OHIO MUNICIPAL LEAGUE INCOME TAX SEMINAR JULY 9, 2015 Did Someone Say the State Changed How Municipalities Audit, Assess, Refund & What’s the 30,000 Rule? Presented by: Amy L. Arrighi, Chief Legal Counsel Amber E. Greenleaf, Assistant Legal Counsel Regional Income Tax Agency

OHIO MUNICIPAL LEAGUE INCOME TAX SEMINAR JULY 9, 2015 Did Someone Say the State Changed How Municipalities Audit, Assess, Refund & What’s the 30,000 Rule?

Dec 29, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

OHIO MUNICIPAL LEAGUEINCOME TAX SEMINAR

JULY 9, 2015

Did Someone Say the State Changed How Municipalities Audit, Assess, Refund & What’s the 30,000 Rule?

Presented by:

Amy L. Arrighi, Chief Legal Counsel

Amber E. Greenleaf, Assistant Legal Counsel

Regional Income Tax Agency

AGENDA

Audits Assessments Refunds 30,000 Rule

AUDIT

718.01(UU) -- “Audit” defined:

The examination of a person or the inspection of the books, records, memoranda or accounts of a person for the purpose of determining municipal income tax liability.

AUDIT

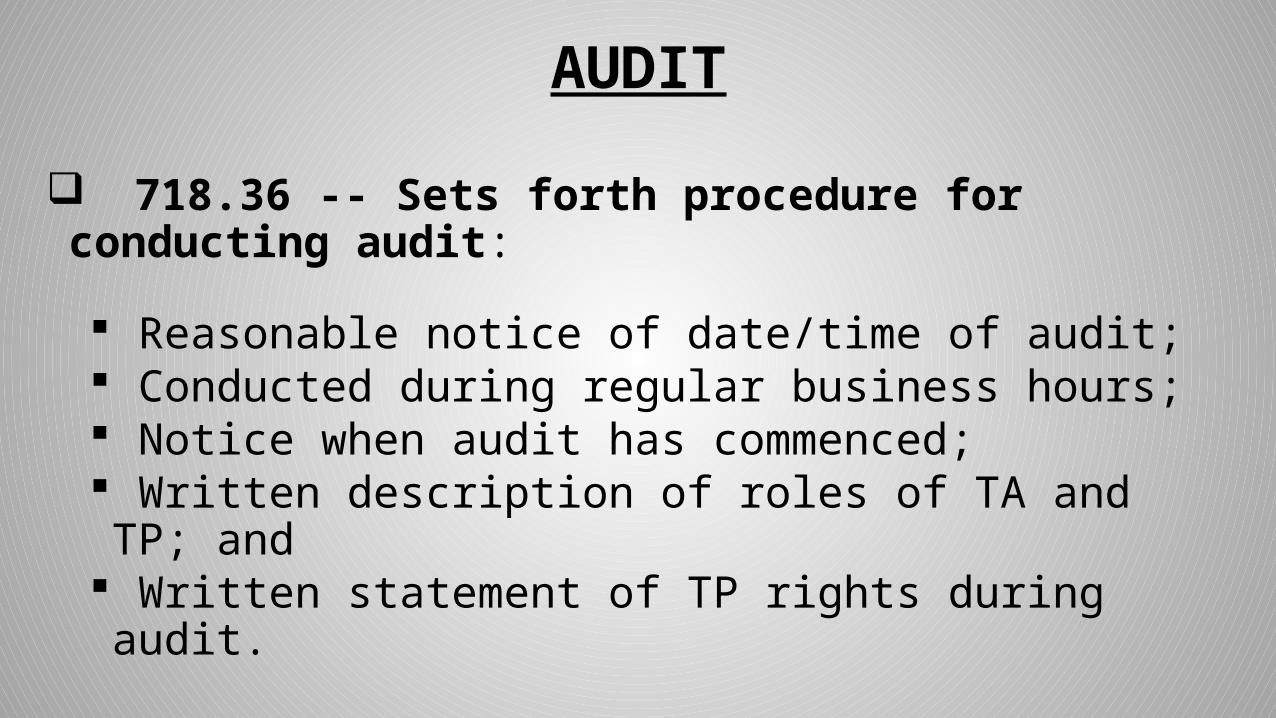

718.36 -- Sets forth procedure for conducting audit:

Reasonable notice of date/time of audit; Conducted during regular business hours; Notice when audit has commenced; Written description of roles of TA and TP; and

Written statement of TP rights during audit.

AUDIT 718.36 Continued -- Provides TP rights during audit:

Represented by attorney, accountant, bookkeeper, etc.;

Right to refuse to answer questions until TP speaks with attorney, accountant, etc.; and

Record the audit.

Failure of TA to comply – penalties.

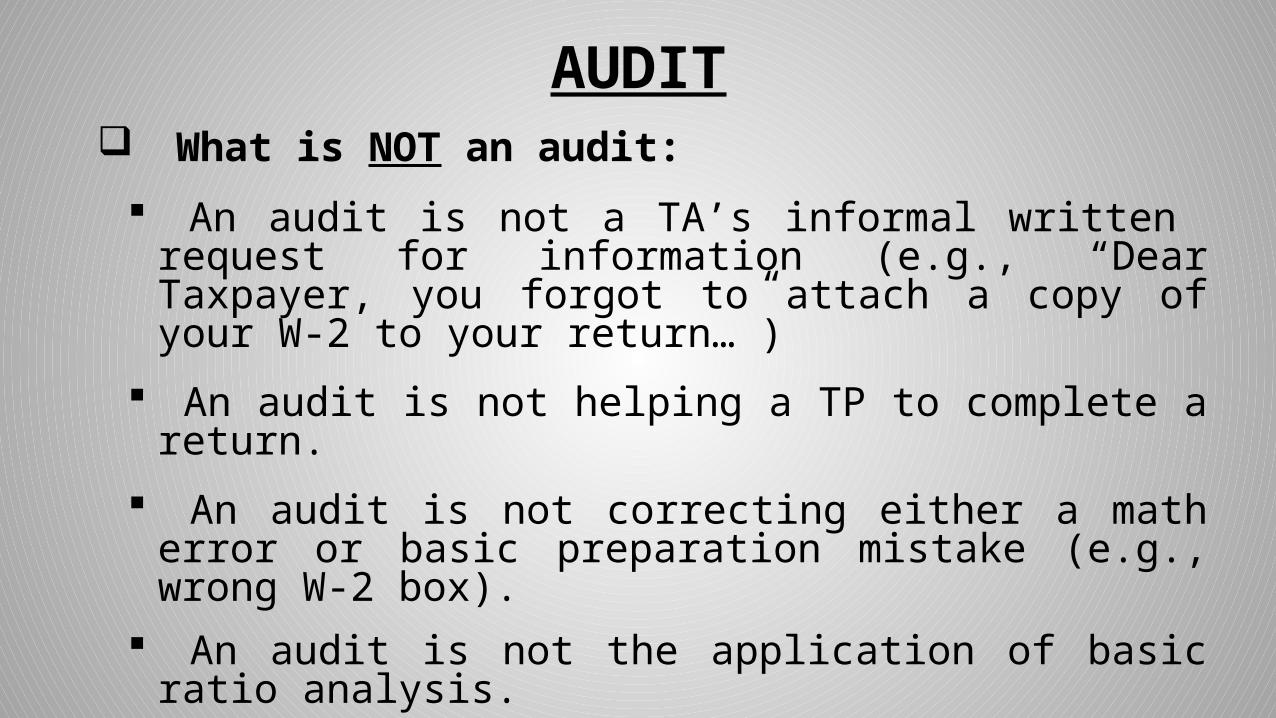

AUDIT What is NOT an audit:

An audit is not a TA’s informal written request for information (e.g., “Dear Taxpayer, you forgot to attach a copy of your W-2 to your return…”)

An audit is not helping a TP to complete a return.

An audit is not correcting either a math error or basic preparation mistake (e.g., wrong W-2 box).

An audit is not the application of basic ratio analysis.

AUDIT What IS an audit:

R.C. code language implies an audit is where the TP sits across the desk from the auditor and answers questions and shows documentation – face-to-face.

Example -- taxpayer assistance at a subpoena

program.

AUDIT How does audit language play with R.C. 718.23 -- Verification of Accuracy of Returns:

Despite “audit” language, TA still authorized to:

Review and examine books, papers, records, fed/state returns, etc.

Establish retention period for TP records

Compel TP to appear at a hearing, examine under oath and compel the production of books, papers, records etc.

TP may be represented at any such hearing

ASSESSMENTS 718.01(PP) -- “Assessment” defined:

A written finding by a municipal TA that commences a TP’s time to appeal to the local board of tax review.

AND – additional requirements:“ASSESSMENT” printed at the top in all capital letters;

Advises TP of appeal rights and how to appeal.

Examples of Assessments:

Full or partial denial of refund requests on amended returns.

Denial of TP request to use a method other than the statutorily prescribed method for allocating net profits to a municipality, or TA’s requirement.

Requiring net profit filers to make a consolidated filing.

ASSESSMENTS

Assessments are NOT:

Billing statements; Requests for additional information; Informal notices denying refund request on originally filed returns;

Notifications of math errors; or Other general correspondence.

ASSESSMENTS

ASSESSMENTS

718.11 Assessments Issued by TA -- How:

TA issuing an assessment to TP required to do the following:

Notify TP of the finding in writing; Inform TP of right to appeal assessment; How to appeal assessment; and Address to which appeal should be sent.

ASSESSMENTS

718.18 Service of Assessments:

Certified mail Unclaimed Undeliverable

Personal service Delivery service Electronic service if authorized by the TP

ASSESSMENTS

718.11 Assessments Appealed to Local Board of Review:

Local boards of review will be more active going forward, hearing appeals from assessments.

TP who wants to appeal assessment required to submit request to board of review -- request must: Be in writing; Include reason(s) why assessment is incorrect or unlawful; and

Be filed within 60 (new) days after TP receives assessment.

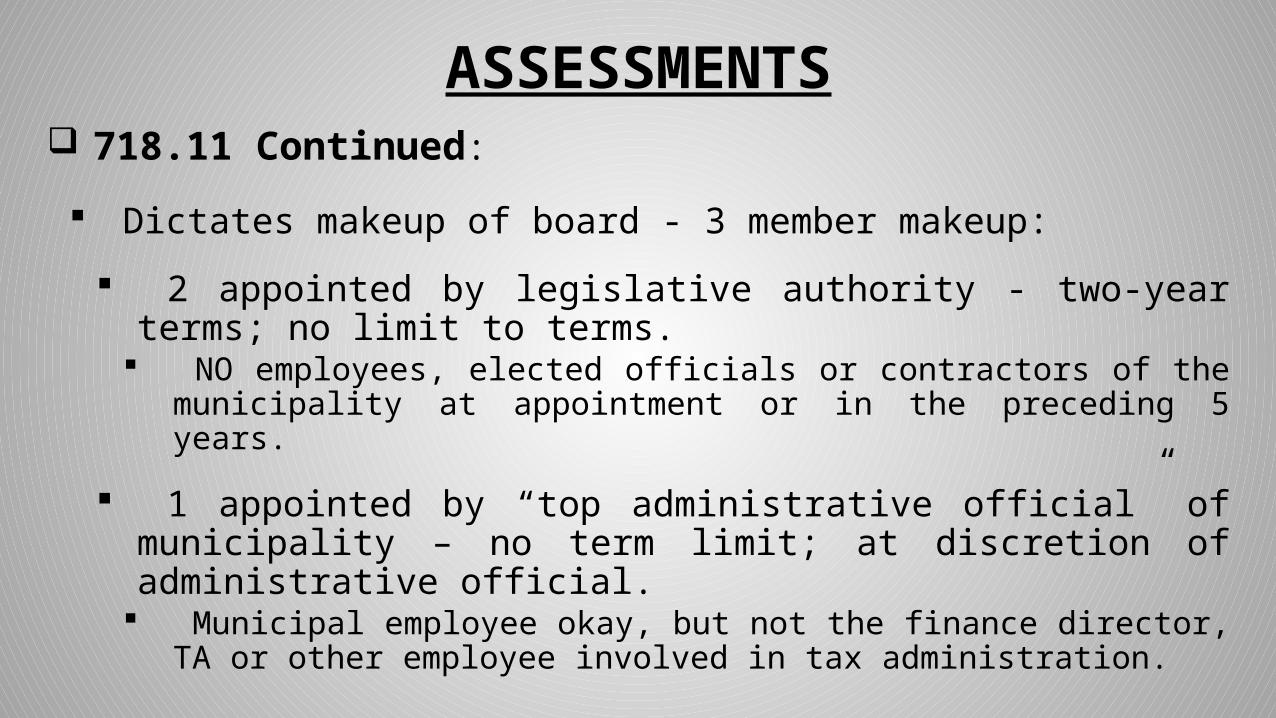

ASSESSMENTS 718.11 Continued:

Dictates makeup of board - 3 member makeup:

2 appointed by legislative authority - two-year terms; no limit to terms. NO employees, elected officials or contractors of the

municipality at appointment or in the preceding 5 years.

1 appointed by “top administrative official” of municipality – no term limit; at discretion of administrative official. Municipal employee okay, but not the finance director,

TA or other employee involved in tax administration.

ASSESSMENTS 718.11 Continued:

Board of review required to schedule hearing within 60 days (new) after receiving request. TP may waive hearing. Parties may agree to continue hearing.

TP permitted to be represented by attorney, CPA or other representative.

ASSESSMENTS 718.11 Continued:

Final determination required to be issued by Board within 90 days after hearing. Copy of determination must be sent by Board via ordinary mail within 15 days of issuing.

The statute of limitations for collections is tolled while appeals are pending before local boards of review, or higher reviewing authority.

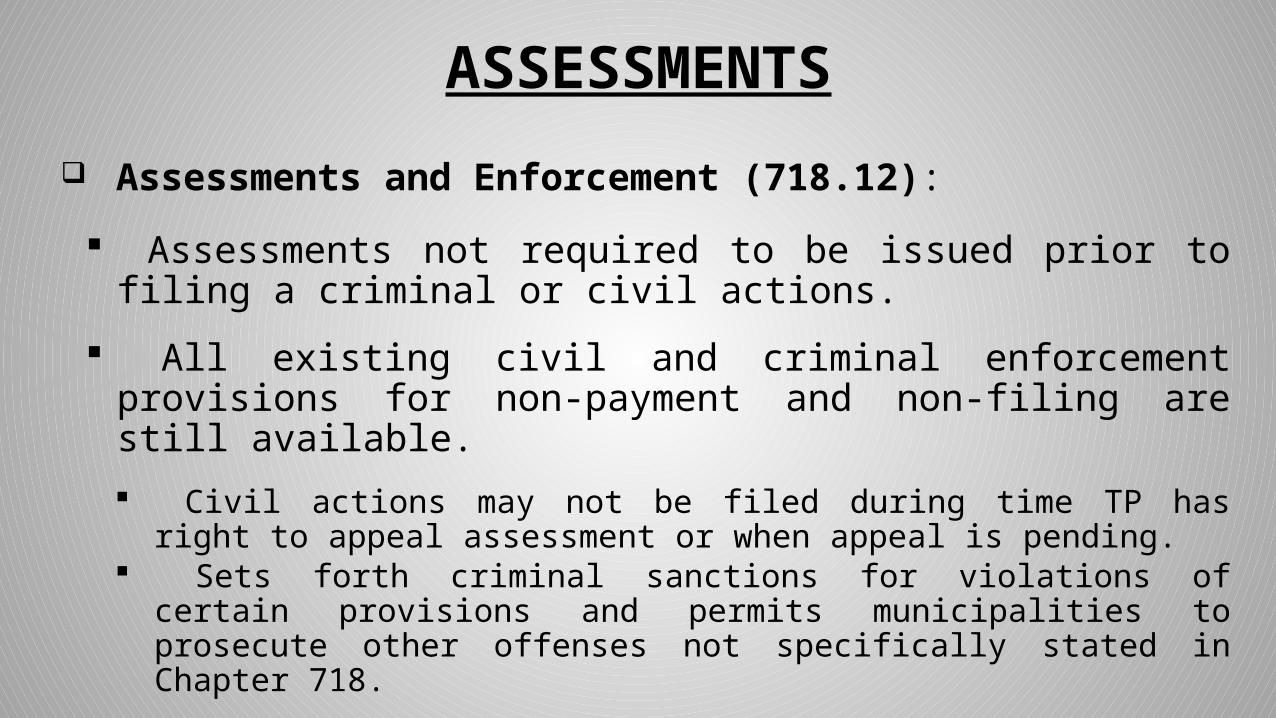

Assessments and Enforcement (718.12):

Assessments not required to be issued prior to filing a criminal or civil actions.

All existing civil and criminal enforcement provisions for non-payment and non-filing are still available.

Civil actions may not be filed during time TP has right to appeal assessment or when appeal is pending.

Sets forth criminal sanctions for violations of certain provisions and permits municipalities to prosecute other offenses not specifically stated in Chapter 718.

ASSESSMENTS

ASSESSMENTS Assessments and Enforcement Continued:

Retains existing statute of limitations: Three years after tax due or return filed, whichever is

later. Six years for cases of fraud, failure to file or omission of

25% or more of income.

Provides for tolling of statute of limitations – NEW.

Municipalities may recover post-judgment costs and fees, including attorneys’ fees, from taxpayers. (May change municipalities’ processes for referring matters to outside collection firms, or for moving unpaid balances to litigation.)

Refunds Minimum, SOL and Assessment:

718.19(A) -- Minimum refunds are $10.01

718.19(B)(1) -- statute of limitations – three years.

718.01(PP) Def. of Assessment: Full or partial denial of refund request on amended return =

assessment. 718.19(B)(2) TA must issue an appealable assessment when a refund is

wholly or partially denied on an amended return.

Informal notices denying refund request on originally filed returns; 718.19(B)(3) TA must notify a TP, in writing, how to request an

appealable assessment when a refund is wholly or partially denied on an original return.

30,000 RULE 718.39 Large Population Municipalities:

All written correspondence from municipality with a population > 30,000, as well as RITA/CCA, must contain the name and contact information of person who can receive inquiries about the correspondence.

RITA’s review of correspondence - examples: Billing statements / notification postcards Forms – WH Letter re: change of password for website Letter re: payment plan Letter re: change in liability

*No penalty for failure to comply.*

Thank you!

Related Documents