Page 1 of 54 WTM/PS/70/ISD/JAN/2014 BEFORE THE SECURITIES AND EXCHANGE BOARD OF INDIA CORAM: PRASHANT SARAN, WHOLE TIME MEMBER ORDER Under Regulation 28 (2) read with Regulation 38 (2) of the Securities and Exchange Board of India (Intermediaries) Regulations, 2008 IN THE MATTER OF IRREGULARITIES IN INITIAL PUBLIC OFFERING In respect of Karvy Stock Broking Limited, Depository Participant [SEBI Registration Nos. IN-DP-NSDL-247-2005 and IN-DP-CDSL-305-2005] ___________________________________________________________________________ 1. Securities and Exchange Board of India (hereinafter referred to as ‘SEBI’) conducted a preliminary examination, upon noticing certain irregularities with respect to the Initial Public Offerings (hereinafter referred to as 'IPO') of different companies. A few individuals/ entities (referred to as 'the key operators') had opened various demat accounts (hereinafter referred to as 'afferent accounts') in fictitious/ benami names and made large number of applications in the IPOs in the category of retail investors in fictitious/ benami names (each of the applications being of small value as to make it eligible for allotment under the retail category). These key operators were found to have cornered/ acquired the IPO shares by making fictitious applications in the retail category through various fictitious/ benami applicants. Pursuant to the allotment, the shares were transferred to the demat account of these key operators. Further, it was also revealed that these key operators had transferred the shares through off-market deals to ultimate beneficiaries, who were the financiers in the process. The preliminary examination inter alia revealed that the depository participant namely Karvy Stock Broking Limited (hereinafter referred to as the 'Karvy DP') had opened various demat accounts in the fictitious/ benami names and aided and abetted various key operators to corner the shares in the IPO. 2. Pursuant to the preliminary investigation, SEBI issued the order dated December 15, 2005 in the IPO of Yes Bank and inter alia directed NSDL to undertake a comprehensive inspection of Karvy DP. Vide this order, Karvy DP was directed to fully co-operate with NSDL in the above inspection. NSDL was directed to submit a report to SEBI detailing the findings of its inspection in a time-bound manner. Further, SEBI issued another order dated January 12, 2006, in the IPO of Infrastructure Development Finance Company Limited (hereinafter referred to as 'IDFC') directing inter alia Karvy DP to complete the

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Page 1 of 54

WTM/PS/70/ISD/JAN/2014

BEFORE THE SECURITIES AND EXCHANGE BOARD OF INDIA CORAM: PRASHANT SARAN, WHOLE TIME MEMBER

ORDER

Under Regulation 28 (2) read with Regulation 38 (2) of the Securities and Exchange Board of India (Intermediaries) Regulations, 2008 IN THE MATTER OF IRREGULARITIES IN INITIAL PUBLIC OFFERING In respect of Karvy Stock Broking Limited, Depository Participant [SEBI Registration Nos. IN-DP-NSDL-247-2005 and IN-DP-CDSL-305-2005] ___________________________________________________________________________

1. Securities and Exchange Board of India (hereinafter referred to as ‘SEBI’) conducted a

preliminary examination, upon noticing certain irregularities with respect to the Initial

Public Offerings (hereinafter referred to as 'IPO') of different companies. A few

individuals/ entities (referred to as 'the key operators') had opened various demat accounts

(hereinafter referred to as 'afferent accounts') in fictitious/ benami names and made large

number of applications in the IPOs in the category of retail investors in fictitious/ benami

names (each of the applications being of small value as to make it eligible for allotment under the retail

category). These key operators were found to have cornered/ acquired the IPO shares by

making fictitious applications in the retail category through various fictitious/ benami

applicants. Pursuant to the allotment, the shares were transferred to the demat account of

these key operators. Further, it was also revealed that these key operators had transferred

the shares through off-market deals to ultimate beneficiaries, who were the financiers in the

process. The preliminary examination inter alia revealed that the depository participant

namely Karvy Stock Broking Limited (hereinafter referred to as the 'Karvy DP') had

opened various demat accounts in the fictitious/ benami names and aided and abetted

various key operators to corner the shares in the IPO.

2. Pursuant to the preliminary investigation, SEBI issued the order dated December 15, 2005

in the IPO of Yes Bank and inter alia directed NSDL to undertake a comprehensive

inspection of Karvy DP. Vide this order, Karvy DP was directed to fully co-operate with

NSDL in the above inspection. NSDL was directed to submit a report to SEBI detailing

the findings of its inspection in a time-bound manner. Further, SEBI issued another order

dated January 12, 2006, in the IPO of Infrastructure Development Finance Company

Limited (hereinafter referred to as 'IDFC') directing inter alia Karvy DP to complete the

Page 2 of 54

process of verifying the identity and address of the dematerialized account holders and to

close/ freeze the dematerialized accounts where they are unable to do the verification not

later than January 31, 2006; to put in place systems and procedures to ensure that in future

no non-genuine dematerialized accounts are opened by them. Karvy DP vide the said order

was asked to submit a detailed report to SEBI narrating the actions taken by them in this

regard and further not to open new dematerialized accounts till the submission of the said

report. Karvy DP was also asked to submit an undertaking to SEBI and obtaining a no-

objection from SEBI for accepting fresh business as a DP.

In the meantime, SEBI had issued another interim order on April 27, 2006 inter alia directing

Karvy DP as under:

"17.4. ... The following financiers of the master account holders are hereby directed not to buy, sell or deal in securities market including in IPOs, directly or indirectly, till further directions: 1. ... 2. .. ... 84. Karvy Stock Broking Limited 85. ... ... 17.7. … I direct that Karvy DP and Pratik DP shall not carry on the activities as DP till the completion of enquiry and passing of final order, excepting for effecting transfer of BO account to another SEBI registered DP on request. Notwithstanding this direction, Karvy DP and Pratik DP shall continue to be governed by the SEBI (Depositories and Participants) Regulations, 1996 and other applicable legal provisions in other respects. 17.8. Since the other business groups of Karvy have appeared to have acted in concert in the gamut of the IPO manipulations, I further direct Karvy Stock Broking Ltd., Karvy Computershare Pvt. Ltd., Karvy Investor Services Ltd. and Karvy Consultants Ltd. not to undertake fresh business as a Registrar to Issue and Share transfer agent, excepting those businesses already contracted as on date."

Subsequent to the personal hearing to Karvy DP, SEBI passed the order dated May 26,

2006, wherein Karvy DP was directed not to act as a DP, pending enquiry and passing of

final orders, except for acting on the instructions of existing beneficial owners (hereinafter

referred to as 'BO'). Karvy DP was also directed to transfer the demat account of an

existing BO to another SEBI registered DP, on request.

3. In the meantime, SEBI had initiated Enquiry proceedings against Karvy DP, being a

registered intermediary, in terms of the Enquiry Regulations, by appointing an Enquiry

Officer under Regulation 5(1) of the Enquiry Regulations vide orders dated May 25, 2006 and

Page 3 of 54

September 18, 2006. The Enquiry Officer enquired into the alleged violation of the Securities

and Exchange Board of India Act, 1992 (hereinafter referred to as the ‘SEBI Act’), the SEBI

(Prohibition of Fraudulent and Unfair Trade Practices Relating to Securities Market)

Regulations, 2003 (hereinafter referred to as the 'PFUTP Regulations'), SEBI (Depositories

and Participants) Regulations, 1996 (hereinafter referred to as 'DP Regulations') and the

provisions of the SEBI (Criteria for Fit and Proper Persons) Regulations, 2004 (hereinafter

referred to as 'Fit and Proper Regulations').

4. The Enquiry Officer in his report dated March 30, 2007, found that Karvy DP had

contravened the provisions of Section 12 A(a), (b) and (c) of the SEBI Act, Regulations 3,

4(1) and 4(2)(p) of the PFUTP Regulations, Regulations 19, 42, 43, 46 and 52 of the DP

Regulations read with Clauses 3, 9, 12, 16, 19, 20 and 22 of the Code of Conduct as specified

in the third schedule under Regulation 20A of the DP Regulations and the provisions under

the Depositories Act, 1996 (hereinafter referred to as the 'DP Act') and SEBI (Disclosure and

Investor Protection) Guidelines, 2000 (hereinafter referred to as 'DIP Guidelines') and

recommended that Karvy DP be prohibited from acting as a DP for a period of 18 months.

The Enquiry Officer later clarified that the prohibition of 18 months recommended by him

against Karvy DP was in respect of taking up new assignment/ fresh business as a DP. The

Enquiry Officer also recommended that the period of prohibition already undergone by the

DP as per the interim orders of SEBI be considered, for the purpose of computing the period

of prohibition recommended by him.

5. Pursuant to the Enquiry Report, SEBI issued a Show Cause Notice (hereinafter referred to

as 'SCN') dated May 04, 2007 to Karvy DP along with a copy of the Enquiry Report,

advising it to show cause as to why the penalty recommended by the Enquiry Officer may

not be enhanced as considered fit by SEBI. Karvy DP sent a reply vide its letter dated May 19,

2007.

6. SEBI had initiated enquiry proceedings against two other entities of the Karvy group, viz.,

Karvy Stock Broking Limited (in the capacity as a Stock Broker) (hereinafter referred to as

'KSBL') and Karvy Computershare Pvt. Limited (Registrar to an Issue) also. On June 22, 2007,

SEBI passed a common order (hereinafter referred to as 'earlier SEBI order') in respect of all

Karvy entities including Karvy DP containing the following directions:

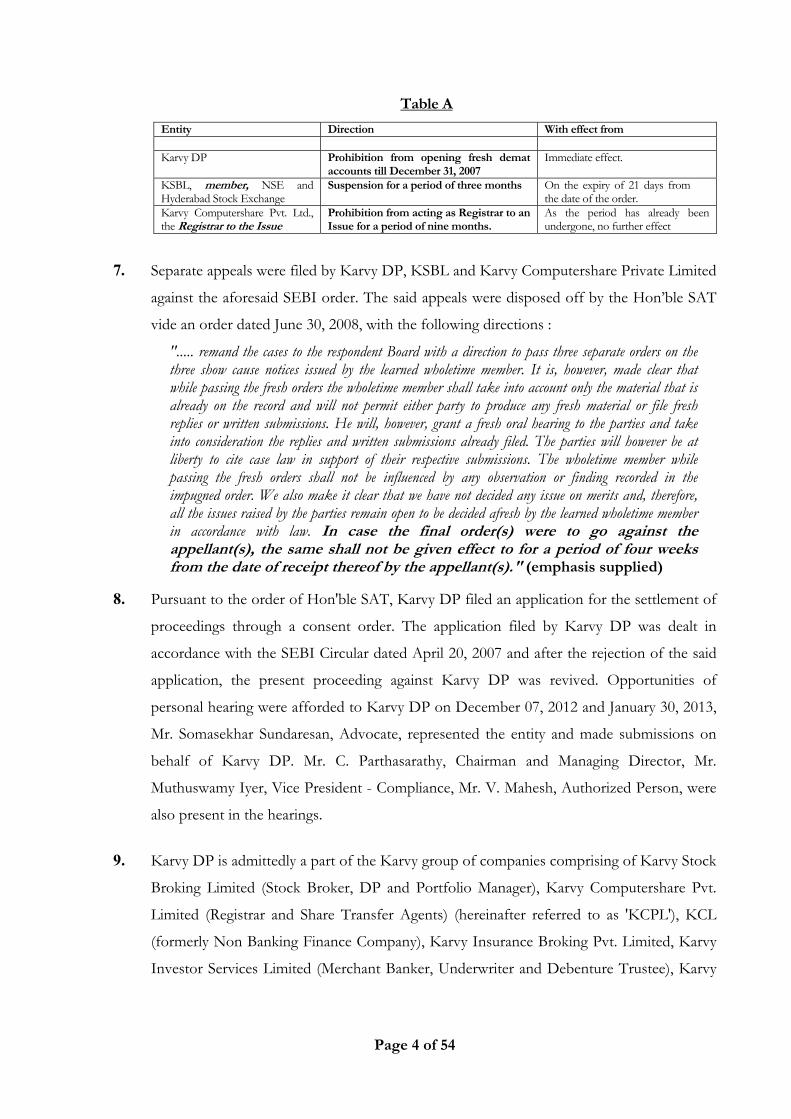

Page 4 of 54

Table A

Entity Direction With effect from Karvy DP Prohibition from opening fresh demat

accounts till December 31, 2007 Immediate effect.

KSBL, member, NSE and Hyderabad Stock Exchange

Suspension for a period of three months On the expiry of 21 days from the date of the order.

Karvy Computershare Pvt. Ltd., the Registrar to the Issue

Prohibition from acting as Registrar to an Issue for a period of nine months.

As the period has already been undergone, no further effect

7. Separate appeals were filed by Karvy DP, KSBL and Karvy Computershare Private Limited

against the aforesaid SEBI order. The said appeals were disposed off by the Hon’ble SAT

vide an order dated June 30, 2008, with the following directions :

"..... remand the cases to the respondent Board with a direction to pass three separate orders on the three show cause notices issued by the learned wholetime member. It is, however, made clear that while passing the fresh orders the wholetime member shall take into account only the material that is already on the record and will not permit either party to produce any fresh material or file fresh replies or written submissions. He will, however, grant a fresh oral hearing to the parties and take into consideration the replies and written submissions already filed. The parties will however be at liberty to cite case law in support of their respective submissions. The wholetime member while passing the fresh orders shall not be influenced by any observation or finding recorded in the impugned order. We also make it clear that we have not decided any issue on merits and, therefore, all the issues raised by the parties remain open to be decided afresh by the learned wholetime member in accordance with law. In case the final order(s) were to go against the appellant(s), the same shall not be given effect to for a period of four weeks from the date of receipt thereof by the appellant(s)." (emphasis supplied)

8. Pursuant to the order of Hon'ble SAT, Karvy DP filed an application for the settlement of

proceedings through a consent order. The application filed by Karvy DP was dealt in

accordance with the SEBI Circular dated April 20, 2007 and after the rejection of the said

application, the present proceeding against Karvy DP was revived. Opportunities of

personal hearing were afforded to Karvy DP on December 07, 2012 and January 30, 2013,

Mr. Somasekhar Sundaresan, Advocate, represented the entity and made submissions on

behalf of Karvy DP. Mr. C. Parthasarathy, Chairman and Managing Director, Mr.

Muthuswamy Iyer, Vice President - Compliance, Mr. V. Mahesh, Authorized Person, were

also present in the hearings.

9. Karvy DP is admittedly a part of the Karvy group of companies comprising of Karvy Stock

Broking Limited (Stock Broker, DP and Portfolio Manager), Karvy Computershare Pvt.

Limited (Registrar and Share Transfer Agents) (hereinafter referred to as 'KCPL'), KCL

(formerly Non Banking Finance Company), Karvy Insurance Broking Pvt. Limited, Karvy

Investor Services Limited (Merchant Banker, Underwriter and Debenture Trustee), Karvy

Page 5 of 54

Comtrade Broking Limited, Karvy Global Services Limited, Karvy Financial Services

Limited and Karvy Inc. (Broker dealer of NASDAQ, USA).

10. Before discussing the charges leveled against Karvy DP in the SCN, let me deal with the

preliminary arguments of Karvy DP:-

a. Action against KCL and not against Karvy DP

The alleged violation in the instant case pertains to the period 2003-2005, when KCL was

the registered DP. Karvy DP in its submissions before SEBI has argued that it cannot be

held liable for the violations committed by KCL. The responsibility, if any, is for the acts

done by KCL in its capacity as a DP and not as a Non Banking Financial Company

('NBFC'). It also said that only the business obligations of KCL was taken over by it and

not the proceedings in connection with any alleged violation committed by KCL.

In this regard, I note that KCL was acting as a DP till September 10, 2005 in NSDL and till

November 29, 2005 in CDSL. Majority of the accounts of the key operators were opened

in NSDL, by August 05, 2005 and in CDSL, by September 22, 2005 and this was during the

period when KCL was a DP. I note that NSDL vide its letter dated June 16, 2005, had also

informed SEBI about the intention of KCL to transfer its DP business to Karvy DP.

Karvy DP has inter alia stated that KCL was one of its group companies and pursuant to

the transfer arrangement, the infrastructure of KCL would be used by Karvy DP.

Thereafter, Karvy DP had started the business of DP by taking over the DP business from

KCL.

I note from the Enquiry Report that the transfer of DP business from KCL to Karvy DP

was approved by SEBI, subject to the covenant for taking over all the assets and liabilities/

obligations, including pending disputes/ grievances of the investors holding DP accounts

with KCL by Karvy DP. Karvy DP in its written submissions has relied upon the judgment

of the Hon'ble High Court of Judicature at Bombay in the matter of SEBI Vs. SKDC

Consultants Limited and argued that it cannot be held liable for the alleged violations

committed by KCL. However, in the instant case, the facts differ, in view of the covenant

discussed above. Therefore, Karvy DP is responsible for the past acts of KCL in view of

the important covenant with Karvy DP about taking over all the assets and liabilities/

obligations, including pending disputes/ grievances of the investors holding DP accounts

with KCL.

Page 6 of 54

Karvy DP has said that the charges in the SCN pertain to financing done by KCL in the

IPO as an NBFC. I would like to emphasize that the present SCN is in respect of the

activities as a DP. As the DP activities of Karvy were handled by KCL prior to the transfer

of business to Karvy DP, the names, KCL and Karvy DP are interchangeably referred/

used in the present order.

b. Enhancement of penalty from that recommended by the Enquiry Officer

With respect to the issue of enhancement of penalty from that recommended by the

Enquiry Officer, the submissions of Karvy DP were that:-

(i) by deciding that the case warrants a higher penalty than what is recommended by the

Enquiry Officer, the principles of natural justice have been discarded.

(ii) SEBI cannot consider any fresh allegations at such stage based on thenew materials

supplied along with the SCN.

In this regard, my observations are as under: the designated member need not restrict

himself to the penalties recommended by the designated authority/ Enquiry Officer. The

powers of the Chairman/ Member while considering the Enquiry Report are sufficiently

wide. Further, the penalty recommended by the Enquiry Officer can either be enhanced or

reduced, depending on the specific facts and circumstances of the case. Regulation 28(1) of

the SEBI (Intermediaries) Regulations, 2008 read with SEBI (Procedure for Holding

Enquiry) Regulations, 2002 (now repealed) empowers the designated member to arrive at a

conclusion different from that of the Enquiry Report. Whenever SEBI is of the view that

the role of the entity under enquiry is serious and that the recommended penalty has to be

enhanced in order to make it commensurate with the violation, a fair opportunity of

defence to the noticee shall precede the contemplated action.

With respect to the allegation of having brought in fresh material post enquiry, I note that

the Enquiry Officer in his report has referred to the material that is alleged to be new by

Karvy DP. However, in the current proceedings, no material is being relied upon which has

not been provided to Karvy DP. Subsequently, Karvy DP has replied to the SCN vide its

letter dated May 19, 2007 and further on June 06, 2007, the written submissions were filed.

Therefore, the principles of natural justice have been duly complied with as Karvy DP has

got the opportunity to defend itself against the allegations leveled in the SCN.

Page 7 of 54

11. In exercise of the quasi-judicial power conferred on me under Section 19 of the SEBI Act,

1992, I, now proceed to consider the SCN, replies/ written submissions and the material

relied upon in the SCN. The SCN dated May 04, 2007, alleged that:-

a. Karvy group companies were acting in concert with each other and were fully aware of

the fictitious/ benami nature of the applicants to whom finance was extended after the

closure of the IPOs.

b. There was no arms' length distance maintained between the group companies of Karvy

which had acted in concert in aiding and abetting the key operators in opening fictitious

demat accounts and providing finance in the name of fictitious/ benami applicants with

the manipulative, deceptive and fraudulent intent to corner the shares in IPOs.

Therefore, the important issues that need to be considered and decided by me in the instant

order are the following:

a. Whether Karvy DP had aided and abetted the key operators in opening of the afferent

accounts and cornering of the shares in the IPO?

b. Whether Karvy DP has failed to maintain arm's length distance between the different

activities of its group entities and in its failure to do so, it acted in complicity with the

other entities of the Karvy group?

12. Whether Karvy DP had aided and abetted the key operators in the opening of the

afferent accounts and cornering of the shares in the IPO?

A broader picture of the role of Karvy DP in the alleged irregularities in the IPO process is

described below. It is an admitted fact that Karvy group entities were associated in various

IPOs, in different roles that are required to be performed in relation to an IPO application.

Starting with the role of DP who opened demat accounts, that of the NBFC who arranged

finance, the stock broker/ syndicate member who undertook the bidding in IPOs and also

that of the Registrar to Issue (hereinafter referred to as 'RTI') who prepared refunds and

further, transferred the shares from the demat account of allottees to the demat account of

the key operator again in the capacity of DP and sale of shares through its stock broking

arm, one is able to identify the presence of Karvy group entities in the entire scheme of

activities of the IPOs.

The different roles of Karvy group are discussed elaborately here, in the sequence of the

events that followed. To begin with, KCL, the financier belonging to the Karvy group

(KCL was also a DP at such point of time) had floated an IPO financing scheme in association

with BhOB, as evident from the copy of the "Idea Paper and Process Flow for Funding

Page 8 of 54

Options for Maruti IPO by Bharat Overseas Bank and Karvy Services" (hereinafter

referred to as 'Idea Paper'), released during June, 2003. I have perused the 'Idea Paper' and

note that the same contains the process flow which starts from the IPO applications, the

opening of demat accounts, bank accounts, procedure for refunds etc. It also states about

the safeguards like marking of lien on the shares until the loan is cleared. I note that as per

the process flow explained in the 'Idea Paper', IPO applications would be filled in by the

investor and a cheque/ DD in favour of the bank towards the margin amount shall be

deposited. The investor would need to open the demat account with Karvy DP with the

bank as joint holder. Karvy DP would then place a lien on the shares deposited into the

investor's account until the investor clears the loan with the bank. The client would deposit

the payment instrument and bid form with the bank along with the account opening

document and documents for the loan. Further, the bank would issue the pay order for the

amount of the application by debiting such amount from the loan account, while taking

into account the amount of margin money of the respective applicants. If the investor is

not allotted shares against the IPO application, refunds would be made to investor by the

RTI through the bank and the refund will be credited to the account, after liquidating the

loan. On allotment, the investor should bring in the required amount if there is shortfall

and fulfil the obligation to the bank after which the lien is released by the bank and the DP

is accordingly informed.

In this context, Karvy DP has argued in its reply that 'Idea Paper' was only a proposal and

that it was not followed in its entirety. However, the facts of the present case show that the

different steps perceived in the 'Idea Paper' did actually materialize, till the end, as seen

from the details that are discussed hereunder:

a. Role in the opening of bank accounts

i. SEBI has noticed that different Karvy entities such as KCL and KSBL had a role in the

opening of the bank accounts for availing finance and making application in the IPOs.

The SCN alleges that the Karvy group entities have introduced certain account holders

at Bharat Overseas Bank (hereinafter referred to as 'BhoB'), Ahmedabad, which were

subsequently used for opening the demat accounts and thereafter to apply in the IPO.

In this regard, I refer to the letter of BhOB dated March 07, 2006 addressed to SEBI,

wherein a particular bank account bearing number 50795 has been discussed. It is

mentioned in this letter of BhoB that the account bearing no: '50795' was opened on

June 17, 2003 for the purpose of availing finance in the IPO of Maruti Udyog Limited

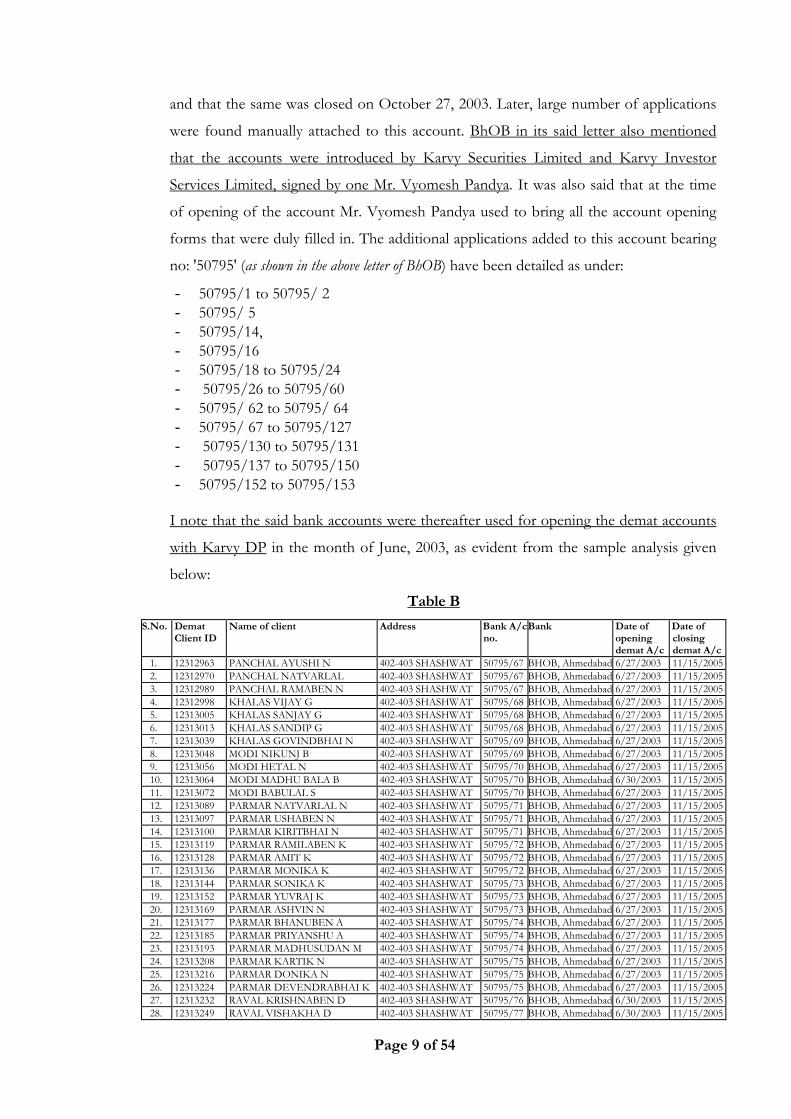

Page 9 of 54

and that the same was closed on October 27, 2003. Later, large number of applications

were found manually attached to this account. BhOB in its said letter also mentioned

that the accounts were introduced by Karvy Securities Limited and Karvy Investor

Services Limited, signed by one Mr. Vyomesh Pandya. It was also said that at the time

of opening of the account Mr. Vyomesh Pandya used to bring all the account opening

forms that were duly filled in. The additional applications added to this account bearing

no: '50795' (as shown in the above letter of BhOB) have been detailed as under:

- 50795/1 to 50795/ 2 - 50795/ 5 - 50795/14, - 50795/16 - 50795/18 to 50795/24 - 50795/26 to 50795/60 - 50795/ 62 to 50795/ 64 - 50795/ 67 to 50795/127 - 50795/130 to 50795/131 - 50795/137 to 50795/150 - 50795/152 to 50795/153

I note that the said bank accounts were thereafter used for opening the demat accounts

with Karvy DP in the month of June, 2003, as evident from the sample analysis given

below:

Table B

S.No. Demat Client ID

Name of client Address Bank A/c no.

Bank Date of opening demat A/c

Date of closing demat A/c

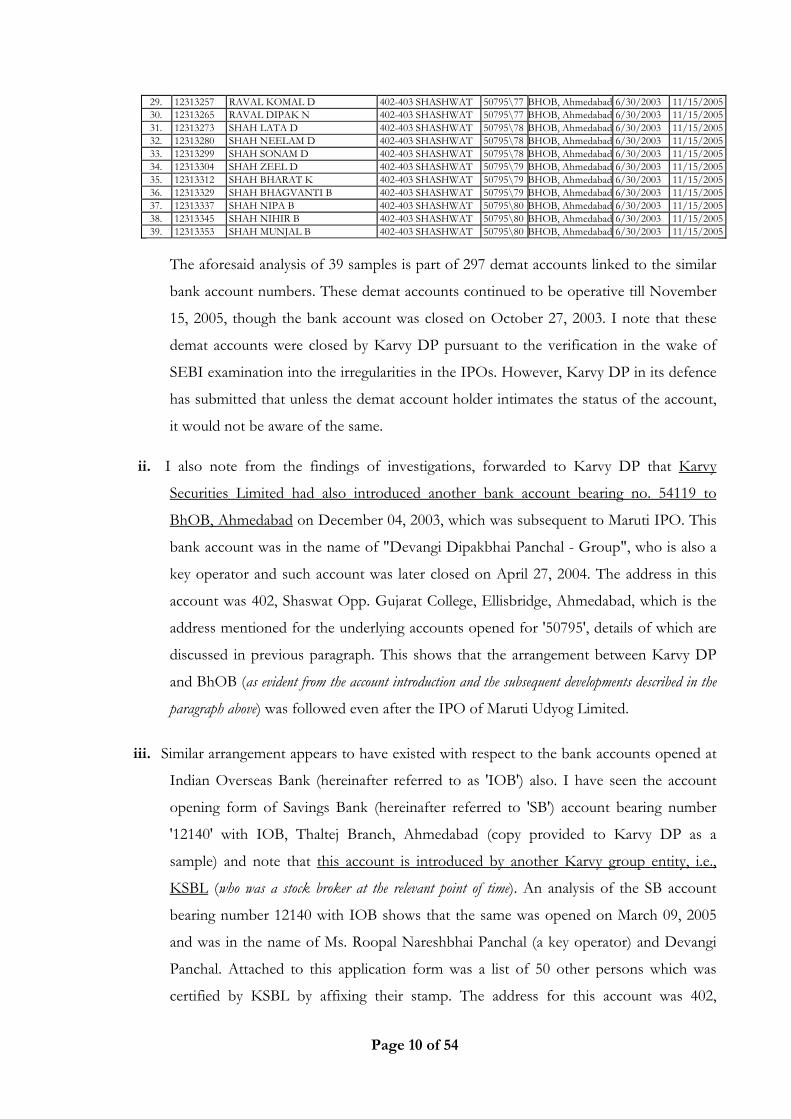

1. 12312963 PANCHAL AYUSHI N 402-403 SHASHWAT 50795/67 BHOB, Ahmedabad 6/27/2003 11/15/20052. 12312970 PANCHAL NATVARLAL 402-403 SHASHWAT 50795/67 BHOB, Ahmedabad 6/27/2003 11/15/20053. 12312989 PANCHAL RAMABEN N 402-403 SHASHWAT 50795/67 BHOB, Ahmedabad 6/27/2003 11/15/20054. 12312998 KHALAS VIJAY G 402-403 SHASHWAT 50795/68 BHOB, Ahmedabad 6/27/2003 11/15/20055. 12313005 KHALAS SANJAY G 402-403 SHASHWAT 50795/68 BHOB, Ahmedabad 6/27/2003 11/15/20056. 12313013 KHALAS SANDIP G 402-403 SHASHWAT 50795/68 BHOB, Ahmedabad 6/27/2003 11/15/20057. 12313039 KHALAS GOVINDBHAI N 402-403 SHASHWAT 50795/69 BHOB, Ahmedabad 6/27/2003 11/15/20058. 12313048 MODI NIKUNJ B 402-403 SHASHWAT 50795/69 BHOB, Ahmedabad 6/27/2003 11/15/20059. 12313056 MODI HETAL N 402-403 SHASHWAT 50795/70 BHOB, Ahmedabad 6/27/2003 11/15/200510. 12313064 MODI MADHU BALA B 402-403 SHASHWAT 50795/70 BHOB, Ahmedabad 6/30/2003 11/15/200511. 12313072 MODI BABULAL S 402-403 SHASHWAT 50795/70 BHOB, Ahmedabad 6/27/2003 11/15/200512. 12313089 PARMAR NATVARLAL N 402-403 SHASHWAT 50795/71 BHOB, Ahmedabad 6/27/2003 11/15/200513. 12313097 PARMAR USHABEN N 402-403 SHASHWAT 50795/71 BHOB, Ahmedabad 6/27/2003 11/15/200514. 12313100 PARMAR KIRITBHAI N 402-403 SHASHWAT 50795/71 BHOB, Ahmedabad 6/27/2003 11/15/200515. 12313119 PARMAR RAMILABEN K 402-403 SHASHWAT 50795/72 BHOB, Ahmedabad 6/27/2003 11/15/200516. 12313128 PARMAR AMIT K 402-403 SHASHWAT 50795/72 BHOB, Ahmedabad 6/27/2003 11/15/200517. 12313136 PARMAR MONIKA K 402-403 SHASHWAT 50795/72 BHOB, Ahmedabad 6/27/2003 11/15/200518. 12313144 PARMAR SONIKA K 402-403 SHASHWAT 50795/73 BHOB, Ahmedabad 6/27/2003 11/15/200519. 12313152 PARMAR YUVRAJ K 402-403 SHASHWAT 50795/73 BHOB, Ahmedabad 6/27/2003 11/15/200520. 12313169 PARMAR ASHVIN N 402-403 SHASHWAT 50795/73 BHOB, Ahmedabad 6/27/2003 11/15/200521. 12313177 PARMAR BHANUBEN A 402-403 SHASHWAT 50795/74 BHOB, Ahmedabad 6/27/2003 11/15/200522. 12313185 PARMAR PRIYANSHU A 402-403 SHASHWAT 50795/74 BHOB, Ahmedabad 6/27/2003 11/15/200523. 12313193 PARMAR MADHUSUDAN M 402-403 SHASHWAT 50795/74 BHOB, Ahmedabad 6/27/2003 11/15/200524. 12313208 PARMAR KARTIK N 402-403 SHASHWAT 50795/75 BHOB, Ahmedabad 6/27/2003 11/15/200525. 12313216 PARMAR DONIKA N 402-403 SHASHWAT 50795/75 BHOB, Ahmedabad 6/27/2003 11/15/200526. 12313224 PARMAR DEVENDRABHAI K 402-403 SHASHWAT 50795/75 BHOB, Ahmedabad 6/27/2003 11/15/200527. 12313232 RAVAL KRISHNABEN D 402-403 SHASHWAT 50795/76 BHOB, Ahmedabad 6/30/2003 11/15/200528. 12313249 RAVAL VISHAKHA D 402-403 SHASHWAT 50795/77 BHOB, Ahmedabad 6/30/2003 11/15/2005

Page 10 of 54

29. 12313257 RAVAL KOMAL D 402-403 SHASHWAT 50795\77 BHOB, Ahmedabad 6/30/2003 11/15/200530. 12313265 RAVAL DIPAK N 402-403 SHASHWAT 50795\77 BHOB, Ahmedabad 6/30/2003 11/15/200531. 12313273 SHAH LATA D 402-403 SHASHWAT 50795\78 BHOB, Ahmedabad 6/30/2003 11/15/200532. 12313280 SHAH NEELAM D 402-403 SHASHWAT 50795\78 BHOB, Ahmedabad 6/30/2003 11/15/200533. 12313299 SHAH SONAM D 402-403 SHASHWAT 50795\78 BHOB, Ahmedabad 6/30/2003 11/15/200534. 12313304 SHAH ZEEL D 402-403 SHASHWAT 50795\79 BHOB, Ahmedabad 6/30/2003 11/15/200535. 12313312 SHAH BHARAT K 402-403 SHASHWAT 50795\79 BHOB, Ahmedabad 6/30/2003 11/15/200536. 12313329 SHAH BHAGVANTI B 402-403 SHASHWAT 50795\79 BHOB, Ahmedabad 6/30/2003 11/15/200537. 12313337 SHAH NIPA B 402-403 SHASHWAT 50795\80 BHOB, Ahmedabad 6/30/2003 11/15/200538. 12313345 SHAH NIHIR B 402-403 SHASHWAT 50795\80 BHOB, Ahmedabad 6/30/2003 11/15/200539. 12313353 SHAH MUNJAL B 402-403 SHASHWAT 50795\80 BHOB, Ahmedabad 6/30/2003 11/15/2005

The aforesaid analysis of 39 samples is part of 297 demat accounts linked to the similar

bank account numbers. These demat accounts continued to be operative till November

15, 2005, though the bank account was closed on October 27, 2003. I note that these

demat accounts were closed by Karvy DP pursuant to the verification in the wake of

SEBI examination into the irregularities in the IPOs. However, Karvy DP in its defence

has submitted that unless the demat account holder intimates the status of the account,

it would not be aware of the same.

ii. I also note from the findings of investigations, forwarded to Karvy DP that Karvy

Securities Limited had also introduced another bank account bearing no. 54119 to

BhOB, Ahmedabad on December 04, 2003, which was subsequent to Maruti IPO. This

bank account was in the name of "Devangi Dipakbhai Panchal - Group", who is also a

key operator and such account was later closed on April 27, 2004. The address in this

account was 402, Shaswat Opp. Gujarat College, Ellisbridge, Ahmedabad, which is the

address mentioned for the underlying accounts opened for '50795', details of which are

discussed in previous paragraph. This shows that the arrangement between Karvy DP

and BhOB (as evident from the account introduction and the subsequent developments described in the

paragraph above) was followed even after the IPO of Maruti Udyog Limited.

iii. Similar arrangement appears to have existed with respect to the bank accounts opened at

Indian Overseas Bank (hereinafter referred to as 'IOB') also. I have seen the account

opening form of Savings Bank (hereinafter referred to 'SB') account bearing number

'12140' with IOB, Thaltej Branch, Ahmedabad (copy provided to Karvy DP as a

sample) and note that this account is introduced by another Karvy group entity, i.e.,

KSBL (who was a stock broker at the relevant point of time). An analysis of the SB account

bearing number 12140 with IOB shows that the same was opened on March 09, 2005

and was in the name of Ms. Roopal Nareshbhai Panchal (a key operator) and Devangi

Panchal. Attached to this application form was a list of 50 other persons which was

certified by KSBL by affixing their stamp. The address for this account was 402,

Page 11 of 54

Shashwat Opp. Gujarat College, Ellisbrdige, Ahmedabad – 380006, which is the same

address mentioned for the other discussed accounts i.e. 50795 and 54119 with BhOB as

discussed above.

It is strange to note that the list of 50 names attached with the account opening form

for the bank account bearing no. 12140 bear a common surname i.e. "SETH", starting

from 'SURESH SETH' and ending with 'ADITI SETH', and that the signatures of

these 50 are in English, Hindi and Gujarati and appear to have been signed by the same

person in similar manner. Further, the signature of the representative of KSBL on the

main bank account introduction column and that in the attached list of 50 names of one

Mr. Mayur Modi. On comparing the signature of Mayur Modi in the KYC form with

respect to account no. 12140 and the signature present in the list of 50 names attached

to that account, it is difficult to say that the signatures are different. Further, the same

Mayur Modi had signed on the introduction column (in the account opening form with respect

to bank account no. 12004 with IOB) on behalf of both KCL (now Karvy DP) and KSBL. I

have perused the affidavit dated June 02, 2007 of Mayur Modi filed before SEBI,

wherein he has denied that the signatures in the lists of 50 names appended to the

account opening forms pertaining to the savings bank account nos. 12140, 12149, 12150

and 12004 are not his. I have also perused the copy of his PAN card annexed with the

affidavit and the signature contained therein and the signatures in the lists containing the

50 names. On perusal, it can be said that in all these the signatures are done by Mayur

Modi with the normal variations in signatures of a person. It is important to bear in

mind that these 50 names in the attached list had their demat accounts with Karvy DP

in the same sequence (as that in the bank account opening form), the demat accounts

starting with BOID IN300394 13130266 - 'SURESH SETH' and ending with BOID

IN300394 13130776 - 'ADITI SETH', all of which were opened on January 05, 2004.

iv. I note that IOB had financed in the IPO of IDFC. The list of the names of the IPO

applicants starting from 'SURESH SETH' to 'ADITI SETH' in the allotment muster in

the IPO of IDFC is identical to the list of names attached to the IOB Thaltej branch

account opening form no. 12140. From an analysis of the demat account opening forms

of such persons at NSDL as submitted by Karvy DP, I note that the BhOB bank

account number 54119 is appearing as their bank account number. The details of the

observation have been tabled below:

Page 12 of 54

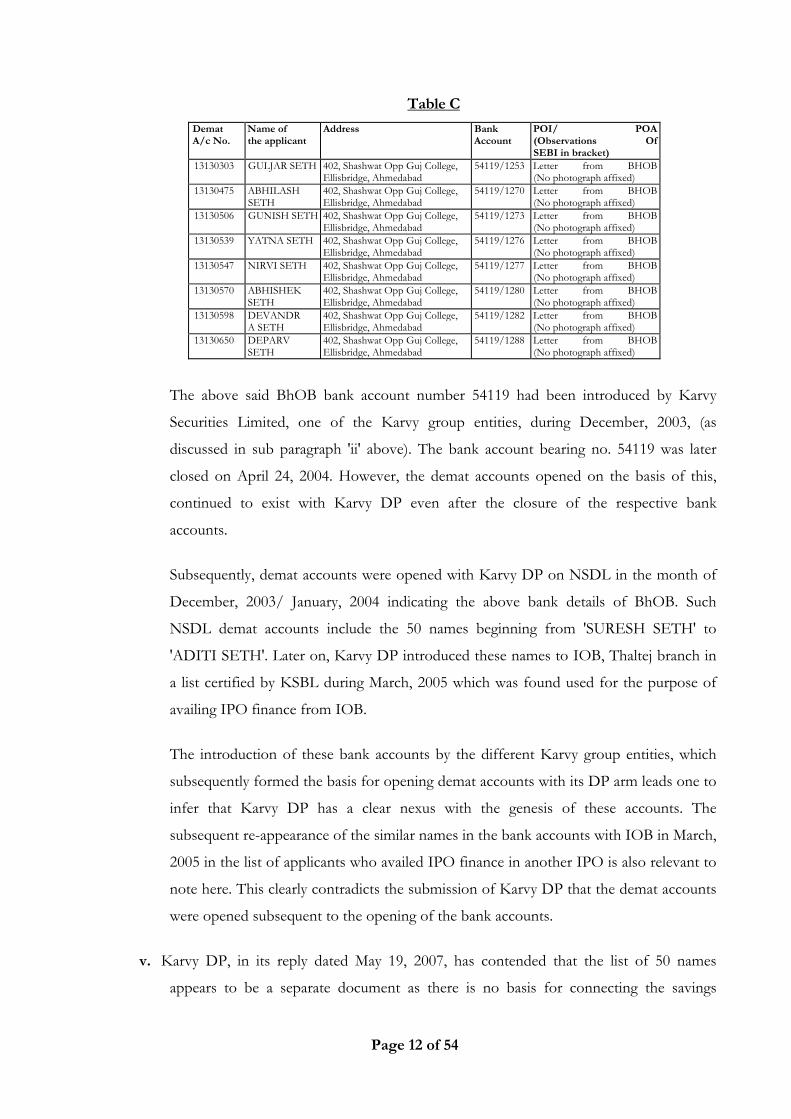

Table C

Demat A/c No.

Name of the applicant

Address Bank Account

POI/ POA(Observations OfSEBI in bracket)

13130303 GULJAR SETH 402, Shashwat Opp Guj College, Ellisbridge, Ahmedabad

54119/1253 Letter from BHOB(No photograph affixed)

13130475 ABHILASH SETH

402, Shashwat Opp Guj College, Ellisbridge, Ahmedabad

54119/1270 Letter from BHOB(No photograph affixed)

13130506 GUNISH SETH 402, Shashwat Opp Guj College, Ellisbridge, Ahmedabad

54119/1273 Letter from BHOB(No photograph affixed)

13130539 YATNA SETH 402, Shashwat Opp Guj College, Ellisbridge, Ahmedabad

54119/1276 Letter from BHOB(No photograph affixed)

13130547 NIRVI SETH 402, Shashwat Opp Guj College, Ellisbridge, Ahmedabad

54119/1277 Letter from BHOB(No photograph affixed)

13130570 ABHISHEK SETH

402, Shashwat Opp Guj College, Ellisbridge, Ahmedabad

54119/1280 Letter from BHOB(No photograph affixed)

13130598 DEVANDR A SETH

402, Shashwat Opp Guj College, Ellisbridge, Ahmedabad

54119/1282 Letter from BHOB(No photograph affixed)

13130650 DEPARV SETH

402, Shashwat Opp Guj College, Ellisbridge, Ahmedabad

54119/1288 Letter from BHOB(No photograph affixed)

The above said BhOB bank account number 54119 had been introduced by Karvy

Securities Limited, one of the Karvy group entities, during December, 2003, (as

discussed in sub paragraph 'ii' above). The bank account bearing no. 54119 was later

closed on April 24, 2004. However, the demat accounts opened on the basis of this,

continued to exist with Karvy DP even after the closure of the respective bank

accounts.

Subsequently, demat accounts were opened with Karvy DP on NSDL in the month of

December, 2003/ January, 2004 indicating the above bank details of BhOB. Such

NSDL demat accounts include the 50 names beginning from 'SURESH SETH' to

'ADITI SETH'. Later on, Karvy DP introduced these names to IOB, Thaltej branch in

a list certified by KSBL during March, 2005 which was found used for the purpose of

availing IPO finance from IOB.

The introduction of these bank accounts by the different Karvy group entities, which

subsequently formed the basis for opening demat accounts with its DP arm leads one to

infer that Karvy DP has a clear nexus with the genesis of these accounts. The

subsequent re-appearance of the similar names in the bank accounts with IOB in March,

2005 in the list of applicants who availed IPO finance in another IPO is also relevant to

note here. This clearly contradicts the submission of Karvy DP that the demat accounts

were opened subsequent to the opening of the bank accounts.

v. Karvy DP, in its reply dated May 19, 2007, has contended that the list of 50 names

appears to be a separate document as there is no basis for connecting the savings

Page 13 of 54

account opening form with the list containing 50 additional names. The argument of

Karvy DP that the list is not part of the account opening form, is not tenable as the

account opening form and the list attached with it, forms a complete set of account

opening form submitted by the respective bank. Further, the names added to the said

bank accounts were in the same order as that in which the demat accounts were held

with Karvy DP and such details were privy to Karvy DP.

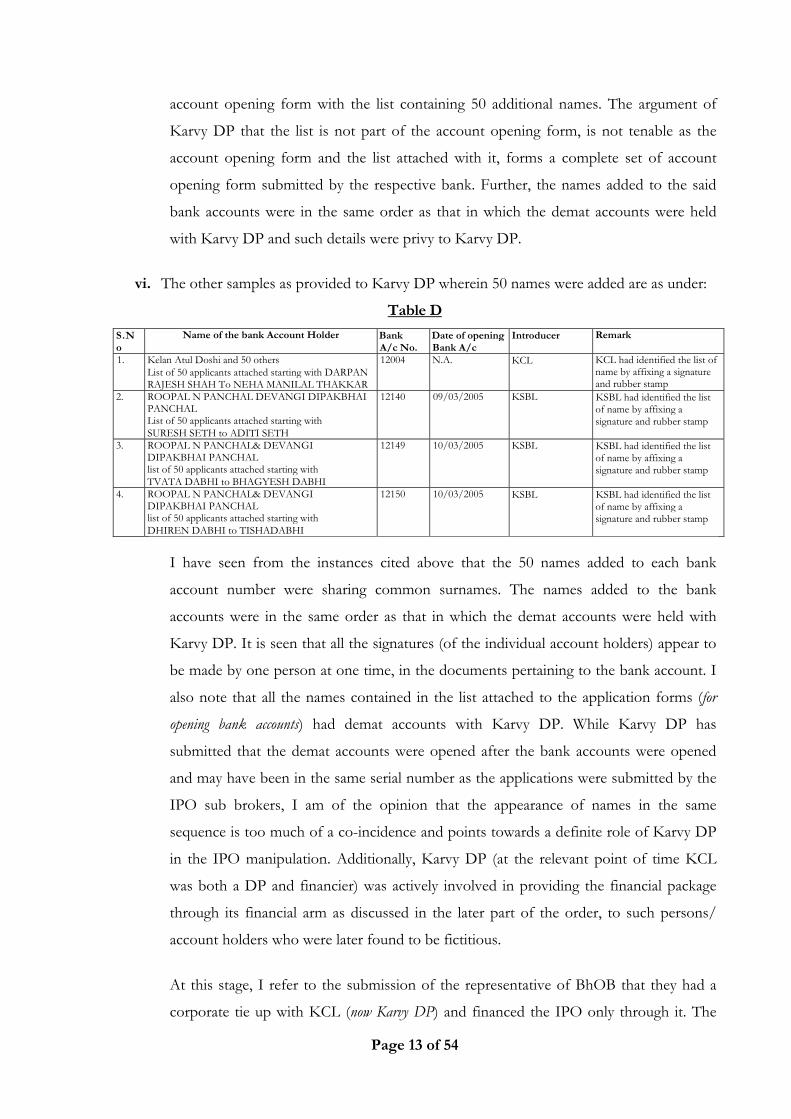

vi. The other samples as provided to Karvy DP wherein 50 names were added are as under:

Table D

S.No

Name of the bank Account Holder Bank A/c No.

Date of opening Bank A/c

Introducer Remark

1. Kelan Atul Doshi and 50 others List of 50 applicants attached starting with DARPAN RAJESH SHAH To NEHA MANILAL THAKKAR

12004 N.A. KCL KCL had identified the list of name by affixing a signature and rubber stamp

2. ROOPAL N PANCHAL DEVANGI DIPAKBHAI PANCHAL List of 50 applicants attached starting with SURESH SETH to ADITI SETH

12140 09/03/2005 KSBL KSBL had identified the list of name by affixing a signature and rubber stamp

3. ROOPAL N PANCHAL& DEVANGI DIPAKBHAI PANCHAL list of 50 applicants attached starting with TVATA DABHI to BHAGYESH DABHI

12149 10/03/2005 KSBL KSBL had identified the list of name by affixing a signature and rubber stamp

4. ROOPAL N PANCHAL& DEVANGI DIPAKBHAI PANCHAL list of 50 applicants attached starting with DHIREN DABHI to TISHADABHI

12150 10/03/2005 KSBL KSBL had identified the list of name by affixing a signature and rubber stamp

I have seen from the instances cited above that the 50 names added to each bank

account number were sharing common surnames. The names added to the bank

accounts were in the same order as that in which the demat accounts were held with

Karvy DP. It is seen that all the signatures (of the individual account holders) appear to

be made by one person at one time, in the documents pertaining to the bank account. I

also note that all the names contained in the list attached to the application forms (for

opening bank accounts) had demat accounts with Karvy DP. While Karvy DP has

submitted that the demat accounts were opened after the bank accounts were opened

and may have been in the same serial number as the applications were submitted by the

IPO sub brokers, I am of the opinion that the appearance of names in the same

sequence is too much of a co-incidence and points towards a definite role of Karvy DP

in the IPO manipulation. Additionally, Karvy DP (at the relevant point of time KCL

was both a DP and financier) was actively involved in providing the financial package

through its financial arm as discussed in the later part of the order, to such persons/

account holders who were later found to be fictitious.

At this stage, I refer to the submission of the representative of BhOB that they had a

corporate tie up with KCL (now Karvy DP) and financed the IPO only through it. The

Page 14 of 54

representative of BhoB, i.e., Mr. Devi Dutt, Chief Manager, BhOB, Ahmedabad has

submitted that out of the list of 12,257 demat accounts of Karvy DP in the IPO of Yes

Bank, only 4-5 demat accounts holders had accounts in BhOB, Ahmedabad and for

operative convenience of the bank, instead of opening individual savings bank account,

a number of individual names were added to a single account by BhOB. It has also been

submitted by him that BhOB has funded 9,327 demat accounts out of the said total of

12,257 demat accounts.

In this context, reference may be drawn to the contention of Karvy DP that the 'Idea

Paper' was just a note on process. However, the contents of this paper does

demonstrate the enthusiasm of Karvy group in charting out a clear plan to handle the

business of IPO process, eager to assume roles in all the areas of the IPO. I note from

the bank forms submitted by IOB and the list attached that Karvy DP had extended the

same scheme to IOB, Thaltej Branch, Ahmedabad. Incidentally, the above discussed

submission of Mr. Devi Dutt and the 'Idea Paper' refers to the same scheme of

arrangement. As a regulator, SEBI is not against the business plans/ arrangements of

various corporates. However, it is SEBI's mandate to ensure that the market players are

rolling out their activities well within the limits of law and keep the securities market

free of fraudulent activities.

On careful examination of the facts, I note that the introduction of the main bank accounts

and the addition of 50 fictitious names to each account paved the way for opening of the

afferent accounts. Karvy DP facilitated the opening of demat accounts for the additional

fictitious names. Therefore, the above discussed conduct of Karvy DP and other entities of

Karvy group can be said to have facilitated the key operators to procure IPO finance from

the banks and hence, it had aided and abetted the key operators in cornering the shares in

various IPOs.

b. Role in the opening of dematerialized accounts

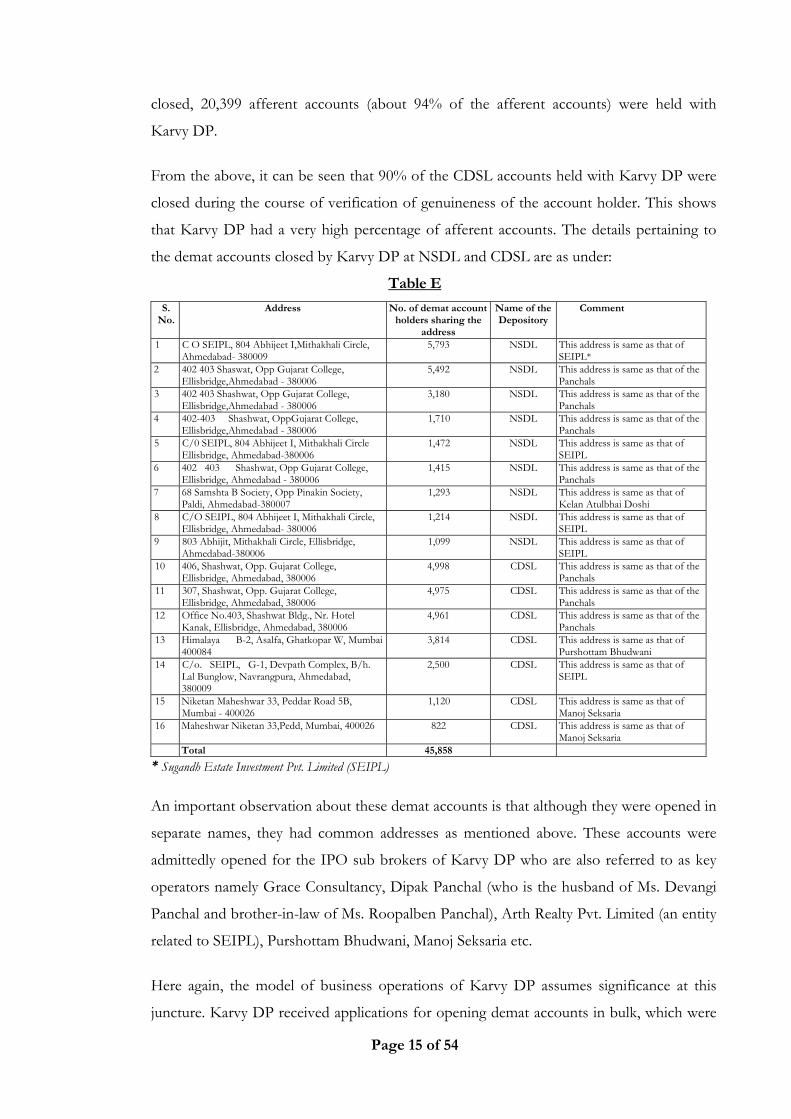

Karvy DP had opened a large number of afferent demat accounts. As can be seen from the

analysis of the total number of demat accounts closed at NSDL and CDSL pursuant to the

SEBI's intervention, out of 37,240 afferent accounts found closed at NSDL, 29,309

afferent accounts were those that were held at Karvy DP, which constitutes 79% of the

total afferent accounts. Similarly at CDSL, out of the 21,698 afferent accounts found

Page 15 of 54

closed, 20,399 afferent accounts (about 94% of the afferent accounts) were held with

Karvy DP.

From the above, it can be seen that 90% of the CDSL accounts held with Karvy DP were

closed during the course of verification of genuineness of the account holder. This shows

that Karvy DP had a very high percentage of afferent accounts. The details pertaining to

the demat accounts closed by Karvy DP at NSDL and CDSL are as under:

Table E

S. No.

Address No. of demat account holders sharing the

address

Name of theDepository

Comment

1 C O SEIPL, 804 Abhijeet I,Mithakhali Circle, Ahmedabad- 380009

5,793 NSDL This address is same as that of SEIPL*

2 402 403 Shaswat, Opp Gujarat College, Ellisbridge,Ahmedabad - 380006

5,492 NSDL This address is same as that of the Panchals

3 402 403 Shashwat, Opp Gujarat College, Ellisbridge,Ahmedabad - 380006

3,180 NSDL This address is same as that of the Panchals

4 402-403 Shashwat, OppGujarat College, Ellisbridge,Ahmedabad - 380006

1,710 NSDL This address is same as that of the Panchals

5 C/0 SEIPL, 804 Abhijeet I, Mithakhali Circle Ellisbridge, Ahmedabad-380006

1,472 NSDL This address is same as that of SEIPL

6 402 403 Shashwat, Opp Gujarat College, Ellisbridge, Ahmedabad - 380006

1,415 NSDL This address is same as that of the Panchals

7 68 Samshta B Society, Opp Pinakin Society, Paldi, Ahmedabad-380007

1,293 NSDL This address is same as that of Kelan Atulbhai Doshi

8 C/O SEIPL, 804 Abhijeet I, Mithakhali Circle, Ellisbridge, Ahmedabad- 380006

1,214 NSDL This address is same as that of SEIPL

9 803 Abhijit, Mithakhali Circle, Ellisbridge, Ahmedabad-380006

1,099 NSDL This address is same as that of SEIPL

10 406, Shashwat, Opp. Gujarat College, Ellisbridge, Ahmedabad, 380006

4,998 CDSL This address is same as that of the Panchals

11 307, Shashwat, Opp. Gujarat College, Ellisbridge, Ahmedabad, 380006

4,975 CDSL This address is same as that of the Panchals

12 Office No.403, Shashwat Bldg., Nr. Hotel Kanak, Ellisbridge, Ahmedabad, 380006

4,961 CDSL This address is same as that of the Panchals

13 Himalaya B-2, Asalfa, Ghatkopar W, Mumbai 400084

3,814 CDSL This address is same as that of Purshottam Bhudwani

14 C/o. SEIPL, G-1, Devpath Complex, B/h. Lal Bunglow, Navrangpura, Ahmedabad, 380009

2,500 CDSL This address is same as that of SEIPL

15 Niketan Maheshwar 33, Peddar Road 5B, Mumbai - 400026

1,120 CDSL This address is same as that of Manoj Seksaria

16 Maheshwar Niketan 33,Pedd, Mumbai, 400026 822 CDSL This address is same as that of Manoj Seksaria

Total 45,858

* Sugandh Estate Investment Pvt. Limited (SEIPL)

An important observation about these demat accounts is that although they were opened in

separate names, they had common addresses as mentioned above. These accounts were

admittedly opened for the IPO sub brokers of Karvy DP who are also referred to as key

operators namely Grace Consultancy, Dipak Panchal (who is the husband of Ms. Devangi

Panchal and brother-in-law of Ms. Roopalben Panchal), Arth Realty Pvt. Limited (an entity

related to SEIPL), Purshottam Bhudwani, Manoj Seksaria etc.

Here again, the model of business operations of Karvy DP assumes significance at this

juncture. Karvy DP received applications for opening demat accounts in bulk, which were

Page 16 of 54

initially procured by IPO sub brokers. In so far as Karvy DP is concerned, the process of

account opening started from preliminary scrutiny of the applications along with the

verification of documents, capturing the data such as name, address, bank details, etc. of

the applicants, verification of the data based on the documents, the scanning of signatures

and finally, the activation of the accounts. According to Karvy DP, the aforesaid process

has to be followed one after the other in the same sequence. Most of the sub brokers are

stated to have captured the data in the required format and submitted the same to Karvy

DP, along with the DP account opening application forms, so that data is uploaded easily

thereby saving time for the DP.

A scrutiny of the details pertaining to the demat accounts opened by Karvy DP exposes

several unusual features in the functioning of the DP that are inconsistent with the normal

market practices. Demat accounts were seen opened on the same day or even within an

interval of one or two days of filing of applications for such account-opening. Additionally,

large number of accounts are seen to have been opened by Karvy DP which had common

addresses (which were that of key operators) as mentioned above, common photographs,

strange combinations of repetitive names and surnames, etc. Thus, it is strange that Karvy

DP did not notice these irregularities, till the time of intervention of SEBI. Multiple

anomalies that were noticed in respect of these demat accounts are detailed under separate

headings below:-

i. Demat accounts having common features opened on the same day or within a gap

of few days from that of application

Karvy DP had argued that the IPO sub brokers had made a request for opening demat

accounts on the same day of filing of the applications, on behalf of their clients.

Following the same, a large number of accounts with common addresses were opened

with Karvy DP on a single day or within a gap of few days. For e.g.- On July 15, 2005,

Karvy DP opened 5,000 demat accounts at CDSL, with the common address of Roopal

Panchal, one of the key operators. On the very next day i.e. July 16, 2005, Karvy DP

opened 5,500 demat accounts at CDSL again with the common address of Roopal

Panchal. Other instances of similar nature have been brought out below:

Table F

S. No. Date of account opening

Address (pertaining to) CDSL (no.)

NSDL (no.)

1 February 16, 2004 C/o Karvy 754 - 2 April 20, 2004 803, Abhijeet I Mithakhali Circle, Ellisbridge, Ahmedabad (Sugandh Estates) - 1,097 3

August 16-17, 2004 402 403, Shashwat, Opp. Gujarat College, Ellisbridge, Ahmedabad 38006 (Roopal Panchal) - 2,385 C/o SEIPL, G-1, Devpath Complex, B/h Lal Bungalow, Ahmedabad (Sugandh Estates) - 4,241

Page 17 of 54

4 October 15-25, 2004 C/o SEIPL , G-1, Devpath Complaex B/h Lal Bungalow, Ahmedabad (Sugandh Estates) - 5,776 5 July 15, 2005 Office No. 403, Shashwat Bldg, Nr. Hotel Kanak, Ellisbridge Ahmedabad (Roopal Panchal) 5,000 - 6 July 16, 2005 307, Shashwat Opp. Gujarat College , Ellisbridge, Ahmedabad (Roopal Panchal) 5,000 -

406, Shashwat Opp. Gujarat College, Ellisbridge, Ahmedabad (Roopal Panchal) 500 - 7 July 19, 2005 402 403, Shashwat, Opp. Gujarat College, Ellisbridge, Ahmedabad 380006 (Roopal Panchal) - 1,004 8 July 20, 2005 402 403, Shashwat, Opp. Gujarat College, Ellisbridge, Ahmedabad 38006 (Roopal Panchal) - 1,532

9 July 21, 2005 402 403, Shashwat, Opp. Gujarat College, Ellisbridge, Ahmedabad 38006 (Roopal Panchal) - 755 10 July 22, 2005 B/2 Himalaya Asalaya Ghatkopar, W, Mumbai (Purshottam Bhudwani) 1,800 -

Niketan Maheshwar, 33, Peddar Road, 5B (Manoj Seksaria) 1,025 - 11 July 25, 2005 Niketan Maheshwar, 33, Peddar Road, 5B( same as Manoj Seksaria ) 522 - 12 August 5, 2005 68, Samashta B. Society, Opp. Pinakin, Soc., Paldi, Ahmedabad (Ketan Atul Bhai Doshi) - 618

3, Payal Complex, Sayajigunj Paldi, Baroda, 3900053 (Biren Kantilal Shah) - 387 13 August 17, 2005 B/2 Himalaya Asalaya Ghatkopar, W, Mumbai (Purshottam Bhudwani) 5,504 - 14 Auugst 27, 2005 C/o SEIPL , G-1, Devpath Complex, B/h Lal Bungalow, Ahmedabad (Sugandh Estates) 2,500 - 15 September 22, 2005 Office no. 402, Shashwat Bldg, Nr. Hotel Kanak Elisbridge, Ahmedabad (Roopal Panchal) 10,000 - Total 37,105 17,795

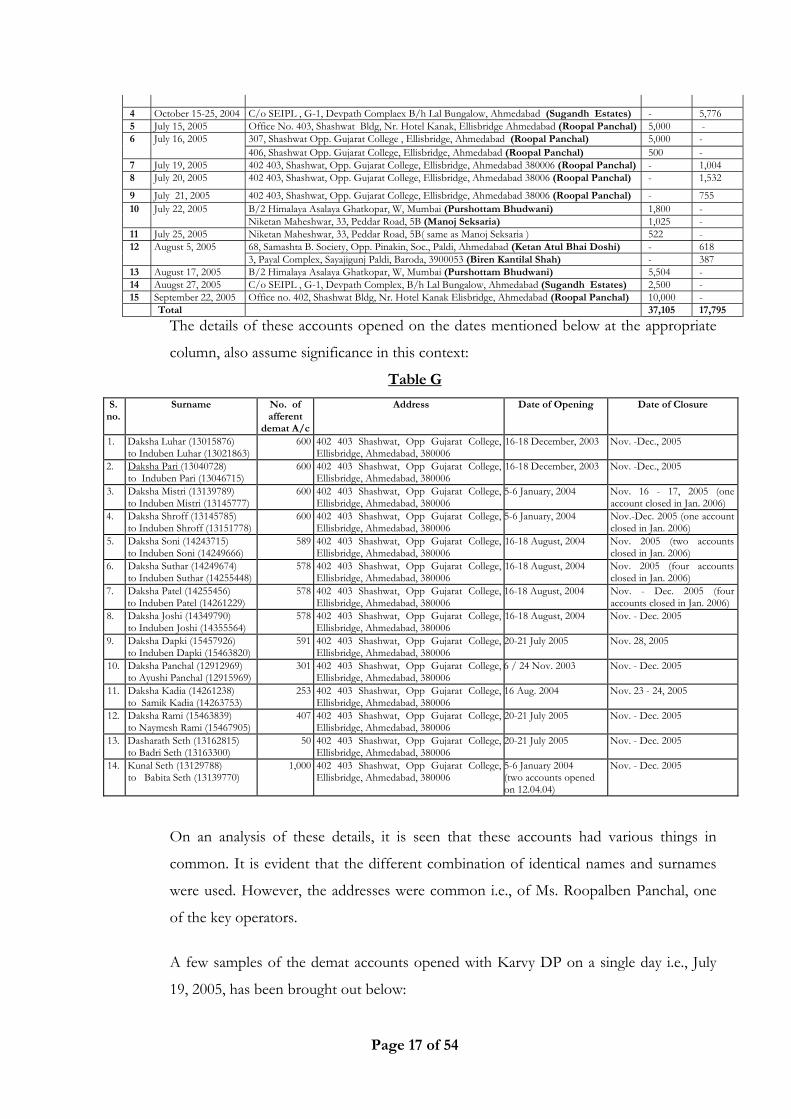

The details of these accounts opened on the dates mentioned below at the appropriate

column, also assume significance in this context:

Table G

On an analysis of these details, it is seen that these accounts had various things in

common. It is evident that the different combination of identical names and surnames

were used. However, the addresses were common i.e., of Ms. Roopalben Panchal, one

of the key operators.

A few samples of the demat accounts opened with Karvy DP on a single day i.e., July

19, 2005, has been brought out below:

S. no.

Surname No. of afferent

demat A/c

Address Date of Opening Date of Closure

1. Daksha Luhar (13015876) to Induben Luhar (13021863)

600 402 403 Shashwat, Opp Gujarat College, Ellisbridge, Ahmedabad, 380006

16-18 December, 2003 Nov. -Dec., 2005

2. Daksha Pari (13040728) to Induben Pari (13046715)

600 402 403 Shashwat, Opp Gujarat College, Ellisbridge, Ahmedabad, 380006

16-18 December, 2003 Nov. -Dec., 2005

3. Daksha Mistri (13139789) to Induben Mistri (13145777)

600 402 403 Shashwat, Opp Gujarat College, Ellisbridge, Ahmedabad, 380006

5-6 January, 2004 Nov. 16 - 17, 2005 (one account closed in Jan. 2006)

4. Daksha Shroff (13145785) to Induben Shroff (13151778)

600 402 403 Shashwat, Opp Gujarat College, Ellisbridge, Ahmedabad, 380006

5-6 January, 2004 Nov.-Dec. 2005 (one account closed in Jan. 2006)

5. Daksha Soni (14243715) to Induben Soni (14249666)

589 402 403 Shashwat, Opp Gujarat College, Ellisbridge, Ahmedabad, 380006

16-18 August, 2004 Nov. 2005 (two accounts closed in Jan. 2006)

6. Daksha Suthar (14249674) to Induben Suthar (14255448)

578 402 403 Shashwat, Opp Gujarat College, Ellisbridge, Ahmedabad, 380006

16-18 August, 2004 Nov. 2005 (four accounts closed in Jan. 2006)

7. Daksha Patel (14255456) to Induben Patel (14261229)

578 402 403 Shashwat, Opp Gujarat College, Ellisbridge, Ahmedabad, 380006

16-18 August, 2004 Nov. - Dec. 2005 (four accounts closed in Jan. 2006)

8. Daksha Joshi (14349790) to Induben Joshi (14355564)

578 402 403 Shashwat, Opp Gujarat College, Ellisbridge, Ahmedabad, 380006

16-18 August, 2004 Nov. - Dec. 2005

9. Daksha Dapki (15457926) to Induben Dapki (15463820)

591 402 403 Shashwat, Opp Gujarat College, Ellisbridge, Ahmedabad, 380006

20-21 July 2005 Nov. 28, 2005

10. Daksha Panchal (12912969) to Ayushi Panchal (12915969)

301 402 403 Shashwat, Opp Gujarat College, Ellisbridge, Ahmedabad, 380006

6 / 24 Nov. 2003 Nov. - Dec. 2005

11. Daksha Kadia (14261238) to Samik Kadia (14263753)

253 402 403 Shashwat, Opp Gujarat College, Ellisbridge, Ahmedabad, 380006

16 Aug. 2004 Nov. 23 - 24, 2005

12. Daksha Rami (15463839) to Naymesh Rami (15467905)

407 402 403 Shashwat, Opp Gujarat College, Ellisbridge, Ahmedabad, 380006

20-21 July 2005 Nov. - Dec. 2005

13. Dasharath Seth (13162815) to Badri Seth (13163300)

50 402 403 Shashwat, Opp Gujarat College, Ellisbridge, Ahmedabad, 380006

20-21 July 2005 Nov. - Dec. 2005

14. Kunal Seth (13129788) to Babita Seth (13139770)

1,000 402 403 Shashwat, Opp Gujarat College, Ellisbridge, Ahmedabad, 380006

5-6 January 2004 (two accounts opened on 12.04.04)

Nov. - Dec. 2005

Page 18 of 54

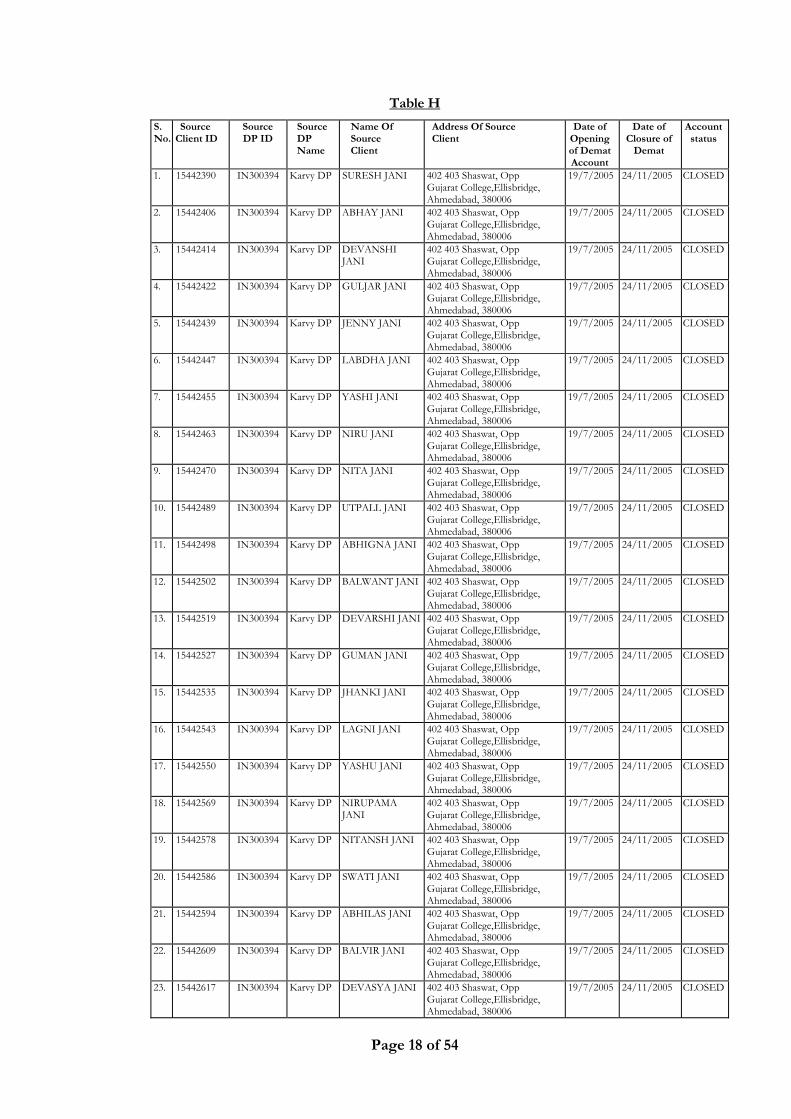

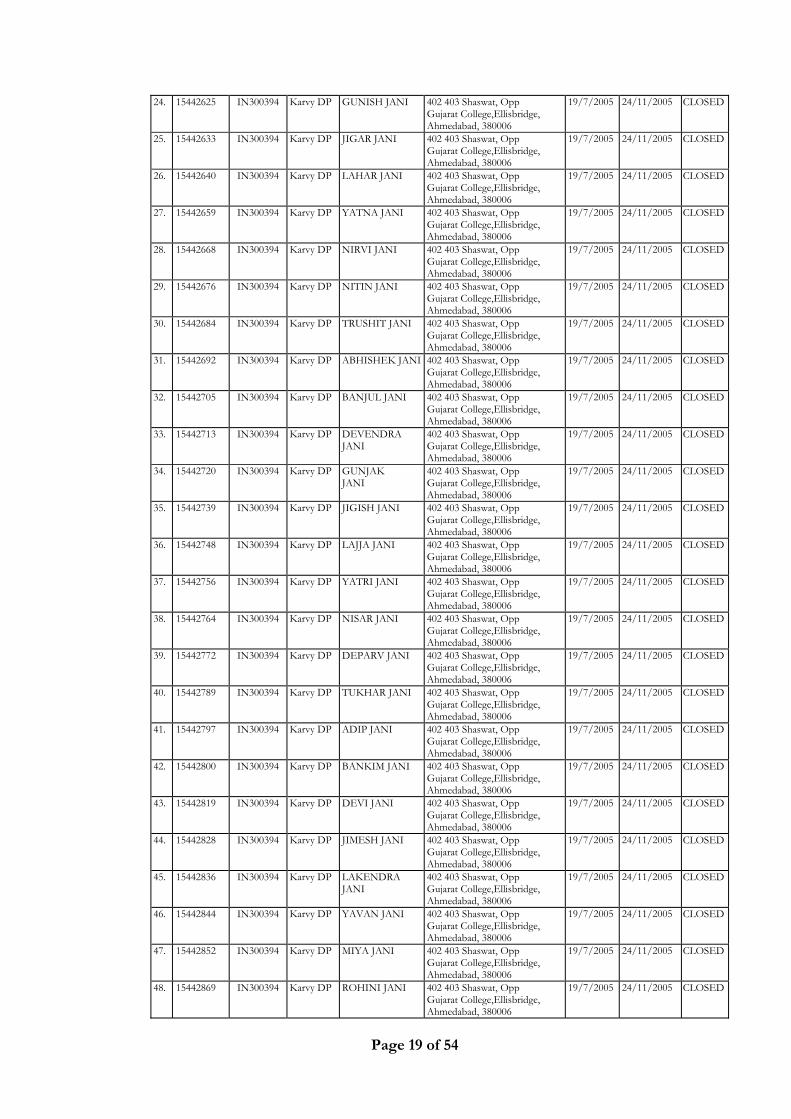

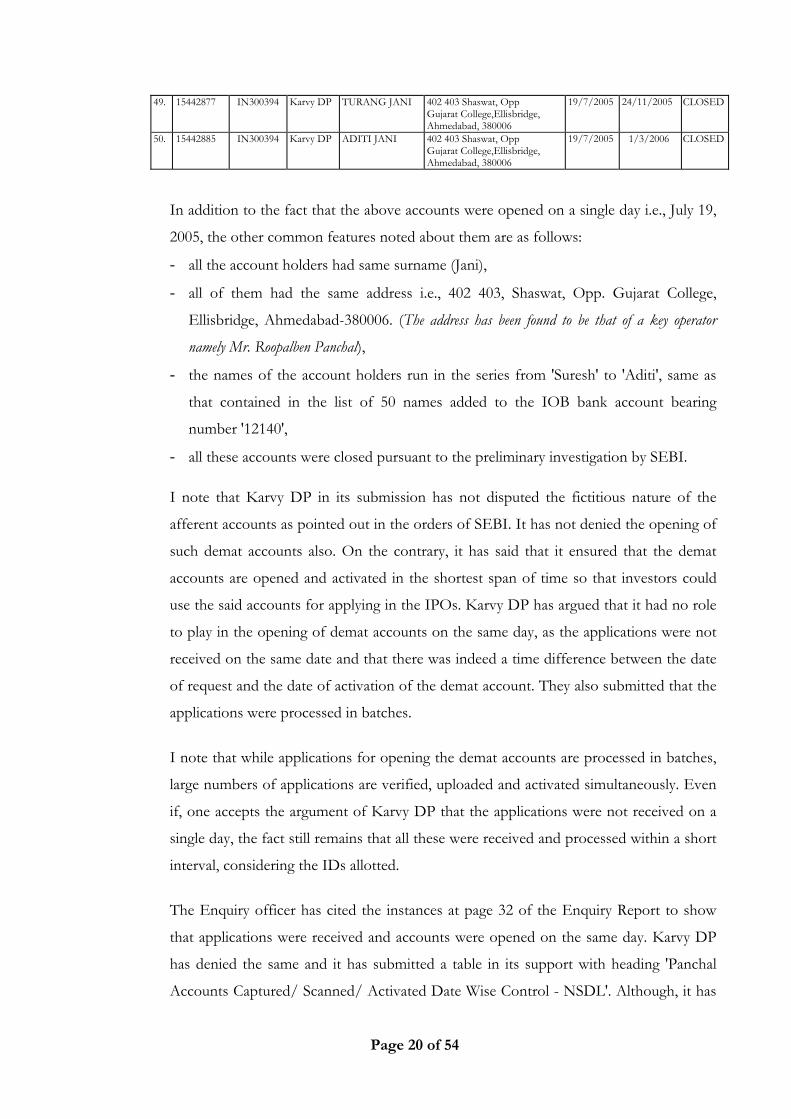

Table H

S. No.

Source Client ID

Source DP ID

Source DP Name

Name Of Source Client

Address Of Source Client

Date of Opening of Demat Account

Date of Closure of

Demat

Accountstatus

1. 15442390 IN300394 Karvy DP SURESH JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

2. 15442406 IN300394 Karvy DP ABHAY JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

3. 15442414 IN300394 Karvy DP DEVANSHI JANI

402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

4. 15442422 IN300394 Karvy DP GULJAR JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

5. 15442439 IN300394 Karvy DP JENNY JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

6. 15442447 IN300394 Karvy DP LABDHA JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

7. 15442455 IN300394 Karvy DP YASHI JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

8. 15442463 IN300394 Karvy DP NIRU JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

9. 15442470 IN300394 Karvy DP NITA JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

10. 15442489 IN300394 Karvy DP UTPALL JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

11. 15442498 IN300394 Karvy DP ABHIGNA JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

12. 15442502 IN300394 Karvy DP BALWANT JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

13. 15442519 IN300394 Karvy DP DEVARSHI JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

14. 15442527 IN300394 Karvy DP GUMAN JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

15. 15442535 IN300394 Karvy DP JHANKI JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

16. 15442543 IN300394 Karvy DP LAGNI JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

17. 15442550 IN300394 Karvy DP YASHU JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

18. 15442569 IN300394 Karvy DP NIRUPAMA JANI

402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

19. 15442578 IN300394 Karvy DP NITANSH JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

20. 15442586 IN300394 Karvy DP SWATI JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

21. 15442594 IN300394 Karvy DP ABHILAS JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

22. 15442609 IN300394 Karvy DP BALVIR JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

23. 15442617 IN300394 Karvy DP DEVASYA JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

Page 19 of 54

24. 15442625 IN300394 Karvy DP GUNISH JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

25. 15442633 IN300394 Karvy DP JIGAR JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

26. 15442640 IN300394 Karvy DP LAHAR JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

27. 15442659 IN300394 Karvy DP YATNA JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

28. 15442668 IN300394 Karvy DP NIRVI JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

29. 15442676 IN300394 Karvy DP NITIN JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

30. 15442684 IN300394 Karvy DP TRUSHIT JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

31. 15442692 IN300394 Karvy DP ABHISHEK JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

32. 15442705 IN300394 Karvy DP BANJUL JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

33. 15442713 IN300394 Karvy DP DEVENDRA JANI

402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

34. 15442720 IN300394 Karvy DP GUNJAK JANI

402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

35. 15442739 IN300394 Karvy DP JIGISH JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

36. 15442748 IN300394 Karvy DP LAJJA JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

37. 15442756 IN300394 Karvy DP YATRI JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

38. 15442764 IN300394 Karvy DP NISAR JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

39. 15442772 IN300394 Karvy DP DEPARV JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

40. 15442789 IN300394 Karvy DP TUKHAR JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

41. 15442797 IN300394 Karvy DP ADIP JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

42. 15442800 IN300394 Karvy DP BANKIM JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

43. 15442819 IN300394 Karvy DP DEVI JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

44. 15442828 IN300394 Karvy DP JIMESH JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

45. 15442836 IN300394 Karvy DP LAKENDRA JANI

402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

46. 15442844 IN300394 Karvy DP YAVAN JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

47. 15442852 IN300394 Karvy DP MIYA JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

48. 15442869 IN300394 Karvy DP ROHINI JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

Page 20 of 54

49. 15442877 IN300394 Karvy DP TURANG JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 24/11/2005 CLOSED

50. 15442885 IN300394 Karvy DP ADITI JANI 402 403 Shaswat, Opp Gujarat College,Ellisbridge, Ahmedabad, 380006

19/7/2005 1/3/2006 CLOSED

In addition to the fact that the above accounts were opened on a single day i.e., July 19,

2005, the other common features noted about them are as follows:

- all the account holders had same surname (Jani),

- all of them had the same address i.e., 402 403, Shaswat, Opp. Gujarat College,

Ellisbridge, Ahmedabad-380006. (The address has been found to be that of a key operator

namely Mr. Roopalben Panchal),

- the names of the account holders run in the series from 'Suresh' to 'Aditi', same as

that contained in the list of 50 names added to the IOB bank account bearing

number '12140',

- all these accounts were closed pursuant to the preliminary investigation by SEBI.

I note that Karvy DP in its submission has not disputed the fictitious nature of the

afferent accounts as pointed out in the orders of SEBI. It has not denied the opening of

such demat accounts also. On the contrary, it has said that it ensured that the demat

accounts are opened and activated in the shortest span of time so that investors could

use the said accounts for applying in the IPOs. Karvy DP has argued that it had no role

to play in the opening of demat accounts on the same day, as the applications were not

received on the same date and that there was indeed a time difference between the date

of request and the date of activation of the demat account. They also submitted that the

applications were processed in batches.

I note that while applications for opening the demat accounts are processed in batches,

large numbers of applications are verified, uploaded and activated simultaneously. Even

if, one accepts the argument of Karvy DP that the applications were not received on a

single day, the fact still remains that all these were received and processed within a short

interval, considering the IDs allotted.

The Enquiry officer has cited the instances at page 32 of the Enquiry Report to show

that applications were received and accounts were opened on the same day. Karvy DP

has denied the same and it has submitted a table in its support with heading 'Panchal

Accounts Captured/ Scanned/ Activated Date Wise Control - NSDL'. Although, it has

Page 21 of 54

said that the dates of receipt of the applications and the activation thereof were

different, there is no mention of the relevant dates in the table submitted by Karvy DP.

Though the demat account once opened cannot be used till the same is activated and

there is a possibility that different processes in account opening can happen on different

dates, in my opinion, details of specific dates of opening and activation thereof are

crucial for deciding the credibility of the submission of Karvy DP. In the absence of

such details, the reply of Karvy DP fails to convince me that there was any difference

between the time of receipt of the application and the activation of the demat account.

I, therefore, concur with the finding of the Enquiry Officer that these accounts

mentioned at Table F, were opened on the same date/ within a few days of receipt of

application.

ii. Demat accounts having common address and photographs

Karvy DP had opened several demat accounts having common addresses, as seen from

the instances in the Tables G and H above. Karvy DP has argued that there was no rule

that prevented the DP from opening demat accounts with common addresses. It is also

said that the requirement of an address for the DP account is for the purpose of

obtaining a correspondence address.

A further allegation against Karvy DP is that the demat account opening forms of Ms.

Roopalben Panchal and SEIPL do not contain the details of the permanent address on

the application forms. Karvy DP in its reply has submitted that the demat accounts were

opened in the ordinary course of business, after complying with the KYC requirements

applicable at the relevant point of time. It has also said that obtaining the permanent

address on the application form was not legally required as per the then prevailing rules.

According to Karvy DP, as the correspondence address was certified by the banks, there

was nothing to excite its suspicion that something could be amiss. Further, it said that

the IPO sub brokers gave their own addresses, at times, for all their clients, for the

purpose of operational convenience.

I note the specific admission of Karvy DP that in certain demat account opening

applications, the addresses used by the applicants were that of the sub-brokers/ key

operators, which addresses were also supported by a letter from the bank. This suggests

that Karvy DP was aware of the fact that different accounts were being opened with the

same address of the sub brokers.

Page 22 of 54

For the regulator, this is a matter of serious concern when a registered intermediary like

Karvy DP opens thousands of accounts for different names having the same address

(knowing that it is not theirs rather belongs to key operators), by merely relying on the

bank's letter and does not bother to undertake necessary verification of their identities.

According to me, a prudent intermediary would have paused at such instances of

opening of demat accounts with common addresses, instead of rushing through the

application and thus it acted as a conduit to the manipulative designs of fraudsters. It

ought to have noted that numerous applications having same addresses were being

received and it should have realized that these were indicative of aberrations in the

market practices and ought to have undertaken the necessary reporting. KYC

compliance for registered intermediaries is sacrosanct and ought to be performed with

extreme caution.

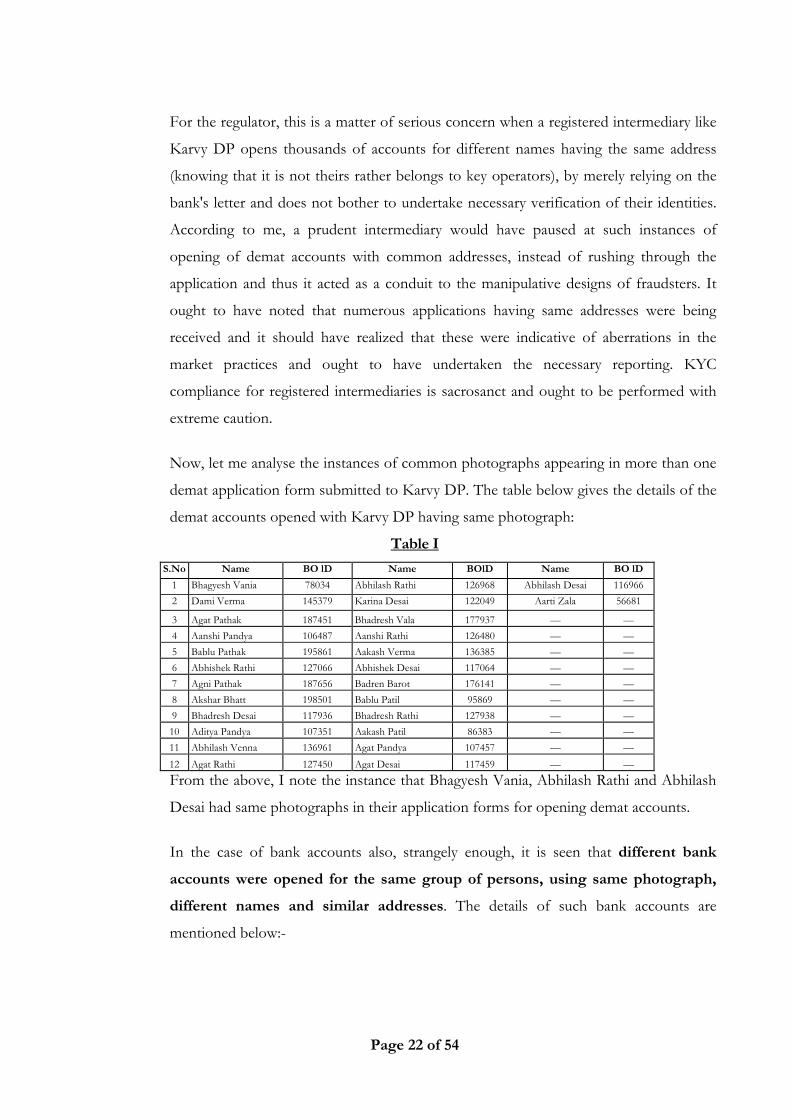

Now, let me analyse the instances of common photographs appearing in more than one

demat application form submitted to Karvy DP. The table below gives the details of the

demat accounts opened with Karvy DP having same photograph:

Table I

S.No Name BO lD Name BOlD Name BO lD

1 Bhagyesh Vania 78034 Abhilash Rathi 126968 Abhilash Desai 116966

2 Dami Verma 145379 Karina Desai 122049 Aarti Zala 56681

3 Agat Pathak 187451 Bhadresh Vala 177937 — —

4 Aanshi Pandya 106487 Aanshi Rathi 126480 — —

5 Bablu Pathak 195861 Aakash Verma 136385 — —

6 Abhishek Rathi 127066 Abhishek Desai 117064 — —

7 Agni Pathak 187656 Badren Barot 176141 — —

8 Akshar Bhatt 198501 Bablu Patil 95869 — —

9 Bhadresh Desai 117936 Bhadresh Rathi 127938 — —

10 Aditya Pandya 107351 Aakash Patil 86383 — —

11 Abhilash Venna 136961 Agat Pandya 107457 — —

12 Agat Rathi 127450 Agat Desai 117459 — —

From the above, I note the instance that Bhagyesh Vania, Abhilash Rathi and Abhilash

Desai had same photographs in their application forms for opening demat accounts.

In the case of bank accounts also, strangely enough, it is seen that different bank

accounts were opened for the same group of persons, using same photograph,

different names and similar addresses. The details of such bank accounts are

mentioned below:-

Page 23 of 54

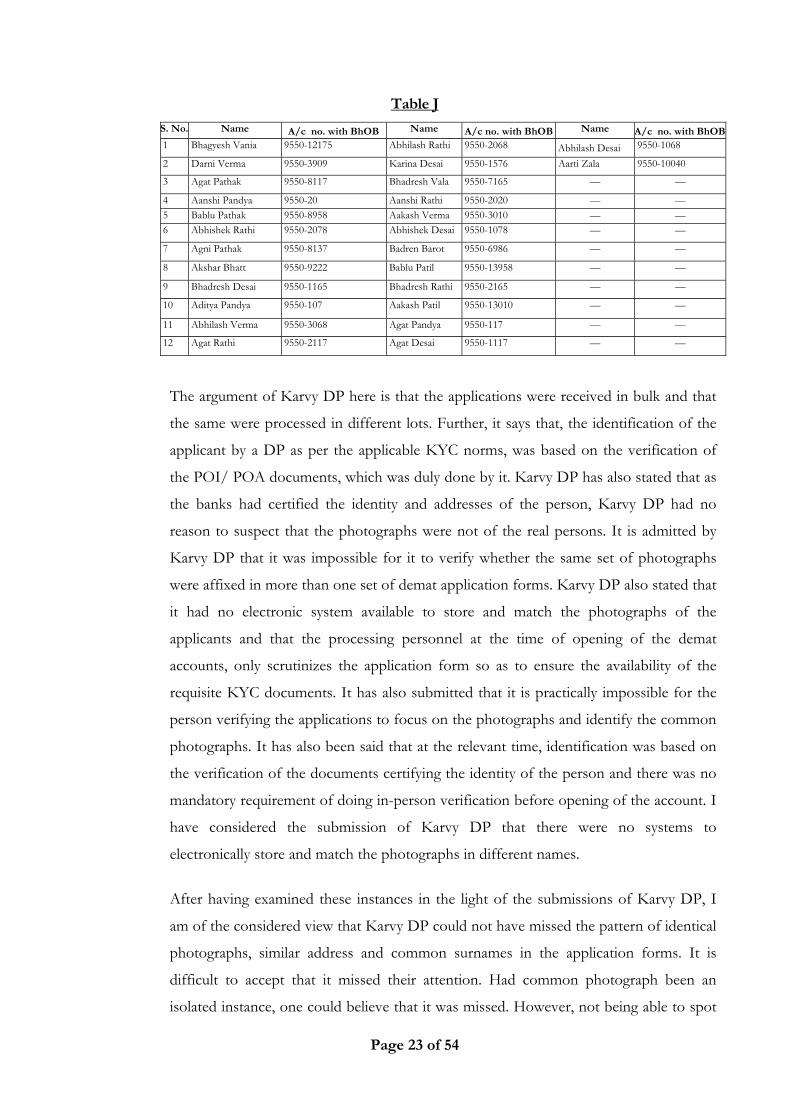

Table J

S. No. Name A/c no. with BhOB Name A/c no. with BhOB Name A/c no. with BhOB1 Bhagyesh Vania 9550-12175 Abhilash Rathi 9550-2068 Abhilash Desai 9550-1068

2 Darni Verma 9550-3909 Karina Desai 9550-1576 Aarti Zala 9550-10040

3 Agat Pathak 9550-8117 Bhadresh Vala 9550-7165 — —

4 Aanshi Pandya 9550-20 Aanshi Rathi 9550-2020 — —

5 Bablu Pathak 9550-8958 Aakash Verma 9550-3010 — — 6 Abhishek Rathi 9550-2078 Abhishek Desai 9550-1078 — —

7 Agni Pathak 9550-8137 Badren Barot 9550-6986 — —

8 Akshar Bhatt 9550-9222 Bablu Patil 9550-13958 — —

9 Bhadresh Desai 9550-1165 Bhadresh Rathi 9550-2165 — —

10 Aditya Pandya 9550-107 Aakash Patil 9550-13010 — —

11 Abhilash Verma 9550-3068 Agat Pandya 9550-117 — —

12 Agat Rathi 9550-2117 Agat Desai 9550-1117 — —

The argument of Karvy DP here is that the applications were received in bulk and that

the same were processed in different lots. Further, it says that, the identification of the

applicant by a DP as per the applicable KYC norms, was based on the verification of

the POI/ POA documents, which was duly done by it. Karvy DP has also stated that as

the banks had certified the identity and addresses of the person, Karvy DP had no

reason to suspect that the photographs were not of the real persons. It is admitted by

Karvy DP that it was impossible for it to verify whether the same set of photographs

were affixed in more than one set of demat application forms. Karvy DP also stated that

it had no electronic system available to store and match the photographs of the

applicants and that the processing personnel at the time of opening of the demat

accounts, only scrutinizes the application form so as to ensure the availability of the

requisite KYC documents. It has also submitted that it is practically impossible for the

person verifying the applications to focus on the photographs and identify the common

photographs. It has also been said that at the relevant time, identification was based on

the verification of the documents certifying the identity of the person and there was no

mandatory requirement of doing in-person verification before opening of the account. I

have considered the submission of Karvy DP that there were no systems to

electronically store and match the photographs in different names.

After having examined these instances in the light of the submissions of Karvy DP, I

am of the considered view that Karvy DP could not have missed the pattern of identical

photographs, similar address and common surnames in the application forms. It is

difficult to accept that it missed their attention. Had common photograph been an

isolated instance, one could believe that it was missed. However, not being able to spot

Page 24 of 54

even one instance among at least a dozen, is a matter of concern. In the case of

common addresses, Karvy DP has admitted that it was aware of the fact that different

accounts were being opened with the same address of the sub broker. It is quite strange

that the processing personnel, employed by Karvy DP, did not sense something amiss

when applications with similar names were coming in front of them through a handful

of key operators. If such a lapse is found in several cases, the obvious conclusion would

be that there was a deliberate omission. Under these circumstances, I am constrained to

conclude that Karvy DP ought not to have ventured into the humongous task of

accepting such number of applications. Further, the admitted failure to have an

appropriate system in place for authentic verification of the applicants, itself leads the

regulator to conclude that Karvy DP was giving leeway to the key operators to open

more and more demat accounts.

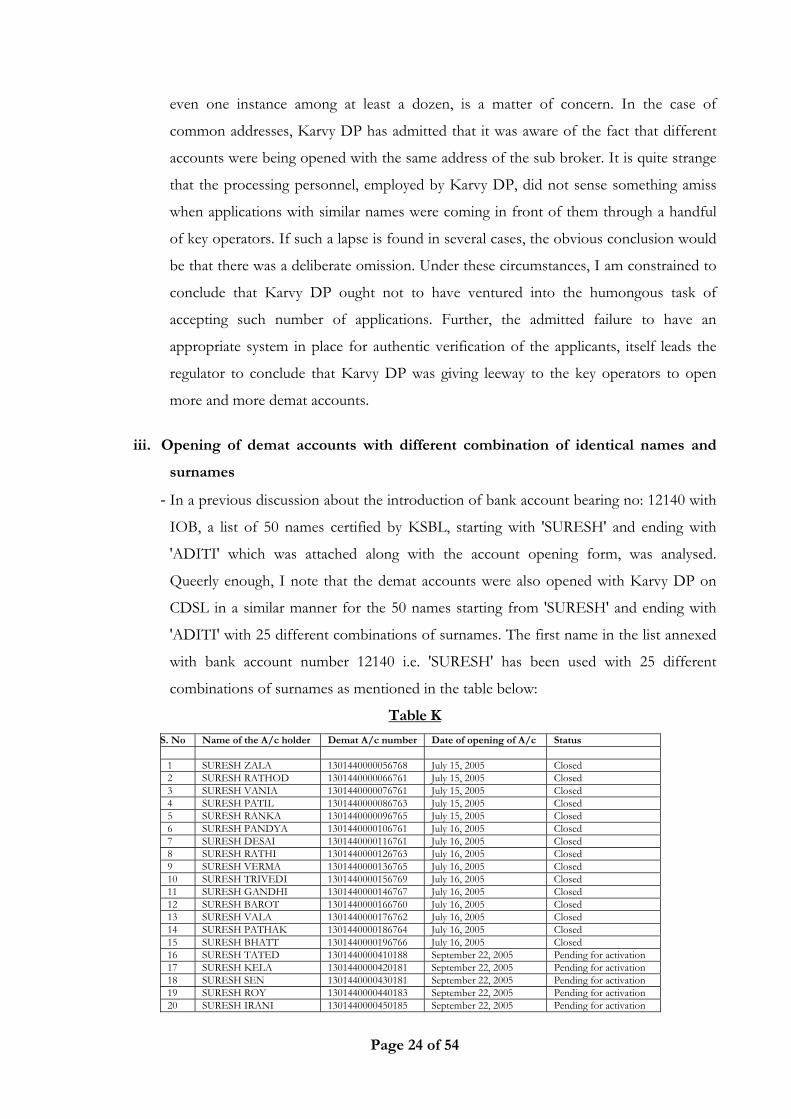

iii. Opening of demat accounts with different combination of identical names and

surnames

- In a previous discussion about the introduction of bank account bearing no: 12140 with

IOB, a list of 50 names certified by KSBL, starting with 'SURESH' and ending with

'ADITI' which was attached along with the account opening form, was analysed.

Queerly enough, I note that the demat accounts were also opened with Karvy DP on

CDSL in a similar manner for the 50 names starting from 'SURESH' and ending with

'ADITI' with 25 different combinations of surnames. The first name in the list annexed

with bank account number 12140 i.e. 'SURESH' has been used with 25 different

combinations of surnames as mentioned in the table below:

Table K

S. No Name of the A/c holder Demat A/c number Date of opening of A/c Status

1 SURESH ZALA 1301440000056768 July 15, 2005 Closed 2 SURESH RATHOD 1301440000066761 July 15, 2005 Closed 3 SURESH VANIA 1301440000076761 July 15, 2005 Closed 4 SURESH PATIL 1301440000086763 July 15, 2005 Closed 5 SURESH RANKA 1301440000096765 July 15, 2005 Closed 6 SURESH PANDYA 1301440000106761 July 16, 2005 Closed 7 SURESH DESAI 1301440000116761 July 16, 2005 Closed 8 SURESH RATHI 1301440000126763 July 16, 2005 Closed 9 SURESH VERMA 1301440000136765 July 16, 2005 Closed 10 SURESH TRIVEDI 1301440000156769 July 16, 2005 Closed 11 SURESH GANDHI 1301440000146767 July 16, 2005 Closed 12 SURESH BAROT 1301440000166760 July 16, 2005 Closed 13 SURESH VALA 1301440000176762 July 16, 2005 Closed 14 SURESH PATHAK 1301440000186764 July 16, 2005 Closed 15 SURESH BHATT 1301440000196766 July 16, 2005 Closed 16 SURESH TATED 1301440000410188 September 22, 2005 Pending for activation 17 SURESH KELA 1301440000420181 September 22, 2005 Pending for activation 18 SURESH SEN 1301440000430181 September 22, 2005 Pending for activation 19 SURESH ROY 1301440000440183 September 22, 2005 Pending for activation 20 SURESH IRANI 1301440000450185 September 22, 2005 Pending for activation

Page 25 of 54

21 SURESH JHA 1301440000460187 September 22, 2005 Pending for activation 22 SURESH KAPUR 1301440000400186 September 22, 2005 Pending for activation 23 SURESH MEHTA 1301440000470189 September 22, 2005 Pending for activation 24 SURESH DAS 1301440000480180 September 22, 2005 Pending for activation 25 SURESH PRASAD 1301440000490182 September 22, 2005 Pending for activation

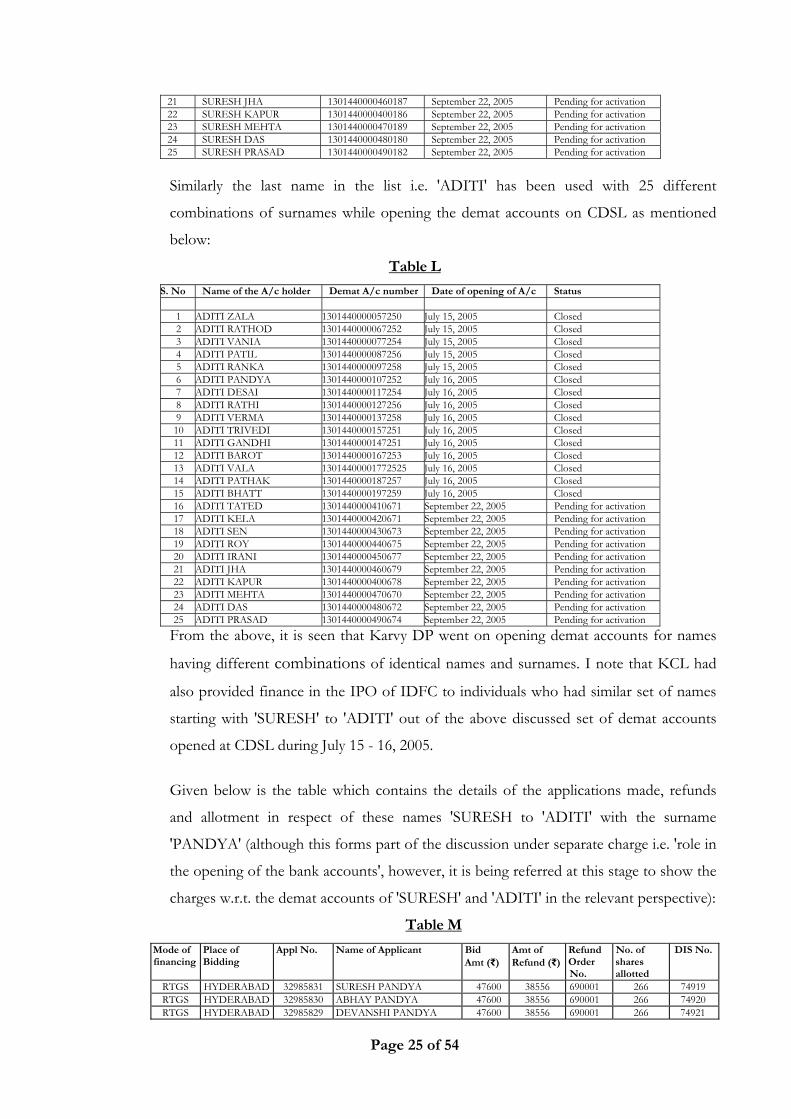

Similarly the last name in the list i.e. 'ADITI' has been used with 25 different

combinations of surnames while opening the demat accounts on CDSL as mentioned

below:

Table L

S. No Name of the A/c holder Demat A/c number Date of opening of A/c Status

1 ADITI ZALA 1301440000057250 July 15, 2005 Closed 2 ADITI RATHOD 1301440000067252 July 15, 2005 Closed 3 ADITI VANIA 1301440000077254 July 15, 2005 Closed 4 ADITI PATIL 1301440000087256 July 15, 2005 Closed 5 ADITI RANKA 1301440000097258 July 15, 2005 Closed 6 ADITI PANDYA 1301440000107252 July 16, 2005 Closed 7 ADITI DESAI 1301440000117254 July 16, 2005 Closed 8 ADITI RATHI 1301440000127256 July 16, 2005 Closed 9 ADITI VERMA 1301440000137258 July 16, 2005 Closed 10 ADITI TRIVEDI 1301440000157251 July 16, 2005 Closed 11 ADITI GANDHI 1301440000147251 July 16, 2005 Closed 12 ADITI BAROT 1301440000167253 July 16, 2005 Closed 13 ADITI VALA 13014400001772525 July 16, 2005 Closed 14 ADITI PATHAK 1301440000187257 July 16, 2005 Closed 15 ADITI BHATT 1301440000197259 July 16, 2005 Closed 16 ADITI TATED 1301440000410671 September 22, 2005 Pending for activation 17 ADITI KELA 1301440000420671 September 22, 2005 Pending for activation 18 ADITI SEN 1301440000430673 September 22, 2005 Pending for activation 19 ADITI ROY 1301440000440675 September 22, 2005 Pending for activation 20 ADITI IRANI 1301440000450677 September 22, 2005 Pending for activation 21 ADITI JHA 1301440000460679 September 22, 2005 Pending for activation 22 ADITI KAPUR 1301440000400678 September 22, 2005 Pending for activation 23 ADITI MEHTA 1301440000470670 September 22, 2005 Pending for activation 24 ADITI DAS 1301440000480672 September 22, 2005 Pending for activation 25 ADITI PRASAD 1301440000490674 September 22, 2005 Pending for activation

From the above, it is seen that Karvy DP went on opening demat accounts for names

having different combinations of identical names and surnames. I note that KCL had

also provided finance in the IPO of IDFC to individuals who had similar set of names

starting with 'SURESH' to 'ADITI' out of the above discussed set of demat accounts

opened at CDSL during July 15 - 16, 2005.

Given below is the table which contains the details of the applications made, refunds

and allotment in respect of these names 'SURESH to 'ADITI' with the surname

'PANDYA' (although this forms part of the discussion under separate charge i.e. 'role in

the opening of the bank accounts', however, it is being referred at this stage to show the

charges w.r.t. the demat accounts of 'SURESH' and 'ADITI' in the relevant perspective):

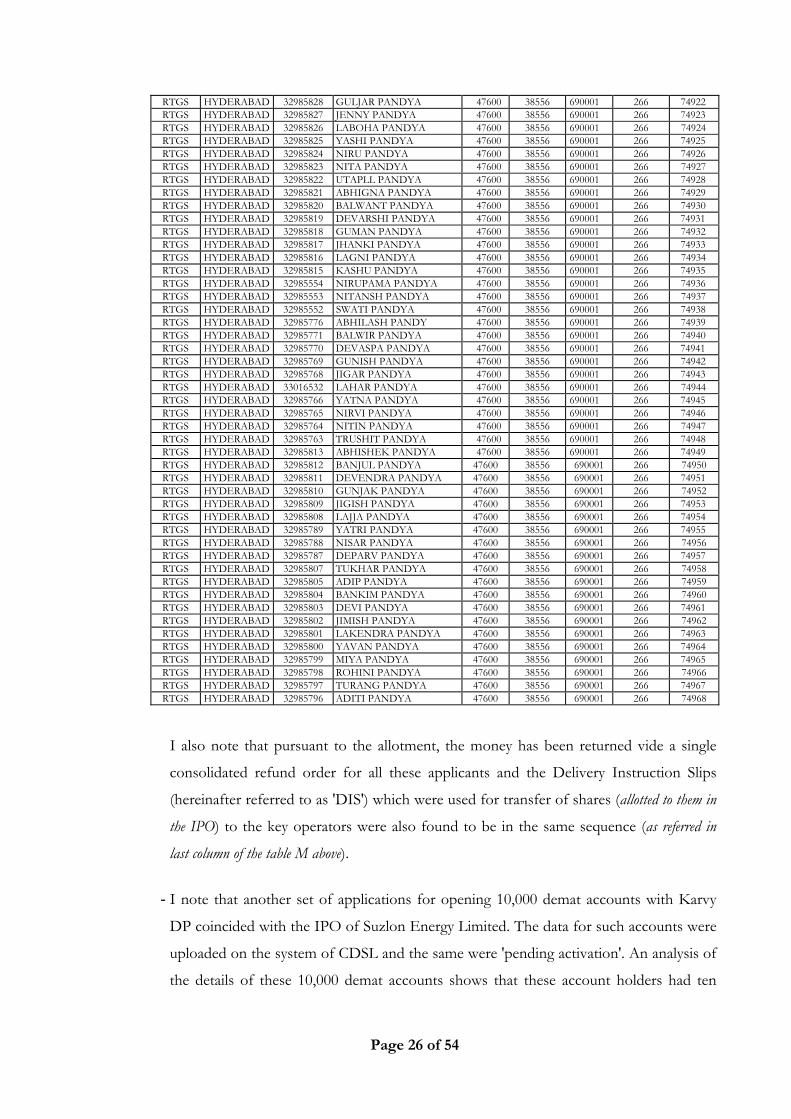

Table M

Mode of financing

Place of Bidding

Appl No. Name of Applicant Bid Amt (₹)