Opportunities for Using Sawmill Residues in Australia Presented by Dean Goble of The Carnot Group Pty Ltd for Forestry and Wood Products Australia 28 August 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Opportunities for Using Sawmill Residues in Australia

Presented by Dean Goble of The Carnot Group Pty Ltd for Forestry and Wood Products Australia

28 August 2013

Outline

1. Residues 2. Energy products

a) Electricity b) CHP c) Solid fuels d) Liquid fuels

3. Non-Energy products 4. Government Incentives 5. Comparison of options 6. Summary

Uses for Sawmill

Residues Attributes to be exploited: • Stored chemical energy • Source of hydrocarbons • Mechanical properties

(fibre) • Organic material for

biological feed • Thermal or acoustic

insulation properties

Sawmill residues

Fast Pyrolysis/Indirect Liquefaction

Char

Bio-oils• Fuel oil• Diesel additive

Syngas

Direct Combustion (in boiler)

Steam

Combustion in IC engine

Combustion in gas turbine

Agrichar

Activated carbon

Chemical &/or mechanical pulping

Blend with nitrogen compounds

Hydrolysis and separation

Steam turbine

GeneratorElectricity

F-T Conversion

Bio-fuels• Petrol additive• Diesel additive• Synthetic NG• Hydrogen• Ethanol

Chemical/physical processing

Chemical products

• Specialty chemicals• Commodity chemicals• Resins• Herbicides• Pesticides• Food Flavourings

Compost

Form withresin, polymer or

other binder Engineered wood products

Press with binding agent

Press with binding agent

Charcoal briquettes

Heat treatment

Carbonisation

Pulp for paper & cardboard

Wood pellets or briquettes

Absorbent/ insulating base

for animal bedding

Other Synthesis Processes

Saccharides

Platform chemicals

• Levulinic Acid/ MTHF

• Furfural• Lignin

Fermentation

Chemical processing

Direct Liquefaction

Steam engine

Fuel cell

Pyrolysis/ Carbonisation

Gasification

Conventional residue uses

Process

Potential Revenue Product

Product

Key

Residue characteristics

Bark – 6 %

Sawdust – 7%

Shavings – 5%

Woodchips – 35%

Hardwood Fuel moisture content (wet basis)

HHV, Higher Heating Value

LHV, Lower Heating Value

(MJ/kg) (MJ/kg) 0% 19 19

10% 17.1 16.8 20% 15.2 14.7 30% 13.3 12.5 40% 11.4 10.4 50% 9.5 8.2

Energy Products

• Heating • Electricity • CHP • Fuels

– Solid (pellets, briquettes, charcoal) – liquid (bio-oil, ethanol, methanol, diesel, DME) – Gas (syngas, hydrogen, SNG)

Electricity

• Steam turbine – established, widely available, robust technology – Steam turbine systems generally feasible >5-10MWe – Can be $5-6m/MWe fully installed – Generation cost around $40/MWh not including cost of capital

• Reciprocating steam engine – Limited availability (Spilling) up to 2,000kWe – Big River Timbers (NSW)

• 430kWe capacity • Integrated into steam circuit for kilns

Sawmill residues

Direct Combustion (in boiler)

Steam Steam turbine

GeneratorElectricity

Steam engine

Electricity

• ORC (Organic Rankine Cycle) – Organic fluid used in place of steam – Efficient at lower T (waste heat or co-gen)

• ORC installed at Gympie Timber Co – 240kWe capacity – using 150degC thermal oil – waste heat from kilns

• ORC at Reid Bros (Victoria) – Excess steam from kilns – gT Energy Technologies under BOO arrangement

Sawmill residues

Direct Combustion (in boiler)

Steam Steam turbine

GeneratorElectricity

Steam engine

Electricity

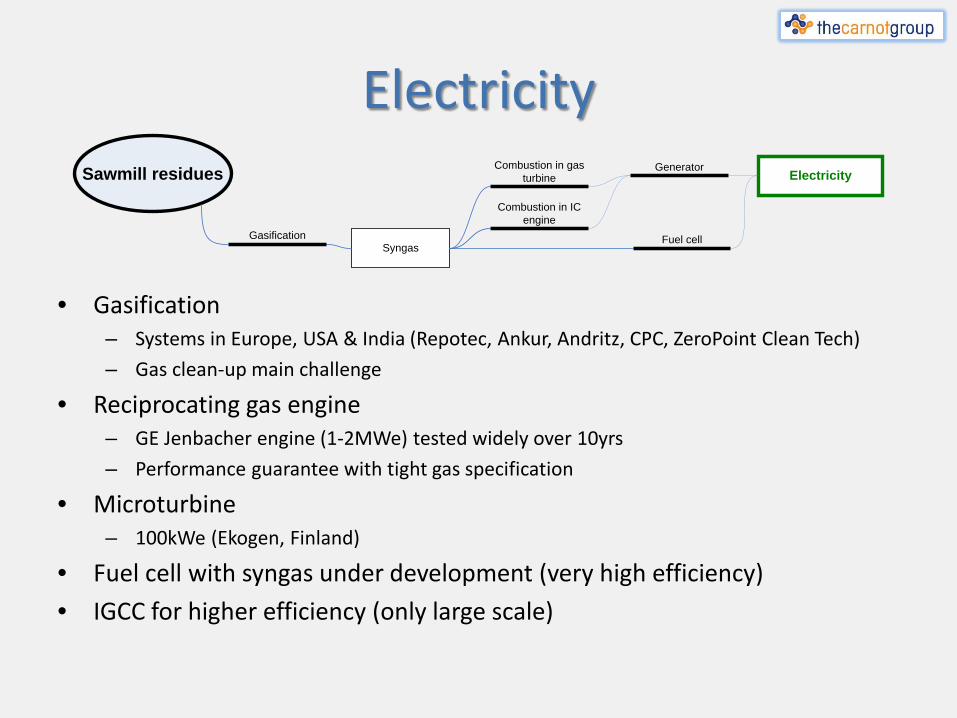

• Gasification – Systems in Europe, USA & India (Repotec, Ankur, Andritz, CPC, ZeroPoint Clean Tech) – Gas clean-up main challenge

• Reciprocating gas engine – GE Jenbacher engine (1-2MWe) tested widely over 10yrs – Performance guarantee with tight gas specification

• Microturbine – 100kWe (Ekogen, Finland)

• Fuel cell with syngas under development (very high efficiency) • IGCC for higher efficiency (only large scale)

Sawmill residues

Syngas

Combustion in IC engine

Combustion in gas turbine

GeneratorElectricity

Fuel cellGasification

Electricity – Efficiency

• At small scale: – Gasification and IC engine

(5-15%) – Steam engine (10-15%) – ORC

• At larger scale – Steam turbine (15-25%)

• Large scale – IGCC (22-37%)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

0 20,000 40,000 60,000 80,000 100,000 120,000 140,000 160,000

Annual residue quantity (Tonne/yr)

Average electrical

output (MWe)

35%

15%

25%

30%

10%

20%

Average electrical output for various conversion efficiencies from hardwood residue with gross heating value of 14MJ/kg (~25%

moisture content wet basis). The green band represents the likely conversion efficiency for a given system capacity.

Electricity – Use

• On-site use – Higher ‘price’ – Cyclic demand

• Low utilisation of installed capacity • Low efficiency – reciprocating engines more level

than turbines

• Sale of Power – Lower price – Grid connection complex, costly and lengthy – Grid interconnect system required

Cogeneration

• Combined heat and power (CHP) – Or Tri-generation (CHCP)

• Europe deployed widely – Steam turbine at larger scale (>5-10MWe) – Recip IC engine and/or ORC at smaller scale

• Key challenge to balance demand – Cyclic or variable demand – Temperature, transfer medium, distance

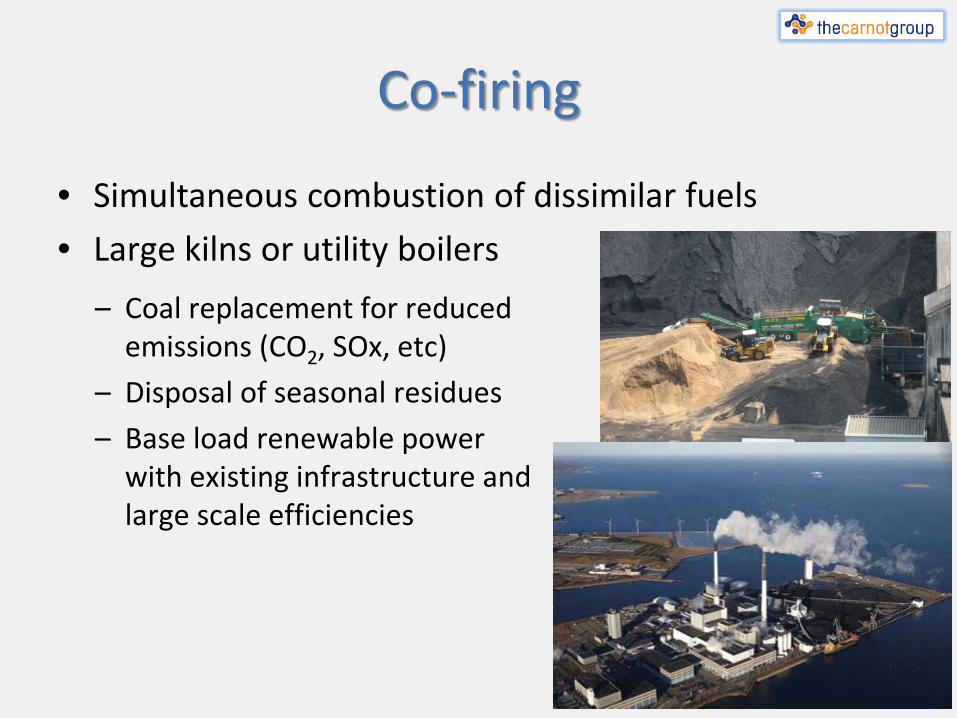

Co-firing

• Simultaneous combustion of dissimilar fuels • Large kilns or utility boilers

– Coal replacement for reduced emissions (CO2, SOx, etc)

– Disposal of seasonal residues – Base load renewable power

with existing infrastructure and large scale efficiencies

Pellets • Feedstock

– >25,000tpa – Dry (<7% moisture) – Sawdust (<3mm)

• Pressed through die • Comparable energy content to

coal, with low NOx & Sox • Consistent fuel

– AS/NZS 4014.6 – US and European standards

Pellets • Market

– $100-350/t delivered to EU

– Australian market very limited

– Asian market potential

Plant Capacity Main machinery supplier

Material Status

Plantation Energy Australia (Albury WA)

250,000 t/y

Kahl Plantation residues

Shut down, Jan 2012

Pellets Heaters Australia (Woodburn NSW)

3000 t/y Ace press by Andritz

Plantation softwood

Start up phase

East Coast Woodshavings (Gatton Qld)

3000 t/y Ace press by Andritz

Wood fines and sawdust

Operating making kitty litter

Scottsdale Hop Growers (Scottsdale Tas)

3000 t/y Ace press by Andritz

Plantation pine residues

Presently not operating, awaiting dryer installation

South Eastern Fibre Exporters (Eden, NSW)

500 kg/h AGICO (agent Arttech, Rosedale, Qld

Hard and softwood fines from chips

Producing pellets using hardwood & softwood

Altus Renewables

125,000 t/y

Andritz LM26,

Folk Fabrication (US)

Softwood sawdust & shavings

Plant to be commissioned in Jan 2013

Australian New Energy

10,000t/y Chinese Wood waste eg sawdust &shavings

Start up phase

Thermal decomposition

• Char – Reductant – Absorbent – Fuel – Soil improver – Sequestrant

Mode Conditions Bio-oil Char Syngas Gasification (>800oC)

high temperature, long residence times 5% 10% 85%

Fast pyrolysis/ indirect liquefaction (600oC)

moderate temperature, short residence time particularly for vapours

75% 12% 13%

Pyrolysis/ Carbonisation (300-550oC)

low temperature, very long residence time 30% 35% 35%

• Syngas – CO, H2, CH4

– CO2, N2

– Fuel – Chemical

feedstock

• Bio-oil – Fuel (blended

or further refined)

– Chemical feedstock

Bio-oil and Bio-fuels

Bio-oil

Weight/Volume basis Energy Basis

Bio-Oil Production Costs Feedstock 13.30 $/tonne 0.76 $/GJ Manufacturing 76.65 $/tonne 4.38 $/GJ Transport (rail transport to nearest port) 19.25 $/tonne 1.10 $/GJ

Total 109.20 0.13

$/tonne $/litre 6.24 $/GJ

Fuel oil Prices Spot price for gas-oil in Singapore 0.82 $/litre 17.00 $/GJ Spot price for No. 2 diesel in Singapore 0.80 $/litre 25.00 $/GJ

Char Production Costs Feedstock 2.63 $/tonne 0.15 $/GJ Manufacturing 4.90 $/tonne 0.28 $/GJ Transport 11.20 $/tonne 0.64 $/GJ

Total 18.73 $/tonne 1.07 $/GJ

• Synthetic crude oil that can be used as fuel or as source of useful chemicals

• Char co-product option • Production cost claims $3-7/GJ ($50-110/tonne)

Bio-oil plants • KiOR (Mississippi)

– 500 bone dry tpd(pine) – output 50million litres per year of bio-fuels – construction completed 2012 for US$213m – Includes hydrotreating to upgrade oil into fuels or

fuel blendstocks

• Dynamotive (Ontario)

– 200 dry tpd (C&D waste) – Operational since 2007

• Licella (NSW) – Uses novel catalytic hydro-thermal process – Demonstration plant operating 3 years – Feasibility study for pre-commercial 150 dry tpd

plant underway

Bio-ethanol • Hydrolysis route

– Builds on first generation ethanol technology, infrastructure and route to market – Co-products from lignin – chemicals, fuels, etc – Combined saccharification and fermentation possible – Other products from sugars also possible – Bio-butanol as alternative fuel

• Higher energy density • Higher blending ratios

– Conversion efficiencies and enzyme cost main challenges

• Gasification route – F-T route used for decades (WWII Germany, SASOL from coal/NG) – Other synthetic fuels under development – BIO-SNG, Bio-hydrogen, Bio-methanol, Bio-

DME – Gasification control and gas clean-up main challenges

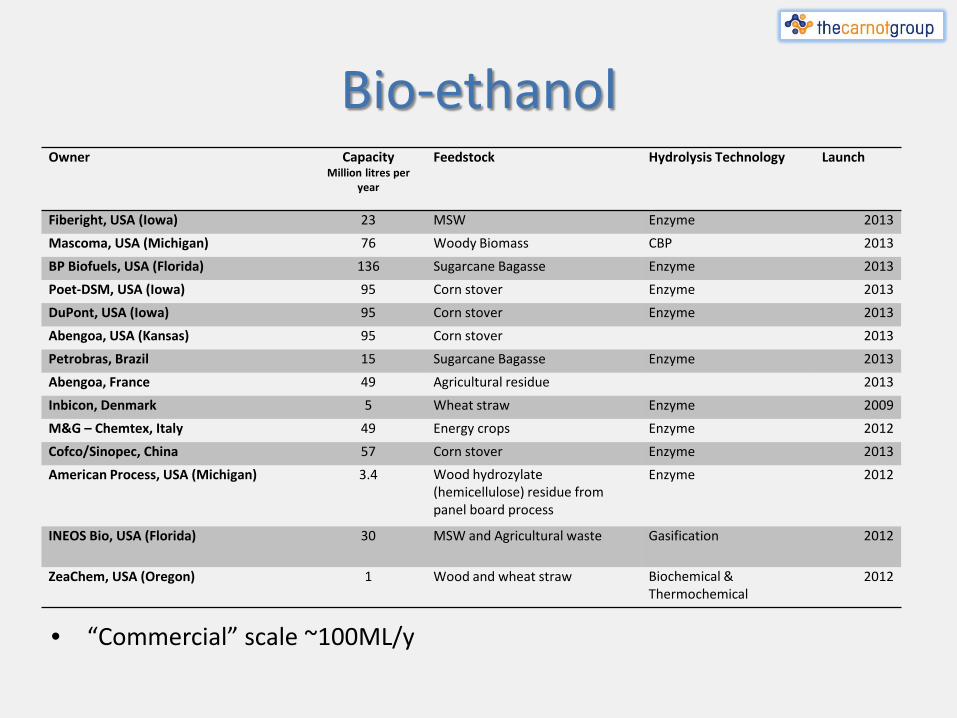

Bio-ethanol

• “Commercial” scale ~100ML/y

Owner Capacity Million litres per

year

Feedstock Hydrolysis Technology Launch

Fiberight, USA (Iowa) 23 MSW Enzyme 2013 Mascoma, USA (Michigan) 76 Woody Biomass CBP 2013 BP Biofuels, USA (Florida) 136 Sugarcane Bagasse Enzyme 2013 Poet-DSM, USA (Iowa) 95 Corn stover Enzyme 2013 DuPont, USA (Iowa) 95 Corn stover Enzyme 2013 Abengoa, USA (Kansas) 95 Corn stover 2013 Petrobras, Brazil 15 Sugarcane Bagasse Enzyme 2013 Abengoa, France 49 Agricultural residue 2013 Inbicon, Denmark 5 Wheat straw Enzyme 2009 M&G – Chemtex, Italy 49 Energy crops Enzyme 2012 Cofco/Sinopec, China 57 Corn stover Enzyme 2013 American Process, USA (Michigan) 3.4 Wood hydrozylate

(hemicellulose) residue from panel board process

Enzyme 2012

INEOS Bio, USA (Florida) 30 MSW and Agricultural waste Gasification 2012

ZeaChem, USA (Oregon) 1 Wood and wheat straw Biochemical & Thermochemical

2012

Fuel product comparison

Biomass product

Typical moisture

content (wet basis)

Net Calorific Value, wet basis (LHV)

Typical bulk density

Gross Energy density (bulk volume basis,

HHV)

% MJ/kg kg/m3 GJ/m3 Hardwood (Eucalypt)

Kiln dried shavings 12 17.6 120 2 Sawdust – green 30 14 180-200 3

Woodchips – air dried 128 30 16

300 4

Solid wood – green 50 8 1150 15 Softwood (P. radiata)

Kiln dried shavings 10 18 135 3 Solid wood – green 50 8 1000 9

Compressed wood Wood pellets 8-10 18 650 12 Charcoal briquettes 5 28-30 1100 31-33 Wood Briquettes 6 19 600-700 12-13

Char - 30 200-250 6-8 Bio-oil 20 17 1200 20 Bio-fuels

Syngas - 5.7

- (12-18MJ/Nm3)

Hydrogen - 142 - (14MJ/Nm3) Ethanol - 30 790 24

Fossil fuels Brown coal (VIC) 65 9 860 8 Black coal (NSW) 8 25 940 23 Fuel Oil - 43 845 36 Diesel - - 850 40 Petrol - - 737 35 Natural gas - - - (36MJ/Nm3)

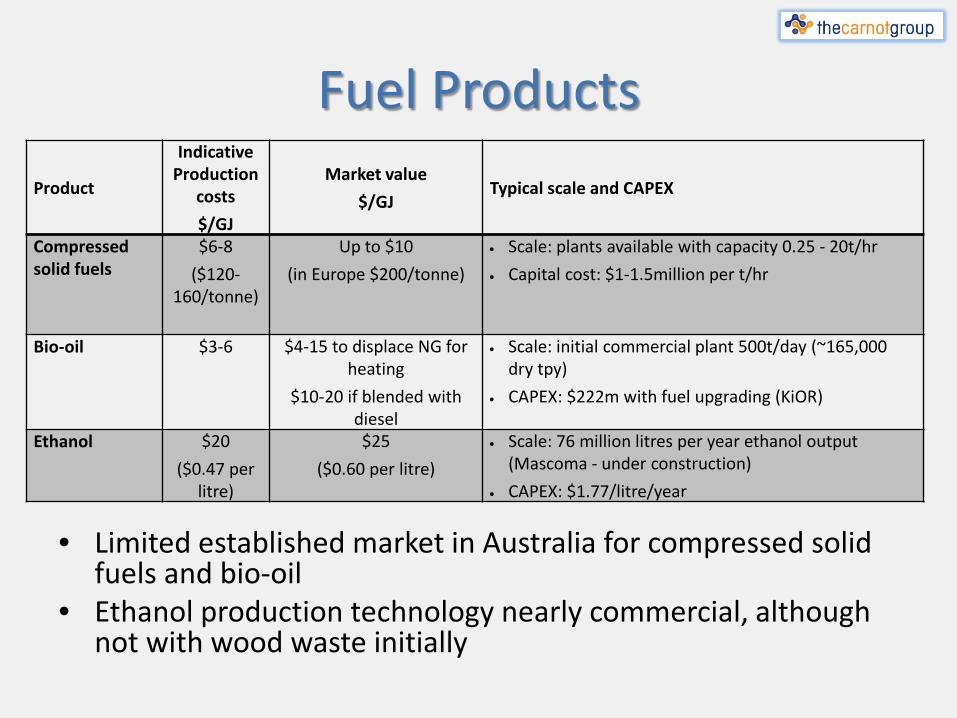

Fuel Products

• Limited established market in Australia for compressed solid fuels and bio-oil

• Ethanol production technology nearly commercial, although not with wood waste initially

Product

Indicative Production

costs $/GJ

Market value $/GJ

Typical scale and CAPEX

Compressed solid fuels

$6-8 ($120-

160/tonne)

Up to $10 (in Europe $200/tonne)

• Scale: plants available with capacity 0.25 - 20t/hr • Capital cost: $1-1.5million per t/hr

Bio-oil $3-6 $4-15 to displace NG for heating

$10-20 if blended with diesel

• Scale: initial commercial plant 500t/day (~165,000 dry tpy)

• CAPEX: $222m with fuel upgrading (KiOR)

Ethanol $20 ($0.47 per

litre)

$25 ($0.60 per litre)

• Scale: 76 million litres per year ethanol output (Mascoma - under construction)

• CAPEX: $1.77/litre/year

Non-Energy Products

• Chemicals – Food flavourings (used now) – Resins, platform chemicals, herbicides, pesticides

• Agrichar • Conventional residue uses

– Engineered wood products – Compost – Pulp & paper – Insulation (eg animal bedding)

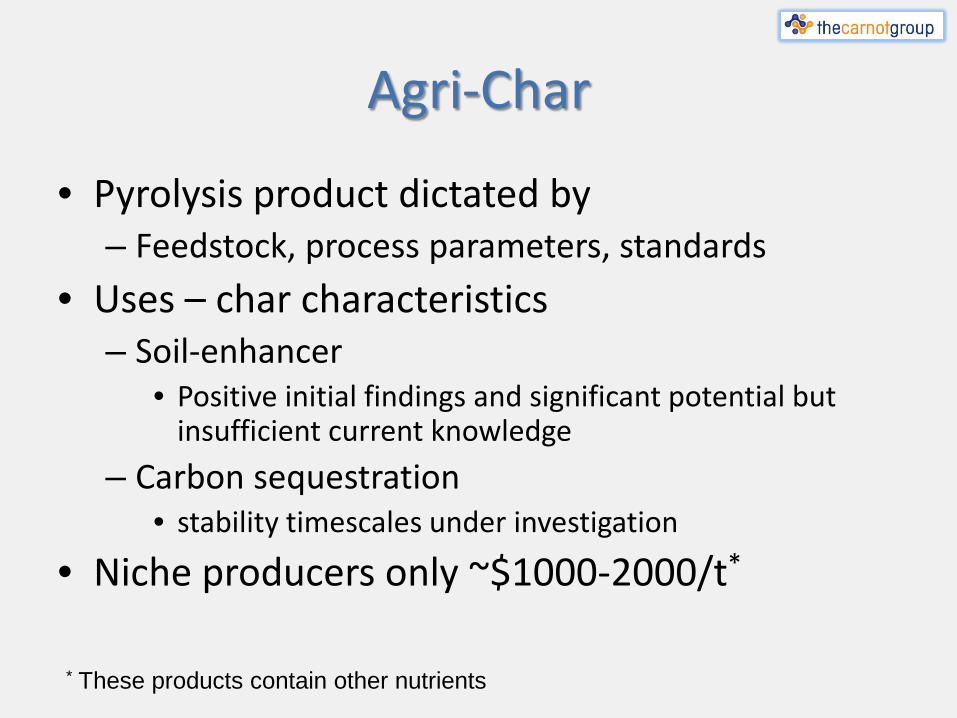

Agri-Char

• Pyrolysis product dictated by – Feedstock, process parameters, standards

• Uses – char characteristics – Soil-enhancer

• Positive initial findings and significant potential but insufficient current knowledge

– Carbon sequestration • stability timescales under investigation

• Niche producers only ~$1000-2000/t*

* These products contain other nutrients

Chemicals

• Food flavourings – Liquid Smoke – Pyrolysis process

• High value • Small market

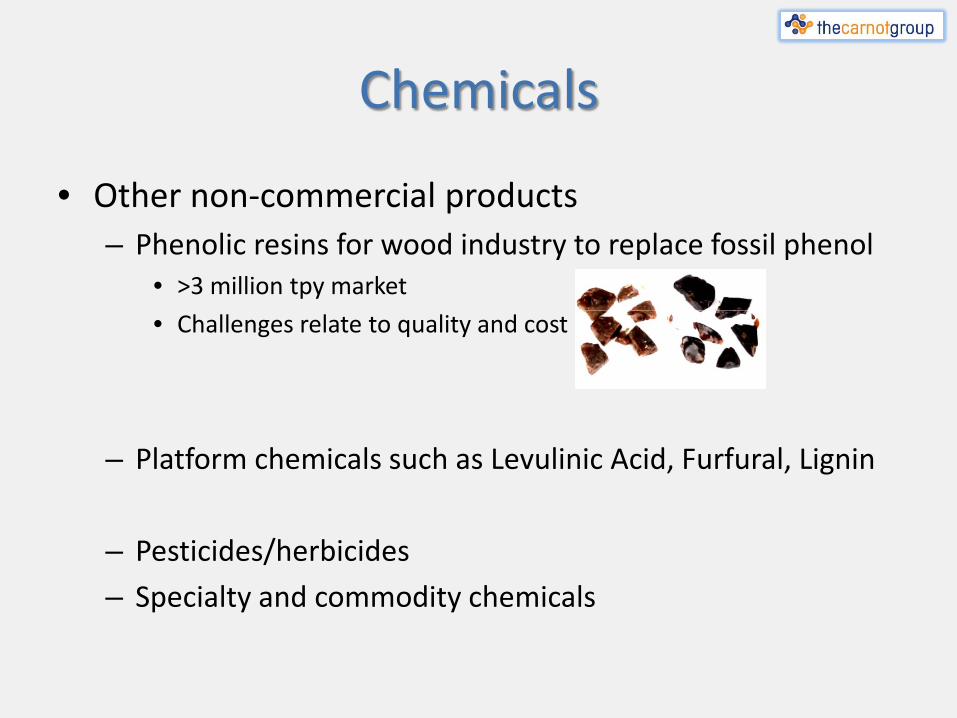

Chemicals

• Other non-commercial products – Phenolic resins for wood industry to replace fossil phenol

• >3 million tpy market • Challenges relate to quality and cost

– Platform chemicals such as Levulinic Acid, Furfural, Lignin

– Pesticides/herbicides – Specialty and commodity chemicals

Pre-treatment

– Required for many of opportunities discussed – Drying

• Solar or air drying – time, space and increased stock • Forced drying energy intensive, requires plant

– Size reduction

Product Equipment Max particle size after reduction

(mm)

Grind energy (MJe/tonne)

Barley straws, corn stover, switch grass Hammer mill 3.2 40 Barley straws, corn stover, switch grass Hammer mill 0.8 100 Poplar chips (10-15% mc) Hammer mill 1.0 432 Pine chips (10-15% mc) Hammer mill 1.0 540 Pine bark (10-15% mc) Hammer mill 1.0 126 Aspen wood Hammer mill 3.0 200 Unspecified wood Attrition mill 0.9 940 Unspecified wood Attrition mill 0.1 2,360

Government Incentive Schemes

• Federal – ARENA (Australian Renewable Energy Agency) statutory

authority with $3.2b guaranteed funding to 2020 – Grants, Venture Capital, Targets, Advice, Accreditation – Carbon Trading

• State – Many programs reduced or ended due to federal schemes – Smaller targeted grants, loans, targets, support

• Generally – Programs are transient or changeable – Not for residues from old growth forest – Can reduce risk or improve viable projects

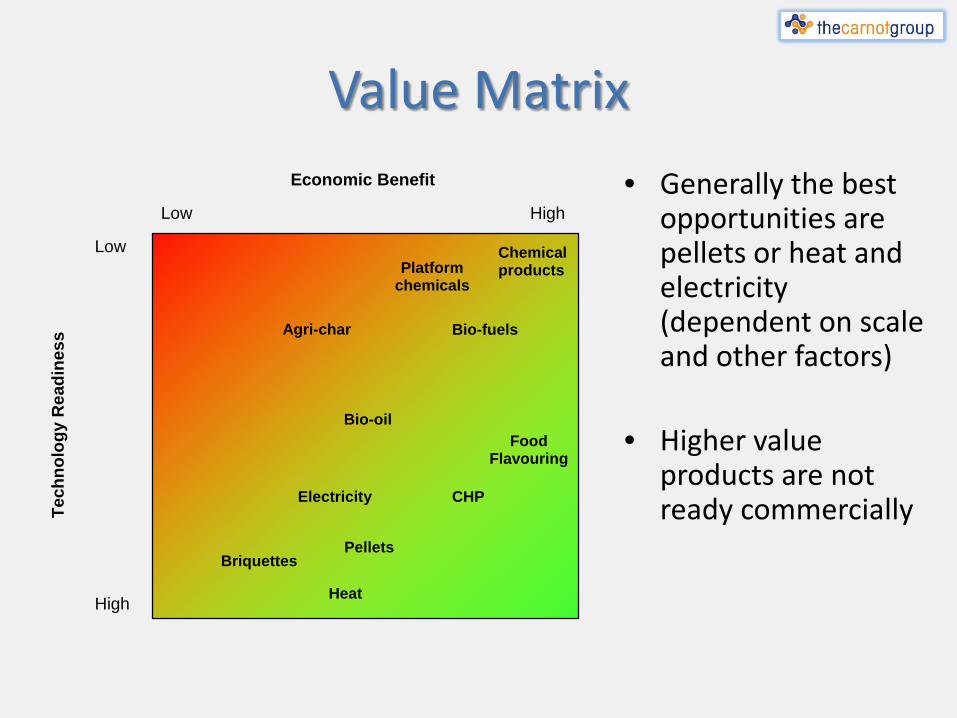

Value Matrix • Generally the best

opportunities are pellets or heat and electricity (dependent on scale and other factors)

• Higher value products are not ready commercially

Economic Benefit Low High

Tech

nolo

gy R

eadi

ness

Low

High

Pellets Briquettes

Agri-char

Heat

Electricity CHP

Bio-oil

Bio-fuels

Chemical products Platform

chemicals

Food Flavouring

Summary • Main process options

– Combustion: using the heat, via a heat transfer medium, for power generation and heating

– Gasification: using the cleaned syngas to fuel an engine for power generation or to produce bio-fuels

– Pyrolysis: to produce char products or bio-oil or bio-fuels – Pelletising: a dense fuel for domestic heating and fuelling small scale

power plant – Hydrolysis and fermentation: production of ethanol or butanol – Various combined thermal and chemical processes: production of

chemicals

• Key opportunities – Pellet technology available but mainly reliant on export market – Heat and power options available and becoming more financially

viable – higher efficiency at larger scale, tailored solution is key – Higher value product technologies not commercially ready, likely suit

large scale

Related Documents