Open economy issues

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Open economy issues

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

2

Outline

1. Empirical facts about international economic relationships

2. Interest rate parity and the Mundell-Fleming model

Production, interest rate and exchange rate under fixed exchange rates

Production, interest rate and exchange rate under flexible exchange rates

1. Empirical facts about international economic relationships

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

3

Introduction Economies are open to international flows

of goods, services and capital

This has important implications:

– Foreign shocks and policies are transmitted

to the domestic economy

– Impact of domestic shocks and policies is

modified

Most economies are small and open – we

can ignore their impact on the ROW, but

note vice versa

The impact depends on the ex. rate

regime

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

4

Openness to trade and finance

Most popular measures:

– Trade openness: (M+X)/GDP

– Financial openness: Foreign assets/GDP &

Foreign liabilities/GDP

Smaller economies are more open

Smaller economies are more prone to

international shocks

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

5

Table 11.1

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

6

World trade as % of GDP

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

7 Source: World Bank Database

0

10

20

30

40

50

60

70

1960 1970 1980 1990 2000 2010

International correlation of

business cycles

An important consequence of openness is

that business cycles and inflation rates are

strongly correlated worldwide

Examples of spillovers: – a positive demand shock in Germany boosts German

imports Polish exports to Germany increase

– financial crisis abroad the foreign owner of a Polish bank

faces solvency problems withdraws profits from the Polish

bank Polish bank has lower capital and grants fewer

loans demand in Poland falls GDP declines

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

8

GDP growth rate (y-o-y)

M.Brzoza-Brzezina: Macroeconomics II – Open economy 9

-8,0

-6,0

-4,0

-2,0

0,0

2,0

4,0

6,0

8,0

10,0

12,019

96Q

1

19

96Q

3

19

97Q

1

19

97Q

3

19

98Q

1

19

98Q

3

19

99Q

1

19

99Q

3

20

00Q

1

20

00Q

3

20

01Q

1

20

01Q

3

20

02Q

1

20

02Q

3

20

03Q

1

20

03Q

3

20

04Q

1

20

04Q

3

20

05Q

1

20

05Q

3

20

06Q

1

20

06Q

3

20

07Q

1

20

07Q

3

20

08Q

1

20

08Q

3

20

09Q

1

20

09Q

3

20

10Q

1

20

10Q

3

20

11Q

1

20

11Q

3

20

12Q

1

20

12Q

3

20

13Q

1

20

13Q

3

20

14Q

1

20

14Q

3

20

15Q

1

20

15Q

3

20

16Q

1

20

16Q

3

20

17Q

1

20

17Q

3

20

18Q

1

20

18Q

3

Euro area Denmark Poland Sweden

Source: Eurostat data

HICP inflation (y-o-y)

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

10

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Euro area Denmark Sweden

Source: Eurostat data

2. Interest rate parity and the

Mundell-Fleming model

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

11

Interest rate parity

To analyse these issues we need a link

between domestic and foreign interest

rates

Assume there is no risk, home bias or

restrictions on international capital flows

Then (simplified) equilibrium requires

𝑖 = 𝑖∗

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

12

M.Brzoza-Brzezina:

Macroeconomics II –

Open economy

i* IFM

Inte

rest ra

te

International Financial Market Equilibrium

Figure 11.1 (a)

Output

i > i*, capital flows in

i < i*, capital flows out

When domestic and foreign rates of

return are not the same, capital will

flow towards the higher returns until

returns are equalized.

13

Fixed vs. flexible exchange rate

We already discussed some differences

between fixed and variable exchange

rates when analysing monetary policy

Here we go further and look at effects of

various domestic and foreign shocks

Note that we consider short-medium

term developments and ignore long-run

issues (e.g. return to potential)!!! M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

14

Model

Our model for this lecture is a variation

of the Mundell-Fleming model

IS curve + Taylor rule + Interest rate

parity (International Financial Markets

curve)

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

15

Mundell-Fleming model

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

16

IS

IFM

TR

Y

i

i*

Fixed exchange rate case

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

17

The model

Under fixed exchange rate interest rates

are always equal

If they deviated, this would result in

apreciation or depreciation of the ex.

rate

This would be inconsistent with the fixed

exchange rate regime

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

18

Demand shocks and fiscal policy

Domestic demand shocks are powerfull

– they are not crowded out by monetary

policy

This is also true for fiscal policy

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

19

M.Brzoza-Brzezina:

Macroeconomics II –

Open economy

i* IFM

Inte

rest ra

te

Demand Shock with Capital Mobility

IS

A

Y‘

Figure 11.5 (a)

B

IS‘

Y Output

Positive demand shock:

IS curve shifts to the right.

At point B, output

has risen to Y‘.

i

20

Monetary policy

As we already know monetary policy is

completely ineffective since 𝑖 = 𝑖∗

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

21

Foreign financial shock

Foreign financial shocks have a

contractionary impact on the domestic

economy

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

22

M.Brzoza-Brzezina:

Macroeconomics II –

Open economy

i*

Inte

rest ra

te

Int. Financial Shock: Fixed Exchange Rates

IS

B

Output

Figure 11.6 (a)

IFM‘

i

IFM A

i*‘

Y‘ Y 23

Devaluation

Devaluation makes domestic goods

more competitive

Foreign demand increases, so does

output

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

24

M.Brzoza-Brzezina:

Macroeconomics II –

Open economy

i*

Figure 11.7 (a): Animation 1 (Demand

for Goods)

Inte

rest ra

te

A Devaluation: (b) Shift in Demand for Goods

IS´

B

Output

Figure 11.7 (a)

IFM

IS

A

A devaluation increases the

demand for domestic goods:

IS curve shifts to the right;

output expands from Y to Y‘.

Y Y‘ 25

Flexible exchange rate case

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

26

The model

Under flexible ex. rates domestic

interest rate can deviate temporarily

from international

This generates capital flows that result

in apreciation or depreciation of the

exchange rate

In the model this is represented as

shifts of the IS curve M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

27

Demand shock and fiscal policy

Domestic demand shocks less powerfull

– they are crowded out by monetary

policy and exchange rate apreciation

This is also true for a fiscal stimulus

Timing matters: crowding out is not

immediate so that fiscal policy can have

temporary effects

Note: ignoring risk hides the potential

depreciating effect of expansionary

fiscal policy M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

28

M.Brzoza-Brzezina:

Macroeconomics II –

Open economy

i* IFM

Figure 11.9 (a): Animation 1

Inte

rest ra

te

IS‘

Demand Shock Under Flexible Exchange Rates

TR

A

Y

Figure 11.9 (a)

i

IS

B

C

Expansionary

demand shock:

IS curve shifts

to the right.

At point B:

i > i*

capital inflow

appreciation

IS curve

shifts back

i

29

Monetary policy

Monetary policy is (as we know)

effective.

It stimulates domestic demand and

affects the exchange rate

This streghtens monetary transmission

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

30

M.Brzoza-Brzezina:

Macroeconomics II –

Open economy

i* IFM

Figure 11.8 (a): Animation 1 (TR

Curve Shift)

Inte

rest ra

te

Monetary Policy Shock: (b) Shift in TR Curve

TR

IS

A

Figure 11.8 (a)

Output

IS‘

TR‘

B

i

Y Y‘

C

i < i*:

capital

outflow,

depreciation

increases

demand for

domestic

goods.

31

Foreign financial shock

Foreign financial shocks have an

expansionary impact on the domestic

economy

But beware: this ignores possible

spillovers through international trade

M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

32

M.Brzoza-Brzezina:

Macroeconomics II –

Open economy

i*

Figure 11.6 (b): Animation 2 (Flexible

Exchange Rates)

Inte

rest ra

te

Int. Financial Shock: Flexible Exchange Rates

IS

A

IS´

Output

Figure 11.06

TR

C

Y Y‘

i

i*‘

At point A:

i=i*

i* increases to i*‘:

capital flows out,

exchange rate

depreciates,

demand for

domestic goods

increases,

IS curve shifts

to the right.

33

M.Brzoza-Brzezina:

Macroeconomics II –

Open economy

Table 11.3: Mundell-Fleming model:

Summary

The Mundell-Fleming Model: Summary Table 11.3

Fixed exchange rates

Flexible ex. rates

Fiscal policy expansion Increase No effect

Monetary policy expansion No effect Increase

Increase in foreign interest

rate

Decrease Increase

Effect on real GDP

Fixed exchange rates

Flexible ex. rates

Exogen. monetary policy

instrument Exchange rate Interest rate

Endogen. monetary policy

instrument Interest rate Exchange rate

34

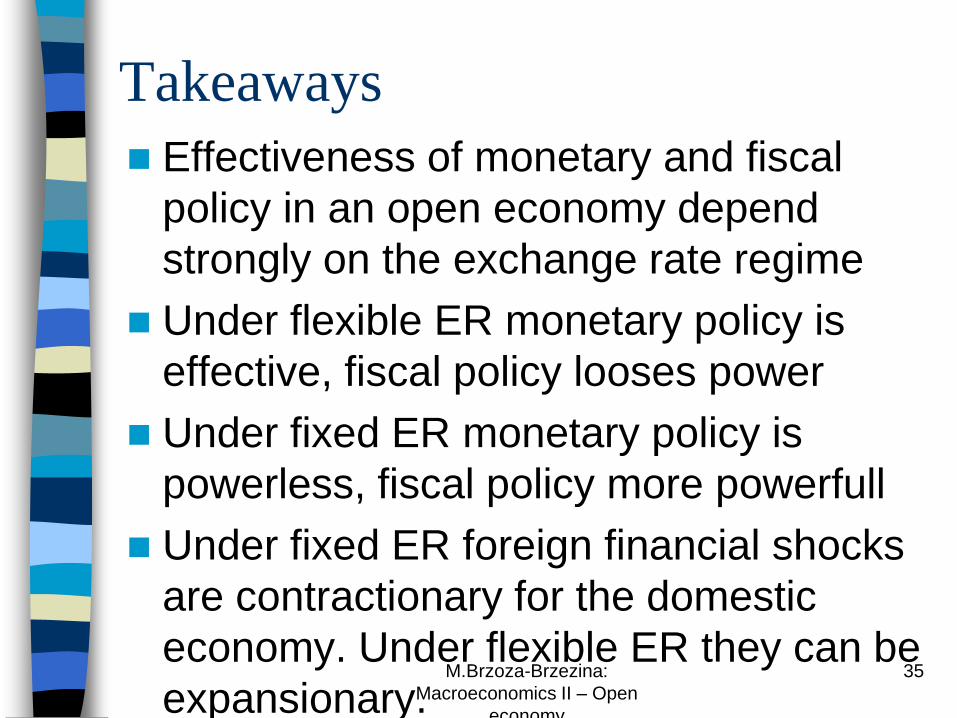

Takeaways

Effectiveness of monetary and fiscal

policy in an open economy depend

strongly on the exchange rate regime

Under flexible ER monetary policy is

effective, fiscal policy looses power

Under fixed ER monetary policy is

powerless, fiscal policy more powerfull

Under fixed ER foreign financial shocks

are contractionary for the domestic

economy. Under flexible ER they can be

expansionary. M.Brzoza-Brzezina:

Macroeconomics II – Open

economy

35

Related Documents