OIL & GAS SAPURAKENCANA PETROLEUM (SAKP MK) 16 May 2012 Dominant offshore service provider Company report Alex Goh [email protected] +603 2036 2291 Rationale for report: Initiation Price RM2.24 (Reference price) Fair Value RM2.68 52-week High/Low N/A Key Changes Fair value Initiation EPS Initiation YE to Jan FY12 FY13F FY14F FY15F Revenue (RMmil) 4,672.6 5,533.4 6,093.9 6,731.7 Core net profit (RMmil) 454.5 504.0 744.5 884.5 EPS (Sen) 9.1 10.1 14.9 17.7 EPS growth (%) 47.5 10.9 47.7 18.8 Consensus net profit (RMmil) n/a n/a n/a DPS (Sen) 0.0 0.0 1.5 1.8 PE (x) 24.7 22.2 15.1 12.7 EV/EBITDA (x) 6.0 5.5 4.0 3.4 Div yield (%) 0.0 0.0 1.5 1.8 ROE (%) 8.8 9.4 13.0 n/a Net Gearing (%) 46.6 86.2 72.7 62.0 Stock and Financial Data Shares Outstanding (million) 5,004.3 Market Cap (RMmil) 11,209.6 Book value (RM/share) 1.02 P/BV (x) 2.2 ROE (%) 8.8 Net Gearing (%) 43.8 Major Shareholders Sapura Holdings (20.0%) Khasera Baru (19.9%) Free Float (%) 48.0 Avg Daily Value (RMmil) n/a Price performance 3mth 6mth 12mth Absolute (%) - - - Relative (%) - - - Investment Highlights We initiate coverage of SapuraKencana Petroleum (SapuraKencana) with a fair value of RM2.68/share, pegged to an FY13F PE of 22x (excluding one-off merger costs of RM131mil), almost at par with an average of 21x for oil & gas stocks with a market capitalisation of over RM5bil. We have rolled forward our valuation benchmark from CY12F PE of 22x, as indicated in our report on 21 March this year. There are no rivals domestically in terms of the comprehensive range and scope of services provided by SapuraKencana. The group provides one-stop service solutions to oil & gas majors by leveraging on its formidable assets to fabricate and install offshore structures with a reach that extends throughout Asia Pacific, India, the Middle East, Latin America, North America and Africa. Its nearest competitors are multi-nationals such as McDermott International, Saipem and Technip. SapuraKencana will be able to synergise the complementary businesses of its merged units with an enlarged balance sheet to enhance their capabilities in securing larger order prospects and reenergise earnings growth momentum. SapuraKencana’s order book of RM14bil remains the largest in the country, larger than Bumi Armada’s RM10bil which includes RM3bil renewable options. Accounting for 2.5x of SapuraKencana’s CY12F merged revenues, earnings for the next two years are already locked-in. SapuraKencana’s tender book of RM12.5bil, of which half stems from overseas projects, will drive the group’s earnings prospects. The group’s 50%-owned joint venture with Seadrill is eager to participate in Petrobras’ next batch of seven flexible pipe-lay vessels. Domestically, we expect SapuraKencana to benefit from fresh news over the next few months from Petronas’ RM15bil fast-tracked programme to develop gas reserves from a cluster of fields in the North Malay basin, off Peninsular Malaysia as well as other enhanced oil recovery jobs in East Malaysia as well as additional marginal field concessions. We expect the group’s balance sheet to remain manageable as net gearing will drop from 0.9x to 0.7x over the next two years, net of progressive capital expenditures and equity contribution of joint venture partners. SapuraKencana, which will be listed tomorrow, will have a potential market capitalisation of over RM10bil rivalling Bumi Armada and will likely lead to its inclusion in the FBMKLCI and MSCI indices. As foreign institutional investors’ holdings are still in the low teens for the two companies, the inclusion in the major indices will naturally likely retain the group’s premium valuation of over 20x. PP 12247/06/2012 (030106) FAIR VALUE: RM2.68

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

OIL & GAS

SAPURAKENCANA PETROLEUM(SAKP MK) 16 May 2012

Dominant offshore service provider

Company report

Alex Goh

+603 2036 2291 Rationale for report: Initiation

Price RM2.24 (Reference price) Fair Value RM2.68 52-week High/Low N/A Key Changes

Fair value Initiation EPS Initiation YE to Jan FY12 FY13F FY14F FY15F Revenue (RMmil) 4,672.6 5,533.4 6,093.9 6,731.7 Core net profit (RMmil) 454.5 504.0 744.5 884.5 EPS (Sen) 9.1 10.1 14.9 17.7 EPS growth (%) 47.5 10.9 47.7 18.8 Consensus net profit (RMmil) n/a n/a n/a DPS (Sen) 0.0 0.0 1.5 1.8 PE (x) 24.7 22.2 15.1 12.7 EV/EBITDA (x) 6.0 5.5 4.0 3.4 Div yield (%) 0.0 0.0 1.5 1.8 ROE (%) 8.8 9.4 13.0 n/a Net Gearing (%) 46.6 86.2 72.7 62.0 Stock and Financial Data

Shares Outstanding (million) 5,004.3 Market Cap (RMmil) 11,209.6 Book value (RM/share) 1.02 P/BV (x) 2.2 ROE (%) 8.8 Net Gearing (%) 43.8 Major Shareholders Sapura Holdings (20.0%)

Khasera Baru (19.9%)

Free Float (%) 48.0 Avg Daily Value (RMmil) n/a Price performance 3mth 6mth 12mth Absolute (%) - - - Relative (%) - - -

Investment Highlights

We initiate coverage of SapuraKencana Petroleum

(SapuraKencana) with a fair value of RM2.68/share, pegged to an FY13F PE of 22x (excluding one-off merger costs of RM131mil), almost at par with an average of 21x for oil & gas stocks with a market capitalisation of over RM5bil. We have rolled forward our valuation benchmark from CY12F PE of 22x, as indicated in our report on 21 March this year.

There are no rivals domestically in terms of the comprehensive range and scope of services provided by SapuraKencana. The group provides one-stop service solutions to oil & gas majors by leveraging on its formidable assets to fabricate and install offshore structures with a reach that extends throughout Asia Pacific, India, the Middle East, Latin America, North America and Africa. Its nearest competitors are multi-nationals such as McDermott International, Saipem and Technip.

SapuraKencana will be able to synergise the complementary businesses of its merged units with an enlarged balance sheet to enhance their capabilities in securing larger order prospects and reenergise earnings growth momentum.

SapuraKencana’s order book of RM14bil remains the largest in the country, larger than Bumi Armada’s RM10bil which includes RM3bil renewable options. Accounting for 2.5x of SapuraKencana’s CY12F merged revenues, earnings for the next two years are already locked-in.

SapuraKencana’s tender book of RM12.5bil, of which half stems from overseas projects, will drive the group’s earnings prospects. The group’s 50%-owned joint venture with Seadrill is eager to participate in Petrobras’ next batch of seven flexible pipe-lay vessels.

Domestically, we expect SapuraKencana to benefit from fresh news over the next few months from Petronas’ RM15bil fast-tracked programme to develop gas reserves from a cluster of fields in the North Malay basin, off Peninsular Malaysia as well as other enhanced oil recovery jobs in East Malaysia as well as additional marginal field concessions.

We expect the group’s balance sheet to remain manageable as net gearing will drop from 0.9x to 0.7x over the next two years, net of progressive capital expenditures and equity contribution of joint venture partners.

SapuraKencana, which will be listed tomorrow, will have a potential market capitalisation of over RM10bil rivalling Bumi Armada and will likely lead to its inclusion in the FBMKLCI and MSCI indices. As foreign institutional investors’ holdings are still in the low teens for the two companies, the inclusion in the major indices will naturally likely retain the group’s premium valuation of over 20x.

PP 12247/06/2012 (030106)

FAIR VALUE: RM2.68

SapuraKencana Petroleum 16 May 2012

AmResearch Sdn Bhd 2

NO RIVAL DOMESTICALLY

Initiate coverage with unchanged fair value of RM2.68/share

We initiate coverage on SapuraKencana Petroleum (SapuraKencana) with a fair value of RM2.68/share, pegged to an FY13F PE of 22x (excluding one-off merger costs of RM131mil), almost at par with an average 21x for oil & gas stocks with a market capitalization of over RM5bil.

We have rolled forward our valuation benchmark from CY12F PE of 22x, as indicated in our report on 21 March this year.

Since the merger announcement of SapuraCrest Petroleum and Kencana Petroleum in July last year, the shares of the merged entity SapuraKencana will finally be listed tomorrow. The reference price for SapuraKencana shares is RM2.24/share (based on the closing share price of SapuraCrest and Kencana together with their cash distribution).

Dominant offshore service provider

SapuraKencana will have the combined assets and resources of both SapuraCrest and Kencana Petroleum to provide integrated services which are unmatched domestically for oil & gas majors. These encompass:

1) A dominant 70% market share of domestic offshore installation work with stakes in four derrick lay vessels (excluding five pipe-lay/derrick vessels under construction),

2) Sole domestic tender rig owner/operator with a fleet of 6 units and two more under construction,

3) One of two concessionaires for a small field risk sharing contract for the Berantai field, with the other

being the Dialog-Roc Oil-Petronas Carigali consortium,

4) One of only two major fabrication yards (the other being Malaysia Marine & Heavy Engineering Holdings) in the country.

5) Other services which provide integrated solutions for oil majors include marine services via a fleet of 9 diving/support vessels, 4 survey vessels, 6 remote-operated vessels, 4 accommodation workboats and four anchor-handling tug supply vessels.

There are no rivals domestically in terms of the comprehensive range and scope of services provided by SapuraKencana. The group provides one-stop service solutions to oil & gas majors by leveraging on its formidable assets to fabricate and install offshore structures with a reach that extends throughout Asia Pacific, India, the Middle East, Latin America, North America and Africa. Its nearest competitors are multi-nationals such as McDermott International, Saipem and Technip.

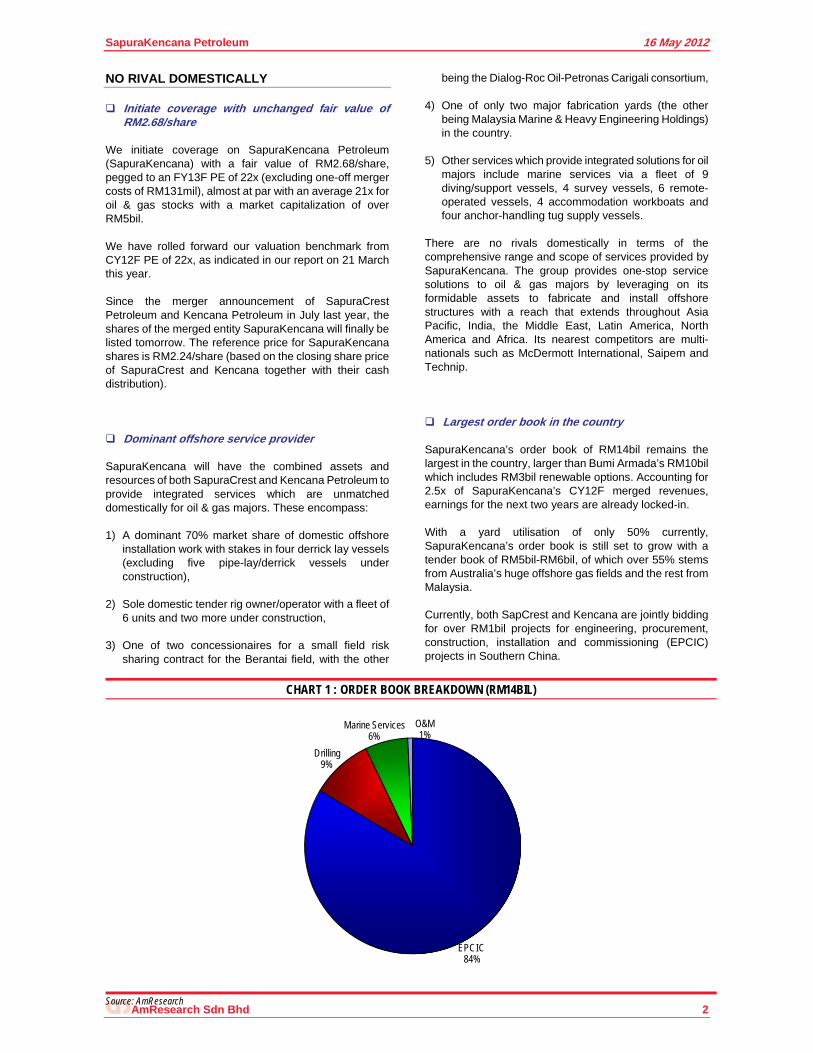

Largest order book in the country

SapuraKencana’s order book of RM14bil remains the largest in the country, larger than Bumi Armada’s RM10bil which includes RM3bil renewable options. Accounting for 2.5x of SapuraKencana’s CY12F merged revenues, earnings for the next two years are already locked-in.

With a yard utilisation of only 50% currently, SapuraKencana’s order book is still set to grow with a tender book of RM5bil-RM6bil, of which over 55% stems from Australia’s huge offshore gas fields and the rest from Malaysia.

Currently, both SapCrest and Kencana are jointly bidding for over RM1bil projects for engineering, procurement, construction, installation and commissioning (EPCIC) projects in Southern China.

CHART 1 : ORDER BOOK BREAKDOWN (RM14BIL)

EPCIC84%

Drilling 9%

Marine Services6%

O&M1%

Source: AmResearch

SapuraKencana Petroleum 16 May 2012

AmResearch Sdn Bhd 3

Huge tender book supports earnings prospects

SapuraKencana will be able to synergise the complementary businesses of its merged units with an enlarged balance sheet to enhance their capabilities in securing larger order prospects and reenergise earnings growth momentum.

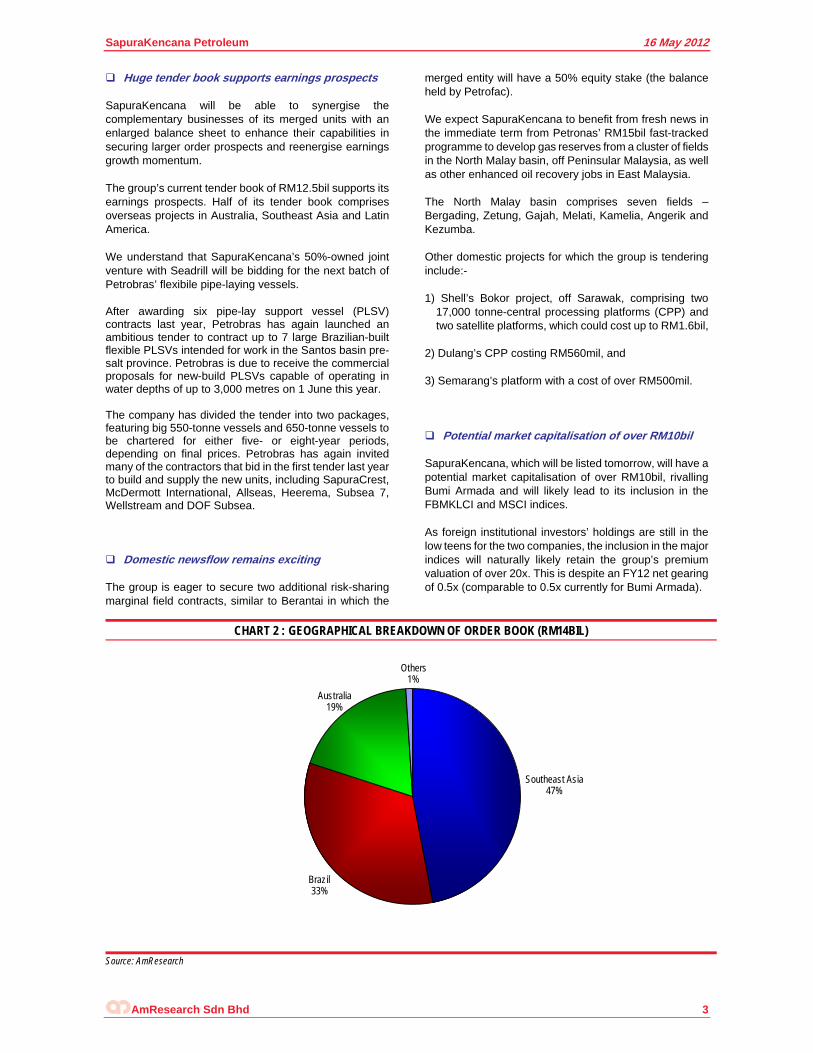

The group’s current tender book of RM12.5bil supports its earnings prospects. Half of its tender book comprises overseas projects in Australia, Southeast Asia and Latin America.

We understand that SapuraKencana’s 50%-owned joint venture with Seadrill will be bidding for the next batch of Petrobras’ flexibile pipe-laying vessels.

After awarding six pipe-lay support vessel (PLSV) contracts last year, Petrobras has again launched an ambitious tender to contract up to 7 large Brazilian-built flexible PLSVs intended for work in the Santos basin pre-salt province. Petrobras is due to receive the commercial proposals for new-build PLSVs capable of operating in water depths of up to 3,000 metres on 1 June this year. The company has divided the tender into two packages, featuring big 550-tonne vessels and 650-tonne vessels to be chartered for either five- or eight-year periods, depending on final prices. Petrobras has again invited many of the contractors that bid in the first tender last year to build and supply the new units, including SapuraCrest, McDermott International, Allseas, Heerema, Subsea 7, Wellstream and DOF Subsea.

Domestic newsflow remains exciting

The group is eager to secure two additional risk-sharing marginal field contracts, similar to Berantai in which the

merged entity will have a 50% equity stake (the balance held by Petrofac).

We expect SapuraKencana to benefit from fresh news in the immediate term from Petronas’ RM15bil fast-tracked programme to develop gas reserves from a cluster of fields in the North Malay basin, off Peninsular Malaysia, as well as other enhanced oil recovery jobs in East Malaysia.

The North Malay basin comprises seven fields – Bergading, Zetung, Gajah, Melati, Kamelia, Angerik and Kezumba.

Other domestic projects for which the group is tendering include:-

1) Shell’s Bokor project, off Sarawak, comprising two 17,000 tonne-central processing platforms (CPP) and two satellite platforms, which could cost up to RM1.6bil,

2) Dulang’s CPP costing RM560mil, and

3) Semarang’s platform with a cost of over RM500mil.

Potential market capitalisation of over RM10bil

SapuraKencana, which will be listed tomorrow, will have a potential market capitalisation of over RM10bil, rivalling Bumi Armada and will likely lead to its inclusion in the FBMKLCI and MSCI indices.

As foreign institutional investors’ holdings are still in the low teens for the two companies, the inclusion in the major indices will naturally likely retain the group’s premium valuation of over 20x. This is despite an FY12 net gearing of 0.5x (comparable to 0.5x currently for Bumi Armada).

CHART 2 : GEOGRAPHICAL BREAKDOWN OF ORDER BOOK (RM14BIL)

Southeast Asia47%

Brazil33%

Australia19%

Others1%

Source: AmResearch

SapuraKencana Petroleum 16 May 2012

AmResearch Sdn Bhd 4

Net gearing will decline to 0.7x

Incorporating the group’s massive capital expenditure programme, we expect SapuraKencana’s FY13F net gearing of 0.9x (gross gearing to reach 1.2x) to remain manageable, as it will drop to 0.7x over the next two years given that the US$1.4bil gross capex will be progressive, while Seadrill will bear half of SapCrest’s commitment to build three flexible pipe-laying support vessels for up to US$900mil in Brazil. As SapuraKencana will own only 50% of the three Petrobras’ pipe-laying vessels, most of its capex will not be consolidated with SapuraKencana’s balance sheet.

Besides the Petrobras vessels, the rest of the capital expenditure will be utilised for:-

1) Two more pipe-laying vessels, costing US$400mil to be deployed regionally in Asia.

2) A tender and semi-tender rig costing US$370mil, and

3) RM300mil for two mobile offshore production units (to be refurbished from two recently acquired but ageing jack-up rigs), marine spread vessels and additional land acquisitions for fabrication capacity.

Management under proven leadership

The management of SapuraKencana will be steered by the proven leadership of its component companies. SapuraCrest’s Dato’ Seri Shahril Shamsuddin, who holds an effective 20% equity in the company, will be the president/group chief executive officer and executive director.

Kencana’s Dato’ Mokhzani Mahathir, who will hold an effective 20% equity stake in the group, will be the executive vice-chairman and executive director. These two will continue to provide strategic directions to the group.

The board of directors will comprise experienced individuals from both companies, such as Kencana’s Chong Hin Loon, who will head the fabrication division, SapCrest’s Reza Abdul Rahim for installation of pipelines and facilities and marine services and Kencana’s Azmi bin Ismail in the drilling, maintenance and retail segment.

SapuraKencana Petroleum 16 May 2012

AmResearch Sdn Bhd 5

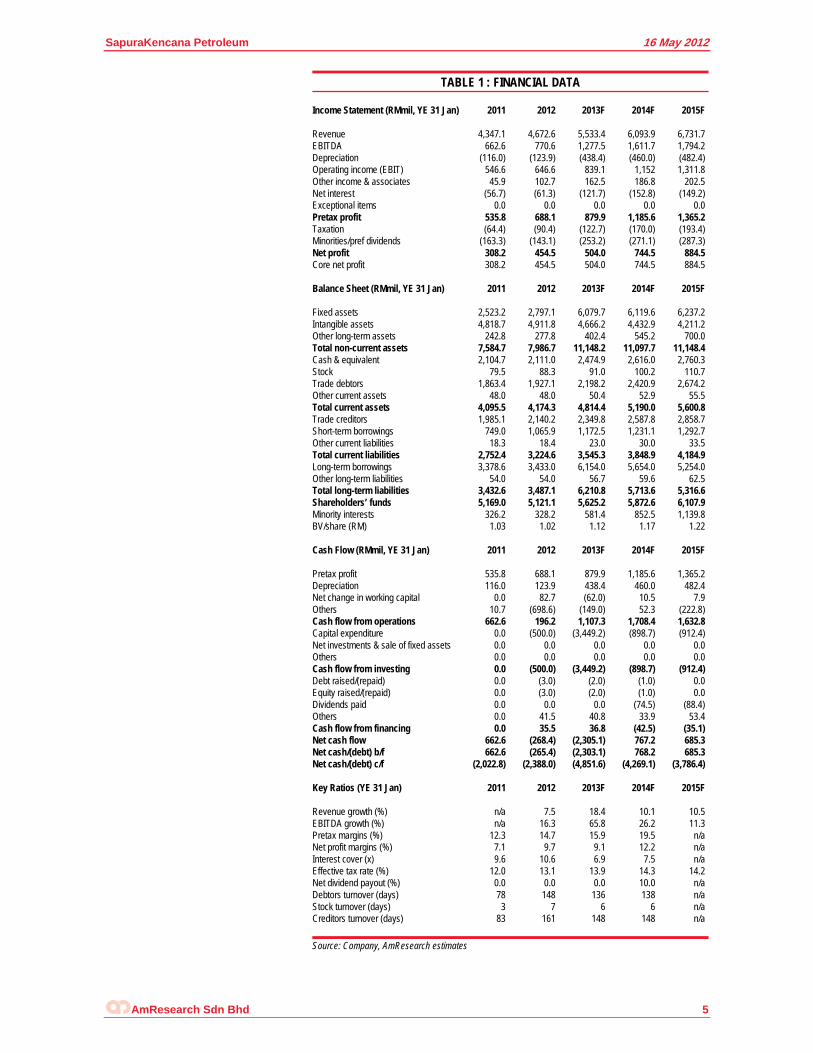

TABLE 1 : FINANCIAL DATA Income Statement (RMmil, YE 31 Jan) 2011 2012 2013F 2014F 2015F Revenue 4,347.1 4,672.6 5,533.4 6,093.9 6,731.7 EBITDA 662.6 770.6 1,277.5 1,611.7 1,794.2 Depreciation (116.0) (123.9) (438.4) (460.0) (482.4) Operating income (EBIT) 546.6 646.6 839.1 1,152 1,311.8 Other income & associates 45.9 102.7 162.5 186.8 202.5 Net interest (56.7) (61.3) (121.7) (152.8) (149.2) Exceptional items 0.0 0.0 0.0 0.0 0.0 Pretax profit 535.8 688.1 879.9 1,185.6 1,365.2 Taxation (64.4) (90.4) (122.7) (170.0) (193.4) Minorities/pref dividends (163.3) (143.1) (253.2) (271.1) (287.3) Net profit 308.2 454.5 504.0 744.5 884.5 Core net profit 308.2 454.5 504.0 744.5 884.5 Balance Sheet (RMmil, YE 31 Jan) 2011 2012 2013F 2014F 2015F Fixed assets 2,523.2 2,797.1 6,079.7 6,119.6 6,237.2 Intangible assets 4,818.7 4,911.8 4,666.2 4,432.9 4,211.2 Other long-term assets 242.8 277.8 402.4 545.2 700.0 Total non-current assets 7,584.7 7,986.7 11,148.2 11,097.7 11,148.4 Cash & equivalent 2,104.7 2,111.0 2,474.9 2,616.0 2,760.3 Stock 79.5 88.3 91.0 100.2 110.7 Trade debtors 1,863.4 1,927.1 2,198.2 2,420.9 2,674.2 Other current assets 48.0 48.0 50.4 52.9 55.5 Total current assets 4,095.5 4,174.3 4,814.4 5,190.0 5,600.8 Trade creditors 1,985.1 2,140.2 2,349.8 2,587.8 2,858.7 Short-term borrowings 749.0 1,065.9 1,172.5 1,231.1 1,292.7 Other current liabilities 18.3 18.4 23.0 30.0 33.5 Total current liabilities 2,752.4 3,224.6 3,545.3 3,848.9 4,184.9 Long-term borrowings 3,378.6 3,433.0 6,154.0 5,654.0 5,254.0 Other long-term liabilities 54.0 54.0 56.7 59.6 62.5 Total long-term liabilities 3,432.6 3,487.1 6,210.8 5,713.6 5,316.6 Shareholders’ funds 5,169.0 5,121.1 5,625.2 5,872.6 6,107.9 Minority interests 326.2 328.2 581.4 852.5 1,139.8 BV/share (RM) 1.03 1.02 1.12 1.17 1.22 Cash Flow (RMmil, YE 31 Jan) 2011 2012 2013F 2014F 2015F Pretax profit 535.8 688.1 879.9 1,185.6 1,365.2 Depreciation 116.0 123.9 438.4 460.0 482.4 Net change in working capital 0.0 82.7 (62.0) 10.5 7.9 Others 10.7 (698.6) (149.0) 52.3 (222.8) Cash flow from operations 662.6 196.2 1,107.3 1,708.4 1,632.8 Capital expenditure 0.0 (500.0) (3,449.2) (898.7) (912.4) Net investments & sale of fixed assets 0.0 0.0 0.0 0.0 0.0 Others 0.0 0.0 0.0 0.0 0.0 Cash flow from investing 0.0 (500.0) (3,449.2) (898.7) (912.4) Debt raised/(repaid) 0.0 (3.0) (2.0) (1.0) 0.0 Equity raised/(repaid) 0.0 (3.0) (2.0) (1.0) 0.0 Dividends paid 0.0 0.0 0.0 (74.5) (88.4) Others 0.0 41.5 40.8 33.9 53.4 Cash flow from financing 0.0 35.5 36.8 (42.5) (35.1) Net cash flow 662.6 (268.4) (2,305.1) 767.2 685.3 Net cash/(debt) b/f 662.6 (265.4) (2,303.1) 768.2 685.3 Net cash/(debt) c/f (2,022.8) (2,388.0) (4,851.6) (4,269.1) (3,786.4) Key Ratios (YE 31 Jan) 2011 2012 2013F 2014F 2015F Revenue growth (%) n/a 7.5 18.4 10.1 10.5 EBITDA growth (%) n/a 16.3 65.8 26.2 11.3 Pretax margins (%) 12.3 14.7 15.9 19.5 n/a Net profit margins (%) 7.1 9.7 9.1 12.2 n/a Interest cover (x) 9.6 10.6 6.9 7.5 n/a Effective tax rate (%) 12.0 13.1 13.9 14.3 14.2 Net dividend payout (%) 0.0 0.0 0.0 10.0 n/a Debtors turnover (days) 78 148 136 138 n/a Stock turnover (days) 3 7 6 6 n/a Creditors turnover (days) 83 161 148 148 n/a

Source: Company, AmResearch estimates

SapuraKencana Petroleum 16 May 2012

AmResearch Sdn Bhd 6

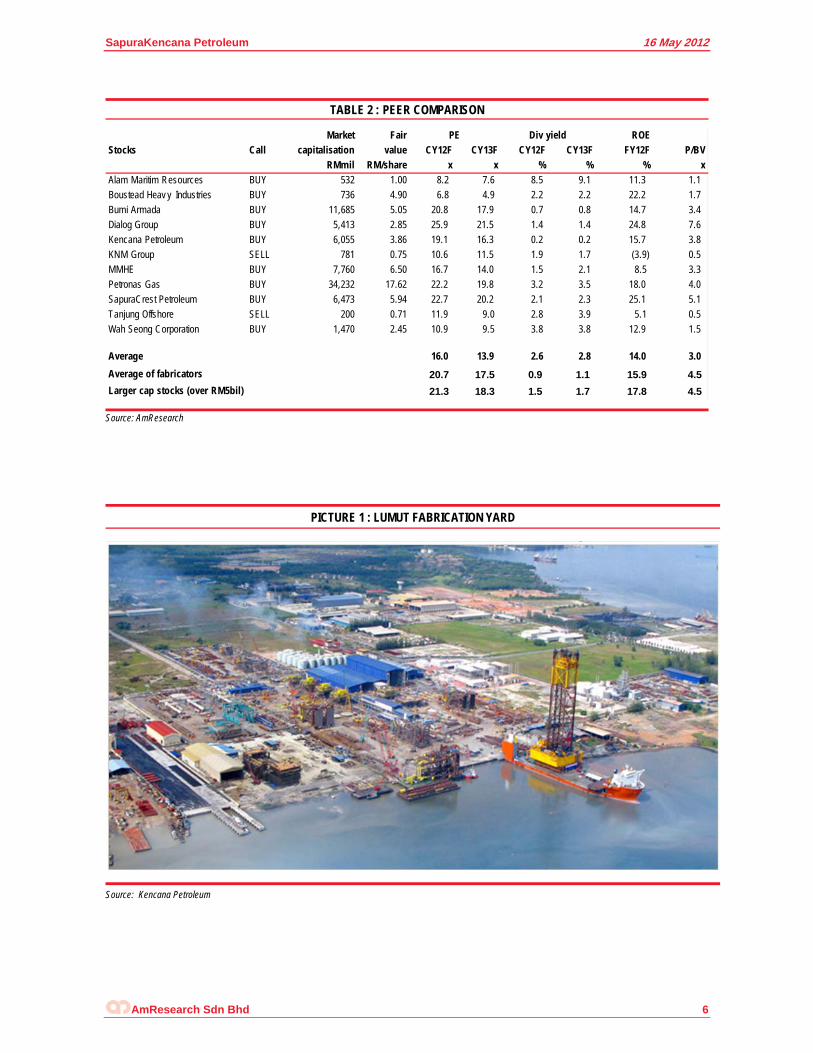

TABLE 2 : PEER COMPARISON

Market Fair ROE

Stocks Call capitalisation value CY12F CY13F CY12F CY13F FY12F P/BV

RMmil RM/share x x % % % x

Alam Maritim Resources BUY 532 1.00 8.2 7.6 8.5 9.1 11.3 1.1

Boustead Heav y Industries BUY 736 4.90 6.8 4.9 2.2 2.2 22.2 1.7

Bumi Armada BUY 11,685 5.05 20.8 17.9 0.7 0.8 14.7 3.4

Dialog Group BUY 5,413 2.85 25.9 21.5 1.4 1.4 24.8 7.6

Kencana Petroleum BUY 6,055 3.86 19.1 16.3 0.2 0.2 15.7 3.8

KNM Group SELL 781 0.75 10.6 11.5 1.9 1.7 (3.9) 0.5

MMHE BUY 7,760 6.50 16.7 14.0 1.5 2.1 8.5 3.3

Petronas Gas BUY 34,232 17.62 22.2 19.8 3.2 3.5 18.0 4.0

SapuraCrest Petroleum BUY 6,473 5.94 22.7 20.2 2.1 2.3 25.1 5.1

Tanjung Offshore SELL 200 0.71 11.9 9.0 2.8 3.9 5.1 0.5

Wah Seong Corporation BUY 1,470 2.45 10.9 9.5 3.8 3.8 12.9 1.5

Average 16.0 13.9 2.6 2.8 14.0 3.0

Average of fabricators 20.7 17.5 0.9 1.1 15.9 4.5

Larger cap stocks (over RM5bil) 21.3 18.3 1.5 1.7 17.8 4.5

PE Div yield

Source: AmResearch

PICTURE 1 : LUMUT FABRICATION YARD

Source: Kencana Petroleum

SapuraKencana Petroleum 16 May 2012

AmResearch Sdn Bhd 7

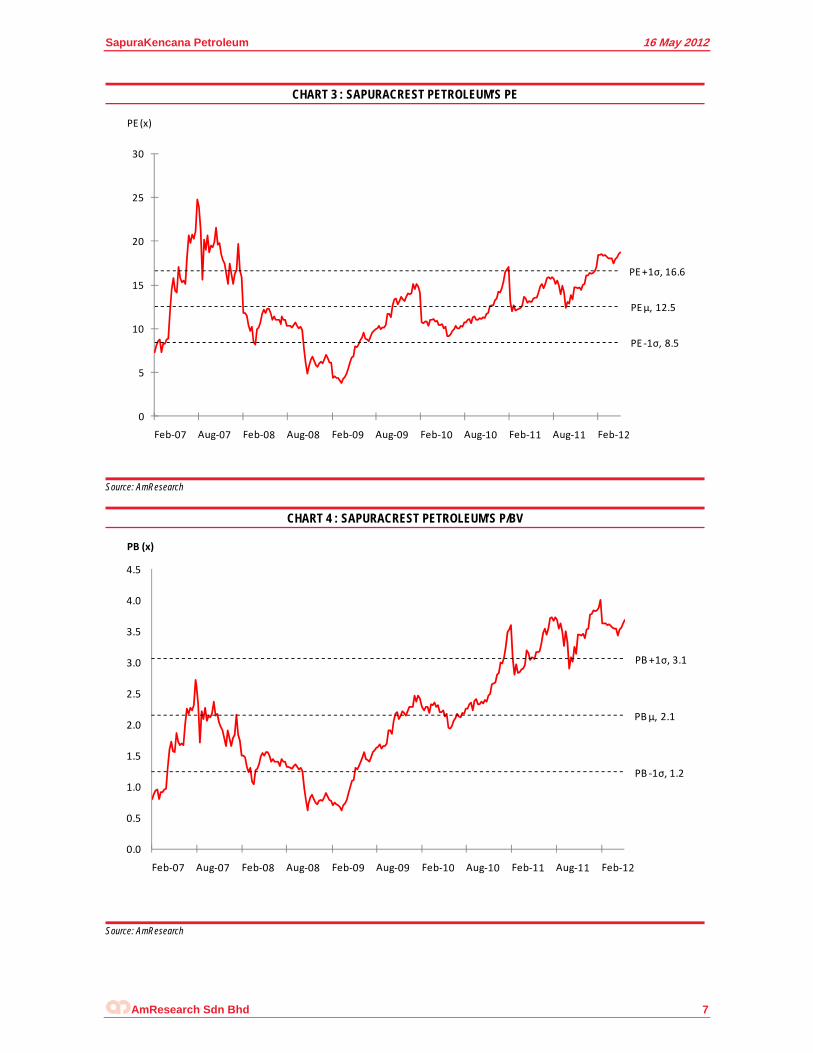

CHART 3 : SAPURACREST PETROLEUM’S PE

PE µ, 12.5

PE +1σ, 16.6

PE ‐1σ, 8.5

0

5

10

15

20

25

30

PE (x)

Source: AmResearch

CHART 4 : SAPURACREST PETROLEUM’S P/BV

PB µ, 2.1

PB +1σ, 3.1

PB ‐1σ, 1.2

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

PB (x)

Source: AmResearch

SapuraKencana Petroleum 16 May 2012

AmResearch Sdn Bhd 8

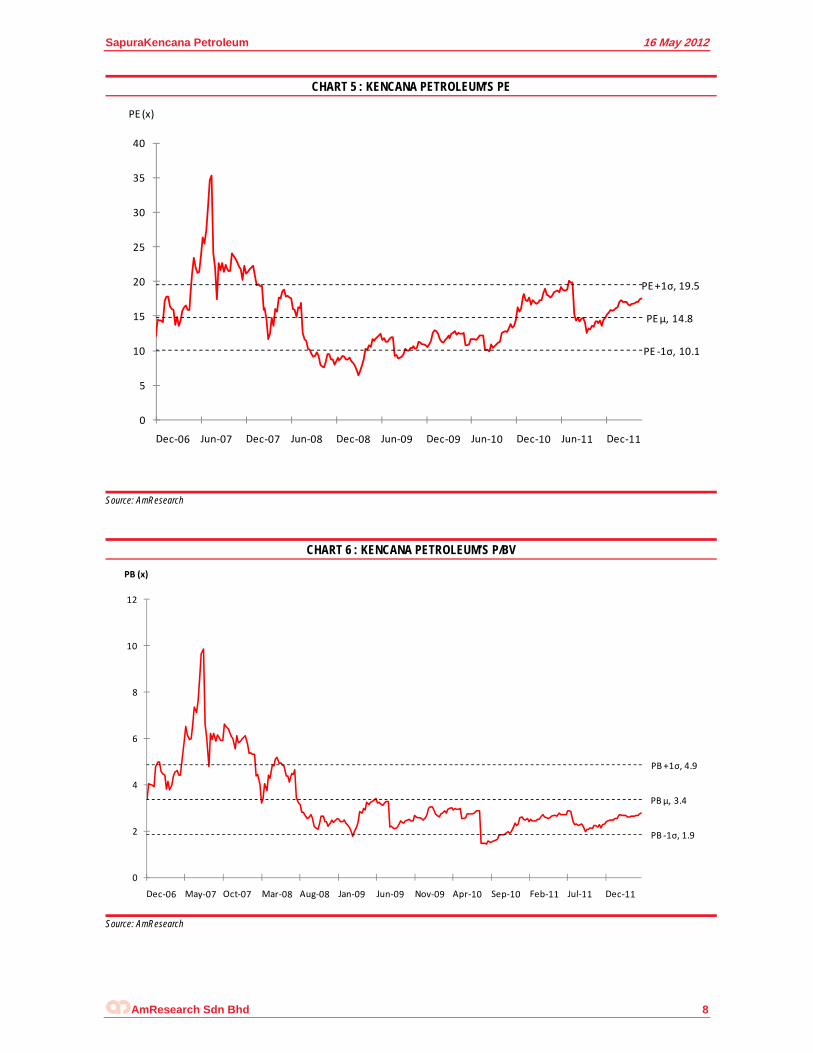

CHART 5 : KENCANA PETROLEUM’S PE

PE µ, 14.8

PE +1σ, 19.5

PE ‐1σ, 10.1

0

5

10

15

20

25

30

35

40

PE (x)

Source: AmResearch

CHART 6 : KENCANA PETROLEUM’S P/BV

PB µ, 3.4

PB +1σ, 4.9

PB ‐1σ, 1.9

0

2

4

6

8

10

12

PB (x)

Source: AmResearch

SapuraKencana Petroleum 16 May 2012

AmResearch Sdn Bhd 9

PICTURE 2 : SAPURA300 HEAVY LIFT PIPELAYING VESSEL

Source: SapuraCrest Petroleum

PICTURE 3 : LTS 3000(HEAVY LIFT PIPELAY VESSEL)

Source: SapuraCrest Petroleum

SapuraKencana Petroleum 16 May 2012

AmResearch Sdn Bhd 10

PICTURE 4 : QP2000 (DERRICK LAY BARGE)

Source: SapuraCrest Petroleum

PICTURE 5 : T3 - SELF-ERECTING TENDER RIG

Source: SapuraCrest Petroleum

SapuraKencana Petroleum 16 May 2012

AmResearch Sdn Bhd 11

PICTURE 6: T-10 SELF-ERECTING TENDER RIG

Source: SapuraCrest Petroleum

PICTURE 7: SARKU SEMANTAN (DIVING SUPPORT ACCOMODATION WORK VESSEL)

Source: SapuraCrest Petroleum

SapuraKencana Petroleum 16 May 2012

AmResearch Sdn Bhd 12

PICTURE 8: SARKU SANTUBONG (DIVING SUPPORT VESSEL)

Source: SapuraCrest Petroleum

PICTURE 9: SATURATION DIVING SYSTEM

Source: SapuraCrest Petroleum

SapuraKencana Petroleum 16 May 2012

AmResearch Sdn Bhd 13

PICTURE 10: REMOTELY OPERATED VEHICLE (TYPHOON ROV)

Source: SapuraCrest Petroleum

PICTURE 11: KM1 (TENDER-ASSISTED RIG)

Source: Kencana Petroleum

SapuraKencana Petroleum 16 May 2012

AmResearch Sdn Bhd 14

PICTURE 12: ANCHOR HANDLING TUG SUPPLY VESSEL WITH DP 2 AND 8,080 BHP CAPABILITY (GEMIA)

Source: Kencana Petroleum

Published by

AmResearch Sdn Bhd (335015-P) (A member of the AmInvestment Bank Group) 1 5 t h F l o o r B a ng u n a n A m B a n k G r ou p 55 Jalan Raja Chulan 50200 Kuala Lumpur Tel: ( 0 3 ) 2 0 7 0 - 2 4 4 4 ( r e s e a r c h ) F a x : ( 0 3 ) 2 0 7 8 - 3 1 6 2

Printed by

AmResearch Sdn Bhd (335015-P) (A member of the AmInvestment Bank Group) 1 5 t h F l o o r B a ng u n a n A m B a n k G r ou p 55 Jalan Raja Chulan 50200 Kuala Lumpur Tel: ( 0 3 ) 2 0 7 0 - 2 4 4 4 ( r e s e a r c h ) F a x : ( 0 3 ) 2 0 7 8 - 3 1 6 2

The information and opinions in this report were prepared by AmResearch Sdn Bhd. The investments discussed or recommended in this report may not be suitable for all investors. This report has been prepared for information purposes only and is not an offer to sell or a solicitation to buy any securities. The directors and employees of AmResearch Sdn Bhd may from time to time have a position in or with the securities mentioned herein. Members of the AmInvestment Group and their affiliates may provide services to any company and affiliates of such companies whose securities are mentioned herein. The information herein was obtained or derived from sources that we believe are reliable, but while all reasonable care has been taken to ensure that stated facts are accurate and opinions fair and reasonable, we do not represent that it is accurate or complete and it should not be relied upon as such. No liability can be accepted for any loss that may arise from the use of this report. All opinions and estimates included in this report constitute our judgement as of this date and are subject to change without notice.

For AmResearch Sdn Bhd

Benny Chew Managing Director

Related Documents