P4 ACCA Workbook Questions & Solutions P4 ACCA Questions & Solutions www.mapitaccountancy.com

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

P4 ACCA Workbook Questions &

Solutions

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Lecture 1 Financial Strategy

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

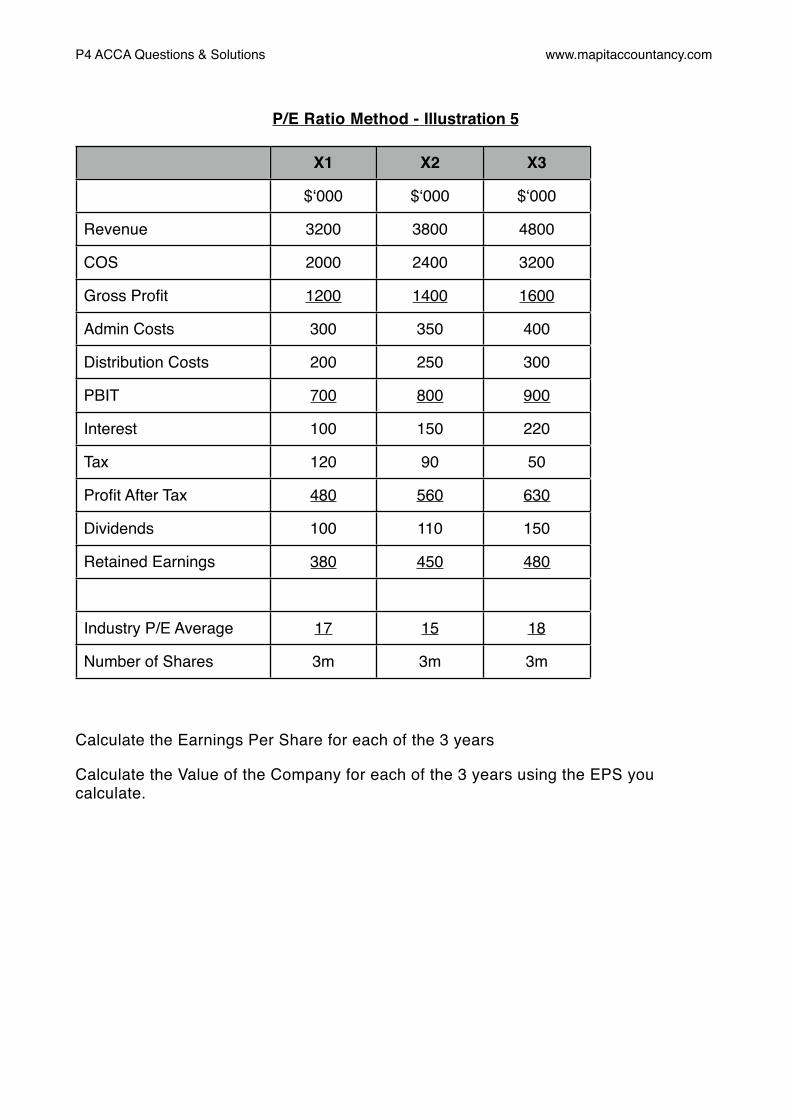

Shareholder Wealth - Illustration 1

Year Share Price Dividend Paid

2007 3.30 40c

2008 3.56 42c

2009 3.47 44c

2010 3.75 46c

2011 3.99 48c

There are 2 million shares in issue.! ! ! ! ! ! ! ! ! ! ! ! Calculate the increase in shareholder wealth for each year:II. Per shareIII. As a percentageIV. For the business as a whole

Solution

Year Share Price

Share Price Growth

Div Paid

Increase in

S’holder Wealth

As a Percentage

Total Shareholder

Return

2007 3.30 40c

2008 3.56 (3.56 - 3.30) = 26c 42c (26 + 42) = 68c

(68 / 330) = 20.6%

2m x 68c = $1.36m

2009 3.47 (3.47 - 3.56) = -9c 44c (-9 + 44) = 35c

(35 / 356) = 9.8%

2m x 35c = $0.70m

2010 3.75 (3.75 - 3.47) = 28c 46c (28 + 46) = 74c

(74 / 347) = 21.3%

2m x 74c = $1.48m

2011 3.99 (3.99 - 3.75) = 24c 48c (24 + 48) = 72c

(72 / 375) = 19.2%

2m x 72c = $1.44m

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

EPS - Illustration 2

2010$‘000

2011$‘000

PBIT 2000 2100

Interest 200 300

Tax 300 400

Profit After Tax 1500 1400

Preference Dividend 300 400

Dividend 800 900

Retained Earnings 400 100

Share Capital (50c) 5000 5000

Reserves 3000 3100

Share Price $2.50 $2.80

Calculate the EPS for 2010 and 2011.

Solution

2010 2011

Profit After Tax 1500 1400

Preference Dividend 300 400

Earnings 1200 1000

No. Ordinary Shares (5000 / 0.50) 10,000 10,000

EPS (Earnings / No. Ordinary Shares) 12c 10c

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Lecture 2 Performance Measurement

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Performance Analysis Illustration

X1 X2 X3

Non Current Assets 500 700 1000

Current Assets 150 200 300

650 900 1300

Ordinary Shares ($1) 300 300 300

Reserves 100 280 430

Loan Notes 150 200 300

Payables 100 120 270

650 900 1300

Revenue 3000 3500 4200

COS 2000 2400 3200

Gross Profit 1000 1100 1000

Admin Costs 300 350 400

Distribution Costs 200 250 300

PBIT 500 500 300

Interest 100 150 220

Tax 120 90 50

Profit After Tax 280 260 30

Dividends 100 110 30

Retained Earnings 180 150 0

Share Price $3.30 $4.00 $2.20

Using the information calculate and comment on the following Ratios:

I. Return on Capital EmployedII. Return on EquityIII. Gross MarginIV. Net MarginV. Operating MarginVI. Revenue GrowthVII. GearingVIII. Interest CoverIX. Dividend CoverX. Dividend YieldXI. P/E Ratio

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Solution

ROCE

X1 X2 X3

Equity + LT Liabilities

Shares 300 300 300

Reserves 100 280 430

LT Loan Notes 150 200 300

Capital Employed 550 780 1030

Non Current Assets + Net Current Assets

Non Current Assets 500 700 1000

Net Current Assets (Current Assets - Current Liabilities)

(150 - 100) = 50 (200 - 120) = 80 (300 - 270) = 30

Capital Employed 550 780 1030

Total Assets - Current Liabilities

Total Assets 650 900 1300

Current Liabilities 100 120 270

Capital Employed 550 780 1030

PBIT 500 500 300

Return on Capital Employed

PBIT / Capital Employed

(500 / 550) = 90.91%

(500 / 780) = 64.10%

(300 / 1030) = 29.13%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

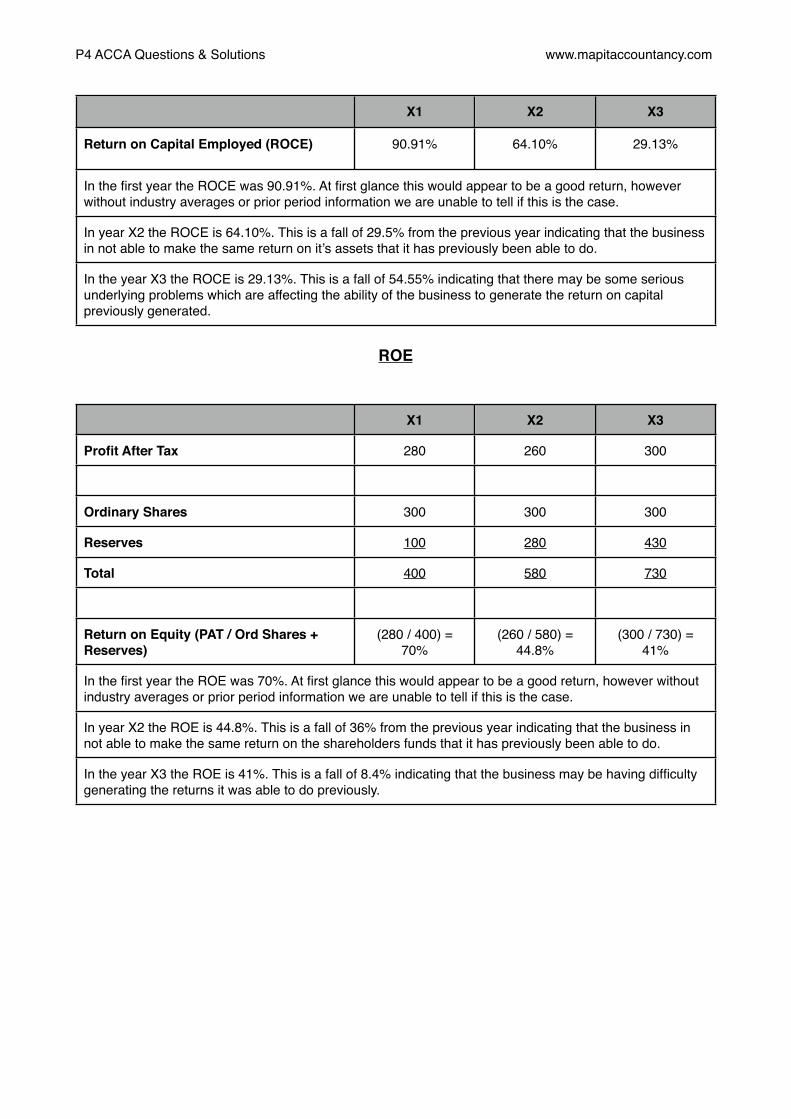

X1 X2 X3

Return on Capital Employed (ROCE) 90.91% 64.10% 29.13%

In the first year the ROCE was 90.91%. At first glance this would appear to be a good return, however without industry averages or prior period information we are unable to tell if this is the case.In the first year the ROCE was 90.91%. At first glance this would appear to be a good return, however without industry averages or prior period information we are unable to tell if this is the case.In the first year the ROCE was 90.91%. At first glance this would appear to be a good return, however without industry averages or prior period information we are unable to tell if this is the case.In the first year the ROCE was 90.91%. At first glance this would appear to be a good return, however without industry averages or prior period information we are unable to tell if this is the case.

In year X2 the ROCE is 64.10%. This is a fall of 29.5% from the previous year indicating that the business in not able to make the same return on it’s assets that it has previously been able to do.In year X2 the ROCE is 64.10%. This is a fall of 29.5% from the previous year indicating that the business in not able to make the same return on it’s assets that it has previously been able to do.In year X2 the ROCE is 64.10%. This is a fall of 29.5% from the previous year indicating that the business in not able to make the same return on it’s assets that it has previously been able to do.In year X2 the ROCE is 64.10%. This is a fall of 29.5% from the previous year indicating that the business in not able to make the same return on it’s assets that it has previously been able to do.

In the year X3 the ROCE is 29.13%. This is a fall of 54.55% indicating that there may be some serious underlying problems which are affecting the ability of the business to generate the return on capital previously generated.

In the year X3 the ROCE is 29.13%. This is a fall of 54.55% indicating that there may be some serious underlying problems which are affecting the ability of the business to generate the return on capital previously generated.

In the year X3 the ROCE is 29.13%. This is a fall of 54.55% indicating that there may be some serious underlying problems which are affecting the ability of the business to generate the return on capital previously generated.

In the year X3 the ROCE is 29.13%. This is a fall of 54.55% indicating that there may be some serious underlying problems which are affecting the ability of the business to generate the return on capital previously generated.

ROE

X1 X2 X3

Profit After Tax 280 260 300

Ordinary Shares 300 300 300

Reserves 100 280 430

Total 400 580 730

Return on Equity (PAT / Ord Shares + Reserves)

(280 / 400) = 70%

(260 / 580) = 44.8%

(300 / 730) = 41%

In the first year the ROE was 70%. At first glance this would appear to be a good return, however without industry averages or prior period information we are unable to tell if this is the case.In the first year the ROE was 70%. At first glance this would appear to be a good return, however without industry averages or prior period information we are unable to tell if this is the case.In the first year the ROE was 70%. At first glance this would appear to be a good return, however without industry averages or prior period information we are unable to tell if this is the case.In the first year the ROE was 70%. At first glance this would appear to be a good return, however without industry averages or prior period information we are unable to tell if this is the case.

In year X2 the ROE is 44.8%. This is a fall of 36% from the previous year indicating that the business in not able to make the same return on the shareholders funds that it has previously been able to do.In year X2 the ROE is 44.8%. This is a fall of 36% from the previous year indicating that the business in not able to make the same return on the shareholders funds that it has previously been able to do.In year X2 the ROE is 44.8%. This is a fall of 36% from the previous year indicating that the business in not able to make the same return on the shareholders funds that it has previously been able to do.In year X2 the ROE is 44.8%. This is a fall of 36% from the previous year indicating that the business in not able to make the same return on the shareholders funds that it has previously been able to do.

In the year X3 the ROE is 41%. This is a fall of 8.4% indicating that the business may be having difficulty generating the returns it was able to do previously.In the year X3 the ROE is 41%. This is a fall of 8.4% indicating that the business may be having difficulty generating the returns it was able to do previously.In the year X3 the ROE is 41%. This is a fall of 8.4% indicating that the business may be having difficulty generating the returns it was able to do previously.In the year X3 the ROE is 41%. This is a fall of 8.4% indicating that the business may be having difficulty generating the returns it was able to do previously.

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Margins

X1 X2 X3

Revenue 3000 3500 4200

Gross Profit 1000 1100 1000

PAT 280 260 30

PBIT 500 500 300

Gross Margin (Gross Profit / Revenue) (1000 / 3000) = 33.33%

(1100 / 3500) = 31.42%

(1000 / 4200) = 23.89%

Net Margin (PAT / Revenue) (280 / 3000) = 9.3%

(260 / 3500) = 7.4%

(30 / 4200) = 0.7%

Operating Margin (PBIT / Revenue) (500 / 3000) = 16.66%

(500 / 3500) = 14.28%

(300 / 4200) = 7.1%

The Gross Margin is 33.33% in X1 and holds reasonably steady in X2 at 31.42%. However in X3 the Gross Margin falls to 23.89% indicating that the business has either had to cut prices to sell the greater volume it has, or the cost of it’s purchases have gone up.

The Gross Margin is 33.33% in X1 and holds reasonably steady in X2 at 31.42%. However in X3 the Gross Margin falls to 23.89% indicating that the business has either had to cut prices to sell the greater volume it has, or the cost of it’s purchases have gone up.

The Gross Margin is 33.33% in X1 and holds reasonably steady in X2 at 31.42%. However in X3 the Gross Margin falls to 23.89% indicating that the business has either had to cut prices to sell the greater volume it has, or the cost of it’s purchases have gone up.

The Gross Margin is 33.33% in X1 and holds reasonably steady in X2 at 31.42%. However in X3 the Gross Margin falls to 23.89% indicating that the business has either had to cut prices to sell the greater volume it has, or the cost of it’s purchases have gone up.

The Net Margin is 9.3% in X1 but begins to fall in X2 with 7.4% achieved, before falling dramatically to 0.7% in X3. The main reason for this is the fall in Gross Profit as other costs have risen in line with expectations given the increase in sales. However another point to note is that interest costs have risen with the increase in long term loans. The extra interest costs have put pressure on the business.

The Net Margin is 9.3% in X1 but begins to fall in X2 with 7.4% achieved, before falling dramatically to 0.7% in X3. The main reason for this is the fall in Gross Profit as other costs have risen in line with expectations given the increase in sales. However another point to note is that interest costs have risen with the increase in long term loans. The extra interest costs have put pressure on the business.

The Net Margin is 9.3% in X1 but begins to fall in X2 with 7.4% achieved, before falling dramatically to 0.7% in X3. The main reason for this is the fall in Gross Profit as other costs have risen in line with expectations given the increase in sales. However another point to note is that interest costs have risen with the increase in long term loans. The extra interest costs have put pressure on the business.

The Net Margin is 9.3% in X1 but begins to fall in X2 with 7.4% achieved, before falling dramatically to 0.7% in X3. The main reason for this is the fall in Gross Profit as other costs have risen in line with expectations given the increase in sales. However another point to note is that interest costs have risen with the increase in long term loans. The extra interest costs have put pressure on the business.

The Operating Margin dropped slightly in X2 to 14.28% from 16.66% the previous year - a fall of almost 15%. In X3 the Operating Margin fell away to 7.1%, a decrease of over 50%. This is due to the decreasing Gross Margin achieved as well as rises in the other expenses.

The Operating Margin dropped slightly in X2 to 14.28% from 16.66% the previous year - a fall of almost 15%. In X3 the Operating Margin fell away to 7.1%, a decrease of over 50%. This is due to the decreasing Gross Margin achieved as well as rises in the other expenses.

The Operating Margin dropped slightly in X2 to 14.28% from 16.66% the previous year - a fall of almost 15%. In X3 the Operating Margin fell away to 7.1%, a decrease of over 50%. This is due to the decreasing Gross Margin achieved as well as rises in the other expenses.

The Operating Margin dropped slightly in X2 to 14.28% from 16.66% the previous year - a fall of almost 15%. In X3 the Operating Margin fell away to 7.1%, a decrease of over 50%. This is due to the decreasing Gross Margin achieved as well as rises in the other expenses.

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Gearing

X1 X2 X3

Debt 150 200 300

Equity Number of Shares

300 300 300

Share Price 3.30 4 2.20

Market Value (300 x 3.30) = 990

(300 x 4) = 1200

(300 x 2.20) = 660

Gearing (Debt / Equity) (150 / 990) = 15%

(200 / 1200) = 16.66%

(300 / 660) = 45.45%

Gearing levels in year X1 are 15%. Without industry averages or prior year data we are unable to assess this level although at first glance it does not seem excessive.Gearing levels in year X1 are 15%. Without industry averages or prior year data we are unable to assess this level although at first glance it does not seem excessive.Gearing levels in year X1 are 15%. Without industry averages or prior year data we are unable to assess this level although at first glance it does not seem excessive.Gearing levels in year X1 are 15%. Without industry averages or prior year data we are unable to assess this level although at first glance it does not seem excessive.Gearing levels in year X1 are 15%. Without industry averages or prior year data we are unable to assess this level although at first glance it does not seem excessive.

In year X2 gearing increases slightly to 16.66%, an increase of 11% from year X1. This is due to debt levels increasing to 200 from 150, although this is offset by the increase in the share price from $3.30 to $4.

In year X2 gearing increases slightly to 16.66%, an increase of 11% from year X1. This is due to debt levels increasing to 200 from 150, although this is offset by the increase in the share price from $3.30 to $4.

In year X2 gearing increases slightly to 16.66%, an increase of 11% from year X1. This is due to debt levels increasing to 200 from 150, although this is offset by the increase in the share price from $3.30 to $4.

In year X2 gearing increases slightly to 16.66%, an increase of 11% from year X1. This is due to debt levels increasing to 200 from 150, although this is offset by the increase in the share price from $3.30 to $4.

In year X2 gearing increases slightly to 16.66%, an increase of 11% from year X1. This is due to debt levels increasing to 200 from 150, although this is offset by the increase in the share price from $3.30 to $4.

In year X3 gearing increases dramatically to 45%, an increase of over 180%. This is due to debt levels rising to 300 from 200 and the share price dropping to $2.20 due to the deteriorating results of the business.

In year X3 gearing increases dramatically to 45%, an increase of over 180%. This is due to debt levels rising to 300 from 200 and the share price dropping to $2.20 due to the deteriorating results of the business.

In year X3 gearing increases dramatically to 45%, an increase of over 180%. This is due to debt levels rising to 300 from 200 and the share price dropping to $2.20 due to the deteriorating results of the business.

In year X3 gearing increases dramatically to 45%, an increase of over 180%. This is due to debt levels rising to 300 from 200 and the share price dropping to $2.20 due to the deteriorating results of the business.

In year X3 gearing increases dramatically to 45%, an increase of over 180%. This is due to debt levels rising to 300 from 200 and the share price dropping to $2.20 due to the deteriorating results of the business.

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

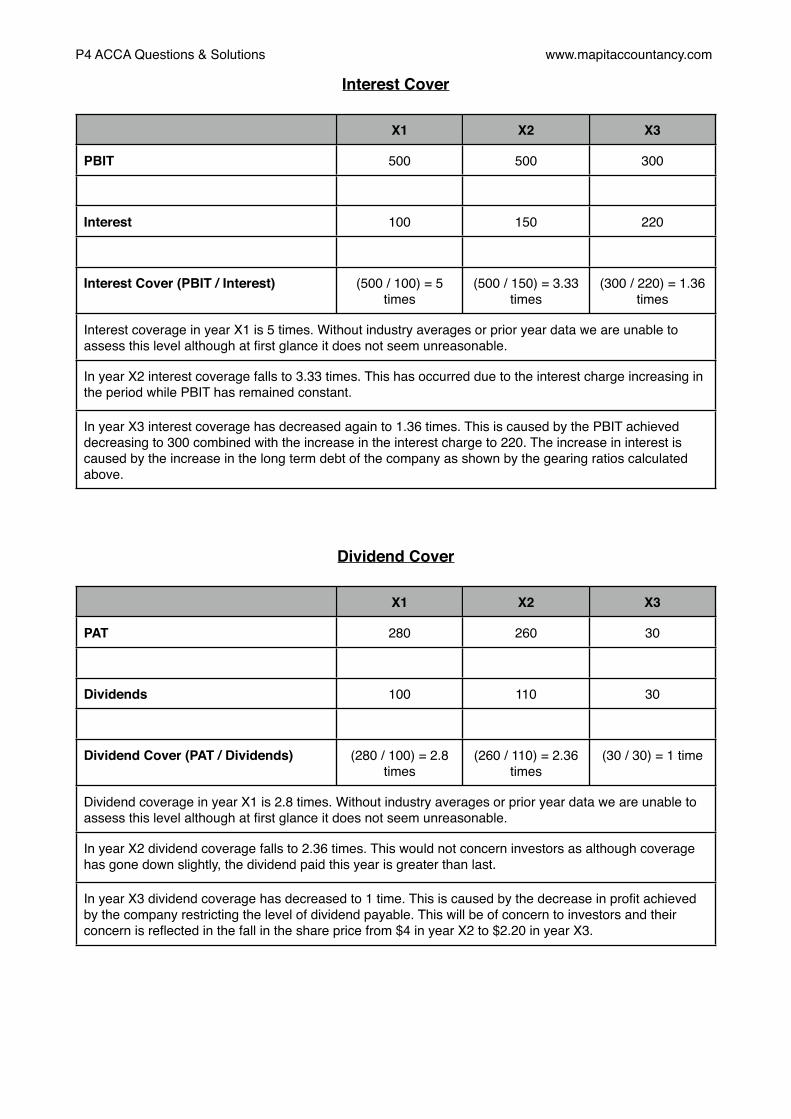

Interest Cover

X1 X2 X3

PBIT 500 500 300

Interest 100 150 220

Interest Cover (PBIT / Interest) (500 / 100) = 5 times

(500 / 150) = 3.33 times

(300 / 220) = 1.36 times

Interest coverage in year X1 is 5 times. Without industry averages or prior year data we are unable to assess this level although at first glance it does not seem unreasonable.Interest coverage in year X1 is 5 times. Without industry averages or prior year data we are unable to assess this level although at first glance it does not seem unreasonable.Interest coverage in year X1 is 5 times. Without industry averages or prior year data we are unable to assess this level although at first glance it does not seem unreasonable.Interest coverage in year X1 is 5 times. Without industry averages or prior year data we are unable to assess this level although at first glance it does not seem unreasonable.

In year X2 interest coverage falls to 3.33 times. This has occurred due to the interest charge increasing in the period while PBIT has remained constant.In year X2 interest coverage falls to 3.33 times. This has occurred due to the interest charge increasing in the period while PBIT has remained constant.In year X2 interest coverage falls to 3.33 times. This has occurred due to the interest charge increasing in the period while PBIT has remained constant.In year X2 interest coverage falls to 3.33 times. This has occurred due to the interest charge increasing in the period while PBIT has remained constant.

In year X3 interest coverage has decreased again to 1.36 times. This is caused by the PBIT achieved decreasing to 300 combined with the increase in the interest charge to 220. The increase in interest is caused by the increase in the long term debt of the company as shown by the gearing ratios calculated above.

In year X3 interest coverage has decreased again to 1.36 times. This is caused by the PBIT achieved decreasing to 300 combined with the increase in the interest charge to 220. The increase in interest is caused by the increase in the long term debt of the company as shown by the gearing ratios calculated above.

In year X3 interest coverage has decreased again to 1.36 times. This is caused by the PBIT achieved decreasing to 300 combined with the increase in the interest charge to 220. The increase in interest is caused by the increase in the long term debt of the company as shown by the gearing ratios calculated above.

In year X3 interest coverage has decreased again to 1.36 times. This is caused by the PBIT achieved decreasing to 300 combined with the increase in the interest charge to 220. The increase in interest is caused by the increase in the long term debt of the company as shown by the gearing ratios calculated above.

Dividend Cover

X1 X2 X3

PAT 280 260 30

Dividends 100 110 30

Dividend Cover (PAT / Dividends) (280 / 100) = 2.8 times

(260 / 110) = 2.36 times

(30 / 30) = 1 time

Dividend coverage in year X1 is 2.8 times. Without industry averages or prior year data we are unable to assess this level although at first glance it does not seem unreasonable.Dividend coverage in year X1 is 2.8 times. Without industry averages or prior year data we are unable to assess this level although at first glance it does not seem unreasonable.Dividend coverage in year X1 is 2.8 times. Without industry averages or prior year data we are unable to assess this level although at first glance it does not seem unreasonable.Dividend coverage in year X1 is 2.8 times. Without industry averages or prior year data we are unable to assess this level although at first glance it does not seem unreasonable.

In year X2 dividend coverage falls to 2.36 times. This would not concern investors as although coverage has gone down slightly, the dividend paid this year is greater than last.In year X2 dividend coverage falls to 2.36 times. This would not concern investors as although coverage has gone down slightly, the dividend paid this year is greater than last.In year X2 dividend coverage falls to 2.36 times. This would not concern investors as although coverage has gone down slightly, the dividend paid this year is greater than last.In year X2 dividend coverage falls to 2.36 times. This would not concern investors as although coverage has gone down slightly, the dividend paid this year is greater than last.

In year X3 dividend coverage has decreased to 1 time. This is caused by the decrease in profit achieved by the company restricting the level of dividend payable. This will be of concern to investors and their concern is reflected in the fall in the share price from $4 in year X2 to $2.20 in year X3.

In year X3 dividend coverage has decreased to 1 time. This is caused by the decrease in profit achieved by the company restricting the level of dividend payable. This will be of concern to investors and their concern is reflected in the fall in the share price from $4 in year X2 to $2.20 in year X3.

In year X3 dividend coverage has decreased to 1 time. This is caused by the decrease in profit achieved by the company restricting the level of dividend payable. This will be of concern to investors and their concern is reflected in the fall in the share price from $4 in year X2 to $2.20 in year X3.

In year X3 dividend coverage has decreased to 1 time. This is caused by the decrease in profit achieved by the company restricting the level of dividend payable. This will be of concern to investors and their concern is reflected in the fall in the share price from $4 in year X2 to $2.20 in year X3.

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Dividend Yield

X1 X2 X3

Number of Shares (300 / 1) 300 300 300

Dividends 100 110 30

Dividends Per Share (100 / 300) = 33c (110 / 300) = 36c (30 / 300) = 10c

Dividend Yield (Dividends Per Share / Share Price)

(33 / 330) = 10% (36 / 400) = 9% (10 / 220) = 4.5%

The Dividend Yield is 10% in year X1. Whilst we do not have comparatives, this seems a reasonable return.The Dividend Yield is 10% in year X1. Whilst we do not have comparatives, this seems a reasonable return.The Dividend Yield is 10% in year X1. Whilst we do not have comparatives, this seems a reasonable return.The Dividend Yield is 10% in year X1. Whilst we do not have comparatives, this seems a reasonable return.

In year X2 the Dividend Yield falls to 9%. This will not be overly concerning to investors as the increase in share price over the year will have more than made up for the slightly lower yield.In year X2 the Dividend Yield falls to 9%. This will not be overly concerning to investors as the increase in share price over the year will have more than made up for the slightly lower yield.In year X2 the Dividend Yield falls to 9%. This will not be overly concerning to investors as the increase in share price over the year will have more than made up for the slightly lower yield.In year X2 the Dividend Yield falls to 9%. This will not be overly concerning to investors as the increase in share price over the year will have more than made up for the slightly lower yield.

In year X3 the Dividend Yield has fallen to 4.5% which is 50% lower than the previous year. This, combined with the fall in share price and reduced profitability will be a major concern to investors.In year X3 the Dividend Yield has fallen to 4.5% which is 50% lower than the previous year. This, combined with the fall in share price and reduced profitability will be a major concern to investors.In year X3 the Dividend Yield has fallen to 4.5% which is 50% lower than the previous year. This, combined with the fall in share price and reduced profitability will be a major concern to investors.In year X3 the Dividend Yield has fallen to 4.5% which is 50% lower than the previous year. This, combined with the fall in share price and reduced profitability will be a major concern to investors.

P/E Ratio

X1 X2 X3

Share Price $3.30 $4 $2.20

Profit After Tax 280 260 30

No. Ordinary Shares 300 300 300

EPS (280 / 300) = 93c (260 / 300) = 86c (30 / 300) = 10c

P/E Ratio (Share Price / EPS) (330 / 93) = 3.54 (400 / 86) = 4.65 (220 / 10) = 22

The P/E Ratio in year X1 is 3.54. We don not have industry comparatives or prior year information with which to compare this.The P/E Ratio in year X1 is 3.54. We don not have industry comparatives or prior year information with which to compare this.The P/E Ratio in year X1 is 3.54. We don not have industry comparatives or prior year information with which to compare this.The P/E Ratio in year X1 is 3.54. We don not have industry comparatives or prior year information with which to compare this.

In year X2 the P/E Ratio increases to 4.65. This indicates that the market expectations for this share have risen since X1 and that investors are now willing to pay 4.65 times what the business earns in a year to own the share.

In year X2 the P/E Ratio increases to 4.65. This indicates that the market expectations for this share have risen since X1 and that investors are now willing to pay 4.65 times what the business earns in a year to own the share.

In year X2 the P/E Ratio increases to 4.65. This indicates that the market expectations for this share have risen since X1 and that investors are now willing to pay 4.65 times what the business earns in a year to own the share.

In year X2 the P/E Ratio increases to 4.65. This indicates that the market expectations for this share have risen since X1 and that investors are now willing to pay 4.65 times what the business earns in a year to own the share.

In year X4 the P/E ratio has increased dramatically to 22. This is unusual as the earnings have decreased to 12% of the previous year. The share price has fallen to reflect this, but not by as much as would be expected. This may indicate that the market feels that the results in year X3 were perhaps a one-off and that next years results will improve.

In year X4 the P/E ratio has increased dramatically to 22. This is unusual as the earnings have decreased to 12% of the previous year. The share price has fallen to reflect this, but not by as much as would be expected. This may indicate that the market feels that the results in year X3 were perhaps a one-off and that next years results will improve.

In year X4 the P/E ratio has increased dramatically to 22. This is unusual as the earnings have decreased to 12% of the previous year. The share price has fallen to reflect this, but not by as much as would be expected. This may indicate that the market feels that the results in year X3 were perhaps a one-off and that next years results will improve.

In year X4 the P/E ratio has increased dramatically to 22. This is unusual as the earnings have decreased to 12% of the previous year. The share price has fallen to reflect this, but not by as much as would be expected. This may indicate that the market feels that the results in year X3 were perhaps a one-off and that next years results will improve.

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Lecture 3Finance Sources

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

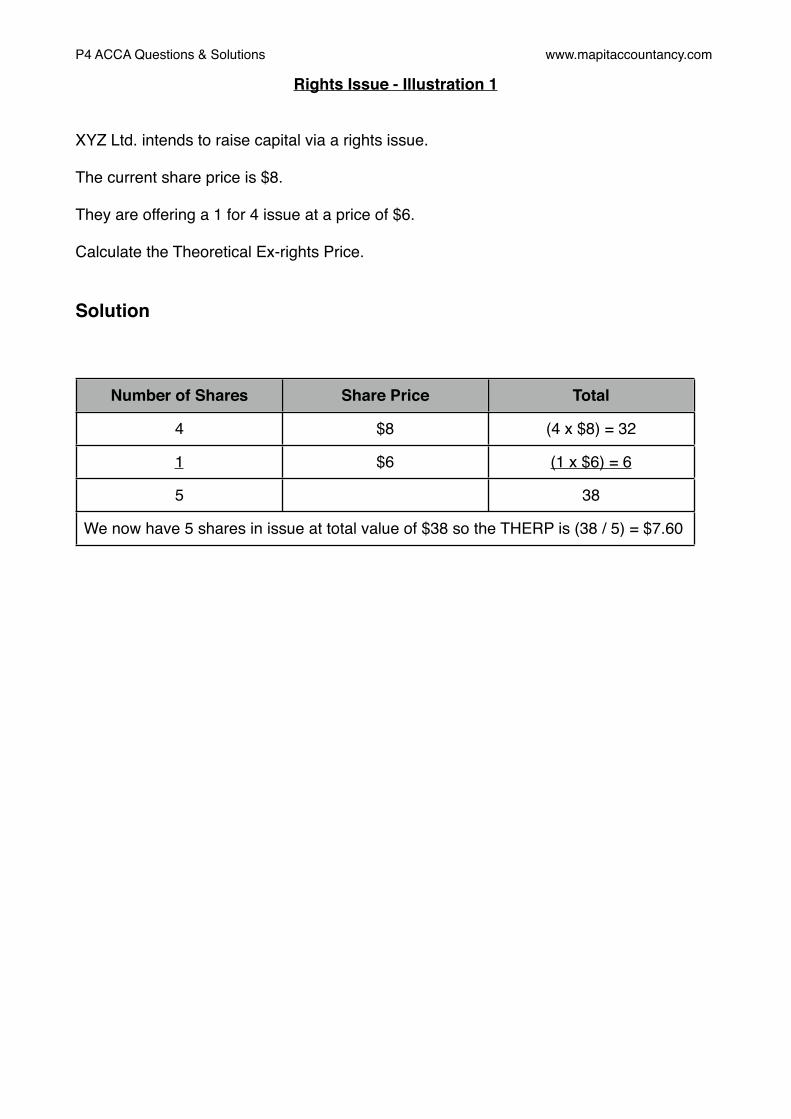

Rights Issue - Illustration 1

XYZ Ltd. intends to raise capital via a rights issue.

The current share price is $8.

They are offering a 1 for 4 issue at a price of $6.

Calculate the Theoretical Ex-rights Price.

Solution

Number of Shares Share Price Total

4 $8 (4 x $8) = 32

1 $6 (1 x $6) = 6

5 38

We now have 5 shares in issue at total value of $38 so the THERP is (38 / 5) = $7.60We now have 5 shares in issue at total value of $38 so the THERP is (38 / 5) = $7.60We now have 5 shares in issue at total value of $38 so the THERP is (38 / 5) = $7.60

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Rights Issue - Illustration 2

ABC Ltd. has decided to raise capital via a rights issue.

The share price is currently $5.50 and ABC intends to raise $5m.

There are currently 6.25m shares in issue and ABC is offering a 1 for 5 rights issue.

Calculate the Theoretical Ex-Rights Price.

Solution

Amount of Capital to raiseAmount of Capital to raise $5m

No. of shares issued (6.25m / 5)No. of shares issued (6.25m / 5) 1.25m

Share issue price ($5m / 1.25m)Share issue price ($5m / 1.25m) $4

Number of Shares Share Price Total

5 $5.50 (5 x 5.50) = 27.5

1 $4 (1 x 4) = 4

6 31.5

We now have 6 shares in issue at total value of $31.5 so the THERP is (31.5 / 6) = $5.25We now have 6 shares in issue at total value of $31.5 so the THERP is (31.5 / 6) = $5.25We now have 6 shares in issue at total value of $31.5 so the THERP is (31.5 / 6) = $5.25

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Lecture 5 Investment Appraisal I

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

ARR - Illustration 1

ABC Ltd are considering expanding their internet cafe business by buying a business which will cost $275,000 to buy and a further $175,000 to refurbish.

They expect the following cash to come in:

Year Net Cash Profits (£)

1 45,000

2 75,000

3 80,000

4 50,000

5 50,000

6 60,000

The equipment will be depreciated to a zero resale value over the same period and, after the sixth year, they can sell the business for $200,000

Calculate the ARR or ROCE of this investment

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Solution

Total Profit over 6 years 45,000 + 75,000 + 80,000 + 50,000 + 50,000 + 60,000

360,000

Total Depreciation Equipment of $175,000 fully depreciated

175,000

Total Profits 185,000

Average Profits $185,000 / 6 years 30,833

Average Investment (Capital Investment + Residual Value) / 2

(450,000 + 200,000) / 2 325,000

ROCE (Ave. Profit / Ave Investment)

30,833 / 325,000 9.5%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Relevant Cash Flow Criteria - Illustration 2

A business is considering investing in a new project. They have already spent $20,000 on a feasibility study which suggests that the project will be profitable.

The headquarters of the company has spare floor space which will be allocated to the project with $7,000 of the current monthly rent allocated to the project.

New equipment costing $2.5m will have to be bought and will be depreciated on a straight line basis over 10 years.

A manager who earns $30,000 per year and currently runs a similar project will also manage the new project taking up 25% of his time.

State whether each of the following items are relevant cash flows and explain your answer.

I. The cost of the feasibility study.

II. The rent charged to the project.

III. The new equipment.

IV. The depreciation on the new equipment.

V. The Managers salary.

Item Relevant Cash Flow?

Explain

Feasibility Study No This is a sunk cost as it has already been paid.

Rent No The rent is not relevant as it must be paid whether the project goes ahead or not. It is not incremental.

New Equipment Yes This is a relevant cash flow.

Depreciation No Depreciation is not a cash-flow but an accounting entry.

Managers Salary No The managers salary must be paid whether the project goes ahead or not so is not relevant.

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Payback Period - Illustration 3

Initial Investment of $5.8m.

Annual Cash Flows of $400,000.

Calculate the Payback Period.

Solution

Payback Period (Initial Investment / Annual Cash Flows)

$5.8m / $400,000 14.5 years

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Payback Period - Illustration 4

Initial Investment of $6.2m.

Cash Flows of:

Year 1: ! $1,200,000

Year 2:! $2,200,000

Year 3:! $2,500,000

Year 4:! $1,700,000

Calculate the Payback Period.

Solution

Year Cash Flows Cumulative Cash Flows

1 1,200,000 1,200,000

2 2,200,000 3,400,000

3 2,500,000 5,900,000

4 1,700,000 7,600,000

Payback period is between 3 and 4 yearsPayback period is between 3 and 4 yearsPayback period is between 3 and 4 years

Additional amount required to return capital (6,200,000 - 5,900,000) = 300,000Additional amount required to return capital (6,200,000 - 5,900,000) = 300,000Additional amount required to return capital (6,200,000 - 5,900,000) = 300,000

Total cash flows in year 4 of 1,700,000 so it will take (300,000 / 1,700,000) x 12 = 2.11 monthsTotal cash flows in year 4 of 1,700,000 so it will take (300,000 / 1,700,000) x 12 = 2.11 monthsTotal cash flows in year 4 of 1,700,000 so it will take (300,000 / 1,700,000) x 12 = 2.11 months

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Discounted Cash-flows - Illustration 5

An investor wants a real return of 10%. Inflation is 5%

What is the MONEY/NOMINAL rate required?

Solution

Use Formula: 1+m = (1+r) x (1+inf)

We are looking for m, therefore:

1+m = (1+0.10) x (1+0.05)

1+m = 1.155

m = 0.155 = 15.5%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Discounted Cash-flows - Illustration 6

A company undertakes a project with the following cash-flows:

Year Cash-Flows

1 5,000

2 7,000

3 8,000

4 10,000

5 11,000

6 9,000

The company has a cost of capital of 10%.

Calculate the present value of the cash flows for each of the six years and in total.

Solution

Year Cash-Flows Discount Rate (From Tables)

Present Value

1 5,000 0.909 4,545

2 7,000 0.826 5,782

3 8,000 0.751 6,008

4 10,000 0.683 6,830

5 11,000 0.621 6,831

6 9,000 0.564 5,076

Total 35,072

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Discounted Cash-flows - Illustration 7

A company undertakes a project with the following cash-flows:

Year Cash-Flows

1 5,000

2 5,000

3 5,000

4 5,000

5 5,000

6 5,000

The company has a cost of capital of 10%.

Calculate the present value of the total cash flows for the six years

Solution

Year Cash-Flows Discount Rate (From Tables)

Present Value

1 5,000 0.909 4,545

2 5,000 0.826 4,130

3 5,000 0.751 3,755

4 5,000 0.683 3,415

5 5,000 0.621 3,105

6 5,000 0.564 2,820

Total 21,770

Years Cash-flow Discount Rate (Annuity Tables)

Present Value

1 - 6 5,000 4.355 21,775

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Discounted Cash-flows - Illustration 8

A company expects to receive $100,000 per year forever.

Their cost of capital is 10%.

Calculate the present value of the perpetuity.

Solution

Annual Cash Flow $100,000

Cost of Capital (10%) 0.10

Perpetuity (Cash-Flow / Cost of Capital) 100,000 / 0.10 = $1m

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Lecture 6 Investment Appraisal II

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

WDA - Illustration 1

A business buys a piece of equipment for $100.

Capital allowances are available at 25% reducing balance.

The tax rate is 30%

After the 4 year project the equipment can be sold for $25.

Solution

Period Balance 25% WDA 30% Tax Saving

Period

1 100.00 25.00 7.50 2

2 75.00 18.75 5.63 3

3 56.25 14.06 4.22 4

4 42.19

Sale of Item -25.00

17.19 5.16 5

Period 0 1 2 3 4 5

Tax Saving

- - 7.5 5.63 4.22 5.16

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Working Capital - Illustration 2

A business requires the following working capital investment into a four year project:

Initial Investment:! ! 30,000

Year 1!! ! ! 35,000

Year 2!! ! ! 45,000

Year 3!! ! ! 32,000

Show the working capital line in the NPV calculation.

Solution

Period 0 1 2 3 4

Total Invested 30,000 35,000 45,000 32,000

Movement to NPV Calculation

-30,000 -5,000 -10,000 13,000 32,000

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

NPV - Illustration 3

A business is evaluating a project for which the following information is relevant:

I. Sales will be $100,000 in the first year and are expected to increase by 5% per year.

II. Costs will be $50,000 and are expected to increase by 7% per year.

III. Capital investment will be $200,000 and attracts tax allowable depreciation of the full value of the investment over the 5 year length of the project.

IV. The tax rate is 30% and tax is payable in the following year.

V. Working Capital invested will be 20% of projected sales for the following year.

VI. General inflation is expected to be 3% over the course of the project and the business uses a real discount rate of 9%.

Calculate the NPV for the project.

Solution

Working 1 - WDAs

Initial Investment WDAs Tax Saving Periods

200,000 (200,000 / 5) = 40,000

(40,000 x 30%) = 12,000

2 - 6

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Working 2 - Inflation

Period 1 2 3 4 5

Sales 100,000 100,000 100,000 100,000 100,000

Inflation - 1.05 1.05 to power of 2

1.05 to power of 3

1.05 to power of 4

Inflated Sales

100,000 105,000 110,250 115,763 121,551

Costs 50,000 50,000 50,000 50,000 50,000

Inflation - 1.07 1.07 to power of 2

1.07 to power of 3

1.07 to power of 4

Inflated Costs

50,000 53,500 57,245 61,252 65,540

Working 3 - Discount Rate

Working

Real Discount Rate In Question 9%

Inflation In Question 3%

Nominal Discount Rate 1 + m = (1 + 0.09) x (1 + 0.03)1 + m = 1.12m = 0.12

12%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Working 4 - Working Capital

Period 0 1 2 3 4 5

Inflated Sales 100,000 105,000 110,250 115,763 121,551

Working Capital Required (20%)

20,000 21,000 22,050 23,153 24,310

Movement -20,000 -1,000 -1,050 -1,103 -1,158 24,310

NPV

Period 0 1 2 3 4 5 6

Inflated Sales (W2)

100,000 105,000 110,250 115,763 121,551

Inflated Costs (W2)

-50,000 -53,500 -57,245 -61,252 -65,540

Profit 50,000 51,500 53,005 54,510 56,011

Tax at 30% -15,000 -15,450 -15,902 -16,353 -16,803

Tax Saving (W1)

12,000 12,000 12,000 12,000 12,000

Capital Investment

-200,000

Working Capital (W4)

-20,000 -1,000 -1,050 -1,103 -1,158 24,310

Total Cash Flows

-220,000 49,000 47,450 48,452 49,451 75,968 -4,803

Discount Rate 12% (W3)

1 0.893 0.797 0.712 0.636 0.567 0.507

Discounted Cash Flows

-220,000 43,757 37,818 34,498 31,451 43,074 -2,435

NPV -31,838

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Lecture 7 - Investment

Appraisal III

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 1

ABC has evaluated a project and come to the following conclusions.

At a discount rate of 10% the NPV will be $100,000

At a discount rate of 15% the NPV will be -$75,000

What is the IRR?

Solution

10 + (100,000/(100,000 +75,000) 5 = 12.85%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 2

Initial Investment (5,000)

Period Cash Flows

1 2,000

2 (1,000)

3 3,500

4 3,800

Cost of Capital 10%

NPV = 1,216

IRR = 19%

Calculate the MIRR.

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Solution

Terminal Value of Inflows

Period Inflow Inflate Value

1 2,000 (1.10)3 2,662

3 3,500 (1.10)1 3,850

4 3,800 1.10 3,800

Terminal ValueTerminal ValueTerminal Value 10,312

Present Value Outflows

Period Outflow Discount Rate PV

0 5,000 1 5,000

2 1,000 0.826 826

Present Value of OutflowsPresent Value of OutflowsPresent Value of Outflows 5,826

Discount Factor where 10,312 x DF (P4) = 5,826

5,826/10,312 = 0.565

Look at tables for Period 4 and find closest to 0.565.

MIRR = 15%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Lecture 8 - Foreign NPV

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 1

Item costs $1,000

€/$ 1 : 2

However inflation in US is 5% and Eurozone 3%

Calculate the exchange rate in one years time.

Solution

Future exchange rate calculation

Exchange rate now x 1+ Inf (counter) / 1 + inf (base)

2 x 1.05 / 1.03 = 2.039

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 2 (i)

US Interest rate = 10%

UK Interest rate = 8%

Exchange rate = €/$ 1 : 2

Predict the exchange rate in 1 year

Solution

Future exchange rate calculation

Exchange rate now x 1+ Int (counter) / 1 + int (base)

2 x 1.10 / 1.08 = 2.037

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 2 (ii)

Current spot rate $/£ 1 : 1

The dollar is expected to strengthen by 7% per anum

Forecast the $:£ rate for the next 4 years.

Solution

Period 0 1 2 3 4

FX Rate 1 1.07 1.145 1.225 1.310

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 3

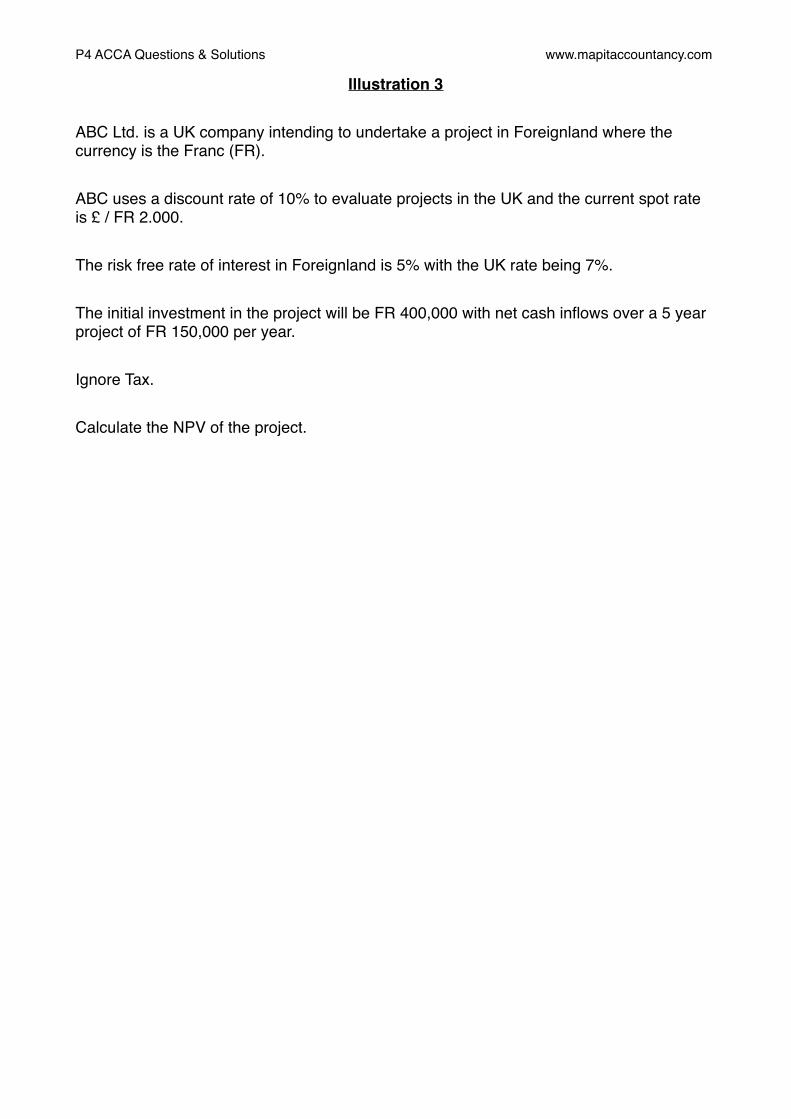

ABC Ltd. is a UK company intending to undertake a project in Foreignland where the currency is the Franc (FR).

ABC uses a discount rate of 10% to evaluate projects in the UK and the current spot rate is £ / FR 2.000.

The risk free rate of interest in Foreignland is 5% with the UK rate being 7%.

The initial investment in the project will be FR 400,000 with net cash inflows over a 5 year project of FR 150,000 per year.

Ignore Tax.

Calculate the NPV of the project.

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Solution

FX CalculationsFX CalculationsFX CalculationsFX CalculationsFX CalculationsFX Calculations

Period 1 2 3 4 5

Rate at start of period 2.000 1.963 1.926 1.890 1.855

IRP (1.05 / 1.07)

(1.05 / 1.07)

(1.05 / 1.07)

(1.05 / 1.07)

(1.05 / 1.07)

FX Rate to use 1.963 1.926 1.890 1.855 1.820

NPV CalculationsNPV CalculationsNPV CalculationsNPV CalculationsNPV CalculationsNPV CalculationsNPV Calculations

Period 0 1 2 3 4 5

Investment -400

Cash Flows (FR) 150 150 150 150 150

FX Rate 2 1.963 1.926 1.890 1.855 1.820

Cash Flows (£) -200.00 76.41 77.88 79.37 80.86 82.42

Discount Rate (10%) 1 0.909 0.826 0.751 0.663 0.621

PV Cash Flows (£) -200.00 69.46 64.33 59.60 53.61 51.18

NPV 98.1998.1998.1998.1998.1998.19

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 4

ABC Ltd. is a UK company intending to undertake a project in Foreignland where the currency is the Franc (FR).

ABC uses a discount rate of 16% to evaluate projects in the UK and the current spot rate is £ / FR 2.000.

The risk free rate of interest in Foreignland is 7% with the UK rate being 9%.

Solution

so....

(1 + DRFoR) / (1 + 0.16) = (1 + 0.07) / (1 + 0.09)

(1 + DRFoR) / (1 + 0.16) = 0.982

(1 + DRFoR) = (1.16 x 0.982)

(1 + DRFoR) = 1.138

DRFoR = 13.8%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 5

ABC Ltd. is a UK company intending to undertake a project in Foreignland where the currency is the Franc (FR).

ABC uses a discount rate of 20% to evaluate projects in the UK and the current spot rate is £ / FR 2.000.

Sterling is expected to appreciate against the Franc by 10% per year.

Solution

so....

If £ appreciates by 10% it will be able to buy 10% more FR which makes one £ worth (2 x 1.1) = 2.2FR

(1 + DRFoR) / (1 + 0.20) = 2.2 / 2

(1 + DRFoR) / (1 + 0.20) = 1.1

(1 + DRFoR) = (1.20 x 1.1)

(1 + DRFoR) = 1.32

DRFoR = 32%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 6

ABC Ltd. is a UK company intending to undertake a project in Foreignland where the currency is the Franc (FR).

ABC uses a discount rate of 10% to evaluate projects in the UK and the current spot rate is £ / FR 2.000.

The risk free rate of interest in Foreignland is 5% with the UK rate being 7%.

The initial investment in the project will be FR 400,000 with net cash inflows over a 5 year project of FR 150,000 per year.

Ignore Tax.

Calculate the NPV of the project by adjusting the discount rate.

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Solution

(1 + DRFoR) / (1 + 0.10) = (1 + 0.05) / (1 + 0.07)

(1 + DRFoR) / (1 + 0.10) = 0.981

(1 + DRFoR) = (1.10 x 0.982)

(1 + DRFoR) = 1.079

DRFoR = 7.9%...say 8%

NPV CalculationsNPV CalculationsNPV CalculationsNPV CalculationsNPV CalculationsNPV CalculationsNPV Calculations

Period 0 1 2 3 4 5

Investment -400

Cash Flows (FR) 150 150 150 150 150

Discount Rate (8%) 1 0.926 0.857 0.794 0.735 0.681

PV Cash Flows (FR) -400.00 138.90 128.55 119.10 110.25 102.15

NPV (FR)NPV (FR)NPV (FR)NPV (FR)NPV (FR)NPV (FR) 198.95

Spot RateSpot RateSpot RateSpot RateSpot RateSpot Rate 2.00

NPV(£)NPV(£)NPV(£)NPV(£)NPV(£)NPV(£) 99.48

This is the same as the NPV in illustration 3 with a slight rounding difference.This is the same as the NPV in illustration 3 with a slight rounding difference.This is the same as the NPV in illustration 3 with a slight rounding difference.This is the same as the NPV in illustration 3 with a slight rounding difference.This is the same as the NPV in illustration 3 with a slight rounding difference.This is the same as the NPV in illustration 3 with a slight rounding difference.This is the same as the NPV in illustration 3 with a slight rounding difference.

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Lecture 9 WACC I

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

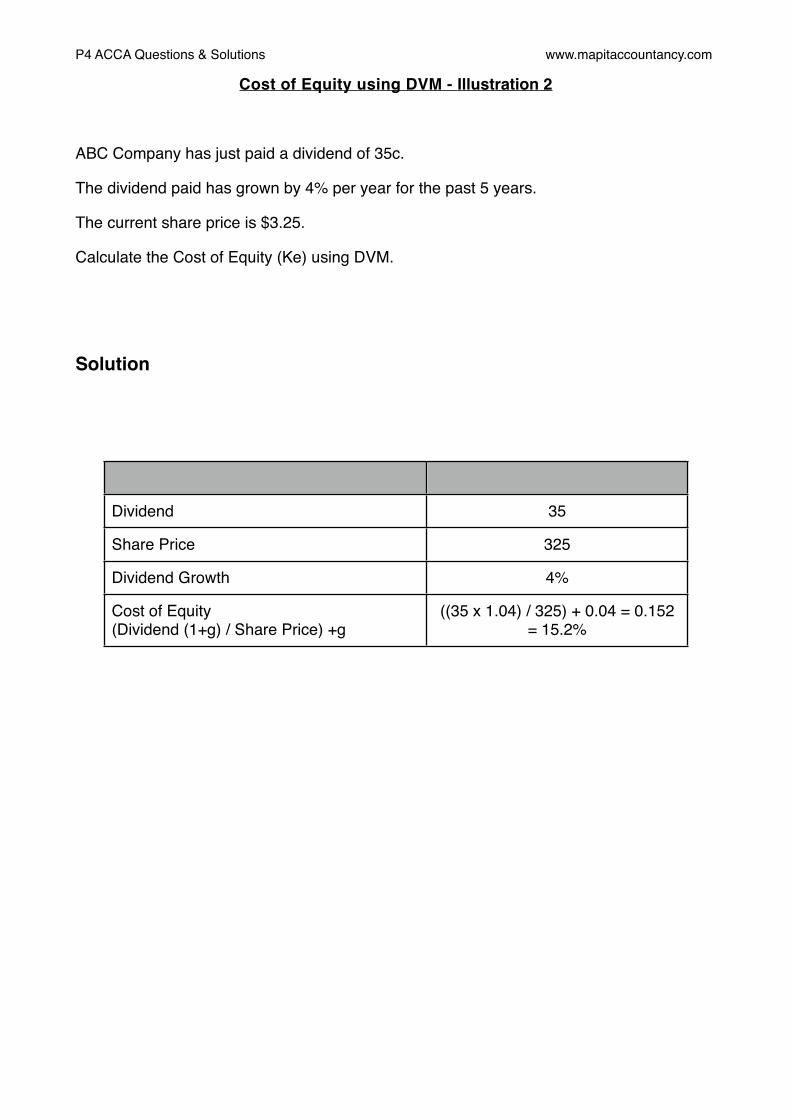

Cost of Equity using DVM - Illustration 1

ABC Company has just paid a dividend of 35c.

The current share price is $3.25.

Calculate the Cost of Equity (Ke) using DVM.

Solution

Dividend 35

Share Price 325

Cost of Equity (Dividend / Share Price) (35 / 325) = 10.76%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Cost of Equity using DVM - Illustration 2

ABC Company has just paid a dividend of 35c.

The dividend paid has grown by 4% per year for the past 5 years.

The current share price is $3.25.

Calculate the Cost of Equity (Ke) using DVM.

Solution

Dividend 35

Share Price 325

Dividend Growth 4%

Cost of Equity (Dividend (1+g) / Share Price) +g

((35 x 1.04) / 325) + 0.04 = 0.152= 15.2%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Cost of Equity using CAPM - Illustration 3

Company A has a Beta of 1.2.

Government bonds are currently trading at 4%.

The average return than investors in the market can expect is 15%.

Calculate the Cost of Equity using CAPM.

Solution

Rf (Risk Free Rate) 4

Rm (Ave Return on the Market) 15

Beta 1.2

Ke = Rf + β(Rm - Rf) (4 + 1.2(15 - 4)) = 17.2%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Cost of Equity using CAPM - Illustration 4

Company A has a Beta of 1.2.

Company B has a Beta of 1.

Government bonds are currently trading at 5%.

The average return than investors in the market can expect is 12%.

Calculate the Cost of Equity using CAPM for each company.

Solution

Company A Company B

Rf (Risk Free Rate) 5 5

Rm (Ave Return on the Market)

12 12

Beta 1.2 1

Ke = Rf + β(Rm - Rf) (5 + 1.2(12 - 5)) = 13.4% (5 + 1(12 - 5)) = 12%

Notice that when Beta is 1 (Company B) Ke is 12% which is the same as the average return on the market.Notice that when Beta is 1 (Company B) Ke is 12% which is the same as the average return on the market.Notice that when Beta is 1 (Company B) Ke is 12% which is the same as the average return on the market.

Also notice that a higher Beta of 1.2 gives a higher Ke of 13.4% showing that a higher Beta means higher risk.Also notice that a higher Beta of 1.2 gives a higher Ke of 13.4% showing that a higher Beta means higher risk.Also notice that a higher Beta of 1.2 gives a higher Ke of 13.4% showing that a higher Beta means higher risk.

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Cost of Equity using CAPM Illustration 5

Company A has a Beta of 1.3.

Company B has a Beta of 1.2.

Government bonds are currently trading at 5%.

The average market risk premium is 6%.

Calculate the Cost of Equity using CAPM for each company.

Solution

Company A Company B

Rf (Risk Free Rate) 5 5

Rm - Rf (Ave Market Risk Premium)

6 6

Beta 1.3 1.2

Ke = Rf + β(Rm - Rf) (5 + 1.3(6) = 12.8% (5 + 1.2(6)) = 12.2%

Remember to look out for the market risk PREMIUM as this is always (Rm - Rf) rather than Rm (Average return on the market)Remember to look out for the market risk PREMIUM as this is always (Rm - Rf) rather than Rm (Average return on the market)Remember to look out for the market risk PREMIUM as this is always (Rm - Rf) rather than Rm (Average return on the market)

Again notice that a higher Beta leads to a higher Ke i.e. more risk.Again notice that a higher Beta leads to a higher Ke i.e. more risk.Again notice that a higher Beta leads to a higher Ke i.e. more risk.

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Lecture 10WACC II

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Irredeemable Debt - Illustration 1

A company has issued 10% irredeemable debt.

The market value of the debt is $90.

The tax rate is 30%

Calculate the cost of debt (Kd).

Solution

Interest paid (Per $100 nominal) $10

Tax Rate 30%

After tax interest (Amount Paid (1 - t)) $10 x (1 - 0.30) = $7

Market Value of Debt (Per $100 nominal) $90

Cost of Debt (After tax interest / Market Value of Debt) (7 / 90) = 7.7%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Redeemable Debt - Illustration 2

A Company has issued debt which is redeemable in 5 years time.

Interest is payable at 8%.

The current market value of the debt is $102.

Ignore taxation.

Calculate the Cost of Debt (Kd).

Solution

Period

Item $ DR 5% PV DR 15% PV

1 -5 Interest 8 4.329 34.63 3.352 26.82

5 Capital 100 0.784 78.40 0.497 49.70

Market Value -102 -102

11.03 -25.48

IRR Calculation: 5 + (11.03 / (11.03 - (25.48)) (15 - 5) = 8.02%IRR Calculation: 5 + (11.03 / (11.03 - (25.48)) (15 - 5) = 8.02%IRR Calculation: 5 + (11.03 / (11.03 - (25.48)) (15 - 5) = 8.02%IRR Calculation: 5 + (11.03 / (11.03 - (25.48)) (15 - 5) = 8.02%IRR Calculation: 5 + (11.03 / (11.03 - (25.48)) (15 - 5) = 8.02%IRR Calculation: 5 + (11.03 / (11.03 - (25.48)) (15 - 5) = 8.02%IRR Calculation: 5 + (11.03 / (11.03 - (25.48)) (15 - 5) = 8.02%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Redeemable Debt - Illustration 3

A Company has issued debt which is redeemable in 5 years time.

Interest is payable at 10%.

The current market value of the debt is $104.

Tax is payable at 30%.

Calculate the Cost of Debt (Kd).

Solution

Period

Item $ DR 5% PV DR 15% PV

1 -5 Interest (10 x (1 - 0.3)

7 4.329 30.30 3.352 23.46

5 Capital 100 0.784 78.40 0.497 49.70

Market Value -104 -104

4.70 -30.84

IRR Calculation: 5 + (4.7 / (4.7 - (30.84)) (15 - 5) = 6.32%IRR Calculation: 5 + (4.7 / (4.7 - (30.84)) (15 - 5) = 6.32%IRR Calculation: 5 + (4.7 / (4.7 - (30.84)) (15 - 5) = 6.32%IRR Calculation: 5 + (4.7 / (4.7 - (30.84)) (15 - 5) = 6.32%IRR Calculation: 5 + (4.7 / (4.7 - (30.84)) (15 - 5) = 6.32%IRR Calculation: 5 + (4.7 / (4.7 - (30.84)) (15 - 5) = 6.32%IRR Calculation: 5 + (4.7 / (4.7 - (30.84)) (15 - 5) = 6.32%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

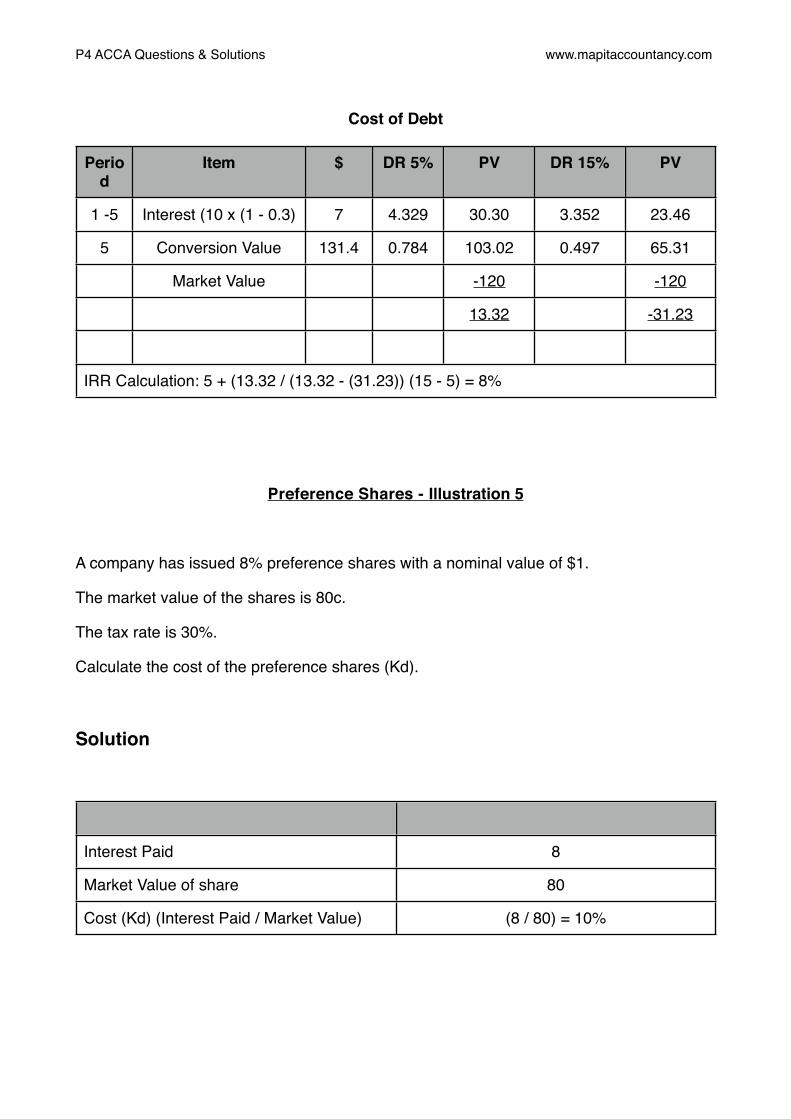

Convertible Debt - Illustration 4

A Company has issued debt which is convertible in 5 years time.

Interest is payable at 10%.

The current market value of the debt is $120.

On conversion, investors will have a choice of either:

I. Cash at a 15% premium; or

II. 18 shares per loan note.

The current share price is $6 and it is expected to grow in value by 4% per year.

Tax is payable at 30%.

Calculate the Cost of Debt (Kd).

Solution

Working 1 - Cash or Convert?

Working

Cash (15% Premium) 100 x 1.15 $115

Shares

Current Value $6

Value in 5 years with 4% growth

6 x (1.04 to the power of 5) $7.30

Number of shares per $100 18

Conversion Value 7.30 x 18 $131.40

The conversion value is higher than the cash so the investors will choose to convert.The conversion value is higher than the cash so the investors will choose to convert.The conversion value is higher than the cash so the investors will choose to convert.

Do an IRR the same as for redeemable but filling $131.40 into the capital repaidDo an IRR the same as for redeemable but filling $131.40 into the capital repaidDo an IRR the same as for redeemable but filling $131.40 into the capital repaid

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Cost of Debt

Period

Item $ DR 5% PV DR 15% PV

1 -5 Interest (10 x (1 - 0.3) 7 4.329 30.30 3.352 23.46

5 Conversion Value 131.4 0.784 103.02 0.497 65.31

Market Value -120 -120

13.32 -31.23

IRR Calculation: 5 + (13.32 / (13.32 - (31.23)) (15 - 5) = 8%IRR Calculation: 5 + (13.32 / (13.32 - (31.23)) (15 - 5) = 8%IRR Calculation: 5 + (13.32 / (13.32 - (31.23)) (15 - 5) = 8%IRR Calculation: 5 + (13.32 / (13.32 - (31.23)) (15 - 5) = 8%IRR Calculation: 5 + (13.32 / (13.32 - (31.23)) (15 - 5) = 8%IRR Calculation: 5 + (13.32 / (13.32 - (31.23)) (15 - 5) = 8%IRR Calculation: 5 + (13.32 / (13.32 - (31.23)) (15 - 5) = 8%

Preference Shares - Illustration 5

A company has issued 8% preference shares with a nominal value of $1.

The market value of the shares is 80c.

The tax rate is 30%.

Calculate the cost of the preference shares (Kd).

Solution

Interest Paid 8

Market Value of share 80

Cost (Kd) (Interest Paid / Market Value) (8 / 80) = 10%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Bank Debt - Illustration 6

A company has a bank loan of $2m at an interest rate of 10%.

The tax rate is 30%.

Calculate the cost of debt (Kd).

Solution

Interest Rate before Tax 10

Tax Rate 30%

After Tax Cost of Debt (10 x (1 - 0.3)) 7%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

WACC - Illustration 7

Company A is funded as follows:

Item Capital Structure Cost

Equity 85% 15%

Debt 15% 7%

Calculate the Weighted Average Cost of Capital.

Solution

Item Capital Structure Cost Ave

Equity 85% 15 12.75

Debt 15% 7 1.05

WACC 13.8

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

WACC - Illustration 8

Company A is funded as follows:

Balance Sheet Extract

Ordinary Shares (50c) 3000

Loan Notes 2000

Bank Loan 1000

The cost to the company of each of the above items has been calculated as:

Ordinary Shares 13%

Loan Notes 8%

Bank Loan 5%

The Loan notes are currently trading at $94.

The current share price is $1.50

Calculate the Weighted Average Cost of Capital.

Solution

Working 1 - Calculate Cost of Capital for each item.

Given in the QuestionGiven in the Question

Ordinary Shares 13%

Loan Notes 8%

Bank Loan 5%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Working 2 - Calculate the Market Value of Debt and Equity.

SFP Market Value

Ordinary Shares (50c)

3000 No. of shares (3000 / 0.50) = 6000Share Price = $1.50

(6000 x $1.50) = 9000

Loan Notes 2000 Loan Notes nominal value (on SFP) = 100Market Value = 94

(2000 x (94 / 100) = 1880

Bank Loan 1000 No market for this so use SFP value

1000

Working 3 - Calculate the weighting of each item.

Item Market Value Weighting

Equity 9000 (9000 / 11,880) = 75.75%

Loan Notes 1880 (1880 / 11,880) = 15.82%

Bank Loan 1000 (1000 / 11,880) = 8.41%

11880

Working 4 - Weighted Average Cost of Capital

Item Market Value

Weighting Cost (W1)

Ave

Equity 9000 (9000 / 11,880) 13 (9000 / 11,880) x 13 = 9.85

Loan Notes 1880 (1880 / 11,880) 8 (1880 / 11,880) x 8 = 1.27

Bank Loan 1000 (1000 / 11,880) 5 (1000 / 11,880) x 5 = 0.42

11880 WACC 11.54%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

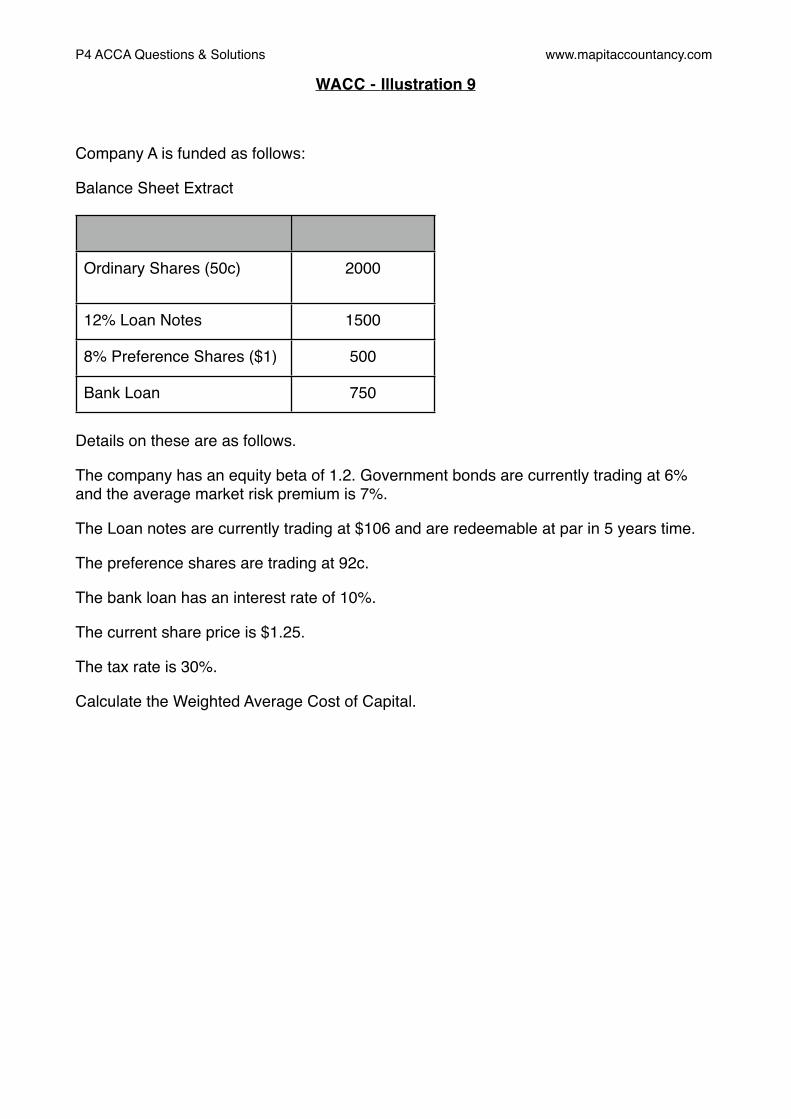

WACC - Illustration 9

Company A is funded as follows:

Balance Sheet Extract

Ordinary Shares (50c) 2000

12% Loan Notes 1500

8% Preference Shares ($1) 500

Bank Loan 750

Details on these are as follows.

The company has an equity beta of 1.2. Government bonds are currently trading at 6% and the average market risk premium is 7%.

The Loan notes are currently trading at $106 and are redeemable at par in 5 years time.

The preference shares are trading at 92c.

The bank loan has an interest rate of 10%.

The current share price is $1.25.

The tax rate is 30%.

Calculate the Weighted Average Cost of Capital.

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Solution

Working 1 - Calculate Cost of Capital for each item.

Cost of Equity using CAPM

Rf (Risk Free Rate) 6

(Rm - Rf)(Ave market risk premium) 7

Beta 1.2

Ke = Rf + β(Rm - Rf) (6 + 1.2(7)) = 14.4%

Cost of 12% Loan Notes

Period

Item $ DR 5% PV DR 15% PV

1 -5 Interest (12 x (1 - 0.3)

8.4 4.329 36.36 3.352 28.16

5 Capital 100 0.784 78.40 0.497 49.70

Market Value -106 -106

8.76 -28.14

IRR Calculation: 5 + (8.76 / (8.76 - (28.14)) (15 - 5) = 7.37%IRR Calculation: 5 + (8.76 / (8.76 - (28.14)) (15 - 5) = 7.37%IRR Calculation: 5 + (8.76 / (8.76 - (28.14)) (15 - 5) = 7.37%IRR Calculation: 5 + (8.76 / (8.76 - (28.14)) (15 - 5) = 7.37%IRR Calculation: 5 + (8.76 / (8.76 - (28.14)) (15 - 5) = 7.37%IRR Calculation: 5 + (8.76 / (8.76 - (28.14)) (15 - 5) = 7.37%IRR Calculation: 5 + (8.76 / (8.76 - (28.14)) (15 - 5) = 7.37%

Cost of Preference Shares

Interest Paid 8

Market Value of share 92

Cost (Kd) (Interest Paid / Market Value) (8 / 92) = 8.7%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Cost of Bank Debt

Interest Rate before Tax 10

Tax Rate 30%

After Tax Cost of Debt (10 x (1 - 0.3)) 7%

Working 2 - Calculate the Market Value of Debt and Equity.

SFP Market Value

Ordinary Shares (50c)

2000 No. of shares (2000 / 0.50) = 4000Share Price = $1.25

(4000 x $1.25) = 5000

12% Loan Notes

1500 Loan Notes nominal value (on SFP) = 100Market Value = 106

(1500 x (106 / 100) = 1590

8% Preference Shares ($1)

500 Preference shares nominal value (on SFP) = $1Market Value = 92c

(500 x (92 / 1)) = 460

Bank Loan 750 No market for this so use SFP figure

750

Working 3 - Calculate the weighting of each item.

Item Market Value Weighting

Equity 5000 (5000 / 7800)

Loan Notes 1590 (1590 / 7800)

Preference Shares 460 (460 / 7800)

Bank Loan 750 (750 / 7800)

7800

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Working 4 - Weighting & Weighted Average Cost of Capital

Item Market Value

Weighting Cost (W1)

Ave

Equity 5000 (5000 / 7800) 14.4 (5000 / 7800) x 14.4 = 9.23

Loan Notes 1590 (1590 / 7800) 7.37 (1590 / 7800) x 7.37 = 1.50

Preference Shares

460 (460 / 7800) 8.7 (460 / 7800) x 8.7 = 0.51

Bank Loan 750 (750 / 7800) 7 (750 / 7800) x 7 = 0.67

7800 WACC 11.91%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Lecture 11 Capital Structure

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Capital Structure - Illustration 1

A company has total capital of $1,000 with debt making up $300 and equity making up $700 of the total. The company’s cost of debt is 5% and cost of equity is 14%.

I. Calculate the company’s current WACC.II. Calculate the WACC if the company substitutes $200 of equity for $200 of debt

causing their cost of equity to rise to 16%.III. Calculate the WACC if the company substitutes $300 of equity for $300 of debt

causing their cost of equity to rise to 25%.

Solution

I.

Item Market Value Weighting Cost WACC

Debt 300 300 / 1000 5% 1.5

Equity 700 700 / 1000 14% 9.8

1000 11.3

II.

Item Market Value Weighting Cost WACC

Debt 500 500 / 1000 5% 2.5

Equity 500 500 / 1000 16% 8

1000 10.5

III.

Item Market Value Weighting Cost WACC

Debt 600 600 / 1000 5% 3

Equity 400 400 / 1000 25% 10

1000 13

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Lecture 12 M & M Formulae

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

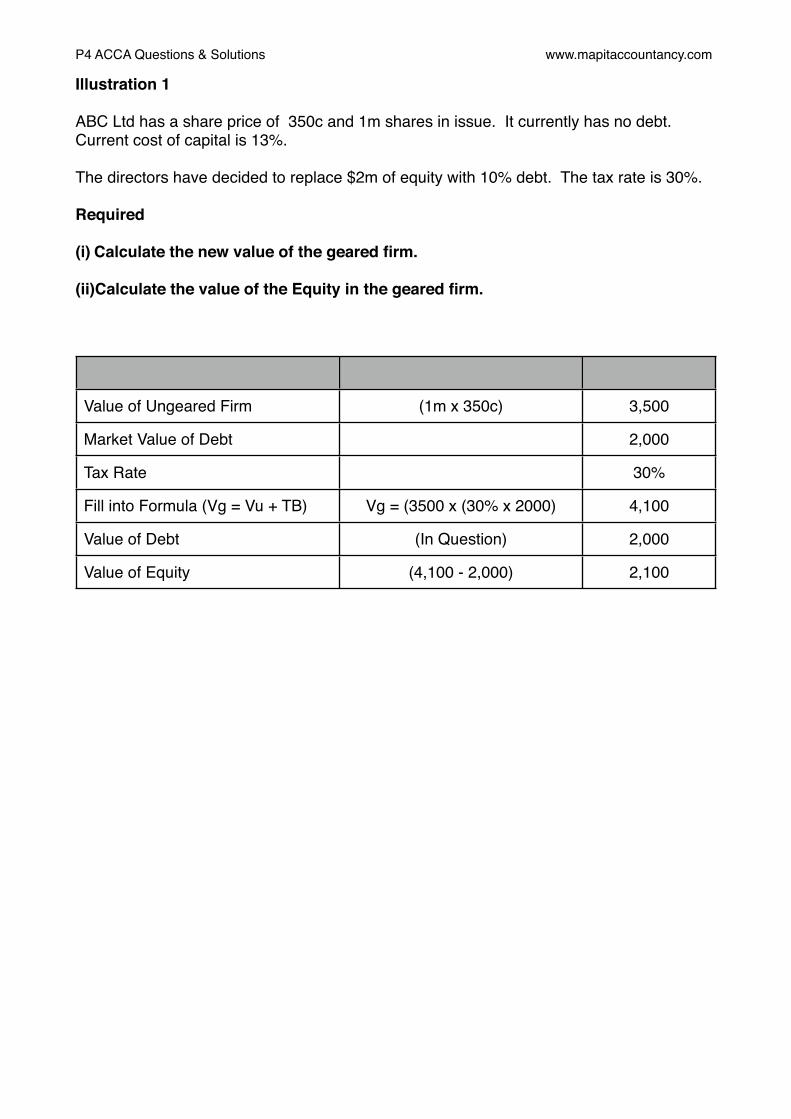

Illustration 1 ABC Ltd has a share price of 350c and 1m shares in issue. It currently has no debt. Current cost of capital is 13%. The directors have decided to replace $2m of equity with 10% debt. The tax rate is 30%. Required

(i) Calculate the new value of the geared firm.

(ii)Calculate the value of the Equity in the geared firm.

Value of Ungeared Firm (1m x 350c) 3,500

Market Value of Debt 2,000

Tax Rate 30%

Fill into Formula (Vg = Vu + TB) Vg = (3500 x (30% x 2000) 4,100

Value of Debt (In Question) 2,000

Value of Equity (4,100 - 2,000) 2,100

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 2

ABC Co. and CD Co. operate in the same industry and are identical in their ability to generate cash flows.

ABC Co. is financed by Equity only of 3m shares with current value of $1 and has a cost of equity calculated at 15%.

CD Co. has the same total capital but within it has irredeemable debt with a market value of $0.9m.

The tax rate is 33%.

Required

(i) Calculate the value of CD Co.

(ii)Calculate the value of the Equity in CD Co.

Solution

Value of Ungeared Firm (3m x 100c) 3,000

Market Value of Debt 900

Tax Rate 33%

Fill into Formula (Vg = Vu + TB) Vg = (3,000 x (33% x 900) 3,297

Value of Debt (In Question) 900

Value of Equity (3,297 - 900) 2,397

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 3

ABC Co. and CD Co. operate in the same industry and are identical in their ability to generate cash flows.

ABC Co. is financed by Equity only of 3m shares with current value of $1 and has a cost of equity calculated at 15%.

CD Co. has the same total capital but within it has irredeemable debt with a market value of $0.9m and cost of debt of 8%.

The tax rate is 33%.

Required

(i) Calculate the Cost of Equity for CD Co.

Solution

Keg = Keu + (Keu - Kd) Vd(1-t)/Ve

Keg = 15 + (15 - 8) 900(1-0.33) / 2397

Keg = 16.76%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 4

ABC Co. and CD Co. operate in the same industry and are identical in their ability to generate cash flows.

ABC Co. is financed by Equity only of 3m shares with current value of $1 and has a cost of equity calculated at 15%.

CD Co. has the same total capital but within it has irredeemable debt with a market value of $0.9m and cost of debt of 8%.

The tax rate is 33%.

Required

(i) Calculate the WACC for CD Co.

Solution

Kadj = Keu (1 - tL)

Kadj = 15 (1 - (0.33 x (900 / 3,297)))

Kadj = 13.65

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Lecture 14Risk Adjusted WACC

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Risk Adjusted WACC - Illustration 1

Company A intends to undertake a project in an unrelated industry.

The following details are relevant:

Item Company A Proxy Company

Equity Beta (βe) 1.2 1.4

Value of Equity 1000 800

Value of Debt 400 500

The risk free rate is 4%.

The average return on the market is 12%.

The post tax cost of debt is 7%.

Calculate the risk adjusted WACC to be used in evaluating the project.

Ignore Tax

Solution

Working 1 - Un-gear the proxy βe to get βa.

Proxy Equity Beta 1.4

Value of Equity of Proxy 800

Value of Debt of Proxy 500

βu = βg(Ve / (Ve + Vd)) 1.4 (800 / (800 + 500)) = 0.86

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Working 2 - Re-gear βa with our capital structure

βa 0.86

Value of Equity of Company A 1000

Value of Debt of Company A 400

βg = βu + (βu -βd) (Vd / Ve) 0.86 + (0.86 x (400 / 1000) = 1.20

Working 3 - Fill into CAPM

Rf (Risk Free Rate) 4

Rm (Ave return on the market) 12

Beta 1.2

Ke = Rf + β(Rm - Rf) (4 + 1.2(12 - 4)) = 13.6%

Working 4 - Risk Adjusted WACC

Item Market Value Weighting Cost Ave

Equity 1000 (1000 / 1400) 13.6 9.71

Debt 400 (400 / 1400) 7 2.00

1400 WACC 11.71

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

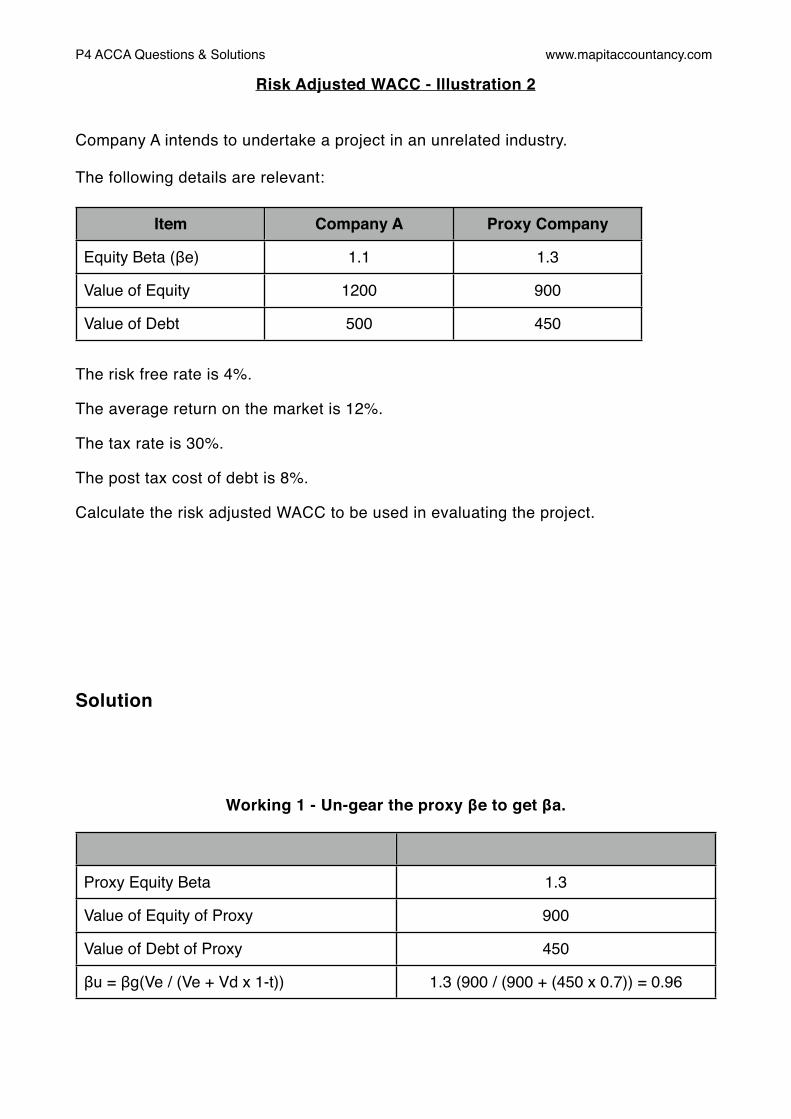

Risk Adjusted WACC - Illustration 2

Company A intends to undertake a project in an unrelated industry.

The following details are relevant:

Item Company A Proxy Company

Equity Beta (βe) 1.1 1.3

Value of Equity 1200 900

Value of Debt 500 450

The risk free rate is 4%.

The average return on the market is 12%.

The tax rate is 30%.

The post tax cost of debt is 8%.

Calculate the risk adjusted WACC to be used in evaluating the project.

Solution

Working 1 - Un-gear the proxy βe to get βa.

Proxy Equity Beta 1.3

Value of Equity of Proxy 900

Value of Debt of Proxy 450

βu = βg(Ve / (Ve + Vd x 1-t)) 1.3 (900 / (900 + (450 x 0.7)) = 0.96

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Working 2 - Re-gear βa with our capital structure

βa 0.96

Value of Equity of Company A 1200

Value of Debt of Company A 500

βg = βu + (βu -βd) (Vd (1-t)/ Ve) 0.96 + (0.96 x 500/1200) = 1.24

Working 3 - Fill into CAPM

Rf (Risk Free Rate) 4

Rm (Ave return on the market) 12

Beta 1.24

Ke = Rf + β(Rm - Rf) (4 + 1.24(12 - 4)) = 13.92%

Working 4 - Risk Adjusted WACC

Item Market Value Weighting Cost Ave

Equity 1200 (1200 / 1700) 13.92 9.83

Debt 500 (500 / 1700) 8 2.35

1700 WACC 12.18

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 3

Company A Company B

Debt/Equity 1/3 1/4

Equity Beta 1.2

Debt Beta 0.3

Assume that the Asset Beta and the Debt Beta of each firm is the same.

Calculate the Equity Beta for Company B.

Solution

Ungear Equity Beta Company A:

Ba = (1.2 (3/4)) + (0.3 (1/4) = 0.9 + 0.075 = 0.975

Regear Asset Beta for Company B:

Be = 0.975 + ((0.975 -0.3) 1/4) = 1.14

or

0.975 = Be (4/5) + 0.3 (1/5)

0.975 - (0.3 x 1/5) = Be (4/5)

0.915 = Be (4/5)

Be = 0.915 x 5/4

Be = 1.14

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Lecture 15 APV

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 1

Cost of Equity in Geared Firm = 12%

Cost of Debt = 8%

Debt/Equity ratio = 1/2

Tax rate = 30%

Calculate the cost of equity in an ungeared firm.

Solution

12% = Keu + (Keu - 8%) (1(1 - 0.3) / 2)

12% = Keu + 0.35Keu - 2.8%

14.8% = 1.35 Keu

Keu = 10.96%

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

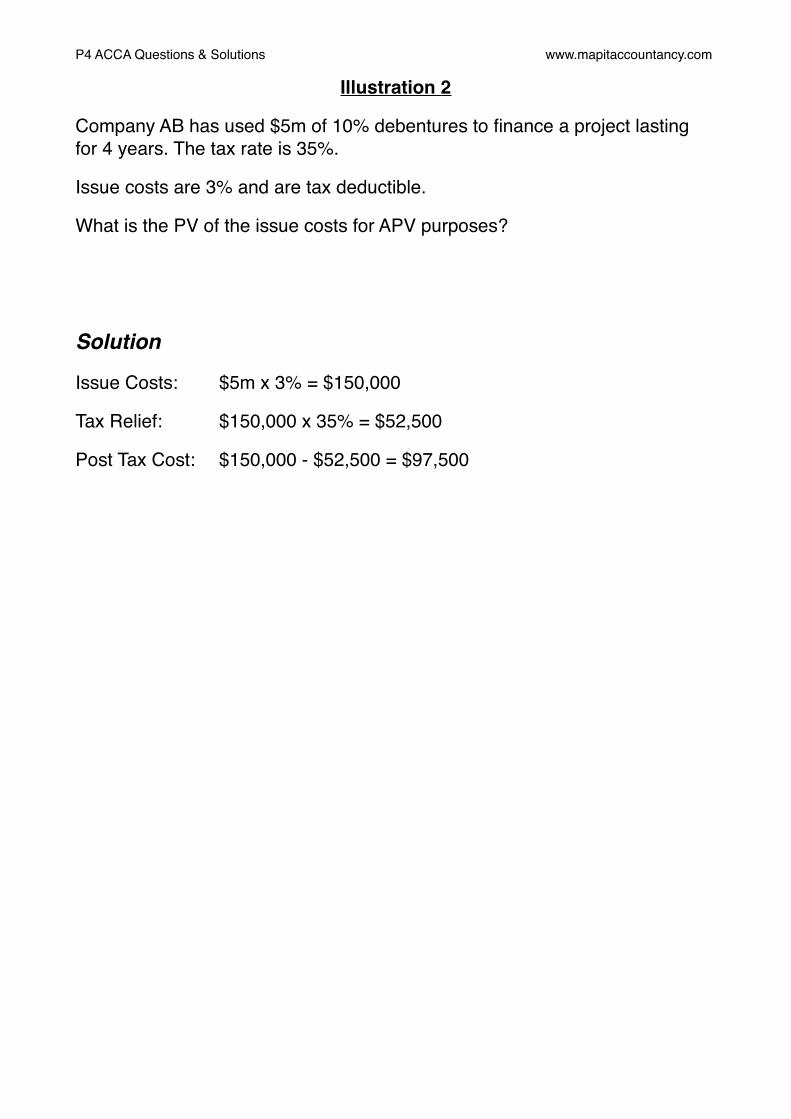

Illustration 2

Company AB has used $5m of 10% debentures to finance a project lasting for 4 years. The tax rate is 35%.

Issue costs are 3% and are tax deductible.

What is the PV of the issue costs for APV purposes?

Solution

Issue Costs:! $5m x 3% = $150,000

Tax Relief:! ! $150,000 x 35% = $52,500

Post Tax Cost:! $150,000 - $52,500 = $97,500

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 3

Company AB has used $5m of 10% debentures to finance a project lasting for 4 years. The tax rate is 35%.

Issue costs are 3% and are tax deductible. These are to be raised along with the finance.

What is the PV of the issue costs for APV purposes?

Solution

Required Finance: ! $5m is 97% of total to raise

! ! ! ! ...so ($5m / 0.97) $5,154,639 must be raised.

Issue Costs:! ! $5,154,639 x 3% = $154,639

Tax Relief:! ! ! $154,639 x 35% = $54,124

Post Tax Cost:! ! $154,639 - $54,124 = $100,515

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 4

Company AB has used $5m of 10% debentures to finance a project lasting for 4 years. The tax rate is 35%.

What is the PV of the tax relief available for APV purposes?

Solution

Annual Interest = $5m x 10% = $500,000

Annual Tax relief = $500,000 x 35% = $175,000

PV Tax relief = $175,000 x 3.170 = $554, 750

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 5

Company AC needs to raise $10m in debt finance for 4 years.

Company AB has raised $7m of 10% debentures and the rest is provided by a subsidised government loan of $3m at 5%.

The tax rate is 30%.

Calculate the financing effects of the debt for APV purposes.

Solution

PV Tax Shield

Annual Interest = ($7m x 10%) + ($3m x 5%) = $850,000

Annual Tax relief = $850,000 x 30% = $255,000

PV Tax relief = $255,000 x 3.170 = $808,350

Cheap Loan

Interest Saved = ($3m x (10% - 5%)) = $150,000

Tax Relief Lost = ($150,000 x 30%) = $45,000

Net Saving = ($150,000 - $45,000) = $105,000

Discount at the cost of debt as even though discounted it has the same risk as a normal loan...

PV Interest Saved = ($105,000 x 3.170) = $332,850

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 6

ABC Co. is considering a project which is expected to generate cash inflows of $500,000 per year for 5 years and cost $500,000 of initial investment.

Costs have been estimated at $350,000 per year.

ABC has a current cost of equity of 14% and a cost of debt of 7% and a current debt to equity ratio of 1/3.

To undertake the the project the $500,000 will be raised through a bond issue of 8% with issue costs of 4% to be raised in addition to the finance.

The tax rate is 30%.

Solution

Un-gear the cost of equity

14% = Keu + (Keu - 7%) (1(1 - 0.3) / 3)

14% = Keu + 0.23Keu - 1.63%

15.63% = 1.23 Keu

Keu = 12.71% say 13%

Base Case NPV

Discount at un-geared Ke of 13%

PV Cash Inflows = ($500,000 x 3.517) = $1,758,500

PV Outflows = ($350,000 x 3.517) = $1,230,950

Net Cash Inflow = $527,550

Initial Investment = $500,000

Base Case NPV = ($527,550 - $500,000) = $27,550

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Issue Costs

Required Finance: ! $500,000 is 96% of total to raise

! ! ! ! ...so ($500,000 / 0.96) $520,833 must be raised.

Issue Costs:! ! $520,833 x 4% = $20,833

Tax Relief:! ! ! $20,833 x 30% = $6,250

Post Tax Cost:! ! $20,833 - $6,250 = $14,583

PV Tax Shield

Annual Interest = ($520,833 x 8%) = $41,666

Annual Tax relief = $41,666 x 30% = $12,500

PV Tax relief = $12,500 x 3.993 = $49,912

APV

Base Case NPV! = ! $27,550

PV Issue Costs ! = ($14,583)

PV Tax Shield ! = $38,040

APV! ! ! = $51,007

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Lecture 16 More Risk

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 1 ABC Ltd is undertaking a project costing $900m with expected net cash flows of $400m in years 1 & 2 then $600m in year 3.

The FD considers that these cash flows may be overestimated by as much as 10% in year 1, 15% in year 2 and 20% in year 3.

The risk free rate is 5% Required

Using certainty equivalents calculate the expected NPV of the project.

Solution

0 1 2 3

Cash Flows -900 400 400 600

Certainty Equivalents 1 0.9 0.85 0.80

CE Cash Flows -900 360 340 480

Discount Rate (5%) 1 0.952 0.907 0.864

Present Value -900 343 308 415

NPVNPVNPVNPV 166

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Lecture 17 Options Pricing I

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 1

Current Share Price:! ! $120Exercise Price:! ! ! $100Risk Free Interest Rate:! ! 10%Variance of Shares:!! ! 25%Time to Expiry:! ! ! 3 months

Solution

Time in Years to Expiry

3 months = 0.25 Years so 0.25 for formula

Standard Deviation of Share Price

Variance is 25% so that’s...0.25

To get SD we need to take square root of this which is 0.5

We work out d1 later but lets say it’s 0.95 when we calculate it....

Find 0.95 on Normal Distribution table.

Read table to find applicable number....0.3289.

0.95 is greater than 0 so add 0.5 to number from the table...

0.3289 + 0.5 = 0.8289....this is N(d1).

Find d1 first...

In(Pa/Pe) + (r + 0.5s2)ts√t

In(120/100) + (0.1 + 0.5 x 0.52)0.250.5 √0.25

0.1823 + 0.056250.25

d1 = 0.95

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Find 0.95 on Normal Distribution table.

Read table to find applicable number....0.3289.

0.95 is greater than 0 so add 0.5 to number from the table...

0.3289 + 0.5 = 0.8289....this is N(d1).

Now d2...

d2 = d1- s√t

d2 = 0.95 - 0.5 √0.25

d2 = 0.7

Find 0.7 on Normal Distribution table.

Read table to find applicable number....0.2580.

0.7 is greater than 0 so add 0.5 to number from the table...

0.2580 + 0.5 = 0.7580....this is N(d2).

Fill into Black-Scholes model...

Call Option Value = PaN(d1) - PeN(d2)e-rt

Call Option Value = (120 x 0.8289) - 100 x 0.7580e-(0.1 x 0.25)

Call Option Value = (99.46 - 73.53) = 25.53

Intrinsic Value: (120 - 100) = $20

Time Value: (25.53 - 20) = $5.53

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

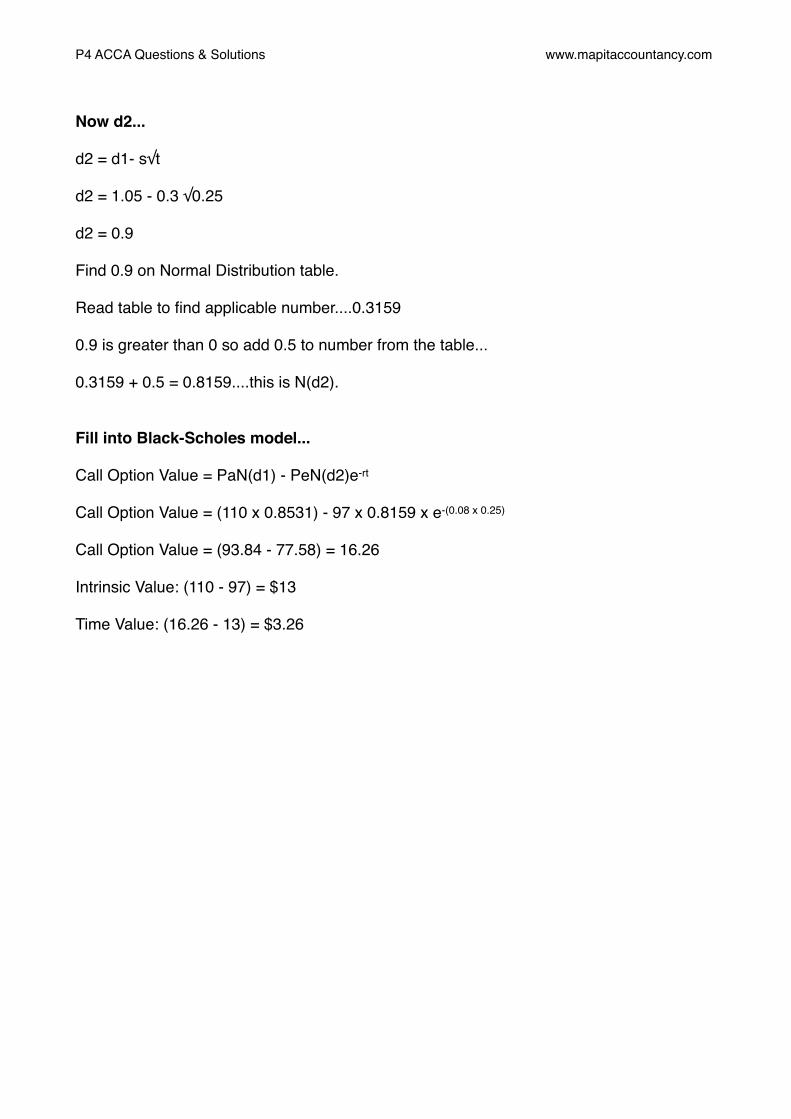

Illustration 2

Current Share Price:! ! $110Exercise Price:! ! ! $97Risk Free Interest Rate:! ! 8%Standard Deviation Shares:! 30%Time to Expiry:! ! ! 3 months

Solution

Time in Years to Expiry

3 months = 0.25 Years so 0.25 for formula

Standard Deviation of Share Price

This is given to us as 30%....so 0.3.

Find d1 first...

In(Pa/Pe) + (r + 0.5s2)ts√t

In(110/97) + (0.08 + 0.5 x 0.32)0.250.3 √0.25

0.126 + 0.031250.15

d1 = 1.05

Find 1.05 on Normal Distribution table.

Read table to find applicable number....0.3531.

1.05 is greater than 0 so add 0.5 to number from the table...

0.3531 + 0.5 = 0.8531....this is N(d1).

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Now d2...

d2 = d1- s√t

d2 = 1.05 - 0.3 √0.25

d2 = 0.9

Find 0.9 on Normal Distribution table.

Read table to find applicable number....0.3159

0.9 is greater than 0 so add 0.5 to number from the table...

0.3159 + 0.5 = 0.8159....this is N(d2).

Fill into Black-Scholes model...

Call Option Value = PaN(d1) - PeN(d2)e-rt

Call Option Value = (110 x 0.8531) - 97 x 0.8159 x e-(0.08 x 0.25)

Call Option Value = (93.84 - 77.58) = 16.26

Intrinsic Value: (110 - 97) = $13

Time Value: (16.26 - 13) = $3.26

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Lecture 18 Options Pricing II

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 1

Current Share Price:! ! $120Exercise Price:! ! ! $100Risk Free Interest Rate:! ! 10%Variance of Shares:!! ! 25%Time to Expiry:! ! ! 3 months

We already calculated in the last lecture that the call option value is $25.53.

Calculate the value of the corresponding put option.

Solution

Put Option Valuation is...

P = c - Pa + Pe x e-rt

P = 25.53 - 120 + 100 x e-(0.1 x 0.25)

P = 25.53 - 120 + 97.53

P = $2.53

P4 ACCA Questions & Solutions www.mapitaccountancy.com!

Illustration 2

ABC Ltd. has an option in CD Ltd. which is due to expire in 6 months.

A dividend of 55 cents is due to be paid in 3 months time and the current share price is $15.

The risk free rate is 10%.

Calculate the dividend-adjusted share price.

Solution

We need the present value of the dividends so...

Divs x e-rt

55 x e-(0.1 x 0.25)

= 53.64c

Subtract this from the share price...

$15 - $0.54 = $14.46

P4 ACCA Questions & Solutions www.mapitaccountancy.com!