Paints Industry Report June 15, 2011 SPA Securities Ltd.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Paints Industry ReportJune 15, 2011

SPA Securities Ltd.

Executive Summary : 01 - 01

Industry Description : 02 - 05

Asian Paints : 07 - 12

Akzo Nobel : 14 - 19

Kansai Nerolac : 21 - 26

Berger Paints : 28 - 33

C o n t e n t s

1

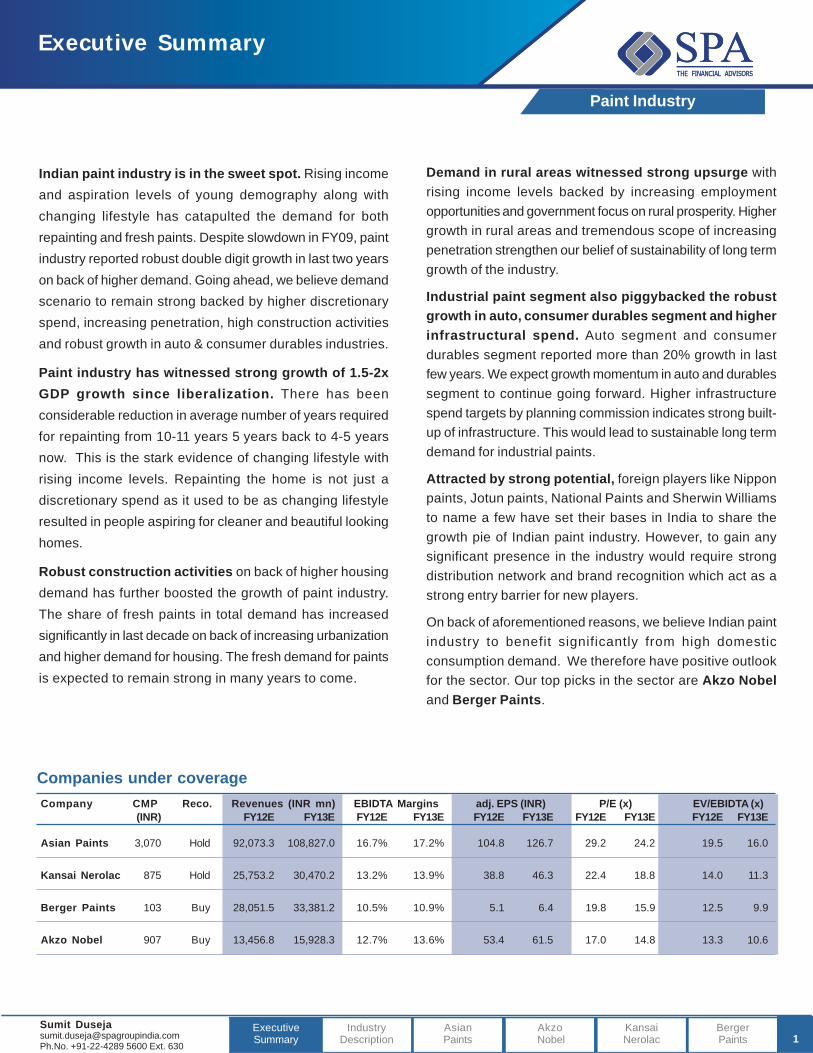

Indian paint industry is in the sweet spot. Rising incomeand aspiration levels of young demography along withchanging lifestyle has catapulted the demand for bothrepainting and fresh paints. Despite slowdown in FY09, paintindustry reported robust double digit growth in last two yearson back of higher demand. Going ahead, we believe demandscenario to remain strong backed by higher discretionaryspend, increasing penetration, high construction activitiesand robust growth in auto & consumer durables industries.

Paint industry has witnessed strong growth of 1.5-2xGDP growth since liberalization. There has beenconsiderable reduction in average number of years requiredfor repainting from 10-11 years 5 years back to 4-5 yearsnow. This is the stark evidence of changing lifestyle withrising income levels. Repainting the home is not just adiscretionary spend as it used to be as changing lifestyleresulted in people aspiring for cleaner and beautiful lookinghomes.

Robust construction activities on back of higher housingdemand has further boosted the growth of paint industry.The share of fresh paints in total demand has increasedsignificantly in last decade on back of increasing urbanizationand higher demand for housing. The fresh demand for paintsis expected to remain strong in many years to come.

Demand in rural areas witnessed strong upsurge withrising income levels backed by increasing employmentopportunities and government focus on rural prosperity. Highergrowth in rural areas and tremendous scope of increasingpenetration strengthen our belief of sustainability of long termgrowth of the industry.

Industrial paint segment also piggybacked the robustgrowth in auto, consumer durables segment and higherinfrastructural spend. Auto segment and consumerdurables segment reported more than 20% growth in lastfew years. We expect growth momentum in auto and durablessegment to continue going forward. Higher infrastructurespend targets by planning commission indicates strong built-up of infrastructure. This would lead to sustainable long termdemand for industrial paints.

Attracted by strong potential, foreign players like Nipponpaints, Jotun paints, National Paints and Sherwin Williamsto name a few have set their bases in India to share thegrowth pie of Indian paint industry. However, to gain anysignificant presence in the industry would require strongdistribution network and brand recognition which act as astrong entry barrier for new players.

On back of aforementioned reasons, we believe Indian paintindustry to benefit significantly from high domesticconsumption demand. We therefore have positive outlookfor the sector. Our top picks in the sector are Akzo Nobeland Berger Paints.

Company CMP Reco. Revenues (INR mn) EBIDTA Margins adj. EPS (INR) P/E (x) EV/EBIDTA (x)(INR) FY12E FY13E FY12E FY13E FY12E FY13E FY12E FY13E FY12E FY13E

Asian Paints 3,070 Hold 92,073.3 108,827.0 16.7% 17.2% 104.8 126.7 29.2 24.2 19.5 16.0

Kansai Nerolac 875 Hold 25,753.2 30,470.2 13.2% 13.9% 38.8 46.3 22.4 18.8 14.0 11.3

Berger Paints 103 Buy 28,051.5 33,381.2 10.5% 10.9% 5.1 6.4 19.8 15.9 12.5 9.9

Akzo Nobel 907 Buy 13,456.8 15,928.3 12.7% 13.6% 53.4 61.5 17.0 14.8 13.3 10.6

Companies under coverage

Executive Summary

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

Sumit [email protected]. +91-22-4289 5600 Ext. 630

Paint Industry

Industry Description

Currently estimated at ~INR 210bn, Indian paint industry hasgrown at a CAGR of ~18.5% in last two years and expected togrow at a CAGR of ~17.5% in next four years to become INR396bn industry in FY15. Indian paint industry growth is closelyrelated with the GDP growth rate and has grown on an average1.5-2x GDP growth rate since liberalization.

Industry Size (INR Bn)

Source: Industry, SPA Research

Industry vs GDP Growth

0%

5%

10%

15%

20%

25%

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12E FY13E

Industry Grow th GDP Grow th

Source: SPA Research

Industry StructureOrganized vs UnorganizedIndian paint industry is dominated by organized sector whichcurrently captures ~67% market share. Organized sector hasgrown at a higher rate vis-à-vis unorganized sector in last fewyears. Unorganized sector mostly offers lower end productslike low end enamels, distempers, lime wash, cement paintetc. Rising disposable income and created awareness frommarketing efforts by organized players resulted in consumerspreferring for better quality and higher end products likeemulsions.

Decorative vs. IndustrialIndian paint industry can be classified into decorative andindustrial paints with the market share in the ratio 80:20.

Decorative Paints (INR ~170bn)General product wise paint classification:

• Premier decorative paints are water based acrylic emulsionsused mostly in metros and other large cities and high end offices

• The medium range consists of solvent based enamels whichare popular in smaller cities and towns

• Distempers are economy products demanded in the semi-urban and rural markets. This segment is dominated byunorganized sector. Margins of distemper lie betweenemulsions and enamels.

In decorative paints segment solvent based paints (enamels)has a larger share of ~33% but there is a significant change intrend towards adopting premium water based paints (emulsions)which are growing at much faster rates of ~20% in volumeterms in last 4-5 years. In emulsions, exterior emulsions aregrowing faster than interior emulsions.

Decorative Paints Breakup (%)

33%

15%

6%

4%

4%

13%

14%12%

Enamels

Interior Emulsions

Exterior Emulsions

Distemper

Cement Paint

Wood Finishes

Putty

Primers, Thinners etc

Source: AC Neilson, SPA Research

Traditionally repainting has dominated the demand for decorativepaints but higher construction activities on back of demand forhousing space has resulted in higher growth for new paintingdemand. Share of fresh demand for paints has increased to~30% currently from ~15% a decade ago.

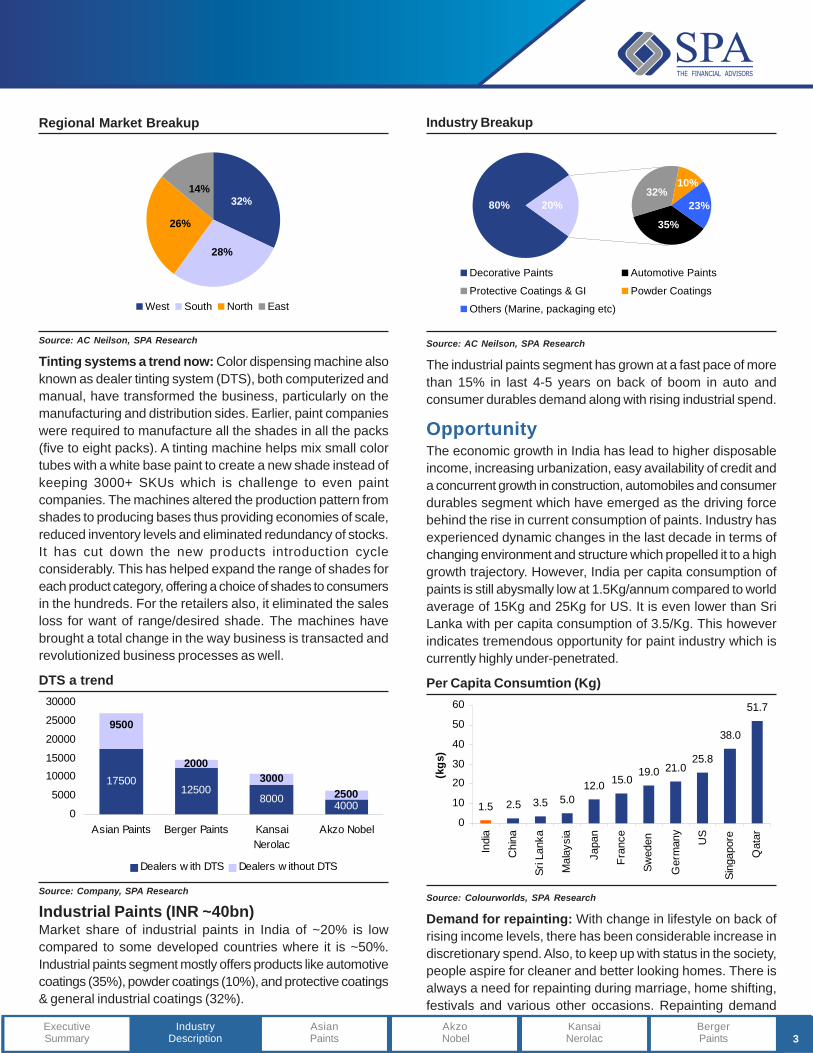

Region-wise classification:Region-wise, West region market accounts for 32% of paintindustry revenues followed by South (28%), North (26%) andEast (14%) in order (Chart). Rural regions and smaller townscontribute 40% of the paint industry sales. Growth in Tier IIand Tier III cities is higher than the growth in urban marketsdue to higher construction activities and increasing rural income.

120

137

148

170 208

396

050

100150200250300350400450

FY07 FY08 FY09 FY10 FY11 FY15

(INR

Bn)

CAGR = 14.7%

CAGR

= 17.

5%

Paint Industry

2Industry

DescriptionAsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

3

Regional Market Breakup

32%14%

28%

26%

West South North East

Source: AC Neilson, SPA Research

Tinting systems a trend now: Color dispensing machine alsoknown as dealer tinting system (DTS), both computerized andmanual, have transformed the business, particularly on themanufacturing and distribution sides. Earlier, paint companieswere required to manufacture all the shades in all the packs(five to eight packs). A tinting machine helps mix small colortubes with a white base paint to create a new shade instead ofkeeping 3000+ SKUs which is challenge to even paintcompanies. The machines altered the production pattern fromshades to producing bases thus providing economies of scale,reduced inventory levels and eliminated redundancy of stocks.It has cut down the new products introduction cycleconsiderably. This has helped expand the range of shades foreach product category, offering a choice of shades to consumersin the hundreds. For the retailers also, it eliminated the salesloss for want of range/desired shade. The machines havebrought a total change in the way business is transacted andrevolutionized business processes as well.

DTS a trend

1750012500

8000 4000

20003000

2500

9500

0

5000

1000015000

20000

25000

30000

Asian Paints Berger Paints KansaiNerolac

Akzo Nobel

Dealers w ith DTS Dealers w ithout DTS

Source: Company, SPA Research

Industrial Paints (INR ~40bn)Market share of industrial paints in India of ~20% is lowcompared to some developed countries where it is ~50%.Industrial paints segment mostly offers products like automotivecoatings (35%), powder coatings (10%), and protective coatings& general industrial coatings (32%).

Industry Breakup

80% 20%32%

35%

10%

23%

Decorative Paints Automotive Paints

Protective Coatings & GI Powder Coatings

Others (Marine, packaging etc)

Source: AC Neilson, SPA Research

The industrial paints segment has grown at a fast pace of morethan 15% in last 4-5 years on back of boom in auto andconsumer durables demand along with rising industrial spend.

OpportunityThe economic growth in India has lead to higher disposableincome, increasing urbanization, easy availability of credit anda concurrent growth in construction, automobiles and consumerdurables segment which have emerged as the driving forcebehind the rise in current consumption of paints. Industry hasexperienced dynamic changes in the last decade in terms ofchanging environment and structure which propelled it to a highgrowth trajectory. However, India per capita consumption ofpaints is still abysmally low at 1.5Kg/annum compared to worldaverage of 15Kg and 25Kg for US. It is even lower than SriLanka with per capita consumption of 3.5/Kg. This howeverindicates tremendous opportunity for paint industry which iscurrently highly under-penetrated.

Per Capita Consumtion (Kg)

1.5 2.5 3.5 5.0

12.0 15.019.0 21.0

25.8

38.0

51.7

0

10

20

30

40

50

60

Indi

a

Chi

na

Sri L

anka

Mal

aysi

a

Japa

n

Fran

ce

Swed

en

Ger

man

y

US

Sing

apor

e

Qat

ar

(kgs

)

Source: Colourworlds, SPA Research

Demand for repainting: With change in lifestyle on back ofrising income levels, there has been considerable increase indiscretionary spend. Also, to keep up with status in the society,people aspire for cleaner and better looking homes. There isalways a need for repainting during marriage, home shifting,festivals and various other occasions. Repainting demand

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

4

therefore has been transforming from more of a discretionaryspend to somewhat need based spend. Significant up-tradingtrend is visible in Tier II and Tier III cities with the shift fromlower and economy products like distempers and enamels tohigh end emulsion paints. Increase in rural income is furthersupporting the sustainability of paint industry growth rate.

Rising Income Level

71.1% 64.6%

17.4%18.6%

11.6% 16.8%

0%

20%

40%

60%

80%

100%

Year 2009 Year 2014E

High Income (> INR200000)

Middle Income (INR100000-200000)

Low Income (<INR100000)

Source: CRISIL, SPA Research

Fresh paint demand: Beside demand for new paints is alsovery strong. Indian demography is quite young with 60% ofpopulation below the age of 30 years which creates a highdemand for housing. Higher housing construction createsdemand for fresh paints in decorative segment. Based on thefindings of Ministry of Housing & Urban Poverty Alleviation,India, there is a shortfall of 24.7mn dwelling units at thebeginning of 11th Five year Plan which will increase to 26.5mnunits by the end of it. This represents high demand for housingconstruction in India.

No of Pakka Households-Urban (mn)

41.245.3

51.057.5

0

10

20

30

40

50

60

70

2001 2005 2010 2015E

(INR

mn)

Source: Ministry of Housing & Urban Poverty Alleviation, SPA Research

Industrial Paints to see high growth: Robust demand forauto (automotive coatings), consumer durables (powdercoatings) and infrastructure spend (performance/protective andgeneral industrial coatings) by private players and governmentcreates fresh demand for industrial paints.

Capacity Addition: To meet the strong ensuing demand, manypaint companies have planned huge capacity expansion in next2 years. Top four domestic companies plan to expandcapacities from cumulative 1.16mn MT in FY11 to 1.68mn MTby FY13.

Capacity (Lakh tonnes/annum)

0

200000

400000

600000

800000

1000000

Asian Paints Berger Paints KansaiNerolac

Akzo Nobel

FY11 FY13E

Source: Company, SPA Research

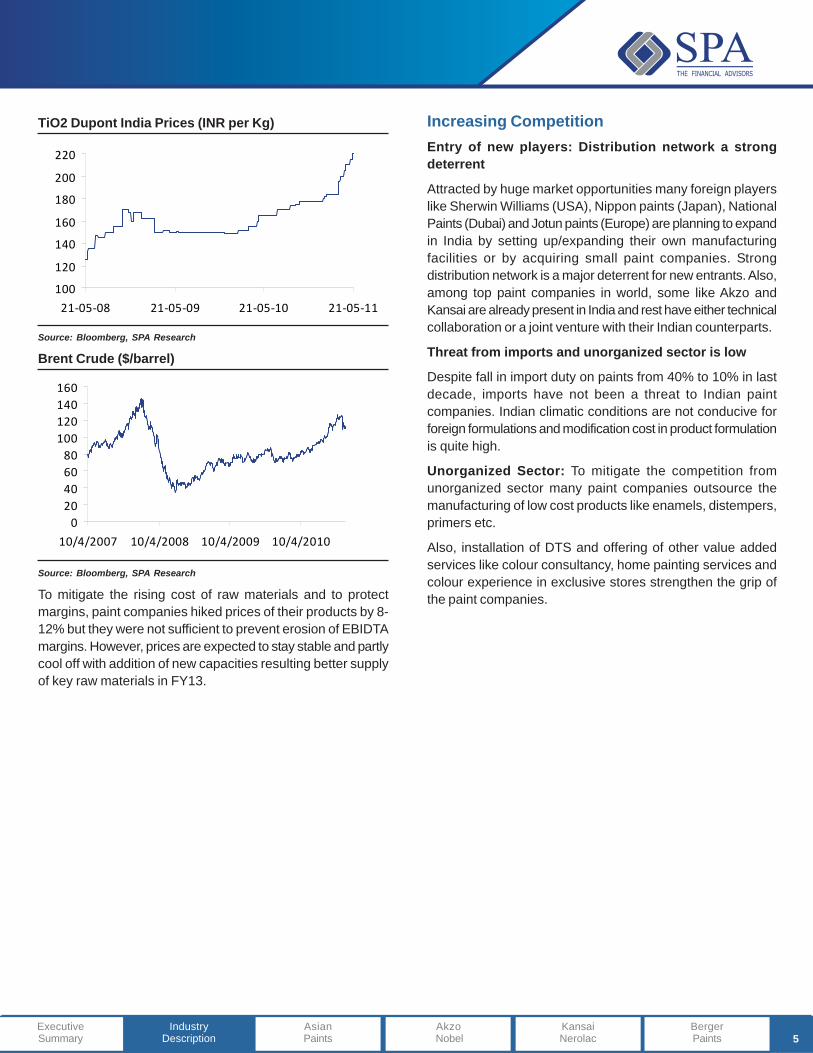

ThreatsRaw material cost inflationManufacturing of paints requires more than 300 differentingredients. Key ingredients like titanium dioxide (TiO2) andoil derivatives constitutes 15-20% and 20-40% of the of rawmaterial cost respectively. Cost of titanium dioxide is witnessinghuge rise due to supply side constraints which arose from thelack of capacity addition and slow restarting of shut down plantsafter 2008-09 recession. The Indian prices of titanium dioxidehave risen by ~29% in FY11 from 155/Kg to 200/Kg. The pricesare continuously rising and have increased by another ~10%in two months since the beginning of FY12. Crude prices havealso witnessed strong upsurge with improvement in globaleconomic environment. Crude prices have risen by ~40% fromUSD 83/barrel to USD 117/barrel in FY11.

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

5

TiO2 Dupont India Prices (INR per Kg)

100

120

140

160

180

200

220

21‐05‐08 21‐05‐09 21‐05‐10 21‐05‐11

Source: Bloomberg, SPA Research

Brent Crude ($/barrel)

020406080

100120140160

10/4/2007 10/4/2008 10/4/2009 10/4/2010

Source: Bloomberg, SPA Research

To mitigate the rising cost of raw materials and to protectmargins, paint companies hiked prices of their products by 8-12% but they were not sufficient to prevent erosion of EBIDTAmargins. However, prices are expected to stay stable and partlycool off with addition of new capacities resulting better supplyof key raw materials in FY13.

Increasing CompetitionEntry of new players: Distribution network a strongdeterrent

Attracted by huge market opportunities many foreign playerslike Sherwin Williams (USA), Nippon paints (Japan), NationalPaints (Dubai) and Jotun paints (Europe) are planning to expandin India by setting up/expanding their own manufacturingfacilities or by acquiring small paint companies. Strongdistribution network is a major deterrent for new entrants. Also,among top paint companies in world, some like Akzo andKansai are already present in India and rest have either technicalcollaboration or a joint venture with their Indian counterparts.

Threat from imports and unorganized sector is low

Despite fall in import duty on paints from 40% to 10% in lastdecade, imports have not been a threat to Indian paintcompanies. Indian climatic conditions are not conducive forforeign formulations and modification cost in product formulationis quite high.

Unorganized Sector: To mitigate the competition fromunorganized sector many paint companies outsource themanufacturing of low cost products like enamels, distempers,primers etc.

Also, installation of DTS and offering of other value addedservices like colour consultancy, home painting services andcolour experience in exclusive stores strengthen the grip ofthe paint companies.

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

This page has been intentionally left blank

Asian PaintsCMP: INR 3,070 Recommendation: HOLD Target: INR 3,168

Dominance to stayDespite increasing competition from domestic and major foreignpaint companies, Asian Paint has maintained its marketleadership and has increased its market share from ~48% inFY04 to ~54% in FY11. We expect it to maintain its dominancegoing forward with further increase in market share backed byhigher sales growth.

Maximum beneficiary of high GDP growth rateAsian Paints is having larger presence in South and Westmarkets which contribute ~60% to overall paint industry sales.Company also has strong presence in fast growing ruralmarkets which contributes ~45% to its overall revenue. Weexpect company to report revenue growth at a 2 year CAGR of19.9% to INR 90,921.2mn in FY13 in its standalone businessbacked by strong volume growth.

High competitive advantage and positioningAsian Paints offers products across all the categories in termsof types of products and customer segmentation. Emulsionwhich is the fastest growing category at ~20% volume growthcontributes ~50% of Asian paints decorative paint segment.Unmatched dealers network of ~27,000 dealers give Asianpaints high competitive advantage. With initiatives like Signaturestores, Colour Ideas, home painting solutions, company isfocusing on increasing services along with product offerings.Company's ad spends (~INR 2931mn) are highest among itspeers giving it stronger brand recall and occupy larger mindshare.

June 15, 2011

International and Industrial business to gain tractionIndustrial Segment: Asian Paints has signed a second equalJV agreement with PPG Industries Inc for Non Decorative andNon- Auto Paints in Jan 2011. The arrangement is subject toregulatory approval and is expected to be completed duringH2FY12. We expect industrial segment business to performwell on back of robust demand of automotives, consumerdurables and higher infrastructure investments.International business: International business division reporteda meager 1.9% growth in FY11 revenues on the back ofslowdown in international economies and disruptions inoperations in MENA region which contributes more than 50%to international business division. Going ahead, withimprovement in international economic environment and betteroperational efficiencies, we expect international business togrow at a 2 year CAGR of 10.2%.

ValuationsAsian paints having dominant position in paint industry is wellpoised to take maximum benefit of high GDP growth rate. Withchanging lifestyle needs, high disposable income and boom inconstruction activities, we expect Asian paints to grow at arevenue CAGR of 18.8% in the next two years. Based on highRoNW, higher EBIDTA margins and strong growth rate, we valuethe stock at 25x FY13E EPS of INR 126.7 which implies atarget price of INR 3,168. We therefore, initiate the coveragewith a Hold rating.

Asian Paints, largest decorative paint company in India has a dominant market share of more than50% in organized sector. The company has presence in 17 counties with 22 manufacturing facilities.It is one of the fastest growing FMCG companies with 4 year revenue CAGR of 20.4%. .

Shareholding (%) Dec-10 Mar-11

Promoters 52.33 52.34

FIIs 14.61 14.45

DIIS 11.38 11.56

Others 21.67 21.66

Key Data

BSE Code 500820

NSE Code ASIANPAINT

Bloomberg Code APNT IN

Reuters Code ASPN.BO

Shares Outstanding (mn) 95.9

Face Value 10

Mcap (INR bn) 294.5

52 Week H/L 3,230/2,283

2W Avg. Qty, BSE 33,512

Sensex 18,132.2

Y/E Mar (INR mn) FY09 FY10 FY11 FY12E FY13E

Net Sales 54,639.0 66,809.4 77,062.4 92,073.3 108,827.0Growth (%) 24.0% 22.3% 15.3% 19.5% 18.2%EBIDTAM (%) 12.3% 18.4% 17.0% 16.7% 17.2%Adj. PAT 3,942.4 8,292.9 8,432.4 10,052.9 12,156.7Growth (%) -4.1% 110.4% 1.7% 19.2% 20.9%Adj. PATM (%) 7.2% 12.4% 10.9% 10.9% 11.2%Adj. EPS (INR) 41.1 86.5 87.9 104.8 126.7DPS 17.5 27.0 32.0 40.0 45.0Dividend Yield (%) 0.6% 0.9% 1.0% 1.3% 1.5%P/E (x) 74.7 35.5 34.9 29.3 24.2P/BV (x) 24.5 17.2 13.5 10.7 8.5EV/EBIDTA 44.6 24.3 22.8 19.5 16.0Net Debt/Equity 0.1 0.1 0.0 0.1 0.0RoACE (%) 31.8% 52.3% 41.1% 39.4% 38.4%RoANW (%) 36.1% 56.9% 43.3% 40.8% 39.2%

Relative share price performance

8090

100110120130140150

Jun‐10

Jul‐1

0

Aug

‐10

Sep‐10

Oct‐10

Nov

‐10

Dec‐10

Jan‐11

Feb‐11

Mar‐11

Apr‐11

May‐11

Asian Paints Sensex

Paint Industry

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

Sumit [email protected]. +91-22-4289 5600 Ext. 630

7

8

Investment Rationale1) Dominance to stay

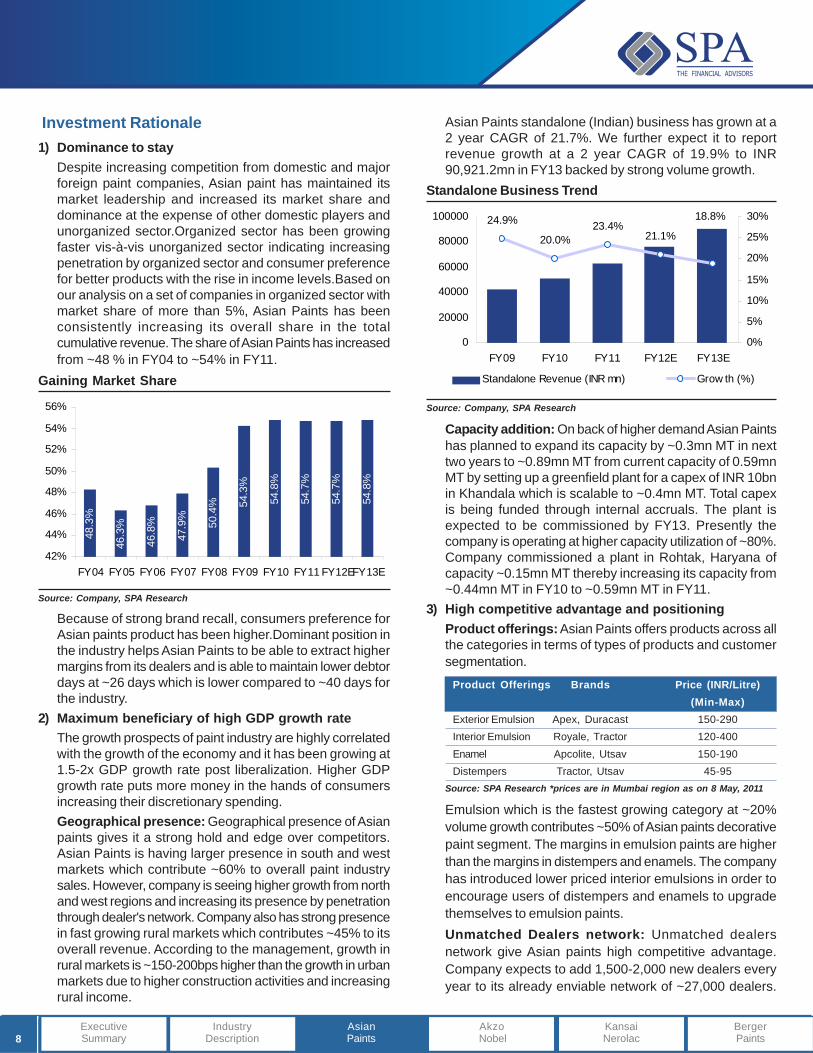

Despite increasing competition from domestic and majorforeign paint companies, Asian paint has maintained itsmarket leadership and increased its market share anddominance at the expense of other domestic players andunorganized sector.Organized sector has been growingfaster vis-à-vis unorganized sector indicating increasingpenetration by organized sector and consumer preferencefor better products with the rise in income levels.Based onour analysis on a set of companies in organized sector withmarket share of more than 5%, Asian Paints has beenconsistently increasing its overall share in the totalcumulative revenue. The share of Asian Paints has increasedfrom ~48 % in FY04 to ~54% in FY11.

Gaining Market Share

48.3

%

46.3

%

46.8

%

47.9

%

50.4

% 54.3

%

54.8

%

54.7

%

54.7

%

54.8

%

42%

44%

46%

48%

50%

52%

54%

56%

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12EFY13E

Source: Company, SPA Research

Because of strong brand recall, consumers preference forAsian paints product has been higher.Dominant position inthe industry helps Asian Paints to be able to extract highermargins from its dealers and is able to maintain lower debtordays at ~26 days which is lower compared to ~40 days forthe industry.

2) Maximum beneficiary of high GDP growth rateThe growth prospects of paint industry are highly correlatedwith the growth of the economy and it has been growing at1.5-2x GDP growth rate post liberalization. Higher GDPgrowth rate puts more money in the hands of consumersincreasing their discretionary spending.Geographical presence: Geographical presence of Asianpaints gives it a strong hold and edge over competitors.Asian Paints is having larger presence in south and westmarkets which contribute ~60% to overall paint industrysales. However, company is seeing higher growth from northand west regions and increasing its presence by penetrationthrough dealer's network. Company also has strong presencein fast growing rural markets which contributes ~45% to itsoverall revenue. According to the management, growth inrural markets is ~150-200bps higher than the growth in urbanmarkets due to higher construction activities and increasingrural income.

Asian Paints standalone (Indian) business has grown at a2 year CAGR of 21.7%. We further expect it to reportrevenue growth at a 2 year CAGR of 19.9% to INR90,921.2mn in FY13 backed by strong volume growth.

Standalone Business Trend

24.9%

20.0%23.4%

21.1%

18.8%

0

20000

40000

60000

80000

100000

FY09 FY10 FY11 FY12E FY13E0%

5%

10%

15%

20%

25%

30%

Standalone Revenue (INR mn) Grow th (%)

Source: Company, SPA Research

Capacity addition: On back of higher demand Asian Paintshas planned to expand its capacity by ~0.3mn MT in nexttwo years to ~0.89mn MT from current capacity of 0.59mnMT by setting up a greenfield plant for a capex of INR 10bnin Khandala which is scalable to ~0.4mn MT. Total capexis being funded through internal accruals. The plant isexpected to be commissioned by FY13. Presently thecompany is operating at higher capacity utilization of ~80%.Company commissioned a plant in Rohtak, Haryana ofcapacity ~0.15mn MT thereby increasing its capacity from~0.44mn MT in FY10 to ~0.59mn MT in FY11.

3) High competitive advantage and positioningProduct offerings: Asian Paints offers products across allthe categories in terms of types of products and customersegmentation.

Product Offerings Brands Price (INR/Litre)(Min-Max)

Exterior Emulsion Apex, Duracast 150-290Interior Emulsion Royale, Tractor 120-400Enamel Apcolite, Utsav 150-190Distempers Tractor, Utsav 45-95

Source: SPA Research *prices are in Mumbai region as on 8 May, 2011

Emulsion which is the fastest growing category at ~20%volume growth contributes ~50% of Asian paints decorativepaint segment. The margins in emulsion paints are higherthan the margins in distempers and enamels. The companyhas introduced lower priced interior emulsions in order toencourage users of distempers and enamels to upgradethemselves to emulsion paints.Unmatched Dealers network: Unmatched dealersnetwork give Asian paints high competitive advantage.Company expects to add 1,500-2,000 new dealers everyyear to its already enviable network of ~27,000 dealers.

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

9

Out of total dealers network ~17,500 dealers have AsianPaints dealer tinting system installed known as Colour Worldwhich enables the company to cut inventory, packagingand space cost helping it aid margins. Dealers have to forkout INR 0.2mn for installation of machine in their shop. Inthis way, Asian Paint is able to strengthen its hold over itsdealership network further reducing any threats fromcompetitors.Initiatives: With initiatives like Signature stores andconverting already existing dealers shop into similar modelas signature stores (known as Colour Ideas, 16 till now),company is focusing on increasing services along withproduct offerings. Through these stores company offerscolour consultancy, demonstration of colour application,varied themes to decorate home and provides technicalassistance in choosing right colour suiting the home andsurroundings. It also offers home painting services in 13cities at a fixed cost per square feet for a particular painttype. Encouraged by the customer response for its signaturestore, company is shortly opening another store inConnaught Place, New Delhi. We believe that this strategyto offer better value to customers would increase thestickiness and loyalty for the company's product along withbrand enhancement.Higher Ad Spends: Company's ad spends are highestamong its peers giving it stronger brand recall and occupylarger mind share. Paint demand comes mostly fromcustomer pull rather than distributor push. Therefore, a strongbrand positioning is critical for higher sales in the industry.

Ad & Publicity Exp. in FY10 (INR mn)

865.0 770.2 679.62,442.5

9.2%

4.4%4.6%

4.0%

0500

10001500200025003000

Asian Paints Akzo Nobel Berger Paints KansaiNerolac

0%

2%

4%

6%

8%

10%

Ad & Publicity Exp. in FY10 (INR mn)

as a % of Net Sales

4) International and Industrial business to gain tractionIndustrial Segment: Asian PPG Industries (APPG), a50:50 JV of Asian Paints with PPG Industries (USA), is thesecond-largest player in the automotive OEM paint segmentwith a market share of ~24%. APPG is one of the largestsuppliers of paints to Hyundai Motor India, General MotorsIndia and it is the sole supplier to New Holland TractorsIndia. Asian PPG is also the leading supplier of acrylic CED

coating to leading two-wheeler companies: Hero HondaMotors Ltd., TVS Motor Company, and Bajaj Auto Ltd. Withthe acquisition of the advanced refinish 2K business fromICI India in March, 2007, Asian PPG became the leader inthe refinish segment.Asian Paints has also signed a second 50:50 JV agreementwith PPG Industries Inc for Non Decorative and Non- AutoPaints in Jan 2011. Industrial businesses of both AsianPaints and PPG will be part of this second JV. Asian Paintsis to take lead in the second venture and PPG to take thelead in APPG in order to utilize their respective strengths tobest capture the growth in infrastructure development andglobally driven markets in India. The arrangement is subjectto regulatory approval and is expected to be completedduring H2FY12.APPG and Industrial paint segment (APICL) of Asian Paintscontributed 4.8% (INR 3.7bn) to consolidated revenues,growing by 23.7% in FY11. We further expect thismomentum in sales growth to sustain on back of robustdemand of automotives, consumer durables and higherinfrastructure investments.

Revenue Trend: APPG* + APICL (INR mn)

30.1%

-1.4%

18.6%23.7%

0500

1000150020002500300035004000

FY08 FY09 FY10 FY11-5%0%5%10%15%20%25%30%35%

Revenue from APPG* + APICL Grow th (%)

Source: Company, SPA Research

International business: International business division reporteda meager 1.9% growth in revenues of INR 9.9bn and contributed12.8% in FY11 consolidated sales. The lower revenue growthwas on the back of slowdown in international economies anddisruptions in operations in MENA region which contributesmore than 50% to international business division.Value Sales (INR mn) FY10 FY11 YoY (%)Caribbean 1,612.0 1,568.0 -2.7%Middle East 5,361.0 5,159.0 -3.8%South Asia 2,008.0 2,403.0 19.7%South Pacific 719.0 750.0 4.3%Total 9,700.0 9,880.0 1.9%

Source: Company, SPA Research

The company has presence in 16 other countries except Indiaalong with 13 manufacturing facilities. It is the largest paintcompany in Caribbean region, top 3 in South Pacific Islandsand South Asian regions. Also the company is third largest inthe Middle East with ~15% market share in Egypt.

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

10

Company has exited loss making unit in Singapore in FY11 inits international business portfolio. Going ahead, withimprovement in international economic environment and betteroperational efficiencies, we expect international business to showimproved performance and grow at a two year CAGR of 10.2%.

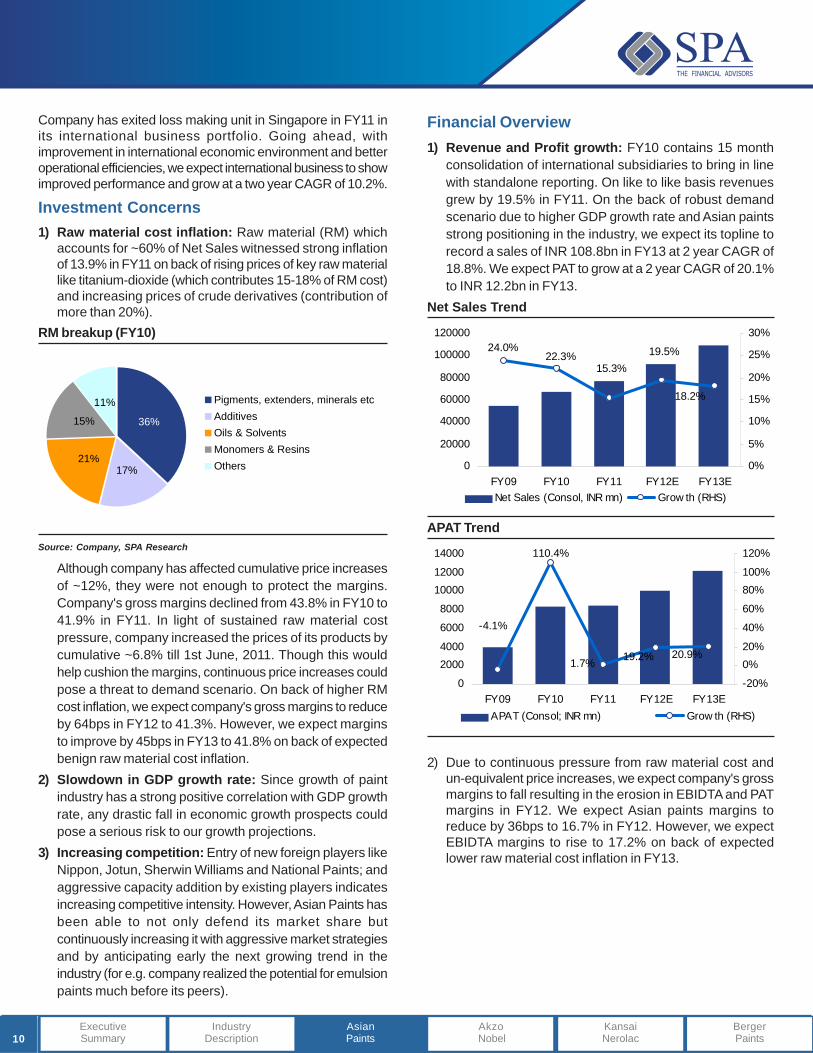

Investment Concerns1) Raw material cost inflation: Raw material (RM) which

accounts for ~60% of Net Sales witnessed strong inflationof 13.9% in FY11 on back of rising prices of key raw materiallike titanium-dioxide (which contributes 15-18% of RM cost)and increasing prices of crude derivatives (contribution ofmore than 20%).

RM breakup (FY10)

17%21%

15%

11%

36%

Pigments, extenders, minerals etcAdditivesOils & SolventsMonomers & ResinsOthers

Source: Company, SPA Research

Although company has affected cumulative price increasesof ~12%, they were not enough to protect the margins.Company's gross margins declined from 43.8% in FY10 to41.9% in FY11. In light of sustained raw material costpressure, company increased the prices of its products bycumulative ~6.8% till 1st June, 2011. Though this wouldhelp cushion the margins, continuous price increases couldpose a threat to demand scenario. On back of higher RMcost inflation, we expect company's gross margins to reduceby 64bps in FY12 to 41.3%. However, we expect marginsto improve by 45bps in FY13 to 41.8% on back of expectedbenign raw material cost inflation.

2) Slowdown in GDP growth rate: Since growth of paintindustry has a strong positive correlation with GDP growthrate, any drastic fall in economic growth prospects couldpose a serious risk to our growth projections.

3) Increasing competition: Entry of new foreign players likeNippon, Jotun, Sherwin Williams and National Paints; andaggressive capacity addition by existing players indicatesincreasing competitive intensity. However, Asian Paints hasbeen able to not only defend its market share butcontinuously increasing it with aggressive market strategiesand by anticipating early the next growing trend in theindustry (for e.g. company realized the potential for emulsionpaints much before its peers).

Financial Overview1) Revenue and Profit growth: FY10 contains 15 month

consolidation of international subsidiaries to bring in linewith standalone reporting. On like to like basis revenuesgrew by 19.5% in FY11. On the back of robust demandscenario due to higher GDP growth rate and Asian paintsstrong positioning in the industry, we expect its topline torecord a sales of INR 108.8bn in FY13 at 2 year CAGR of18.8%. We expect PAT to grow at a 2 year CAGR of 20.1%to INR 12.2bn in FY13.

Net Sales Trend

24.0%22.3%

18.2%

15.3%19.5%

0

20000

40000

60000

80000

100000

120000

FY09 FY10 FY11 FY12E FY13E0%

5%

10%

15%

20%

25%

30%

Net Sales (Consol, INR mn) Grow th (RHS)

APAT Trend

110.4%

20.9%19.2%1.7%

-4.1%

0

20004000

6000

8000

1000012000

14000

FY09 FY10 FY11 FY12E FY13E-20%

0%20%

40%

60%

80%100%

120%

APAT (Consol; INR mn) Grow th (RHS)

2) Due to continuous pressure from raw material cost andun-equivalent price increases, we expect company's grossmargins to fall resulting in the erosion in EBIDTA and PATmargins in FY12. We expect Asian paints margins toreduce by 36bps to 16.7% in FY12. However, we expectEBIDTA margins to rise to 17.2% on back of expectedlower raw material cost inflation in FY13.

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

11

Margin Profile

38.3%43.8% 41.9% 41.3% 41.8%

12.3%18.4% 17.0% 16.7% 17.2%

7.2%12.4% 10.9% 10.9% 11.2%

0%

10%

20%

30%

40%

50%

FY09 FY10 FY11 FY12E FY13E

Gross Margins EBIDTA Margins APAT Margins

3) Going forward, we expect return on average capitalemployed (RoACE) and return on average net-worth(RoANW) to get in line with its long term average of above35% after disproportionately high in FY10.

Return Profile

39.4% 38.4%

56.9%

39.2%

41.1%

52.3%

31.8%

40.8%43.3%

36.1%

30%

35%

40%

45%

50%

55%

60%

FY09 FY10 FY11 FY12E FY13ERoACE RoANW

ValuationsAsian paints having dominant position in paint industry is wellpoised to take maximum benefit of high GDP growth rate. Withchanging lifestyle needs, high disposable income and boom inconstruction activities, we expect Asian paints to grow at arevenue CAGR of 18.8% in the next two years. Based on highRoNW, higher EBIDTA margins and strong growth rate, wevalue the stock at 25x FY13E EPS of INR 126.7 which impliesa target price of INR 3,168. We therefore, initiate the coveragewith a Hold rating.

30

25

20

10

0

500

1000

15002000

2500

3000

3500

Apr-

06

Apr-

07

Apr-

08

Apr-

09

Apr-

10

Apr-

11

Source: SPA Research

Company BriefAsian Paints is the largest decorative paint company in Indiasince last 4 decades and has a dominant market share ofmore than 50% in organized sector. The company has presencein 17 counties with 22 manufacturing facilities. It is one of thefastest growing FMCG companies with a 4 year CAGR of20.4%. It is also the third largest player in industrial paintswith a market share of ~ 13%. Chemical business whichcontributed 1% to consolidated revenue of FY11 consists ofPhthalic Anhydride and Pentaerythritol, which are used in thepaint manufacturing process.

Revenue Breakup (FY11)

81%

1%

5%

13%

APL - Paints

Chemicals

APPG* + APICL

International

Decorative Manufacturing Facilities in India

Bhandup (Mumbai, Maharashtra)

Ankleshwar (Gujarat)

Patancheru (Andhra Pradesh)

Kasna (Uttar Pradesh)

Sriperumbudur (Chennai, Tamil Nadu)

Rohtak (Haryana) - Commissioned in April 2010

Kesurdi (Maharashtra) Will be ready by 2013

Source: Company, SPA Research

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

12

Financials

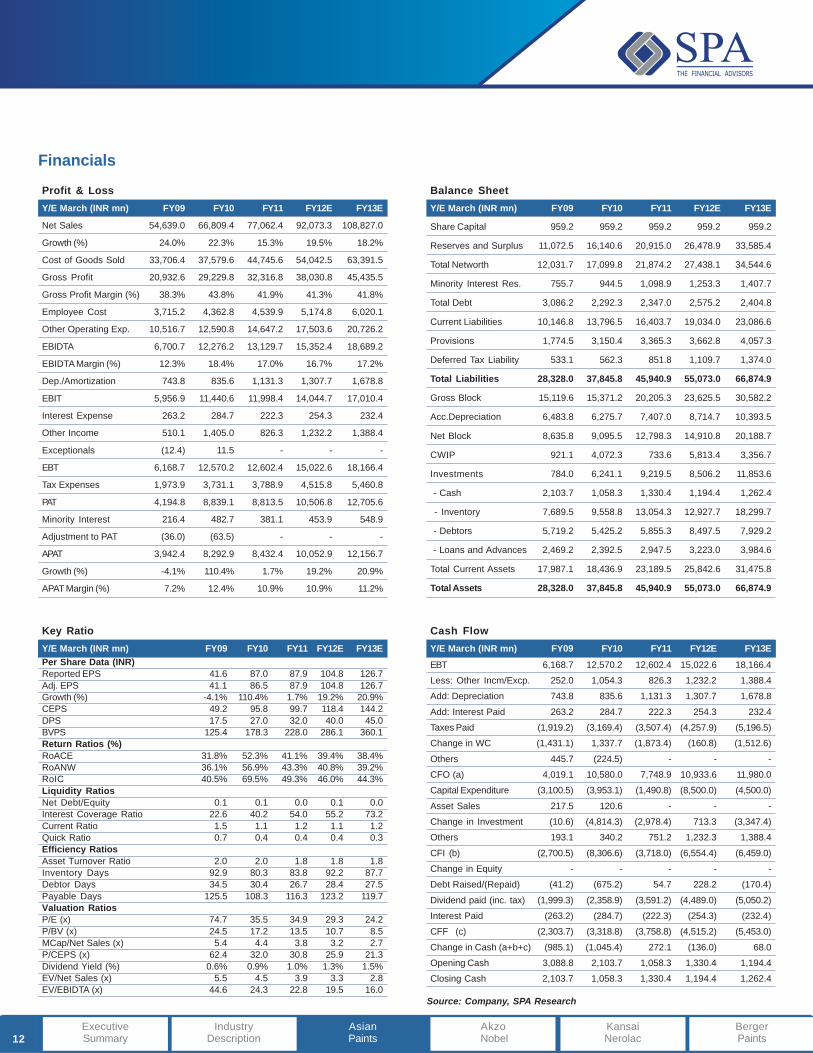

Balance Sheetmn)Y/E March (INR mn) FY09 FY10 FY11 FY12E FY13E

Share Capital 959.2 959.2 959.2 959.2 959.2

Reserves and Surplus 11,072.5 16,140.6 20,915.0 26,478.9 33,585.4

Total Networth 12,031.7 17,099.8 21,874.2 27,438.1 34,544.6

Minority Interest Res. 755.7 944.5 1,098.9 1,253.3 1,407.7

Total Debt 3,086.2 2,292.3 2,347.0 2,575.2 2,404.8

Current Liabilities 10,146.8 13,796.5 16,403.7 19,034.0 23,086.6

Provisions 1,774.5 3,150.4 3,365.3 3,662.8 4,057.3

Deferred Tax Liability 533.1 562.3 851.8 1,109.7 1,374.0

Total Liabilities 28,328.0 37,845.8 45,940.9 55,073.0 66,874.9

Gross Block 15,119.6 15,371.2 20,205.3 23,625.5 30,582.2

Acc.Depreciation 6,483.8 6,275.7 7,407.0 8,714.7 10,393.5

Net Block 8,635.8 9,095.5 12,798.3 14,910.8 20,188.7

CWIP 921.1 4,072.3 733.6 5,813.4 3,356.7

Investments 784.0 6,241.1 9,219.5 8,506.2 11,853.6

- Cash 2,103.7 1,058.3 1,330.4 1,194.4 1,262.4

- Inventory 7,689.5 9,558.8 13,054.3 12,927.7 18,299.7

- Debtors 5,719.2 5,425.2 5,855.3 8,497.5 7,929.2

- Loans and Advances 2,469.2 2,392.5 2,947.5 3,223.0 3,984.6

Total Current Assets 17,987.1 18,436.9 23,189.5 25,842.6 31,475.8

Total Assets 28,328.0 37,845.8 45,940.9 55,073.0 66,874.9

Profit & LossY/E March (INR mn) FY09 FY10 FY11 FY12E FY13E

Net Sales 54,639.0 66,809.4 77,062.4 92,073.3 108,827.0

Growth (%) 24.0% 22.3% 15.3% 19.5% 18.2%

Cost of Goods Sold 33,706.4 37,579.6 44,745.6 54,042.5 63,391.5

Gross Profit 20,932.6 29,229.8 32,316.8 38,030.8 45,435.5

Gross Profit Margin (%) 38.3% 43.8% 41.9% 41.3% 41.8%

Employee Cost 3,715.2 4,362.8 4,539.9 5,174.8 6,020.1

Other Operating Exp. 10,516.7 12,590.8 14,647.2 17,503.6 20,726.2

EBIDTA 6,700.7 12,276.2 13,129.7 15,352.4 18,689.2

EBIDTA Margin (%) 12.3% 18.4% 17.0% 16.7% 17.2%

Dep./Amortization 743.8 835.6 1,131.3 1,307.7 1,678.8

EBIT 5,956.9 11,440.6 11,998.4 14,044.7 17,010.4

Interest Expense 263.2 284.7 222.3 254.3 232.4

Other Income 510.1 1,405.0 826.3 1,232.2 1,388.4

Exceptionals (12.4) 11.5 - - -

EBT 6,168.7 12,570.2 12,602.4 15,022.6 18,166.4

Tax Expenses 1,973.9 3,731.1 3,788.9 4,515.8 5,460.8

PAT 4,194.8 8,839.1 8,813.5 10,506.8 12,705.6

Minority Interest 216.4 482.7 381.1 453.9 548.9

Adjustment to PAT (36.0) (63.5) - - -

APAT 3,942.4 8,292.9 8,432.4 10,052.9 12,156.7

Growth (%) -4.1% 110.4% 1.7% 19.2% 20.9%

APAT Margin (%) 7.2% 12.4% 10.9% 10.9% 11.2%

Cash Flowmn)Y/E March (INR mn) FY09 FY10 FY11 FY12E FY13E

EBT 6,168.7 12,570.2 12,602.4 15,022.6 18,166.4

Less: Other Incm/Excp. 252.0 1,054.3 826.3 1,232.2 1,388.4

Add: Depreciation 743.8 835.6 1,131.3 1,307.7 1,678.8

Add: Interest Paid 263.2 284.7 222.3 254.3 232.4

Taxes Paid (1,919.2) (3,169.4) (3,507.4) (4,257.9) (5,196.5)

Change in WC (1,431.1) 1,337.7 (1,873.4) (160.8) (1,512.6)

Others 445.7 (224.5) - - -

CFO (a) 4,019.1 10,580.0 7,748.9 10,933.6 11,980.0

Capital Expenditure (3,100.5) (3,953.1) (1,490.8) (8,500.0) (4,500.0)

Asset Sales 217.5 120.6 - - -

Change in Investment (10.6) (4,814.3) (2,978.4) 713.3 (3,347.4)

Others 193.1 340.2 751.2 1,232.3 1,388.4

CFI (b) (2,700.5) (8,306.6) (3,718.0) (6,554.4) (6,459.0)

Change in Equity - - - - -

Debt Raised/(Repaid) (41.2) (675.2) 54.7 228.2 (170.4)

Dividend paid (inc. tax) (1,999.3) (2,358.9) (3,591.2) (4,489.0) (5,050.2)

Interest Paid (263.2) (284.7) (222.3) (254.3) (232.4)

CFF (c) (2,303.7) (3,318.8) (3,758.8) (4,515.2) (5,453.0)

Change in Cash (a+b+c) (985.1) (1,045.4) 272.1 (136.0) 68.0

Opening Cash 3,088.8 2,103.7 1,058.3 1,330.4 1,194.4

Closing Cash 2,103.7 1,058.3 1,330.4 1,194.4 1,262.4

Key Ratiomn)Y/E March (INR mn) FY09 FY10 FY11 FY12E FY13EPer Share Data (INR)Reported EPS 41.6 87.0 87.9 104.8 126.7Adj. EPS 41.1 86.5 87.9 104.8 126.7Growth (%) -4.1% 110.4% 1.7% 19.2% 20.9%CEPS 49.2 95.8 99.7 118.4 144.2DPS 17.5 27.0 32.0 40.0 45.0BVPS 125.4 178.3 228.0 286.1 360.1Return Ratios (%)RoACE 31.8% 52.3% 41.1% 39.4% 38.4%RoANW 36.1% 56.9% 43.3% 40.8% 39.2%RoIC 40.5% 69.5% 49.3% 46.0% 44.3%Liquidity RatiosNet Debt/Equity 0.1 0.1 0.0 0.1 0.0Interest Coverage Ratio 22.6 40.2 54.0 55.2 73.2Current Ratio 1.5 1.1 1.2 1.1 1.2Quick Ratio 0.7 0.4 0.4 0.4 0.3Efficiency RatiosAsset Turnover Ratio 2.0 2.0 1.8 1.8 1.8Inventory Days 92.9 80.3 83.8 92.2 87.7Debtor Days 34.5 30.4 26.7 28.4 27.5Payable Days 125.5 108.3 116.3 123.2 119.7Valuation RatiosP/E (x) 74.7 35.5 34.9 29.3 24.2P/BV (x) 24.5 17.2 13.5 10.7 8.5MCap/Net Sales (x) 5.4 4.4 3.8 3.2 2.7P/CEPS (x) 62.4 32.0 30.8 25.9 21.3Dividend Yield (%) 0.6% 0.9% 1.0% 1.3% 1.5%EV/Net Sales (x) 5.5 4.5 3.9 3.3 2.8EV/EBIDTA (x) 44.6 24.3 22.8 19.5 16.0

Source: Company, SPA Research

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

This page has been intentionally left blank

Akzo Nobel India

Plans to fill the product gap; bid to renew market shareAkzo Nobel India (formerly ICI India) is known for its strongbrand Dulux in premium market segment and ICI in economymarket segment. Due to lack of product offerings for mid-marketand lower-market segment, company has been continuouslylosing market share to competition. However, with the completerevamp of top management team in last two years, companyis expecting to aggressively launch new products in mid marketsegment to fill the product gaps and renew efforts to gain marketshare. We believe that company would record revenue CAGRof 20.5% in next two years on back of new product launchesand increased sales & marketing efforts.

EBIDTA margins to expandGoing ahead, we expect Akzo to benefit from higher operatingleverage on back of expanding revenue base. Therefore webelieve that company's EBIDTA margins to improve by 140bpsfrom 12.2% in FY11 to 13.6% in FY13. On the back ofimprovement in margins and higher revenue growth, we expectAkzo's operating PAT to grow at a two year CAGR of 29.8% toINR 1244.0mn in FY13.

Strong balance sheet with investments of INR 10bnAs per FY2011 balance sheet, Akzo's cash and liquidinvestments stood close to ~INR10.2bn transforming into INR275.6 per share (30% of market capitalisation). Going ahead,we expect the cash and liquid investments surplus to increaseto INR 10.8bn (INR 294.4 per share) in FY2013, despiteaccounting for a capex of INR 2.2bn over next two years, drivenby strong operating cash flows, high treasury income andimprovement in margins.

June 15, 2011

Refinish paint business to ride the growth of autoownershipRefinish paint business which caters to refinish paint forautomotives contributes ~15% to Akzo's overall revenues.Company has enhanced its focus to cater this business segment.With increasing ownership of automotives and tough roadtravelling conditions, we expect good demand for refinish paints.Therefore, we expect the business to perform well going forward.

Renewed focus to growCompany is backed by the parent company Akzo Nobel,Netherlands which has consistently ranked as world's largestpaint company. Backed by the renewed efforts from parentcompany with its bigger plans for Indian market, Akzo Nobelmanagement has guided to become Euro 1bn entity by 2015.To achieve the target company is undergoing massive capacityexpansion plans. It plans to double its capacity from current~80,000 MT to ~160,000 MT by FY13.

ValuationsExpect re-rating of valuation multiple: At CMP of INR 910,Akzo is trading at a PEG of 0.6 compared to 1.2, 1.2 and 0.7 forAsian Paints, Kansai Nerolac and Berger Paints respectively.We expect company to trade atleast on a PEG of 0.85 (avggrowth of 29.8% in next two years), which is 30% discount tomarket leader Asian Paints. We believe the valuations are justifiedon back of higher growth in revenue and profits, improved marginsand return on networth, and lowest capital employed amongstpeers. This implies 25.4x FY13 EPS of INR 33.8 translatinginto target price of INR 1,157 (25.4x FY13 core EPS + 300/share from Investment surplus) giving an upside of 28%. Weinitiate the coverage with BUY.

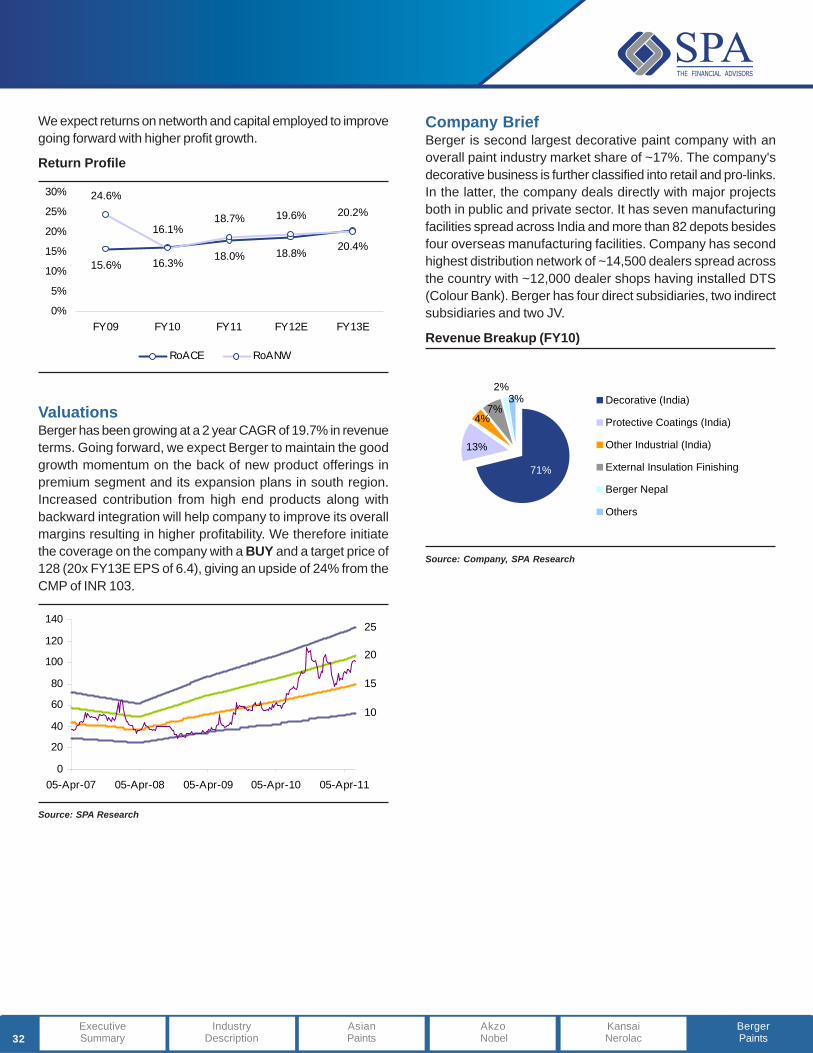

Akzo Nobel India (Akzo) known for its premium segment product Dulux has a market share of ~9-10%. Company's business can be broadly divided into decorative paints and refinish auto paintswhere later contributes ~15% to its revenues. Erstwhile ICI, the companies name was changed toAkzo Nobel in FY10 after it was acquired by largest paint company in the world in 2008.

Shareholding (%) Dec-10 Mar-11

Promoters 56.40 56.40

FIIs 1.17 1.24

DIIS 19.60 18.30

Others 22.83 23.98

Key Data

BSE Code 500710

NSE Code AKZOINDIA

Bloomberg Code AKZO IN

Reuters Code ICI.BO

Shares Outstanding (mn) 36.8

Face Value 10

Mcap (INR bn) 33.4

52 Week H/L 970/616

2W Avg. Qty, BSE 7,689

Sensex 18,132.2

Y/E Mar (INR mn) FY09 FY10 FY11 FY12E FY13E

Net Sales 9,087.0 9,471.0 10,968.2 13,456.8 15,928.3Growth (%) -3.6% 4.2% 15.8% 22.7% 18.4%EBIDTAM (%) 12.9% 13.4% 12.2% 12.7% 13.6%Adj. PAT 951.0 1,593.0 1,664.1 1,968.4 2,263.5Growth (%) 20.5% 67.5% 4.5% 18.3% 15.0%Operating PAT 611.0 692.3 737.9 968.6 1,244.0Growth (%) 9.2% 13.3% 6.6% 31.3% 28.4%Optng. PATM (%) 6.7% 7.3% 6.7% 7.2% 7.8%Adj. EPS (INR) 25.0 43.2 45.2 53.4 61.5Operational EPS 16.0 18.8 20.0 26.3 33.8DPS 16.0 16.0 18.0 18.0 20.0Dividend Yield (%) 1.8% 1.8% 2.0% 2.0% 2.2%P/E (x) 36.3 21.0 20.1 17.0 14.8P/BV (x) 3.6 3.4 3.1 2.8 2.5EV/EBIDTA 21.8 18.8 17.5 13.2 10.5Net Debt/Equity (1.0) (1.0) (0.9) (0.9) (0.8)RoACE (%) 15.5% 15.7% 14.0% 16.9% 17.5%RoANW (%) 11.0% 16.2% 16.0% 17.1% 17.7%

Relative share price performance

8090

100110120130140150

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr-

11

May

-11

Akzo Sensex

Paint Industry

Sumit [email protected]. +91-22-4289 5600 Ext. 630

14Industry

DescriptionAsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

CMP: INR 907 Recommendation: Buy Target: INR 1,157

15

Investment Rationale1) Plans to fill the product gap: bid to renew market share

Akzo Nobel (formerly ICI) is known for its strong brand Duluxin premium market segment and ICI in economy marketsegment. Company has highest average realization per litreof ~INR 157 compared to INR 110, INR 105 and INR 85 forKansai Nerolac, Asian Paints and Berger respectively(Chart).

Avg. Realization FY11 (INR/Lt)

80

105 110

157

020406080

100120140160180

Berger Asian Paints Kansai Akzo Nobel

Source: Company, SPA Research

Due to lack of product offerings for mid-market and lower-marketsegment, company has been continuously losing market shareto competition. Akzo's market share fell to ~9% in FY11compared to ~16% in FY04 (Chart).

Akzo Nobel (ICI) Market Share Trend

16.6% 16.3% 16.1%14.0%

12.8%10.9%

9.5% 9.1%

0%2%4%6%8%

10%12%14%16%18%

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11

Source: SPA Research

However, with the complete revamp of top management team inlast two years, company is expecting to aggressively launchnew products in mid market segment to fill the product gapsand renew efforts to gain market share. Company reported amuch improved YoY growth of 15.9% in FY11 after flattish growthin FY08 to FY10.

Net Sales Trend

15.8%

22.7%18.4%

4.2%

-3.6%

4.7%

-2,0004,0006,0008,000

10,00012,00014,00016,00018,000

FY08 FY09 FY10 FY11 FY12E FY13E-5%

0%

5%

10%

15%

20%

25%

Net Sales (INR mn) Grow th (RHS)

Source: Company, SPA Research

We believe that company would maintain a CAGR of 20.5% innext two years on back of new product launches and increasedsales & marketing efforts.

2) EBIDTA margins to expandAkzo's gross margins is highest compared to its peers dueto its presence largely in premium paints. However, despitethis, Akzo's OPM has been ~600bps lower vis-à-vis AsianPaints owing to significantly higher overheads, particularlyA&P spends (~at 9% of revenue compared to ~3.5-4.5%for its peers), due to lower revenue base.

Margins Comparison (FY11)

47.4%

12.2%

42.3%

18.1%

0%

10%

20%

30%

40%

50%

Gross Profit Margins EBIDTA Margins

Akzo Nobel Asian Paints

Source: Company, SPA Research

Going ahead, we expect Akzo to benefit from higher operatingleverage as overheads get spread over a larger revenue base.Therefore we believe that company's EBIDTA margins to improveby 140bps from 12.2% in FY11 to 13.6% in FY13.

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

16

Margin Trend

43.9%49.0% 47.3% 46.8% 47.2%

12.9% 13.4% 12.2% 12.7% 13.6%

0%

10%

20%

30%

40%

50%

60%

FY09 FY10 FY11 FY12E FY13E

Gross Margins EBIDTA Margins

Source: Company, SPA Research

On the back of improvement in margins and higher revenuegrowth, we expect Akzo's operating PAT to grow at a two yearCAGR of 29.8% to INR 1244.0mn in FY13.

Operational PAT Trend

9.2%13.3%

31.3% 28.4%

-2.2%

6.6%

0200400600800

100012001400

FY08 FY09 FY10 FY11 FY12E FY13E-5%0%5%10%15%20%25%30%35%

Operational PAT Grow th (%)

Source: Company, SPA Research

3) Strong balance sheet with liquid investments of INR 10bnOver the years, the company had divested several of itsbusinesses accumulating significant cash surplus on itsbalance sheet. Hence, as per FY2011 balance sheet, Akzo'scash and liquid investments stood close to ~INR10.2bntransforming into INR 275.6 per share (30% of marketcapitalisation). Going ahead, we expect the cash and liquidinvestments surplus to increase to INR 10.8bn (INR 294.4per share) in FY2013, despite accounting for a capex of INR2.2bn over next two years, driven by strong operating cashflows, high treasury income and improvement in margins.

Investment & Cash Surplus/Share

205.4184.8

244.3264.6 275.6

299.9 294.4

0

50

100

150

200

250

300

350

FY07 FY08 FY09 FY10 FY11 FY12E FY13E

Source: Company, SPA Research

4) Refinish paint business to ride the growth of auto ownershipRefinish paint business which caters to refinish paint forautomotives contributes ~15% to Akzo's overall revenues.Company has enhanced its focus to cater this businesssegment and is focusing to revamp the brand strategy for'Eterna' with clear market segmentation. The businesscontinued its focus on demand generation throughprogrammes like "The Great Finishers Club", colourworkshops and training in colour matching skills for painters.

Total Vehicles Ownership (mn)

102.4125.2

168.4

372.2

050

100150200250300350400

2001 2003 2006 2013E

Source: Company, SPA Research

With increasing ownership of automotives and tough roadtravelling conditions, we expect good demand for refinish paints.Therefore, we expect the business to perform well going forward.

5) Renewed focus to growRenewed focus to grow: Company is backed by the parentcompany Akzo Nobel, Netherlands which has consistentlyranked as world's largest paint company for many yearsand has strong global brands. Backed by the renewedefforts from parent company with its strong plans for Indianmarket, Akzo Nobel management has guided to becomeEuro 1bn entity by 2015. Currently it's trading at MCap of2.9x Net Sales. Assuming it maintains the same MCap toNet Sales ratio in FY15, company needs to grow its revenueat a CAGR of ~20% for next four years.

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

17

Doubling Capacity: To achieve the target company isundergoing massive capacity expansion plans. It plans todouble its capacity from current ~80,000 MT to ~160,000MT by FY13. It is quadrupling the capacity of its Hyderabadplant to 40,000 MT per annum. The additional capacity isslated to be available by Q2FY12 in this facility. Akzo plansto set up a green-field manufacturing facility in MadhyaPradesh or Karnataka with capacity between 0.05-0.1mnMT at an investment of up to INR 2.5bn, to be commissionedby FY13.

Capacity & Utilization89.5% 90.0%

76.5%85.4%

72.8%58.0%

0

50000

100000

150000

200000

FY08 FY09 FY10 FY11 FY12 FY130%

20%

40%

60%

80%

100%

Capacity (MT) Utilization (RHS)

Source: Company, SPA Research

Investment Risk1) High raw material cost inflation

Higher than expected increase in raw material cost inflationalong with inability to pass the same could pose a downsiderisk to our profit projections. Akzo is at higher risk fromincrease in prices of titanium dioxide compared to its peers.This is because TiO2 has highest percentage of ~19% inraw material cost (compared to ~14%-17% for others)

RM breakup (FY10)

16%

17%

16%16%

19%

16%

Pigments, Tinters, Extenders

Latex, Monomers

Resins

Solvents

Titanium Dioxide

Others

Source: Company, SPA Research

2) Inability to successfully launch new product categoriesCompany's attempt to regain the market share by launchingmid-segment products would be failed if it's unable to launchand market the products at the right price points and increaseits distribution reach to Tier II and Tier III cities with highergrowth rates.

Financial OverviewNet Sales Trend

15.8%

22.7%18.4%

4.2%

-3.6%

4.7%

-2,0004,0006,0008,000

10,00012,00014,00016,00018,000

FY08 FY09 FY10 FY11 FY12E FY13E-5%

0%

5%

10%

15%

20%

25%

Net Sales (INR mn) Grow th (RHS)

Operational PAT Trend

9.2%13.3%

31.3% 28.4%

-2.2%

6.6%

0200400600800

100012001400

FY08 FY09 FY10 FY11 FY12E FY13E-5%0%5%10%15%20%25%30%35%

Operational PAT Grow th (%)

Margin Trend

43.9%49.0% 47.3% 46.8% 47.2%

12.9% 13.4% 12.2% 12.7% 13.6%

7.8%7.2%6.7%7.3%6.7%0%

10%

20%

30%

40%

50%

60%

FY09 FY10 FY11 FY12E FY13EGross Margins EBIDTA Margins

Operational PAT Margins

Doubling Capacity

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

18

Return profile

15.5% 15.7%14.0%

16.9% 17.5%

16.2% 15.8%17.1% 17.7%

11.0%

0%

5%

10%

15%

20%

FY09 FY10 FY11 FY12E FY13E

RoACE RoANW

ValuationsExpect re-rating of valuation multiple: At CMP of INR 910,Akzo is trading at a PEG of 0.6 compared to 1.2, 1.2 and 0.7for Asian Paints, Kansai Nerolac and Berger Paints respectively.We expect company to trade atleast on a PEG of 0.85 (avggrowth of 29.8% in next two years), which is 30% discount tomarket leader Asian Paints. We believe the valuations arejustified on back of higher growth in revenue and profits,improved margins and return on networth, and lowest capitalemployed amongst peers. This implies 25.4x FY13 EPS ofINR 33.8 translating into target price of INR 1,157 (25.4x FY13core EPS + 300/share from Investment surplus) giving an upsideof 28%.We initiate the coverage with BUY.

Company BriefAkzo Nobel known for its premium segment product Duluxhas a market share of ~9-10%. Company's business can bedivided into decorative paints and refinish auto paints in theratio of 85:15. Erstwhile ICI, the companies name was changedto Akzo Nobel in FY10 after it was acquired by largest paintcompany in the world in 2008. Akzo has three manufacturingfacilities in Hyderabad (AP), Thane (Maharashtra) and Mohali(Punjab). Company is planning to launch new products to caterfast growing mid-market segment to regain its market share.

Companies CMP PAT Gr PAT Gr EPS (INR) EPS (INR) P/E (x) P/E (x) PEG (x)(INR) FY12E FY13E FY12 FY13 FY12 FY13

Asian Paints 3,070 19.2% 20.9% 104.8 126.7 29.3 24.2 1.2

Kansai Nerolac 875 11.4% 19.4% 38.8 46.3 22.6 18.9 1.2

Berger Paints 103 21.4% 24.6% 5.1 6.4 20.2 16.1 0.7

Akzo Nobel 907 31.3% 28.4% 26.3 33.8 24.0 18.0 0.6Source: SPA Research

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

19

Financials

Balance Sheetmn)Y/E March (INR mn) FY09 FY10 FY11 FY12E FY13E

Share Capital 381.0 368.0 368.0 368.0 368.0

Reserves and Surplus 9,330.0 9,553.0 10,548.2 11,740.9 13,142.5

Total Networth 9,711.0 9,921.0 10,916.5 12,108.9 13,510.5

Total Debt - - - - -

Current Liabilities 2,019.0 2,236.0 2,744.9 3,509.7 3,807.9

Provisions 1,537.0 1,552.0 1,696.8 1,528.0 1,228.0

Deferred Tax Liability (Net) 58.0 21.0 41.0 64.6 92.6

Total Liabilities 13,325.0 13,730.0 15,399.2 17,211.3 18,639.0

Gross Block 3,255.0 3,495.0 3,725.0 4,425.0 5,385.0

Acc. Depreciation 1,924.0 2,114.0 2,330.6 2,575.1 2,869.4

Net Block 1,331.0 1,381.0 1,394.4 1,849.9 2,515.6

CWIP 16.0 23.0 169.1 300.0 240.0

Investments 9,152.0 9,602.0 9,849.9 10,900.4 10,696.2

- Cash 147.0 143.0 303.1 147.4 147.6

- Inventory 1,008.0 972.0 1,531.8 1,489.9 2,106.3

- Debtors 757.0 808.0 701.4 1,138.5 1,039.3

- Loans and Advances 914.0 801.0 1,449.5 1,385.0 1,893.9

Total Current Assets 2,826.0 2,724.0 3,985.8 4,161.0 5,187.2

Total Assets 13,325.0 13,730.0 15,399.2 17,211.3 18,639.0

Profit & LossY/E March (INR mn) FY09 FY10 FY11 FY12E FY13ENet Sales 9,087.0 9,471.0 10,968.2 13,456.8 15,928.3Growth (%) -3.6% 4.2% 15.8% 22.7% 18.4%Cost of Goods Sold 5,099.0 4,826.0 5,775.3 7,161.5 8,415.3Gross Profit 3,988.0 4,645.0 5,192.9 6,295.2 7,513.0Gross Profit Margin (%) 43.9% 49.0% 47.3% 46.8% 47.2%Employee Cost 446.0 608.0 696.6 798.3 918.0Other Operating Exp 2,384.0 2,776.0 3,165.8 3,800.2 4,442.5EBIDTA 1,158.0 1,261.0 1,330.5 1,696.7 2,152.5EBIDTA Margin (%) 12.9% 13.4% 12.2% 12.7% 13.6%Dep./Amortization 213.0 212.0 216.6 244.5 294.3EBIT 945.0 1,049.0 1,113.9 1,452.2 1,858.2Interest Expense 29.0 11.0 7.6 17.2 15.3Other Income 876.0 962.0 967.8 1,113.0 1,105.5Exceptionals 1,995.0 - 112.8 - -EBT 3,787.0 2,000.0 2,186.9 2,548.1 2,948.4Tax Expenses 841.0 407.0 432.6 579.6 684.9PAT 2,946.0 1,593.0 1,754.3 1,968.4 2,263.5Adjustment to PAT (1,995.0) - (112.8) - -APAT 951.0 1,593.0 1,641.5 1,968.4 2,263.5Growth (%) 20.5% 67.5% 3.0% 19.9% 15.0%APAT Margin (%) 10.5% 16.8% 15.0% 14.6% 14.2%Operating PAT 611.0 692.3 737.9 968.6 1,244.0Growth (%) 9.2% 13.3% 6.6% 31.3% 28.4%Operating PAT Margin (%) 6.7% 7.3% 6.7% 7.2% 7.8%

Cash Flowmn)Y/E March (INR mn) FY09 FY10 FY11 FY12E FY13E

EBT 1,792.0 2,000.0 2,186.9 2,548.1 2,948.4

Less: Other Incm/Excp 965.0 959.0 1,080.6 1,113.0 1,105.5

Add: Depreciation 213.0 212.0 216.6 244.5 294.3

Add: Interest Paid 29.0 11.0 7.6 17.2 15.3

Taxes Paid (858.0) (456.0) (412.6) (556.0) (657.0)

Change in WC (210.0) 160.0 (592.8) 434.0 (727.9)

Others 19.0 140.0 - - -

CFO (a) 20.0 1,108.0 325.1 1,574.7 767.6

Capital Expenditure (297.0) (271.0) (376.1) (1,000.0) (1,200.0)

Asset Sales 2,272.0 (7.0) 112.8 - -

Change in Investment 908.0 823.0 46.2 - -

Others (54.0) 210.0 1,080.6 1,113.0 1,105.5

CFI (b) 2,829.0 755.0 863.5 113.0 (94.5)

Change in Equity (154.0) (696.0) - - -

Debt Raised/(Repaid) - - - - -

Dividend paid (inc. tax) (356.0) (710.0) (771.0) (775.7) (861.9)

Interest Paid (29.0) (11.0) (7.6) (17.2) (15.3)

CFF (c) (539.0) (1,417.0) (778.6) (792.9) (877.2)

Change in Cash (a+b+c) 2,310.0 446.0 410.0 894.9 (204.1)

Opening Cash 6,987.0 9,297.0 9,743.0 10,153.0 11,047.9

Closing Cash 9,297.0 9,743.0 10,153.0 11,047.9 10,843.8

Key Ratiomn)Y/E March (INR mn) FY09 FY10 FY11 FY12E FY13EPer Share Data (INR)Reported EPS 77.0 42.6 47.6 53.4 61.5Adj. EPS 25.0 43.2 45.2 53.4 61.5Growth (%) 21.5% 73.1% 4.5% 18.3% 15.0%Operational EPS 16.0 18.8 20.0 26.3 33.8Growth (%) 9.2% 13.3% 6.6% 31.3% 28.4%CEPS 305.8 490.0 510.6 600.8 694.4DPS 16.0 16.0 18.0 18.0 20.0BVPS 255.1 269.3 296.4 328.7 366.8Return Ratios (%)RoACE 15.5% 15.7% 14.0% 16.9% 17.5%RoANW 11.0% 16.2% 16.0% 17.1% 17.7%RoIC 38.6% 16.4% 17.7% 18.0% 18.7%Liquidity RatiosNet Debt/Equity (1.0) (1.0) (0.9) (0.9) (0.8)Interest Coverage Ratio 32.6 95.4 146.6 84.4 121.4Current Ratio 0.8 0.7 0.9 0.8 1.0Quick Ratio 0.3 0.3 0.2 0.3 0.2Efficiency RatiosAsset Turnover Ratio 0.7 0.7 0.7 0.8 0.8Inventory Days 80.4 74.9 79.1 77.0 78.0Debtor Days 36.5 30.4 25.3 25.2 25.2Payable Days 167.5 160.9 157.4 159.4 158.7Valuation RatiosP/E (x) 36.3 21.0 20.1 17.0 14.8P/BV (x) 3.6 3.4 3.1 2.8 2.5MCap/Net Sales (x) 3.8 3.6 3.1 2.5 2.1P/CEPS (x) 3.0 1.9 1.8 1.5 1.3Dividend Yield (%) 1.8% 1.8% 2.0% 2.0% 2.2%EV/Net Sales (x) 2.8 2.5 2.1 1.7 1.4EV/EBIDTA (x) 21.8 18.8 17.5 13.2 10.5 Source: Company, SPA Research

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

This page has been intentionally left blank

Kansai Nerolac Paints

Dominant player in Industrial Paint SegmentKNP is the dominant player in industrial paints segment withmarket share of more than 40% and contributes ~50% to itsoverall revenue. It is a leader in automotive paints and powdercoatings with a market share of ~60% and ~27% respectively.KNP has a strong technological backup from its parent companyKansai (Japan) which is the largest paint company in Japan andhas been featured in top 10 paints companies in the world.

Growth momentum to moderate in FY12KNP has registered robust revenue growth on the back of strongdemand for automotives, consumer durables and infrastructuredevelopment. In line with expected slowdown in auto segmentand other industrial segments in the current year, we expectKNP revenue growth to slow down to 20.3% in FY12 from 25.3%in FY11 on back of lower volume growth.

Focus towards increasing decorative paintscontributionCompany has plans to increase sales in decorative segmentby launching aggressive nationwide campaign and increasingdistribution reach. KNP recently roped in Shahrukh Khan topromote its product in decorative segment. Kansai has plansto open 30 new exclusive Nerolac brand stores in South.

June 15, 2011

Increasing capacity on higher demandanticipationIn order to fulfill higher demand for paints both in industrial anddecorative segments, company plans to add ~0.1mn MT ofcapacity to its current capacity of ~0.2mn MT/annum. In orderto increase the capacity company is setting up a greenfieldplant in Hosur (TN) at an estimated capex of ~INR 6bn. Theplant is expected to be fully commissioned by FY13.

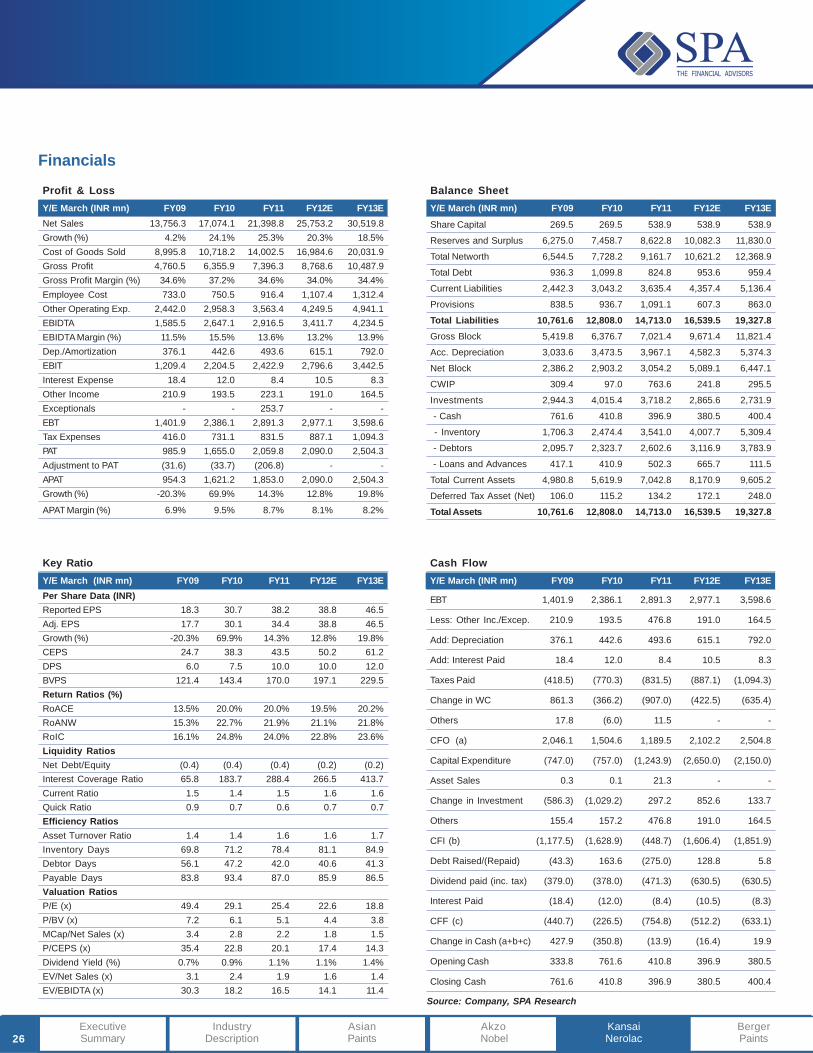

ValuationsKansai Nerolac is expected to maintain its dominant share inindustrial paints segment and benefit from strong growth ofautomotive and consumer durables industry. Also, withcompany's focus to increase contribution from decorative paintsegment will reduce RM cost pressure due to better ability topass cost through price increases. We expect KNP to grow atrevenue CAGR of 19.3% in the next two years. On back oflong term growth in industrial segment and dominant positionof KNP in industrial paints, we value the stock at 20x FY13E.This works out to be a 1 year target price of INR 926 with anupside of 6% from CMP of INR 875. We therefore, initiate thecoverage with a Hold rating.

Kansai Nerolac Paints (KNP), formerly known as Goodlass Nerolac became a wholly-ownedsubsidiary of Kansai Paint Company (Japan) after it took over the entire stake of the company in1999 and changed its name in 2006. The company has presence in both decorative and industrialpaints segment which contributes equally to its revenues. In India, it is third largest player indecorative segment and largest player in Industrial paints segment with a market share of ~14% and~42% respectively. It has the dominant share in auto paint segment of ~60%.

Shareholding (%) Dec-10 Mar-11

Promoters 69.27 69.27

FIIs 6.05 5.92

DIIS 5.07 4.97

Others 19.61 19.84

Key Data

BSE Code 500165

NSE Code KANSAINER

Bloomberg Code KNPL IN

Reuters Code KANE.BO

Shares Outstanding (mn) 53.9

Face Value 10

Mcap (INR bn) 47.2

52 Week H/L 1,055/720

2W Avg. Qty, BSE 1,207

Sensex 18,132.2

Y/E Mar (INR mn) FY09 FY10 FY11 FY12E FY13E

Net Sales 13,756.3 17,074.1 21,398.8 25,753.2 30,519.8

Growth (%) 4.2% 24.1% 25.3% 20.3% 18.5%

EBIDTAM (%) 11.5% 15.5% 13.6% 13.2% 13.9%

Adj. PAT 954.3 1,621.2 1,853.0 2,090.0 2,504.3

Growth (%) -20.3% 69.9% 14.3% 12.8% 19.8%

Adj. PATM (%) 6.9% 9.5% 8.7% 8.1% 8.2%

Adj. EPS (INR) 17.7 30.1 34.4 38.8 46.5

DPS 6.0 7.5 10.0 10.0 12.0

Dividend Yield (%) 0.7% 0.9% 1.1% 1.1% 1.4%

P/E (x) 49.4 29.1 25.4 22.6 18.8

P/BV (x) 7.2 6.1 5.1 4.4 3.8

EV/EBIDTA 30.3 18.2 16.5 14.1 11.4

Net Debt/Equity (0.4) (0.4) (0.4) (0.2) (0.2)

RoACE (%) 13.5% 20.0% 20.0% 19.5% 20.2%

RoANW (%) 15.3% 22.7% 21.9% 21.1% 21.8%

Relative share price performance

80

90

100

110

120

130

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr-

11

May

-11

KNP Sensex

Paint Industry

Sumit [email protected]. +91-22-4289 5600 Ext. 630

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary 21

CMP: INR 875 Recommendation: HOLD Target: INR 926

22

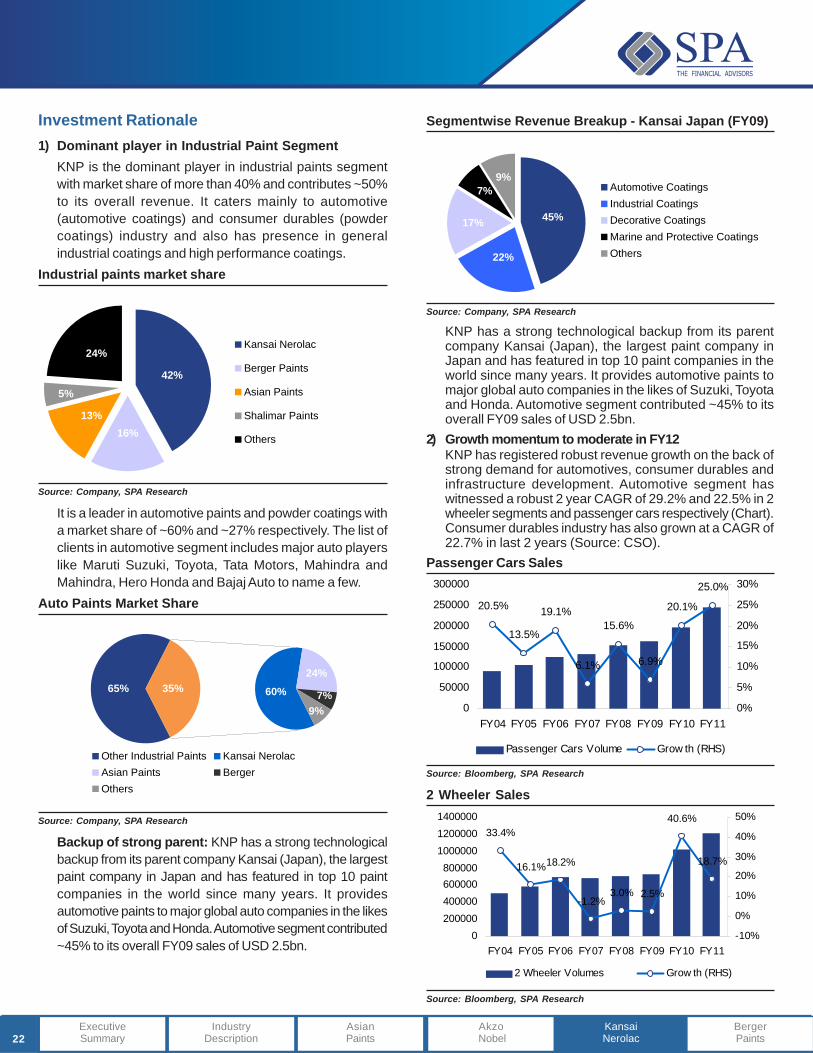

Investment Rationale1) Dominant player in Industrial Paint Segment

KNP is the dominant player in industrial paints segmentwith market share of more than 40% and contributes ~50%to its overall revenue. It caters mainly to automotive(automotive coatings) and consumer durables (powdercoatings) industry and also has presence in generalindustrial coatings and high performance coatings.

Industrial paints market share

16%13%

24%

42%

5%

Kansai Nerolac

Berger Paints

Asian Paints

Shalimar Paints

Others

Source: Company, SPA Research

It is a leader in automotive paints and powder coatings witha market share of ~60% and ~27% respectively. The list ofclients in automotive segment includes major auto playerslike Maruti Suzuki, Toyota, Tata Motors, Mahindra andMahindra, Hero Honda and Bajaj Auto to name a few.

Auto Paints Market Share

65% 35%

9%7%

24%

60%

Other Industrial Paints Kansai NerolacAsian Paints BergerOthers

Source: Company, SPA Research

Backup of strong parent: KNP has a strong technologicalbackup from its parent company Kansai (Japan), the largestpaint company in Japan and has featured in top 10 paintcompanies in the world since many years. It providesautomotive paints to major global auto companies in the likesof Suzuki, Toyota and Honda. Automotive segment contributed~45% to its overall FY09 sales of USD 2.5bn.

Segmentwise Revenue Breakup - Kansai Japan (FY09)

22%

45%

7%9%

17%

Automotive CoatingsIndustrial CoatingsDecorative CoatingsMarine and Protective CoatingsOthers

Source: Company, SPA Research

KNP has a strong technological backup from its parentcompany Kansai (Japan), the largest paint company inJapan and has featured in top 10 paint companies in theworld since many years. It provides automotive paints tomajor global auto companies in the likes of Suzuki, Toyotaand Honda. Automotive segment contributed ~45% to itsoverall FY09 sales of USD 2.5bn.

2) Growth momentum to moderate in FY12KNP has registered robust revenue growth on the back ofstrong demand for automotives, consumer durables andinfrastructure development. Automotive segment haswitnessed a robust 2 year CAGR of 29.2% and 22.5% in 2wheeler segments and passenger cars respectively (Chart).Consumer durables industry has also grown at a CAGR of22.7% in last 2 years (Source: CSO).

Passenger Cars Sales

20.5%

13.5%

19.1%

6.1%

15.6%

6.9%

20.1%

25.0%

0

50000

100000

150000

200000

250000

300000

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY110%

5%

10%

15%

20%

25%

30%

Passenger Cars Volume Grow th (RHS)

Source: Bloomberg, SPA Research

2 Wheeler Sales

33.4%

16.1%18.2%

-1.2%3.0% 2.5%

40.6%

18.7%

0200000400000600000800000

100000012000001400000

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11-10%

0%

10%

20%

30%

40%

50%

2 Wheeler Volumes Grow th (RHS)

Source: Bloomberg, SPA Research

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

23

Based on estimates of SIAM, four wheeler segment isexpected to grow at ~16% and 2 Wheeler segment at ~12%in volume terms in FY12 after reporting more than 20%volume CAGR in last two years. In line with expectedslowdown in auto segment and other industrial segmentsin the current year, we expect KNP revenue growth to slowdown to 20.3% in FY12 from 25.3% in FY11 on back oflower volume growth. Further we expect volume growth topick up in FY13 but lower value growth component to resultrevenue to grow at 18.5% in FY13 to INR 30,519.8mn.

Net Sales Trend

4.2%

24.1% 25.3%

20.3%18.3%

05000

100001500020000250003000035000

FY09 FY10 FY11 FY12E FY13E0%

5%

10%

15%

20%

25%

30%

Net Sales (INR mn) Grow th (RHS)

Source: Company, SPA Research

3) Focus towards increasing Decorative PaintscontributionKNP has a market share of ~14% in decorative paintssegment and contributes another 50% to its overall revenue.KNP offers products across all categories through somerenowned brands like Nerolac Impressions, Pearls, Beauty,Suraksha and Excel (Chart).

Product Category BrandsInterior Emulsions Impression, BeautyExterior Emulsion Suraksha, ExcelEnamels Impressions, Satin, SyntheticDistempers Beauty, Pearls

Source: Company, SPA Research

In decorative paint segment, emulsions contribute around 32%,Enamels 25% and distemper 12%. Remaining is contributedby primers, putty, fillers etc. Similar for the industry, emulsionsare growing at faster rate and have higher margins comparedto other paints.

Kansai (India) Revenue Breakup

50% 50%31%

12%25%

32%

Industrial Paints Emulsions

Enamles Distempers

Others (primers, putty, fillers etc)

Source: Company, SPA Research

Decorative segment has short cycle of payment which reducesworking capital needs and ability to pass higher raw materialcost inflation compared to industrial paints segment. Companywas able to pass 80% of raw material cost increases indecorative segment while passing the cost increase in industrialsegment comes with a lag due to long term contracts withinstitutions. Also, in industrial paints segment there is continuouspressure from the companies to reduce cost of paints. Companyhas plans to increase sales in decorative segment by launchingaggressive nationwide campaign and increasing distributionreach. KNP recently roped in Shahrukh Khan to promote itsproduct in decorative segment.

Increasing reach: Traditionally it has higher presence in northmarkets which contributes 26% to overall decorative paintindustry sales. Company however has aggressive plans toincrease its presence in south markets and increase its sharefrom decorative segment in its overall revenue. Kansai hasplanned to open 30 new exclusive Nerolac brand stores in southto increase awareness of products. It also setting up itsmanufacturing facility is Hosur, Tamil Nadu to improve itsdistribution reach in the south markets.

4) Increasing capacity on higher demand anticipationKNP is the second largest player in India and has an overallmarket share of ~18% in the paint industry. In order to fulfillhigher demand for paints both in industrial and decorativesegments, company plans to add ~0.1mn MT of capacityto its current capacity of ~0.2mn MT/annum. In order toincrease the capacity company is setting up a greenfieldplant in Hosur (TN) at an estimated capex of ~INR 6bn. Theplant is expected to be fully commissioned by FY13.

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

24

Capacity & Utilization

69.4% 69.0%78.4%

87.2% 84.8% 86.3%

050000

100000150000200000250000300000350000

FY08 FY09 FY10 FY11 FY12 FY130%

20%

40%

60%

80%

100%

Capacity Utilization (RHS)

Source: Company, SPA Research

Investment Concerns1) Rising raw material cost

KNP is at higher margin erosion risk compared to otherplayers in the industry in the environment of high raw materialcost inflation. Company has highest raw material as a %net sales among the paint companies under our coverage.

Raw material as a % of sales (FY11)

52.7%57.7%

63.7% 65.4%

0%

10%

20%

30%

40%

50%

60%

70%

Akzo Nobel Asian Paints Berger KansaiNerolac

Source: Company, SPA Research

RM breakup (FY10)

53%

6%

34%

7% Pigments, Extenders and ResinsOrganic Acids and AnhydridesSolvents, Oils and Fatty AcidsOthers

Source: Company, SPA Research

Due to 50% contribution from industrial paints segment andlong term nature of contracts, company is not able toimmediately pass the raw material cost to its institutional

clients which affect its margins. In decorative paintssegment, company was able to pass 80% of cost inflationin FY11. Increase in cost of key raw material like titaniumdioxide and crude based derivatives by ~29% and ~40%in FY11 resulted in gross profit margins falling by 267 bpsfrom 37.2% to 34.6%. Company however is intending totake calibrated price hike in contracts in industrial segment.

2) Rising competitionWith increasing competitive environment in the paintindustry, KNP like all other players is at risk of losing marketshare to other competitors.

Financial OverviewCompany's revenue has grown at a 2 year CAGR of 24.7% toINR 21,398.8mn in FY11. Going forward, with expected slowdownin automotive industry on back of rising fuel prices and interestrate cost along with some slowdown in other industrial segment,we expect company to witness a moderate growth in revenuescompared to last two years. We expect its revenue and profitto grow at a 2 year CAGR of 19.4% and 16.3% in next twoyears to INR 30,519.8mn and INR 2,504.3mn respectively.

Net Sales Trend

4.2%

24.1% 25.3%

20.3%18.3%

05000

100001500020000250003000035000

FY09 FY10 FY11 FY12E FY13E0%

5%

10%

15%

20%

25%

30%

Net Sales (INR mn) Grow th (RHS)

S

APAT Trend

-20.0%

69.7%

15.4% 11.4%19.4%

0

500

1000

1500

2000

2500

3000

FY09 FY10 FY11 FY12E FY13E-40%

-20%

0%

20%

40%

60%

80%

APAT (INR mn) Grow th (RHS)

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

25

Due to continued pressure on raw material cost, we expectcompany's EBIDTA margins to shrink by 38bps YoY in FY12,cushioned partly by passing on raw material cost inflation butregain 63bps in FY13 on back of expected improvement ineconomic environment.

Margin Trend

KNP has been able to maintain good return profile of morethan 20% in last two years. We expect company to continueto maintain more than 20% return on average networth(RoANW) in next 2 years.

KNP has been able to maintain good return profile of morethan 20% in last two years. We expect company to continueto maintain more than 20% return on average networth(RoANW) in next 2 years.

KNP has been able to maintain good return profile of morethan 20% in last two years. We expect company to continueto maintain more than 20% return on average networth(RoANW) in next 2 years.

Return Profile

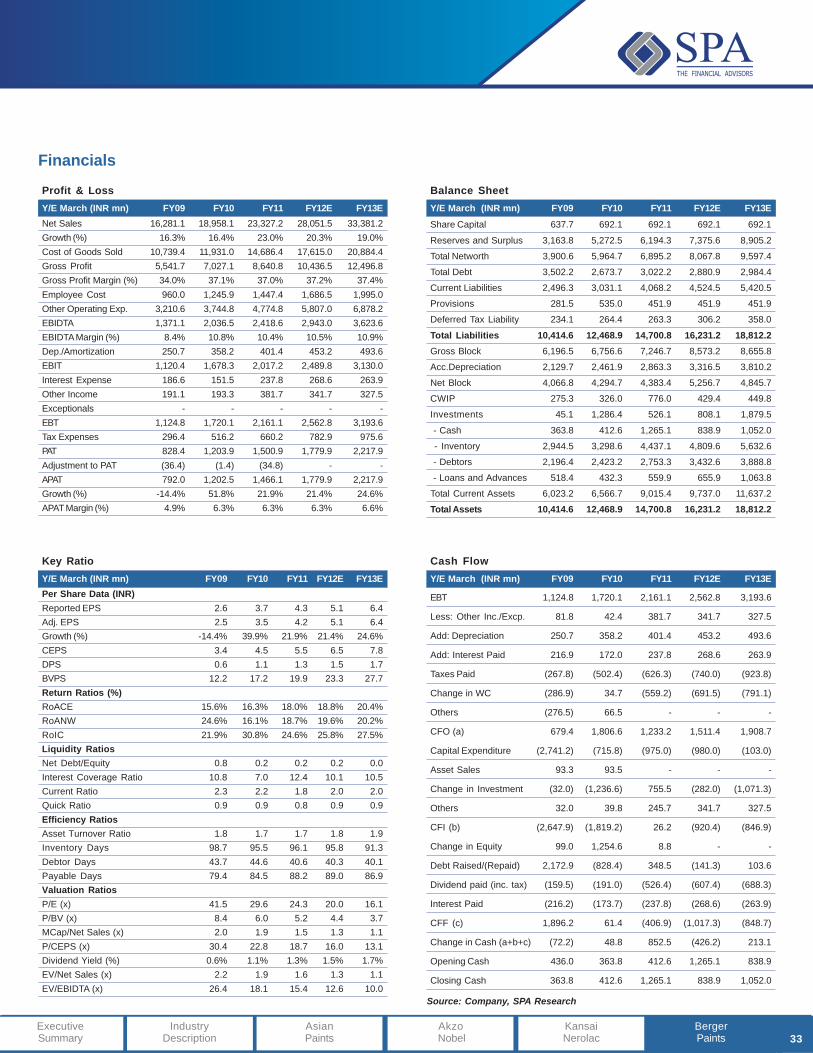

ValuationsKansai Nerolac is expected to maintain its dominant share inindustrial paints segment and benefit from strong growth ofautomotive and consumer durables industry. Also, withcompany's focus to increase contribution from decorative paintsegment will reduce RM cost pressure due to better ability topass cost through price increases. We expect KNP to grow atrevenue CAGR of 19.3% in the next two years. On back oflong term growth in industrial segment and dominant positionof KNP in industrial paints, we value the stock at 20x FY13E.This works out to be a 1 year target price of INR 926 with anupside of 6% from CMP of INR 875. We therefore, initiate thecoverage with a Hold rating.

IndustryDescription

AsianPaints

Akzo Nobel

KansaiNerolac

BergerPaints

ExecutiveSummary

13.5%

20.0% 20.0% 19.5% 20.1%15.4%

22.8% 22.2% 21.1% 21.7%

5%