Outperforming the Benchmark: Identifying Investment Strategies for the US REIT Market using Google Trends Karim F. S. Rochdi | Marian Alexander Dietzel ERES 2014 Annual Meeting, Bucharest

Outperforming the Benchmark: Identifying Investment Strategies for the US REIT Market using Google Trends Karim F. S. Rochdi | Marian Alexander Dietzel.

Dec 23, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Outperforming the Benchmark: Identifying Investment Strategies for the US REIT Market using Google TrendsKarim F. S. Rochdi | Marian Alexander Dietzel

ERES 2014 Annual Meeting, Bucharest

2

Textmasterformate durch Klicken bearbeiten

Agenda

1. Motivation and Theoretical Background

2. Data

3. Research Design and Methodology

4. Analysis and Findings

5. Conclusions

Outperforming the Benchmark: Identifying Investment Strategies for the US REIT Market using Google Trends

3

Textmasterformate durch Klicken bearbeiten

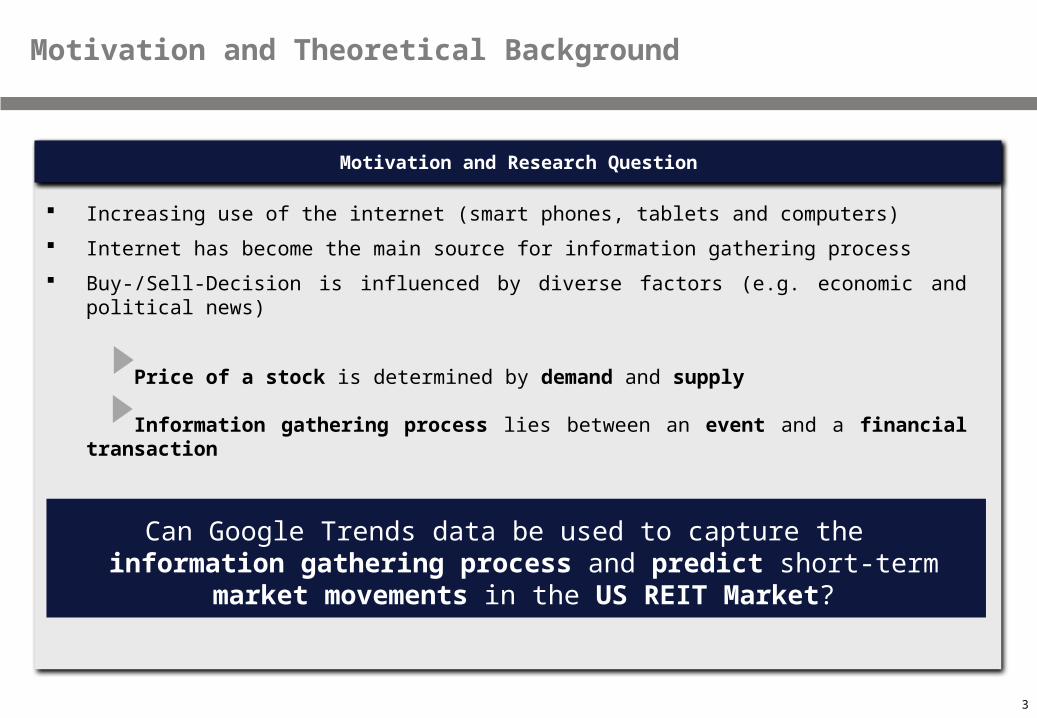

Can Google Trends data be used to capture the information gathering process and predict short-term market

movements in the US REIT Market?

Motivation and Theoretical Background

Increasing use of the internet (smart phones, tablets and computers)

Internet has become the main source for information gathering process

Buy-/Sell-Decision is influenced by diverse factors (e.g. economic and political news)

Price of a stock is determined by demand and supply

Information gathering process lies between an event and a financial transaction

Motivation and Research Question

4

Textmasterformate durch Klicken bearbeitenRelationship between Google Trends Data and Financial Markets

Motivation and Theoretical Background

Da, Z., Engelberg, J. and Gao, P. (2011), “In Search of Attention”, The Journal of Finance, Vol. 66 No. 5, pp. 1461-99.

Drake, M. S., Roulstone, D. T. and Thornock, J. R. (2012), “Investor Information Demand: Evidence from Google Searches Around Earning Announcements”, Journal of Accounting Research, Vol. 50 No. 4, pp. 1001-40.

Da, Z., Engelberg, J. and Gao, P. (2013). “The sum of all fears: investor sentiment and asset prices”. SSRN eLibrary.

Preis, T., Moat, H.S. and Stanley, E. (2013), “Quantifying Trading Behavior in Financial Markets Using Google Trends”, Nature - Scientific Reports, Vol. 3 No. 1684, pp. 1-6.

Kristoufek, L. (2013), “Can Google Trends search queries contribute to risk diversification?”, Nature - Scientific Reports, Vol. 3 No. 2713, pp. 1-5.

Main empirical findings are that Google Trends data are significantly related to trading activity, stock liquidity, volatility, earnings surprises and

market movements.

5

Textmasterformate durch Klicken bearbeitenRelationship between Google Trends Data and the Real Estate Market

Motivation and Theoretical Background

Beracha, E. and Wintoki, J. (2012), “Predicting Future Home Price Changes Using Current Google Search Data,” Journal of Real Estate Research, forthcoming.

Hohenstatt, R., Kaesbauer, M. and Schaefers, W. (2011), “’Geco’ and its Potential for Real Estate Research: Evidence from the U.S. Housing Market”, Journal of Real Estate Research, Vol. 33 No. 4., pp. 471-506.

Hohenstatt, R. and Kaesbauer, M. (2013), “GECO’s Weather Forecast’ for the U.K. Housing Market: To What Extent Can We Rely on Google ECOnometrics?”, Journal of Real Estate Research, forthcoming.

Wu, L. and Brynjolfsson, E. (2009), “The Future of Prediction: How Google Searches Foreshadow Housing Prices and Sales”, Working papers, Wharton School, University of Pennsylvania.

The studies demonstrate Google‘s predictive abilities for the real estate market on both a state and national level

6

Textmasterformate durch Klicken bearbeitenGoogle Data

Data

Search Volume Indices (SVI) derived from Google Trends (http://www.google.com/trends/)

Normalized values, scaled measured between 0 and 100

The weekly data covers search queries conducted from Sunday to Saturday.

Google Trends makes the newest weekly data available with an approximate two day delay.

7

Textmasterformate durch Klicken bearbeitenCluster Formation

Research Design and Methodology

Covering different aspects of real estate

real estate reits affordable housing properties+property real estate

management real estate broker …

Real Estate

Representing the mood, circumstances, desires

and fears of Google users

hate happy energy conflict cash health …

General Sentiment

Covering financial topics

fed bonds derivatives dividend currency investor …

Finance

8

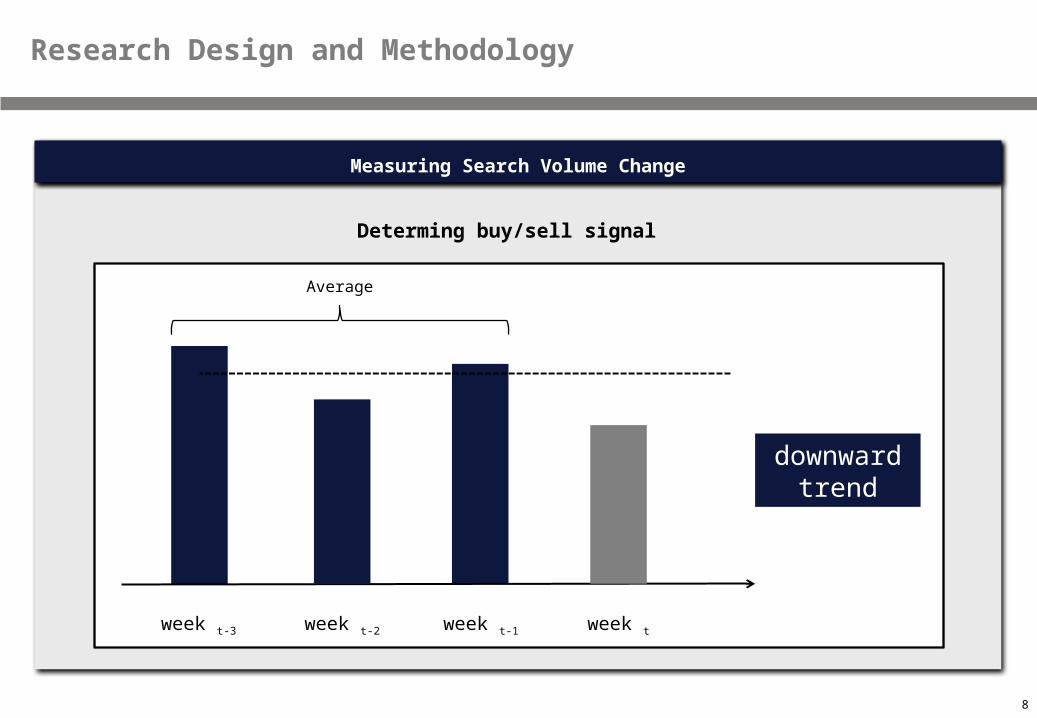

Textmasterformate durch Klicken bearbeitenMeasuring Search Volume Change

Research Design and Methodology

Determing buy/sell signal

Average

week t-3 week t-2 week t-1 week t

downward trend

9

Textmasterformate durch Klicken bearbeitenMeasuring Search Volume Change

Research Design and Methodology

Determing buy/sell signal

Average

week t-3 week t-2 week t-1 week t

upward trend

10

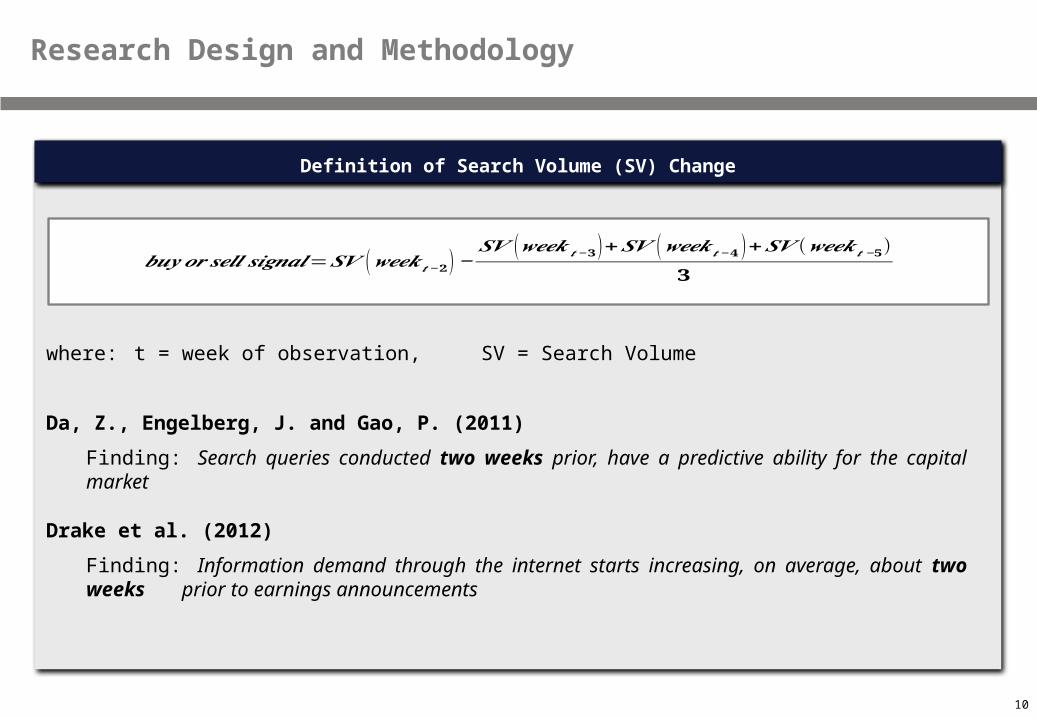

Textmasterformate durch Klicken bearbeitenDefinition of Search Volume (SV) Change

Research Design and Methodology

where: t = week of observation, SV = Search Volume

Da, Z., Engelberg, J. and Gao, P. (2011)

Finding: Search queries conducted two weeks prior, have a predictive ability for the capital market

Drake et al. (2012)

Finding: Information demand through the internet starts increasing, on average, about two weeks prior to earnings announcements

𝒃𝒖𝒚 𝒐𝒓 𝒔𝒆𝒍𝒍 𝒔𝒊𝒈𝒏𝒂𝒍=𝑺𝑽 (𝒘𝒆𝒆𝒌𝒕−𝟐 )−𝑺𝑽 (𝒘𝒆𝒆𝒌𝒕−𝟑 )+𝑺𝑽 (𝒘𝒆𝒆𝒌𝒕−𝟒 )+𝑺𝑽 (𝒘𝒆𝒆𝒌𝒕−𝟓)

𝟑

11

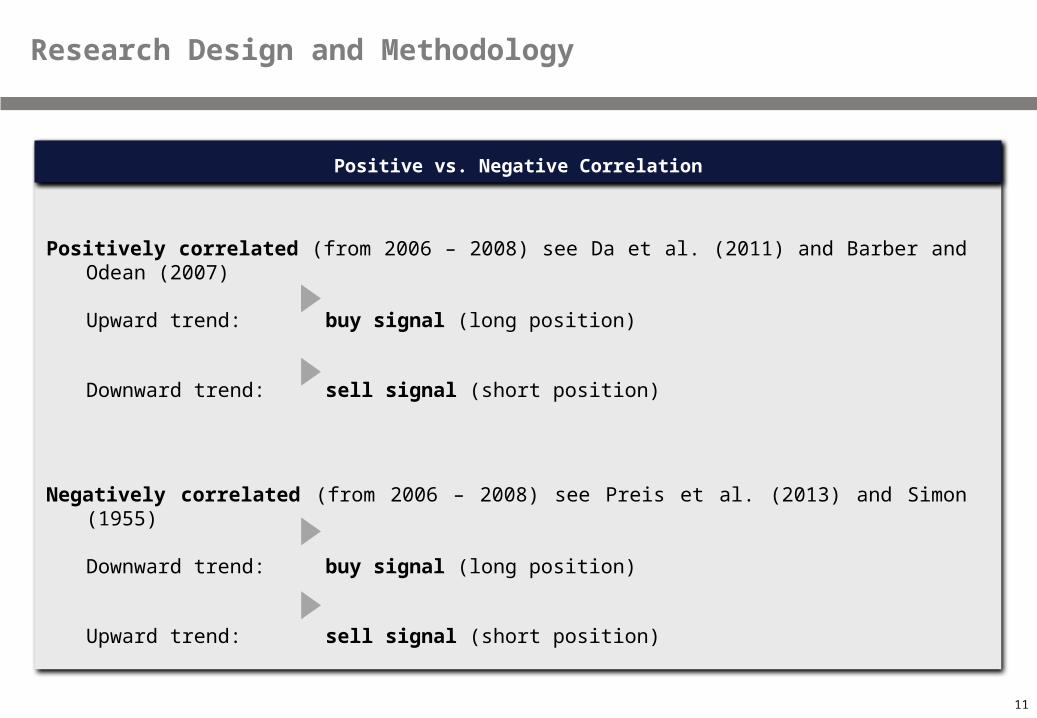

Textmasterformate durch Klicken bearbeitenPositive vs. Negative Correlation

Research Design and Methodology

Positively correlated (from 2006 – 2008) see Da et al. (2011) and Barber and Odean (2007)

Upward trend: buy signal (long position)

Downward trend: sell signal (short position)

Negatively correlated (from 2006 – 2008) see Preis et al. (2013) and Simon (1955)

Downward trend: buy signal (long position)

Upward trend: sell signal (short position)

12

Textmasterformate durch Klicken bearbeiten

Reinvestment Strategy

First Trade: Monday, February 20, 2006

Last Trade: Monday, December 30, 2013

Reinvestment assumption

Absolute Investment Performance (AIP):

Conventional Strategies

Buy-and-Hold-Strategy: 1.58 % (0.20 % p. a.)

Random Strategy (purely random signals): 72.27 % (7.04 % p. a.)

Momentum Strategy: -53.5 % (-9.13 % p. a.)

𝐴𝐼𝑃= 𝑉𝑎𝑙𝑢𝑒𝑤𝑒𝑒𝑘 411𝑉𝑎𝑙𝑢𝑒𝑤𝑒𝑒𝑘 1 − 1

Methodology

Research Design and Methodology

13

Textmasterformate durch Klicken bearbeitenPerformance Ranking (Top 15)

Empirical Results

Rank Category Search Terms AIP p.a. AIP Rolling 6-month

returnsRolling 6-month

risk of loss Hit Rate

1 real estate properties+property 47,8% 2181,6% 31,7% 27,9% 57,1%2 real estate condos 43,5% 1696,9% 37,2% 27,6% 54,9%3 real estate realty trust+realty trusts 43,1% 1656,2% 27,4% 35,8% 54,0%

4 real estateflip house+flip houses+flipping house+flipping houses

42,0% 1554,8% 29,5% 33,2% 53,2%

5 real estate Real Estate Agencies 38,6% 1262,8% 29,0% 27,6% 53,0%6 real estate realtor+realtors 35,8% 1054,7% 30,1% 34,3% 53,2%7 real estate Real Estate_cat 34,0% 940,1% 31,5% 39,4% 52,8%8 real estate apartments+apartment 32,9% 872,2% 27,7% 34,0% 52,3%9 real estate Real Estate Listings 31,1% 772,0% 32,0% 40,2% 52,5%

10 real estatereal estate agent+real estate agents+real estate agencies

30,0% 715,8% 26,9% 35,3% 53,2%

11 real estateremax+re/max+zillow+trulia+yahoo homes+redfin+frontdoor+apartmentguide+curbed+ziprealty+hotpads

29,8% 707,8% 28,3% 47,3% 52,5%

12 real estate real estate company+real estate companies 29,6% 695,1% 19,5% 32,0% 56,6%13 finance earnings 29,6% 693,8% 17,8% 26,1% 54,0%14 finance Credit & Lending 28,9% 660,4% 15,9% 24,8% 54,7%15 general politics 27,6% 601,0% 21,2% 32,0% 50,1%

58 conventional RANDOM 7,04% 72,27% 3,78% 50,00% 49,99%87 conventional BUY-AND-HOLD 0,2% 1,6% 2,8% 39,1% -128 conventional MOMENTUM -9,13% -53,5% -3,2% 56,3% 48,9%

.. .. .. ..

..

.. .. .. ..

14

Textmasterformate durch Klicken bearbeiten

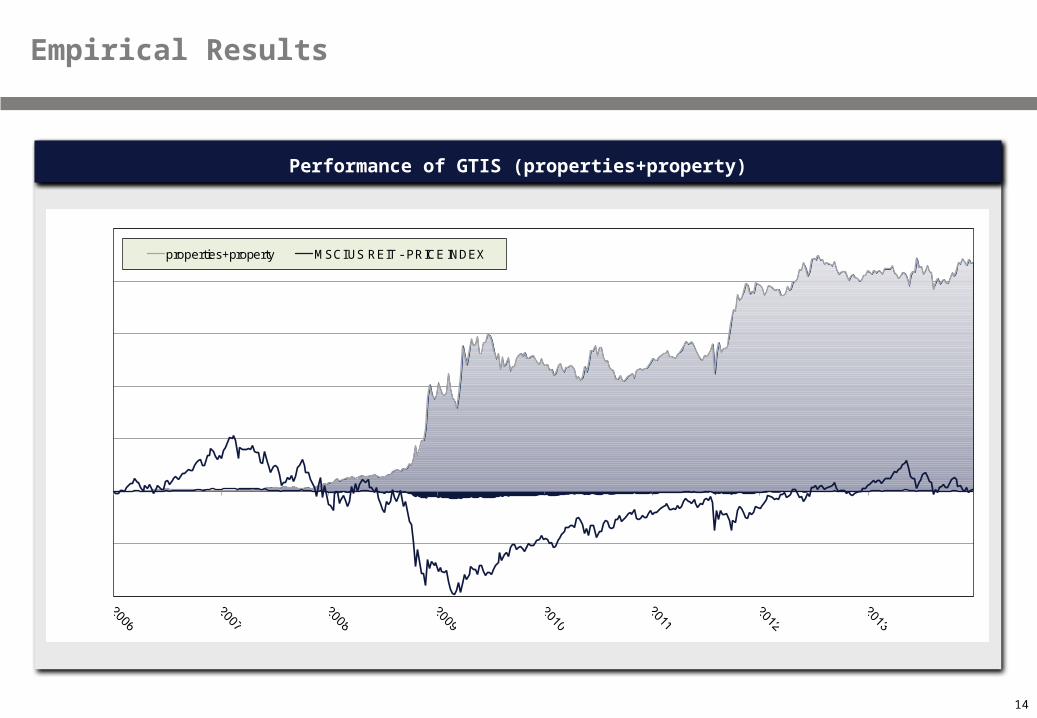

-1000%

-500%

0%

500%

1000%

1500%

2000%

2500%

properties+property MSCI US REIT - PRICE INDEX

Performance of GTIS (properties+property)

Empirical Results

15

Textmasterformate durch Klicken bearbeitenPerformance Measures (sub periods)

Empirical Results

Rank Category Search Terms AIP p.a.Rolling 6-month

returns AIP p.a.Rolling 6-month

returns AIP p.a.Rolling 6-month

returns

1 real estate properties+property 47,8% 31,7% 84,0% 28,0% 5,2% 1,8%2 real estate condos 43,5% 37,2% 108,6% 59,1% 18,1% 8,5%3 real estate realty trust+realty trusts 43,1% 27,4% 64,4% 28,2% -7,1% -5,1%

4 real estateflip house+flip houses+flipping house+flipping houses

42,0% 29,5% 100,1% 36,3% 4,5% -0,1%

5 real estate Real Estate Agencies 38,6% 29,0% 58,3% 19,6% 28,7% 13,7%6 real estate realtor+realtors 35,8% 30,1% 86,1% 34,7% 14,0% 7,0%7 real estate Real Estate_cat 34,0% 31,5% 130,7% 65,0% 12,9% 4,3%8 real estate apartments+apartment 32,9% 27,7% 109,9% 50,8% 5,4% 0,7%9 real estate Real Estate Listings 31,1% 32,0% 94,7% 52,3% -6,0% -4,1%

10 real estatereal estate agent+real estate agents+real estate agencies

30,0% 26,9% 45,5% 20,4% 10,2% 4,8%

11 real estateremax+re/max+zillow+trulia+yahoo homes+redfin+frontdoor+apartmentguide+curbed+ziprealty+hotpads

29,8% 28,3% 102,6% 58,6% 2,4% -1,3%

12 real estate real estate company+real estate companies 29,6% 19,5% 9,0% 8,7% 8,8% 5,3%13 finance earnings 29,6% 17,8% 92,0% 45,4% 15,5% 6,2%14 finance Credit & Lending 28,9% 15,9% 53,2% 21,2% 20,9% 9,0%15 general politics 27,6% 21,2% 73,2% 25,4% 23,0% 13,3%

CRISIS (09/15/2008 - 02/21/2011) RECENT YEARS (2012-2013)OVERALL (2006 - 2013)

58 conventional RANDOM 7,0% 3,8% 15,8% 6,3% 1,0% 0,6%87 conventional BUY-AND-HOLD 0,2% 2,8% 0,1% 15,6% 6,4% 2,8%128 conventional MOMENTUM -9,1% -3,2% -1,7% -6,4% 11,9% 6,2%

.. .. .. .. .. .. .. ....

16

Textmasterformate durch Klicken bearbeitenMain Findings

Findings and Conclusion

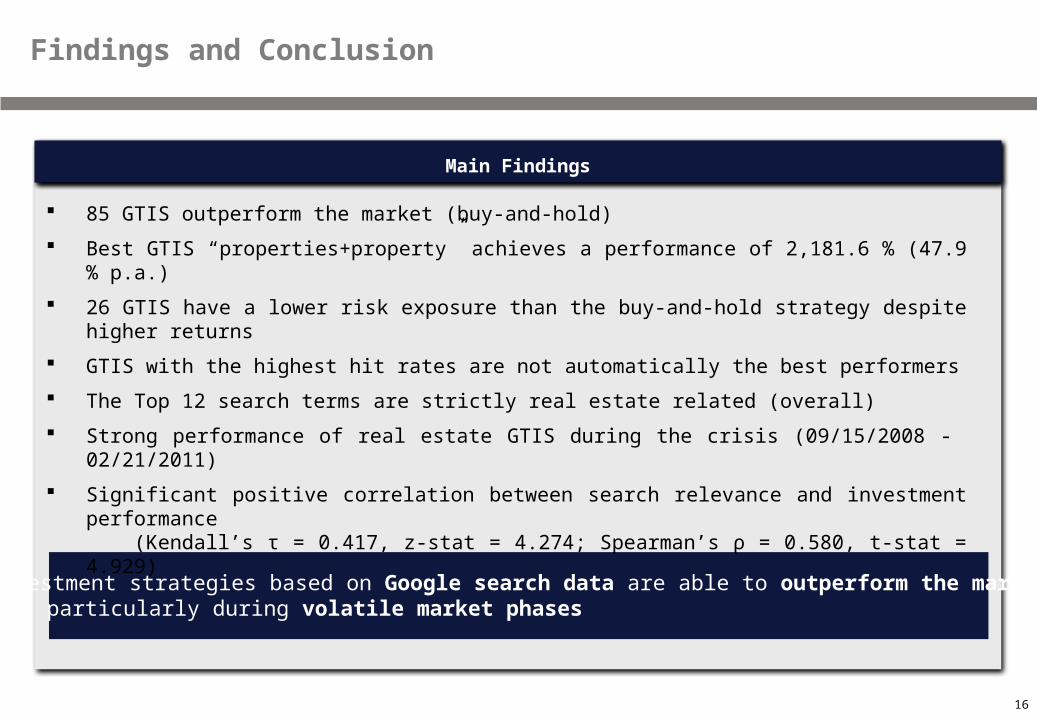

85 GTIS outperform the market (buy-and-hold)

Best GTIS “properties+property” achieves a performance of 2,181.6 % (47.9 % p.a.)

26 GTIS have a lower risk exposure than the buy-and-hold strategy despite higher returns

GTIS with the highest hit rates are not automatically the best performers

The Top 12 search terms are strictly real estate related (overall)

Strong performance of real estate GTIS during the crisis (09/15/2008 - 02/21/2011)

Significant positive correlation between search relevance and investment performance(Kendall’s τ = 0.417, z-stat = 4.274; Spearman’s ρ = 0.580, t-stat = 4.929)

Investment strategies based on Google search data are able to outperform the market particularly during volatile market phases

17

Textmasterformate durch Klicken bearbeitenIdentifying Investment Strategies for the US REIT Market using Google Trends

Outperforming the Benchmark

Thanks for listening. Feel free to ask any questions

Related Documents