790.03 v5 02-16-16 [IN ACCORDANCE WITH CALIFORNIA INSURANCE CODE (CIC) SECTION 12938, THIS REPORT WILL BE MADE PUBLIC AND PUBLISHED ON THE CALIFORNIA DEPARTMENT OF INSURANCE (CDI) WEBSITE] WEBSITE PUBLISHED REPORT OF THE MARKET CONDUCT EXAMINATION OF THE CLAIMS PRACTICES OF OLD REPUBLIC INSURANCE COMPANY NAIC # 24147 CDI # 1489-4 AS OF APRIL 30, 2018 ADOPTED JUNE 26, 2019 STATE OF CALIFORNIA CALIFORNIA DEPARTMENT OF INSURANCE MARKET CONDUCT DIVISION FIELD CLAIMS BUREAU

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

790.03 v5 02-16-16

[IN ACCORDANCE WITH CALIFORNIA INSURANCE CODE (CIC) SECTION 12938,

THIS REPORT WILL BE MADE PUBLIC AND PUBLISHED ON THE CALIFORNIA DEPARTMENT OF INSURANCE (CDI) WEBSITE]

WEBSITE PUBLISHED REPORT OF THE MARKET CONDUCT EXAMINATION OF THE CLAIMS PRACTICES OF

OLD REPUBLIC INSURANCE COMPANY NAIC # 24147 CDI # 1489-4

AS OF APRIL 30, 2018

ADOPTED JUNE 26, 2019

STATE OF CALIFORNIA

CALIFORNIA DEPARTMENT OF INSURANCE MARKET CONDUCT DIVISION

FIELD CLAIMS BUREAU

790.03 v5 02-16-16

NOTICE

The provisions of Section 735.5(a) (b) and (c) of the California

Insurance Code (CIC) describe the Commissioner’s authority

and exercise of discretion in the use and/or publication of

any final or preliminary examination report or other

associated documents. The following examination report is

a report that is made public pursuant to California Insurance

Code Section 12938(b)(1) which requires the publication of

every adopted report on an examination of unfair or

deceptive practices in the business of insurance as defined

in Section 790.03 that is adopted as filed, or as modified or

corrected, by the Commissioner pursuant to Section 734.1.

790.03 v5 02-16-16

TABLE OF CONTENTS

FOREWORD ................................................................................................................... 1

SCOPE OF THE EXAMINATION ................................................................................... 2

EXECUTIVE SUMMARY ................................................................................................ 4

DETAILS OF THE CURRENT EXAMINATION .............................................................. 5

TABLE OF TOTAL ALLEGED VIOLATIONS ................................................................ 6

SUMMARY OF EXAMINATION RESULTS .................................................................. 10

1

790.03 v5 02-16-16

FOREWORD

This report is written in a “report by exception” format. The report does not

present a comprehensive overview of the subject insurer’s practices. The report

contains a summary of pertinent information about the lines of business examined,

details of the non-compliant or problematic activities that were discovered during the

course of the examination and the insurer’s proposals for correcting the deficiencies.

When a violation that reflects an underpayment to the claimant is discovered and the

insurer corrects the underpayment, the additional amount paid is identified as a

recovery in this report.

While this report contains violations of law that were cited by the examiner,

additional violations of CIC § 790.03 or other laws not cited in this report may also apply

to any or all of the non-compliant or problematic activities that are described herein.

All unacceptable or non-compliant activities may not have been discovered.

Failure to identify, comment upon or criticize non-compliant practices in this state or

other jurisdictions does not constitute acceptance of such practices.

Alleged violations identified in this report, any criticisms of practices and the

Company responses, if any, have not undergone a formal administrative or judicial

process.

This report is made available for public inspection and is published on the

California Department of Insurance website (www.insurance.ca.gov) pursuant to

California Insurance Code section 12938(b)(1).

2

790.03 v5 02-16-16

SCOPE OF THE EXAMINATION

Under the authority granted in Part 2, Chapter 1, Article 4, Sections 730, 733,

and 736, and Article 6.5, Section 790.04 of the California Insurance Code; and Title 10,

Chapter 5, Subchapter 7.5, Section 2695.3(a) of the California Code of Regulations, an

examination was made of the claim handling practices and procedures in California of:

Old Republic Insurance Company NAIC # 24147

Group NAIC # 0150

Hereinafter, the Company listed above also will be referred to individually as

ORIC, or the Company.

This examination covered the claim handling practices of the aforementioned

Company on Commercial Automobile, and Workers Compensation claims closed during

the period from May 1, 2017 through April 30, 2018, and claims open as of April 30,

2018. The examination was made to discover, in general, if these and other operating

procedures of the Company conform to the contractual obligations in the policy forms,

the California Insurance Code (CIC), the California Code of Regulations (CCR) and

case law.

To accomplish the foregoing, the examination included:

1. A review of the guidelines, procedures, training plans and forms adopted by

the Company for use in California including any documentation maintained by the

Company in support of positions or interpretations of the California Insurance Code, Fair

Claims Settlement Practices Regulations, and other related statutes, regulations and

case law used by the Company to ensure fair claims settlement practices.

3

790.03 v5 02-16-16

2. A review of the application of such guidelines, procedures, and forms, by

means of an examination of a sample of individual claim files and related records.

3. A review of the California Department of Insurance’s (CDI) market analysis

results; and if any, a review of consumer complaints and inquiries about this Company

closed by the CDI during the period May 1, 2017 through April 30, 2018, a review of

previous CDI market conduct claims examination reports on this Company; and a

review of prior CDI enforcement actions.

The review of the sample of individual claim files was conducted at the offices of

California Department of Insurance in Los Angeles and San Francisco, California.

4

790.03 v5 02-16-16

EXECUTIVE SUMMARY

The Commercial Automobile and Workers Compensation claims reviewed were

closed from May 1, 2017 through April 30, 2018, referred to as the “review period”. The

examiners randomly selected 169 ORIC claim files for examination. The examiners

cited 39 alleged claims handling violations of the California Insurance Code and the

California Code of Regulations from this sample file review.

The results of the market analysis review revealed that during 2017, enforcement

action was taken in the state of Missouri. This action alleged the Company failed to

include sales taxes and other applicable fees in total loss settlements on Commercial

and Private Passenger Automobile claims. The examiner focused on this issue during

the course of the file review. This issue also is reflected in the results of this

examination.

Findings of this examination included the failure to ask if a child passenger

restraint system was in the vehicle at the time of loss; the failure to conduct its business

in its own name; the failure to conduct and diligently pursue a thorough, fair and

objective investigation; and the failure to include, in the settlement, all applicable taxes,

one-time fees incident to transfer of evidence of ownership of a comparable automobile;

the license fee and other annual fees computed based upon the remaining term of the

current registration.

5

790.03 v5 02-16-16

DETAILS OF THE CURRENT EXAMINATION

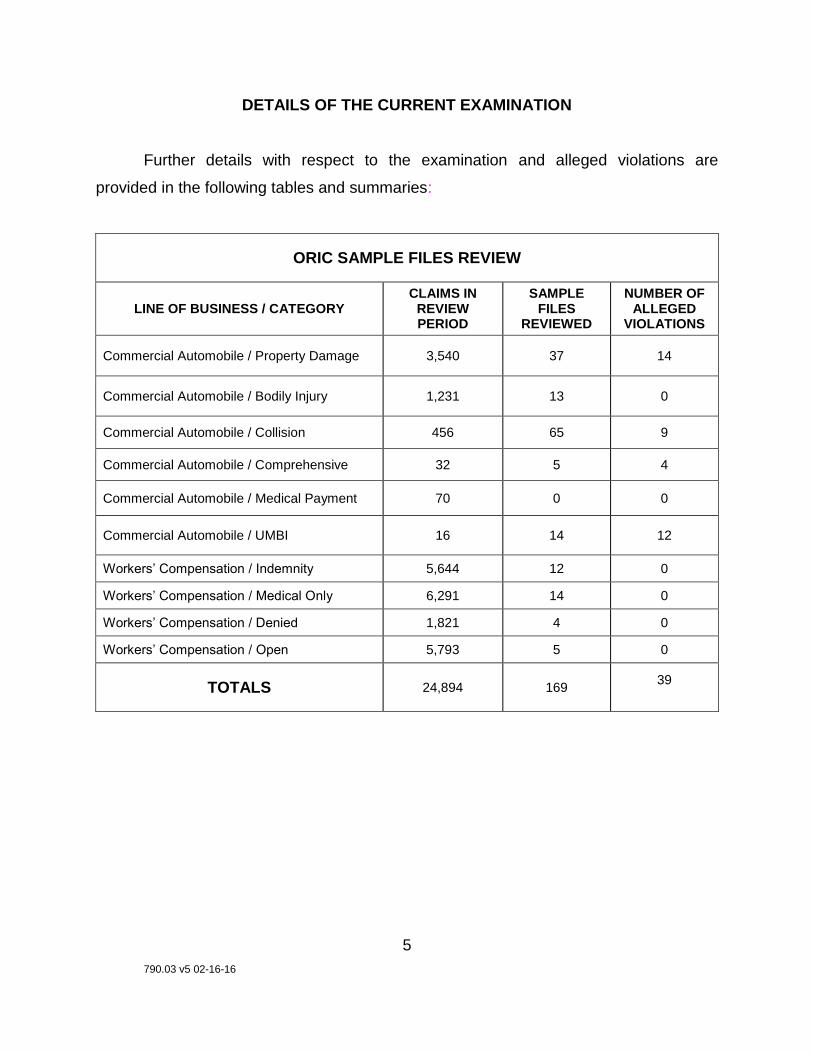

Further details with respect to the examination and alleged violations are

provided in the following tables and summaries:

ORIC SAMPLE FILES REVIEW

LINE OF BUSINESS / CATEGORY CLAIMS IN

REVIEW PERIOD

SAMPLE FILES

REVIEWED

NUMBER OF ALLEGED

VIOLATIONS

Commercial Automobile / Property Damage 3,540 37 14

Commercial Automobile / Bodily Injury 1,231 13 0

Commercial Automobile / Collision 456 65 9

Commercial Automobile / Comprehensive 32 5 4

Commercial Automobile / Medical Payment 70 0 0

Commercial Automobile / UMBI 16 14 12

Workers’ Compensation / Indemnity 5,644 12 0

Workers’ Compensation / Medical Only 6,291 14 0

Workers’ Compensation / Denied 1,821 4 0

Workers’ Compensation / Open 5,793 5 0

TOTALS 24,894 169 39

6

790.03 v5 02-16-16

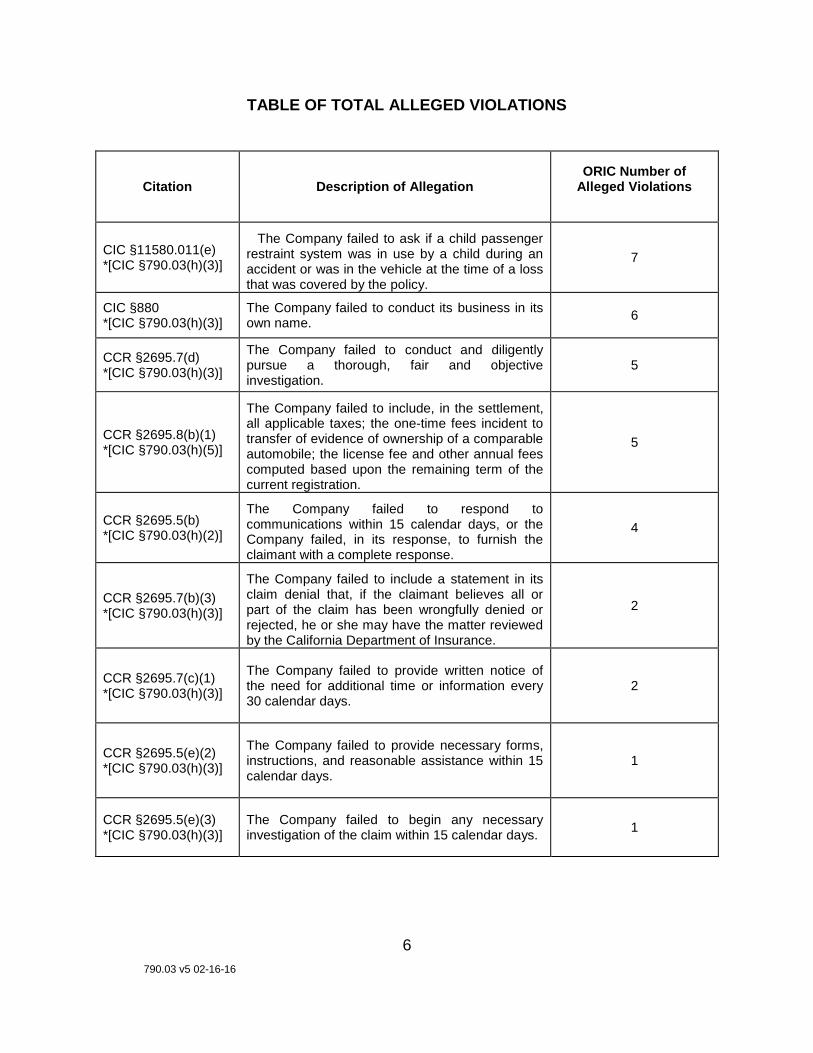

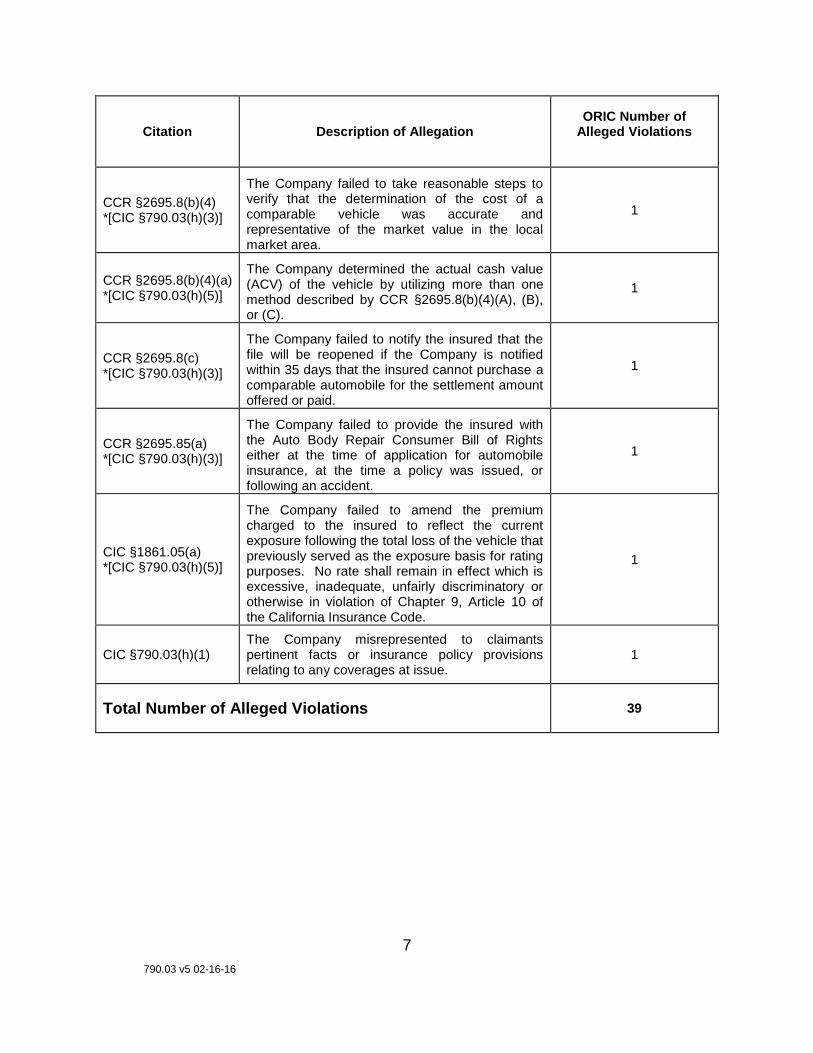

TABLE OF TOTAL ALLEGED VIOLATIONS

Citation Description of Allegation ORIC Number of

Alleged Violations

CIC §11580.011(e) *[CIC §790.03(h)(3)]

The Company failed to ask if a child passenger restraint system was in use by a child during an accident or was in the vehicle at the time of a loss that was covered by the policy.

7

CIC §880 *[CIC §790.03(h)(3)]

The Company failed to conduct its business in its own name.

6

CCR §2695.7(d) *[CIC §790.03(h)(3)]

The Company failed to conduct and diligently pursue a thorough, fair and objective investigation.

5

CCR §2695.8(b)(1) *[CIC §790.03(h)(5)]

The Company failed to include, in the settlement, all applicable taxes; the one-time fees incident to transfer of evidence of ownership of a comparable automobile; the license fee and other annual fees computed based upon the remaining term of the current registration.

5

CCR §2695.5(b) *[CIC §790.03(h)(2)]

The Company failed to respond to communications within 15 calendar days, or the Company failed, in its response, to furnish the claimant with a complete response.

4

CCR §2695.7(b)(3) *[CIC §790.03(h)(3)]

The Company failed to include a statement in its claim denial that, if the claimant believes all or part of the claim has been wrongfully denied or rejected, he or she may have the matter reviewed by the California Department of Insurance.

2

CCR §2695.7(c)(1) *[CIC §790.03(h)(3)]

The Company failed to provide written notice of the need for additional time or information every 30 calendar days.

2

CCR §2695.5(e)(2) *[CIC §790.03(h)(3)]

The Company failed to provide necessary forms, instructions, and reasonable assistance within 15 calendar days.

1

CCR §2695.5(e)(3) *[CIC §790.03(h)(3)]

The Company failed to begin any necessary investigation of the claim within 15 calendar days.

1

7

790.03 v5 02-16-16

Citation Description of Allegation ORIC Number of

Alleged Violations

CCR §2695.8(b)(4) *[CIC §790.03(h)(3)]

The Company failed to take reasonable steps to verify that the determination of the cost of a comparable vehicle was accurate and representative of the market value in the local market area.

1

CCR §2695.8(b)(4)(a) *[CIC §790.03(h)(5)]

The Company determined the actual cash value (ACV) of the vehicle by utilizing more than one method described by CCR §2695.8(b)(4)(A), (B), or (C).

1

CCR §2695.8(c) *[CIC §790.03(h)(3)]

The Company failed to notify the insured that the file will be reopened if the Company is notified within 35 days that the insured cannot purchase a comparable automobile for the settlement amount offered or paid.

1

CCR §2695.85(a) *[CIC §790.03(h)(3)]

The Company failed to provide the insured with the Auto Body Repair Consumer Bill of Rights either at the time of application for automobile insurance, at the time a policy was issued, or following an accident.

1

CIC §1861.05(a) *[CIC §790.03(h)(5)]

The Company failed to amend the premium charged to the insured to reflect the current exposure following the total loss of the vehicle that previously served as the exposure basis for rating purposes. No rate shall remain in effect which is excessive, inadequate, unfairly discriminatory or otherwise in violation of Chapter 9, Article 10 of the California Insurance Code.

1

CIC §790.03(h)(1) The Company misrepresented to claimants pertinent facts or insurance policy provisions relating to any coverages at issue.

1

Total Number of Alleged Violations 39

8

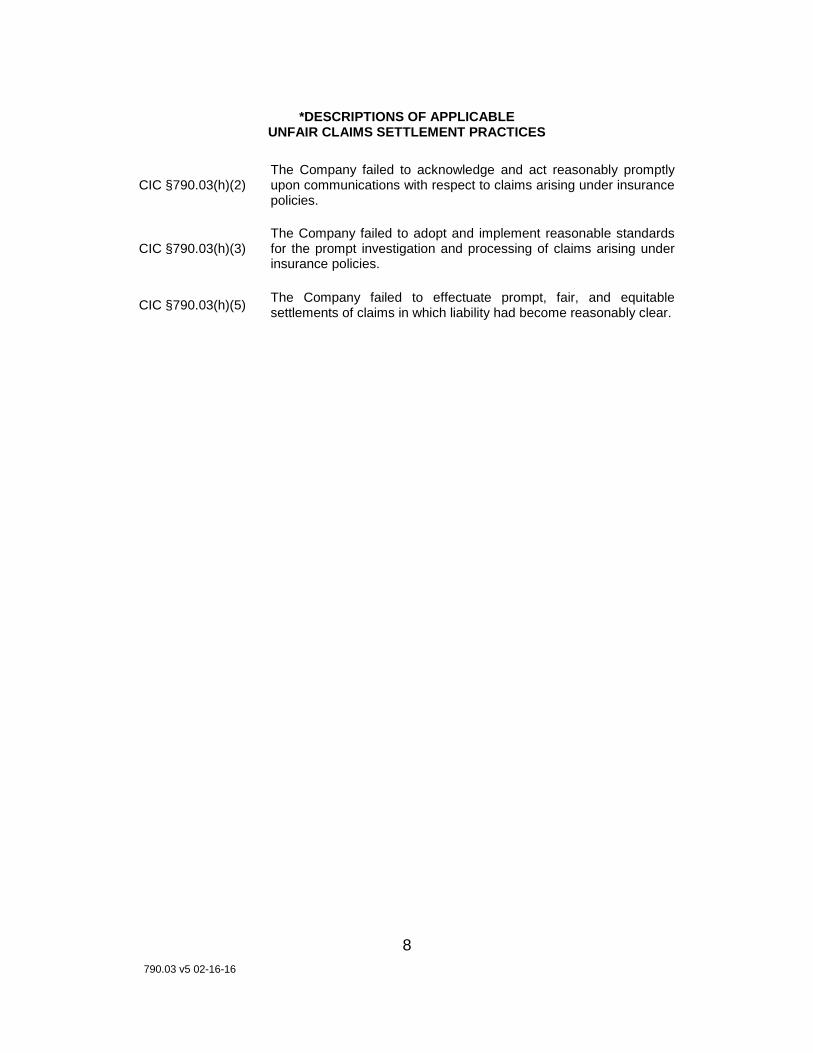

790.03 v5 02-16-16

*DESCRIPTIONS OF APPLICABLE UNFAIR CLAIMS SETTLEMENT PRACTICES

CIC §790.03(h)(2) The Company failed to acknowledge and act reasonably promptly upon communications with respect to claims arising under insurance policies.

CIC §790.03(h)(3) The Company failed to adopt and implement reasonable standards for the prompt investigation and processing of claims arising under insurance policies.

CIC §790.03(h)(5) The Company failed to effectuate prompt, fair, and equitable settlements of claims in which liability had become reasonably clear.

9

790.03 v5 02-16-16

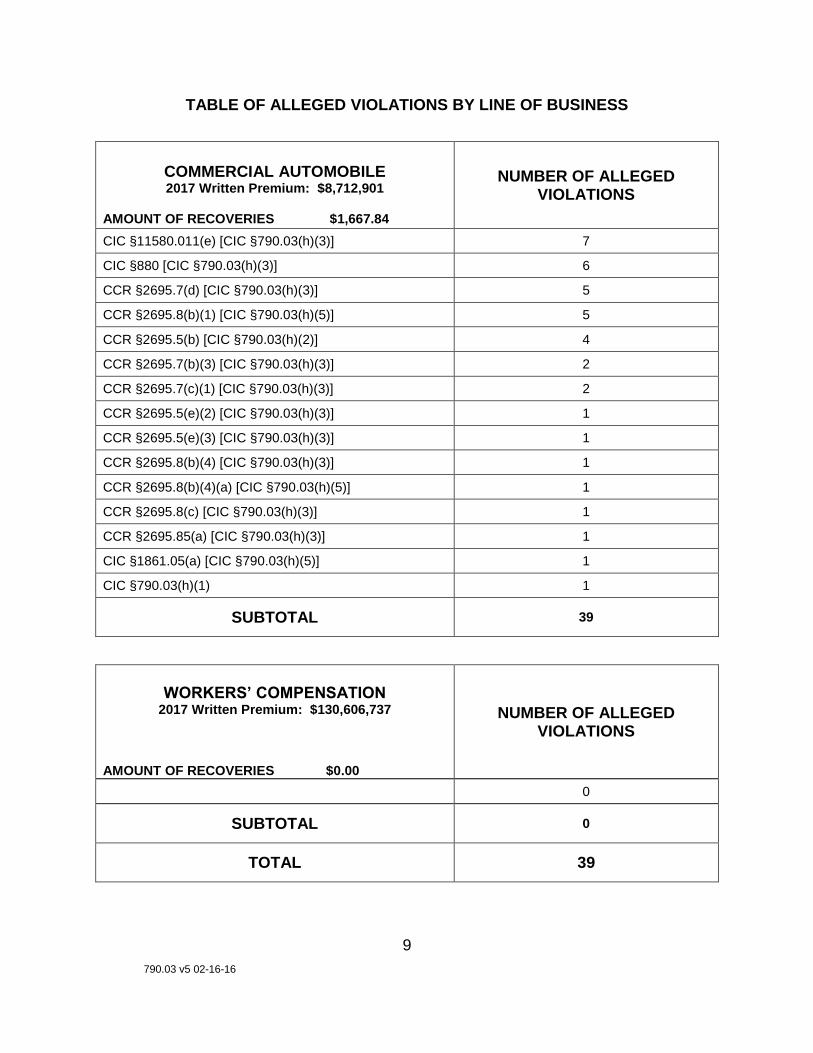

TABLE OF ALLEGED VIOLATIONS BY LINE OF BUSINESS

COMMERCIAL AUTOMOBILE 2017 Written Premium: $8,712,901

AMOUNT OF RECOVERIES $1,667.84

NUMBER OF ALLEGED VIOLATIONS

CIC §11580.011(e) [CIC §790.03(h)(3)] 7

CIC §880 [CIC §790.03(h)(3)] 6

CCR §2695.7(d) [CIC §790.03(h)(3)] 5

CCR §2695.8(b)(1) [CIC §790.03(h)(5)] 5

CCR §2695.5(b) [CIC §790.03(h)(2)] 4

CCR §2695.7(b)(3) [CIC §790.03(h)(3)] 2

CCR §2695.7(c)(1) [CIC §790.03(h)(3)] 2

CCR §2695.5(e)(2) [CIC §790.03(h)(3)] 1

CCR §2695.5(e)(3) [CIC §790.03(h)(3)] 1

CCR §2695.8(b)(4) [CIC §790.03(h)(3)] 1

CCR §2695.8(b)(4)(a) [CIC §790.03(h)(5)] 1

CCR §2695.8(c) [CIC §790.03(h)(3)] 1

CCR §2695.85(a) [CIC §790.03(h)(3)] 1

CIC §1861.05(a) [CIC §790.03(h)(5)] 1

CIC §790.03(h)(1) 1

SUBTOTAL 39

WORKERS’ COMPENSATION

2017 Written Premium: $130,606,737

AMOUNT OF RECOVERIES $0.00

NUMBER OF ALLEGED VIOLATIONS

0

SUBTOTAL 0

TOTAL 39

10

790.03 v5 02-16-16

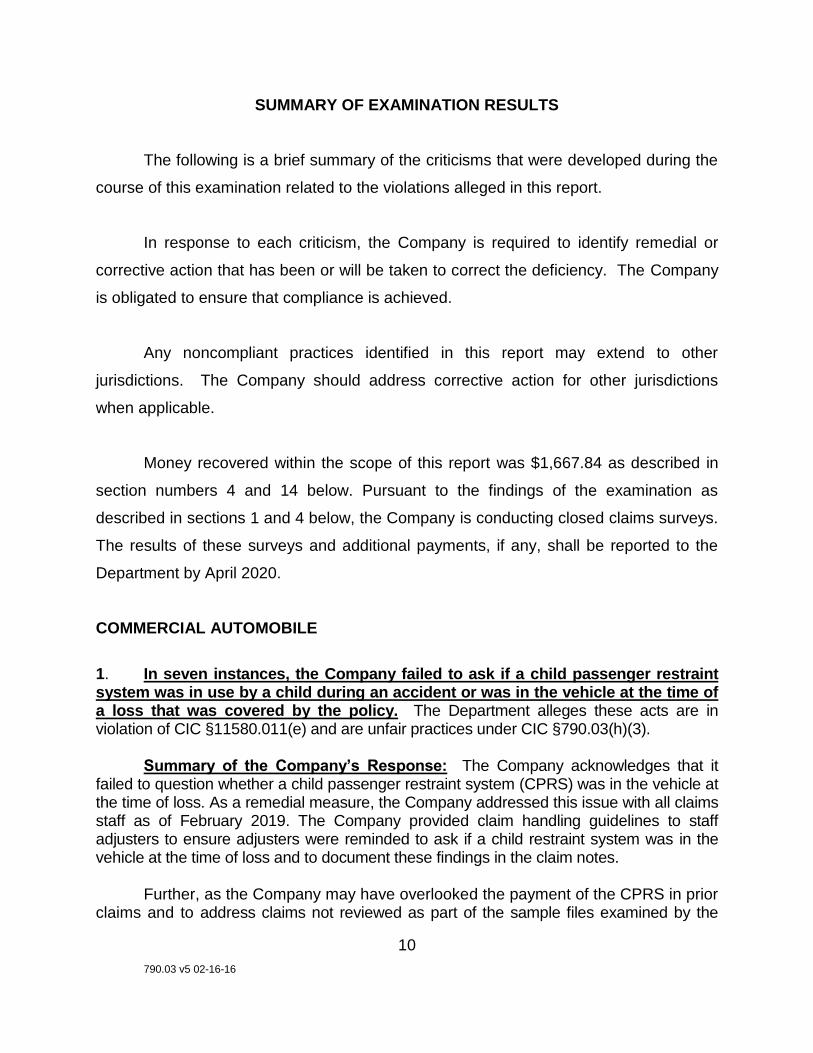

SUMMARY OF EXAMINATION RESULTS

The following is a brief summary of the criticisms that were developed during the

course of this examination related to the violations alleged in this report.

In response to each criticism, the Company is required to identify remedial or

corrective action that has been or will be taken to correct the deficiency. The Company

is obligated to ensure that compliance is achieved.

Any noncompliant practices identified in this report may extend to other

jurisdictions. The Company should address corrective action for other jurisdictions

when applicable.

Money recovered within the scope of this report was $1,667.84 as described in

section numbers 4 and 14 below. Pursuant to the findings of the examination as

described in sections 1 and 4 below, the Company is conducting closed claims surveys.

The results of these surveys and additional payments, if any, shall be reported to the

Department by April 2020.

COMMERCIAL AUTOMOBILE

1. In seven instances, the Company failed to ask if a child passenger restraint system was in use by a child during an accident or was in the vehicle at the time of a loss that was covered by the policy. The Department alleges these acts are in violation of CIC §11580.011(e) and are unfair practices under CIC §790.03(h)(3). Summary of the Company’s Response: The Company acknowledges that it failed to question whether a child passenger restraint system (CPRS) was in the vehicle at the time of loss. As a remedial measure, the Company addressed this issue with all claims staff as of February 2019. The Company provided claim handling guidelines to staff adjusters to ensure adjusters were reminded to ask if a child restraint system was in the vehicle at the time of loss and to document these findings in the claim notes.

Further, as the Company may have overlooked the payment of the CPRS in prior claims and to address claims not reviewed as part of the sample files examined by the

11

790.03 v5 02-16-16

CDI, the Company is conducting a three year internal audit for the period of February 2016 through February 2019 related to the requirements specified in CIC Section 11580.011(e). The findings of the internal audit, as well as additional payments, if any, will be provided to the Department by April, 2020. 2. In six instances, the Company failed to conduct its business in its own name. The correspondence sent to claimants identified the name of the Company’s Third Party Administrator (TPA), but did not identify the name of the underwriting insurer. The Department alleges these acts are in violation of CIC §880 and are unfair practices under CIC §790.03(h)(3). Summary of the Company’s Response: The Company acknowledges its correspondence did not include the name of ORIC, the underwriting insurer. Effective February 4, 2019, the system has been automated so that the Company’s name is shown on all correspondence sent to claimants. Further, the TPAs involved are all on notice of the requirements in CIC Section 880, and all have confirmed that ORIC’s name as the insurer is included on all insured/claimant correspondence going forward. The Company also conducted refresher training with staff from November 28, 2018 through December 28, 2018. 3. In five instances, the Company failed to conduct and diligently pursue a thorough, fair and objective investigation. Four instances involved delays in following up with the claimant or the claimant’s attorney to resolve Uninsured Motorist Bodily Injury claims. In one instance, the Company failed to follow its own procedures to request a police report for a collision claim. The Department alleges these acts are in violation of CCR §2695.7(d) and are unfair practices under CIC §790.03(h)(3). Summary of the Company’s Response: The Company acknowledges these findings. As a remedial measure, the Company communicated these findings with the respective supervisors and operational leads to monitor claims handling activities to ensure regulatory compliance. The Company’s TPAs also conducted refresher training with staff. The training, entitled Auto Liability Claims California State Regulations Training, was given by all California claims adjusters November 28, 2018 through December 28, 2018. 4. In five instances, the Company failed to comply with the requirements of CCR §2695.8(b)(1) as described below:

4(a). In two instances, the Company failed to include, in the settlement, the one-time fees incident to transfer of evidence of ownership of a comparable vehicle.

4(b). In two instances, the Company failed to include, the settlement, the

license fee and other annual fees computed based upon the remaining terms of the current registration.

12

790.03 v5 02-16-16

4(c). In one instance, the Company failed to include, in the settlement, all applicable taxes. The Department alleges these acts are in violation of CCR §2695.8(b)(1) and are unfair practices under CIC §790.03(h)(5). Summary of the Company’s Response to 4(a), 4(b) and 4(c): The Company acknowledges the findings in all of these identified claims. As a remedial measure, the Company reopened these identified claims and issued additional settlement payments of $386.84. The Company states the branch managers for the TPAs conducted staff training and provided written handouts and directions for handling total loss claim settlements. All instructions and changes were implemented by the Company and its TPAs as of February 2019.

Further, as the Company may have overlooked the payment of the sales taxes and vehicle fees in prior claims and to address claims not reviewed as part of the sample files examined by the CDI, the Company is conducting a three year internal self-audit for the period of February 2016 through February 2019 related to the requirements specified in CCR Section 2695.8(b)(1). In the event it is shown on any file that applicable taxes and fees were unpaid, the Company will issue additional payments. The findings of the internal audit, and additional payments, if any, will be reported to the Department by April 2020.

5. In four instances, the Company failed to respond to communications within 15 calendar days. The four claims involved Uninsured Motorist Bodily Injury coverage. The Company failed to acknowledge the claimants’ representatives’ request for coverage information or respond to payment demand requests. The Department alleges these acts are in violation of CCR §2695.5(b) and are unfair practices under CIC §790.03(h)(2). Summary of the Company’s Response: The Company acknowledges it failed to respond to the claimants’ attorneys for coverage information within 15 days. The Company states its procedure is to discuss and disclose all pertinent coverage information with the claimants’ representatives as applicable and follow-up with written correspondence. To ensure regulatory compliance, the Company conducted refresher training November 28, 2018 through December 28, 2018, to address timely communications in accordance with CCR Section 2695.5(b). 6. In two instances, the Company failed to include a statement in its claim denial that, if the claimant believes all or part of the claim has been wrongfully denied or rejected, he or she may have the matter reviewed by the California Department of Insurance. The Department alleges these acts are in violation of CCR §2695.7(b)(3) and are unfair practices under CIC §790.03(h)(3). Summary of the Company’s Response: The Company acknowledges its denial notices and email communications did not include the relevant CDI language on these identified claims. The Company states these were adjuster errors as the Company’s standard denial notice does include the required CDI language on all denied claims. As a remedial measure, the Company communicated these findings to the appropriate

13

790.03 v5 02-16-16

supervisors and operational leads to monitor claims handling activities to ensure regulatory compliance. The Company’s TPA also provided individual coaching to the claims adjusters and conducted refresher training with staff on November 9, 2018. 7. In two instances, the Company failed to provide written notice of the need for additional time or information every 30 calendar days. The Department alleges these acts are in violation of CCR §2695.7(c)(1) and are unfair practices under CIC §790.03(h)(3). Summary of the Company’s Response: The Company acknowledges these findings. As a remedial measure, the Company communicated these findings to the appropriate supervisors and operational leads to monitor claims handling activities to ensure regulatory compliance. 8. In one instance, the Company failed to provide necessary forms, instructions, and reasonable assistance within 15 calendar days. The Company failed to provide necessary forms, instructions, and reasonable assistance within 15 calendar days on a third party liability claim. The Department alleges this act is in violation of CCR §2695.5(e)(2) and is unfair practice under CIC §790.03(h)(3).

Summary of the Company’s Response: The Company acknowledges the claims adjuster did not reach out to the parties involved in the claim. The examiner and team leads involved were notified of this audit finding on August 2018. All parties were re-trained on California-specific requirements by taking the TPA’s self-paced training module entitled Auto Liability Claims California State Regulations Training. 9. In one instance, the Company failed to begin any necessary investigation of the claim within 15 calendar days. The Company failed to begin an investigation under a third party liability claim after receiving additional information including photographs from its own insured confirming the loss. The Department alleges this act is in violation of CCR §2695.5(e)(3) and is an unfair practices under CIC §790.03(h)(3). Summary of the Company’s Response: The Company acknowledges this finding, and has reviewed the TPA’s training module for California Auto/General Liability (GL) claims, and is satisfied that such training goes over in detail all of the requisite information necessary to successfully adjudicate a California auto/GL claim. The TPA’s training module is entitled Auto Liability Claims California State Regulations Training, and all individuals handling California claims completed the training between November 28, 2018 and December 28, 2018, to ensure that the TPA’s adjusters will comply with such requirements in the future.

In addition, the TPA re-opened the identified claim in order to comply with regulatory requirements. On February 19, 2019, to account for damage to the claimant’s side mirror the TPA sent a letter to the claimant to initiate contact and notify them of information needed for proof of claim. The new adjuster assigned to the claim will

14

790.03 v5 02-16-16

continue to monitor the claim in accordance with CCR Section 2695.5(e)(3), and related regulations. The Department will be notified of the results of this investigation, and if applicable, any settlement payments. 10. In one instance, the Company failed to explain in writing the determination of the cost of a comparable vehicle at the time the settlement offer was made. Determination of the actual cash value (ACV) was not explained. The Department alleges this act is in violation of CCR §2695.8(b)(4) and is an unfair practice under CIC §790.03(h)(3). Summary of the Company’s Response: The Company acknowledges the ACV valuation report was not sent with the settlement offer. As a result of the audit examination, the Company sent a copy of the valuation report to the claimant’s attorney on October 25, 2018. The Company also conducted training and provided a total loss template letter to claims staff on February 19, 2019.

11. In one instance, the Company determined the actual cash value (ACV) of the vehicle by utilizing more than one method described by CCR §2695.8(b)(4)(A). When comparable automobiles are available or were available in the local market area in the last 90 days, the average cost of two or more such comparable automobiles shall be used. The Company used 16 comparable vehicles of which only the first three listed were in the local market of San Diego. The remaining vehicles were over 100 miles or more away. The Department alleges this act is in violation of CCR §2695.8(b)(4)(A), and is an unfair practice under CIC §790.03(h)(3). Summary of the Company’s Response: The Company states an outside appraiser was used to obtain the valuation report and it was the appraiser that went outside of the local market. The Company states, in this instance, although vehicles were used outside of the local market, the claimant was made whole in the total loss settlement due to the GAP coverage on the policy. The Company believes this to be a one-time occurrence, due to the uniqueness of the vehicle. Going forward, the Company will ensure that any appraiser, either independent or in-house, is aware of the State’s regulations pursuant to CCR §2695.8(b)(4)(A). 12. In one instance, the Company failed to notify the insured that the file will be reopened if the Company is notified within 35 days that the insured cannot purchase a comparable automobile for the settlement amount offered or paid. The Department alleges this act is in violation of CCR §2695.8(c) and is an unfair practice under CIC §790.03(h)(3). Summary of the Company’s Response: The Company acknowledges the insured was not notified at the time of settlement that the file would be reopened if the Company is notified within 35 days that the insured cannot purchase a comparable automobile for the settlement amount offered or paid. The Company, through its servicing Third Party Administrator, sent a letter to the insured on January 23, 2019,

15

790.03 v5 02-16-16

which stated the insured’s rights under CCR Section 2695.8(c). The TPA is monitoring for a response to the same. The Company also sent an email on February 19, 2019, to the claims team discussing the audit results, and notifying the team that it needs to use this notification letter as a template going forward on all future first party total loss settlements when addressing the insured’s rights pursuant to CCR Section 2695.8(c). 13. In one instance, the Company failed to provide the insured with the Auto Body Repair Consumer Bill of Rights either at the time of application for automobile insurance, at the time a policy was issued, or following an accident. The Department alleges this act is in violation of CCR §2695.85(a) and is unfair practice under CIC §790.03(h)(3). Summary of the Company’s Response: The Company acknowledges this finding and states this letter is system generated. It is the Company’s practice to send the Auto Body Repair Consumer Bill of Rights notice at the time policies are issued. In this instance, the Company states the letter failed to generate due to invalid data and the adjuster did not regenerate the letter. To correct this error, the Company initiated a system diary trigger that will notify the handling examiner of a letter failure. Further, the Company also communicated this issue to the appropriate supervisors and operational leads to monitor claims handling activities to ensure regulatory compliance. 14. In one instance, the Company failed to amend the premium charged to the insured to reflect the current exposure following the total loss of the vehicle that previously served as the exposure basis for rating purposes. No rate shall remain in effect which is excessive, inadequate, unfairly discriminatory or otherwise in violation of Chapter 9, Article 10 of the California Insurance Code. The Department alleges this act is in violation of CIC §1861.05(a) and is an unfair practice under CIC §790.03(h)(5). Summary of the Company’s Response: The Company states the policy is an auditable policy and it does not add or delete vehicles during the course of the policy period. The Company determines the final number of vehicles at the end of the policy term and used an average of the beginning and ending counts to calculate the final premium. After further review, the Company noted the total loss vehicle was included on the vehicle list that was received from the insured. The Company states this was an inadvertent oversight and has issued the insured an unearned premium refund for $1,281.00 on November 13, 2018.

The Company revised its communications to its premium audit vendors, reinforcing their responsibility to obtain accurate vehicle lists at audit to ensure that the Company can account for the correct number of autos and calculate the appropriate amount of premium. These changes will be fully implemented and will impact the Company’s May 1, 2019 policy expirations.

The Company states although this one instance has been identified in the exam,

16

790.03 v5 02-16-16

it believes the process is working well overall and this particular instance was an outlier. With respect to the audit, the Company relies on its insureds to provide their vehicle counts and listing of autos. The insured, in this case, provided a listing of the autos at audit and had inadvertently included the totaled auto. The insureds normally are sure to remove any deleted autos from their final audit exposure to ensure they are paying the right premium for their exposure. To reinforce this, the Company enhanced its instructions to the audit vendor (the Company currently uses one audit vendor), to prompt additional focus on added and deleted autos to ensure it is capturing the correct exposure. The Company also enhanced its notice of audit to the insured as a reminder to update any added and deleted autos. The Company provided the Department with a copy of its updated instructions to its policyholders on April 4, 2019. 15. In one instance, the Company misrepresented to claimants pertinent facts or insurance policy provisions relating to any coverages at issue. The Company misrepresented its procedures practices regarding disclosure of policy coverage and benefits pertaining to a liability claim. The Department alleges this act is in violation of CIC §790.03(h)(1). Summary of the Company’s Response: The Company acknowledges the claims handler erred in statements made to the claimant’s authorized representative. The claims handler received individual counseling and coaching to ensure statutory compliance. WORKERS’ COMPENSATION:

There were no alleged violations or criticisms of insurer practices made within the

scope of this report in the Workers’ Compensation category of claims.

Related Documents

![Oslobođenje [broj 24147, 25.2.2014]](https://static.cupdf.com/doc/110x72/577ccf8f1a28ab9e789009e8/oslobodenje-broj-24147-2522014.jpg)