[Working Paper Series - GWP2013/01] GWP 2013/01 This research is a GoldEdge Working Paper Series, WP 2013/10 | © Bernard Tetteh Narkotey, April 2013 1 Oil and Gas Sector Firm-Level Productivity and the Long-Run National Revenue Generation Nexus – An Empirical Study of the Emerging Ghanaian Oil and Gas Sector Working Paper Series - The GoldEdge Group Bernard Tetteh Narkotey, Analyst Email: [email protected] [email protected] Keywords: oil and gas, sector, productivity, policy initiatives, government oil revenue, firm-level capital and operational costs Abstract This paper dissects with great acuteness, eminent issues revolving around the nascent Ghanaian oil and gas sector with primary scholarly focus on identifying the long-term link that exist between government income generation ability and firm-level productivity in the sector. Issues regarding initiatives that could propel the sector for growth had been raised. Further, attempts have been made to uncover and outline some emerging sector needs. Empirical revenue and productivity regression model is formulated in which factors such as firm-level productivity, capital and operational costs and gross pre-tax revenue are regressed against the proxy measurement of government revenue generation ability. The data had been sourced from the World Bank’s nineteen year (19) estimation of revenue and output generation ability of the discovered oil fields in the sector. It is established in this study that the Ghanaian oil and gas sector is nascent, with growth prospects that need to be managed effectively to avoid an imbalanced cross sectorial economic growth. There exist a significant relationship between oil and gas sector firm-level output and government ability to generate tax revenues. However, both output and government oil revenues are likely to peak after six years of exploration and production commencing 2011 and thereafter decline into the long-term. Although an inverse relationship is found between capital and operational costs and proceeds to be generated by the government in the long-run, minimal evidence exists to establish a direct and significant effect. Policy interventions that seek to manage oil price volatility by exploring alternate oil price-risk hedging strategies such as oil futures and options are highly commended in this paper. Sector policies and programmes that seek to eliminate production bottlenecks and imbalanced cross- sectorial GDP growth contribution in boom times are highly commended. Introduction Oil discoveries in recent times in large quantities in Ghana, has drawn both local and international attention to the Ghanaian economy with high concern on policy directions that would strategically position the nation for high alpha generating investments in the oil and gas sector. International energy companies—investors, equipment suppliers, contractors, and consulting firms—are shifting their attention from Europe and North America to developing countries which are likely to offer more business opportunities in the oil and gas sector in the future, following the

Oil and gas sector research a gold edge working paper series - 2013

Apr 09, 2017

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

[Working Paper Series - GWP2013/01] GWP 2013/01

This research is a GoldEdge Working Paper Series, WP 2013/10 | © Bernard Tetteh Narkotey, April 2013 1

Oil and Gas Sector Firm-Level Productivity and the Long-Run National Revenue

Generation Nexus – An Empirical Study of the Emerging Ghanaian Oil and Gas Sector

Working Paper Series - The GoldEdge Group

Bernard Tetteh Narkotey, Analyst Email: [email protected]

Keywords: oil and gas, sector, productivity, policy initiatives, government oil revenue, firm-level capital and operational costs

Abstract This paper dissects with great acuteness, eminent issues revolving around the nascent Ghanaian oil and gas sector with primary scholarly focus on identifying the long-term link that exist between government income generation ability and firm-level productivity in the sector. Issues regarding initiatives that could propel the sector for growth had been raised. Further, attempts have been made to uncover and outline some emerging sector needs. Empirical revenue and productivity regression model is formulated in which factors such as firm-level productivity, capital and operational costs and gross pre-tax revenue are regressed against the proxy measurement of government revenue generation ability. The data had been sourced from the World Bank’s nineteen year (19) estimation of revenue and output generation ability of the discovered oil fields in the sector. It is established in this study that the Ghanaian oil and gas sector is nascent, with growth prospects that need to be managed effectively to avoid an imbalanced cross sectorial economic growth. There exist a significant relationship between oil and gas sector firm-level output and government ability to generate tax revenues. However, both output and government oil revenues are likely to peak after six years of exploration and production commencing 2011 and thereafter decline into the long-term. Although an inverse relationship is found between capital and operational costs and proceeds to be generated by the government in the long-run, minimal evidence exists to establish a direct and significant effect. Policy interventions that seek to manage oil price volatility by exploring alternate oil price-risk hedging strategies such as oil futures and options are highly commended in this paper. Sector policies and programmes that seek to eliminate production bottlenecks and imbalanced cross-sectorial GDP growth contribution in boom times are highly commended.

Introduction Oil discoveries in recent times in large quantities in Ghana, has drawn both local and international attention to the Ghanaian economy with high concern on policy directions that would strategically position the nation for high alpha generating investments in the oil and gas sector.

International energy companies—investors, equipment suppliers, contractors, and consulting firms—are shifting their attention from Europe and North America to developing countries which are likely to offer more business opportunities in the oil and gas sector in the future, following the

[Working Paper Series - GWP2013/01] GWP 2013/01

This research is a GoldEdge Working Paper Series, WP 2013/10 | © Bernard Tetteh Narkotey, April 2013 2

increased energy demand and oil find mania in these economies (Razavi, 1996). Effective natural resource management initiatives in such boom periods are essential for a sustained cross-sectorial development (Collier and Goderis, 2007). Significance of the oil sector in any economy and the need for policy measures that effectively manage the sector dynamics for a maximized benefit had been extensively explored in existing oil and gas literature, such as evident in Mitchell (2013), Collier (2012), Kastning (2011), CEPA (2010), and World Bank (2009). (Collier and Goderis, 2007) noted that a large existing literature suggests that there is a resource curse-where natural resource abundant countries tend to grow slower than resource scarce countries. However, Collier and Goderis, 2007), just as Raddatz (2007) and Deaton and Miller (1995) observe in their study that resource curse is avoided by countries with sufficiently good institutions and even for low-income countries find natural commodity booms significantly raise growth. In Prempeh and Kron (2012), it has been firmly established that the Ghanaian oil and gas sector is novel; legislation, regulations and policies in the sector are under development and the primary focus of their implementations by the government centre on revenue mobilisation, revenue maximization and revenue spending. Following developments in the sector so far, there appear to be justifiably optimistic expectations about the role of oil sector in the development of the Ghanaian economy (CEPA, 2010). There had been directional calls at all levels–from the Global and national front, for development and strengthening of institutional and policy framework that are

necessary to provide the right frame of direction needed to manage the sector growth potentials. In 2011, the World Bank, International Monetary Fund (IMF) showed its ascent and commendation of the contraction of a $3 billion Chinese loan by the Ghana government to finance critical infrastructure development in the country especially in the oil and gas sector. Considering the collective effort at all levels-global and national, to support development of the oil sector, research initiatives that seeks to develop essential embodiment of knowledge and technical dynamics that could serve as reference points for sector policy formulation and implementation, as well as serving the needs of sector investors and players to reduce market information asymmetry for robust functioning sector, would be much welcomed. It is in the light of this depth that this study seeks to address the pertinent sector issues regarding the status of the sector, required support services or needs, the sector activities effects with the ultimate aim of examining the link that will exist between government income generation ability and firm-level productivity in the long-run; again to examine the need for policy initiatives that would propel growth in the sector. Empirical literature and Sector issues

The oil discovery – some stylised facts

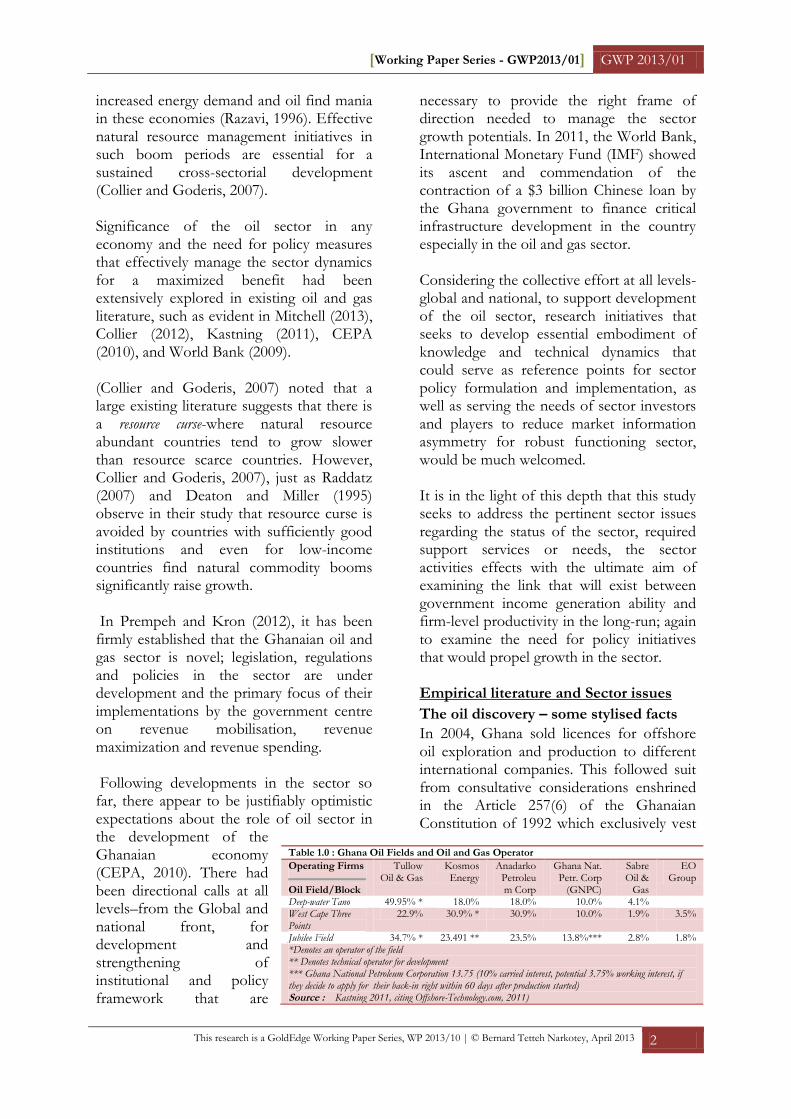

In 2004, Ghana sold licences for offshore oil exploration and production to different international companies. This followed suit from consultative considerations enshrined in the Article 257(6) of the Ghanaian Constitution of 1992 which exclusively vest

Table 1.0 : Ghana Oil Fields and Oil and Gas Operator

Operating Firms

Oil Field/Block

Tullow Oil & Gas

Kosmos Energy

Anadarko Petroleum Corp

Ghana Nat. Petr. Corp

(GNPC)

Sabre Oil &

Gas

EO Group

Deep-water Tano 49.95% * 18.0% 18.0% 10.0% 4.1% West Cape Three Points

22.9% 30.9% * 30.9% 10.0% 1.9% 3.5%

Jubilee Field 34.7% * 23.491 ** 23.5% 13.8%*** 2.8% 1.8% *Denotes an operator of the field ** Denotes technical operator for development *** Ghana National Petroleum Corporation 13.75 (10% carried interest, potential 3.75% working interest, if they decide to apply for their back-in right within 60 days after production started) Source : Kastning 2011, citing Offshore-Technology.com, 2011)

[Working Paper Series - GWP2013/01] GWP 2013/01

This research is a GoldEdge Working Paper Series, WP 2013/10 | © Bernard Tetteh Narkotey, April 2013 3

mineral deposits in the state. Large quantities of crude light and sweet oil off the shores of the Western Atlantic Coast - “Jubilee fields” were discovered June 2007 and development of the production site started right away in December 2010 (Kastning, 2011).The Jubilee field, located in the Gulf of Guinea, 60 km off the Ghanaian coast, near the Côte d’Ivoire border and its spread out in the Deep-water Tano and West Cape Three Points blocks. The wells are at a water depth between 1,100 and 1,300 meters and at a total depth between 3,400 and 4,200 meters. The field covers

110 km², which is about the size of 155 football pitches [Kastning 2011, citing Offshore-Technology.com, 2011]. Gas coming along with the Oil finds

Kastning (2011) citing Tullow (2011) indicated that It is estimated that the field contains an additional 1.2 trillion cubic feet of gas, which are approximately 162 million barrels of oil equivalent (mmboe). This measurement of gas in the unit of barrel is based on the approximate energy released by burning one barrel of crude oil. Extimates in the World Bank (2011) report showed that at peak the phase one (1) Jubilee

production, could produce 120 million cubic

feet of gas per day and that at a world market

natural gas liquid prices and a dry gas price of US$2 per thousand cubic feet, gross revenues would be roughly US$260 million per year. This was extimated to be less than a tenth of gross

estimated oil revenue. Gas is 100% recoverable [Tullow Oil, 2010]. In geological terms, the Jubilee field is a continuous stratigraphic trap with combined hydrocarbon columns in excess of 600 meters (Kastning, 2011).

How the oil field operations had been

organised

An overview of operations in the field was

presented in Kastning (2011). Kastning

(2011) indicated that nine production wells

bring the oil and gas from below ground to

the surface. In addition there exist eight

drillings to inject gas and water. This is done

to maintain the field pressure and to get rid

of the gas, as long as there is no pipeline to

the shore. Again, Kastning (2011)

emphasized that constant gas flaring is

forbidden in Ghana. The seventeen (17)

connects to the Floating, Production,

Storage and Offloading (FPSO)-Kwame

Nkrumah vessel. On the FPSO a daily

0

500

1000

1500

2000

2500

3000

3500

0

20

40

60

80

100

120

140Jubilee Phase I Base Case IMF Projected Output

Output ('000 bpd) Gross Revenue (US$ million)

[Working Paper Series - GWP2013/01] GWP 2013/01

This research is a GoldEdge Working Paper Series, WP 2013/10 | © Bernard Tetteh Narkotey, April 2013 4

maximum of 120,000 barrels of crude oil is

to be separated from gas and water. Most of

these by-products are then pumped back

through the injection wells. For resource

usage efficiency, 15% of the gas is used for

power generation to run the FPSO.

Transport ships collect the oil from the

FPSO every seven (7) to ten (10) days and

ship to worldwide refineries. During the first

phase, four drilling rigs were already under

contract to finish the exploration and

development of the remaining areas of the

field, namely the southeast part. What explains the variations in productivity outturns?

The existing observation on the oil productivity outturns of the field regarding the first two years of production – 2010 and

2011 (being 106.9 bpd and 120.5 bpd) shows a significant variation by a 38% and 30% down (66.3 and 84.7 bpd) for the two years respectively compared to the earlier estimates by the World Bank Staff in late 2009. Shortfalls in output had been attributed to production bottlenecks in the Jubilee Fields in the Ghana 2013 Budget. Nonetheless, reference could be made to the fact that sufficient information was not available on the Ghana petroleum sector for driving the assumptions for the earlier World Bank forecasts. Would the negative effects raised in the oil literature hold? Does the Dutch disease appear looming? Ghana already has a growing non-tradable (non-agricultural sector) sector. The service sector leads the 2012 7.1% GDP growth, recording the highest 8.8% GDP growth rate (GSS, 2012). Would the World Bank 2009 prediction that without Reforms, oil could lower per capita

incomes in the long run still possess a looming economic threat, considering the output turnouts so far? According to the Word Bank (2009) oil literature, comparing the baseline scenario (where real disposable per capita incomes would grow by 3.4 percent per year) with the first alternative scenario, suggested that after the initial demand boom (which would peak in 2015 and get exhausted by 2020), Ghana‘s long-term growth trajectory would actually shift down in comparison to a non-oil scenario. The long term per capita income growth rate would decelerate to 2.4 percent and, by 2029 real per capita incomes would be 14 percent lower (World Bank, 2009). This prediction in the World Bank literature departs from observation in Collier and Goderis, 2007), as well as Raddatz (2007) and Deaton and Miller (1995) who observe

that oil discoveries and boom times would not necessarily translate into economic slowdowns, but rather countries with

sufficiently good institutions and even for low-income countries, natural commodity booms significantly raise growth. It is worth focussing our discussion in this literature on the sector’s ability to meet future national consumption. Questions regarding how the present energy demands of Ghana would look like in the future? Would such demands be meet in a sustainable way if reliance is placed on forecasted internal production capacities? How could the expected revenue best insured – would strategic hedging options

Table 2.0 : Jubilee Phase I Base Case Projected Output

Year 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Output ('000 bpd)

106..9 120..5 120.5 120..5 120..5 101.4 89 79.5 69.9 61.6

Actual Outturn

66.3

84.7

83.3*

-

-

-

-

-

-

-

Source: World Bank staff calculations-2009

8.96 8.79 9.32

111.21 109.24 113.05

2.56 2.63 2.69

-

20

40

60

80

100

120

2008 2009 2010

Th

ou

san

ds

Energy Annual consumption -Ghana and selected neibouring countries (kt of oil equivalent)

Ghana

Nigeria

Togo

[Working Paper Series - GWP2013/01] GWP 2013/01

This research is a GoldEdge Working Paper Series, WP 2013/10 | © Bernard Tetteh Narkotey, April 2013 5

such as oil futures, oil options and insurance be explored to complement existing stabilisation funds? How do the nation’s energy (oil related) consumption stand

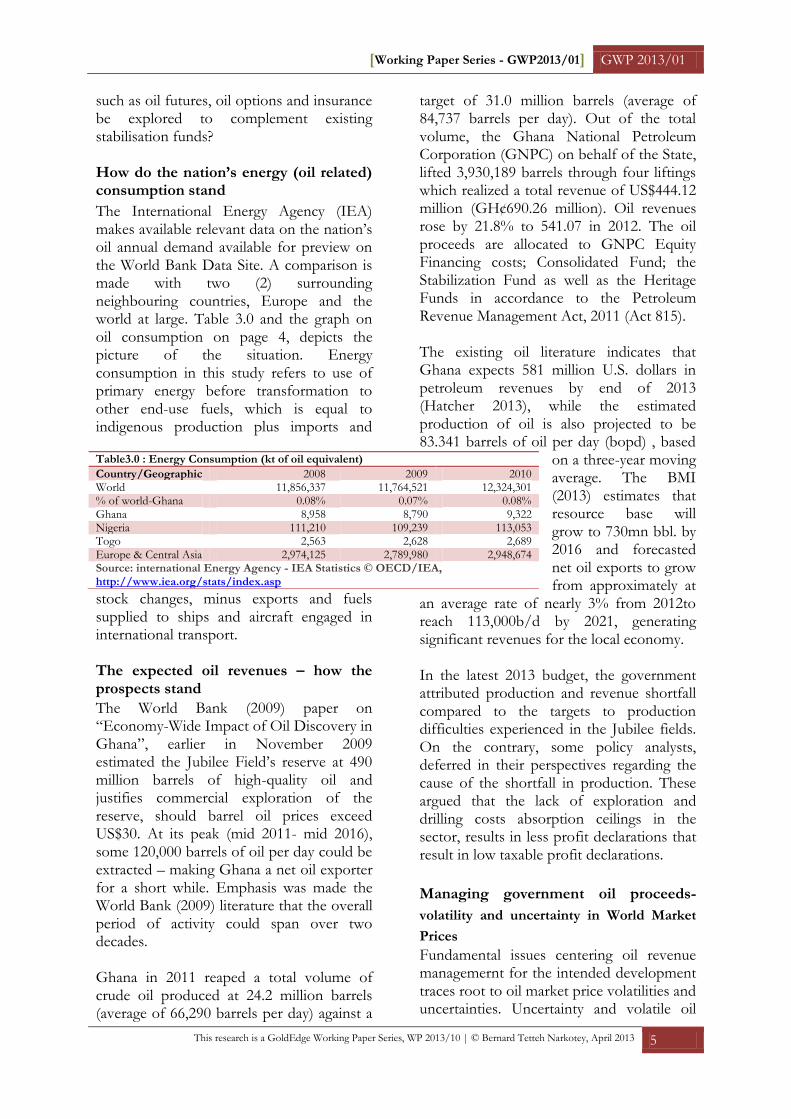

The International Energy Agency (IEA) makes available relevant data on the nation’s oil annual demand available for preview on the World Bank Data Site. A comparison is made with two (2) surrounding neighbouring countries, Europe and the world at large. Table 3.0 and the graph on oil consumption on page 4, depicts the picture of the situation. Energy consumption in this study refers to use of primary energy before transformation to other end-use fuels, which is equal to indigenous production plus imports and

stock changes, minus exports and fuels supplied to ships and aircraft engaged in international transport. The expected oil revenues – how the prospects stand

The World Bank (2009) paper on “Economy-Wide Impact of Oil Discovery in Ghana”, earlier in November 2009 estimated the Jubilee Field’s reserve at 490 million barrels of high-quality oil and justifies commercial exploration of the reserve, should barrel oil prices exceed US$30. At its peak (mid 2011- mid 2016), some 120,000 barrels of oil per day could be extracted – making Ghana a net oil exporter for a short while. Emphasis was made the World Bank (2009) literature that the overall period of activity could span over two decades. Ghana in 2011 reaped a total volume of crude oil produced at 24.2 million barrels (average of 66,290 barrels per day) against a

target of 31.0 million barrels (average of 84,737 barrels per day). Out of the total volume, the Ghana National Petroleum Corporation (GNPC) on behalf of the State, lifted 3,930,189 barrels through four liftings which realized a total revenue of US$444.12 million (GH¢690.26 million). Oil revenues rose by 21.8% to 541.07 in 2012. The oil proceeds are allocated to GNPC Equity Financing costs; Consolidated Fund; the Stabilization Fund as well as the Heritage Funds in accordance to the Petroleum Revenue Management Act, 2011 (Act 815). The existing oil literature indicates that Ghana expects 581 million U.S. dollars in petroleum revenues by end of 2013 (Hatcher 2013), while the estimated production of oil is also projected to be 83.341 barrels of oil per day (bopd) , based

on a three-year moving average. The BMI (2013) estimates that resource base will grow to 730mn bbl. by 2016 and forecasted net oil exports to grow from approximately at

an average rate of nearly 3% from 2012to reach 113,000b/d by 2021, generating significant revenues for the local economy. In the latest 2013 budget, the government attributed production and revenue shortfall compared to the targets to production difficulties experienced in the Jubilee fields. On the contrary, some policy analysts, deferred in their perspectives regarding the cause of the shortfall in production. These argued that the lack of exploration and drilling costs absorption ceilings in the sector, results in less profit declarations that result in low taxable profit declarations.

Managing government oil proceeds-

volatility and uncertainty in World Market

Prices

Fundamental issues centering oil revenue managemernt for the intended development traces root to oil market price volatilities and uncertainties. Uncertainty and volatile oil

Table3.0 : Energy Consumption (kt of oil equivalent)

Country/Geographic 2008 2009 2010 World 11,856,337 11,764,521 12,324,301 % of world-Ghana 0.08% 0.07% 0.08% Ghana 8,958 8,790 9,322 Nigeria 111,210 109,239 113,053 Togo 2,563 2,628 2,689 Europe & Central Asia 2,974,125 2,789,980 2,948,674 Source: international Energy Agency - IEA Statistics © OECD/IEA, http://www.iea.org/stats/index.asp

[Working Paper Series - GWP2013/01] GWP 2013/01

This research is a GoldEdge Working Paper Series, WP 2013/10 | © Bernard Tetteh Narkotey, April 2013 6

prices can cause boom-bust cycles in economic management and growth (CEPA, 2010). Volatility in world market prices and government revenues could create macroeconomic instability in the economy, raising risks and reducing the risk-adjusted profitability of investments.

Daniel (2001) noted in his work that the

governments typically bear two kinds of oil

price risks. First and foremost many

governments in oil producing developing

countries obtain substantial revenue from oil

production/exploration. Second many of

these governments also try to smooth

domestic oil-product prices to mitigate the

social, economic, and political impact of

large and frequent changes in the oil product

prices. In both cases the fiscal position of

the government depends substantially on

the oil price (Daniel, 2001).

In oil and gas literature, two common

alternatives had been theoretically

propounded to mitigate the oil price risk

exposure that oil producing countries face

(Daniel, 2001 and Arrau and Stijn, 1992). In

Daniel (2001) oil futures and options are

emphasized as effective government

revenue hedging strategies compared to the

use of stabilization funds observed in Arrau

and Stijn (1992). Nonetheless, lack of

knowledge of effectiveness of these hedging

options and fear of loss of political will had

been the major impediment for designing

and implementing programmes that place

premium on the proposed hedging strategies

in the oil and gas literature.

Some highlights of the oil and gas sector

needs and support services trend

In oil and gas literature, strong arguments

had been made for policies and programmes

that strengthen institutions since strong

institutional structures are regarded as

foundations for avoiding economic

imbalance and instabilities in oil exploration

and producing and countries.

Institutional structures that ensure sound

financial markets, trade and arbitration,

competitive markets and resource

allocations, fiscal and monitory disciplines,

well segmented and integrated upstream,

mid-stream and downstream valued based

oil service delivering entities, investors,

contractors and business advisors would be

much needed for take-offs in the sector.

The GBI Research (2013) indicated that as

a result of increased logistics activity in the

oil and gas sector due to increasing

international and domestic trades, the

demand for oil and gas storage capacity is a

current important trend in the oil and gas

sector that is witnessing a rise at the major

global supply hubs. The trend is expected to

continue, with the major terminal operators

worldwide as the key beneficiaries.

However, the supply chain operators which

are relatively having less proximity from the

main storage hubs are not expected to

benefit substantially from the current

scenario.

Markest and Markets (2012) finds that the

use of Hydraulic fracturing which is mainly

concentrated in North America, where

many leading oil field service companies –

Schlumberger (U.S.), Halliburton (U.S.),

Baker Hughes (U.S.), and other medium and

small players – operate is now gaining

popularity in other oil exploration

economies. While the North American

hydraulic fracturing market is reaching

maturity, the Rest of the World’s (ROW)

market is still in its infancy. Markets and

Markets (2012) indicate that the Hydraulic

fracturing is the propagation of fractures

[Working Paper Series - GWP2013/01] GWP 2013/01

This research is a GoldEdge Working Paper Series, WP 2013/10 | © Bernard Tetteh Narkotey, April 2013 7

through layers of rock using pressurized

fracturing fluid. The technique is primarily

used in the extraction of resources from low

permeability reservoirs – such as shale gas,

tight gas, CBM, and unconventional liquids

– which are difficult to recover through

regular drilling procedures. Hydraulic

fracturing services are now being provided

by oilfield service companies (such as

Halliburton) to oil and gas companies (such

as Shell). Hydraulic fracturing was first used

in 1947, since then scores of wells have been

fractured.

Nonetheless, Hydraulic Fracturing is facing

a lot of public opposition due to potential

environmental hazards caused by fracturing.

Water usage, water contamination, and

seismic activity are the most important

concerns related to hydraulic fracturing.

Because of these environmental concerns,

the growth of hydraulic fracturing market in

the rest of the world market is somewhat

lessened. In fact, some companies have even

banned the use of hydraulic fracturing. This

presents an opportunity to oilfield service

companies to use ‘waterless’ hydraulic

fracturing or foam fracturing.

Exploring faster means for detecting and

measuring precisely the volume of oil in

wells could also be considered a key be

catalysts for an oil boom. The Reuters

(2013) reports Total Plc.’s launch of a new

supercomputer-Pangea that will help find oil

15times faster than before. The machine

helps gauge more precisely the potentials of

oil exploration wells and the size of oil

reserves. [Since this paper appears a working document,

details of latest oil sector need assessment and analytics could be

obtained by writing to the author. E-mail:

[email protected].…….]

Econometric model specification and Design The empirical analysis involves the application of cross-section data econometric methods with a balanced panel dataset that combines both and looks at multiple variables and how they change over the course of time with a random effect regressions of selected variable over estimated data point period 2010-2020 for a single case study country, Ghana. The individual effects in the random effects model are specified through a variable that is uncorrelated with the independent variables. In fixed effects models, a correlation between the individual error term and the predictor variables is assumed. Some proxies are employed in measuring dependent and independent terms in the regression models.

As evident in Dioda (2012), Gupta (2007) and Bird et al. (2004), proceeds from oil taxation, royalties and fees, had been used to proxy national revenue proceeds from oil exploration and production and this is the dependent variable adopted in model specification. Unlike, in existing literature such as Gupta (2007), that size of the economy expressed as GDP at purchasing power parity is employed as control variable and regressed against revenue, this paper ignores this level of measurement to reflect the complete impact at the firm-level productivity level. The size of firm-level production is used instead and is expressed as the logarithm of output per thousand barrels. The size of operational costs which is also a determinant of firm-level after tax revenue is also expressed as the logarithm of capital and operational costs of exploration and production. Hence, the regression model is formulated as follows:

…….. (1)

….. (2)

Generally, the dependent in equation (1) is

given as on the left of the equation,

[Working Paper Series - GWP2013/01] GWP 2013/01

This research is a GoldEdge Working Paper Series, WP 2013/10 | © Bernard Tetteh Narkotey, April 2013 8

being the constant for i in time t. is a set

of vector variables such as short-term debt, long term debt or firm size. The error term

is denoted

consisting of two

components where accounts

for any unobservable firm-specific effects that are not included in the regression model

and caters for the remaining

disturbances in the regression which varies with the individual firms and time.

In equation (2), denotes the size of

revenue the government could realises through tax, royalties and licensing from the existing oil fields over the estimated time

span, denotes the size of firm-level

output capacity while is a control

variable denoting operating and capital costs of oil exploration and production. is also a control variable denoting the gross pre-tax oil revenue from the oil field. The size of firm-level operating and capital costs as well as gross pre-tax oil proceeds were included in the model as control variables with the double purpose of evaluating their effect on government revenue and to strengthen the model through a robustness check. The empirical use of independed variables such as trade openness observed in Bird (2004), share of agriculture over GDP as proxy variable for national development level in Dioda (2012); literacy rate in Mahdavi (2008), foreign aid and debt/GDP ratio in Profeta and Scabrosetti (2010); internal conflicts and fiscal capacity in Cárdenas, Eslava and Ramirez (2010) have not been followed in this paper. Though this may place some level of limitations on the results, the approach in this paper had been chosen against the backdrop of highly limited data available on the Ghanaian petroleum sector.

Another very significant issue to be considered in interpreting the results of the econometric model in this paper is the use of forecasted data set that are largely based on tested assumptions by the of the World Bank staff in the November 2009 oil

literature. The results of this analysis would therefore largely depend on the accuracy and validity of assumptions underlining the forecasted dataset. According to the source of the data-set- World Bank (2009), the base case –the Jubilee Fields, was defined as a single offshore field with 500 million bbl. of recoverable oil reserves; output capacity of 120,000 bpd of oil and 120 mmscfd of gas; output at peak capacity for 5 years followed by 14 years of declining output; first production in 2011; re-injection of all gas; capital cost of $4 billion (including purchase of FPSO).

Key highlights on the data-set in the literature involve:

An oil price of $50 results in total government revenues of $8.6 billion (56 percent) and government share of net cash flow of 55 percent; a price of $100 resulting in total government revenues of $29.3 billion (+51 percent) and government share of net cash flow of 72 percent

At an oil price of $30 the Jubilee Field project is marginally economic (16 percent IRR pre-tax) and generates just $3 billion of government revenue

A 25 percent capital cost overrun on its own reduces total government revenues by 14% and, when combined with a $50 oil price, reduces total government revenues by over 60 percent

A two-year period of peak production, as against five years, on its own reduces total government revenues by some 60 percent and, when combined with a $50 oil price, reduces total government revenues by over 80 percent.

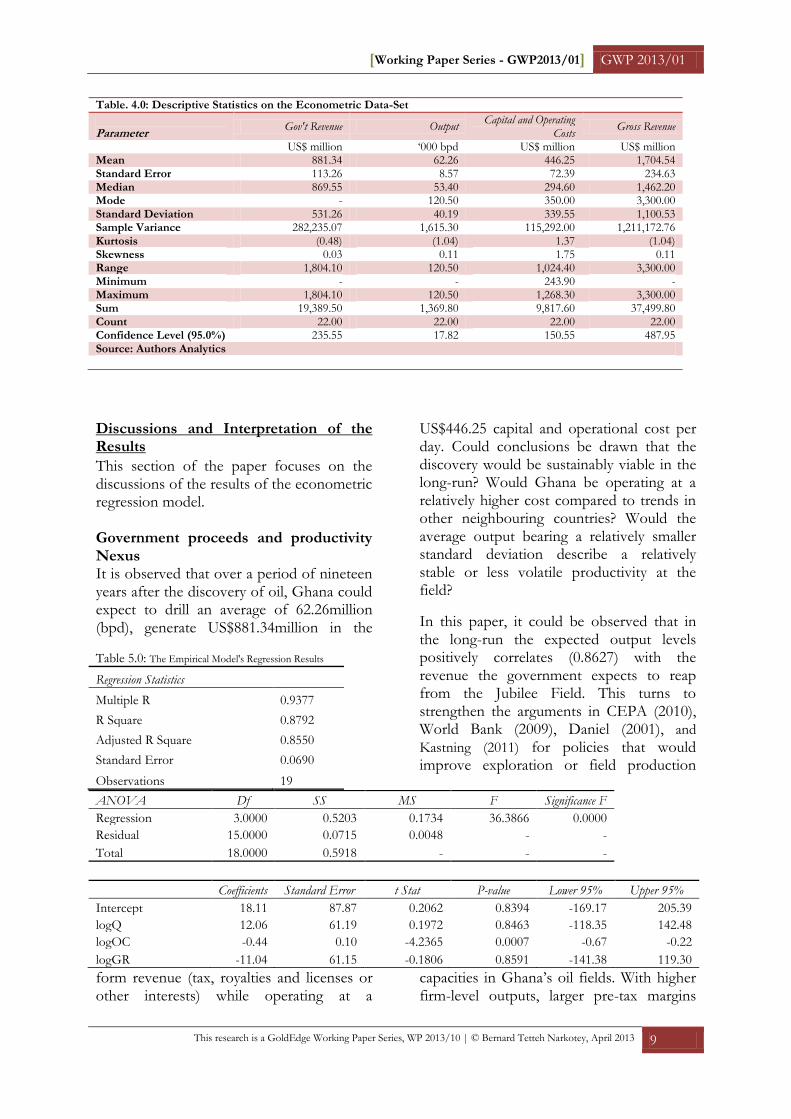

The summary statistics on the data-set is presented in table 4.0. Below:

[Working Paper Series - GWP2013/01] GWP 2013/01

This research is a GoldEdge Working Paper Series, WP 2013/10 | © Bernard Tetteh Narkotey, April 2013 9

Discussions and Interpretation of the Results

This section of the paper focuses on the discussions of the results of the econometric regression model. Government proceeds and productivity Nexus It is observed that over a period of nineteen years after the discovery of oil, Ghana could expect to drill an average of 62.26million (bpd), generate US$881.34million in the

form revenue (tax, royalties and licenses or other interests) while operating at a

US$446.25 capital and operational cost per day. Could conclusions be drawn that the discovery would be sustainably viable in the long-run? Would Ghana be operating at a relatively higher cost compared to trends in other neighbouring countries? Would the average output bearing a relatively smaller standard deviation describe a relatively stable or less volatile productivity at the field?

In this paper, it could be observed that in the long-run the expected output levels positively correlates (0.8627) with the revenue the government expects to reap from the Jubilee Field. This turns to strengthen the arguments in CEPA (2010), World Bank (2009), Daniel (2001), and

Kastning (2011) for policies that would improve exploration or field production

capacities in Ghana’s oil fields. With higher firm-level outputs, larger pre-tax margins

Table. 4.0: Descriptive Statistics on the Econometric Data-Set

Parameter

Gov't Revenue Output Capital and Operating

Costs Gross Revenue

US$ million ‘000 bpd US$ million US$ million Mean 881.34 62.26 446.25 1,704.54 Standard Error 113.26 8.57 72.39 234.63 Median 869.55 53.40 294.60 1,462.20 Mode - 120.50 350.00 3,300.00 Standard Deviation 531.26 40.19 339.55 1,100.53 Sample Variance 282,235.07 1,615.30 115,292.00 1,211,172.76 Kurtosis (0.48) (1.04) 1.37 (1.04) Skewness 0.03 0.11 1.75 0.11 Range 1,804.10 120.50 1,024.40 3,300.00 Minimum - - 243.90 - Maximum 1,804.10 120.50 1,268.30 3,300.00 Sum 19,389.50 1,369.80 9,817.60 37,499.80 Count 22.00 22.00 22.00 22.00 Confidence Level (95.0%) 235.55 17.82 150.55 487.95 Source: Authors Analytics

Table 5.0: The Empirical Model's Regression Results

Regression Statistics

Multiple R 0.9377

R Square 0.8792

Adjusted R Square 0.8550

Standard Error 0.0690

Observations 19

ANOVA Df SS MS F Significance F Regression 3.0000 0.5203 0.1734 36.3866 0.0000 Residual 15.0000 0.0715 0.0048 - - Total 18.0000 0.5918 - - -

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 18.11 87.87 0.2062 0.8394 -169.17 205.39

logQ 12.06 61.19 0.1972 0.8463 -118.35 142.48

logOC -0.44 0.10 -4.2365 0.0007 -0.67 -0.22

logGR -11.04 61.15 -0.1806 0.8591 -141.38 119.30

[Working Paper Series - GWP2013/01] GWP 2013/01

This research is a GoldEdge Working Paper Series, WP 2013/10 | © Bernard Tetteh Narkotey, April 2013 10

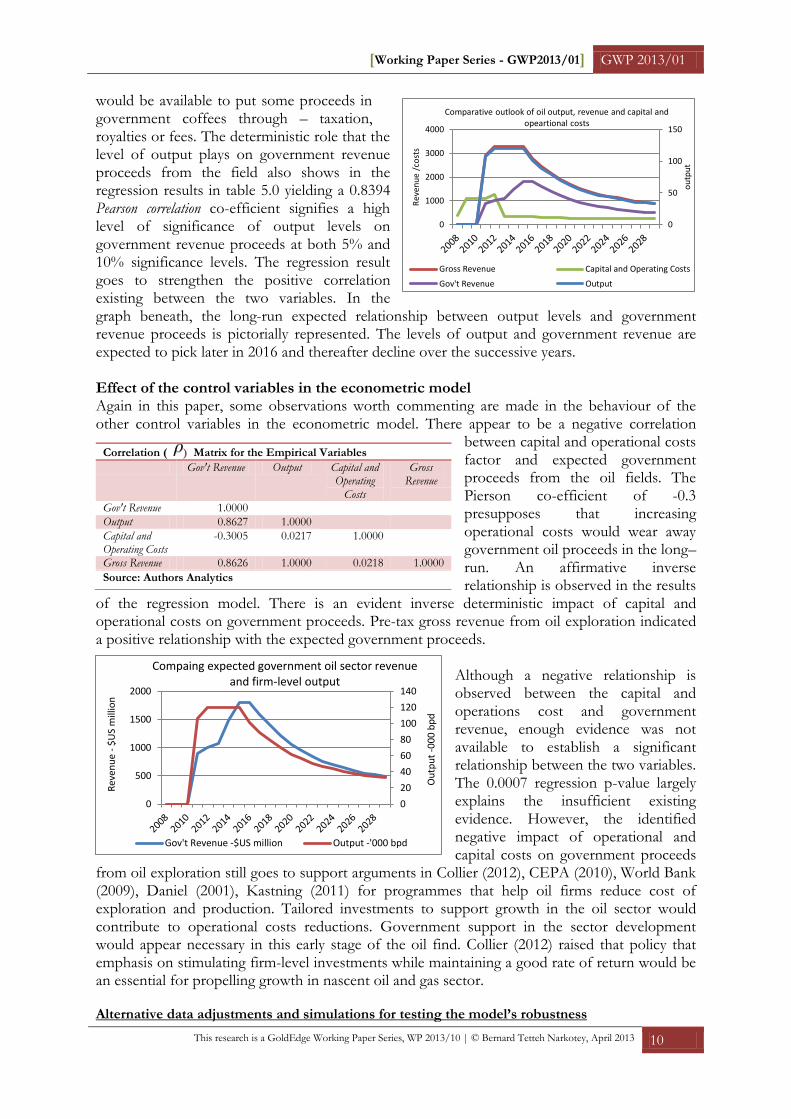

would be available to put some proceeds in government coffees through – taxation, royalties or fees. The deterministic role that the level of output plays on government revenue proceeds from the field also shows in the regression results in table 5.0 yielding a 0.8394 Pearson correlation co-efficient signifies a high level of significance of output levels on government revenue proceeds at both 5% and 10% significance levels. The regression result goes to strengthen the positive correlation existing between the two variables. In the graph beneath, the long-run expected relationship between output levels and government revenue proceeds is pictorially represented. The levels of output and government revenue are expected to pick later in 2016 and thereafter decline over the successive years. Effect of the control variables in the econometric modelAgain in this paper, some observations worth commenting are made in the behaviour of the other control variables in the econometric model. There appear to be a negative correlation

between capital and operational costs factor and expected government proceeds from the oil fields. The Pierson co-efficient of -0.3 presupposes that increasing operational costs would wear away government oil proceeds in the long–run. An affirmative inverse relationship is observed in the results

of the regression model. There is an evident inverse deterministic impact of capital and operational costs on government proceeds. Pre-tax gross revenue from oil exploration indicated a positive relationship with the expected government proceeds.

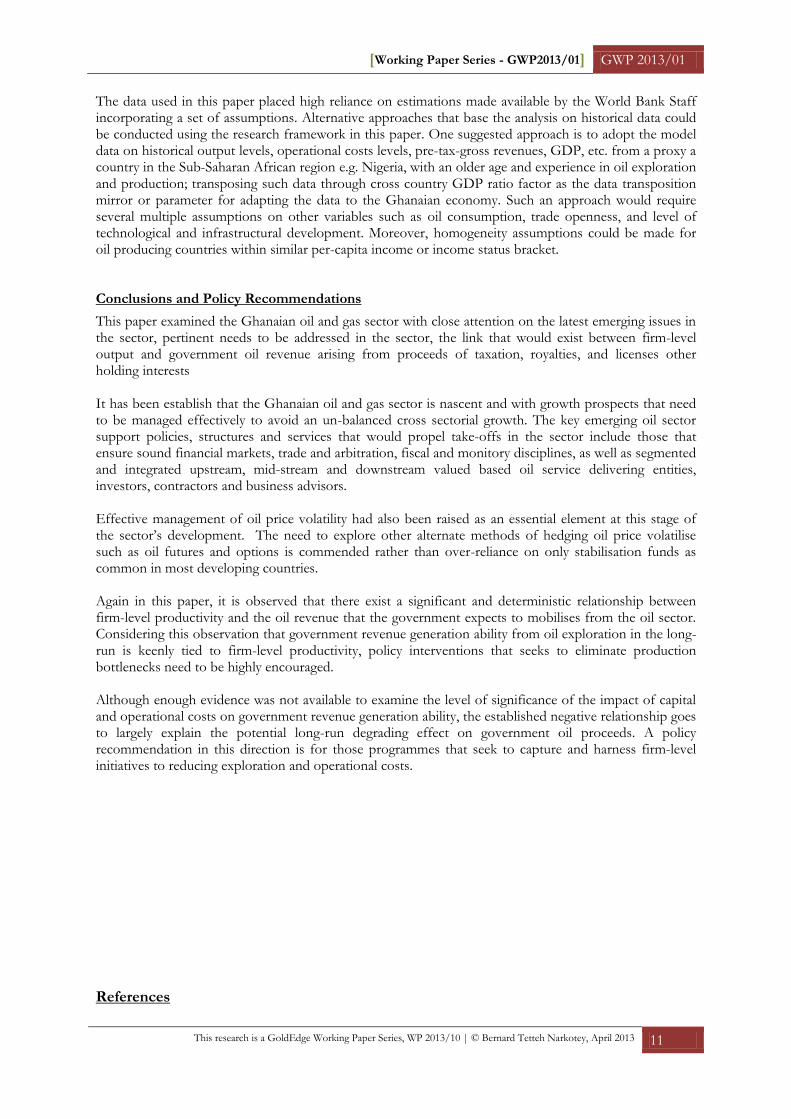

Although a negative relationship is observed between the capital and operations cost and government revenue, enough evidence was not available to establish a significant relationship between the two variables. The 0.0007 regression p-value largely explains the insufficient existing evidence. However, the identified negative impact of operational and capital costs on government proceeds

from oil exploration still goes to support arguments in Collier (2012), CEPA (2010), World Bank (2009), Daniel (2001), Kastning (2011) for programmes that help oil firms reduce cost of exploration and production. Tailored investments to support growth in the oil sector would contribute to operational costs reductions. Government support in the sector development would appear necessary in this early stage of the oil find. Collier (2012) raised that policy that emphasis on stimulating firm-level investments while maintaining a good rate of return would be an essential for propelling growth in nascent oil and gas sector. Alternative data adjustments and simulations for testing the model’s robustness

Correlation ( ) Matrix for the Empirical Variables

Gov't Revenue Output Capital and Operating

Costs

Gross Revenue

Gov't Revenue 1.0000

Output 0.8627 1.0000

Capital and Operating Costs

-0.3005 0.0217 1.0000

Gross Revenue 0.8626 1.0000 0.0218 1.0000

Source: Authors Analytics

0

50

100

150

0

1000

2000

3000

4000

ou

tpu

t

Rev

enu

e /c

ost

s

Comparative outlook of oil output, revenue and capital and opeartional costs

Gross Revenue Capital and Operating Costs

Gov't Revenue Output

0

20

40

60

80

100

120

140

0

500

1000

1500

2000

Ou

tpu

t -0

00

bp

d

Rev

enu

e -

$U

S m

illio

n

Compaing expected government oil sector revenue and firm-level output

Gov't Revenue -$US million Output -'000 bpd

[Working Paper Series - GWP2013/01] GWP 2013/01

This research is a GoldEdge Working Paper Series, WP 2013/10 | © Bernard Tetteh Narkotey, April 2013 11

The data used in this paper placed high reliance on estimations made available by the World Bank Staff incorporating a set of assumptions. Alternative approaches that base the analysis on historical data could be conducted using the research framework in this paper. One suggested approach is to adopt the model data on historical output levels, operational costs levels, pre-tax-gross revenues, GDP, etc. from a proxy a country in the Sub-Saharan African region e.g. Nigeria, with an older age and experience in oil exploration and production; transposing such data through cross country GDP ratio factor as the data transposition mirror or parameter for adapting the data to the Ghanaian economy. Such an approach would require several multiple assumptions on other variables such as oil consumption, trade openness, and level of technological and infrastructural development. Moreover, homogeneity assumptions could be made for oil producing countries within similar per-capita income or income status bracket. Conclusions and Policy Recommendations

This paper examined the Ghanaian oil and gas sector with close attention on the latest emerging issues in the sector, pertinent needs to be addressed in the sector, the link that would exist between firm-level output and government oil revenue arising from proceeds of taxation, royalties, and licenses other holding interests It has been establish that the Ghanaian oil and gas sector is nascent and with growth prospects that need to be managed effectively to avoid an un-balanced cross sectorial growth. The key emerging oil sector support policies, structures and services that would propel take-offs in the sector include those that ensure sound financial markets, trade and arbitration, fiscal and monitory disciplines, as well as segmented and integrated upstream, mid-stream and downstream valued based oil service delivering entities, investors, contractors and business advisors. Effective management of oil price volatility had also been raised as an essential element at this stage of the sector’s development. The need to explore other alternate methods of hedging oil price volatilise such as oil futures and options is commended rather than over-reliance on only stabilisation funds as common in most developing countries. Again in this paper, it is observed that there exist a significant and deterministic relationship between firm-level productivity and the oil revenue that the government expects to mobilises from the oil sector. Considering this observation that government revenue generation ability from oil exploration in the long-run is keenly tied to firm-level productivity, policy interventions that seeks to eliminate production bottlenecks need to be highly encouraged. Although enough evidence was not available to examine the level of significance of the impact of capital and operational costs on government revenue generation ability, the established negative relationship goes to largely explain the potential long-run degrading effect on government oil proceeds. A policy recommendation in this direction is for those programmes that seek to capture and harness firm-level initiatives to reducing exploration and operational costs.

References

[Working Paper Series - GWP2013/01] GWP 2013/01

This research is a GoldEdge Working Paper Series, WP 2013/10 | © Bernard Tetteh Narkotey, April 2013 12

Arrau, P. and Stijn, C. (1992), “Commodity Stabilisation Funds”, World Bank Policy Research Working Paper 835, Washington: World Bank

Bird, R. M., J. Martínez-Vásquez and B. Torgler (2004), “Societal Institutions And Tax Effort In Developing Countries”, Andrew Young School of Policy Studies, Georgia State University, Working Paper 04-06

BMI (2013), “Ghana Oil and Gas Report Q1 2013”, the Ghana Oil Online Webpage. Availability at: http://ghanaoilonline.org/2013/01/ghana-oil-and-gas-report-q1-2013/. Cited: 1st April 2013

Centre for Policy Analysis [CEPA] (2010), “Ghana: The Emerging Oil Economy Prospects and Challenges”, Centre for Policy Analysis No. 4 Prempeh II Street GIMPA Campus, Greenhill – Accra Collier, P and Goderis, B. (2007), “Commodity Prices, Growth, and the Natural Resource Curse: Reconciling a Conundrum”, University of Oxford. Available online at: http://economics.ouls.ox.ac.uk/13218/1/2007-15text.pdf. Cited 2nd April 2013 Collier, P. (2012), “Managing Ghana's Oil Discovery”, Centre for the Study of African Economies, Department of Economics, Oxford University. Available online at: http://www.ug.edu.gh/icde/ANYSC_Prof_%20Collier_KeyNote_Address.pdf. Cited 31st March 2013 Daniel, A.J. (2001), “Hedging Oil Price Risk”, IMF – Working Paper – WP01//185. Available online at: http://www.imf.org/external/pubs/ft/wp/2001/wp01185.pdf.c. Cited: 31st March, 2013 Deaton, A. S. and Miller, R I (1995), “International Commodity Prices, Macroeconomic Performance, and Politics in Sub-Saharan Africa”, Princeton Studies in International Finance 79 Dioda, L. (2012), “Structural Determinants Of Tax Revenue In Latin America And The Caribbean, 1990-2009,” Comisión Económica para América Latina y el Caribe (CEPAL), Subregional Headquarters In Mexico. Copy available online at: http://www.eclac.cl/mexico/noticias/documentosdetrabajo/8/48538/2012-041_Structural-determinants_of_tax_revenue-L.1087.pdf. Cited: 31st March, 2013 GBI Research (2013), “Oil and Gas Storage Industry to 2015 - Cost Reduction Strategies in the Form of Storage Facility Sharing to Boost the Market”, Copy available online http://www.researchandmarkets.com/reports/2063647/oil_and_gas_storage_industry_to_2015_cost. Cited 31st March 2013 Ghana Statistical Service (2012), “Provisional Gross Domestic Product”, 2012 Provisional. Available at: http://www.statsghana.gov.gh/docfiles/GDP/provisional_gdp_2012.pdf. Cited: 31st March, 2013 Gupta, A. S. (2007), “Determinants Of Tax Revenue In Developing Countries”, IMF Working Paper (WP/07/184) International Energy Agency (2013), “Energy Consumption”. Available online at: http://data.worldbank.org/ - IEA Statistics, OECD/IEA, http://www.iea.org/stats/index.asp. Cited: 31st March, 2013

[Working Paper Series - GWP2013/01] GWP 2013/01

This research is a GoldEdge Working Paper Series, WP 2013/10 | © Bernard Tetteh Narkotey, April 2013 13

Kastning, T. (2011), “Basic Overview of Ghana’s Emerging Oil Industry”, Friedrich Ebert Stiftung. Copy available online at http://www.fesghana.org/uploads/PDF/BasicOverview_OilEconomy_Ghana_2011.pdf. Cited: 30th March 2013 Mahdavi, S. (2008), “The level and composition of tax revenue in developing countries: Evidence from unbalanced panel data”, International Review of Economics and Finance, Vol.17, pp. 607-617 Markets and Markets (2012), “Hydraulic Fracturing Market by Resource & Well Type - Global Trends & Forecasts up till 2017”, Pages: 195. Copy available online at: http://www.researchandmarkets.com/reports/2205061/hydraulic_fracturing_market_by_resource_and_well Ministry of Finance (2013), “The 2013 Budget Statement and Economic Policy”, Ministry of Finance Public Relations Office – (New Building, Ground Floor, Room 002 or 004) Available online: http://www.mofep.gov.gh/sites/default/files/budget/2013_Budget_Statement.pdf Mitchel, J. (2013), “What Next for the Oil and Gas Industry?” EC-JRC Workshop, cited 29th March 2013 copy available online athttp://ec.europa.eu/dgs/jrc/downloads/events/20130131_worksho/20130131_workshop34_michell.pdf Offshore-Technology.com (2011): Jubilee Field, Ghana. Available online at http://www.offshore technology.com/projects/jubilee-field/, cited 30th March 2013 Prempeh, K.H, and Kroon, C. (2012), “The Political Economy Analysis of the Oil & Gas Sector in Ghana: Summary of Issues for STAR-Ghana, Star Ghana. Available online at:http://www.starghana.org/assets/STAR%20Ghana%20Recommendations%20and%20Summary%20of%20Issues%20for%20Oil%20&%20Gas%20Call.pdf. Cited 31st March 2013 Profeta, P. and S. Scabrosetti (2010), “The Political Economy of Taxation: Lessons for Developing Countries”, Edward Elgar Publishing Limited Raddatz, C (2007), “External Shocks Responsible for the Instability of Output in Low-Income Countries?” Journal of Development Economics, Vol. 84pp155-187 Razavi, H. (1996), “Financing Oil and Gas Projects in Developing Countries”, Finance and Development, pp2-5, A publication of the World Bank’s Industry and Energy Department Tullow Oil (2010), “On Track Jubilee Special Feature”, Copy available online athttp://files.thegroup.net/library/tullow/annualreport2009/pdfs/tullowar09_jubilee.pdf, Tullow Oil (2010): On Track Jubilee Special Feature. Available online at http://files.the-group.net/library/tullow/annualreport2009/pdfs/tullowar09_jubilee.pdTullow Oil (2011), “Enyenra (Owo)/Tweneboa”, Available online at

http://www.tullowoil.com/index.asp?pageid=58

World Bank (2009), “Economy-Wide Impact of Oil Discovery in Ghana”, Report No. 47321-GH, PREM 4 Africa Region

Related Documents