1 Oil & Natural Gas: The Evolving Freight Transportation Impacts Prepared for July 30, 2013 Jackson Hole, WY GE Capital Q3 All Employee Meeting Logis&cs Engineering Supply Chain CIT Rail Resources Conference

Oil & Natural Gas. The Evolving Freight Transportation Impacts

Jul 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Oil & Natural Gas: The Evolving Freight Transportation Impacts Prepared for

July 30, 2013 Jackson Hole, WY

GE Capital Q3 All Employee Meeting

Logis&cs Engineering Supply Chain

CIT Rail Resources Conference

2

» Boutique consulting firm specializing in logistics, engineering, and supply chain § Established in 2001 § Over 100 clients and 250 engagements

» Headquarters in Chicago USA, with team members throughout the US and with “on the ground” experience in: § North America / Europe / South America / Asia / Middle East

» Consulting services § Strategy & optimization § Assessments & benchmarking § Transportation assets & infrastructure § Logistics operations § M&A/investments/private equity

» Key industry verticals § Oil & gas § Chemicals & plastics § Wind energy & project cargo § Bulk commodities (minerals, mining, agricultural) § Industrial manufactured goods § Private equity

About PLG Consulting

3

The Shale Development Revolution – Big Picture

Disruptive Technologies

• Hydraulic Fracturing • Horizontal Drilling

Continuous Evolution

• Constant Change • Rapid Change

Market Dynamics • Supply & Demand • Customers • Price • Logistics

3

4

Hydraulic Fracturing and Horizontal Drilling

» Rapid evolution of drilling technology § Fracking first used in 1947 § Revolutionary advances since 2009 § Time required for drilling 15,000+ ft. well cut in half in last

two years (nine days vs. 18) § Dramatic increase in efficiency per rig, making rig count

alone no longer a significant indicator of production § Hydraulic fracturing/horizontal drilling yields 3-10x the

initial production rate of conventional wells

» US uniquely positioned for the techniques § Private mineral rights § Drilling intensity (wells per acre) § 90% of rig fleet equipped for horizontal drilling

» Rapid ROI for E&P companies § Typical well earns back capital cost in 1-2 years § Depending on play productivity, “break even” point of

$40-85/bbl § Liquid plays providing highest returns

Source: L. Maugeri, Harvard Kennedy School; RBN; PLG analysis

5

Representative Productivity Gains – Fayetteville Shale Play

Source: Southwestern Energy investor presentation, June 2013

6

Shale Driving Growth in Natural Gas and Crude Oil Production

Source: Baker Hughes 2013

GAS OIL THERMAL

Source: Baker Hughes

U.S. Crude Oil Production

Source: EIA

April 2013 7.35 MM bpd

» 1,759 rigs in operation in USA as of June 21, 2013

» Dramatic production growth § 700% increase in gas production since 2007; forecast to grow 9

Bcf/d from 2012-2018 § Domestic oil production at 21 year high; forecast to reach 10MM

bbl/d by 2018

» IEA projects US to surpass Saudi Arabia in oil output, Russia in gas output by 2020

7

US Shale Plays

Gas: Marcellus Haynesville Barnett Oil: Bakken Eagle Ford Permian Basin

Most Active Plays

Utica (NGLs) Niobrara Mississippi Lime

Emerging Plays

8

Shale Development Supply Chain and Downstream Impacts

Feedstock (Ethane)

Byproduct (Condensate)

Home Heating (Propane)

Other Fuels

Other Fuels

Gasoline

Inputs >> Wellhead >> Direct Output >> Thermal >> Fuels >> Raw Materials >> Downstream Products

Gas

NGLs

Crude

Proppants

OCTG

Chemicals

Water

Cement

Generation Process Feedstocks

All Manufacturing

Steel

Fertilizer (Ammonia)

Methanol

Chemicals

Petroleum Products

Petrochemicals

» Over $95B in new announced “energy intensive” industrial plant expansions will come on-line over the next five years » Shale development impact on the railcar industry is long-term, wide-ranging, and positive with only one exception

9

Hydraulic Fracturing Materials Inputs and Logistics – Per Well

Materials

Chemicals

Clean Water/ Cement

Proppants

OCTG (Pipe)

Source to Transloading

2

Local source

40

5

Transloading to Wellhead Site

8

~1,000

160

20

47 Total Railcars

~1,200 Total Truckloads

Oil/Gas/NGLs

Truck, Rail, Pipeline

Waste Water

~500 Total Truckloads

10

Correlation of Operating Rig Count with Sand and Crude Shipments

STCC 14413 (sand) and 13111 (petroleum) Source: US Rail Desktop, Baker Hughes

1,695

1,814

1,270

886 939

1,073

1,299

1,467

1,604 1,665 1,691

1,798

1,911 1,972 1,948 1,965

1,864 1,763 1,762 1,759

0

500

1,000

1,500

2,000

2,500

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2007 Avg. 2008 Avg. 2009 2010 2011 2012 2013

Ope

ratin

g O

nsho

re R

igs

Car

load

s

Operating On Shore Rigs All Sand Carloads Petroleum Carloads

11

All Sand Handled by Railroad

STCC 14413 Source: US Rail Desktop

12

» Wisconsin sand mining industry § 72 operational frac sand mines § 20 in development, 13 permitted, and 17

proposed § New applications are still coming in for new

mines

» Minnesota silica sand mining § 17 active frac sand mining facilities § Over 20 facilities in the planning stages

» Large barriers to entry § 1 - 3 years to find, permit, and start § Transportation key to success

» Industry consolidation continues § Focus on integrated supply chain

(US Silica)

Sand Mining Frac Sand Industry Across Wisconsin, May 1, 2013

Source: WisconsinWatch.org

Source: MPR News

Minnesota Frac Sand Mining, May 1, 2013

12 Source: WisconsinWatch.org, MPR News, May 2013

13

Processed Sand Total Delivered Cost

Source: PLG analysis

» Benchmark cost with well-executed performance § Example unit train movement from

Wisconsin to Texas with total delivered cost of approx. $180/ton

§ Logistics drives ~60% of total delivered sand cost

» Potential for significant cost add-ons caused by strategic and tactical issues

§ Sub-optimal logistics network design or infrastructure - Manifest service (rail) - Multi-carrier vs. single line haul (rail) - Equipment/driver shortages

§ Poor planning and/or execution - Rail and/or truck demurrage costs – Performance penalties

§ Uncompetitive sand price § Poor sand quality

14

Changes in Sand Logistics Model and Costs

» Rail rate advantage for volume and unit train vs. manifest service § On a per-ton basis between Wisconsin and Texas, spreads are 17-29%

» Western carriers are driving single line hauls and encouraging longer trains to Eagle Ford via pricing differentials

» Canadian and Eastern carriers are aggressively working to grow their markets by providing very competitive pricing and securing sand originations § CN/Superior Silica Sands – Poskin (Barron), WI

» Major sand providers establishing “in the play” transloading facilities to provide ready access to product § U.S. Silica - East Liverpool, OH § U.S. Silica – San Antonio, TX § Potential 2nd facility under consideration in San Antonio, TX

» Post-boom market maturation Source: PLG analysis

15

Sand Railcar Market Conditions

» Conditions are normalizing § Builder backlog has been resolved

– Wait time is now attributable to other car types in the pipeline

§ Many surplus cars have found homes § 2013 total production of sand cars will be closer to the

historical average of 2,000 – 3,000 units

» Lease market settling into familiar patterns § Traditional pricing behavior: Newer/286k cars more

expensive than older/263k cars § Cars with sub-optimal design (i.e. older grain cars) being

flushed out and replaced where possible § Lessors placing modest “spec” orders § Credit-worthiness of lessee is still a critical criteria § Market is still trying to find its feet

» Looking forward § Positive developments in housing/construction should

equate to additional demand for small cube hoppers § General optimism that demand from sand shippers may

also strengthen

16

Shale Play Product Flows Outbound

» Natural Gas § Majority via pipelines, some trucks

» Natural Gas Liquids (NGLs) § Requires processing (fractionation) § 3-9 gallons/MCF (thousand cubic feet)

– Ethane ~42-65% – Propane ~28% – Normal Butane ~8% – Iso-Butane ~9% – Condensate ~13%

» Crude Oil § Bakken play as a model § Surging Permian and Eagle Ford development

17

Shale Development Natural Gas Impacts

» Industry a “victim of its own success” § Fracking results in oversupply; gas prices down

33% since 2010 § Breakeven gas price at 10% IRR: ~$3.25 mm/btu § Rigs leave Marcellus, other gas plays for oil plays

(~700 “non producing” wells in PA) § Helped to deflate frac sand boom

» Lower gas prices have resulted in 10-13% market share capture from coal for thermal generation

» Low gas prices fueling industrial

renaissance § Overall manufacturing (cost of electricity; “re-

shoring”) § Specific sectors that use natural gas as a

feedstock – Methanol (16MM m/t new capacity under consideration) – Steel – Fertilizer

17 Source: RBN, PLG analysis

Source: RBN

18

Source: EIA, Deloitte

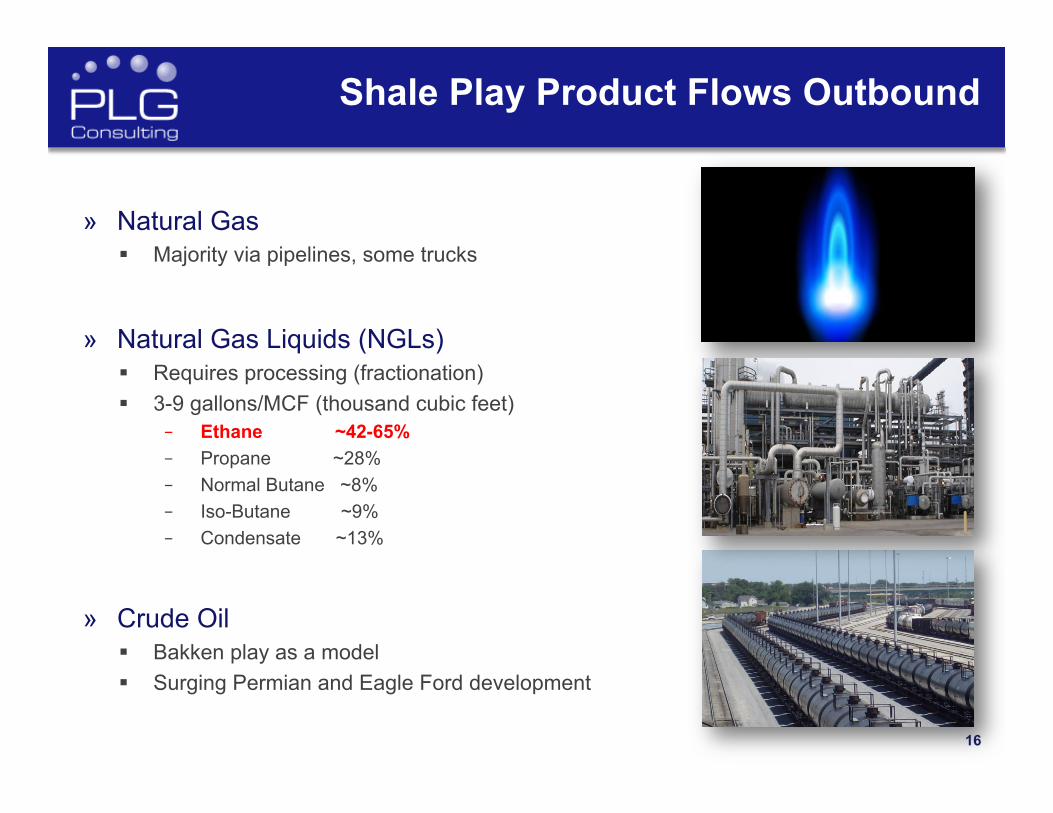

Natural Gas Displacement of Coal for Thermal Generation

» Natural gas now supplying approx. 30% of thermal fuel demand (~13% share capture from coal)

» Despite recent increases in prices, natural gas

share capture expected to maintain or grow § Environmental regulations of coal burning § Scheduled coal unit retirements § Eastern US transition through 2018: 18GW coal retirements

vs. 26GW of new natural gas plants under development

» Adversely affecting coal industry, railroad coal loadings

18 Source: RBN Energy, June 2013

Fuel Cost Comparison for Electricity Generation

Source: Bentek, PLG analysis

19

Shale Related Rail Traffic Still Small Relative to Coal Volumes

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2008

2009

2010

2011

2012

2013

Sand Crude

Coal

Car

load

s

Quarterly Data

Sand

Crude

Coal

STCC 14413 (sand), 13111 (petroleum), 11212 (coal) Source: US Rail Desktop

Railcars Handled: Sand, Crude, & Coal

20

Coal, Crude & Sand Trends: Carloads and Revenue

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

-

1

2

3

4

5

6

7

8

9

10

2008 2009 2010 2011 2012

Bill

ions

Mill

ions

Carloads Revenue

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

-

100

200

300

400

500

600

700

800

900

2008 2009 2010 2011 2012

Bill

ions

Thou

sand

s

Sand Crude Revenue

STCC 14413 (sand), 13111 (petroleum), 11212 (coal) Source: US Rail Desktop

Total Coal Carloads and Revenue Combined Sand and Crude Carloads and Revenue

21

Shale Gas Driving Steel Manufacturing Comeback in US

» Shale gas boom makes direct-reduced iron steel economical § Not new technology, but preferable with lower cost natural gas § DRI process uses natural gas in place of coal to produce iron § Cost of production 20% lower per ton vs. traditional blast furnace

» U.S. jobs and international investment § Steel production in the U.S has shrunk 13% since Jan. 2008 – Compare to 20% growth in steel production internationally

§ At least five new DRI steel plants being considered in the U.S. – now economical for the first time in 30 years due to low cost of natural gas

§ Both domestic and international firms investing in the technology

» Reciprocal growth § Increased demand for U.S. steel creates greater demand for U.S. gas § Tubular steel products has 8% yearly growth in demand, driven by

increase in shale oil and gas (Oilprice.com) § Joint venture between Nucor Corp. and Encana Corp. commits $3

billion to development of new gas wells to support DRI plants § Voestalpine $740MM investment in Texas § Potential US Steel-Republic Steel JV to produce DRI § DRI-derived steel of higher quality than that created from recycled

scrap, further driving demand

Source: World Steel Association

22

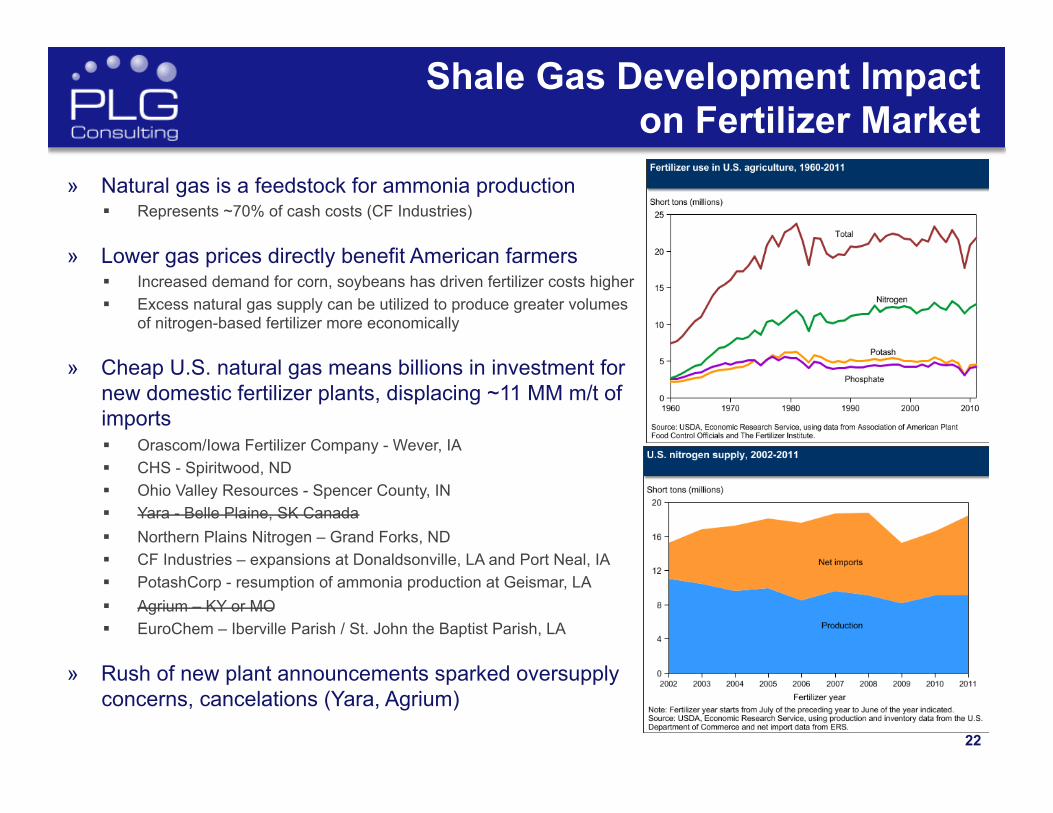

Shale Gas Development Impact on Fertilizer Market

» Natural gas is a feedstock for ammonia production § Represents ~70% of cash costs (CF Industries)

» Lower gas prices directly benefit American farmers § Increased demand for corn, soybeans has driven fertilizer costs higher § Excess natural gas supply can be utilized to produce greater volumes

of nitrogen-based fertilizer more economically

» Cheap U.S. natural gas means billions in investment for new domestic fertilizer plants, displacing ~11 MM m/t of imports § Orascom/Iowa Fertilizer Company - Wever, IA § CHS - Spiritwood, ND § Ohio Valley Resources - Spencer County, IN § Yara - Belle Plaine, SK Canada § Northern Plains Nitrogen – Grand Forks, ND § CF Industries – expansions at Donaldsonville, LA and Port Neal, IA § PotashCorp - resumption of ammonia production at Geismar, LA § Agrium – KY or MO § EuroChem – Iberville Parish / St. John the Baptist Parish, LA

» Rush of new plant announcements sparked oversupply concerns, cancelations (Yara, Agrium)

23

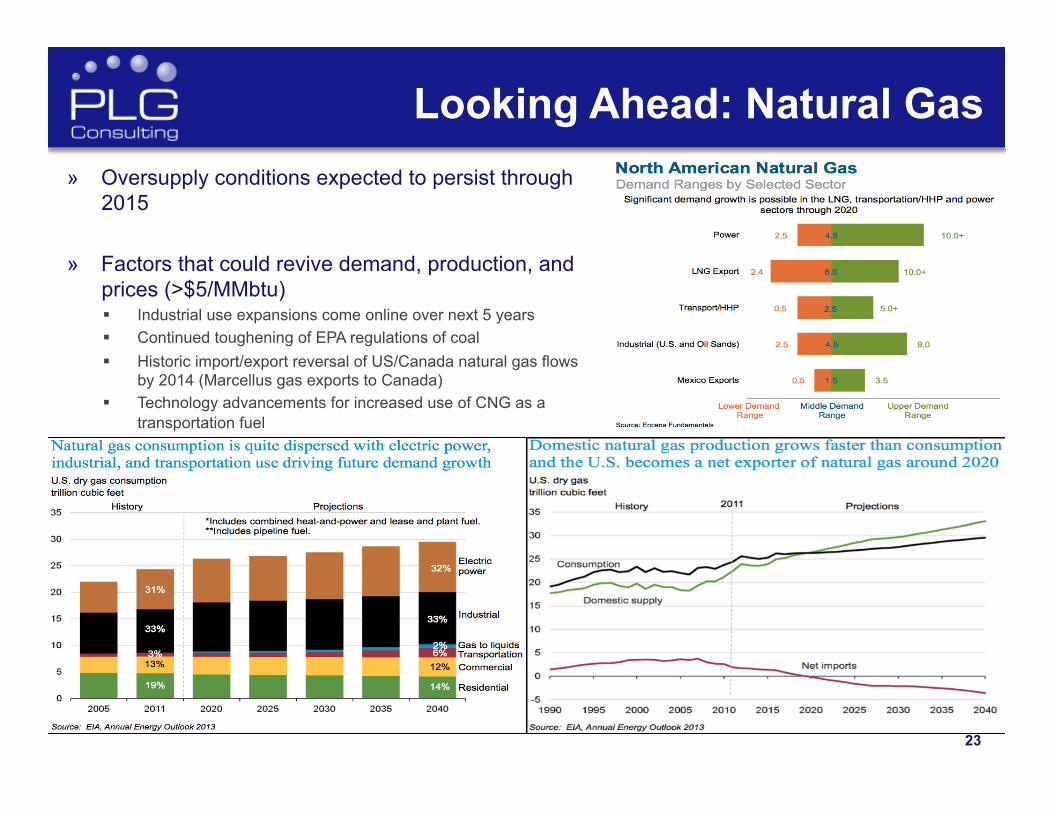

Looking Ahead: Natural Gas » Oversupply conditions expected to persist through

2015 » Factors that could revive demand, production, and

prices (>$5/MMbtu) § Industrial use expansions come online over next 5 years § Continued toughening of EPA regulations of coal § Historic import/export reversal of US/Canada natural gas flows

by 2014 (Marcellus gas exports to Canada) § Technology advancements for increased use of CNG as a

transportation fuel

24

LNG Export Opportunity » Political/policy battle between domestic industrial users and

producers

» Sabine Pass, LA and Freeport, TX now permitted for exports § 3.4 Bcf/day export capacity to come online by 2015 § Represents ~5% of projected US dry gas production

» 20 additional terminal applications totaling 29 Bcf/day of export capacity pending before FERC

Source: Waterborne Energy Inc. Data in $US/MMBtu Source: Congressional Research Service, EIA

Selected US Natural Gas Import & Export Infrastructure

25

Shale Development NGL Impacts

» Leading NGL and “wet gas” plays are Eagle Ford, Utica § Significant investment and expansion of gathering,

fractionation, and takeaway capacity underway in the Utica Play

§ Takeaway capacity in Eagle Ford well exceeds current production (4x)

» Requires fractionation facilities proximal to production § “Y-grade” must be separated into purified products § 75% of fractionation capacity in US Gulf Coast § Mt. Belvieu, TX major trading & storage hub § 500 Mb/d of new fractionation capacity planned for

Utica § Utica NGL production growth expected to exceed

600% between 2013-2015

» Similar to dry gas, strong production due to fracking has resulted in oversupply and depressed prices § Chemical industry benefits

26 Source: American Chemistry Council, May 2013

Shale Development Impact: Chemical Industry

» Abundant ethane supplies have sparked chemical industry renaissance

§ 100% of captured ethane is “cracked” to make ethylene, the most basic building block in the chemicals supply chain

§ Planned expansions will increase US ethylene capacity 33% (11 MMmt) by 2017

§ USA is now the low-cost producer of ethylene-based chemicals due to abundant supplies of ethane from shale plays (up to 60% raw materials cost advantage)

Source: EIA

§ Domestic end-use of materials, i.e. plastics, will expand significantly

§ Up to 40% of new petrochemical output will be for export

§ New demand for plastic resin hoppers, specialty and pressure tank cars

27

Natural Gas & Petrochemical Downstream Products

Feedstock/ Intermediary

Finished Products

Natural Gas, OIl

Ethane, Naphtha, etc.

Ethylene

Miscellaneous

Vinyl Acetate

Linear Alcohols

Ethyl Benzene

Ethylene Oxide

Ethylene Dichloride

High Density Polyethylene

Low-Density Polyethylene

Adhesives, coatings, textile/paper. finishing, flooring

Detergents

Styrene

Ethylene Glycol

Vinyl Chloride

House wares, crates, drums, food containers,

bottles.

Food packaging, film, trash bags, diapers, toys

PVC

Antifreeze

Fibers

PET

Miscellaneous

Polystyrene

SAN

SBR

Latex

Miscellaneous

Medical gloves, carpeting, coatings

Tire, hose

Instrument lenses, house wares

Insulation, cups

Siding, windows, frames, pipe, medical

tubing

Pantyhose, carpets, clothing

Bottles, film

28

Looking Ahead: NGLs

Source: Canadian Energy Research Ins&tute

Source: Sunoco Logis&cs

» US NGL production forecast to increase by 1.6MM b/d from 2012-2018

» The (somewhat) hidden Condensate story

§ Used as diluent for heavy Canadian tar sands oil – critical for transportation as “Dilbit”

§ Significant investment in infrastructure being made to deliver Eagle Ford, Utica condensate to Western Canada

§ Primary delivery via pipeline, but major rail volumes ex. Utica are required to get to Midwest pipeline injection points

§ Canadian diluent import demand expected to grow from 200 Mb/d to 500 Mb/d by 2018

» Expect export market for NGLs to expand § Pipeline reversals undertaken to meet demand,

particularly ex. Utica to Sarnia, ON petrochemical complex and export storage and dock facilities in Philadelphia

§ US projected to export over 1MM bb/d of NGLs by 2018

Source: RBN, PLG analysis

29

Shale Development Crude Oil Impacts

» Dramatic increases in US production due to hydraulic fracturing and horizontal drilling § 7.35 MM bbl./day § Projected to grow by ~30% over next four years § Strong play in Bakken; surging Permian and Eagle Ford development § “Tight” oil sources driving overall North American growth § Production forecasts frequently revised upward

Source: Morgan Stanley, February 2013

30

Driving Toward “Oil Independence?” » Decreasing dependency on foreign crude

§ Combination of US shale plus Canadian oil sands estimated to reduce imports to <15% by 2020

» Supply isn’t enough – “independence” also relies on lower domestic fuels consumption § CAFE standards the primary driver

31

Displacement of Waterborne Crudes by Mid-Continent Sources

» Reducing imports means reducing waterborne crudes § West African imports already down ~70% from 2010 levels

» Mid-continent sources displacing imports at coasts, making rail critical to the total crude market § Bakken as case study for large crude by rail operations

Source: BENTEK Energy

32

Some Basic Facts About Crude Oil: Grades and Qualities

» Not all crudes are created equal – light/sweet vs. heavy/sour § Heavy/sour crudes include Western

Canada, Venezuela, Mexico, Alaska North Slope (ANS), Middle East (light/sour)

§ Heavy/sour has higher sulfur content, yield for asphalt, diesel

» Refineries are generally configured to run certain types of crude § Significant investments made ($48B

since 2005) at select refineries to install coker units that will allow processing of heavy/sour

§ Major heavy/sour refining clusters: Texas Gulf Coast, Chicago, southern Illinois, California

Source: RBN Energy

33

Some Basic Facts About Crude Oil: Major Production and Refining Areas

» The special case of the Canada Oil Sands § Heavy/sour crude has a natural home in Midwest and US Gulf

Coast (~2.8 MM bpd demand at USGC) § Pipeline capacity to US Midwest refining centers is at capacity § Pipeline developments to coasts, US markets still 2+ years

away § Railbit/dilbit via rail requires coiled, lined/insulated cars

» Brent, WTI, and US shale play crudes (Bakken, Permian, Niobrara, Eagle Ford) are light/sweet § US is close to saturation point on light/sweet crude at mid-

continent and USGC refining areas Source: CAPP, June 2013

Source: Turner Mason, RBN Energy

US Crude Oil Production Growth by Grade

Source: RBN Energy

34

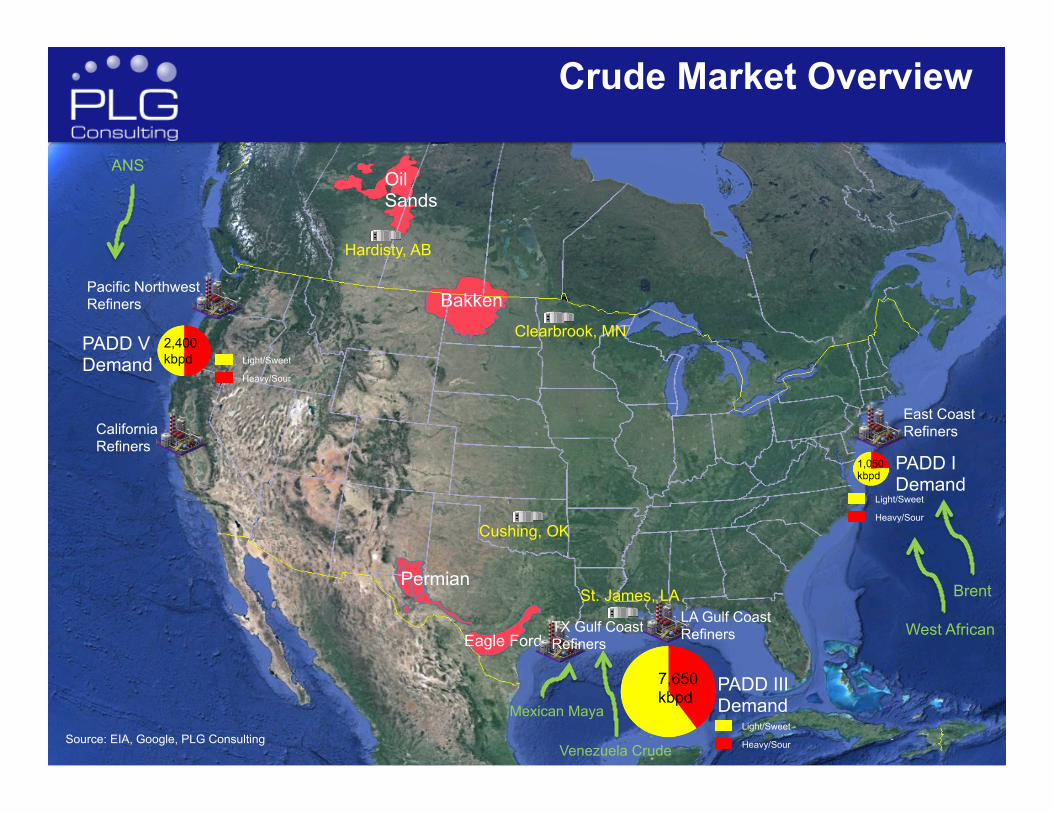

Crude Market Overview

Bakken

Oil Sands

Permian

Eagle Ford

Hardisty, AB

Clearbrook, MN

Cushing, OK

St. James, LA

East Coast Refiners

Pacific Northwest Refiners

California Refiners

TX Gulf Coast Refiners

LA Gulf Coast Refiners

PADD I Demand

PADD III Demand

7,650 kbpd

PADD V Demand

2,400 kbpd

1,050 kbpd

Light/Sweet

Heavy/Sour

Light/Sweet

Heavy/Sour

Light/Sweet

Heavy/Sour

Brent

Mexican Maya

Venezuela Crude

West African

ANS

Source: EIA, Google, PLG Consulting

35

Bakken Oil Production and Logistics - History

» 2010-2011 discount of ~$8-12/bbl for Bakken crude vs. peer WTI § Undervalued due to logistics constraints “stranding” the oil

» Early objective of crude-by-rail was to bridge gap until pipelines built, but has now become the primary transport mode for Bakken crude § ~70% rail market share § Pipelines operating below capacity; some project cancelations

» Significant development of crude by rail loading terminals in 2011-2012 § Takeaway capacity now exceeds production § Bakken vs. WTI differential near even (within ~$3) § Rail captures majority market share

Source: North Dakota Pipeline Authority, PLG Analysis

Source: EIA, North Dakota Pipeline Authority, PLG

~810,000 BPD May 2013

First outbound unit train shipment December, 2009

36

Crude Oil by Rail – North Dakota Terminals

North Dakota Crude Oil Rail Loading Capacity (Barrels Per Day) Rail Terminals 2013 2014* 2015* Rail Carrier EOG Rail, Stanley, ND (Up to 90,000 BOPD) 65,000 65,000 65,000 BNSF

Inergy COLT Hub, Epping, ND (Q2 2012) 120,000 120,000 120,000 BNSF

Hess Rail, Tioga, ND (Up to 120,000 BOPD) 60,000 60,000 60,000 BNSF

Bakken Oil Express, Dickinson, ND 100,000 100,000 100,000 BNSF

Savage Services, Trenton, ND (Q2 2012 Unit Trains) 90,000 90,000 90,000 BNSF

Enbridge, Berthold, ND (Q4 2012) 80,000 80,000 80,000 BNSF

Great Northern Midstream, Fryburg, ND (Q1 2013) 60,000 60,000 60,000 BNSF

Musket, Dore, ND (Q2 2012) 60,000 60,000 60,000 BNSF

Plains, Ross, ND 65,000 65,000 65,000 BNSF

Global/Basin Transload, Zap, ND (Estimate Not Confirmed) 40,000 40,000 40,000 BNSF

BNSF Total Capacity 740,000 740,000 740,000

Plains - Van Hook, New Town, ND 65,000 65,000 65,000 CP

Dakota Plains, New Town, ND 30,000 80,000 80,000 CP

Global Partners, Stampede, ND 60,000 60,000 60,000 CP

CP Total 155,000 205,000 205,000

Various Sites in Minot, Dore, Donnybrook, and Gascoyne 30,000 30,000 30,000

Total Crude Oil Rail Loading Capacity 925,000 975,000 975,000

*Project still in the review or proposed phase Year End System Capacity

Source: North Dakota Pipeline Authority (June 2013), PLG Analysis

37

North Dakota Class I Railroads and Crude Oil Terminals

Map by PLG Consulting 37

38

Bakken Area Outbound Pipelines

38

North Dakota Crude Oil Pipeline Capacity (Barrels Per Day) Pipelines 2013 2014* 2015* Butte Pipeline 160,000 160,000 160,000 Butte Loop* (Late 2014) - 110,000 110,000 Enbridge Mainline North Dakota 210,000 210,000 210,000 Enbridge Bakken Expansion Program (Q1-11/Q1-13) 145,000 145,000 145,000 Plains Bakken North (Q2 2013, Up to 75,000 BOPD) 50,000 50,000 50,000 High Prairie Pipeline* - 150,000 150,000 Enbridge Sandpiper* (Q1 2016) - - - TransCanada Keystone XL* (2015) - - 100,000 TransCanada Bakken Marketlink * (4Q 2015) - - 100,000

Hiland Partners Double H Pipeline (Q3 2014, Up to 100,000 BOPD) 50,000 50,000 Pipeline Total 565,000 875,000 1,075,000 *Project Still in the Review or Proposed Phase Year End System Capacity

Source: North Dakota Pipeline Authority (June 2013)

39

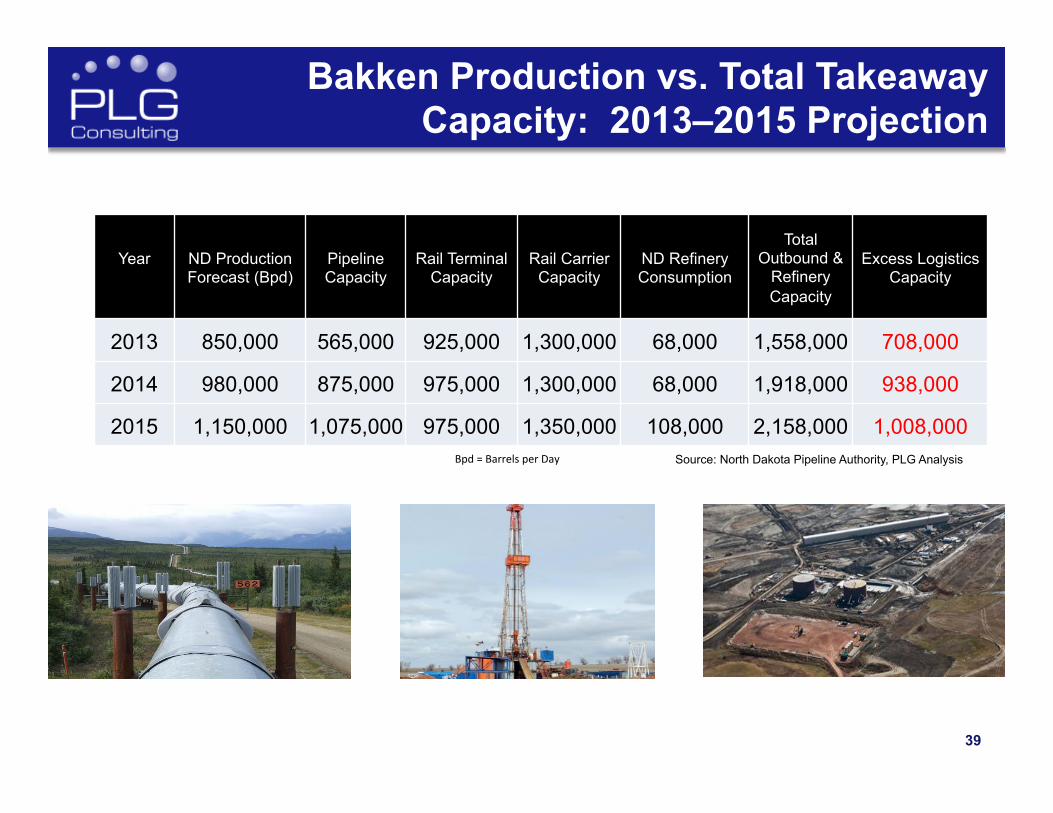

Bakken Production vs. Total Takeaway Capacity: 2013–2015 Projection

Year

ND Production Forecast (Bpd)

Pipeline Capacity

Rail Terminal Capacity

Rail Carrier Capacity

ND Refinery Consumption

Total Outbound &

Refinery Capacity

Excess Logistics Capacity

2013 850,000 565,000 925,000 1,300,000 68,000 1,558,000 708,000

2014 980,000 875,000 975,000 1,300,000 68,000 1,918,000 938,000

2015 1,150,000 1,075,000 975,000 1,350,000 108,000 2,158,000 1,008,000 Source: North Dakota Pipeline Authority, PLG Analysis Bpd = Barrels per Day

40

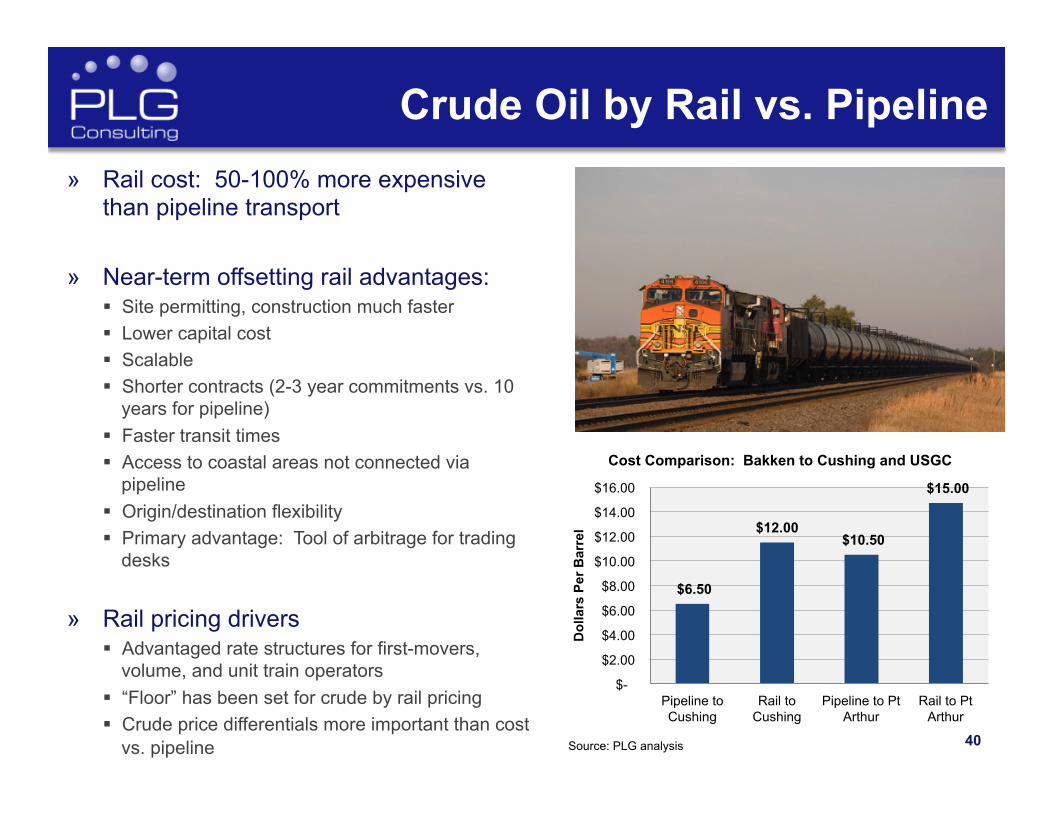

Crude Oil by Rail vs. Pipeline

$6.50

$12.00 $10.50

$15.00

$-

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

Pipeline to Cushing

Rail to Cushing

Pipeline to Pt Arthur

Rail to Pt Arthur

Dol

lars

Per

Bar

rel

Source: PLG analysis

» Rail cost: 50-100% more expensive than pipeline transport

» Near-term offsetting rail advantages: § Site permitting, construction much faster § Lower capital cost § Scalable § Shorter contracts (2-3 year commitments vs. 10

years for pipeline) § Faster transit times § Access to coastal areas not connected via

pipeline § Origin/destination flexibility § Primary advantage: Tool of arbitrage for trading

desks

» Rail pricing drivers § Advantaged rate structures for first-movers,

volume, and unit train operators § “Floor” has been set for crude by rail pricing § Crude price differentials more important than cost

vs. pipeline

Cost Comparison: Bakken to Cushing and USGC

41

All Crude Handled by Railroad Volume Growth

STCC 13111 Source: US Rail Desktop

42

Source: CAPP Report, 2013

Crude Oil Pipelines: Existing and Planned

» Current pipelines ex. Bakken operating below capacity § However, volumes have

increased over past 60 days

» Pipeline industry has been challenged by new dynamic NA oil market § Fixed routes, long lead times § 10 year commitments required

for new build pipeline projects § Lack of subscription interest in

KM Freedom project (Permian-California)

» Several natural gas pipeline conversions planned § Trunkline (ETP) – Patoka, IL-

St. James, LA § Energy East (TransCanada) –

Hardisty, AB-St. Johns, NS

43 43

Crude Tank Car Market Conditions

» Potential bottleneck: Railcars § Current order backlog runs to early 2015 (~48,000 cars) § Major purchases by oil majors and midstream companies § Extremely tight market with very high lease rates § Current crude by rail fleet ~30,000 railcars, or 1-1.5 MM bbl./day

equivalent § Short term demand is highly dependent on WTI – Brent spread

» Railcar type is important § General service 31k gallon capacity cars can hold more crude

than heavier coiled cars § Coiled cars can transport heavier crudes that need heat to

offload – Some shippers prefer the general purpose (GP) rail cars because

the larger capacity can be significant on their transportation cost for hauling lighter crudes

– Some lessors prefer to have more coiled cars that have more uses than general service cars built to hedge themselves on an oversupply of general service tank cars if/when the crude by rail market declines

» Key question: If/is/when will the crude tank car industry become overbuilt?

44

0

500

1,000

1,500

2,000

2,500

3,000

Mar-13 Sep-13 Mar-14 Sep-14 Mar-15 Sep-15

Thou

sand

bbl

/day

Best-Case Crude by Rail Potential vs. Crude Railcar Capacity

Other Production Sources Williston (Bakken)

Oil Sands Crude Railcar Capacity

Forecast of Crude Railcar Supply and Demand

» Production increases vs. railcar capacity increases § March crude fleet was ~30k cars and

backlog was ~48.2k Backlog runs through mid 2015

§ If pipelines and local refining can consume production increases in Permian and Eagle Ford, crude by rail will be primarily Bakken and Canadian Oil Sands productions

» Under best-case scenario for rail market share capture, data suggests existing & planned tank car fleet exceeds demand

Sources: CAPP, AAR, NDPA, GATX, and PLG analysis

Railcar backlog is through mid 2015; retirement of old railcars will reduce capacity if no additional railcars built

Q1 2013 originated rail carloads of crude petroleum were 97,135, which equates to 755,000 barrels per day (assume 700/bbl. average capacity)

Assumptions: • 80% of projected Williston Basin production • 80% utilization of Oil Sands announced 300 kbpd of rail terminals through 2014, and 80% utilization of an additional 300 kbpd for 2015 • 30,000 crude railcars in March and build rate of 21,500 railcars/year through 2015 with attrition rate of 7,800 railcars/year • 700 bbl. average railcar capacity and average 17 day turn • Other production sources at constant 165 kbpd

45 45

Shale Development and Crude By Rail: Current Market Dynamics

» Recent History: § Original (2009-2010) objective of crude by rail to “bridge the gap” until pipelines built § By 2012, crude by rail viewed as a core mode of transportation and means of arbitrage – Differentials made rail attractive: Bakken and WTI trading at ~$10-$15/bbl. less than Brent; Alberta Bitumen trading at ~$30/bbl. less

than Brent – Market response: E&P, midstream players willing to rapidly deploy significant capital to enable access and capitalize on spreads

– Multi-modal logistics hubs in shale plays and at destination markets (i.e. Cushing, OK, St. James, LA, Pt. Arthur, TX, Albany, NY, Bakersfield, CA)

– Lease and purchase of railcar fleets – Pipeline expansions, reversals, new construction

– Refineries installing unit train receiving capability - particularly coastal refineries previously captive to waterborne imports (i.e. Philadelphia, PA, St. John, NB, Anacortes, WA, Ferndale, WA)

» Today: § Spreads have narrowed, limiting arbitrage opportunities and slowing crude by rail growth § Price differentials driving trading and logistics patterns

45

Key Drivers

Supply Sources

Oil Prices

Destination Markets

Capital

46

Oil Sands

Hardisty, AB

Heavy/Sour Crude Logistics and Price Differentials – July 2013

$89

Heavy/Sour at TX GC Mexican Maya (ship): $98 WCS (pipe): $107 WCS (rail): $113

Spread Dec. 2012 July 2013 Change Mexican Maya - WCS $33.55/bbl $8.90/bbl -$24.65/bbl

Crude Prices from July 2013 Sources: EIA, CME Group, Platts, Google, PLG analysis 46

TX Gulf Coast Refiners

Pacific Northwest Refiners

California Refiners

PADD III Demand

7,650 kbpd

PADD V Demand

2,400 kbpd Light/Sweet

Heavy/Sour

Light/Sweet

Heavy/Sour Mexican Maya

Marine

Rail Pipeline

Clearbrook, MN

Chicago, IL

47

Light/Sweet Crude Logistics and Price Differentials – July 2013

Bakken

Permian

Eagle Ford

East Coast Refiners

Pacific Northwest Refiners

California Refiners

TX Gulf Coast Refiners

LA Gulf Coast Refiners

$6

Light/Sweet at TX GC Bakken (pipe): $107 Brent (ship): $108 WTI (pipe): $111

Light/Sweet at PNW Bakken (rail): $109 Brent (ship): $108

Light/Sweet at EC Bakken (rail): $111 Brent (ship): $108

Light/Sweet at LA GC Bakken (rail): $111 LLS (local): $110

Spread Dec. 2012 July 2013 Change Brent - WTI $21.83/bbl $2.82/bbl -$19.01/bbl LLS - WTI $20.00/bbl $4.90/bbl -$15.10/bbl WTI - Bakken (Clearbrook) $3.00/bbl $2.54/bbl -$0.46/bbl Brent

ANS

Brent

47

Crude Prices from July 2013 Sources: EIA, Bloomberg, Platts, Baytex Energy, Google, CME Group, PLG analysis

PADD I Demand

PADD III Demand

7,650 kbpd

PADD V Demand

2,400 kbpd

1,050 kbpd

Light/Sweet

Heavy/Sour

Light/Sweet

Heavy/Sour

Light/Sweet

Heavy/Sour

Marine

Rail Pipeline

Chicago, IL

Clearbrook, MN

Cushing, OK

St. James, LA

$96 (wellhead)

WTI:$105

48 48

Looking Ahead: North American Crude Oil Logistics

» The gusher of new US light/sweet shale oil production made possible by fracking has upended the traditional oil logistics and trading patterns § Result: “Wrong place/wrong oil” supply displacements, i.e. Cushing overflow § Rapid investment in new logistics infrastructure, routes, modes, and terminals – Bakken now sufficiently developed; next immediate areas for significant investment are Utica, Oil Sands,

Permian, coastal areas and intermediate routes and facilities that support bitumen transport in particular

» A “new normal” in crude oil flows will emerge in conjunction with

continued North American oil production over the next five years § Continued shifts of mid-continent light/sweet to coastal destinations § New modes and infrastructure to get Canadian bitumen to USGC, with or without Keystone

XL § Permian, Eagle Ford to meet USGC light/sweet demand; Bakken flows primarily east-west § Significant oversupply of light/sweet and super-light grades

» Expect eventual government approval of light/sweet crude oil and condensate exports on a limited basis, similar to LNG

» Primary threats to crude by rail business 1. Narrow WTI-Brent spread 2. Glut of Permian and Eagle Ford light sweet oil displacing rail volumes to USGC to Gulf

Coast (but somewhat offset by new rail deliveries from Oil Sands) 3. Continued pipeline development 4. Water-borne Eagle Ford crude deliveries to USEC

49

Looking Ahead: Crude Oil Anticipated Production Growth and Product Flows

Source: BENTEK Energy, CAPP, Railroad Commission of Texas, ND Pipeline Association, Google, PLG Consulting

= Current 2013 = Future 2017

Anticipated Production Growth

Permian 1,680 1,200 +40%

1,600 800 Eagle Ford

+100%

Bakken +56% 871

1,363

Marine

East Coast Refiners

Oil Sands

2,590 1,985 +30%

Hardisty, AB

Cushing, OK

LA Gulf Coast Refiners

Light/Sweet

St. James, LA

Rail Pipeline

Pacific Northwest Refiners

California Refiners

TX Gulf Coast Refiners

Heavy/Sour

Clearbrook, MN

Chicago, IL

50

Thank You! For follow up questions and information, please contact PLG:

+1-312-957-7757 / [email protected]

Taylor Robinson, President

Graham Brisben, CEO

Jean Arndt, Vice President

Jeff Dowdell, Senior Consultant

Gordon Heisler, Senior Consultant

Jeff Rasmussen, Senior Consultant

Jay Olberding, Analyst

This presentation is available at: WWW.PLGCONSULTING.COM

Professional Logistics Group

Related Documents