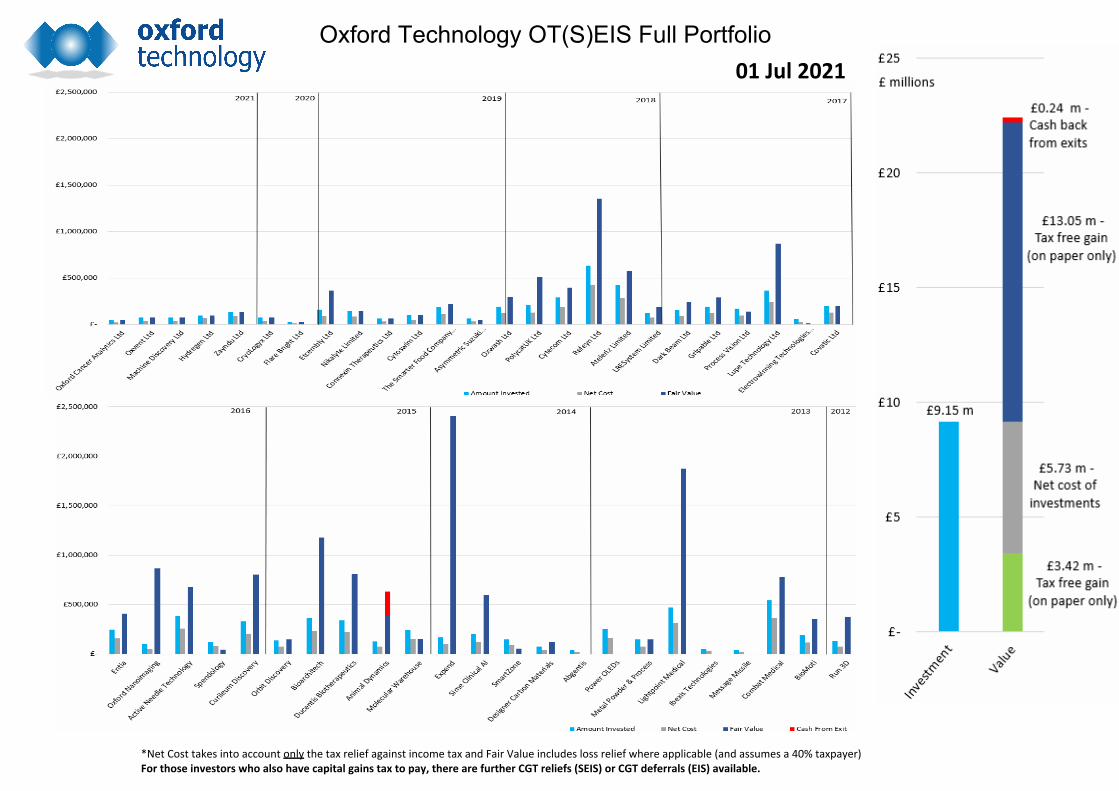

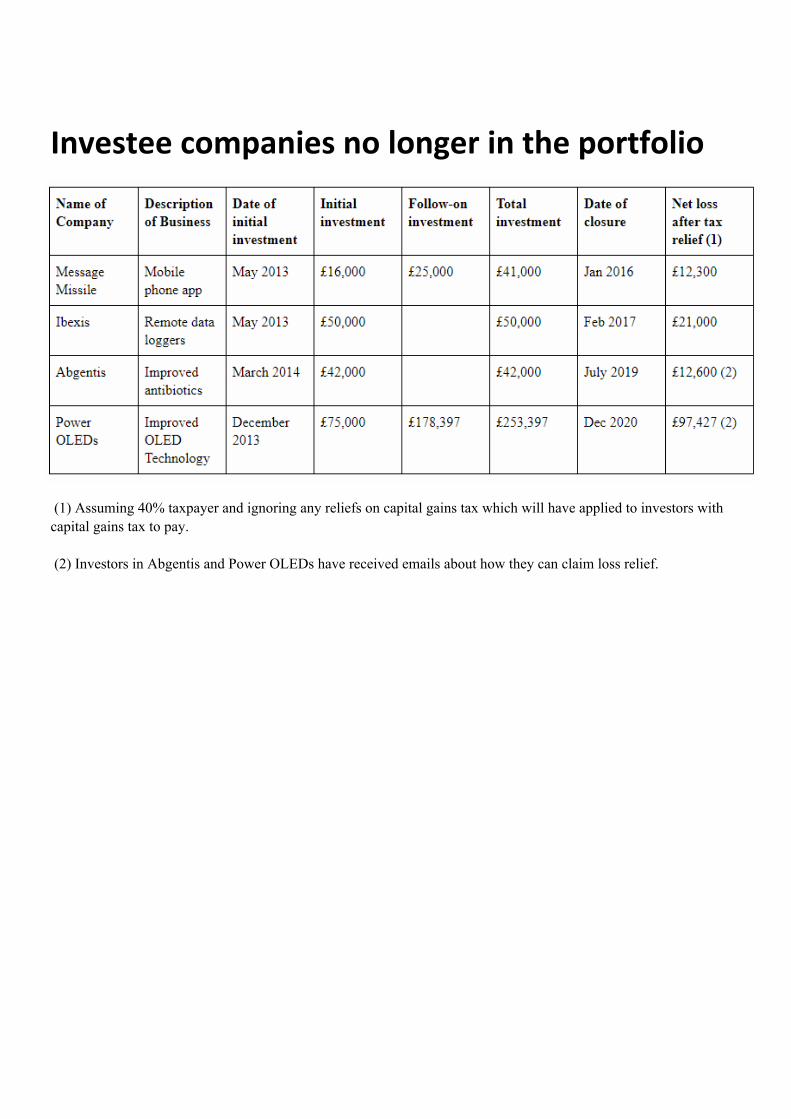

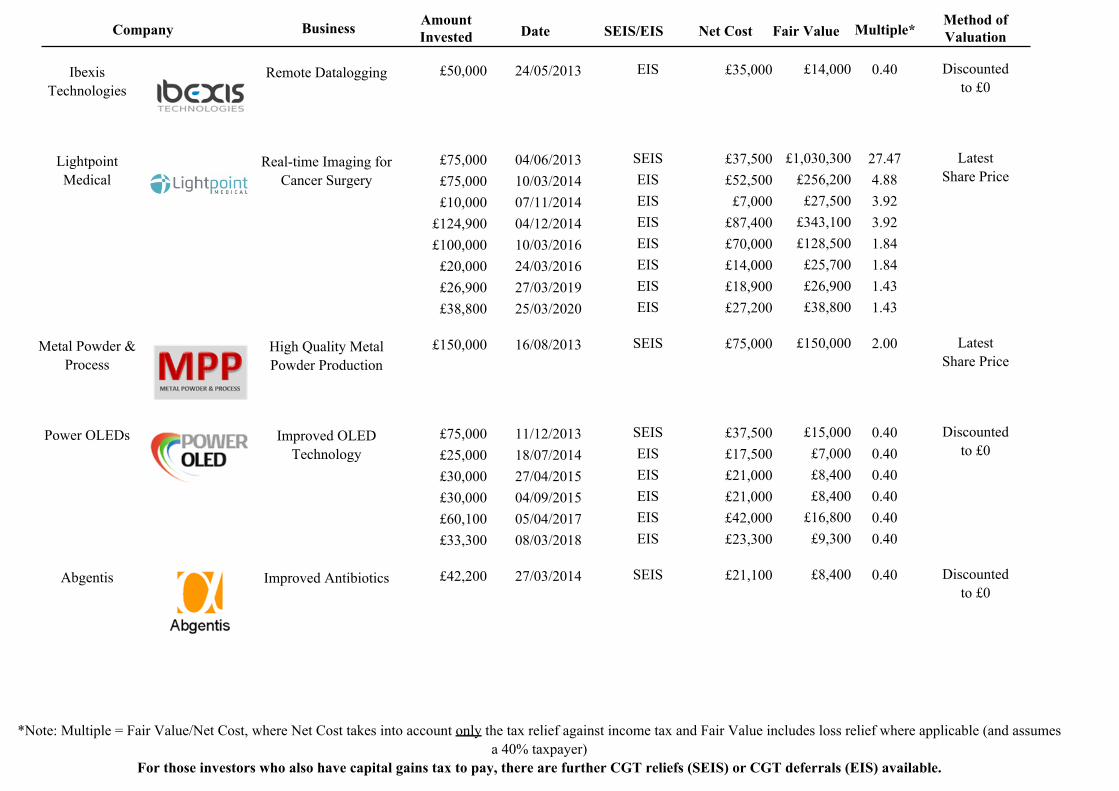

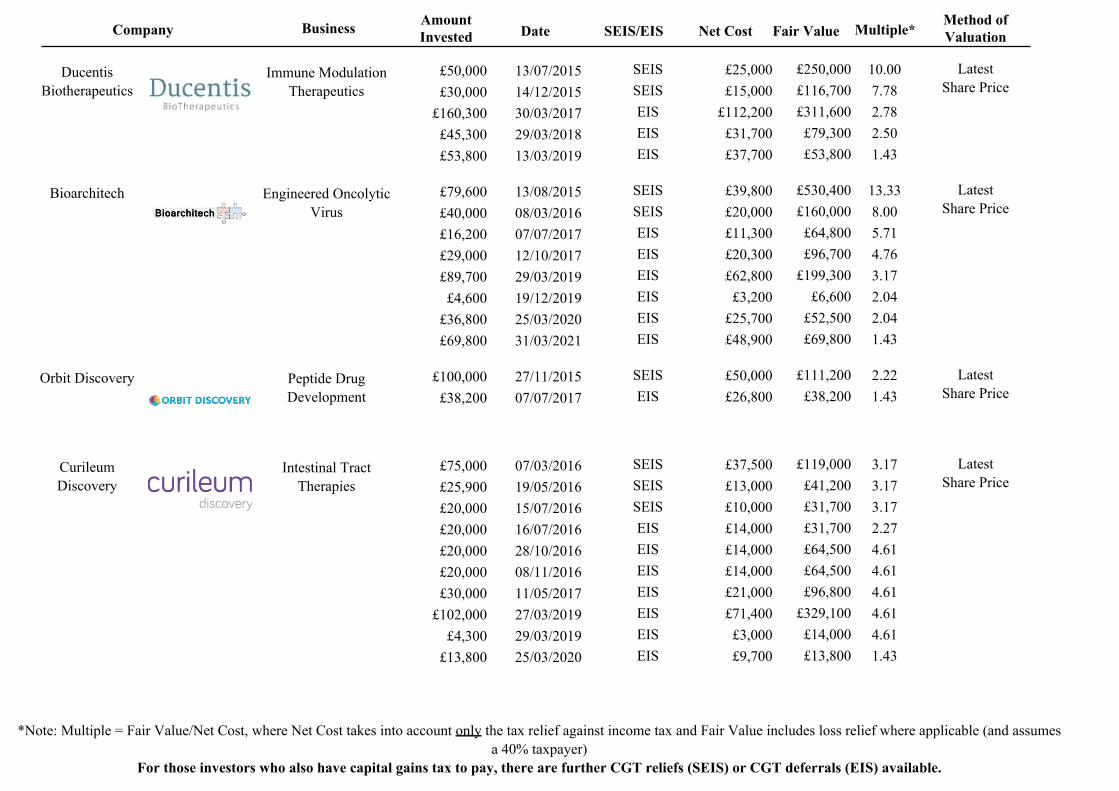

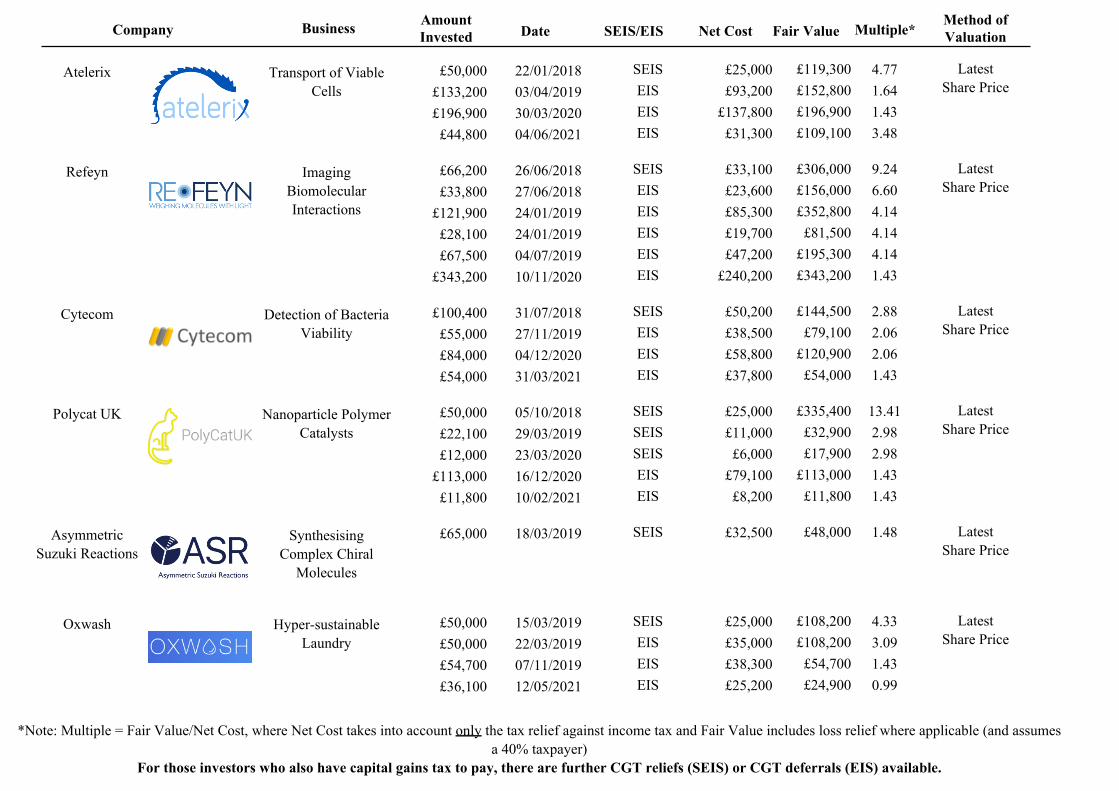

Oxford Technology OT(S)EIS Full Portfolio *Net Cost takes into account only the tax relief against income tax and Fair Value includes loss relief where applicable (and assumes a 40% taxpayer) For those investors who also have capital gains tax to pay, there are further CGT reliefs (SEIS) or CGT deferrals (EIS) available. 01 Jul 2021

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Oxford Technology OT(S)EIS Full Portfolio

*Net Cost takes into account only the tax relief against income tax and Fair Value includes loss relief where applicable (and assumes a 40% taxpayer)For those investors who also have capital gains tax to pay, there are further CGT reliefs (SEIS) or CGT deferrals (EIS) available.

01 Jul 2021

Oxford Technology Combined SEIS and EIS Fund

- OT(S)EIS -Quarterly Report to 01 July 2021

SummaryBy 1st July 2021, OT(S)EIS had completed 170 investments in 50 companies.

The figures for the fund as a whole since its inception are as follows:

Gross amount raised by OT(S)EIS £ 11.15mGross amount invested by OT(S)EIS: £ 9.16mCash back to investors via tax reliefs (1): £ 3.42mNet cost of these investments after tax reliefs (2): £ 5.73mCash back from exits (3): £ 0.24mFair value of remaining portfolio (4): £ 18.78mTotal value: £ 22.44mTax free gain (on paper only so far): £ 13.05mAfter tax losses on the three failures: £ 0.14m

(1) The cash back takes some time to arrive, but it comes in the end. First, the company has to meet certainHMRC requirements (eg starting to trade and spending 70% of the money invested). Then we inform HMRCwho must give us approval before we complete and send the forms to investors who can then reclaim the taxwhen they do their next tax return.

(2) Assuming only income tax relief for a 40% taxpayer. The net cost will be even less for investors in thefund who also have capital gains tax to pay.

(3) In June 2016, OT(S)EIS invested £75,000 as an SEIS investment in Animal Dynamics at 14p per share, so7p per share after tax relief. In March 2019, investors who had opted to sell their shares in Animal Dynamicsreceived payment of 97p per share, so approximately 14 x the after tax share price. Other investors opted tokeep their shares. The company is doing well.

(4) Includes cash back from exits. Valuations are all done by valuing the shares held by OT(S)EIS at the mostrecent price paid by investors in the company. If, following an investment, things have gone wrong, then thevaluation is reduced. But if things have gone well, the valuation is not increased. To this extent the valuationsare conservative. For example, by December 2015, it was clear that Combat Medical was making excellentprogress with its improved treatment for bladder cancer. But the valuation of this investment was notincreased until investment was received in March 2016 at a higher share price. No allowance for fees has beenincluded in the figures above.

Obviously nothing really counts until there are exits. In a sense, the share price achieved at exit is the only onethat matters apart from the original purchase price of the shares. And exits are typically expected in a 5-10year timescale. But the most recent share price paid is a fair guide to a true valuation.

PresentationsAt 10am on the first Thursday of every month, Oxford Technology hosts a Zoom meeting at which existinginvestee companies who are raising additional capital make presentations to investors. The meetings are openfor anyone to attend. After the presentations and before questions, there is a live performance of a Schubertimpromptu, by pianist Anita D’Attellis. Sign up on the website, and we’ll send you an invitation. In order toinvest, you have to certify that you are a sophisticated investor or a HNW. The next meetings are at 10am on:

Thursday 5 August Schubert Op 142 No 3Thursday 2 September Schubert Op 142 No 4Thursday 7 October Schubert wrote 8 impromptus only, so we will move on to something else.

Please make a note in your diary.

During the last quarter, there were presentations from The Smarter Food Company, Connexin, Cytecom,Zayndu, OxVent, and Atelerix. All of these companies received investment as a result of their presentations,and two of them became fully subscribed by lunchtime on the day. This is very helpful to them; it means thefounders can get back to concentrating on what really matters for their businesses - improving their productsand making sales.

Investments in OT(S)EISWhile it is very good that those who attend the Zoom presentations and make direct investments in those whopresent, please consider making an additional investment in OT(S)EIS as well. The reasons are:

You make a single investment and we do all the work. You get a spread of about 5-6 SEIS investments, whichspreads the risks, and then a similar number of EIS investments. We send you the forms necessary to claimyour tax reliefs, send you a report with a valuation each quarter and we actively help the investees.

2 Typically the companies that are presenting are companies which are seeking EIS investment. They arecompanies in which we already made an SEIS investment often at a significantly lower share price. Forexample, in Jan 20 we made an SEIS investment in Etcembly at 40p per share (so 20p after SEIS tax relief).In Dec 20, Etcembly gave a presentation and raised £1.6m of EIS investment at £1.58 per share ( so £1.10after EIS tax relief - more than 5x the after tax share price of the earlier SEIS investment). So the investors inOT(S)EIS who had thereby acquired SEIS shares in Etcembly did very well.

3. Unless we raise capital for OT(S)EIS, we are not able to make the initial SEIS investments in start-ups, andthere wouldn't be companies to present later.

I have myself invested in OT(S)EIS 7 times, so that I have shares in every investee company, bar one - anadministrative error on my part!

New investments

OxCan - Oxford Cancer AnalyticsIn June, OT(S)EIS invested £100,000 in OxCan, a company founded by Peter Liu and Andreas Halner twoOxford DPhil researchers with medical training, who have developed machine learning algorithms to detectearly stage lung cancer with 86% sensitivity and specificity over 99%. They are focusing on recurrent lungcancer as the first niche.

USA+ fundWe continue to believe that there is a good opportunity to create a larger fund, maybe £50m which wouldinvest in those of the earlier investments in the portfolio which are doing well, and which might also providean exit for some of the SEIS and EIS investors. The concept is very simple. Since we invest in companies atthe very earliest stage, typically when there are one of two people in a lab with an idea, and because we getactively involved (almost all investments are within an hour’s drive) we get to know the founders very well.And we know the things which the founders might prefer that we didn't know - problems with personnel andpatents, for example. This puts us in a very good position to be able to judge which investees companies areworth backing with significantly larger investments of several £m. A particular aim would be to use Bijan(who helped build Synopsys in California from 300 to 13,000 people) to help these companies get started inthe US. The valuations of technology companies are generally significantly higher in the US than in the UK,so this should benefit the initial UK investors.

News in Brief

Run3D continues to make good progress, and opened three new clinics during the quarter, brining the total to23 globally.

Lightpoint has a new CEO to drive sales and financing, while David Tuch continues to focus on science andstrategy as Executive Chairman.

Expend’s revenues continue to grow. It received about £400,000 of investment in the last quarter. Monthlyrevenue, while affected by Covid lockdowns, continues to grow and is up 230% from last year.

Oxwash continues to see rising sales at its three sites (Oxford, London, Cambridge). It hopes to beginoperating its hub and spoke expansion plan during the next quarter. It has £2m in cash and a burn rate of £50kper month, but reducing.

Polycat is in commercial negotiations with several large global companies who may use its (now certified)anti-viral permeable material in air conditioning systems and in medical gloves and clothing.

Funds

Oxford Technology manages two funds:

1. OT(S)EIS - The Start-up Fund: Investors' money is invested over 3 years - Approx. 1/3 (less fees) in SEISinvestments in year 1, 1/3 in EIS investments in year 2 in those of the earlier SEIS investees which are doingwell, and the same again in year 3. SEIS investments are very high risk and some failures are to be expected,although there have been very few so far which is why the track record is so good. So it takes 3-4 years beforeall the tax reliefs are obtained, which does not suit everybody.

2. OTEIS - The Development Fund: Investors have all their money invested within one year in EISinvestments, mainly in earlier OT(S)EIS investments which are developing well. So this fund has a lower riskprofile than OT(S)EIS and investors can claim their tax reliefs more quickly.

It is possible to invest in both funds. Information Memorandums and Application forms can be downloadedfrom www.oxfordtechnology.com

SEIS Tax Reliefs Summary- Income Tax bill reduced by 50% of investment- Income Tax bill reduced further if the business fails - up to 22.5%- 50% relief against capital gains which is not merely deferred but cancelled- No tax on Capital Gains from investments- No inheritance tax on shares after 2 years- Tax reliefs can be claimed as if the investment had been made in the previous financial year, if the investorwishes

EIS Tax Reliefs Summary- Income Tax bill reduced by 30% of investment- Income Tax bill reduced further if the business fails - up to 31.5%- The payment of tax on a capital gain can be deferred where the gain is invested in EIS shares. The CapitalGain to be deferred can be made three years before, or one year after the investment- No tax on Capital Gains from investments- No inheritance tax on shares after 2 years- Tax reliefs can be claimed as if the investment had been made in the previous financial year, if the investorwishes.

For more in depth details, please consult HMRC or your financial advisor.

Example SEIS investment

An individual investor with income tax of £25,000 to pay and capital gains of £100,000 in the 2019/2020 taxyear on which tax of £20,000 at the 20% rate is due to be paid invests £10,000 in an SEIS qualifying companyin 2019/2020.

Investment: £10,000Income tax bill reduced by 50% of this: - £ 5,000Capital Gains tax bill reduced by: - £ 1,000Net cost of investment: £ 4,000

If the above investor also had income tax of £25,000 and capital gains of £100,000 in the 2018/2019 tax yearon which tax of £20,000 at the 20% rate had been due then they could choose whether to treat their 2019/2020investment as having been made in 2018/2019 and claim relief in that year. This would result in a reduction incapital gains tax of £1,000 and therefore a net cost of investment of £4,000.

Should the investee company fail, the remaining part of the investment on which income tax relief has notbeen claimed (£5,000 in this example), may be set against the investor's income tax liability. For a 45%taxpayer, this relief is worth £2,250. For a 40% taxpayer, this relief is worth £2,000. For a 20% tax payer, thisrelief is worth £1,000.

So for a 45% taxpayer with capital gains tax to pay, the total loss on the investment of £10,000 would bereduced to £1,750 if the investment was made in 2019/2020 and not carried back to the previous year. If theinvestments succeeds, and the shares are sold for £20,000 (so twice the purchase price) the £20,000 would betax free, a multiple of more than 5 times the net cost.

Fees for OT(S)EIS

Initial fee: 1%Management fee: Annual fees on gross sum invested are as follows:Years 1-3: 2%Years 4-7: 1.5% (deferred to be paid only from proceeds of exits)Year 8 and onwards: 0%

Any interest earned on uninvested capital will be used first for paying the management fee. The investeecompanies will mainly be within an hour’s drive of Oxford as OTM will be actively involved in helpinginvestee companies especially in the early days. OTM may charge the investee companies a separate fee forthis help and involvement.

The Custodian’s fees: This will be 0.15% + VAT annually (NB – at the outset this was 0.35% but from 2017has been reduced). There is a receiving agent fee of up to £25 + VAT for each subscription. There will also bea £15 fee for each holding that is transferred into the individual investor’s name (it is not intended that thisshould happen frequently). There may also be a small charge for making a distribution. The fees will be paidfrom the investor’s cash pool.

Performance Incentive: Once a typical investor, defined as a 40% taxpayer with no capital gains tax to shelter,has received a return of £1.20 (including tax benefits) for each £1.00 invested then 20% of all furtherpayments to all investors who invested at the same time will be paid to OTM as a performance incentive.

China Office - [email protected] Technology has an office in Shanghai in China, run by Chenjie Ma, who read engineering at Oxford,who speaks English and Chinese and who understands both cultures. She worked at Oxford Technology inOxford before going to run the office in China. It is naturally a great help to our investee companies to have aChinese speaker on their side if/when they are seeking to make their first sales in China.

California Office - [email protected] Technology also has an office in Menlo Park just outside San Francisco in California. This office isrun by Bijan Kiani. Oxford Technology invested in his first start-up business, INCA, in the 1980s. Thebusiness did very well and 3i later invested. INCA was ultimately sold to a company in California for whomBijan then went to work. After a few years, Bijan was headhunted by Synopsys to head up their sales andbusiness development strategy. Synopsys employed 300 people at that time. Bijan played a major part in itsgrowth to 13,000 people today and the No 1 position in its field (Electronic Design Automation). In 2019,Bijan contacted OTM, saying that while he had enjoyed working with Synopsys and building a large andsuccessful business, what he had really enjoyed most was the early days of his first business, working withOTM to get it all going and getting the first sales contracts in the US etc. What he would now like to dowould be to help our investees in the UK get going in the US. He has been as good as his word, and all theCEOs of our investees who have worked with Bijan have said how helpful and useful he has been.

£100,000£15,000£10,000£3,000

£10,200

SEISSEIS

Non SEIS/EISEISEIS

18/12/201218/10/201318/10/201310/11/201729/03/2019

25.13%

FundShareholding

Date Amount TypeShare Price£0.15£0.15£0.15£0.30£0.45

Description of BusinessRun3D is the brainchild of Dr Jessica Leitch, who is an International runner herself (representing Wales) and who hasa D.Phil from Oxford in the biomechanics of running. Runners have reflective balls attached to their various joints(hips, knees, ankles) and also at various other points on their legs and then run on a treadmill. Special cameras capturethe image of the balls at 200 frames/sec. This data is then fed into a computer programme. The computer then outputs acomplete gait analysis, giving every detail of the gait, the angle of heel-strike, the rotation and rate of rotation of eachjoint etc. The analysis can be used to modify the gait for two purposes, to reduce the likelihood of injury and toincrease speed.

Progress since InvestmentInitial progress was quite good. The company opened its own Run3D centre in Oxford, and also opened fivefranchises. But it then became clear that improvements in the software were needed, so Run3D then spent the next twoyears, in collaboration with a company in Amsterdam and with the help of a grant, rewriting the software from scratch.The new software was used for the first time in summer 2016, and was a big step forward - easier to use and with manynew features. In Q1 21, all the data (at last!) went into the cloud so that every time a Run3D gait was done anywhere inthe world, the (anonymised) data went into the cloud, enabling Run3D to quickly compile databases of different typesof runners, eg Elite Female Marathon Runners, Male runners over 60 etc. Also in Q1 21 Run3D’s AI went live tointerpret the results. One of the difficulties that Run3D has faced is that it produces a vast amount of data (themovement of every joint and element at 200 frames per second). While an experienced podiatrist can interpret thisdata, some younger physiotherapists have found it daunting. The new add-on software automatically interprets a gaitreport, and makes suggestions as to what the issues might be, making Run3D less complicated to use and moreappealing to a wider market of less-experienced clinicians.

The table below summarises developments:Date UK Ireland USA Holland Other Overseas Mobile Total Total PayingSep 2017 5 1 6 6Dec 2017 6 1 1 8 8Dec 2018 7 1 1 2 11 11 Dec 2019 8 2 1 1 2 1 15 15Dec 2020 11 2 0 4 2 1 20 20Jun 2020 11 2 0 4 2 1 20 0 (CV19)Mar 2021 11 2 0 4 3 1 21 18*Jun 2021 14 2 0 4 3 1 24 22**

* -2 due to Covid ** Premises

Recent DevelopmentsRun 3D has had an excellent quarter. Three new clinics have opened. Run 3D is also now being used in regularly

China and the first paying clinic should open in Q3. Also, the first mobile event in the US should happen in Q3. Twoclinicians have asked to buy shares and will do so at 60p per share.

£0.45

ValuationShare Price

£1,494,501

CompanyValuation

www.run3d.co.uk

Run 3D

£75,000£40,000£74,700

SEISEISEIS

08/01/201328/05/201431/03/2021

15.52%

FundShareholding

Date Amount TypeShare Price£0.05£0.05£0.12

Description of BusinessBioMoti is based on technology from Queen Mary University of London. Its founders are Dr. Davidson Ateh and Prof.Jo Martin who was appointed as Head of Pathology for the NHS in early 2013. The chairman is Keith Powell who haslong experience in early stage biotechnology companies.

Tumour cells including those from ovarian, breast, pancreatic, colon, prostate, and bladder cancer overexpress aparticular ligand, CD95L on their surfaces. CD95L helps tumours to avoid the immune system by killing off certainclasses of immune cells and is also associated with triggering cancer metastasis. The scientists have discovered that if asmall particle is coated with CD95R (which binds to CD95L), the cancer cell will engulf the particle and draw it inside.By loading a chemotherapeutic drug into a biodegradable particle coated with the receptor molecule, it is possible todeliver high concentrations of chemotherapy drug into the cancer cells.

Biomoti’s first product uses paclitaxel to target ovarian cancer in a much more efficacious and less toxic manner, withthe potential to extend use to further cancers such as hard to treat breast cancers. BioMoti’s technology, calledOncojanTM, can dramatically increase the efficacy of standard clinical treatments whilst reducing side-effects in healthytissues. Preclinical tests have shown remarkably good results, with 65-fold reductions in tumour burden, doubling ofmedian survival and significant decreases in toxicity seen in an ovarian cancer model when the technology is appliedand compared with the current clinical standard-of-care.

Progress since InvestmentThe final bits of data are in on the pre-clinical model and the results. This confirms that Oncojans deliver on thepromise of higher activity and lower toxicity than the standard of care delivery for paclitaxel. It enables the drug togive performance similar to cisplatin, a much more powerful drug which has limitations which the Oncojans would nothave. Although only observed (as there was quite a lot of variation and relatively few samples) the Oncojans seem toencourage the penetration of Cytotoxic T cells into the tumour environment.

BioMoti has had first results with a new manufacturing technique. The results so far are too good… the drug loadingwas too high. As in the past the problem has always been relatively low loadings of drug, we think this problem can beovercome.

Recent DevelopmentsDavidson has been working on setting up a base in Mauritius to make use of the lower costs and has been pursuingfurther funding. Both activities have been a little slow, but some progress is being made, if primarily in eliminating theroutes that won’t work. One area where progress is being made is on the manufacturing options of which BioMoti nowhas more than ever before. Picking the best one will be important, but it’s good that there are now several options.

£0.12

ValuationShare Price

£2,297,312

CompanyValuation

www.biomoti.com

BioMoti

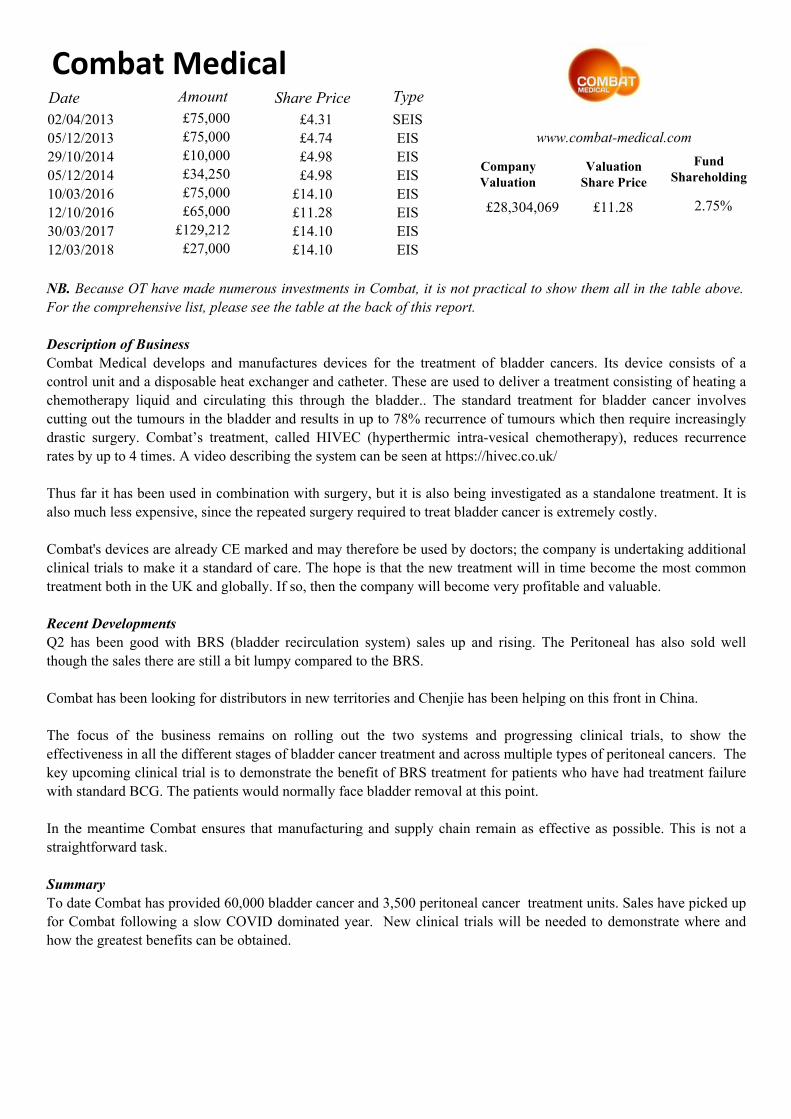

£75,000£75,000£10,000£34,250£75,000£65,000

£129,212£27,000£54,223

SEISEISEISEISEISEISEISEISEIS

02/04/201305/12/201329/10/201405/12/201410/03/201612/10/201630/03/201712/03/201826/03/2021

2.75%

FundShareholding

Date Amount TypeShare Price£4.31£4.74£4.98£4.98

£14.10£11.28£14.10£14.10£11.28

NB. Because OT have made numerous investments in Combat, it is not practical to show them all in the table above.For the comprehensive list, please see the table at the back of this report.

Description of BusinessCombat Medical develops and manufactures devices for the treatment of bladder cancers. Its device consists of acontrol unit and a disposable heat exchanger and catheter. These are used to deliver a treatment consisting of heating achemotherapy liquid and circulating this through the bladder.. The standard treatment for bladder cancer involvescutting out the tumours in the bladder and results in up to 78% recurrence of tumours which then require increasinglydrastic surgery. Combat’s treatment, called HIVEC (hyperthermic intra-vesical chemotherapy), reduces recurrencerates by up to 4 times. A video describing the system can be seen at https://hivec.co.uk/

Thus far it has been used in combination with surgery, but it is also being investigated as a standalone treatment. It isalso much less expensive, since the repeated surgery required to treat bladder cancer is extremely costly.

Combat's devices are already CE marked and may therefore be used by doctors; the company is undertaking additionalclinical trials to make it a standard of care. The hope is that the new treatment will in time become the most commontreatment both in the UK and globally. If so, then the company will become very profitable and valuable.

Recent DevelopmentsQ2 has been good with BRS (bladder recirculation system) sales up and rising. The Peritoneal has also sold wellthough the sales there are still a bit lumpy compared to the BRS.

Combat has been looking for distributors in new territories and Chenjie has been helping on this front in China.

The focus of the business remains on rolling out the two systems and progressing clinical trials, to show theeffectiveness in all the different stages of bladder cancer treatment and across multiple types of peritoneal cancers. Thekey upcoming clinical trial is to demonstrate the benefit of BRS treatment for patients who have had treatment failurewith standard BCG. The patients would normally face bladder removal at this point.

In the meantime Combat ensures that manufacturing and supply chain remain as effective as possible. This is not astraightforward task.

SummaryTo date Combat has provided 60,000 bladder cancer and 3,500 peritoneal cancer treatment units. Sales have picked upfor Combat following a slow COVID dominated year. New clinical trials will be needed to demonstrate where andhow the greatest benefits can be obtained.

£11.28

ValuationShare Price

£28,304,069

CompanyValuation

www.combat-medical.com

Combat Medical

£75,000£75,000£10,000

£125,000£100,000£20,000£27,000£38,800

SEISEISEISEISEISEISEISEIS

04/06/201310/03/201407/11/201404/12/201410/03/201624/03/201627/03/201925/03/2020

6.90%

FundShareholding

Date Amount TypeShare Price£0.047£0.190£0.238£0.238£0.509£0.509£0.65£0.65

Description of BusinessIn cancer surgery, a surgeon cannot see whether the entirety of a tumour has been removed. In prostate cancer surgery,for example, roughly one quarter of surgeries will leave some cancerous tissue behind after surgery. Lightpoint hasdeveloped an imaging technology based on existing imaging PET and SPECT radiopharmaceuticals, to providesurgeons with a real time image of the cancer. The patient is injected with an imaging drug (a radioactive tracercommonly used in medical imaging) which is taken up by cancerous tissue, so the surgeon is able to see the tinyamounts of light emitted from the tissue. Lightpoint is very actively engaged with surgeons to ensure that the productsare best suited to their needs.

Progress since InvestmentLightpoint launched its first product in Q1 2018. The LightPath® Imaging System enables surgeons to determinewhether the tissue they have removed during surgery is surrounded by a clear margin of healthy tissue. The companyreceived early commercial sales for LightPath® in the UK, Germany and the Netherlands and a number of placementunits in the US.

There are six active clinical trials underway with LightPath® in multiple cancer indications. The company has wonnumerous grants and awards in recognition of the impact its technologies will have in cancer surgery. Lightpointrecorded the first sales of its single use add-on for LightPath®. Patient recruitment has been completed in a multi-centre clinical trial of LightPath® in breast-conserving surgery.

The company has grown and adapted as the market feedback has directed it towards in-vivo applications suitable forlaparoscopic and robot-assisted surgery where the benefit of limiting the removal of healthy tissue is greatest; prostatecancer surgery in particular. The company has strengthened its medical advisory board with specialists from theprostate cancer field.

Its second product is SENSEI, a robotic laparoscopic probe for prostate cancer surgery. The probe will have twoapplications: sentinel node detection and metastatic node detection.

Recent DevelopmentsIn May 2021 Graeme Smith was appointed as CEO of Lightpoint, bringing to bear his three decades of medtechcommercial, corporate finance and sales and marketing experience. David Tuch will remain Executive Chair to providescientific, technical and strategic direction.

KU Leuven and Institut Paoli-Calmettes, Marseille joined the SENSEI prostate cancer clinical trial, while Hospital delMar in Barcelona has already treated eight patients with the same device. SENSEI was used in its first cervicalprocedure as part of a new investigator-initiated study at The University Medical Centre Utrecht, Netherlands.SENSEI now has distributors in Spain, Portugal, Australia and Italy, and there is interest from many other countries.The Australian distributor has announced a first sale in the country.

In summary, SENSEI is doing very well for Lightpoint and the future continues to look bright..

£0.65

ValuationShare Price

£27,215,587

CompanyValuation

www.lightpointmedical.com

Lightpoint Medical

£150,000 SEIS16/08/2013

12.00%

FundShareholding

Date Amount TypeShare Price£1.25

Description of BusinessMetal Powder & Process (MPP) was established to produce high quality metal powders by gas atomisation for theaerospace, medical, and other industries. Metal is melted at the top of the atomiser, a machine the size of a small house,poured through a nozzle and blasted by jets of supersonic argon gas, and so turned into dust. The use of powderedmetals has been growing steadily over the last 50 years. It is less expensive to produce certain components, e.g. gearwheels used in cars, by metal injection moulding powdered steel, than it is to start with solid steel and then cut eachtooth on a machine. Metal injection moulding also produces parts which can be stronger and more accurate. Nowdemand is increasing even more quickly due to the rapid growth of 3D printing of metal parts.

Due to the incorporation of some novel technology, it is hoped that the atomiser (known as Bertha) operated by MPPwill produce powder of higher purity than the powders produced by existing atomisers. This, in turn, should make thepowder suitable for use in the aerospace industry. In the past, the aerospace industry has been reluctant to usepowdered metal since the impurities which are present in powders produced by existing designs of atomisers arepotential crack-initiation sites.

Progress since InvestmentWork on completing and commissioning Bertha has been continuing since the investment. The first sales wereachieved in Q1 2015 for trial quantities. In Q4 2016, and after a development programme lasting about a year aimed atproducing powder of a novel alloy for an overseas customer, MP&P received its first significant order. This order wasworth >£1m, to be delivered at steadily increasing monthly quantities. This was a great achievement and an importantmilestone in the development of the company, but it brought new challenges. In Q2 2017, Bertha produced her firsttitanium powder. During Q1 2021 the new fluidised bed, owned by MP&P’s sister company PSI, became operational.This will be used, initially experimentally, to coat particles used in battery anodes in electric vehicles in a way which, itis hoped, will result in longer life batteries, capable of a significantly increased number of charge/discharge cycles. Ifthis works, the potential is large. The rig will also be used to heat treat post-production metal powders to make themmore suitable for repairing military aircraft in remote locations. The other use for the rig will be to recondition wastepowder from AM operations. Several of these developments are grant-funded and with several parties involved.

Recent DevelopmentsBertha has been mainly used for research and development purposes in the last quarter, producing ever largerquantities of a novel powder for a customer, in a paid programme.

£1.25

ValuationShare Price

£1,250,000

CompanyValuation

www.metalpowderprocess.co.uk

Metal Powder & Process

£75,000 SEIS03/04/2014

14.71%

FundShareholding

Date Amount TypeShare Price£0.75

Description of BusinessProfessor Kyriakos Porfyrakis developed a method of producing small quantities of endohedral fullerenes, whileworking in the Materials Department of Oxford University. Carbon exists in many forms, including graphite anddiamond. But carbon can also exist as fullerenes, hollow spheres of carbon atoms, the simplest of which is made up of60 carbon atoms. Kyriakos has developed a method of making fullerenes which contain an atom of another elementinside. At the time of the investment, the elements chosen were Gadolinium, Yttrium and Nitrogen. It was believed thatthese novel materials will have potential uses as a better contrast agent for MRI scans, for improving the efficiency ofphotovoltaics, and for use in certain quantum computing applications. There had been considerable interest fromresearchers around the world. Production capacity at the time of investment was about 1 gram per month. This is aclassic high risk, high potential reward investment.

Progress since InvestmentProduction of the materials and research continued in the lab. An important milestone was achieved in Q3 2014, whenDCM received its first order, £22,000 for 0.2mg of a nitrogen-containing fullerene, with a purity of 1 in 1,000, so 200micrograms of the N@C60. This is a price of more than £100m per gram, so we think this might be the most expensivematerial on the planet.

The material is being used in a research project whose aim is to produce an extremely accurate atomic clock on a chipso that it could be used in a mobile phone. This would enable GPS to be much more accurate which would have manypotential applications including controlling driverless cars. In Q1 2018, a contract was signed with LocatorX, a UScompany, which will be seeking to commercialise the atomic-clock-on-a-chip application. DCM agrees to supplyLocatorX N@C60 exclusively for this application and they agree to buy only from DCM. DCM received 100,000founder shares in LocatorX. LocatorX raised some capital in Q1 2019, although not as much as originally hoped.

Recent DevelopmentsProgress has remained slow, but a small technical milestone has been achieved in the atomic clock project in that thereference signal, which had been detected in the UK before, but which had not been detected by the US scientistsengaged on the project has now been detected. So, all being well, the signal from the N in the N @C60 molecules willnow also be detected. This, in turn, should become the basis of an atomic clock.

Professor Porfyrakis is the now Head of Research for the school of Engineering at the University of Greenwich, andhis work on N@C60 will continue at Greenwich. The labs are all beginning to reopen as the pandemic is comingunder control.

£1.25

ValuationShare Price

£849,875

CompanyValuation

www.designercarbon.com

Designer Carbon Materials

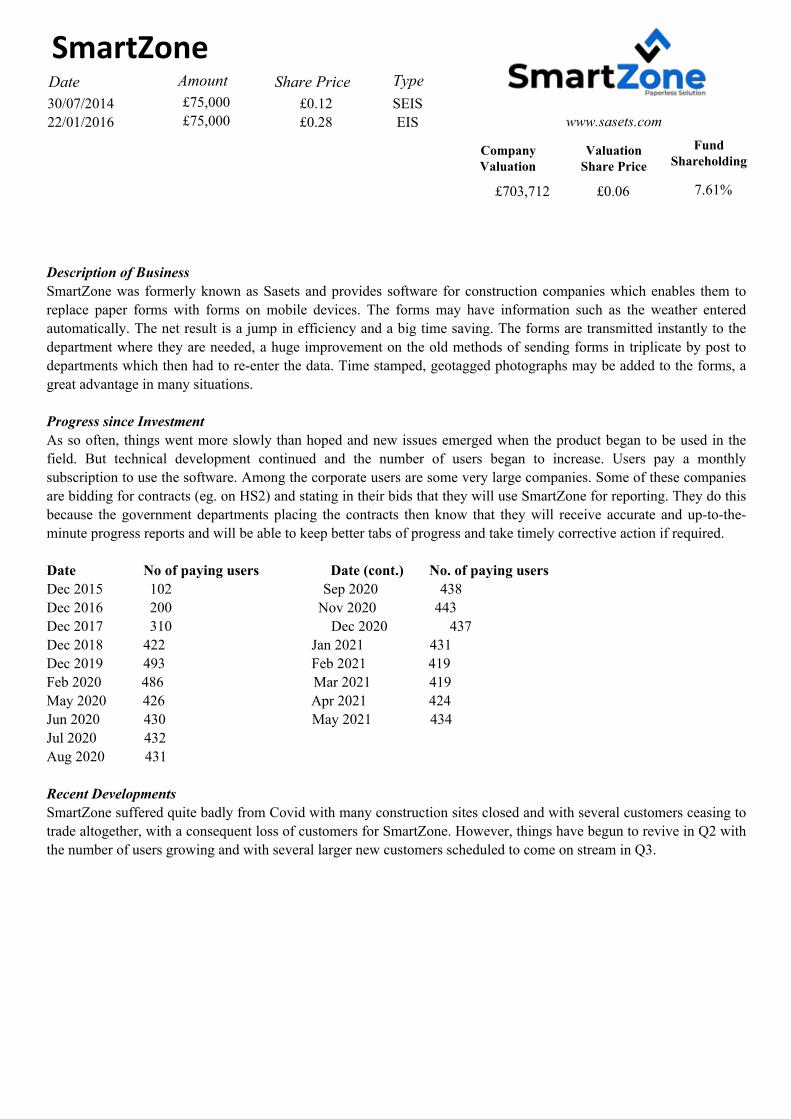

£75,000£75,000

SEISEIS

30/07/201422/01/2016

7.61%

FundShareholding

Date Amount TypeShare Price£0.12£0.28

Description of BusinessSmartZone was formerly known as Sasets and provides software for construction companies which enables them toreplace paper forms with forms on mobile devices. The forms may have information such as the weather enteredautomatically. The net result is a jump in efficiency and a big time saving. The forms are transmitted instantly to thedepartment where they are needed, a huge improvement on the old methods of sending forms in triplicate by post todepartments which then had to re-enter the data. Time stamped, geotagged photographs may be added to the forms, agreat advantage in many situations.

Progress since InvestmentAs so often, things went more slowly than hoped and new issues emerged when the product began to be used in thefield. But technical development continued and the number of users began to increase. Users pay a monthlysubscription to use the software. Among the corporate users are some very large companies. Some of these companiesare bidding for contracts (eg. on HS2) and stating in their bids that they will use SmartZone for reporting. They do thisbecause the government departments placing the contracts then know that they will receive accurate and up-to-the-minute progress reports and will be able to keep better tabs of progress and take timely corrective action if required.

Date No of paying users Date (cont.) No. of paying usersDec 2015 102 Sep 2020 438Dec 2016 200 Nov 2020 443Dec 2017 310 Dec 2020 437Dec 2018 422 Jan 2021 431Dec 2019 493 Feb 2021 419Feb 2020 486 Mar 2021 419May 2020 426 Apr 2021 424Jun 2020 430 May 2021 434Jul 2020 432Aug 2020 431

Recent DevelopmentsSmartZone suffered quite badly from Covid with many construction sites closed and with several customers ceasing totrade altogether, with a consequent loss of customers for SmartZone. However, things have begun to revive in Q2 withthe number of users growing and with several larger new customers scheduled to come on stream in Q3.

£0.06

ValuationShare Price

£703,712

CompanyValuation

www.sasets.com

SmartZone

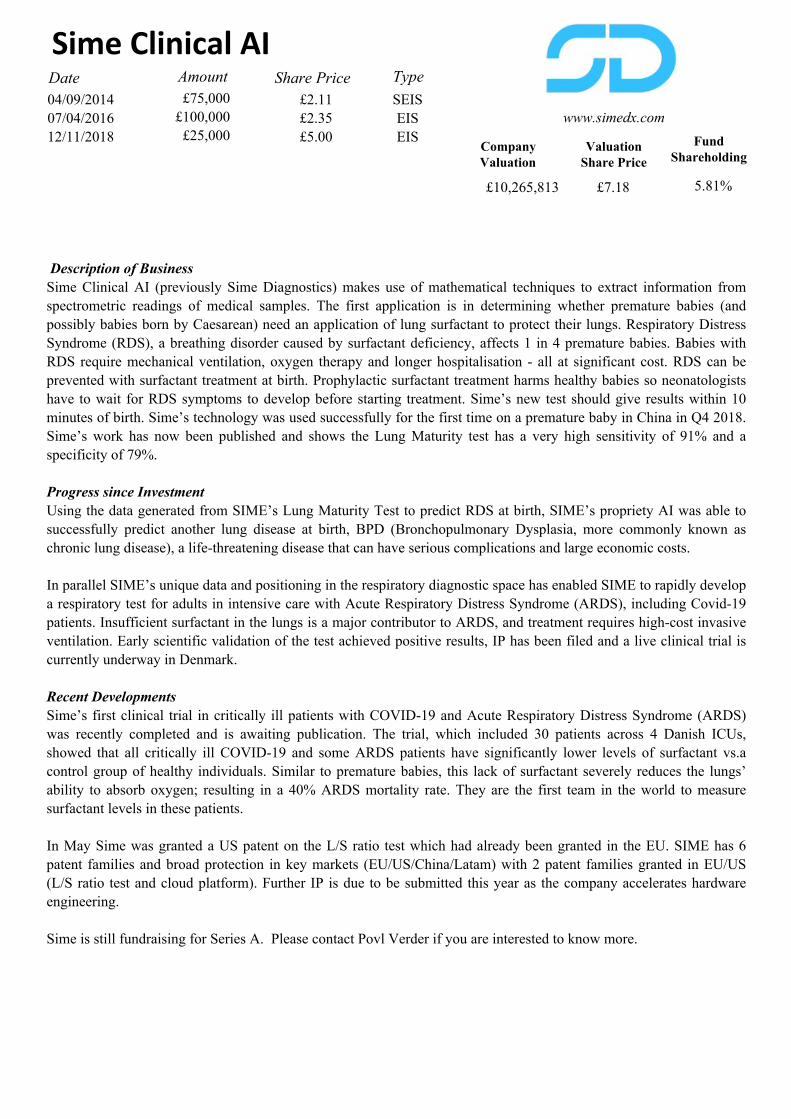

£75,000£100,000£25,000

SEISEISEIS

04/09/201407/04/201612/11/2018

5.81%

FundShareholding

Date Amount TypeShare Price£2.11£2.35£5.00

Description of BusinessSime Clinical AI (previously Sime Diagnostics) makes use of mathematical techniques to extract information fromspectrometric readings of medical samples. The first application is in determining whether premature babies (andpossibly babies born by Caesarean) need an application of lung surfactant to protect their lungs. Respiratory DistressSyndrome (RDS), a breathing disorder caused by surfactant deficiency, affects 1 in 4 premature babies. Babies withRDS require mechanical ventilation, oxygen therapy and longer hospitalisation - all at significant cost. RDS can beprevented with surfactant treatment at birth. Prophylactic surfactant treatment harms healthy babies so neonatologistshave to wait for RDS symptoms to develop before starting treatment. Sime’s new test should give results within 10minutes of birth. Sime’s technology was used successfully for the first time on a premature baby in China in Q4 2018.Sime’s work has now been published and shows the Lung Maturity test has a very high sensitivity of 91% and aspecificity of 79%.

Progress since InvestmentUsing the data generated from SIME’s Lung Maturity Test to predict RDS at birth, SIME’s propriety AI was able tosuccessfully predict another lung disease at birth, BPD (Bronchopulmonary Dysplasia, more commonly known aschronic lung disease), a life-threatening disease that can have serious complications and large economic costs.

In parallel SIME’s unique data and positioning in the respiratory diagnostic space has enabled SIME to rapidly developa respiratory test for adults in intensive care with Acute Respiratory Distress Syndrome (ARDS), including Covid-19patients. Insufficient surfactant in the lungs is a major contributor to ARDS, and treatment requires high-cost invasiveventilation. Early scientific validation of the test achieved positive results, IP has been filed and a live clinical trial iscurrently underway in Denmark.

Recent DevelopmentsSime’s first clinical trial in critically ill patients with COVID-19 and Acute Respiratory Distress Syndrome (ARDS)was recently completed and is awaiting publication. The trial, which included 30 patients across 4 Danish ICUs,showed that all critically ill COVID-19 and some ARDS patients have significantly lower levels of surfactant vs.acontrol group of healthy individuals. Similar to premature babies, this lack of surfactant severely reduces the lungs’ability to absorb oxygen; resulting in a 40% ARDS mortality rate. They are the first team in the world to measuresurfactant levels in these patients.

In May Sime was granted a US patent on the L/S ratio test which had already been granted in the EU. SIME has 6patent families and broad protection in key markets (EU/US/China/Latam) with 2 patent families granted in EU/US(L/S ratio test and cloud platform). Further IP is due to be submitted this year as the company accelerates hardwareengineering.

Sime is still fundraising for Series A. Please contact Povl Verder if you are interested to know more.

£7.18

ValuationShare Price

£10,265,813

CompanyValuation

www.simedx.com

Sime Clinical AI

£75,000£17,131£3,000

£13,000£31,000£29,300

SEISEISEISEISEISEIS

23/12/201409/02/201704/12/201728/08/201829/03/201925/03/2020 12.41%

FundShareholding

Date Amount TypeShare Price£0.005£0.060£0.160£0.10£0.10£0.10

Description of BusinessExpend saves businesses time, money and effort by consolidating management, payment and accounting tools into ahighly autonomous platform. Expend is a feature-rich, award-winning platform that assists the management ofcompany expenses and spending. The automated, innovative expense management suite includes optional paymentcards, receipt and invoice management, mileage tracking, spend approvals and expense reimbursements. Expend keepsbusinesses efficient by simplifying the process for finance professionals and employees alike. Expend gives control,visibility and accountability over company spending. Everything is filed neatly into the company’s accounting software- regardless of the type of payment. Expend is growing well and has a hybrid revenue model bringing income from amonthly SaaS subscription as well as from payment interchange and fees, much like a bank.

Progress since InvestmentSince the initial investment, Expend has worked hard to develop its software and business model and has developed astrong customer following, won awards for its technology, and built a solid reputation in the accounting and fintechspace in the UK.

Growth has been steady over the last couple of years and has accelerated significantly in 2020. Expend is now trustedby an increasing number of companies across various sectors, including Bumble, AgeUK, Capitalise, Côte Restaurantsand more. The platform supports companies of many sizes, from one to 500+ employees. Feedback from customers hasbeen very good.

Expend has developed its commercial offering since launch and now benefits from a hybrid, multi-revenue model.Like a typical SaaS business, Expend enjoys monthly recurring revenue from subscriptions and also generates incomewhen people use its payment products and cards like a bank (for example through payment interchange when a card isused, and fees for items like foreign exchange transactions).

Recent DevelopmentsExpend has continued to make steady progress with revenues more than doubling since the start of the pandemic.Towards the end of Q2, Expend closed its fundraising round, having raised more than £900,000 at 15p per share, fromits existing investors and Seedrs.

The monthly burn rate has now fallen to below £25,000 per month and continues to fall each month as revenues rise.But Expend is actively seeking to hire a CTO whose major task will be to oversee the development programme. Thereis a constant need to refine and improve the software and to add new features. There are now three customers withabout 100 users each and a total of more than 8000 users. Enquiries from potential large users are now being receivedfrom all over the world at an increasing rate.

In summary, Expend is doing well and continues to have the potential to take off in a much bigger way.

£0.15

ValuationShare Price

£19,382,132

CompanyValuation

www.expend.io

Expend

£75,000£75,000£20,000£52,000£20,000

SEISEISEISEISEIS

21/04/201502/02/201624/03/201614/09/201622/09/2017

4.97%

FundShareholding

Date Amount TypeShare Price£0.60£0.80£0.80£0.97£2.00

Description of BusinessMolecular Warehouse (MW) has technology to rapidly develop and test new proteins for diagnostic and therapeuticuses. MW has developed a new type of sensor for diagnostics which yields new quantitative devices. The devices takea small drop of fluid and give a numeric readout in seconds without any additional operations (like a blood glucosesensor but for almost any physiological analyte).

The key technology is an enzyme with a hinge which we call a biosensor. When the hinge is open the enzyme doesn’twork and no signal is produced. When the molecule of interest is present, the enzyme is pulled into shape and theenzyme can function happily and produces a signal that is easily read.

These biosensors can be used for many applications where it is useful to know how much of a molecule is present. Onearea is therapeutic drug monitoring. There are several drugs where it is important that a patient has neither too little nortoo much drug in their system, so patients need to be monitored until the dosing is accurately determined. MW willallow patients to measure this themselves with high accuracy and communicate back to the doctors. Its first productsare aimed at the transplant market and will allow accurate monitoring of drug levels outside a hospital environment.

For the development of new sensors, MW makes use of the services of the Queensland University of TechnologyBrisbane where a large number of proprietary and commercial tools are brought together in one location allowing veryrapid development of new products or leads.

Progress since InvestmentThe company has developed a sensor for calcium which may have applications in monitoring kidney disease andhyperparathyroidism. The sensor demonstrates the functionality of the whole system of biosensor, reader and software.It is not however a sensor which is likely to be commercially successful.

MW had also been developing enzyme cascade based sensors for Theophylline (used in therapy for respiratorydiseases) and Lithium (for treating bipolar disorder). MW divided into two entities in May 2020: Luas Diagnostics haslicensed IP from MW and will develop the enzyme cascade based sensors. MW has a minority stake in Luas, whichhas now also become the distributor of a 20 minute Covid antibody test and a Covid antigen test. The lab in Guildfordwas closed and Andrea has taken on the role of caretaker, while Kirill Alexandrov is developing new technology forMW in the lab in Brisbane.

Recent DevelopmentsThe technical performance of the Molecular Warehouse biosensors has improved again. Some of the key parameterswhich matter for a sensor are: the dynamic range (the difference between the signal generated at full scale relative tothe noise level), the speed of a sensor (how long the sensor takes to make a reading), the stability of a sensor (how wellit stands up to temperature and storage time). Kirill’s team has made great progress on all of these, which has led toone of the embodiments of the sensor being tested in a client application for which it wasn’t fast enough last year.

Molecular Warehouse needs to fundraise in order to keep making this kind of progress and will be doing so soon.

£0.50

ValuationShare Price

£3,095,712

CompanyValuation

www.MWdiagnostics.com

Molecular Warehouse

£75,000£35,220£3,000

£14,400

SEISEISEISEIS

29/06/201527/11/201730/07/201830/03/2020

1.30%

FundShareholding

Date Amount TypeShare Price£0.14£0.36£0.97£0.97

Description of BusinessAnimal Dynamics is a spin-out company from Oxford University. It was founded by Dr Adrian Thomas, Professor ofBiomechanics in the Animal Flight research group in Zoology, and Alex Caccia, an entrepreneur with start-upexperience in media, technology and manufacturing and a background in finance. Adrian is an expert on how animals -birds, fish and insects - move through water and air and on land. Unsurprisingly, over millions of years, they haveevolved very efficient means of doing this. Animal Dynamics aims to adapt the techniques and structures used byanimals to create more efficient and effective means of flying and moving through water and over land.

Progress since InvestmentAnimal Dynamics has three vehicle development programmes:

1 . Stork: A system for delivering packages to front-line troops. The system could also be used to provide disasterrelief in areas where roads no longer exist. In Q4 2017, Animal Dynamics won a contract against 100 bidders todevelop this system, and has subsequently delivered the first production units. This is now the company’s lead productwith full-scale production of the STM (135 kg payload, 180 km range, autonomous) planned for 2023.

2. Skeeter: A micro drone like a dragonfly. The Company successfully delivered the Skeeter project to Dstl inApril, and achieved the target flight time and wind tolerance. This is a world class technical achievement, and has builtunique skills in air vehicle control systems. The Skeeter nano-UAS project is on hold whilst the company focuses onStork. During the year, the Skeeter R&D team also explored a larger propeller aircraft, after winning a DASA grant tobuild a highly gust tolerant mid-sized UAS called Shearwater. This project was also delivered successfully, and is onhold while focus shifts to Stork.

3. Malolo: Two underwater R&D projects were successfully completed in 2019, exploring the potential ofunderwater autonomous systems using flapping propulsion. The first was a navigation system using the Earth'smagnetic field to aid navigation, and achieved useful resolution on both latitude and longitude; the second is RayDrive,which is an underwater vehicle based on the configuration of manta rays. The prototype vehicle delivers highefficiency, low noise signature and moves well. But this programme too, is on hold.

In July 2018, Animal Dynamics raised £6m at 97p per share. The round was very oversubscribed and 50% of theSEIS shareholders took the opportunity to exit at this price (14x the initial after tax share price.) The others opted tostay for the ride.

Recent DevelopmentsThe Company is progressing well with the development of STM (135Kg payload), and the ground test vehicle has beencompleted during Q2 , with the flying test of first prototype X1 vehicle due to go into trials in Q3. In addition, asanticipated, the UK MOD’s trials programme - known as Project Theseus - has been announced, and the Company hasbeen preparing bid responses. There has been continued interest in the smaller ST25 Vehicle, which is now in service.All engineering development is now being done with a view to shipping a fully certified aviation product, which meansthat each system and sub system needs extensive design, documentation and testing, under inspection from the aviationauthorities, and the hard work putting this in place is paying off with stellar reports being received on safety-criticalprocesses.

£0.97

ValuationShare Price

£29,844,844

CompanyValuation

www.animal-dynamics.com

Animal Dynamics

£50,000£30,000

£160,275£45,000£53,820

SEISSEISEISEISEIS

13/07/201514/12/201530/03/201729/03/201813/03/2019

16.92%

FundShareholding

Date Amount TypeShare Price£0.14£0.18£0.36£0.40£0.70

Description of BusinessCD200 is a protein that modulates the activity of mature immune cells. It protects certain tissues in the body such asmuscles and nerve tissue from the immune cells. People who have low levels of the CD200 receptor on their immunecells are at higher risk of autoimmune diseases. The herpes virus is able to survive in the human body by producing aprotein very similar to CD200 – a viral homologue.

CD200 acts on both the innate and adaptive arms of the immune system but does not impair the function of immatureimmune cells so response to infections is not affected, making it an attractive target. Other groups have carried outresearch on naturally occurring CD200 and its homologues. They are effective but not practical, because they wouldrequire very frequent injections. By modifying CD200, Ducentis is seeking to turn it into a practical treatment. Thereare many autoimmune diseases that might benefit from such a treatment, including arthritis.

Progress since InvestmentDucentis has made excellent progress since the investment. It first designed and then made a modified CD200 proteinwhich requires between 1/100 and 1/1000 of the wild type CD200 to produce the same binding effect. Ducentis hasapplied for a patent on this molecule. An injection of this molecule might then be a treatment for Rheumatoid Arthritisand other autoimmune diseases. Two large pharma companies responded very quickly, signed NDAs and entered intodiscussions with Ducentis. But they would like to see more data before signing a deal. Ducentis has developed a rangeof new molecules all closely related to CD200, but with varying and much higher levels of affinity. This will enableDucentis or its partners to fine tune their therapies as they progress through the pre-clinical and clinical programmes.Ducentis has raised a round of >£1.5m to continue its development programme. The cornerstone investor was LifeArc.One major pharma company, Eli Lilly, has announced a programme in CD200: we see this as a positive developmentas it shows it is a target of interest, while the applications are broad enough that there will be room for several winners.

Recent DevelopmentsDucentis has had excellent results in the lab, with clear results in several pre-clinical models. Results from competitorshave helped narrow down the choices with regards to the most likely clinical indications. This is very helpful, asCD200 acts on several pathways in parallel and the broad range of activity makes it tricky to accurately predict the bestindications.

£0.70

ValuationShare Price

£4,794,346

CompanyValuation

www.ducentisbio.com

Ducentis Biotherapeutics

£80,000£40,000£16,200£29,000£90,000£4,636

£36,800£69,810

SEISSEISEISEISEISEISEISEIS

13/08/201508/03/201607/07/201712/10/201729/03/201919/12/201925/03/202031/03/2021

25.61%

FundShareholding

Date Amount TypeShare Price£0.60£1.00£1.00£1.20£1.80£2.80£2.80£4.00

Description of BusinessBioarchitech aims to improve cancer treatment by creating a virus which is targeted to a tumour cell. Once inside thetumour cell, the virus produces a second virus which then kills the tunour cell and produces molecules whichencourage the immune system to finish the task. This type of potent immunotherapy is being developed to stimulate apatient’s own immune system into destroying an otherwise incurable disease.

The CEO is Dr Geoff Hale who has an international reputation in therapeutic immunology. As a scientist, he haspublished over 300 articles on the mechanisms of action of antibodies. He was formerly head of the TherapeuticAntibody Centre at Oxford University, and was the founder and CEO of BioAnaLab Ltd, a successful spin-out fromOxford which grew from nothing to c 50 people. Kevin Maskell is the principal researcher and developed the ideatogether with LiLi Wang and Hannah Chen. From 2002 -2009, Kevin was a research assistant in the department ofclinical pharmacology at Oxford University, then principal scientific director of DDS, a subsidiary of Merck Millipore.Before starting Bioarchitech, he was a senior scientist at Oxford Cancer Biomarkers.

Progress since InvestmentBioarchitech has been inserting the instructions for different types of therapeutic proteins into the DNA of a vaccinestrain of vaccinia virus and has produced therapeutic levels of these proteins from cancer cells. Bioarchitech hasdeveloped several therapeutic proteins including bispecific T cell engager (BiTE), an immune activator that binds totissue surrounding a tumour and checkpoint inhibitors to two immune cell receptors. These technologies are nowworking in vitro. There is a video which shows breast cancer incubated with BiTE protein being killed by T cells overa four-day period, while in the control with no BiTE protein, cancer proliferates. As the virus replicates andmanufactures the therapy within tumours this is a potential cure for cancer with a single treatment.

Recent DevelopmentsIn early March 21, Kevin Maskell gave a Zoom presentation to Oxford Technology investors. By the end of March,more than £1m had been raised including £400,000 from Geoff Hale. This will enable Bioarchitech to demonstrate itstechnology in vivo over the next 18 months. Various large pharma companies have expressed interest already but haveall said that they wish to see in vivo data before committing to bring this treatment to clinical trials.

Conversations are now going on with two potential partners, one in the US and another in Holland.

£4.00

ValuationShare Price

£4,607,616

CompanyValuation

www.bioarchitech.com

Bioarchitech

£100,000£38,245

SEISEIS

27/11/201507/07/2017

1.42%

FundShareholding

Date Amount TypeShare Price£0.73£0.81

Description of BusinessPeptides are short chains of amino acids (the building blocks of proteins). They are an increasingly popular class ofpharmaceuticals, sitting in between conventional small molecules and biologics such as antibodies and proteins. Theycan be made chemically like small molecules, but can be very specific like the biologics.

The founders are Prof Graham Ogg and Prof Terence Rabbitts FRS. The technology behind Orbit comes from OxfordUniversity's Weatherall Institute of Molecular Medicine. It enables the rapid selection of peptides that bind ontopotential drug targets and do not show unintended binding. The approach consists of creating millions of micron-sizedbeads each with a unique peptide and mixing them with the target molecule. The beads that bind can then be identifiedand larger quantities produced. If necessary, new beads can be made which are similar to those that bind best - anevolutionary approach. A particular capability which Orbit has is to be able to screen agonist peptides at very highthroughput, that is peptides that switch cell activities on. These are more difficult to find than peptides that blockactivity which often just have to bind on and get in the way of another molecule binding.

The company will partner with large pharmaceutical companies wishing to develop new peptide drugs but will alsodevelop its own portfolio. It is hoped the technology works rapidly enough to enable tens of drug discoveryprogrammes to be run each year.

Progress since InvestmentOrbit has now developed a way to select peptides that bind to targets in solution, as opposed to only on surfaces andhas its first customers. Orbit completed a funding round of £5.25m in May 2018. Now at the Oxford Science Park, theteam expanded to 29 employees. Due to different interests among the major shareholders Orbit split into twocompanies. One company will focus on T Cells , and will be called T-Cypher. Shareholders of Orbit will have thebeneficial ownership of 1/9th of a share in T-Cypher for every share they currently hold in Orbit. T-Cypher currentlyhas 12,401,540 fully diluted shares.

Recent DevelopmentsOrbit’s technical progress has been very good, the delays it had experienced due to COVID have now mostly beenovercome. Their high throughput screening is working ever more smoothly and the number of peptides which can bescreened in one go is increasing and will be in the millions. Once that has been achieved Orbit will be able to startmarketing its services again.

SummaryOrbit is now concentrating on completing the whole development chain so that new peptides that are active on difficultdrug targets, can be identified and developed more quickly and effectively than by any other process. The process ofscreening for hits is now running smoothly, and has now been extended to include finding agonist peptides. Whilerefining its external service proposition Orbit has been progressing its internal drug development, both as a way ofimproving the technology and as a way of generating future value.

£0.81

ValuationShare Price

£10,552,682

CompanyValuation

www.orbitdiscovery.com

Orbit Discovery

£75,000£25,950£20,000£20,000£20,000£20,000£30,000

£102,000£4,300

SEISSEISSEISEISEISEISEISEISEIS

07/03/201619/05/201615/07/201616/07/201628/10/201608/11/201611/05/201727/03/201929/03/2019

20.76%

FundShareholding

Date Amount TypeShare Price£0.63£0.63£0.63£0.63£0.31£0.31£0.31£0.31£0.31

Description of BusinessDr Jeff Moore established Curileum Discovery in labs adjacent to St Mark’s Hospital in London, one of the fewhospitals in the world that specialises entirely in treating serious gastrointestinal diseases. Curileum aims to discoverdrugs to intervene early with treatments to prevent disease progression in colorectal cancer and inflammatory boweldisease. The company generates “mini-gut” organoids from patient and healthy gut mucosa to discover andcharacterise drug candidates before testing in preclinical in vivo models. These gut organoids are microscopic three-dimensional cellular structures that mimic the structural and functional properties of the mucosal layer of the gut.From these studies, two of the novel drug candidates that the company discovered are in preclinical development forlicensing to pharmaceutical companies.

Progress since InvestmentCurileum has made excellent progress with its science and now has four main programmes running:• PLE015 - a novel small molecule drug candidate isolated from a Traditional Chinese Medicine plant extract to reducethe formation of colorectal polyps, the first stage of bowel cancer.• Regenerative stem cell therapy for Crohn’s fistulising - discovered a previously uncharacterised stem cell thatremodels and fills in fistulas in an in vivo animal model.• CSR1 - a soluble molecule which is present in inflamed guts and that causes stem cells to convert to mast cells,causing excessive inflammation instead of producing ordinary mucosal cells. Curileum has also found a substance thatwill block the action of CSR1.• CryptDx - a diagnostic platform in development to detect development of colorectal cancer at the disease initiationstage for early therapeutic intervention.

During Q4 20, Curileum raised £282,575 in EIS investment, mostly from existing investors.

Recent DevelopmentsCurileum still has the four programmes running, but the rest of this report will focus on two of them.

PLE015. In vivo preclinical testing of the purified small molecule drug will finally begin on 28th June after themany months of disruption caused by Covid lockdowns. The studies are designed to confirm the reduction of polypformation observed with the crude plant extract and also test if PLE015 can reverse polyp progression to cancer.Results from these studies at the end of the summer will be added to a composition of matter patent application,completing pharmaceutical companies’ checklist for engaging in licensing discussions.

Stem cell therapy candidate for healing of fistulas. Perianal fistulas is an incurable and debilitating condition thataffects up to 40% of all patients with Crohn's disease and has a frequency of 1:10,000 in the general population.Currently, no treatments effectively seal a cleaned fistula. Instead, a cell therapy to reduce inflammation, that Takedarecently acquired for $600m, only extends periods between cleanings.

Curileum has discovered an adult stem cell that has the capacity to produce a wide range of cell types in the culturedish. Curileum has tested the regenerative capacity in an in vivo preclinical fistula model. Three months aftertreatment, the fistula tract was remodelled and nearly filled in with healthy cells. Curileum has filed a patentapplication on this promising therapy, allowing the company to start licensing discussions with pharmaceuticalcompanies during Q3.

£1.00

ValuationShare Price

£3,884,675

CompanyValuation

www.curileum.com

Curileum Discovery

£37,500£62,500£25,000

SEISEISEIS

01/04/201620/10/201613/09/2017

4.42%

FundShareholding

Date Amount TypeShare Price£1.00£1.00£1.00

Description of BusinessSpendology was founded by three entrepreneurs from software, foreign exchange and personal finance backgrounds.The business provides a white label solution for the travel industry which allows tour operators, airlines and travelagents to offer a mail order travel cash add-on service to their holiday customers. Last year, British travellersexchanged £27bn in cash here in the UK before they travelled, with 22% using a supermarket, 21% the Post Office and14% their travel agent. With 83% of travel customers buying currency, Spendology Cloud allows the travel industry toincrease turnover, boost profits and enhance customer retention. Spendology Cloud is the only solution which providespayments, order management, compliance, wholesale notes, pick and pack and customer support, all via white labeland no upfront cost.

Summer 2021Mintel recently launched its annual Travel Money report and found that despite the prevalence of card use in the UKduring the pandemic, over two-thirds of Brits intending to travel this year are planning to take cash with them. Mintelalso predicts a full recovery and in fact an increase in pre-pandemic spend levels on travel cash within 5 years.Predicted card growth is modest compared with domestic growth, with credit cards rising from 43% to 49%, debitcards from 43% to 47% and prepaid cards from 15% to 17%. It looks like cash will remain king for overseas travel formany years to come despite the pandemic.

Overseas travel in Summer 2021 looks like being highly challenging, with the complexities of our traffic light system,the determination of some EU member states to quarantine Brits on arrival, differing rules on vaccines and testing, andof course the unknowns of infection rates, vaccination rates, and variants of concern all to come. However, there is atrickle of business at this early stage - £125k last month and £250k likely this month - and this should increase astraffic to the additional green destinations rises.

The FutureSpendology has kept overheads low throughout the pandemic and raised £660k to provide working capital as thebusiness grows to be self-financing. With low burn rates and furlough support, the business now has sufficient capitalto last through to Summer 2022 with minimal revenues. The company has taken the opportunity to invest in someadditional product development, introducing "agent-led orders" so that individual travel agents can more pro-activelysell travel cash over-the-phone and face-to-face to customers before they depart. In Q3 the company will launch ‘Click& Collect’ for clients with physical branches, both for customers ordering via the website and mobile app, and foragent-led orders. It will also be launching ‘Post Office Collect’ - allowing clients without branches to offer physicalcollection from 12,500 Post Office and Royal Mail Delivery Offices. Spendology is confident that its platform will behighly attractive to travel companies desperately seeking incremental revenues and expects a surge of interest onceholiday travel resumes.

£0.36

ValuationShare Price

£1,018,977

CompanyValuation

www.spendology.com

Spendology

£50,000£65,000£18,656£30,000£28,000

£102,000£32,100£55,655

SEISEISEISEISEISEISEISEIS

05/04/201623/08/201607/03/201729/03/201702/01/201818/03/201925/03/202024/03/2021

13.46%

FundShareholding

Date Amount TypeShare Price£0.12£0.19£0.19£0.19£0.26£0.35£0.35£0.42

Description of BusinessDoctors make use of long needles for taking biopsies or making deep injections, but the needles are difficult to see onultrasound, and long thin needles often deflect and do not end up exactly where intended. Active Needle Technologyprovides minute longitudinal ultrasound movement to the needle. This results in the needle being very bright on theultrasound (from all directions) and much less deflection. The ultrasound drive also has an additional benefit in that theamount of force required to insert the needle is much reduced. In early studies, this has been shown to result in lesspain upon insertion and less risk of overshoot.

The technology was originally invented and initially developed by Dr Muhammad Sadiq at Dundee University. Thecompany is being led by Ian Quirk who has been a design, regulatory and clinical development specialist in medicaldevices for over 25 years, most recently at Lightpoint Medical.

ANT has identified biopsy needles as a market where all the advantages of the Active Needle come to bear, while theextra cost of the ultrasound driver will only have a small impact on the gross margin. The alternative products (withoutANT’s advantages) cost ~$200.

Additional applications have emerged for ANT. One is a low pain, low trauma ultrasonic tattoo system (Trademarkedas TranQuill), which has a $3bn a year addressable market. The second is pre-clinical injection system (PRECIS),aimed at blue chip pharma companies drug and vaccine safety screening studies. ANT is working with Astra Zenecaand GlaxoSmithKline in the design and commercialisation of these specialised, high precision needles. Importantly,this project was proposed by AZ and GSK – so that they are set to become the first customers.

Progress this QuarterIn May, the company reached a significant milestone with the award of a CE mark for its initial medical product: thehigh visibility biopsy device. This landmark achievement allows Active Needle to market the device in the EU, EEA,and with minor registration, the UK. The company will require additional funds to progress this phase of scale up, aprocess which is ongoing.

In tattooing the company is in the preparative phase for a grant worth c. £220k from Innovate UK to completedevelopment and achieve scale up for launch. This project is expected to start in July.

Active Needle continues its relationship with AstraZeneca (AZ) and GlaxoSmithKline (GSK), who have testedadvanced prototypes and have provided very encouraging feedback. Following completion of this testing phase, due toend this month, the next step is to discuss orders and contracts to supply.

To help support all these developments, Active Needle still has some shares available from its recent round at 42p pershare

£0.42

ValuationShare Price

£5,043,225

CompanyValuation

www.activeneedle.com

Active Needle Technology

£100,000 SEIS29/04/2016

1.46%

FundShareholding

Date Amount TypeShare Price£20.00

Description of BusinessOxford Nanoimaging is a spin out from the biological physics lab of Prof Achillefs Kapanidis at Oxford University. Itspecialises in super resolution microscopy, which refers to being able to resolve dimensions smaller than thewavelength of light. Prof Kapanidis, Robert Crawford and Bo Jing have invented an optical assembly which allows amicroscope to be shrunk from the size of a small car to the footprint of a tablet (with a PC sized box under the bench).This not only gives a big advantage in crowded and expensive laboratories, it also does away with many of theadjustments and control requirements of other super resolution microscopes, making it suitable for beginners andexperts. With the microscope, it has been possible to image the processes of DNA repair in a cell. The expertise in thecompany is not only in the device, but also in the molecular biology techniques and the image processing. A bit like asmart phone, we expect there will be advances both in the hardware and in the applications that can run on it. Thecompany is aiming for rapid expansion, with a distribution network being developed around the world. The companyalso has the backing of Oxford University Innovation and Oxford Science Innovation.

Progress since InvestmentGood initial progress was made with sales of nanoimagers exceeding expectations. In March 2017, the company raised£3m at £62.50 per share compared to the initial price of £20 per share to accelerate the rate of growth. In Q2 2018, thecompany raised $25m at £173.40 per share. The money came from existing shareholders, and from new shareholdersfrom New York, China, Singapore and London.

Recent DevelopmentsONI is making encouraging progress with sales rising steadily.

Sales 2019 2020Q1 £ 0.8m £0.5mQ2 £ 1.5m £0.9mQ3 £ 1.6m £2.0mQ4 £ 2.3m £3.7m

ONI has developed an ‘EV kit’. This consists of a flow chip, a reagent cartridge and a data analysis package, andenables researchers to characterise EVs - Extracellular Vesicles. It provides fully automatic end-to-end workflow.ONI recently received the first major order for 500 kits at $448 each.

ONI’s CODI platform - a cloud based platform for Collaborative Discovery has now been deployed to 31customers. The plan is to bundle CODI into the annual system licence fee. Progress has apparently been made onvirus detection but details are confidential.

ONI has opened an office in San Diego and will be moving headquarters to this location. The cash balance at theend of Q4 was $9.1m, $3.3m ahead of plan.

The number of publications making use of ONI’s Nanoimager are increasing steadily with 25 of the 63publications appearing in Google scholar having been published in 2021.

£173.40

ValuationShare Price

£59,353,433

CompanyValuation

www.oxfordni.com

Oxford Nanoimaging

£75,000£9,500

£48,554£90,000£26,020

SEISEISEISEISEIS

19/05/201621/10/201630/11/201701/02/201924/03/2021

1.83%

FundShareholding

Date Amount TypeShare Price£14.78£14.78£21.96£31.79£35.64

Description of BusinessEntia was founded by Dr Toby Basey-Fisher and Millie Clive-Smith in 2015. Entia has developed a blood testingtechnology and service to make life-changing health conditions easier to live with by enabling treatment andmanagement to take place in the home.

Entia’s first product measured red blood cells and haemoglobin for anaemia sufferers. Anaemia affects over aquarter of the world’s population (including 4 million people in the UK) but remains difficult to diagnose and monitorowing to a lack of accessible blood tests. With Entia’s technology, anaemia sufferers can receive a blood test in 1minute that used to require a visit to a hospital, which might take weeks to arrange. A pinprick of blood is taken andplaced on a strip which is then fed into the hand-held, battery-powered AptusTM device.

Entia started production and distribution of AptusTM in 2018. This required setting up quality managementsystems and obtaining a CE mark. First sales have been achieved and the product has been very well received. To date,Entia has secured distribution deals worth over £1.3m pa with 9 distributors. However, Entia has stopped pushing theproduct, which doesn’t have connectivity, and is focussing entirely on the home based devices where benefits ofusability and accuracy are the greatest.

Progress Since InvestmentHome monitoring has become the main focus for Entia, with multiple large pharma companies very interested in thebenefits Entia will provide for their patients. The new devices can be connected to the user's mobile phone by wi-fi sothe results are communicated instantly both to the patient and to the doctors in the hospital.

Entia has begun work on Luma, a version of the anaemia testing technology which patients can use in their ownhomes. Entia has won a £1m Innovate UK grant to help develop Luma and is receiving significant UK patient interestto purchase the system.

Entia is currently working on a home monitoring blood test, AffinityTM, for people receiving systemic cancertherapy.

The company now employs 45 people. To date, the company has raised £6.2m through equity financing and £3mfrom government grants. This has allowed it to develop a multi-award winning team, establish world-leading clinicalpartnerships and positively change thousands of lives with its innovative products.

Recent DevelopmentsEntia has raised £8m on a post money valuation of £27m. Their project with the first pharma company is progressingwell. The Development Fund made a small investment in the round. Entia is increasingly focussing on cancer as thebenefits it brings to patients are clear. The trial of Luma with Chronic Kidney Disease patients which had been held upby Covid is now underway.

SummaryFollowing the early market success of AptusTM, Entia has refocused on the home testing devices,Affinity and Luma,and is now focussing increasingly on cancer, where the value of the technology and platform is most easilyappreciated. Entia continues to develop well as a company and its various technology platforms are becoming evermore robust.

£35.64

ValuationShare Price

£22,407,759

CompanyValuation

www.entia.co

Entia

£39,776£60,224£30,000£68,000

SEISEISEISEIS

02/02/201706/02/201705/02/201831/03/2021

6.44%

FundShareholding

Date Amount TypeShare Price£8.00£8.00

£16.00£9.41

Description of BusinessIncreasingly people are receiving their news and entertainment through their mobile devices.Newspaper circulationsare falling, especially among the young. This creates both a problem and an opportunity for news and broadcastorganisations.

Founded in 2017, Covatic’s app sits on a user's phone, and gets to understand the likes and tastes of the user. So itwill know that a user is a Manchester United fan, a fisherman and is interested in butterflies. This information can thenbe used to enable broadcasters to upload clips of Manchester United goals so that they may be played at any time infuture without an internet connection. Information about butterflies and fishing will be uploaded. A user may alsochange his preferences. “Please don't send me stories about Covid.” But, and this is the key point about Covatic, thedetails of the user’s browsing habits etc remain on the phone and are not uploaded.

For the last 20 years, Google and many others have collected as much data about people as they can, (by means ofcookies) and are then able to know their browsing history, where they are and where they travel, and what they buyonline. And this data was then used to target advertising. Both Google and Apple have recently made new releaseswhich allow people to opt out of being tracked by others and 85% of people are now opting out. This is a seismic shiftin the advertising industry. But Google will still be able to track people, even though the precise way in which it mightor might not use this data is contained in the weeds of complicated terms and conditions contracts. And a similarsituation with Apple.

Covatic offers a clean alternative. Covatic will not track anyone’s browsing history and all the data about the usersstays on the phone at all times. But Covatic’s software, contained in the users app (eg Sky, BBC, Bauer, Discoverychannel etc) will know a great deal about the user but without tracking the browsing history at all. So the app can thencategorise a user as a particular type. For example, this user is a female aged 30-40 who lives at a certain postcode andhas two children of 2 and 4, and has a weekly supermarket shopping spend of £50-75 and owns a small car.

The customer, eg Sky Sports, can then use this data to categorise people into several of thousands of categories.For example poor young mothers with children under 1. And it will know that it has 105,000 people in this category.It can then offer the manufacturer of nappies the opportunity to send an ad to all these people. The personal details ofthe the recipients and particularly their browsing history has never left their phone, and is unknown to Sky