P2P Report Prepared for Media Defender, Inc.

P2P Report Prepared for Media Defender, Inc.. 2 A larger volume of CD sales in 2006 were lost to borrowing, rather than to P2P How Were Lost CD Sales.

Jan 03, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

P2P ReportPrepared for Media Defender, Inc.

2

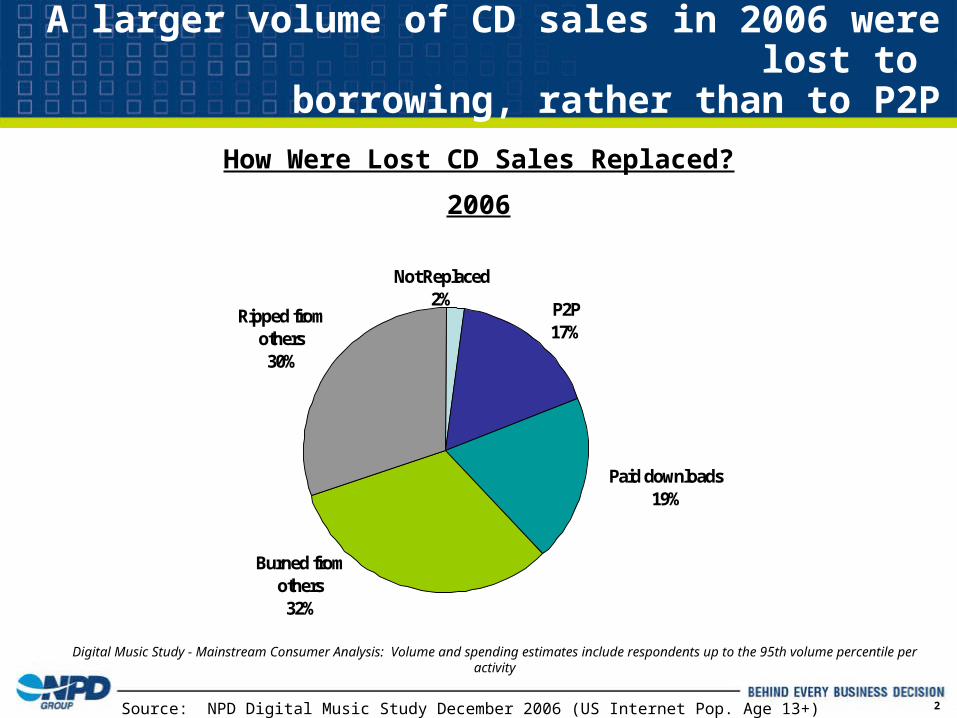

A larger volume of CD sales in 2006 were lost to borrowing, rather than to P2P

How Were Lost CD Sales Replaced?

2006

Ripped from others

30%

Paid downloads19%

Not Replaced2%

P2P17%

Burned from others

32%

Source: NPD Digital Music Study December 2006 (US Internet Pop. Age 13+)

Digital Music Study - Mainstream Consumer Analysis: Volume and spending estimates include respondents up to the 95th volume percentile per activity

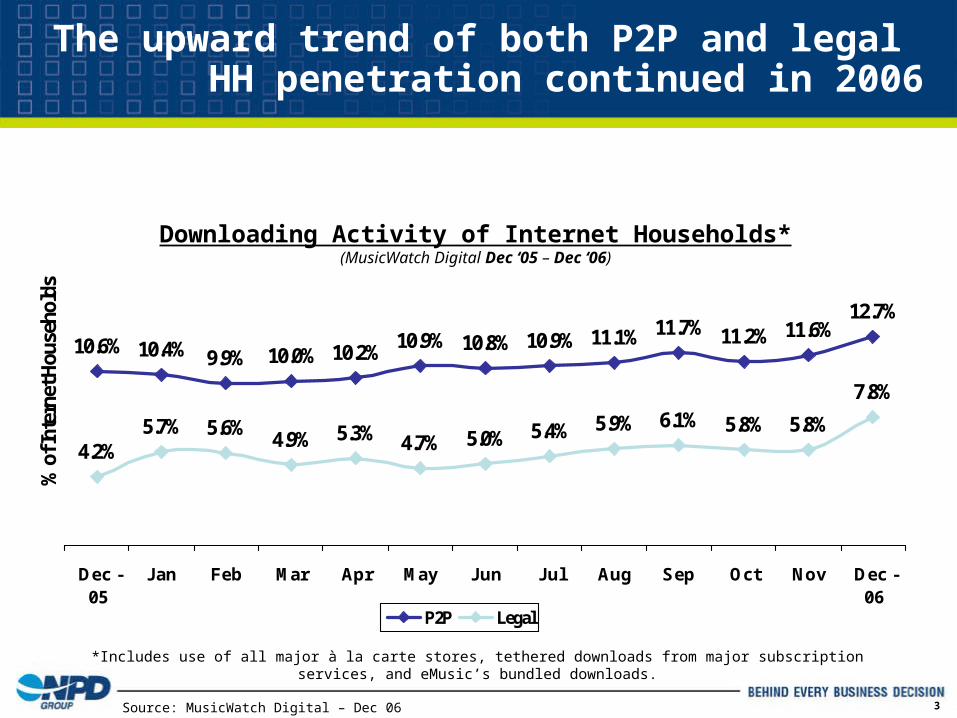

3

10.6% 10.4% 9.9% 10.0% 10.2%10.9% 10.8% 10.9% 11.1% 11.7% 11.2% 11.6%

12.7%

7.8%

5.8%5.8%6.1%5.9%5.4%5.0%5.7%

4.2%5.6%

4.9% 5.3% 4.7%

Dec -05

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec -06

% o

f Int

erne

t Hou

seho

lds

P2P Legal

The upward trend of both P2P and legal HH penetration continued in 2006

Downloading Activity of Internet Households*(MusicWatch Digital Dec ‘05 – Dec ‘06)

*Includes use of all major à la carte stores, tethered downloads from major subscription services, and eMusic’s bundled downloads.

Source: MusicWatch Digital – Dec 06

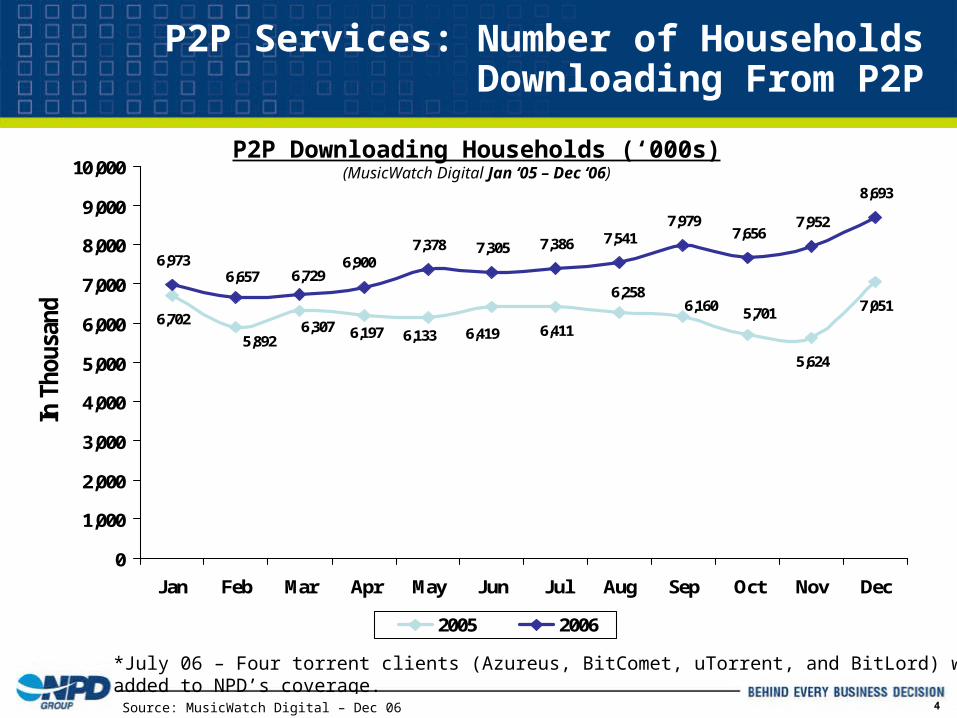

4

P2P Services: Number of Households Downloading From P2P

6,7027,051

6,9737,305

8,693

6,419

5,624

5,7016,1606,258

6,4116,1336,1976,3075,892

7,9527,656

7,9797,5417,3867,378

6,9006,7296,657

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

In T

hous

ands

2005 2006

P2P Downloading Households (‘000s)(MusicWatch Digital Jan ‘05 – Dec ‘06)

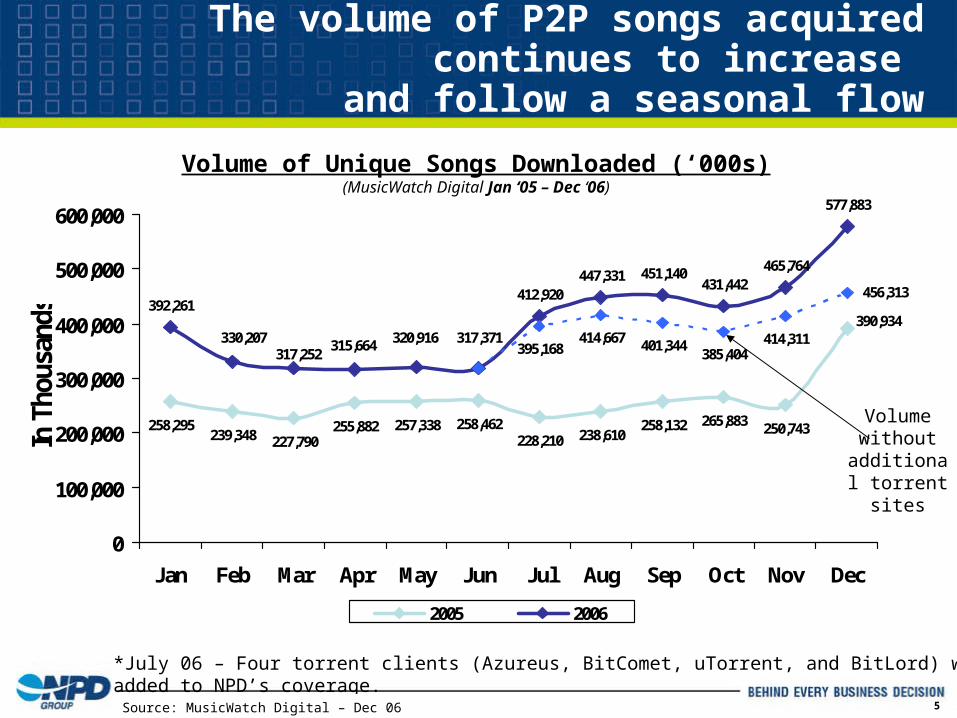

*July 06 – Four torrent clients (Azureus, BitComet, uTorrent, and BitLord) were added to NPD’s coverage.

Source: MusicWatch Digital – Dec 06

5

The volume of P2P songs acquired continues to increase and follow a seasonal flow

258,295

392,261

577,883

395,168414,667 401,344

385,404414,311

250,743265,883258,132238,610228,210

257,338255,882227,790239,348

258,462

390,934

465,764431,442

451,140447,331412,920

320,916315,664317,252

330,207 317,371

456,313

0

100,000

200,000

300,000

400,000

500,000

600,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

In T

hous

ands

2005 2006Line 3

Volume of Unique Songs Downloaded (‘000s)(MusicWatch Digital Jan ‘05 – Dec ‘06)

*July 06 – Four torrent clients (Azureus, BitComet, uTorrent, and BitLord) were added to NPD’s coverage.

Volume without

additional torrent sites

Source: MusicWatch Digital – Dec 06

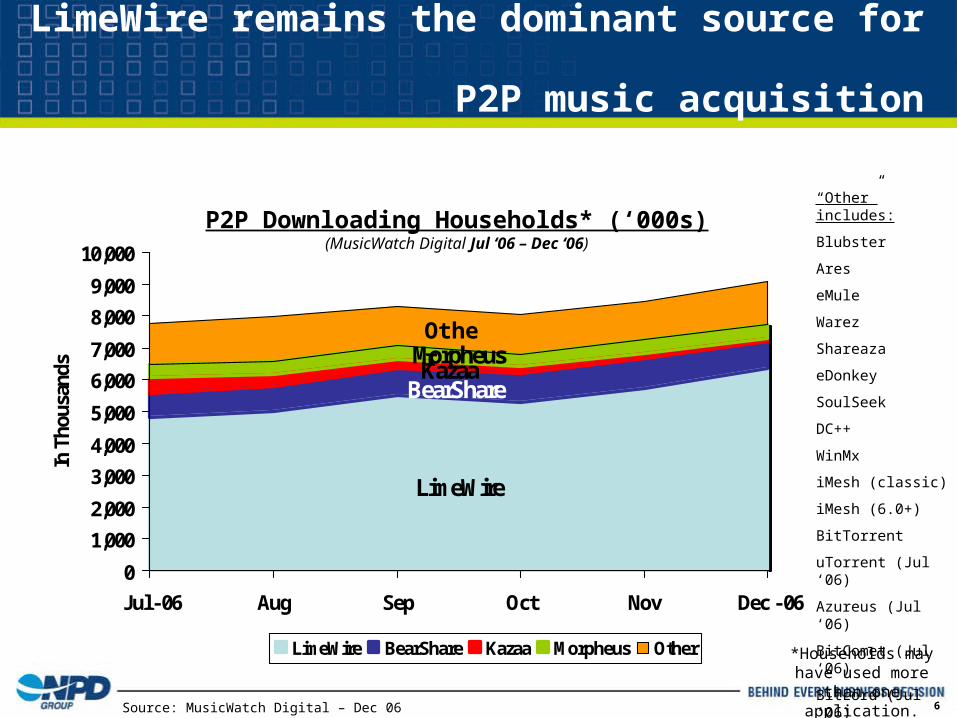

6

LimeWire

BearShareKazaa

Morpheus

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Jul - 06 Aug Sep Oct Nov Dec - 06

In T

hous

ands

LimeWire BearShare Kazaa Morpheus Other

LimeWire remains the dominant source for P2P music acquisition

“Other” includes:

Blubster

Ares

eMule

Warez

Shareaza

eDonkey

SoulSeek

DC++

WinMx

iMesh (classic)

iMesh (6.0+)

BitTorrent

uTorrent (Jul ‘06)

Azureus (Jul ‘06)

BitComet (Jul ‘06)

BitLord (Jul ‘06)

*Households may have used more than one application.

P2P Downloading Households* (‘000s)(MusicWatch Digital Jul ‘06 – Dec ‘06)

Other

Source: MusicWatch Digital – Dec 06

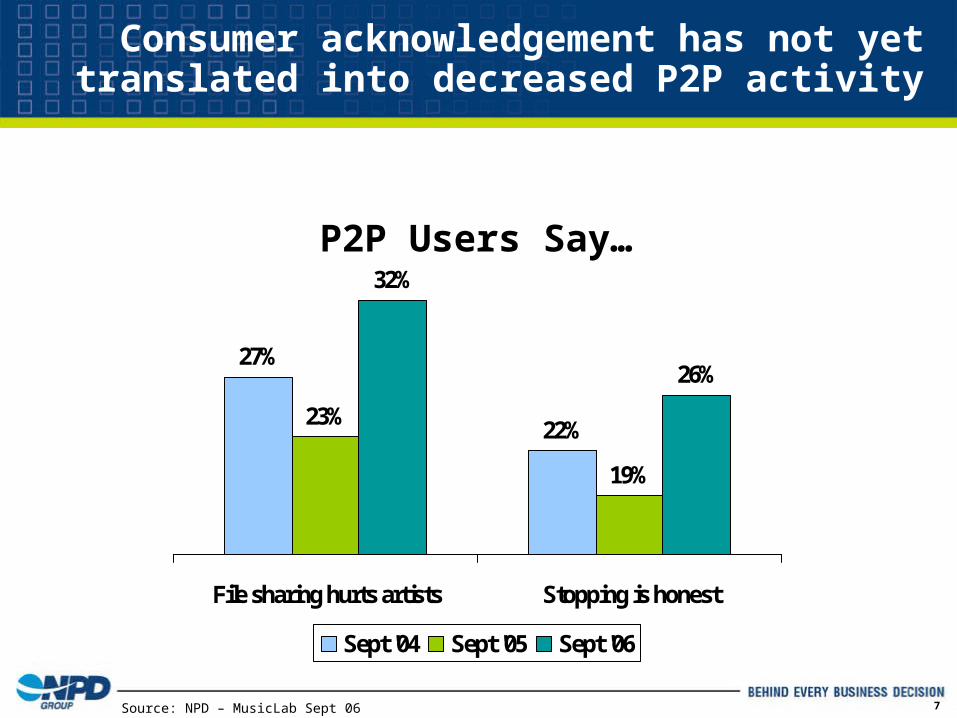

7

Consumer acknowledgement has not yet translated into decreased P2P activity

27%

22%23%

19%

32%

26%

File sharing hurts artists Stopping is honest

Sept '04 Sept '05 Sept '06

P2P Users Say…

Source: NPD – MusicLab Sept 06

8

Reasons For Downloading More From Free File-Sharing Services

Why did you start or download more music from free file-sharing services?(Those who downloaded from free file-sharing services in past year)

28%

26%

25%

24%

23%

22%

21%

17%

13%

11%

30%

33%

37%

55%56%

51%

Like to buy specific songs instead of the full album

Purely because the music is free

If I like the song I can download/stream it instantly

I'm listening to more music on my computer

Can burn songs as much as I want

There's more music available from free services

It's easier to find music using free services

Find more music I like through digital services

Have faster/better Internet access

Free services offer more than just music

Downloading more in place of buying CD's

Burning more mixes with downloads

I have no method to pay for downloads

Music is compatible with my portable player

Have a better computer (hardware and/or software)

Share more of the music I buy with others

Source: NPD Digital Music Study December 2006 (US Internet Pop. Age 13+)

Digital Music Study - Mainstream Consumer Analysis: Volume and spending estimates include respondents up to the 95th volume percentile per activity

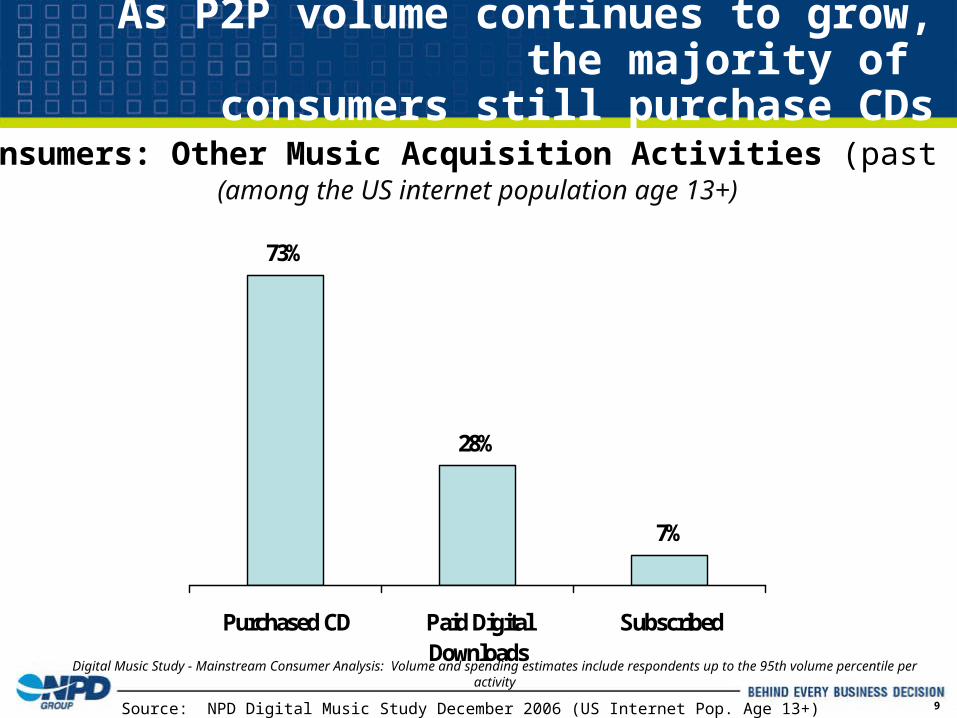

9

P2P Consumers: Other Music Acquisition Activities (past year) (among the US internet population age 13+)

As P2P volume continues to grow, the majority of consumers still purchase CDs

73%

28%

7%

Purchased CD Paid DigitalDownloads

Subscribed

Source: NPD Digital Music Study December 2006 (US Internet Pop. Age 13+)

Digital Music Study - Mainstream Consumer Analysis: Volume and spending estimates include respondents up to the 95th volume percentile per activity

10

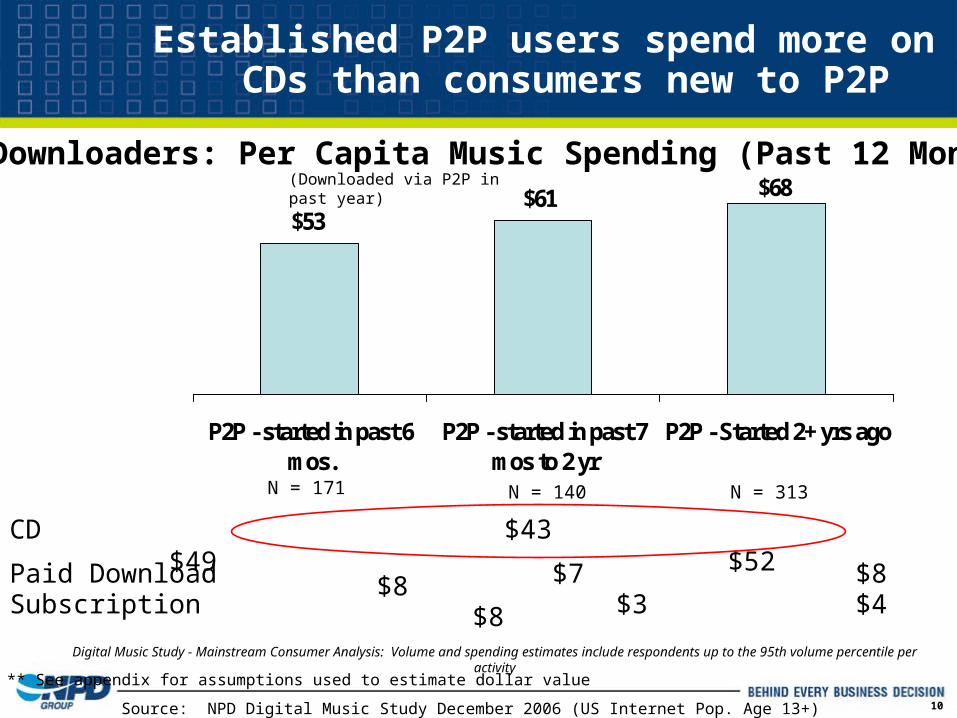

$61$53

$68

P2P - started in past 6mos.

P2P - started in past 7mos to 2 yr

P2P - Started 2+ yrs ago

(Downloaded via P2P in past year)P2P Downloaders: Per Capita Music Spending (Past 12 Months)

CD $43 $49 $52

Subscription $3 $4 $8

** See appendix for assumptions used to estimate dollar value

N = 171 N = 313N = 140

Source: NPD Digital Music Study December 2006 (US Internet Pop. Age 13+)

Paid Download $7 $8 $8

Established P2P users spend more onCDs than consumers new to P2P

Digital Music Study - Mainstream Consumer Analysis: Volume and spending estimates include respondents up to the 95th volume percentile per activity

11

Appendix

12

Value Definitions

The following per-unit cost assumptions were used to calculate the per capita value.

Year 2006 Year 2005Full length CD 12.80$ 13.00$ CD Single 7.97$ 7.02$ Digital Album 9.99$ 9.99$ Digital Track 0.99$ 0.99$ *Subscription Fee 8.45$ 7.80$

*Subscription Fee is self reported. Figure reported in table above is an average for all subscribers

Source: NPD Digital Music Study December 2005 and 2006 (US Internet Pop. Age 13+)

Related Documents