L B Finance PLC | Annual Report 2020/21 OUR BUSINESS ENVIRONMENT AND OUTLOOK Global Economic Highlights Sri Lankan Economic Highlights and its Impact – PESTEL Analysis Influencing Market Drivers, Risks and Opportunities SWOT Analysis Market Forces and Competitive Landscape GLOBAL ECONOMIC HIGHLIGHTS As COVID-19 continued to spread around the world with rapid escalation of the virus in some countries, the global economy tipped into a recession, the severity of which has not been seen for three quarters of a century. On the back of weak global trade, anemic investment and the collapse of international tourism, the global economy is estimated to have contracted by an unprecedented 4.3% in 2020. While advanced economies appear to have exhibited a greater degree of resilience to stave off the recessionary pressures, emerging economies seem to have been slipping into a deepening slump as the year progressed. Meanwhile, as corporations around the world began facing the reality of high debt burdens amidst sluggish growth, the strength of the global financial system was put to the test as the balance sheets of banks and financial institutions over the world came under pressure due to falling profitability and asset quality deterioration. However on a positive note, aggressive policy actions by Central Banks helped to prevent the global financial system from falling into crisis year under review. Source: Global Economic Prospects - January 2021 SRI LANKAN ECONOMIC HIGHLIGHTS AND ITS IMPACT PESTEL Analysis Political Operating environment Relative stability on the political front enabled targeted policies to be implemented to help Sri Lanka in overcoming initial pandemic related setbacks and ensure the rapid restoration of normal economic activity. Fiscal policy was reoriented towards supporting the ailing economy. However, pressures on the fiscal sector were aggravated by constrained access to foreign financing in 2020 amidst unfavourable global financial market conditions and downgrades of Sri Lanka’s rating by sovereign rating agencies. Heightened global uncertainties and the cautious approach adopted by investors towards Foreign Direct Investment (FDI) led to a moderation in the country’s financial account. Meanwhile subdued inflationary pressures and well-anchored inflation expectations provided the necessary impetus for the Central Bank to significantly relax its monetary policy stance during 2020. Key monetary policy easing measures implemented by the Central Bank in 2020, included the reduction of the key policy interest rates to historic lows with a downward adjustment of 250 basis points in total, and lowering of the Statutory Reserve Ratio (SRR) applicable on rupee deposit liabilities of Licensed Commercial Banks (LCBs) by a total of 300 basis points and the bank rate by 650 basis points. These monetary policy easing measures were focused on lowering costs of funds for businesses and individuals, ensuring adequate liquidity in the money market and facilitating the smooth functioning of the financial system under the challenging circumstances caused by the pandemic. Source: CBSL AR 2020

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

L B Finance PLC | Annual Report 2020/21

OUR BUSINESS ENVIRONMENT AND OUTLOOK

Global Economic Highlights

Sri Lankan Economic

Highlights and its Impact

– PESTEL Analysis

Influencing Market Drivers,

Risks and Opportunities

SWOT Analysis

Market Forces and

Competitive Landscape

GLOBAL ECONOMIC HIGHLIGHTS

As COVID-19 continued to spread around the world with rapid escalation of the virus in some countries, the global economy tipped into a recession, the severity of which has not been seen for three quarters of a century. On the back of weak global trade, anemic investment and the collapse of international tourism, the global economy is estimated to have contracted by an unprecedented 4.3% in 2020.

While advanced economies appear to have exhibited a greater degree of resilience to stave off the recessionary pressures, emerging economies seem to have been slipping into a deepening slump as the year progressed. Meanwhile, as corporations around the world began facing the reality of high debt burdens amidst sluggish growth, the strength of the global financial system was put to the test as the balance sheets of banks and financial institutions over the

world came under pressure due to falling profitability and asset quality deterioration. However on a positive note, aggressive policy actions by Central Banks helped to prevent the global financial system from falling into crisis year under review.

Source: Global Economic Prospects - January 2021

SRI LANKAN ECONOMIC HIGHLIGHTS AND ITS IMPACT

PESTEL Analysis

Political

Operating environment

Relative stability on the political front enabled targeted policies to be implemented to help Sri Lanka in overcoming initial pandemic related setbacks and ensure the rapid restoration of normal economic activity. Fiscal policy was reoriented towards supporting the ailing economy. However, pressures on the fiscal sector were aggravated by constrained access to foreign financing in 2020 amidst unfavourable global financial market conditions and downgrades of Sri Lanka’s rating by sovereign rating agencies. Heightened global uncertainties and the

cautious approach adopted by investors towards Foreign Direct Investment (FDI) led to a moderation in the country’s financial account.

Meanwhile subdued inflationary pressures and well-anchored inflation expectations provided the necessary impetus for the Central Bank to significantly relax its monetary policy stance during 2020. Key monetary policy easing measures implemented by the Central Bank in 2020, included the reduction of the key policy interest rates to historic lows with a downward adjustment of 250 basis points

in total, and lowering of the Statutory Reserve Ratio (SRR) applicable on rupee deposit liabilities of Licensed Commercial Banks (LCBs) by a total of 300 basis points and the bank rate by 650 basis points. These monetary policy easing measures were focused on lowering costs of funds for businesses and individuals, ensuring adequate liquidity in the money market and facilitating the smooth functioning of the financial system under the challenging circumstances caused by the pandemic.

Source: CBSL AR 2020

L B Finance PLC | Annual Report 2020/21

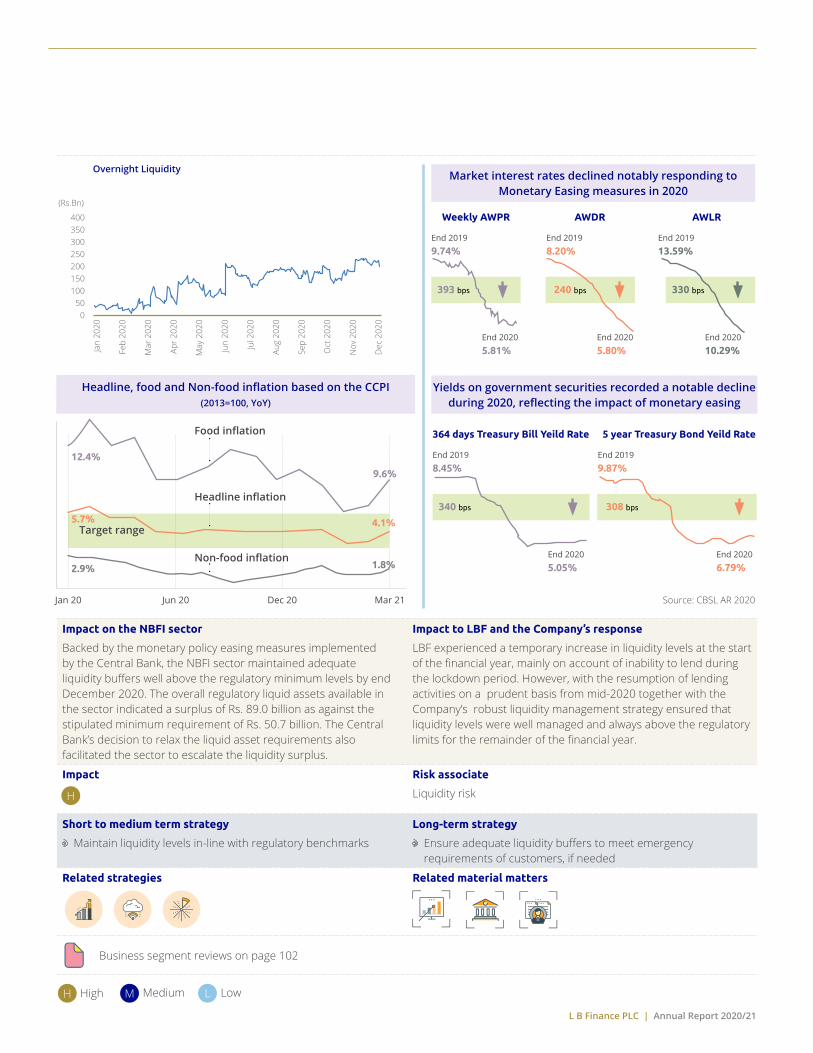

Impact on the NBFI sector

Backed by the monetary policy easing measures implemented by the Central Bank, the NBFI sector maintained adequate liquidity buffers well above the regulatory minimum levels by end December 2020. The overall regulatory liquid assets available in the sector indicated a surplus of Rs. 89.0 billion as against the stipulated minimum requirement of Rs. 50.7 billion. The Central Bank’s decision to relax the liquid asset requirements also facilitated the sector to escalate the liquidity surplus.

Impact to LBF and the Company’s response

LBF experienced a temporary increase in liquidity levels at the start of the financial year, mainly on account of inability to lend during the lockdown period. However, with the resumption of lending activities on a prudent basis from mid-2020 together with the Company’s robust liquidity management strategy ensured that liquidity levels were well managed and always above the regulatory limits for the remainder of the financial year.

Impact Risk associate

Liquidity risk

Short to medium term strategy

Maintain liquidity levels in-line with regulatory benchmarks

Long-term strategy

Ensure adequate liquidity buffers to meet emergency requirements of customers, if needed

Related strategies Related material matters

Business segment reviews on page 102

High Medium LowH M L

Overnight Liquidity

050

100150200250300350400

Jan

2020

Feb

2020

Mar

202

0

Apr 2

020

May

202

0

Jun

2020

Jul 2

020

Aug

2020

Sep

2020

Oct

202

0

Nov

202

0

Dec

202

0

(Rs.Bn)

Market interest rates declined notably responding to Monetary Easing measures in 2020

Yields on government securities recorded a notable decline during 2020, reflecting the impact of monetary easing

Headline, food and Non-food inflation based on the CCPI (2013=100, YoY)

Weekly AWPR

364 days Treasury Bill Yeild Rate

AWDR

5 year Treasury Bond Yeild Rate

AWLR

End 20199.74%

End 20198.45%

393 bps

340 bps

240 bps

308 bps

330 bps

End 20205.81%

End 20205.05%

Jan 20 Jun 20 Dec 20

Food inflation

Headline inflation

Non-food inflation

Target range

Mar 21

End 20198.20%

End 20199.87%

End 20205.80%

End 20206.79%

End 201913.59%

End 202010.29%

12.4%

5.7%

2.9% 1.8%

4.1%

9.6%

H

Source: CBSL AR 2020

L B Finance PLC | Annual Report 2020/21

OUR BUSINESS ENVIRONMENT AND OUTLOOK

Economic

Operating environment

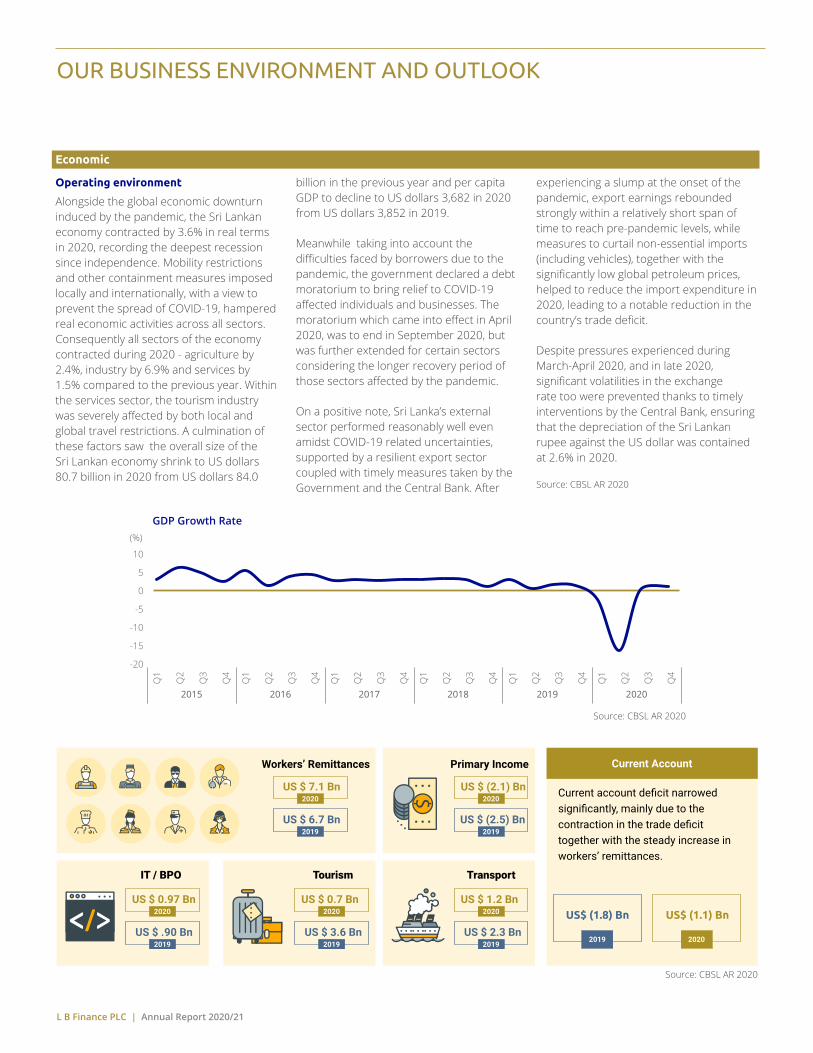

Alongside the global economic downturn induced by the pandemic, the Sri Lankan economy contracted by 3.6% in real terms in 2020, recording the deepest recession since independence. Mobility restrictions and other containment measures imposed locally and internationally, with a view to prevent the spread of COVID-19, hampered real economic activities across all sectors. Consequently all sectors of the economy contracted during 2020 - agriculture by 2.4%, industry by 6.9% and services by 1.5% compared to the previous year. Within the services sector, the tourism industry was severely affected by both local and global travel restrictions. A culmination of these factors saw the overall size of the Sri Lankan economy shrink to US dollars 80.7 billion in 2020 from US dollars 84.0

billion in the previous year and per capita GDP to decline to US dollars 3,682 in 2020 from US dollars 3,852 in 2019.

Meanwhile taking into account the difficulties faced by borrowers due to the pandemic, the government declared a debt moratorium to bring relief to COVID-19 affected individuals and businesses. The moratorium which came into effect in April 2020, was to end in September 2020, but was further extended for certain sectors considering the longer recovery period of those sectors affected by the pandemic.

On a positive note, Sri Lanka’s external sector performed reasonably well even amidst COVID-19 related uncertainties, supported by a resilient export sector coupled with timely measures taken by the Government and the Central Bank. After

experiencing a slump at the onset of the pandemic, export earnings rebounded strongly within a relatively short span of time to reach pre-pandemic levels, while measures to curtail non-essential imports (including vehicles), together with the significantly low global petroleum prices, helped to reduce the import expenditure in 2020, leading to a notable reduction in the country’s trade deficit.

Despite pressures experienced during March-April 2020, and in late 2020, significant volatilities in the exchange rate too were prevented thanks to timely interventions by the Central Bank, ensuring that the depreciation of the Sri Lankan rupee against the US dollar was contained at 2.6% in 2020.

Source: CBSL AR 2020

GDP Growth Rate

-20

-15

-10

-5

0

5

10

2015

Q1

Q2

Q3

Q4

(%)

2016

Q1

Q2

Q3

Q4

2017

Q1

Q2

Q3

Q4

2018

Q1

Q2

Q3

Q4

2019

Q1

Q2

Q3

Q4

2020

Q1

Q2

Q3

Q4

Source: CBSL AR 2020

US$ (1.8) Bn US$ (1.1) Bn

Source: CBSL AR 2020

L B Finance PLC | Annual Report 2020/21

Impact on the NBFI sector

Lending by the NBFI sector slowed considerably during 2020 as business activities continued to contract amidst the COVID-19 lockdowns and curtailment of vehicle imports. Credit provided by the sector contracted by 5.7 % compared to the contraction of 3.0% in 2019. Consequently, sector assets recorded negative growth of 2.2% during the year reaching Rs. 1,401.6 billion by end December 2020.

Sector-wide asset quality deteriorated significantly in 2020. With the NBFI sectors’ main target market - self employed individuals and MSME’s being among the worst affected pandemic induced economic downturn, the NBFI sector gross NPL ratio shot up to 13.9% by end December 2020 from 10.6 % reported as at end December 2019, showing a severe deterioration in the sector-wide asset quality. It should also be noted that NPLs of the sector could be underestimated due to debt moratorium together with other concessions and NPL levels may increase further after the end of the debt moratorium.

A combination of weak credit growth and higher NPL’s saw the NBFI sector reporting a significant deterioration in profitability for 2020. Net interest income - the key measure of sector profitability declined by 5.3% to Rs.111.2 billion from the figure reported in 2019.

The sector continued to be funded mainly through public deposits in 2020 as well. However, given the muted interest in deposits amidst the record low interest rates, the sectors’ deposit base contracted by 1.1% in 2020 compared to the previous year.

Source: CBSL AR 2020

Impact to LBF and the Company’s response

The inability to lend during the two months lockdown period as well as the CBSL’s decision to ban the import of vehicles, had a sizable impact on LBF’s core auto finance business. However quick action by the Company to reorient its focus towards available opportunities from mid-2020 helped to ensure consistent lending throughout the remainder of the year.

The ambiguity surrounding the announcement of the debt moratoriums caused a spike in the Company NPL’s in the Q1 of the financial year. However, proactive recovery action ensured LBF’s NPL ratio was brought under control by end September 2020 and remained consistent from that point on.

LBF’s performance for the current financial year was also somewhat affected. However, proactive lending along with strict recovery action ensured the Company’s performance was more or less on par with the previous year.

With the low interest rate environment proving to be a deterrent in attracting new deposits, LBF’s deposit mobilization activities were driven primarily with the intention of minimizing the Company’s asset and liability mismatch and also lowering the cost of funds.

Impact Risk associate

Credit risk

Interest rate risk

Short to medium term strategy

Keep satisfactory control of recoveries to minimise the impact at the end of the moratorium

Leverage on market opportunities to pursue organic and inorganic growth

Long-term strategy

Focus on further lowering funding costs

Related strategies Related material matters

MD’s statement on page 37, Business segment reviews on page 102

High Medium LowH M L

H

L B Finance PLC | Annual Report 2020/21

OUR BUSINESS ENVIRONMENT AND OUTLOOK

Social

Operating Environment

In the midst of the adverse impact of the COVID-19 pandemic, average disposable income was subject to erosion as organisations began declaring pay cuts and laying off employees as part of cost control initiatives aimed at managing the pandemic impact. As a result, Sri Lanka’s unemployment rate rose above 5% for the first time since 2009. Unemployment rate amongst females, youth and educationally qualified persons increased considerably in

2020 aggravating the inequalities further, while a marked decline in labour force participation rate was also observed with pandemic related mobility restrictions and isolation orders preventing employees from reporting to their workplaces.

The Government continued to provide relief via the financial sector, to the businesses and individuals facing severe hardships stemming from the pandemic. And, given the disproportionately

high impact of COVID-19 on low-income segments of the population, the Government paid an allowance and provided other relief measures to vulnerable families and individuals enabling them to meet their daily needs.

Source: CBSL AR 2020

Impact on the NBFI sector

With the entire social fabric of the country disrupted due to the pandemic, the NBFI sector had to reconsider its approach towards stakeholder value creation, with special focus on minimising their financial stress in these uncertain times.

Impact to LBF and the Company’s response

A large majority of LBF’s customers are individuals and SME’s, who were among the worst hit by the pandemic induced economic slowdown. Taking a proactive approach to support these customers, LBF took immediate action to assist eligible customers to benefit from the debt moratorium scheme. Other customers were supported by way of reschedulement plans, fee waivers and additional grace periods for the repayment.

To provide employees a sense of financial security during these uncertain times, no salary cuts or retrenchments were announced in the FY 2020/21. All LBF employees were paid their full salary throughout the pandemic period. All bonus entitlements were also paid in full, while field staff who were unable to earn their other benefits during the lockdown period, were provided the opportunity to recommence earning other benefit upon the resumption of normal business activities.

Impact Risk associate

Reputational risk

High Medium LowH M

M

L

Labour market indicators

8.592 Mn(2019)

52.3%(2019)

8.181 Mn(2019)

203,087(2019)

8.273 Mn(2020)

5.5%(2020)

8.467 Mn(2020)

50.6%(2020)

7.999 Mn(2020)

53,713(2020)

7.832 Mn(2019)

4.8%(2019)Labour force

Labour force participation rate

Employeed population

Departures for foreign employment

Economically inactive population

Unemployment rate

Source: CBSL AR 2020

L B Finance PLC | Annual Report 2020/21

Technological

Operating environment

During 2020, COVID-19 created an unprecedented change in the lifestyles of people around the world. Demand for traditional goods and services changed significantly with need for Information

Technology related services becoming the top priority. E-commerce became the new norm as merchants who had previously relied on conventional sales through physical outlets quickly adopted online sales platforms. At the same time,

customers also rapidly shifted to online shopping due to lockdowns and travel restrictions imposed to prevent the rapid spread of COVID-19.

Source: CBSL AR 2020

Short to medium term strategy

Develop new technology based solutions tailored to meet the needs of different customer segments

Long-term strategy

Track customer satisfaction and loyalty as a more frequent indicator across business units, channels, product interactions and customer journey moments

Related strategies Related material matters

MD’s statement on page 37, Strategic & resource allocation on page 74, Business segment reviews on page 102, Social and relationship capital on page 176

High Medium LowH M L

L B Finance PLC | Annual Report 2020/21

OUR BUSINESS ENVIRONMENT AND OUTLOOK

Impact on the NBFI sector

For the NBFI sector, the surge in demand for digital technology was the ideal opportunity to accelerate its digital strategy. Most NBFI’s were seen encouraging their customers to use online financial services to minimise their visits to branches. This resulted in increased usage of online banking websites and mobile banking applications. In yet another interesting development, even those with low levels of IT literacy were seen using these online financial services for their daily needs.

On the other hand, the boom of e-commerce poses a growth threat to information security, including customers’ sensitive data.

Impact to LBF and the Company’s response

As was the case across the industry, LBF too, saw a massive increase in the use of its digital platforms. A total of over one million transactions were channeled through LB CIM, the Company’s wallet application during the FY 2020/21, a 253.78% fold increase compared to the previous year.

As part of its ongoing efforts to build cyber resilience, LBF successfully completed its 3rd consecutive re-certification of the ISO 27001:2013 Information Security Standard for a further three-year period. A comprehensive new due diligence programme was also rolled out during the year in-line with industry best practices set under the IT audit framework by ISACA.

Impact Risk associate

Cyber security risk

Short to medium term strategy

Further strengthen information security architecture by implementing the data protection protocol and by investing in the latest DLP (Data Leakage Prevention) and PAM (Privilege Access Management) software

Long-term strategy

Further enhance the reliability of the BCP model by moving to a cloud-based environment

Related strategies Related material matters

MD’s statement on page 37, Strategic & resource allocation on page 74, Intellectual capital on page 166

Environment

Operating environment

While climate change issues may have taken a back seat in 2020 due to pandemic, such environmental concerns are ongoing both locally and in the global context. In the Global Climate Risk Index 2019, Sri Lanka was ranked 30 out of 180 countries in 2019 and was ranked 23 out of 180 countries in terms of overall performance over the

period 2000 – 2019. While it seems the country has moved out of the 10 most affected countries’ category in the index, climate change related vulnerabilities still persist.

Clear examples include the decline in the country’s forest cover. According to the forest cover assessment survey – 2015

(published in 2020) by the Department of Forest Conservation, the estimated total forest cover of the country was 1,865,671 hectares representing 28.4% of the land in Sri Lanka. The sizable decline from previously noted figures is attributed to population growth and rapid urbanisation in recent years.

Source: CBSL AR 2020

High Medium LowH M L

H

L B Finance PLC | Annual Report 2020/21

Impact on the NBFI sector

The most impactful way in which the NBFI sector can contribute towards reducing the country’s climate change risk, is by financing environmentally friendly projects. Many of the large NBFI’s in Sri Lanka have already entered the green lending sphere through products that focus on leasing hybrid vehicles and renewable energy financing

Impact to LBF and the Company’s response

As part of its auto finance business, LBF maintains a special green lending line which offers concessionary terms for the lease of hybrid vehicles and electric vehicles, which are deemed to have a significantly lower carbon footprint compared to traditional diesel or petrol vehicles

Impact Risk associate

Liquidity risk

Short to medium term strategy

Establish greed buildings and digital branches

Process automation

Long-term strategy

Expanded the coverage of green lending line to include renewable energy projects

Related strategies Related material matters

Strategy & resource allocation on page 74, Natural capital on page 196, Business segment reviews on page 102

Legal

Operating environment

The Financial Sector Consolidation Master Plan (FSCMP) was introduced in 2020 to address non-compliance with the

minimum core capital requirement and/or the minimum capital adequacy ratios by NBFI’s. The Central Bank also continued to introduce law reforms to major legislations during the year, key among them

amendments to the Finance Business Act to augment the regulatory and supervisory powers on non-bank financial institutions.

Source: CBSL AR 2020

Impact on the NBFI sector

The FSCMP and the revisions to the Finance Business Act are primarily aimed at maintaining the stability of NBFI’s in order to safeguard the interest of depositors, thereby enhancing the overall credibility of the sector as a whole

Impact to LBF and the Company’s response

LBF has always been a keen proponent of early adoption of regulations. In this year too, the Company continued to review and reorient itself to take cognizance of the latest regulatory developments as well as proposed changes come into effect in due course

Impact Risk associate

Liquidity risk

Short to medium term strategy

Maintain liquidity levels in line with regulatory benchmarks

Long-term strategy

Early adapted the new regulations which are imposed by the regulatory bodies

Related strategies Related material matters

MD’s statement on page 37, Strategy & resource allocation on page 74

High Medium LowH

H

M L

L

L B Finance PLC | Annual Report 2020/21

OUR BUSINESS ENVIRONMENT AND OUTLOOK

INFLUENCING MARKET DRIVERS, RISKS AND OPPORTUNITIES

There are a number of distinct factors that are shaping the financial services industry now and will continue to do so into the future. Linked to these market drivers are risks and opportunities, both general to

the external environment and a number that are specific to LBF. These are actively assessed and appropriate responses implemented, with the performance monitored both against our strategic

ambitions as well as through our principal and key risks as defined in our Risk Management Framework. Read more about on our Risk Management Report.

Competition and technological changeIncreasing competition, technology and the pace of change, impacts our ability to remain relevant to our customers as well as our competitiveness and the associated operational risk

LBF context

Launch L B finance CIM (Cash In Mobile) digital wallet to engage our customers to digital transactions

Market drivers

Disruption through new digitally-led competitor platforms which have the capacity to influence customer preferences

The need for threat detection software to safeguard against security breaches, and the possibility of data leakage

Ever increasing sophistication of cybercrime, fraud risk and financial crime requires continuous monitoring and ongoing investment to protect customers and the Group

Opportunities

Focus on creating innovative products and solutions to cater to maintain top of mind recall across a broader spectrum of customer segments

Leveraging on AI tools to strengthen resilience and protect against cyber crime

Key risks

Reputational risk (specifically brand risk) and people risk

Mitigation activities

Ongoing employee education on the prevention of cyber related risks

Ongoing investment in technology platforms, processes and controls including monitoring

Regulatory oversightNew and emerging regulations impact on our operations as well as our products and services

LBF context

Early adapted the new regulations which are imposed by the regulatory bodies

Market drivers

The increasing pace and evolving complexity of regulatory and statutory requirements across the Group’s operation

Opportunities

Maintaining a coordinated, comprehensive and forward-looking approach to evaluate regulatory change and respond through early adoption

Key risks

Market risk

Mitigation activities

Participating in regulatory and statutory advocacy groups across all stakeholder groups

L B Finance PLC | Annual Report 2020/21

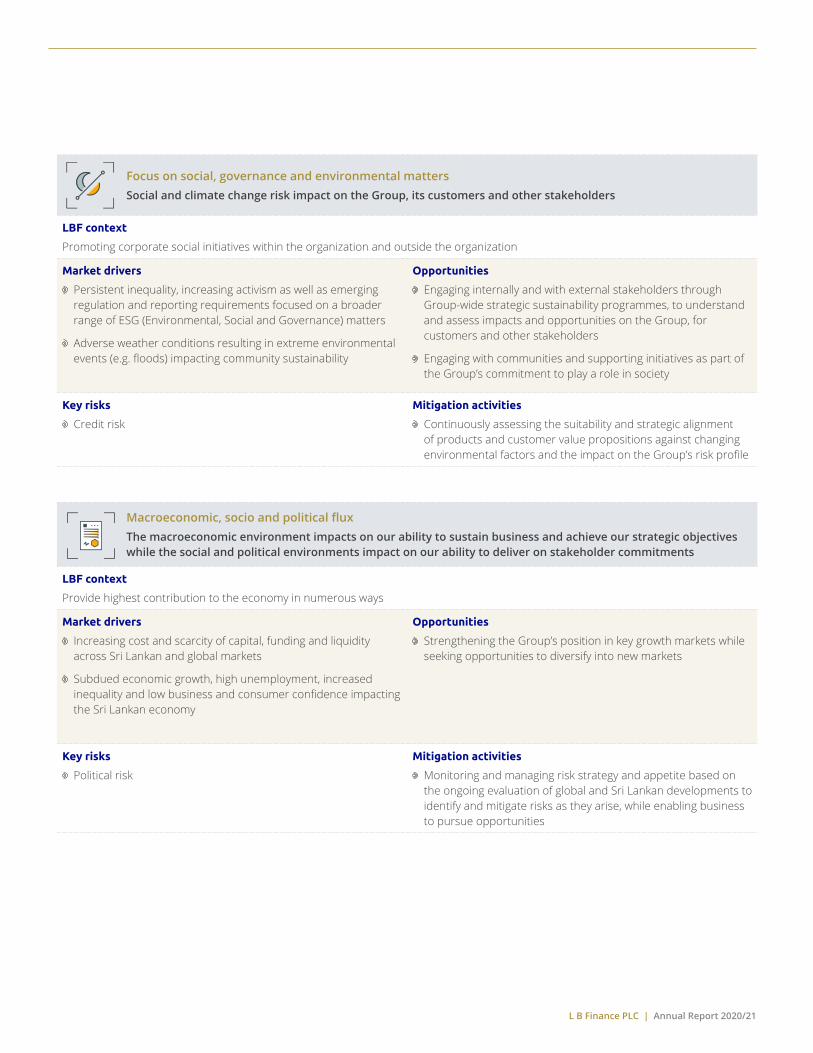

Focus on social, governance and environmental mattersSocial and climate change risk impact on the Group, its customers and other stakeholders

LBF context

Promoting corporate social initiatives within the organization and outside the organization

Market drivers

Persistent inequality, increasing activism as well as emerging regulation and reporting requirements focused on a broader range of ESG (Environmental, Social and Governance) matters

Adverse weather conditions resulting in extreme environmental events (e.g. floods) impacting community sustainability

Opportunities

Engaging internally and with external stakeholders through Group-wide strategic sustainability programmes, to understand and assess impacts and opportunities on the Group, for customers and other stakeholders

Engaging with communities and supporting initiatives as part of the Group’s commitment to play a role in society

Key risks

Credit risk

Mitigation activities

Continuously assessing the suitability and strategic alignment of products and customer value propositions against changing environmental factors and the impact on the Group’s risk profile

Macroeconomic, socio and political fluxThe macroeconomic environment impacts on our ability to sustain business and achieve our strategic objectives while the social and political environments impact on our ability to deliver on stakeholder commitments

LBF context

Provide highest contribution to the economy in numerous ways

Market drivers

Increasing cost and scarcity of capital, funding and liquidity across Sri Lankan and global markets

Subdued economic growth, high unemployment, increased inequality and low business and consumer confidence impacting the Sri Lankan economy

Opportunities

Strengthening the Group’s position in key growth markets while seeking opportunities to diversify into new markets

Key risks

Political risk

Mitigation activities

Monitoring and managing risk strategy and appetite based on the ongoing evaluation of global and Sri Lankan developments to identify and mitigate risks as they arise, while enabling business to pursue opportunities

L B Finance PLC | Annual Report 2020/21

OUR BUSINESS ENVIRONMENT AND OUTLOOK

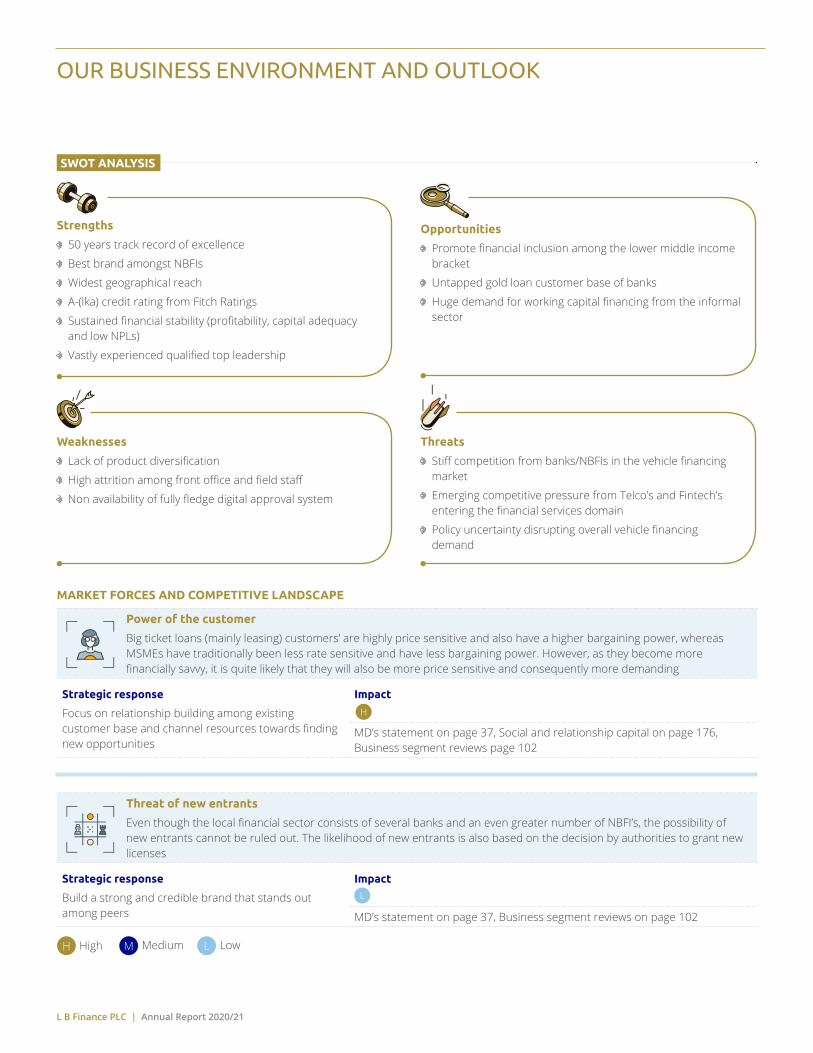

Strengths

50 years track record of excellence

Best brand amongst NBFIs

Widest geographical reach

A-(lka) credit rating from Fitch Ratings

Sustained financial stability (profitability, capital adequacy and low NPLs)

Vastly experienced qualified top leadership

Weaknesses

Lack of product diversification

High attrition among front office and field staff

Non availability of fully fledge digital approval system

Opportunities

Promote financial inclusion among the lower middle income bracket

Untapped gold loan customer base of banks

Huge demand for working capital financing from the informal sector

Threats

Stiff competition from banks/NBFIs in the vehicle financing market

Emerging competitive pressure from Telco’s and Fintech’s entering the financial services domain

Policy uncertainty disrupting overall vehicle financing demand

SWOT ANALYSIS

MARKET FORCES AND COMPETITIVE LANDSCAPE

Power of the customer

Big ticket loans (mainly leasing) customers’ are highly price sensitive and also have a higher bargaining power, whereas MSMEs have traditionally been less rate sensitive and have less bargaining power. However, as they become more financially savvy, it is quite likely that they will also be more price sensitive and consequently more demanding

Strategic response

Focus on relationship building among existing customer base and channel resources towards finding new opportunities

Impact

MD’s statement on page 37, Social and relationship capital on page 176, Business segment reviews page 102

Threat of new entrants

Even though the local financial sector consists of several banks and an even greater number of NBFI’s, the possibility of new entrants cannot be ruled out. The likelihood of new entrants is also based on the decision by authorities to grant new licenses

Strategic response

Build a strong and credible brand that stands out among peers

Impact

MD’s statement on page 37, Business segment reviews on page 102

High Medium LowH

H

M L

L B Finance PLC | Annual Report 2020/21

High Medium Low

Competitive rivalry

Number of competitors

The financial sector of Sri Lanka consists of 33 banks and 43 NBFI’s operating in the space

Switching cost

The switching cost for a customer is low due to a high concentration of service providers

Customer loyalty

Traditionally Sri Lankan customers have been reasonably loyal; however, competitive tactics among entities have greatly reduced loyalty levels especially across high net worth customer segments

Strategic response

Improve product mix, customer service and process efficiency to attract and retain customers. Explore new ways of delivering value and innovative means of utilising existing resources to extend our range of offerings

Impact

MD’s statement on page 37, Social and relationship capital on page 176, Business segment reviews on page 102

Power of the business partners

As a financial institution, our major suppliers comprise of support services. Given that they only provide support services, the bargaining power of business partners are low

Strategic response

Focus on a diversified pool of support service providers to reduce risk of over- dependence on any specific group of service providers

Impact

Social and relationship capital on page 176, Business segment reviews on page 102

Threat of substitute products

Low threat within the NBFI Industry. However, if we consider loan and leasing products from banks and the leasing companies as substitute products, then the threat is high. Additionally, for some segments, there exists a high threat of substitute products; for instance, in vehicle loans where some of the vehicle suppliers themselves offer the vehicles in installments, removing the need of getting a financier involved. There is a material threat in the medium and long run, with the potential for innovating alternative ways of creating value in meeting lending needs of businesses and individuals

Strategic response

Stay updated with industry best practices and new opportunities offered through technology and incentives

Impact

Social and relationship capital on page 176, Business segment reviews on page 102

L B Finance PLC | Annual Report 2020/21

OUR BUSINESS ENVIRONMENT AND OUTLOOK

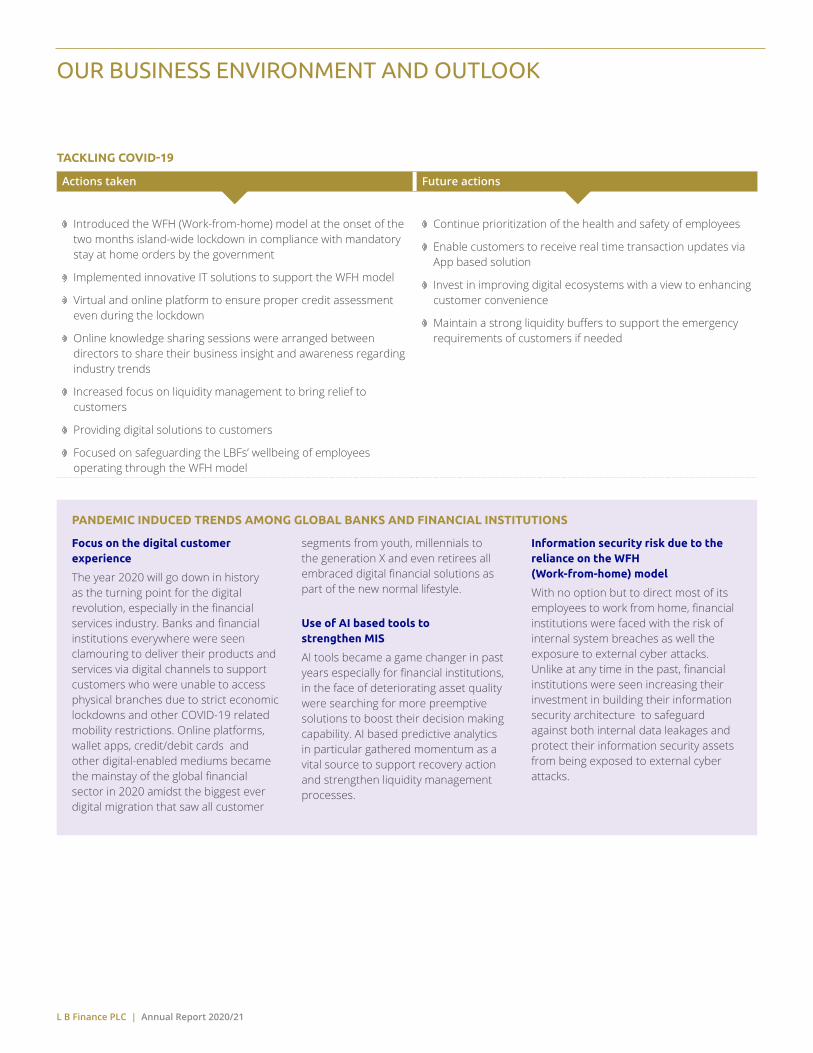

TACKLING COVID-19

Actions taken Future actions

Introduced the WFH (Work-from-home) model at the onset of the two months island-wide lockdown in compliance with mandatory stay at home orders by the government

Implemented innovative IT solutions to support the WFH model

Virtual and online platform to ensure proper credit assessment even during the lockdown

Online knowledge sharing sessions were arranged between directors to share their business insight and awareness regarding industry trends

Increased focus on liquidity management to bring relief to customers

Providing digital solutions to customers

Focused on safeguarding the LBFs’ wellbeing of employees operating through the WFH model

Continue prioritization of the health and safety of employees

Enable customers to receive real time transaction updates via App based solution

Invest in improving digital ecosystems with a view to enhancing customer convenience

Maintain a strong liquidity buffers to support the emergency requirements of customers if needed

PANDEMIC INDUCED TRENDS AMONG GLOBAL BANKS AND FINANCIAL INSTITUTIONS

Focus on the digital customer experience

The year 2020 will go down in history as the turning point for the digital revolution, especially in the financial services industry. Banks and financial institutions everywhere were seen clamouring to deliver their products and services via digital channels to support customers who were unable to access physical branches due to strict economic lockdowns and other COVID-19 related mobility restrictions. Online platforms, wallet apps, credit/debit cards and other digital-enabled mediums became the mainstay of the global financial sector in 2020 amidst the biggest ever digital migration that saw all customer

segments from youth, millennials to the generation X and even retirees all embraced digital financial solutions as part of the new normal lifestyle.

Use of AI based tools to strengthen MIS

AI tools became a game changer in past years especially for financial institutions, in the face of deteriorating asset quality were searching for more preemptive solutions to boost their decision making capability. AI based predictive analytics in particular gathered momentum as a vital source to support recovery action and strengthen liquidity management processes.

Information security risk due to the reliance on the WFH (Work-from-home) model

With no option but to direct most of its employees to work from home, financial institutions were faced with the risk of internal system breaches as well the exposure to external cyber attacks. Unlike at any time in the past, financial institutions were seen increasing their investment in building their information security architecture to safeguard against both internal data leakages and protect their information security assets from being exposed to external cyber attacks.

Related Documents