ONCOR ELECTRIC DELIVERY WHOLESALE CUSTOMER DIRECT ASSIGNMENT STUDY 2017 RATE CASE This study was prepared and is submitted to fulfill the'requirements of the Order on Rehearing of the Public Utility Commission pf Texas in Docket No. 35717, Finding of FacfNos. 173A and 174A and Ordering Paragraph No. 6 and to fulfill the requirement of Project No. 38808 Submitted by Oncor Electric Delivery Company LLC March 17, 2017 4799

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ONCOR ELECTRIC DELIVERY WHOLESALE CUSTOMER DIRECT

ASSIGNMENT STUDY

2017 RATE CASE

This study was prepared and is submitted to fulfill the'requirements of the Order on Rehearing of the Public Utility Commission pf Texas in

Docket No. 35717, Finding of FacfNos. 173A and 174A and Ordering Paragraph No. 6 and to fulfill the requirement of Project No. 38808

Submitted by Oncor Electric Delivery Company LLC

March 17, 2017

4799

TABLE OF CONTENTS

I. EXECUTIVE SUMMARY 2

A. Overview of Study 2

B. Overview of Methodology 4

C. Summary of Results 6

D. Implications of Wholesale Rates Based on Direct Assignment 7

II. STUDY METHODOLOGY 8

A. Description of Study Methodology 8 1. Identification of Service Arrangement 8 2. Identification of Substation Facilities and Original Costs 8 3. Identification of Distribution Line Facilities and Original Costs 9 4. Assignment of Accumulated Depreciation and Calculation of Net Plant 9 5. Allocation of Joint Plant 10 6. Development of Direct Assignment Class Revenue Requirements 12 7. Calculation of Revenue Coverage Factors 14 8. Calculation of POI-Specific Revenue Requirements 14

B. Illustration of Study Methodology 15 C. Study Results 18

III. DIRECT ASSIGNMENT RATE DESIGN OPTIONS 19

A. Calculation of POI-Specific Demand-Based Rates 19

B. Calculation of POI-Specific Fixed Monthly Charge§ 19

N. ONCOR'S FOSITION ON DIRECT ASSIGNMENT FOR WHOLESALE CUSTOMERS 21 A. Impact on Retail Customers 222 B. Stranded Costs 222 C. Changes to Facilities and Loads 233 D. Backstand Capabilities 244 E. New POIs 244

V. CONCLUSION 255

VI. SUPPORTING INFORMATION 266

Page 1 4800

ONCOR ELECTRIC, DELIVERY WHOLESALE CUSTOMER DIRECT ASSIGNMENT STUDY

I. EXECUTIVE SUMMARY

A. Overview of Study

This Wholesale Customer Direct Assignment Study ("Direct Assignment Study") is submitted in compliance with the order of the Public Utility Commission of Texas ("PUC" or "Commissioe) made on October 12, 2012 in Project No. 38808. In its October 12, 2012 open meeting in PUC Project No. 38808, the PUC directed Oncor Electric Delivery Company LLC ("Oncor or "Company") "to file in its next comprehensive base-rate case an updated study on the direct assignment 'of wholesale distribution costs." Furthermore, the PUC required that "the updated study should use the same`methodology as was used ie Project No. 38808 and that the study "incorporate data taken from the same test year upon which Oncor's proposed base rates are to be established." 1

The study below is consistent in its approach to the methodology employed in Project No. 38808 and Docket No. 35717. In the Order on Rehearing issued on November 30, 2009 in Docket No. 35717 ("Order on Rehearine), Finding of Fact 174A and Ordering Paragraph 6, Oncor was ordered to maintain and prepare information providing for the direct assignment of costs to wholesale customers. Specifically, FOF 174A stated:

Oncor should be ordered to maintain data adequate for the direct assigninent of costs to those wholesale classes and to prepare a direct assignment study for those classes for consideration in a future project to evaluate whether direct assignment should be used for allocating costs to the wholesale classes of customers or for consideration in Oncor's next rate proceeding.

In Ordering Paragraph 6 of the Order on Rehearing, the Cominission ordered the following:

Oncor shall perform a direct assignmént study for the wholesale classes and provide that study to the Commission in at [sic] future project to evaluate direct assignment of costs for wholesale classes or for consideration to assign wholesale costs according to that study in its next rate proceeding.2

Letter dated October 17, 2012, from Brennan J. Foley, Attorney-PUC Legal Division, to Jo Ann Biggs, Mark Davis, and Campbell McGinnis re Project No. 38808. 2 Docket No. 35717, Order on Rehearing dated: November 30, 2009, Ordering Paragraph No. 6, page 37.

Page 2

4801

The study contained herein, the underlying doéumentation, and supporting material are fully responsive to the Conmiission's requirements and comport with the requirements of the Commis'sion's Order on Rehearing in Docket No. 35717 and with the PUC's requirements in Project No. 38808. It should be noted, however, that Oncor does not agree that such direct assignments are appropriate for use in setting rates for wholesale customer classes. Oncor's recommendation that the results of the Direct Assignment Study not be used to allocate costs or set rates is more fully explained in the Direct Testimony of Mr. J. Michael Sherburne in this filing.

As explained below, the methods employed to directly assign distribution costs to wholesale customers in this Study are consistent with the recommendations of the wholesale intervenors in Dockef No. 35717 and with the Commission Staff in Project No. 38808.

This Direct Assignment Study is presented in five sections. The first section is introductory and provides an overview of the study approach and methodology as well as a summary of the results and implications of Direct Assignments. The second section is a detailed desdription of the study methodology and explains how gross plant, accumulated depreciation, other rate base items, capital costs, taxes, and expenses were directly assigned to the 65 wholesale Points of Interconnection ("POIs") on Oncor's System. This section also .surnmarizes and presents the results of the Direct Assignment Study. The third section takes the results of the Direct Assignment Study and presents two rate design options for recovering the distribution revenue requirement ("revenue requiremenr) from wholesale POIs. The fourth section contains Oncor's opinion as to the appropriateness of relying upon the results of the Direct Assignment Study to allocate costs and design rates applicable to Oncor wholesale customers. The final section of this report provides the attachments and workpapers referenced in this Direct Assignment Study. Portions of the information are confidential or highly sensitive confidential and will be made available only after execution of a certification to be bound, by the draft protective order set forth in Section VII of this Rate Filing Package or a protective order issued in this docket.

The objective of this Direct Assignment Study is to identify the distribution costs associated with providing delivery service to wholesale custorners by directly assigning to those customers the costs of the specific distribution facilities used to serve their POIs. The corollary to the direct assignment objective , of the study is the concurrent requirement that wholesale customers not be allocated costs of facilities that serve only retail customers. Once the direct assignment of distribution plant to wholesale customers was calculated, the resulting information was incoreorated into a modified version3 of Oncor's Rate Class Cost of Service ("COS") model from this filing to determine the total

3 Oncor's Rate Class COS filed in this study was modified to reflect the plant amounts directly assigned to the wholesale rate classes instead of having those amounts allocated to the wholesale rate classes. In addition, because the METR and TBILLTDCS functions were not changed in this study, those functions were removed from the modified COS, which only focuses on the DIST function.

Page 3

4802

cost of serving wholesale customers using direct assignment and the resulting impact on retail customers. In addition, the direct assignment information was used to calculate revenue requirements for each wholesale POI. The process utilized to calculate revenue requirements for existing POIs also serves as a framework for analyzing and Calculating new rates that may result from: (1) the'added investment for facility upgrades needed as a result of significant changes in the POI load or delivery characteristics; (2) investment incurred as a result of equipment replacement or facility reconfiguration; or (3) the addition of new POIs that are not included in this study.

' B. Overview of Methodology

The data in this report reflects a combination of cost allocation information from the following: (1) substation transformer, distribution feeder, POI and retail load data from calendar year 2016; and (2) directly assigned distribution plant amounts from the year ended December 31, 2016. Total system revenue requirement information and account detail used in the study are those amounts that are proposed in ,this docket. This information was used to facilitate comparison of the results of direct assignments with the results of traditional system average cost allocations.

In preparing direct assignments to wholesale customers in this study, facilities used to serve individual. POIs were identified using Oncor's Distribution Information System ("DIS") and Fixed Asset Management ("FAM") system. These systems contain an inventory of specific property units used to serve each POI. From this information, the original cost or an estimate of the original cost of the facilities was obtained from the FAM system based on the type, size and vintage year of the facilities. The accumulated depreciation associated with the gross plant accounts for each POI was then determined using depreciatiOn rates employed in this dockèt.

Because the substations that serve 61 of the 65 POIs serve both retail and wholesale loads, the facilities (referred to as "plant') associated with each substation was apportiõned between the retail and wholesale loads served by the substation trising a load ratio share. Likewise, in most instances, the distribution feeders serving wholesale POIs also .serve retail consumers. Of the 51 wholesale POIs taking service on a distribution line some distance away from the substation, only five .do not share a feeder or feeder segment with retail cukomers, and the costs of the feeders or feeder segments associated with those five POIs were directly assigned to those POIs. For the other 46 wholesale POIs that share feeders with retail customers, feeder costs were allocated between the wholesale POIs and the retail customers using a load ratio share calculation. The use of that calculation to apportion costs is consistent with the methodology emplOyed by the Tex-La witness in Docket No. 357174 and approved for use by the PUC in Project No. 38808.

4 See Tex-La Ex. 1 (Direct Testiinony and Exhibits of James Daniel on behalf of Tex-La, Exhibit JWD-3) in PUC Docket No. 35717.

Page 4

4803

a , Once the gross plant and accumulated depreciation amounts for substation

transformers and distribution ,lines were determined and allocated to each POI, this information was incorporated into a modified version of Oncor's rate class COS study that was filed in the current docket. The COS Study then allocated the oilier rate•base components, operation and maintenance ("O&M") expense, depreciation expense, taxes, and other expense items to the Substation Transformation and Distribution Line sub-functions, resulting in the establishment of overall revenue requirements for the Substation Transformation sub-function and the Distribution Line Service sub-function. The resulting revenue requirements were then used to calculate revenue coverage factors that represent the amount of revenue required to recover expenses and earn a return on investment for every dollar of net distribution plant associated with the • wholesale Substation Transformation and Distribution Line sub-functions. The revenue coverage factors were then used to assign a revenue requirement to each individual wholesale POI based on the net substation plant and distribution line plant allocated to each POI. Since the Direct Assignment Study calculates 'detailed POI-by-POI costs of service, Oncor calculated individual rates that reflect the specific costs to serve each individual POI.

Page 5 4804

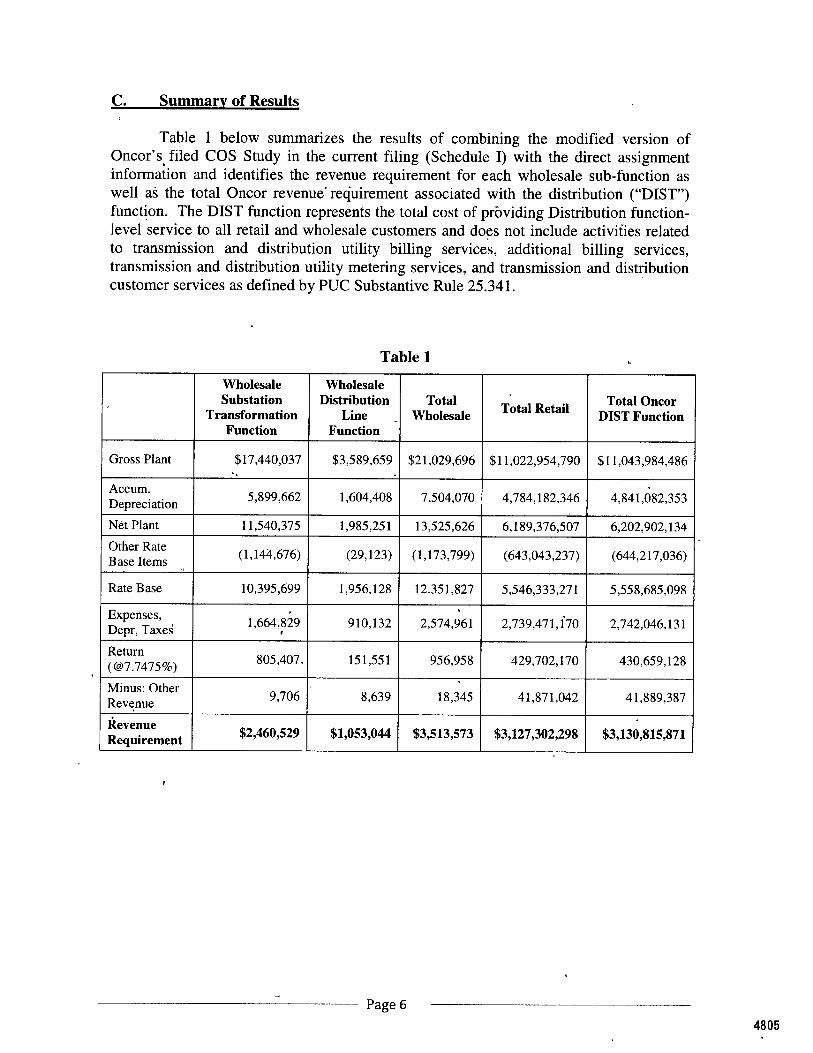

C. Summary of Results

Table 1 below summarizes the results of combining the modified version of Oncor's. filed COS Study in the current filing (Schedule I) with the direct assignment information and identifies the revenue requirement for each wholesale sub-function as well aS the total Oncor revenue requirement associated with the distribution ("DIST") function. The DIST function represents the total cost of prõviding Distribution function-level service to all retail and wholesale customers and does not include activities related to transmission and distribution utility billing services, additional billing services, transmission and distribution utility metering services, and transmission and distribution customer services as defined by PUC Substantive Rule 25.341.

Table 1

Wholesale Substation

Transformation Function

Wholesale Distribution

Line Function

Total Wholesale Total Retail Total Oncor

DIST Function

Gross Plant $17,440,037 $3,589,659 $21,029,696 $11,022,954,790 $11,043,984,486

Accum. Depreciation 5,899,662 1,604,408 7,504,070 4,784,182,346 4,841,082,353

Net Plant 11,540,375 1,985,251 13,525,626 6,189,376,507 6,202,902,134

Other Rate Base Items (1,144,676) (29,123) (1,173,799) (643,043,237) (644,217,036)

Rate Base 10,395,699 1,956,128 12.351,827 5,546,333,271 5,558,685,098

Expenses, Depr, Taxe 1,664,89 910,132 2,574,961 2,739,471, 00 2,742,046,131

Return (@7.7475%) 805,407. 151,551 956,958 429,702,170 430,659,128

Minus: Other Reve.nue 9,706 8,639 18,345 41,871,042 41,889,387

Revenue Requirement $2,460,529 $1,053,044 $3,513,573 $3,127,302,298

. $3,130,815,871

Page 6

D. Implications of Wholesale Rates Based on Direct Assignment

Table 2 below summarizes the revenue requirement of the wholesale customer classes under three different scenarios: (1) based on the wholesale direct assignment study; (2) based on the non-cost based rates currently in effect as ordered in Oncor's most recent rate case, Docket No. 38929; and (3) based on the fully allocated system average cost of service study filed in the current docket.

Table 2 shows that directly assigning costs to wholesale customers results in a 111.27% increase dyer their current non-cost based settlement rates. Table 2 further shows that direct assignment results in a revenue requirement that fs 34.65% below the revenue requirement calculated for wholesale classes using a fully allocated system average cost of service study, which is the method used to calculate Oncor's retail rates. Thus, Table 2 shows that direct assignment of costs to the wholesale classes more closely reflects the true cost of service when compared to the rates currently in effect and that the costs determined using direct assignment are still significantly below those observed under a fully allocated system average model. As a result, under a direct assignment approach, $1.86M in costs that should be paid by wholesale customers will have to be recovered from Oncor's retail classes.

Table 2

Direct Assignment

Current Non- Cost Based Rates

System Average COS

Revenue Requirement $3,513,573 $1,663,079 $5,376,196

Difference in Rev Req Under Direct Assignment $0 $1,850,494 ($1,862,623)

% Difference - 111.27% -34.65%

Page 7

4806

II. STUDY METHODOLOGY

A. Description of Study Methodology

The process of directly assigning costs to wholesale customers required a number of steps and several sources of information. The steps undertaken and sources of information Were as follows:

1. Identification of Service Arrangement

Oncor's wholesale distribution customers take service one of two ways: Substation Transformation Service ("XFMR") is provided to wholesale customers who receive service at an Oncor substation, with the point of interconnection located on the low voltage side of the substation tran'sformer. In some cases Where Oncor also serves retail or other wholesale customers from the same transformer, the point of interconnection may be located a few spans away from the substation fence, and in that event, is still considered Substation Transformation service. Distribution Line Service ("DLS") is provided to wholesale customers who receive service at a point of interconnection located on a distribution feeder at a'point located physically away from the substation. This service includes substation transformation service due to the need to transform power to a lower level voltage prior to its being distributed through distribution lines.

For each wholesale distribution POI, Oncor confirmed whether the POI is served directly from a substation transformer (XFMR) or from a point away from the substation on the distribution feeder (DLS). POIs served from distribution feeders were further identified as either being the sole customer served from the feeder 'or as a wholesale POI sharing a feeder with retail, or, other wholesale customers. Of the 65 wholesale POIs included in this study, 14 take substation transformation service (XFMR) and 51 take distribution line service (DLS). The detailed feeder maps for the 51 DLS POIs are located in Attachment 1. Detailed information for substation facilities can be useful in identifying the equipment necessary to serve these wholesale POIs. The substation one-lines for all 65 POIs are located in WP/Direct Assignment Study/4. Portions of the information are confidential or highly sensitive confidential and will be made available only after execution of a certification to be bound by the draft protective order set forth in Section VII of this Rate Filing Package or a protective order issued in this docket.

2. Identification of Substation Facilities and Original Costs

To determine the original substation costs for each substation that serves a wholesale POI, an inventory of all property units within the respective substatipn was obtained from the FAM system, which is a part of Oncor's Financial Information Management ("FIM") system. The information contained in FAM includes the vintage year, in-service date, the installed cost of each piece of equipment located in the substation, and additions and retirements by year as well as the functionalization of each

Page 8

4807

property unit ,as either Transmission, Distribution or Common based on the specific equipment use. Plant amounts that are assignable to the , Transmission function and recoverable through Transmission Cost of Service ("TCOS") are removed from the substation plant costs in this study, ensuring that -there was no duplication of TCOS facilities in the directly assigned wholesale distribution costs. The cost of those substation property units that are designated as Common to both Transmission and Distribution functions were allocated to the respective function based on the ratio of Transmission equipment cost and Distribution equipment cost to the total Trthismission and Distribution equipment cost of each substation. Again, this allaation is consistent with that used in the TCOS process to assign a ,portion of the Common costs to the Transmission function;ensuring that no duplication of Transmission costs occurs in the directly assigned costs. The total Distribution cost associated with the Substation Transformation function was then determined by summing the total costs of the property units functionalized as Distribution and the portion of the Common costs that were allocated to the Distribution function as of the end of the December 31, 2016 test year.

3. Identification of Distribution Line Facilities and Original Costs

: To identify the distribution facilities that are used to serve the wholesale DLS

POIs, Oncor's DIS was queried to identify all distribution line equipment, by property unit and vintage year, as of December 31, 2016. DIS is the information system used in the design and engineering of distribution facilities throughout the Oncor system. This database contains the electrical connectivity maps of all distribution feeder facilities, including information on conductor sizes, protective devices, transformers, and other equipment necessary to provide service to individual customer points of delivery. Once the inventory of the property units used to serve individual POIs was determined, a cost was assigned to each property unit based on the average price of the equipment by vintage year contained in the FAM system. Average price by vintage year was used because Oncor's.FAM system does not record precise costs of individual distribution line facilities. As recognized in Docket No. 35717, there are situations where Oncor's accounting system cannot identify the precise costs of individual items. In these cases, Oncor can apply vintage year avdrage costs to particular' sections or components of its delivery s'ystem.5 These property unit costs Were then rolled up to the respective FERC account for each individual POI.

4. Assignment of Accumulated Depreciation and Calculation of Net Plant

Because accumulated depreciation is not maintained by property unit for distribution plant, for purposes of this direct assignment study, a theoretical book depreciation reserve amount was developed for each asset identified in Steps 2 and 3 above using the average service life, remaining life and net salvage factors in the current docket. In that computation, the vintage balances within each asset group are multiplied

5 Proposal for Decision in PUC Docket No. 35717, page 223 and Finding of Fact No. 171 in Order on Rehearing, dated Noyember 30, 2009.

Page 9

4808

by the theoretical reserve ratio for each vintage. The straight-line remaining-life theoretical reserve ratio at any given age (RR) is calculated as:

Average RemaiTyng Life RR = 1

* (1 — Net Salvage Ratio) Average Service Life

After the theoretical reserve computation was made for each account and vintage, a proration factor was developed so that the sum of all accounts and vintages within a function equaled the per book accumulated depreciation.

Using the original plant values from Steps 2 and 3 above and the allOcated depreciation reserve amounts from this step, net plant by FERC account was calculated for each POI. Workpapers supporting the development' of accumulated depreciation by FERC account will be provided upon request.

5. Allocation of Joint Plant

The vast majority of substation and distribution feeder facilities that are used to serve wholesale POIs are also used to serve retail customers. Substations that serve 61 of the 65 wholesale POIs also serve retail or other wholesale customers. In addition, of the 51 feeders that serve DLS POIs, 46 also provide service to retail customers. Therefore, to assign costs directly to wholesale POIs, the costs of these jointly shared facilities were apportioned between retail and wholesale customers through a multi-step allocation process based on load share ratios.

a. Assignment of Substation Transformation Plant

Substation costs assigned to the Distribution function as identified in Step 2 above include amounts booked in account 349, Land Owned in Fee; account 350, Land and Land Rights; account 352, Structures and Improvements; account 353, Station Equipment; account ,354, Towers and Fixtures; account 355, Poles and Fixtures; account 356, Overhead Conductors and Devices; account 357, Underground Conduit; account 358, Underground Conductors and Devices; account 359, Roads and Trails; account 360, Land and Land Rights; and account 361, Structures and Improvements; account 362, Station Equipment; account 363, Storage Battery Equipment; account 374, Land Owned in Fee. Since substation costs are comprised of a significant amount of joint costs (i.e., switching equipment, buses, relays, cooling equipment, platforms, foundations, fences, etc.), it is necessary to allocate substation costs between the transformer serving the POI and other transformers co-located in the same substation that serve retail load or other wholesale load based on the transformer capacity ratings. The first two steps in allocating substation costs used in this study are: (1) identify the installed capacity of each transformer located in the substation; and (2) calculate the ratio of the capacity of the transformer serving the wholesale POI to the total installed capacity of all load serving transformers at that substation. Attachment 2 contains the capacity ratings of each transformer located in a substation that' serves a wholesale POI as well as the pro-rata calculation for assignment of costs to the POI-serving transformer.

Page 10 4809

Because virtually all of the transformers that serve wholesale POIs serve both wholesale and retail loads, the substation costs that have been assigned to POI-serving transformers identified above must be further apportioned between the wholesale POIs and the retail customers or other wholesale POIs served by that transformer. Therefore, two allocations must occur before the costs are considered to be directly assigned. This is accomplished using a load ratio share calculation based on the wholesale POI's contribution to the ttansformer's peak demand. Attachment 2 also contains the following data to calculate the load ratio share for each POI: (1) the peak demand of the substation transformer that serves each POI determined from Oncor's Supervisory Control and Data Acquisition ("SCADA") system; and (2) the POI load at the date and time of the transformer peak as measured by the Interval Data Recorder ("IDR") meter installed at each POI.

The resulting allocated substation plant represents the total plant directly assigned to wholesale XFMR POIs because these customers are served at the substation and are not assigned any feeder costs. The detailed calculations of the directly assigned substatidn costs for each wholesale POI are contained in Attachment 3. DLS POIs are assigned the costs of substations as described above plus the costs of distribution feeders used to serve the wholesale POI as deScribed below.

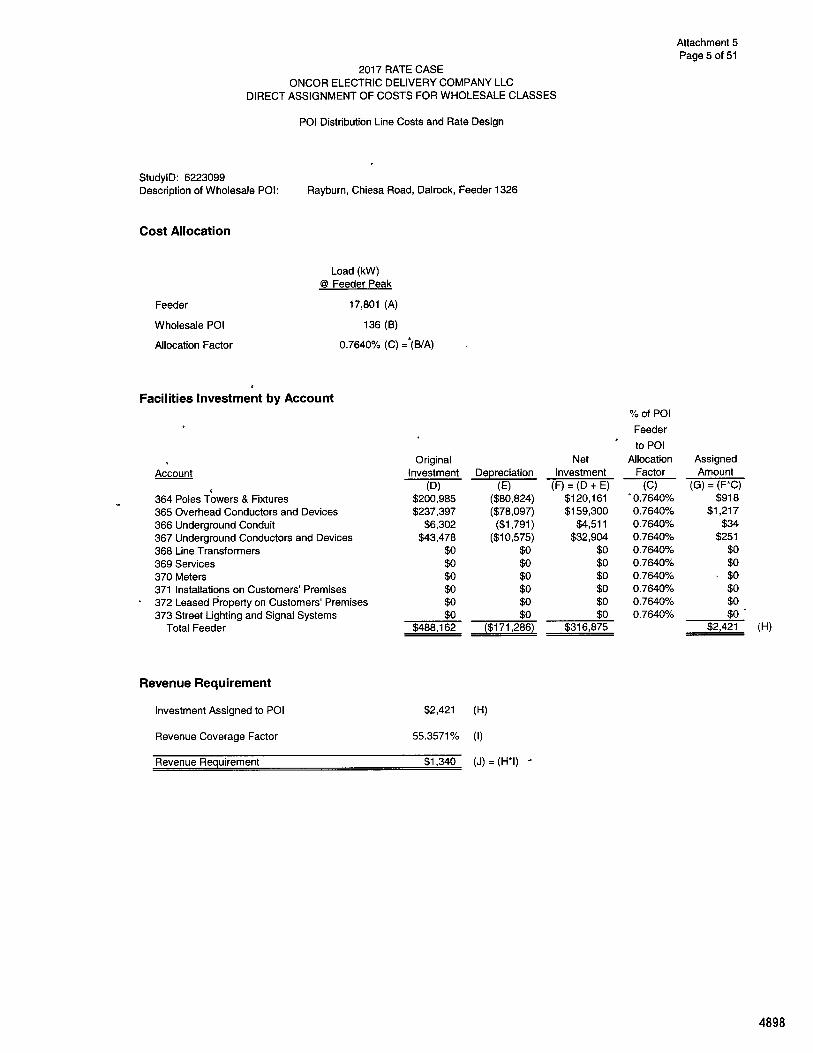

b. Assignment of Distribution Feeder Plant

The cost of distribution feeders identified in Step 3 above 'consists of amounts booked in accounts 364, Poles, Towers, and Fixtures; account 365, Overhead Conductors and Devices; account 366, Underground Conduit; and account 367, Underground conductors and Devices; 368, Line Transformers; 369, Services; 370, Meters; 371, Installations on Customers Premises; 372, Leased Property on Customers' Premises; 373, Street Lighting and Signal Systems that directly serve specific DLS POIs. Because distribution feeder facilities that serve 46 of the 51 DLS POIs also serve retail customers, the costs of these shared facilities had to be apportioned among the wholesale POI and the retail customers based on' the load ratio share of wholesale load to• feeder load to arrive at a cost that could be directly assigned to individual DLS POIs.

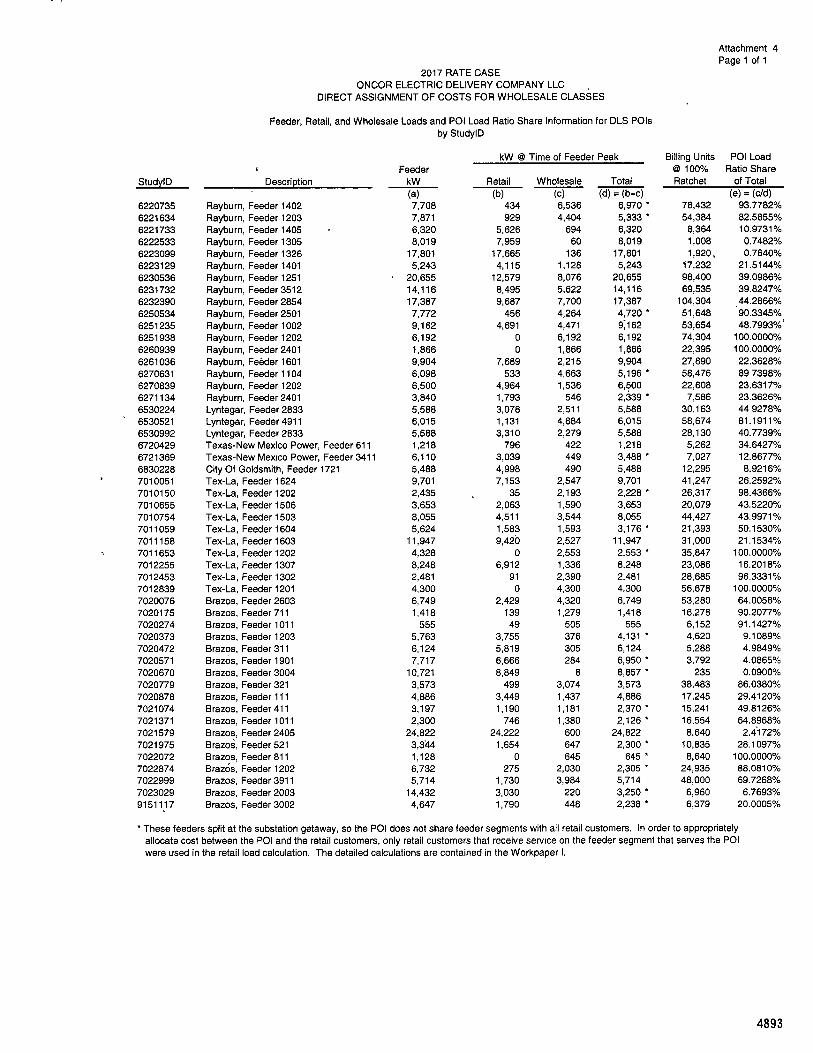

To accomplish this, the following information for each feeder that serves a DLS POI was obtained: (1) the 2016 calendar year peak demand of the feeder used to serve each wholesale DLS POI as determined by 'Oncor's SCADA syStem; and (2) the DLS POI load at the date and time of the feeder peak as measured by the IDR meter at each wholesale DLS POI. This information for each respective DLS POI is listed in Attachment 4.

Next, the retail load was calculated for each distribution feeder that serves a DLS POI. Depending upon the configuration of the feeder and the distribution of retail loads along the feeder, two different approaches were employed to develop the retail load. For 32 of the 51 DLS POIs; the distribution feeder segments that serve the DLS POI were the same feeder segments used to serve the entire retail customer load of the feeder. In this

Page 11

4810

straightforward kenario, the retail loads are calculated as the difference between the total feeder load at the time of the feeder peak and the- DLS POI' s load at that time. Using a load ratio share approach, the costs of the facilities used to serve the DLS POIs are allocated between the DLS POIs and all retail customers on the feeders.

For the remaining 19 DLS POIs, the distribution feeders split at the substation getaway and the POIs do not share feeder segments with all retail customers on the feeder. Therefore, a simple allocation of costs between the POIs and all retail customers on the feeder was not appropriate. Instead, the allocation had to be limited to only those retail loads that were served from the same feeder segments as the DLS POI load. To deterinine the retail load on the feeder segments that also served the DLS POI, Oncor's DIS was first utilized to identify the retail customers by premise number that were served from the same distribution feeder segments used to serve each DLS POI. For retail premises with an advanced meter, the loads were retrieved from a user-version of the Company's Meter Data Management System ("MDMS"). The MDMS is the repository for interval usage data, meter reads, and other meter information for customers with advanced meters. For retail premises with an IDR meter, loads were identified from the Company's MV-90 system. The MV-90 system is used to store interval data that is used for billing and load research analyses. The retail load from advanced meter premises was added to any retail load from IDR premises also served from the feeder segments to determine the total retail load of the feeder segments..The load ratio šhare was then calculated bydividing the DLS POI load at the time of the feeder peak by the sum of the DLS POI load and the estimated retail load at the time of the feeder peak. Finally, the load ratio share was multiplied by the respective net feeder investment calculated in Step 4 to calculate the portion of the distribution line costs that are directly assigned to each DLS POI. The retail loads associated with each DLS POI-servihg feeder or feeder segment are summarized in Attathment 4. The details of the retail load calculations for the 19 feeders that split at the substation getaway are contained in the attached Workpaper I. Feeder segmentation maps are provided in Workpaper III for these 19 DLS POI feeders. Portions of the information are confidential or highly sensitive confidential and will be made available only after execution of a certification to be bound by the draft protective order set forth in Section VII of this Rate FilingTackage or a protective order issued in this docket .

The resulting allocated distribution line plant 'added to the allocated substation plant described above represent the total plant directly assigned to wholesale POIs taking DLS service since tliese customers utilize substation and distribution feeder facilities. The detailed calculations for the directly assigned distribution line plant for each DLS POI are contained in Attachment 5.

6. Development of Direct Assignment Class Revenue Requirements

Once directly assigned plant has been identified for each wholesale POI, it is then necessary to determine the effects of these direct assignments upon the overall costs of providing service to, the Wholesale rate classes. Revenue requirements were developed for the Substation Transformation and Distribution Line functions by inputting the

Page 12

4811

directly assigned plant amounts into the modified Rate Class COS model. This step is necessary to allocate other items such as O&M expense, Administrative and General ("A&G") expense, and taxes to wholesale POIs to establish a revenue requirement for these customers.

First, the directly assigned portions of gross plant and accumulated depreciation balances associated with each POI were totaled by FERC account to yield the total Wholesale gross plant and accumulated depreciation for each account. The total directly assigned amounts for the Substation Transformation and Distribution Line functions, are shown in Attachments 6 and 7, respectively. These amounts were then entered into the Rate Class COS study and directly assigned to Wholesale sub-function. The directly assigned portions of Accounts 353, 360, 361, 362, and 374 were assigned to the Substation Transformation function, and the directly assigned portions of Accounts 364, 365, 366, 367, 368 and 369 were assigned to the Distribution Line Service function. The directly assigned amounts for each account were then subtracted from their respective account totals within the DIST ' funCtion set forth in Schedule II-I DIST of the current filing to yield a retail amount, which was allocated among the retail rate classes using a conventional allocation methodology.

It should be noted that the capacitor portion .of account 368 has been allocated among all classes, including the Substation Transformation function, on the basis of Rate Class non-coincident peak ("NCP") demands. Capacitors are used and useful for all end users on the grid, whether upstream or downstream from the capacitor. Because of this bidirectional impact, the capacitor portion of account 368 was allocated using standard average cost allocation methodology rather than being directly assigned. The other portion of account 368 that is relevant to Wholesale DLS Service, pertaining to regulators, protectors, and primary transformers, is directly assigned as detailed earlier.

- At this point in the process, all operating plant accounts contained the directly assigned amounts (and allocated capacitors) in the Wholesale functions and the allocated amounts if' the retail rate classes. General Plant accounts were allocated on the basis of Net Operating Plant, which reflected the reductions in the Net Operating Plant brought about by directly assigning costs to Wholesale customers. The remaining Rate Base accounts, although allocated by traditional methods, experienced similar changes due to the impact of directly assigning Net Operating Plant.

The impact of direct assignment flows through to the other accounts. For example, account 584, Undergrourid Line Expense, is allocated on the basis of account 367, Underground Conductors and Devices. Since the amount of account 367 was greatly reduced for Wholesale, there was a corresponding reduction in the Wholesale portion of account 584. There was a similar reduction in the Wholesale portion of Depreciation and Amortization Expense for account 367. Likewise, the change in the Wholesale portion of Return on Rate Base had a significant impact on the Wholesale portion of Federal Income Tax.

Page 13

4812

The results of these changes to the Rate Class COS produced Revenue Requirements for the Wholesale Substation Transformation and Wholesale 'Distribution Line functions, as shown in Table 3 below. The detailed Rate Class COS can be found in the attached Schedule II, including supporting information in Workpaper II.

7. Calculation of Revenue Coverage Factors

Using the resulting revenue requirements for the Substation Transformation and Distribution Line functions and the net plant' directly assigned to each function, Oncor calculated substation and feeder revenue "coverage factors by: (1) dividing the Substation Transformation revenue requirement by the net substation plant directly assigned to wholesale customers, and (2) dividing the Distribution Line revenue requirement by the net feeder plant directly assigned to wholesale customers, respectively. Refer to Table 3 below for the detailed caleulations. These revenue coverage factors represent the amount of revenue required per dollar of net plant for the respective functions and are used to calculate POI-specific revenue requirements for Substation Transformation and Distribution Line functions.

Table 3

Revenue 'Requirement

Directly Assigned Net Plant

Revenue Coverage Factor

(a) (b) (a/b) Substation Transformation function $2,460,529 $11,058,025 22.2511% Distribution Line function $1,053,044 $1,902,274 55.3571%

8. Calculation of POI-Specific Revenue Requirements

For each XFMR POI, the specific revenue requirement was determined by multiplying the Substation Transformation Revenue Coverage Factor calculated above, 22.2511%, by the net substation plant investment directly assigned to each POI.

For each DLS POI, two separate calculations were made to determine the total revenue requirement for wholesale distribution service: (1) calculation of the revenue requirement for the Substation Transformation function, and (2) calculation of the revenue requirement for Distribution Line function. The revenue requirement for the Substation Transformation function was calculated as described above. Similarly, the revenue requirement for the Distribution Line function was determined by multiplying the Distribution Line Revenue Coverage Factor calculated in Step 7 above, 55.3571%, by the net feeder plant investment directly assigned to each DLS POI. The revenue requirement calculations by sub-function for each wholesale POI are found in Attachment 8.

liage 14 4813

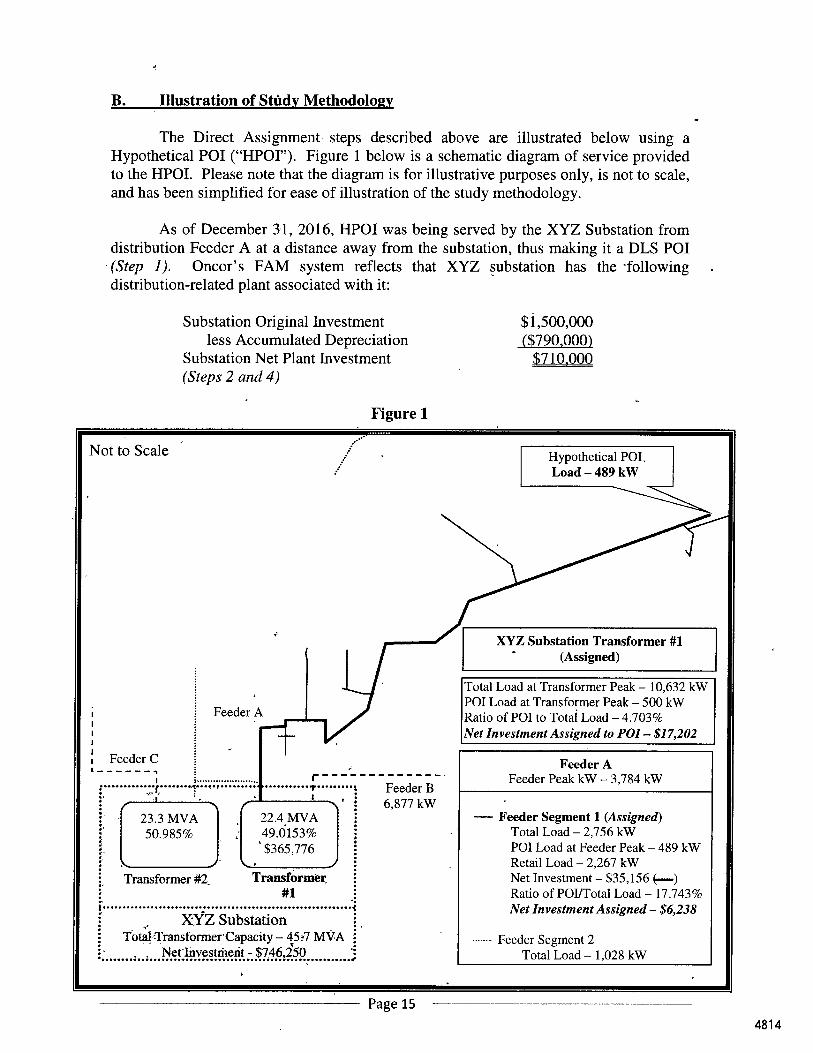

Feeder C

Not to Scale Hypothetical POI. Load — 489 kW

Feeder A

23.3 MVA 50.985%

Transformer #2_

XYZ Substation Total,TransformerCapacity — 45i7 MVA

NetInvestrherit - $746,150

XYZ Substation Transformer #1 (Assigned)

Total Load at Transformer Peak — 10,632 kW POI Load at Transformer Peak — 500 kW Ratio of POI to Total Load — 4.703% Net Investment Assigned to POI — $17,202

Feeder A Feeder Peak kW — 3,784 kW

— Feeder Segment 1 (Assigned) Total Load — 2,756 kW POI Load at Feeder Peak — 489 kW Retail Load — 2,267 kW Net Investment — $35,156 Ratio of POI/Total Load — 17.743% Net Investment Assigned — $6,238

Feeder Segment 2 Total Load — 1,028 kW

Feeder B 6,877 kW

22.4 MVA 49.6153% $365,776

Transformer. #1

B. Illustration of Stfidv Methodology

The Direct Assignment- steps described above are illustrated below using a Hypothetical POI ("HP0r). Figure 1 below is a schematic diagram of service provided to the HPOI. Please note that the diagram is for illustrative purposes only, is not to scale, and has been simplified for ease of illustration of the study methodology.

As of December 31, 2016, HPOI was being served by the XYZ Substation from distribution Feeder A at a distance away from the substation, thus making it a DLS POI (Step 1). Oncor's FAM system reflects that XYZ substation has the following distribution-related plant associated with it:

Substation Original Investment

$1,500,000 less Accumulated Depreciation

($790,000)

Substation Net Plant Investment

$710.000 (Steps 2 and 4)

Figure 1

Page 15

4814

The XYZ Substation has two transformers, one that serves retail load exclusively (Transformer 2) and one that serves a mixture of retail loads and the HPOI (Transformer 1). Because the substation consists of significant costs that are common to both transformers, it is first necessary to allocate the net substation ,plant investment between the transformers. This is accomplished using the transformer capacity ratings. Transformer 1 is rated at 22.4 MVA and Transformer 2 is rated at 23.3 MVA. Using a ratio share of installed capacity to assign a portion of the net substation investment to the transformer that serves the HPOI, 49.0153% of the XYZ net substation investment is assigned to HPOI-serving transformer as follows (Step 5a):

Transformer MVA Rating Percent of Total # 1 (HPOIjserving) 22.4 49.0153% # 2 23.3 50.9847% Total 45.7 100.0000%

Transformer 1 Allocation of Substation Plant: Substation Net Plant Investment . $746,250 Transformer 1 Percentage.Allocation x 49.0153% Substation Net Plant Assigned to Transformer 1 $365,776

Because the transformer serving the wholesale HPOI also serves retail load, the substation investment assigned to Transformer 1 is then further allocated between the HPOI and retail load. This is done by means of a load ratio share allocation. The load on Transformer 1 at the time of the transformer peak was 10,632 kW, and the HPOI load at the same time of the transformer peak was 500 kW, or 4.703% of the total Transformer 1 load. The HPOI's portion of the assigned transformer costs is calculated as follows:

500 kW HPOI — Assigned Substation Investment =

10,632 kW * $365,776 = $17,202

As the HPOI is a DLS POI that is served from a point on the distribution feeder away from the substation, the additional step of assigning feeder investment (i.e., primary distribution conductors, devices and poles) is necessary to determine the total cost of service to this HPOI. The first step in this process is to identify the cost of the distribution feeder facilities along Feeder A that are used to serve the ,HPOI (represented by the heavy solid green line on Figure 1). Based on information obtained from DIS and the FAM system, the following costs were identified:

HPOI-Serving Feeder Original Investment $109,796 less Accumulated Depreciation ($74,640)

Net Plant Investment of HPOI-Serving Feeder Segments $35,156 (Steps 3 and 4)

Next, Oncor determined feeder peak load information for Feeder A. Based on data obtained from Oncor's SCADA system, Feeder A experienced a peak demand of 3,784 kW. The HPOI load at the time of the feeder peak was 489 kW as recorded by the

Page 16

4815

HPOI's IDR meter. Next, 289 retail eustomers that share distribution feeder facilities, with the HPOI beyond the substation getaway were identified using DIS. Using interval usage data obtained from meter data storag . systems (MDMS and MV-90) for the retail customers served from the feeder segment, the total load attributed to the retail customers at the time of the feeder peak was calculated at 2,267 kW. Next, the load ratio share of the POI load to the total load on the portion of the distribution feeder that serves the HPOI was calculated as follows:

kW Percent of Total HPOI Load 489 17.743%' Retail Load on HPOI-Serving Feeder Segment 2 267 82.257% Total Load on HPOI-Serving Feeder Segment 2,756 100.000%

The ratio of the HPOI load to the total load on the feeder segment used to serve the HPOI was then applied to the net plant investment of the distribution feeder that serves the HPOI as follows:

Net Piant Investment of HPOI-Serving Feeder Segment $35,156 HPOI Feeder Load Percentage x 17.743% HPOI-Assigned Feeder Investment $63_21 (Step 5b)

To calculate the revenue requirement for the Substation Transformation function and the Distribution Line function, the Revenue Coverage Ratios calculated in Table 3 above were multiplied by the net plant investment for substation facilities and distribution line facilities that are directly assigned to HPOI.

Substation Distribution Line Transformation Function • Function

HPOI Assigned Net Plant Investment $17,202 $6,328

Revenue Coverage Factor x 22.2511% x 55.3571%

Revenue Requirement $3828 $3503

Page 17

4816

C. Study Results

During the Direct Assignment Study period, calendar year 2016, Oncor served 65 POIs consisting of 14 XFMR and 51 DLS POIs. A summary of the number of POIs, bST type, that Oncor has with each of its wholesale customers is shown in Table 4 below.

Table 4

Wholesale Customer XFMR DLS Total POIs Braios 0 18 18

Lyntegar EC 1 3 4 City of Goldsmith 0 1 1

RaybUrn 11 17 28 Tex-La 0 10 10 TNMP 2 2 4

Total Wholesale 14 ,. 51 65

The revenue requirements for the Wholesale Substation Transformation and Distribution Line functions resulting from the incorporation of the directly assigned plant amounts into the modified version of the COS Study filed in Schedule II-I of Oncor's current rate increase application are summarized in Table 5 below. These amounts represent the revenue requirement for Oncor's wholesale customers served at distribution voltage, including associated O&M and A&G expense, depreciation, taxes and other cost of service items utilizing the direct assignment methodology.

Table 5

Wholesale Substation Transformation

Function

Wholesale Distribution Line

Function

Total Wholesale

Gross Plant $17,440,037 $3,589,659 $21,029,696

Accum. Depreciation 5,899,662 1,604,408 7,504,070

Net Plant 11,540,375 1,985,251 13,525,626

Other Rate Base Items (1,144,676) (29,123) • (1,173,799)

Rate Base 10,395,699 1,956,128 12,351,827

Expenes, Depr, Taxes 1,664,829 910,132 2,574,961

Return (@7.7475%) 805,407 151,551 956,958

Minus: Other Revenue ' 9,706 8,639 18,345

Revenue Requirement $2,460,529 $1,053,044 $3,513,573

Page 18

4817

III. DIRECT ASSIGNMENT RATE DESIGN OPTIONS

The concept of direct assignment involves directly assigning costs to individual customers based on the specific facilities that are used to serve the customers. Although, as explained by Oncor witness Mr. J. Michael Sherburne, Oncor does not agree that direct assignments for Wholesale customer classes are appropriate, Oncor believes that if (Ikea assignment of costs is ordered for Wholesale customers, then it should naturally follow that POI-specific rates should be consistently charged based on those costs that are directly assigned to individual wholesale POIs. To do otherwise and charge a "blended" or average rate to all wholesale POIs would result in the subsidization of some wholes'ale POIs by other POIs and run counter to the whole premise of direct assignment. Therefore, Oncor has taken the logical next step after the study was completed and converted the POI-specific revenue requirements into POI-specific rates using two different rate design options. For more information regarding the issues involved in designing and applying wholesale rates using directly assigned plant costs;please refer to the Direct Prefiled Testimony of Mr. Sherburne.

A. Calculation of POI-Specific Demand-Based Rates

The first rate design option involves dividing the POI-specific revenue requirement by the annual number of billing units, which is calculated by multiplying the POI's 2016 peak demand by 12 (i.e., at 100% ratchet). The resulting $/kW rate is the POI-specific rate that would be multiplied by the POI's 12-month peak demand and billed to the wholesale POI monthly. Attachment 9 provides a summary of the total rate for wholesale transmission service at distribution voltage for each XFMR and DLS POI.

Returning to the HPOI, based on the IIPOI's peak demand during the 2016 calendar year of 740 kW, the annual billing units at 100% ratchet equal 8,880 kW. Dividing the revenue requirement for each function by the annual billing units, the rates for Substation Transformation and,Distribution Line function for the HPOI are obtained as follows:

Substation Transformation

Function

Distribution Line Function

Total

Revenue Requirement $3,828 $3,503 $7,331 Annual Billing kW 8,880 ~ 8,880 ~ 8,880

POI Rate ($/Billing kW) $0.43 $0.39 $0.83

B. Calculation of POI-Specific Fixed Monthly Charges

Another rate design option involves calculating a POI-specific fixed monthly chaige by dividing the POI-specific revenue requirement by 12 months. This rather simplistic approach is consistent with the concept of direct assignment in that the charge

Page 19

4818

for distribution service is based on the cost of facilities directly used to serve the POI and is not directly tied to the wholesale POI s annual peak demand. For example, again returning to the HPOI with a total revenue requirement of $7,331 based on directly assigned costs, this HPOI should be required to pay $7,331 annually, or $610.92 monthly, for service regardless of the demand it places on the system, provided the existing distribution facilities are sufficient to accommodate the demand. The POI-specific charges under a fixed monthly charge approach are found in Attachment 10.

Page 20

4819

IV. ONCOR'S POSITION ON DIRECT ASSIGNMENT FOR WHOLESALE CUSTOMERS

As stated in the overview of this Direct Assignment Study and in testimony filed in Docket No. 35717 and in the current docket, Oncor does tiot agree that direct assignment of costs for wholesale customers on Oncor's network is appropriate. Oncor's position is consistent with the Electric Utility Cost Allocation Manual published by the National Association of Regulatory Utility Commissioners ("NARUC") in Jahuary, 1992, which states: "Direct assignments of such costs implies that the facilities can be considered entirely apart from the integrated system. In fact, the case for the independence of the facilities must be unequivocal since the customer must be willing to bear all the costs of service that, due to the unintegrated character of the facilities, may be just as high for service that is less reliable than service on the integrated system." (page 83). This concept was further discussed in a presentation entitled "Cost Allocation, Cost of Service Studies, and The Principles of Designing Rates" that was presented on January 23, 2009, by representaiiVes from the Oklahoma Corporation Commission,in association with the NARUC Energy Regulatory Partnership Program and The Petroleum and Natural Gas Regulatory Board of India. That presentation stated: "Most utility investments serve many different customer groups which use the facilities differently and Direct' Assignment is not possible. Thus, it is virtually impossible for a utility to attribute specific cost responsibility for these 'common costs and direct assignment is rarely used as for a complete service study." (page. 10; emphasis in the original).

As these two references suggest, direct assignment of costs is generally limited to those situations: (1) where the facilities to be directly assigned are not integrated into the larger system, such as long radial transmission lines; (2) where costs are clearly incurred by the company on behalf of a single customer or class, such as streetlight fixtures which are directly assigned to the street lighting class; and (3) where facilities are not shared with other customers or classes. Even though Oncor has produced a Direct Assignment Study for its wholesale customers in this project, as the documentation supports, delivery service to the overwhelming majority of Oncor wholesale POIs is not consistent with any of these situations, thereby supporting the conclusion that assigning costs in this manner to Oncor's wholesale customers is not an appropriate iise of direcrassignment.

Aside from this fundamental misapplication of the Concept of direct assignment, in general, Oncor remains very concerned about the asymmetrical benefits that wholesale customers receive from directly assigning plant to wholesale POIs. Wholesale customers would benefit from lower rates that result from the direct assignment of specific substation's, transformers, and distribution lines when compared to the fully allocated system average cost of service approach used for all other rate classes. Yet, they receive all of the benefits of being a part of an integrated system. Before the decision to base rates for wholesale customers on direct assignment is made, the implications that follow from directly assigning these costs should be fully understood and properly vetted.

Page 21

4820

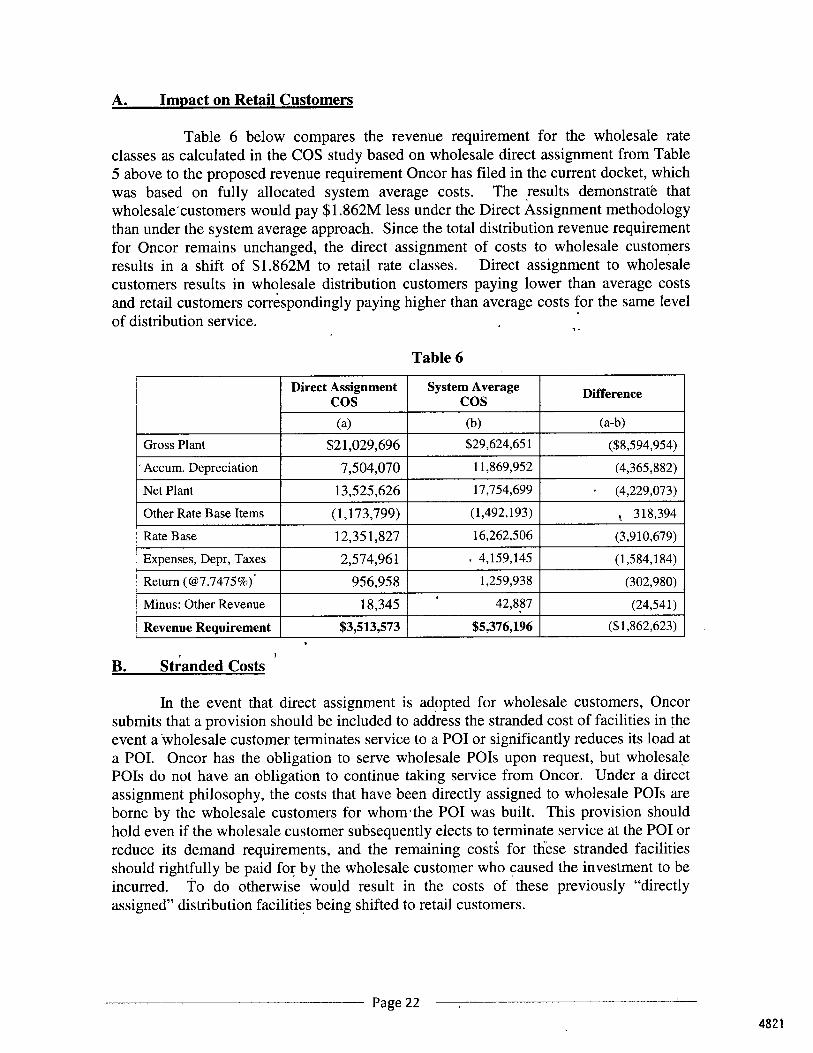

A. Impact on Retail Customers

Table 6 below compares the revenue requirement for the wholesale rate classes as calculated in the COS study based on wholesale direct assignment from Table 5 above to the proposed revenue requirement Oncor has filed in the current docket, which was based on fully allocated system average costs. The results demonstrate that wholesale'customers would pay $1.862M less under the Direct Assignment methodology than under the system average approach. Since the total distribution revenue requirement for Oncor remains unchanged, the direct assignment of costs to wholesale customers results in a shift of $1.862M to retail rate classes. Direct assignment to wholesale customers results in wholesale distribution customers paying lower than average costs and retail customers correspondingly paying higher than average costs for the same level of distribution service.

Table 6

Direct Assignment COS

System Average COS

Difference

(a) (b) (a-b)

Gross Plant $21,029,696 $29,624,651 ($8,594,954)

' Accum. Depreciation 7,504,070 11,869,952 (4,365,882)

Net Plant 13,525,626 17,754,699 (4,229,073)

Other Rate Base Items (1,173,799) (1,492,193) , 318,394

Rate Base 12,351,827 16,262,506 (3,910,679)

Expenses, Depr, Taxes 2,574,961 , 4,159,145 (1,584,184)

Return (@7.7475%) 956,958 1,259,938 (302,980)

Minus: Other Revenue 18,345 42,887 (24,541)

Revenue Requirement $3,513,573 $5,376,196 ($1,862,623)

B. Stranded Costs

In the event that direct assignment is adopted for wholesale customers, Oncor submits that a provision should be included to address the stranded cost of facilities in the event a wholesale customer terminates service to a POI or significantly reduces its load at a POI. Oncor has the obligation to serve wholesale POIs upon request, but wholesale POIs do not have an obligation to continue taking service from Oncor. Under a direct assignment philosophy, the costs that have been directly assigned to wholesale POIs are borne by the wholesale customers for whom' the POI was built. This provision should hold even if the wholesale customer subsequently elects to terminate service at the POI or reduce its demand requirements, and the remaining costš for these stranded facilities should rightfully be paid for by the wholesale customer who caused the investment to be incurred. To do otherwise Would result in the costs of these previously "directly assigner distribution facilities being shifted to retail customers.

Page 22

4821

This abandonment of directly assigned facilities by wholesale customers is not a theoretical issue. It is a real and present issue. As pointed out in Oncor witness Mr. Sherburne's Direbt Pre-filed Testimony in in this case, Oncor has experienced as significant decline in the number of wholesale delivery points since the previous direct assignment study was undertaken. In fact, 23 wholesale POIs that were part of the Project No. 38808 study have ceased taking service. As an examp1e,1 using the HPOI illustration above, if the customer decided to terminate service at this HPOI, the net plant assigned to retail customers would increase by $23,440 with absolutely no change in the facilities used by these customers. Although the directly assigned plant aMount for the HPOI is not a large enough amount by itself to have a significant impact upon retail rates, the abandonment of several large POIs could have a material impact on the rates paid by retail customers. For example, betWeen January 1, 2010, and December 31, 2016, $5,178,374 of net plant "directly assigner to 23 wholesale POIs in the Project No. 38808 study has been stranded, by the wholesale customers who have ceased taking service at these abandoned wholesale POIs.

Wholesale customers should not be allowed to receive lower rates resulting from directly assigned costs, but then be allowed to forego cost responsibility by abandoning the investment that was directly serving them. To prevent retail customers from being saddled with the cost of idle facilities in a direct assignment environment, a provision for the payment of stranded costs should be included if the use of direct assignment for wholesale customers is adopted by the Commission. The stranded cost calculation should be based on the amount of the un-depreciated balance of the directly assigned plant in service, plus the cost of removal of facilities, less any salvage value of the removed facilities. This would hold retail customers harmless from abandonment of directly assigned plant by wholesale customers while requiring wholesale customers to pay for the plant that was built to direct1ST serve their load.

C. , Changes to Facilities and Loads

The distribution network is not stagnant; changes occur on a daily basis due to many factors, including equipment change-outs as a result of damage or aging facilities, upgrades as a result of load growth, and service re-routes as a result of an evolving network. As a result, it is not uncommon'for Oncor to be required to modify the facilities used to serve a POI at any point in time. In keeping true to the concept of direct assignment, changes in the make-up of the facilities used to serve a POI should result iñ a change to the rate charged to that POI. However, because of the significant amount of work that goes into a direct assignment study, Oncor believes it is impractical and inappropriate to recalculate rates every time a change is made to the distribution network used to serve wholesale customers. Oncor further submits that in most cases, change-out of facilities would result in an increase in the rates charged.to wholesale POIs due to the replacement of older, depreciated facilities with newer facilities, thus increasing the net plant associated with the POI. However, this issue is avoided with the use of rates based on system average costs.

Page 23

4822

In addition, the direct assignment amounts for any substation or feeder that serves a combination of retail and wholesale load will change over time as customer loads, which are the basis for separation of costs between the wholesale POIs and the retail load, vary from year to year. Although Oncor anticipates that most changes will be fairly minor from year to year, changes are inevitable and will necessitate the complete reallocation of costs between retail and wholesale customers, at a minimum with each rate case, as wholesale and retail loads on directly assigned substations and feeders change.

D. Backstand Capabilities

Noticeably missing from the calculation of directly assigned costs are those costs associated with backstand capabilities. While not, in place for every wholesale POI, Oncor attempts to build in this kind of capability where it is prudent based on the number of customers potentially impacted by an outage and the costs to provide such capability. In fact, the majority of the 65 wholesale POIs have some level of backstand capability. However, there is _no elegant way to appropriately assign costs for the redundancy to wholesale POIs under a direct assignment methodology. As a result, retail customers will be required to fund this capability in its entirety even though wholesale POIs — and ultimately their retail custom6rs — benefit from this backstand capability. Again, this issue of subsidization of costs by retail rate classes is avoided with the use of rdtes bašed on system average costs.

E. New POIs

If the' Commission endorses the use of direct assignment of costs to wholesale customers, then the Commission should also approve a standard, easily implemented means for developing a rate for service to new wholesale POIs. Unlike a system-average rate that would apply to new and existing customers, a specific rate would need to be calculated based on the facilities directly used to serve new POIs. Oncor submits that the calculation of a new rate should be based on the same approach employed in this direct assignment study and the wholesale customers contracted demand.

Page 24

4823

V. CONCLUSION

Oncor has complied with the Commission's Order in Project No. 38808 to submit a direct assignment study for wholesale distribution customers that employs information and data consistent with its filed rate increase proposal. While the rates resultink from this direct assignment study may be considered by some to be more reflective of the costs to serve these wholesale customer classes than are tariffs based upon average cost allocations, the resulting rates are still significantly below what wholesale rates would be if based on a fully allocated system average cost of service (i.e., the same methodology used to determine retail rates for comparable service).

After undertaking this study, .Oncor remains convinced that the use of direct assignments to determine the costs of service for wholesale distribution customers is not appropriate. Oncor believes it is inappropriate to use one methodology to apportion part of a single asset (i.e., the substation transformer, pole, span of conductor, etc.) to one rate class (i.e., direct assignment) and a different methodology (i.e., system average) to apportion the remainder of that same asset to other rate classes, when all customers using that asset use it in a similar manner. Because retail rates are correctly based on system average costs, and because as shown in this study almost all operating plant assets used by wholesale customers are shared with retail customers, Oncor maintains that wholesale rates should also be based on the same methodoloiy of system average costs. In addition, the requirement to allocate costs between retail and wholesale customers that share common facilities is contrary to the main principles of "direct assignmenr and further demonstrates the integrated nature of Oncor's distribution system. Of all the operating plant costs assigned to wholesale customers in this study, most are derived from assets actually shared by both wholesale and retail customers, and are therefore "directly assigner on the basis of an allocation. Lastly, direct assignment to this customer group raises` other issues such as proper allocation of costs associated with backstand capabilities, treatment of stranded costs, the on-koing need to update costs as a result of facility changes, addition of new POIs, and ultimately whether it is appropriate for retail customers whose rates are based on system average costs to subsidize wholesale customers.

For these reasons, ,Oncor encourages the Commission to reject the direct assignment of costs for wholesale customers served from Oncor's distribution network and to apply the system average cost of service model to the Wholesale rate classes.

Page 25

4824

VI. SUPPORTING INFORMATION A. Attachments

1. Feeder Maps for Wliolesale DLS POIs * 2. Transformer Plate Rating and Transformer Peak 3. POI Substation Costs and Rate Design 4. Feeder, Retail, and Wholesale Loads and POI Load Ratio

Share Information for DLS POIs by StudyID 5. POI Distribution Line Costs and Rate Design 6. Summary of Directly Assigned Substation Investment by

Account 7. Summary of Directly Assigned Feeder Investment by Account 8. Revenue Requirement for the Substation Transformation

Function by POI 9. POI-Specific Rate for Wholesale Distribution Service Based on

Billing Demand 10. POI-Specific Flat Monthly Charge for Wholesale Distribution

Service Based B. Workpapers

WP/I Feeder Segmentations and Retail Loads @ Feeder Peak WP/II-I-1.6a

Summary of Customer Impact: Compared to System average (without adjustment)

WP/II-I-1.3 Workpaper - Wherein Certain Wholesale Plant Accounts Are Directly Assigned Schedules II-I-1-DIST and II-1-2 DIST with Direct Assignment

WP/III Feeder Segmentation Maps *

WP/IV Substation One-Lines *

WP/V Letter from Brennan J. Foley

* This information is highly sensitive confidential and will be made available only after execution of a certification_ to be bound by the draft protective order set forth in Section • VII of,this Rate Filing Package or a protective order issued in this docket.

Page 26

4825

Attachment 1 PageI of 1

2017 Rate Cáse Oncor Electric Delivery Company LLC

Wholesale Customer Direct Assignment Study

Feeder Maps for Wholesale DLS POls

(51 pages)

This information is highly sensitive confidential and will be made avaifable only after execution of a certification to, be bound by the draft protective order set forth in Section VII of this Rate Filing Package or a protectiVe order issued in this docket.

4826

Attachment 2 Page 1 of 1

2017 RATE CASE ONCOR ELECTRIC DELIVERY COMPANY LLC

DIRECT ASSIGNMENT OF COSTS FOR WHOLESALE CLASSES

Transformer Plate Rating and Transformer Peak

'StudylD PO1 Name Substation

Name

Plate Rating (MVA) of Transformers @ Substation kW @ Transformer Peak POI Load

Ratio Share of Transformer

Assigned Facility (A) #1 #2 #3 - #4

P01 Transformer as Percent of

Total Transformer

kW Wholesale

P01 (a) (b) (c) (d).(db)

6220735 Raybum, Cooper Highway Sulphur Springs East 28.0 (A) 100.0000% 22,818 5,668 24.8404% 6221634 Raybum, Commerce East Commerce 28.0 (A) 100.0000% 14,573 3,076 21 1080% 6221733 Rayburn, Commerce West Commerce South 25.0 (A) 28 0 47.1698% 16,325 463 2.8367% 6222533 Raybum, Mesquite Valley Mesquite 46.7. (A) 46 7 50 0000% 31,762 60 0 1889% 6223099 Raybum, Chiesa Road Dalrock 46.7 46.7 (A) 46,7 33.3333% 17,801 136 0.7640% 6223129 Rayburn, Commerce South Cornmerce South 25 0 (A) 28 0 47.1698% 16,325 1,264 7 7427% 6230536 Rayburn, Mckinney East Mckinney 46.7 28.0 28 0 (A) 46 7 31.2584% 31,595 4,780 15.1289% 6231435_1 # Rayburn, Gordonville - A Gordonville 10 5 (A) 100 0000% 6,768 4,825 71 3006% ' 6231435_2 # Raybum, Gordonville - B Gordonville 10.5 (A) 100.0000% 6,768 1,464 21.6391% 6231732 Raybum, Mckinney Hwy 380 W Mckinney White 46.7 (A) 46.7 50 0000% 36,871 5,702 15.4646% 6232101 # Raybum, Allen North Allen North 46.7 46 7 (A) 46 7 46 7 25 0000% 32,120 17,252 53.7110% 6232390 Rayburn, Stacy Road Allen North 46.7 46 7 (A) 46 7 46.7 25 0000% 32,120 7,556 23 5242% 6232459 * Rayburn, Mckinney South Mckinney South 46 7 (A) 46 7 50 0000% 51,184 11,658 22.7771% 6250534 Rayburn, Cartwnght Terrell South 28 0 (A) 100.0000% 21,591 2,740 12 6904% 6251235 Raybum, Cobb Switch Wills Point 28.0 28.0 (A) 50.0000% 9,162 4,471 48 7993% 6251433 # Rayburn, Duck Cove Duck Cove 7 5 (A) 100 0000% 7,125 7,125 100 0017% 6251631_1 # Rayburn, Seven Points - A Seven Points 10.5 (A) 10.5 50.0000% 6,175 6,175 100 0000% 6251631_2 # Raybum, Seven Points - B Seven Points 10 5 10 5 (A) 50 0000% 8,732 8,732 100.0000% 6251730 # Raybum, Kemp Kemp South 23 3 23.3 (A) 50 0000% 16,780 16,780 100 0000% 6251938 Rayburn, Tool Cedar Creek 10 5 10.5 (A) 50.0000% 6,192 6,192 100.0000% 6260939 Raybum, Minter Deport 10 5 (A) 100.0000% 3,766 1,728 45 8869% 6261036 Rayburn, Marvin North Pans East 28.0 (A) 25 0 52.8302% 17,441 2,215 12.6981% 6270631 Rayburn, Massey Lake Tennessee Colony 10.5 (A) 23.3 31 0651% 6,098 4,663 76.4675% 6270839 Rayburn, Malakoff Malakoff 2 9.4 (A) 10 5 47 1831% 6,500 1,536 23.6317% 6270938 # Raybum, Poynor Poynor 7.5 (A) 100.0000% 4,539 1,283 28 2701% 6271134 Rayburn, Neches Neches Pump 6 3 (A) 100.0000% 4,092 433 10 5761% 6271200 # Rayburn, Willow Springs Willow Springs 28 0 (A) 100.0000% 9,312 6,815 73.1839% 6271639 # Rayburn, Carroll Springs Carroll Springs 10 5 (A) 100.0000% 7,452 6,169 82.7779% 6530125 # Lyntegar, Key Substation Key 10 5 (A) 100.0000% 6,189 4,055 65 5238% 6530224 Lyntegar, Punkin Center Lamesa 9.4 20 0 22 4 (A) 18.1467% 6,271 2,511 40.0385% 6530521 Lyntegar, Welch Take-Off Welch 22.4 (A) 100.0000% 12,269 4,864 39.6473% 6530992 Lyntegar, North Lamesa Lamesa 9 4 20 0

-22.4 (A) 18 1467% 6,271 2,279 36.3367%

6720338 # Texas-New Mexico Power, Emory Emory 10 5 (A) 100.0000% 4,666 4,666 100 0000% 6720429 Texas-New Mexico Power, South Bend South Bend 2 0 (A) 100 0000% 1,218 422 34 6427% 6720536 * Texas-New Mexico Power, Deport Deport 10.5 (A) 100.0000% 3,766 2,016 53 5348% 6721369 Texas-New Mexico Power, Mentone Mason 28.0 (A) 100 0000% 24,066 325 1 3513% 6830228 City Of Goldsmith, Goldsmith # 2 Goldsmith 46.7 (A) 23 3 66.7143% 12,523 462 3 6911% 7010051 Tex-La, Owentown Hwy 271 Tyler Northeast 28 0 28 0 (A) 50 0000% 14,555 2,343 16 0963% 7010150 Tex-La, Cushing Cushing 10 5 (A) 10 5 50 0000% 6,267 2,148 34 2799% 7010655 Tex-La, Shawnee Rd Nacogdoches South 28.0 (A) 28 0 50.0000% 15,385 1,489 9 6780% 7010754 Tex-La, Oak Ridge Nacogdoches South 28 0 (A) 28.0 50.0000% 15,385 3,544 23.0345% 7011059 Tex-La, Oakwood South Long Lake 10.5 (A) 10 5 50 0000% 5,624 1,593 28 3162% 7011158 Tex-La, Lufkin Hwy 94 Hudson 28.0 (A) 28.0 50.0000% 21,079 2,443 11 5895% 7011653 Tex-La, North Centerville 12 5 Centerville 1-45 12.0 10 5 (A) 9.4 10 5 28 3019% 4,328 2,553 58 9862% 7012255 Tex-La, Zavalla Hwy 147 Huntington 28 0 (A) 47 0 37.3333% 14,336 1,336 9 3214% 7012453 Tex-La, Huntington Huntington 46.7 28 0 (A) 62 5167% 14,244 2,062 14.4768% 7012839 Tex-La, North Centerville 25 Centerville 1-45 10 5 (A) 12 5 9 4 10 5 24 4755% 7,014 4,254 60 6453% 7020076 Brazos, Venus Venus SW 22 4 (A) 100 0000% 15,000 3,600 24 0001% 7020175 Brazos, Seymour Seymour 8.4 (A) 100 0000% 1,670 1,331 79 6675% 7020274 Brazos, B K - Bomarton Bomarton 4 0 (A) 100 0000% 555 505 , 91 1427% 7020373 Brazos, Pettibone Cameron 10 5 9 4 10 5 (A) 34 5395% 5,763 376 6 5295% 7020472 Brazos, J A C - Henrietta Hennetta 20.0 (A) 100.0000% 9,441 305 3.2335% 7020571 Brazos, Thorndale North Thorndale North 10 5 (A) 100 0000% 7,717 284 3 6804% 7020670 Brazos, Stillhouse Hollow Dam Salado Switch 23.3 23 3 (A) 50 0000% 10,721 8 0.0743% 7020779 Brazos, Leon Plant Leon EBAA 28.0 (A) 100 0000% 19,591 2,375 12 1205% 7020878 Brazos, Deleon Deleon 10 5 (A) 100 0000% 7,852 1,138 14 4871% 7021074 Brazos, North Gorman Gorman 8 0 (A) 100 0000% 5,928 1,218 20 5521% 7021371 Brazos, Hwy 101 Colony Creek 10 5 (A) 100 0000% 2,300 1,380 59 9696% 7021579 Brazos, Lake Dallas Corinth 46 7 47 0 47.0 (A) 33 1912% 33,361 640 1 9184% 7021975 Brazos, Jacksboro Highwajr Graham East 22.4 (A) 23 3 49 0153% 10,615 508 4.7817% 7022072 Brazos, Markley PME Markley 10 5 (A) 100 0000% 1,128 645 57 1959% 7022874 Brazos, Jewett Jewett 23 3 (A) 100 0000% 14,413 2,026 14 0577% 7022999 Brazos, Hickory Creek Corinth South 47 0 (A) 100.0000% 17,943 3,940 21.9584% 7023029 Brazos, Mambnno Hwy Decordova Dam 23 3 23.3 (A) 50 0000% 14,592 220 1 5077% 9151117 Brazos, Oak Grove Fairfield West 28.0 (A) 100 0000% 20,961 330 1 5755%

# XFMR Only

4827

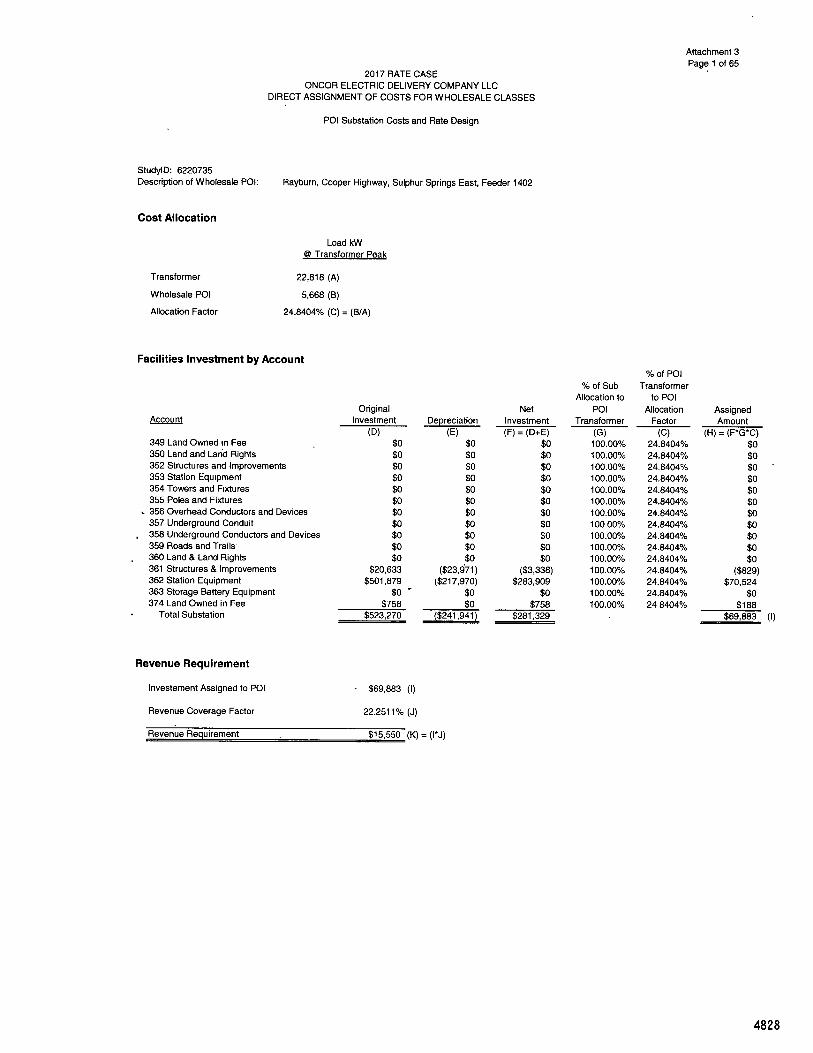

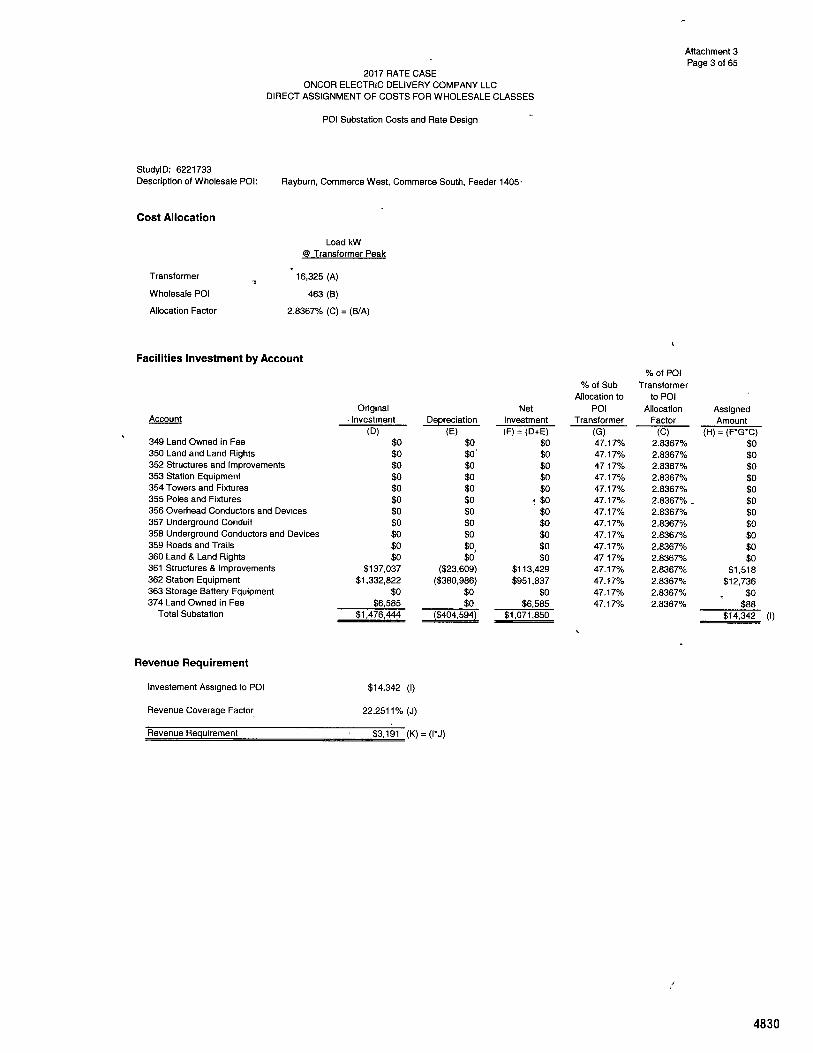

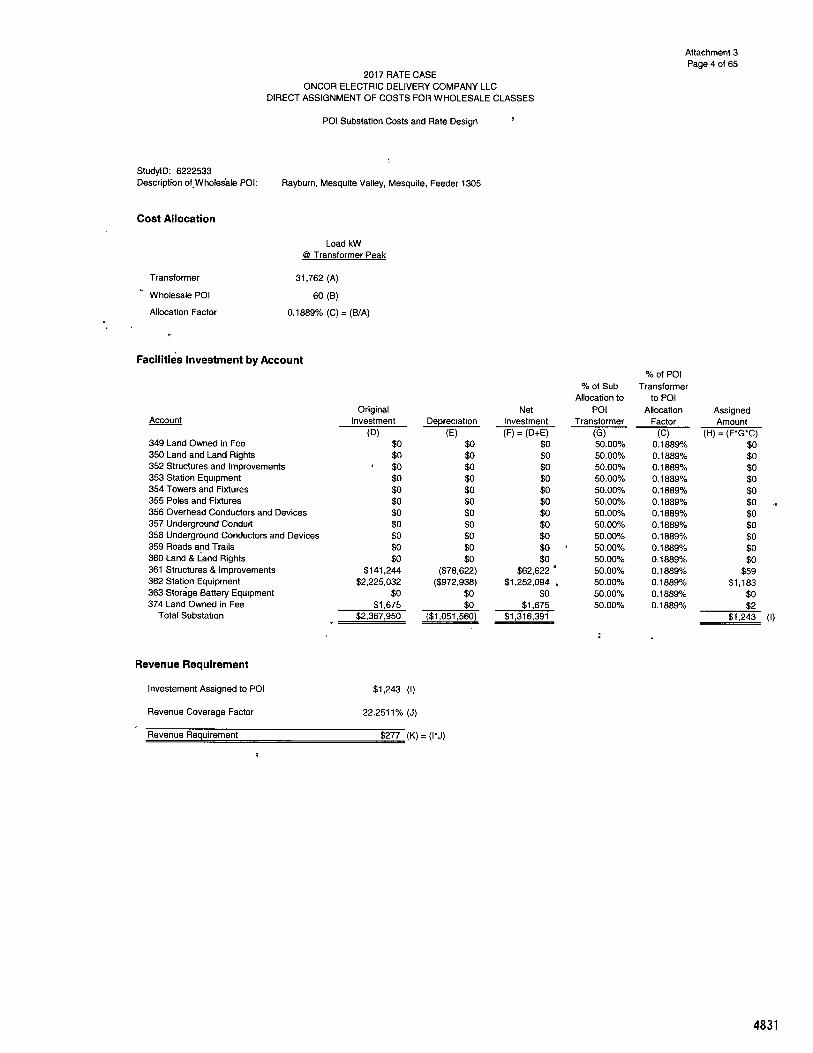

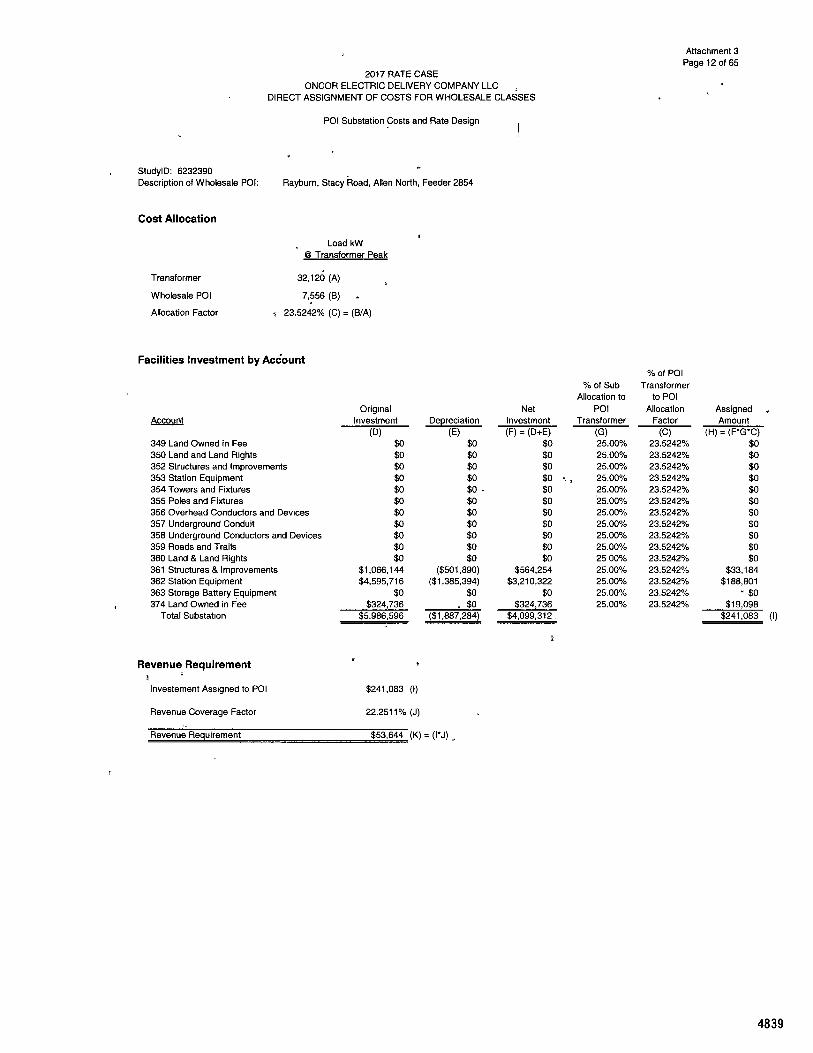

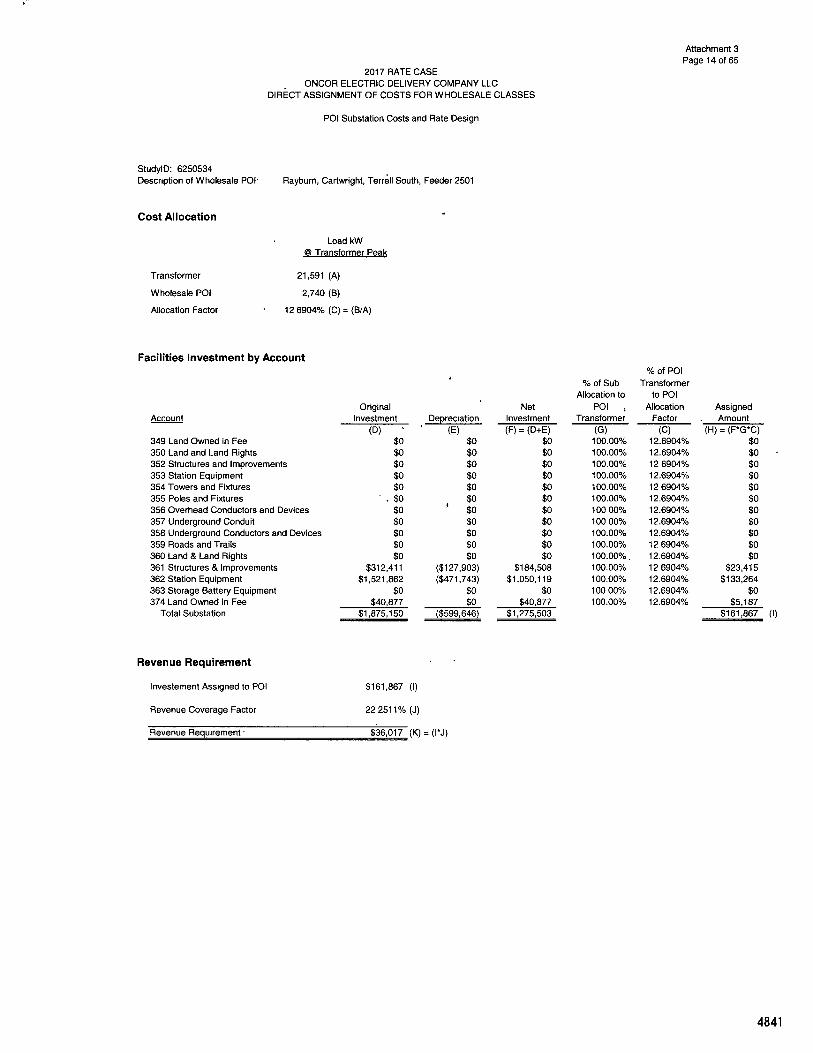

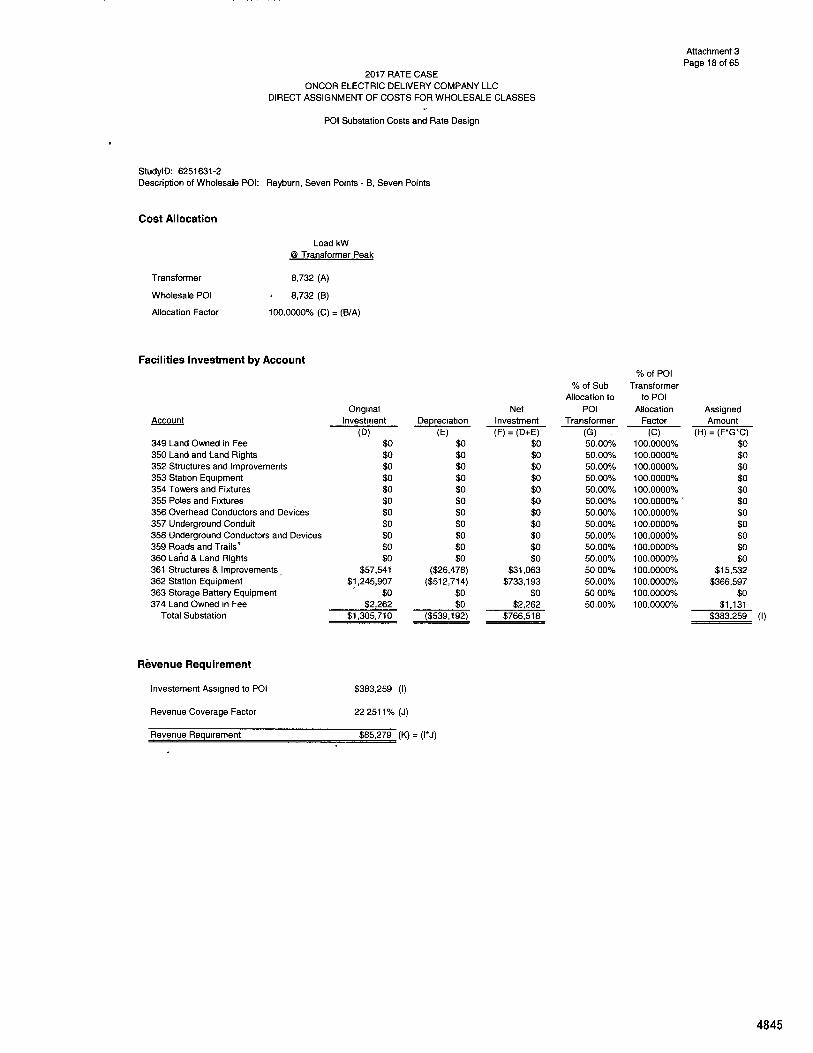

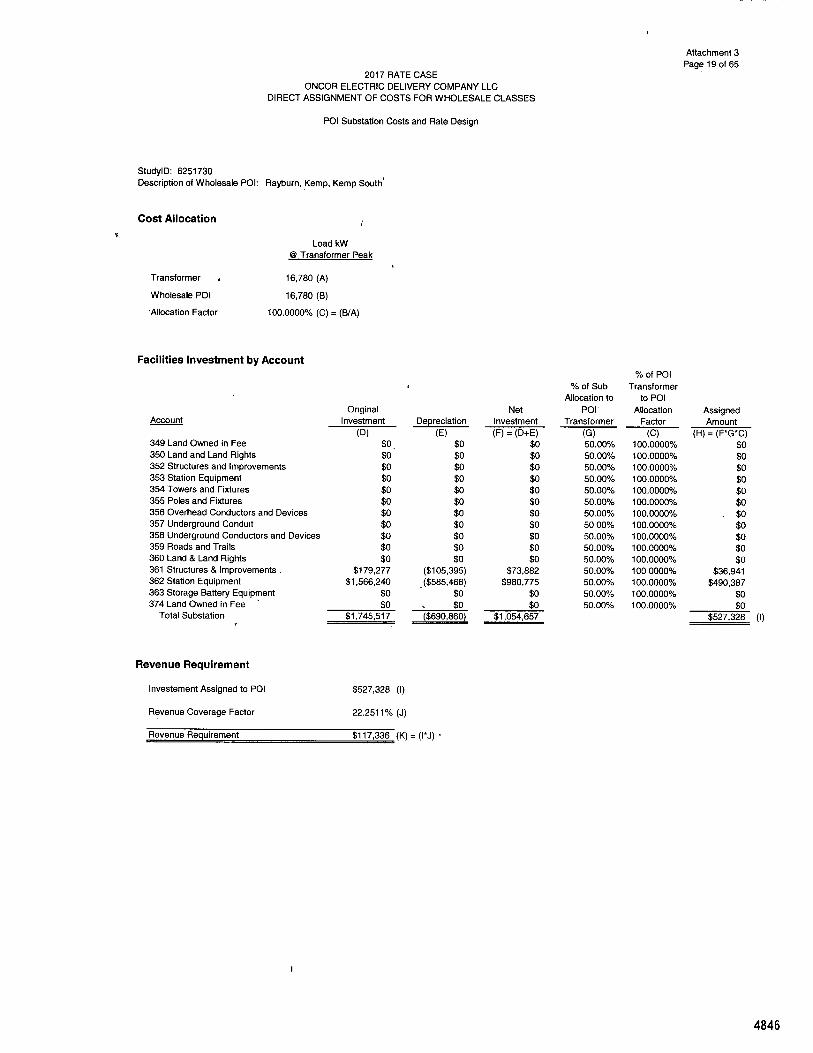

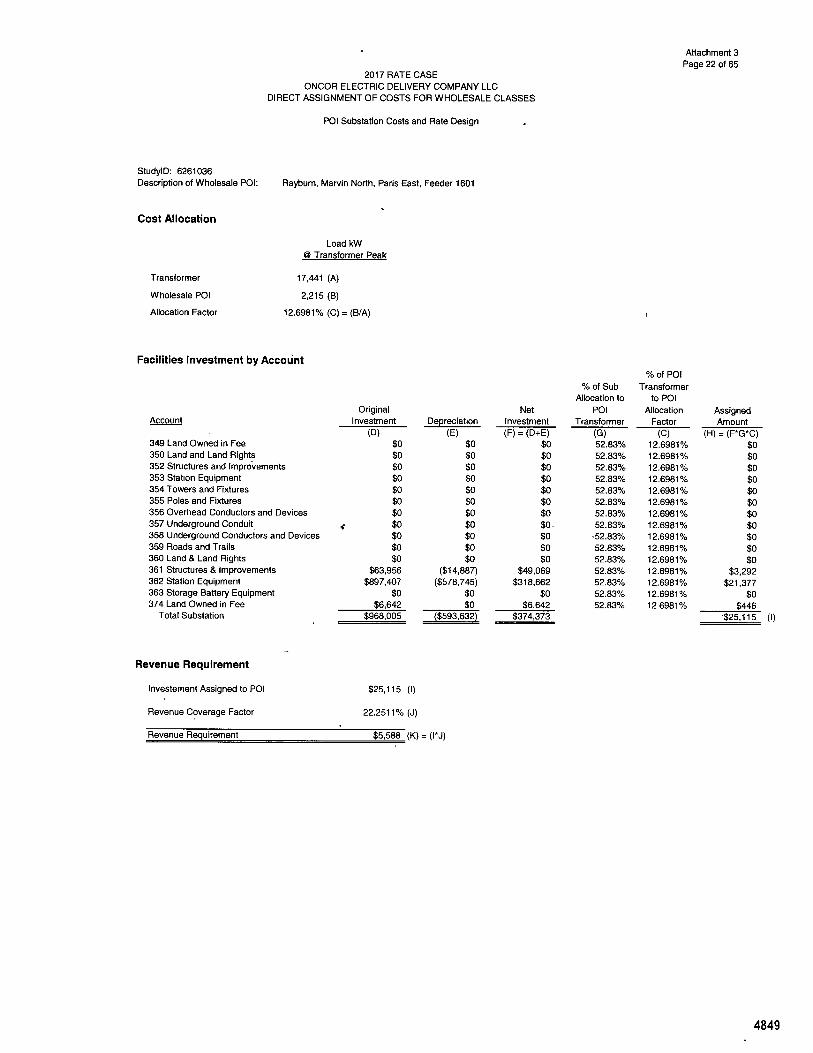

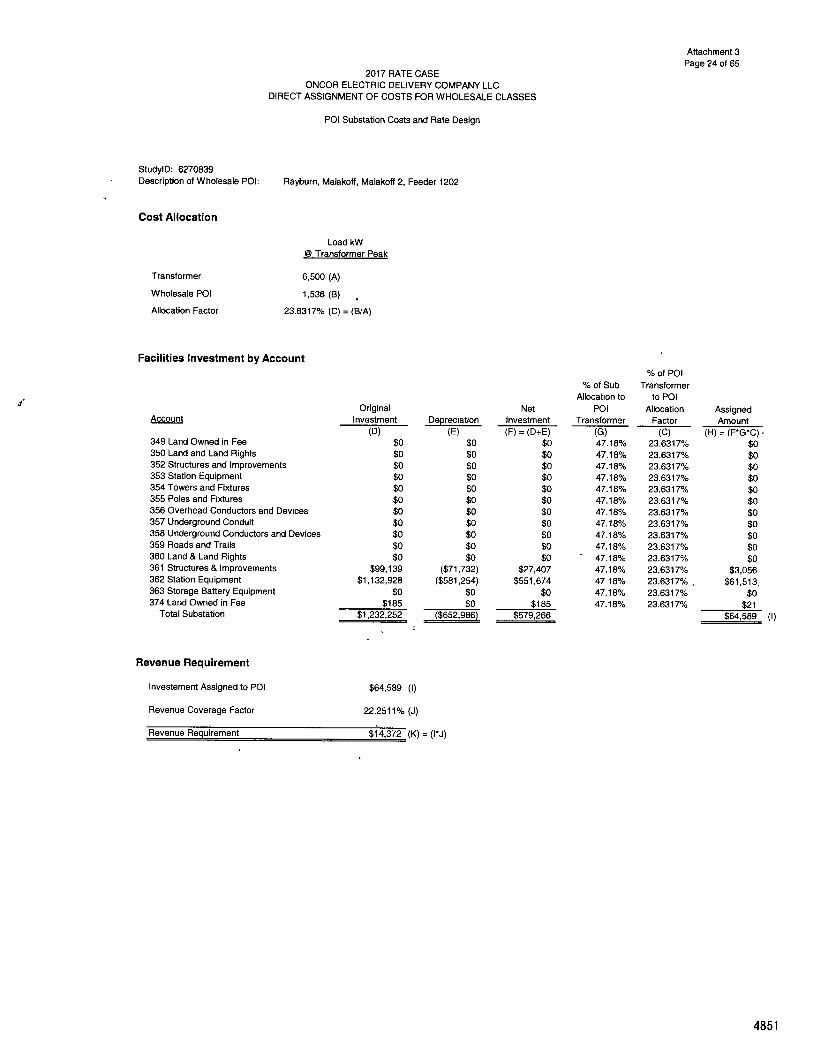

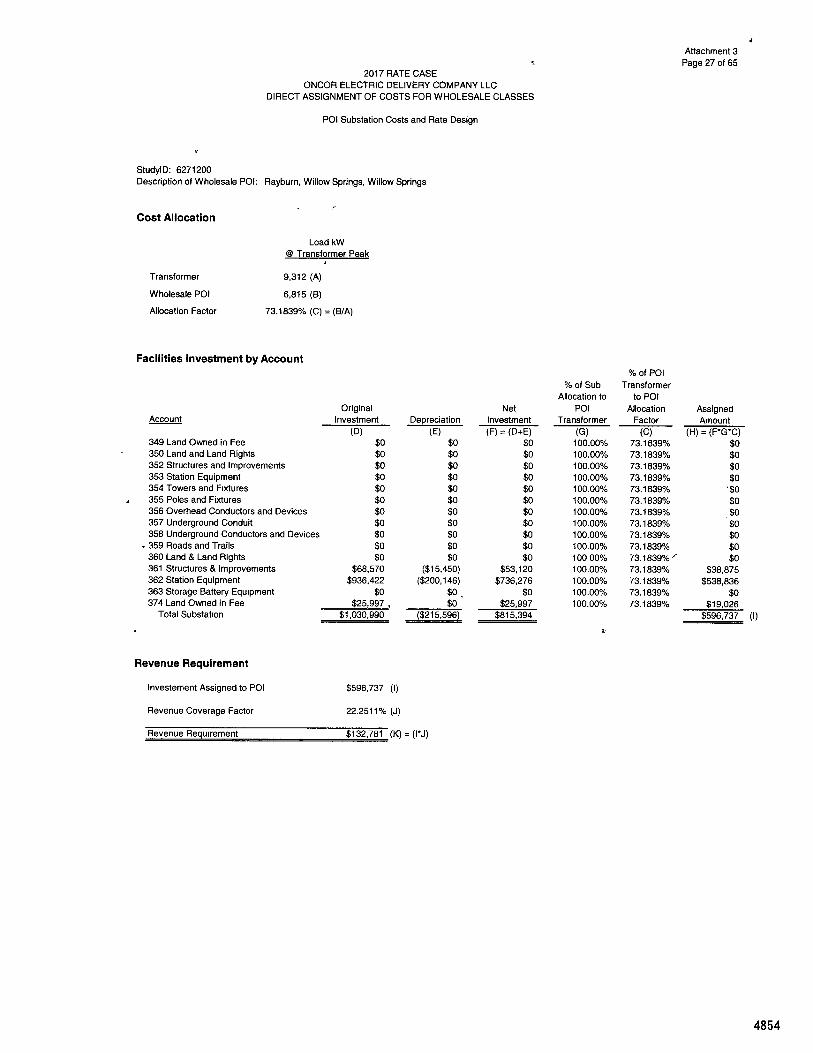

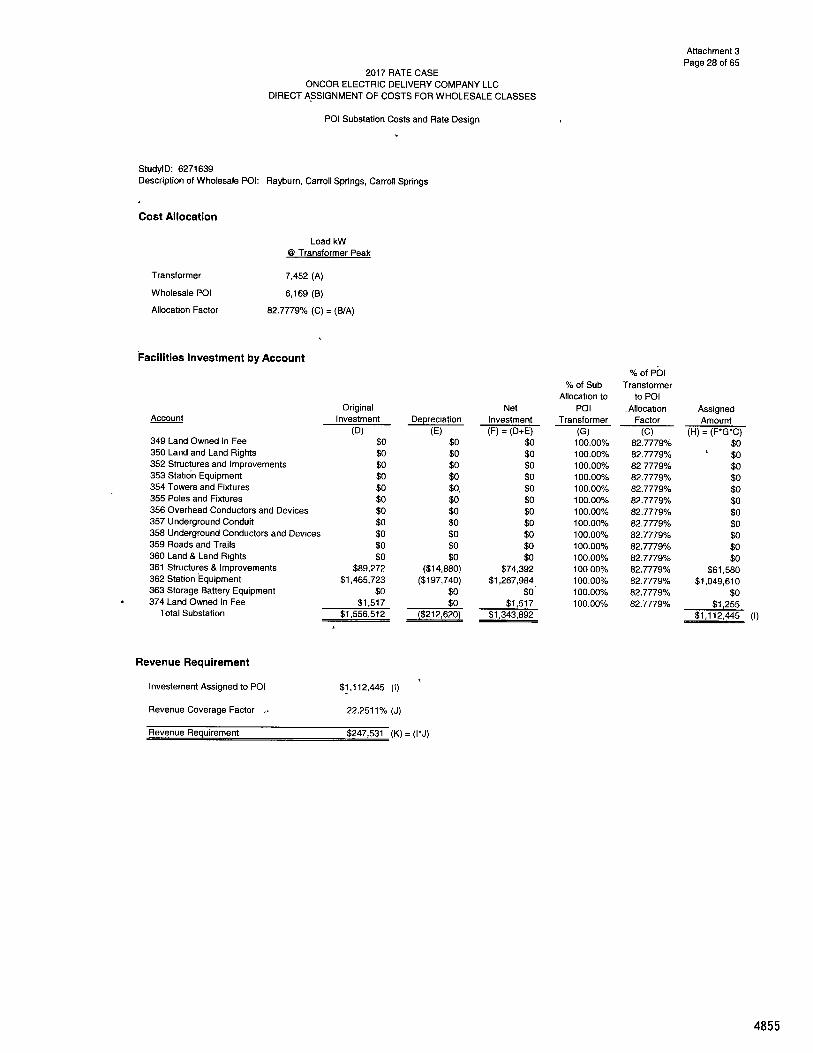

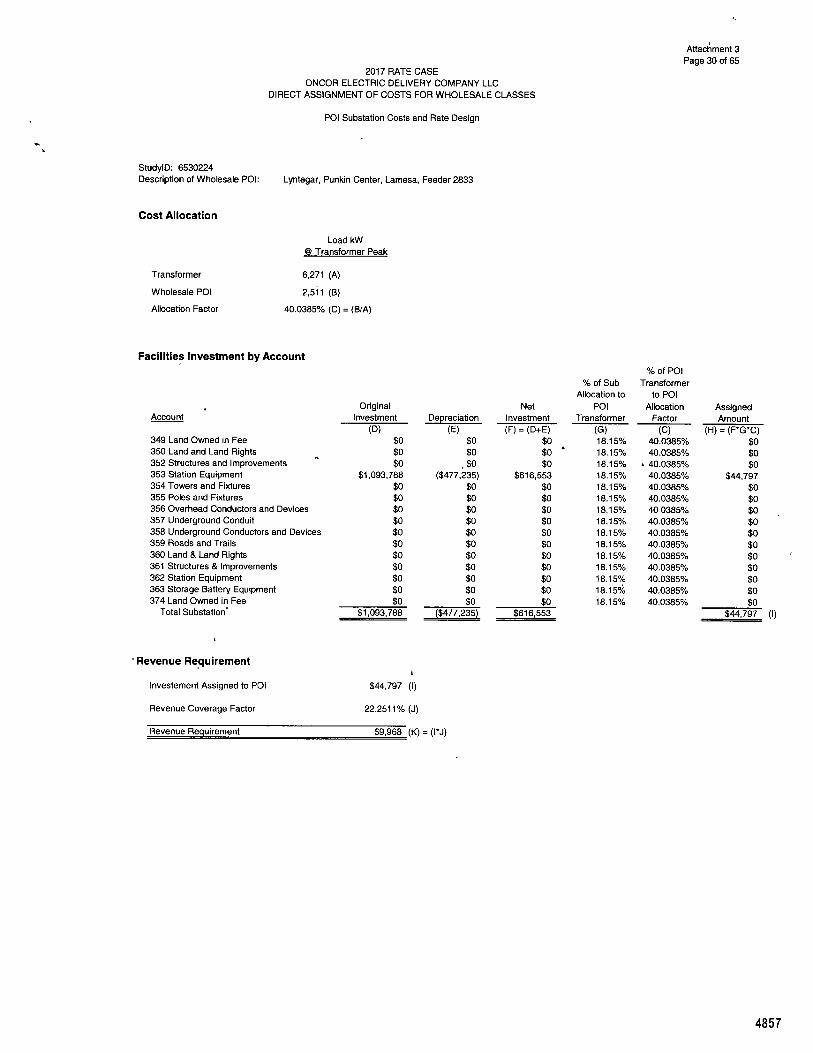

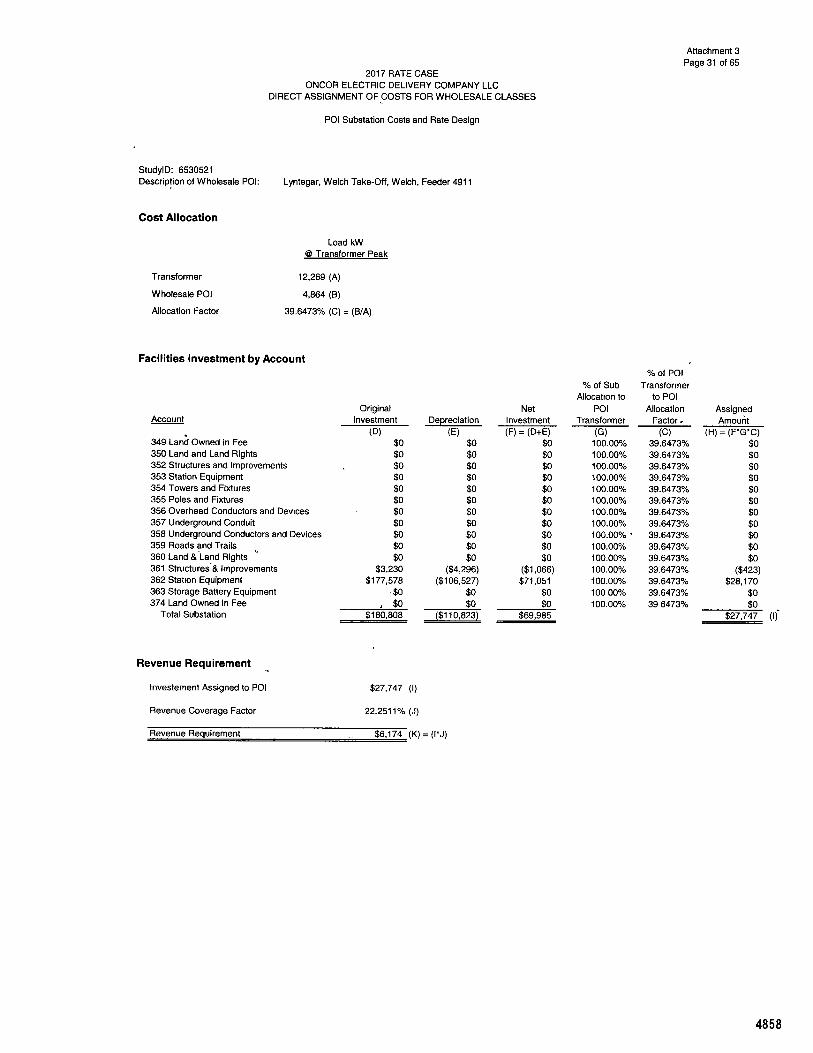

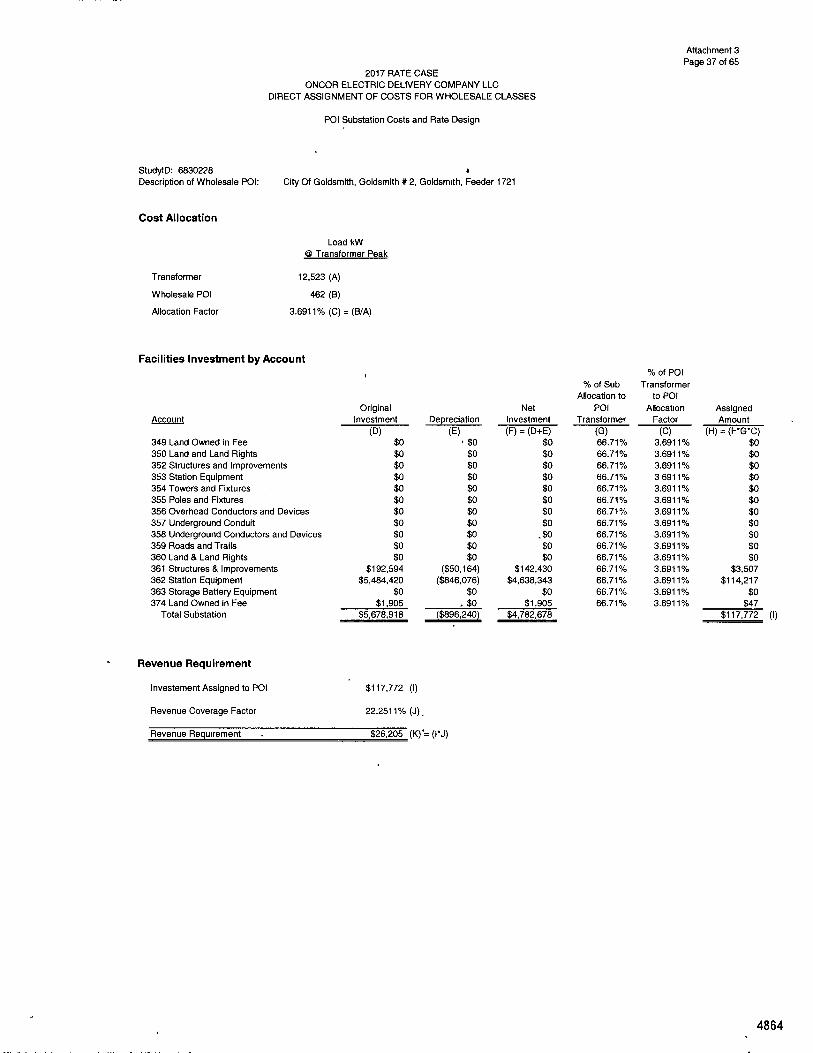

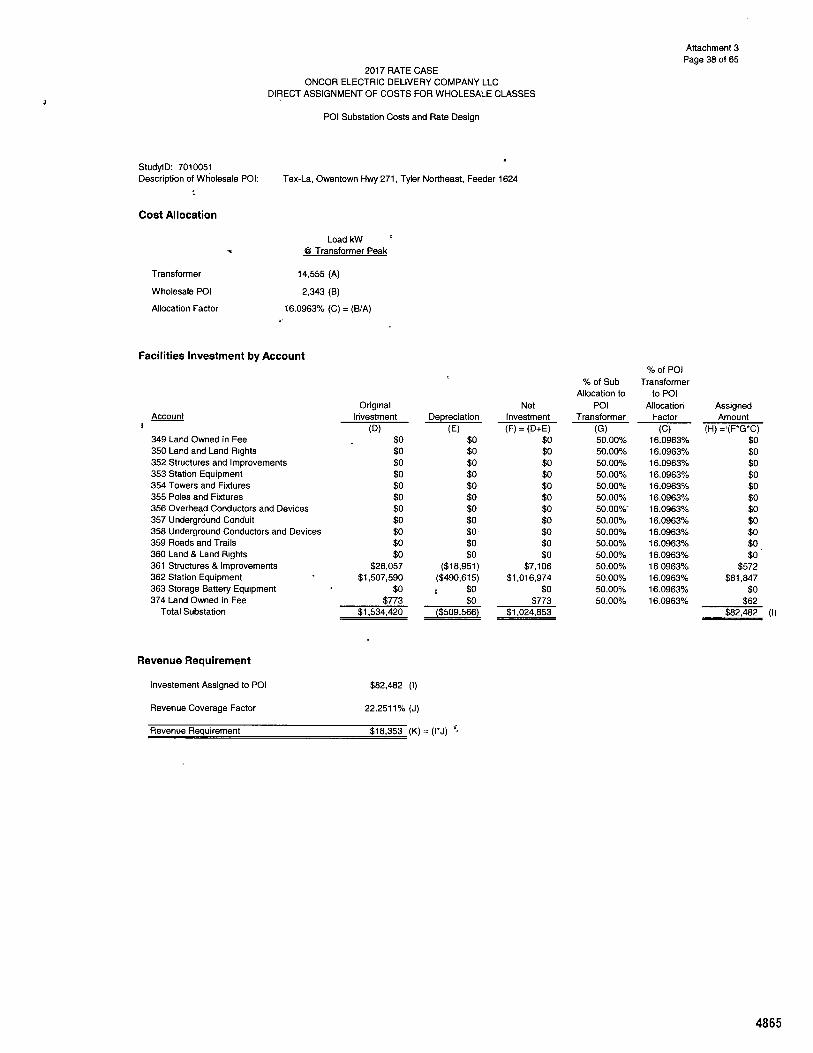

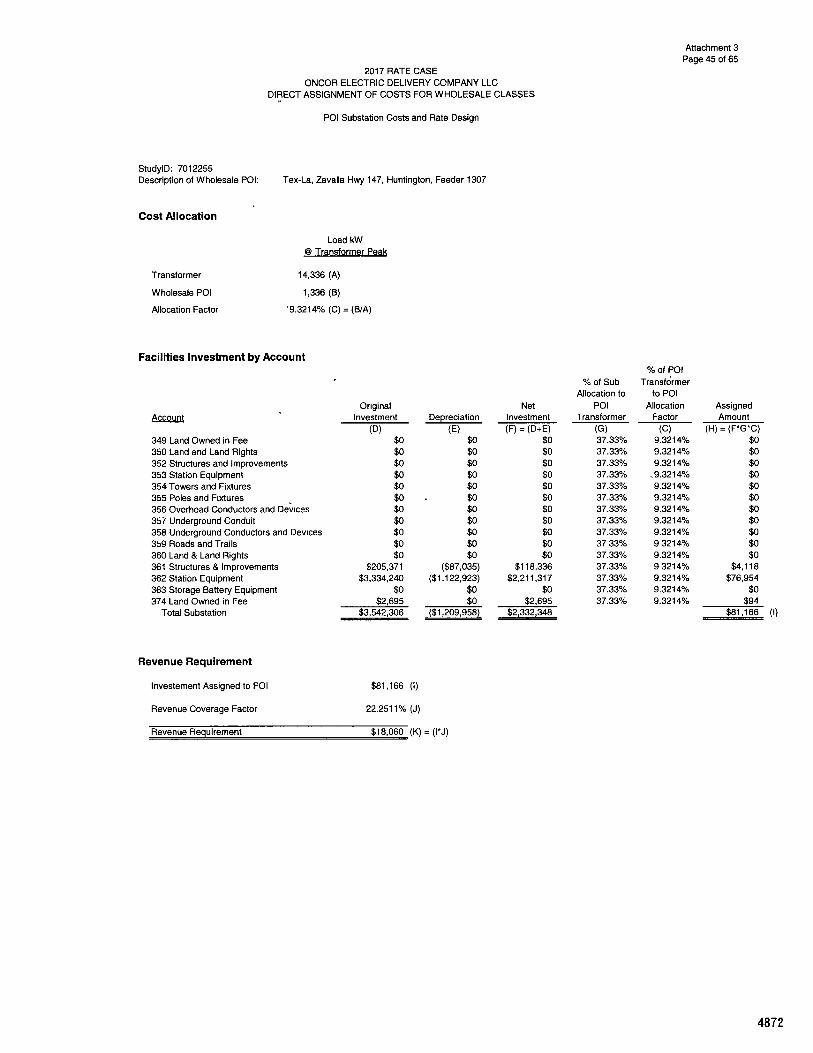

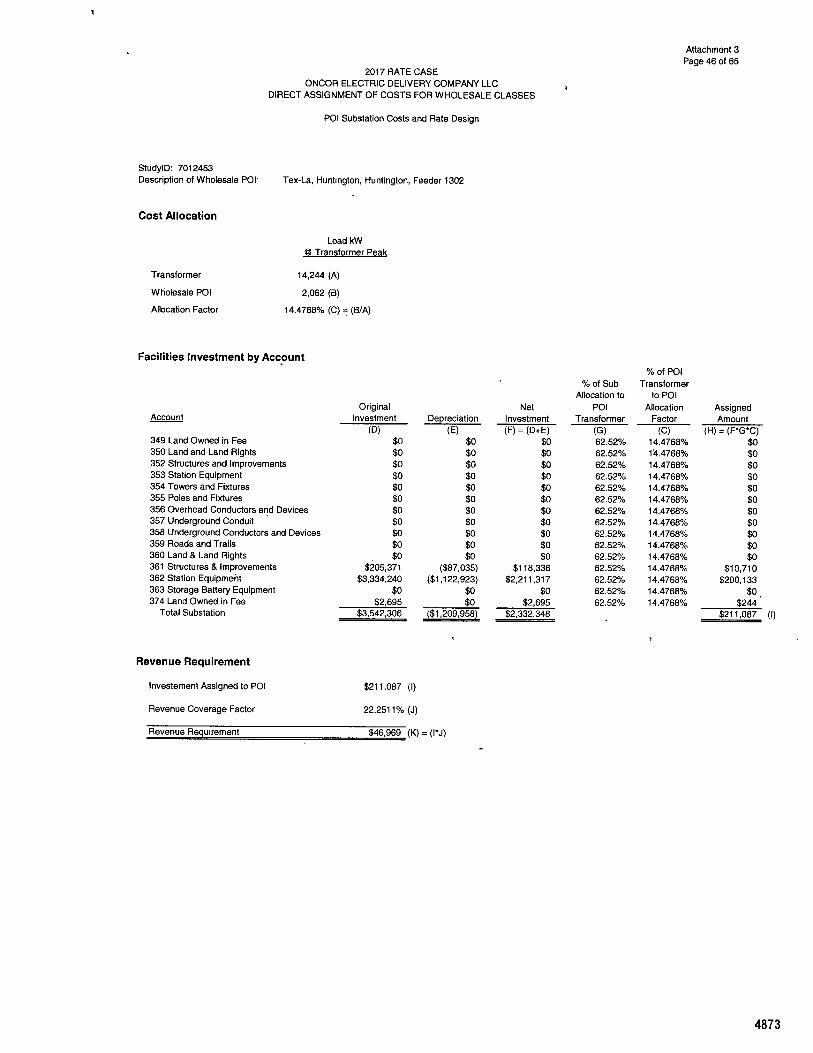

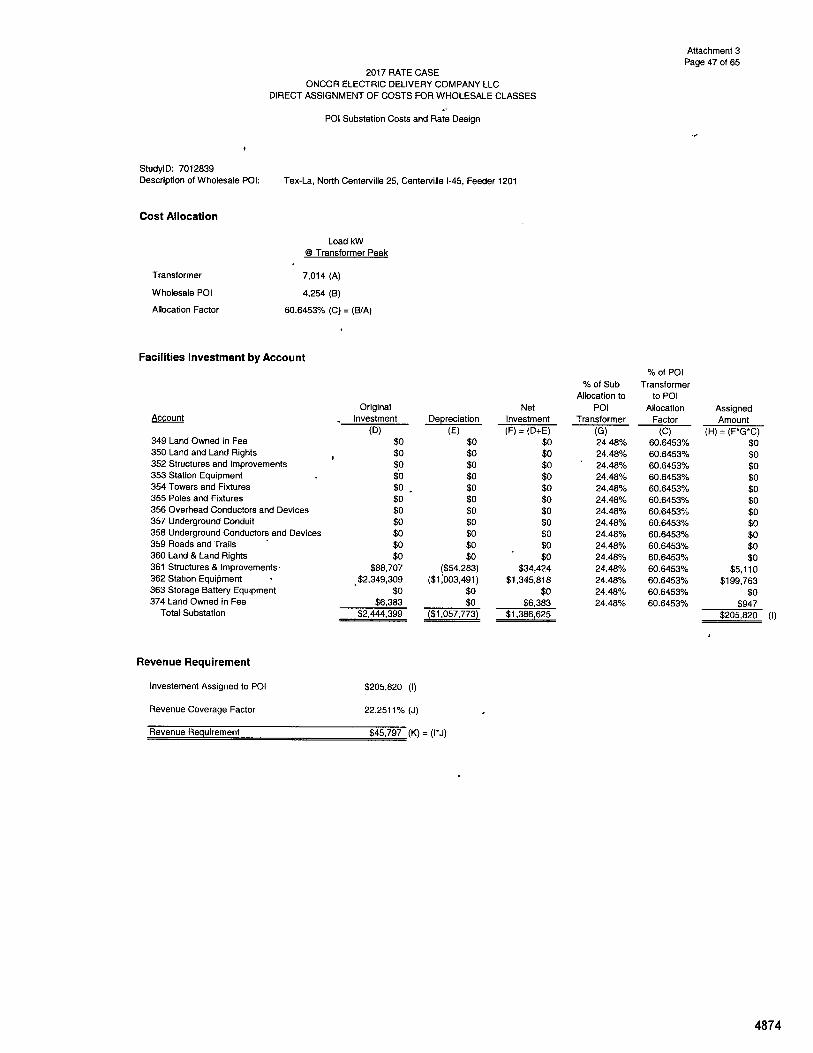

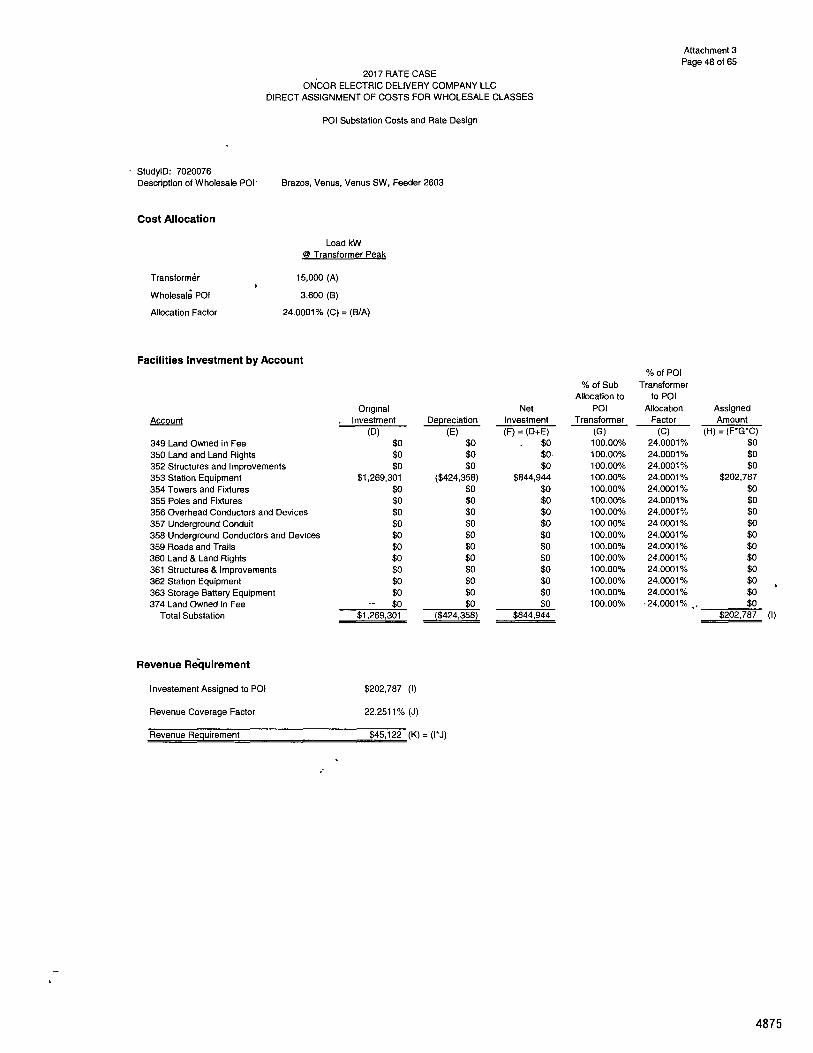

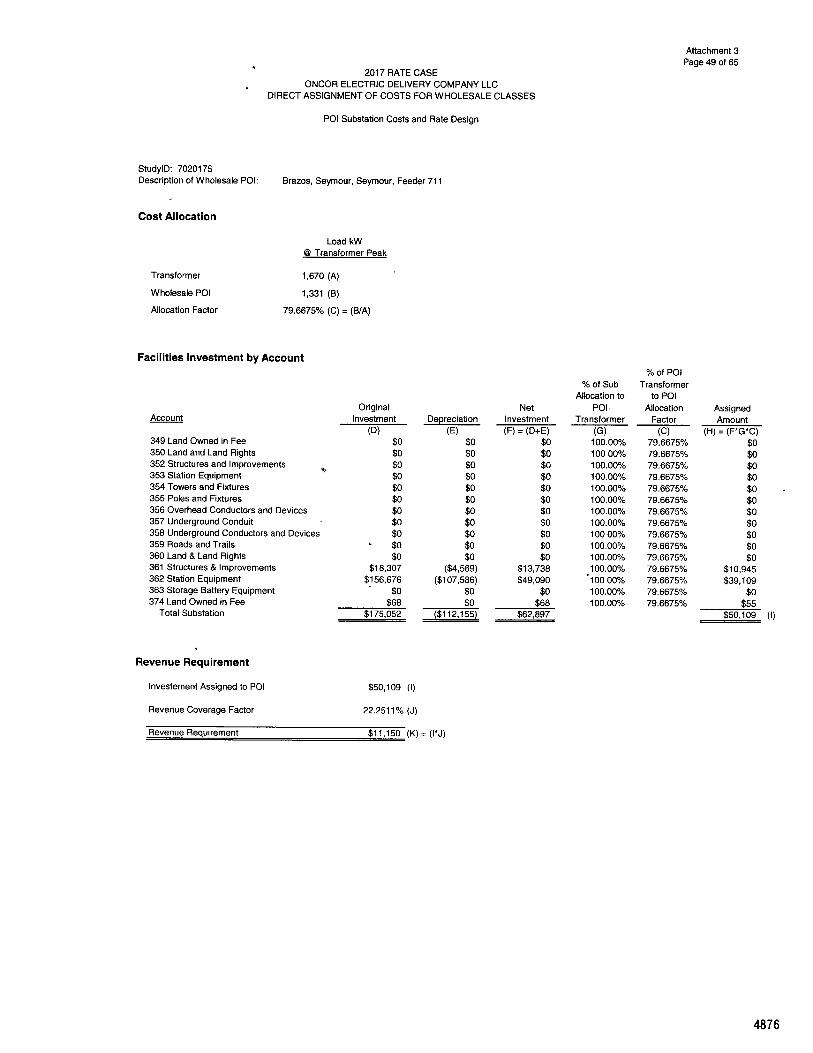

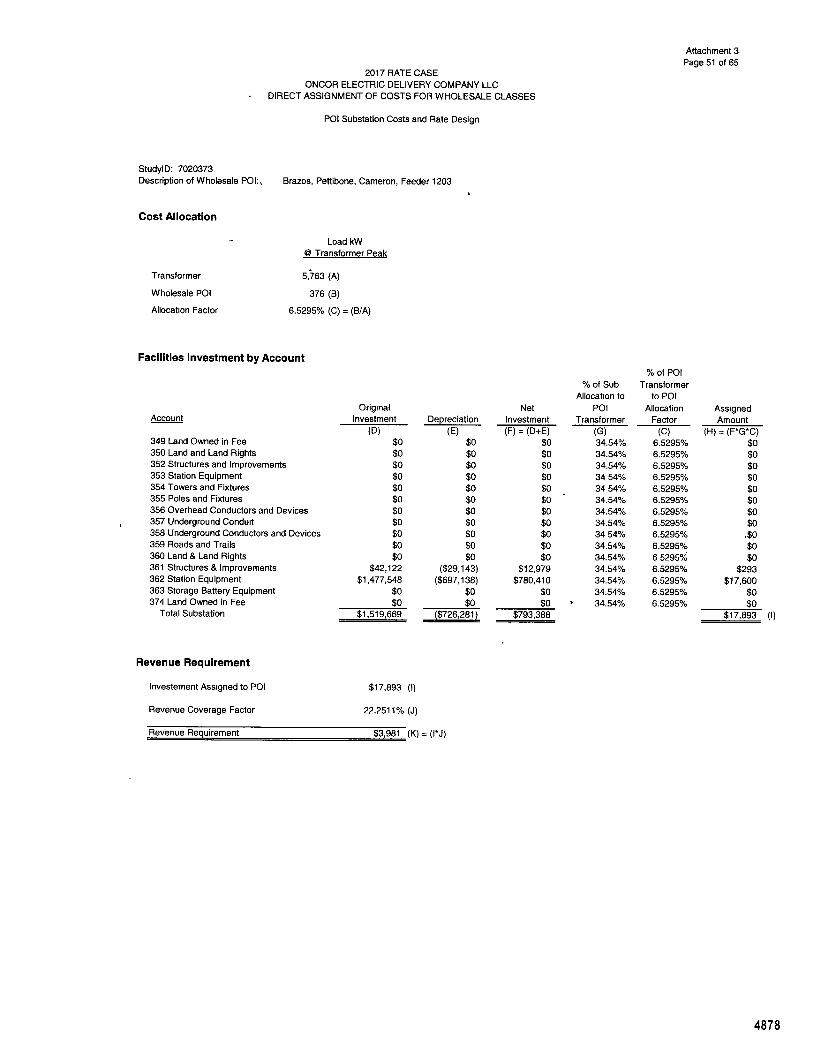

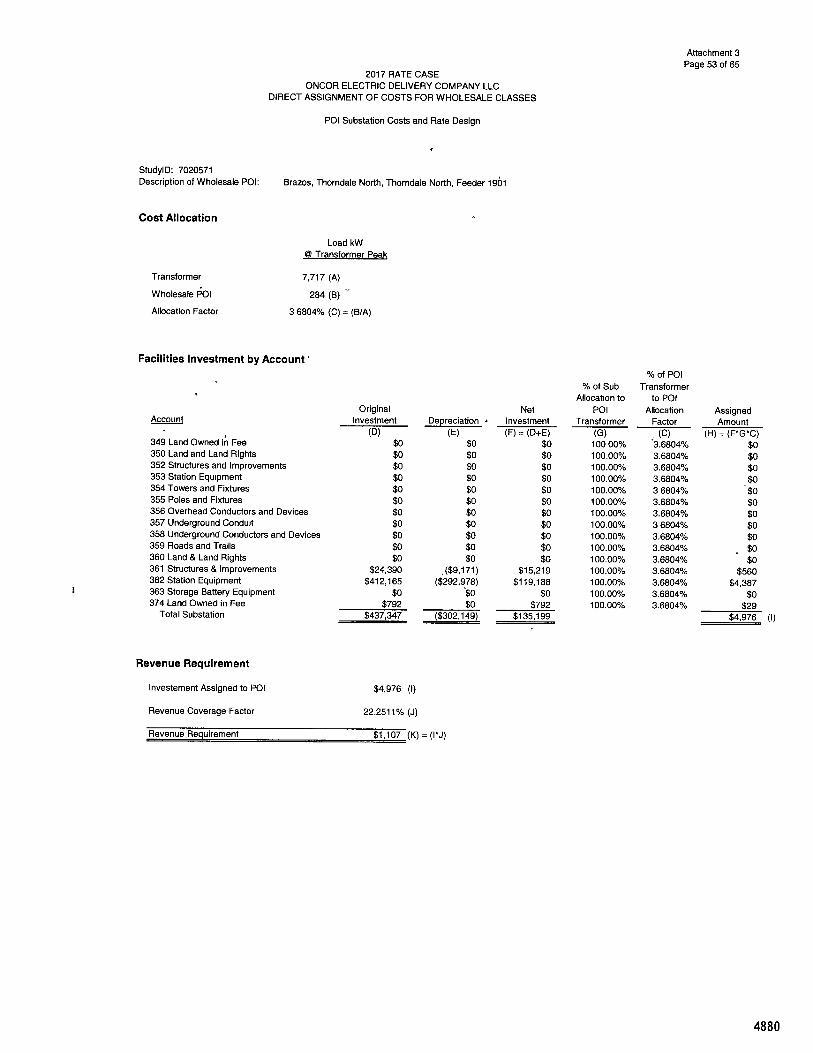

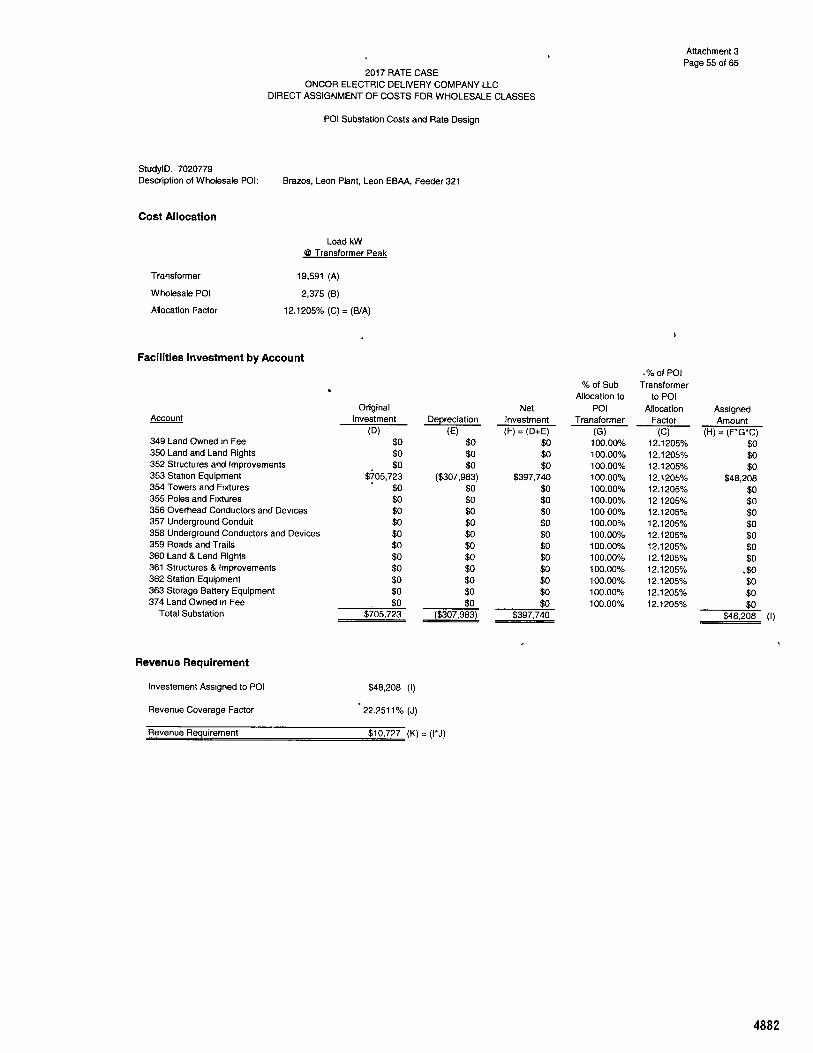

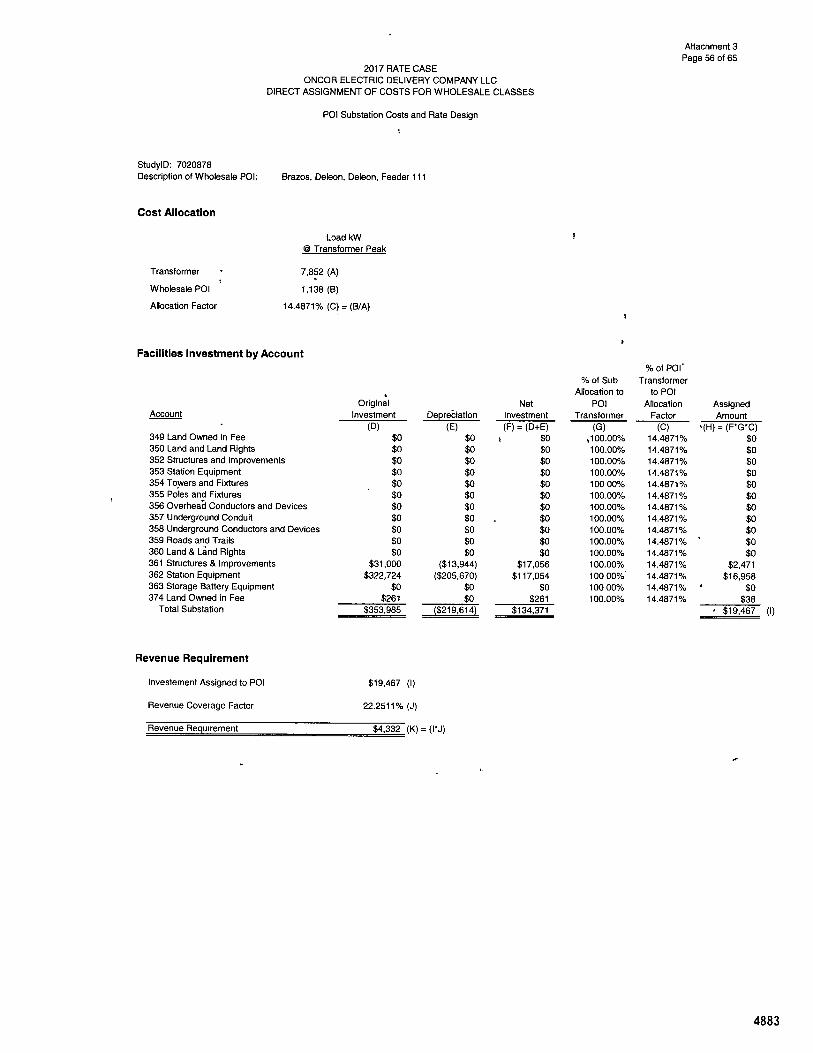

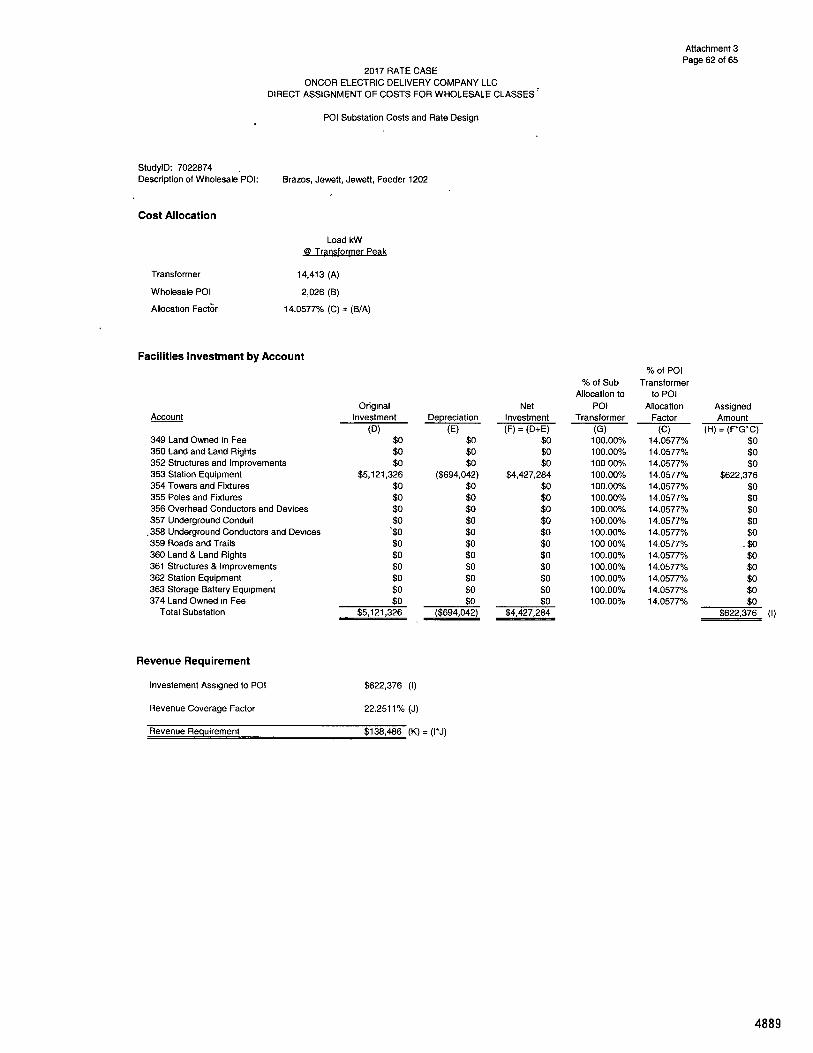

Attachment 3 Page 1 of 65

2017 RATE CASE ONCOR ELECTRIC DELIVERY COMPANY LLC

DIRECT ASSIGNMENT OF COSTS FOR WHOLESALE CLASSES

POI Substation Costs and Rate Design

StudylD: 6220735 Description of Wholesale POI: Rayburn, Cooper Highway, Sulphur Springs East, Feeder 1402

Cost Allocation

Load kW CO Transformer Peak

Transformer 22,818 (A)

Wholesale POI 5,668 (B)

Allocation Factor 24.8404% (C) = (B/A)

Facilities Investment by Account % of POI

% of Sub Transformer Allocation to to POI

Original Net POI Allocation Assigned Account Investment Depreciation Investment Transformer Factor Amount

(D) (E) (F) = (D+E) (G) (C) (H) = (F*G*C) 349 Land Owned in Fee $0 $0 $0 100.00% 24.8404% $0 350 Land and Land Rights $0 $0 $0 100.00% 24.8404% $0 352 Structures and Improvements $0 $0 $0 100.00% 24.8404% $0 353 Station Equipment $0 $0 $0 100.00% 24.8404% $0 354 Towers and Fixtures $0 $0 $0 100.00% 24.8404% $0 355 Poles and Fixtures $0 $0 $0 100.00% 24.8404% $0 356 Overhead Conductors and Devices $0 $0 $0 100.00% 24.8404% $0 357 Underground Conduit $0 $0 $0 100 00% 24.8404% $o 358 Underground Conductors and Devices $0 $0 $0 100.00% 24.8404% $0 359 Roads and Trails $0 $0 $0 100.00% 24.8404% $0 360 Land & Land Rights $0 $0 $0 100.00% 24.8404% $0 361 Structures & Improvements $20,633 ($23,471) ($3,338) 100.00% 24.8404% ($829) 362 Station Equipment $501,879 ($217,970) $283,909 100.00% 24.8404% $70,524 363 Storage Battery Equipment $o - $o $0 100.00% 24.8404% $0 374 Land Owned in Fee $758 $0 $758 100.00% 24 8404% $188

Total Substation $523,270 ($241,941) $281,329 $69,883 (I)

Revenue Requirement

Investement Assigned to POI - $69,883 (I)

Revenue Coverage Factor

22.2511% (J)

Revenue Requirement $15,550 (K) = (I*J)

4828

Attachment 3

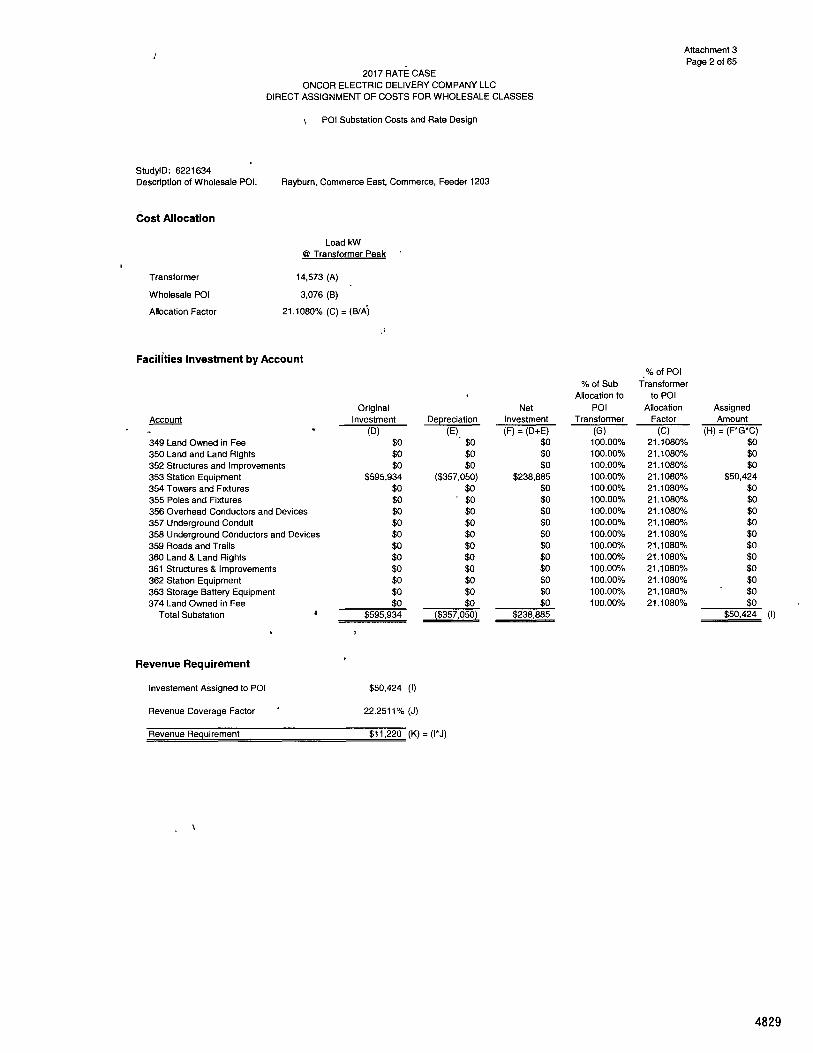

2017 RATE CASE Page 2 of 65

ONCOR ELECTRIC DELIVERY COMPANY LLC DIRECT ASSIGNMENT OF COSTS FOR WHOLESALE CLASSES

% POI Substation Costs and Rate Design

StudyID: 6221634 Description of Wholesale POI: Rayburn, Commerce East, Commerce, Feeder 1203

Cost Allocation

Load kW @ Transformer Peak '

Transformer 14,573 (A)

Wholesale POI 3,076 (B)

Allocation Factor 21.1080% (C) = (B/k)

Facilities Investment by Account .% of POI

% of Sub Transformer Allocation to to POI

Original Net POI Allocation Assigned Account Investment Depreciation Investment Transformer Factor Amount

(D) (E) (F) = (D+E) (G) (C) (H) = (PG*C) 349 Land Owned in Fee $0 ' $0 $0 100.00% 21.1080% $0 350 Land and Land Rights $0 $0 $0 100.00% 21.1080% $0 352 Structures and Improvements $0 $0 $0 100.00% 21.1080% $0 353 Station Equipment $595,934 ($357,050) $238,885 100.00% 21.1080% $50,424 354 Towers and Fixtures $0 $0 $0 100.00%0 21.1080% $0 355 Poles and Fixtures $0 $0 $0 100.00% 21.1080% $0 356 Overhead Conductors and Devices $0 $0 $0 100.00% 21.1080% $0 357 Underground Conduit $0 $0 $0 100.00% 21.1080% $0 358 Underground Conductors and Devices $0 $0 $0 100.00% 21.1080% $0 359 Roads and Trails $0 $0 $0 100.00% 21.1080% $o 360 Land & Land Rights $0 $0 $0 100.00% 21.1080% $0 361 Structures & Improvements $0 $0 $0 100.00% 21.1080% $0 362 Station Equipment $0 $0 $0 100.00% 21.1080% $0 363 Storage Battery Equipment $0 $0 $0 100.00% 21.1080% $0 374 Land Owned in Fee $0 $0 $0 100.00% 21.1080% $o

Total Substation $595,934 ($357,050) $238,885 $50,424 (I)

Revenue Requirement

Investement Ašsigned to POI $50,424 (I)

Revenue Coverage Factor 22.2511% (J)

Revenue Requirement $11,220 (K) = (I*J)

4829

Attachment 3 Page 3 of 65

2017 RATE CASE ONCOR ELECTRIC DELIVERY COMPANY LLC

DIRECT ASSIGNMENT OF COSTS FOR WHOLESALE CLASSES

POI Substation Costs and Rate Design

StudylD: 6221733 Description of Wholesale P01: Rayburn, Commerce West, Commerce South, Feeder 1405'

Cost Allocation

Load kW @ Transformer Peak

Transformer 16,325 (A)

Wholesale POI 463 (B)

Allocation Factor 2.8367% (C) = (B/A)

Facilities Investment by Account % of POI

% of Sub Transformer Allocation to to P01

Original Net POI Allocation Assigned Account • Investment ..12.2En Investment Transformer Factor Amount

(D) (E) (F) = (D+E) (G) (C) (H) = (F*G*C) 349 Land Owned in Fee $0 $0 $0 47.17% 2.8367% $0 350 Land and Land Rights $0 $0' $0 47.17% 2.8367% $0 352 Structures and Improvements $0 $0 $0 47 17% 2.8367% $0 353 Station Equipment $0 $0 $0 47.17% 2.8367% $0 354 Towers and Fixtures $0 $0 $0 47.17% 2.8367% $0 355 Poles and Fixtures $0 $0 i $0 47.17% 2.8367% $0 356 Overhead Conductors and Devices $0 $0 $0 47.17% 2.8367% $0 357 Underground Conduit $0 $0 $0 47.17% 2.8367% $0 358 Underground Conductors and Devices $0 $0 $0 47.17% 2.8367% $0 359 Roads and Trails $0 $0i $0 47.17% 2.8367% $0 360 Land & Land Rights $0 $0 $0 47 17% 2.8367% $0 361 Structures & Improvements $137,037 ($23,609) $113,429 47.17% 2.8367% $1,518 362 Station Equipment $1,332,822 ($380,986) $951,837 47.17% 2.8367% $12,736 363 Storage Battery Equipment $0 $0 $0 47.17% 2.8367% , $0 374 Land Owned in Fee $6,585 $0 $6,585 47.17% 2.8367% $88

Total Substation $1,476,444 ($404,594) $1,071,850 $14,342 (I)

Revenue Requirement

Investement Assigned to POI $14,342 (I)

Revenue Coverage Factor 22.2511% (J)

Revenue Requirement $3,191 (K) = (I*J)

4830

Attachment 3 Page 4 of 65

2017 RATE CASE ONCOR ELECTRIC DELIVERY COMPANY LLC

DIRECT ASSIGNMENT OF COSTS FOR WHOLESALE CLASSES

POI Substation Costs and Rate Design

StudylD: 6222533 Description otWholeiale POI: Rayburn, Mesquite Valley, Mesquite, Feeder 1305

Cost Allocation

Load kW @ Transformer Peak

Transformer 31,762 (A)

Wholesale POI 60 (B)

Allocation Factor 0.1889% (C) = (B/A)

Facilities investment by Account % of POI

% of Sub Allocation to

Transformer to POI

Original Net POI Allocation Assigned Account Investment Depreciation Investment Transformer Factor Amount

(D) (E) (F) = (D+E) (G) (C) (H) = (F*G*C) 349 Land Owned in Fee $0 $0 $0 50.00% 0.1889% $0 350 Land and Land Rights $0 $0 $0 50.00% 0.1689% $0 352 Structures and Improvements $0 $0 $0 50.00% 0.1889% $0 353 Station Equipment $0 $0 $0 50.00% 0.1889% $0 354 Towers and Fixtures $0 $0 $0 50.00% 0.1889% $0 355 Poles and Fixtures $0 $0 $0 50.00% 0.1889% $0 356 Overhead Conductors and Devices $0 $0 $0 50.00% 0.1889% $0 357 Underground Conduit $0 $0 $0 50.00% 0.1889% $0 358 Underground Conductors and Devices $0 $0 $0 50.00% 0.1889% $0 359 Roads and Trails $0 $0 $0 ' 50.00% 0.1889% $0 360 Land & Land Rights $0 $0 $0 50.00% 0.1889% $0 361 Structures & Improvements $141,244 ($78,622) $62,622 ' 50.00% 0.1889% $59 362 Station Equipment $2,225,032 ($972,938) $1,252,094 , 50.00% 0.1889% $1,183 363 Storige Battery Equipment $0 $0 $0 50.00% 0.1889% $0 374 Land Owned in Fee $1,675 $0 $1,675 50.00% 0.1889% $2

Total Substation $2,367,950 ($1,051,560) $1,316,391 $1,243 (I)

Revenue Requirement

Investement Assigned to POI $1,243 (I)

Revenue Coverage Factor 22.2511% (J)

Revenue Requirement $277 (K) = (I*J)

4831

Attachment 3 Page 5 of 65

2017 RATE CASE ONCOR ELECTRIC DELIVERY COMPANY LLC

DIRECT ASSIGNMENT OF COSTS FOR WHOLESALE CLASSES

POI Substation Costs and Rate Design

StudylD: 6223099 ' Description of Wholesale POI: Rayburn, Chiesa Road, Da!rock, Feeder 1326

Cost Allocation

Load kW @ Transformer Peak

Transformer 17,801 (A)

Wholesale POI 136 (B)

Allocation Factor 0.7640% (C) = (B/A)

Facilities Investment by Account % of POI

% of Sub Allocation to

Transformer to POI

Original Net POI Allocation Assigned Account Investment Depreciation Investment Transformer Factor Amount