Oklahoma and health reform Grace-Marie Turner Galen Institute August 12, 2008

Oklahoma and health reform Grace-Marie Turner Galen Institute August 12, 2008.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Oklahoma andhealth reform

Grace-Marie TurnerGalen Institute

August 12, 2008

Who are the Who are the uninsured?uninsured?

Workers transitioning between jobsWorkers transitioning between jobs Small business employeesSmall business employees Workers in low-wage jobs and their Workers in low-wage jobs and their

dependentsdependents Young adultsYoung adults Minorities, especially HispanicsMinorities, especially Hispanics Undocumented workersUndocumented workers

Uninsured rates in 2006

*According to the U.S. Census Bureau press release on the Current Population Survey, “the rates for Minnesota, Hawaii, Iowa, Wisconsin and Maine were lower than the rates of the other 45 states and the District of Columbia. The rates for these five states were not statistically different from one another.”

Source: U.S. Census Bureau, Current Population Survey, 2007 Annual Social and Economic Supplement. Last revised: August 28, 2007. http://pubdb3.census.gov/macro/032007/health/h06_000.htm.

NumberNumber PercentPercent

Wisconsin*Wisconsin* 481,000481,000 8.88.8

Oklahoma Oklahoma 661,000661,000 18.918.9

TexasTexas 5,704,0005,704,000 24.524.5

United StatesUnited States 46,995,00046,995,000 15.815.8

Income distributionState Median Annual Income

Wisconsin $48,874

Oklahoma $40,001

Texas $43,425

U.S. $46,071

Oklahoma’s health insurance marketOklahoma’s health insurance market

36 coverage mandates. (Idaho has the 36 coverage mandates. (Idaho has the fewest with 14. Maryland the most w/ 60)*fewest with 14. Maryland the most w/ 60)*

Oklahoma does not require Oklahoma does not require guarantee issueguarantee issue. . ME, MA, NV, NJ, NY, VT require all health ME, MA, NV, NJ, NY, VT require all health plans to guarantee issuance to individuals **plans to guarantee issuance to individuals **

Oklahoma has modified Oklahoma has modified community ratingcommunity rating in in the individual market; NJ, NY, VT require the individual market; NJ, NY, VT require full community rating for all individual policies full community rating for all individual policies

* http://www.cahi.org/cahi_contents/resources/pdf/HealthInsuranceMandates2008.pdf **Summary of State Guarantee Issue and Rating Requirements. America’s Health Insurance Plans. December 2007.

Cost of mandatesCost of mandates

MandatedMandated benefits currently increase the benefits currently increase the cost of basic health coverage from a little cost of basic health coverage from a little less than 20% to more than 50%, less than 20% to more than 50%, depending on the state and its mandates.*depending on the state and its mandates.*

Numerous mandates and heavy Numerous mandates and heavy regulations drive up costs. New Yorkers regulations drive up costs. New Yorkers pay on average 3.5 times as much as pay on average 3.5 times as much as residents of Iowa for insurance. ($98 vs. residents of Iowa for insurance. ($98 vs. $338)**$338)**

*“Health Insurance Mandates in the States 2008,” Council for Affordable Health Insurance, January 2008. *“Health Insurance Mandates in the States 2008,” Council for Affordable Health Insurance, January 2008. www.cahi.org**”The Cost and Benefits of Individual Health Insurance Plans: 2007” Forrester Research based upon eHealthInsurance data**”The Cost and Benefits of Individual Health Insurance Plans: 2007” Forrester Research based upon eHealthInsurance data

Cost of individual insurance

I could buy a $3,000 deductible policy in I could buy a $3,000 deductible policy in Oklahoma City for $200/mo. on Oklahoma City for $200/mo. on eHealthInsurance.com*eHealthInsurance.com* The most expensive is The most expensive is $400/mo. for a PPO with a $1,000 deductible. $400/mo. for a PPO with a $1,000 deductible. Choice of 10 plan options. Someone 20 years Choice of 10 plan options. Someone 20 years younger would pay $100/mo. for a higher younger would pay $100/mo. for a higher deductible plan and $275/mo. for a lower-deductible plan and $275/mo. for a lower-deductible policy.deductible policy.

eHealthInsurance says the average individual eHealthInsurance says the average individual policy nationwide costs $148 a month.policy nationwide costs $148 a month.

* http://www.ehealthinsurance.com

Costs of Job-Based Insurance

Individual

– Oklahoma $4,088

– U.S. $3,991

Family

– Oklahoma $10,985

– U.S. $10,728

Kaiser Family Foundation, State Health Facts 2005. www.statehealthfacts.org

Many states believe that a Many states believe that a high uninsured rate impacts high uninsured rate impacts

the business climate and the business climate and quality of life for citizens.quality of life for citizens.

Pressure for government to fill the gap:

$0 $75,000Income

Massachusetts Massachusetts and universal coverageand universal coverage

Former Gov. Mitt Former Gov. Mitt Romney worked with Romney worked with Democratic legislators Democratic legislators to pass sweeping to pass sweeping health reformhealth reform

How is it working out?How is it working out?

Massachusetts Healthcare ReformMassachusetts Healthcare Reform

Medicaid money was the impetus for creating Medicaid money was the impetus for creating the MA Health Reform Plan the MA Health Reform Plan

The state stood to lose $385 million in The state stood to lose $385 million in uncompensated care funds if it didn’t take uncompensated care funds if it didn’t take action on reformaction on reform

Therefore, the Republican governor, Therefore, the Republican governor, Democratic legislature, hospitals, businesses Democratic legislature, hospitals, businesses and other interest groups were highly and other interest groups were highly motivated to develop a planmotivated to develop a plan

Positive aspects of the MA planPositive aspects of the MA plan

The health insurance “Connector” allows workers to The health insurance “Connector” allows workers to purchase insurance from competing private insurerspurchase insurance from competing private insurers

Those with incomes up to 300% of poverty receive Those with incomes up to 300% of poverty receive subsidies to buy coverage subsidies to buy coverage

Employees can purchase health insurance with pre-Employees can purchase health insurance with pre-tax dollarstax dollars

Insurance is portable and can move with a worker Insurance is portable and can move with a worker from job to jobfrom job to job

The plan addresses the “free rider” problem by The plan addresses the “free rider” problem by mandating that everyone must be in the systemmandating that everyone must be in the system

Danger points of Massachusetts’ planDanger points of Massachusetts’ plan

The state has imposed a mandate on individuals The state has imposed a mandate on individuals to purchase insurance while leaving in place to purchase insurance while leaving in place rules and mandates that have driven out rules and mandates that have driven out competition and driven up costs, such as competition and driven up costs, such as guaranteed issue and more than 40 coverage guaranteed issue and more than 40 coverage mandates. mandates.

The only policies that will be offered through the The only policies that will be offered through the state program to those under 300% of poverty state program to those under 300% of poverty eligible for a new state subsidy have no eligible for a new state subsidy have no deductible and must cover all mandates.deductible and must cover all mandates.Only offered by Medicaid HMOs.Only offered by Medicaid HMOs.

Dangers for companiesDangers for companiesEmployers face stiff penalties if they do not offer Employers face stiff penalties if they do not offer access to insurance. access to insurance.

The legislature inserted in the law a provision that The legislature inserted in the law a provision that forces employers with 11 or more employees to forces employers with 11 or more employees to pay a $295 per-employee fine if they don’t pay a $295 per-employee fine if they don’t offer offer access toaccess to health insurance and to pay health costs health insurance and to pay health costs above $50,000 for their uninsured workers who above $50,000 for their uninsured workers who seek free care.seek free care.

Individual mandates quickly become employer Individual mandates quickly become employer mandates. Employers must pay at least one-third mandates. Employers must pay at least one-third of premium costs, and legislators are considering of premium costs, and legislators are considering boosting their required shareboosting their required share

Bureaucracy and enforcementBureaucracy and enforcement

The law requires every employer and employee in the The law requires every employer and employee in the state to sign "under oath" a Health Insurance state to sign "under oath" a Health Insurance Responsibility Disclosure form. Responsibility Disclosure form.

It creates at least 10 new boards and commissions, such It creates at least 10 new boards and commissions, such as the Health Care 10 Quality and Cost Council, the as the Health Care 10 Quality and Cost Council, the Payment Policy Advisory Board, and the Health Access Payment Policy Advisory Board, and the Health Access Bureau. Bureau.

New and existing state agencies will be checking on New and existing state agencies will be checking on individuals' insurance status, monitoring their income to individuals' insurance status, monitoring their income to see if they qualify for subsidies, and tracking individual see if they qualify for subsidies, and tracking individual health habits (like smoking and wellness activities). health habits (like smoking and wellness activities).

Pushback from individual mandatePushback from individual mandate

““The dreaded Individual Mandate Call (IMC) The dreaded Individual Mandate Call (IMC) usually begins, ‘I’m uninsured. I heard that a usually begins, ‘I’m uninsured. I heard that a new law says that everyone in Massachusetts new law says that everyone in Massachusetts has to have health insurance by July 1st or they has to have health insurance by July 1st or they could get fined on their taxes.’ could get fined on their taxes.’ ““People are angry and, at times, very angry. People are angry and, at times, very angry. Earlier today, a caller responded, ‘So you mean Earlier today, a caller responded, ‘So you mean to tell me that I’m punished even though I only to tell me that I’m punished even though I only have $10 left each month for food after I pay my have $10 left each month for food after I pay my bills?’ Then she violently hung up on me…We bills?’ Then she violently hung up on me…We hear this story often.”hear this story often.”

Massachusetts’ Health Care for All Helpline blogger Massachusetts’ Health Care for All Helpline blogger Kate BicegoKate Bicego

Massachusetts ConnectorMassachusetts Connector

Four premium levels for same coverage through Four premium levels for same coverage through the subsidized Commonwealth Care program the subsidized Commonwealth Care program

Six health insurance plans offer coverage Six health insurance plans offer coverage through the unsubsidized Commonwealth through the unsubsidized Commonwealth Choice planChoice plan

Many continue to be covered under job-based Many continue to be covered under job-based plansplans

Largest enrollment in no-cost plansLargest enrollment in no-cost plansEnrollment by Plan Type as of May 1st

Total: 176,879 enrolled individuals

Type 1 (0-100% FPL), 79,039,

45%

Type 2A (100-150% FPL),

47,469, 27%

Type 2B (150-200% FPL),

29,234, 17%

Type 3 (200-300% FPL, low

premium), 16,716, 9%

Type 4 (200-300% FPL, low copays), 4,421,

2%

Commonwealth Care Commonwealth Care Enrollment Nov ‘06 – Dec ‘07Enrollment Nov ‘06 – Dec ‘07

Enrollment (thousands) as of the first of the month

0

20

40

60

80

100

120

140

160

Nov '06 Dec '06 J an '07 Feb '07 Mar '07 Apr '07 May '07 J un '07 J ul '07 Aug '07 Sep '07 Oct '07 Nov '07 Dec '07

Premium-paying

No premium

Commonwealth Care Commonwealth Care Enrollment Sept ‘07 – May ‘08Enrollment Sept ‘07 – May ‘08

Enrollment (thousands) as of the first of the month

0

50

100

150

200

Sep '07 Oct '07 Nov '07 Dec '07 J an '08 Feb '08 Mar '08 Apr '08 May '08

Premium-payingNo premium

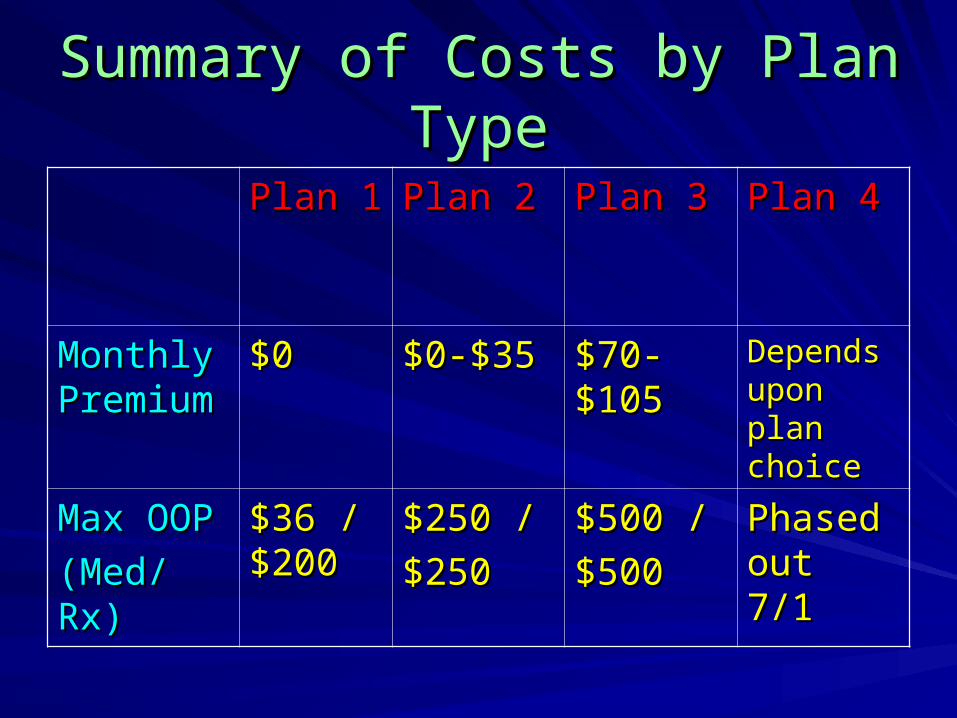

Summary of Costs by Plan TypeSummary of Costs by Plan Type

Plan 1Plan 1 Plan 2Plan 2 Plan 3Plan 3 Plan 4Plan 4

Monthly Monthly PremiumPremium

$0$0 $0-$35$0-$35 $70-$70-$105$105

Depends Depends upon plan upon plan choicechoice

Max OOPMax OOP

(Med/Rx)(Med/Rx)

$36 / $36 / $200$200

$250 /$250 /

$250$250

$500 /$500 /

$500$500

Phased Phased out 7/1out 7/1

Enrollment in Enrollment in Commonwealth ChoiceCommonwealth Choice

14,69815,922

17,161 17,490 17,907 18,122

0

5,000

10,000

15,000

20,000

Dec '07 Jan '08 Feb '08 Mar '08 Apr '08 May '08

1. Enrollment (members) as of the first of the month

Typical connector pricesTypical connector prices

CoverageCoverage Annual premiumAnnual premium

Young adultYoung adult $$2,0002,000 deductible deductible $2,280$2,280

HMO/ no ded.HMO/ no ded. $6,096$6,096

Young familyYoung family $1,500/$3,000 ded.$1,500/$3,000 ded. $7,200$7,200

HMO/ low ded.HMO/ low ded. $18,300$18,300

Empty-nest coupleEmpty-nest couple $2,000/$4,000 ded.$2,000/$4,000 ded. $7,800$7,800

HMO/ no ded.HMO/ no ded. $21,804$21,804

Risks moving forwardRisks moving forward

For consumers…For consumers…– State approved a 12% insurance rate increase State approved a 12% insurance rate increase

for next yearfor next year– Fines to individuals continue to riseFines to individuals continue to rise

$219 in first year$219 in first year

Up to $912 this year; $1,824 for uninsured couplesUp to $912 this year; $1,824 for uninsured couples– Shortage of doctors in some areas taking new patientsShortage of doctors in some areas taking new patients

Rising costs for taxpayersRising costs for taxpayers

Crowd-out of job-based insuranceCrowd-out of job-based insurance

Taxpayer costs are risingTaxpayer costs are rising

State budget calls for $869 million in fiscal State budget calls for $869 million in fiscal 2009, but the bill could be closer to $1.1 billion2009, but the bill could be closer to $1.1 billion

About 330,000 Massachusetts residents are About 330,000 Massachusetts residents are newly enrolled in coverage, but at least 263,000 newly enrolled in coverage, but at least 263,000 are in free or subsidized plansare in free or subsidized plans

A new study shows that mandates add $1.3 A new study shows that mandates add $1.3 billion to the cost of health insurance a yearbillion to the cost of health insurance a year

2929

2008 Draft Affordability Schedule 2008 Draft Affordability Schedule Proposed March 20Proposed March 20thth

Individuals Couples Families

Annual Gross Income Range

2008 Proposed

Annual Gross Income Range

2008 Proposed

Annual Gross Income Range

2008 Proposed

$0 - $15,612 (150%) $0 $0 - $21,012 (150%) $0 $0 - $26,412 (150%) $0

$15,613 - $20,808 (200%) $39 $21,013 - $28,008 (200%) $78 $26,413 - $35,208 (200%) $78

$20,809 - $26,016 (250%) $77 $28,009 - $35,016 (250%) $154 $35,209 - $44,016 (250%) $154

$26,017 - $31,212 (300%) $116 $35,017 - $42,012 (300%) $232 $44,017 - $52,812 (300%) $232

$31,213 - $37,500 (360%) $165 $42,013 - $52,500 (375%) $297 $52,813 - $70,000 (398%) $352

$37,501 - $42,500 (408%) $220 $52,501 - $62,500 (446%) $396 $70,001 - $90,000 (511%) $550

$42,501 - $52,500 (505%) $330 $62,501 - $82,500 (589%) $550 $90,001 - $110,000 (625%) $792

>$52,501 n/a >$82,501 n/a >$110,001 n/a

So what is the alternative?So what is the alternative?

The Vision:The Vision:

Engaging consumers as Engaging consumers as partners in managing health partners in managing health costs and getting the best costs and getting the best valuevalue for health care dollars for health care dollars

Common themes

Focus on:

Personal responsibility by recipientsIncentives for patient participation Wellness and prevention services Better coordination of careGreater focus on disease management Data collection and outcomes reports

Some tools available now

Flexible Spending Accounts – available since the mid ‘80s

– “Use it or lose it” flaw

Health Reimbursement Arrangements– Created in 2002

Health Savings Accounts – Available since 2004

Top three priorities for reformTop three priorities for reform

Lighten the regulatory burden on health Lighten the regulatory burden on health insurance and services to boost insurance and services to boost competitioncompetition

Allow greater portability of health insuranceAllow greater portability of health insurance

Provide new subsidies for the uninsuredProvide new subsidies for the uninsured

An innovative program:An innovative program:The Healthy Indiana PlanThe Healthy Indiana Plan

A novel way of increasing access to health A novel way of increasing access to health insurance for the uninsuredinsurance for the uninsured

A jointly-funded POWER account -- $1,100A jointly-funded POWER account -- $1,100

Medicaid coverage for medical costs above Medicaid coverage for medical costs above that, including preventive care that, including preventive care

Unused POWER balances roll over to help Unused POWER balances roll over to help fund next year’s accountfund next year’s account

Georgia’s new law

Allow individuals to deduct HSA premiums from state taxes

$250 annual tax credit to small businesses to enroll employees in HSA plans

Allow insurance companies to reward people for healthy behavior

Federal proposalsFederal proposals

Give individuals and families tax Give individuals and families tax deductions or credits to purchase private deductions or credits to purchase private health insurancehealth insurance

Allow people to buy health insurance from Allow people to buy health insurance from other statesother states

Create more options for people to use Create more options for people to use SCHIP and Medicaid dollars for private SCHIP and Medicaid dollars for private coveragecoverage

What will the future hold?Elections will determine the

direction of change. But…

The new president will definitely determine the direction of reform, toward a greater role for government in our health sector or a much more functional private and competitive market for health insurance and health care

Related Documents