CIMA Paper P3 Performance Strategy For exams in 2012 theexpgroup.com Notes

P3 Express Notes

Oct 22, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CIMA Paper P3 Performance Strategy For exams in 2012

theexpgroup.com

Notes

ExPress Notes CIMA P3 Performance Strategy

Page | 2 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

Contents

About ExPress Notes 3

1. Management Control Systems 7

2. Risk and Internal Control 11

3. Review and Audit of Control Systems 24

4. Management of Financial Risk 27

5. Risk and Control in Information Systems 48

ExPress Notes CIMA P3 Performance Strategy

Page | 3 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

START About ExPress Notes

We are very pleased that you have downloaded a copy of our ExPress notes for this paper. We expect that you are keen to get on with the job in hand, so we will keep the introduction brief.

First, we would like to draw your attention to the terms and conditions of usage. It’s a condition of printing these notes that you agree to the terms and conditions of usage. These are available to view at www.theexpgroup.com. Essentially, we want to help people get through their exams. If you are a student for the CIMA exams and you are using these notes for yourself only, you will have no problems complying with our fair use policy.

You will however need to get our written permission in advance if you want to use these notes as part of a training programme that you are delivering.

WARNING! These notes are not designed to cover everything in the syllabus!

They are designed to help you assimilate and understand the most important areas for the exam as quickly as possible. If you study from these notes only, you will not have covered everything that is in the CIMA syllabus and study guide for this paper.

Components of an effective study system

On ExP classroom courses, we provide people with the following learning materials:

• The ExPress notes for that paper • The ExP recommended course notes / essential text or the ExPedite classroom

course notes where we have published our own course notes for that paper • The ExP recommended exam kit for that paper. • In addition, we will recommend a study text / complete text from one of the CIMA

official publishers, but we do not necessarily give this as part of a classroom course, as we think that it can sometimes slow people down and reduce the time that they are able to spend practising past questions.

ExP classroom course students will also have access to various online support materials, including:

• The unique ExP & Me e-portal, which amongst other things allows “view again” of the classroom course that was actually attended.

• ExPand, our online learning tool and questions and answers database

Everybody in the World has free access to CIMA’s own database of past exam questions, answers, syllabus, study guide and examiner’s commentaries on past sittings. This can be

ExPress Notes CIMA P3 Performance Strategy

Page | 4 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

an invaluable resource. You can find links to the most useful pages of the CIMA database that are relevant to your study on ExPand at www.theexpgroup.com.

How to get the most from these ExPress notes

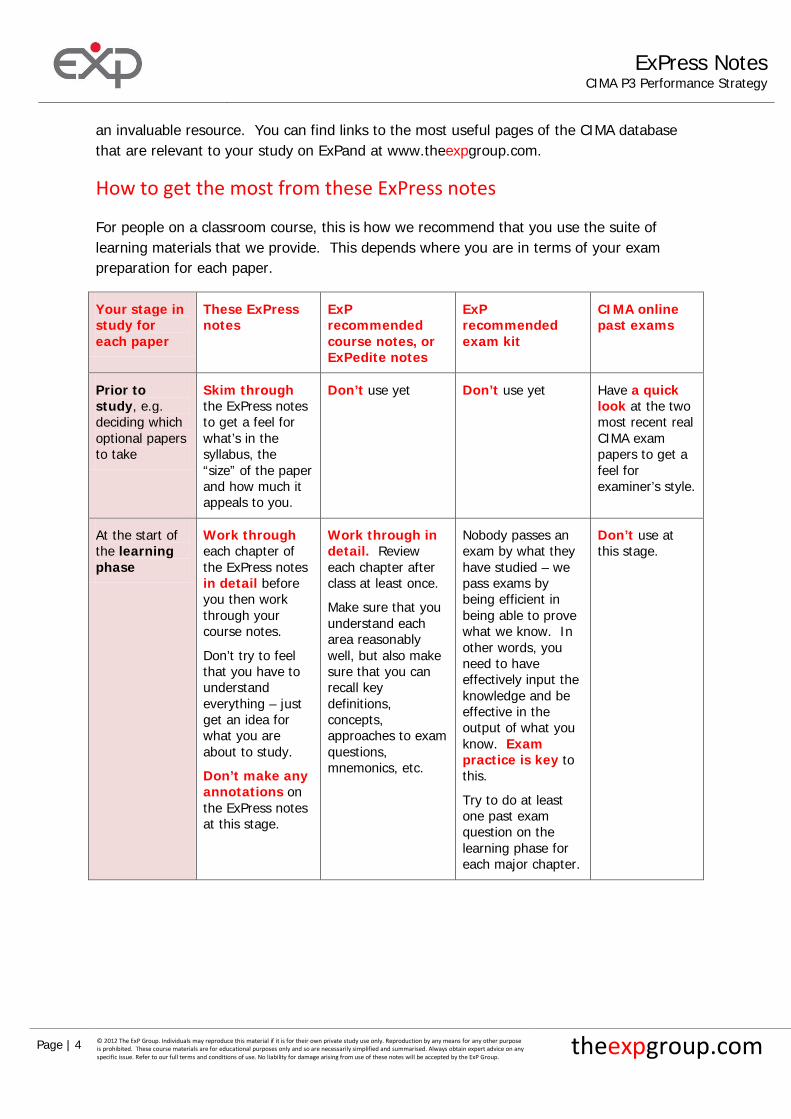

For people on a classroom course, this is how we recommend that you use the suite of learning materials that we provide. This depends where you are in terms of your exam preparation for each paper.

Your stage in study for each paper

These ExPress notes

ExP recommended course notes, or ExPedite notes

ExP recommended exam kit

CIMA online past exams

Prior to study, e.g. deciding which optional papers to take

Skim through the ExPress notes to get a feel for what’s in the syllabus, the “size” of the paper and how much it appeals to you.

Don’t use yet Don’t use yet Have a quick look at the two most recent real CIMA exam papers to get a feel for examiner’s style.

At the start of the learning phase

Work through each chapter of the ExPress notes in detail before you then work through your course notes.

Don’t try to feel that you have to understand everything – just get an idea for what you are about to study.

Don’t make any annotations on the ExPress notes at this stage.

Work through in detail. Review each chapter after class at least once.

Make sure that you understand each area reasonably well, but also make sure that you can recall key definitions, concepts, approaches to exam questions, mnemonics, etc.

Nobody passes an exam by what they have studied – we pass exams by being efficient in being able to prove what we know. In other words, you need to have effectively input the knowledge and be effective in the output of what you know. Exam practice is key to this.

Try to do at least one past exam question on the learning phase for each major chapter.

Don’t use at this stage.

ExPress Notes CIMA P3 Performance Strategy

Page | 5 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

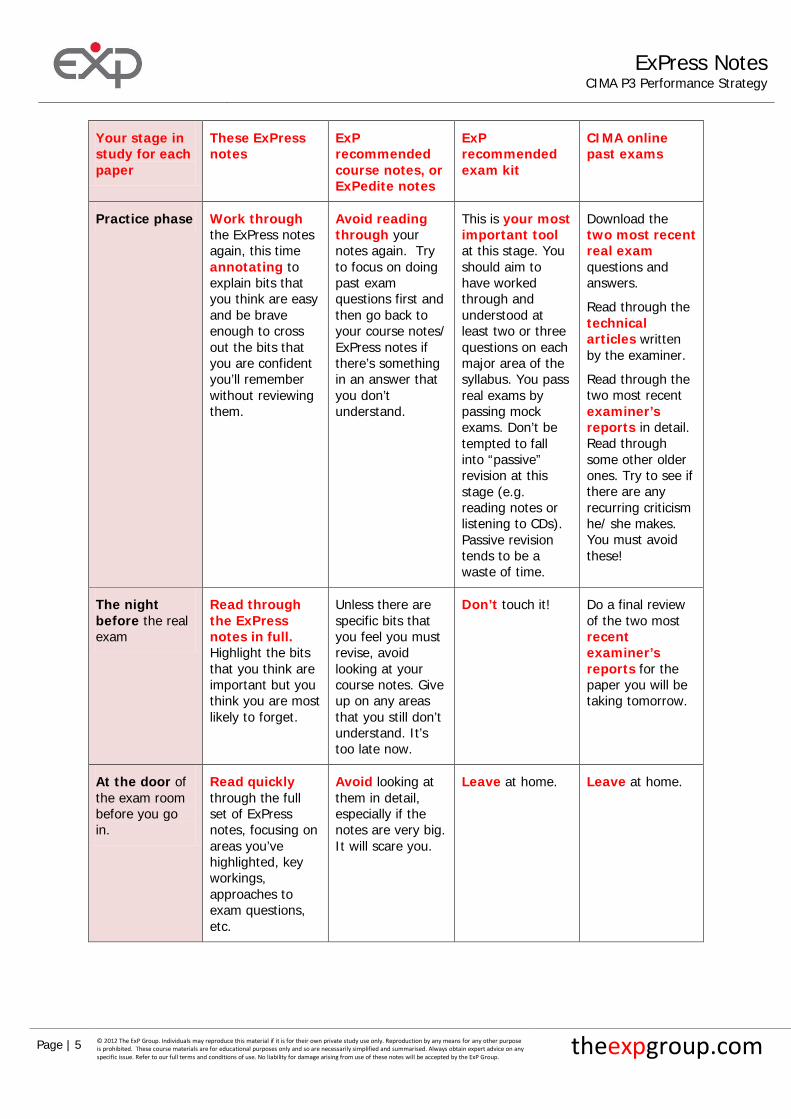

Your stage in study for each paper

These ExPress notes

ExP recommended course notes, or ExPedite notes

ExP recommended exam kit

CIMA online past exams

Practice phase Work through the ExPress notes again, this time annotating to explain bits that you think are easy and be brave enough to cross out the bits that you are confident you’ll remember without reviewing them.

Avoid reading through your notes again. Try to focus on doing past exam questions first and then go back to your course notes/ ExPress notes if there’s something in an answer that you don’t understand.

This is your most important tool at this stage. You should aim to have worked through and understood at least two or three questions on each major area of the syllabus. You pass real exams by passing mock exams. Don’t be tempted to fall into “passive” revision at this stage (e.g. reading notes or listening to CDs). Passive revision tends to be a waste of time.

Download the two most recent real exam questions and answers.

Read through the technical articles written by the examiner.

Read through the two most recent examiner’s reports in detail. Read through some other older ones. Try to see if there are any recurring criticism he/ she makes. You must avoid these!

The night before the real exam

Read through the ExPress notes in full. Highlight the bits that you think are important but you think you are most likely to forget.

Unless there are specific bits that you feel you must revise, avoid looking at your course notes. Give up on any areas that you still don’t understand. It’s too late now.

Don’t touch it! Do a final review of the two most recent examiner’s reports for the paper you will be taking tomorrow.

At the door of the exam room before you go in.

Read quickly through the full set of ExPress notes, focusing on areas you’ve highlighted, key workings, approaches to exam questions, etc.

Avoid looking at them in detail, especially if the notes are very big. It will scare you.

Leave at home. Leave at home.

ExPress Notes CIMA P3 Performance Strategy

Page | 6 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

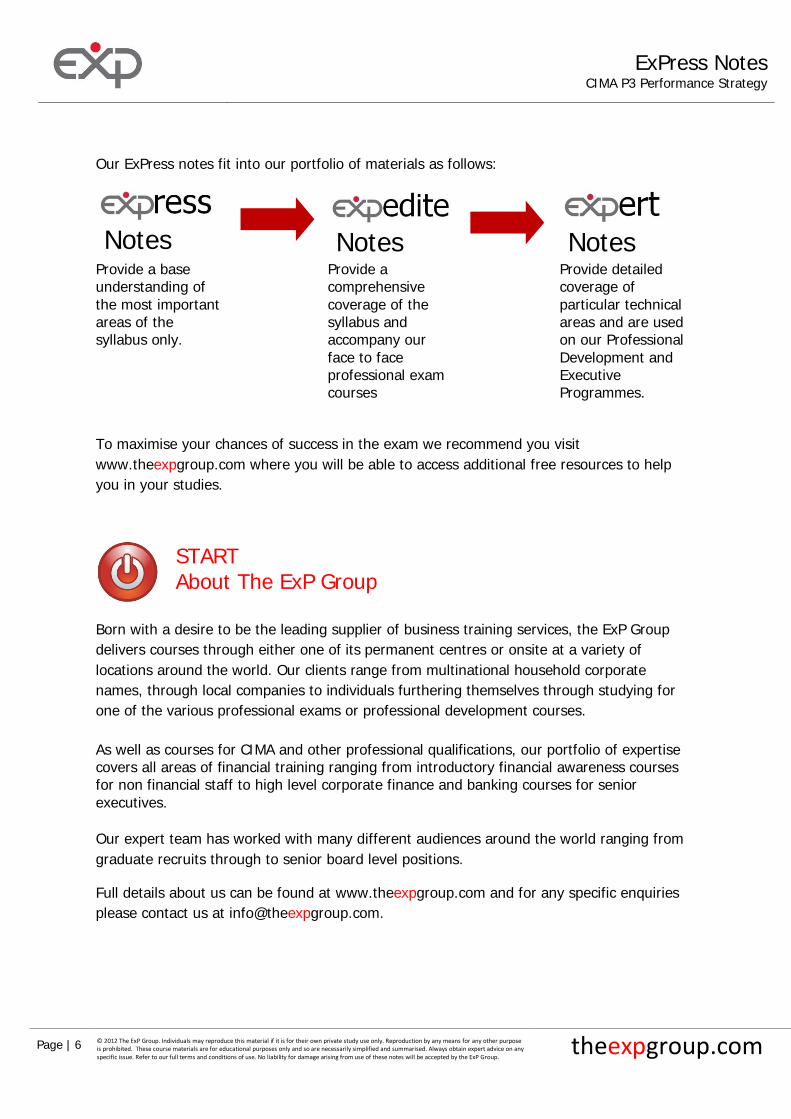

Our ExPress notes fit into our portfolio of materials as follows:

Notes

Notes

Notes

Provide a base understanding of the most important areas of the syllabus only.

Provide a comprehensive coverage of the syllabus and accompany our face to face professional exam courses

Provide detailed coverage of particular technical areas and are used on our Professional Development and Executive Programmes.

To maximise your chances of success in the exam we recommend you visit www.theexpgroup.com where you will be able to access additional free resources to help you in your studies.

START About The ExP Group

Born with a desire to be the leading supplier of business training services, the ExP Group delivers courses through either one of its permanent centres or onsite at a variety of locations around the world. Our clients range from multinational household corporate names, through local companies to individuals furthering themselves through studying for one of the various professional exams or professional development courses.

As well as courses for CIMA and other professional qualifications, our portfolio of expertise covers all areas of financial training ranging from introductory financial awareness courses for non financial staff to high level corporate finance and banking courses for senior executives.

Our expert team has worked with many different audiences around the world ranging from graduate recruits through to senior board level positions.

Full details about us can be found at www.theexpgroup.com and for any specific enquiries please contact us at [email protected].

ExPress Notes CIMA P3 Performance Strategy

Page | 7 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

Chapter 1

Management Control Systems

START The Big Picture

This chapter addresses the evaluation of management control systems in the context of organizational objectives and structures.

KEY KNOWLEDGE The Purpose of Management Control Systems

Management control systems consist of formalized information-based procedures and techniques employed by managers in order to direct the activities of an organization toward pre-defined objectives. All management control systems address the following basic issues within an organization:

ExPress Notes CIMA P3 Performance Strategy

Page | 8 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

• Measuring activities – both financial and non-financial – based on relevant data provided by an effective management accounting system;

• Informing and supporting decisions relating to resource allocation; • Providing communication to and motivating staff

The overall goal is to ensure that all efforts within the organization – both individual and collective – are defined and coordinated so that the objectives of the organization are fulfilled.

KEY KNOWLEDGE Achieving control within organizations

An organization can influence desired behavior on the part of its staff through a number of instruments, including:

• Employment contracts; • Internal policies and procedures; • Discipline and incentive schemes; • Performance appraisals/feedback; • Reporting lines that are consistent with responsibilities and organizational objectives

KEY KNOWLEDGE Design of Management Control Systems

There are two schools of thought which address the design of management control systems: Contingency school: There is no single, universally-valid management control system; instead, the appropriate design depends on a number of factors relating to:

• Organizational objectives; • Environment in which the organization operates; • The organization’s (internal) structure

This school is associated with the work done by David Otley.

ExPress Notes CIMA P3 Performance Strategy

Page | 9 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

Institutional school: Reporting systems develop in response to norms that are internal to the organization and/or influenced by other organizations in the same industry (associated with di Maggio and Powell) Business structure and management accounting/control Management accounting/control systems must be appropriate to the structure of the businesses they serve. The way in which a business is organized – e.g. a functional, divisional or network form – has implications for the way in which performance is managed and measured. Modern approaches to business structure are “integrative” in nature, as they explicitly take into account the linkages between people, operations, strategy and technology.

KEY KNOWLEDGE Achieving goal congruence within organizations

Management control systems should be consistent with encouraging managers to aim for common goals, which (a) should be consistent with organization’s objectives and (b) should be specific, objective and verifiable. Goal congruence can be facilitated by organization based on responsibility centres, which:

• Assign responsibility (obligation to perform) for activities to be performed within the responsibility centre;

• Delegate authority to direct and exact performance of assigned activities; • Establish duty to report performance and accountability for failure to meet obligation; • Evaluate performance (with consequent feed-back ensuring controllability of the

responsibility system)

ExPress Notes CIMA P3 Performance Strategy

Page | 10 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

This applies to all types of organizations, whether centralized or decentralized, an irrespective of levels within the organization:

• Cost centres: Responsible for current expenses only; • Revenue centres: Responsible for revenues, but not current expenses other than

marketing expenses; • Profit centres: Responsible for revenues and current expenses • Investment centres: Responsible for revenues, current expenses and capital

expenditure

KEY KNOWLEDGE Cost of Quality

There are four elements to learn:

• Internal Failure Costs: Defects discovered before delivery (to the customer);

• External Failure Costs: Defects which reach the customer;

• Prevention Costs: Design, training and other efforts made to prevent defects from occurring n the first place;

• Appraisal Costs: Verification and control efforts to ensure that quality is achieved in products and services

ExPress Notes CIMA P3 Performance Strategy

Page | 11 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

Chapter 2

Risk and Internal Control

START The Big Picture

This chapter addresses the variety of risks facing an organization and the risk management strategy and internal controls that exist in response to those risks. It is useful to start with CIMA’s definition of Risk Management: “the process of understanding and managing the risks that the organization is inevitably subject to in attempting to achieve its corporate objectives”. (CIMA Official Terminology)

KEY KNOWLEDGE Types of Risks

Risk management at the enterprise level addresses all risks affecting a company. These can be classified as follows (diagram on next page):

ExPress Notes CIMA P3 Performance Strategy

Page | 12 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

Enterprise Risk

Operational risk Financial risk

Process risk Credit risk

People risk Market (price) risk

Systems risk Gearing risk

Event risk

Business risk

Operational (or Operating) Risk One may view this category as including all risks that can arise in the course of operating a business, though by definition they are clearly distinguished from financial risks. It will be seen that the list of risks presented below can be expanded and sub-divided according to a particular company’s specific circumstances. Process Risk This relates to the processes within a business and evaluates them from the standpoint of pure risks, as well as (a) economy, (b) efficiency and (c) effectiveness. People Risk All risks connected to human resources, including quality and sufficiency of staff, and issues of recruitment, training, compensation, honesty and morale. There is an important link to corporate culture and explicit and implicit attitudes displayed by management; i.e. how they cultivate risk awareness, or encourage profits with(out) regard to the methods employed in achieving them. Systems Risk Information systems and communications in the broadest sense of the term, including IT hard/software, capacity, reliability (back-up) and policies relating to accuracy, access (passwords) and data integrity.

ExPress Notes CIMA P3 Performance Strategy

Page | 13 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

Event/Hazard Risk Risk of losses resulting from single events that may have a high or low impact. Natural disasters and human actions, whether intentional (terrorism) or not (accidents), fall within this category. Some companies may include fraud in this category though fraud and malfeasance are also clearly the result of the actions of people (see “people risk”). Business Risk This is a broad category with indistinct boundaries, but it generally covers risks to a company’s ability to generate returns from its ordinary operations, including its strategy, business model, competitive position, political/legal environment (including regulatory/ compliance/ intellectual property), products, marketing, clients and reputation. Process, people and systems risks can be seen as being mainly internal in nature; the other risks are generally seen as being external.

KEY KNOWLEDGE International operations

The challenge presented by international operations can be analyzed using the above categories; such operations add complexity to a company’s operations since they confront it with differing:

• Cultural norms

• Political stability

• Efficiency and honesty of the judicial system

• Regulatory enforcement Just to name a few!

ExPress Notes CIMA P3 Performance Strategy

Page | 14 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

KEY KNOWLEDGE Key risk concepts

There are several key concepts relating to risk: Probability: measures the likelihood that a certain event will occur; Severity (or impact): quantifies the loss which results if the undesired outcome occurs; Exposure: Is the degree to which one is confronted by the particular type of risk The above factors can be combined into a quantification of the risk of loss by multiplying the financial consequences if the undesired event occurs by the probability factor: Risk = Probability x Severity x Exposure Note: This can be condensed to Risk = Probability x Financial consequences This is essentially the application of the expected value technique to risk.

Volatility: refers to the variability or the spread of all likely outcomes of an uncertain factor to which a business is exposed. Statistically, volatility is measured by standard deviation.

KEY KNOWLEDGE Risk Mapping

Seve

rity

Hig

h

Detect/Monitor

Prevent (at source)

Low

Low control

Monitor

Low High

Likelihood

ExPress Notes CIMA P3 Performance Strategy

Page | 15 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

KEY KNOWLEDGE Risk Response Strategy

It is management’s responsibility to adopt a “risk response strategy”, which results from the specific identification and assessment of each type of risk facing the organization. The responses can come under one of the four following (generic) headings:

(1) Avoid: Discontinuing (or not starting) an activity that causes unacceptable risks;

(2) Reduce (or prevent): Taking (internal) action to reduce the risk;

(3) Insure (transfer or share): Transferring the risk to a 3rd

party (such as an insurer) or sharing the risk with a partner;

(4) Accept (or retain): the risk is considered small and it is not worth the effort to protect against it.

Refer back to the risk map: One could chart the above risk responses as a progression from upper right (High Severity/High Likelihood = Avoidance) to the lower left (Low Severity/Low Likelihood = Acceptance).

KEY KNOWLEDGE Risk & Corporate Objectives

Achieving a clear and explicit articulation of corporate objectives, and the connection to risk appetite/acceptance, is the duty of senior management. This perspective begins at the most senior corporate strategy and policy-making level, where strategic objectives are established. This is a “top-down” process. Following from the establishment of corporate objectives, a company’s business strategy can be seen, among other purposes, as reconciling corporate objectives with the level of risk accepted in pursuing strategic and financial goals.

ExPress Notes CIMA P3 Performance Strategy

Page | 16 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

These elements are tied together by the culture of the organization (incl. attitudes to risk) and its management control and other systems.

Objectives (strategy)

Risks Returns(Rewards)

KEY KNOWLEDGE Risk Management Processes

There exist a number of risk management models. Since they have similar objectives, they will resemble each other in their process steps. From a generic point of view, these embrace:

• Risk identification and awareness

At the policy level, this involves the need to define explicitly the organisation’s risk appetite (the types and levels of risks it is willing to tolerate). There is also a need to agree common definitions of risks. One can refer to this a “common language” of risk or “risk glossary. There is an effort to “inventory” risks; this means categorizing risks, including an understanding of their causes and degree of impact.

• Risk management and assessment

This is concerned with methods and techniques used to evaluate risks, including methodologies to prioritize risks (risk-ranking) and to quantify them.

Culture & Systems

ExPress Notes CIMA P3 Performance Strategy

Page | 17 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

• Risk response and control Risk response means effective action-taking to ensure that the identified risks are addressed in conformity with policy. This requires an assignment of responsibilities to individuals -- who does what.

• Risk monitoring and reporting A system of monitoring the ERM process, including periodic evaluations as to whether the system is accomplishing its purpose, is indispensable. The costs of maintaining the system must be outweighed by the benefits.

Management is accountable to shareholders, and other stakeholders, by a system of periodic reporting.

KEY KNOWLEDGE CIMA Risk Management Cycle

The student is advised to refer also to CIMA’s Risk Management Cycle (contained in CIMA publication Fraud Risk Management: A Guide to Good Practice): www.cimaglobal.com The student might also refer to COSO (Committee of Sponsoring Organisations of the Treadway Commission) which addresses Enterprise Risk Management (ERM) through its eight Components and four Objectives categories. The Components are:

• Internal environment

• Objective setting

• Event identification

• Risk assessment

• Risk response

• Control activities

ExPress Notes CIMA P3 Performance Strategy

Page | 18 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

• Information and communication

• Monitoring

The Objectives address:

• Strategy

• Operations

• Financial Reporting

• Compliance

KEY KNOWLEDGE ERM Implementation

Defining Enterprise Risk Management (ERM) in conceptual terms is merely the first step. Moving from theory to practical implementation begins with:

1. The Board of Directors’ explicit responsibility for risk management oversight

This may be accompanied by the establishment of a Risk Committee at the board level, or including the responsibility within the scope of the Audit Committee;

2. Creation of a risk management team under the leadership of a senior-level executive (Chief Risk Officer, CRO, or VP – Risk) with a reporting line into the Board

The real test of the effectiveness of a risk management process is measured by the degree to which:

3. The methods and norms of ERM are successfully disseminated throughout the organization. Effective implementation requires important commitments at all levels of the organization, manifested by:

• Clear written policies and procedures;

• Staff training;

ExPress Notes CIMA P3 Performance Strategy

Page | 19 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

• Disciplinary steps for violations;

• Constant management reinforcement (both in word and deed)

KEY KNOWLEDGE Internal Control

The IIA (Institute of Internal Auditors) have provided the following useful definition:

“An internal control is any action taken by management to enhance the likelihood that established objectives and goals will be achieved. Management plans, organises and directs the performance of sufficient actions to provide reasonable assurance that objectives and goals will be achieved. Thus, control is the result of proper planning, organising and directing by management.”

The internal control function should be regarded as a process designed to provide reasonable (not absolute) assurance that the company is in a position to achieve its objectives; it should be integral to a company’s operations, not an external imposition. Responsibilities include:

• Safeguarding of corporate assets; • Checking the accuracy and reliability of corporate accounting data; • Promoting operational efficiency; • Ensuring adherence to accounting and financial control policies

KEY KNOWLEDGE COSO – Internal Controls

A widely-used framework of internal control in the USA is the COSO Internal Control – Integrated Framework, which consists of five components:

• Control Environment – setting the “tone at the top”;

• Risk Assessment - identification risks (to the achievement of objectives);

• Information and Communication – internal data flow (timely, relevant, etc.);

• Control Activities - the policies and procedures;

• Monitoring – verification processes to assess the quality/effectiveness of internal

controls

ExPress Notes CIMA P3 Performance Strategy

Page | 20 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

•

KEY KNOWLEDGE Types of Controls

• Corporate controls = general policy statements, established core culture and overall

monitoring procedures, corporate governance • Management controls = planning and performance monitoring • Business process controls = authorisation limits and reconciliation • Transaction controls include = accuracy and completeness checks

You may use the mnemonic SOAPSPAM to generate ideas for types of control: • Segregation of duties • Organisational controls (eg set authority limits) • Authorisation • Physical • Supervision • Personnel, eg background checks • Arithmetical and reconciliations • Management – the tone from the top, including existence of an internal audit

department.

KEY KNOWLEDGE Features of a good system

Essential features of any good system of internal control

As a useful aide memoire when asked to evaluate a described system of internal control within a question scenario, you could make use of the mnemonic PCRAM.

Plan of organisation

Custody procedures

Recording procedures

Authorisation procedures

Management supervision

ExPress Notes CIMA P3 Performance Strategy

Page | 21 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

KEY KNOWLEDGE The Turnbull Report

The UK Turnbull report gives us a useful summary of the main purposes of an internal control system, by stating that internal control consists of “the policies, processes, tasks, behaviour and other aspects of a company that taken together:

• Facilitate its effective and efficient operation by enabling it to respond to significant business, operational, financial, compliance and other risks to achieving the company’s objectives. This includes safeguarding the assets from inappropriate use or from loss and fraud and ensuring that liabilities are identified and managed.

• Help to ensure the quality of internal and external reporting.

• Help ensure compliance with applicable laws and regulation, and also with internal policies with respect to conduct of business.”

The Turnbull committee recognised that while a sound internal control system cannot eliminate poor judgment in decision-making, it may minimize that risk to a significant degree. Further, the committee stated: “Reviewing the effectiveness of internal controls is an essential part of the board's responsibilities…”; at the same time, “Management is accountable to the board for monitoring the system of internal control and for providing assurance to the board that it has done so.” The board is responsible for the disclosures on internal control in the company's annual report and accounts.

KEY KNOWLEDGE Corporate Governance

There is an close connection between corporate governance and risk management: in order to fulfill its corporate governance role faithfully, the directors of the company have to ensure that there is in place at the company a robust system of internal controls and risk management systems. There are several models of corporate governance:

ExPress Notes CIMA P3 Performance Strategy

Page | 22 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

• Shareholder-based models: typical of the US and the UK; and • Stakeholder-based: common on the Continent (Europe) and Japan

KEY KNOWLEDGE Sarbanes Oxley (US)

In the US, Sarbanes-Oxley is Federal legislation dating from 2002 that prescribes corporate governance principles for publicly-quoted US corporations. It seeks to safeguard the economic interests of the shareholders, by promoting an active market where corporate control can change hands in an effort to promote the most efficient allocation of economic resources.

KEY KNOWLEDGE Combined Code (UK)

In the UK, this is a set of principles of good corporate governance which sets forth a code of best practice aimed at companies listed on the London Stock Exchange. It is overseen by a body called the Financial Reporting Council. The Combined Code on Corporate Governance is the result of the collective efforts of numerous commissions formed in the UK to study and make recommendations on the subject (e.g. Cadbury, Greenbury and Hampel) and incorporates conclusions from the following committees:

• Turnbull: Guidance on internal control (as described earlier); • Smith: Guidance on audit committees; • Higgs: Suggestions for good practice

Some key features of the Combined Code include: Comply or explain: Deviations from the Code may be justified “in particular circumstances”; Board Composition: At least half the Board (excluding the chairman) should be independent non-executive directors; Separation of Chairman and CEO roles: These should not be exercised by the same individual;

ExPress Notes CIMA P3 Performance Strategy

Page | 23 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

Non-Executive Directors’ duties: Include “scrutinise the performance of management” and satisfy themselves that financial controls and systems of risk management are “robust and defensible”; Executive remuneration: No director should be involved in deciding his or her own remuneration; Audit Committee: At least three members, all be independent non-executive directors; Audit Committee role: Oversee the effectiveness of internal controls and to liaise with the internal and external auditors.

KEY KNOWLEDGE Internal Audit

The role of the internal audit is to make sure that the company’s internal controls are appropriate and working properly. Internal auditors are employees and report to management. However, they can also have a reporting line to the Audit committee of the board, so that their professional independence is not compromised.

KEY KNOWLEDGE CIMA Ethical Guidelines

The student is expected to be fully familiar with CIMA Ethical Guidelines which can be accessed via: www.cimaglobal.com

ExPress Notes CIMA P3 Performance Strategy

Page | 24 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

Chapter 3

Review and Audit of Control Systems

KEY TERMINOLOGY Internal Auditing

The IIA defines internal auditing as follows:

“Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organisation’s operations.

It helps an organisation accomplish its objectives by bringing a systematic disciplined approach to evaluate and improve the effectiveness of risk management, control and governance processes.”

ExPress Notes CIMA P3 Performance Strategy

Page | 25 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

KEY KNOWLEDGE Internal vs. External Auditing

FUNDAMENTAL DIFFERENCES BETWEEN INTERNAL AND EXTERNAL AUDITORS

Both internal auditors and external auditors will have a major interest in the effectiveness of a company’s internal control systems. Both are assurance providers and as such will make use of similar techniques and procedures.

The external auditor should approach internal audit as any other aspect of internal control before placing any reliance upon the work of internal audit to perhaps reduce the level of some of their own testing. Key factors to consider in assessing the potential reliability of the work of internal audit will include such matters as:

• Qualifications • Experience • Quality of audit documentation • Independence • Management response to internal auditor recommendations

Effective co-operation between the two sets of auditors can help to avoid unnecessary duplication of effort, with a consequent benefit of time and cost savings. However, it is important for the external auditor to always be aware of certain fundamental differences as indicated below:

INTERNAL AUDITOR EXTERNAL AUDITOR SCOPE MANAGEMENT ISAs + REGULATIONS APPROACH MANAGEMENT ISAs + REGULATIONS RESPONSIBILITY MANAGEMENT SHAREHOLDERS

NB under Corporate Governance provisions, the head of internal audit should be appointed by and report to the Audit Committee. The Audit Committee should also be responsible for determining the nature and scope of the work of internal audit.

KEY KNOWLEDGE Areas of Focus

ExPress Notes CIMA P3 Performance Strategy

Page | 26 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

TYPICAL AREAS OF INTERNAL AUDIT INVOLVEMENT

These would include, but not be restricted to the following (any of which you need to be prepared to write briefly about):

• VFM audits (the 3 Es) • IT audit • Financial audit • Operational audit

KEY KNOWLEDGE Audit Steps

Steps in auditor’s consideration and approach to internal control systems

1. Ascertain details of systems (interview, ICQs, etc). 2. Record details of systems (narrative notes, flowcharts, etc). 3. Confirm details of systems (walk through test). 4. Evaluate the client systems. If system is assessed as being sound then proceed to

step 5. If system is assessed as being inherently weak, then there is no purpose to carrying out tests of control in that area. Such weaknesses should be discussed with management and documented in an internal report. In this area of the activity it will then be necessary to design and carry out an extended programme of substantive testing.

5. Test the systems (tests of control). 6. Assess the results of tests of control. If tests of control confirm that the system is

working satisfactorily then proceed to step 6. If tests of control reveal that a system evaluated as being sound in theory is not working satisfactorily in practice then proceed as in step 4 where system was evaluated as being inherently weak.

7. Design and carry out limited programme of substantive testing.

ExPress Notes CIMA P3 Performance Strategy

Page | 27 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

Chapter 4

Management of Financial Risk

START The Big Picture

This section is a summary of sources and mitigation of financial risk associated with international operations and also trading of financial instruments.

KEY KNOWLEDGE Political Risk

Political risk factors can be identified as part of an overall PESTEL analysis:

ExPress Notes CIMA P3 Performance Strategy

Page | 28 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

PESTEL Analysis

An analysis of the external macro environment. The organisation is unlikely to be able to influence these factors but it should have an awareness of the issues.

Political - global, national and local changes and trends. Taxation policies. Relationships between certain countries.

Economic - global, regional and local issues. Exchange rates. Link to topical issues such as global recession, current interest rates for funding.

Social - changes in behavior and expectations in society. Demographics, lifestyle.

Technological - changes including hardware, software, e-issues, materials and services. Global communications.

Legal - changes and predicted changes to regional (e.g. EU) and national legislation. Regulatory bodies. Changes to employment law.

Environmental – what are the environmental considerations such as recycling, pollution, attitude of the media, customers, etc.

KEY KNOWLEDGE Interest Rate Risk

Interest rate risk This refers to the risk of loss (or profit) from a change in interest rates on interest rate-bearing assets and liabilities. Interest rate gap exposure The risk of interest-bearing assets and liabilities having different periods and re-set dates, so that a rise or fall in interest rates causes their values to change to differing degrees; the result is a gain or loss on the net position. Basis risk The risk of the prices of interest-bearing assets and liabilities not moving in line with each other over time; this can occur when imperfect hedges are employed.

ExPress Notes CIMA P3 Performance Strategy

Page | 29 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

KEY KNOWLEDGE Managing Interest Rate Risk

There are various methods used to manage interest rate risk:

(a) Matching and smoothing: This is the process of matching assets and liabilities with similar interest rate conditions (fixed/floating) so as to “smooth”, or minimize, the impact of rate fluctuation;

(b) Asset and liability management (ALM): This is the active management of interest rate risk by actively adjusting the combination of the fixed/floating interest rate profile of a firm, using also external hedging instruments to this end;

(c) Forward rate agreements (FRA): A contract which allows buyers and sellers to fix an interest rate in advance for a specified currency, amount and settlement date.

KEY KNOWLEDGE Forward Rate Agreements

(months)

Period of uncertainty <<<<<<<<<<< Loan period >>>>>>>>>> (2 months) (3 months) 3% 5% A borrower planning to take a loan in 2 months (see diagram) can buy an FRA today (t=0) to protect against a rise in rates. The FRA contract rate is agreed at e.g. 3% (t=0). This becomes an 2x5 FRA at a price of 3% (2x5 means 2-by-5 and refers to the 2 and 3 month periods shown in the diagram above)

• If rates rise to e.g. 5% when the loan is taken (t=2), then the borrower gets 2% (5-3);

5 4 3 2 1 0

ExPress Notes CIMA P3 Performance Strategy

Page | 30 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

• If rates had dropped below 3% at t=2, then the borrower would have paid the difference

Other derivatives exist to hedge interest rate risk:

KEY KNOWLEDGE Interest Rate Futures

An interest rate future is a contract based on an underlying interest rate instrument which permits interest rates to be fixed in advance of the day on which they would take effect.

Interest rate futures can be bought and sold on organised exchanges and can be classified according to the term of the underlying asset, i.e. short-term interest rate futures and long-term interest rate futures (or bond futures). Short-term interest rate futures are based on underlying assets taking the form of “notional” money market deposits or instruments such as US Treasury bills of standard amount and specified term.

Examples of 3-month instruments include:

Instrument Standard (notional) deposit amount • 3-month Eurodollar USD 1 million • 3-month Sterling GBP 500,000 • 3-month Euro EUR 1 million • 3-month Euroswiss CHF 1 million • 90-day US Treasury bill USD 1 million

Price quotation of Interest Rate Futures The price of an interest rate futures contract reflects the value of the underlying instrument traded in advance, i.e. before the underlying instrument takes effect (or when interest starts accruing). The prices are quoted as a discount from a par value of 100.

ExPress Notes CIMA P3 Performance Strategy

Page | 31 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

A price of 92.00, for example, reflects an interest rate for an underlying deposit of 8% per annum (100 - 92.00 = 8.00). The higher the interest rate is, the larger the discount from the par value of 100, and therefore the lower the price of the future will be. (This is similar to how bond prices move, i.e. inversely to movements in interest rates.) Prices are quoted to one hundredth of 1%, or 0.01%; a price of 93.70, for example, reflects an interest rate of 6.30% (100 - 93.70). The price of a future can move up or down by increments of at least 0.01 (0.01%, which is the equivalent of one basis point, also called a “tick”).

Purchase of an interest rate future

Technically, the buyer of an interest rate future is buying a future money market deposit or placement (the underlying instrument) and is fixing in advance the interest rate (and, in effect, the stream of interest income) to be received.

Settlement Date

The settlement date of the future corresponds to the day on which the underlying instrument would begin, i.e. the deposit or placement takes effect.

Market Price Dynamics

As mentioned above, the value of a futures contract behaves similarly to a bond: if interest rates go up, then the value of the futures contract will decline, since the future (fixed) stream of interest income will have a lower value. The buyer of such a futures contract will incur a loss on the contract.

EXAMPLE

At the end of August, a dealer buys one 3-month Eurodollar interest rate futures contract which settles at the end of September. The market price of the contract is 93.50 (reflecting an interest rate of 6.50%). The futures contract has a daily quoted price, reflecting the

ExPress Notes CIMA P3 Performance Strategy

Page | 32 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

market rate, and must be settled any time until the end of September, at which time the future expires (and the notional placement would commence).

If interest rates fall to 5.00% in the middle of September, the future’s price would rise to 95.00. The dealer could sell the future at this price. Alternatively, he could continue holding the future until the settlement date, at which point he would have to sell the future at the governing market price. If by settlement, interest rates had risen to 5.50%, then the dealer would obtain a price of 94.50. At the prices mentioned (above) the dealer’s net gain/loss would be:

• Sale at 95.00: 150 tick gain • Sale at 94.50: 100 tick gain

The value of a tick for a 3-month Eurodollar contract is USD 25 (.01% x 1m x 3/12) The value of a tick for a 3-month Sterling contract is GBP 12.50 (.01% x 0.5m x 3/12) Use of Interest rate futures

Interest rate futures allow buyers and sellers to:

• Hedge a position, i.e. protect themselves against a change in interest rates by fixing rates in advance of an intended transaction (depositors or borrowers);

• Take a position, i.e. to benefit from a change in interest rates, provided rates move in a favourable direction.

Hedging -- The Borrower’s perspective

The borrower’s underlying position is cash “short”; if the price of cash (the interest rate) rises, then the borrower loses. The appropriate hedge transaction is one in which a rise in interest rates will result in a profit. Appropriate hedging strategy for a borrower: Sell futures.

Hedging -- The Depositor’s perspective The appropriate hedging strategy for a depositor: Buy futures.

ExPress Notes CIMA P3 Performance Strategy

Page | 33 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

Other Features and Terminology

Settlement dates

All contracts have a defined starting date when trading can begin, and a last day when trading ceases (and open positions must be closed). These dates are defined in advance by the respective exchange (these are publicized on their websites).

Contracts carry the name of the month in which they settle. A June contract on the 3-month Euro, for example, can be bought and sold on a daily basis until two business days before the third Wednesday of the month on the London International Financial Futures Exchange (LIFFE).

Positions: Open/Closed/Squared

This follows the general definition: An open position exists if the buyer (or seller) is long (or short) a financial instrument (or instruments, on a net basis). A position is closed if the long or short position is eliminated by making an off-setting sale or purchase of instruments.

Settlement Terms

All short terms interest rate futures contracts are settled by cash, i.e. the difference between the originally agreed price and the price at the time of closing the contract.

Note: Long term (bond) futures are settled by physical delivery of the instrument, i.e. the seller delivers the bond to the buyer at the previously agreed price.

Initial, maintenance and variation margins

Before trading on an exchange, market participants are required to make a deposit (“initial” margin) to cover trading losses. On a daily basis, the potential gain or loss on the trading position is calculated and potential losses are counted against the margin. The amount of the margin may not fall below a minimum level (called the “maintenance” margin). Fluctuations in the level of required margin is referred to as “variation” margin.

ExPress Notes CIMA P3 Performance Strategy

Page | 34 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

KEY KNOWLEDGE Interest Rate Swaps

An interest rate swap is an agreement between two counterparties to exchange streams of interest payments with different bases (see next paragraph). The interest payments are based on an agreed amount of a notional principal and for a specified period of time. An interest rate swap allows a company to change a fixed rate into floating rate (and vice versa) on a loan without altering the loan contract itself. If a borrower has a floating (variable) rate debt and expects interest rates to rise, it can avoid this rise by swapping its floating rate commitment into fixed rate.

Interest Rate Bases

The interest payments on long-term borrowings and investments may be set on different bases, e.g. either at a fixed rate or at a variable (or floating) rate. In the case of floating rate loans, the interest rate is normally defined in the loan contract by specifying a pre-determined spread (reflecting the credit risk) over a benchmark interest rate, such as LIBOR.

Companies borrowing for medium and long terms (i.e. more than one year, but more typically in a 3 to 7 year period) need to determine the cheapest way to find the necessary funding. Interest rate swaps provide flexibility to companies seeking to secure the best deal terms by entering into an exchange of one set of interest payments for another.

EXAMPLE

Two companies X and Y require financing in the same currency and for identical maturities. Their borrowing terms for fixed and floating rates are shown below:

Company Fixed rate Floating rate

X 5.7 3 month Libor + 10

Y 6.0 3 month Libor + 20

ExPress Notes CIMA P3 Performance Strategy

Page | 35 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

If X is looking for floating rate finance and Y fixed rate, then each could achieve the following borrowing terms via a swap:

X: LIBOR p.a.; and

Y: 5.90 % p.a.

The above terms share benefits equally between the two companies (10 b.p. each) and no bank fees are assumed.

KEY KNOWLEDGE Interest Rate Options

Interest Rate Guarantees

Interest rate guarantees form another category of derivatives which allow market participants to profit (or lose!), or alternatively, to hedge against, movements in interest rates. They operate on the basis of the classic options mechanism.

These are bilateral (OTC) contracts giving the buyer the right to buy or to sell specifically-defined Forward Rate Agreements (FRA) by an expiry date corresponding to the FRA settlement date. The borrower using an option to hedge avoids higher interest rates, but benefits from lower rates. An option allows you to “having your cake and eat it”.

• A borrower’s option is a “call” option hedging against rising interest rates;

• A lender will buy a “put” option;

• Position takers, as opposed to hedgers, can act on their respective views on the market: those believing that rates will go up will buy a Call while those acting on the belief in a decline will buy a Put.

The above options are essentially short-term instruments. Interest rate guarantees can also be arranged for longer terms, for example to hedge medium-term borrowings and deposits (referred to as “caps” and “floors”).

ExPress Notes CIMA P3 Performance Strategy

Page | 36 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

Exchange-traded interest rate options These contracts are structured as options to buy or sell interest rate futures contracts as the underlying asset. The value of the option is therefore based on the futures price, which in turn is based on the movement in interest rates (e.g. LIBOR).

A company planning to borrow GBP can protect themselves against a rise in interest rates by buying put options (which gives the right to sell GBP interest rate futures) at a strike price reflecting the maximum rate to be paid (excluding the loan margin).

KEY KNOWLEDGE Foreign Exchange Risk

Foreign exchange risk occurs when a company is potentially affected by changes in foreign exchange rates. Companies with assets, liabilities, revenues or expenses denominated in currencies different fro its home currency is exposed to foreign exchange risk.

KEY KNOWLEDGE Types of foreign exchange risk

There are three categories of foreign exchange risk: (i) Transaction risk: This refers to the foreign exchange risks relating to the purchase or

sale of goods in foreign currencies, or the borrowing or investing of foreign currencies. Assuming that the risk has not been neutralized through “hedging” (to be discussed), then an actual risk of loss exists in cash terms to the company.

(ii) Economic risk: Economic risk refers to the long-term impact of foreign exchange rate

movements on the international competitiveness of a company. Economic exposure can be viewed as strategic in nature, while transaction exposure has a tactical character.

ExPress Notes CIMA P3 Performance Strategy

Page | 37 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

(iii) Translation risk: This is the impact of changing exchange rates on the reporting of assets and liabilities within a group containing one or more foreign subsidiaries. Losses here are not necessarily realized in cash, but are reported as accounting losses due to exchange rate differences.

KEY KNOWLEDGE Foreign Exchange Risk - Illustration

Assume a company wins a law suit that will bring a guaranteed payment of GBP 1m in 6 months.

The company is now LONG GBP 1m. If the GBP depreciates, the company will suffer a foreign exchange loss.

To mitigate this risk, the company can sell GBP forward with maturity (value date) in 6 months.

Banks will provide forward quotations. The forward contract entered into with the bank is known as an Over-the-Counter (OTC) contract, which takes the form of a bilateral transaction between two counterparties.

KEY KNOWLEDGE Long and Short Positions

A long position is the equivalent of having an asset in a given currency. If the price of that currency goes down, then the holder of the currency makes a loss.

A short position is the equivalent of having a liability in a given currency. If the price of that currency goes down, then the holder of the short position makes a gain.

KEY KNOWLEDGE Forward (Swap) Points

Another way of quoting the forward (mentioned earlier) is by calculating the forward (or swap) points:

ExPress Notes CIMA P3 Performance Strategy

Page | 38 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

GBPUSD Spot 1.4800 – 1.4810 6-month Fwd points 217 -- 190

1.4583 – 1.4620

The forward (fwd) points (or pips) are the difference between the spot and forward prices and are expressed as an adjustment to the spot price:

GBPUSD Spot 1.4800 – 1.4810 6 mo Fwd points 217 -- 190

• The forward points are the points by which the spot has to be adjusted to derive the forward rate

• When the points decline, from left to right, then they are deducted from the spot rate

• When the points increase, from left to right, then they are added to the spot rate • The currency with the higher level of interest rates trades at a lower price (relative to

the other currency) in the forward market.

KEY KNOWLEDGE Managing Foreign Currency Risk

There are a number of methods by which a company can protect (hedge) itself against adverse movement in exchange rates.

(a) Currency of invoice: A firm can invoice in its home currency, thus avoiding forex risk

altogether;

(b) Netting and matching: A firm can systematically match and offset foreign currency payables and receivables when planning its forex purchase and sales; also identifying a liability (such as a cost) denominated in the same currency as an asset.

(c) Leading and lagging: Timing the receipts and payments of foreign currencies so as to collect depreciating currencies more quickly and to slow payments of such currencies;

ExPress Notes CIMA P3 Performance Strategy

Page | 39 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

(d) Forward exchange contracts: Buying and selling currencies on a forward basis with banks;

(e) Money market hedging: See example below;

(f) Asset and liability management: Firms can actively adjust their assets and liabilities according to the currencies in which they are denominated so as to limit forex risk.

KEY KNOWLEDGE Hedging

Hedging refers to the transaction by which a company or individual effectively mitigates (eliminates) their currency risk, i.e. eliminates a long or short position by neutralizing (squaring) that position.

In the cases described earlier, the company had the opportunity to hedge its foreign exchange risks by use of the money market and/or the forward market.

Money market hedge A firm will receive GBP 1m in 6 months. It fears a decline in the value of the GBP. Spot rate: GBPUSD 1.4800 – 10 GBP 6-month interest rates: 4 7/8 - 5 % p.a. USD 6-month rates: 2 - 2 ¼ % p.a.

1. Borrow GBP 975,610 for 6 months at 5%; 2. Sell GBP 975,610 and buy USD at 1.4800 (= USD 1,443,903); 3. Place USD 1,443,903 for 6 months at 2%; 4. At maturity, receive GBP 1m and repay the loan of GBP 1m (principal plus interest).

Net position in GBP: 0; 5. Receive USD maturing deposit (USD 1,458,342)

The net result is that GBP has been sold in advance for USD at GBPUSD 1.4583. Using the same market data as above, a money market hedge can be constructed for a company paying GBP 1m in 6 months:

1. Borrow USD 1,445,760 for 6 months at 2¼%; 2. Sell USD 1,445,760 and buy GBP 976,205 in the spot market; 3. Deposit GBP for 6 months at 4 7/8%;

ExPress Notes CIMA P3 Performance Strategy

Page | 40 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

4. At maturity, repay USD 1,462,025 and receive GBP 1,000,000

Conclusion: The (implied) GBPUSD 6-month forward is 1.4620

Other types of derivatives include:

KEY KNOWLEDGE Currency Futures

These are contracts, transacted over an exchange, representing a standard amount of currency which can be bought or sold with a specified future settlement (delivery) date, at a rate expressed in another currency. Settlement is guaranteed by the exchange, which acts as counterparty. Some exchanges are:

• Chicago Mercantile Exchange • Euronext – LIFFE • Tokyo Financial Exchange

Futures compared to Forwards

Buying, on 15 May, one contract of June EUR futures (against USD) at the market price of 1.4300

is the economic equivalent of

buying EUR 100,000 against USD at a forward rate of 1.4300 as quoted by a bank on 15 May (trade date) for value (settlement) date in June corresponding to the future contract settlement date above.

On the final day of trading a futures contract (2 working days before settlement date) the futures price will be the same as the corresponding spot rate.

Futures used for hedging purposes

Illustration

Take the company expecting to receive GBP 1m after 6 months.

The company now has a third possibility to hedge itself against a declining GBP: It can sell GBP futures.

To hedges its GBP 1m long position using futures, consideration must be given to:

ExPress Notes CIMA P3 Performance Strategy

Page | 41 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

Settlement date: The appropriate futures contract will not settle before the expected date of receipt of the currency inflow (GBP 1m); in other words, the future contract must cover the entire period of risk.

No. of contracts: This is determined by dividing the amount to be hedged (in the above example, GBP 1m) by the standard size of a GBP contract (GBP 62,500); therefore, in the above case, 16 contracts will be sold.

Closing out of the futures contract

When the expected receipt of GBP 1m takes place, then the futures contract will have served its purpose and the futures position must be closed, or “squared”.

EXAMPLE

Assume GBP 1m was expected in August and the company hedged this exposure by selling 16 contracts of the September GBPUSD futures at a rate of 1.4585.

Assume further that on the day (in August) that the GBP 1m is actually received:

GBPUSD spot rate: 1.4050

September GBP futures: 1.3980

Company’s position at settlement date

The GBP has depreciated against the USD.

When received, the GBP 1m is sold at spot 1.4050 (proceeds are USD 1,405,000);

The futures position is closed out by buying back (closing out) the 16 contracts at 1.3980:

16 contracts sold at 1.4585 = USD 1,458,500

16 contracts bought at 1.3980 = USD 1,398,000

Profit on futures = USD 60,500

The company’s net receipt in selling GBP 1m is USD 1,465,500.

Tick value

In the example above, the smallest price movement in the GBP futures contract is either +/- 0.0001 USD per GBP. This smallest increment (up or down) is called a “tick” and is valued at USD 6.25 (GBP 62,500 x USD 0.0001).

ExPress Notes CIMA P3 Performance Strategy

Page | 42 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

Counterparty Risks/Margin Requirements

These risks are excluded by the exchange where currency futures are traded, as the exchange requires that all clients deposit in advance a cash amount known as “margin” to cover losses.

Market (Price) risk

When a client buys or sells a future, his position is subsequently marked-to-market on a daily basis and potential losses must be covered by the client by providing additional margin.

Settlement risk

This is usually excluded for currency futures by cash settlement of the difference.

Basis Risk

This refers to situation where a hedge does not “fit” (or exactly offset the risk of) the underlying situation. This can occur due to a mismatch in maturities.

KEY KNOWLEDGE Currency Swaps

A company can use swaps to borrow a foreign currency without foreign exchange risk by fixing the exchange rate corresponding to the maturity date of the loan. Swaps (long-term)

EXAMPLE

A US company is looking to expand in Japan and seeks finance of Yen 950m. It can borrow at the following fixed rates: USD 5.0% and JPY 3.0%. A Japanese company is seeking to buy an American company and seeks USD 10m of financing. It can borrow at the following fixed rates: USD 5.4% and JPY 2.5%. The current spot rate is USDJPY 95.00

ExPress Notes CIMA P3 Performance Strategy

Page | 43 © 2012 The ExP Group. Individuals may reproduce this material if it is for their own private study use only. Reproduction by any means for any other purpose is prohibited. These course materials are for educational purposes only and so are necessarily simplified and summarised. Always obtain expert advice on any specific issue. Refer to our full terms and conditions of use. No liability for damage arising from use of these notes will be accepted by the ExP Group. theexpgroup.com

A ‘fixed for fixed’ currency swap for 5 years would look like this: