Document of The World Bank FOR OFFICIAL USE ONLY Report No: 67680-ET PROJECT APPRAISAL DOCUMENT ON A PROPOSED CREDIT IN THE AMOUNT OF SDR 32.2 MILLION (US$50 MILLION EQUIVALENT) TO THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA FOR A WOMEN ENTREPRENEURSHIP DEVELOPMENT PROJECT APRIL 26, 2012 Social Development Unit Sustainable Development Department Country Department AFCE3 Africa Region This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No: 67680-ET

PROJECT APPRAISAL DOCUMENT

ON A

PROPOSED CREDIT

IN THE AMOUNT OF SDR 32.2 MILLION

(US$50 MILLION EQUIVALENT)

TO THE

FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA

FOR A

WOMEN ENTREPRENEURSHIP DEVELOPMENT PROJECT

APRIL 26, 2012

Social Development Unit

Sustainable Development Department

Country Department AFCE3

Africa Region

This document has a restricted distribution and may be used by recipients only in the

performance of their official duties. Its contents may not otherwise be disclosed without World

Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

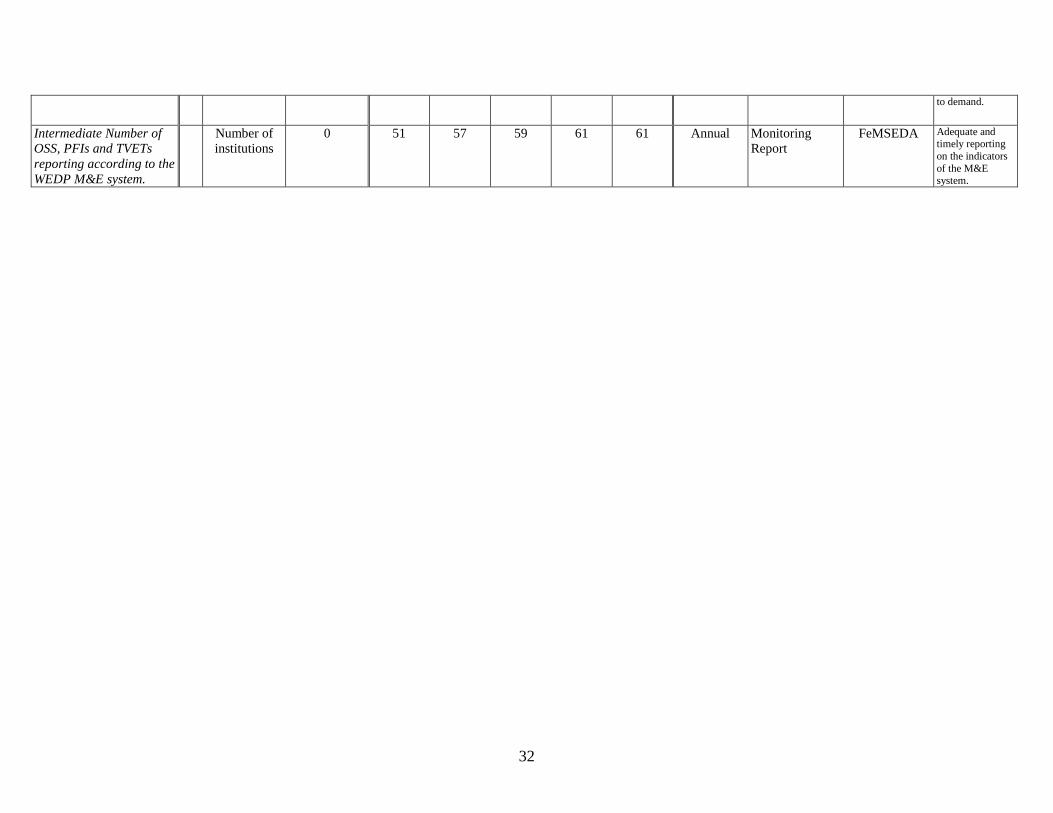

rized

Pub

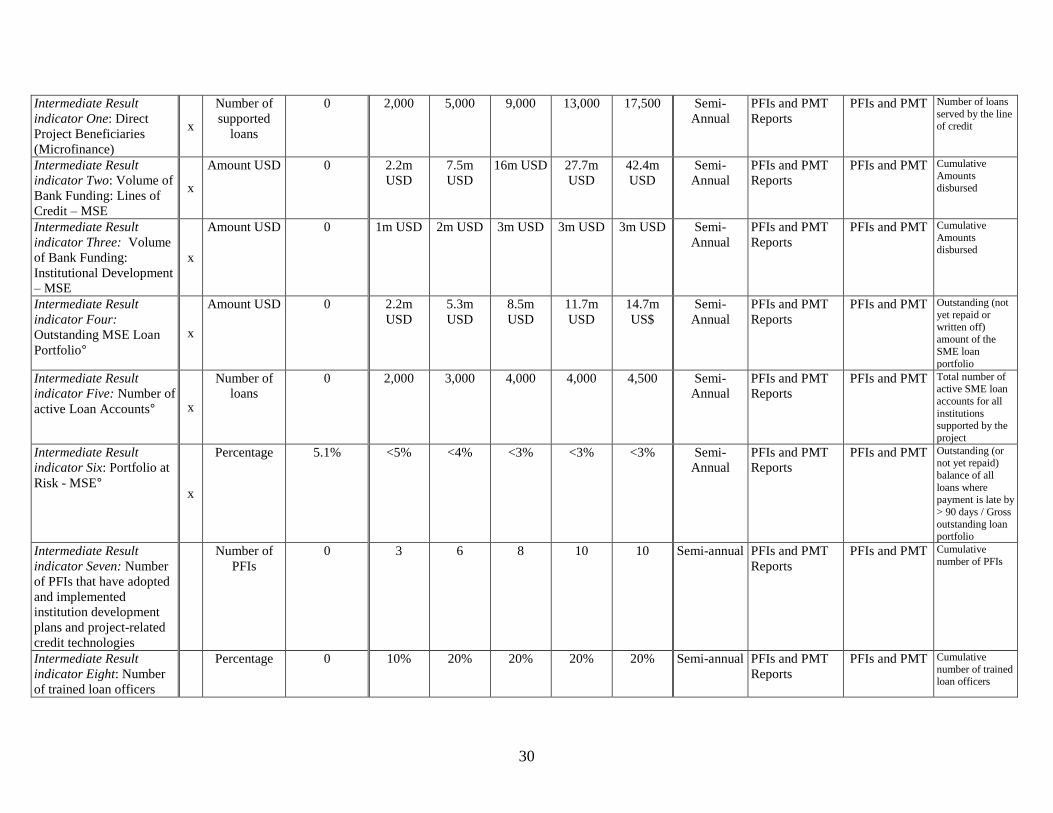

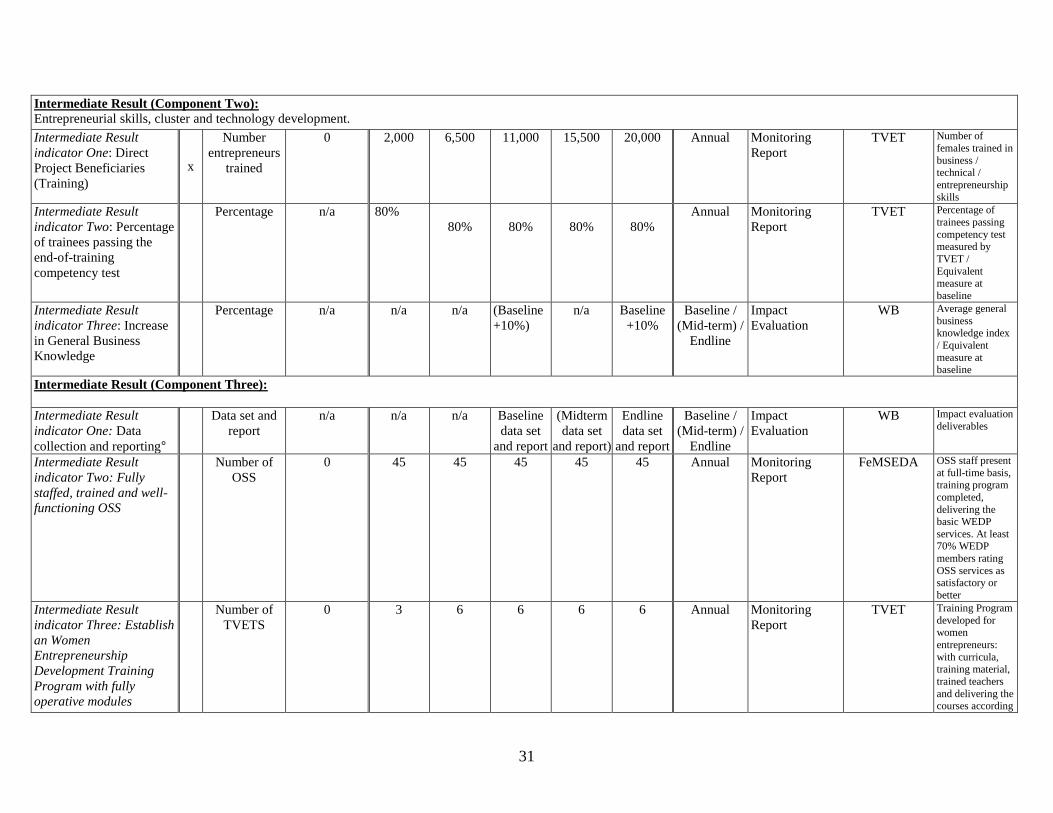

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

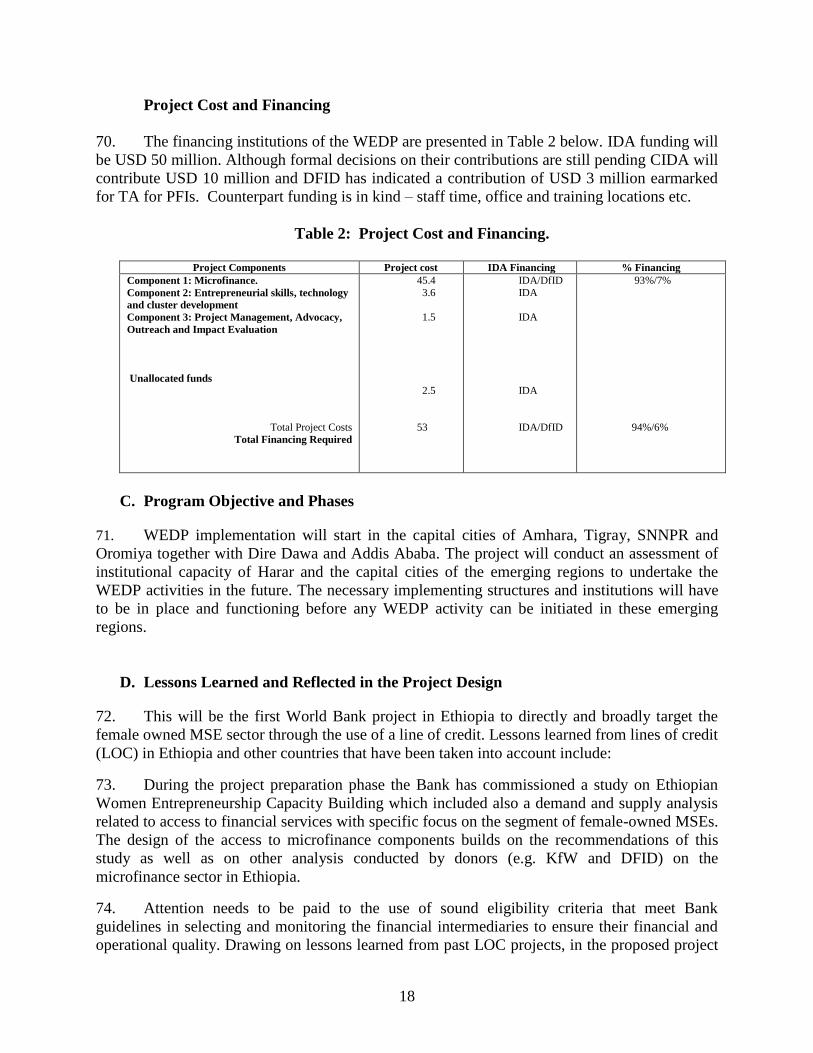

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

ii

CURRENCY EQUIVALENTS

(Exchange Rate Effective as of Feb 29, 2012)

Currency Unit = Ethiopian Birr

USD1 = BIRR 17

USD1 = SDR 0.6427

FISCAL YEAR

July 8 – July 7

ABBREVIATIONS AND ACRONYMS

AEMFI Association of Ethiopian MFIs

AfDB African Development Bank

AGP Agricultural Growth Program BOM Board of Management

CIDA Canadian International Development Agency CBB Construction and Business Bank

CBE Commercial Bank of Ethiopia CDAs Cluster Development Agents

CEFE Competency based Economies through Formation of Enterprise

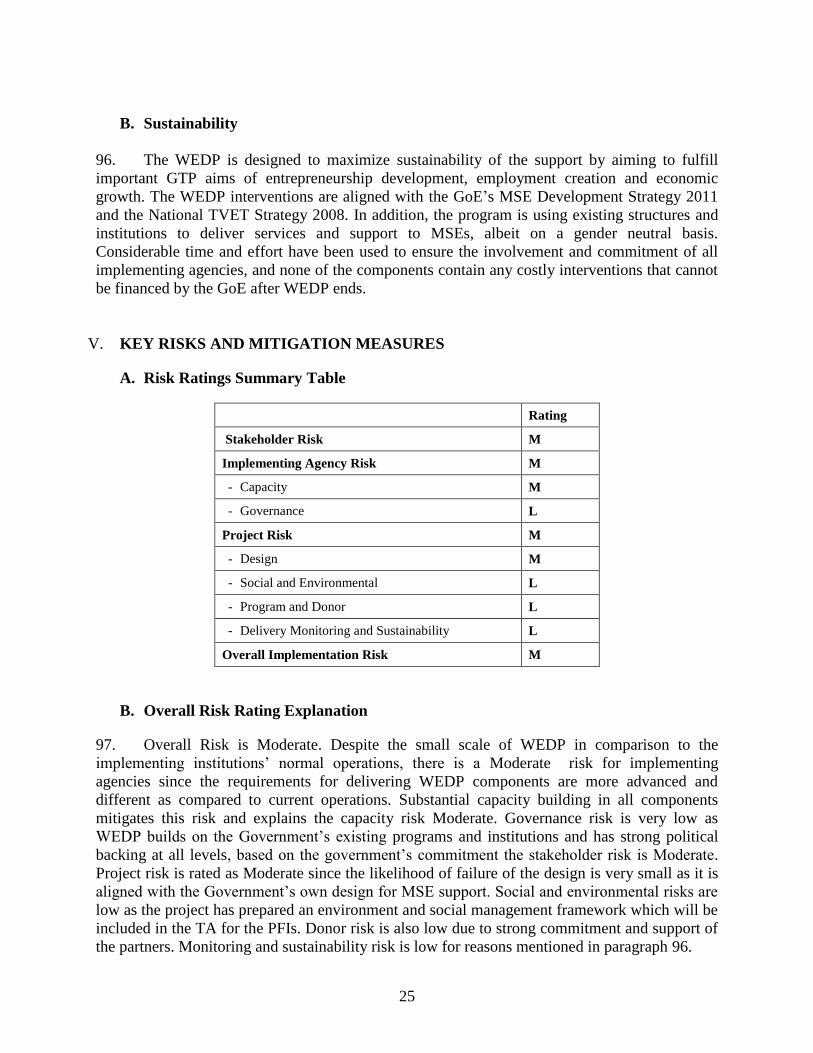

CPAR Country Procurement Assessment Report

CQS Selection Based on Qualifications

CSA Central Statistical Agency CPI Consumer Price Index

DA Designated Account

DBE Development Bank of Ethiopia

DFID Department for International Development

DPs Development Partners

EDQAF Ethiopia Data Quality Assessment Framework

EDRI Ethiopia Development and Research Institute EMC Executive Management Committee

EMCP Expenditure Management Control

EPRDF Ethiopia People‘s Revolutionary Democratic Front

ERR Economic Rate of Return

ESMF Environmental & Social Safeguards Management Framework

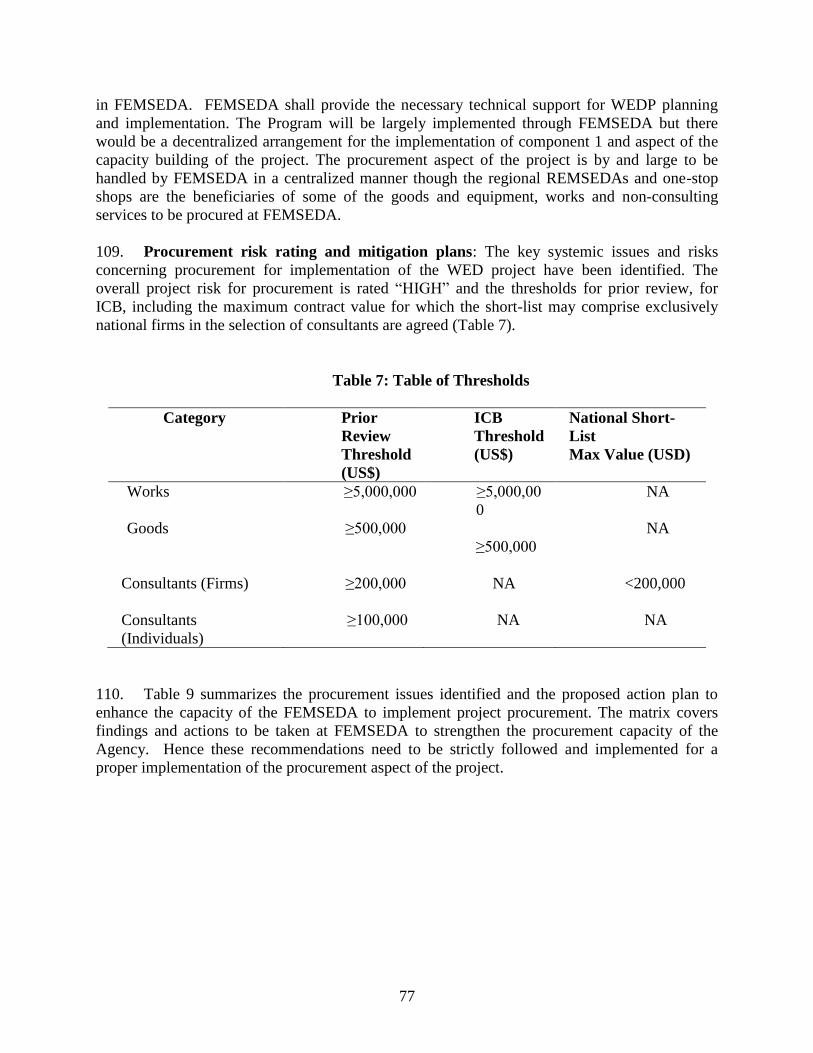

FA Fiduciary Assessments FAP Finance and Accounts Process

FEMSEDA Federal Micro and Small Enterprise Development Agency

FM Financial Management

FMM Financial Management Manual

FMRs Financial Management Reports

FPPA Federal Public Procurement and Property Administration Agency

FRR Financial Rate of Return

GAC Governance and Anti-Corruption

iii

GDP Gross Domestic Product

GMT Grassroots Management Training

GoE Government of Ethiopia

GTP Growth and Transformation Plan

GIZ Deutsche Gesellschaft für Internationale Zusammenarbeit (German

Association for International Cooperation)

HPR House of Peoples‘ Representatives IAP Internal Audit Process

IBEX Integrated Budget and Expenditure

IC Individual Consultants

ICB International Competitive Bidding

IDA International Development Agency

IFAD International Fund for Agricultural Development IFC International Finance Corporation

IFRs Interim unaudited Financial Reports

KAB Know About Business

KfW Kreditanstalt für Wiederaufbau (German Development Institute)

LCS Least Cost Selection

LOC Lines of Credit

M&E Monitoring and Evaluation

MDGs Millennium Development Goals

MDTF Multi Donor Trust Fund

MFI Micro-Finance Institutions

MoFED Ministry of Finance and Economic Development

MOU Memorandum of Understanding

MoUDC Ministry of Urban Development and Construction

MoWY&CA Ministry of Women, Youth and Children‘s Affairs

MSE Micro and Small Enterprise

MSME Micro, Small and Medium Enterprises

NAP National Action Plan for Gender

NBE National Bank of Ethiopia

NCB National Competitive Bidding

NGO Non-Governmental Organizations

NPLs Non Performing Loans

NPMT National Project Management Team

NTA National TVET Agency

OFAG Office of the Federal Auditor General

OM Operational Manual

OSS One Stop Shops

PAD Project Appraisal Document

PBS II Protection of Basic Services Phase II Project

PDO Project Development Objective

PEFA Public Expenditure and Financial Accountability

PFEA Public Financial Enterprise Supervising Agency

PFIs Participating Financial Institutions

PFM Public Financial Management

PIM Project Implementation Manual

PIU Project Implementation Unit

PMT Project Management Team

iv

PPA Property Administration Agency

P-RAMS Procurement Risk Assessment and Management Systems

PSCAP Program Public Sector Capacity Building Program

PSNP Productive Safety Net Program

QBS Quality Based Selection

QCBS Quality and Cost-Based Selection

REMSEDA Regional Micro and Small Enterprise Development Agency RMP Risk Management Process

RUFIP Rural Financial Intermediation Program

SBD Standard Bidding Documents

SIP Strategic Investment Project

SLAs Subsidiary Loan Agreements

SLMP Sustainable Land Management Program

SNNPR Southern Nations, Nationalities, and Peoples Region

SOEs Statement of Expenditures

TA Technical Assistance

TCAs Technical Cooperation Agreements

TOT Training of Trainers

TVET Technical and Vocational Education and Training

UNIDO United Nations Industrial Development Organization

USAID DCA United States Agency for International Development-Development Credit

Authority

WB World Bank

WEDP Women Entrepreneurship Development Project

Vice President: Obiageli Katryn Ezekwesili

Country Director: Guang Zhe Chen

Sector Director: Jamal Saghir

Sector Manager: Ian Bannon

Task Team Leader: Yasmin Tayyab

v

ETHIOPIA

WOMEN ENTREPRENEURSHIP DEVELOPMENT PROJECT

TABLE OF CONTENTS

Page

I. STRATEGIC CONTEXT .................................................................................................1

A. Country Context ............................................................................................................ 1

B. Sectoral and Institutional Context ................................................................................. 2

C. Higher Level Objectives to which the Project Contributes .......................................... 4

II. PROJECT DEVELOPMENT OBJECTIVES ................................................................5

III. PROJECT DESCRIPTION ..............................................................................................6

A. Project Components ...................................................................................................... 6

B. Project Financing ........................................................................................................ 17

C. Program Objective and Phases.................................................................................... 18

D. Lessons Learned and Reflected in the Project Design ................................................ 18

IV. IMPLEMENTATION .....................................................................................................20

A. Institutional and Implementation Arrangements ........................................................ 20

B. Sustainability............................................................................................................... 25

V. KEY RISKS AND MITIGATION MEASURES ..........................................................25

A. Risk Ratings Summary Table ..................................................................................... 25

B. Overall Risk Rating Explanation ................................................................................ 25

VI. APPRAISAL SUMMARY ..............................................................................................26

A. Financial Management ................................................................................................ 26

B. Procurement ................................................................................................................ 27

C. Social and environment (including Safeguards) ......................................................... 28

Annex 1: Results Framework and Monitoring .........................................................................29

Annex 2: Detailed Project Description of Components 1 and 2 ..............................................33

Annex 3: Implementation Arrangements ..................................................................................46

Annex 4: Operational Risk Assessment Framework (ORAF) ... ………………………………….84

Annex 5: Implementation Support Plan ....................................................................................87

vi

Annex 6: Compliance with OP 8.30 Financial Intermediary Lending ...................................91

Annex 7: Map of Ethiopia ........................................................................................................107

vii

PAD DATA SHEET

Ethiopia

Women Entrepreneurship Development Project (P122764)

PROJECT APPRAISAL DOCUMENT .

AFRICA

AFTCS

.

Basic Information

Date: 26-Apr-2012 Sectors: Microfinance (85%), Vocational training (12%), Other industry (3%)

Country Director: Guang Zhe Chen Themes: Micro, Small and Medium Enterprise support (100%)

Sector Manager/Director: Ian Bannon/Jamal Saghir

Project ID: P122764 EA Category: B - Partial Assessment

Lending Instrument: Specific Investment Loan Team Leader(s): Yasmin Tayyab

Joint IFC: No .

Borrower: Ministry of Finance and Economic Development

Responsible Agency: Federal Micro and Small Enterprise Development Agency

Contact: Ato Gebremeskel Challa Title: Director General

Telephone No.: 251-0911254312 Email: [email protected] .

Project Implementation Period: Start Date: 25May-2012 End Date: Dec 31-2017

Expected Effectiveness Date: 02-Jul-2012

Expected Closing Date: 31-Dec-2017 .

Project Financing Data(USDM)

[ ] Loan [ ] Grant Credit Term: Standard with 40 years maturity

[ X ] Credit [ ] Guarantee

For Loans/Credits/Others

Total Project Cost (USDM): 53.00

Total Bank Financing (USDM): 50.00 .

Financing Source Amount(USDM)

BORROWER/RECIPIENT 0.00

International Development Association (IDA) 50.00

UK British Department for International Development (DFID)1 3.00

Total 53.00 .

Expected Disbursements (in USD Million)

Fiscal Year 2013 2014 2015 2016 2017 2018

Annual 4.20 7.30 9.70 12.90 15.90 0.00

Cumulative 4.20 11.50 21.20 34.10 50.00 50.00 0.00 0.00 0.00 .

1 DFID is providing USD 3 million as technical assistance to the Participating Financial Institutions.

viii

Project Development Objective(s)

The project development objective of the WEDP is to increase the earnings and employment of MSEs owned or partly owned by the participating female

entrepreneurs in the targeted cities. This will be achieved by: i) tailoring financial instruments to the needs of the participants and ensuring availability of

finance; and ii) developing the entrepreneurial and technical skills of the target group and supporting cluster, technology and product development for their

businesses. .

Components

Component Name Cost (USD Millions)

Component 1: Access to Microfinance 42.40

Component 2: Entrepreneurial skills, Technology and Cluster Development. 6.10

Component 3: Project Management, Advocacy and Outreach, Monitoring Evaluation and

Impact Evaluation.

1.50

.

Compliance

Policy

Does the project depart from the CAS in content or in other significant respects? Yes [ ] No [ X ] .

Does the project require any waivers of Bank policies? Yes [ ] No [ X ]

Have these been approved by Bank management? Yes [ ] No [ ]

Is approval for any policy waiver sought from the Board? Yes [ ] No [ X ]

Does the project meet the Regional criteria for readiness for implementation? Yes [ X ] No [ ] .

Safeguard Policies Triggered by the Project Yes No

Environmental Assessment OP/BP 4.01 X

Natural Habitats OP/BP 4.04 X

Forests OP/BP 4.36 X

Pest Management OP 4.09 X

Physical Cultural Resources OP/BP 4.11 X

Indigenous Peoples OP/BP 4.10 X

Involuntary Resettlement OP/BP 4.12 X

Safety of Dams OP/BP 4.37 X

Projects on International Waterways OP/BP 7.50 X

Projects in Disputed Areas OP/BP 7.60 X

.

Legal Covenants

Name Recurrent Due Date Frequency

The Subsidiary Financing Agreement

Description of Covenant

The Subsidiary Financing Agreement has been entered into between the Recipient and DBE.

Name Recurrent Due Date Frequency

The National Project Management Team at FEMSEDA and

the PMT at DBE

Description of Covenant

The National Project Management Team at FEMSEDA and the PMT at DBE has been established with a composition and mandate satisfactory to the

ix

Association.

Name Recurrent Due Date Frequency

Financial management system 31-Oct-2012

Description of Covenant

(FA, Sched. 2, Sec. II.B.1) Maintain or cause to be maintained a financial management system in accordance with the provisions of Section 4.09 of the General Conditions.

Name Recurrent Due Date Frequency

Developing PIM and OM.

Description of Covenant

The Recipient has adopted the PIM and OM in accordance with the provisions of Section I.B of Schedule 2 to this Agreement.

Name Recurrent Due Date Frequency

Description of Covenant

.

Team Composition

Bank Staff

Name Title Specialization Unit

Yasmin Tayyab Senior Social Development

Specialist

Team Lead AFTCS

Espen Villanger Senior Economist Senior Economist AFTP2

Gelila Woodeneh Communications Officer Communications Officer AFRSC

Meron Tadesse Techane Financial Management

Analyst

Financial Management Analyst AFTFM

Shimelis Woldehawariat Badisso Procurement Specialist Procurement Specialist AFTPC

Elena Bonometti Consultant Gender Specialist PRMGE

Francesco Strobbe Young Professional Financial Economist AFTFE

Desta Solomon E T Consultant Skills Development AFTCS

Senidu Fanuel Private Sector Development

Spec.

Private Sector Development Spec. AFTFE

Niklas Buehren E T Consultant Impact Evaluation AFTPM

Rajiv Sondhi Senior Finance Officer Senior Finance Officer CTRLA

Jonathan David Pavluk Senior Counsel Senior Counsel LEGAF

Ernestina Attafuah Senior Program Assistant Senior Program Assistant AFTUW

Dawit Tadesse Team Assistant Team Assistant AFCE3

Jose C. Janeiro Sr. Finance Officer Financial Management CTRLA

.

Locations

Country First Administrative

Division

Location Planned Actual Comments

Ethiopia Adis Abeba Astedader Adis Abeba Astedader X Addis Ababa - capital chartered

City and the following:

Tigray Region - capital Mekele

Southern Nations Nationalities

x

Peoples Region - capital Adama

Oromiya Region - capital

Hawassa

Amhara Region - capital Bahar

Dar

Dire Dawa - chartered city .

.

1

I. STRATEGIC CONTEXT

A. Country Context

1. Stimulating entrepreneurship can contribute substantially to non-farm income

generation and employment in Ethiopia. Official government figures indicate that the

Ethiopian real GDP per capita has grown by 6.5 percent on average per year since 2001/02.

However, even though the private sector has expanded rapidly in Ethiopia for the last decade, it

has done so from a low starting point. According to the latest figures on employment the formal

private sector is still very small; paid work in this sector accounted for less than 5 percent of total

employment. Most people are dependent on subsistence agriculture, and around 80 percent of the

workforce makes a living in agriculture. The hard and vulnerable life in agriculture, coupled with

few jobs in the formal sector, the large expansion of education, the high population growth and a

rapid acceleration of urbanization (World Bank 2010) all contribute to a large and increasing

percentage of people in the micro and small enterprise (MSE2) sector. Some of these MSEs,

however, have a large potential for income and employment growth but are lacking the necessary

skills, services, finance and support to grow their businesses.

2. MSEs will have to play a major role during the transformation of the Ethiopian

economy. Experience from a range of countries indicate that the Ethiopian economic growth will

not continue unless a structural transformation takes place where workers move from subsistence

agriculture to higher productivity activities.3 The manufacturing sector, which has played the

lead role in initial stages of such transformations, has been growing in value terms at similar

rates as GDP in Ethiopia but remains miniscule in comparison to the total labor force. Only

around 13 percent of the employed population in urban areas is engaged in manufacturing as of

2011, and the corresponding annual growth in employment has been a modest 4 percent during

the last three years (CSA 2009, 2010 and 2011). While there are many initiatives in Ethiopia to

spur high-productive labor intensive production, where the expansion of the rose farm industry is

one success story, it is also recognized that the micro and small enterprises have to play a role in

the transformation (Government of Ethiopia Growth and Transformation Plan 2010/11 –

2014/15, World Bank 2011).

3. Unleashing the potential of women in the economic sector would increase GDP

growth substantially. Recent estimates illustrate the potential of including women in the

economic sectors: reducing gender inequalities in education and the labor market could increase

the annual GDP growth in the country by around 1.9 percentage points (World Bank 2008)4.

Women are marginalized in the business realm in similar ways as in education and the labor

market. Although the potential of unleashing women entrepreneurs is recognized, no estimate of

2 The Government of Ethiopia MSE Strategy 2011 definitions are applied throughout the PAD: A Microenterprise is

defined as a private service/manufacturing business with less than Birr 50,000/100,000 (USD 3,000/6,000) in total

assets excluding buildings and/or less than five employees including family members. A small enterprise is defined

as a private service/manufacturing business with assets in the range Birr 50,000 - 500,000/Birr 100,000 - 1.5 Million

(USD 3,000 – 30,000/USD 6,000 to USD 90,000) and/or 6-30 employees. If there is conflict between the two

criteria, value of assets will determine classification. 3 World Bank (2011): ―Light Manufacturing in Africa‖, Volume I.

4 World Bank (2008): ―Unleashing the Potential of Ethiopian Women‖.

2

the likely impacts on GDP is available (World Bank 2009a). Moreover, data confirms the

disadvantaged position of women in the economic sectors. The unemployment rate among

females is more than twice as large as that of males in urban areas (CSA 2010), the wage gap

between men and women with similar background for doing the same job is around 50 percent

(World Bank 2009a), the share of women without education is almost twice as high as that of

men,5 microenterprises owned by women earn only a fraction of those owned by men (World

Bank 2009b), and women face much larger barriers for doing business than men do (World Bank

2009c). Taking into account the economic potential of women in the society, business

operations, asset ownership, investment and decision-making, the GDP gains of reducing gender

inequalities for the economy as a whole is likely to be higher than the above estimate for

education and the labor market.

4. Supporting female entrepreneurs may be one of the most viable approaches for

realizing the economic potential of the current generations of women– and hence for

increasing economic growth, creating employment and promoting gender equality. The

constraints women entrepreneurs are facing are lack of access to finance, land, training,

education, and effective business networks (Triodos Facet 2011). Particularly, Microfinance in

Ethiopia has a low coverage for women and do not provide suitable financing for women

entrepreneurs. Together with the underdevelopment of the financial sector, this suggests a large

potential for micro finance services. Moreover, in terms of employment in urban areas, the

private sector consists mainly of MSEs. According to the 2011 Urban Employment

Unemployment Survey, over 50 percent of the employed women in urban areas operate or work

for MSEs, which is their main vehicle for income generation.

5. The Government has a strong interest in supporting the MSE sector, particularly

for increasing women‟s income. MSE development is key to the GoE‘s efforts to increase the

economic empowerment of women, and the development of small scale income generating

activities for women is a specific aim of the new 5-year plan of the Government – the Growth

and Transformation Plan 2011-2015 (GTP). The Micro Finance Institution (MFI) sector is also

of particular importance to the GoE. The new National Microfinance Strategy has been

circulated, and the GTP specifically addresses the issue of raising the number of female clients to

access loans from MFIs. In addition, the GoE‘s National Action Plan for Gender (NAP) aims at

eliminating gender and cultural biases that hinder women from participating equally in economic

engagements. The Development and Change Package of Ethiopian Women developed by the

MoWY&CA clearly outlines the Government‘s view that development of micro and small

enterprises has a key role in generating employment for women.

B. Sectoral and Institutional Context

6. The smaller the business, the lower is productivity, so making MSEs grow is key to

income growth. However, MSE growth is limited by entrepreneurs‘ low education, skills and

knowledge (technical, entrepreneurial and managerial). Given that skills and knowledge are

important for business development and growth, this is a main challenge for Ethiopian MSEs.

5 The Ethiopia Demographic and Health Survey 2011, preliminary version. More precisely, women without

education in the age group 15 to 49 account for 50.8 percent, while the corresponding figure for men is 29.5 percent.

3

Unfortunately, the availability of training is limited and the quality of services is often low. Only

7 percent of all MSEs and 6 percent of women in MSEs had access to training (Ethiopia

Development and Research Institute -EDRI, 2004). Moreover, the training is not tailored well to

the needs of those who manage these enterprises, particularly the needs of female entrepreneurs

(Triodos Facet 2011, Grunder 2010).

7. Lack of access to finance is one of the biggest constraints for MSE development in

Ethiopia (GTZ 2007, World Bank 2009b, Triodos Facet 2011). Ethiopia is among the most

under banked countries in Sub-Saharan Africa (2010 Doing Business), and access to finance is

listed as the most severe hindrance by entrepreneurs themselves. The Ethiopian microfinance

sector is relatively young (started in 1997) and consists of 31 regulated MFIs that reach over 2.5

million clients (June 2011) with an outstanding loan balance of Birr 6.5 billion (384 million

USD) and a balance of saving of Birr 3.4 billion (199 million USD). The MFIs have a rural

orientation and largely work with the group-lending methodology. The industry is very

concentrated, with more than 80 percent of the clients (and more than 90 percent of outstanding

loans) being served by the 5 largest MFIs. Moreover, as these large MFIs are restricted to their

own ―territory‖ – being one of the regions – competition in the industry is very limited. These 5

largest MFIs are also very much influenced by their respective regional governments, which

practically own the MFI and provide below market-rate funds. MFIs are supervised by the

National Bank of Ethiopia and operate within a clear regulatory framework6. The Ethiopia

Investment Climate Assessment 2006 finds the huge collateral requirement to be a critical

obstacle as the value of collateral is one of the highest in the developing world (173 percent of

loan amount). Women entrepreneurs face higher barriers than men, especially in providing

collateral. Most assets accepted by lenders are registered to men and there are cultural barriers

for women using collateral, so this avenue of finance is almost closed for female entrepreneurs.

Even if the number of microfinance institutions doubled in the last decade and total lending and

number of clients has increased rapidly, the situation for individual female entrepreneurs in the

cities remains the same. MFI lending is almost entirely group based and the average loan size is

very low – only Birr 2,200 (USD 140) in 2009. Hence, the current MFI lending practice is not

suited for growth-oriented women entrepreneurs.

8. Substantial opportunities exist to increase earnings of existing MSEs by providing

the operators with the necessary entrepreneurial and technical skills, facilitating the utilization of

more productive technologies and making finance for such investments available. High import

costs result in high prices on most imported goods, giving considerable scope to domestic

entrepreneurs to profit from this price differential. Moreover, since well-managed light

manufacturing firms in Ethiopia has a comparable productivity to similar firms in China, there is

a huge untapped potential for Ethiopian entrepreneurs to use existing simple technologies to

compete with imports of simple manufactured products (World Bank 2011). In Ethiopia, three

government technical institutes are mandated to provide technical support and technology

transfer to selected manufacturing industries – the Textile Industry Development Institute, the

Leather Development Institute and the Metal Industry Development Institute. These have

attracted quite some donor attention and support given the perceived potential in these sectors for

export, income and employment growth. This upgrading of the institutes can also benefit MSEs

6 See NBE proclamation no. 40/1996 and no. 626/2009 together with NBE directive no. 18/2006.

4

through transfer of technology and technical assistance especially to strengthen the clusters in the

cities.

9. The new GoE MSE Strategy provides a coherent and suitable framework for

support to growth-oriented female operated MSEs aiming at improving the provision of

demand-driven business development services, high quality technical training and technology

transfer. Nevertheless, there are different levels of understanding and practice in implementing

institutions (REMSEDA, Technical and Vocational Education and Training (TVET) institutions

and One Stop Shops) with respect to how the new strategy should guide the support. In

particular, there is not a clear understanding and appreciation of demand driven approaches, the

benefits of stimulating competition and the role of private initiative and entrepreneurship. It will

be critical to create a level of awareness of the new strategies for MSE development, build

capacity in all implementing institutions and shift the mindset of involved personnel away from

central planning and towards market based approaches. This process will enable them to respond

to the demands of the changing environment.

C. Higher Level Objectives to which the Project Contributes

10. The higher-level goal of the WEDP is to supplement the other interventions in

Ethiopia to accelerate broad-based sustained growth for employment creation and poverty

reduction in urban areas. The WEDP complements several other programs and investments in

Ethiopia. In particular, it provides a platform to stimulate growth in urban areas complementing

the growth-oriented rural Bank funded programs like the Agricultural Growth Program (AGP),

the Productive Safety Net Program (PSNP) and Sustainable Land Management Program

(SLMP). The WEDP also complements and is integrated with several major donors‘ efforts to

expand finance and support entrepreneurship: The KfW Capital Link project provides guarantees

for private banks‘ on-lending to MFIs, the USAID DCA provides guarantees to private banks to

lend to female entrepreneurs with medium businesses, and the RUFIP (Rural Financial

Intermediation Program) funded by IFAD and AfDB provides loans to MFIs for on-lending to

people in rural areas.

11. The WEDP also aims to help achieve the government‟s five year poverty reduction

strategy (the GTP) and the Millennium Development Goals (MDGs). The WEDP will

constitute one implementing tool for achieving the GTP aims in the MSE sector and will

contribute to the first MDG by reducing the number of people exposed to poverty through

employment creation within participating MSEs. The program will also contribute to the third

MDG by promoting gender equality and empowering women – especially through building skills

and knowledge and contributing to their employment and economic independence. Finally, the

WEDP contributes to MDG 8 on partnerships and the Paris Declaration on Aid Effectiveness

through the substantial donor coordination approach taken in the preparation and implementation

of the program.

12. The WEDP will contribute to the fulfillment of the World Bank Africa Strategy

2011-2016, particularly Pillar I (Competitiveness and Employment) by stimulating urban

economic growth and employment generation, and the World Bank‟s Road Map to Gender

5

Mainstreaming ( 2011 -2013) by focusing on the “economic empowerment” of women. The

WEDP will increase productivity in the MSE sector and create new economic opportunities in

the major cities through demand and supply linkages and through direct support of new activities

and introduction of profitable investments for the female entrepreneurs. This in turn will lead to

an increase in employment opportunities – especially among women as female entrepreneurs

tend to hire more women than men. The WEDP will also decrease the vulnerability of urban

households to economic shocks – particularly the recurring food price shocks - since higher

incomes will enable them to create buffers to mitigate impacts of price spikes. Through

transparency in all components of the program—in particular, by emphasizing outreach and

citizen feedback, providing a mechanism for entrepreneurs themselves to suggest improvements

in the program, and building knowledge—the WEDP will also contribute to improved

governance and accountability.

II. PROJECT DEVELOPMENT OBJECTIVES

13. The project development objective of the WEDP is to increase the earnings and

employment of MSEs owned or partly owned by the participating female entrepreneurs in the

targeted cities. This will be achieved by: i) tailoring financial instruments to the needs of the

participants and ensuring availability of finance; and ii) developing the entrepreneurial and

technical skills of the target group and supporting cluster7, technology and product development

for their businesses.

14. Key PDO results indicators will be (1) enterprise earnings and (2) enterprise

employment. In addition, intermediate results indicators for the sub-components are included; for

details refer to the Results Framework, Annex 1.

15. The project beneficiaries are micro and small enterprises in the targeted areas that are:

owned or partly owned by women entrepreneurs, not full-time in school, and who are committed

to growing their enterprise.

16. The program is designed so that female entrepreneur participants choose the

WEDP activity that is most beneficial for growing their MSE, and no compulsory

combination or sequence of activities is imposed. Women interested in participating in WEDP

and fulfilling the criteria for project beneficiaries listed above will be issued a WEDP

membership card before any WEDP finance, training or services are granted. The members will

go through different selection criteria depending on the specific WEDP activity: (1) Those who

seek finance will go through an ―eligibility for finance and granting procedure for growth-

oriented female entrepreneurs‖ as determined by the financial institution involved, (2) those who

want to be trained will be deemed eligible by a skills enhancement/training and selecting

mechanism, and (3) participants within clusters chosen for WEDP support will be qualified by a

separate set of criteria. Estimates of demand for microfinance and projections of loan

disbursement suggest that the WEDP funds for this component will cater for at least 17.500

7 Industrial clusters are the concentration of economic activities of a certain sector in a certain location producing similar and closely related

goods. Industrial clusters provide a wide range of advantages that enable enterprises become competitive and profitable. These advantages could

be generated either through unplanned positive externalities such as industry specialization, labor pooling, and knowledge spillovers or through a deliberate joint action.

6

women entrepreneurs8. Given the indications from the targeted group that training and skills

development are necessary to grow their business, the aim of the entrepreneurial and technical

skill enhancement is to offer such training to all WEDP members that takes WEDP

microfinance. Adding the estimated number of WEDP members that would only seek training

indicates that the total number of WEDP participants will be around 20,000 female

entrepreneurs. Further details of the selection processes and expected number of participants are

presented under each component, below.

17. WEDP will be a national urban project covering the four major cities in four regions:

Mekele in Tigray, Bahar Dar in Amhara, Hawwasa in SNNP and Adama in Oromiya and the two

chartered cities, Addis Ababa and Dire Dawa. Neighboring suburbs and satellite cities may be

included based on the available resources and capacity for program implementation. The exact

definition of eligible cities will be detailed in the Project Implementation Manual and

Operational Manual. The project will undertake a resource and implementation assessment for

Harar and the four emerging regions (Afar, Somali, Benishangul-Gumuz and Gambela) during

project implementation to come up with recommendations to expand WEDP activities to these

four regions in the future.

III. PROJECT DESCRIPTION

A. Project Components

18. The Project has three components with a total investment of USD 53 million, each

described below (See Annex 2 for a detailed project description).

Component 1: Access to Microfinance. (USD 45.4 million)

19. The aim of the component is to facilitate access to financial services for female growth-

oriented entrepreneurs by providing working capital and investment finance through a dedicated

line of credit. At the same time, the component aims at improving the capacity of existing MFIs

to serve female growth-oriented entrepreneurs with tailored financial products. The component is

based on a two-tier structure where the Development Bank of Ethiopia (DBE) will act as an MSE

finance wholesaler engaged in the business of lending to qualified Participating Financial

Institutions (PFIs) with the specific requirement of on-lending only to female-owned or partly

female-owned micro and small enterprises. The PFIs will engage in the retail distribution of sub

loans to this specific target of MSE clients. The lending activities operated by DBE and the MFIs

triggers OP 8.30 Financial Intermediary Lending, and WEDP has been designed to fully comply

with this operational policy (refer to Annex 6 for compliance and clearance).

20. Women entrepreneurs eligible for applying for the financial products provided under

WEDP would be women with full ownership of an MSE or who are at least part-owner of the

enterprise and have a growth-oriented business - as assessed by the PFIs. The PFIs will develop

8 WEDP team‘s projections based on a gradually increasing number of borrowers and average loan size throughout

the WEPD implementation.

7

their own assessment criteria and will determine the granting of finance among eligible women

entrepreneurs.

21. The component will consist of two closely interlinked sub-components: (i) a Credit

Facility in DBE for on lending to Participating Financial Institutions which in turn will on-lend

to female-owned/partly female-owned MSEs and (ii) a TA Facility to support: (a) capacity

building and MSE loan administration in the PFIs; and (b) capacity building of the project

management team (PMT) within DBE.

22. The design of the component follows two guiding principles: on one side removing the

obstacles to access to finance for the targeted women entrepreneurs; on the other side it aims at

using, to the maximum extent possible, existing institutions and services, in order to avoid

duplications.

23. The project uses an incentive approach to support MFI up-scaling to supply loans on an

individual basis9 and other tailored financial products to female-owned/partly female-owned

MSEs. The incentive approach would combine the provision of appropriate financing

instruments to PFIs (i.e. line of credit) with commitments from participating institutions to

strengthen their lending capability to female owned/partly female-owned MSEs over time.

Technical assistance will be a mandatory condition for PFIs to access the Credit Facility.

24. The project plans to establish a dedicated PMT under the DBE. This PMT will act as an

MSE finance wholesaler engaged in the business of lending to qualified PFIs with the specific

requirement of on-lending (and providing additional financial products) only to female-

owned/partly female-owned MSEs . The PFIs will engage in the retail distribution of sub loans to

this specific target of MSE clients.

25. Via the two-tier institutional framework, this component will introduce international best

practices in Ethiopia and promote the engagement in individual lending (versus group lending) in

providing efficient financial services to female-owned/partly female-owned MSEs. The

institutional capacity building of both the PMT in DBE and PFIs will be provided by a

consulting firm with a proven track record of international experience on similar capacity

building assignment. The institutional and human resource development components of the

project are intended to create the culture and lay the foundation for a wider promotion of

financial services to micro and small entrepreneurs throughout the country.

26. Subcomponent 1a: Credit facility (USD 42.4 million). This sub-component will consist

of a credit facility in DBE for on lending to PFIs for the purpose of on-lending to female-

owned/partly female-owned MSEs. Despite the distortions existing in the Ethiopian financial

sector, the subcomponent has been designed in compliance with OP 8.30 requirements (Annex

6). The PMT under DBE will provide medium-term subsidiary loans in domestic currency to

PFIs, with maturity from 3 to 5 years in accordance with the Subsidiary Loan Agreements

between DBE and individual PFIs. DBE would make arrangements for on-lending the funds to

the selected PFIs against the prior month‘s loan book or against a loan demand schedule to be

prepared by the PFI in advance. Once the allocated amount is drawn down, the PFI would be free

9 Although traditional group lending will not be excluded.

8

to revolve the loan as long as it utilizes the funds for supporting female-owned/partly female-

owned MSEs, in conformity with the WEDP guidelines. With the support and technical

assistance from the TA Facility, the PFIs will set their preferred lending conditions and design

the most appropriate instruments to serve the target segment. DBE will assume the full credit risk

on the PFIs and the PFIs will assume full credit risk on the final beneficiaries. DBE will not lend

directly to MSEs.

27. Targeted PFIs will include both government supported and other (NGO or donor backed

or fully private) registered MFIs currently regulated and supervised by the National Bank of

Ethiopia (NBE). A list of potential PFIs have been assessed based on clear eligibility criteria (see

Attachment 1, Annex 2).This due diligence process will ensure minimum performance and

profitability of the PFIs. Table 1 below gives basic information about the most likely MFI

candidates for WEDP.

Table 1: Basic information about the potential PFIs.

28. The selection criteria takes into account PFI ownership and financial situation,

institutional and management capacity, interest in and commitment to servicing the female-

owned/partly female-owned MSE market, quality of financial reporting and governance,

willingness to strictly adopt and adhere to prescribed policies and procedures and to utilize the

TA facility.

29. All PFIs will be required to enter Technical Cooperation Agreements (TCAs) and

subsidiary loan agreements (SLAs). The mandatory technical assistance, and consequently the

access to the line of credit, will be phased in gradually. Additional PFIs can be added

subsequently, subject to their compliance with the set of required eligibility criteria.

30. Subcomponent 1b: TA facility (USD 3million). A critical success factor and a key goal

of the project are to build the institutional and human resource capacity of PFIs to effectively

service the female MSE client market. An assessment study of selected Ethiopian MFIs

conducted in December 2011 revealed a number of institutional weaknesses which need to be

addressed in order to ensure that PFIs are able to properly utilize funds received through the

program and support the WEDP target group with relevant, timely services. In particular,

weaknesses were noted in the areas of cash-flow-based lending techniques, savings mobilization,

financial and operational reporting, risk management and corporate governance.

ADCSI ACSI DECSI OCSSCO SFPI Wasasa Harbu OMO Average Total

Q1 2011-12 Q1 2011-12 Q1 2011-12 Q1 2011-12 Q1 2011-12 Q1 2011-12 Q1 2011-12 Q1 2011-12 Q1 2011-12 Q1 2011-12

GENERAL INFORMATION

Number of branches 134 238 157 249 10 24 13 168 124 993

Number of employees 690 3,000 2,041 2,407 168 225 88 1,263 1,235 9,882

Number of outstanding loans 159,783 689,951 392,639 515,280 33,421 55,866 19,359 382,405 281,088 2,248,704

Percent of women borrowers 64% 68% 51% 37% 56.3% 43.8% 47.2% 30.3% 50%

Average loan amount (USD) 205 165 281 149 101 127 89 108 153

Government ownership (%) 96% 25% 25% 83% 0% 0% 0% 80% 39%

BALANCE SHEET SUMMARY (USD)

Total assets 45,102,650 195,231,508 155,945,657 95,300,010 4,988,949 8,138,070 2,224,018 50,249,227 69,647,511 557,180,089

Net loans 32,240,577 111,370,377 107,504,628 75,265,986 3,294,712 6,960,469 1,685,636 36,457,709 46,847,512 374,780,093

Total deposits 10,169,317 84,499,941 57,285,914 46,255,892 1,303,928 2,041,725 629,556 18,776,723 27,620,374 220,962,995

Equity 22,845,936 56,162,898 39,625,307 25,684,725 1,993,288 2,865,126 959,121 11,454,809 20,198,901 161,591,209

9

31. In order to make the credit facility effective, PFIs will receive a mandatory, specific,

high-quality, technical assistance by a consulting firm with proven relevant international

experience to help build capacity in individual lending/financial services to female-owned/partly

female-owned MSEs before any credit is given. This capacity building will enable PFI officials

and staff to serve female MSE operators adequately - training them in assessing MSE business

proposals, individual lending provision, gender-sensitive customer care, and developing suitable

financial products for the target group. This will be done in partnership with DFID. All the cost

related to this component will be covered by DFID.

32. The TA facility will work with the PFIs in developing and executing a plan for absorbing

and applying international best practices and credit technologies. New or existing MSE finance

departments that will be set up/empowered by PFIs as a condition of their participation in the

project will be the main focus of this TA. The TA will include training PFI loan officers and the

MSE extension staff at the One Stop Shops, strengthening lending policies and procedures,

putting in place the prerequisites for the accounting, risk management and management

information systems, supporting sub-loan application preparation, screening and decision-

making, and supporting sub-loan monitoring and collections.

33. To benefit from subcomponent 1b, PFIs will be required to enter into TCA with the PMT

in DBE. Under such agreements, PFIs will receive TA free of charge for a period deemed

appropriate after the initial gap assessment for building the necessary capacity to undertake the

WEDP assignment. The PFIs will have access to the Credit Facility only if they enter into such

TCA with the PMT, since the success of the Credit Facility depends on the application of

modern MSE lending technologies, introduction of gender sensitive products and the capacity of

loan administration within PFIs.

Component 2: Entrepreneurial skills, technology and cluster development (USD

6.1million)

34. The aim of this component is to develop growth-oriented women entrepreneurs‟

skills, facilitate their access to more productive technologies that can raise their incomes, and

help unleash synergies from clustering. This will be achieved through designing and

implementing a capacity building technical assistance program to strengthen the capacity of the

institutions that will provide direct services to the WEDP participants, particularly the One Stop

Shops and TVET colleges, and the supporting/coordinating institutions such as the City MSE

Development Offices.

35. FeMSEDA will have the direct responsibility for planning, designing and

coordinating Component 2 in close collaboration with the National TVET Agency. FEMSEDA

will also have the overall responsibility for ensuring the implementation of the delivery of high

quality training and support to WEDP members along two main subcomponents; (1)

entrepreneurship training, technical skills enhancement, technology development and mentoring

and (2) cluster development.

10

36. WEDP members will have to apply for the training module(s) they see most suited

to their needs. The capacity building will aim to develop functional and relevant training

modules suitable to the needs of WEDP members seeking entrepreneurial and technical skills

enhancement. Based on individual participation, the WEDP member will be enrolled in the

module of interest if she meets the following criteria:

having sufficient numeracy and literacy skills to follow the training as determined by the provider of training

committed to focusing on business as a full-time activity, and willing to pay a commitment fee for the training.

37. FeMSEDA will coordinate with relevant implementing institutions to develop an

annual training plan for all entrepreneurship skills and technical training modules required

under WEDP. The training plan will have two components: i) Detailing the capacity building of

the implementing agencies and relevant staff (ReMSEDAs, City MSE Offices, TVET institutes

and the OSS); and ii) Detailing the training modules for the WEDP entrepreneurs. It will be

FeMSEDA‘s responsibility that necessary curricula and training material for all WEDP training

modules are developed and made available to the institutions. All staff in implementing

institutions will have to go through an orientation on the principles of private sector development

programs, the functioning of markets, demand-based approaches and the role of entrepreneurs in

economic growth of a country.

38. WEDP participants will be required to fill out feedback-forms on the relevance,

quality and usefulness of services and trainings provided throughout the program. This feedback

as well as the collection of quantitative and qualitative data (e.g. evaluation questionnaire, focus

group discussions, etc.) will enable FeMSEDA and the TVET institutions, on one side to monitor

the process and revise the support accordingly, and on the other side to identify potential social

issues and other challenges and take corrective actions.

39. Subcomponent 2a: Entrepreneurship and technology development. This subcomponent

will build capacity to ensure delivery of basic and advanced entrepreneurship training, support in

utilizing more productive technology, coaching and mentoring and business information to

growth-oriented women entrepreneurs eager to develop their entrepreneurial skills, improve the

quality of their product and services, and invest in more productive technology or access new

markets. The initial needs assessment of training and related services will be conducted by One

Stop Shops (20 in Addis Ababa and 5 for each of the other cities). A more comprehensive

training needs assessment of the entrepreneurs will be conducted by the TVETs colleges. This

will result in more specific training recommendations to the entrepreneur and in providing

feedback to the TVETs for further development of the training program to better suit the WEDP

members‘ needs.

40. The initial assessment and guidance offered in the OSS to eligible WEDP members

will enable them to select the suitable training module on offer and apply to the relevant TVET

college for WEDP training. The guidance will focus on the business idea of the entrepreneur, on

the viability of the proposed business and the potential participant will be guided on how to

develop the idea further, for example through business health checks and analysis. This process

will help eligible women with desire to grow to expand by identifying growth opportunities

11

within their existing businesses or identify new business opportunities with high potential for

growth. The result of this process will enable WEDP members to further refine their business

idea, which will be a key component for further development in several of the WEDP training

modules. WEDP members seeking training will thus have to invest time and efforts in

developing the business idea from an early stage and also chose and apply for participation in the

training program. This represents an additional mechanism to ensure that only women who are

eager to participate will actually go through the process. Applications will be on an individual

basis, and selected participants will be required to pay a nominal commitment fee.

41. The WEDP entrepreneurship skills development plan for women entrepreneurs will detail

the modules to be provided by TVET colleges to WEDP participants. All modules will combine

classroom teaching with practical workshops where participants are trained in applying the

knowledge to their own business. The full set of modules including the specific curricula and

training material will be adapted according to best international practice with the help of

consultants with appropriate expertise. The modules will likely include (i) basic entrepreneurial

skills training, (ii) advanced entrepreneurial skills training, (iii) technical training suited to

WEDP participants based on their demands, iv) training to introduce new technologies among

WEDP MSEs, (v) advisory services, including coaching and mentoring, and assistance in

business plan preparation, (vi) marketing skills training, and (vii) financial skills training.

42. Combination of services and/or training will be proposed according to the development

stage of the businesses and experience and skills of entrepreneurs (start-ups, experienced micro-

entrepreneurs, or established small enterprises). Delivery of services and training will be shaped

by the principles of relevance of the content and tailored to the needs of the target group.

FeMSEDA will investigate the demand for training from the growth-oriented female

entrepreneurs in ensuring a demand-driven development of the curricula.

43. The training will take into account the specific constraints many women entrepreneurs

face such as time, mobility and level of education. The basic business skills and entrepreneurship

training will be provided through classroom lessons and workshops with practical examples at

TVET colleges to improve their entrepreneurial, business and financial management skills.

Existing training modules used by TVETs will be reviewed and updated and adapted, and new

modules may be developed to meet the different needs of the entrepreneurs. The advanced

training will provide skills for the entrepreneurs with growing and more complex MSEs, and

could include managing financial portfolio, business financing and investment, business

expansion, laws and regulations, registration and licensing, advanced marketing, market and

profit analysis, contract management and labor management. A specific MSE business and

technology development program will be developed within the TVET colleges for addressing

challenges to using more productive and appropriate technology, address production capacity

constraints and quality/standard issues of products and services of MSEs. This will be designed

so as to cater to the needs of the target group as separate from the high school graduates entering

the TVET training colleges.

44. After completing a training module, entrepreneurs will be required to provide a one page

‗action plan‘ that specifies how the knowledge provided will be implemented in her business.

This will both serve to ensure a practical focus of the training and provide feedback to

12

facilitators/trainers whether the entrepreneur was able to understand the content in a useful way.

This would also serve as basis for further advice and coaching purposes.

45. Women entrepreneurs will also be provided with business advice services in OSS on

demand in order to deal with specific business challenges. This service could include basic

support, such as filling in loan applications, how to assess market prices or identifying sources of

supply of inputs. Market studies will be conducted in the localities to identify high potential

businesses ideas in subsectors and to provide up-to-date, relevant and reliable market

information to serve as pointers for the women enterprises. Information resulting from the

different market studies will support the OSS staff in orienting women entrepreneurs towards

specific business opportunities in different sectors and sub-sectors suitable to the WEDP

members. Complemented by the TVET training, these services will be geared towards

supporting the women MSEs to respond to the existing demand – or stimulating the potential

demand.

46. City MSE Offices and ReMSEDAs will, in conjunction with women entrepreneurs

associations, chambers of commerce and other relevant private institutions, organize events to

promote mentoring arrangements and linkages between entrepreneurs. The private institutions

can identify experienced entrepreneurs who would volunteer to mentor or coach WEDP

members on a regular basis, and co-organize the events to let the women MSEs link with the

resource persons on a mutually agreed basis. Mentors and coaches will go through a basic

orientation on aims and responsibilities. Women entrepreneurs associations, chambers of

commerce and other business associations will be encouraged to create space for networking and

to develop linkages between WEDP participants and other successful entrepreneurs to share

information and experiences.

47. All personnel in the OSSs selected for WEDP will be required to take a course with

topics on competition, markets, doing business and the role of public support to the private

sector. The aim is to create a change in mindset towards an appreciation of demand driven

approaches and an understanding of the benefits of stimulating competition. Moreover, the role

of private initiative and entrepreneurship in growing businesses will be elaborated. This training

will also include customer care, communication, net working and information management to

enable OSS staff to play the key role of entry point for women entrepreneurs seeking information

and advice and enable them to respond to changing demands in a changing environment.

48. In addition to support for skill development, some upgrading of the OSS offices will be

included. This will serve a double purpose: A welcoming and user friendly environment will be

more attractive for users as well as for personnel, and an upgrade in the OSS equipment

(including transport and informational technology) will represent an additional incentive for the

personnel, in order to mitigate the high turn-over in these institutions.

49. Subcomponent 2b: Cluster Development. WEDP will support cluster development

according to international best practice and in a way that spurs income and employment growth

for female owned/partly female-owned MSEs. Industrial clusters are the concentration of

economic activities of a certain sector in a certain location producing similar and closely related

goods. Industrial clusters provide a wide range of advantages that enable enterprises become

13

competitive and profitable. These advantages could be generated either through unplanned

positive externalities such as industry specialization, labor pooling, and knowledge spillovers or

through deliberate joint actions. Such joint actions may include bulk purchase and storage of raw

materials, combined marketing campaign, joint advertising, joint purchase and hiring of

equipment, joint lobbying of local authorities, joint application of credit, etc. Joint actions in

clusters do not emerge automatically and require efforts for the identification and achievement of

shared goals and depend on the gradual process of trust building and coordination.

50. WEDP will support natural clusters within the chosen sectors mainly through facilitating

market linkages and technology transfer and inducing network and joint actions among

entrepreneurs in order to help boost their collective power and innovate their ways of doing

business. The approach will be based on the lessons learned from the UNIDO cluster

development program for MSEs implemented in four natural clusters in Ethiopia from 2005 until

2009. A key principle was to train agents who operate as impartial facilitators among cluster

actors and help them share information and coordinate their endeavors. These facilitators known

as cluster development agents (CDAs) worked on a daily basis in a specific cluster supporting all

stages of technical assistance starting from the formulation of a diagnostic study that help

identify core problems faced in the cluster, to organizing and coordinating collective activities,

promoting and coaching business networks, facilitating linkages with input suppliers, designers,

training institutions and medium and large scale firm, in order to solve the identified problems.

51. It will be the City MSE Development offices in each of the 6 target cities that assess and

identify natural clusters with potential (as identified in the project development objective, see

paragraph 13 above) for WEDP support in their city. The City MSE Office will select natural

cluster(s) that is to be supported under WEDP based on the following criteria:

- natural clusters in the priority sectors selected by the government.

- natural clusters that have potential for rapid growth and employment generation.

- clusters where a good proportion of the members are women and/or sectors where a

lot of women operate in and can potentially be supported as a cluster (like pottery,

spinning, bamboo crafting and food processing).

- clusters that are accessible to various supporting institutions and operate in areas that

have appropriate infrastructure.

52. The cluster training program will be based on the need assessment of the potentially

growth-oriented clusters to be supported under WEDP based on the criteria mentioned above,

and will also include a program for training the CDAs. Mapping of existing clusters and

identification of the various stakeholders and partners that can contribute to the clusters‘

development will be conducted such as input suppliers, output buyers and sectoral associations.

53. The core problems in each cluster will be identified through a diagnostic study and a

work plan will be formulated in order to solve these problems through networking and joint

actions. This will be done by the CDAs, who are staff members of the OSS. Among the various

facilitators working at the OSS, potential candidates will be identified as CDAs by City MSE

Office. The selection of the CDA at the OSS will be based on his/her commitment for intense

pro-active interaction with all local players and institutional partners and flexibility to deal with

various administrative bodies in mobilizing their support for the cluster.

14

54. The training module for CDAs will include the specifics of cluster development, conflict

management and resolution, gender issues, network building and project management and

evaluation. The CDA training will be managed by FEMSEDA and conducted by a qualified

institution or consultant in collaboration with FeMSEDA in-house CDA expertise. Moreover, the

training will provide guidelines on how to best support women entrepreneurs across the value

chain in clusters without jeopardizing the existing forward and backward linkages and networks

with the existing male entrepreneurs in the cluster.

Component 3: Project Management, advocacy and outreach, Monitoring & Evaluation

and Impact Evaluation (USD 1.5 million)

55. Subcomponent 3a Project Management Team (USD 0.35 million) will establish a

National Project Management Team (NPMT) within FeMSEDA under the Ministry of Urban

Development and Construction (MoUDC). The operational responsibility for the project

implementation in the regions will rest with the City Offices, MFIs and TVET colleges using

OSS as the entry point. The existing federal coordinating body for MSE development, the

National MSE Development Council, will be supplemented with representatives of the Chamber

of Commerce and Sectoral Association and the Ethiopian Women Entrepreneurs Association and

will have the overall coordinating role of the WEDP. This will ensure coordination and support

from the multiple sectors involved in the project.

56. Subcomponent 3b Communication, advocacy and outreach (USD 0.35 million) will build

awareness; expand the outreach and understanding and acceptance of WEDP among (1) the

beneficiaries and (2) relevant stakeholders, especially the husbands of the participants who will

receive a tailored information package to ensure consent. Potential WEDP participants will be

given detailed and thorough information about the different components of the program and the

respective application and selection procedures, the aims and the requirements of participants. It

will ensure that the objectives of the project as well as the methods for attaining them are clearly

understood and help increase political and social commitment and contribute to the development

objective of the project. This will be achieved through information workshops, trainings to

federal, regional and woreda level implementers and will include preparation and publication of

materials aimed at raising entrepreneurship awareness.

57. This subcomponent will ensure public access to information to make transparency a

foundation of WEDP. Information about the project components, procedures, complaint

mechanisms, processes (especially criteria for selecting participants) and the role and

responsibilities of each stakeholders will be publicly available at all levels. Microfinance

application procedures, entrepreneurial skills development opportunities, means of benefiting

from the technology and product development processes would be made clear using various

channels including meetings, broadcast through public media such as newspapers, mobile

phones, radio and TV.

58. In addition, this subcomponent will document and disseminate results, lessons learned

and good practices. Successful beneficiaries will be recognized and promoted by publicizing

15

their achievements and contributions to the development process and poverty reduction.

Beneficiary testimonials and other channels will be used to spread success stories, document and

disseminate good practices and lessons learned. Showcasing examples of successful

collaborations between government officials, MFIs, project beneficiaries and other relevant

stakeholders will be used to strengthen partnerships and build strategic alliances among

stakeholders. In addition, it will help build a dynamic and evolving knowledge base to improve

the quality of the project activities.

59. Subcomponent 3c Monitoring & Evaluation (USD 0.3 million): The NPMT will be

responsible for developing and establishing a suitable monitoring and evaluation (M&E) system

to accurately track and assess the progress of WEDP implementation. This includes the

identification of mechanisms and methodologies to continuously benchmark the main inputs and

outputs as well as to measure outcomes on the basis of the objectives and targets specified in the

sections above. In addition, the M&E system will prepare and disseminate quarterly reports as

well as meaningful feedback to the NPMT on the advancement of the activities within the scope

of the project and in compliance with the guidelines and procedures developed in the PIM.10

The

WEDP implementing institutions that will collect data and report progress for the WEDP M&E

system will assign direct responsibility for these tasks to staff with adequate competencies to

ensure the fulfillment of all reporting requirements.

60. The NPMT will contract a highly qualified consultant with documented relevant

experience to development a turn-key WEDP M&E system including the design of required

informational channels based on the processes and procedures that will be outlined in the PIM.

This consultancy will also detail the responsibilities of implementing agencies for accurate and

timely reporting. Although the data collection and reporting on WEDP will be based on the

existing structures and FeMSEDA's own M&E system, the consultant will be required to

highlight selective but necessary additions and adoptions in order to provide the full overview of

WEDP activities and progress in a coherent manner. This may also include the development or

alignment of reporting templates. Issuing WEDP membership in the OSS will provide the

foundation for tracking relevant activities of WEDP entrepreneurs. The consultant will be asked

to provide recommendations on how to integrate data collected by all implementing institutions,

namely FeMSEDA, TVET colleges, OSSs and PFIs in order to create a single comprehensive

database capturing all WEDP activities on participant/member level. This task includes the

identification of a suitable place within the organizational M&E structure of FeMSEDA for

placing this database.

61. The PFIs will not be asked to change their internal M&E systems or reporting practices.

However, the PFIs will be required to commit to detailed reporting standards as a prerequisite for

participating in the WEDP line of credit. PFIs will report necessary WEDP information to the

PMT at the DBE, which in turn submits aggregated and systematized information to FeMSEDA.

The DBE PMT will submit various progress reports, the format and required periodicity of

which will be included in the Operations Manual, including output and outcome indicators (six-

monthly) and financial management reports (FMRs) (quarterly).. The information required from

the PFIs will include but not be restricted to the results indicators. The performance and

implementation progress of Component 1 will be monitored through several indicators, in line

10

The PIM will be updated based on the recommendations of the M&E consultancy.

16

with the World Bank Micro, Small and Medium Enterprise (MSME) Finance core sector

indicators: (1) Direct project beneficiaries (borrowers); (2) volume of bank funding: lines of

credit; (3) volume of bank funding: institutional development; (4) outstanding SME loan

portfolio; (5) number of active loan accounts; (6) portfolio at risk; (7) number of PFIs that have

adopted and implemented institution development plans and project-related credit technologies

and (8) number of trained loan officers. The World Bank team will be working with the DBE

PMT and the consultants to design the required reporting templates in the Operations Manual,

and to ensure that the PFIs are well accustomed to collecting such information from their clients.

The financial performance of the PFIs will be monitored through independent auditors‘ reports

and separate letters confirming adherence to prudential norms. PFIs will be required to provide

the relevant data to the project management.

62. The initial TA provided to the PFIs will ensure that the institutions are well accustomed

to collecting the necessary information from their clients and to aggregate the data in order to

compute the specified indicators. Similarly, TVET is already collecting all necessary information

for the computation of the relevant results indicators, namely (1) number of direct project

beneficiaries (trainees) and (2) percentage of trainees passing the end-of-training competency

test. Additional reporting requirements and monitoring indicators are planned to be specified by

the M&E consultant.

63. Subcomponent 3d: Impact Evaluation (USD 0.5 million): Making impact evaluation an

integral part of the WEDP reflects the desire expressed by stakeholders to systematically

investigate the effectiveness of the project. Such analysis will not only allow for a

comprehensive stocktaking and review of the project's achievements but it will also help to

identify the underlying mechanisms and constraints affecting its mode of functioning.

64. The analysis will be based to a large extent on the quantitative comparison of a treatment

group with an adequate control group. By definition, access to all or a specific subset of the

project components is given to the treatment group only. It is crucial, however, to tailor the

selection of the treatment and the control group to the intervention. This exercise is key to

guarantee statistical identification of changes that can be causally linked to the intervention. The

main challenge will lie in identifying project features that offer the potential to select a control

group sufficiently suitable to allow for the envisaged analysis. Such features include but are not

restricted to capacity constraints, phase-in stages, treatment status randomization and cut-off

rules.

65. The empirical analysis will mainly build on survey data deliberately collected for this

purpose: (1) a base-line survey which will be carried out prior to respondents' exposure to any

relevant intervention activities; (2) an end-line survey which will be administered after the

project has been well into operation and (3) conditional on sufficient implementation a mid-term

survey. The information will be collected from representatives of both the treatment group as

well as the control group. While the empirical analysis will be carried out by impact evaluation

experts from the World Bank, the data collection will necessarily be contracted out to an

organization/firm with extensive experience and capacity in the administration of large-scale

surveys. In addition, an effort will be made to integrate other data sources such as the

administrative records compiled through the M&E system at the OSS, TVET and PFI level.

17

66. Primarily, WEDP is designed to allow participating women to materialize their

entrepreneurial potential through access to microfinance and skills development. The main focus

of the impact assessment will be on standard business performance measures such as sales,

profit, investment and employment which are closely connected to the PDO. Nevertheless, the

impact evaluation offers the opportunity to broaden the outcome space such that additional and

potentially important determinants of the well-being of female entrepreneurs can be analyzed as

well. Typically, these determinants lie outside the scope of customary M&E systems and may

include indicators for intra-household bargaining power and decision-making, expectations and

aspirations.

67. Although the empirical research methodology described above will be at the core of the

impact evaluation component, complementary quantitative or qualitative studies may be

conducted selectively in order to investigate project components or features that are identified as

having decisive influence on the impact of WEDP. Primarily, these studies are planned to be

carried out by highly qualified consultants. The research focus of this component will, however,

further expand to potential pilot interventions within WEDP. Conditional on the suitability of

such interventions for carrying out sound impact evaluation, the aim will be to identify

innovative mechanisms through which female entrepreneurs can be supported. Examples for

such pilot interventions explicitly designed as trials may include compulsory training courses,

training with sole focus on innovation like with business idea competitions and crèches/nurseries

offered to full-time female entrepreneurs.

68. The key performance indicators for the project and its components are listed in the

Results Framework Annex 1. The details of the M&E system and the list of indicators to be

collected will be included in the M&E module of the PIM.

B. Project Financing

Lending Instrument

69. Specific Investment Lending (SIL): Although a significant amount of the loan proceeds