Office of Legislative Audits Update ASBO Conference May 2014

Office of Legislative Audits Update ASBO Conference May 2014.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Office of Legislative AuditsUpdate

ASBO Conference May 2014

Objective 1

Differences Between

Round One and Round Two Audits

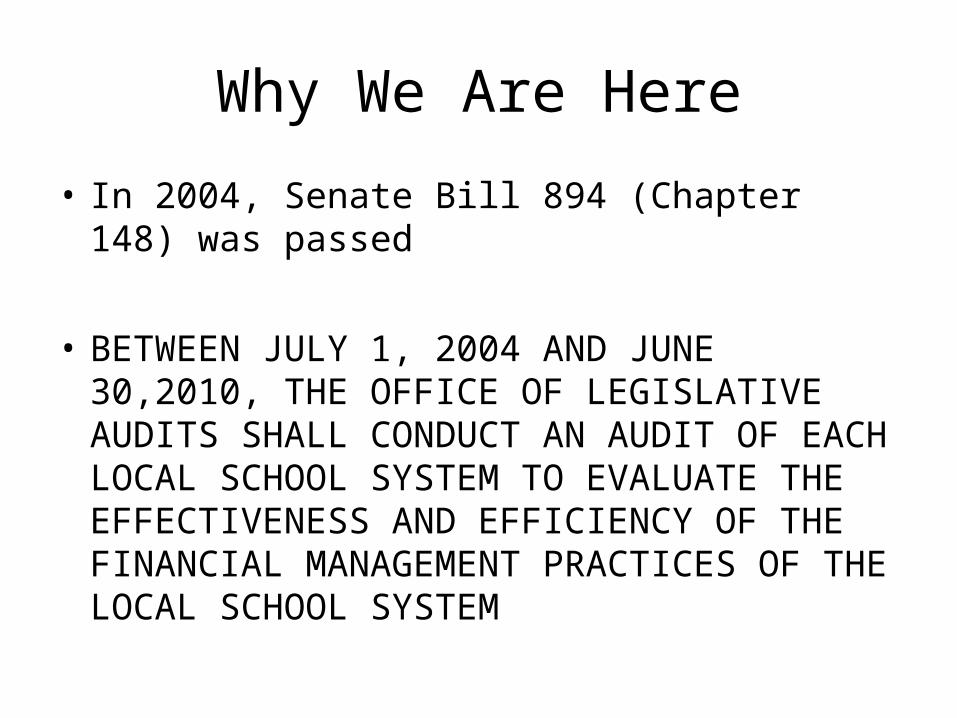

Why We Are Here

• In 2004, Senate Bill 894 (Chapter 148) was passed

• BETWEEN JULY 1, 2004 AND JUNE 30,2010, THE OFFICE OF LEGISLATIVE AUDITS SHALL CONDUCT AN AUDIT OF EACH LOCAL SCHOOL SYSTEM TO EVALUATE THE EFFECTIVENESS AND EFFICIENCY OF THE FINANCIAL MANAGEMENT PRACTICES OF THE LOCAL SCHOOL SYSTEM

Audit Procedures

• SECTION 5. AND BE IT FURTHER ENACTED, That 45 days prior to the initiation of the first financial management practices audit required by this Act, the Office of Legislative Audits shall submit the scope, measurements, and process the Office plans to use in conducting the required audits to the Joint Audit Committee for approval

Audit Procedures

• As required by the Law, we developed the procedures.

• 11 Chapters

• Joint Audit Committee directed that we perform all procedures at all LEAs

2010 Legislation

• Senate Bill 58 (Chapter 58)• [Between July 1, 2004 and June 30, 2010,] AT

LEAST ONCE EVERY 6 YEARS, the Office of Legislative Audits shall conduct an audit of each local school system to evaluate the effectiveness and efficiency of the financial management practices of the local school system.

Differences Between Rounds 1 and 2

• OLA is no longer required to perform all steps in the procedures approved by the JAC

• We use professional judgment in selecting what procedures to perform

• We consider materiality and risk• More of an impact at the small LEAs

Round 2 Completed Audits

• Allegany• Anne Arundel• Baltimore City• Carroll• Frederick• Kent• Prince George’s

Round 2 Completed Audits

• Queen Anne’s• Somerset• Talbot• Washington• Wicomico

Round 2 Audits In Progress

• Baltimore County• Harford County• St. Mary’s County

F/Y 15 Audits

• Calvert - Summer 2014• Howard – Fall 2014• Montgomery – Winter 2015• Cecil – Winter 2015• Caroline – Winter 2015

Planned F/Y 16 Audits

• Charles• Dorchester• Garrett• Worcester

Objective 2

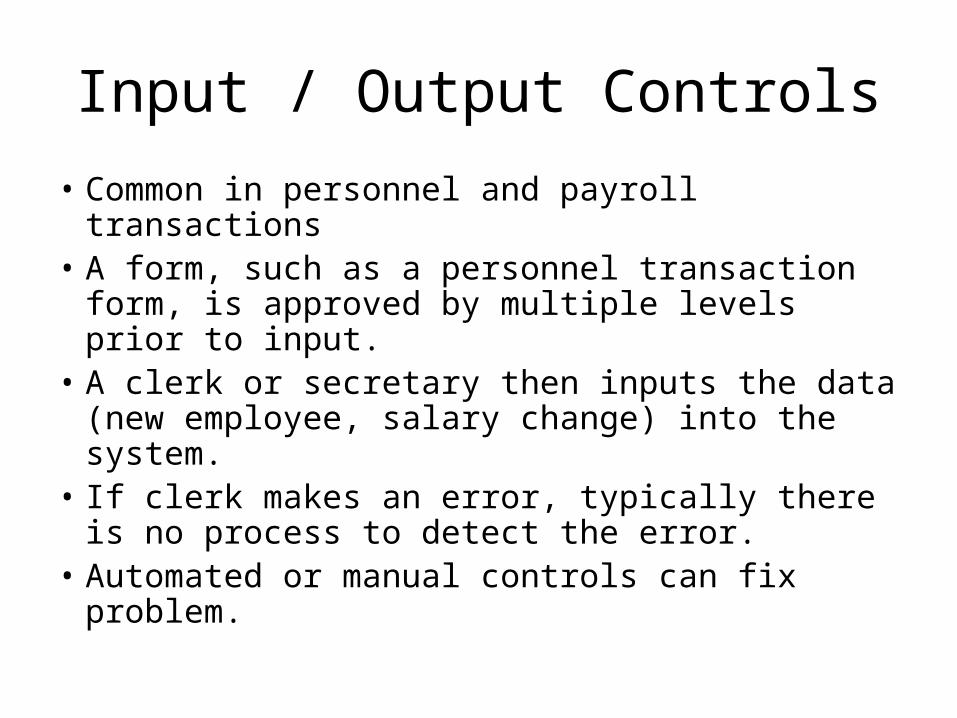

Input / Output Controls

• Common in personnel and payroll transactions• A form, such as a personnel transaction form, is

approved by multiple levels prior to input.• A clerk or secretary then inputs the data (new

employee, salary change) into the system. • If clerk makes an error, typically there is no

process to detect the error. • Automated or manual controls can fix problem.

Access to Critical Files

• At many LEAs, an excessive number of employees have the ability to change critical files.

• If the employee rarely processes changes to the files, we generally deem access unnecessary.

• Even if controls over changes are adequate, this could still be an exception.

• Employee access should be periodically reviewed.

Procurement Policies

• Policies are sometimes not comprehensive in that they do not address services or specify when school boards should approve contracts.

• This is not a compliance issue.• When goods or services are available from

more than one source, competitive procurements should be used.

• Bids not always obtained

TransportationVerification of Manifests

• At some LEAs, bus contractor manifests are accepted with no verification.

• Where data exists, OLA has seen overpayments to the contractors.

• GPS is ideal for monitoring and verification, but may be too expensive.

• Some LEAs tell the contractors the route mileage and time.

• Internet maps or ride alongs could be used for verifications.

Transportation Basis for Contractor Rates

• Many LEAs lack a sound basis for rates used to determine bus contractor pay. Mainly PVA and maintenance.

• Comparison with other LEAs is not necessarily valid.

• PVA includes a return on investment and should consider market interest rates.

• Processes for determining amounts paid to bus contractors should be in writing and explained to Board.

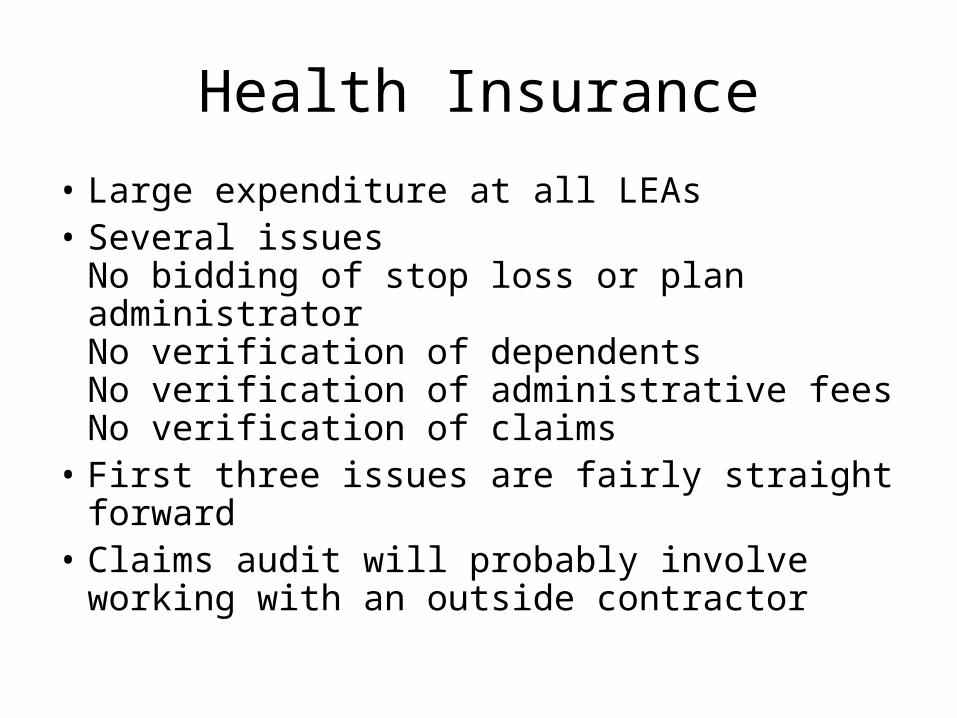

Health Insurance

• Large expenditure at all LEAs• Several issues

No bidding of stop loss or plan administratorNo verification of dependentsNo verification of administrative feesNo verification of claims

• First three issues are fairly straight forward• Claims audit will probably involve working

with an outside contractor

Objective 3

• Lessons learned on other OLA audits that may be applicable to LEA audits.

• For example, Level 3 (L3) credit card data:

CPC Audit Report

http://www.ola.state.md.us/Reports/Performance/CPC14.pdf

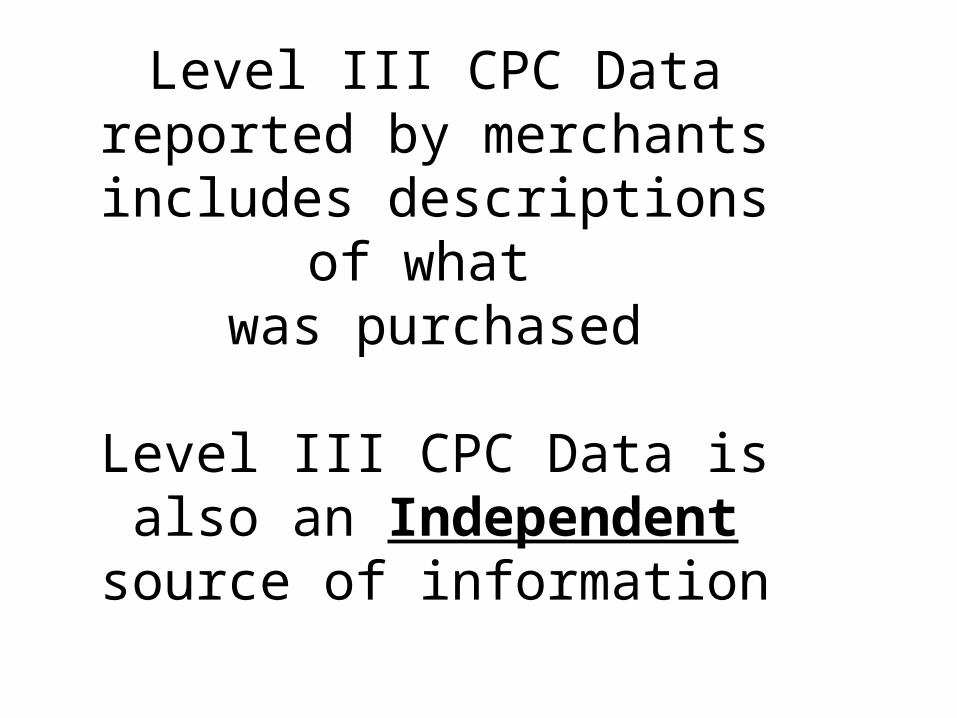

Level III CPC Datareported by merchants

includes descriptions of what was purchased

Level III CPC Data is also an Independent source of

information

Related Documents