1 Risk management applications of option strategies Mai Thu Hien Faculty of Banking and Finance Foreign Trade University Email: [email protected] Web: http://web.ftu.edu.vn/maithuhien/ Outline • Introduction to option • Risk management using option strategies: – Option strategies for equity portfolios – Interest rate option strategies – Option portfolio risk management strategies (Delta Gamma Vega) – Option portfolio risk management strategies (Delta, Gamma, Vega) • Option pricing – Principles of option pricing (Properties of stock options) – Binomial trees – The Black-Scholes-Merton model – The Greek letters Readings • Multinational Business Finance, Eiteman, 12e, 2010 • Options, Futures and other Derivatives, Hull, 8e, 2012 • An Introduction to Derivatives and Risk management, Chance and Brooks, 7e, 2008 CFA L l 1 (2009) 2 (2010) 3 (2011) • CFA Level 1 (2009),2 (2010),3 (2011)

Option.forstudentFX

Oct 24, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Risk management applications of option strategiesp g

Mai Thu HienFaculty of Banking and Finance

Foreign Trade UniversityEmail: [email protected]

Web: http://web.ftu.edu.vn/maithuhien/

Outline

• Introduction to option• Risk management using option strategies:

– Option strategies for equity portfolios– Interest rate option strategies– Option portfolio risk management strategies (Delta Gamma Vega)– Option portfolio risk management strategies (Delta, Gamma, Vega)

• Option pricing– Principles of option pricing (Properties of stock options)– Binomial trees– The Black-Scholes-Merton model– The Greek letters

Readings

• Multinational Business Finance, Eiteman, 12e, 2010• Options, Futures and other Derivatives, Hull, 8e, 2012• An Introduction to Derivatives and Risk management,

Chance and Brooks, 7e, 2008CFA L l 1 (2009) 2 (2010) 3 (2011)• CFA Level 1 (2009),2 (2010),3 (2011)

2

An introduction to option

Options• An option is a contract giving the option purchaser (the

buyer) the right, but not the obligation, to buy or sell a given amount of the undelying asset at a fixed price per unit for a specified time period (until the maturity date)

• There are two basic types of options, puts and calls.A call is an option to buy the undelying asset

5

A put is an option to sell the undelying asset • The buyer of an option is termed the holder, while the

seller of the option is referred to as the writer or grantor.• An American option gives the buyer the right to exercise

the option at any time between the date of writing and the expiration or maturity date.

• An European option can be exercised only on its expiration date.

6

3

Foreign currency options

• Every option has three different price elements:The exercise or strike price – the price at which the undelying asset can be purchased (call) or sold (put).The premium – the cost, price, or value of the option itself usually paid in advance by the buyer to the

7

itself- usually paid in advance by the buyer to the seller. An option‘s value at expiration is called its payoff.The underlying or actual spot price in the market.

The concept of moneyness of an option

• For Put OptionsIn-the-Money = Spot Price is below Option Strike (Exercise) PriceOut-of-the Money = Spot Price is above Option Strike (Exercise) PriceAt the Money = Spot Price and Strike (Exercise) Price

8

At-the-Money = Spot Price and Strike (Exercise) Price are the same

• For Call OptionsIn-the-Money = Spot Price is above Option Strike (Exercise) PriceOut-Of-the-Money = Spot Price is below Option Strike (Exercise) PriceAt-The Money = Spot Price and Option Strike (Exercise) Price are the same

Example

Strike price Spot price Calls Puts

A contract is traded at the spot price of $1,170

9

1,175 > 1,170 OTM ITM1,170 = 1,170 ATM ATM1,165 < 1,170 ITM OTM

4

Profit/loss for a call option

• Spot price > Strike price: the buyer would excercise the option and possesses an unlimited profit potential.

• Spot price < Strike price: the buyer would choose not to excercise the option and his total loss would be limited to only what he paid for the option (limited loss potential).

• Strike price < Spot price < break-even price: the gross

10

Strike price Spot price break even price: the gross profit earned on excercising the option and selling the underlying currency covers part (but not all) of the premium cost.

Profit/loss for a put option

• Spot price < Strike price: the buyer would excercise the option and has unlimited profit potential (up to a maximum of strike price minus primium, when spot price would be zero)

• Spot price > Strike price: the buyer would choose not to i th ti d ld l l th i

11

excercise the option and so would lose only the premium paid for the option (limited loss potential).

• Break-even price < Spot price < Strike price: the buyer will recoup part (but not all) of the premium cost, the writer will lose part, but not all, of the premium received

Profit and Loss for the Buyer of a Call Option

• Buyer of a call:– Assume purchase of August call option on Swiss

francs with strike price of 58½ ($0.5850/SF), and a premium of $0.005/SF

– At all spot rates below the strike price of 58.5, the

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

p ppurchase of the option would choose not to exercise because it would be cheaper to purchase SF on the open market

– At all spot rates above the strike price, the option purchaser would exercise the option, purchase SF at the strike price and sell them into the market netting a profit (less the option premium)

5

Profit (US cents/SF)

+ 1.00

+ 0.50Unlimited profit

Strike price

“Out of the money” “In the money”

“At the money”

Profit and Loss for the Buyer of a Call Option on Swiss francs

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

Loss

0

- 0.50

- 1.00

57.5 58.0 59.0 59.558.5Limited loss

Unlimited profit

Break-even price

Spot price(US cents/SF)

The buyer of a call option on SF, with a strike price of 58.5 cents/SF, has a limited loss of 0.50 cents/SF at spot rates less than 58.5 (“out of the money”), and an unlimited profit potential at spot rates above 58.5 cents/SF (“in the money”).

Exhibit 8.4 Buying a Call Option on Swiss Francs (long call)

14 Profit = (Spot Rate – Strike Price) - Premium

Profit and Loss for the Writer of a Call Option

• Writer of a call:– What the holder, or buyer of an option loses, the writer

gains– The maximum profit that the writer of the call option can

make is limited to the premium

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

p– If the writer wrote the option naked, that is without owning

the currency, the writer would now have to buy the currency at the spot and take the loss delivering at the strike price

– The amount of such a loss is unlimited and increases as the underlying currency rises

– Even if the writer already owns the currency, the writer will experience an opportunity loss

6

Profit (US cents/SF)

+ 1.00

+ 0.50Limited profit Break-even price

Strike price“At the money”

Profit and Loss for the Writer of a Call Option on Swiss francs

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

Loss

0

- 0.50

- 1.00

57.5 58.0 59.0 59.558.5

Unlimited loss

Spot price(US cents/SF)

The writer of a call option on SF, with a strike price of 58.5 cents/SF, has a limited profit of 0.50 cents/SF at spot rates less than 58.5, and an unlimited loss potential at spot rates above (to the right of) 59.0 cents/SF.

Exhibit 8.5 Selling a Call Option on Swiss Francs (short call)

17 Profit (loss) = Premium – (Spot Rate – Strike Price)

Profit and Loss for the Buyer of a Put Option

• Buyer of a Put:– The basic terms of this example are similar to those just

illustrated with the call– The buyer of a put option, however, wants to be able to sell the

underlying currency at the exercise price when the market price of that currency drops (not rises as in the case of the call option)

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

of that currency drops (not rises as in the case of the call option)– If the spot price drops to $0.575/SF, the buyer of the put will

deliver francs to the writer and receive $0.585/SF– At any exchange rate above the strike price of 58.5, the buyer of

the put would not exercise the option, and would lose only the $0.05/SF premium

– The buyer of a put (like the buyer of the call) can never lose more than the premium paid up front

7

Profit (US cents/SF)

+ 1.00

+ 0.50 Profit up

Strike price

“In the money” “Out of the money”

“At the money”

Profit and Loss for the Buyer of a Put Option on Swiss francs

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

Loss

0

- 0.50

- 1.00

57.5 58.0 59.0 59.558.5Limited loss

to 58.0Spot price(US cents/SF)

The buyer of a put option on SF, with a strike price of 58.5 cents/SF, has a limited loss of 0.50 cents/SF at spot rates greater than 58.5 (“out of the money”), and an unlimited profit potential at spot rates less than 58.5 cents/SF (“in the money”) up to 58.0 cents.

Break-evenprice

Exhibit 8.6 Buying a Put Option on Swiss Francs (long put)

20 Profit = (Strike Price – Spot Rate) - Premium

Profit and Loss for the Writer of a Put Option

• Seller (writer) of a put:– In this case, if the spot price of francs drops below

58.5 cents per franc, the option will be exercised

– Below a price of 58.5 cents per franc, the writer will

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

p p ,lose more than the premium received fro writing the option (falling below break-even)

– If the spot price is above $0.585/SF, the option will not be exercised and the option writer will pocket the entire premium

8

Profit (US cents/SF)

+ 1.00

+ 0.50

Strike price

Break-evenprice

“At the money”

Profit and Loss for the Writer of a Put Option on Swiss francs

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

Loss

0

- 0.50

- 1.00

57.5 58.0 59.0 59.558.5Unlimited lossup to 58.0

Limited profit

Spot price(US cents/SF)

The writer of a put option on SF, with a strike price of 58.5 cents/SF, has a limited profit of 0.50 cents/SF at spot rates greater than 58.5, and an unlimited loss potential at spot rates less than 58.5 cents/SF up to 58.0 cents.

Exhibit 8.7 Selling a Put Option on Swiss Francs (short put)

23 Profit (loss) = Premium – (Strike Price – Spot Price)

Call Option position ST ≤ X ST > X

Option value at expiration (payoffs) cT

Long Call cT = max (0, ST – X)0 *(OTM) ST – X (ITM)

Short Call -cT = -max (0, ST – X)0 X - ST

Profit Π

Long Call c – c = max (0 S – X) – cLong Call cT – c0 = max (0, ST – X) – c0

-c0 ST - X– c0

Short Call -cT + c0

c0 X - ST + c0

Breakeven point Maximum profit Minimum lossLong Call ST* = X + c0 ∞ c0

Short Call ST* = X + c0 c0 ∞c0 : call option premium*/: cT cannot sell for less than zero because that would mean that the option seller would have to pay the option buyer. A buyer would not pay more than zero because the option will expire an instant later with no value). Special case: ST = X option is treated as OTM because the option is 0 at expiration.

9

Example

Call option: exercise price: USD2000, premium c = USD81.75.

• Determine the value at expiration and profit for a buyer under two outcomes: the price of underlying at expiration is USD1900 and 2100

• Determine the maximum profit and loss to the buyer• Determine the breakeven price of the underlying at

expiration • Graph the value at expiration and the profit

Example

• For ST = 1900, cT = max (0, ST – X) = max(0, 1900 - 2000) = 0Π = cT – c0 = 0 – 81.75 = -81.75

• For ST = 2100, cT = max(0, 2100 - 2000) = 100Π = 100 – 81.75 = 18.25Maximum profit of the buyer: ∞Maximum loss of the buyer = c0 = 81.75

• ST*= X + c0 = 2000 + 81.75 = 2081.75

ST = 1900, cT = 0, Π = -81.75 ST = 2100, cT = 100, Π = 18.25Maximum profit of the buyer: ∞Maximum loss of the buyer = c0 = 81.75ST*= 2081.75

Value at Expiration

$

2000-81.75

2081.75

1900 2100 Value of Underlying at Expiration

100

Profit (Long call)

0

10

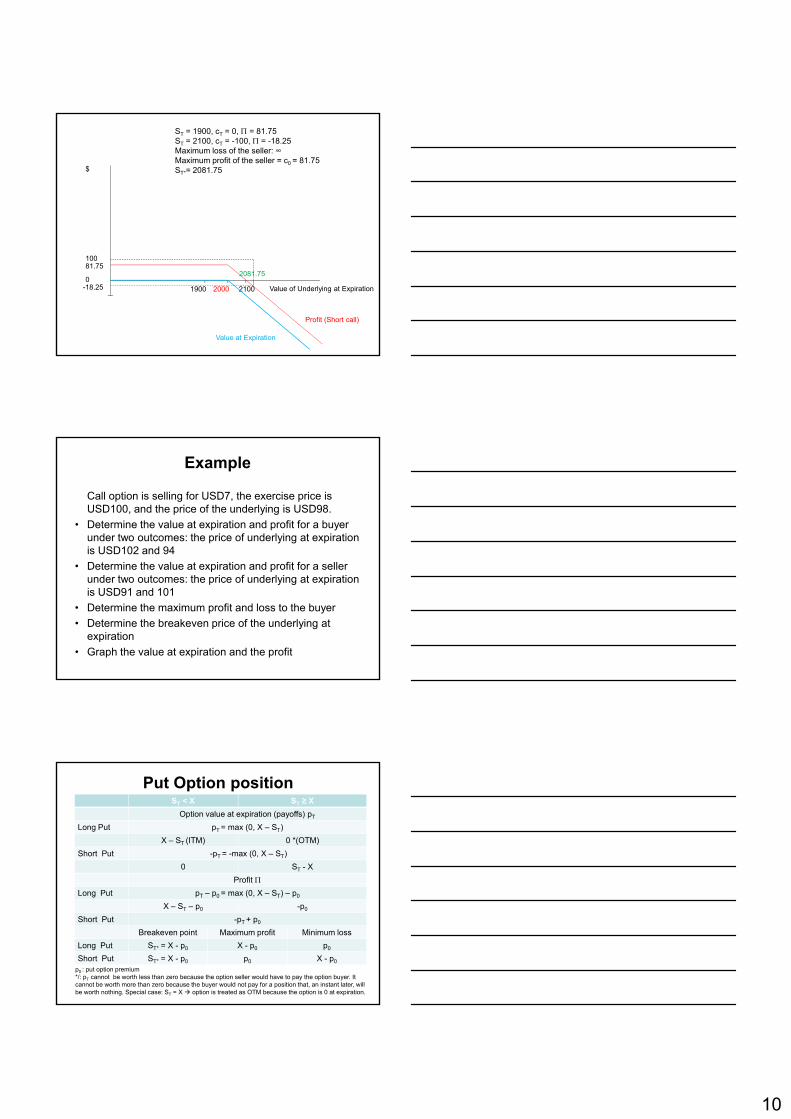

ST = 1900, cT = 0, Π = 81.75 ST = 2100, cT = -100, Π = -18.25Maximum loss of the seller: ∞Maximum profit of the seller = c0 = 81.75ST*= 2081.75$

2000

81.752081.75

1900 2100 Value of Underlying at Expiration

100

Value at Expiration

Profit (Short call)

0-18.25

Example

Call option is selling for USD7, the exercise price is USD100, and the price of the underlying is USD98.

• Determine the value at expiration and profit for a buyer under two outcomes: the price of underlying at expiration is USD102 and 94

• Determine the value at expiration and profit for a seller under two outcomes: the price of underlying at expiration is USD91 and 101

• Determine the maximum profit and loss to the buyer• Determine the breakeven price of the underlying at

expiration • Graph the value at expiration and the profit

Put Option position ST < X ST ≥ X

Option value at expiration (payoffs) pT

Long Put pT = max (0, X – ST)X – ST (ITM) 0 *(OTM)

Short Put -pT = -max (0, X – ST)0 ST - X

Profit ΠLong Put pT – p0 = max (0, X – ST) – p0

X – ST – p0 -p0

Short Put -pT + p0

Breakeven point Maximum profit Minimum lossLong Put ST* = X - p0 X - p0 p0

Short Put ST* = X - p0 p0 X - p0p0 : put option premium*/: pT cannot be worth less than zero because the option seller would have to pay the option buyer. It cannot be worth more than zero because the buyer would not pay for a position that, an instant later, will be worth nothing. Special case: ST = X option is treated as OTM because the option is 0 at expiration.

11

ExamplePut option: Exercise price USD2000, premium p = USD79.25.

• Determine the value at expiration and profit for a buyer under two outcomes: the price of underlying at expiration is USD1900 and 2100

• Determine the maximum profit and loss to the buyer• Determine the breakeven price of the underlying at expiration • Graph the value at expiration and the profit

Example

• For ST = 1900, pT = max (0, X – ST) = max(0, 2000 - 1900) = 100Π = pT – p0 = 100 – 79.25 = 20.75

• For ST = 2100, pT = max(0, 2000 - 2100) = 0Π = 0 – 79.25 = -79.25Maximum profit to the buyer: X – p0 = 2000 – 79.25 = 1920.75Maximum loss to the buyer : p0 = 79.25

• ST*= X – p0 = 2000 – 79.25 = 1920.75

For ST = 1900, pT = 100, Π = 20.75 For ST = 2100, pT = 0, Π = 79.25Maximum profit to the buyer: X – p0 = 2000 – 79.25 = 1920.75Maximum loss to the buyer : p0 = 79.25ST*= X – p0 = 2000 – 79.25 = 1920.75

Value at Expiration

$

2000-79.25

1920.75

1900

2100

Value of Underlying at Expiration

100

Profit (Long put)

020.75

12

For ST = 1900, pT = -100, Π = -20.75 For ST = 2100, pT = 0, Π = -79.25Maximum profit to the seller: p0 = 79.25Maximum loss to the seller: X – P0 = 2000 – 79.25 = 1920.75ST*= X – p0 = 2000 – 79.25 = 1920.75

$

2000-79.25

1920.75

1900 2100 Value of Underlying at Expiration

Value at Expiration Profit (Short put)

020.7579.25

-100

ExamplePut option is selling for USD4 in which the exercise price is USD60 and the price of the underlying is USD62.

• Determine the value at expiration and profit for a buyer under two outcomes: the price of underlying at expiration is USD62 and 55

• Determine the value at expiration and profit for a seller under two outcomes: the price of underlying at expiration is USD51 and 68

• Determine the maximum profit and loss to the buyer• Determine the breakeven price of the underlying at expiration • Graph the value at expiration and the profit

Hedging using option strategies for equity portfoliog q y p

13

Risk management using option strategies • Risk management strategies with options and the underlying:

– covered call, protective put

• Risk management strategies (spread) involve taking a position in two or more options of the same type (two or more calls or two or more puts):

– Money spread (different strike prices and the same expiration date)• bull spreads (market goes up, 2 calls or puts), • bear spreads (market goes down, 2 calls or puts), • butterfly spreads (combining bull and bear spread in options with 3 different strike price)

Time (calendar) spread (the same strike prices and different expiration dates)– Time (calendar) spread (the same strike prices and different expiration dates)– Diagonal spread (different strike prices and different expiration dates)

• Combination is an option trading strategy that involves taking a position in both calls and puts on the same stock:

– collars (involves the offsetting the payment of the put premium by selling a call with a premium equal to the put premium)

– straddle (if we expect that the market to be volatile but do not have strong feelings on the direction). The straddle has other variations such as straps, strips, strangles.

– box spreads (combine bull and bear spread with different strike price).

Risk management strategies with options and the underlying

Examine the option strategies for holders of the underlying without selling the underlying by:

• Selling a call on the underlying (covered call)• Buying a put on the underlying (protective put)

Covered calls• A covered call is a position in which an investor owns the underlying and

sell a call. Selling a call provides some protection to the holder of the underlying against a fall in the price of the underlying.

• The value of the position at expiration is easily found as the value of the underlying plus the value of the short call:VT = ST – max(0,ST – X)Th f V S if S ≤ XTherefore: VT = ST if ST ≤ X

VT = ST – (ST – X) = X if ST > X• The value of the position at the start of the contract is the initial value of

the underlying minus the call premium: V0 = S0 – c0

14

Covered calls• The profit for the covered call is the change in the value of the position

at expiration and at the start:Π = VT – V0 = ST – max(0,ST – X) – (S0 – c0)Π = ST – S0 - max(0,ST – X) + c0the profit from the underlying the profit form selling the call

• Breaking it down into ranges:Π = ST – S0 + c0 if ST ≤ XΠ = ST – S0 – (ST – X) + c0 = X – S0 + c0 if ST > XTh i fit i X S h S X b if S X thThe maximum profit is X – S0 + c0 when ST = X because if ST > X, the call will be exercised at X and thus the seller’s profit is limited to X. If ST< X, the option will not be exercised, the profit of the seller is simply the profit from the underlying ST – S0 and the profit is maximized when ST = X.The maximum loss is S0 - C0 when ST = 0 because the maximum loss from the underlying if the underlying value went to zero, thus the loss from the underlying is the cost from buying the underlying S0, but the seller receives the premium from the sale of the call. Thus, the maximum loss is S0 - c0.

• Breakeven point ST* means Π = 0 when ST ≤ X or ST* = S0 - c0

Example Consider a covered call with the exercise price of USD2050, the premium c = USD59.98, the underlying asset is USD2000.

• Determine the value of the position at expiration and the profit under the following outcomes: the price of the underlying is USD2100 and 1900

• Determine the maximum profit and loss• Determine the breakeven price at expiration

ExampleConsider a bond selling for USD98 per USD100 face value. A call option selling for USD8 has an exercise price of USD105. Answer the following questions about a covered call.

• Determine the value of the position at expiration and the profit under the following outcomes: the price of the underlying is USD110 and 88

• Determine the maximum profit and loss• Determine the breakeven price at expiration

15

Protective put• A protective put is a strategy in which an investor holds an asset and a

put on the asset. It provides downside protection while retaining the upside potential, but it does so at the expense of requiring the payment of cash up front. In contrast, a covered call generates cash up front but removes some of the upside potential.

• The value at expiration is found by combing the value of the two strategies of buying the asset and buying the put:VT = ST + max(0,X - ST)Thus: VT = ST + (X - ST) = X if ST ≤ X

VT = ST if ST > X• The initial value of the position is the initial price of the underlying plus

the premium on the put: V0 = S0 + p0

Protective put• The profit is the change in the value of position. Hence,

Π = VT – V0 = ST + max(0,X - ST) – (S0 + p0)• The profit can be broken down as follows

Π = X – (S0 + p0) if ST ≤ XΠ = ST – (S0 + p0) if ST > XThe maximum profit is infinite ∞ because the put holder hasThe maximum profit is infinite because the put holder has no profit limit on the upside. The maximum loss when we sell the underlying for exercise price, but the up front cost of the underlying and the put is ST = S0 + p0. Thus the maximum loss is S0 + p0 – X.

• The breakeven value ST* means Π = 0 if ST > X, hence ST*= S0 + p0

If Π = X – (S0 + p0) when ST ≤ X, there is not value of the underlying that will allow us to breakeven.

ExampleProtective Put with the exercise price of USD1950, p = USD56.01, the underlying asset is USD2000.

• Determine the value of the position at expiration and the profit under the following outcomes: the price of the underlying is USD2100 and 1900

• Determine the maximum profit and loss• Determine the breakeven price at expiration

16

ExampleConsider a currency selling for USD0.875. A put option selling for USD0.075 has an exercise price of USD0.90. Answer the following questions about a protective put.

• Determine the value of the position at expiration and the profit under the following outcomes: the price of the underlying is USD0.96 and 0.75

• Determine the maximum profit and loss• Determine the breakeven price at expiration

Covered Call and Protective Put position ST ≤ X ST > X

Value at expiration Covered Call VT = ST - max (0, ST – X)

ST XProtective Put VT = ST + max (0,X – ST)

X ST

Profit Π

Covered Call VT – V0 = ST – S0 - max(0,ST – X) + c0

ST – S0 + c0 X – S0 + c0

Protective Put VT - S0 – p0

X – (S0 + p0) ST – (S0 + p0) Breakeven point Maximum profit Minimum loss

Covered Call ST* = S0 - c0 X – S0 + c0 S0 - c0

Protective Put ST* = S0 + p0 ∞ S0 + p0 - X

Combinations

• A combination is an option strategy that involves taking a position in both calls and puts on the same stock. – collars (involves the offsetting the payment of the put premium

by selling a call with a premium equal to the put premium)– straddle (if we expect that the market to be volatile but do not

have strong feelings on the direction). The straddle has other variations such as straps, strips, strangles.

– box spreads (combine bull and bear spread with diffenrent strike price).

17

Collars• A collar is a strategy which involves the offsetting the payment of the

put premium by selling a call with a premium equal to the put premium and a strike price above the current price of the underlying.

• When this offsetting occurs, no net premium is required upfront and it is sometimes called a zero-cost collar.

• It is not necessary that the call premium offset the put premium and the call premium can even more than the put premium.

• A collar is a modified version of a protective put and a covered call and requires different strike prices for each. If we want the call premium to offset the put premium, the strike price on the call muss be set such that the price of the call equals the price of the put.

• We thus can select any strike price of the put. Then the call strike price is selected by determining which strike price will produce a call premium equal to the put premium.

• Although the put can have any strike price, typically the put strike price is lower than the current value of the underlying. The call strike price then must be above the current value of the underlying.

Collars• Let the put strike price be X1 and the call strike price be

X2. • The value of the position at expiration is the sum of the

value of the underlying asset, the value of the long put, and the value of the short call: VT = ST + max(0, X1 – ST) - max(0, ST – X2) T T ( 1 T) ( T 2)

• The profit Π = VT – V0, where V0 = S0 (the value of the underlying):Π = VT – V0 = ST + max(0, X1 – ST) - max(0, ST – X2) – S0

CollarsThe underlying Long put Short call Total

Value at expiration VT = ST + max(0, X1 – ST) - max(0, ST – X2) ST ≤ X1 ST X1 – ST 0 X1

X1 < ST < X2 ST 0 0 ST

ST ≥ X2 ST 0 ST - X2 X2

Profit Π = VT – V0 = ST + max(0, X1 – ST) - max(0, ST – X2) – S0

ST ≤ X1 X1 – S0ST ≤ X1 X1 S0

X1 < ST < X2 ST – S0

ST ≥ X2 X2 – S0

Breakeven point Maximum profit Minimum lossCollar ST* = S0 X2 – S0 S0 – X1

18

Example

Consider the Nasdaq example. Suppose we use the put with X1 = 1950, p1 = 56.01. So now we need a call with premium of 56.01. The call with strike price of 2000 is worth 81.75. By trial and error, we have the call with the strike price of X2 = 2060 and the call price c2 = 56.01. Now we buy the put with a strike price of 1950 for 56 01Now we buy the put with a strike price of 1950 for 56.01 and sell the call with strike price of 2060 for 56.01. This transition requires no cash up front.

• Determine the value at expiration and profit under the outcomes in which the asset price at expiration is 1900, 2000, and 2100.

• Determine the maximum profit and loss• Determine the breakeven asset price at expiration

Zero-cost collar (buy put with strike price X1, sell call with strike price X2, put and call premium offset)

X1 X2S0

Example

The holder of a stock worth USD42 is considering placing a collar on it. A put with an exercise price of USD40 costs USD5.32. A call with the same premium would require an exercise price of USD50.59.

• Determine the value at expiration and profit under the outcomes in which the asset price at expiration is 55, 48, and 35.

• Determine the maximum profit and loss• Determine the breakeven asset price at expiration

19

Range forwards• Collars are also known as range forwards. • A range forward contract is a variation on a standard

forward contract for hedging foreign exchange risk. • A range forward contract is created by buying a European

put option with a strike price of X1 and selling a European call option with a strike price X where X < S < Xcall option with a strike price X2, where X1 < S0 < X2.

• As strike price of the call and the put in a range forward contract are moved closer, the range forward becomes a regular forward contract.

• Like a forward, a collar requires no initial outlay other than the underlying

• Unlike a forward, which has a strictly linear payoff profile, the collar payoff break at the two strike price, thus creating a range.

Range forward(a short range-forward contract is used to hedge a future foreign currency inflow)

• Consider a company that knows it will receive GBP1 million in 3 months. Suppose that the 3-month forward rate is USD1.52/GBP.

• The company could lock in this exchange rate by entering into a short forward contract to sell GBP1 million in 3 months.

• An alternative is to buy a European put option with a strike price of X1 and sell a European call option with a strike price X2, where X1 < 1.5200 < X2

• If ST < X1 : the put option is exercised and the company sells GBP at X1

• If X1 < ST < X2: neither option is exercised and the company gets the current exchange rate for GBPrate for GBP

• If ST > X2: the call option is exercised and the company sells GBP at X2

Asset price

PayoffX2

X2

X1

X1

Exchange rate in the market

Exchange rate realized when range-forward contract is used

Range forward(a long range-forward contract is used to hedge a future foreign currency outflow)

• Consider a company that knows it will pay GBP1 million in 3 months. Suppose that the 3-month forward rate is USD1.52/GBP.

• The company could lock in this exchange rate by entering into a long forward contract to buy GBP1 million in 3 months.

• An alternative is to sell a European put option with a strike price of X1 and buy a European call option with a strike price X2, where X1 < 1.5200 < X2

• If ST < X1 : the put option is exercised and the company buys GBP at X1

• If X1 < ST < X2: neither option is exercised and the company gets the current exchange rate for GBPrate for GBP

• If ST > X2: the call option is exercised and the company buys GBP at X2

Asset price

PayoffX2

X2

X1

X1

Exchange rate in the market

Exchange rate realized when range-forward contract is used

20

Option Pricing

Notationc: European call option

price

p: European put optionprice

S0: Stock price today

C: American call option price

P: American put optionprice

ST: Stock price at option

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 201259

S0: Stock price today

K or X: Strike price

T: Life of option

σ: Volatility of stock price

maturity

D: PV of dividends paid during life of option

r Risk-free rate for maturity T with cont. comp.

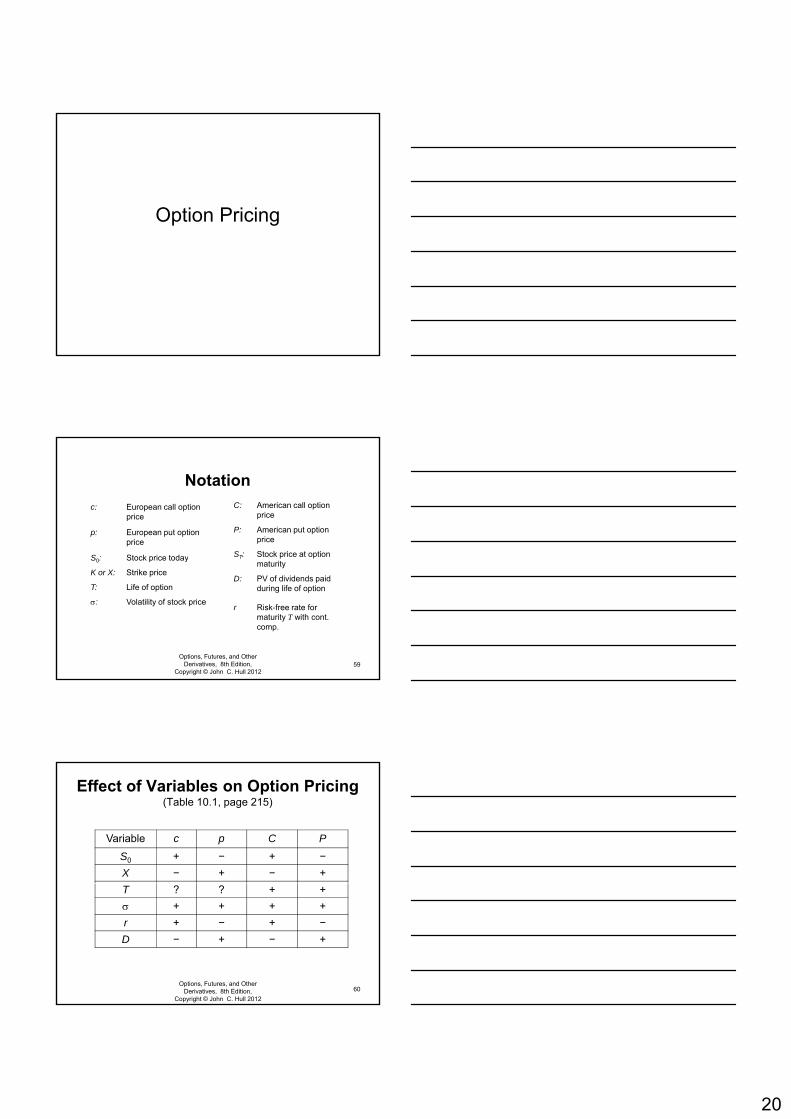

Effect of Variables on Option Pricing (Table 10.1, page 215)

Variable c p C P

S0 + − + −X − + − +

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 2012

T ? ? + +σ + + + +r + − + −D − + − +

60

21

American vs European Options

An American option is worth at least as much as the corresponding European option

C ≥ cP ≥ p

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 201261

Maximum and minimum values of options

Option Minimum Value Maximum Value (upper bound)European call c0 ≥ 0 c0 ≤ S0

American call C0 ≥ 0 C0 ≤ S0

European put p0 ≥ 0 p0 ≤ X/(1+r)T or p0 ≤ Xe-rT (T=n/365)

• The minimum value of any option is zero.• The maximum value of a European and an American call

is the current value of underlying. • The maximum value of a European put is the present

value of the exercise price. The maximum value of an American put is the exercise price.

American put P0 ≥ 0 P0 ≤ X

Lower bound for a European call onnon-dividend-paying stock

• Portfolio A: One European call on a stock + a zero coupon bond (with a face value equal to the exercise price and the current value equal to the present value of the exercise price) that provides a payoff of X at time T. This involves borrowing or lending an amount of money equal to the present value of exercise price with repayment of the full exercise price.

• Portfolio B: one share of the stock• The investor can buy the call and the bond and sell short the stock.

Short selling involves borrowing the asset and selling it At expiration weShort selling involves borrowing the asset and selling it. At expiration we shall buy back the asset.

Value at expirationCurrent value ST ≤ X ST > X

Portfolio ABuy call c0 0

(not exercise)ST - X

(exercise)

Buy bond X/(1+r)T or Xe-rT X XTotal = max(ST,X) at T X ST

Portfolio B Sell short stock -S0 -ST (minus sign means buying back)

-ST

Total c0 - S0 + X/(1+r)T X - ST 0

22

Lower bound for a European call on non-dividend-paying stock

• This combination has a negative value in no case at expiration. Thus, the current value of the position must be positive c0 - S0 + X/(1+r)T ≥ 0 c0 + X/(1+r)T ≥ S0

c0 ≥ S0 - X/(1+r)T

• Or we can say at time T portfolio A is worth max(S X)• Or we can say at time T, portfolio A is worth max(ST,X). Portfolio B is worth ST. Hence A is always worth as much as, and can be worth more than, B at option’s maturity (A ≥ B). In the absence of arbitrage, this must also be true today. Thus c0 + X/(1+r)T ≥ S0

• Because the worst that can happen to a call is that it expires worthless, its value cannot be negative. This means that c0 ≥ 0, and therefore c0 ≥ max(0, S0 - X/(1+r)T)

Calls: An Arbitrage Opportunity?• Suppose that

c = 3 S0 = 20 T = 1 r = 10% X = 18 D = 0

• Is there an arbitrage opportunity?

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 201265

Lower bound for a European put on non-dividend-paying stock

• Portfolio C: One European put on a stock + one share. • Portfolio D: a zero coupon bond paying off X at time T.• The investor can buy the put and the underlying, and borrow by issuing

the bond.

Value at expirationCurrent value ST < X ST ≥ X

Buy put p X - S 0Portfolio C Buy put p0 X - ST (exercise)

0(not exercise)

Buy stock S0 ST ST

Total = max (ST, X) at T X ST

Portfolio D Issue bond -X/(1+r)T or -Xe-rT -X -XTotal p0 + S0 - X/(1+r)T 0 ST – X

23

Lower bound for a European put on non-dividend-paying stock

• The total payoff is never less than zero. Consequently, the initial value of the combination must not be less than zero. Therefore p0 + S0 - X/(1+r)T ≥ 0 p0 ≥ S0 - X/(1+r)T . Suppose that X/(1+r)T - S0 is negative. Then the put price must be greater than a negative number.

• Or we can say portfolio C is worth max(ST, K) in time T and portfolio D is worth X in time T. Hence C is always worth as much as, and can be worth more than, D in time T (C ≥ D). In the absence of arbitrage, this must also be true today. Thus p0 + S0 ≥ X/(1+r)T p0 ≥ X/(1+r)T - S0

• Because the worst that can happen to a put is that it expires worthless, its value cannot be negative. This means that p0≥ 0, and therefore p0 ≥ max(0, X/(1+r)T - S0)

Puts: An Arbitrage Opportunity?• Suppose that

p = 1 S0 = 37T = 0.5 r = 5%X = 40 D = 0

• Is there an arbitrage opportunity?

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 201268

Lower bound for options on non-dividend-paying stock

• For a European call: The lower bound of a European call is either zero or the underlying price minus the present value of the exercise price, which is greaterc0 ≥ Max[0,S0 – X/(1+r)T] or c0 ≥ Max[0,S0 – Xe-rT]

• For a European put: The lower bound of a European put is the greater of either zero or the present value of the exercise price minus the

d l i iunderlying pricep0 ≥ Max[0, X/(1+r)T - S0] or p0 ≥ Max[0, Xe-rT- S0]

• For American options: The lower bound of an American option price is its current intrinsic valueC0 ≥ Max(0,S0 – X)P0 ≥ Max(0,X - S0)However an American call should not be worth less than a European call. Thus, the lower bound of the European call holds for American calls as well: C0 ≥ Max[0,S0 – X/(1+r)T] or C0 ≥ Max[0,S0 – Xe-rT]

24

Lower bound for options on non-dividend-paying stock

Option Lower boundEuropean call c0 ≥ Max[0,S0 – X/(1+r)T] or c0 ≥ Max[0,S0 – Xe-rT] American call C0 ≥ Max[0,S0 – X/(1+r)T] or C0 ≥ Max[0,S0 – Xe-rT] European put p0 ≥ Max[0, X/(1+r)T - S0] or p0 ≥ Max[0, Xe-rT- S0] American put P0 ≥ Max(0,X - S0)

Example

Consider call and put options expiring in 42 days, in which the underlying is at 72 and the risk - free rate is 4.5%. The underlying makes no cash payments during the life of the options.

A Find the lower bounds for European calls and puts withA. Find the lower bounds for European calls and puts with exercise prices of 70 and 75.

B. Find the lower bounds for American calls and puts with exercise prices of 70 and 75.

Put-Call Parity: No Dividends

• Assume the stocks pays no dividends. The put and call options have the same strike price and time to maturity

• Consider the following 2 portfolios:Co s de t e o o g po t o os– Portfolio A: European call on a stock + zero-coupon bond

that pays X at time T (a fiduciary call consists of buying a European call and a risk-free bond, which allows protection against downside losses)

– Portfolio C: European put on the stock + the stock (a protective put consists of buying a European put and the underlying asset)

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 201272

25

Values of Portfolios

Value at expirationCurrent value ST ≤ X ST > X

Portfolio A Buy call c0 0 ST − XBuy bond X/(1+r)T] or Xe-rT] X XTotal c0 + X/(1+r)T] X ST

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 201273

Portfolio C Buy put p0 X− ST 0Buy stock S0 ST ST

Total p0 + S0 X ST

• Suppose that

Examples

c = 6.64 S0 = 33.19T = 219/365 = 0.6 r = 4% X = 30 D = 0

• Illustrate the put-call parity assuming stock prices at expiration of 20 and 40

74

p = 2.75 Bond price = 30/(1 + 0.04)0.6 = 29.30

The Put-Call Parity Result (Equation 10.6, page 222)

• The fiduciary call and protective put are worth max(ST , K ) at the maturity of the options

• To avoid arbitrage, their values today must be the same. Thus,c + Xe -rT = p + S or c + X/(1+r)T = p + S : Put call parityc0 + Xe rT = p0 + S0 or c0 + X/(1+r)T = p0 + S0 : Put-call parity(+: buy, -: sell)

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 201275

26

Synthetics• c0 + X/(1+r)T = p0 + S0 c0 = p0 + S0 - X/(1+r)T

• The right-hand side is equivalent to a call, it is referred as to a synthetic call.

• The call and the synthetic call produce the same thing at maturity but in different ways

V l t i ti

76

Value at expirationCurrent value ST ≤ X ST > X

Call Buy call c0 0 ST − XSyntheticcall

Buy put p0 X− ST 0

Buy stock S0 ST ST

Issue bond -X/(1+r)T -X -XTotal p0 + S0 - X/(1+r)T 0 ST − X

Synthetics• c0 + X/(1+r)T = p0 + S0 p0 = c0 - S0 + X/(1+r)T

• The right-hand side is equivalent to a put, it is referred as to a synthetic put.

Value at expirationCurrent value ST ≤ X ST > X

77

Put Buy put P0 X− ST 0Synthetic put Buy call c0 0 ST − X

Short stock -S0 -ST -ST

Buy bond X/(1+r)T X XTotal c0 - S0 + X/(1+r)T X− ST 0

Alternative combinations of calls, puts, the underlying (the stock), and risk-free bonds

Strategy Consisting of Worth Equates to

Strategy Consisting of ST > X

Fiduciary call

Long call + long bond

c0 +X/(1+r)T = Protectiveput

Long put + long underlying

p0 + S0

Long call Long call c0 = Synthetic call

Long put + long underlying

+ short bond

p0 + S0 -X/(1+r)T

78

short bondLong put Long put p0 = Synthetic

putLong call +

short underlying + long bond

c0 – S0 + X/(1+r)T

Long underlying

Long underlying

S0 = Syntheticunderlying

Long call + long bond +

short put

c0 + X/(1+r)T –

p0

Long bond Long bond X/(1+r)T = Syntheticbond

Long put + long underlying

+ short call

p0 + S0 - c0

27

• Suppose that

Arbitrage Opportunities

c = 3 S0 = 31 T = 0.25 r = 10% X = 30 D = 0

• What are the arbitrage possibilities when:– the price of three month European put option p = 2.25?– the price of three month European put option p = 1?

Options, Futures, and Other Derivatives, 8th Edition,

Copyright © John C. Hull 201279

• Suppose that

Arbitrage Opportunities

c = 7.5, p = 4.25 S0 = 99 T = 0.5 r = 10% X = 100 D = 0

• What is the arbitrage possibility?

80

• Suppose European call and put options. The underlying makes no cash payments during the life of option.

Arbitrage Opportunities

c = 8, p = 3.75 S0 = 48T = 115/365 r = 4.5% X 45 D 0

A. Identifying the mispricing by comparing the price of the actual call with the price of the synthetic call

B. Based on your answer in Part A, demonstrate how an arbitrage transaction is executed

81

X = 45 D = 0

28

Put-Call Parity: No Dividends(for American options)

Put-call parity does not hold for American optionsS0 – X ≤ C0 – P0 ≤ S0 – Xe-rT or S0 – X ≤ C0 – P0 ≤ S0 – X/(1 + r)T

• An American call option on a non-dividend-paying stock:X = 20, T = 5 months, C0 = 1.5, S0 = 19, r = 10%19 – 20 ≤ C – P ≤ 19 – 20-0.1x5/12

1 ≥ P – C ≥ 0.181.68 ≤ P ≤ 2.50

Bounds for options on non-dividend-paying stock

Option BoundCall Max[0,S0 – X/(1+r)T] ≤ c0, C0 ≤ S0 or

Max[0,S0 – Xe-rT] ] ≤ c0, C0 ≤ S0

European put Max[0, X/(1+r)T - S0] ≤ p0 ≤ X/(1+r)T or Max[0, Xe-rT- S0] ] ≤ p0 ≤ Xe-rT

• Note: An American option call on a non-dividend-paying stock should not be exercised early (p.225-226). It can be optimal to exercise an American put option on a non-dividend-paying stock before expiration date.

American put Max(0,X - S0) ≤ P0 ≤ X

Lower bound for options and put-call parity ondividend-paying stock

Lower bound for a European call on dividend-paying stock• Portfolio A: One European call on a stock + an amount of cash equal to D +

X/(1+r)T or D + Xe-rT

• Portfolio B: one share of the stockc0 ≥ max[0, S0 - D - X/(1+r)T]

Lower bound for a European call on dividend-paying stock• Portfolio C: One European put on a stock + one share. • Portfolio D: an amount of cash equal to D + X/(1+r)T or D + Xe-rTq ( )

p0 ≥ max[0, D + X/(1+r)T - S0 ]Early exercise• Sometimes it is optimal to exercise an American call prior to an ex-dividend

date• It is never optimal to exercise a call at other times (see 14.12)Put-call parity for European option c0 + D + Xe -rT = p0 + S0 or c0 + D + X/(1+r)T = p0 + S0Put-call parity does not hold for American optionS0 – D - X ≤ C0 – P0 ≤ S0 – Xe-rT or S0 – D- X ≤ C0 – P0 ≤ S0 – X/(1 + r)T

29

Swiss Franc Option Quotation (U.S. Cents/SF)Calls - Last Puts - Last

Option & Underlying

Strike price

Aug Sep Dec Aug Sep Dec

58.51 58 0.71 1.05 1.28 0.27 0.89 1.8158 51 58½ 0 50 0 50 0 99

85

58.51 58½ 0.50 - - 0.50 0.99 -58.51 59 0.30 0.66 1.21 0.90 1.36 -

Each option =SF62,500. The August, September, and December listings are the option maturities or expiration dates. Source: Eiteman (2007), p.214

Spot rate 58½ means $0.5850/SF

Speculation and Hedging using optiong p

Speculation using spot and options

Suppose that it is October and a speculator considers that the GBP is likely to increase in value over the next 2 months. The GBP price is currently USD 2 and a 2-month call option with a strike price of USD 2.05 is currently selling for USD0.05. Assuming that the speculator is g g pwilling to invest USD 2,000. There are two possible alternatives. One alternative is to purchase GBP 1,000, the other involves the purchase of 40,000 call options. Suppose that the speculator’s hunch is correct and the price of GBP rises/falls to USD 2.2/1.8 by December.

87John Hull

30

Hedging using forward and options

• Suppose that it is September and an importer considers that the GBP is likely to increase in value over the next 3 months. The GBP price is currently USD 1.9 and a 3-month call option with a strike price of USD 2.05 is currently selling for USD0.05. Assuming that the y g gimporter will have to pay GBP100,000 for its import contract. There are two possible alternatives. One alternative is to purchase forward GBP 100,000 at the forward price of USD2.0, the other involves the purchase of 4,000,000 call options. Suppose that the importer’s expectation is correct and the price of GBP rises/falls to USD 2.2/1.8 by December.

John Hull