By Research Department Dec 2021 OUTLOOK 2022

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

By Research Department

Dec 2021

OUTLOOK 2022

MACROECONOMY

FIXED INCOME MARKET

EQUITY MARKET

INDUSTRY AND STOCK PICKS

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

3

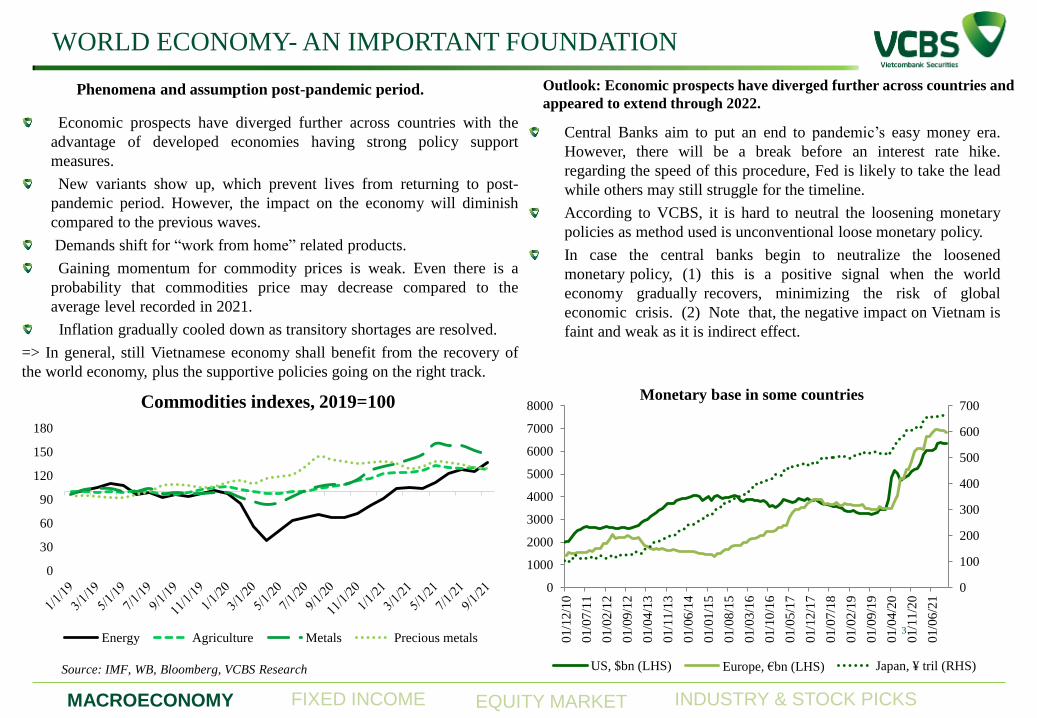

Source: IMF, WB, Bloomberg, VCBS Research

Economic prospects have diverged further across countries with the

advantage of developed economies having strong policy support

measures.

New variants show up, which prevent lives from returning to post-

pandemic period. However, the impact on the economy will diminish

compared to the previous waves.

Demands shift for “work from home” related products.

Gaining momentum for commodity prices is weak. Even there is a

probability that commodities price may decrease compared to the

average level recorded in 2021.

Inflation gradually cooled down as transitory shortages are resolved.

=> In general, still Vietnamese economy shall benefit from the recovery of

the world economy, plus the supportive policies going on the right track.

Phenomena and assumption post-pandemic period. Outlook: Economic prospects have diverged further across countries and

appeared to extend through 2022.

Central Banks aim to put an end to pandemic’s easy money era.

However, there will be a break before an interest rate hike.

regarding the speed of this procedure, Fed is likely to take the lead

while others may still struggle for the timeline.

According to VCBS, it is hard to neutral the loosening monetary

policies as method used is unconventional loose monetary policy.

In case the central banks begin to neutralize the loosened

monetary policy, (1) this is a positive signal when the world

economy gradually recovers, minimizing the risk of global

economic crisis. (2) Note that, the negative impact on Vietnam is

faint and weak as it is indirect effect.

WORLD ECONOMY- AN IMPORTANT FOUNDATION

0

100

200

300

400

500

600

700

0

1000

2000

3000

4000

5000

6000

7000

8000

01/1

2/1

0

01/0

7/1

1

01/0

2/1

2

01/0

9/1

2

01/0

4/1

3

01/1

1/1

3

01/0

6/1

4

01/0

1/1

5

01/0

8/1

5

01/0

3/1

6

01/1

0/1

6

01/0

5/1

7

01/1

2/1

7

01/0

7/1

8

01/0

2/1

9

01/0

9/1

9

01/0

4/2

0

01/1

1/2

0

01/0

6/2

1

Monetary base in some countries

US, $bn (LHS) Europe, €bn (LHS) Japan, ¥ tril (RHS)

0

30

60

90

120

150

180

Commodities indexes, 2019=100

Energy Agriculture Metals Precious metals

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

EXPECTATION OF VIETNAM ECONOMIC REBOUND POST- PANDEMIC

4

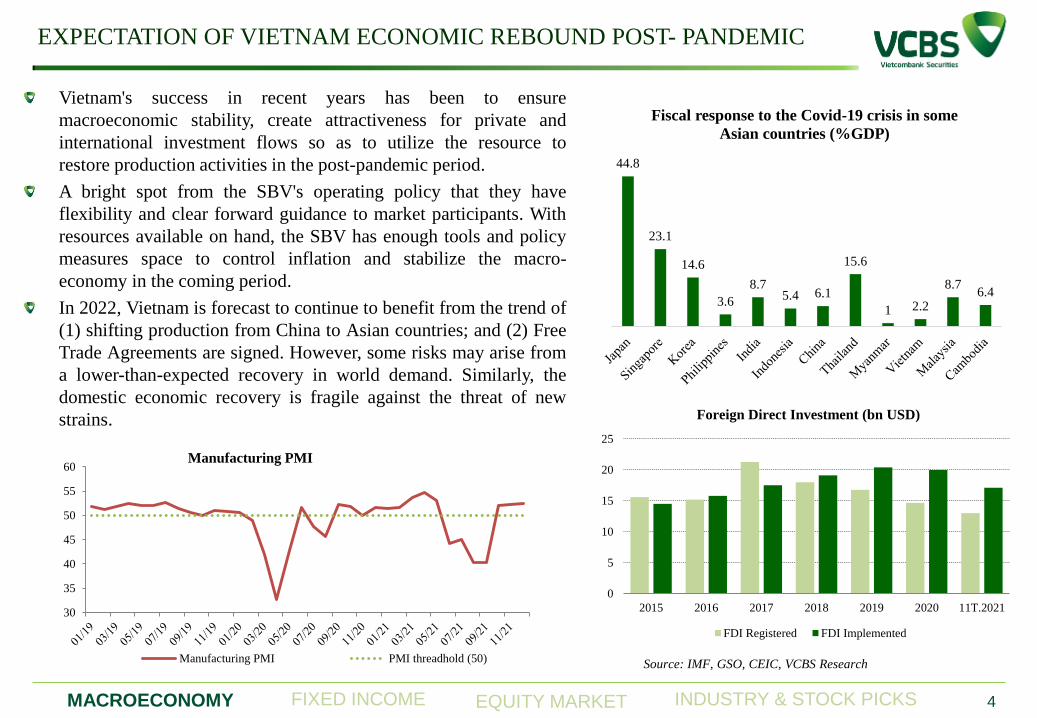

Vietnam's success in recent years has been to ensure

macroeconomic stability, create attractiveness for private and

international investment flows so as to utilize the resource to

restore production activities in the post-pandemic period.

A bright spot from the SBV's operating policy that they have

flexibility and clear forward guidance to market participants. With

resources available on hand, the SBV has enough tools and policy

measures space to control inflation and stabilize the macro-

economy in the coming period.

In 2022, Vietnam is forecast to continue to benefit from the trend of

(1) shifting production from China to Asian countries; and (2) Free

Trade Agreements are signed. However, some risks may arise from

a lower-than-expected recovery in world demand. Similarly, the

domestic economic recovery is fragile against the threat of new

strains.

Source: IMF, GSO, CEIC, VCBS Research

44.8

23.1

14.6

3.6

8.7 5.4 6.1

15.6

1 2.2

8.7 6.4

Fiscal response to the Covid-19 crisis in some

Asian countries (%GDP)

0

5

10

15

20

25

2015 2016 2017 2018 2019 2020 11T.2021

Foreign Direct Investment (bn USD)

FDI Registered FDI Implemented

30

35

40

45

50

55

60Manufacturing PMI

Manufacturing PMI PMI threadhold (50)

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

GROW REBOUNDS BUT STILL VULNERABLE TO NEW WAVE OF THE

PANDEMIC

5

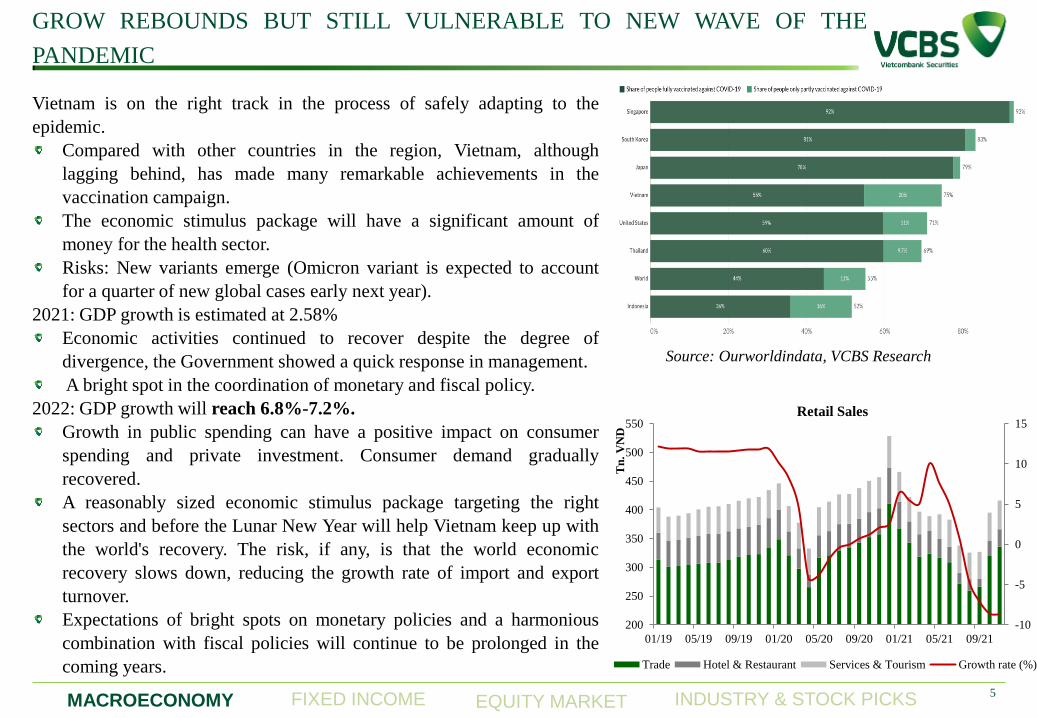

Vietnam is on the right track in the process of safely adapting to the

epidemic.

Compared with other countries in the region, Vietnam, although

lagging behind, has made many remarkable achievements in the

vaccination campaign.

The economic stimulus package will have a significant amount of

money for the health sector.

Risks: New variants emerge (Omicron variant is expected to account

for a quarter of new global cases early next year).

2021: GDP growth is estimated at 2.58%

Economic activities continued to recover despite the degree of

divergence, the Government showed a quick response in management.

A bright spot in the coordination of monetary and fiscal policy.

2022: GDP growth will reach 6.8%-7.2%.

Growth in public spending can have a positive impact on consumer

spending and private investment. Consumer demand gradually

recovered.

A reasonably sized economic stimulus package targeting the right

sectors and before the Lunar New Year will help Vietnam keep up with

the world's recovery. The risk, if any, is that the world economic

recovery slows down, reducing the growth rate of import and export

turnover.

Expectations of bright spots on monetary policies and a harmonious

combination with fiscal policies will continue to be prolonged in the

coming years.

Source: Ourworldindata, VCBS Research

75.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

Q4 Q1 Q2 Q3 Q4 Q1

2019 2020 2021

GDP index , 2019Q4=100

Philippines

Malaysia

Việt Nam

-10

-5

0

5

10

15

200

250

300

350

400

450

500

550

01/19 05/19 09/19 01/20 05/20 09/20 01/21 05/21 09/21

Tn

. V

ND

Retail Sales

Trade Hotel & Restaurant Services & Tourism Growth rate (%)

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

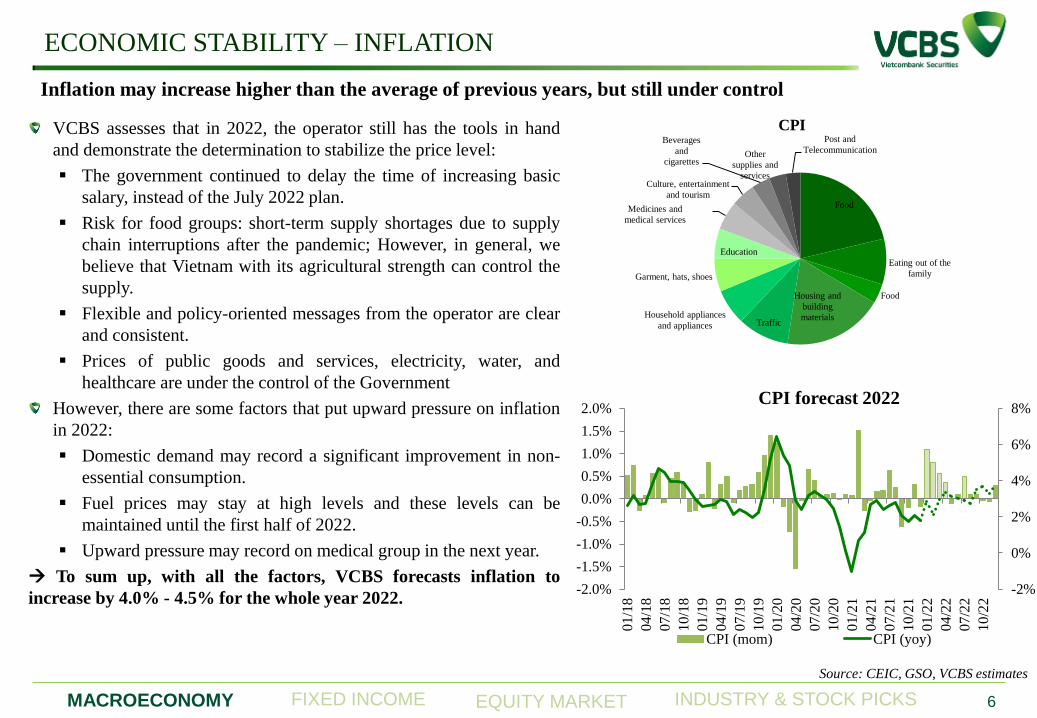

VCBS assesses that in 2022, the operator still has the tools in hand

and demonstrate the determination to stabilize the price level:

The government continued to delay the time of increasing basic

salary, instead of the July 2022 plan.

Risk for food groups: short-term supply shortages due to supply

chain interruptions after the pandemic; However, in general, we

believe that Vietnam with its agricultural strength can control the

supply.

Flexible and policy-oriented messages from the operator are clear

and consistent.

Prices of public goods and services, electricity, water, and

healthcare are under the control of the Government

However, there are some factors that put upward pressure on inflation

in 2022:

Domestic demand may record a significant improvement in non-

essential consumption.

Fuel prices may stay at high levels and these levels can be

maintained until the first half of 2022.

Upward pressure may record on medical group in the next year.

To sum up, with all the factors, VCBS forecasts inflation to

increase by 4.0% - 4.5% for the whole year 2022.

ECONOMIC STABILITY – INFLATION

6

Source: CEIC, GSO, VCBS estimates

Inflation may increase higher than the average of previous years, but still under control

Food

Eating out of the

family

Food Housing and

building

materials Traffic

Household appliances

and appliances

Garment, hats, shoes

Education

Medicines and

medical services

Culture, entertainment

and tourism

Beverages

and

cigarettes Other

supplies and

services

Post and

Telecommunication

CPI

-2%

0%

2%

4%

6%

8%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

01/1

8

04/1

8

07/1

8

10/1

8

01/1

9

04/1

9

07/1

9

10/1

9

01/2

0

04/2

0

07/2

0

10/2

0

01/2

1

04/2

1

07/2

1

10/2

1

01/2

2

04/2

2

07/2

2

10/2

2

CPI forecast 2022

CPI (mom) CPI (yoy)

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

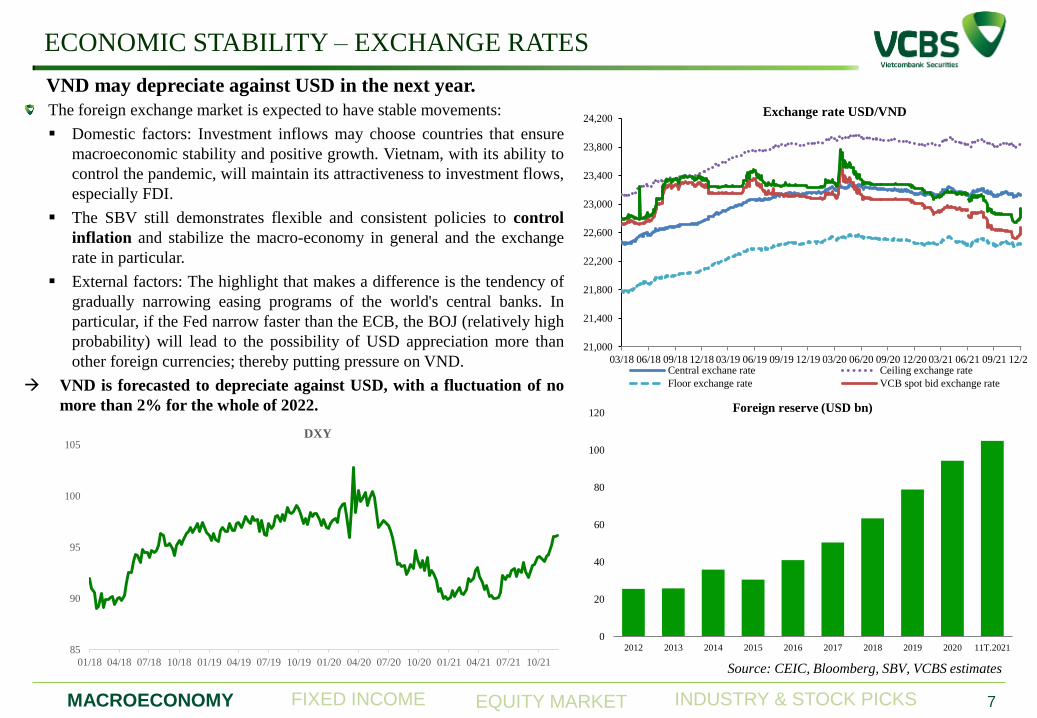

The foreign exchange market is expected to have stable movements:

Domestic factors: Investment inflows may choose countries that ensure

macroeconomic stability and positive growth. Vietnam, with its ability to

control the pandemic, will maintain its attractiveness to investment flows,

especially FDI.

The SBV still demonstrates flexible and consistent policies to control

inflation and stabilize the macro-economy in general and the exchange

rate in particular.

External factors: The highlight that makes a difference is the tendency of

gradually narrowing easing programs of the world's central banks. In

particular, if the Fed narrow faster than the ECB, the BOJ (relatively high

probability) will lead to the possibility of USD appreciation more than

other foreign currencies; thereby putting pressure on VND.

VND is forecasted to depreciate against USD, with a fluctuation of no

more than 2% for the whole of 2022.

ECONOMIC STABILITY – EXCHANGE RATES

7

Source: CEIC, Bloomberg, SBV, VCBS estimates

VND may depreciate against USD in the next year.

0

20

40

60

80

100

120

2012 2013 2014 2015 2016 2017 2018 2019 2020 11T.2021

Foreign reserve (USD bn)

85

90

95

100

105

01/18 04/18 07/18 10/18 01/19 04/19 07/19 10/19 01/20 04/20 07/20 10/20 01/21 04/21 07/21 10/21

DXY

21,000

21,400

21,800

22,200

22,600

23,000

23,400

23,800

24,200

03/18 06/18 09/18 12/18 03/19 06/19 09/19 12/19 03/20 06/20 09/20 12/20 03/21 06/21 09/21 12/21

Exchange rate USD/VND

Central exchane rate Ceiling exchange rate

Floor exchange rate VCB spot bid exchange rate

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

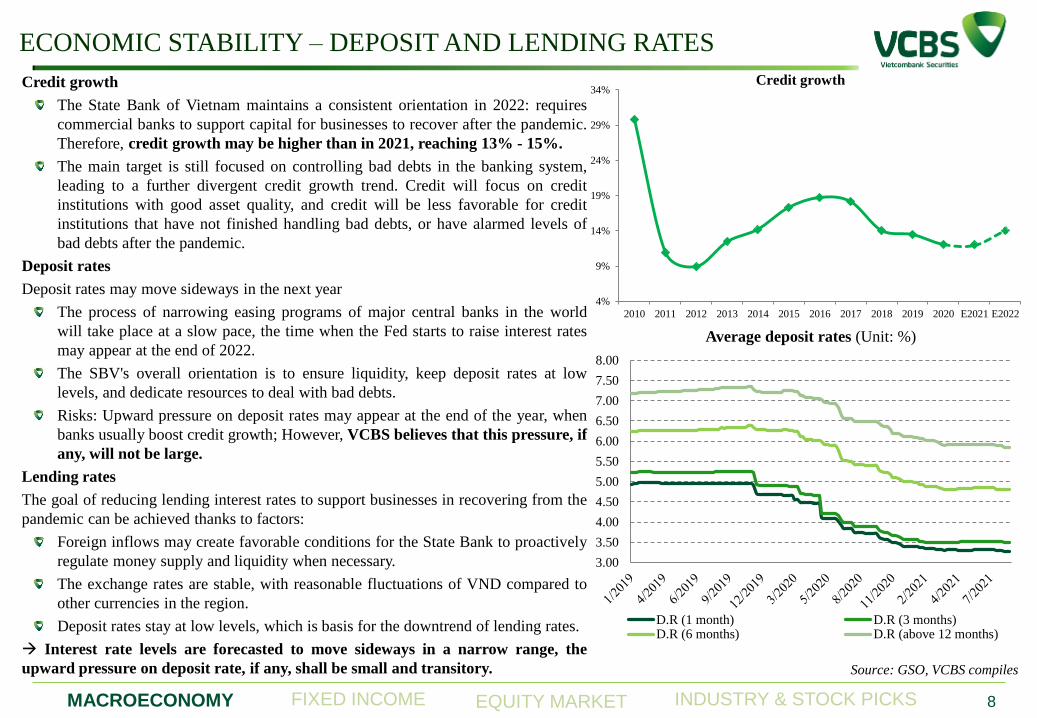

ECONOMIC STABILITY – DEPOSIT AND LENDING RATES

8

Source: GSO, VCBS compiles

Credit growth

The State Bank of Vietnam maintains a consistent orientation in 2022: requires

commercial banks to support capital for businesses to recover after the pandemic.

Therefore, credit growth may be higher than in 2021, reaching 13% - 15%.

The main target is still focused on controlling bad debts in the banking system,

leading to a further divergent credit growth trend. Credit will focus on credit

institutions with good asset quality, and credit will be less favorable for credit

institutions that have not finished handling bad debts, or have alarmed levels of

bad debts after the pandemic.

Deposit rates

Deposit rates may move sideways in the next year

The process of narrowing easing programs of major central banks in the world

will take place at a slow pace, the time when the Fed starts to raise interest rates

may appear at the end of 2022.

The SBV's overall orientation is to ensure liquidity, keep deposit rates at low

levels, and dedicate resources to deal with bad debts.

Risks: Upward pressure on deposit rates may appear at the end of the year, when

banks usually boost credit growth; However, VCBS believes that this pressure, if

any, will not be large.

Lending rates

The goal of reducing lending interest rates to support businesses in recovering from the

pandemic can be achieved thanks to factors:

Foreign inflows may create favorable conditions for the State Bank to proactively

regulate money supply and liquidity when necessary.

The exchange rates are stable, with reasonable fluctuations of VND compared to

other currencies in the region.

Deposit rates stay at low levels, which is basis for the downtrend of lending rates.

Interest rate levels are forecasted to move sideways in a narrow range, the

upward pressure on deposit rate, if any, shall be small and transitory.

4%

9%

14%

19%

24%

29%

34%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 E2021 E2022

Credit growth

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

7.50

8.00

Average deposit rates (Unit: %)

D.R (1 month) D.R (3 months)D.R (6 months) D.R (above 12 months)

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME 9

Source: VCBS Research

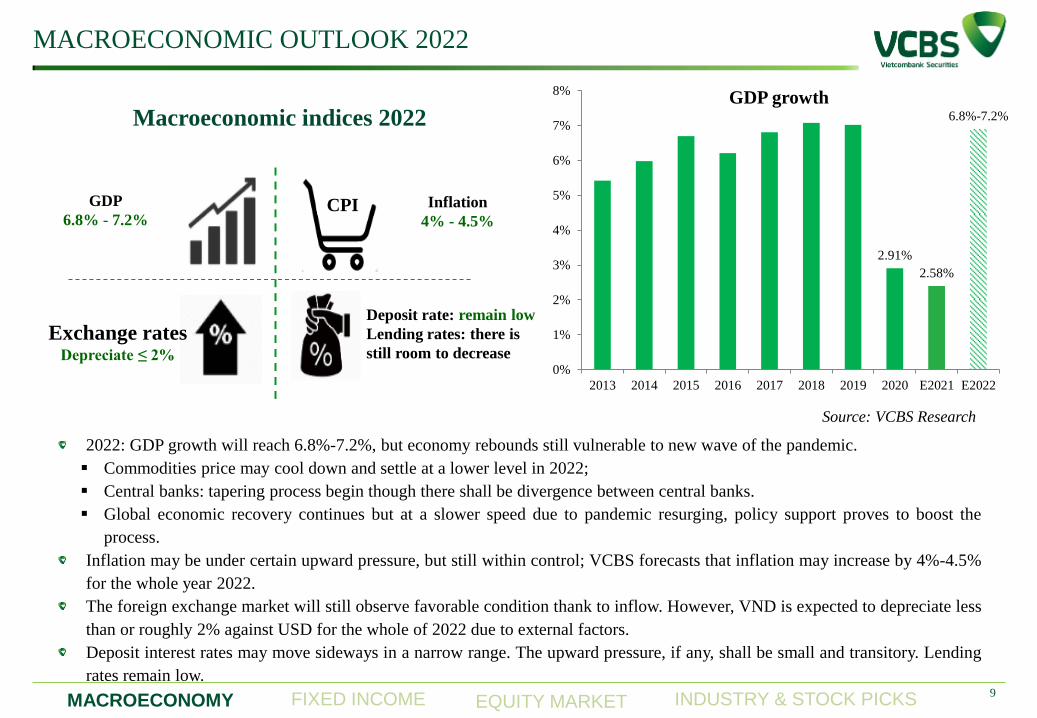

Macroeconomic indices 2022

CPI

Deposit rate: remain low

Lending rates: there is

still room to decrease

GDP

6.8% - 7.2%

Exchange rates Depreciate ≤ 2%

Inflation

4% - 4.5%

MACROECONOMIC OUTLOOK 2022

2.91%

2.58%

6.8%-7.2%

0%

1%

2%

3%

4%

5%

6%

7%

8%

2013 2014 2015 2016 2017 2018 2019 2020 E2021 E2022

GDP growth

2022: GDP growth will reach 6.8%-7.2%, but economy rebounds still vulnerable to new wave of the pandemic.

Commodities price may cool down and settle at a lower level in 2022;

Central banks: tapering process begin though there shall be divergence between central banks.

Global economic recovery continues but at a slower speed due to pandemic resurging, policy support proves to boost the

process.

Inflation may be under certain upward pressure, but still within control; VCBS forecasts that inflation may increase by 4%-4.5%

for the whole year 2022.

The foreign exchange market will still observe favorable condition thank to inflow. However, VND is expected to depreciate less

than or roughly 2% against USD for the whole of 2022 due to external factors.

Deposit interest rates may move sideways in a narrow range. The upward pressure, if any, shall be small and transitory. Lending

rates remain low.

MACROECONOMY

FIXED INCOME MARKET

EQUITY MARKET

INDUSTRY AND STOCK PICKS

MACROECONOMY EQUITY MARKET INDUSTRY AND STOCKS PICK FIXED INCOME

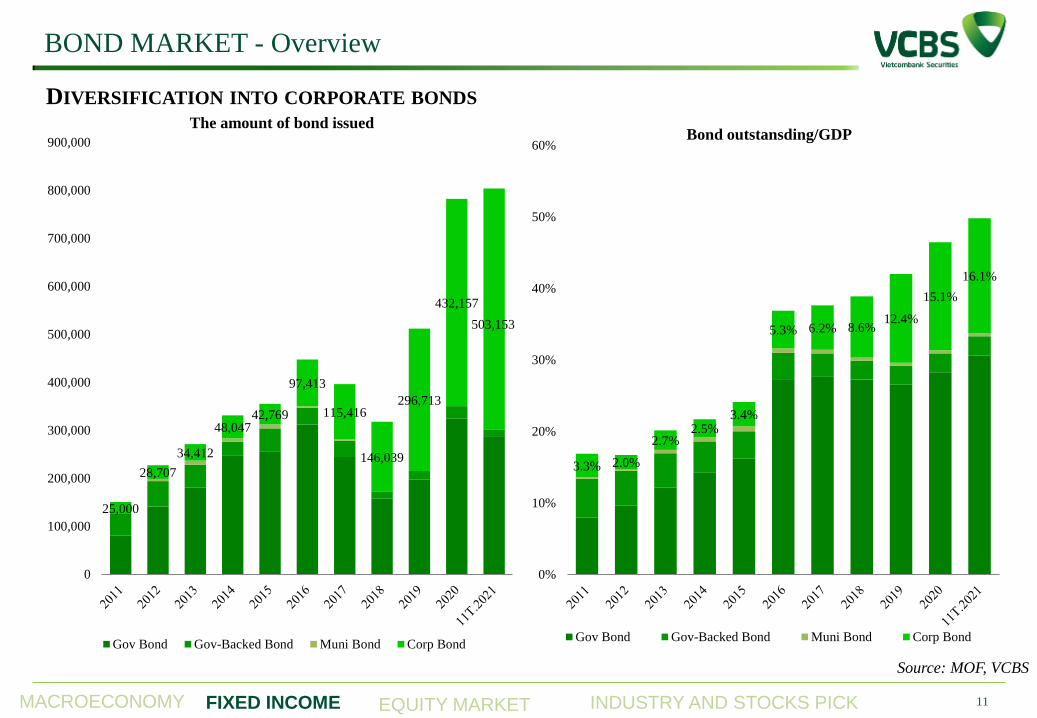

BOND MARKET - Overview

11

DIVERSIFICATION INTO CORPORATE BONDS

Source: MOF, VCBS

25,000

28,707

34,412

48,047 42,769

97,413

115,416

146,039

296,713

432,157

503,153

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

The amount of bond issued

Gov Bond Gov-Backed Bond Muni Bond Corp Bond

3.3% 2.0%

2.7% 2.5%

3.4%

5.3% 6.2% 8.6% 12.4%

15.1%

16.1%

0%

10%

20%

30%

40%

50%

60%Bond outstansding/GDP

Gov Bond Gov-Backed Bond Muni Bond Corp Bond

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

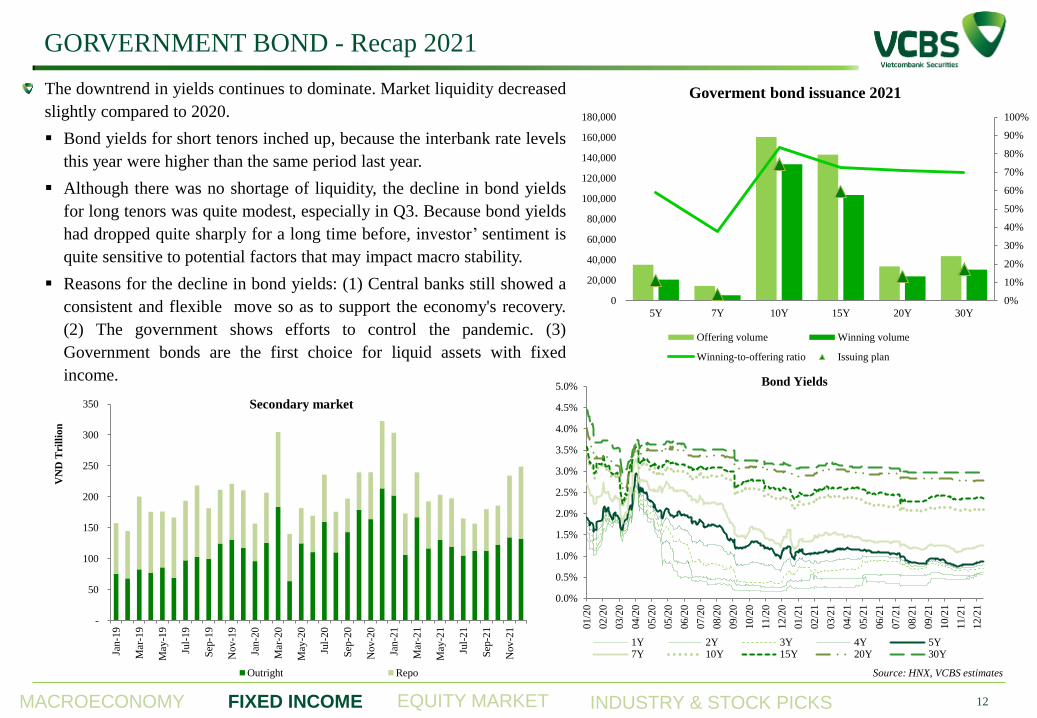

GORVERNMENT BOND - Recap 2021

12

Source: HNX, VCBS estimates

The downtrend in yields continues to dominate. Market liquidity decreased

slightly compared to 2020.

Bond yields for short tenors inched up, because the interbank rate levels

this year were higher than the same period last year.

Although there was no shortage of liquidity, the decline in bond yields

for long tenors was quite modest, especially in Q3. Because bond yields

had dropped quite sharply for a long time before, investor’ sentiment is

quite sensitive to potential factors that may impact macro stability.

Reasons for the decline in bond yields: (1) Central banks still showed a

consistent and flexible move so as to support the economy's recovery.

(2) The government shows efforts to control the pandemic. (3)

Government bonds are the first choice for liquid assets with fixed

income.

-

50

100

150

200

250

300

350

Jan-1

9

Mar

-19

May

-19

Jul-

19

Sep

-19

Nov

-19

Jan-2

0

Mar

-20

May

-20

Jul-

20

Sep

-20

Nov

-20

Jan-2

1

Mar

-21

May

-21

Jul-

21

Sep

-21

Nov

-21

VN

D T

ril

lio

n

Secondary market

Outright Repo

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

01

/20

02

/20

03

/20

04

/20

05

/20

05

/20

06

/20

07

/20

08

/20

09

/20

10

/20

11

/20

12

/20

01

/21

02

/21

03

/21

04

/21

05

/21

06

/21

07

/21

08

/21

09

/21

10

/21

11

/21

12

/21

Bond Yields

1Y 2Y 3Y 4Y 5Y7Y 10Y 15Y 20Y 30Y

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

5Y 7Y 10Y 15Y 20Y 30Y

Goverment bond issuance 2021

Offering volume Winning volume

Winning-to-offering ratio Issuing plan

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

INTERBANK RATES – Forecast 2022

13

Source: Bloomberg, VCBS estimates

In 2022, we expect stable liquidity, interbank rates may increase slightly by 20-50 bps compared to the levels in 2020-2021

Liquidity will be stable and abundant when Vietnam is an ideal destination for foreign capital flows.

The macroeconomic stability (inflation under control, stable exchange rate) will be factors to support liquidity.

However, liquidity is unlikely to be redundant as in 2020-2021 when resources in the next year will be focused on economic

activities to support businesses to recover from the pandemic.

Interbank rates are highly dependent on the SBV's management and orientation in the open market through repo and bills.

We expect liquidity will be stable and abundant, interbank rate levels may increase slightly, especially around certain times,

such as inflation pressure, seasonal effect.

Liquidity in the interbank market will remain stable and abundant. However, the average interest rates may increase slightly

Recap 2021

Interbank rates are under slight upward pressure,

but still at low levels and far away from OMO rate

(2.5%/year).

Liquidity in the market in 1H.2021 is not too

abundant when new resources can only appear on

the market from July after the forward contracts

are due and the State Bank changes the method of

buying foreign currency. Accordingly, in the

2H.2021, interbank rates have decreased again.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

02

/12/2

0

17

/12/2

0

01

/01/2

1

16

/01/2

1

31

/01/2

1

15

/02/2

1

02

/03/2

1

17

/03/2

1

01

/04/2

1

16

/04/2

1

01

/05/2

1

16

/05/2

1

31

/05/2

1

15

/06/2

1

30

/06/2

1

15

/07/2

1

30

/07/2

1

14

/08/2

1

29

/08/2

1

13

/09/2

1

28

/09/2

1

13

/10/2

1

28

/10/2

1

12

/11/2

1

27

/11/2

1

12

/12/2

1

27

/12/2

1

ON 1W 2W 1M

Interbank rates

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

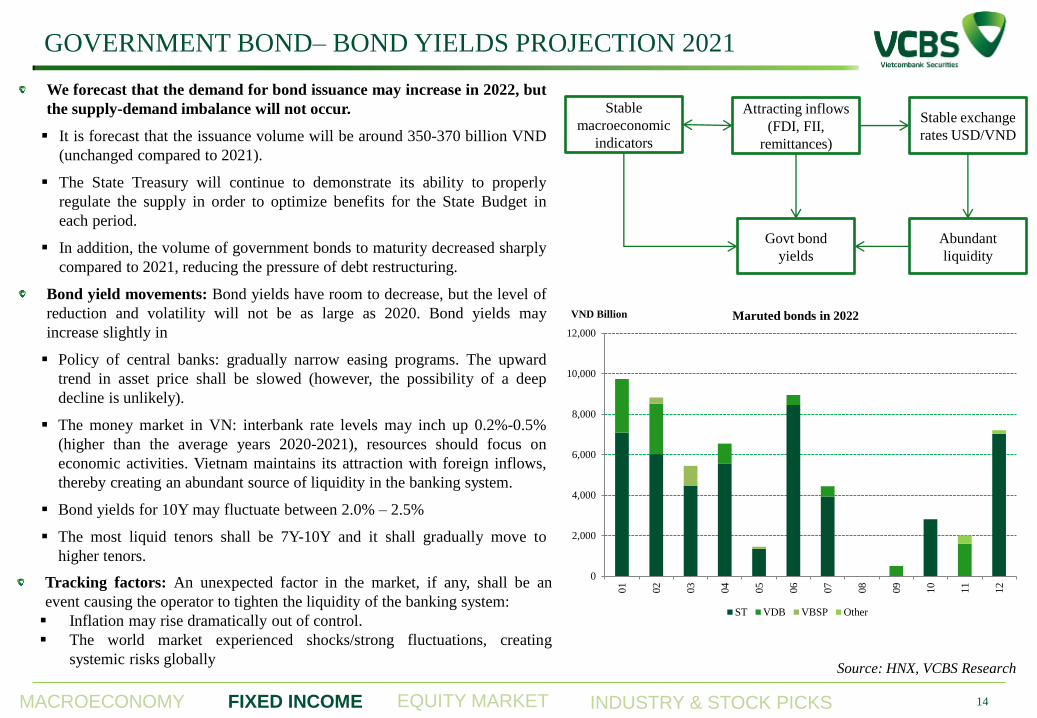

GOVERNMENT BOND– BOND YIELDS PROJECTION 2021

14

We forecast that the demand for bond issuance may increase in 2022, but

the supply-demand imbalance will not occur.

It is forecast that the issuance volume will be around 350-370 billion VND

(unchanged compared to 2021).

The State Treasury will continue to demonstrate its ability to properly

regulate the supply in order to optimize benefits for the State Budget in

each period.

In addition, the volume of government bonds to maturity decreased sharply

compared to 2021, reducing the pressure of debt restructuring.

Bond yield movements: Bond yields have room to decrease, but the level of

reduction and volatility will not be as large as 2020. Bond yields may

increase slightly in

Policy of central banks: gradually narrow easing programs. The upward

trend in asset price shall be slowed (however, the possibility of a deep

decline is unlikely).

The money market in VN: interbank rate levels may inch up 0.2%-0.5%

(higher than the average years 2020-2021), resources should focus on

economic activities. Vietnam maintains its attraction with foreign inflows,

thereby creating an abundant source of liquidity in the banking system.

Bond yields for 10Y may fluctuate between 2.0% – 2.5%

The most liquid tenors shall be 7Y-10Y and it shall gradually move to

higher tenors.

Source: HNX, VCBS Research

Stable

macroeconomic

indicators

Attracting inflows

(FDI, FII,

remittances)

Stable exchange

rates USD/VND

Abundant

liquidity

Govt bond

yields

Tracking factors: An unexpected factor in the market, if any, shall be an

event causing the operator to tighten the liquidity of the banking system:

Inflation may rise dramatically out of control.

The world market experienced shocks/strong fluctuations, creating

systemic risks globally

0

2,000

4,000

6,000

8,000

10,000

12,000

01

02

03

04

05

06

07

08

09

10

11

12

VND Billion Maruted bonds in 2022

ST VDB VBSP Other

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME 15

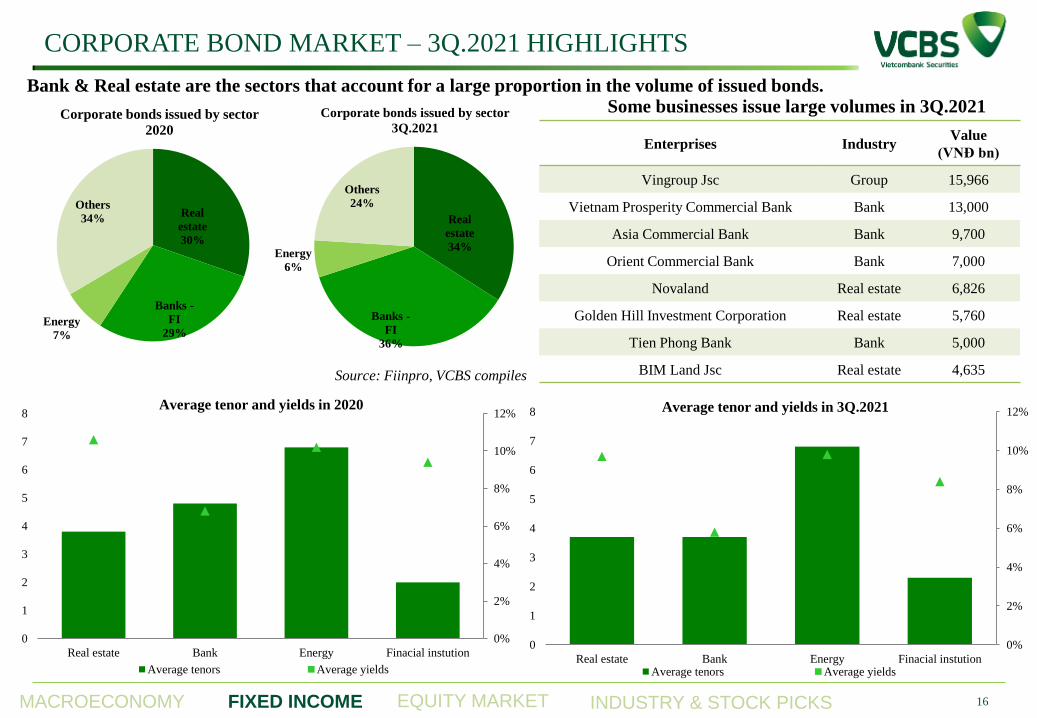

Source: Fiinpro, VCBS compiles

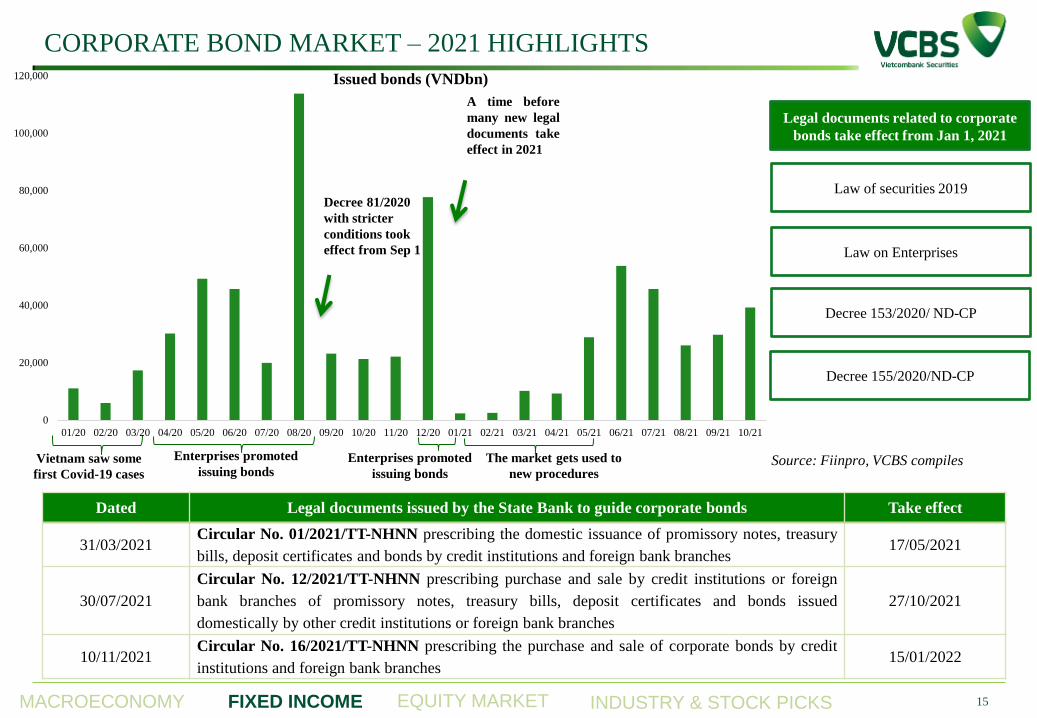

CORPORATE BOND MARKET – 2021 HIGHLIGHTS

Enterprises promoted

issuing bonds

Decree 81/2020

with stricter

conditions took

effect from Sep 1

Vietnam saw some

first Covid-19 cases

A time before

many new legal

documents take

effect in 2021

The market gets used to

new procedures Enterprises promoted

issuing bonds

0

20,000

40,000

60,000

80,000

100,000

120,000

01/20 02/20 03/20 04/20 05/20 06/20 07/20 08/20 09/20 10/20 11/20 12/20 01/21 02/21 03/21 04/21 05/21 06/21 07/21 08/21 09/21 10/21

Issued bonds (VNDbn)

Legal documents related to corporate

bonds take effect from Jan 1, 2021

Law of securities 2019

Law on Enterprises

Decree 153/2020/ ND-CP

Decree 155/2020/ND-CP

Dated Legal documents issued by the State Bank to guide corporate bonds Take effect

31/03/2021 Circular No. 01/2021/TT-NHNN prescribing the domestic issuance of promissory notes, treasury

bills, deposit certificates and bonds by credit institutions and foreign bank branches 17/05/2021

30/07/2021

Circular No. 12/2021/TT-NHNN prescribing purchase and sale by credit institutions or foreign

bank branches of promissory notes, treasury bills, deposit certificates and bonds issued

domestically by other credit institutions or foreign bank branches

27/10/2021

10/11/2021 Circular No. 16/2021/TT-NHNN prescribing the purchase and sale of corporate bonds by credit

institutions and foreign bank branches 15/01/2022

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME 16

Bank & Real estate are the sectors that account for a large proportion in the volume of issued bonds.

Source: Fiinpro, VCBS compiles

0%

2%

4%

6%

8%

10%

12%

0

1

2

3

4

5

6

7

8

Real estate Bank Energy Finacial instution

Average tenor and yields in 2020

Average tenors Average yields

CORPORATE BOND MARKET – 3Q.2021 HIGHLIGHTS

0%

2%

4%

6%

8%

10%

12%

0

1

2

3

4

5

6

7

8

Real estate Bank Energy Finacial instution

Average tenor and yields in 3Q.2021

Average tenors Average yields

Real

estate

30%

Banks -

FI

29% Energy

7%

Others

34%

Corporate bonds issued by sector

2020

Real

estate

34%

Banks -

FI

36%

Energy

6%

Others

24%

Corporate bonds issued by sector

3Q.2021

Some businesses issue large volumes in 3Q.2021

Enterprises Industry Value

(VNĐ bn)

Vingroup Jsc Group 15,966

Vietnam Prosperity Commercial Bank Bank 13,000

Asia Commercial Bank Bank 9,700

Orient Commercial Bank Bank 7,000

Novaland Real estate 6,826

Golden Hill Investment Corporation Real estate 5,760

Tien Phong Bank Bank 5,000

BIM Land Jsc Real estate 4,635

MACROECONOMY

FIXED INCOME MARKET

EQUITY MARKET

INDUSTRY AND STOCK PICKS

UPDATES ON

COMMODITIES PRICE

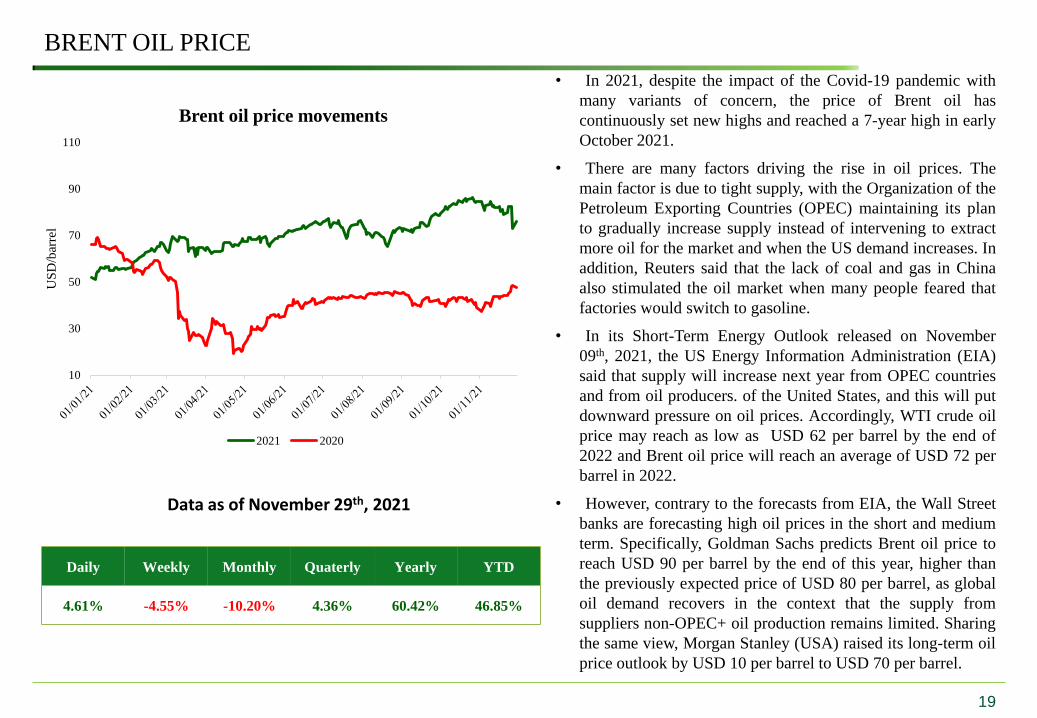

BRENT OIL PRICE

19

Daily Weekly Monthly Quaterly Yearly YTD

4.61% -4.55% -10.20% 4.36% 60.42% 46.85%

Data as of November 29th, 2021

• In 2021, despite the impact of the Covid-19 pandemic with

many variants of concern, the price of Brent oil has

continuously set new highs and reached a 7-year high in early

October 2021.

• There are many factors driving the rise in oil prices. The

main factor is due to tight supply, with the Organization of the

Petroleum Exporting Countries (OPEC) maintaining its plan

to gradually increase supply instead of intervening to extract

more oil for the market and when the US demand increases. In

addition, Reuters said that the lack of coal and gas in China

also stimulated the oil market when many people feared that

factories would switch to gasoline.

• In its Short-Term Energy Outlook released on November

09th, 2021, the US Energy Information Administration (EIA)

said that supply will increase next year from OPEC countries

and from oil producers. of the United States, and this will put

downward pressure on oil prices. Accordingly, WTI crude oil

price may reach as low as USD 62 per barrel by the end of

2022 and Brent oil price will reach an average of USD 72 per

barrel in 2022.

• However, contrary to the forecasts from EIA, the Wall Street

banks are forecasting high oil prices in the short and medium

term. Specifically, Goldman Sachs predicts Brent oil price to

reach USD 90 per barrel by the end of this year, higher than

the previously expected price of USD 80 per barrel, as global

oil demand recovers in the context that the supply from

suppliers non-OPEC+ oil production remains limited. Sharing

the same view, Morgan Stanley (USA) raised its long-term oil

price outlook by USD 10 per barrel to USD 70 per barrel.

10

30

50

70

90

110

US

D/b

arre

l

Brent oil price movements

2021 2020

STEEL

20

Daily Weekly Monthly Quaterly Yearly YTD

-0.40% 1.49% -9.44% -9.66% 21.43% 13.16%

• China's spot steel price has increased sharply since Q4.2020

and maintained this upward trend until May 2021, reaching the

highest level since mid-2008. Recently, although it has slowed

down, the average steel price worldwide demand has reached

USD 711 per ton, more than 21% higher comparing to the price

of only USD 582 per ton last year.

• Meanwhile, iron ore prices in 2021 and the following years are

forecasted to continue to decline due to increased supply but

reduced demand. Iron ore prices on the Chinese market on

November 18th, 2021, fell to the lowest level in more than a

year due to the gloomy demand outlook for steel and steel

materials in the world's second largest steel producer.

• Many different opinions on the prospect of steel prices in the

coming period was made. Specifically, the international

financial rating agency of Fitch Solutions forecasts an average

global steel price of USD 600 per ton in 2022 and USD 535 per

ton in 2023-2025. Steel demand growth will slow down in

China and increasing protectionism in the global steel market

will boost steel production in affected countries. The

combination of these two factors will help the steel market

loosen and drag prices down in the medium term

• The World Steel Association (Worldsteel) forecasts the steel

demand to grow 4.5% in 2021 and reach 1,855 million tons

after 0.1% growth in 2020; will then increase by 2.2% to 1,896

million tons in 2022. These figures assume that positive

progress in COVID-19 vaccination programs will weaken the

epidemic, the spread of variants of the SARS-CoV-2 virus will

cause less damages and disrupting supply chains than previous

waves.

Data as of November 29th, 2021

450

550

650

750

850

950

1,050

CN

Y/t

on

Steel price movements

2021 2020

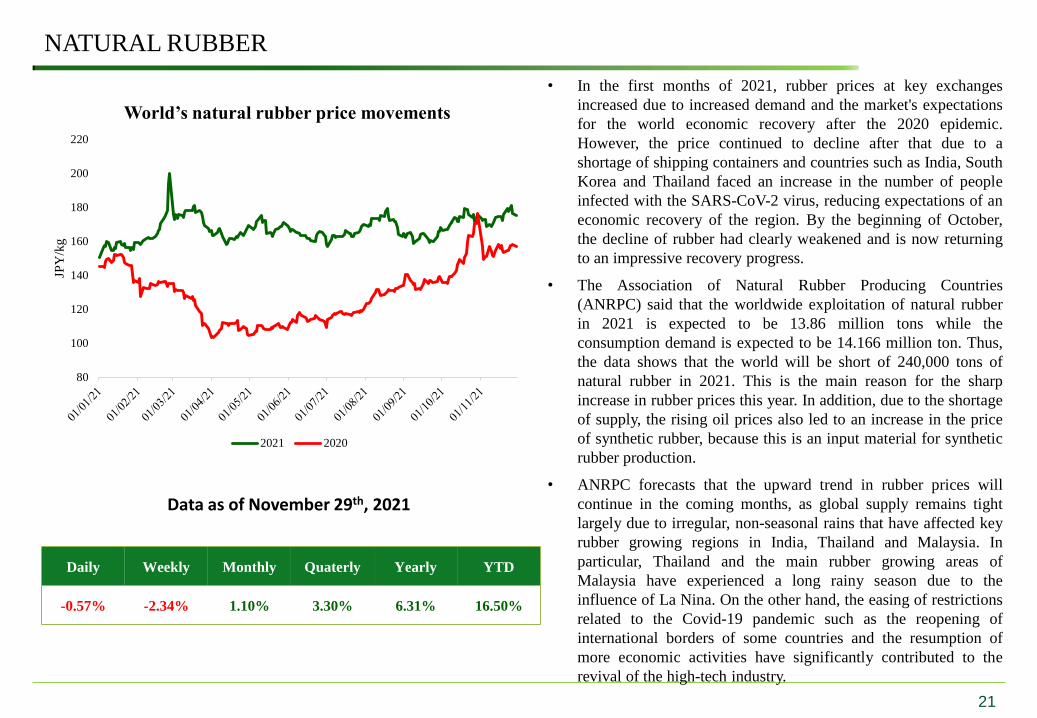

NATURAL RUBBER

21

Daily Weekly Monthly Quaterly Yearly YTD

-0.57% -2.34% 1.10% 3.30% 6.31% 16.50%

• In the first months of 2021, rubber prices at key exchanges

increased due to increased demand and the market's expectations

for the world economic recovery after the 2020 epidemic.

However, the price continued to decline after that due to a

shortage of shipping containers and countries such as India, South

Korea and Thailand faced an increase in the number of people

infected with the SARS-CoV-2 virus, reducing expectations of an

economic recovery of the region. By the beginning of October,

the decline of rubber had clearly weakened and is now returning

to an impressive recovery progress.

• The Association of Natural Rubber Producing Countries

(ANRPC) said that the worldwide exploitation of natural rubber

in 2021 is expected to be 13.86 million tons while the

consumption demand is expected to be 14.166 million ton. Thus,

the data shows that the world will be short of 240,000 tons of

natural rubber in 2021. This is the main reason for the sharp

increase in rubber prices this year. In addition, due to the shortage

of supply, the rising oil prices also led to an increase in the price

of synthetic rubber, because this is an input material for synthetic

rubber production.

• ANRPC forecasts that the upward trend in rubber prices will

continue in the coming months, as global supply remains tight

largely due to irregular, non-seasonal rains that have affected key

rubber growing regions in India, Thailand and Malaysia. In

particular, Thailand and the main rubber growing areas of

Malaysia have experienced a long rainy season due to the

influence of La Nina. On the other hand, the easing of restrictions

related to the Covid-19 pandemic such as the reopening of

international borders of some countries and the resumption of

more economic activities have significantly contributed to the

revival of the high-tech industry.

Data as of November 29th, 2021

80

100

120

140

160

180

200

220

JPY

/kg

World’s natural rubber price movements

2021 2020

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

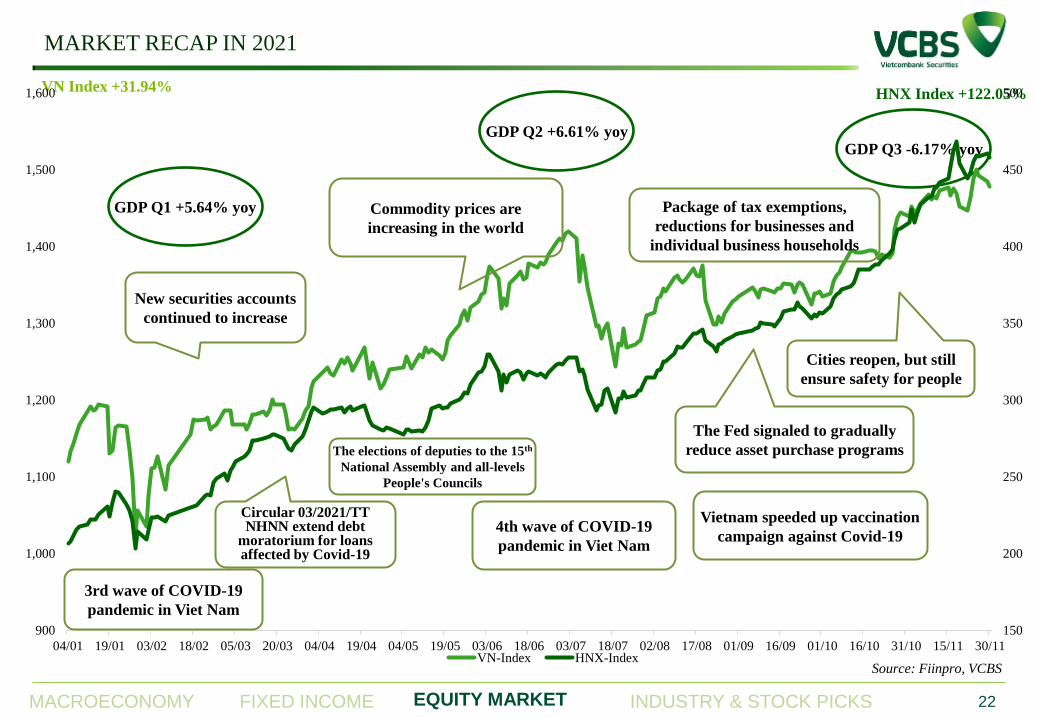

MARKET RECAP IN 2021

22

Source: Fiinpro, VCBS

VN Index +31.94% HNX Index +122.05%

GDP Q3 -6.17% yoy

150

200

250

300

350

400

450

500

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

04/01 19/01 03/02 18/02 05/03 20/03 04/04 19/04 04/05 19/05 03/06 18/06 03/07 18/07 02/08 17/08 01/09 16/09 01/10 16/10 31/10 15/11 30/11VN-Index HNX-Index

4th wave of COVID-19

pandemic in Viet Nam

New securities accounts

continued to increase

Commodity prices are

increasing in the world

Vietnam speeded up vaccination

campaign against Covid-19

The Fed signaled to gradually

reduce asset purchase programs

Package of tax exemptions,

reductions for businesses and

individual business households

Cities reopen, but still

ensure safety for people

3rd wave of COVID-19

pandemic in Viet Nam

GDP Q2 +6.61% yoy

GDP Q1 +5.64% yoy

The elections of deputies to the 15th

National Assembly and all-levels

People's Councils

Circular 03/2021/TT NHNN extend debt

moratorium for loans affected by Covid-19

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

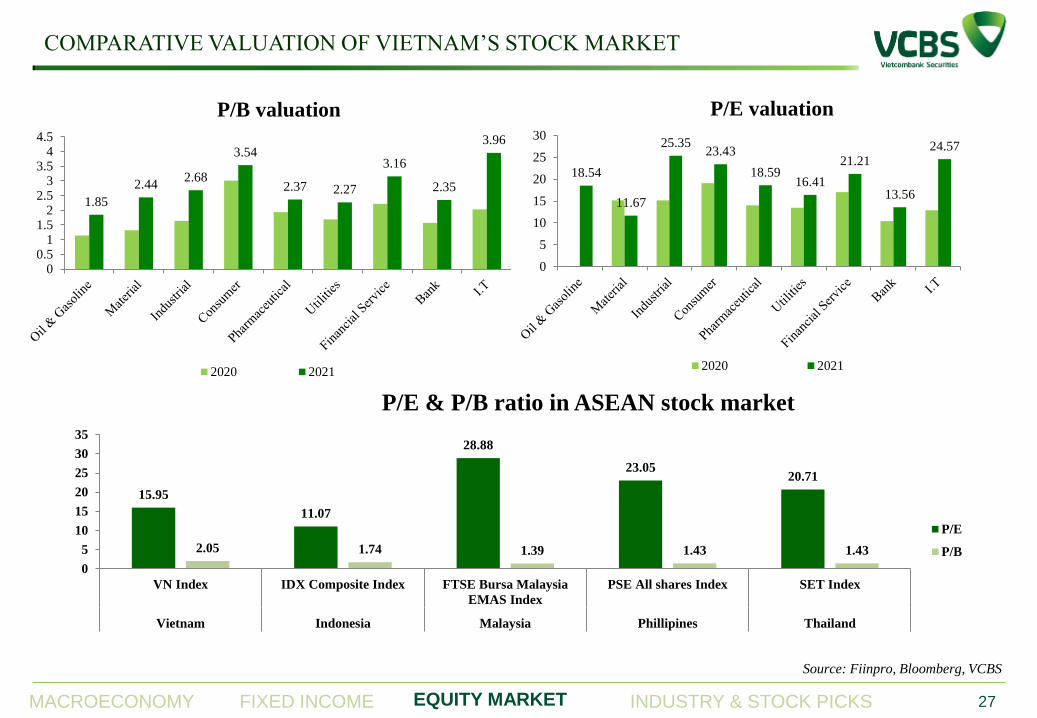

COMPARATIVE VALUATION OF VIETNAM’S STOCK MARKET

27

Source: Fiinpro, Bloomberg, VCBS

15.95

11.07

28.88

23.05 20.71

2.05 1.74 1.39 1.43 1.43

0

5

10

15

20

25

30

35

VN Index IDX Composite Index FTSE Bursa Malaysia

EMAS Index

PSE All shares Index SET Index

Vietnam Indonesia Malaysia Phillipines Thailand

P/E & P/B ratio in ASEAN stock market

P/E

P/B

1.85

2.44 2.68

3.54

2.37 2.27

3.16

2.35

3.96

00.5

11.5

22.5

33.5

44.5

P/B valuation

2020 2021

18.54

11.67

25.35 23.43

18.59 16.41

21.21

13.56

24.57

0

5

10

15

20

25

30

P/E valuation

2020 2021

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

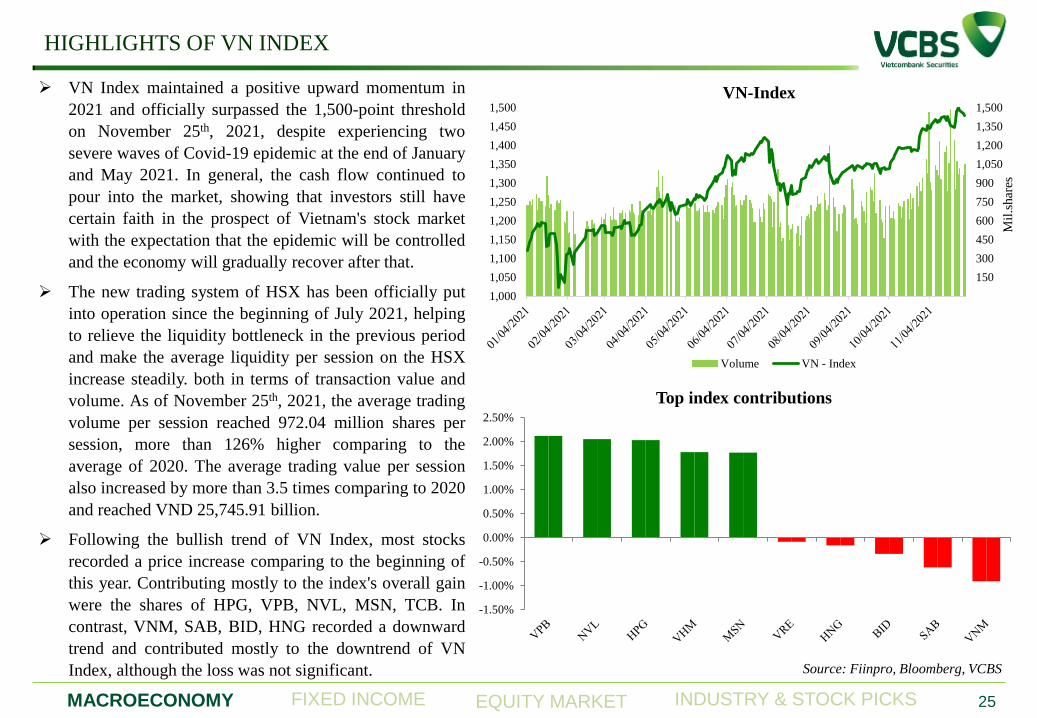

HIGHLIGHTS OF VN INDEX

25

Source: Fiinpro, Bloomberg, VCBS

VN Index maintained a positive upward momentum in

2021 and officially surpassed the 1,500-point threshold

on November 25th, 2021, despite experiencing two

severe waves of Covid-19 epidemic at the end of January

and May 2021. In general, the cash flow continued to

pour into the market, showing that investors still have

certain faith in the prospect of Vietnam's stock market

with the expectation that the epidemic will be controlled

and the economy will gradually recover after that.

The new trading system of HSX has been officially put

into operation since the beginning of July 2021, helping

to relieve the liquidity bottleneck in the previous period

and make the average liquidity per session on the HSX

increase steadily. both in terms of transaction value and

volume. As of November 25th, 2021, the average trading

volume per session reached 972.04 million shares per

session, more than 126% higher comparing to the

average of 2020. The average trading value per session

also increased by more than 3.5 times comparing to 2020

and reached VND 25,745.91 billion.

Following the bullish trend of VN Index, most stocks

recorded a price increase comparing to the beginning of

this year. Contributing mostly to the index's overall gain

were the shares of HPG, VPB, NVL, MSN, TCB. In

contrast, VNM, SAB, BID, HNG recorded a downward

trend and contributed mostly to the downtrend of VN

Index, although the loss was not significant.

150

300

450

600

750

900

1,050

1,200

1,350

1,500

1,000

1,050

1,100

1,150

1,200

1,250

1,300

1,350

1,400

1,450

1,500

Mil

.shar

es

VN-Index

Volume VN - Index

-1.50%

-1.00%

-0.50%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

Top index contributions

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

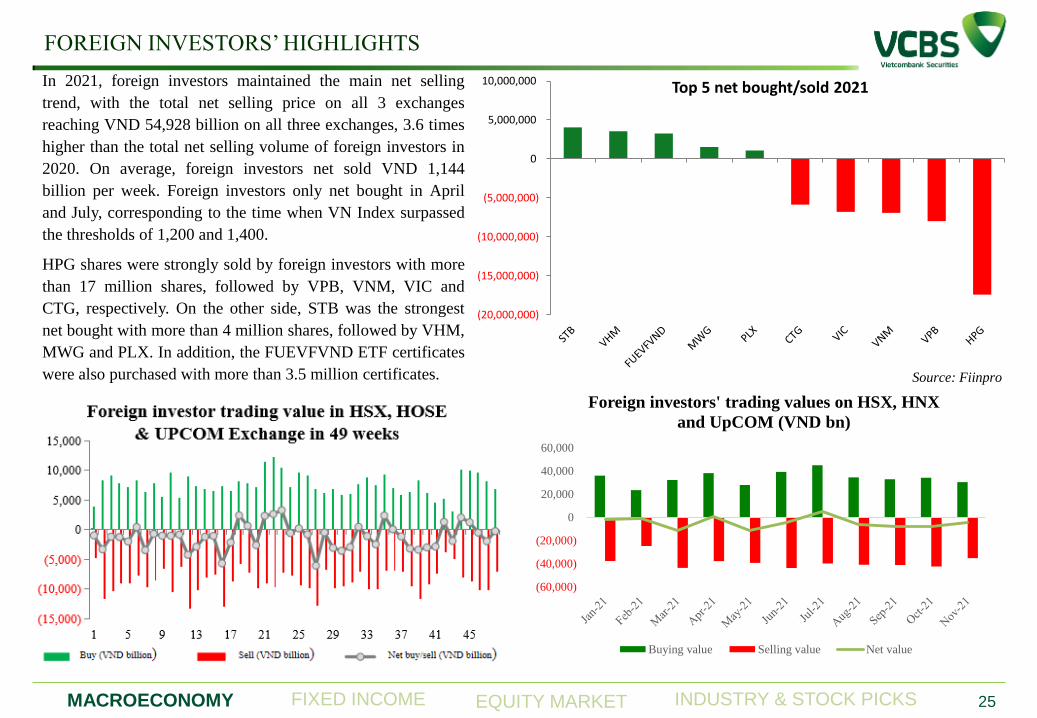

FOREIGN INVESTORS’ HIGHLIGHTS

25

Source: Fiinpro

In 2021, foreign investors maintained the main net selling

trend, with the total net selling price on all 3 exchanges

reaching VND 54,928 billion on all three exchanges, 3.6 times

higher than the total net selling volume of foreign investors in

2020. On average, foreign investors net sold VND 1,144

billion per week. Foreign investors only net bought in April

and July, corresponding to the time when VN Index surpassed

the thresholds of 1,200 and 1,400.

HPG shares were strongly sold by foreign investors with more

than 17 million shares, followed by VPB, VNM, VIC and

CTG, respectively. On the other side, STB was the strongest

net bought with more than 4 million shares, followed by VHM,

MWG and PLX. In addition, the FUEVFVND ETF certificates

were also purchased with more than 3.5 million certificates.

(20,000,000)

(15,000,000)

(10,000,000)

(5,000,000)

0

5,000,000

10,000,000 Top 5 net bought/sold 2021

(60,000)

(40,000)

(20,000)

0

20,000

40,000

60,000

Foreign investors' trading values on HSX, HNX

and UpCOM (VND bn)

Buying value Selling value Net value

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

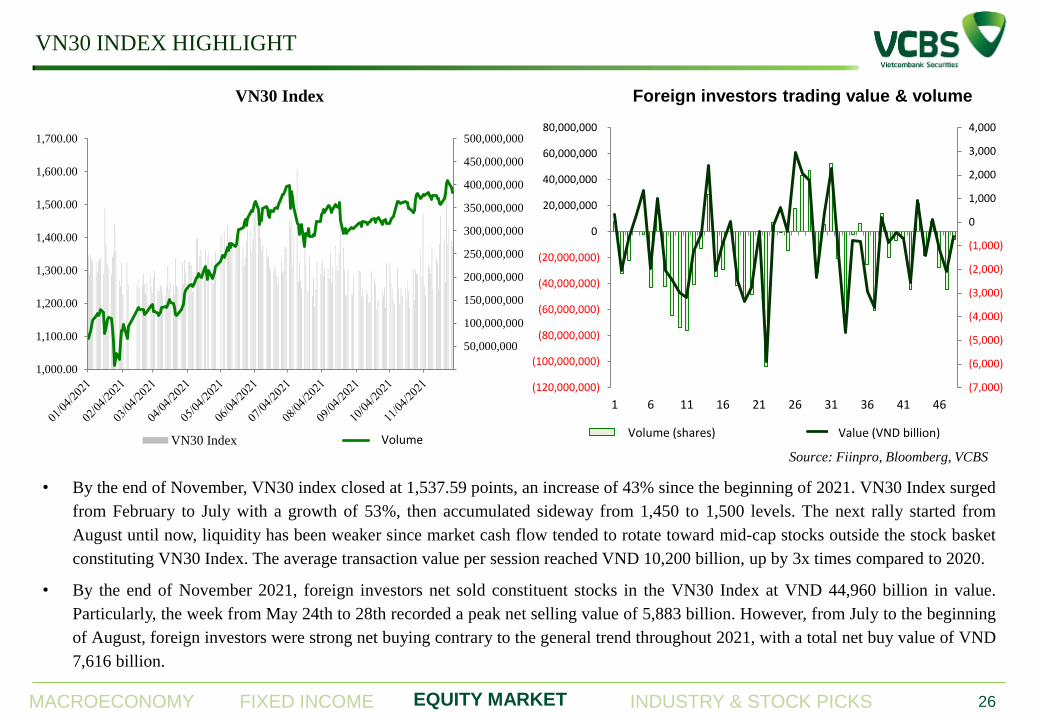

VN30 INDEX HIGHLIGHT

26

Source: Fiinpro, Bloomberg, VCBS

• By the end of November, VN30 index closed at 1,537.59 points, an increase of 43% since the beginning of 2021. VN30 Index surged

from February to July with a growth of 53%, then accumulated sideway from 1,450 to 1,500 levels. The next rally started from

August until now, liquidity has been weaker since market cash flow tended to rotate toward mid-cap stocks outside the stock basket

constituting VN30 Index. The average transaction value per session reached VND 10,200 billion, up by 3x times compared to 2020.

• By the end of November 2021, foreign investors net sold constituent stocks in the VN30 Index at VND 44,960 billion in value.

Particularly, the week from May 24th to 28th recorded a peak net selling value of 5,883 billion. However, from July to the beginning

of August, foreign investors were strong net buying contrary to the general trend throughout 2021, with a total net buy value of VND

7,616 billion.

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

350,000,000

400,000,000

450,000,000

500,000,000

1,000.00

1,100.00

1,200.00

1,300.00

1,400.00

1,500.00

1,600.00

1,700.00

VN30 Index

VN30 Index Đóng cửa

(7,000)

(6,000)

(5,000)

(4,000)

(3,000)

(2,000)

(1,000)

0

1,000

2,000

3,000

4,000

(120,000,000)

(100,000,000)

(80,000,000)

(60,000,000)

(40,000,000)

(20,000,000)

0

20,000,000

40,000,000

60,000,000

80,000,000

1 6 11 16 21 26 31 36 41 46

Foreign investors trading value & volume

Khối lượng ròng(CP) Giá trị ròng(tỷ VNĐ) Volume

Volume (shares) Value (VND billion)

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

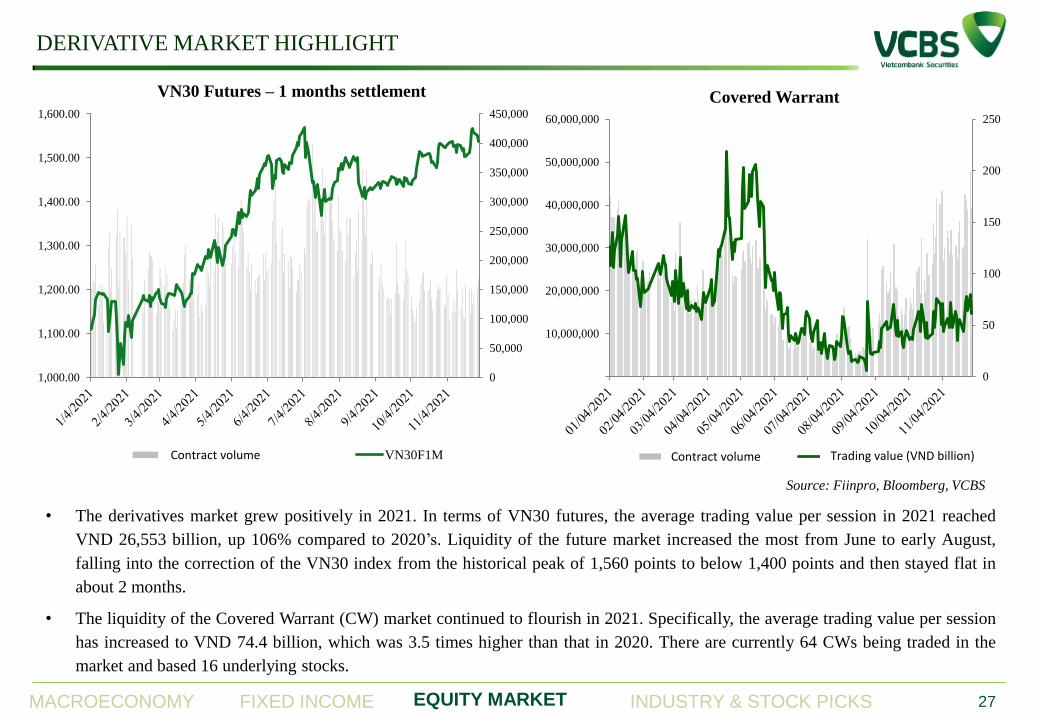

DERIVATIVE MARKET HIGHLIGHT

27

Source: Fiinpro, Bloomberg, VCBS

• The derivatives market grew positively in 2021. In terms of VN30 futures, the average trading value per session in 2021 reached

VND 26,553 billion, up 106% compared to 2020’s. Liquidity of the future market increased the most from June to early August,

falling into the correction of the VN30 index from the historical peak of 1,560 points to below 1,400 points and then stayed flat in

about 2 months.

• The liquidity of the Covered Warrant (CW) market continued to flourish in 2021. Specifically, the average trading value per session

has increased to VND 74.4 billion, which was 3.5 times higher than that in 2020. There are currently 64 CWs being traded in the

market and based 16 underlying stocks.

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

1,000.00

1,100.00

1,200.00

1,300.00

1,400.00

1,500.00

1,600.00

VN30 Futures – 1 months settlement

KLGD (Hợp đồng) VN30F1M

0

50

100

150

200

250

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

Covered Warrant

KLGD GTGD (tỷ đồng) Contract volume Contract volume Trading value (VND billion)

STOCK MARKET

OUTLOOK IN 2022

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

In 2022, we forecast that Vietnam's economy will gradually regain the economic growth momentum as in the pre-

epidemic period, but along with higher inflation. Deposit rates may increase slightly; however, still stay at low levels

thanks to abundant liquidity in the banking system.

In such a context, the stock market continues to be an attractive investment channel - especially for individual

investors. Although we expect inflow from domestic investors to have a certain growth in 2022, it will be less

exciting than in 2021. It is because the price level of stocks is already at a higher level than that at the beginning of

2021, and the recovery of the economy also opens up other options for domestic investors to invest. Thus, we

forecast that the highest peak of VN Index in 2022 may reach 1,580 – 1,600 points, equivalent to an increase of

6-8% compared to the peak of 2021.

The new trading system of HSX has been officially put into commission since July 2021, which has helped remove

the "bottleneck" in order-matching liquidity on the HSX. It is difficult to record an "explosive" increase like in the

second half of 2021. However, we forecast that the upward trend in liquidity will continue in 2022. In specific,

2022’s average trading volume is forecasted to increase slightly compared to 2021’s, reaching over 1 billion

shares per session on all three exchanges, equivalent to an increase of about 8-10% yoy. The average trading

value in 2022 is expected to increase by 17-20% compared to 2021, corresponding to about 28,000-30,000

billion VND per session on all three exchanges.

FORECAST OF VN INDEX IN 2022

29

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

INVESTMENT SUGGESTIONS IN 2022

30

“PANNING FOR GOLD”

Covid-19 epidemic has put the Vietnam’s economy through a period of changes, both inside the domestic economy as well as

in the global economic context. Vietnam’s government has been implementing many measures to both restore production in the

context of the "new normal" and reform the nation’s economic development model. On the other hand, major economies in the

world are also gradually innovate their "growth engines" towards the goal of a more environment-friendly economy as well as

bringing better equality among people. In such a scenario, we expect that Vietnam’s stock market will face a high level of

volatility in 2022 with many short bullish waves interspersed with bearish shocks, although the overall trend is still going up.

We also expect that the polarization among stocks - which started

in Q4.2021 - will continue. Therefore, investment opportunities

in 2022 will need to be more selective and go deeper into each

listed company, based on business results as well as growth

prospects in the context of "new normal" economy. Some of the

investment suggestions that we introduce in 2022 will be:

Real estate businesses with a big land bank and strong finance,

as well as having a clear growth target in 2022;

Private joint stock commercial banks maintained a growth rate

higher than the industry average - especially small-sized ones;

Retail businesses of luxury goods witnessing customers’

demand bounce back after social distancing period;

A number of companies operating in resource-exploitation-related industries such as crude oil extracting, cement, mining and

processing of non-ferrous metal,...

Finally, a few large-cap stocks can lead the trend of the overall market for some time and create short bullish waves of VN

Index.

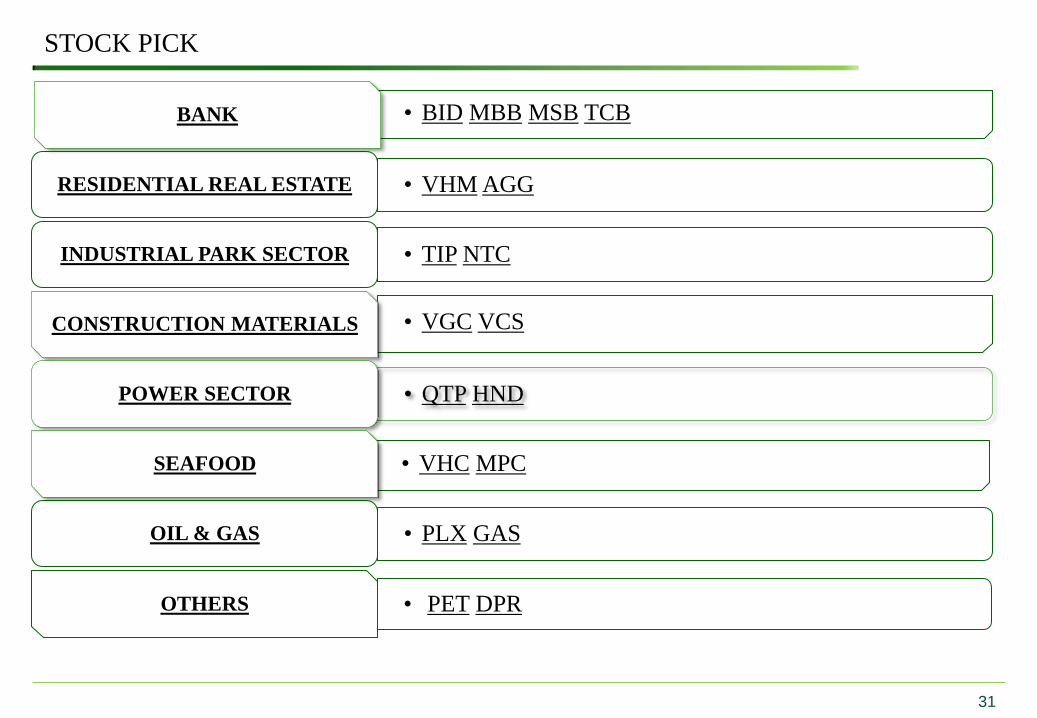

STOCK PICK

31

• BID MBB MSB TCB BANK

• VHM AGG RESIDENTIAL REAL ESTATE

• TIP NTC INDUSTRIAL PARK SECTOR

• VGC VCS CONSTRUCTION MATERIALS

• QTP HND POWER SECTOR

• VHC MPC SEAFOOD

• PLX GAS OIL & GAS

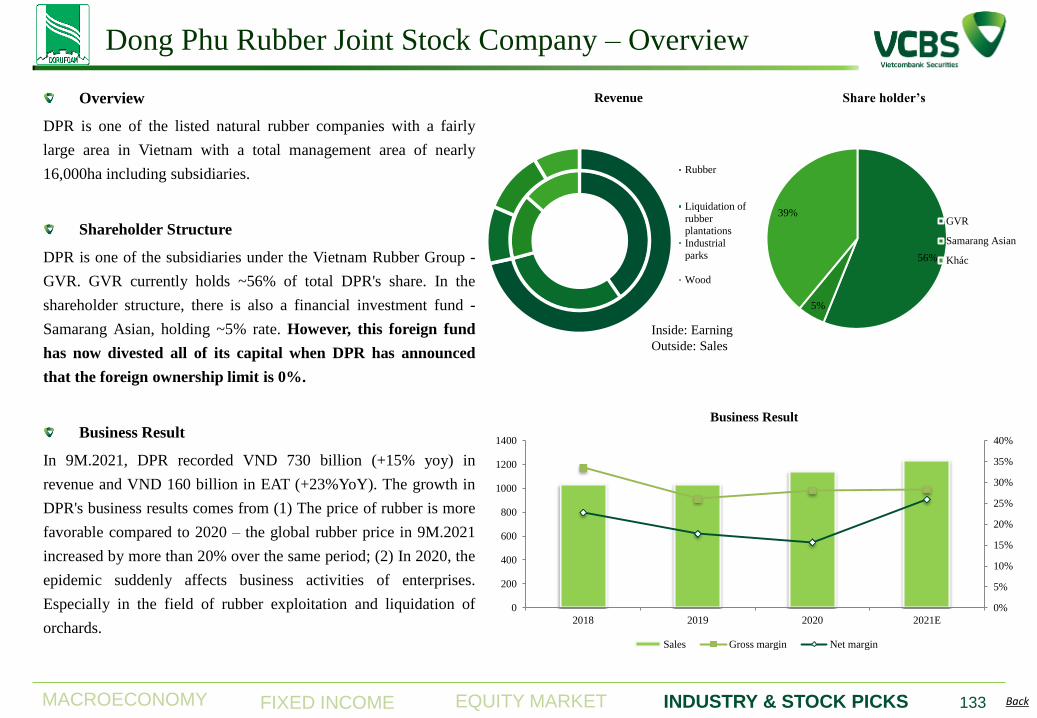

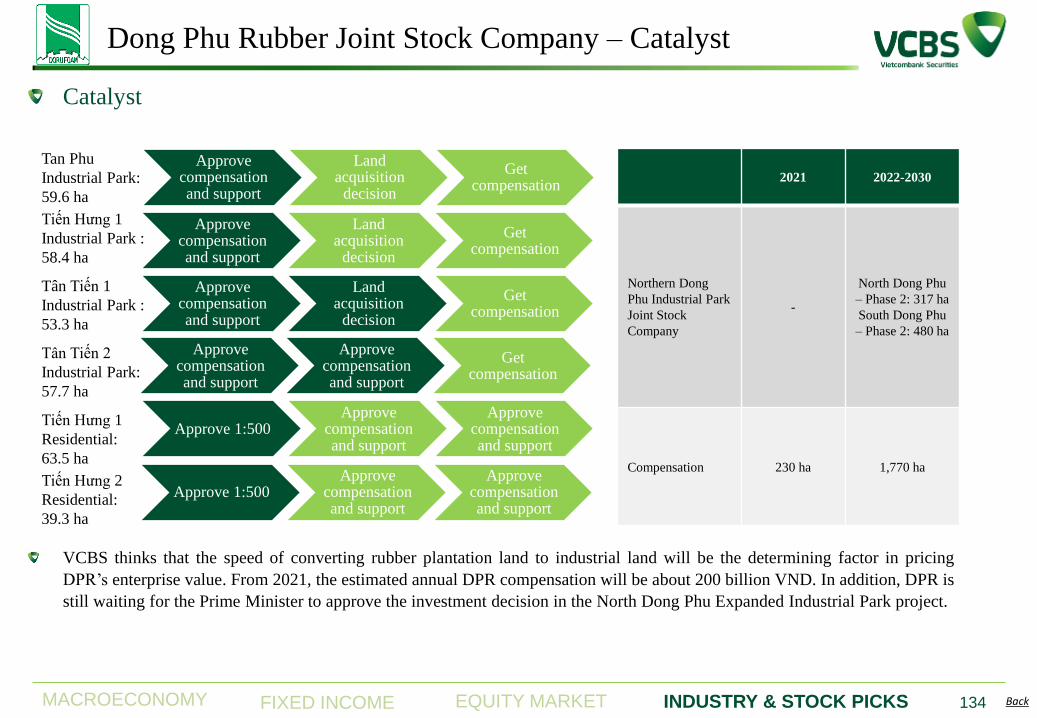

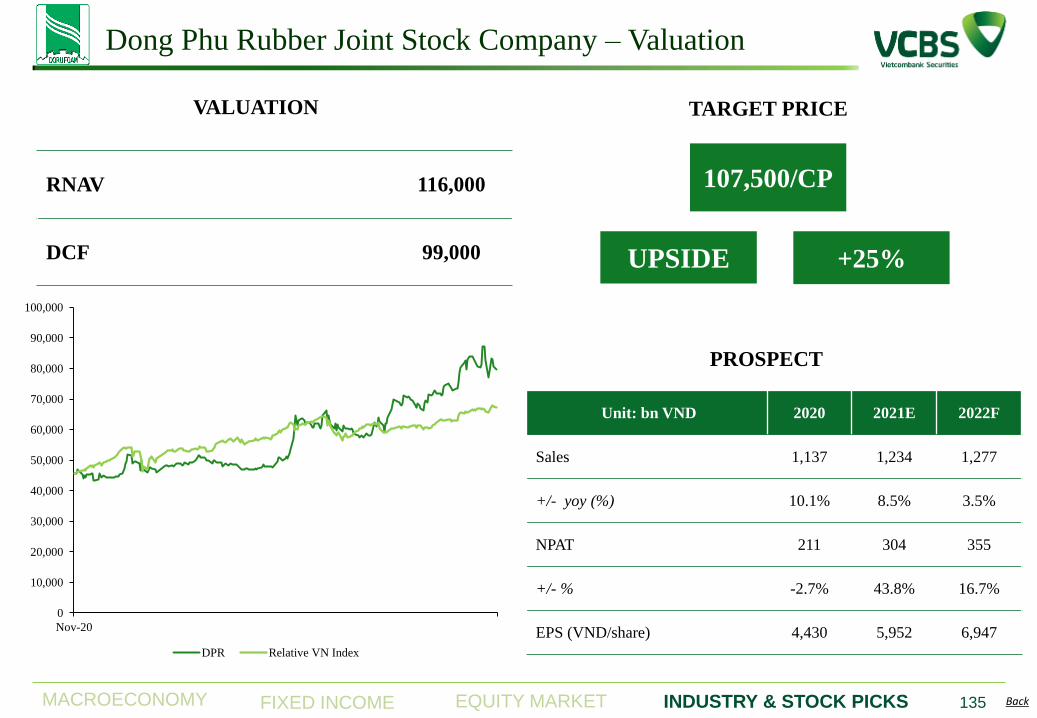

• PET DPR OTHERS

BANKING SECTOR

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

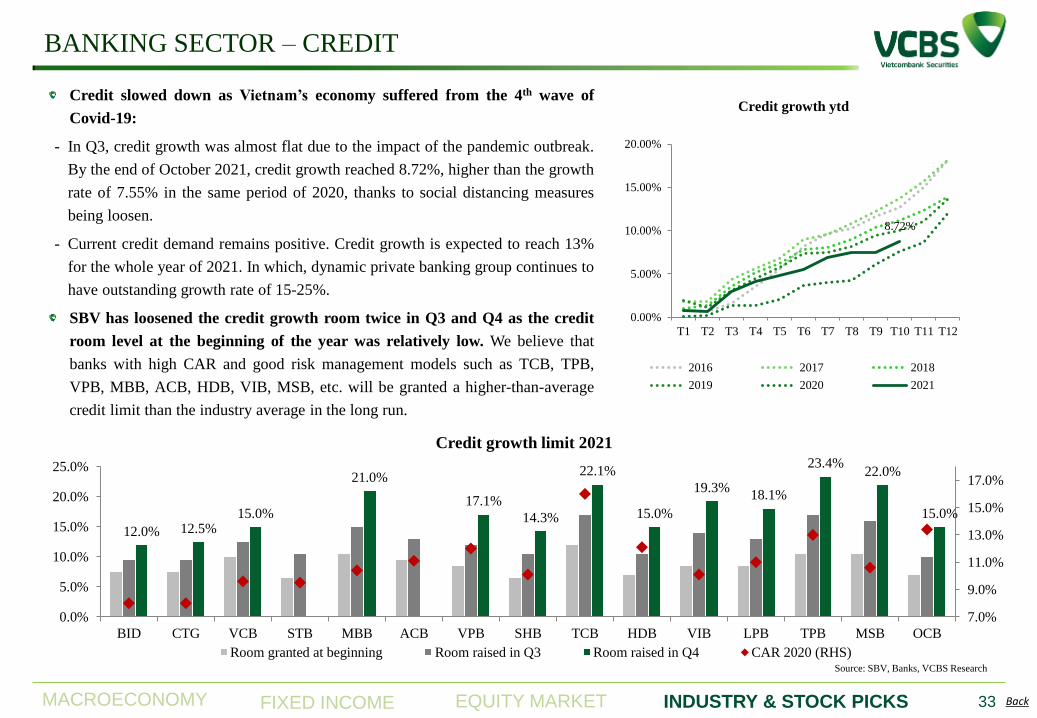

BANKING SECTOR – CREDIT

Credit slowed down as Vietnam’s economy suffered from the 4th wave of

Covid-19:

- In Q3, credit growth was almost flat due to the impact of the pandemic outbreak.

By the end of October 2021, credit growth reached 8.72%, higher than the growth

rate of 7.55% in the same period of 2020, thanks to social distancing measures

being loosen.

- Current credit demand remains positive. Credit growth is expected to reach 13%

for the whole year of 2021. In which, dynamic private banking group continues to

have outstanding growth rate of 15-25%.

SBV has loosened the credit growth room twice in Q3 and Q4 as the credit

room level at the beginning of the year was relatively low. We believe that

banks with high CAR and good risk management models such as TCB, TPB,

VPB, MBB, ACB, HDB, VIB, MSB, etc. will be granted a higher-than-average

credit limit than the industry average in the long run.

8.72%

0.00%

5.00%

10.00%

15.00%

20.00%

T1 T2 T3 T4 T5 T6 T7 T8 T9 T10 T11 T12

Credit growth ytd

2016 2017 2018

2019 2020 2021

Source: SBV, Banks, VCBS Research

12.0% 12.5% 15.0%

21.0%

17.1%

14.3%

22.1%

15.0%

19.3% 18.1%

23.4% 22.0%

15.0%

7.0%

9.0%

11.0%

13.0%

15.0%

17.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

BID CTG VCB STB MBB ACB VPB SHB TCB HDB VIB LPB TPB MSB OCB

Credit growth limit 2021

Room granted at beginning Room raised in Q3 Room raised in Q4 CAR 2020 (RHS)

33

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

BANKING SECTOR – CREDIT

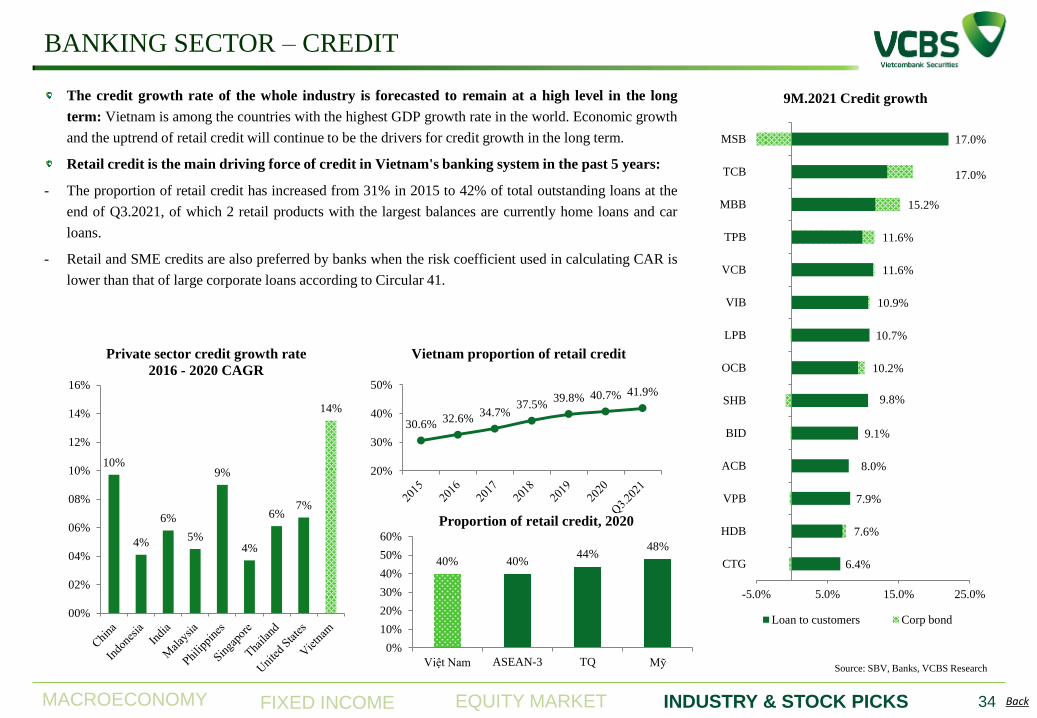

The credit growth rate of the whole industry is forecasted to remain at a high level in the long

term: Vietnam is among the countries with the highest GDP growth rate in the world. Economic growth

and the uptrend of retail credit will continue to be the drivers for credit growth in the long term.

Retail credit is the main driving force of credit in Vietnam's banking system in the past 5 years:

- The proportion of retail credit has increased from 31% in 2015 to 42% of total outstanding loans at the

end of Q3.2021, of which 2 retail products with the largest balances are currently home loans and car

loans.

- Retail and SME credits are also preferred by banks when the risk coefficient used in calculating CAR is

lower than that of large corporate loans according to Circular 41.

10%

4%

6%

5%

9%

4%

6% 7%

14%

00%

02%

04%

06%

08%

10%

12%

14%

16%

Private sector credit growth rate

2016 - 2020 CAGR

30.6% 32.6%

34.7% 37.5%

39.8% 40.7% 41.9%

20%

30%

40%

50%

Vietnam proportion of retail credit

Source: SBV, Banks, VCBS Research

6.4%

7.6%

7.9%

8.0%

9.1%

9.8%

10.2%

10.7%

10.9%

11.6%

11.6%

15.2%

17.0%

17.0%

-5.0% 5.0% 15.0% 25.0%

CTG

HDB

VPB

ACB

BID

SHB

OCB

LPB

VIB

VCB

TPB

MBB

TCB

MSB

9M.2021 Credit growth

Loan to customers Corp bond

40% 40% 44%

48%

0%

10%

20%

30%

40%

50%

60%

Việt Nam ASEAN-3 TQ Mỹ

Proportion of retail credit, 2020

34

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

BANKING SECTOR – CREDIT

35

9.1% 6.4% 11.6% 8.0% 15.2% 7.9% 17% 7.6% 10.9% 11.6% 10.2% 17%

Credit

growth

Q3.2021

Source: SBV, Banks, VCBS Research

5%

10%

15%

20%

25%

30%

35%

BID AGRB CTG VCB ACB MBB VPB TCB HDB VIB TPB OCB MSB

Customer loan growth CAGR 2018 - 2020

Average: 17,6%

Average: 23,9%

Average: 26,4%

Average: 11,9%

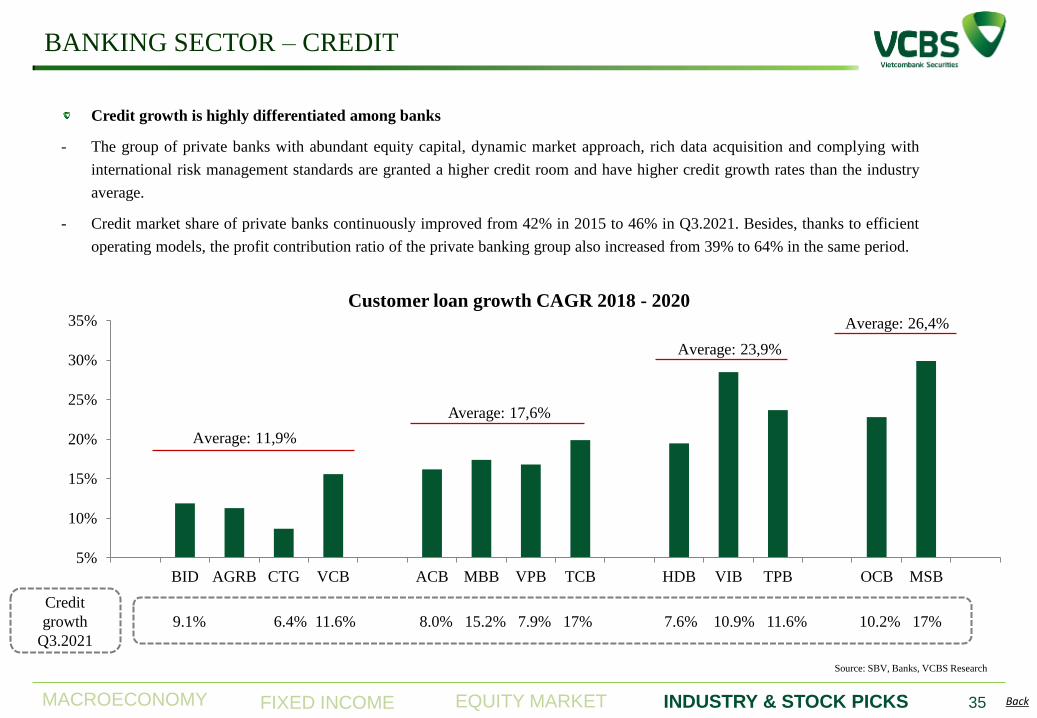

Credit growth is highly differentiated among banks

- The group of private banks with abundant equity capital, dynamic market approach, rich data acquisition and complying with

international risk management standards are granted a higher credit room and have higher credit growth rates than the industry

average.

- Credit market share of private banks continuously improved from 42% in 2015 to 46% in Q3.2021. Besides, thanks to efficient

operating models, the profit contribution ratio of the private banking group also increased from 39% to 64% in the same period.

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

BANKING SECTOR – CREDIT

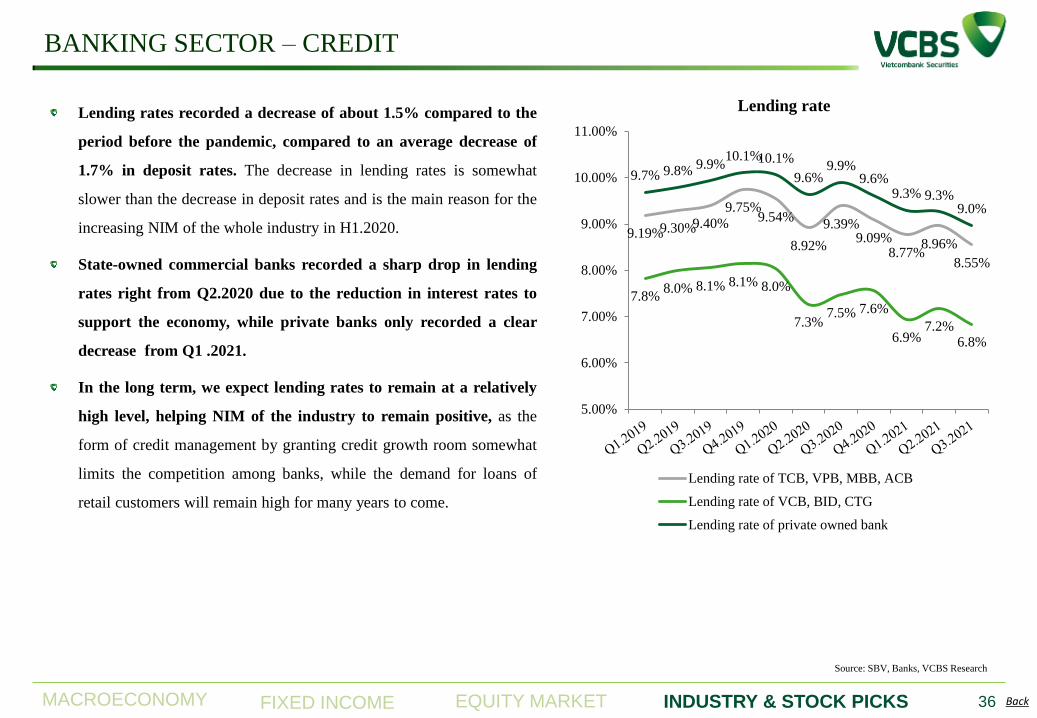

Lending rates recorded a decrease of about 1.5% compared to the

period before the pandemic, compared to an average decrease of

1.7% in deposit rates. The decrease in lending rates is somewhat

slower than the decrease in deposit rates and is the main reason for the

increasing NIM of the whole industry in H1.2020.

State-owned commercial banks recorded a sharp drop in lending

rates right from Q2.2020 due to the reduction in interest rates to

support the economy, while private banks only recorded a clear

decrease from Q1 .2021.

In the long term, we expect lending rates to remain at a relatively

high level, helping NIM of the industry to remain positive, as the

form of credit management by granting credit growth room somewhat

limits the competition among banks, while the demand for loans of

retail customers will remain high for many years to come.

Source: SBV, Banks, VCBS Research

9.19% 9.30% 9.40%

9.75% 9.54%

8.92%

9.39% 9.09%

8.77% 8.96%

8.55%

7.8% 8.0% 8.1% 8.1% 8.0%

7.3% 7.5% 7.6%

6.9% 7.2%

6.8%

9.7% 9.8% 9.9%

10.1% 10.1%

9.6% 9.9%

9.6% 9.3% 9.3%

9.0%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

11.00%

Lending rate

Lending rate of TCB, VPB, MBB, ACB

Lending rate of VCB, BID, CTG

Lending rate of private owned bank

36

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

BANKING SECTOR – DEPOSIT

At the end of September 2021, deposits from customers increased by

5.31% ytd, lower than credit growth of 7.42%.

The whole banking system recorded an increase in CASA ratio to

20.1% in Q3.2021 due to the sharp drop in term deposit interest rates to

a level that is no longer attractive enough, along with the boom of

securities and real estate markets attracting a large amount of cash flow.

We believe the interest rate trend will remain at a low level in the near

future, causing CASA ratio of the whole industry to continue to increase.

- The competition for CASA is increasingly fierce as many banks accept

to sacrifice part of service fees and invest in digital transformation to

attract new customers. Banks that have recorded a rapid increase in the

number of regular customers such as TCB, MBB, TPB, MSB... will have

more abundant deposits and reduce costs of fund in the long term.

Banks look to low-cost funding in the international market to make

more room to lower lending rates:

- International funding organizations such as IFC and ADB often require

funded banks to use capital for good purposes, have a good risk

management system, etc. The interest rates of these loans are usually set

pegged to international interbank interest rates and is currently around

1%/year.

- The cost of converting foreign currency into VND is now sharply

reduced, helping to promote capital raising from international credit

institutions.

Funding

organizations Limit Announcement time

VND billion USD million

VIB ADB 5,980 260 Q4.2021

IFC 3,312 144 Q1.2020

TPB IFC Q1.2020

OCB IFC 6,440 280 Q3.2021

VPB IFC 2,300 100 Q2.2020

HDB ADB 3,450 150 Q3.2021

MSB Commerzbank 2,300 100 Q4.2021

Seabank ADB 690 30 Q2.2021

Source: SBV, Banks, VCBS Research

18.7%

17.5% 17.2%

17.8%

16.9%

19.9% 19.4% 19.4%

20.1%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

15%

16%

17%

18%

19%

20%

21%

Demand deposit growth thanks to low term

deposit rate

CASA ratio Sum of listed banks' CASA

37

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

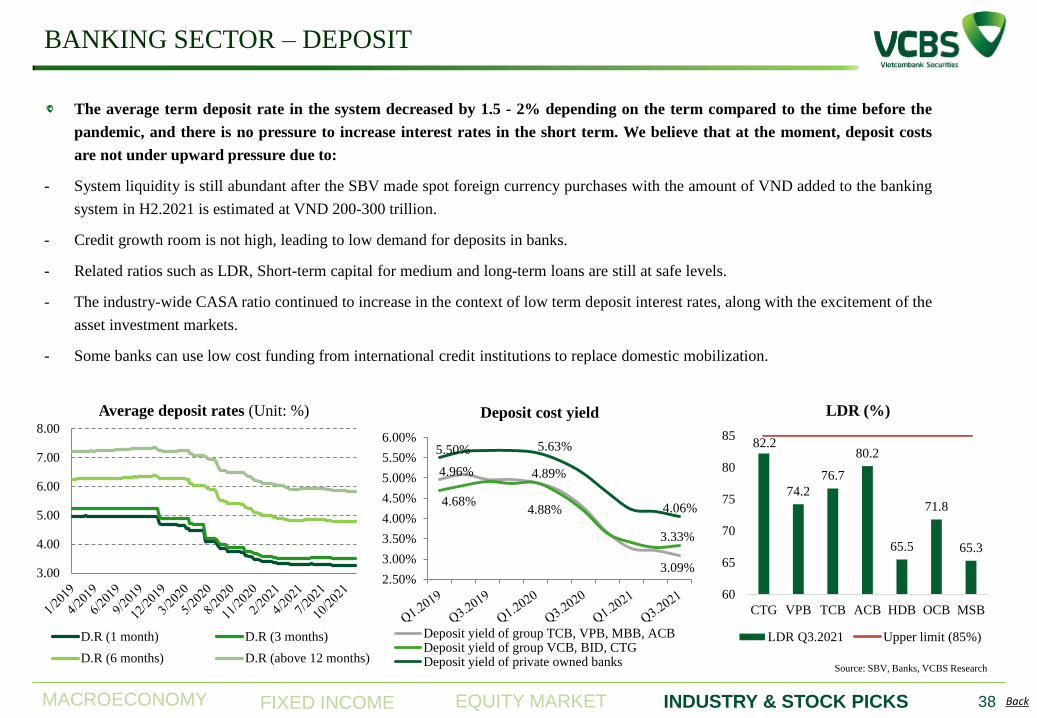

BANKING SECTOR – DEPOSIT

The average term deposit rate in the system decreased by 1.5 - 2% depending on the term compared to the time before the

pandemic, and there is no pressure to increase interest rates in the short term. We believe that at the moment, deposit costs

are not under upward pressure due to:

- System liquidity is still abundant after the SBV made spot foreign currency purchases with the amount of VND added to the banking

system in H2.2021 is estimated at VND 200-300 trillion.

- Credit growth room is not high, leading to low demand for deposits in banks.

- Related ratios such as LDR, Short-term capital for medium and long-term loans are still at safe levels.

- The industry-wide CASA ratio continued to increase in the context of low term deposit interest rates, along with the excitement of the

asset investment markets.

- Some banks can use low cost funding from international credit institutions to replace domestic mobilization.

Source: SBV, Banks, VCBS Research

3.00

4.00

5.00

6.00

7.00

8.00

Average deposit rates (Unit: %)

D.R (1 month) D.R (3 months)

D.R (6 months) D.R (above 12 months)

4.96% 4.89%

3.09%

4.68% 4.88%

3.33%

5.50% 5.63%

4.06%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

5.50%

6.00%

Deposit cost yield

Deposit yield of group TCB, VPB, MBB, ACBDeposit yield of group VCB, BID, CTGDeposit yield of private owned banks

82.2

74.2

76.7

80.2

65.5

71.8

65.3

60

65

70

75

80

85

CTG VPB TCB ACB HDB OCB MSB

LDR (%)

LDR Q3.2021 Upper limit (85%)

38

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

BANKING SECTOR – NIM

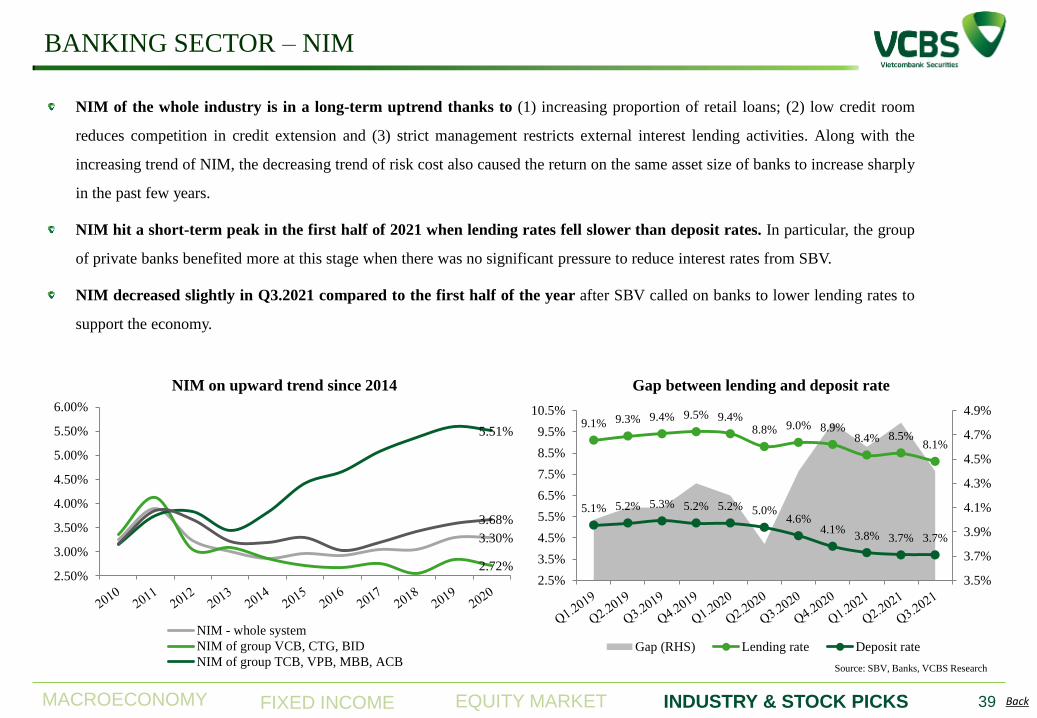

NIM of the whole industry is in a long-term uptrend thanks to (1) increasing proportion of retail loans; (2) low credit room

reduces competition in credit extension and (3) strict management restricts external interest lending activities. Along with the

increasing trend of NIM, the decreasing trend of risk cost also caused the return on the same asset size of banks to increase sharply

in the past few years.

NIM hit a short-term peak in the first half of 2021 when lending rates fell slower than deposit rates. In particular, the group

of private banks benefited more at this stage when there was no significant pressure to reduce interest rates from SBV.

NIM decreased slightly in Q3.2021 compared to the first half of the year after SBV called on banks to lower lending rates to

support the economy.

Source: SBV, Banks, VCBS Research

3.30%

2.72%

5.51%

3.68%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

5.50%

6.00%

NIM on upward trend since 2014

NIM - whole system

NIM of group VCB, CTG, BID

NIM of group TCB, VPB, MBB, ACB

9.1% 9.3% 9.4% 9.5% 9.4% 8.8% 9.0% 8.9%

8.4% 8.5% 8.1%

5.1% 5.2% 5.3% 5.2% 5.2% 5.0% 4.6%

4.1% 3.8% 3.7% 3.7%

3.5%

3.7%

3.9%

4.1%

4.3%

4.5%

4.7%

4.9%

2.5%

3.5%

4.5%

5.5%

6.5%

7.5%

8.5%

9.5%

10.5%

Gap between lending and deposit rate

Gap (RHS) Lending rate Deposit rate

39

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

BANKING SECTOR – NON-INTEREST INCOME

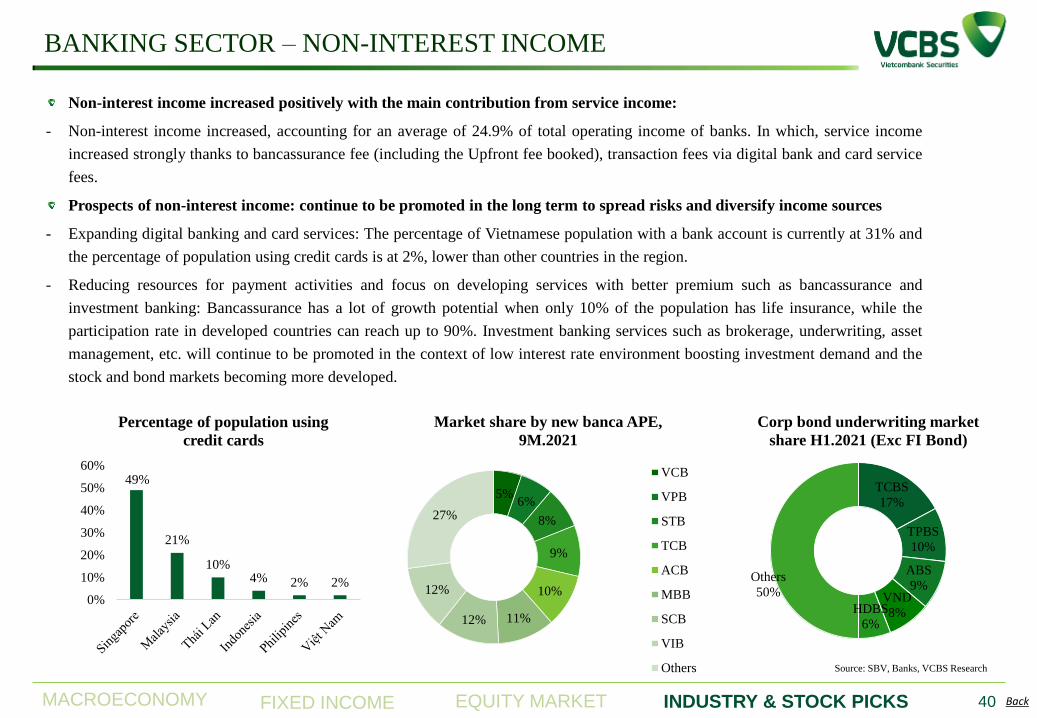

Non-interest income increased positively with the main contribution from service income:

- Non-interest income increased, accounting for an average of 24.9% of total operating income of banks. In which, service income

increased strongly thanks to bancassurance fee (including the Upfront fee booked), transaction fees via digital bank and card service

fees.

Prospects of non-interest income: continue to be promoted in the long term to spread risks and diversify income sources

- Expanding digital banking and card services: The percentage of Vietnamese population with a bank account is currently at 31% and

the percentage of population using credit cards is at 2%, lower than other countries in the region.

- Reducing resources for payment activities and focus on developing services with better premium such as bancassurance and

investment banking: Bancassurance has a lot of growth potential when only 10% of the population has life insurance, while the

participation rate in developed countries can reach up to 90%. Investment banking services such as brokerage, underwriting, asset

management, etc. will continue to be promoted in the context of low interest rate environment boosting investment demand and the

stock and bond markets becoming more developed.

49%

21%

10% 4% 2% 2%

0%

10%

20%

30%

40%

50%

60%

Percentage of population using

credit cards

Source: SBV, Banks, VCBS Research

5% 6%

8%

9%

10%

11% 12%

12%

27%

Market share by new banca APE,

9M.2021

VCB

VPB

STB

TCB

ACB

MBB

SCB

VIB

Others

TCBS

17%

TPBS

10%

ABS

9% VND

8% HDBS

6%

Others

50%

Corp bond underwriting market

share H1.2021 (Exc FI Bond)

40

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

BANKING SECTOR – DIGITIZATION & OPERATING COSTS

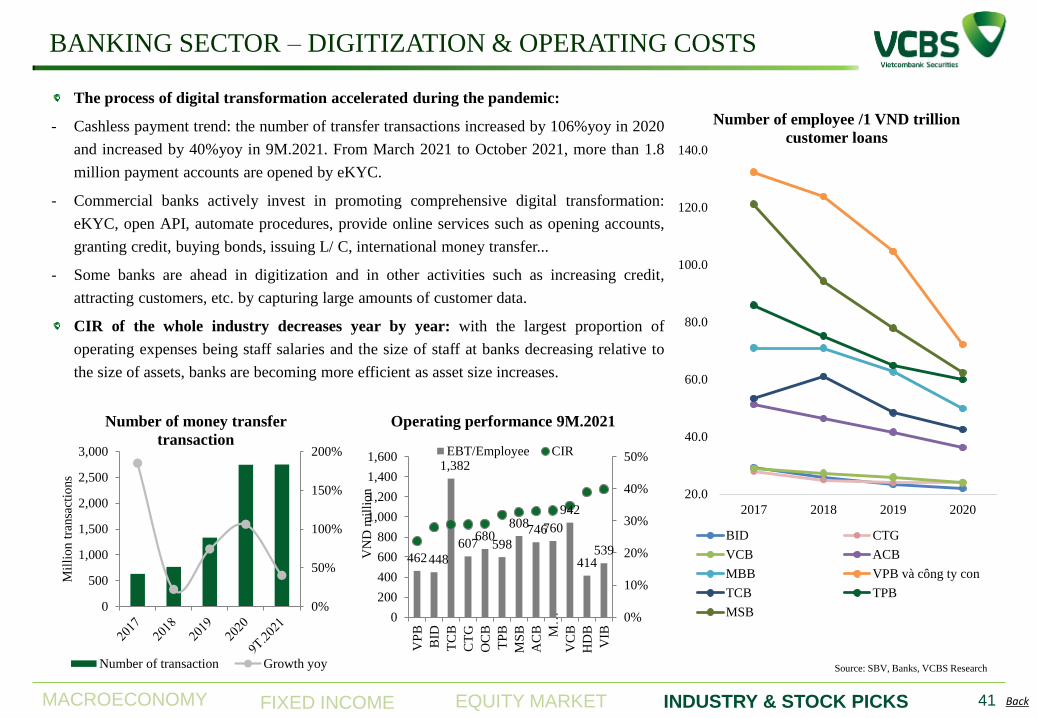

The process of digital transformation accelerated during the pandemic:

- Cashless payment trend: the number of transfer transactions increased by 106%yoy in 2020

and increased by 40%yoy in 9M.2021. From March 2021 to October 2021, more than 1.8

million payment accounts are opened by eKYC.

- Commercial banks actively invest in promoting comprehensive digital transformation:

eKYC, open API, automate procedures, provide online services such as opening accounts,

granting credit, buying bonds, issuing L/ C, international money transfer...

- Some banks are ahead in digitization and in other activities such as increasing credit,

attracting customers, etc. by capturing large amounts of customer data.

CIR of the whole industry decreases year by year: with the largest proportion of

operating expenses being staff salaries and the size of staff at banks decreasing relative to

the size of assets, banks are becoming more efficient as asset size increases.

20.0

40.0

60.0

80.0

100.0

120.0

140.0

2017 2018 2019 2020

Number of employee /1 VND trillion

customer loans

BID CTG

VCB ACB

MBB VPB và công ty con

TCB TPB

MSB

Source: SBV, Banks, VCBS Research

462 448

1,382

607 680

598

808 746 760

942

414 539

0%

10%

20%

30%

40%

50%

0

200

400

600

800

1,000

1,200

1,400

1,600

VP

B

BID

TC

B

CT

G

OC

B

TP

B

MS

B

AC

B M…

VC

B

HD

B

VIB

VN

D m

illi

on

Operating performance 9M.2021

EBT/Employee CIR

0%

50%

100%

150%

200%

0

500

1,000

1,500

2,000

2,500

3,000

Mil

lio

n t

ransa

ctio

ns

Number of money transfer

transaction

Number of transaction Growth yoy

41

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

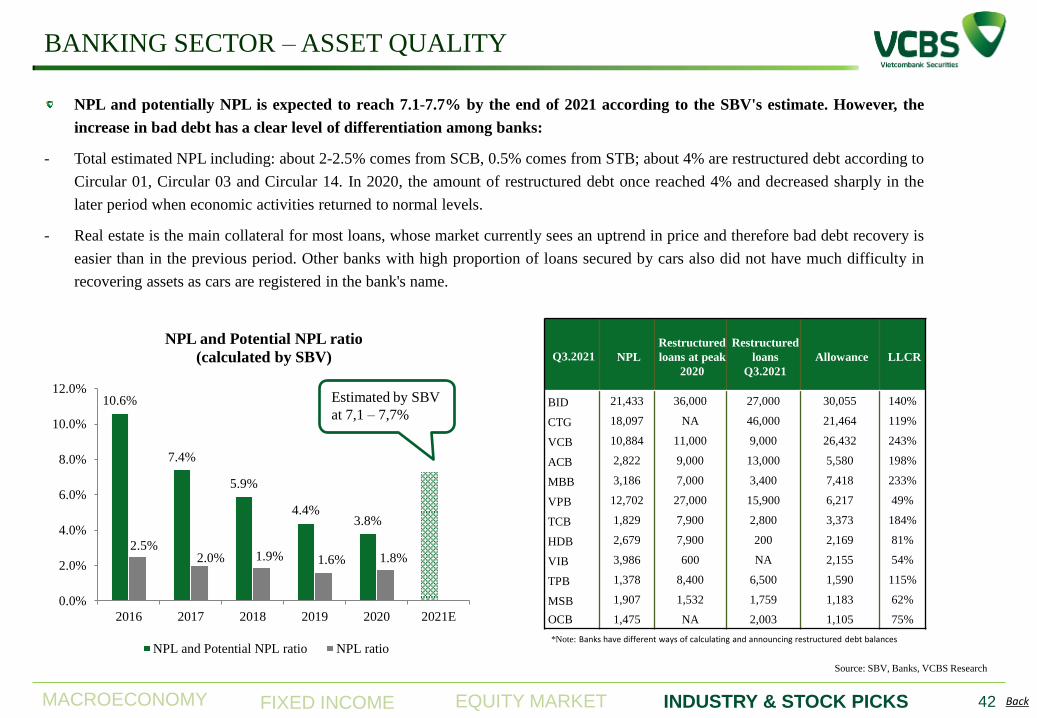

BANKING SECTOR – ASSET QUALITY

NPL and potentially NPL is expected to reach 7.1-7.7% by the end of 2021 according to the SBV's estimate. However, the

increase in bad debt has a clear level of differentiation among banks:

- Total estimated NPL including: about 2-2.5% comes from SCB, 0.5% comes from STB; about 4% are restructured debt according to

Circular 01, Circular 03 and Circular 14. In 2020, the amount of restructured debt once reached 4% and decreased sharply in the

later period when economic activities returned to normal levels.

- Real estate is the main collateral for most loans, whose market currently sees an uptrend in price and therefore bad debt recovery is

easier than in the previous period. Other banks with high proportion of loans secured by cars also did not have much difficulty in

recovering assets as cars are registered in the bank's name.

Q3.2021 NPL

Restructured

loans at peak

2020

Restructured

loans

Q3.2021

Allowance LLCR

BID 21,433 36,000 27,000 30,055 140%

CTG 18,097 NA 46,000 21,464 119%

VCB 10,884 11,000 9,000 26,432 243%

ACB 2,822 9,000 13,000 5,580 198%

MBB 3,186 7,000 3,400 7,418 233%

VPB 12,702 27,000 15,900 6,217 49%

TCB 1,829 7,900 2,800 3,373 184%

HDB 2,679 7,900 200 2,169 81%

VIB 3,986 600 NA 2,155 54%

TPB 1,378 8,400 6,500 1,590 115%

MSB 1,907 1,532 1,759 1,183 62%

OCB 1,475 NA 2,003 1,105 75%

*Note: Banks have different ways of calculating and announcing restructured debt balances

Source: SBV, Banks, VCBS Research

10.6%

7.4%

5.9%

4.4% 3.8%

2.5% 2.0% 1.9% 1.6% 1.8%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2016 2017 2018 2019 2020 2021E

NPL and Potential NPL ratio

(calculated by SBV)

NPL and Potential NPL ratio NPL ratio

Estimated by SBV

at 7,1 – 7,7%

42

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

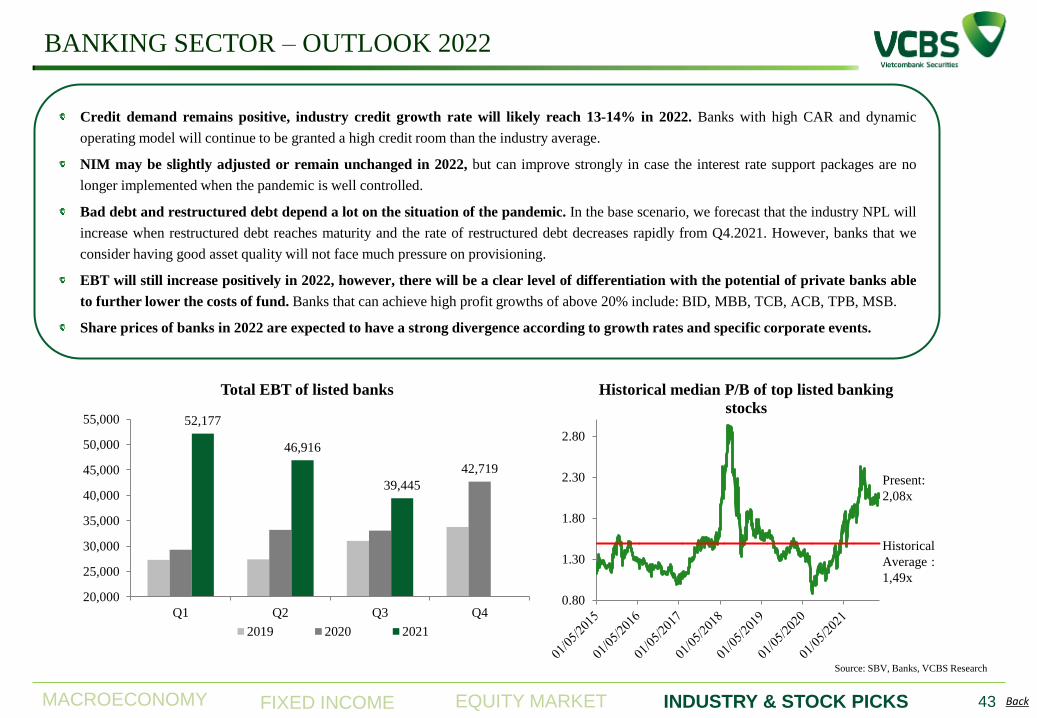

BANKING SECTOR – OUTLOOK 2022

Credit demand remains positive, industry credit growth rate will likely reach 13-14% in 2022. Banks with high CAR and dynamic

operating model will continue to be granted a high credit room than the industry average.

NIM may be slightly adjusted or remain unchanged in 2022, but can improve strongly in case the interest rate support packages are no

longer implemented when the pandemic is well controlled.

Bad debt and restructured debt depend a lot on the situation of the pandemic. In the base scenario, we forecast that the industry NPL will

increase when restructured debt reaches maturity and the rate of restructured debt decreases rapidly from Q4.2021. However, banks that we

consider having good asset quality will not face much pressure on provisioning.

EBT will still increase positively in 2022, however, there will be a clear level of differentiation with the potential of private banks able

to further lower the costs of fund. Banks that can achieve high profit growths of above 20% include: BID, MBB, TCB, ACB, TPB, MSB.

Share prices of banks in 2022 are expected to have a strong divergence according to growth rates and specific corporate events.

0.80

1.30

1.80

2.30

2.80

Historical median P/B of top listed banking

stocks

Present:

2,08x

Historical

Average :

1,49x

42,719

52,177

46,916

39,445

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

Q1 Q2 Q3 Q4

Total EBT of listed banks

2019 2020 2021

Source: SBV, Banks, VCBS Research

43

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

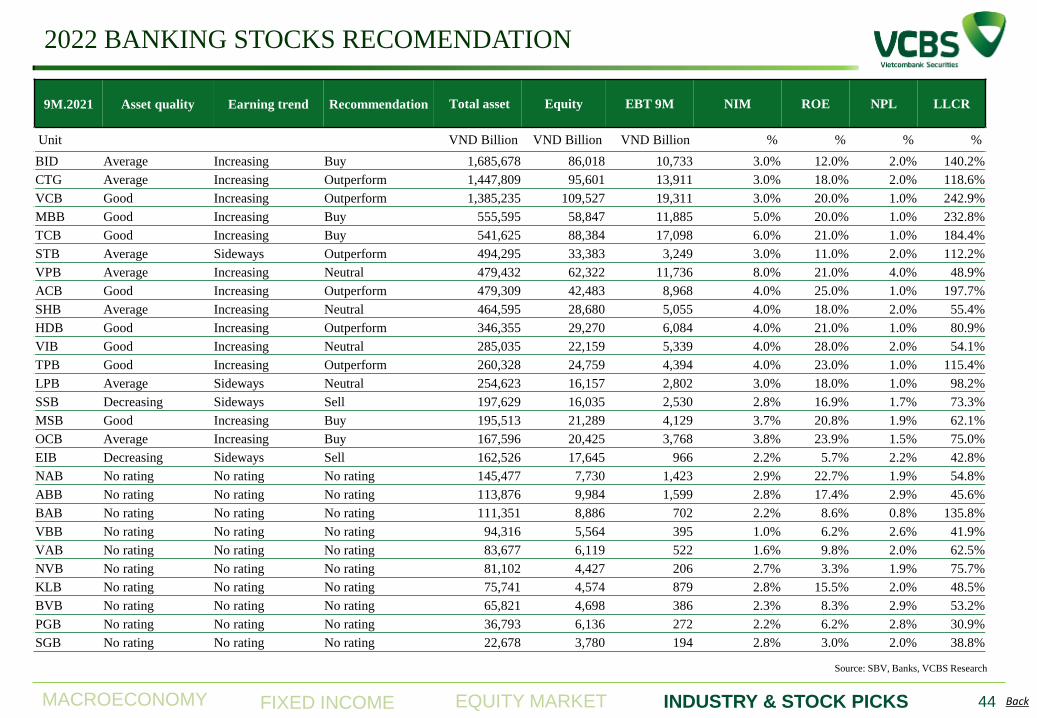

2022 BANKING STOCKS RECOMENDATION

9M.2021 Asset quality Earning trend Recommendation Total asset Equity EBT 9M NIM ROE NPL LLCR

Unit VND Billion VND Billion VND Billion % % % %

BID Average Increasing Buy 1,685,678 86,018 10,733 3.0% 12.0% 2.0% 140.2%

CTG Average Increasing Outperform 1,447,809 95,601 13,911 3.0% 18.0% 2.0% 118.6%

VCB Good Increasing Outperform 1,385,235 109,527 19,311 3.0% 20.0% 1.0% 242.9%

MBB Good Increasing Buy 555,595 58,847 11,885 5.0% 20.0% 1.0% 232.8%

TCB Good Increasing Buy 541,625 88,384 17,098 6.0% 21.0% 1.0% 184.4%

STB Average Sideways Outperform 494,295 33,383 3,249 3.0% 11.0% 2.0% 112.2%

VPB Average Increasing Neutral 479,432 62,322 11,736 8.0% 21.0% 4.0% 48.9%

ACB Good Increasing Outperform 479,309 42,483 8,968 4.0% 25.0% 1.0% 197.7%

SHB Average Increasing Neutral 464,595 28,680 5,055 4.0% 18.0% 2.0% 55.4%

HDB Good Increasing Outperform 346,355 29,270 6,084 4.0% 21.0% 1.0% 80.9%

VIB Good Increasing Neutral 285,035 22,159 5,339 4.0% 28.0% 2.0% 54.1%

TPB Good Increasing Outperform 260,328 24,759 4,394 4.0% 23.0% 1.0% 115.4%

LPB Average Sideways Neutral 254,623 16,157 2,802 3.0% 18.0% 1.0% 98.2%

SSB Decreasing Sideways Sell 197,629 16,035 2,530 2.8% 16.9% 1.7% 73.3%

MSB Good Increasing Buy 195,513 21,289 4,129 3.7% 20.8% 1.9% 62.1%

OCB Average Increasing Buy 167,596 20,425 3,768 3.8% 23.9% 1.5% 75.0%

EIB Decreasing Sideways Sell 162,526 17,645 966 2.2% 5.7% 2.2% 42.8%

NAB No rating No rating No rating 145,477 7,730 1,423 2.9% 22.7% 1.9% 54.8%

ABB No rating No rating No rating 113,876 9,984 1,599 2.8% 17.4% 2.9% 45.6%

BAB No rating No rating No rating 111,351 8,886 702 2.2% 8.6% 0.8% 135.8%

VBB No rating No rating No rating 94,316 5,564 395 1.0% 6.2% 2.6% 41.9%

VAB No rating No rating No rating 83,677 6,119 522 1.6% 9.8% 2.0% 62.5%

NVB No rating No rating No rating 81,102 4,427 206 2.7% 3.3% 1.9% 75.7%

KLB No rating No rating No rating 75,741 4,574 879 2.8% 15.5% 2.0% 48.5%

BVB No rating No rating No rating 65,821 4,698 386 2.3% 8.3% 2.9% 53.2%

PGB No rating No rating No rating 36,793 6,136 272 2.2% 6.2% 2.8% 30.9%

SGB No rating No rating No rating 22,678 3,780 194 2.8% 3.0% 2.0% 38.8%

Source: SBV, Banks, VCBS Research

44

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

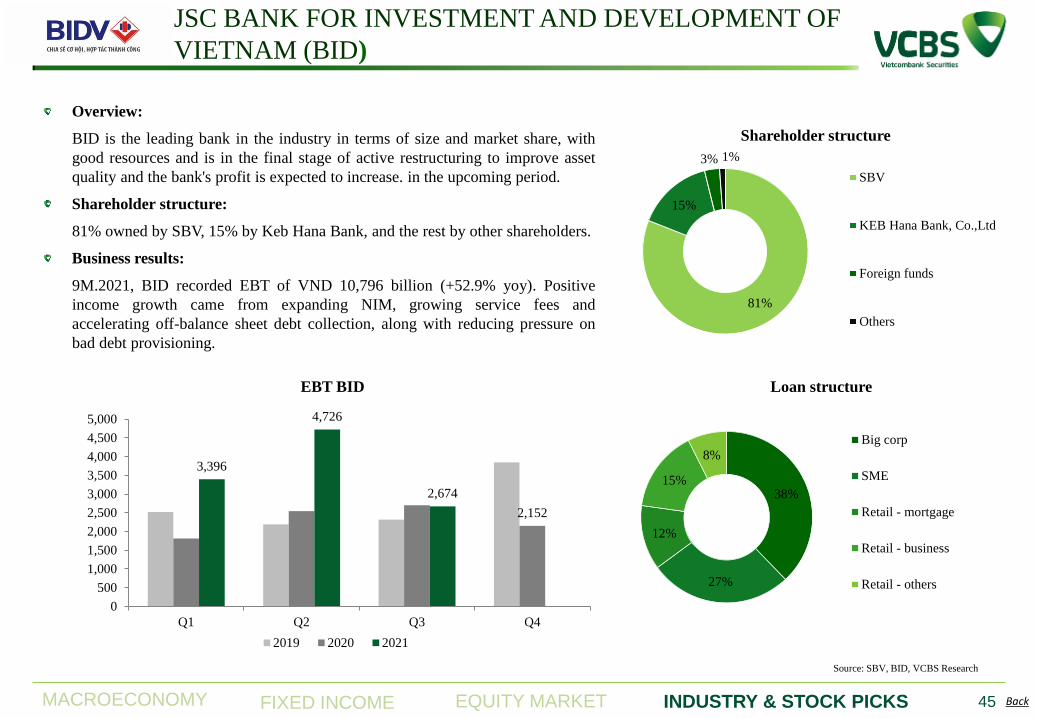

JSC BANK FOR INVESTMENT AND DEVELOPMENT OF

VIETNAM (BID)

Source: SBV, BID, VCBS Research

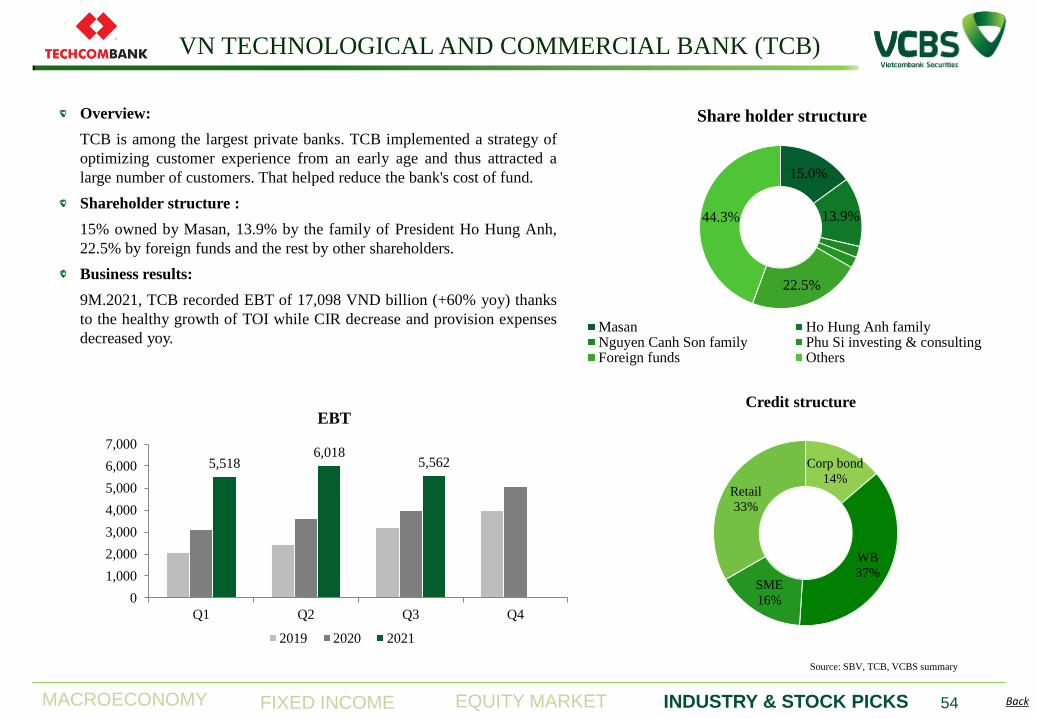

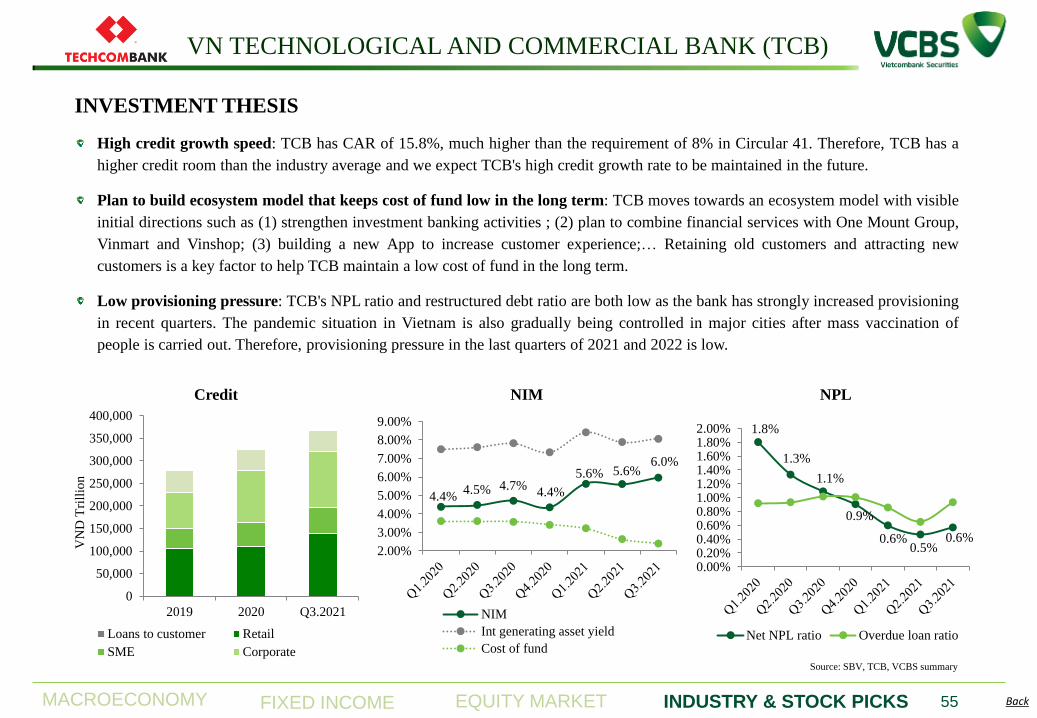

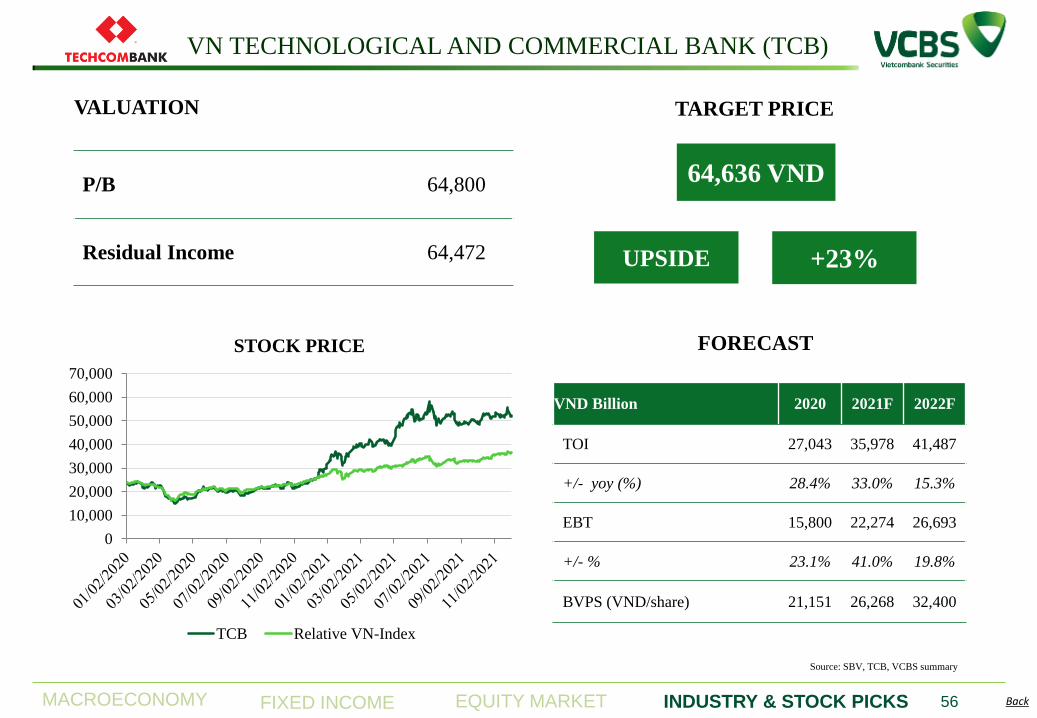

Overview:

BID is the leading bank in the industry in terms of size and market share, with

good resources and is in the final stage of active restructuring to improve asset

quality and the bank's profit is expected to increase. in the upcoming period.

Shareholder structure:

81% owned by SBV, 15% by Keb Hana Bank, and the rest by other shareholders.

Business results:

9M.2021, BID recorded EBT of VND 10,796 billion (+52.9% yoy). Positive

income growth came from expanding NIM, growing service fees and

accelerating off-balance sheet debt collection, along with reducing pressure on

bad debt provisioning.

45

38%

27%

12%

15%

8%

Loan structure

Big corp

SME

Retail - mortgage

Retail - business

Retail - others

81%

15%

3% 1%

Shareholder structure

SBV

KEB Hana Bank, Co.,Ltd

Foreign funds

Others

2,152

3,396

4,726

2,674

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Q1 Q2 Q3 Q4

EBT BID

2019 2020 2021

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

Source: SBV, BID, VCBS Research

46

INVESTMENT THESIS

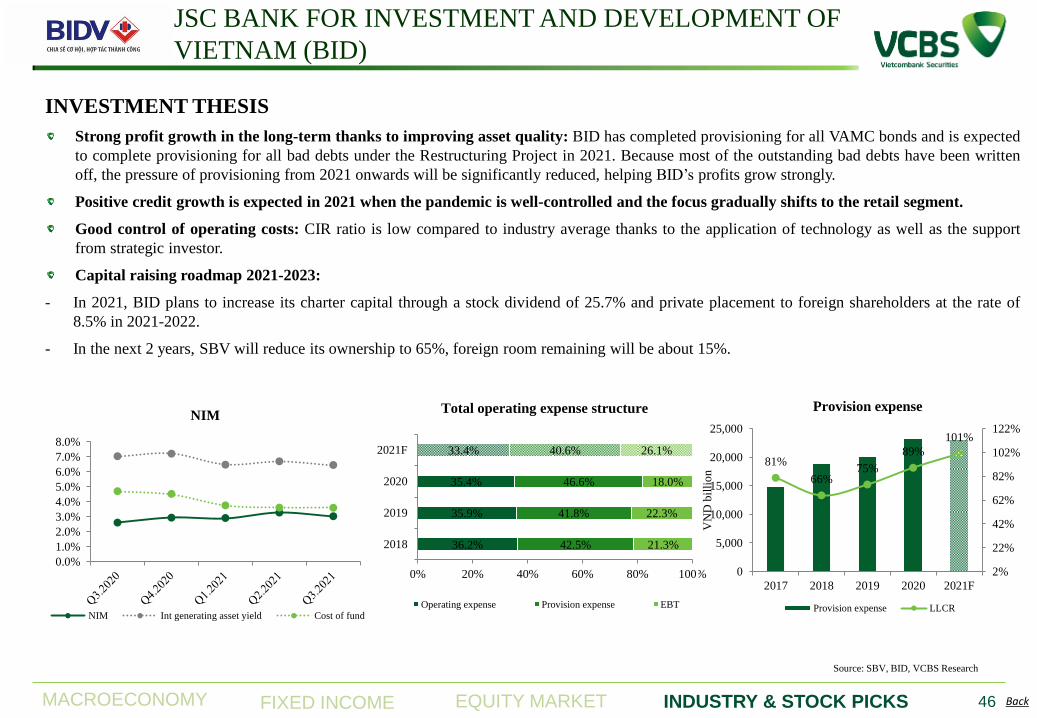

Strong profit growth in the long-term thanks to improving asset quality: BID has completed provisioning for all VAMC bonds and is expected

to complete provisioning for all bad debts under the Restructuring Project in 2021. Because most of the outstanding bad debts have been written

off, the pressure of provisioning from 2021 onwards will be significantly reduced, helping BID’s profits grow strongly.

Positive credit growth is expected in 2021 when the pandemic is well-controlled and the focus gradually shifts to the retail segment.

Good control of operating costs: CIR ratio is low compared to industry average thanks to the application of technology as well as the support

from strategic investor.

Capital raising roadmap 2021-2023:

- In 2021, BID plans to increase its charter capital through a stock dividend of 25.7% and private placement to foreign shareholders at the rate of

8.5% in 2021-2022.

- In the next 2 years, SBV will reduce its ownership to 65%, foreign room remaining will be about 15%.

JSC BANK FOR INVESTMENT AND DEVELOPMENT OF

VIETNAM (BID)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

NIM

NIM Int generating asset yield Cost of fund

36.2%

35.9%

35.4%

33.4%

42.5%

41.8%

46.6%

40.6%

21.3%

22.3%

18.0%

26.1%

0% 20% 40% 60% 80% 100%

2018

2019

2020

2021F

Total operating expense structure

Operating expense Provision expense EBT

81%

66% 75%

89%

101%

2%

22%

42%

62%

82%

102%

122%

0

5,000

10,000

15,000

20,000

25,000

2017 2018 2019 2020 2021F

VN

D b

illi

on

Provision expense

Provision expense LLCR

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

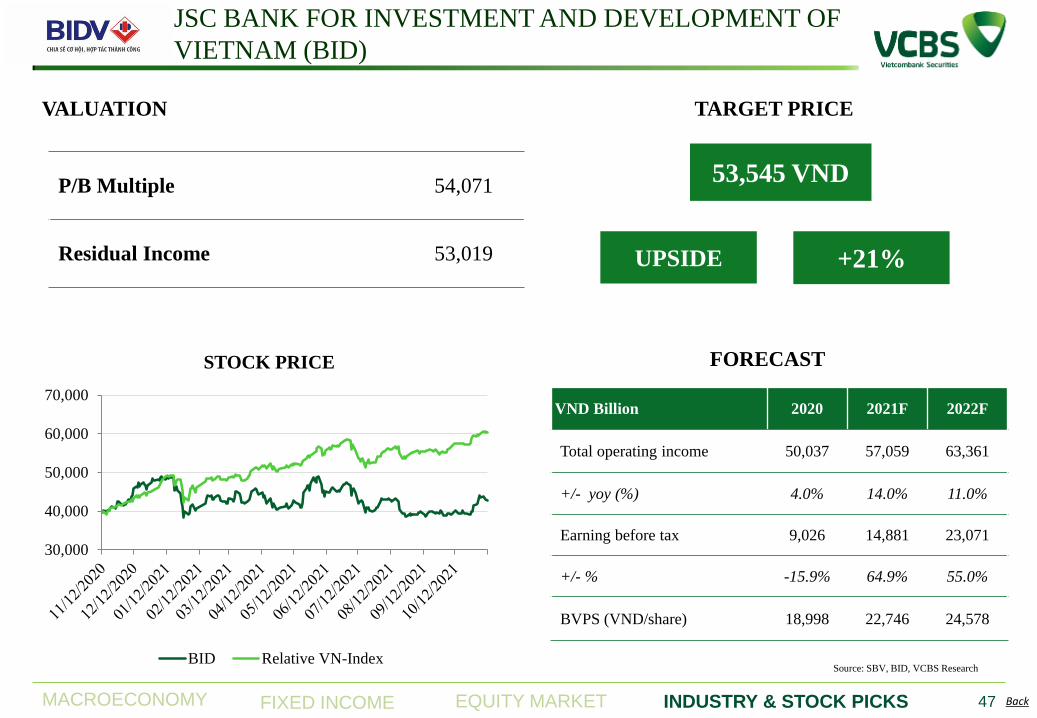

Source: SBV, BID, VCBS Research

FORECAST

53,545 VND

TARGET PRICE

+21% UPSIDE

VND Billion 2020 2021F 2022F

Total operating income 50,037 57,059 63,361

+/- yoy (%) 4.0% 14.0% 11.0%

Earning before tax 9,026 14,881 23,071

+/- % -15.9% 64.9% 55.0%

BVPS (VND/share) 18,998 22,746 24,578

47

VALUATION

P/B Multiple 54,071

Residual Income 53,019

JSC BANK FOR INVESTMENT AND DEVELOPMENT OF

VIETNAM (BID)

30,000

40,000

50,000

60,000

70,000

STOCK PRICE

BID Relative VN-Index

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

MILITARY COMMERCIAL JOINT STOCK BANK (MBB)

Source: SBV, MBB, VCBS Research

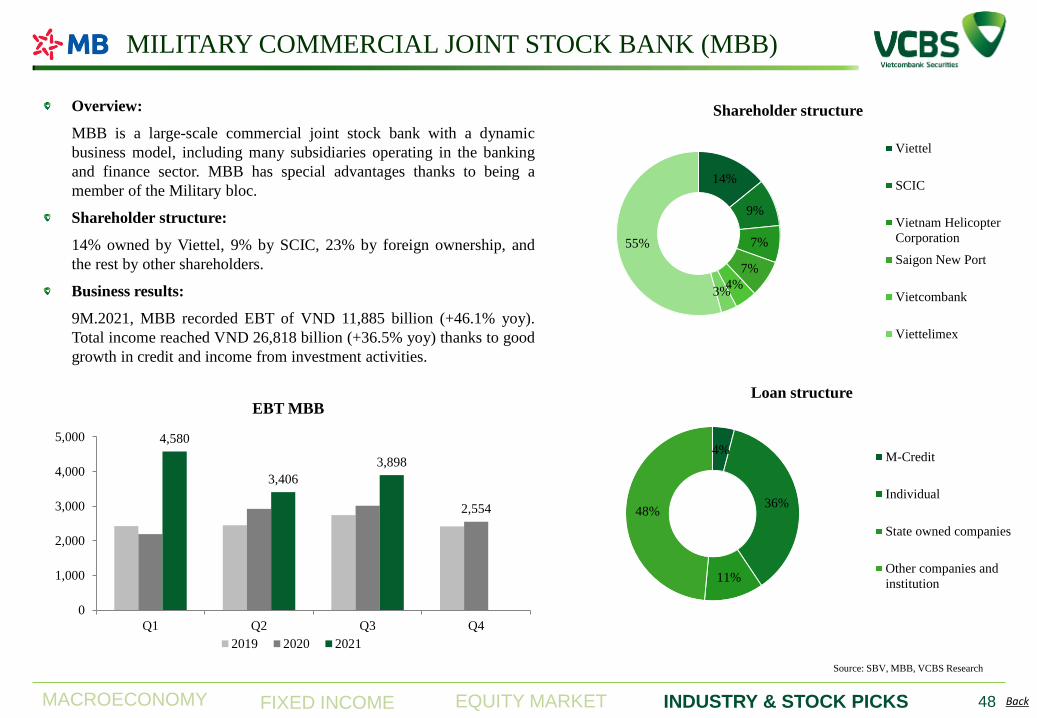

Overview:

MBB is a large-scale commercial joint stock bank with a dynamic

business model, including many subsidiaries operating in the banking

and finance sector. MBB has special advantages thanks to being a

member of the Military bloc.

Shareholder structure:

14% owned by Viettel, 9% by SCIC, 23% by foreign ownership, and

the rest by other shareholders.

Business results:

9M.2021, MBB recorded EBT of VND 11,885 billion (+46.1% yoy).

Total income reached VND 26,818 billion (+36.5% yoy) thanks to good

growth in credit and income from investment activities.

48

14%

9%

7%

7%

4% 3%

55%

Shareholder structure

Viettel

SCIC

Vietnam Helicopter

Corporation

Saigon New Port

Vietcombank

Viettelimex

4%

36%

11%

48%

Loan structure

M-Credit

Individual

State owned companies

Other companies and

institution

2,554

4,580

3,406

3,898

0

1,000

2,000

3,000

4,000

5,000

Q1 Q2 Q3 Q4

EBT MBB

2019 2020 2021

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

Source: SBV, MBB, VCBS Research

INVESTMENT THESIS

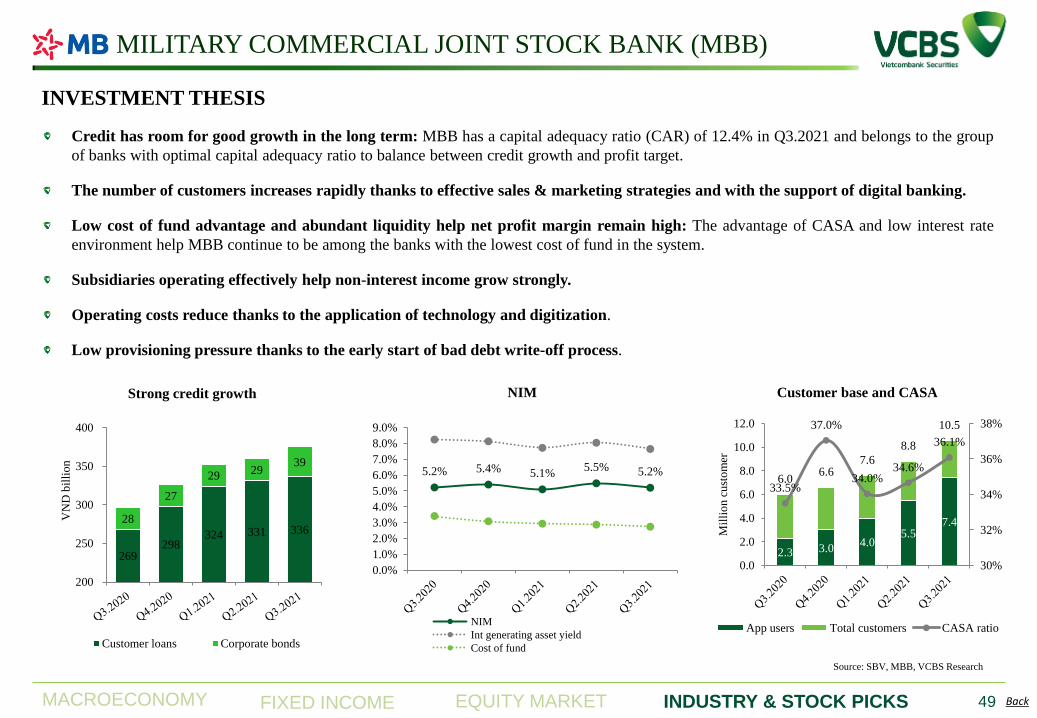

Credit has room for good growth in the long term: MBB has a capital adequacy ratio (CAR) of 12.4% in Q3.2021 and belongs to the group

of banks with optimal capital adequacy ratio to balance between credit growth and profit target.

The number of customers increases rapidly thanks to effective sales & marketing strategies and with the support of digital banking.

Low cost of fund advantage and abundant liquidity help net profit margin remain high: The advantage of CASA and low interest rate

environment help MBB continue to be among the banks with the lowest cost of fund in the system.

Subsidiaries operating effectively help non-interest income grow strongly.

Operating costs reduce thanks to the application of technology and digitization.

Low provisioning pressure thanks to the early start of bad debt write-off process.

49

MILITARY COMMERCIAL JOINT STOCK BANK (MBB)

5.2% 5.4% 5.1% 5.5% 5.2%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

NIM

NIM

Int generating asset yield

Cost of fund

2.3 3.0 4.0

5.5 7.4

6.0 6.6

7.6

8.8

10.5

33.5%

37.0%

34.0% 34.6%

36.1%

30%

32%

34%

36%

38%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Mil

lio

n c

ust

om

er

Customer base and CASA

App users Total customers CASA ratio

269 298

324 331 336 28

27

29 29

39

200

250

300

350

400

VN

D b

illi

on

Strong credit growth

Customer loans Corporate bonds

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

Source: SBV, MBB, VCBS Research

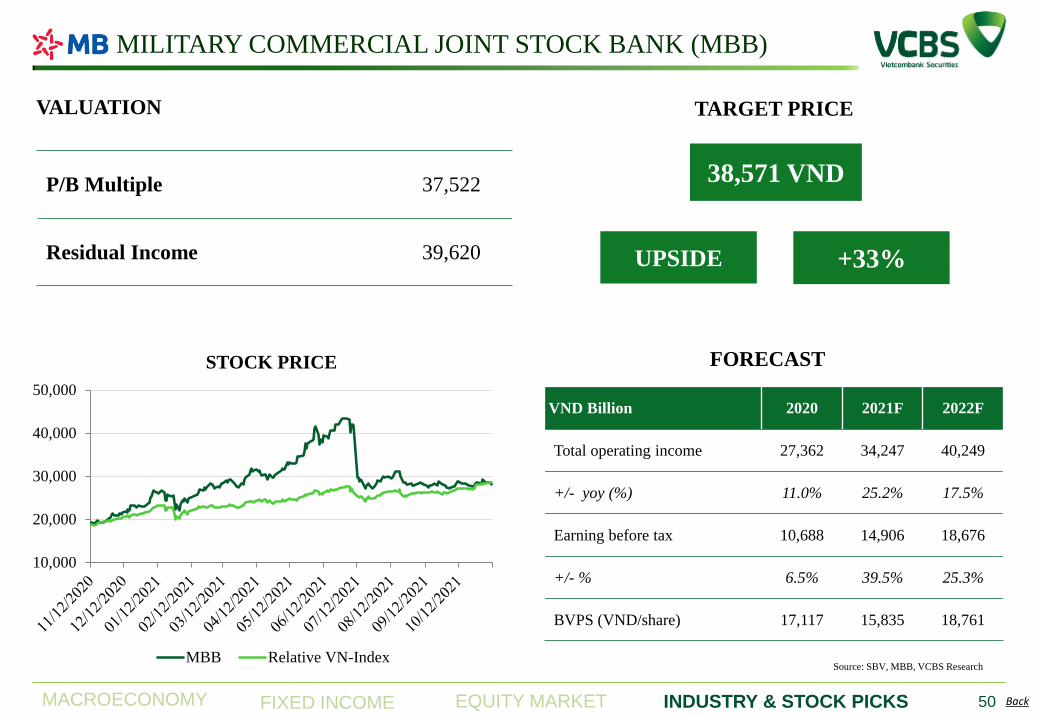

P/B Multiple 37,522

Residual Income 39,620

FORECAST

VALUATION

38,571 VND

TARGET PRICE

+33% UPSIDE

VND Billion 2020 2021F 2022F

Total operating income 27,362 34,247 40,249

+/- yoy (%) 11.0% 25.2% 17.5%

Earning before tax 10,688 14,906 18,676

+/- % 6.5% 39.5% 25.3%

BVPS (VND/share) 17,117 15,835 18,761

50

MILITARY COMMERCIAL JOINT STOCK BANK (MBB)

10,000

20,000

30,000

40,000

50,000

STOCK PRICE

MBB Relative VN-Index

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

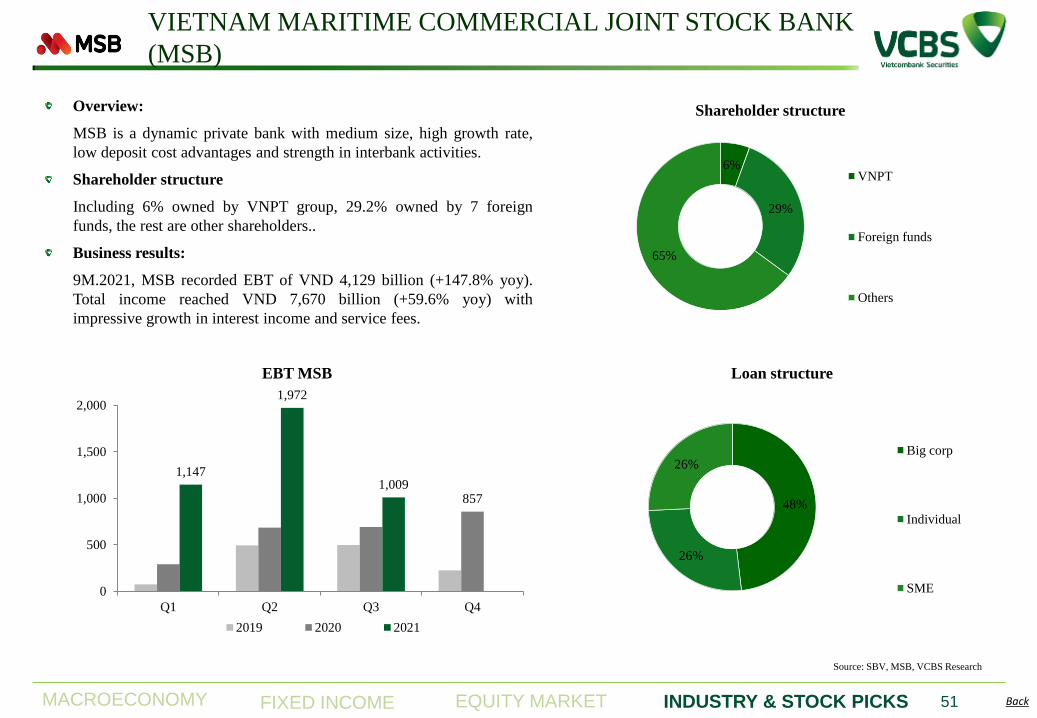

Overview:

MSB is a dynamic private bank with medium size, high growth rate,

low deposit cost advantages and strength in interbank activities.

Shareholder structure

Including 6% owned by VNPT group, 29.2% owned by 7 foreign

funds, the rest are other shareholders..