Overview of key trends in the global LPG markets CIS and Eastern Europe highlights Saint Petersburg 2012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Overview of key trends in the global LPG markets

CIS and Eastern Europe highlights

Saint Petersburg 2012

The Global and European LPG market

� During the world economic crisis, the LPG market remained stable

� Over the last decade, the world LPG output has been showing a steady growth

� The current outlook for LPG is positive

� According to the World Liquefied Petroleum Gas Association(WLPGA), in 2011 the global LPG output reached 259.6 m tonnes, which is a 5 % increase over 2010 y.o.y.

� United States is the major producer accounting for 50.4 m tonnes, oralmost 20 % of the global output

� The Middle East, in particular, Qatar, Iran and Saudi Arabia produced 65.31 m tonnes of LPG

� Europe produced 25.8 m tonnes

� China produced 21.82 m tonnes

� Africa produced 18.61 m tonnes

� None of the regions saw a reduction in LPG output 2

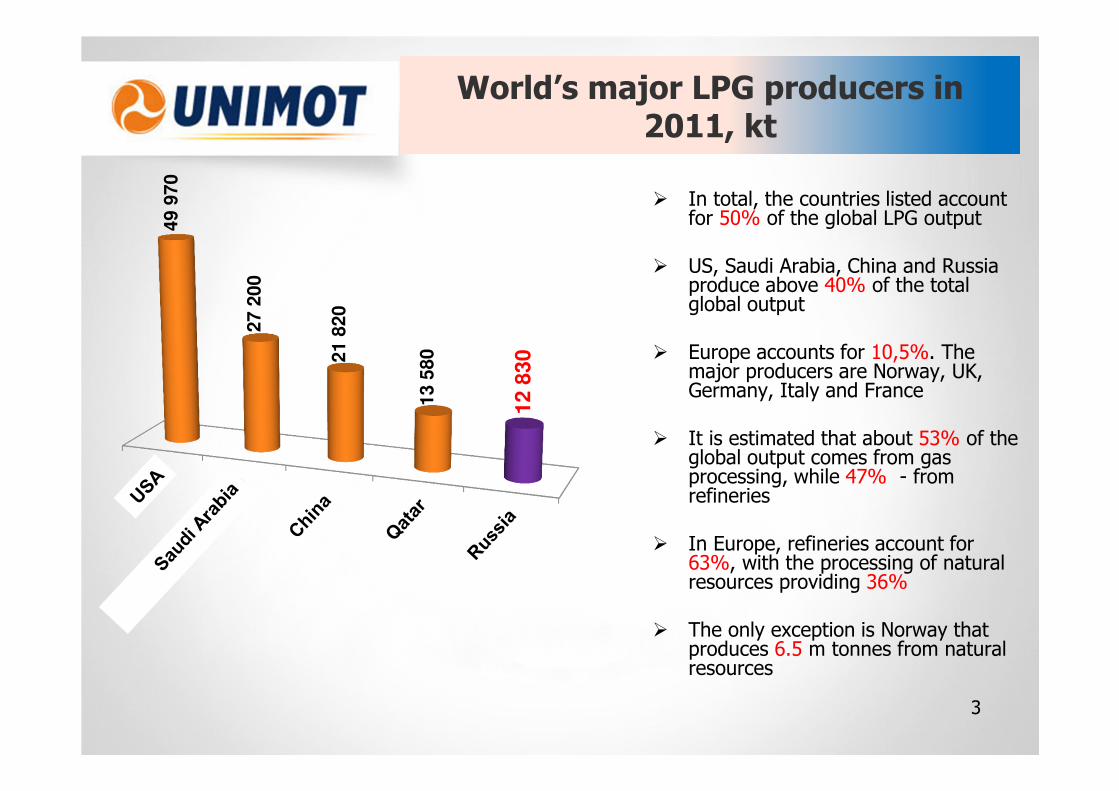

World’s major LPG producers in 2011, kt

3

49 9

70

27 2

00

21 8

20

13 5

80

12

83

0

� In total, the countries listed account for 50% of the global LPG output

� US, Saudi Arabia, China and Russia produce above 40% of the total global output

� Europe accounts for 10,5%. The major producers are Norway, UK, Germany, Italy and France

� It is estimated that about 53% of the global output comes from gas processing, while 47% - from refineries

� In Europe, refineries account for63%, with the processing of natural resources providing 36%

� The only exception is Norway that produces 6.5 m tonnes from natural resources

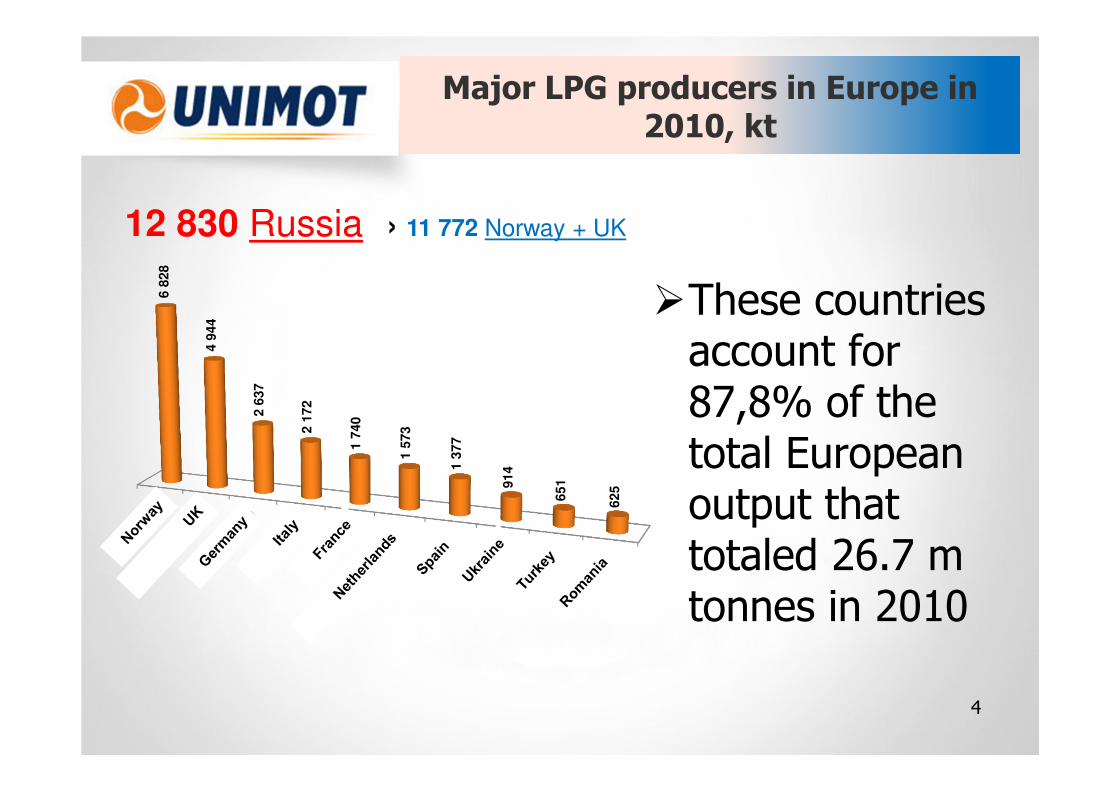

Major LPG producers in Europe in 2010, kt

4

6 8

28

4 9

44

2 6

37

2 1

72

1 7

40

1 5

73

1 3

77

914

651

625

�These countries account for87,8% of the total European output that totaled 26.7 m tonnes in 2010

12 830 Russia › 11 772 Norway + UK

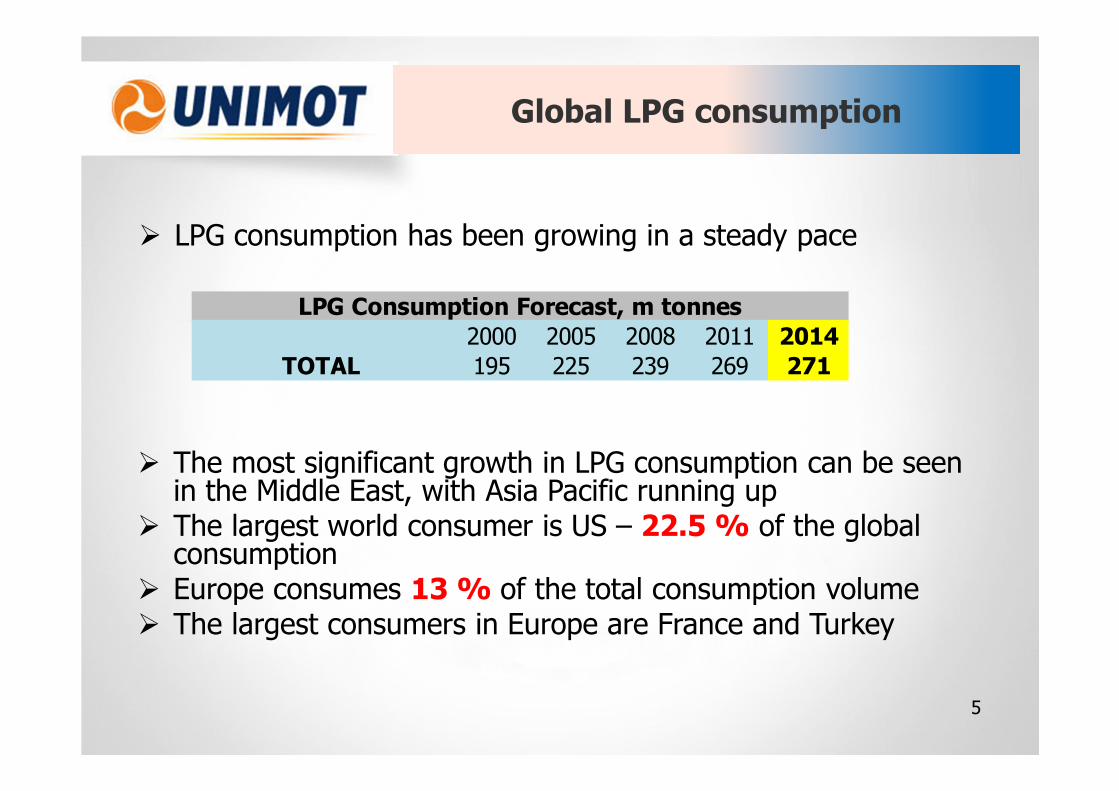

Global LPG consumption

� LPG consumption has been growing in a steady pace

5

� The most significant growth in LPG consumption can be seen in the Middle East, with Asia Pacific running up

� The largest world consumer is US – 22.5 % of the global consumption

� Europe consumes 13 % of the total consumption volume� The largest consumers in Europe are France and Turkey

2000 2005 2008 2011 2014

TOTAL 195 225 239 269 271

LPG Consumption Forecast, m tonnes

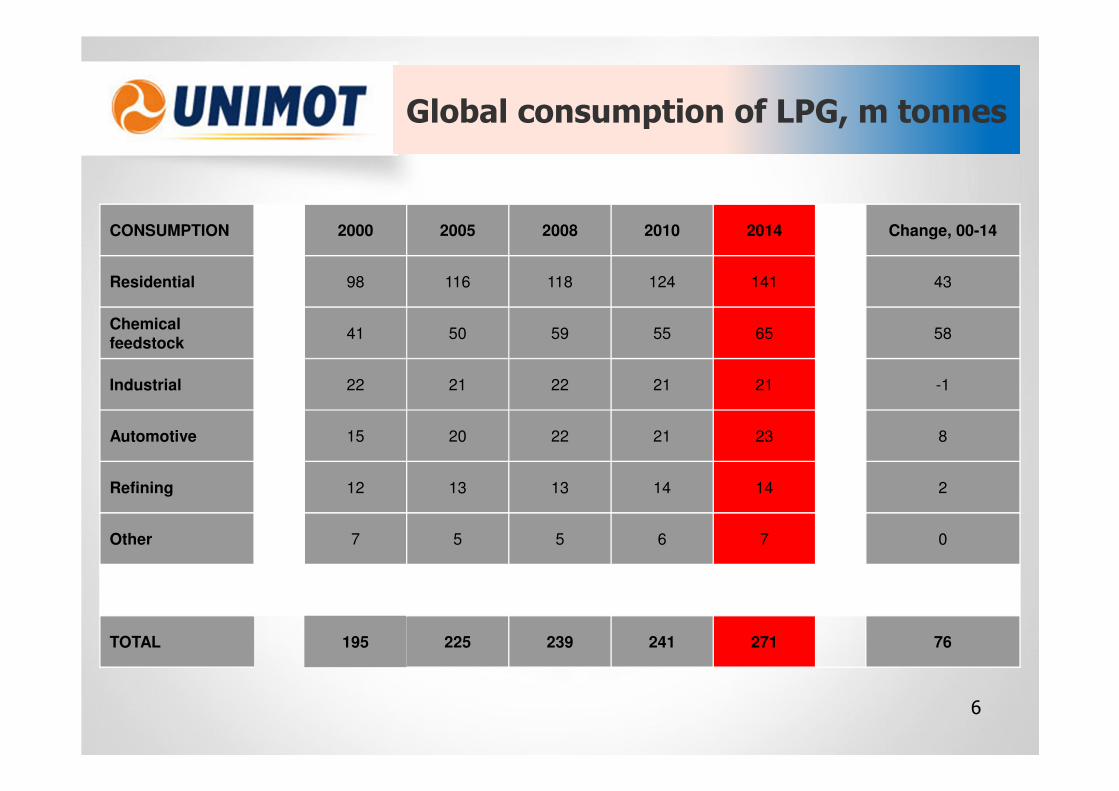

CONSUMPTION 2000 2005 2008 2010 2014 Change, 00-14

Residential 98 116 118 124 141 43

Chemical feedstock

41 50 59 55 65 58

Industrial 22 21 22 21 21 -1

Automotive 15 20 22 21 23 8

Refining 12 13 13 14 14 2

Other 7 5 5 6 7 0

TOTAL 195 225 239 241 271 76

Global consumption of LPG, m tonnes

6

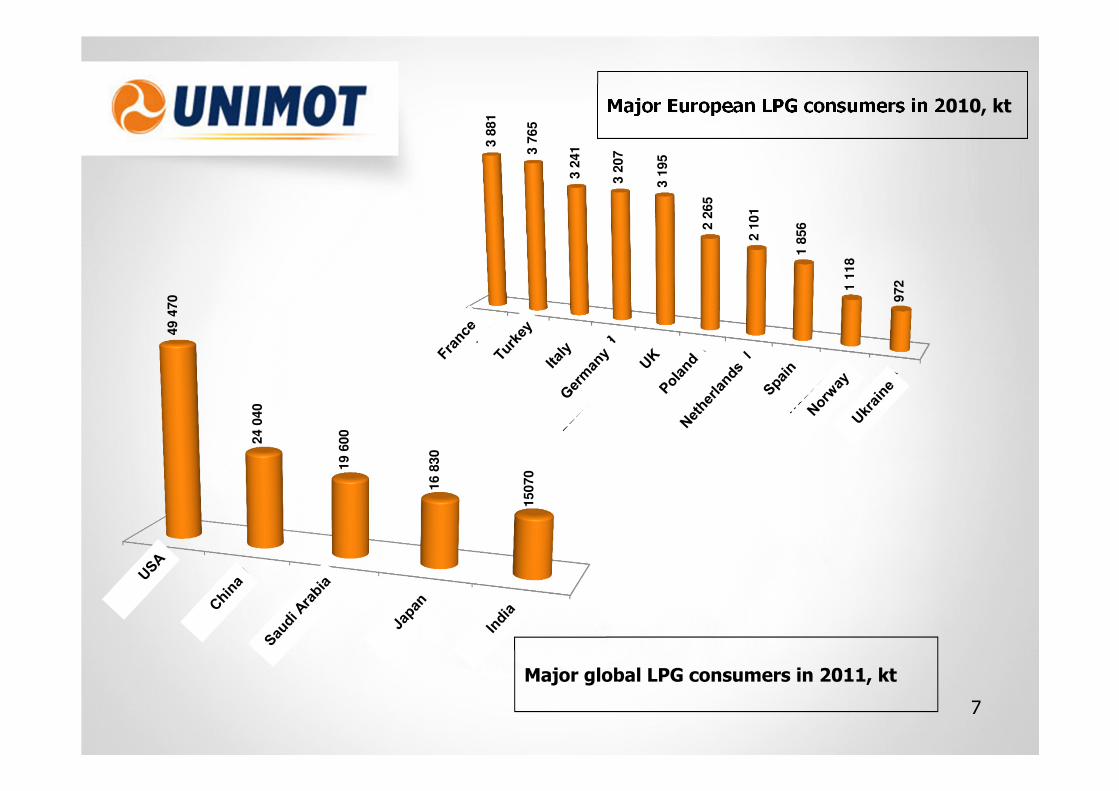

Major global LPG consumers in 2011, kt

49 4

70

24 0

40

19 6

00

16 8

30

15070

Major European LPG consumers in 2010, kt

3 8

81

3 7

65

3 2

41

3 2

07

3 1

95

2 2

65

2 1

01

1 8

56

1 1

18

972

7

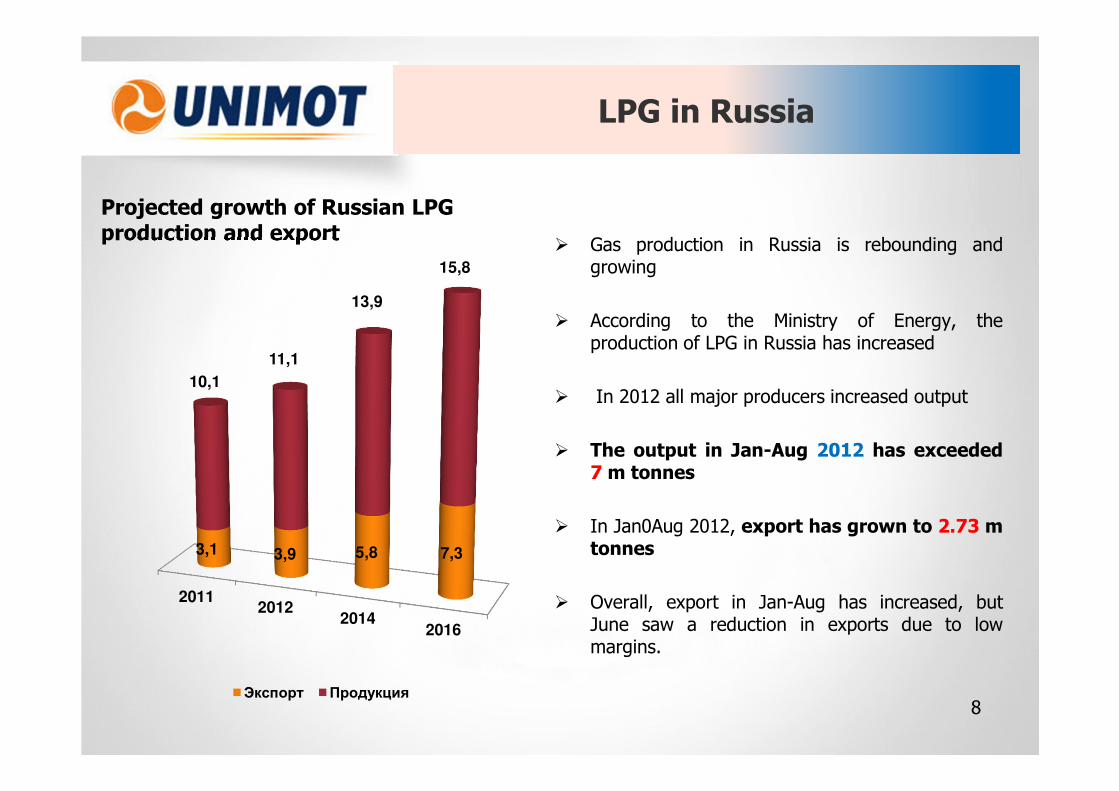

LPG in Russia

� Gas production in Russia is rebounding andgrowing

� According to the Ministry of Energy, theproduction of LPG in Russia has increased

� In 2012 all major producers increased output

� The output in Jan-Aug 2012 has exceeded7 m tonnes

� In Jan0Aug 2012, export has grown to 2.73 mtonnes

� Overall, export in Jan-Aug has increased, butJune saw a reduction in exports due to lowmargins.

Projected growth of Russian LPG production and export

20112012

20142016

3,1 3,9 5,8 7,3

10,1

11,1

13,9

15,8

Экспорт Продукция8

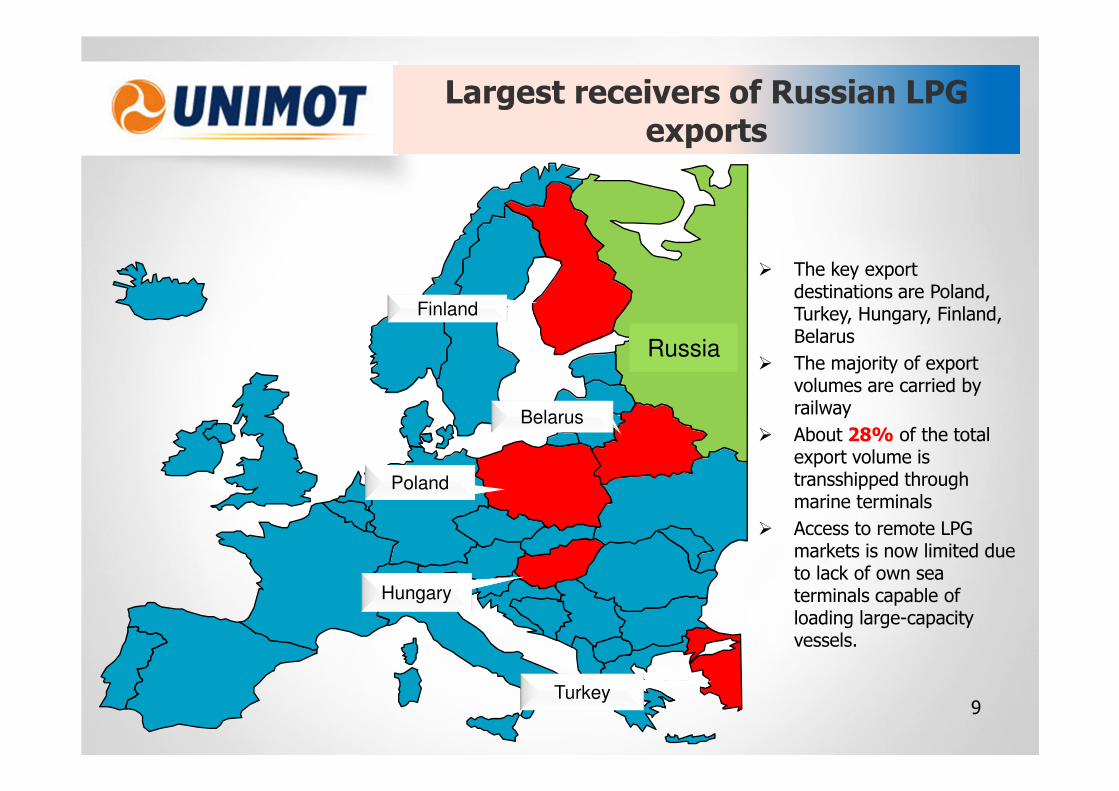

Largest receivers of Russian LPG exports

9

� The key export destinations are Poland, Turkey, Hungary, Finland, Belarus

� The majority of export volumes are carried by railway

� About 28% of the total export volume is transshipped through marine terminals

� Access to remote LPG markets is now limited due to lack of own sea terminals capable of loading large-capacity vessels.

Russia

Hungary

Turkey

Finland

Belarus

Poland

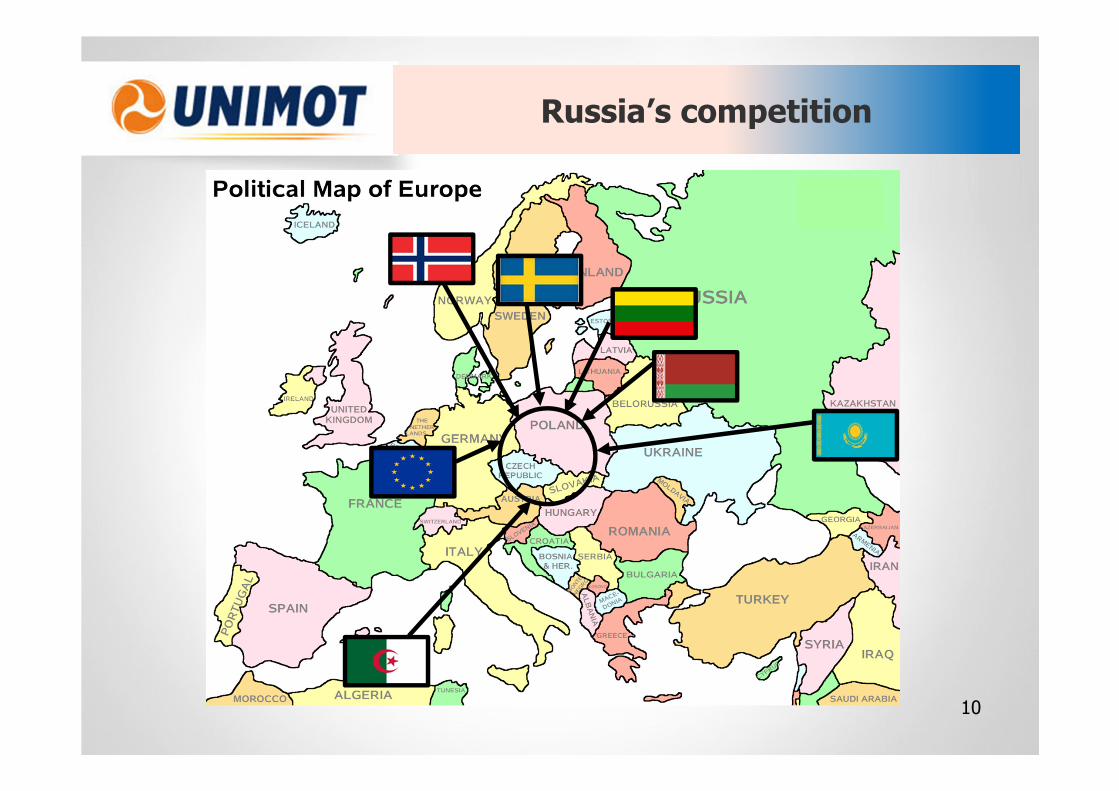

Russia’s competition

10

HOW RUSSIA CAN BECOME MORE COMPETITIVE

� ACCESS WESTERN MARKETS

� INVEST IN QUALITY COMPLYING WITH WESTERN STANDARDS: PN-EN 589:2009

� IMPROVE INFRASTRUCTURE

11

20112012

20142016

3,1 3,9 5,8 7,3

10,111,1

13,9

15,8

Экспорт Продукция

� DIVERSIFY EXPORT DESTINATIONS IN ORDER TO GAIN ACCESS TO END CONSUMERS

� ACCEPT DIFFERENT PRICING FORMULAS

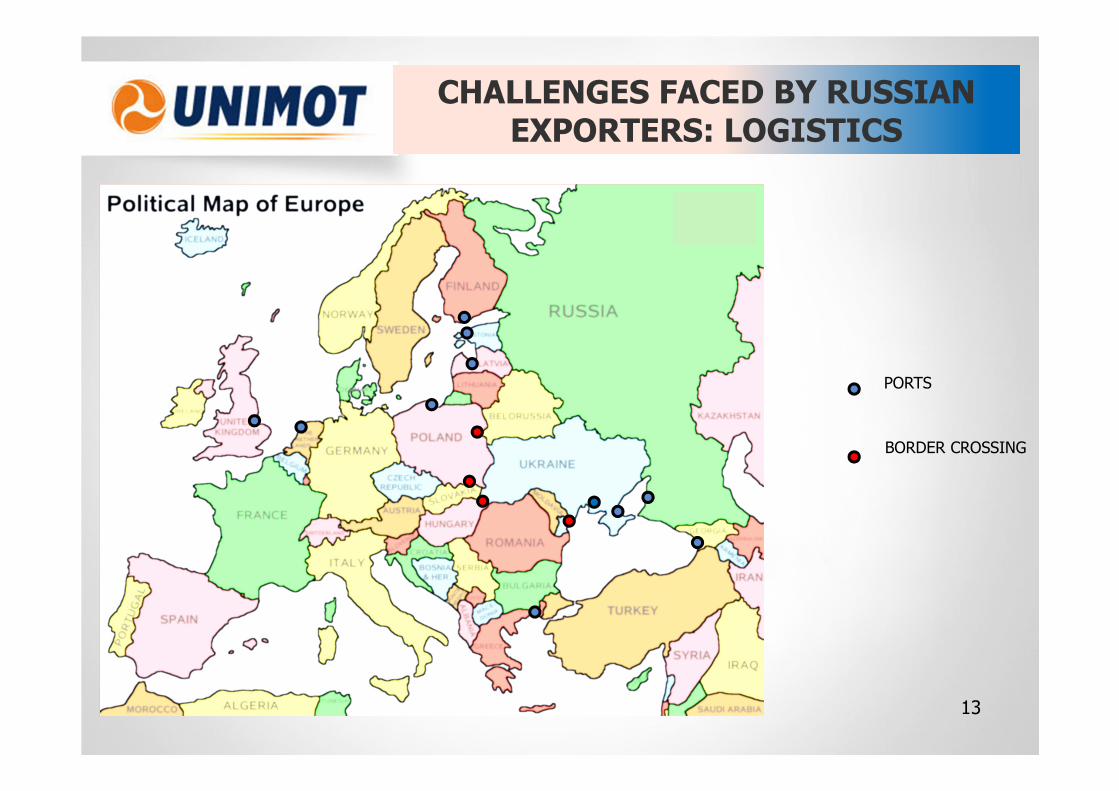

CHALLENGES FACED BY RUSSIAN EXPORTERS: LOGISTICS

� BY LAND

� Railway

� Terminals

12

� BY SEA

� Terminals

� PAPERWORK

CHALLENGES FACED BY RUSSIAN EXPORTERS: LOGISTICS

13

PORTS

BORDER CROSSING

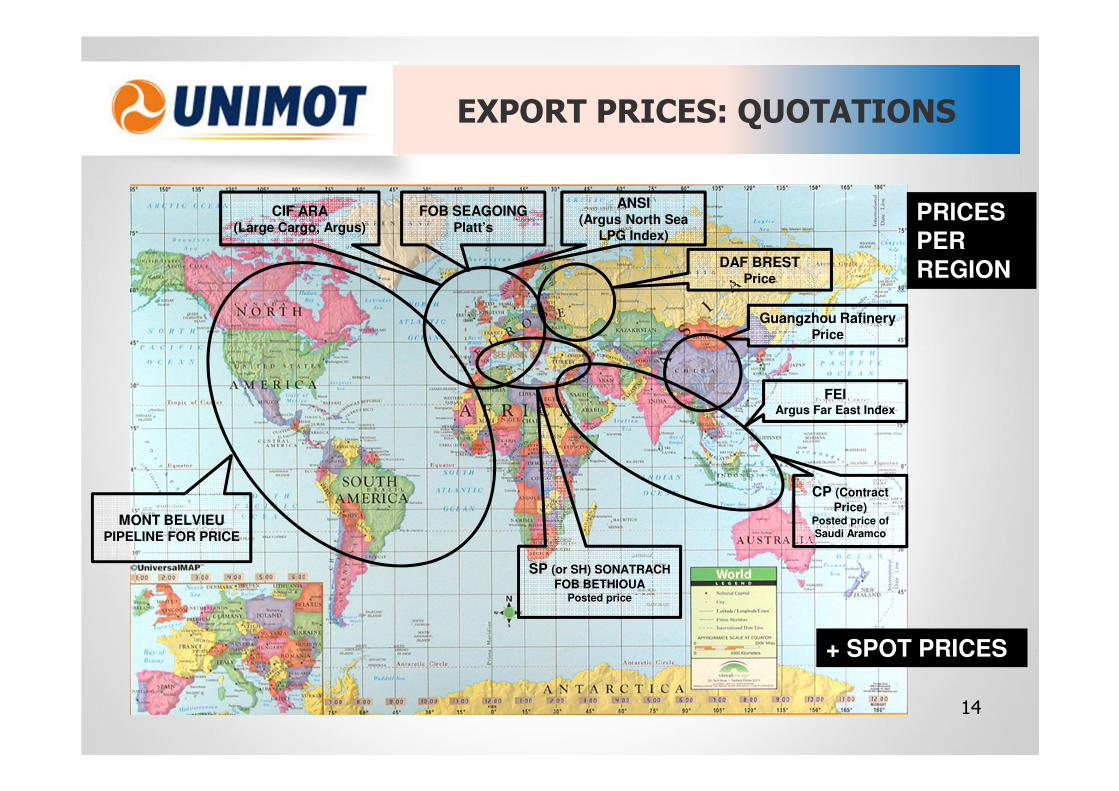

EXPORT PRICES: QUOTATIONS

14

MONT BELVIEU PIPELINE FOR PRICE

CIF ARA(Large Cargo, Argus)

FOB SEAGOINGPlatt’s

ANSI(Argus North Sea

LPG Index)

DAF BRESTPrice

Guangzhou RafineryPrice

FEIArgus Far East Index

CP (Contract

Price)Posted price of Saudi Aramco

SP (or SH) SONATRACH

FOB BETHIOUAPosted price

PRICES

PER REGION

+ SPOT PRICES

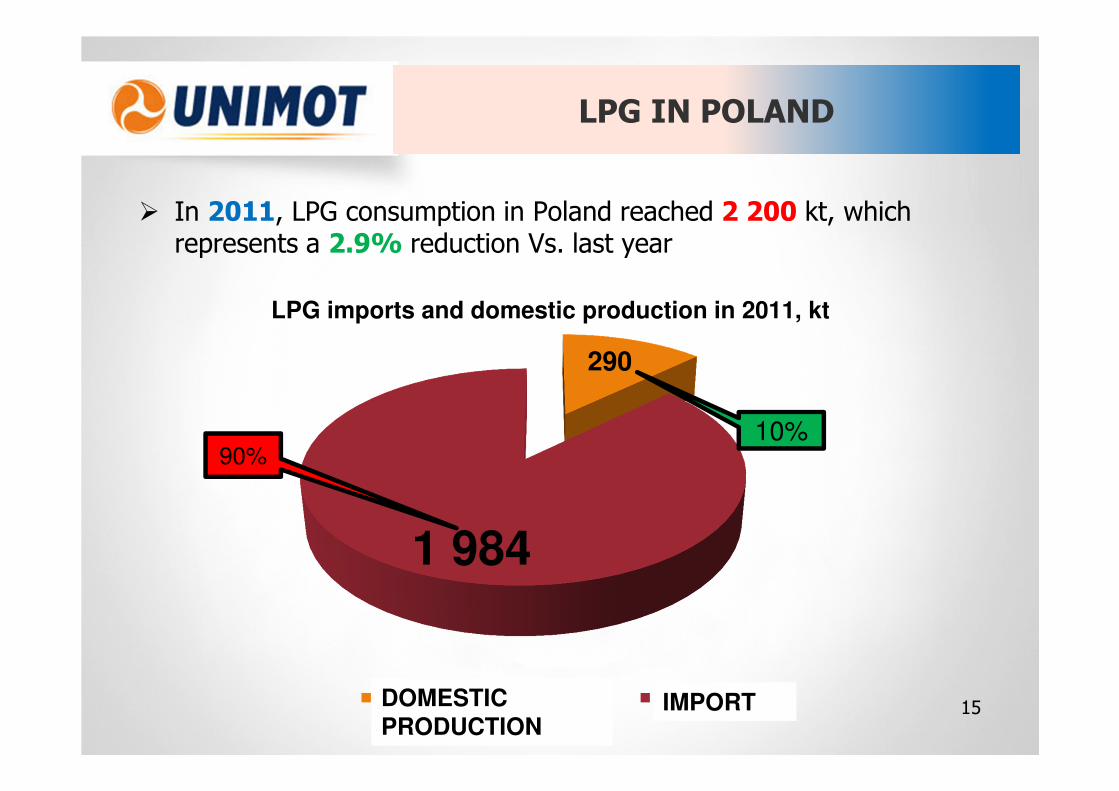

LPG IN POLAND

� In 2011, LPG consumption in Poland reached 2 200 kt, which represents a 2.9% reduction Vs. last year

15

290

1 984

ВНУТРЕНЯЯ ПРОДУКЦИЯ ИМПОРТ

LPG imports and domestic production in 2011, kt

90%10%

IMPORTDOMESTIC PRODUCTION

KEY SOURCES OF IMPORTSin 11 months of 2011

РОССИЯ50%

КАЗАХСТАН23%

БЕЛОРУССИЯ10%

ЛИТВА7%

ГЕРМАНИЯ2%

ЧЕХИЯ2%

ШВЕЦИЯ2%

ВЕЛИКОБРИТАНИЯ1%

ДРУГИЕ3%

UK

Lithuania

Belarus

Kazakhstan

Russia

16

Check Republic Sweden Other

Germany

QUESTIONS AND COMMENTS

ADAM SIKORSKI

Unimot Express [email protected]

+ 48 22 830 70 70

www.unimot.pl

Related Documents

![#CiveItUp LPG (LPG a) IOCL Cl / BPCL D / HPCL C] LPG àà àa … · · 2018-02-28iocl cl / bpcl d / hpcl c] lpg àà àa-r/àkft lpg àž lpg t:- lpg dgcc (poi) lpg 17 lpg id"](https://static.cupdf.com/doc/110x72/5ae5ebd07f8b9acc268cac07/civeitup-lpg-lpg-a-iocl-cl-bpcl-d-hpcl-c-lpg-a-cl-bpcl-d-hpcl-c.jpg)