On My Radar: Blood in the Streets, Indeed February 21, 2017 by Steve Blumenthal of CMG Capital Management Group “Perhaps the biggest risk facing investors this year and beyond is whether bond yields will suffer a sustained rise. We are increasingly worried that the bond market is undergoing a secular pivot from bullish to bearish, and that investors are facing an asymmetric risk profile with limited upside and plenty of downside.” – Ned Davis Research, Featured Report (February 9, 2017) Page 1, ©2018 Advisor Perspectives, Inc. All rights reserved.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

On My Radar: Blood in the Streets, IndeedFebruary 21, 2017

by Steve Blumenthalof CMG Capital Management Group

“Perhaps the biggest risk facing investors this year and beyond is whether bond yieldswill suffer a sustained rise.

We are increasingly worried that the bond market is undergoing a secular pivot frombullish to bearish, and that investors are facing an asymmetric risk profile with limitedupside and plenty of downside.”

– Ned Davis Research, Featured Report (February 9, 2017)

Page 1, ©2018 Advisor Perspectives, Inc. All rights reserved.

Hat tip to my friends at 361 Capital for the photo.

We sipped the QE juice and loved the taste. Now we’re full… the game has changed. The Fed hadassets worth $858 billion on its books in the week ended August 1, 2007 just before the start of thefinancial crisis, and the same stood at $2.24 trillion at the end of 2009. It stands at a surreal $4.5trillion today. The Fed printed and bought $1.7 trillion in mortgage bonds and they bought governmentbonds. (See Understanding the Federal Reserve Balance Sheet.)

Slowdown, taper, reverse?

I believe we are facing a secular pivot in bonds. After 35 years of one of the greatest bull markets thatsent rates from the mid-teens to near zero, it’s endgame. I’m pretty sure more than a few investors areunaware of the risk this poses. Inflation eats into returns and who wants to buy from your client that2.4% yielding piece of paper when they can get 4%, 5% or 6%.

And speaking of 6%, it just might be here in a few short years.

Bloomberg wrote a piece this week entitled, “Everyone is Suddenly Worried about this U.S. Mortgage-Bond Whale.” A few highlights:

Page 2, ©2018 Advisor Perspectives, Inc. All rights reserved.

Almost a decade after it all began, the Federal Reserve is finally talking about unwinding its grandexperiment in monetary policy. And when it happens, the knock-on effects in the bond marketcould pose a threat to the U.S. housing recovery.The talk has prompted some on Wall Street to suggest the Fed will start its drawdown as soon asthis year, which has refocused attention on its $1.75 trillion stash of mortgage-backed securities.While the Fed also owns Treasuries as part of its $4.45 trillion of assets, its MBS holdings havelong been a contentious issue, with some lawmakers criticizing the investments as beyond what’sneeded to achieve the central bank’s mandate.Yet, because the Fed is now the biggest source of demand for U.S. government-backedmortgage debt and owns a third of the market, any move is likely to boost costs for home buyers.In the past year alone, the Fed bought $387 billion of mortgage bonds just to maintain itsholdings. Getting out of the bond-buying business as the economy strengthens could help lift 30-year mortgage rates past 6 percent within three years, according to Moody’s Analytics Inc.(emphasis mine)

Source: Bloomberg

The bottom line for bond investors is this: When interest rates rise, bonds lose value. I shared the nextchart in July 2016 (interestingly just two days from the 1.37% low in yields). It shows how much moneyis lost for every 1% increase in rates. The top section is the 10-year Treasury. The bottom is the 30-year Treasury. As a quick aside, I know I’ve shared this chart with you several times, but I believe it isworth revisiting. I just don’t believe the average investor knows just how much risk they are taking onwith their so called “safe” investments.

Page 3, ©2018 Advisor Perspectives, Inc. All rights reserved.

1.37% was the low yield back on July 13, 2016. The 10-year Treasury is currently yielding 2.42% andthe 30-year is yielding 3.02%. That adds up to a -8.84% loss in value for the 10-year and call it a -16%for the 30-year. Maybe rates move back down, but I’m not so sure. I’m a bit more worried about whatthose losses will look like when yields rise to 3.4%, 4.4% and 5.4% (similar to where they were in2007). -30% is a real risk.

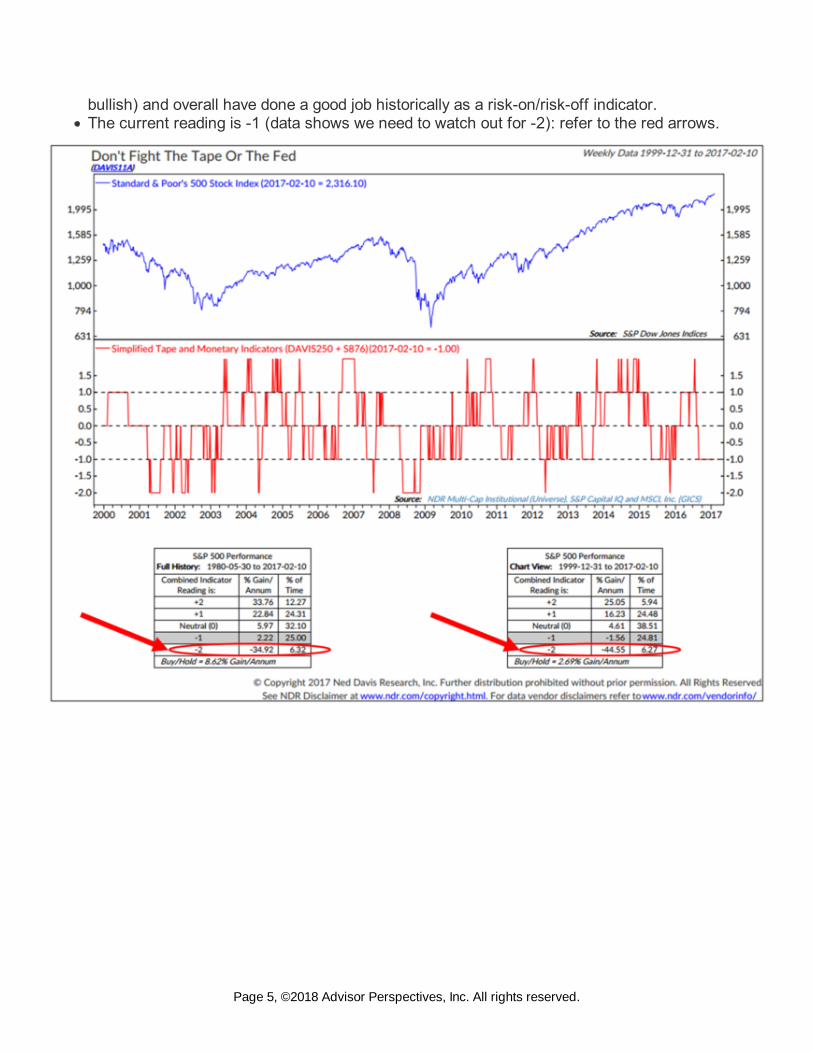

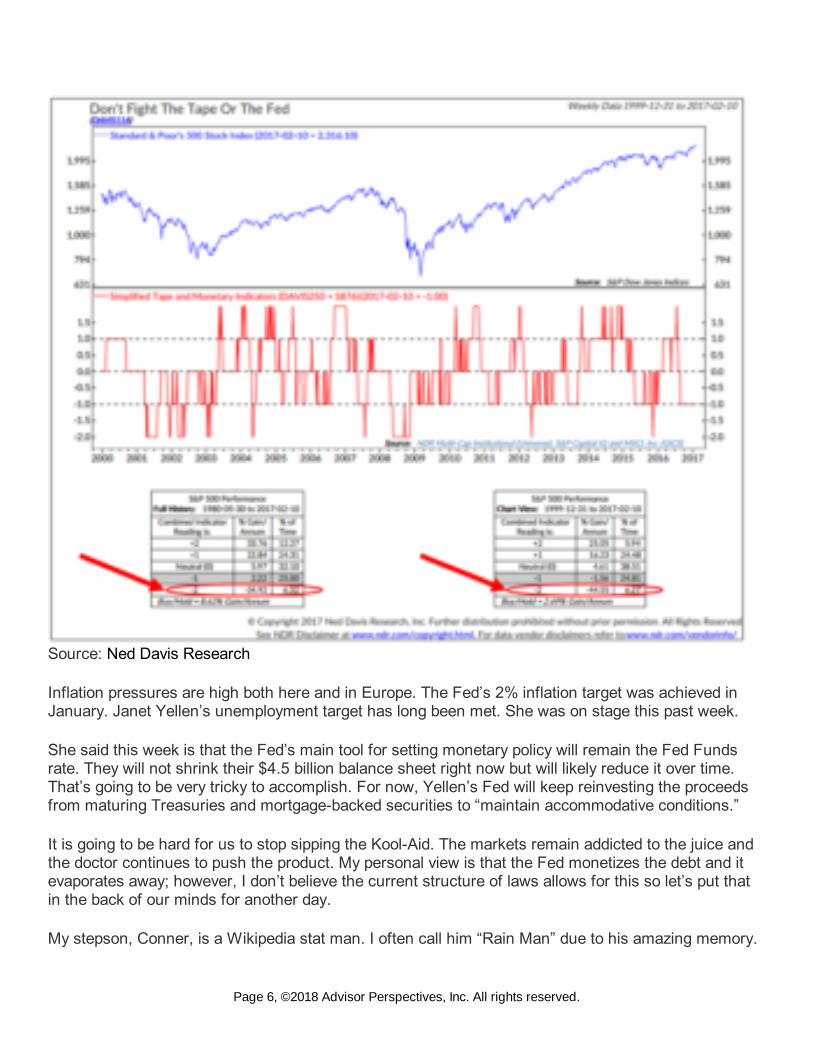

As for equities, the number one rule many of us were taught is “Don’t Fight the Fed.” I like to add“trend” into that equation and, as you’ll see in the next chart, the math is compelling.

When the Fed raises rates (don’t fight them) and the trend turns negative, equities underperform.Focus on the red arrows. Two different time periods are measured, however, the message is thesame. The big corrections come when both the Fed and trend turn negative. I wrote some time ago inOMR to “watch out for minus 2.” We currently sit at -1. I’ll share this chart from time to time –especially if -2 is triggered.

Here is how you read the chart:

The top section plots the S&P 500 Index but focus on the middle section.NDR has a Multi-Cap Tape Composite Model to measure the technical health of the broad equitymarket. That model aggregates the signals of over 100 component indicators and generates asignal based on the percentage of the component indicators that are giving a bullish signal for theS&P 500. It measures momentum and trend.The Fed component is really an interest rate component, which measures the trend in rates bylooking at the yield on the 10-year Treasury note. When the 10-week trend in yields are lowerthan their 70-week trend in yields, the S&P 500 has produced larger gains. When it is higher, theS&P 500 has performed poorly. It’s that simple.The combined indicator can produce a score of -2 (both indicators are bearish) to +2 (both

Page 4, ©2018 Advisor Perspectives, Inc. All rights reserved.

bullish) and overall have done a good job historically as a risk-on/risk-off indicator.The current reading is -1 (data shows we need to watch out for -2): refer to the red arrows.

Page 5, ©2018 Advisor Perspectives, Inc. All rights reserved.

Source: Ned Davis Research

Inflation pressures are high both here and in Europe. The Fed’s 2% inflation target was achieved inJanuary. Janet Yellen’s unemployment target has long been met. She was on stage this past week.

She said this week is that the Fed’s main tool for setting monetary policy will remain the Fed Fundsrate. They will not shrink their $4.5 billion balance sheet right now but will likely reduce it over time.That’s going to be very tricky to accomplish. For now, Yellen’s Fed will keep reinvesting the proceedsfrom maturing Treasuries and mortgage-backed securities to “maintain accommodative conditions.”

It is going to be hard for us to stop sipping the Kool-Aid. The markets remain addicted to the juice andthe doctor continues to push the product. My personal view is that the Fed monetizes the debt and itevaporates away; however, I don’t believe the current structure of laws allows for this so let’s put thatin the back of our minds for another day.

My stepson, Conner, is a Wikipedia stat man. I often call him “Rain Man” due to his amazing memory.

Page 6, ©2018 Advisor Perspectives, Inc. All rights reserved.

I wish I had his quick recall. Anyway, on the way to school this morning, we were talking about thestock market (he owns Bristol-Myers Squibb and he’s happy with the move of late).

Out of nowhere Conner said, “The time to buy is when there’s blood in the streets.” He’s fascinatedwith the stories behind some of the world’s wealthiest people and he went on to tell me about BaronRothschild, the 18 century banker that made a fortune buying in the panic that followed the Battle ofWaterloo against Napoleon. “Blood in the streets” is one of Rothschild’s famous quotes. It seemedapropos for today.

I’m keeping one eye on the Fed, the other on trend and mentally preparing myself for a BaronRothschild – Sir John Templeton like moment. It’s not now! I told Conner the buying opportunity of hislifetime is coming.

That potential remains ahead. Blood in the streets? The end of the great debt super cycle? Probable inmy view. Three to five years? Maybe sooner? Don’t know. As the great Stan Druckenmiller commenteda few years ago… Fed policy is, “fraught with unappreciated risk.”

And about the Fed… if you ever wanted to get a candid behind the curtain view of what we are dealingwith inside the Fed, grab a coffee and I encourage you to go to your favorite book store and buy thejust released book, Fed Up: An Insider’s Take on Why the Federal Reserve Is Bad for Americaby former Fed insider, Danielle DiMartino Booth. Below you’ll find a short summary. It’s an insider’scandid no-holds-barred, highly critical look at the Fed.

The book is outstanding… “Blood in the streets” – indeed.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribehere. ♦

Included in this week’s On My Radar:

Fed Up, by Danielle DiMartino BoothCharts of the Week — InflationTrade Signals – High Inflationary Pressures

Fed Up, by Danielle DiMartino BoothJohn Mauldin shared a post in his weekly Outside the Box this week. I’m going to shamelessly borrowfrom John’s piece: Here are the highlights:

Today’s Outside the Box is a special treat. My good friend and fellow Texan Danielle DiMartinoBooth’s new book, Fed Up: An Insider’s Take on Why the Federal Reserve Is Bad for America,was out officially yesterday, on Valentine’s Day, and already there are dozens of reviews all overthe internet.

th

Page 7, ©2018 Advisor Perspectives, Inc. All rights reserved.

Ten years ago, Danielle left a trading gig on Wall Street to work directly for Dallas Federal ReservePresident Richard Fisher. She helped him gain insights into the economy and aided in crafting hisspeeches and writings. Those of us who knew her knew that she was a gifted writer; and whenFisher resigned and Danielle left the Fed, she started her own website and newsletter; and nowher talent is apparent to many more people. She is the third most followed person on LinkedIn,after less than a year.

And then we come to her book. It’s a simply devastating account of what actually goes on insidethe Federal Reserve. To say she eviscerates that august institution is to be kind. I saw hertreatment of the Fed coming, because Danielle and I have shared many conversations in which wedespaired of the impact the Federal Reserve is having on Main Street. But what do you expectwhen you have a bunch of Ph.D.s who share an economic philosophy and an attitude that letsthem think they know just how to manage the US economy and control the price of the mostvaluable commodity in the world, the interest rate on the US dollar.

That low rates devastate middle-class savers and retirees (as they enrichen Wall Street and thebig banks) seems not to register on the Fed’s cost-benefit analysis scale. I think longtime readerspretty well know how I feel about the Federal Reserve and their policies.

You can go to the Amazon page for Fed Up and read most of the book’s first chapter, but Ipersuaded Danielle to let me take you right to the end of the book and her summary of how theFed should be reorganized. This is a powerful to-do list that I hope every Congressman andSenator will read. It is crucially important that they reorganize this institution that is playing havocwith Main Street. After you read Fed Up, I think you too will be ready to join the movement todemand the restructuring of our central bank. We should remove the Fed’s dual mandate,reinforce its oversight functions, and so forth, while understanding that there is a role for anindependent central bank – just not the role subscribed to by the academics who currently run theFed.

Following is the final chapter and summary of how the Fed should be reorganized:

Culture Shock

“If it were possible to take interest rates into negative territory, I would be voting for that.”Janet Yellen, February 2010

As her fame has grown, Janet Yellen is recognized in restaurants and airports around the world.But her world has narrowed. Because the Fed chairman can so easily move markets with a fewcasual words, Yellen can’t get together regularly and shoot the breeze with businesspeople oranalysts who follow the Fed for a living. She must rely on her instincts, her Keynesian training, andthe MIT Mafia.

“You can’t think about what is happening in the economy constructively, from a policy standpoint,

Page 8, ©2018 Advisor Perspectives, Inc. All rights reserved.

unless you have some theoretical paradigm in mind,” Yellen had told Lemann of the New Yorker in2014.

One of Lemann’s final observations: “The Fed, not the Treasury or the White House or Congress,is now the primary economic policymaker in the United States, and therefore the world.”

But what if Yellen’s theoretical paradigm is dead wrong?

The woman who “did not see and did not appreciate what the risks were with securitization, thecredit rating agencies, the shadow banking system, the SIVs … until it happened” has led usstraight into an abyss.

It’s time to climb out. The Federal Reserve’s leadership must come to grips with its role in creatingthe extraordinary circumstances in which it now finds itself. It must embrace reforms to regain itscredibility.

Even Fedwire finally admitted in August 2016 that the Federal Reserve had lost its mojo, with astory headlined “Years of Fed Missteps Fueled Disillusion with the Economy and Washington.” Inan effort to explain rising extremism in American politics in a series called “The Great Unraveling,”Jon Hilsenrath described a Fed confronting “hardened public skepticism and growing self-doubt.”

Mistakes by the Fed included missing the housing bubble and financial crisis, being “blinded” tothe slowdown in the growth of worker productivity, and failing to anticipate how inflation behaved inregard to the job market. The Fed’s economic projections of GDP and how fast the economy wouldgrow were wrong time and again.

People are starting to wake up. A Gallup poll showed that Americans’ confidence that the Fed wasdoing a “good” or “excellent” job had fallen from 53 percent in September 2003 to 38 percent inNovember 2014. Another poll in April 2016 showed that only 38 percent of Americans had a greatdeal or fair amount of confidence in Yellen, while 35 percent had little or none – a huge shift fromthe early 2000s when 70 percent and higher expressed confidence (however misguided) inGreenspan.

In early 2016, Yellen told an audience in New York that it was too bad the government had leanedso heavily on the Fed while “tax and spending policies were stymied by disagreements betweenCongress and the White House.” Maybe if she hadn’t been throwing money at them, lawmakersmight have gotten their house in order.

“The Federal Reserve is a giant weapon that has no ammunition left,” Fisher told CNBC onJanuary 6, 2016.

The Fed must retool and rearm.

First things first. Congress should release the Fed from the bondage of its dual mandate.

Page 9, ©2018 Advisor Perspectives, Inc. All rights reserved.

A singular focus on maintaining price stability will place the duty of maximizing employment backinto the hands of politicians, making them responsible for shaping fiscal policy that ensuresAmerican businesses enjoy a traditionally competitive landscape in which to build and growbusiness.

The added bonus: shedding the dual mandate will discourage future forays into unconventionalmonetary policy.

Next, the Fed needs to get out of the business of trying to compel people to spend by manipulatinginflation expectations. Not only has it introduced a dangerous addiction to debt among all players inthe economy, it has succeeded in virtually outlawing saving.

Most seniors pine for a return to the beginning of this century when they could get a five-yearjumbo CD with a 5 percent APR, offset by inflation somewhere in the neighborhood of 2 percent.Traditionally, 2 to 3 percentage points above inflation is where that old relic, the fed funds rate,traded. The math worked.

Under ZIRP, only fools save for a rainy day. The floor on overnight rates must be permanentlyraised to at least 2 percent and Fed officials should pledge to never again breach that floor. Notonly will it preserve the functionality of the banking system, it will remind people that saving isgood, indeed a virtue. And that debt always has a price.

Limit the number of academic PhDs at the Fed, not just among the leadership but on the staffs ofthe Board and District Banks. Bring in more actual practitioners – businesspeople who have beenon the receiving end of Fed policy, CEOs and CFOs, people who have been on the hot seat, whohave witnessed the financialization of the country and believe that American companies shouldmake things and provide services, not just move money around.

Governors should be given terms of five years, like District Bank presidents, with term limits tobring in new blood and fresh ideas.

Grant all the District Bank presidents, not just New York’s, a permanent vote on the FOMC. Whyshould Wall Street, not Main Street, dominate the Fed’s decision making?

While we’re at it, let’s redraw the Fed’s geographical map to better reflect America’s economicpowerhouses.

California’s economy alone is the sixth biggest in the world. Add another Fed Bank to the TwelfthDistrict to better represent how the Western states have flourished over the last hundred years.

Why does Missouri have two Fed banks? Minneapolis and Cleveland can be absorbed into theChicago Fed. Do Richmond, Philadelphia, and Boston all need Fed District Banks? Consolidate inrecognition of the fact that it isn’t 1913 anymore.

Slash the Fed’s bloated Research Department. It’s hard to argue that a thousand Fed economists

Page 10, ©2018 Advisor Perspectives, Inc. All rights reserved.

are productive and providing value-added insight when their forecasting skills are no better thanthe flip of a coin and half of their studies cannot be replicated.

Send most of the PhD economists back to academia where they belong. Require the rest to focuson research that benefits the Fed, studying how its policies impact American taxpayers andcitizens. (Did the Fed do any studies about how ZIRP and QE would impact banking andconsumers before it imposed them? No.)

Now take all the money you’ve saved and aim it squarely at Wall Street investment banks intent onalways staying one step ahead of the Fed’s regulatory reach. Hire brilliant people for the Fed’s Sup& Reg departments and pay them market rates. Rest assured this will be ground zero of the nextcrisis.

And mix it up. One of Rosenblum’s students applied for a job at the New York Fed. He came froma blue-collar background, spent seven years in the military, and earned his MBA from SMU on theGI Bill. Smart guy. But he couldn’t get to first base at the New York Fed. They hire people fromYale and Harvard and NYU – people just like themselves. Others need not apply.

Then the top Ivy Leaguers stay for two years and move on to bigger money at Citibank or GoldmanSachs. It’s a tribe that’s been bred over ninety years and slow to change.

But if the culture of extreme deference at the New York Fed (which also exists in District Banks toa lesser degree) is not quashed, regulatory capture will continue with disastrous results. The Fedmust give bank examiners the resources they need to understand the ever-evolving financialinnovations created by Wall Street and back them up when they challenge high-paid bankers wholive to skirt the rules.

Regulators must focus on the big picture as well as nodes of risk. Interconnectedness took downthe economy in 2008, not just the shenanigans of a few rogue banks.

Focus on systemic risk and regulation around the FOMC table. Create a post with equal powerand authority to that of the chair to focus on supervision and regulation. Yellen talks aboutmonetary policy ad nauseam, but when challenged by the press or Congress on regulatory policyshe stumbles and mumbles and does her best doe-in-the-headlights impersonation. Markets needpredictability and transparency when it comes to Fed policy, not guesswork, parsing of the chair’swords, and manipulation of FOMC minutes.

Finally, let nature take its course. Reengage creative destruction. Markets by their nature aresupposed to be volatile. Zero interest rates prevent the natural failures of weak companies,weighing down the economy with overcapacity for generations.

Recessions might have been more frequent, the financial losses greater for some, but if the Fedhad let the economy heal on its own, America would have been stronger in the end and thebedrock of our nation, capitalism, would not have been corrupted.

Page 11, ©2018 Advisor Perspectives, Inc. All rights reserved.

I could never have imagined how my near decade-long journey at the Federal Reserve would playout.

In the beginning, I had been a “risk radar” to benefit myself and those closest to me. I wanted tostay out of debt and make certain that my children had great educations and a foundation offinancial savvy so that they could pursue their versions of the American dream.

But I realize now the stakes are much higher.

We’ve become a nation of haves and have-nots thanks to Fed policies that benefit the wealthiestinvestors, punish the savers and the retired, and put the nation’s balance sheet at risk.

As consumers on the receiving end of Fed policies, we must reform our education system so thatthe American dream can be accessible to everyone. We must campaign for Congress to stophiding behind the Fed’s skirts.

And we must demand that the Fed stop offering excuse after excuse for its failures. Short-terminterest rates must return to some semblance of normality and the Fed’s outrageously swollenbalance sheet must shrink in size. And most of all, the Fed must never follow Europe by takinginterest rates into negative territory.

No more excuses. The Fed’s mandate isn’t to have a perfect world. That only exists in fairy tales,dreams and the Fed’s econometric models.

SB here: I pre-ordered and my copy arrived this week. I’m taking it home and will read it this weekend.Probably with a glass of red wine in hand. I may need it!

Charts of the Week — Inflation

Page 12, ©2018 Advisor Perspectives, Inc. All rights reserved.

Page 13, ©2018 Advisor Perspectives, Inc. All rights reserved.

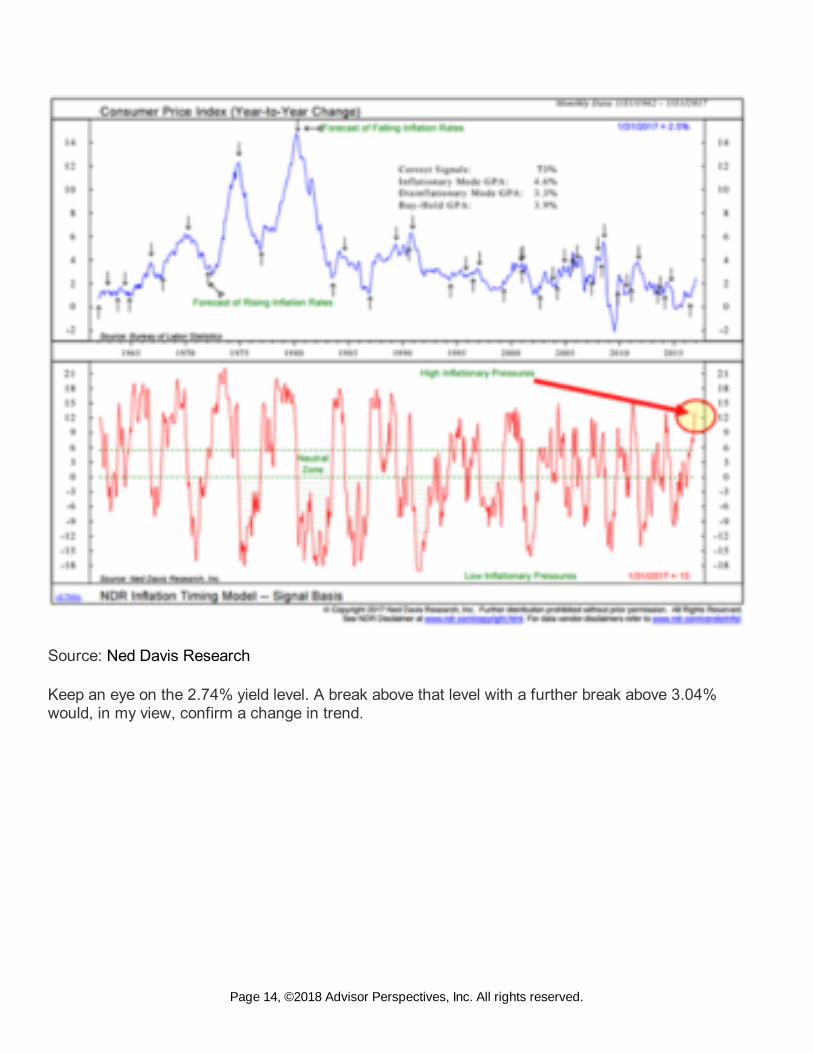

Source: Ned Davis Research

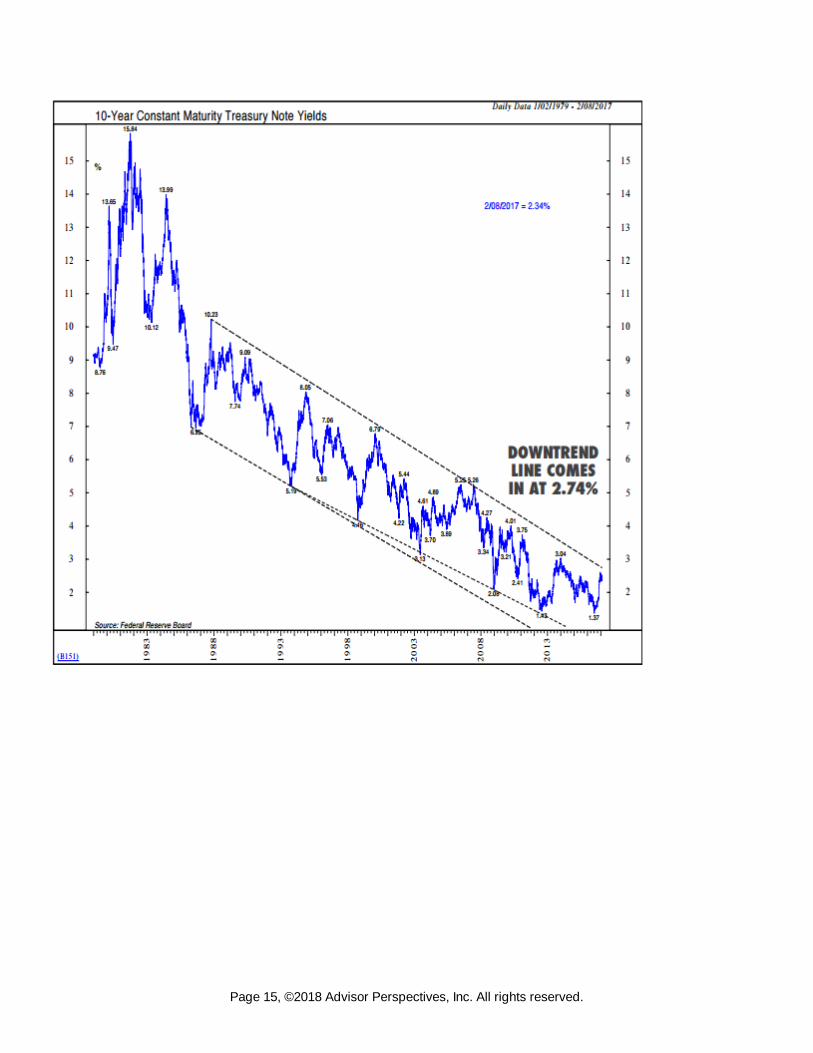

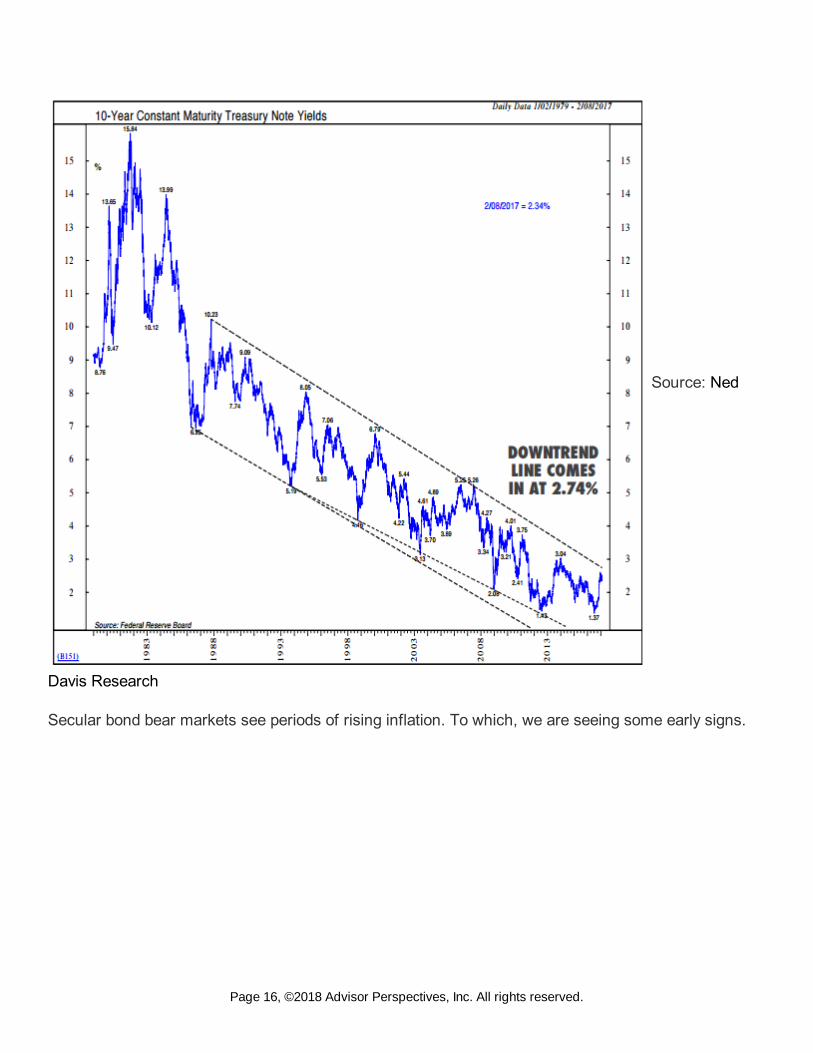

Keep an eye on the 2.74% yield level. A break above that level with a further break above 3.04%would, in my view, confirm a change in trend.

Page 14, ©2018 Advisor Perspectives, Inc. All rights reserved.

Page 15, ©2018 Advisor Perspectives, Inc. All rights reserved.

Source: Ned

Davis Research

Secular bond bear markets see periods of rising inflation. To which, we are seeing some early signs.

Page 16, ©2018 Advisor Perspectives, Inc. All rights reserved.

Page 17, ©2018 Advisor Perspectives, Inc. All rights reserved.

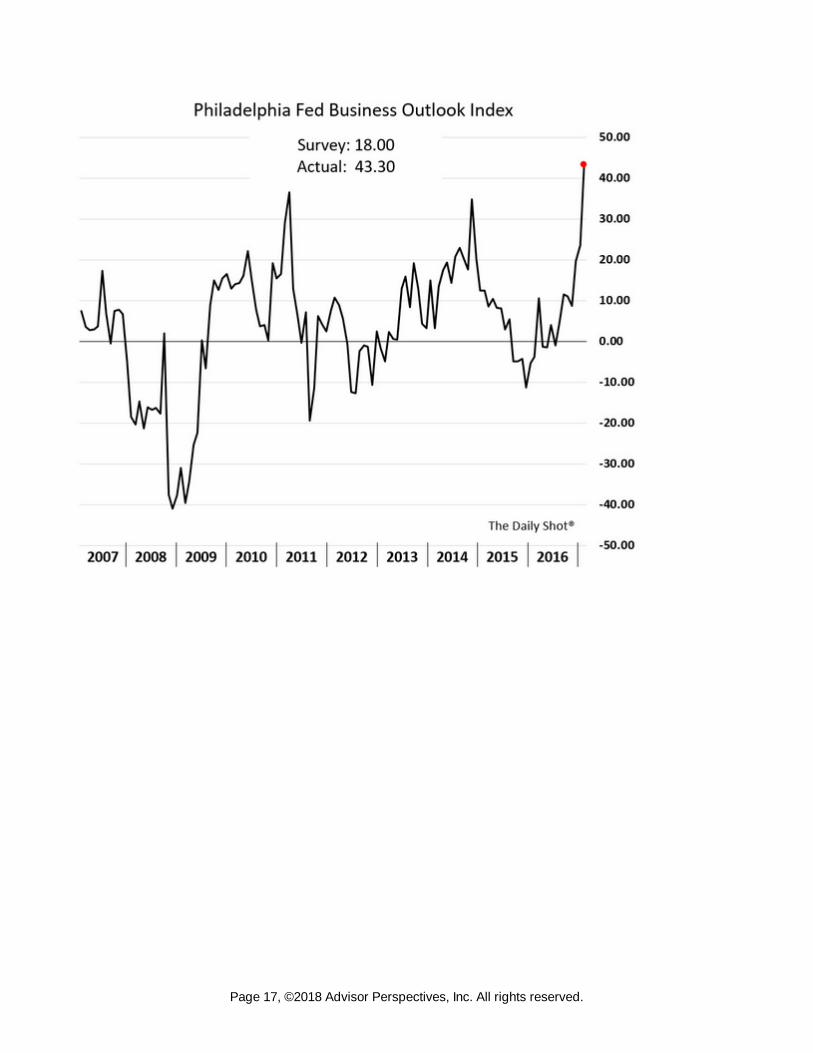

Manufacturers are busy. Note the work hours component is strong.

Page 18, ©2018 Advisor Perspectives, Inc. All rights reserved.

Page 19, ©2018 Advisor Perspectives, Inc. All rights reserved.

Page 20, ©2018 Advisor Perspectives, Inc. All rights reserved.

Page 21, ©2018 Advisor Perspectives, Inc. All rights reserved.

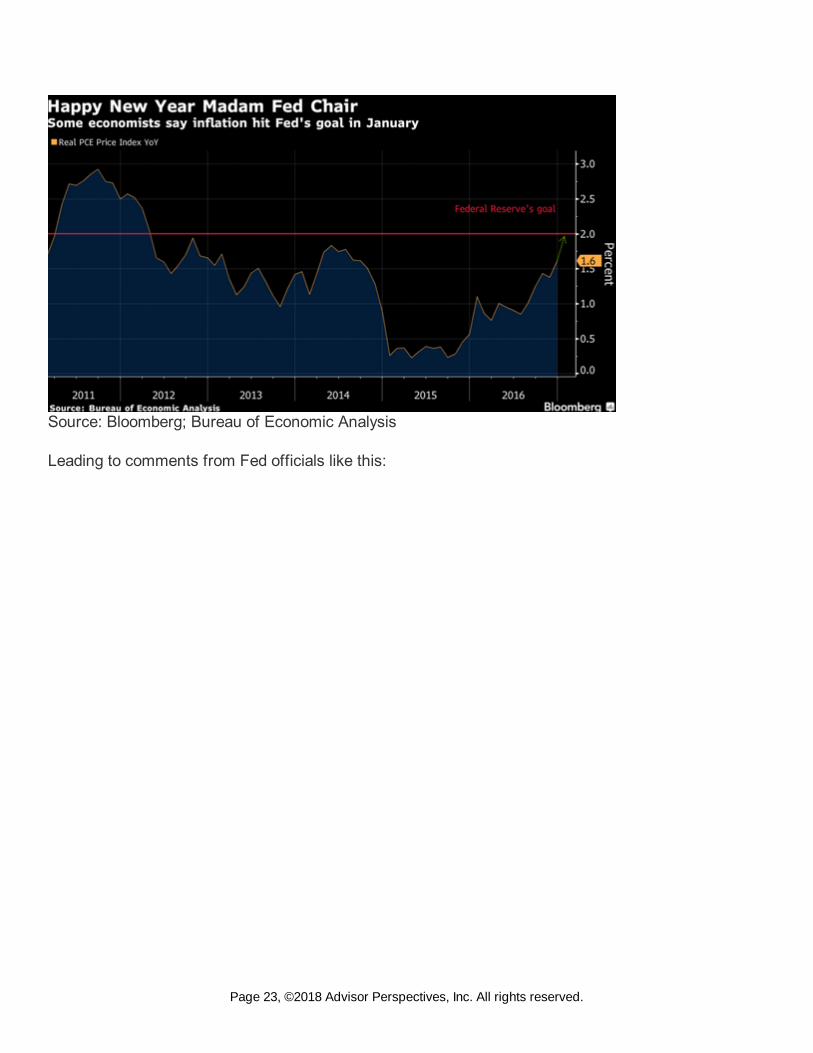

Inflation hit the Fed’s goal of 2% in January.

Page 22, ©2018 Advisor Perspectives, Inc. All rights reserved.

Source: Bloomberg; Bureau of Economic Analysis

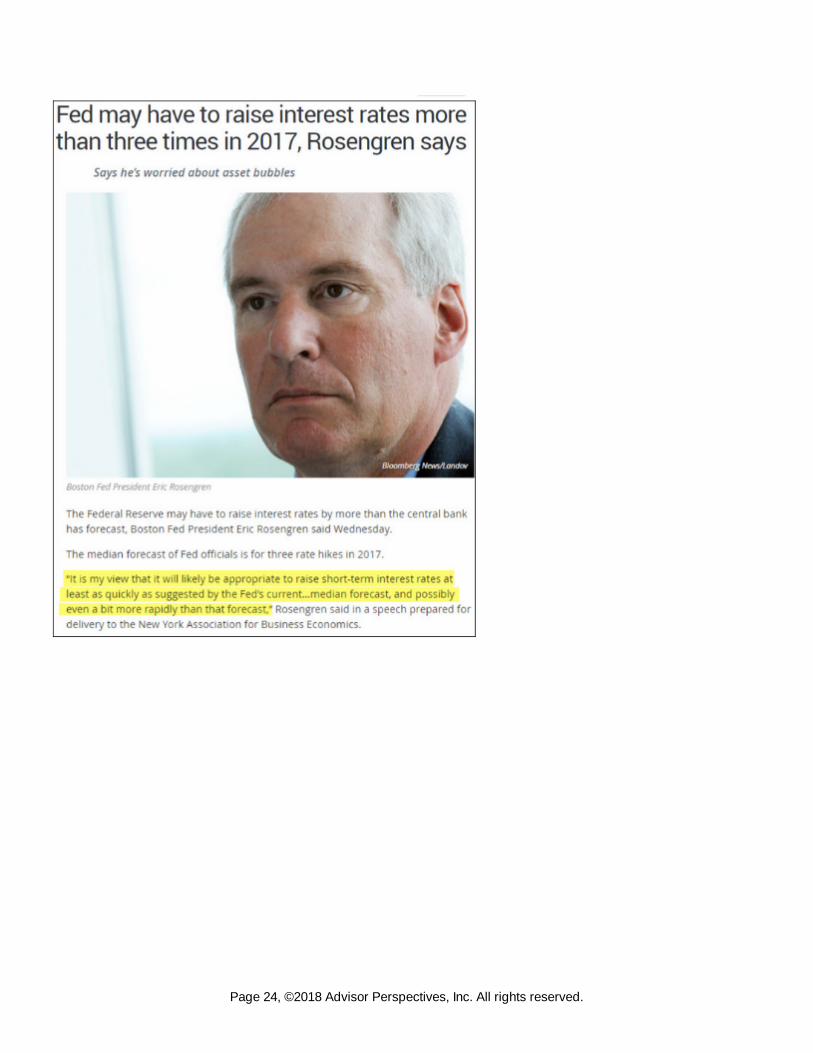

Leading to comments from Fed officials like this:

Page 23, ©2018 Advisor Perspectives, Inc. All rights reserved.

Page 24, ©2018 Advisor Perspectives, Inc. All rights reserved.

Source of many of these charts – The Daily Shot, WSJ (a great daily read for WSJ subscribers).

Most economists are calling for a modest rise in inflation. Somewhere in the 2% range. NDR has afairly benign outlook for 2017 – somewhere in the 2.1% to 2.3% range but sees great risk in 2018.

Looking at where market participants are placing their bets, TIPS (Treasury Inflation ProtectionSecurities) and inflation swaps are signaling long-term inflation in the 2.10% to 2.50% range.

It may be early in the move, but this is most certainly a risk worth noting. Keep it On Your Radar. I’mhappy Susan and I refinanced our mortgage back in July and I’m happy that our tactical bond tradingstrategies have navigated the early up interest innings well.

As you’ll see next in the Trade Signals section, the bearish trend for bonds remains… though HY andconvertible bonds continue to be in up trends.

Page 25, ©2018 Advisor Perspectives, Inc. All rights reserved.

Major point here is: Coming off of a 5,000-year low in interest rates is no small thing. Risk isasymmetrically largely skewed to the upside (yields) and downside (bond returns).

Trade Signals – High Inflationary PressuresS&P 500 Index — 2,340 (2-15-2017)

Click here for the charts and explanations.

Personal NoteIt will be 65 degrees in Philadelphia this weekend! Brianna is coming home from New York and theplan is to play a little golf. The bigger plan is a birthday celebration Sunday evening for Brie andSusan’s oldest boy Tyler. Steak and lobster is on the menu. I just love when we get together for bigdinners and this weekend all eight of us are home.

Maybe we can get a fire going outside though it is a bit too soon to bring out the patio furniture. Happilythat day should be here soon enough.

I’ll be presenting at a meeting in Kansas City on February 23. I’ll be in front of a large group ofindividual investors and, frankly, I love those presentation opportunities the most. We’ll look at thelatest valuation and forward return assumptions as well as discuss the risks in bonds.

Mauldin and I are presenting on March 14 and 15 in the metropolitan NYC area along with JoshJalinski, “The Financial Quarterback.” Josh is a popular financial radio talk show host on iHeart Radioand works closely with Mauldin Solutions and CMG. We’ll be presenting the Mauldin Solutions CoreStrategy.

If you’re an individual investor and are interested in attending, please call 888-988-5674 (JOSH) toreserve a seat. Let Josh’s team know I sent you to him and please feel free to email me if you’d like tolearn more.

Dallas follows for an advisor event on March 28-29. If you are an independent advisor and you’d like tolearn more about the Mauldin Solutions Core Strategy, John and team will be hosting a series of duediligence meetings in Dallas. The strategy will be available on certain platforms in March. Details tofollow.

Years ago I worked for Merrill Lynch and then Prudential Securities. Do you remember the tagline,“When EF Hutton talks, people listen?” George Ball, chairman of Tectonic Holdings, ran EF Huttonand is largely responsible for creating that slogan. George left EF Hutton and became president ofPrudential Securities. He was my boss when I worked there. We met several times at companyretreats and events. I was one of thousands of brokers but felt I got to know him after listening to him

Page 26, ©2018 Advisor Perspectives, Inc. All rights reserved.

on the squawk box that sat atop each rep’s desk. Remember those? Seems so long ago.

Anyway, Tectonic Advisors is one of the ETF strategists in the Mauldin Solutions Core Strategy, alongwith CMG. I’ve recently had a chance to reconnect with George at the Inside ETFs Conference lastmonth. What a powerful and engaging human being and what great joy for me to speak with himagain. Much more to share with you in the weeks ahead.

Hope you have some fun plans for your weekend ahead. Call your favorite mentor and tell him or herwhat you love about them. I bet it will lift you both. Wishing you the very best!

If you find the On My Radar weekly research letter helpful, please tell a friend … also note thesocial media links below. I often share articles and charts via Twitter that I feel may be worth your time.You can follow me @SBlumenthalCMG.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribehere. ♦

With kind regards, Steve

Stephen B. Blumenthal Executive Chairman & CIO CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as itsExecutive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steveshares his views on macroeconomic research, valuations, portfolio construction, asset allocation andrisk management.

The objective of the letter is to provide our investment advisors clients and professional investmentmanagers with unique and relevant information that can be incorporated into their investment processto enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate abouteducating advisors and investors about tactical investing. We launched CMG AdvisorCentral a yearago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper,“Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you.

Page 27, ©2018 Advisor Perspectives, Inc. All rights reserved.

You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase pagedevoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trendfollowing and investor sentiment for many years. I find that reviewing various sentiment, trend andother historically valuable rules-based indicators each week helps me to stay balanced and disciplinedin allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe riskmanagement is paramount in a long-term investment process. When to hedge, when to become moreaggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results.Different types of investments involve varying degrees of risk. Therefore, it should not be assumed thatfuture performance of any specific investment or investment strategy (including the investments and/orinvestment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. orany of its related entities (collectively “CMG”) will be profitable, equal any historical performancelevel(s), be suitable for your portfolio or individual situation, or prove successful. No portion of thecontent should be construed as an offer or solicitation for the purchase or sale of any security.References to specific securities, investment programs or funds are for illustrative purposes only andare not intended to be, and should not be interpreted as recommendations to purchase or sell suchsecurities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/orrecommendations of CMG (and those of other investment and non-investment professionals) as of aspecific prior date. Due to various factors, including changing market conditions, such discussion mayno longer be reflective of current recommendations or opinions. Derivatives and options strategies arenot suitable for every investor, may involve a high degree of risk, and may be appropriate investmentsonly for sophisticated investors who are capable of understanding and assuming the risks involved.Moreover, you should not assume that any discussion or information contained herein serves as thereceipt of, or as a substitute for, personalized investment advice from CMG or the professionaladvisors of your choosing. To the extent that a reader has any questions regarding the applicability ofany specific issue discussed above to his/her individual situation, he/she is encouraged to consult withthe professional advisors of his/her choosing. CMG is neither a law firm nor a certified publicaccounting firm and no portion of the newsletter content should be construed as legal or accountingadvice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized orunrealized, by any CMG client from any specific funds or securities. Please note: In the event thatCMG references performance results for an actual CMG portfolio, the results are reported net of

Page 28, ©2018 Advisor Perspectives, Inc. All rights reserved.

advisory fees and inclusive of dividends. The performance referenced is that as determined and/orprovided directly by the referenced funds and/or publishers, have not been independently verified, anddo not reflect the performance of any specific CMG client. CMG clients may have experiencedmaterially different performance based upon various factors during the corresponding time periods.

The CMG Tactical Fixed Income Index, CMG Tactical All Asset Index, CMG Tactical Equity Index andCMG Beta Rotation Index are rules-based indexes that reect the theoretical performance an investorwould have obtained had it invested in the manner shown and do not represent actual returns, asinvestors cannot invest directly in the Indexes. The CMG Tactical Fixed Income Index, CMG TacticalAll Asset Index, CMG Tactical Equity Index and CMG Beta Rotation Index returns represented do notreect the actual trading of any client account. No representation is being made that any client will or islikely to achieve results similar to those presented herein. Unless noted, performance results arepresented net of a 2.50% maximum annual fee deducted from the account balance quarterly, inarrears.

Any nancial product based on the CMG Tactical Fixed Income Index, CMG Tactical All Asset Index,CMG Tactical Equity Index and CMG Beta Rotation Index or any index derived therefrom that isoffered by CMG Capital Management Group, Inc. is not sponsored, endorsed, sold or promoted bySolactive AG and Solactive AG makes no representation regarding the advisability of investing in theproduct.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical resultsthat were achieved by means of the retroactive application of a back-tested model, such results haveinherent limitations, including: (1) the model results do not reflect the results of actual trading usingclient assets, but were achieved by means of the retroactive application of the referenced models,certain aspects of which may have been designed with the benefit of hindsight; (2) back-testedperformance may not reflect the impact that any material market or economic factors might have hadon the adviser’s use of the model if the model had been used during the period to actually manageclient assets; and (3) CMG’s clients may have experienced investment results during thecorresponding time periods that were materially different from those portrayed in the model. PleaseAlso Note: Past performance may not be indicative of future results. Therefore, no current orprospective client should assume that future performance will be profitable, or equal to anycorresponding historical index. (e.g., S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 TotalMarket Index) is also disclosed. For example, the S&P 500 Total Return Index (the “S&P 500 ”) is amarket capitalization-weighted index of 500 widely held stocks often used as a proxy for the stockmarket. S&P Dow Jones chooses the member companies for the S&P 500 based on market size,liquidity, and industry group representation. Included are the common stocks of industrial, financial,utility, and transportation companies. The historical performance results of the S&P 500 (and those ofor all indices) and the model results do not reflect the deduction of transaction and custodial charges,nor the deduction of an investment management fee, the incurrence of which would have the effect ofdecreasing indicated historical performance results. For example, the deduction combined annualadvisory and transaction fees of 1.00% over a 10-year period would decrease a 10% gross return to an8.9% net return. The S&P 500 is not an index into which an investor can directly invest. The historicalS&P 500 performance results (and those of all other indices) are provided exclusively for comparison

®® ®

®

®

®®

Page 29, ©2018 Advisor Perspectives, Inc. All rights reserved.

purposes only, so as to provide general comparative information to assist an individual in determiningwhether the performance of a specific portfolio or model meets, or continues to meet, his/herinvestment objective(s). A corresponding description of the other comparative indices, are availablefrom CMG upon request. It should not be assumed that any CMG holdings will correspond directly toany such comparative index. The model and indices performance results do not reflect the impact oftaxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

Certain information contained herein has been obtained from third-party sources believed to bereliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation,he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King ofPrussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The aboveviews are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisorthat CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosurestatement discussing advisory services and fees is available upon request or via CMG’s internet website at www.cmgwealth.com/disclosures.

© CMG Captial Management Group

Page 30, ©2018 Advisor Perspectives, Inc. All rights reserved.

Related Documents