, 2008 and a mature stance byPPP's new leadership as well as PML(N) to participate in the elections haveprovided investors a degree of comfort regarding the transition to a democraticallyelected government. Yet, investors remain cautious keeping in mind that there's"many a slip betwixt the cup and the lips".

The Central Bank’s latest quarterly review (for quarter ended Sep 2007) indicates thatpolitical uncertainty has created a drag on the economy and this was before BB'sassassination and consequent law & order crisis. While the law & order situation hasbeen brought under control, investors will be keeping a wary eye on the political sceneleading up to the election in six week's time. As such, 1QCY2008 is expected towitness high market volatility driven by news flow from the political front. That said,our oft repeated point regarding stronger market resilience than in the past was againdemonstrated last week when the KSE-100 Index staged a smart recovery in thesecond half of the week and closed 4% down from its most recent peak. In the firsthalf of the week the Index had been down 10% from its peak.

By most valuation measures the Pakistan market is arguably the cheapest in theAsian (ex Japan) region. The question investors have to address is whether thePakistan market could be a value trap in 2008 if longer term political risk premiumhas significantly increased? That risk cannot be discounted at this point. However,we need to keep in mind that much more is at stake in Pakistan than merely the stockmarket. The geo-political dynamic of this region has meant that what happens inPakistan is not simply a domestic issue. It has significant regional and global implications.That is why we believe the powers that be - both internal and external, are likely toleave no stone unturned to focus on: (i) medium term socio-political stability; (ii) anew concerted and sustained campaign against terrorism & extremism post theelections; (iii) ensuring sufficient economic growth to keep the domestic politicalconstituencies aligned to the first two objectives. In the above context, we believe thatless risk averse investors will likely find significant potential for outperformance inPakistan in 2008.

In this report we have focused primarily on numbers. Both fundamental sectorand company performance in 2007 and forecasts for 2008 are provided, as wellas market and valuation data. We believe that this comprehensive databank ofAKD covered universe should prove useful for investors as they mull over theirnear term and longer term investment exposure to Pakistan. .

AKD Universe - Valuation MultiplesFY07A/F FY08F FY09F

EPS (%) 0.66 20.44 11.23

PER (x) 12 .7 10.5 9.5P/BVS (x) 3.08 2.64 2.29Dividend Yield (%) 4 .4 4.9 5.5

ROE (%) 24.25 25.02 24.1

KSE-100 Index

9,500

10,600

11,700

12,800

13,900

15,000

Dec-06 Apr-07 Jun-07 Sep-07 Jan-08

Index

-

100

200

300

400

500

600

Shares (mn)

Volume(mn) KSE-100 Index Readers are recommended to also keep in mind risk factors (pleasesee page 63) when investing in equities.

02

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Please see important disclosures and disclaimerson the last page of this report.

Analyst Tel no. E-mail CoverageFaiza Naeem (9221) 111 253 111 faiza.naeem@akdsecuri ties.net Telecom, Fert ilizer, Autos & Paper & Board

Naveed Vakil (9221) 111 253 111 naveed.vakil@akdsecuri ties.net E&P, Oil & Gas MarketingUmer Pervez (9221) 111 253 111 umer.pervez@akdsecuri ties.net Power, Insurance, Chemical & Texti les

Raza Jafri (9221) 111 253 111 raza.jafri@akdsecuri ties.net Commercial BanksFurqan Ayub (9221) 111 253 111 furqan.ayub@akdsecuri ties.net CementQas im Anwar (9221) 111 253 111 qas im.anwar@akdsecuri ties.net Technical Analyst

Rizwan Ahmed (9221) 586 9314 rizwan.ahmed@akdsecuri ties.net Research OperationsAbdul Wadood (9221) 111 253 111 abdul .wadood@akdsecuri ties.net Research Production

Hassan Quadri (9221) 111 253 111 hassan.quadri@akdsecuri ties.net Research Production

AKD Research Team

AKD Universe: Growth vs Value Ranking

Source: AKD Research

03

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Priced on January 04, 2008

PER (x) P/BVS (x) Div Yield PB/ROE PEG RatioSymbol 2009F Symbol 2008F Symbol 2008F Symbol 2008F Symbol 2009GADT 4.2 GADT 0.50 FFC 11% HCAR 2.1 MLCF 0.0FCCL 5.7 NML 0.52 AGTL 10% NESTLE 2.6 CHCC 0.1ACPL 6.0 DGKC 0.68 MLCF 10% PKGS 4.8 SHEL 0.2PSMC 6.4 MLCF 0.81 KAPCO 10% ENGRO 5.2 GADT 0.3PIOC 6.4 HUBC 1.25 FFBL 10% ULEVER 5.9 FCCL 0.3MTL 6.4 FCCL 1.32 HUBC 9% AICL 6.3 ACPL 0.3MLCF 6.9 CHCC 1.52 PIOC 8% MCB 6.7 PICT 0.3AGTL 7.0 PSMC 1.53 OGDC 8% DGKC 7.2 HBL 0.4CHCC 7.0 MTL 1.64 PTC 7% PTC 7.7 BAFL 0.4INDU 7.1 PIOC 1.78 MTL 6% ICI 8.0 UBL 0.5AKBL 7.6 ACPL 1.85 ULEVER 6% PICT 8.1 PSMC 0.5NML 7.8 LUCK 1.93 INDU 6% HUBC 8.3 DGKC 0.6BAFL 7.9 PTC 1.94 ACPL 6% LUCK 8.5 FFBL 0.6PPL 8.4 SNGP 1.98 SNGP 5% SHEL 8.5 PPL 0.6HBL 8.4 AKBL 2.01 PSO 5% UBL 8.6 SNGP 0.6KAPCO 8.6 HCAR 2.09 SHEL 5% THALL 9.3 OGDC 0.6OGDC 8.6 BAFL 2.10 PPL 5% SNGP 9.4 AGTL 0.7LUCK 9.0 SHEL 2.15 ICI 4% BAFL 9.9 INDU 0.7PICT 9.2 ICI 2.18 GADT 4% MLCF 10.0 LUCK 0.7FFC 9.3 KAPCO 2.28 BAFL 4% PSO 10.1 AKBL 0.7DGKC 9.6 THALL 2.37 THALL 4% OGDC 10.1 NML 0.8SNGP 9.8 INDU 2.42 UBL 3% FFBL 10.3 ICI 0.9THALL 10.0 PKGS 2.61 FCCL 3% HBL 10.3 PSO 0.9UBL 10.5 ENGRO 2.63 PICT 3% NML 10.4 NESTLE 1.1FFBL 10.7 AGTL 2.70 NML 3% PPL 10.5 HUBC 1.1SHEL 10.7 HBL 2.79 CHCC 2% AKBL 10.8 THALL 1.2HUBC 11.2 PICT 2.82 PKGS 2% CHCC 10.9 MCB 1.2ICI 11.4 PSO 3.18 MCB 2% FFC 11.1 ULEVER 1.3PSO 12.3 UBL 3.41 NESTLE 2% KAPCO 11.3 FFC 1.4PTC 12.8 PPL 3.65 DGKC 2% PIOC 12.3 PKGS 1.5MCB 13.6 AICL 3.94 AKBL 2% PSMC 12.8 MTL 1.5AICL 14.0 FFBL 4.09 ENGRO 2% INDU 12.8 PTC 3.9ULEVER 14.4 FFC 4.23 HBL 2% AGTL 13.3 KAPCO 5.6PKGS 18.0 OGDC 4.49 AICL 1% ACPL 13.8 ENGRO 6.8ENGRO 18.1 MCB 5.05 LUCK 1% MTL 14.7 AICL n.mNESTLE 27.0 ULEVER 15.23 HCAR 0% FCCL 15.0 PIOC n.mHCAR 29.2 NESTLE 20.62 PSMC 0% GADT 20.4 HCAR n.m

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

04

10,000

11,000

12,000

13,000

14,000

15,000

16,000

Moody's upgradesPakistan Outlook

Rumors of anextension incapital gainstax

ABN Amro - Primedeal news flow

PresidentialReference againstthe Chief Justice

SECP and KSE agree onbonus and rights with

execution of CLN system

SECP not to take punitiveaction against brokers forthe Mar05 s tock market

meltdown

PM states thatconstitutional

provisions do not barthe imposition of

emergency

Riots disrupt Karachiamid clashes on arrival

of the CJ

Gen. Musharraf steps down from COAS

Nawas Sharif returns to Pakistan

Elections areannounced

State ofEmergencydeclared

Gen. Kiyaniappointed as

VCOAS

Singtel deal withWarid in the

making

The Political Backdrop of KSE-100 in 2007

Temasek Groupbuyout of PICIC

BAFLannounces

decision to sellportion of Warid

stake

Lal Masjid crisis reaches peakand ends with military operation.

S&P lowers outlook onPakistan’s credit rating

SC declares referenceagainst the CJ as illegaland restores him to his

post

PML-Q Pres. statedthat govt. is considering

options includingemergency

Rumors about theimposit ion ofemergency

Progress reported intalks between the

government and PPP

Former PM NawazSharif is sent back intoexile

BB announces herreturn to Pakistan

President winselection and NRO

finalized

BB arrives in Pakistan andholds procession which ismet with a suicide bombing

on her convoy Rumors over SBPregulations on banking

provisions

Clamp down on politicalactivists. Commonwealthgives ten day deadline to

restore constitution

Emergency lifted,Constitution restored

Anticipation ofEmergency lifting

Corporate results Corporate resultsCorporate resultsCorporate results

Rumours on CLN and liquidityissues on CFS financing forbonus shares

Assassination of PPPChairperson - Banazir

Bhutto

New Electiondate announced

05

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

ContentsRegional Index Performance .............................................................................................................................06Regional PER/EPS ............................................................................................................................................07Sectoral Performance Dec 29, 2006 to Jan 04, 2008 (All Shares) ....................................................................08Changing Sector Weightage ..............................................................................................................................09Top 20 (KSE-100) Price Performances & Top 20 (All Share) Volume Leaders..................................................10Market - PER & PB Band (FY08F).....................................................................................................................11AKD Universe Valuation & Fundamental Ratios ...............................................................................................12KSE-100 Index - Technical Outlook ...................................................................................................................13AKD Universe - PER versus EPS Growth (2008) & PB versus ROE (2008) ....................................................14Sectoral 12 Month Fundamental Outlook ..........................................................................................................15Economic Snapshot ...........................................................................................................................................16Non-Banking Companies with year-end June Results .....................................................................................17Companies with year-end December Results ..................................................................................................18AKD Universe Sector - Valuation Data...............................................................................................................19AKD Universe Companies - Price Performance ................................................................................................20AKD Universe Companies - Valuation Data.......................................................................................................21AKD Universe Companies - Valuation Data.......................................................................................................22

SectorsCommercial Banks.............................................................................................................................................24Oil & Gas Exploration Cos. ................................................................................................................................25Fertilizer .............................................................................................................................................................26Telecom Sector ..................................................................................................................................................27Insurance ...........................................................................................................................................................28FMCGs...............................................................................................................................................................29OMCs.................................................................................................................................................................30Cement ..............................................................................................................................................................31Power Generation .............................................................................................................................................32Autos..................................................................................................................................................................33Gas T&D ............................................................................................................................................................34Chemicals ..........................................................................................................................................................35Textiles ...............................................................................................................................................................36Transport ............................................................................................................................................................37Paper & Board ...................................................................................................................................................38Agri Autos...........................................................................................................................................................39

Top Picks for 2008Bank Al-Falah Limited ........................................................................................................................................41D.G. Khan Cement.............................................................................................................................................44Engro Chemical Limited .....................................................................................................................................46Fauji Fertilizer Company ....................................................................................................................................48Habib Bank Limited ............................................................................................................................................50Hub Power Company.........................................................................................................................................53Lucky Cement ....................................................................................................................................................55Nishat Mil ls.........................................................................................................................................................57Oil & Gas Development Co. Ltd .........................................................................................................................59Pakistan State Oil ..............................................................................................................................................61

Risk Factors......................................................................................................................63

Company Technicals .......................................................................................................64

06

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Regional Markets’ Performance

Regional Valuations

PBV ROE (%) DY (%)2008 2009 2008 2009 2008 2008 2008

Pakistan 10.55 9.48 20.44 11.23 2.6 25.0 4.9

Thailand 10.90 10.20 18.10 7.30 1.9 17.3 3.9Singapore 14.80 12.90 3.90 14.70 2.1 14.1 3.5Malaysia 16.00 14.40 7.20 11.90 2.4 14.7 3.7Indonesia 16.10 13.90 11.90 16.00 4.3 26.8 2.7

China 19.00 16.20 21.90 17.20 3.4 18.0 1.9Hong Kong 20.90 17.90 (8.30) 16.60 2.2 10.3 2.6India 22.20 17.80 21.10 23.50 4.1 18.6 1.0

Source: Datastream & AKD Research

Source: Datastream

2002-2007 2003 2004 2005 2006 2007 2008Return YTD*

Indonesia (JKSE) 546% 63% 45% 16% 55% 52% 0.7%

India (SENSEX) 501% 73% 13% 42% 47% 47% 2.0%

Pakistan (KSE-100) 421% 66% 39% 54% 5% 40% 1.3%

Vietnam Index (VNINDEX) 406% -9% 43% 29% 143% 23% -2.6%

Philippines (PSEi) 255% 42% 26% 15% 42% 21% -3.8%

Sri Lanka (CSEALL) 214% 30% 42% 28% 42% -6% -2.1%

Thailand (SET) 136% 110% -13% 7% -5% 26% -4.2%

Malaysia (KLSE) 124% 23% 14% -1% 22% 32% 1.5%

NIKKEI 225 JAPAN 78% 24% 8% 40% 7% -11% -4.0%

S&P 500 (U.S) 67% 26% 9% 3% 14% 4% -3.9%

FTSE (U.K) 64% 14% 8% 17% 11% 4% -1.7%

*From Dec 31, 2007 to Jan 04, 2008

Priced on Dec 31, 2007 except Pakistan which is on Jan 04, 2008

PER EPS Growth

07

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Regional PER/EPS

Source: Datastream

Regional P/B and ROE

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

22.00

24.00

6.00 8.00 10.00 12.00 14.00 16.00 18.00 20.00 22.00

PER08

EPS Growth08

IndonesiaMalaysia Philippines

India

Pakistan

Thailand

1.00

2.00

3.00

4.00

5.00

14.00 16.00 18.00 20.00 22.00 24.00 26.00 28.00

PBV2008

ROE 2008

Indonesia

Malaysia

Philippines

India

Pakistan

Thailand

Source: Datastream

08

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Sectoral Performance Dec 29, 2006 to Jan 04, 2008 (All Share)

Source: AKD Research

*New companies listed in 2007 are not included in the performance which are BPGF, POAF, ARM, AHL, JSIL, PASL, HBL, SCBPL, HIRAT,

FLYNG, DSL, SPL & PACE.

( ) Numbers in parenthesis indicate number of companies l isted in the sector.

-31%

-17%

1%

5%

7%

8%

13%

15%

21%

22%

26%

27%

28%

38%

41%

42%

45%

45%

47%

47%

49%

50%

57%

58%

63%

67%

70%

70%

83%

97%

98%

125%

138%

150%

312%

197%

-50% 0% 50% 100% 150% 200% 250% 300% 350%

Textile Weaving (18)

Leasing (19)

Telco & Tech. (9)

Closed-&-Mutual Funds (24)

Sugar & Allied (37)

Oil & Gas Exploration (4)

Textile Spinning (108)

Modarabas (35)

Power G&D (13)

Synthetic (19)

Oil & Gas Marketing (6)

Glass & Ceramics (10)

Vanaspati (12)

Miscellaneous (28)

Fertilizer (4)

Kse-100 Index

Transport (6)

Auto Assembler (12)

Pharmaceuticals (8)

Cement (21)

All Share Index

Textile Composite (59)

Cable & Elect, (9)

Auto Parts (12)

Tobacco (3)

Chemicals (24)

Banking (25)

Food & Allied (22)

Paper & Board (10)

Refining (4)

Engineering (14)

Jute (6)

Investment Banks (26)

Insurance (38)

Woolen (5)

Leather (5)

09

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Changing Sector Weightage

SECTOR NAME Dec-07 Dec-06 Dec-05 Dec-04 Dec-03

COMMERCIAL BANKS* 33.32 25.06 15.97 9.79 9.30

OIL & GAS EXPLORATION COMPANIES 21.03 29.24 30.50 25.73 3.97

FERTILIZER 4.96 5.30 6.27 7.45 7.67

OIL & GAS MARKETING COMPANIES 4.72 5.62 6.75 8.20 12.12

TELECOM & TECHNOLOGY 4.54 6.85 10.54 12.15 22.13

INSURANCE 4.00 1.93 1.05 1.15 1.62

INVESTMENT BANKS/COS./SECURITIES 3.95 2.14 1.83 2.24 1.01

FOOD & PERSONAL CARE-PRUDUCTS 3.89 3.31 2.78 3.64 5.41

CEMENT 3.19 3.18 4.32 3.95 3.88

POWER GENERATION & DISTRIBUTION 2.65 3.47 3.96 4.26 7.93

AUTOMOBILE ASSEMBLER 2.10 2.49 2.14 2.55 3.69

TOBACCO 1.78 1.65 1.47 2.24 1.58

REFINING 1.70 1.30 2.08 2.24 1.76

PHARMACEUTICALS 1.45 1.47 1.51 2.08 2.39

CHEMICALS 1.35 1.39 1.81 3.14 4.80

TRANSPORT 0.87 0.91 1.41 1.68 1.60

TEXTILE COMPOSITE 0.81 0.80 1.55 1.53 1.24

PAPER & BOARD 0.71 0.59 0.83 1.11 1.49

SYNTHETIC & RAYON 0.57 0.76 0.93 1.96 2.54

CABLE & ELECTRICAL GOODS 0.55 0.34 0.29 0.33 0.37

MISCELLANEOUS 0.49 0.68 0.40 0.56 1.24

ENGINEERING 0.29 0.25 0.29 0.41 0.17

JUTE 0.23 0.16 0.11 0.11 0.17

CLOSED-END-MUTUAL FUNDS 0.22 0.49 0.62 0.48 0.71

GLASS & CERAMICS 0.18 0.22 0.09 0.16 0.11

LEATHER & TANNERIES 0.10 0.04 0.03 0.04 0.04

AUTOMOBILE PARTS & ACCESSORIES 0.07 0.06 0.09 0.18 0.29

TEXTILE SPINNING 0.07 0.06 0.08 0.15 0.10

SUGAR & ALLIED INDUSTRIES 0.07 0.09 0.09 0.12 0.10

LEASING COMPANIES 0.05 0.07 0.09 0.14 0.24

MODARABAS 0.02 0.05 0.04 0.08 0.17

TEXTILE WEAVING 0.02 0.04 0.06 0.11 0.11

WOOLEN 0.01 0.01 0.01 0.01 0.04

VANASPATI & ALLIED INDUSTRIES 0.01 0.01 0.01 0.01 0.01

Total 100.00 100.00 100.00 100.00 100.00Source: AKD Research* excluding Standard Chartered Bank Pakistan Ltd., banking sector weight in Dec 07 would be approx. 29%

10

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Top 20 (KSE-100) Price Performance

Top 20 (All Share) Volume Leaders

S.# Company Symbol 1Year Chg. 3M Chg.

1 Jahangir Siddiqui & Company JSCL 1,231% 126%2 Bata (Pakistan) BATA 292% 28%3 Pakistan Reinsurance PAKRI 288% -2%4 Attock Refinery ATRL 278% 21%5 EFU General Insurance EFUG 254% 45%6 Thal Limited THALL 197% 22%7 New Jubilee Insurance NJICL 197% 10%8 Rafhan Maize Products RMPL 161% 27%9 P.N.S.C. PNSC 145% 5%10 Arif Habib Securities AHSL 138% 23%11 Mari Gas MARI 124% 8%12 Adamjee Insurance AICL 118% -10%13 Bannu Woollen BNWM 116% 33%14 Azgard Nine Limited ANL 110% 10%15 Lucky Cement LUCK 105% -14%

16 Pakistan Tobacco PAKT 102% -4%17 Meezan Bank MEBL 98% 8%18 Attock petroleum APL 82% 19%19 Atlas Honda ATLH 82% 42%20 Packages Ltd PKGS 80% 0%

Source: KSE & AKD Research

Source: KSE & AKD Research

S.# Company Symbol 1Yr Avg Daily % of Total 1Yr Avg Value (US$mn) Market AD Value Volume (mn)

1 National Bank of Pakistan NBP 40.98 10.1% 10.242 Oil & Gas Development Co. Ltd. OGDC 33.32 8.2% 16.763 Pakistan Petroleum Limited PPL 29.41 7.2% 7.494 Pak Oilfields POL 26.67 6.5% 4.85

5 MCB Bank MCB 22.81 5.6% 4.586 Lucky Cement LUCK 20.65 5.1% 11.477 DG Khan Cement DGKC 18.79 4.6% 11.478 Arif Habib Securities AHSL 17.93 4.4% 7.429 Bank of Punjab BOP 16.19 4.0% 10.6610 Engro Chemical ENGRO 15.78 3.9% 4.0911 Pakistan State Oil PSO 13.71 3.4% 2.2412 Adamjee Insurance AICL 12.65 3.1% 2.6813 Askari Bank Limited AKBL 10.28 2.5% 6.6914 Habib Bank Limited HBL 9.78 2.4% 2.19

15 J.O.V. & Company Ltd. JOVC 9.24 2.3% 4.4016 Attock Refinery ATRL 8.24 2.0% 2.6017 Nishat Mills NML 8.19 2.0% 4.2818 Bank Al-Falah BAFL 7.67 1.9% 9.1919 Fauji Fertilizer Bin Qasim FFBL 7.02 1.7% 11.1020 PTCL (A) PTC 6.65 1.6% 7.69

11

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

AKD Universe - PER Band (FY08F)

Source: KSE & AKD Research

AKD Universe - PB Band (FY08F)

Source: KSE & AKD Research

Jul-03 May-04 Apr-05 Mar-06 Feb-07 Jan-08

(x)

11.5

10.0

8.5

7.0

Jul-03 May-04 Apr-05 Mar-06 Feb-07 Jan-08

(x)

3.0

2.5

2.0

1.5

*AKD Universe comprises 71% of KSE-100 Index capitalization

12

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

AKD Universe Valuation

AKD Fundamental Ratios (%)

January 04, 2008 FY05A FY06A FY07A/F FY08F FY09F

EPS (PkR) 7.59 9.24 9.30 11.20 12.46EPS Chg (%) 34.29 21.69 0.66 20.44 11.23Price to Earnings (x) 15.56 12.79 12.70 10.55 9.48Price to Book (x) 4.24 3.52 3.08 2.64 2.29Price to CF (x) 11.92 12.55 11.87 10.01 8.54Earnings Yield (%) 6.43 7.82 7.87 9.48 10.55Dividend Yield (%) 3.7 4.7 4.4 4.9 5.5Payout (%) 57.80 59.78 55.65 52.04 52.22EV / EBITDA (x) 7.64 6.59 6.91 5.87 5.41FCFE Yield (%) 4.8% 4.3% 5.9% 7.3% 9.5%Price to Sales (x) 2.48 1.92 1.72 1.49 1.37Book Value per Share (PkR) 27.86 33.52 38.34 44.75 51.69Return on Equity (%) 27.24 27.56 24.25 25.02 24.10Return on Assets (%) 5.40 5.67 5.11 5.51 5.63Chg in Sales (%) 29.69 29.49 11.46 15.39 9.16Gross Margin (%) 34.63 32.75 30.57 31.41 31.44Operating Margin (%) 22.90 21.90 19.68 21.22 21.53Net Margin (%) 15.95 14.99 13.54 14.13 14.40

Non-Financial Sector 2005A 2006A 2007A/E 2008F 2009F

Sales Growth 24% 27% 9% 16% 10%Gross Margin 25% 23% 20% 21% 21%Operating Margin 19% 18% 15% 16% 16%Net Margin 14% 12% 11% 11% 11%LT Debt / Equity 19% 19% 21% 20% 18%CA/CL (x) 1.98 1.81 1.97 1.98 0.27Growth in Operating CF 20% -5% 6% 19% 17%ROE 29% 29% 24% 25% 25%

Banking Sector 2005A 2006A 2007E 2008F 2009F

Asset Growth 17% 15% 13% 10% 9%Deposits Growth 15% 11% 14% 9% 7%Loan Growth 31% 17% 7% 13% 11%Net Int Inc. Growth 76% 32% 11% 13% 11%Fee Inc. Growth 14% 27% 12% 16% 13%Net Int Inc./Total Income 80% 80% 84% 79% 79%L/D Ratio 67% 71% 66% 69% 71%ROA 2.0% 2.5% 2.3% 2.6% 2.7%

Source: AKD Research

13

Pakistan Market: 2007 - 2008 AKD Securities Limited January 2008

Qasim Anwar Technical Analyst [email protected]

Major Support 13,146~13,350 levels Short Term Target 14,480~17,580 levels Intermediate Target 16,280~16,400 levels Long Term Target 15,300~15,500 levels Moving Averages 004-Week 14,561.76 006-Week 14,453.24 020-Week 13,727.41 030-Week 13,659.87 100-Week 11,825.12 DEMAND / SUPPORT LEVEL S1 13,146~13,350 S2 12,800~12,950 S3 12,076~12,337 SUPPLY / RESISTANCE LEVEL R1 14,200~14,290 R2 14,908 R3 15,320 R4 16,415~16,500 R5 16,930~17,000 R6 17,480~17,580

§ During the year 2007, KSE 100-index posted a whooping gain of 40.2% or 4,035 points to settle at 14,075 levels from 10,040 levels on year ended December 29, 2006. Looking at the Index’s movement over the last three years, the series of successively higher peaks and troughs along with the rising OBV (On Balance Volume) suggests that the primary bullish trend is intact, despite high volatility witnessed in recent months.

§ The rising long-term channel on weekly chart is leading towards our

December 2008 objective of 17,480~17,574 levels – anticipated around 123.6% Fibonacci Projection (9,696-14,290). Recent movements suggest that a breakout above the formidable resistance around 14,200~14,290 levels would push the index to hit its short-term target of 15,300~15,500 levels (76.4% Fibonacci Projection (9,696-14,290). Once these levels are achieved, a smoother rally could be constructed toward the Index’s intermediate target of 16,280~16,400 levels around 100% Fibonacci Projection (9,696-14,290), which if also breached (on weekly closing basis) then our 2008 objective will be on cards.

§ On the down side, two major supports exist between 13,399~13,550 levels

and 12,800~12,881 levels if market takes any near-term dip. § INVESTMENT PERSPECTIVE: Take selective positions in fundamentally

strong scrips at weekly close above 14,290 levels for the KSE-100 Index. Short-term trading oriented investors are suggested to cut positions if Index slips below 14,100~14,200 levels (on weekly closing basis). For investors with 3-month horizon strategy of buy on dips up to 13,548 levels should yield positive results.

KSE-100 Index Closing Index: 14,259.60

Pakistan Stock Market

14

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

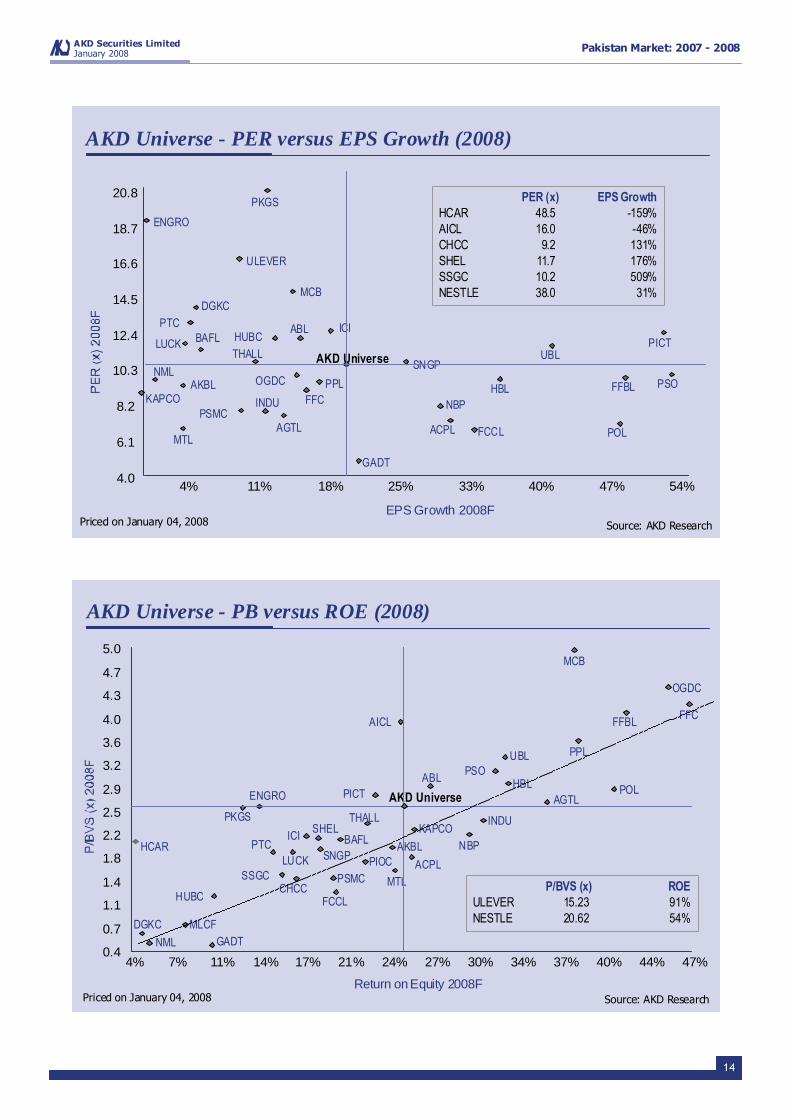

AKD Universe - PER versus EPS Growth (2008)

Source: AKD Research

PER (x) EPS GrowthHCAR 48.5 -159%AICL 16.0 -46%CHCC 9.2 131%SHEL 11.7 176%SSGC 10.2 509%NESTLE 38.0 31%

4.0

6.1

8.2

10.3

12.4

14.5

16.6

18.7

20.8

4% 11% 18% 25% 33% 40% 47% 54%

EPS Growth 2008F

PPL

ACPL

FFCINDU

ULEVER

THALL

PTC

PSOOGDC

LUCK

PSMC

SNGPUBL

DGKC

ENGRO

GADT

NMLFFBL

PICT

AKBL

PKGS

HBL

MTLFCCLAGTL

BAFL HUBC

MCB

AKD Universe

POL

NBPKAPCO

ABL ICI

Priced on January 04, 2008

AKD Universe - PB versus ROE (2008)

P/BVS (x) ROEULEVER 15.23 91%NESTLE 20.62 54%

Source: AKD Research

0.4

0.7

1.1

1.4

1.8

2.2

2.5

2.9

3.2

3.6

4.0

4.3

4.7

5.0

4% 7% 11% 14% 17% 21% 24% 27% 30% 34% 37% 40% 44% 47%

Return on Equity 2008F

PPL

ACPL

FFC

INDU

MLCF

THALL

PTC

PSO

OGDC

LUCKPSMC

SNGP

UBL

DGKC

ENGRO

FFBL

PICT

AKBL

PKGS

HBL

MTL

FCCL

BAFL

HUBC

AICL

AGTL

KAPCOSHELHCAR

PIOC

CHCC

AKD Universe

MCB

SSGC

ICINBP

POLABL

GADTNML

Priced on January 04, 2008

15

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Sectoral 12 Month Fundamental Outlook

Source: AKD Sector Analysts’ Expectations

Sector Demand CapacityUtilization

PricingPower Margins Leverage RoE 3Yr EPS

Growth

Oil & Gas (E&P)

Banking

Telecom (Fixed)

Telecom (Cellular)

Fertil izer

Oil Marketing

Cement

Au to

Insuarance

Power Generation

Better than 2007 Worse than 2007 Stable

How the Analysts view their sectors' 2008 performance

We asked our sector analysts to provide a considered fundamental outlook for their sectors for 2008.The above chart captures their views. The key point to note is that despite a higher level of uncertainty,most sectors (with the exception of autos and fixed line telephony) are expected to see demand risingat or above last year's level. This should enable increasing capacity utilization which is especially welcomefor sectors such as oil & gas, cement and cellular players who have recently enhanced their capacities.

The flip side of higher capacity is however, that pricing power has been diluted with only 3 out of 10sectors expected to show improvement in pricing power. Two of the three (Oil & gas exploration and Oilmarketing) are expected to benefit from reduction in subsidies to end-users while the fertilizer sector isexpected to benefit from rising government support to farmers in the form of agri-credit & higher offtakeprices of key grains in line with the global trend in food prices. Along with diluted pricing power, thepressure of costs in key raw materials as well as energy will likely keep margins under pressure in allcovered sectors.

At the same time, continued strong cash flows are expected to bring down borrowing requirements andthus ease financial expenses. As a result, earnings growth is expected to remain healthy with ROE's inmost sectors (except autos & power) expected to improve compared to 2007. .

16

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

FY08

Provisional Original SBP

FY07 targets projection

Growth rates (percent)

GDP 7.0 7.2 6.6 - 7.0

Inflation 7.8 6.5 6.5 - 7.5

Monetary assets (M2) 19.3 13.7* 13.5 - 14.5

billion US Dollars

Exports (fob-BoP data) 17.1 18.9 18.3

Imports (fob-BoP data) 27.0 29.6 28.9

Exports (fob-Customs data) 17.0 19.2 19.2

Imports (cif-Customs data) 30.5 32.3 32.3

Workers' remittances 5.5 5.8 6.0 - 6.5

percent of GDP

Budgetary balance -4.3 -4.0** -4.0

Current account balance -0.5 -5.0 -5.2(*) Announced in MPS Jul-Dec FY08: (**) Budget estimates. Source: State Bank of Pakistan

Selected Economic Indicators FY06 FY07 FY08

Growth rate (percent)

Large scale manufacturing Jul-Sep 9.0 10.4 6.9

Exports (FOB) Jul-Oct 14.6 4.1 10.9

Imports (FOB) Jul-Oct 37.4 14.5 3.4

Tax revenue (CBR) Jul-Oct 20.8 17.9 14.4

CPI (12 month MA) Nov 9.0 7.9 7.6

Private sector credit Jul- 1st Dec 12.2 7.0 5.4

Money supply (M2) Jul- 1st Dec 3.4 4.2 4.2

million US Dollars

Total liquid reserves -1 End-Nov 11,255 12,298 15,778

Home remittances Jul-Oct 1,372 1,644 2,081

Foreign private investment Jul-Oct 696 1,741 1,642

percent of GDP -2

Fiscal deficit Jul-Sep 0.5 1.0 1.6

Trade deficit Jul-Oct 2.1 2.5 2.0

Current a/c deficit Jul-Oct 1.7 2.4 1.81- With SBP & commercial banks.2- Based on full-year GDP in the denominator. For FY08 estimated full year GDP has been used. Source: State Bank of Pakistan

Fiscal Performance Indicators (Jul-Sep) as percent of GDP (1) FY06 FY07 FY08

Fiscal balance -0.5 -1.0 -1.6

Primary balance 0.1 -0.3 -0.5

Revenue balance 0.2 0.1 -0.31 Based on projected full-year GDP Source: State Bank of Pakistan

Economic Snapshot

17

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

AKD Universe Companies’ Fundamental Performance

Sales Growth Gross Operating Operating EPS Growth Net (%) Margin Profit Margin (%) Margin

Pakistan Telecom Company -7% n.a -46% 22% -43% 17%Cherat Cement Company 2% 6% -97% 1% -97% 0%DG Khan Cement 21% 17% -61% 14% -45% 12%Lucky Cement 19% 27% -12% 21% 53% 20%Maple Leaf Cement Factory -30% 10% -78% 5% -97% 0%Fauji Cement -23% 20% -71% 16% -77% 7%Pioneer Cement 40% 5% -155% -5% n.a -12%Attock Cement Pakistan Limited -10% 25% -59% 21% -72% 8%Oil & Gas Development Company 10% 66% 3% 63% 0% 44%Pakistan Petroleum Limited 17% n.a. 25% 68% 26% 47%Pak Oilfields Limited -8% 61% -3% 60% 3% 51%Sui Southern Gas Company -2% 9% 32% 7% -21% 2%Sui Northern Gas Piplines 13% 13% 18% 3% 30% 3%Pakistan State Oil 21% 4% 444% 3% 271% 2%Shell Pakistan Limited -5% 7% -442% 3% n.a 2%Hub Power Company Limited 13% 8% 2% 8% -16% 5%Kot Addu Power Company 16% 23% 17% 22% 17% 13%Pakistan Int'l Container Terminal 28% 41% 31% 33% 37% 17%Millat Tractors Limited 3% 12% -4% 6% -3% 6%Indus Motors 11% 13% 45% 11% 46% 9%Nishat Mills -1% 19% 5% 11% 14% 11%Gadoon Textile 2% 11% -32% 7% -37% 3%

Source: Company Reports

Non-Banking Companies with year-end June (1QFY08 vs 1QFY07)

Sales Growth Gross Margin Operating Profit Operating Margin EPS Growth (%) Net Margin

(%) 2007 2007 2007 2007 (%) 2007 2007

Pakistan Telecom Company -6% n.a -38% 26% -25% 24%Cherat Cement Company 4% 18% -60% 13% -66% 7%DG Khan Cement -19% 32% -51% 29% -33% 25%Lucky Cement 55% 29% 11% 24% 32% 20%Maple Leaf Cement Factory -27% 12% -82% 9% -96% 1%Fauji Cement -21% 35% -48% 30% -46% 19%Pioneer Cement 10% 18% -61% 13% -114% -3%Attock Cement Pakistan Limited 28% 36% -8% 29% -12% 18%Oil & Gas Development Company 4% 39% -6% 11% -1% 7%Pakistan Petroleum Limited 21% n.a 23% 11% 25% 6%Pak Oilfields Limited 20% 33% 24% 11% 29% 7%Sui Southern Gas Company 6% 9% 47% 4% -67% 0%Sui Northern Gas Piplines 6% 15% 7% 5% -28% 2%Pakistan State Oil 17% 4% -35% 2% -38% 1%Shell Pakistan Limited -2% 6% -81% 1% -77% 1%Hub Power Company Limited 12% 14% 1% 13% -4% 8%Kot Addu Power Company -4% 26% -16% 26% -6% 16%Pakistan Int'l Container Terminal 22% 42% 36% 35% 14% 16%Millat Tractors Limited 2% 12% 4% 10% 5% 8%Indus Motors 22% 11% 9% 9% 4% 6%Nishat Mills 5% 17% -15% 9% 3% 10%Gadoon Textile 13% 12% -13% 8% -21% 4%

Non-Banking Companies with year-end June Results (FY2007-06)

Source: Company Reports

18

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

AKD Universe Companies’ Fundamental Performance

Non-Banking Companies with year-end December Results (FY2007-06)Sales Growth Gross Margin Operating Profit Operating Margin EPS Growth (%) Net Margin

(%) 2006 2006 2006 2006 (%) 2006 2006Fauji Fertilizer Company 18% 32% 2% 23% -5% 15%

Engro Chemical -4% 24% 4% 16% 10% 14%

Fauji Fertilizer Bin Qasim Ltd. 3% 32% -3% 20% 0% 17%

Unilever Pakistan Limited 19% 38% 4% 13% 3% 8%

Nestle Pakistan Limited 29% 28% 24% 12% 18% 6%

Al-Ghazi Tractor 17% 18% 2% 17% 16% 14%

ICI Pakistan 6% 21% 35% 13% -35% 7%

Pak Suzuki Motors 33% 12% 50% 12% 50% 7%

Honda Atlas Car 55% 5% 974% 3% 335% 3%

Adamjee Insurance Co. Limited 32% 9% 40% 40% 36% 30%

Packages Limited 11% 16% -16% 10% 20% 16%Source: Company Reports

Source: Company Reports

Non-Banking Companies with year-end December (9MCY07 vs 9MCY06)Sales Growth Gross Operating Operating EPS Growth Net

(%) Margin Profit Margin (%) Margin

Fauji Fertil izer Company -3% 39% 24% 21% 27% 21%

Engro Chemical 33% 24% 18% 12% 17% 12%

Fauji Fertil izer Bin Qasim Ltd. -9% 34% 37% 20% 16% 20%

Unilever Pakistan Limited 10% 40% 11% 8% 4% 8%

Nestle Pakistan Limited 28% 29% 64% 7% 74% 7%

Al-Ghazi Tractor 1% 18% 1% 14% 4% 14%

ICI Pakistan 11% 20% 10% 7% 19% 7%

Pak Suzuki Motors 8% 11% -10% 7% -14% 7%

Honda Atlas Car -13% 4% -151% 1% n.a 1%

Adamjee Insurance Co. Limited 5% 10% 21% 41% 20% 38%

Packages Limited 13% 16% 12% 10% -9% 10%

19

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

2007A/F 2008F 2009F 2007A/F 2008F 2009F 2007A/F 2008F 2009F 2006A 2007A/F 2008F 2007A/F 2008F

Banks 7% 26% 14% 13.6 10.8 9.5 3.8 3.0 2.4 2.0% 2.5% 3.5% 30% 31%

E&P 5% 19% 15% 11.3 9.5 8.2 5.0 4.1 3.4 6.1% 7.0% 7.0% 44% 43%

Telecom -25% 5% 2% 13.6 13.0 12.8 2.0 1.9 1.9 11.9% 4.8% 6.6% 14% 15%

Fertilizer 17% 21% -3% 13.5 11.2 11.6 4.1 3.5 3.4 5.9% 6.2% 7.7% 30% 31%

FMCGs 13% 20% 29% 33.7 28.1 21.7 21.3 18.8 15.5 1.6% 2.5% 3.2% 63% 67%

OMCs -49% 69% -13% 17.5 10.3 11.9 3.1 2.8 2.7 7.9% 4.7% 5.3% 18% 28%

Cement -28% 27% 33% 13.0 10.2 7.7 1.3 1.1 1.0 2.9% 1.3% 3.3% 10% 10%

Power -5% 4% 5% 10.5 10.1 9.6 1.7 1.7 1.6 13.3% 10.7% 9.6% 16% 16%

Autos -3% 11% 17% 5.3 4.7 4.1 2.3 1.9 1.5 1.6% 1.8% 2.5% 26% 24%

Gas T&D -36% 74% 14% 18.3 10.5 9.2 2.0 1.8 1.7 4.6% 3.7% 6.5% 11% 17%

Insurance 180% -46% 14% 7.7 14.3 12.5 4.4 3.5 2.9 0.8% 1.3% 1.5% 57% 25%

Chemical 25% 19% 10% 14.9 12.5 11.4 2.4 2.2 2.0 2.8% 3.9% 4.4% 16% 17%

Paper & Board -7% 12% 16% 23.4 20.8 18.0 2.8 2.6 2.4 1.7% 2.1% 2.4% 12% 13%

Textile -1% 4% 23% 9.3 9.0 7.3 0.5 0.5 0.5 1.7% 2.6% 2.7% 6% 6%

Agri Autos 12% 11% 7% 8.1 7.3 6.8 2.6 2.3 2.0 7.6% 8.7% 9.1% 32% 31%

Jute 12% 11% 7% 11.9 10.7 10.0 2.8 2.4 2.0 1.7% 1.2% 3.6% 24% 22%

Transport 14% 52% 34% 18.9 12.4 9.2 3.5 2.8 2.3 0.0% 0.0% 2.9% 18% 23%

AKD Universe 1% 20% 11% 12.7 10.5 9.5 3.1 2.6 2.3 4.7% 4.4% 4.9% 24% 25%

EPS Growth PER* (x) P/BVS* (x) Dividend Yield*

*Priced on January 04, 2008

AKD Universe Sector - Valuation DataROE

2007A/F 2008F 2009F 2007A/F 2008F 2009F 2007A/F 2008F 2009F 2007A/F 2008F 2009F

Banks 18.8% 12.7% 10.9% n.a n.a n.a 58.5% 62.5% 63.8% 39.7% 42.2% 43.1%

E&P 9.1% 18.1% 12.4% -2% 34% 12% 61.1% 63.2% 65.0% 43.8% 44.1% 45.2%

Telecom -6.5% 1.4% 1.9% 0% -41% 35% 26.1% 31.1% 30.9% 24.2% 25.0% 25.0%

Fertilizer 10.4% 15.5% 14.2% 108% 16% -43% 21.6% 21.7% 18.5% 16.3% 17.1% 14.5%

FMCGs 21.5% 20.0% 19.4% -36% 123% -35% 11.4% 11.3% 11.8% 6.5% 6.5% 7.1%

OMCs 11.9% 18.1% 6.6% 58% -5% 236% 1.8% 3.1% 2.4% 1.2% 1.7% 1.4%

Cement 5.4% 49.3% 16.2% -59% 90% 27% 22.8% 26.0% 27.8% 15.6% 14.7% 16.7%

Power 3.3% 0.9% 1.4% -41% 29% 3% 19.4% 19.9% 19.9% 12.2% 12.6% 13.1%

Autos 5.5% 22.3% 10.4% n.m 25% 18% 7.8% 7.9% 8.0% 4.9% 4.8% 5.1%

Gas T&D 6.1% 9.0% 12.1% -69% 81% 44% 4.5% 5.0% 5.2% 1.6% 2.6% 2.6%

Insurance 20.0% 17.5% 18.1% n.m -30% 79% 86.6% 43.4% 41.7% 69.6% 32.0% 30.9%

Chemical 12.5% 8.7% 7.4% n.m 101% -7% 14.0% 15.3% 15.5% 8.3% 9.0% 9.2%

Paper & Board 4.6% 28.7% 19.4% n.m -50% 46% 10.5% 10.3% 13.4% 13.8% 12.0% 11.7%

Textile 6.8% 8.3% 8.7% 35% -17% 30% 8.5% 9.1% 9.5% 8.1% 7.8% 8.8%

Agri Autos 6.5% 7.8% 7.2% 53% 13% 6% 13.7% 14.4% 14.5% 11.0% 11.2% 11.2%

Jute 12.8% 12.9% 9.4% 45% 17% 31% 17.9% 17.2% 16.9% 11.1% 10.9% 10.7%

Transport 22.5% 27.7% 17.2% -6% -11% 38% 35.1% 37.8% 40.0% 15.8% 18.9% 21.7%

AKD Universe 11.5% 15.4% 9.2% 2% 19% 18% 19.7% 21.2% 21.5% 13.5% 14.1% 14.4%

Operating CF GrowthRevenue Growth Operating Margin Net Margin

Source: AKD Research

20

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Source: AKD Research

AKD Universe Companies - Price PerformanceMkt. Cap 6M AD Val Price (PkR) % Chg. 12M (Price-PkR) 3M (Price-PkR) 1W (Price-PkR)* Chg from 1 Year

Company (US$mn) (US$mn) 4-Jan-08 in CY07 High Low High Low High Low All Time High STD

MCB 4,091 20.79 398.80 86% 433.00 222.17 433.00 338.00 399.95 363.45 -8% 16%

NBP 3,109 34.50 233.50 20% 278.85 201.74 278.85 214.10 233.50 214.10 -16% 5%

HBL 2,656 9.78 235.80 -19% 298.70 218.00 298.70 218.00 239.90 218.00 -21% 6%

UBL 2,429 3.78 183.80 50% 224.25 123.68 205.70 157.65 183.80 166.00 -18% 13%

ABL 1,175 1.35 133.60 71% 145.45 77.58 141.25 120.40 137.45 128.00 -8% 15%

BAFL 572 6.43 53.90 68% 65.10 33.15 62.10 48.80 53.90 49.40 -17% 15%

AKBL 511 7.83 104.05 49% 105.95 71.67 105.95 84.60 104.05 98.60 -2% 9%

OGDC 8,528 31.13 121.45 6% 132.80 104.90 132.80 113.40 121.45 113.40 -36% 4%

PPL 3,066 26.63 248.95 18% 276.82 212.73 276.82 233.00 248.95 233.00 -13% 5%

POL 1,080 27.15 335.50 -4% 373.95 280.25 363.85 305.55 335.50 307.40 -29% 6%

PTC 3,485 4.54 41.85 -6% 61.35 38.75 56.00 38.75 42.05 38.75 -53% 9%

FFC 995 3.27 123.50 17% 129.15 103.70 127.00 114.85 125.20 118.75 -14% 5%

ENGRO 829 20.13 262.50 66% 296.70 158.65 296.70 241.00 265.75 241.00 -12% 17%

FFBL 658 6.77 43.15 51% 48.30 28.40 48.30 39.50 43.15 39.50 -11% 15%

NESTLE 1,348 0.01 1,820 74% 1,855 1,036 1,855 1,480 1,820 1,800 -2% 12%

ULEVER 525 0.04 2,420 21% 2,625 2,000 2,625 2,280 2,420 2,280 -8% 7%

PSO 1,166 13.11 416.50 42% 434.00 297.85 434.00 373.00 416.50 387.00 -15% 9%

SHEL 373 0.37 417.00 5% 499.10 370.00 460.00 394.90 417.00 394.90 -38% 7%

LUCK 510 19.64 118.70 98% 143.05 58.00 143.05 107.70 118.70 107.70 -17% 22%

DGKC 389 13.39 94.00 49% 120.00 62.25 117.10 85.50 94.70 85.50 -23% 14%

ACPL 123 0.12 104.70 58% 126.90 65.80 126.10 90.00 104.70 95.00 -21% 12%

MLCF 118 1.09 19.45 18% 25.90 14.82 24.40 18.05 19.45 18.05 -54% 13%

FCCL 329 1.64 15.55 0% 19.50 14.45 17.95 14.45 15.55 14.45 -31% 10%

PIOC 86 0.53 31.00 39% 51.50 21.20 38.55 28.55 31.60 28.55 -54% 20%

CHCC 64 0.09 40.90 0% 63.85 37.45 48.00 37.45 40.90 38.80 -57% 13%

KAPCO 721 0.77 50.15 23% 62.55 40.50 56.75 47.00 50.80 48.45 -20% 11%

HUBC 718 1.29 31.40 28% 36.15 24.64 36.15 29.25 31.40 30.20 -25% 8%

PSMC 434 0.69 327.75 17% 429.00 272.70 429.00 311.00 329.65 311.00 -24% 11%

INDU 393 0.78 306.00 57% 406.00 193.25 406.00 297.00 319.20 297.00 -25% 18%

HCAR 62 0.40 52.80 58% 81.40 31.08 81.40 48.85 54.10 48.85 -35% 27%

SNGP 592 1.18 66.00 1% 86.20 58.50 71.40 61.50 66.00 61.50 -41% 8%

SSGC 294 0.98 26.85 14% 31.70 24.00 29.15 25.45 26.85 25.45 -42% 6%

AICL 556 15.32 333.00 121% 417.00 152.15 417.00 310.90 358.35 323.45 -20% 27%

ICI 441 3.30 194.60 68% 234.30 117.40 234.30 162.65 196.65 177.55 -17% 18%

PKGS 432 3.83 360.95 80% 416.20 193.81 416.20 340.00 363.80 340.00 -13% 21%

NML 267 5.14 102.40 17% 133.75 88.30 132.90 95.00 105.20 95.00 -23% 11%

GADT 23 0.00 59.10 -6% 84.45 56.05 74.00 56.10 59.10 56.10 -52% 11%

AGTL 199 0.03 283.95 30% 293.00 199.90 291.50 250.00 283.95 268.10 -3% 12%

MTL 89 0.05 290.00 3% 342.45 256.50 320.00 256.50 290.00 270.50 -15% 7%

THALL 144 0.17 290.00 198% 303.00 97.04 303.00 238.00 290.00 275.00 -4% 24%

PICT 85 0.32 68.95 21% 84.80 50.70 75.45 58.50 70.40 64.75 -40% 14%

*1week: Dec 27, 07 - Jan 04, 2008

21

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Company 2007A/F 2008F 2009F 2007A/F 2008F 2009F 2007A/F 2008F 2009F 2006A 2007A/F 2008F

MCB 29% 20% 12% 15.9 13.3 11.9 5.5 4.3 3.4 1.8% 2.1% 2.4%

NBP 28% 16% 5% 8.8 7.5 7.2 1.9 1.6 1.3 1.7% 2.1% 2.6%

HBL -14% 38% 19% 13.3 9.6 8.1 3.0 2.3 1.8 0.4% 1.5% 1.7%

UBL -4% 41% 11% 16.4 11.6 10.5 4.0 3.2 2.7 2.2% 2.7% 3.3%

ABL 35% 16% 8% 12.2 10.5 9.8 3.2 2.6 2.2 1.9% 2.6% 3.0%

BAFL 75% 14% 26% 11.4 9.9 7.9 2.5 2.1 1.7 0% 2.8% 3.7%

AKBL 45% 20% 13% 9.6 8.0 7.1 2.2 1.8 1.5 1.0% 1.4% 1.9%

OGDC -1% 15% 15% 11.4 9.9 8.6 5.3 4.5 3.8 7.2% 8.2% 7.8%

PPL 25% 18% 14% 11.2 9.5 8.4 4.7 3.6 2.9 3.6% 4.4% 4.8%

POL 3% 48% 18% 10.5 7.1 6.0 3.6 2.9 2.3 4.5% 4.5% 7.2%

PTC -25% 5% 2% 13.6 13.0 12.8 2.0 1.9 1.9 11.9% 4.8% 6.6%

FFC 25% 16% -3% 10.5 9.0 9.3 4.4 4.2 4.3 8.1% 9.5% 11.1%

ENGRO 4% 0% 5% 19.1 19.1 18.1 3.6 2.6 2.4 3.4% 1.8% 1.8%

FFBL 14% 49% -9% 14.5 9.7 10.7 4.4 4.1 4.1 5.8% 6.7% 10.1%

NESTLE 21% 31% 41% 49.8 38.0 27.0 23.5 20.6 16.4 0.3% 1.5% 2.1%

ULEVER 6% 10% 17% 18.4 16.8 14.4 17.1 15.2 13.5 5.0% 5.2% 5.9%

PSO -38% 53% -19% 15.2 9.9 12.3 3.4 3.2 3.0 8.2% 5.0% 5.3%

SHEL -77% 176% 9% 32.3 11.7 10.7 2.4 2.1 2.0 7.2% 3.8% 5.3%

LUCK 32% 4% 31% 12.3 11.8 9.0 3.3 1.9 1.3 0.8% 1.1% 1.3%

DGKC -33% 5% 46% 14.7 13.9 9.6 0.7 0.7 0.6 1.6% 1.6% 2.1%

ACPL -12% 31% 20% 9.5 7.2 6.0 2.2 1.9 1.5 4.8% 4.3% 5.7%

FCCL -46% 33% 17% 8.9 6.7 5.7 1.6 1.3 1.1 9.6% 0.0% 3.2%

CHCC -66% 131% 31% 21.2 9.2 7.0 1.8 1.5 1.3 5.1% 2.4% 2.4%

KAPCO -6% 0% 3% 8.8 8.9 8.6 2.3 2.3 2.2 16.2% 12.0% 10.3%

HUBC -4% 13% 8% 13.7 12.1 11.2 1.2 1.2 1.2 9.9% 9.1% 8.8%

PSMC -8% 10% 23% 8.6 7.8 6.4 1.9 1.5 1.2 0.0% 0.0% 0.0%

INDU 4% 12% 10% 8.8 7.8 7.1 3.0 2.4 2.0 3.9% 4.2% 5.8%

HCAR n.m n.m 66% n.m 48.5 29.2 2.5 2.1 1.8 0.0% 0.0% 0.4%

SNGP -28% 27% 9% 13.5 10.7 9.8 2.2 2.0 1.8 4.5% 4.5% 5.3%

SSGC -67% 509% 25% 62.1 10.2 8.2 1.7 1.6 1.5 4.8% 1.9% 8.8%

AICL 180% -46% 14% 7.7 14.3 12.5 4.4 3.5 2.9 0.8% 1.3% 1.5%

ICI 25% 19% 10% 14.9 12.5 11.4 2.4 2.2 2.0 2.8% 3.9% 4.4%

PKGS -7% 12% 16% 23.4 20.8 18.0 2.8 2.6 2.4 1.7% 2.1% 2.4%

NML 3% 1% 24% 9.8 9.7 7.8 0.5 0.5 0.5 1.5% 2.4% 2.6%

GADT -21% 22% 16% 6.0 4.9 4.2 0.5 0.5 0.5 4.2% 4.2% 4.2%

AGTL 15% 14% 8% 8.6 7.5 7.0 3.0 2.7 2.4 7.9% 9.1% 10.4%

MTL 5% 4% 5% 7.1 6.8 6.4 1.9 1.6 1.4 6.9% 7.6% 6.2%

THALL 12% 11% 7% 11.9 10.7 10.0 2.8 2.4 2.0 1.7% 1.2% 3.6%

PICT 14% 52% 34% 18.9 12.4 9.2 3.5 2.8 2.3 0.0% 0.0% 2.9%

EPS Growth PER* (x) P/BVS* (x) Dividend Yield*

*Priced on January 04, 2008

AKD Universe Companies - Valuation Data

22

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

07A/F 2008F 2009F 2007A/F 2008F 2009F 2007A/F 2008F 2009F 2007A/F 2008F 2009F Company

34% 32% 29% 35.8% 19.5% 12.6% 67.3% 67.7% 67.2% 44.9% 45.2% 44.8% MCB

22% 21% 18% 31.6% 13.7% 4.2% 58.0% 59.3% 59.4% 37.7% 38.5% 38.6% NBP

23% 24% 22% 25.7% 8.6% 4.8% 38.5% 50.4% 56.6% 23.2% 29.4% 33.3% HBL

24% 28% 25% 22.4% 16.7% 11.7% 32.6% 39.7% 38.9% 22.4% 27.2% 26.9% UBL

27% 25% 23% 42.2% 8.7% 3.2% 36.1% 38.6% 40.3% 24.2% 25.8% 26.8% ABL

25% 23% 23% 20.8% 12.1% 8.3% 35.4% 36.7% 39.3% 24.5% 23.9% 25.6% BAFL

23% 22% 21% 20.7% 8.3% 6.9% 32.2% 35.7% 37.6% 21.4% 23.8% 25.0% AKBL

46% 45% 45% 3.6% 18.9% 11.7% 60.9% 63.4% 65.6% 45.5% 44.2% 45.6% OGDC

42% 38% 34% 20.6% 17.1% 12.4% 60.1% 61.5% 62.2% 43.8% 44.0% 44.6% PPL

35% 41% 39% 19.6% 16.2% 16.4% 63.8% 65.6% 67.4% 34.3% 43.8% 44.2% POL

14% 15% 15% -6.5% 1.4% 1.9% 26.1% 31.1% 30.9% 24.2% 25.0% 25.0% PTC

42% 47% 46% 22.5% 5.3% 7.4% 20.8% 20.0% 18.8% 15.8% 17.5% 15.8% FFC

19% 14% 13% 12.4% 13.4% 8.8% 17.3% 16.2% 15.0% 13.4% 11.9% 11.5% ENGRO

30% 42% 38% -16.8% 49.6% 35.1% 30.8% 32.1% 21.6% 22.7% 22.6% 15.2% FFBL

47% 54% 61% 25.0% 20.0% 20.0% 11.4% 11.9% 13.3% 6.0% 6.6% 7.7% NESTLE

92% 91% 93% 17.9% 20.0% 18.8% 11.4% 10.6% 10.2% 7.1% 6.4% 6.3% ULEVER

22% 32% 24% 17.3% 19.2% 7.1% 2.2% 3.1% 2.3% 1.3% 1.7% 1.3% PSO

7% 18% 19% -1.9% 14.6% 5.0% 0.8% 2.8% 2.9% 0.6% 1.5% 1.5% SHEL

27% 16% 15% 55.5% 45.3% 19.7% 24.5% 24.6% 27.3% 20.3% 14.6% 15.9% LUCK

5% 5% 7% -19.3% 79.1% 17.7% 29.0% 24.2% 26.3% 25.3% 14.9% 18.4% DGKC

23% 26% 26% 28.5% 10.5% 14.4% 29.1% 33.4% 34.3% 17.9% 21.2% 22.2% ACPL

17% 20% 19% -20.9% 19.1% 7.1% 30.4% 34.8% 35.1% 19.1% 21.4% 23.2% FCCL

8% 17% 19% 3.6% 22.8% 12.0% 12.9% 19.4% 22.9% 7.3% 13.8% 16.1% CHCC

26% 26% 26% -4.1% 3.2% 2.2% 25.7% 26.0% 25.6% 15.9% 15.3% 15.5% KAPCO

9% 10% 11% 12.1% -1.3% 0.6% 13.2% 13.4% 13.8% 8.5% 9.7% 10.5% HUBC

22% 20% 19% 14.2% 26.4% 3.0% 9.8% 9.4% 10.1% 5.7% 5.0% 5.9% PSMC

34% 31% 29% 22.2% 20.3% 16.2% 8.9% 8.2% 8.0% 6.4% 5.9% 5.7% INDU

-9% 4% 6% -33.5% 14.5% 21.1% -1.5% 2.1% 2.0% -1.6% 0.8% 1.1% HCAR

16% 18% 18% 6.0% 4.2% 12.9% 4.5% 4.9% 5.0% 2.3% 2.9% 2.8% SNGP

3% 16% 18% 6.3% 16.7% 10.9% 4.4% 5.1% 5.4% 0.4% 2.2% 2.4% SSGC

57% 25% 23% 20.0% 17.5% 18.1% 86.6% 43.4% 41.7% 69.6% 32.0% 30.9% AICL

16% 17% 18% 12.5% 8.7% 7.4% 14.0% 15.3% 15.5% 8.3% 9.0% 9.2% ICI

12% 13% 14% 4.6% 28.7% 19.4% 10.5% 10.3% 13.4% 13.8% 12.0% 11.7% PKGS

6% 5% 6% 4.6% 11.4% 9.4% 8.8% 9.5% 10.1% 9.7% 8.9% 10.0% NML

9% 10% 11% 12.9% 0.0% 6.6% 7.7% 7.8% 8.0% 3.7% 4.5% 4.9% GADT

35% 36% 35% 10.8% 11.3% 9.3% 17.7% 18.7% 18.8% 14.2% 14.5% 14.4% AGTL

27% 24% 22% 2.5% 4.3% 5.1% 9.8% 9.7% 9.8% 7.7% 7.7% 7.7% MTL

24% 22% 20% 12.8% 12.9% 9.4% 17.9% 17.2% 16.9% 11.1% 10.9% 10.7% THALL

18% 23% 25% 22.5% 27.7% 17.2% 35.1% 37.8% 40.0% 15.8% 18.9% 21.7% PICT

ROE Revenue Growth Operating Margin Net Margin

Source: Company Reports & AKD Estimates

AKD Universe Companies - Valuation Data

23

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Sectors

24

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Commercial Banks

Beyond Provisioning!

Advances growth, at an estimated 5% in CY07 has been sharply slower this year. Depositshowever, have continued to show solid growth, at 30%YoY in 3QCY07. Going forward, the bankingsector is well poised to take advantage of expected demand pickup from the corporate side whilethe potential in SME and consumer financing is high as well.

The banking sector was again one of the better performers in the Pakistani market in 2007, itsmarket cap growing by 48.6%YoY. On a relative basis, the listed banking sector outperformed thebenchmark KSE-100 Index by 8.6%YoY in 2007.

The Forced Sale Value (FSV) regulation, while reducing systemic risk in the banking system willlead to one-off higher provisions in 2007 confining sector EPS growth to 7% We expect the bottomline to make a strong comeback next year with estimated EPS growth of 26% in CY08. .

The AKD Banking Universe is trading at a CY08 Tier-I P/B of 3.0x and PER of 10.8x, againstmarket CY08 P/B of 2.6x and PER of 10.55x. We remain Overweight on the banking sector inview of attractive growth opportunities. Our top picks are HBL and BAFL with upsides of 50.6%and 41.2% to their respective target prices of PkR355 and PkR76.10.

Sector Valuation & Relative Performance

Banking - Valuation Multiples

Sector Market cap. (US$mn) 12,8391M 3M 6M 12M

Absolute (%) 1.5 (0 .9) (3.2) 48.6Rel. Index (%) (0.1) (2 .0) (6.0) 8.6

PkR/USD61.25

Banking Sector vs KSE-100 Index

-8%

3%

14%

25%

36%

47%

Dec-06 Mar-07 Jun-07 Sep-07 Jan-08

KSE-100 Index Commercial Banks

Companies Covered

AKBL BAFL HBL UBL ABL

MCB NBP (Under Restriction)

CY06A CY07E CY08F CY09FEPS (PkR) 13.83 14.76 18.63 21.28EPS growth 42% 7% 26% 14%PER (x) 14.5 13.6 10.8 9.4Tier I BVS (PkR) 44.7 52.4 66.5 82.7PB (Tier I) (x) 4.5 3.8 3.0 2.4PB (Total Equity) (x) 3.6 3.2 2.6 2.1ROE/PB Tier-I (x) 8.2 7.9 10.4 11.7Loan to Deposit 71% 66% 69% 71%Market Cap to Deposits 42% 37% 34% 31%Growth in Loan Book 17% 7% 13% 11%Cost/Income 39% 41% 37% 36%ROE (Tier-I) 37% 30% 31% 29%ROE (Total Equity) 28% 25% 26% 25%ROA 2.5% 2.3% 2.6% 2.7%Sec. Topline Inc. as % of AKD Universe 14% 15% 15% 15%Sector NPAT as % of AKD Universe 29% 31% 33% 34%

33.3% weight in KSE-100 Index

25

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Oil & Gas Exploration

Fast Track Development!

The E&P sector gained 7.3%YoY in absolute terms and thus underperformed the benchmarkKSE-100 Index by 33% during CY07.

Going forward, we expect the sector to outperform against the market as exploration activity picksups and subsequent discovery news flow comes in, especially in an environment of record highoil prices.

For FY08, we expect the Exploration and Production sector to post a bottomline growth of 19%YoYthrough fast track development of new discoveries, production ramp ups from company portfoliosand higher price environment. We recommend OGDC as our top pick on the back of managementefficacy, offering an upside of 20.6% to our target price of PkR146.50.

The E&P sector trades at a forward PER of 9.5x which is at discount to the market multiple of10.55x. The sector also offers an attractive dividend yield of 7% against the market's averagedividend yield of 5%.

We remain Overweight on the sector, and believe that, given E&P sector’s 2nd highest weight inthe KSE-100 Index, its performance will underpin index performance in 2008. .

Sector Valuation & Relative Performance

E&P Sector - Valuation Multiples

Sector Market Cap. (US$mn) 12,8391M 3M 6M 12M

Absolute (%) (0.7) (2.5) 1.1 7.3Rel. Index (%) (2.3) (3.6) (1.7) (32.7)

FY06A FY07A FY08F FY09FEPS (PkR) 12.47 13.08 15.57 17.93EPS growth 45% 5% 19% 15%PER (x) 11.9 11.3 9.5 8.2ROE 47% 44% 43% 41%ROA 35% 33% 34% 34%BVS (PkR) 26.6 29.7 36.3 43.9P/BVS (x) 5.6 5.0 4.1 3.4CFS (PkR) 14.4 14.1 19.0 21.2P/CFS (x) 10.3 10.5 7.8 7.0DPS (PkR) 9.0 10.3 10.4 12.0Dividend yield 6% 7% 7% 8%Payout Ratio 72% 79% 67% 67%EV/EBITDA (x) 7.03 5 .78 5.01 4 .29Sector Sales as % of AKD Universe 10% 10% 10% 11%Sector NPAT as % of AKD Universe 31% 33% 32% 34%

PkR/USD61.25

E&P Sector vs KSE-100 Index

-10%

1%

12%

23%

34%

45%

Dec-06 Mar-07 Jun-07 Sep-07 Jan-08

KSE-100 Index Oil & Gas Expl

Companies Covered

OGDC PPL POL - Under review

21.0% weight in KSE-100 Index

26

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Fertilizer

Strong prices looking for volumetric growth

The fertilizer sector gained 36.7% over the past one year, but was still short of the index’s gainof 40%YoY. While Engro and FFBL performed above the market, FFC, the sector heavy weight,pulled the average down.

With 19.2% outperfromance relative to the index, Engro has been the main driver for the overallsector’s performance followed by FFBL which generated interest on the back of the company’sDAP expansion plans combined with continuously increasing DAP prices. FFC, with its defensivenature was sidelined by investors looking for growth in 2007.

Sector’s performance in CY08 is l ikely to be a function of strong DAP and urea prices withexpansions likely to drive volumetric growth in a supply starved sector. With an additional advantageof being well diversified, Engro is likely to dominate the sector’s performance on the back ofnewsflow regarding separate listing of Engro Polymer and Engro Foods. .

Fertilizer sector trades at a marginal premium to the index, which we believe is justified owingto sector average dividend yield of 7.7% as well as 21%YoY earnings growth in CY08 whichshould lead to outperformance against the market in CY08. We remain overweight on the sector.

Sector Valuation & Relative Performance

Fertilizer Sector - Valuation MultiplesCY06A CY07E CY08F CY09F

EPS (PkR) 5.94 6.93 8 .36 8.09EPS growth 0% 17% 21% -3%PER (x) 15.8 13.5 11.2 11.6ROE 31% 30% 31% 29%ROA 14% 14% 14% 12%BVS (PkR) 19.0 22.9 26.9 27.9P/BVS (x) 4.9 4.1 3.5 3.4CFS (PkR) 2.0 7.6 8.4 6.1P/CFS (x) 46.9 12.4 11.2 15.5DPS (PkR) 5.6 5.8 7.2 6.8Dividend yield 5.9% 6.2% 7.7% 7.3%Payout Ratio 94% 84% 87% 84%EV/EBITDA (X) 10.0 8.1 7.9 6.9Sector Sales as % of AKD Universe 4% 4% 4% 5%Sector NPAT as % of AKD Universe 5% 5% 5% 5%

Sector Market cap. (US$mn) 3,030 1M 3M 6M 12M

Absolute (%) (3.3) (5 .2) 3 .9 36.7Rel. Index (%) (4.9) (6 .3) 1 .1 (3.3)

PkR/USD61.25

Fertilizer Sector vs KSE-100 Index

-10%

1%

12%

23%

34%

45%

Dec-06 Mar-07 Jun-07 Sep-07 Jan-08

KSE-100 Index Fertilizer

Companies Covered

ENGRO FFBL FFC

5.0% weight in KSE-100 Index

27

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Telecom Sector

Harder the fall, faster the rise!

The telecom sector underperformed the index by 50% over the past one year, making it the worstperforming major sector in the KSE-100.

PTCL has been marred by disappointing quarterly results on the back of plunging fixed line revenues.The company saw a continuous decline in not only its topline but also its bottomline which had beenhit by high bad debt provisioning as well as Technical Assistance fee of 3% of Revenues. .

We believe that PTCL’s earnings are likely to trough in 2008 because of declining fixed line revenuesand also owing to PkR17bn worth of VSS payments, which should translate into an EPS of PkR3.21for FY08. However, efficiency gains are likely to start positively impacting the bottomline from 1HFY09onwards which should be further supported with growth in i ts cellular subsidiary. .

While the company may seem expensive on FY08 valuations (PER:13.03x), we consider this atransition phase and believe investors still need to price in the impact of broadband, VSS and Ufoneinto its stock price. However, except for its cellular subsidiary, Ufone, other initiatives are unlikelyto fully show their positive impact on the bottom line until FY10.

Sector Valuation & Relative Performance

Telecom Sector - Valuation MultiplesFY06A FY07A FY08F FY09F

EPS (PkR) 4.07 3.07 3.21 3.27EPS growth -22% -25% 5% 2%PER (x) 10.27 13.65 13.03 12.79ROE 20% 14% 15% 15%ROA 14% 9% 10% 10%BVS (PkR) 20.7 21.2 21.6 22.1P/BVS (x) 2.0 2.0 1.9 1.9CFS (PkR) 6.9 6.9 4.1 5.5P/CFS (x) 6.1 6.1 10.2 7.6DPS (PkR) 5.0 2.0 2.8 2.8Dividend yie ld 11.9% 4.8% 6.6% 6.6%Payout Ratio 123% 65% 86% 84%EV/EBITDA (X) 4.5 6.1 5.6 5.7Sector Sales as % of AKD Universe 5% 4% 4% 3%Sector NPAT as % of AKD Universe 10% 7% 6% 6%

Sector Market Cap. (US$mn) 3,1211M 3M 6M 12M

Absolute (%) (5.3) (25.0) (26.9) (9.8)Rel. Index (%) (6.9) (26.1) (29.7) (49.8)

PkR/USD61.25

PTC vs KSE-100 Index

-15%

-5%

5%

15%

25%

35%

45%

Dec-06 Mar-07 Jun-07 Sep-07 Jan-08

KSE-100 Index Telecom

Company Covered

PTC

4.5% weight in KSE-100 Index

28

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Insurance

Premiums unjustified

The AKD non-life insurance sector universe handsomely outperformed the benchmark KSE-100Index by 78% during CY07 on the back of strong underwriting portfolios and favorable capitalmarket conditions.

For CY08, we expect the bottom line to contract by 46%YoY as compared with CY07. Thiscontraction is a result of a higher base effect under the head of investment income in CY07 asthe sector continued to aggressively book unrealized capital gains ahead of the exemption ofcapital gains tax expiring in CY07. Furthermore, core underwriting profitability is expected to beimpacted in CY08 following the recent acts of arson in the country.

With non-life insurance penetration at 0.5% compared with insurance penetration in emergingmarkets average of 1.3%, non-life insurers of Pakistan are poised to increase penetration byidentifying profitable opportunities and building attractive new general insurance businesses.Expectation of at least 6% real economic growth and introduction of broad retail products underpinthe likelihood of increased penetration.

The insurance sector trades at a forward CY08 PER of 14.3x versus the market PER of 10.55x.We maintain our Neutral stance on the sector.

Sector Valuation & Relative Performance

Insurance Sector - Valuation Multiples

CY06A CY07E CY08F FY09FEPS (PkR) 15.43 43.16 23.30 26.57EPS growth 36% 180% -46% 14%PER (x) 21.59 7.71 14.29 12.53ROE 42% 57% 25% 23%ROA 14% 25% 11% 11%BVS (PkR) 37.06 75.98 94.43 115.49P/BVS (x) 8.98 4.38 3.53 2.88CFS (PkR) (2.77) 8.24 5.74 10.28P/CFS (x) (120.14) 40.43 57.96 32.38DPS (PkR) 2.80 4.25 4.85 5.50Dividend yield 0.8% 1.3% 1.5% 1.7%Payout Ratio 18% 10% 21% 21%Sector Sales as % of AKD Universe 0.4% 0.4% 0.4% 0.5%Sector NPAT as % of AKD Universe 0.8% 2.1% 0.9% 1.0%

Sector Market cap. (US$mn) 2,9231M 3M 6M 12M

Absolute (%) (9.8) (10.5) 4.5 117.9Rel. Index (%) (11.3) (11.6) 1.7 77.8

PkR/USD61.25

AICL vs KSE-100 Index

-15%

15%

45%

75%

105%

135%

165%

Dec-06 Mar-07 Jun-07 Sep-07 Jan-08

KSE-100 Index Insurance

Company Covered

AICL

4.0% weight in KSE-100 Index

29

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Consumer Wave!

Sector Valuation & Relative Performance

FMCGs

Sector Market cap. (US$mn) 2,6331M 3M 6M 12M

Absolute (%) (0.7) 10.3 15.1 50.4Rel. Index (%) (2.2) 9.1 12.3 10.4

FMCGs - Valuation MultiplesCY06A CY07E CY08F CY09F

EPS (PkR) 51.28 57.99 69.72 90.14EPS growth 9% 13% 20% 29%PER (x) 38.14 33.73 28.06 21.70ROE 69% 63% 67% 71%ROA 16% 15% 16% 18%BVS (PkR) 74.37 91.96 104.28 126.29P/BVS (x) 26.30 21.27 18.76 15.49CFS (PkR) 64.04 40.80 91.07 58.79P/CFS (x) 30.54 47.95 21.48 33.27DPS (PkR) 31.52 49.67 62.35 72.75Dividend yield 1.6% 2.5% 3.2% 3.7%Payout Ratio 61% 86% 89% 81%EV/EBITDA (x) 1.4 1.4 0.9 12.4Sector Sales as % of AKD Universe 3% 3% 4% 4%Sector NPAT as % of AKD Universe 1% 2% 2% 2%

PkR/USD61.25

FMCGs Sector vs KSE-100 Index

-10%

1%

12%

23%

34%

45%

56%

67%

78%

Dec-06 Mar-07 Jun-07 Sep-07 Jan-08

KSE-100 Index FMCGs

Riding the consumer wave, the FMCG sector was able to outperform the index by 10.4%. In absoluteterms the sector gained 50.4%.

The sector’s performance was mainly led by Unilever and Nestle which reported an impressivegrowth of 32%YoY in their combined bottomlines in 9MCY07 on the back of aggressive marketingand deeply penetrating distribution network.

Going forward, we expect the FMCG sector to continue marketing aggressively which can slightlyimpact operating margins but will continue to pay off in terms of increasing topline going forward.For CY08, we expect the FMCG sector to report a bottomline growth of 20%. .

While the sector may seem expensive on valuations when compared to the AKD universe valuations,it still trades at a discount to its regional counterparts. The fact that FMCG sector has an RoE of67% and and companies like Unilever and Nestle are perceived to be run on global managementstandards justify the sector’s premium to the market valuations. While Nestle trades near our fairvalue, at current price, Unilever is our top pick with a fair value of PkR2,472. .

Companies Covered

NESTLE ULEVER

3.9% weight in KSE-100 Index

30

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

OMCs

The year of Inventory Gains!

The Oil Marketing Sector gained 28.2%YoY in absolute terms; however the sector underperformedthe KSE-100 by 11.8% in 2007.

Over the past three months, the OMC sector has outperformed the KSE-100 by 6% on the backof growth witnessed in overall sales volumes and expectations of windfall inventory gains due torising international and refined product prices.

Volume growth is the key long term driver in the OMC Sector where we estimate a 3-year volumeCAGR of 7% with PSO as our top pick offering an upside of 12.7% to our target price of PkR469.5.Our liking for PSO is premised upon volume outperformance through aggressive retail level initiativesand long term industrial supply contracts, particularly for power sector as well as several largeprojects expected to commence in CY09.

On estimated FY08 EPS, the sector is trading at 10.31x which is slightly below the market multipleof 10.55x. On forward P/BVS, the sector is at a slight premium trading at 2.85x versus the marketFY08 P/BVS of 2.6x. We maintain our Overweight stance on the sector.

Overweight

Sector Valuation & Relative Performance

OMCs Sector - Valuation MultiplesFY06A FY07A FY08F FY09F

EPS (PkR) 46.98 23.85 40.40 35.01EPS growth 31% -49% 69% -13%PER (x) 8.87 17.47 10.31 11.90ROE 34% 18% 28% 22%ROA 11% 5% 7% 6%BVS (PkR) 136.85 134.33 146.33 155.82P/BVS (x) 3.04 3.10 2.85 2.67CFS (PkR) 10.71 16.92 16.02 53.87P/CFS (x) 38.90 24.63 26.01 7.73DPS (PkR) 33.03 19.79 22.00 24.48Dividend yie ld 7.9% 4.7% 5.3% 5.9%Payout Ratio 70% 83% 54% 70%EV/EBITDA (x) 6 .2 11.9 6.2 7 .6Sector Sales as % of AKD Universe 30% 30% 31% 30%Sector NPAT as % of AKD Universe 5% 3% 4% 3%

Sector Market Cap. (US$mn) 2,8881M 3M 6M 12M

Absolute (%) (2.6) 7.3 1.4 28.2Rel. Index (%) (4.2) 6.1 (1 .4) (11.8)

PkR/USD61.25

OMCs Sector vs KSE-100 Index

-5%

5%

15%

25%

35%

45%

Dec-06 Mar-07 Jun-07 Sep-07 Jan-08

KSE-100 Index OMCs

Companies Covered

PSO SHEL

3.3% weight in KSE-100 Index

31

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Cement

Light at the end of the tunnel

Even though the cement sector has underperformed the index over the past three months by 17%,it managed to report outperformance of 15.1% against the index for 2007 as a whole. .

The sector’s performance has been a function of cement prices as well as newsflow regardingcement export to India. After the resumption of price agreement in Feb 07, stock prices began tomove up, resulting in the overall sector perfromance outpacing index performance in 1HCY07.However decline in output prices followed by disappointing 1QFY08 results dampened the sector’sperformance in 2HCY07.

Cement prices have started moving upwards again from Oct/Nov 2007, driving interest back intothe sector. We believe that price concensus among manufacturers combined with greater exportopportunities on the export front should drive the sector’s earnings in CY08. .

The sector trades at a PER of 10.52x, which is at a slight discount to the market PER of 10.55x.The sector trades at a cheap EV/MT of US$82.36 and FY08 P/B of 1.1x, 58% discount to themarket P/B of 2.64x.

Sector Valuation & Relative Performance

Cement Sector - Valuation MultiplesFY06A FY07A FY08F FY09F

EPS (PkR) 5.47 3.60 5.05 6.67EPS growth 60% -34% 40% 32%PER (x) 9.71 14.77 10.52 7.96ROE 20% 9% 11% 12%ROA 9% 5% 6% 8%BVS (PkR) 27.7 39.6 46.5 54.5P/BVS (x) 1.9 1 .3 1.1 1.0CFS (PkR) 8.3 3 .4 6.4 8.1P/CFS (x) 6.4 15.8 8.3 6.6DPS (PkR) 1.6 0 .7 1.7 2.0Dividend yield 2.9% 1.3% 3.3% 3.8%Payout Ratio 28% 20% 35% 30%EV/EBITDA (x) 6.20 8.52 6.27 5.42Sector Sales as % of AKD Universe 3% 2% 3% 3%Sector NPAT as % of AKD Universe 4% 3% 3% 4%

Sector Market Cap. (US$mn) 2,3841M 3M 6M 12M

Absolute (%) (3.3) (15.9) (19.0) 55.1Rel. Index (%) (4.9) (17.0) (21.8) 15.1

PkR/USD61.25

Cement Sector vs KSE-100 Index

-20%

-5%

10%

25%

40%

55%

70%

Dec-06 Mar-07 Jun-07 Sep-07 Jan-08

KSE-100 Index Cement

Companies Covered

ACPL CHCC DGKC FCCL

LUCK MLCF PIOC

3.2% weight in KSE-100 Index

32

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Power Generation

Horizon of the expansion chapter!

The AKD Universe power sector gained 18.8%YoY in absolute terms but underperformed thebenchmark KSE-100 Index by 21.2% in CY07.

For FY08, we forecast the sector to post a bottomline growth of 4%YoY in line with pre-definedtariff structures.

Pakistan's electricity infrastructure is under tremendous pressure with power consumption expectedto grow at 8%-9% p.a. The existing demand and supply gap in power consumption is estimatedto grow at 1,000MW/year and is expected to reach approximately 5,550MW by CY10 unless newgeneration capacity is brought on line on a fast-track basis.

We are now beginning to see some real signs of investment activity in the power sector with therecent signing of Implementation Agreements (IAs) with seven companies totaling 1,210MWs ofpower generation capacity and financial close by six companies. This brightens expansion prospectsfor companies under our coverage.

The power sector trades at a forward FY08 PER of 10.08x versus the market at 10.55x and providesa dividend yield of 9.6%. We maintain our Overweight stance on the sector. .

Sector Valuation & Relative Performance

Power Sector - Valuation MultiplesFY06A FY07A FY08F FY09F

EPS (PkR) 3.97 3.75 3.92 4.12EPS growth -40% -5% 4% 5%PER (x) 9.95 10.53 10.08 9.58ROE 16% 16% 16% 17%ROA 10% 10% 11% 12%BVS (PkR) 24.59 23.62 23.76 24.18P/BVS (x) 1.61 1.67 1.66 1.63CFS (PkR) 6.88 4.08 5.27 5.44P/CFS (x) 5.74 9.69 7.49 7.26DPS (PkR) 5.26 4.21 3.79 3.97Dividend yie ld 13.3% 10.7% 9.6% 10.1%Payout Ratio 133% 112% 97% 96%EV/EBITDA (x) 4 .8 4.6 5.3 5.9Sector Sales as % of AKD Universe 4.4% 4.1% 3.5% 3.3%Sector NPAT as % of AKD Universe 3.9% 3.6% 3.2% 3.0%

Sector Market Cap. (US$mn) 1,7911M 3M 6M 12M

Absolute (%) 0.2 (9.3) (15.7) 18.8Rel. Index (%) (1.4) (10.4) (18.5) (21.2)

PkR/USD61.25

Power Sector vs KSE-100 Index

-6%

4%

14%

24%

34%

44%

Dec-06 Mar-07 Jun-07 Sep-07 Jan-08

KSE-100 Index Power

Companies Covered

HUBC KAPCO

2.7% weight in KSE-100 Index

33

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Autos

Shrinking margins reduce speed

Having gained by 36.6%YoY, the auto sector underperformed the index by 3.4% in CY07. Theincrease in JPY/USD and steel prices coupled with plans to lower production kept price performancelimited.

While most auto companies reported an increase in their quarterly earnings, higher input costs (fromJune onwards) drove investor interest out of the sector even as volumes posted a marginal improvementof 0.4%YoY.

We believe that the impact of JPY appreciation and higher steel prices, which is likely to becomeobvious in 4QCY07 and 1QCY08 results, is likely to be further priced in by investors. The sectorunderperformed the index by 15% over the past one month and is likely to lose more market cap.However, we think PSMC is worth looking at on the back of increasing volumes through low endmarket positioning.

Auto sector is trading at a discount to the market PER of 10.55x. However, keeping in mind higherinput costs as well as lower volumes, we expect the auto sector to underperform the index, justifyingthe discount on valuations.

Sector Valuation & Relative Performance

Auto Sector - Valuation Multiples

FY06A FY07A/E FY08F FY09FEPS (PkR) 22.17 18.43 21.93 25.91EPS growth 73% -17% 19% 18%PER (x) 8.68 10.44 8.77 7 .42ROE 34% 22% 21% 21%ROA 14% 11% 11% 11%BVS (PkR) 65.73 83.23 102.28 124.80P/BVS (x) 2.93 2 .31 1.88 1 .54CFS (PkR) (14.33) 17.44 21.87 25.77P/CFS (x) (13.42) 11.03 8.79 7 .46DPS (PkR) 3.12 3 .38 4.74 5 .46Dividend yield 1.6% 1.8% 2.5% 2.8%Payout Ratio 14% 18% 22% 21%EV/EBITDA (x) 3.6 4.0 3.3 3.1Sector Sales as % of AKD Universe 7.8% 7.4% 7.8% 7.9%Sector NPAT as % of AKD Universe 3.2% 2.7% 2.6% 2.8%

Sector Market Cap. (US$mn) 1,6041M 3M 6M 12M

Absolute (%) (13.7) (11.2) (6.7) 36.6Rel. Index (%) (15.3) (12.3) (9.5) (3.4)

PkR/USD61.25

Autos Sector vs KSE-100 Index

-6%

4%

14%

24%

34%

44%

54%

64%

74%

Dec-06 Mar-07 Jun-07 Sep-07 Jan-08

KSE-100 Index Autos

Companies Covered

HCAR INDU PSMC

1.6% weight in KSE-100 Index

34

AKD Securities LimitedJanuary 2008 Pakistan Market: 2007 - 2008

Capex to lead earnings growth!

Sector Valuation & Relative Performance

Gas T&D

Gas T&D - Valuation Multiples