Opportunity for Employers Under the ACA: The Small Business Health Care Tax Credit Thank You For Joining TelePayroll’s Webinar – We Will Begin At 10:00 AM

Opportunity for Employers Under the ACA: The Small Business Health Care Tax Credit Thank You For Joining TelePayroll’s Webinar – We Will Begin At 10:00.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Opportunity for Employers Under the

ACA: The Small Business

Health Care Tax CreditThank You For Joining TelePayroll’s Webinar – We Will Begin

At 10:00 AM

Carri Lemmon

Quality Assurance Manager

TelePayroll, Inc.

(800) 442-4988 ext. 122

www.telepayroll.com

History And TerminologyThe Affordable Care Act, or ACA, was signed into law on March 23rd, 2010. The ACA is the federal legislation that includes the Small Business Health Care Tax Credit provisions. The ACA resulted in the addition of Internal Revenue Code § 45R:

• Code § 45R is the federal law that provides a tax credit to eligible small employers who provide health care coverage to their employees.

• A small employer is eligible for the credit if it has fewer than 25 full-time equivalent employees, and the average annual wages of its employees are less than $50,000 (adjusted for inflation beginning in 2014).

• The terminology and acronyms we will be using today include:

• FTE: Full Time Equivalent Employee

• SHOP: Small Business Health Options Program

• QHP: Qualified Health Plan

Agenda

1. Small Business Health Care Tax Credit Overview

2. Which Employers Are Eligible to Receive The Credit?

3. Exceptions And Limits

4. Calculating The Credit

5. Claiming The Credit

6. What TelePayroll Can Do To Assist You

7. What’s Next and Q&A Session

Small Business Health Care Tax Credit Overview

An employer with less than 25 Full-Time Equivalent (FTE) employees paying less than an average of $50,000 in wages annually, that also pays at least 50% of the premium for employee only health insurance coverage is eligible for the Small Business Health Care Tax Credit

Generally, for tax years beginning 2014 or later, coverage offered must be under a Qualified Health Plan (QHP) purchased through a Small Business Health Options Program (SHOP) to qualify for the tax credit.

The credit can be taken for two consecutive years beginning 2014, prior years do not count toward the two year limit. The credit is claimed on your income tax return by filing IRS form 8941

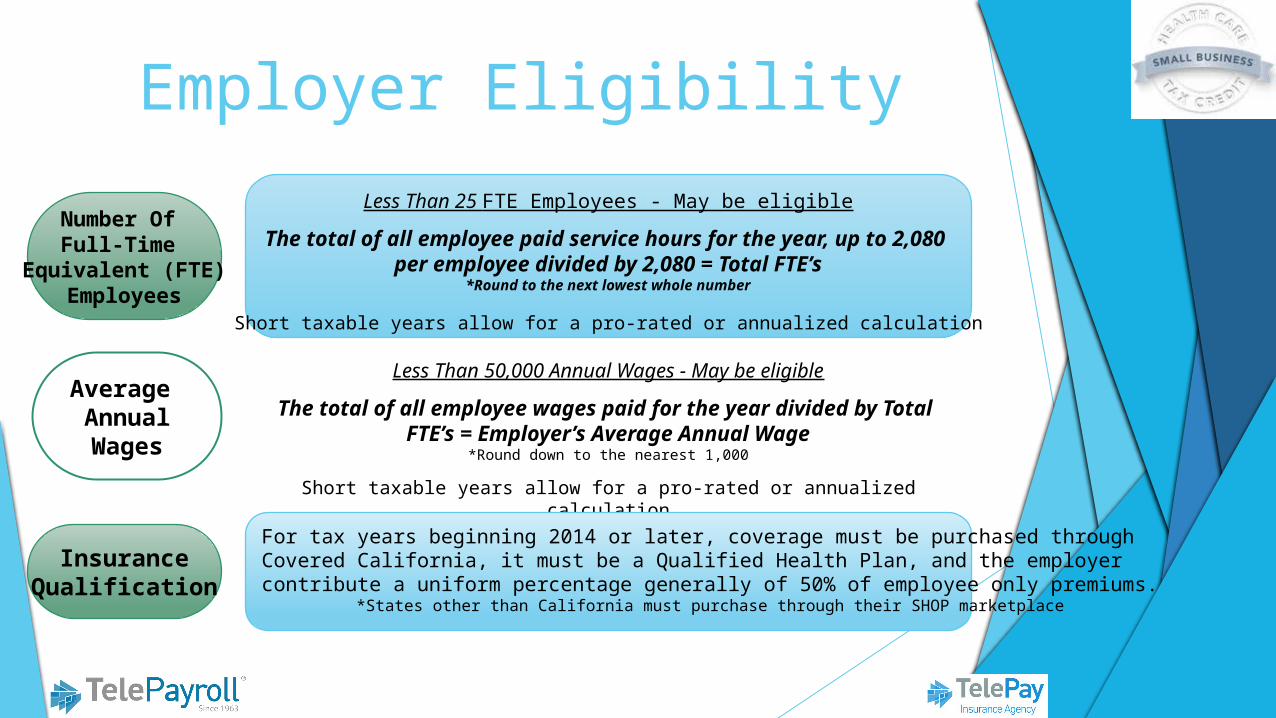

Employer Eligibility

Less Than 50,000 Annual Wages - May be eligible

The total of all employee wages paid for the year divided by Total

FTE’s = Employer’s Average Annual Wage*Round down to the nearest 1,000

Short taxable years allow for a pro-rated or annualized calculation

Number Of Full-Time

Equivalent (FTE)Employees

Average AnnualWages

InsuranceQualification

Less Than 25 FTE Employees - May be eligible

The total of all employee paid service hours for the year, up to 2,080 per employee divided by 2,080 = Total FTE’s

*Round to the next lowest whole number

Short taxable years allow for a pro-rated or annualized calculation

For tax years beginning 2014 or later, coverage must be purchased through Covered California, it must be a Qualified Health Plan, and the employer contribute a uniform percentage generally of 50% of employee only premiums.

*States other than California must purchase through their SHOP marketplace

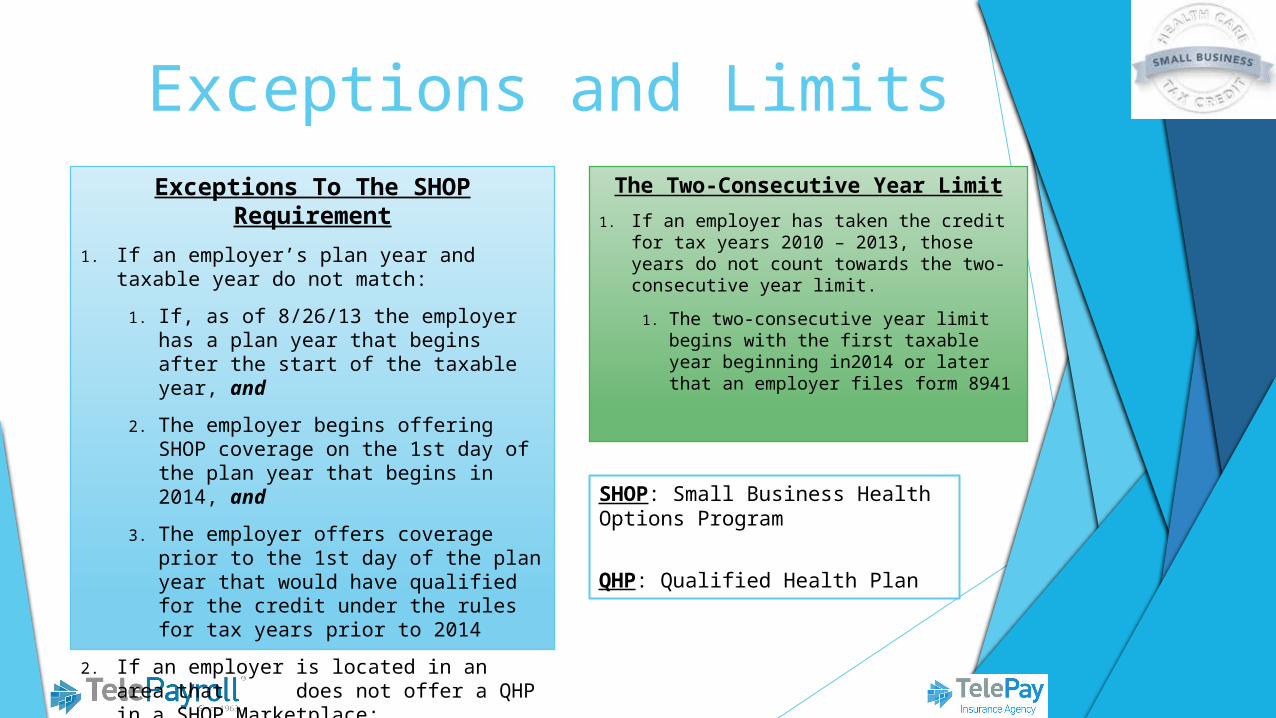

Exceptions and LimitsExceptions To The SHOP

Requirement

1. If an employer’s plan year and taxable year do not match:

1. If, as of 8/26/13 the employer has a plan year that begins after the start of the taxable year, and

2. The employer begins offering SHOP coverage on the 1st day of the plan year that begins in 2014, and

3. The employer offers coverage prior to the 1st day of the plan year that would have qualified for the credit under the rules for tax years prior to 2014

2. If an employer is located in an area that does not offer a QHP in a SHOP Marketplace:

1. Pre 2014 rules apply.

The Two-Consecutive Year Limit

1. If an employer has taken the credit for tax years 2010 – 2013, those years do not count towards the two-consecutive year limit.

1. The two-consecutive year limit begins with the first taxable year beginning in2014 or later that an employer files form 8941

SHOP: Small Business Health Options Program

QHP: Qualified Health Plan

Calculating the Credit – 2014/2015

Credit Reductions• Over 10 FTEs: Maximum allowed credit x FTE’s in excess of

10/15 = Reduction • Over 25,000 Average Wages: Maximum allowed credit x

Wages over 25,000 / 25,400 (2014) = Reduction

Expenses That Count Towards The Credit

Health insurance premiums paid by the employer, up to the average premium for the small group market in the employer’s rating area, are eligible but are limited by the percentage of the premium the employer contributes.

Different credit and reduction percentages and calculations, as well as reportingrequirements, may exist for tax-exempt organizations and members of control groups. Family member, owner, and non-employee exemptions may also apply.

Maximum Credit

• 50% of the employer’s eligible premium payments

Claiming the CreditEmployers can receive the small

business tax credit by completing IRS Form 8941 and attaching it to their

income tax return.

How can we help you?

Claiming the Credit

How We Can Assist You

TelePay Insurance clients will have their credit calculated and form 8941 information provided

directly as part of our services.

TelePayroll and TelePay Insurance can provide you with your IRS form 8941 information

to claim your credit.

TelePay Insurance can provide you with a Qualifying Plan

from Covered California

Thank you for listening!

TelePay InsuranceMichael Gilberstadt

(800) 442-4988 ext. 101

All participants will receive a follow up email with the following:

1. A copy of this presentation

2. Information about TelePayroll ACA Services

3. Information from TelePay Insurance

General ComplianceCarri Lemmon

(800) 442-4988 ext. 122

Related Documents