Offshore Wind in Europe Key trends and statistics 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Subtittle if needed. If not MONTH 2018Published in Month 2018

Offshore Wind in Europe

Key trends and statistics 2018

Offshore Windin Europe

windeurope.org

Key trends and statistics 2018Published in February 2019

TEXT AND ANALYSIS: WindEurope Business IntelligenceFlorian SelotDaniel FraileGuy Brindley

EDITORS:

Colin Walsh, WindEurope

DESIGN:

Laia Miró, WindEurope

FINANCE DATA:

Clean Energy Pipeline.All currency conversions made at EUR/ GBP 0.8774 and EUR/USD 1.1330Figures include estimates for undisclosed values

PHOTO COVER:

Courtesy of MHI Vestas Offshore Wind

MORE INFORMATION:

[email protected]+32 2 213 18 68

This report summarises construction and financing activity in European offshore wind farms from 1 January to 31 December 2018.

WindEurope regularly surveys the industry to determine the level of installations of foundations and turbines, and the subsequent dispatch of first power to the grid. The data includes demonstration sites and factors in decommissioning where it has occurred. Annual installations are expressed in gross figures while cumulative capacity represents net installations per site and country. Rounding of figures is at the discretion of the author.

DISCLAIMER

This publication contains information collected on a regular basis throughout the year and then verified with relevant members of the industry ahead of publication. Neither WindEurope, nor its members, nor their related entities are, by means of this publication, rendering professional advice or services. Neither WindEurope nor its members shall be responsible for any loss whatsoever sustained by any person who relies on this publication.

CO

NTE

NTS

EXECUTIVE SUMMARY ..................................................................................................... 7

1. OFFSHORE WIND INSTALLATIONS ........................................................................... 11

1.1 Overview ......................................................................................................................... 11

1.2 National breakdown of 2018 installations ....................................................... 14

1.3 Cumulative installations ........................................................................................... 18

2. TRENDS: TURBINE SIZE, WIND FARM LOCATION ............................................. 20

2.1 Wind turbine rated capacity ................................................................................... 20

2.2 Wind farm size .............................................................................................................. 21

2.3 Water depth and distance to shore .................................................................... 22

3. INDUSTRY ACTIVITY AND SUPPLY CHAIN ............................................................ 25

3.1 Wind turbine manufacturers ................................................................................. 25

3.2 Wind farm owners ...................................................................................................... 27

3.3 Substructures and foundations ............................................................................ 29

3.4 Cables .............................................................................................................................. 31

4. INVESTMENTS ...................................................................................................................... 33

4.1 Financing activity in 2018 ........................................................................................ 33

4.2 Offshore wind debt finance .................................................................................... 36

4.3 Acquisition activity ...................................................................................................... 37

7Offshore Wind in Europe - Key trends and statistics 2018WindEurope

EXECUTIVE SUMMARY

FIGURE A Annual offshore wind installations by country and cumulative capacity (MW)

Source: WindEurope

In 2018 Europe connected 409 new offshore wind tur-bines to the grid across 18 projects. This brought 2,649 MW of net additional capacity.

Europe now has a total installed offshore wind capacity of 18,499 MW. This corresponds to 4,543 grid-connected wind turbines across 11 countries.

UK Germany Belgium Denmark Spain Sweden

Netherlands France Finland Norway Portugal

0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Cum

ula

tive

Inst

alle

d C

ap

aci

ty (M

W)

Ann

ual I

nsta

lled

Ca

pa

city

(MW

)

20082009

20102011

20122013

20142015

20162017

2018

Cumulative Installed Capacity (MW)

8 Offshore Wind in Europe - Key trends and statistics 2018WindEurope

Executive summary

Separately, twelve new offshore wind projects reached Final Decision Investment (FID) in 2018. Investments in new assets amounted to €10.3bn. This financed 4.2 GW

of additional capacity, which will come on line in the next couple of years.

FIGURE B New offshore wind investments and capacity financed: 2010-2018 (€bn)

Source: WindEurope

Installations in 2018

• Europe added 2,649 MW of net offshore capacity. This is 15.8% lower than in 2017, which was a record year.

• The 2,649 GW represent 409 grid-connected offshore wind turbines across 18 wind farms.

• 15 wind farms were completed (fully grid-connected). Another 3 got partial grid connection and will continue to connect turbines in 2019. Construction work started on other 6 wind farms where no turbines have yet been grid-connected.

• Installations in the UK and Germany accounted for 85% of all new additions.

• Siemens Gamesa Renewable Energy and MHI Vestas Offshore Wind accounted for 95% of all the connected turbines in 2018 (62% and 33% respectively).

• For the first time in Europe, GE Renewable Energy connected their latest turbine: the Haliade 150-6 MW. 20 of these turbines were grid-connected at the Merkur wind farm, Germany.

Cumulative installations

• 4,543 offshore turbines are now installed and grid-connected, making a cumulative total of 18,499 MW.

• Including sites with partial grid-connected turbines, there are now 105 offshore wind farms in 11 European countries.

• The UK has the largest amount of offshore wind capacity in Europe with 44% of all installations in MW. Second is Germany with 34%, followed by Denmark (7%), Belgium (6.4%) and the Netherlands (6%).

8.4

6.15.0

7.28.8

13.1

18.2

7.5

10.3

0

2

4

6

8

10

12

14

16

18

20

0

2

4

6

8

10

12

14

16

18

20

2010 2011 2012 2013 2014 2015 2016 2017 2018

GW€b

n

Total investments (€bn) New capacity financed (GW)

9Offshore Wind in Europe - Key trends and statistics 2018WindEurope

Executive summary

Trends: turbine and wind farm size, depth, distance from shore

• The average size of newly-installed offshore wind turbines in 2018 was 6.8 MW, a 15% increase on 2017. The UK connected the largest turbine in the world (the V164-8.8 MW from MHI Vestas Offshore Wind).

• The average size of wind farms in construction in 2018 was 561 MW. In the UK, construction work started on the largest wind farm in the world: the 1,200 MW Hornsea One project.

• The world’s current largest operational wind farm – Walney 3 extension (657 MW) – was fully connected in the UK.

• The largest wind farm in Germany – Borkum Riffgrund II (465 MW) – was fully commissioned.

• The largest wind farm in Belgium – Rentel 309 MW – was fully connected.

Financing highlights

• Investments in new offshore wind amounted to €10.3bn, a 37% increase from 2017.

• Twelve projects reached FID, totalling 4.2 GW of additional capacity.

• The 37% increase in investments generated an 86% increase in capacity financed.

• Refinancing of offshore wind farms hit a record level of €8.5bn, bringing total investments including transmission lines (€0.7bn) to €19.6bn.

• Non-recourse debt for new and operational wind farms raised €16.5bn.

• There were 3.8 GW of project acquisition activity and 2.3 GW of potential projects acquired at the pre-development stage.

Photo: Ørsted

11Offshore Wind in Europe - Key trends and statistics 2018WindEurope

1. Separately, 2.75 MW were boosted into 3.3 MW due to rotor and blade upgrades in 5 turbines. See page 14 for more info.2. WindEurope Market Outlook, September 2017.3. WindEurope Market Outlook, September 2017.

1.1 OVERVIEW

Europe connected 2,649 MW of net offshore wind power capacity in 2018. This is 15.8 % lower than in 2017, which was a record year. It added 2,660 MW of new (gross) ca-pacity. 7 turbines were fully decommissioned at the Ut-grunden I wind farm in Sweden, which was commissioned back in 2000. This accounts for the decommission of 10.5 MW in 20181. Installations were in line with previously forecasted scenarios2.

The UK and Germany connected slightly less capacity than in 2017, with 1,312 MW and 969 MW respectively. Den-mark had new connections for the first time since 2013

(61 MW), and Belgium doubled its annual installations in comparison to 2017 (309 MW). The Netherlands did not grid-connect any offshore wind, but is set to have a record year in 2019 with about 1 GW of new offshore installations3.

Europe’s cumulative offshore wind capacity reached 18,499 MW at the end of 2018. Including sites with partial grid connection, there are now 105 offshore wind farms in 11 European countries and 4,543 grid-connected wind turbines.

OFFSHORE WIND INSTALLATIONS

1.

12 Offshore Wind in Europe - Key trends and statistics 2018WindEurope

Offshore wind installations

FIGURE 1 Annual offshore wind installations by country and cumulative capacity (MW)

Source: WindEurope

UK Germany Belgium Denmark Spain Sweden

Netherlands France Finland Norway Portugal

0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Cum

ula

tive

Inst

alle

d C

ap

aci

ty (M

W)

Ann

ual I

nsta

lled

Ca

pa

city

(MW

)

20082009

20102011

20122013

20142015

20162017

2018

Cumulative Installed Capacity (MW)

TABLE 1 Overview of grid-connected offshore wind power projects at the end of 2018

COUNTRYNO. OF WIND

FARMS CONNECTED

CUMULATIVE CAPACITY

(MW)

NO. OF TURBINES

CONNECTED

NET CAPACITY CONNECTED

IN 2018

NO. OF TURBINES

CONNECTED IN 2018

TOTAL 105 18,499 4,543 2,649 409

United Kingdom 39 8,183 1,975 1,312 222

Germany 25 6,380 1,305 969 136

Denmark 14 1,329 514 61 42

Belgium 7 1,186 274 309 8

Netherlands 6 1,118 365 0 1

Sweden 4 192 79 -10 -7

Finland 3 71 19 0 0

Ireland 1 25 7 0 0

Spain 2 10 2 5 1

France 2 2 2 2 2

Norway 1 2 1 0 0

-

3

GW

GWGross installations in 2017

Cumulativeinstalled capacity

at the end of 2018

8.2

1.3

6.4

1

1.3

0.06

1.20.3

1.1

0.2

0.003

0.01

0.005

0.002

0.002

0.05

0.07

0.002

18.5 GWTOTAL EUROPE

OF NEW OFFSHOREWIND POWER IN EUROPE

2.6 GW

13Offshore Wind in Europe - Key trends and statistics 2018WindEurope

Source: WindEurope

14 Offshore Wind in Europe - Key trends and statistics 2018WindEurope

Offshore wind installations

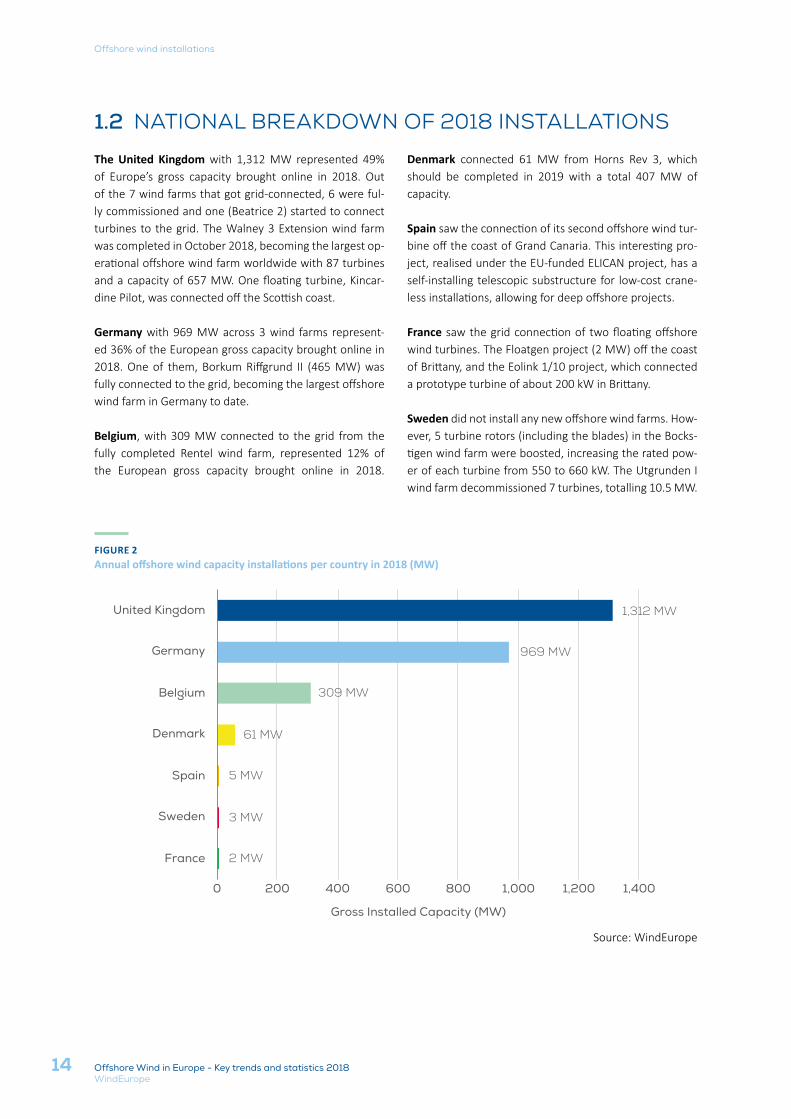

1.2 NATIONAL BREAKDOWN OF 2018 INSTALLATIONS

The United Kingdom with 1,312 MW represented 49% of Europe’s gross capacity brought online in 2018. Out of the 7 wind farms that got grid-connected, 6 were ful-ly commissioned and one (Beatrice 2) started to connect turbines to the grid. The Walney 3 Extension wind farm was completed in October 2018, becoming the largest op-erational offshore wind farm worldwide with 87 turbines and a capacity of 657 MW. One floating turbine, Kincar-dine Pilot, was connected off the Scottish coast.

Germany with 969 MW across 3 wind farms represent-ed 36% of the European gross capacity brought online in 2018. One of them, Borkum Riffgrund II (465 MW) was fully connected to the grid, becoming the largest offshore wind farm in Germany to date.

Belgium, with 309 MW connected to the grid from the fully completed Rentel wind farm, represented 12% of the European gross capacity brought online in 2018.

Denmark connected 61 MW from Horns Rev 3, which should be completed in 2019 with a total 407 MW of capacity.

Spain saw the connection of its second offshore wind tur-bine off the coast of Grand Canaria. This interesting pro-ject, realised under the EU-funded ELICAN project, has a self-installing telescopic substructure for low-cost crane-less installations, allowing for deep offshore projects.

France saw the grid connection of two floating offshore wind turbines. The Floatgen project (2 MW) off the coast of Brittany, and the Eolink 1/10 project, which connected a prototype turbine of about 200 kW in Brittany.

Sweden did not install any new offshore wind farms. How-ever, 5 turbine rotors (including the blades) in the Bocks-tigen wind farm were boosted, increasing the rated pow-er of each turbine from 550 to 660 kW. The Utgrunden I wind farm decommissioned 7 turbines, totalling 10.5 MW.

FIGURE 2 Annual offshore wind capacity installations per country in 2018 (MW)

Source: WindEurope

2 MW

3 MW

5 MW

61 MW

309 MW

969 MW

1,312 MW

0 200 400 600 800 1,000 1,200 1,400

France

Sweden

Spain

Denmark

Belgium

Germany

United Kingdom

Gross Installed Capacity (MW)

15Offshore Wind in Europe - Key trends and statistics 2018WindEurope

Offshore wind installations

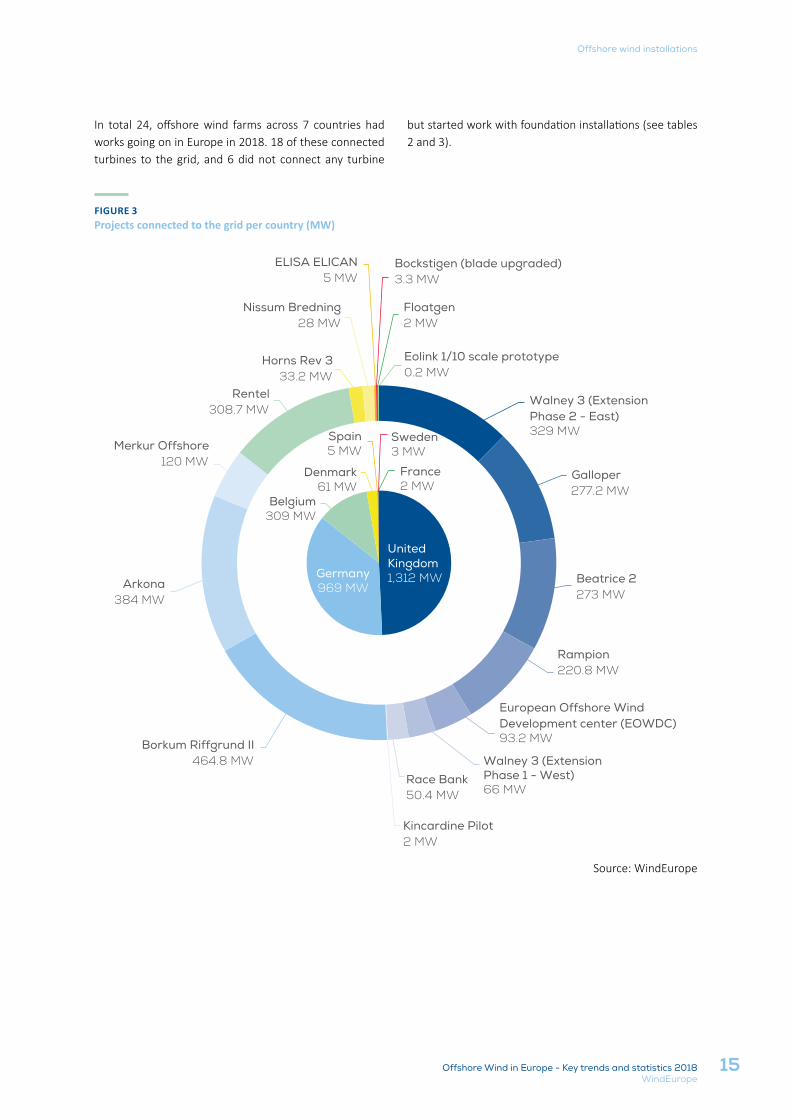

FIGURE 3 Projects connected to the grid per country (MW)

Source: WindEurope

In total 24, offshore wind farms across 7 countries had works going on in Europe in 2018. 18 of these connected turbines to the grid, and 6 did not connect any turbine

but started work with foundation installations (see tables 2 and 3).

Walney 3 (Extension Phase 2 - East) 329 MW

Galloper277.2 MW

Beatrice 2273 MW

Rampion220.8 MW

European Offshore Wind Development center (EOWDC)93.2 MW

Walney 3 (ExtensionPhase 1 - West)66 MW

Race Bank50.4 MW

Kincardine Pilot2 MW

Borkum Riffgrund II464.8 MW

Arkona384 MW

Merkur Offshore120 MW

Rentel308.7 MW

Horns Rev 333.2 MW

Nissum Bredning28 MW

ELISA ELICAN5 MW

Bockstigen (blade upgraded) 3.3 MW

Floatgen2 MW

Eolink 1/10 scale prototype 0.2 MW

Belgium309 MW

Denmark61 MW

Spain5 MW

Sweden3 MW

France2 MW

United Kingdom1,312 MWGermany

969 MW

16 Offshore Wind in Europe - Key trends and statistics 2018WindEurope

4. One bar <25% grid connected. 2 bars <50% grid connected. 3 bars <75% grid connected. 4 bars <100% grid connected. 5 bars: fully grid connected

TABLE 2Summary of work carried out at European offshore wind farms with grid connection during 2018

COUNTRY WIND FARMCAPACITY

CONNECTED IN 2018 (MW)

NUMBER OF TURBINES

CONNECTED IN 2018TYPE STATUS4

United kingdom

Walney Extension Phase East 329 47 Bottom-fixed

Galloper 277.2 44 Bottom-fixed

Beatrice 2 273 39 Bottom-fixed

Rampion 220.8 64 Bottom-fixed

EOWDC 93.2 11 Bottom-fixed

Walney Extension Phase West 66 8 Bottom-fixed

Race Bank 50.4 8 Bottom-fixed

Kincardine Pilot 2 1 Floating

Germany

Borkum Riffgrund II 464.8 56 Bottom-fixed

Arkona 384 60 Bottom-fixed

Merkur Offshore 120 20 Bottom-fixed

Belgium Rentel 308.7 42 Bottom-fixed

DenmarkHorns Rev 3 33.2 4 Bottom-fixed

Nissum Bredning 28 4 Bottom-fixed

Spain ELISA ELICAN 5 1 Bottom-fixed

Sweden Bockstigen (boosted) 3.3 5 Bottom-fixed

FranceFloatgen 2 1 Floating

Eolink Prototype 0.2 1 Floating

Offshore wind installations

17Offshore Wind in Europe - Key trends and statistics 2018WindEurope

TABLE 3Summary of work carried out at European offshore wind farms without grid connection during 2018

COUNTRY WIND FARMFOUNDATIONS

INSTALLED IN 2018

TOTAL NUMBER OF

FOUNDATIONS

TYPE OF FOUNDATIONS

United KingdomEast Anglia 1 37 102 Jacket

Hornsea One 156 174 Monopile

Germany

Deutsche Bucht 29 31 Monopile

Hohe See 63 71 Monopile

Trianel Windpark Borkum 2 32 32 Monopile

Belgium Norther 44 44 Monopile

The North Sea registered the largest amount of grid con-nections (1,651 MW), representing 62% of the installa-tions. This was followed by the Irish Sea (15%), with the Walney 3 extension Phase 2 - East and Walney 3 exten-sion Phase 1 - West. The Baltic Sea saw 14% of the instal-

lations, driven by connections in the Arkona wind farm. The Atlantic Ocean registered 9% of the new installations, driven by the work in Rampion wind farm.

FIGURE 4 Gross annual installations by sea basin in 2018 (MW)

Source: WindEurope

229 MW

387 MW

395 MW

1,651 MW

0 500 1,000 1,500 2,000

Atlantic Ocean

Baltic Sea

Irish Sea

North Sea

Net Installed Capacity in 2018 (MW)

Offshore wind installations

18 Offshore Wind in Europe - Key trends and statistics 2018WindEurope

FIGURE 5Cumulative Installed capacity (MW) and number of turbines by country

Source: WindEurope

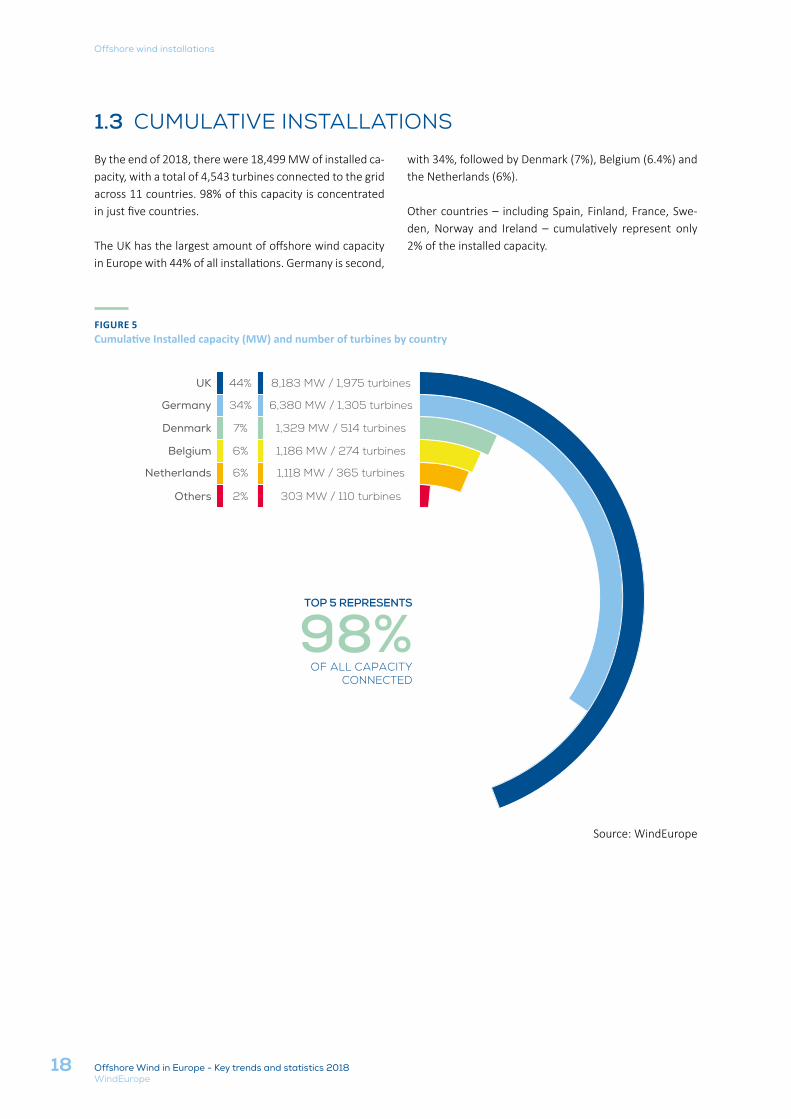

1.3 CUMULATIVE INSTALLATIONS

By the end of 2018, there were 18,499 MW of installed ca-pacity, with a total of 4,543 turbines connected to the grid across 11 countries. 98% of this capacity is concentrated in just five countries.

The UK has the largest amount of offshore wind capacity in Europe with 44% of all installations. Germany is second,

with 34%, followed by Denmark (7%), Belgium (6.4%) and the Netherlands (6%).

Other countries – including Spain, Finland, France, Swe-den, Norway and Ireland – cumulatively represent only 2% of the installed capacity.

TOP 5 REPRESENTS

98%OF ALL CAPACITY

CONNECTED

6,380 MW / 1,305 turbines

1,186 MW / 274 turbines

1,329 MW / 514 turbines

1,118 MW / 365 turbines

UK

Germany

Denmark

Belgium

Netherlands

Others 303 MW / 110 turbines

8,183 MW / 1,975 turbines44%

34%

7%

6%

6%

2%

Offshore wind installations

19Offshore Wind in Europe - Key trends and statistics 2018WindEurope

The North Sea accounts for 70% of all offshore wind capacity in Europe, followed by the Irish Sea with 16%, the Baltic Sea with 12%, and the Atlantic Ocean with 2%.

FIGURE 6Cumulative Installed capacity by sea basin (MW)

Source: WindEurope

413 MW

2,218 MW

2,928 MW

12,938 MW

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000

Atlantic Ocean

Baltic Sea

Irish Sea

North Sea

Net Installed Capacity (MW)

Offshore wind installations

20 Offshore Wind in Europe - Key trends and statistics 2018WindEurope

FIGURE 7Yearly average of newly installed offshore wind turbine rated capacity (MW)

Source: WindEurope

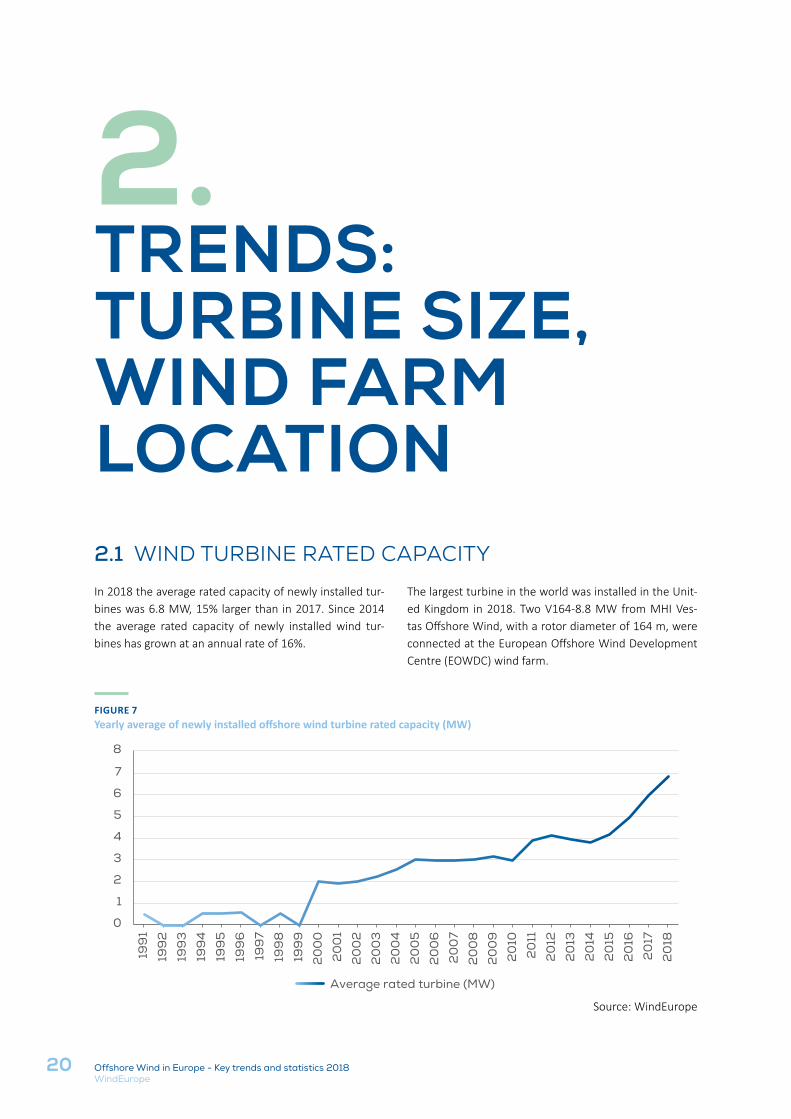

2.1 WIND TURBINE RATED CAPACITY

In 2018 the average rated capacity of newly installed tur-bines was 6.8 MW, 15% larger than in 2017. Since 2014 the average rated capacity of newly installed wind tur-bines has grown at an annual rate of 16%.

The largest turbine in the world was installed in the Unit-ed Kingdom in 2018. Two V164-8.8 MW from MHI Ves-tas Offshore Wind, with a rotor diameter of 164 m, were connected at the European Offshore Wind Development Centre (EOWDC) wind farm.

TRENDS: TURBINE SIZE, WIND FARM LOCATION

2.

0

1

2

3

4

5

6

7

8

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Average rated turbine (MW)

21Offshore Wind in Europe - Key trends and statistics 2018WindEurope

Trends: turbine size, wind farm location

FIGURE 8Average size of commercial offshore wind farms in construction and grid-connected in the given year

Source: WindEurope

2.2 WIND FARM SIZE

In the last ten years, the average offshore wind farm has increased in size from 79.6 MW in 2007 to 561 MW in 2018. The 1,200 MW Hornsea One project (174 turbines) is the largest offshore wind farm to reach Final Investment

Decision (FID) to date. Its construction started in 2018, with 156 foundations already installed by the end of the year. So far, no turbines have been installed.

Average wind farm size (MW)

0

100

200

300

400

500

600

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Most of the wind farms in construction are using turbines above 6 MW (the average rated power for the turbines is 6.8 MW, indicated by the red line in figure 9). The only

wind farms using turbines below 6 MW are Rampion in the United Kingdom and a few demonstration projects (mostly floating).

FIGURE 9Average turbine rated capacity and number of turbines of wind farms under construction in 2018

Source: WindEurope

Num

ber

of

turb

ines

per

win

d f

arm

Turbine Rated Capacity (MW)

United Kingdom Germany Belgium Denmark France Spain Sweden

0

100

200

0 1 2 3 4 5 6 7 8 9

Turbine average rated power in 2018

22 Offshore Wind in Europe - Key trends and statistics 2018WindEurope

Trends: turbine size, wind farm location

FIGURE 10Average water depth and distance to shore of offshore wind farms under construction in 2018. The size of the bubble indicates the overall capacity of the site

Source: WindEurope

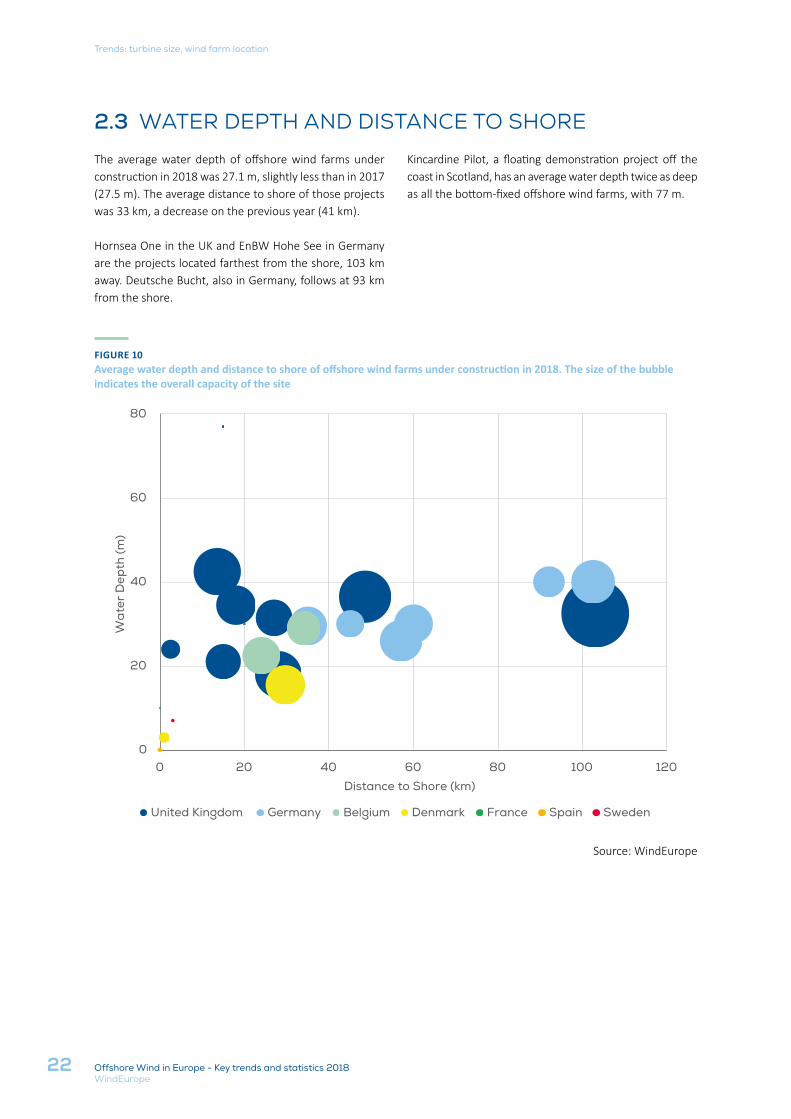

2.3 WATER DEPTH AND DISTANCE TO SHORE

The average water depth of offshore wind farms under construction in 2018 was 27.1 m, slightly less than in 2017 (27.5 m). The average distance to shore of those projects was 33 km, a decrease on the previous year (41 km).

Hornsea One in the UK and EnBW Hohe See in Germany are the projects located farthest from the shore, 103 km away. Deutsche Bucht, also in Germany, follows at 93 km from the shore.

Kincardine Pilot, a floating demonstration project off the coast in Scotland, has an average water depth twice as deep as all the bottom-fixed offshore wind farms, with 77 m.

0

20

40

60

80

0 20 40 60 80 100 120

Wa

ter

Dep

th (m

)

Distance to Shore (km)

United Kingdom Germany Belgium Denmark France Spain Sweden

23Offshore Wind in Europe - Key trends and statistics 2018WindEurope

Trends: turbine size, wind farm location

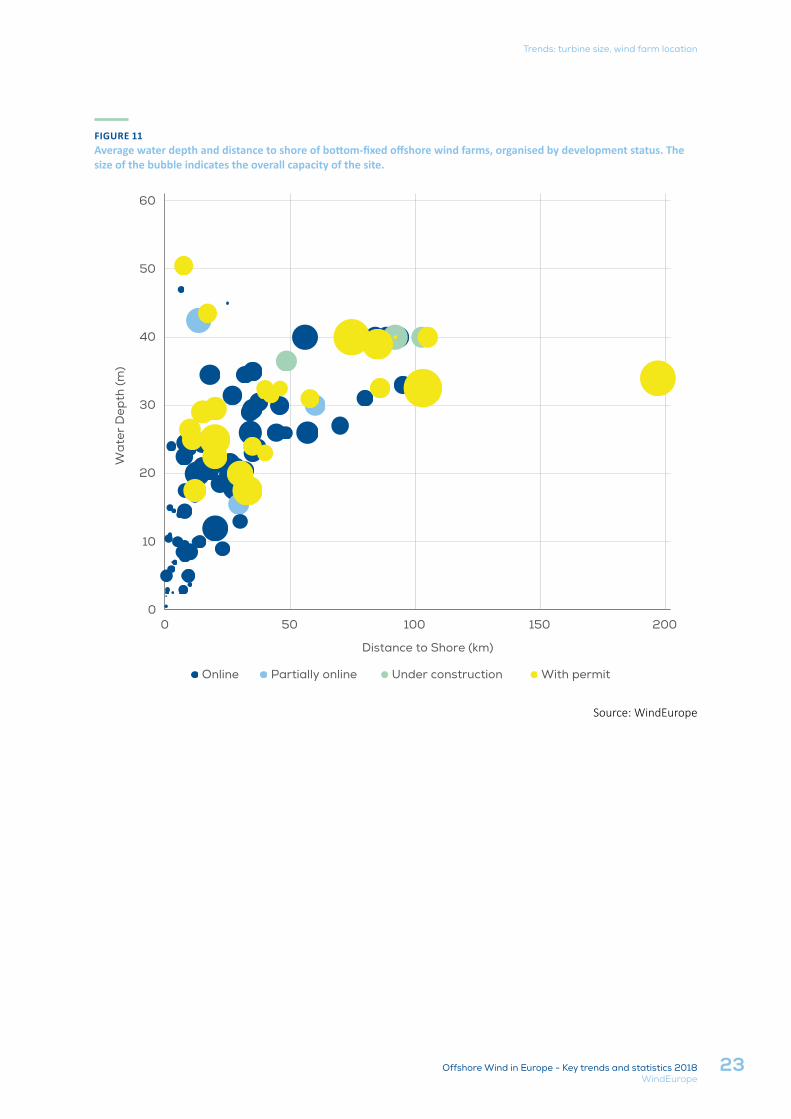

FIGURE 11Average water depth and distance to shore of bottom-fixed offshore wind farms, organised by development status. The size of the bubble indicates the overall capacity of the site.

Source: WindEurope

0

10

20

30

40

50

60

0 50 100 150 200

Wa

ter

Dep

th (m

)

Distance to Shore (km)

Online Partially online Under construction With permit

Photo: GE Renewable Energy

25Offshore Wind in Europe - Key trends and statistics 2018WindEurope

5. Adwen offshore company has been merged with Siemens Gamesa.

3.1 WIND TURBINE MANUFACTURERS

Siemens Gamesa Renewable Energy5 supplied 62.2% of all the new capacity in 2018. MHI Vestas Offshore Wind followed with 33.3%. Other turbine suppliers include GE renewable Energy and Eolink (prototype).

GE Renewable Energy connected its Haliade 150-6 MW turbine for the first time in Europe. In 2018, 20 of these turbines were connected at the Merkur offshore wind farm in Germany (another 44 will be connected in 2019).

INDUSTRY ACTIVITY AND SUPPLY CHAIN

3.

FIGURE 12

Wind turbine manufacturers’ share of the 2018 annual capacity (MW) and number of turbines connected to the grid

Source: WindEurope

Siemens Gamesa62%245 Turbines1,655 MW Connected

MHI Vestas Offshore Wind33%150 Turbines885 MW Connected

GE Renewable Energy5%20 Turbines120 MW Connected

Eolink1 Turbine<1 MW Connected

26 Offshore Wind in Europe - Key trends and statistics 2018WindEurope

Industry activity and supply chain

Siemens Gamesa Renewable Energy has the most off-shore wind turbines in Europe with 69% of the total in-stalled capacity (see figure 13). MHI Vestas Offshore Wind is the second largest turbine supplier with 24%, followed

by Senvion (5%). These 3 manufacturers represent 98% of the total number of turbines connected in Europe at the end of 2018.

FIGURE 13

Wind turbine manufacturers’ share at the end of 2018

Source: WindEurope

TOP 3 REPRESENT

98%OF ALL TURBINES

CONNECTED

Siemes Gamesa

MHI Vestas

Senvion

Bard Engineering

Others

GE Renewable Energy

69%

24%

5%

2%

1%

1%

12.8 GW / 3,115 turbines

3.8 GW / 1,068 turbines

1.2 GW / 206 turbines

0.4 GW / 80 turbines

0.07 GW / 46 turbines

0.15 GW / 28 turbines

27Offshore Wind in Europe - Key trends and statistics 2018WindEurope

Industry activity and supply chain

6. Grid-connected market shares are indicative only. Projects owned or developed by several companies have been split according to their respective shares. Where the shares are not known, they have been split in equal parts between the partners.

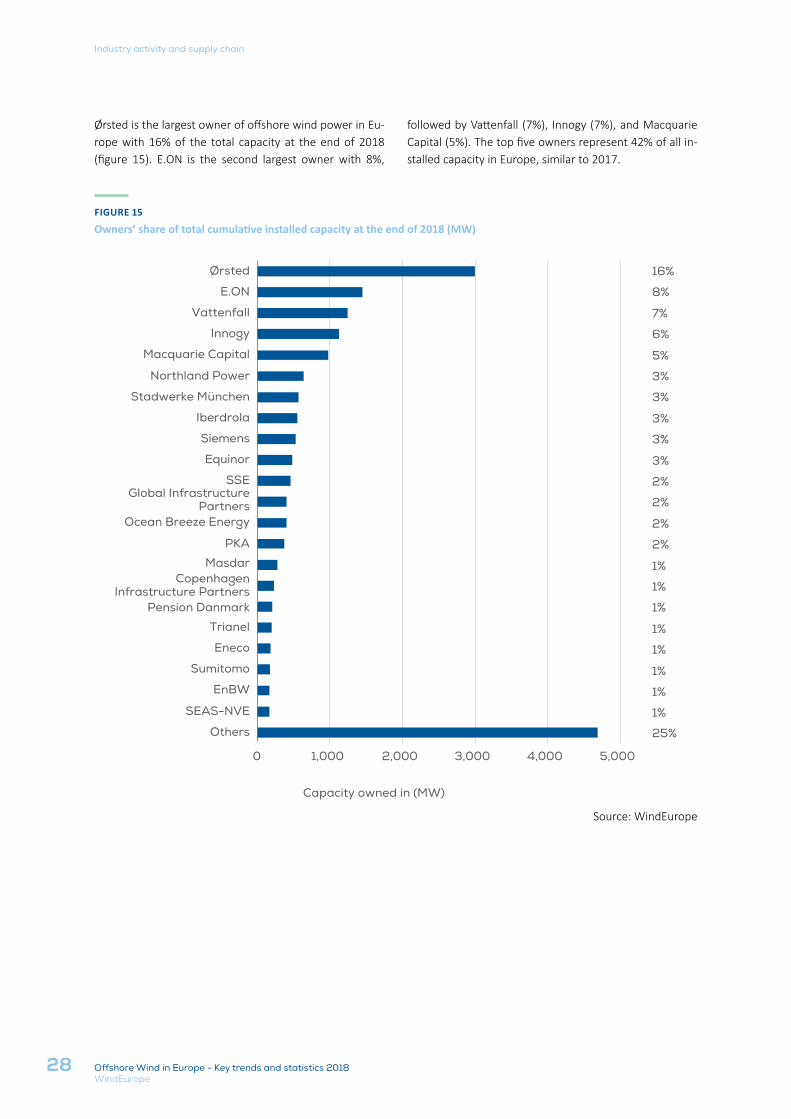

3.2 WIND FARM OWNERS

Ørsted connected the largest amount of wind capacity in 2018, representing 17%6, followed by E.ON with 11%. Global Infrastructure Partners with 9%, Equinor with 7%,

and Macquarie Capital with 6% complete the top five owners with new capacity last year. Together they account for 51% of all new capacity in 2018.

FIGURE 14

Owners’ share of 2018 annual installations (MW)

Source: WindEurope

0 50 100 150 200 250 300 350 400 450 500

Others (below 50 MW)

Enbridge

DEME NV

Partners Group

SDIC Power

Siemens

Innogy

CopenhagenInfrastructure Partners

PFA

PKA

SSE

Vattenfall

Macquarie Capital

Equinor

Global InfrastructurePartners

E.ON

Ørsted

Capacity owned in MW

17%

11%

9%

7%

7%

5%

4%

4%

4%

4%

3%

3%

3%

2%

2%

2%

15%

28 Offshore Wind in Europe - Key trends and statistics 2018WindEurope

FIGURE 15

Owners’ share of total cumulative installed capacity at the end of 2018 (MW)

Source: WindEurope

0 1,000 2,000 3,000 4,000 5,000

Others

SEAS-NVE

EnBW

Sumitomo

Eneco

Trianel

Pension Danmark

CopenhagenInfrastructure Partners

Masdar

PKA

Ocean Breeze Energy

Global InfrastructurePartners

SSE

Equinor

Siemens

Iberdrola

Stadwerke München

Northland Power

Macquarie Capital

Innogy

Vattenfall

E.ON

Ørsted

Capacity owned in (MW)

16%

8%

7%

6%

5%

3%

3%

3%

3%

3%

2%

2%

2%

2%

1%

1%

1%

1%

1%

1%

1%

1%

25%

Ørsted is the largest owner of offshore wind power in Eu-rope with 16% of the total capacity at the end of 2018 (figure 15). E.ON is the second largest owner with 8%,

followed by Vattenfall (7%), Innogy (7%), and Macquarie Capital (5%). The top five owners represent 42% of all in-stalled capacity in Europe, similar to 2017.

Industry activity and supply chain

29Offshore Wind in Europe - Key trends and statistics 2018WindEurope

7. Shares are calculated according to the actual number of individual foundations installed in 2018. Where the project developer con-tracted more than one company to manufacture the foundations, and where the respective shares (in case of consortia/joint venture) were not specified, foundations installed were split in equal parts between the partners.

3.3 SUBSTRUCTURES AND FOUNDATIONS

Monopiles remained the most popular substructure type in 2018, representing 74.5% of all installed foundations, a decrease compared to 2017 (86%). Jackets were the sec-ond most used substructure, with 119 jackets installed in 2018, representing 24.5% of all foundations installed.

One floating barge was commissioned for the Floatgen project and 2 floating semi-sub structures were commis-

sioned respectively for the Eolink Prototype and the Kin-cardine project.

On the supplier side, EEW installed 49% of all foundations in 2018, followed by Sif (29%) and Steelwind Nordenham (7%).

FIGURE 16Foundations installed in 2018 by manufacturing company7

Source: WindEurope

EEW

Sif

Steelwind Nordenham

Lamprell

ST3 Offshore

Navantia-Windar Consortium

Smulders

Esteyco

Bouygues Travaux Publics

ASM Industries

Chouteaux Metalform

0 50 100 150 200 250

Monopile Jacket Semi-Sub Gravity Base Barge

Industry activity and supply chain

30 Offshore Wind in Europe - Key trends and statistics 2018WindEurope

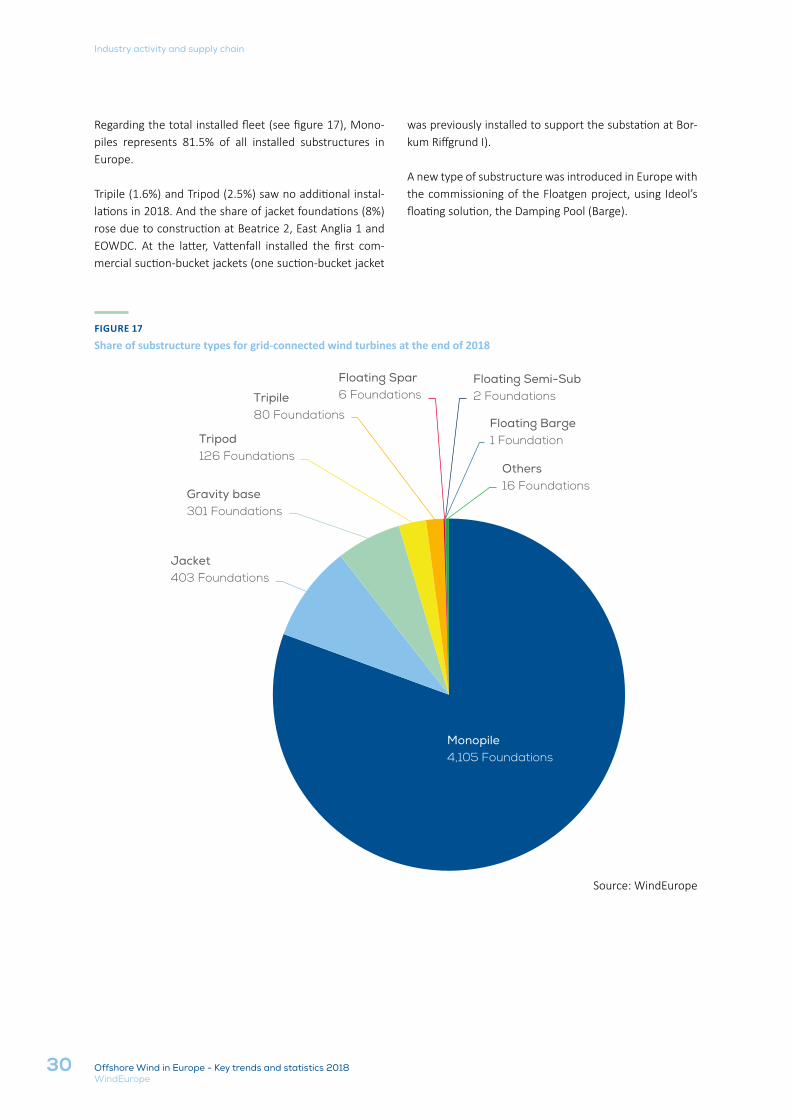

Regarding the total installed fleet (see figure 17), Mono-piles represents 81.5% of all installed substructures in Europe.

Tripile (1.6%) and Tripod (2.5%) saw no additional instal-lations in 2018. And the share of jacket foundations (8%) rose due to construction at Beatrice 2, East Anglia 1 and EOWDC. At the latter, Vattenfall installed the first com-mercial suction-bucket jackets (one suction-bucket jacket

was previously installed to support the substation at Bor-kum Riffgrund I).

A new type of substructure was introduced in Europe with the commissioning of the Floatgen project, using Ideol’s floating solution, the Damping Pool (Barge).

FIGURE 17

Share of substructure types for grid-connected wind turbines at the end of 2018

Source: WindEurope

Monopile4,105 Foundations

Jacket403 Foundations

Gravity base301 Foundations

Tripod126 Foundations

Tripile80 Foundations

Floating Spar 6 Foundations

Floating Semi-Sub 2 Foundations

Floating Barge1 Foundation

Others16 Foundations

Industry activity and supply chain

31Offshore Wind in Europe - Key trends and statistics 2018WindEurope

FIGURE 19Share of energised export cable by supplier in 201810

Source: WindEurope

In terms of export cables9 in 2018 (figure 19), 8 export cables manufactured by NKT Group were energised, rep-resenting 53.3% of the annual market.

Prysmian, Ls Cable & System, and JDR Cable Systems each had a 13.3% share, and Nexans represented the remain-ing 6.7%.

8. Shares are calculated taking into account the number of grid-connected turbines in each wind farm during 2018.9. In Germany, the export cable is the cable connecting the offshore HVDC substation to the land. In other countries the export cable is

understood as the cable connecting the wind farm to land.10. Shares are calculated by taking into account the number of export cables in fully completed new wind farms.

FIGURE 18Share of energised intra-array cables by supplier in 2018

Source: WindEurope

42% of new intra-array cables8 energised in 2018 were from Nexans. JDR Cable Systems (32.1%) and Prysmian (16.1%) were the other suppliers with energised intra-ar-ray cables.

With the commissioning of the Blyth offshore wind farm last year, Nexans has now supplied 2 new wind farms with its new 66 kV cable technology.

3.4 CABLES

Nexans175 Cables

JDR Cable Systems166 Cables

PRYSMIAN Powerlink67 cables

NKT Group8 cables

PRYSMIAN Powerlink2 cables

Ls Cable & System2 cables

JDR Cable Systems2 cables

Nexans1 cable

Industry activity and supply chain

32

Chapter name

Offshore Wind in Europe - Key trends and statistics 2018WindEurope

Photo: Ørsted

33Offshore Wind in Europe - Key trends and statistics 2018WindEurope

4.

4.1 FINANCING ACTIVITY IN 2018

New offshore wind investments in Europe increased to €10.3bn, up 37% from 2017. After the drop in Final Invest-ment Decisions (FID) in 2017 as the market transitioned to auctions, investments in offshore wind recovered to the

third highest level on record. Project costs in 2018 were lower than in the previous three years, allowing 4.2 GW of additional capacity to be financed. This is the second highest amount after a record year in 2016.

FIGURE 20New offshore wind investments and capacity financed: 2010 – 2018 (€bn)

Source: WindEurope

8.4

6.15.0

7.28.8

13.1

18.2

7.5

10.3

0

2

4

6

8

10

12

14

16

18

20

0

2

4

6

8

10

12

14

16

18

20

2010 2011 2012 2013 2014 2015 2016 2017 2018

GW€b

n

Total investments (€bn) New capacity financed (GW)

INVESTMENTS

34 Offshore Wind in Europe - Key trends and statistics 2018WindEurope

Investments

TABLE 4Investment in European offshore wind farms in 2018

TOTAL INVESTMENTS (€BN)

NEW CAPACITY FINANCED (MW)

NUMBER OF PROJECTS

United Kingdom 5.4 1,858 3

Netherlands 1.4 732 1

Denmark 1.1 605 1

Belgium 1.8 706 2

Germany 0.4 258 2

Italy 0.1 30 1

Portugal 0.1 25 1

Norway 0.0 4 1

Total 10.3 4,217 12

Since 2010 the UK has attracted 48% of new investments, worth €40bn, making it the biggest offshore wind market over the last nine years. Germany follows with 34% or €28bn invested over the same period.

12 projects reached Final Investment Decision (FID) in 2018, 95% of which were concentrated in four countries: the UK, Belgium, Denmark and the Netherlands. The ma-jority of the new capacity financed – a total of 52% – was

in the UK, including Triton Knoll and Moray East, totalling 1.8 GW of capacity between them. Other significant pro-jects were Kriegers Flak (606 MW) in Denmark and Seam-ade (487 MW) in Belgium.

35Offshore Wind in Europe - Key trends and statistics 2018WindEurope

Investments

FIGURE 22Investments in the offshore wind sector in 2018 (€bn)

Source: WindEurope

FIGURE 21Offshore wind investments by country since 2010

Source: WindEurope

82%OF OFFSHORE WIND INVESTMENTS SINCE

2010 HAVE BEEN IN THE UK AND GERMANY

18 % 34 % 48 % UK

GermanyOther countries

€7.5bn

€4.6bn

€0bn

€10.3bn

€8.5bn

€0.7bn

Construction of newoffshore wind projects

Refinancing offshore wind projects

2017

2018

Investments in transmission lines:construction and refinancing

In addition to the investments in new wind farms, 2018 also saw €8.5bn in refinancing transactions, an 85% in-crease over 2017. With the addition of new investments

in transmission assets of €0.7bn, offshore wind generated a total financing activity of €19.6bn.

36 Offshore Wind in Europe - Key trends and statistics 2018WindEurope

FIGURE 23Non-recourse debt trends per type of transaction (€bn)

Source: WindEurope

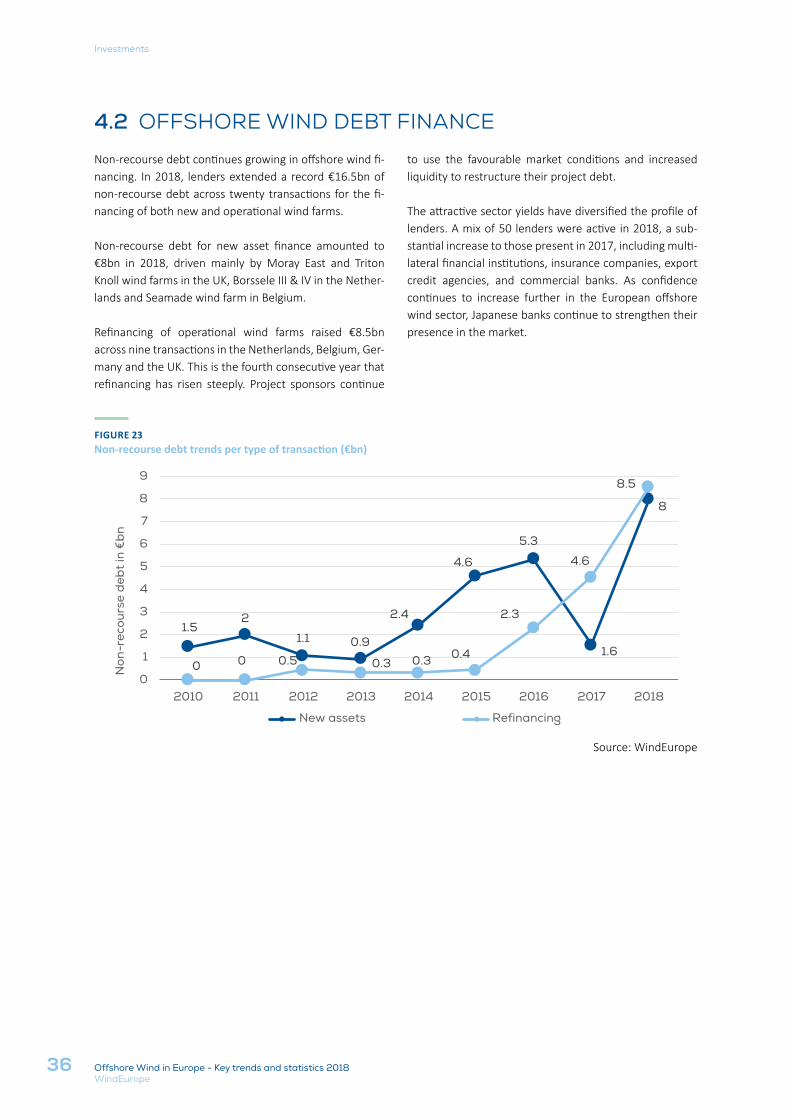

4.2 OFFSHORE WIND DEBT FINANCE

Non-recourse debt continues growing in offshore wind fi-nancing. In 2018, lenders extended a record €16.5bn of non-recourse debt across twenty transactions for the fi-nancing of both new and operational wind farms.

Non-recourse debt for new asset finance amounted to €8bn in 2018, driven mainly by Moray East and Triton Knoll wind farms in the UK, Borssele III & IV in the Nether-lands and Seamade wind farm in Belgium.

Refinancing of operational wind farms raised €8.5bn across nine transactions in the Netherlands, Belgium, Ger-many and the UK. This is the fourth consecutive year that refinancing has risen steeply. Project sponsors continue

to use the favourable market conditions and increased liquidity to restructure their project debt.

The attractive sector yields have diversified the profile of lenders. A mix of 50 lenders were active in 2018, a sub-stantial increase to those present in 2017, including multi-lateral financial institutions, insurance companies, export credit agencies, and commercial banks. As confidence continues to increase further in the European offshore wind sector, Japanese banks continue to strengthen their presence in the market.

1.52

1.1 0.9

2.4

4.6

5.3

1.6

8

0 0 0.5 0.3 0.3 0.4

2.3

4.6

8.5

0

1

2

3

4

5

6

7

8

9

2010 2011 2012 2013 2014 2015 2016 2017 2018

Non

-rec

ours

e d

ebt

in €

bn

New assets Refinancing

Investments

37Offshore Wind in Europe - Key trends and statistics 2018WindEurope

11. Excluding pre-development phase of projects.

4.3 ACQUISITION ACTIVITY

Project acquisition activity11 increased 30% compared to 2017, totalling 3.8 GW. The equity mix continues to be approx-imately one third coming from financial investors, and two thirds from power producers.

FIGURE 24Project acquisition activity in 2018 by type of investor

Source: WindEurope

Financial services1,255 MW

33%

Power producers2,537 MW 67%

Infrastructurefunds647 MW 17%

Assetmanagers

173 MW 5%

Diversifiedfinancial services435 MW 11%

3.8 GWACQUISITION ACTIVITY

The majority of transactions happened at the pre-con-struction stage, the most critical phase for a project’s fundraising, with a record of 2.7 GW acquired. Mean-while, 2018 bucked the trend of previous years, where

transactions at the construction and operation phase had increased significantly. There were 630 MW acquired at the construction phase and 425 MW at the operational phase, a 2% increase and a 4% decrease, respectively.

Investments

38 Offshore Wind in Europe - Key trends and statistics 2018WindEurope

Investments

FIGURE 25Acquisition activity per project stage 2015-2018

Source: WindEurope

In addition to those listed above, acquisitions in the pre-development stage amounted to the equivalent of 2.3 GW of potential projects.

Pre-construction Construction In operation

2015 2016 2017 2018

0

500

1,000

1,500

2,000

2,500

3,000

windeurope.org

Rue Belliard 40, 1040 Brussels, Belgium T +32 2 213 1811 · F +32 2 213 1890

WindEurope is the voice of the wind industry, active-ly promoting wind power in Europe and worldwide. It has over 400 members with headquarters in more than 35 countries, including the leading wind turbine manufacturers, component suppliers, research insti-tutes, national wind energy associations, developers, contractors, electricity providers, financial institutions, insurance companies and consultants. This combined strength makes WindEurope Europe’s largest and most powerful wind energy network.

53520-1903-1004www.artoosgroup.eu

PRINTED BY ARTOOSGROUP

53520-1903-1004www.artoosgroup.eu

PRINTED BY ARTOOSGROUP

Related Documents