1 Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER OESA AUTOMOTIVE SUPPLIER BAROMETER Q3 2019 SUPPLY CHAIN & GLOBALIZATION

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

OESA AUTOMOTIVE SUPPLIER BAROMETERQ3 2019

SUPPLY CHAIN & GLOBALIZATION

2Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

Executive Summary

Supplier Barometer Index (SBI)

SBI Score = 37;

up 2 points from Q2

Despite a modest gain, the outlook

remains deep in negative territory, 13

points below the neutral threshold of

50, remaining near the lowest levels

since 2009. Continued trade tensions

and poor vehicle sales of programs

supplied weigh on the outlook of

supplier executives across firms of all

sizes, with larger suppliers reflecting

greater pessimism.

Trade policy is identified as the

greatest industry threat, followed

by the impact of weak demand of

programs supplied.

Trade policy remains the greatest

industry threat within a dynamic

environment. As progress is being

made on USMCA, threats remain

including proposed 232 tariffs on

autos and auto parts and others.

Net profitability is deteriorating

across a wide range of system

areas and program segments

Growing margins are only reflected

for electrical/electronics systems

that support SUV and truck

programs.

Margins for products that support

car programs show the greatest

level of decline.

Tariffs along with higher labor rates,

material prices and interest rates

are raising supplier cost pressures.

U.S. is the regional leader

in N.A. production with

expected growth in U.S.

and Mexico

For supplier products

produced in North America,

respondents expect growth in

U.S. and Mexico.

Surveyed supplier

import/export balance is

skewed

As a median value, 10% of

current U.S. production is

exported outside of the U.S.

while 30% of material (on a

dollar basis) needed for

production is purchased

outside of the U.S.

Most exports are sent to

Mexico, Canada and Europe.

The rate of exports is

increasing to Mexico and Asia

excluding China.

3Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

Executive Summary

Most suppliers anticipate supply chain rationalization

14% of respondent companies have a direct supply base that is too

large. Given that, a 13% average reduction in the number of their

direct suppliers is planned by those companies.

17% of respondent companies have an indirect supply base that is

too large with an equal percentage reduction planned for.

One of the primary causal factors in supply chain

concerns is timing issues

Respondents indicate that timing issues and quality concerns

are not only the most likely scenarios that would disrupt their

supply chains but would also have the most severe impact on

their business.

Labor issues and shortages of raw materials and/or

components are also of great concern.

Risks associated with meeting customer production

requirements:

Supply Chain Risks are timing or delay related, quality and a

rising trend of financial distress within the supply base.

Internal production risks are lead times, labor issues and

launch related issues.

The supply base remains healthy on average, yet weak

financial metrics are a key contributor to rising quality issues.

On average, 17% of company suppliers are

directed buy as required by customers, down

from 20% last year

Increasing risk with “watch list” direct suppliers

On average, respondents include 3.4% of their direct suppliers on

internal company “watch lists” up from 3.0% last year.

Quality and financial metrics were the primary reasons for direct

suppliers being added to or continuing on the “watch list”.

Sourcing constraints for electrical/electronics and

powertrain systems are at the highest risk

Survey participants indicate sourcing constraints are impacted

by trade policy uncertainty as customers delay decisions.

Suppliers are cautious to make new capital investments.

4Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SUPPLIER OUTLOOK

5Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

37

20

30

40

50

60

70

80

Ja

n-2

009

Ja

n-2

010

Ja

n-2

011

Ja

n-2

012

Ja

n-2

013

Ja

n-2

014

Ja

n-2

015

Ja

n-2

016

Ja

n-2

017

Ja

n-2

018

Ja

n-2

019

Euro

Crisis

Begins

Japan

Tsunami/

Grexit Crisis

US

Fiscal

Cliff

Lehman

Collapse

0%

20%

40%

60%

80%

Sig

nific

an

tly m

ore

optim

istic

So

mew

ha

t m

ore

optim

istic

Un

ch

ang

ed

So

mew

ha

t m

ore

pessim

istic

Sig

nific

an

tly m

ore

pessim

istic

Q2 2019 Q3 2019

293 responses

Describe the general twelve month outlook for your business. Over the past three months, has your opinion become…?

Current Supplier Outlook (Share of Respondents) Supplier Barometer Index: (SBI and 6m Average)

SBI Score = 37; increased 2 points from Q2, but remains deep in negative territory on

continued trade tensions, poor sales of programs supplied and weakness in the U.S. economy

OESA Supplier Barometer: Q3 2019 Results

US Tax

Reform

6Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

>$1

billion

7%17%

11%17%

24%

6% 9%14% 14%

6% 8%

33% 33% 42%36%

24%

36% 21%31%

21%23%

50% 44%42% 39%

71%51%

57%

56%

68% 62%

4%4% 7% 6% 7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Significantly more pessimistic

Somewhat more pessimistic

Unchanged

Somewhat more optimistic

Significantly more optimistic

41.7 43.5 43.8 46.2 33.8 37.2 35.7 39.6 31.6 33.3

<$50

million$50-$150

million

$501 million –

$1 billion

Quarterly

SBI ∆

$151-$500

million

Regardless of revenue size, responses continue to reflect a high level of pessimism;

Smaller firms were slightly more optimistic in comparison to larger size firms, but remain pessimistic on net

OESA Supplier Barometer: Q3 2019 Results By Revenue

Describe the general twelve month outlook for your business. Over the past three months, has your opinion become..?

May July May July May July May July May July

7Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Changes in government trade policy

Poor sales of vehicles in programs supplied

Weakness in the U.S. Economy

Implementation of new government regulations

Likelihood of higher interest rates

Inability to address internal labor constraints

Terrorism or some type of international event

Inability to fulfill customer volumes

1=Greatest threat 2 3 4 5 6 7 8 9 10=Smallest threat

Average

Rating

3.4

4.2

4.6

5.4

6.2

6.3

7.2

7.4

2.9

3.9

4.4

5.4

6.0

5.5

6.7

7.4

MayJuly

Trade policy remains the greatest industry threat, at 3.4 in the third quarter, up slightly from Q2

Poor sales of programs supplied was identified as the second largest threat at 4.2

OESA Supplier Barometer: Industry Threats

What are the greatest threats to the industry over the next 12 months?

8Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

Increased Profitability Unchanged Decreased Profitability

Net profitability is deteriorating across nearly all system areas and program segments;

Net profitability increased for electrical/electronics for SUV and Truck programs

OESA Supplier Barometer: Industry ProfitabilityFor each of the following system areas, please indicate the direction of profit margins.

Powertrain

Chassis

Exterior

Interior/HVAC

Electrical/Electronics

-0.48

-0.46

-0.42

-0.36

-0.21

-0.13

-0.14

-0.16

-0.07

0.07

-0.11

-0.13

-0.16

-0.13

0.09

-0.29

-0.31

-0.27

-0.15

-0.04

Passenger car programs SUV programs Truck programs Overall*Net

Profitability

*Net

Profitability

*Net

Profitability

*Net

Profitability

0% 50% 100% 0% 50% 100% 0% 50% 100% 0% 50% 100%

*Net profitability is a weighted average where increased profitability = 1,

unchanged = 0, and decreased profitability = -1

9Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

GLOBALIZATION

10Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

5770

6

6

3724

0%

20%

40%

60%

80%

100%

2019 2018

United States Canada Mexico

For your products produced in North America,

identify the percent manufactured in each of the

following countries.

How do you expect that these percentages will

change over the next 5 years?

8%

35%

10%

44%

36%

74%

35%

23%

14%

13%

0% 20% 40% 60% 80% 100%

United States

Canada

Mexico

Significant Increase Some Increase No Change

Some Decrease Significant Decrease

North American ProductionU.S. leads North American production and is expected to grow along with Mexico

11Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SourcingCustomer and supplier sourcing localization continued to increase in 2019

4%

6%

3%

24%

31%

24%

19%

28%

29%

21%

21%

39%

31%

47%

59%

0% 20% 40% 60% 80% 100%

2019

2018

2019

2018

Extensive Increase Moderate Increase Minimal Increase No Change

Minimal Decrease Moderate Decrease Extensive Decrease

... pursue with your suppliers?

... see from your customers?

Over the past year, what level of manufacturing localization activity/effort did you...

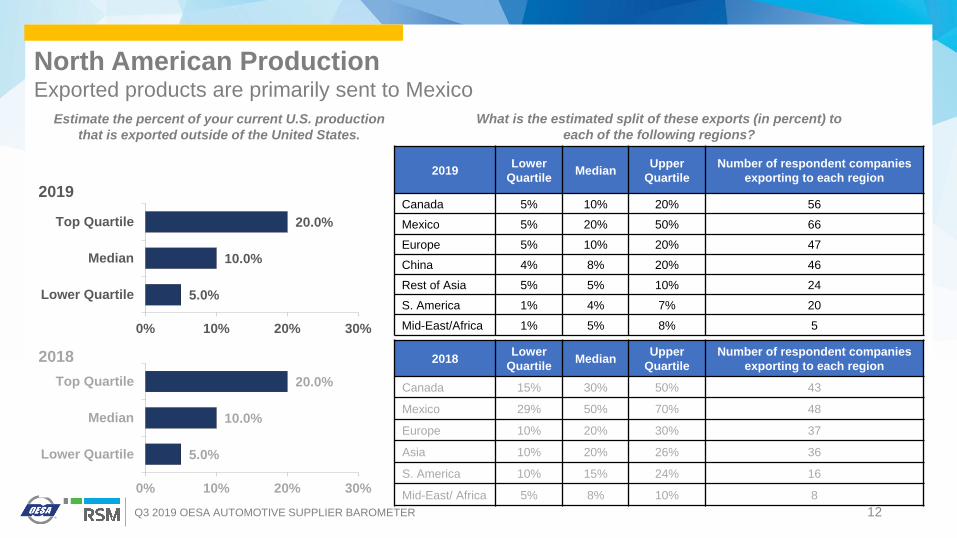

12Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

2019Lower

QuartileMedian

Upper

Quartile

Number of respondent companies

exporting to each region

Canada 5% 10% 20% 56

Mexico 5% 20% 50% 66

Europe 5% 10% 20% 47

China 4% 8% 20% 46

Rest of Asia 5% 5% 10% 24

S. America 1% 4% 7% 20

Mid-East/Africa 1% 5% 8% 5

5.0%

10.0%

20.0%

0% 10% 20% 30%

Lower Quartile

Median

Top Quartile

Estimate the percent of your current U.S. production

that is exported outside of the United States.

What is the estimated split of these exports (in percent) to

each of the following regions?

5.0%

10.0%

20.0%

0% 10% 20% 30%

Lower Quartile

Median

Top Quartile

2018

2019

2018Lower

QuartileMedian

Upper

Quartile

Number of respondent companies

exporting to each region

Canada 15% 30% 50% 43

Mexico 29% 50% 70% 48

Europe 10% 20% 30% 37

Asia 10% 20% 26% 36

S. America 10% 15% 24% 16

Mid-East/ Africa 5% 8% 10% 8

North American ProductionExported products are primarily sent to Mexico

13Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

For each region, please describe the direction of

your export plan over the next 5 years.

36%

17%

15%

15%

8%

7%

58%

72%

80%

85%

74%

89%

92%

6%

11%

18%

0% 20% 40% 60% 80% 100%

Mexico

China

Europe

Rest of Asia

Canada

South America

MidEast/Africa

Increasing No Change Decreasing2018

2019

28%

25%

11%

10%

7%

63%

63%

80%

80%

78%

93%

9%

12%

9%

10%

16%

Mexico

Asia

S. America

Europe

Canada

Mid-East/Africa

What major factors drive this regional export plan?

Canada

• Lower demand for cars is driving lower shipments.

• GM plant shutdowns.

• OEM Reductions.

Mexico

• Focused on utilizing local production for facilities in

Mexico for Mexico market.

• Supplementing Mexico facility with US plant capabilities.

Europe • OEM global vehicles.

China• Moving south.

• New program increasing this customer destination.

Rest of

Asia

• OEM global vehicles.

• Tooling capacity.

S. America • OEM global vehicles.

Mid-East/

Africa• No comments provided

SourcingThe majority of U.S. exports are planned for Mexico and China, with less exports to Canada

14Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

What is the regional split of your total (by dollar value) of

materials/components purchased for U.S. production?

20.0%

30.0%

50.0%

0% 20% 40% 60%

Lower Quartile

Median

Top Quartile

Estimate the percent of your current material costs for

U.S. production (by dollar value) that is purchased

outside of the United States.

20.0%

45.0%

55.0%

0% 20% 40% 60%

Lower Quartile

Median

Top Quartile

2018

2019

U.S. Production ImportsImbalance between imports and exports

2019Lower

QuartileMedian

Upper

Quartile

Number of respondent companies

exporting to each region

Canada 5% 5% 15% 39

Mexico 10% 20% 40% 51

Europe 5% 10% 17% 50

China 10% 23% 40% 56

Rest of Asia 5% 13% 22% 29

S. America 1% 10% 15% 7

Mid-East/Africa 6% 25% 48% 4

2018Lower

QuartileMedian

Upper

Quartile

Number of respondent companies

exporting to each region

Canada 5% 10% 25% 33

Mexico 10% 25% 40% 33

Europe 5% 7% 20% 35

Asia 14% 35% 60% 48

S. America 9% 10% 15% 4

Mid-East/Africa 13% 23% 44% 4

15Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

2018

2019

19%

13%

74%

79%

75%

82%

100%

100%

7%

8%

20%

16%

Mexico

Asia

Europe

S. America

Mid-East/Africa

Canada

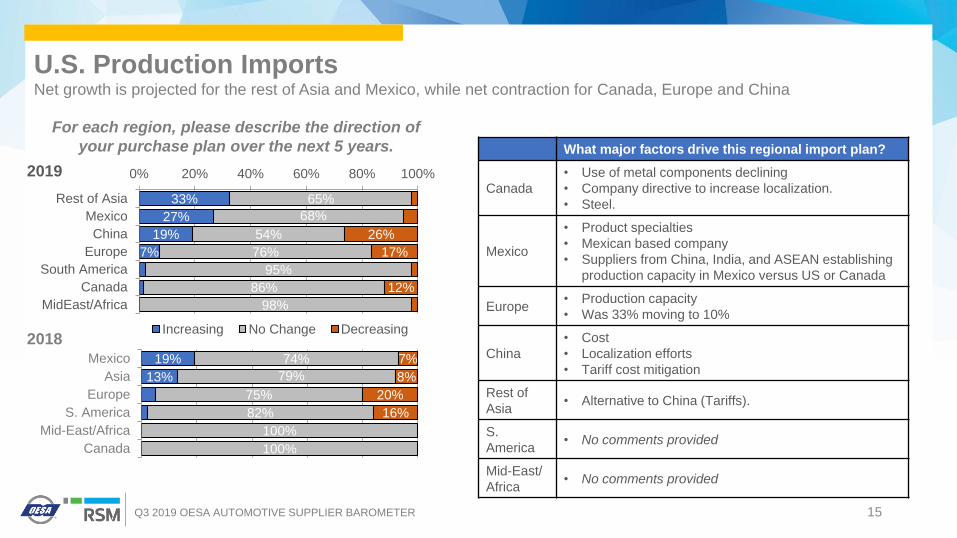

What major factors drive this regional import plan?

Canada

• Use of metal components declining

• Company directive to increase localization.

• Steel.

Mexico

• Product specialties

• Mexican based company

• Suppliers from China, India, and ASEAN establishing

production capacity in Mexico versus US or Canada

Europe• Production capacity

• Was 33% moving to 10%

China

• Cost

• Localization efforts

• Tariff cost mitigation

Rest of

Asia• Alternative to China (Tariffs).

S.

America• No comments provided

Mid-East/

Africa• No comments provided

33%

27%

19%

7%

65%

68%

54%

76%

95%

86%

98%

26%

17%

12%

0% 20% 40% 60% 80% 100%

Rest of Asia

Mexico

China

Europe

South America

Canada

MidEast/Africa

Increasing No Change Decreasing

For each region, please describe the direction of

your purchase plan over the next 5 years.

U.S. Production ImportsNet growth is projected for the rest of Asia and Mexico, while net contraction for Canada, Europe and China

16Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SUPPLY CHAIN

17Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

3415%

13963%

3315%

167%

NA capacity expansion will occur

NA capacity rationalization will occur

NA production constraints will occur

None of these

How do you see North American supply chain capacity changing over the next year?

Comments (Selected):

• Expansion into new vehicle architecture; Rationalization of traditional manufacturing

• Troubled suppliers are already starting to be identified.

• There is more focus on localizing NA production leading to a requirement to expand NA capacity. This is coupled with

a decrease in customer demands over the next 12 months.

• Capacity planning based upon market trends verses customer projected volumes.

• Impact of tariff policy

• Any of these outcomes are equally possible, hence the uncertainty to make investments.

• With the reduction of car assembly there will be a rationalization of these types of plants.

• The use of digital technology in the Tier-1 operations is evolving from volume driven OEM programs to respond more

quickly to more trim levels with high speed flexibility.

• Suppliers will work to ensure proper capacity and breakeven points, so will likely avoid over-capacity and actually

remove excess capacity.

• Much business moving back from Asia (in particular) to North America.

• As a result of the 301 tariffs, we are moving production to Europe, not North America.

• I think companies will wait and see what happens with China tariffs and USMCA before making decisions.

• Electric car maker entrants and Chinese entrants will complicate the picture for overall capacity, but will negatively

impact many existing participants.

• I believe we'll see companies fold due to poor quote assumptions and losing money on high volume.

• Volumes decline and we have too much capacity.

• Due to Section 403 in NAFTA goes away

• High amount of capacity in the market currently drive profitability down

• I feel we will have open capacity that will need to be filled.

CapacityRationalization is anticipated

18Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

12% 12%5%

71% 75%

66%

17% 12%

29%

0%

20%

40%

60%

80%

100%

2019 2018 2017

Too Small Appropriately Sized Too Large

23% 18%26%

64% 68% 58%

14% 13% 16%

0%

20%

40%

60%

80%

100%

2019 2018 2017

Too Small Appropriately Sized Too Large

Direct Suppliers

Considering your 2019-2020 North American production planning volumes expectation, in terms of the number of

your NA suppliers, select the relative size of your current supply base

If your supply base is too large, over the next year, what percent

reduction levels are you planning for (based on number of suppliers)?Average -13% Average -17%

Size of Supply Base

Indirect Suppliers

19Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

23%

24%

32%

11%

10%

23%

33%

29%

10%

6%

0% 10% 20% 30% 40%

None

1% - 2%

3% - 5%

6% - 8%

> 8%

Percent of Respondents

What percent of your North American direct material

suppliers are currently on your “watch list?”

Direct Supplier RiskQuality issues and financial metrics increased the percentage of “watch list” suppliers

31%

28%

21%

13%

3%

3%

26%

23%

20%

24%

3%

4%

0% 10% 20% 30% 40%

Quality

Financialmetrics

Deliveryperformance

Capacityconstraints

Managementrelated

Other

Percent of Respondents

2019

2018

What is the primary reason companies are being added

to or continuing on the supplier “watch list?”

20Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

37%

36%

48%

51%

53%

20%

30%

26%

23%

24%

19%

26%

20%

9%

7%

15%

8%

1%

6%

4%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Electrical/Electronics

Powertrain

Chassis

Interior/HVAC

Exterior

No Concern Minimal Concern Moderate Concern Significant Concern

Percent of respondents

For each of the following system areas, select your level of concern in having future sourcing constraints

Sourcing ConstraintsElectrical/Electronics and Powertrain systems face the highest sourcing risks

21Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

Severity on your Business

Pro

babili

ty o

f O

ccurr

ence

Short shipments from suppliers

Long-lead product/system delivery constraints

Sub-tier financial distressSub-tier capacity constraints from suppliers

shared across other customers

Logistics constraints Raw material shortages

Quality related concerns

Receiving late customer engineering change

orders

Having late or delayed critical part validation

3.00

3.25

3.50

3.75

4.00

4.25

4.50

4.75

3.50 3.75 4.00 4.25 4.50 4.75 5.00

Rating scale for both probability and severity is 1-7, with 7 being highly probable and very severe

Within your supply chain, over the next 12 months, rate the likelihood of occurrence and the severity that each of the

following possible scenarios would have on your business.

Supplier Concern ScenariosTiming issues are not only the most disruptive, but also the most likely

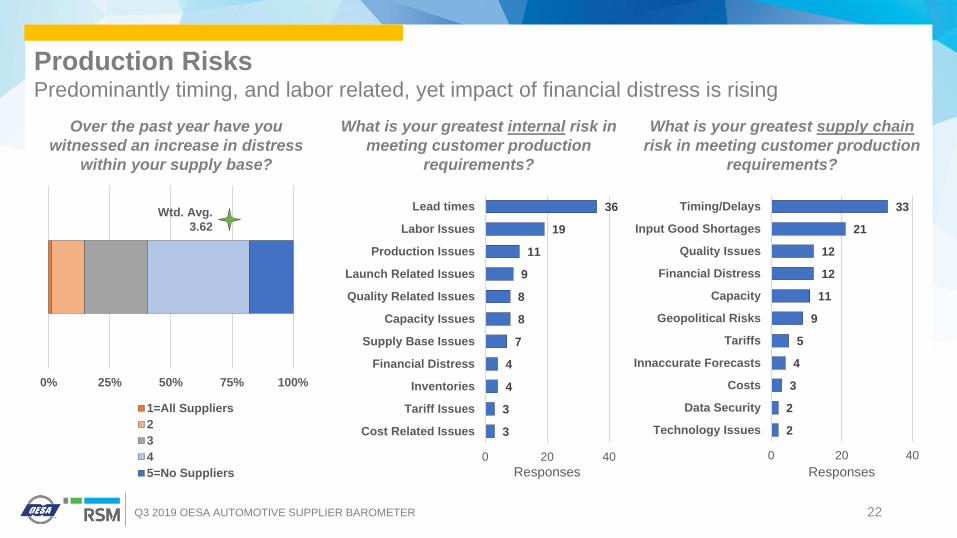

22Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

What is your greatest internal risk in

meeting customer production

requirements?

Production RisksPredominantly timing, and labor related, yet impact of financial distress is rising

3

3

4

4

7

8

8

9

11

19

36

0 20 40

Cost Related Issues

Tariff Issues

Inventories

Financial Distress

Supply Base Issues

Capacity Issues

Quality Related Issues

Launch Related Issues

Production Issues

Labor Issues

Lead times

Responses

2

2

3

4

5

9

11

12

12

21

33

0 20 40

Technology Issues

Data Security

Costs

Innaccurate Forecasts

Tariffs

Geopolitical Risks

Capacity

Financial Distress

Quality Issues

Input Good Shortages

Timing/Delays

Responses

What is your greatest supply chain

risk in meeting customer production

requirements?

0% 25% 50% 75% 100%

1=All Suppliers

2

3

4

5=No Suppliers

Over the past year have you

witnessed an increase in distress

within your supply base?

Wtd. Avg.

3.62

23Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

3.5%

1.7%

8.7%

9.2%

17.3%

59.5%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0%

Greater than 80 Less thanor equal to 100

Greater than 60 Less thanor equal to 80

Greater than 40 Less thanor equal to 60

Greater than 20 Less thanor equal to 40

Greater than 10 Less thanor equal to 20

Less than or equal to 10

What percent of your suppliers are customer required directed buy arrangements?

Median = 5%

Mean = 16.5%

Percent of Respondents

Directed BuyThe majority of respondents indicate that fewer than 10% of their suppliers are directed buy

Less than or

equal to 10

Greater than 10 Less than

or equal to 20

Greater than 20 Less than

or equal to 40

Greater than 40 Less than

or equal to 60

Greater than 60 Less than

or equal to 80

Greater than 80 Less than

or equal to 100

24Q3 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

The information and opinions contained in this report are for general information purposes. Comments are edited only for

spelling and may contain grammatical errors due to their verbatim nature. Responses to this survey are confidential.

Therefore, only aggregated results will be reported and individual responses will not be released or shared.

Antitrust Statement:

Respondents/participants should not contact competitors to discuss responses, or to discuss the issues dealt with in the

survey. It is an absolute imperative to consult legal counsel about any contacts with competitors. All pricing and other terms

of sale decisions and negotiating strategies should be handled on an individual company basis.

OESA Automotive Supplier Barometer is a survey of the top

executives of OESA regular member companies. The OESA

Automotive Supplier Barometer takes the pulse of the suppliers'

twelve month business sentiment. In addition, it provides a snapshot

of the industry commercial issues, business environment and

business strategies that influence the supplier industry.

www.oesa.org.

Survey Methodology

• Data collected July 15 – July 23 via invitation to online survey.

• Executives of OESA supplier companies.

• 176 complete survey responses were received, with 293 responses total.

Contacts

Mike Jackson

Executive Director

Strategy and Research

248.430.5954

Joe Zaciek

Manager

Research and Industry Analysis

248.430.5960

Larry Keyler

RSM Detroit Office Managing Partner

317.805.6205

Original Equipment Suppliers Association

25925 Telegraph Road

Suite 350

Southfield, Michigan 48033

RSM US LLP is the leading provider of audit, tax and consulting

services focused on the middle market, with nearly 10,000

professionals nationwide. It is a licensed CPA firm and the U.S.

member of RSM International, a global network of independent audit,

tax and consulting firms with more than 41,000 people in 116

countries. RSM uses its deep understanding of the needs and

aspirations of clients to help them succeed. For more information, visit

rsmus.com, like us on Facebook at RSM US LLP, follow us on Twitter

@RSMUSLLP or connect with us on LinkedIn.

Related Documents