TBLI 2013: Application of ESG Signals in Portfolio Construction msci.com msci.com Portfolio Construction June 18, 2013 Olga Emelianova MSCI ESG IVA Rating Research

Olga emelianova room b, 19th floor-workshop 13

Aug 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TBLI 2013: Application of ESG Signals in Portfolio Construction

msci.commsci.com

Portfolio Construction

June 18, 2013

Olga Emelianova

MSCI ESG IVA Rating Research

Current trends in ESG investment

• Do we see any growth in SRI or ESG integration?

• What drives investment strategies?

• What tools are available?

msci.com 2msci.com

Increased Focus on ESG Integration by Investors

� Asset Owners are increasingly interested in incorporating long term sustainability issues and scrutinizing the ESG performance of asset managers

� 7% of the total global investable market is subject to PRI ESG integration

� Asset owners and managers increasingly finding ESG to be a material topic for engagement: tripling of ‘FOR’ votes on E&S proxy proposals since 1999

20.6%

25%

Average Vote Results for All E&S Proxy ProposalsUN PRI Signatories & AUM

msci.com 3

7.4%7.6%

8.7%9.4%

12.0%12.1%

9.8%

12.5%

15.0%14.0%

16.3%

18.3%

20.6%

0%

5%

10%

15%

20%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source: ISS Checklist

Source: UNPRI 2011 Report on Progress

The Evolution of ESG Investment Mandates

Socially Responsible Screening

• Supports screening on religious, ethical, and divestment criteria (e.g. weapons, tobacco, Sudan, etc.)

ESG Ethical Evaluation

msci.com

• Analyzes & monitors ‘ESG controversies’ and violations of global norms such as the UN Global Compact

ESG Integration

• Identifies ESG related investment risks and opportunities not often captured by conventional analysis

4

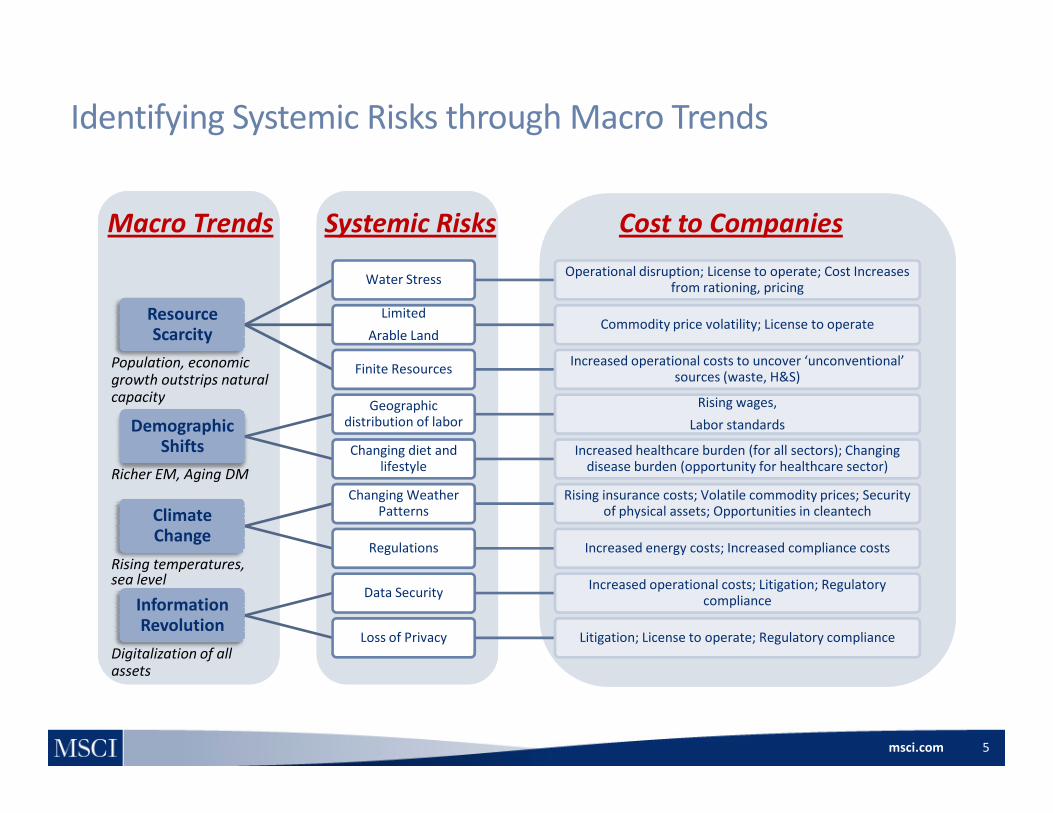

Identifying Systemic Risks through Macro Trends

Resource

Scarcity

Water StressOperational disruption; License to operate; Cost Increases

from rationing, pricing

Limited

Arable LandCommodity price volatility; License to operate

Finite Resources Increased operational costs to uncover ‘unconventional’

sources (waste, H&S)

Geographic Rising wages,

Population, economic growth outstrips natural capacity

Macro Trends Systemic Risks Cost to Companies

msci.com 5

Demographic

Shifts

Geographic distribution of labor

Rising wages,

Labor standards

Changing diet and lifestyle

Increased healthcare burden (for all sectors); Changing disease burden (opportunity for healthcare sector)

Climate

Change

Changing Weather Patterns

Rising insurance costs; Volatile commodity prices; Security of physical assets; Opportunities in cleantech

Regulations Increased energy costs; Increased compliance costs

Information

Revolution

Data SecurityIncreased operational costs; Litigation; Regulatory

compliance

Loss of Privacy Litigation; License to operate; Regulatory compliance

Richer EM, Aging DM

Rising temperatures, sea level

Digitalization of all assets

ESG assessment: company level

• Are there implications of ESG performance on companies’ capacity for long-term growth?

• Can we anticipate ESG-related events or assess long-term performance risks?

msci.com 6msci.com

Examples: ESG Events and Performance

0

1

2

3

4

5

6

Aug-11 Feb-12 Aug-12

Aquarius Platinum Limited

May 2012: work stoppages ordered by Government

March 2012: Rated ‘CCC’

Bottom quartile ranking on

‘Health & Safety’

BB

20

11

CCC

20

12

CCC

msci.com 7

0

20

40

60

80

100

120

Oct-10 Feb-11 Jun-11 Oct-11 Feb-12 Jun-12 Oct-12

Monster Beverage

Oct 23rd FDA probe of five reported death linked to Monster Energy Drink

20

11

B

20

12

CCC

June, 2012: Downgrade to ‘CCC’

Bottom quartile ranking on

‘Nutrition & Health’

Other examples: Massey Energy, Sun Hung Kai Properties, Carnival, Zijin Mining, Foxconn

Disclaimer: Examples only. Past performance is not indicative of future performance

Examples: ESG Factors and Financial Performance

2013 Q1 Results

0%

10%

Yum! Brands

2011 IVA Profile: ”the company's high exposure (to food safety problems) compared to peers does not appear to be adequately countered by strategies to reduce food safety incidents”

20

10

B

20

11

CCC2

01

2CCC

50

60

Top Three Issues Cited by Chinese

Respondents as a ‘Very Big Problem’

msci.com 8

Same Store

Sales

Operating

Profit

-50%

-40%

-30%

-20%

-10%

0%

China

US

-41%

-20%

Source: Data from Yum! Brands Investor Presentation May 8, 2013

0

10

20

30

40

50

Corrupt

Officials

Gap

between

Rich &

Poor

Food

Safety

% R

esp

on

de

nts

2008

2012

Source: Pew Research Project, Global Attitudes Survey China 2012

Management

� Unlike traditional SRI ratings, MSCI ESG IVA ratings examine companies’ exposure to ESG-related risks and the management capacity to mitigate such risks

� Companies with higher risk profiles are expected to demonstrate stronger mitigation systems

MSCI ESG IVA Rating Model

msci.com 9

Level of

Exposure

Management

Capacity

� Type of operations

� Location of operations

� Size of operation, etc.

� Policies & commitments

� Programs & initiatives

� Performance indicators

� Controversies

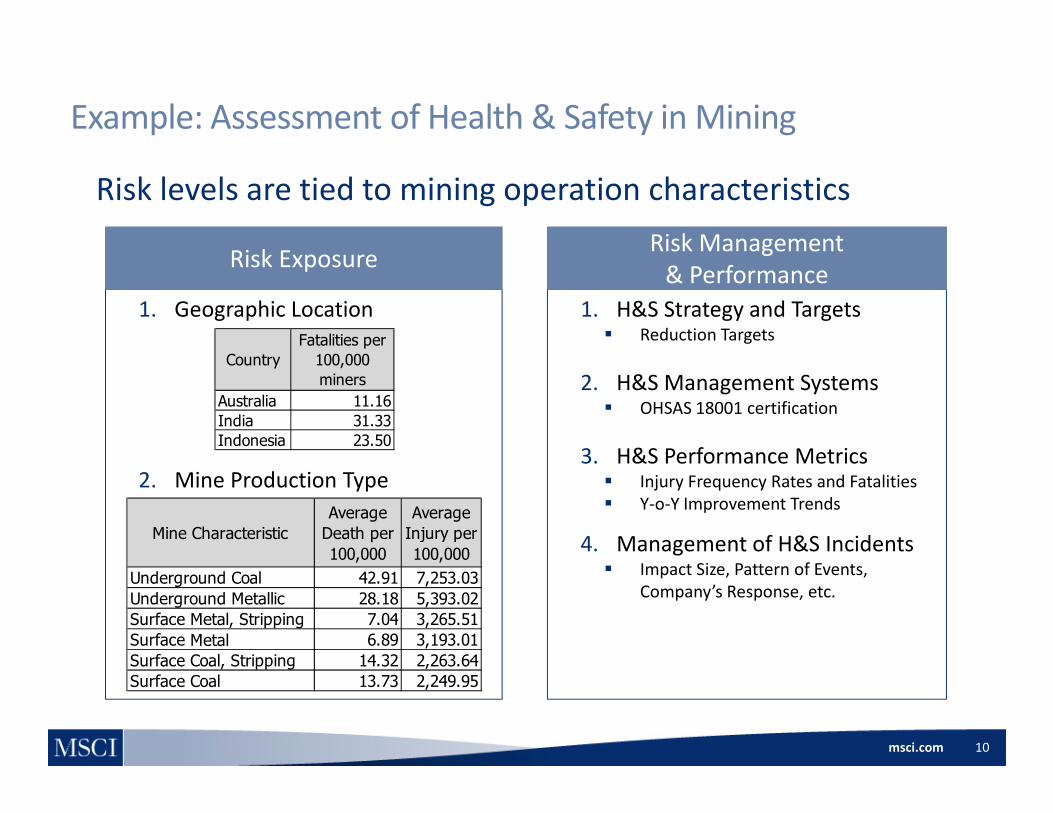

Example: Assessment of Health & Safety in Mining

1. Geographic Location 1. H&S Strategy and Targets� Reduction Targets

2. H&S Management Systems� OHSAS 18001 certification

Risk Management

& PerformanceRisk Exposure

Country

Fatalities per

100,000

miners

Australia 11.16

Risk levels are tied to mining operation characteristics

msci.com

2. Mine Production Type

� OHSAS 18001 certification

3. H&S Performance Metrics� Injury Frequency Rates and Fatalities

� Y-o-Y Improvement Trends

4. Management of H&S Incidents� Impact Size, Pattern of Events,

Company’s Response, etc.

10

Australia 11.16

India 31.33

Indonesia 23.50

Mine Characteristic

Average

Death per

100,000

Average

Injury per

100,000

Underground Coal 42.91 7,253.03

Underground Metallic 28.18 5,393.02

Surface Metal, Stripping 7.04 3,265.51

Surface metal 6.89 3,193.01

Surface Coal, Stripping 14.32 2,263.64

Surface Coal 13.73 2,249.95

Surface Metal, Stripping

Calculating Key Issue Scores (0-10): RisksHow Well Is the Company Managing the Issue, Given Its Specific Risk Level?

4

5

6

7

8

9

10

Ris

k M

an

ag

em

en

t

Key Issue Score = 10

Key Issue

Score = 2

Key Issue

Score = 10

msci.com 11

� When risk exposure=0 and risk management=0, the KI score=5

� When risk exposure=10, the highest KI score is capped at 7 (because there are risks that can’t be fully managed even if company is doing everything possible)

� When risk management<5, it is not possible to get KI score=10 even if exposure is very low (we set a minimum for ‘management’attention)

0

1

2

3

0 1 2 3 4 5 6 7 8 9 10

Risk Exposure

Key Issue

Scores = 0

Source: MSCI ESG Research

Example: Company Performance on H&S Key Issue

= 10,000 employees

Alcoa

BHP Billiton

Norsk Hydro

Boliden

Cameco

Anglo AmericanRio Tinto

Xstrata

Freeport-McMoRan

Inmet

5

10

Top Quartile Second Quartile Third Quartile Bottom Quartile

Risk Management

Moderate Management

(Safety management structure average for

industry, some

Strong Management of Key Issue

(Regular audits, strong improvements, leading

performance)

msci.com 12

Sumitomo Metal

Peabody Energy

Inmet

ENRC

Glencore

KGHMGrupo Mexico

CONSOL Energy

Arch Coal

Ivanhoe Mines

Lynas Corp

Coal India

MMC Norilsk

China Shenhua Energy

Kazakhmys

Vedanta Res.

Sterlite (India)South. Copper

First Quantum

Alpha Natural

0

4 5 6 7 8 9 10

Risk Exposure

industry, some improvement, average

performance)

Poor Management (Average to poor safety metrics, lack of stringent

management systems

and programs)

Moderate Risk (Regions with higher safety standards and metrics such as Australia, lower risk operations such

as surface mining)

High Risk(High risk countries such as China and high risk operations such as

primary processing or underground

coal mining)

Darden

McDonalds Corp

5

6

7

8

9

10

Finding Value in ESG Analysis:Benchmarking Exposure and Management of Food Safety Risks

Low Risk Exposure,Strong Risk Management

•Traceability

•Testing

•Employee Training

•Franchisee Training

•Certification

•Etc.

msci.com

Domino's

McDonalds Corp

Chipotle Mexican

Grill

Starbucks Corp

Yum! Brands

0

1

2

3

4

0 1 2 3 4 5 6 7 8 9 10

13

High Risk Exposure,

Poor Risk Management

•higher % revenues from products prone to

recalls, high health impact

•Larger, more complex operations

Risk Management

Risk Exposure

Source: MSCI ESG Research IVA Industry Report; Restaurants, 2012

ESG assessment: portfolio level

• Can ESG factors be integrated in portfolios?

• Z. Nagy, D. Cogan, and D. Sinnreich “Optimizing ESG Factors in Portfolio Construction” (December 2012)

msci.com 14msci.com

“ESG Factors in Portfolio Construction”: Three ESG-tilt Strategies� Approach

� Use case: Asset owner seeks to raise ESG profile of global portfolio without incurring large tracking error

�Combine MSCI ESG IVA Ratings with Barra Global Equity Model to build optimizedportfolios with higher ESG scores

�Keep risk, performance and structural characteristics equivalent to benchmarks like the MSCI World Index (risk reducing or index enhancing, rather than alpha seeking)

� Strategy 1: ESG exclusion

� Worst-in-class approach excludes low-rated (‘CCC’) companies

msci.com

� Worst-in-class approach excludes low-rated (‘CCC’) companies

� Strategy 2: ESG tilt

� Best-in-class approach overweights higher-rated ESG companies, underweights lower-rated ones

� Strategy 3: ESG momentum

� ‘Best-effort’ approach overweights companies with ESG ratings upgrades over the

preceding 12-month period and underweights companies with ratings downgrades

� Time series: Feb. 2007 – Dec. 2012 for ESG Exclusion & ESG Tilt; Feb. 2008 – Dec. 2012 for ESG Momentum

15

Performance Analysis: Comparing the Three ESG Tilt Strategies

� During the sample period all three strategies showed potential to improved ESG

characteristics of a portfolio while limiting tracking error, impact on risk-adjusted returns

� The best active returns and highest information ratio during the sample period came with

companies showing ESG momentum – i.e. their IVA ratings improved over a recent time

period

Comparison of ESG Strategies, February 2008 – December 2012

ESG strategyESG

ESG TiltESG

msci.com 16

ESG strategyESG

ExclusionESG Tilt

ESG

Momentum

Active return (annual, %) 0.10 0.05 0.35

Common factor contribution (annual, %) 0.06 0.03 0.08

Asset specific contribution (annual, %) 0.05 0.01 0.27

Tracking error (ex-post, annual %) 0.45 0.46 0.36

Information ratio 0.23 0.10 0.97

Average improvement in ESG score 1.27 1.21 0.46

Average relative improvement in ESG score (%) 23 22 8

Disclaimer: Past performance is not a predictor of future results

About MSCI ESG Research

� The leading provider of tools to measure and manage ESG Risk for asset owners, investment managers,

and consultants

� Over 60 asset owners with $2.3 trillion in assets depend on MSCI ESG Research

� Over 500 clients with $15 trillion in assets globally

� ESG ratings and research expertise produced 100% in-house

� Signatory to the Principles for Responsible Investment (www.unpri.org)

msci.com

� Signatory to the Principles for Responsible Investment (www.unpri.org)

� Direct successor to IRRC (1972), KLD (1988) and Innovest (1998)

� Staff of 140+, including more than 90 in ESG research

� Americas: New York, Boston, San Francisco, Toronto, Ann Arbor, Rockville

� EMEA: Paris, London, Geneva

� APAC: Tokyo, Sydney, Manila, Mumbai, Hong Kong, Beijing

� Products and services:� ESG research and ratings

� Screening data

� Custom research

� Indices

17

MSCI ESG Global Client Service

Americas + 1.212.804.5299

Asia Pacific + 612.9033.9339

Europe, Middle East and Africa + +44.207.618.2510

msci.com 18msci.com

www.msci.com/esg

Notice and Disclaimer� This document and all of the information contained in it, including without limitation all text, data, graphs, charts (collectively, the “Information”) is the property of MSCI Inc. or its

subsidiaries (collectively, “MSCI”), or MSCI’s licensors, direct or indirect suppliers or any third party involved in making or compiling any Information (collectively, with MSCI, the “Information Providers”) and is provided for informational purposes only. The Information may not be reproduced or redisseminated in whole or in part without prior written permission from MSCI.

� The Information may not be used to create derivative works or to verify or correct other data or information. For example (but without limitation), the Information may not be used to create indices, databases, risk models, analytics, software, or in connection with the issuing, offering, sponsoring, managing or marketing of any securities, portfolios, financial products or other investment vehicles utilizing or based on, linked to, tracking or otherwise derived from the Information or any other MSCI data, information, products or services.

� The user of the Information assumes the entire risk of any use it may make or permit to be made of the Information. NONE OF THE INFORMATION PROVIDERS MAKES ANY EXPRESS OR IMPLIED WARRANTIES OR REPRESENTATIONS WITH RESPECT TO THE INFORMATION (OR THE RESULTS TO BE OBTAINED BY THE USE THEREOF), AND TO THE MAXIMUM EXTENT PERMITTED BY APPLICABLE LAW, EACH INFORMATION PROVIDER EXPRESSLY DISCLAIMS ALL IMPLIED WARRANTIES (INCLUDING, WITHOUT LIMITATION, ANY IMPLIED WARRANTIES OF ORIGINALITY, ACCURACY, TIMELINESS, NON-INFRINGEMENT, COMPLETENESS, MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE) WITH RESPECT TO ANY OF THE INFORMATION.

� Without limiting any of the foregoing and to the maximum extent permitted by applicable law, in no event shall any Information Provider have any liability regarding any of the Information for any direct, indirect, special, punitive, consequential (including lost profits) or any other damages even if notified of the possibility of such damages. The foregoing shall not exclude or limit any liability that may not by applicable law be excluded or limited, including without limitation (as applicable), any liability for death or personal injury to the extent that such injury results from the negligence or willful default of itself, its servants, agents or sub-contractors.

� Information containing any historical information, data or analysis should not be taken as an indication or guarantee of any future performance, analysis, forecast or prediction. Past performance does not guarantee future results.

� None of the Information constitutes an offer to sell (or a solicitation of an offer to buy), any security, financial product or other investment vehicle or any trading strategy.

msci.com 19msci.com

� You cannot invest in an index. MSCI does not issue, sponsor, endorse, market, offer, review or otherwise express any opinion regarding any investment or financial product that may be based on or linked to the performance of any MSCI index.

� MSCI’s indirect wholly-owned subsidiary Institutional Shareholder Services, Inc. (“ISS”) is a Registered Investment Adviser under the Investment Advisers Act of 1940. Except with respect to any applicable products or services from ISS (including applicable products or services from MSCI ESG Research, which are provided by ISS), neither MSCI nor any of its products or services recommends, endorses, approves or otherwise expresses any opinion regarding any issuer, securities, financial products or instruments or trading strategies and neither MSCI nor any of its products or services is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

� The MSCI ESG Indices use ratings and other data, analysis and information from MSCI ESG Research. MSCI ESG Research is produced by ISS or its subsidiaries. Issuers mentioned or included in any MSCI ESG Research materials may be a client of MSCI, ISS, or another MSCI subsidiary, or the parent of, or affiliated with, a client of MSCI, ISS, or another MSCI subsidiary, including ISS Corporate Services, Inc., which provides tools and services to issuers. MSCI ESG Research materials, including materials utilized in any MSCI ESG Indices or other products, have not been submitted to, nor received approval from, the United States Securities and Exchange Commission or any other regulatory body.

� Any use of or access to products, services or information of MSCI requires a license from MSCI. MSCI, Barra, RiskMetrics, IPD, ISS, FEA, InvestorForce, and other MSCI brands and product names are the trademarks, service marks, or registered trademarks of MSCI or its subsidiaries in the United States and other jurisdictions. The Global Industry Classification Standard (GICS) was developed by and is the exclusive property of MSCI and Standard & Poor’s. “Global Industry Classification Standard (GICS)” is a service mark of MSCI and Standard & Poor’s.

© 2013 MSCI Inc. All rights reserved. Apr 2013

Related Documents