PAGE 1 : INTRODUCTION PAGE 2 : DEFINITIONS PAGE 3 : OBJECTIVES OF BI-RTGS PAGE 4 : CLEARING SETTLEMENT MECHANISM PAGE 5 : PAYMENT SYSTEM RISKS PAGE 6 : CHARACTERISTICS OF BI-RTGS SYSTEM A. V-SHAPED STRUCTURE B. PARTICIPANTS OF BI-RTGS C. BI-RTGS FUND TRANSFER MECHANISM D. WINDOW TIME FRAME E. RTGS TRANSACTION CHARGES F. NO MONEY NO GAME G. CAPPING H. QUEUE MANAGEMENT AND GRIDLOCK RESOLUTION I. INTRADAY LIQUIDITY FACILITY & SHORT-TERM FUNDING FACILITY J. BI-SCRIPTLESS SECURITIES SETTLEMENT SYSTEM (BI-SSSS) K. BYLAWS

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PAGE 1 : INTRODUCTION

PAGE 2 : DEFINITIONS

PAGE 3 : OBJECTIVES OF BI-RTGS

PAGE 4 : CLEARING SETTLEMENT MECHANISM

PAGE 5 : PAYMENT SYSTEM RISKS

PAGE 6 : CHARACTERISTICS OF BI-RTGS SYSTEM

A. V-SHAPED STRUCTURE

B. PARTICIPANTS OF BI-RTGS

C. BI-RTGS FUND TRANSFER MECHANISM

D. WINDOW TIME FRAME

E. RTGS TRANSACTION CHARGES

F. NO MONEY NO GAME

G. CAPPING

H. QUEUE MANAGEMENT AND GRIDLOCK RESOLUTION

I. INTRADAY LIQUIDITY FACILITY & SHORT-TERM FUNDING FACILITY

J. BI-SCRIPTLESS SECURITIES SETTLEMENT SYSTEM (BI-SSSS)

K. BYLAWS

L. INFORMATION TECHNOLOGY SECURITY AND DISASTER

RECOVERY PLAN (DRP)

M. IMPLEMENTATION OF BI-RTGS SYSTEM AT BANK INDONESIA

BRANCH OFFICES

PAGE 7 : HISTORICAL REVIEW OF RTGS SYSTEM

DEVELOPMENT IN INDONESIA

INTRODUCTION

In recent years, nearly all developed countries that are members of

G-10 have implemented a Real-Time Gross Settlement (RTGS) system for

interbank transfer transactions. According to a BIS report, hitherto, at least

30 countries have introduced a RTGS system. Furthermore, the European

Central Bank has mandated that each EU member must implement a RTGS

system, which can assimilate with the EU’s TARGET RTGS system to help

support economy integration.

Similar steps have also been taken in the Asia/Pacific region such as

in Hong Kong, Korea, Australia, China, New Zealand and Thailand. In

Indonesia, a RTGS system was implemented on 17th November 2000 known

as the Bank Indonesia Real-Time Gross Settlement (BI-RTGS) system. The

BI-RTGS system in Indonesia is considered extremely important as

settlement of the high-value payment system (HVPS) with systemic risk

potential prior to the BI-RTGS system accounted for 92% of total payment

transactions in Indonesia.

In general, RTGS implementation in various countries is based on

several key reasons. Firstly, reams of literature and numerous empirical

studies have intensively provided greater understanding to a number of

central banks regarding how to manage the various risks in the Large/High

Value Transfer System (LVTS/HVPS). RTGS employs a settlement

mechanism that is considered adequate to minimize systemic risk. Secondly,

the system can avoid float (a condition where the payer account has been

debited, however, the recipient account has not yet been credited), which

supports effective monetary management. Notwithstanding, demand from

this system on its participants to become more disciplined in terms of

managing their liquidity also buttresses effective banking policy. Thirdly, the

RTGS system can be integrated with other settlement systems such as the

securities settlement systems in the money market and stock market.

Consequently, securities delivery is simultaneous with payment settlement

(Delivery Versus Payment (DVP) mechanism). Additional links can also be

appended to the RTGS system of other countries in order to minimize

settlement failure risk when settlementing cross-border payments.

DEFINITIONS

“The Bank Indonesia Real-Time Gross Settlement system, hereafter

referred to as the BI-RTGS system, is an electronic fund transfer system

amongst participating members in rupiah, for which settlement is performed

in real-time per individual transaction”.

Using the BI-RTGS system, members transmit fund transfers to the

RTGS Central Computer (RCC) at Bank Indonesia through an RTGS

terminal at their station for settlement processing. If the settlement process

is successful the payment transaction proceeds automatically and

electronically to recipient members. Success of the settlement process

depends on sufficient funds of the sender participant because under the BI-

RTGS system members are only permitted to credit other members. In other

words, participants of BI-RTGS must ensure an adequate account balance is

held at Bank Indonesia prior to transferring funds to other BI-RTGS

members.

OBJECTIVES OF BI-RTGS

1. To minimize settlement risk in the national payment system;

2. To provide an additional fund transfer facility that is efficient, timely,

secure and reliable;

3. To improve settlement verification;

4. To improve the efficiency and effectiveness of fund management for

banks, through the centralized checking account policy at Bank

Indonesia using the BI-RTGS system; and

5. To provide information that supports effective monetary policy as well

as operate as an early warning system for bank supervisors.

CLEARING SETTLEMENT MECHANISM

Prior to the BI-RTGS system, interbank transaction settlements, either

in the interest of the bank or its customers, were processed through clearing.

In contrast to the BI-RTGS system, which applies a gross settlement method

(each payment transaction is settled individually), the clearing system uses a

netting method in its settlement process. Netting or net settlement is a final

settlement process conducted at the end of day, by offsetting payment

liabilities with the rights of the recipients. As a result, at the end of the day

there is just one net right or liability to be settled for each member account.

Under the netting system there was always a risk that at the end of

day one or several banks would experience a large clearing deficit. This was

possible because all interbank transactions, both retail value and large

value, are calculated through the clearing system. If the clearing deficit value

of a member bank exceeds its current account balance held at Bank

Indonesia, the account would become overdrawn, which is subsequently

covered by Bank Indonesia if the respective bank is unable to clear its

overdraft until the next day. The possibility of this debit balance has become

relatively negligible since the application of Failure-to-Settle in the National

Clearing System of Bank Indonesia.

PAYMENT SYSTEM RISKS

In general there are two types of risk in the payment system; credit

risk and liquidity risk. Credit risk occurs when a counterparty cannot fulfill

their obligation to make full payment, either on the due date or in the future.

Whereas liquidity risk emerges when a counterparty is unable to make full

payment on the due date, however, can (maybe) at a later date. This can

create liquidity problems for the recipient counterparty and, in turn, increase

the cost of funds as said counterparty is forced to seek funds on the money

market.

In addition to the risks highlighted, Bank Indonesia as supervisor of

the payment system in Indonesia is particularly interested in systemic risk

that could occur in Indonesia’s payment system. Systemic risk is the risk of

failure by one participant in fulfilling its liabilities that can, in turn, cause other

members to also suffer liquidity shortfalls and subsequently be unable to

meet their respective liabilities. Such a failure, in the most extreme condition,

could precipitate financial turmoil that can undermine payment system

stability or even disrupt overall economic stability.

Implementation of the BI-RTGS system is expected to minimize the

possibility of such risks. With the ability to continuously process fund

transfers in real-time during the specified window and due to the fact that

new payment transactions are only calculated if the payer account held at

Bank Indonesia is sufficient, the BI-RTGS system can minimize or perhaps

even eliminate risks in the settlement process. Under the BI-RTGS system,

providing that the payer account is sufficient, settlement and credit

processing to the recipient account is instant with the funds received ready

for immediate use, including to pay for business activities. Using such a

system encourages the effective expansion of economic activities.

The implementation of BI-RTGS is expected to meet the range of

requirements put forward by various parties regarding the availability of a

faster payment mechanism that minimizes risk, as necessary when settling

economic transactions through DVP, for instance the trade of stocks and

securities papers. With the availability of such a mechanism, fund transfers

through BI-RTGS (payment leg) can be coordinated with final the transfer of

assets (delivery leg), thus simultaneous settlement can occur between the

handover of assets and the respective payment. This will minimize risk in the

securities market.

It is worth noting that the implementation of BI-RTGS can minimize

potential systemic risk through three approaches. First, a significant decline

in intraday interbank exposure is accomplished, as the possibility of “failure

of a participant to cover its particular losses/liquidity shortfall due to the

inability of another participant to fulfill its liabilities” is minimized. Second, the

BI-RTGS system can prevent the possibility of unwinding payments, which

can trigger systemic risk in a net settlement system. Third, as participating

members can process settlements at anytime during the allotted window,

settlements are no longer concentrated at specific times of the day. This

allows sufficient time for banks to settle any liquidity shortfall by borrowing

funds from other bank or await incoming transfers from other members.

CHARACTERISTICS OF THE BI-RTGS SYSTEM

The BI-RTGS system is the eighth RTGS system developed and

operated by an EMEAP member country (Executive Meeting of East

Asia/Pacific Central Bankers). The other seven are Thailand, Hong Kong,

Singapore, Malaysia, South Korea, Australia and New Zealand.

The BI-RTGS system was implemented gradually. During the initial

phase, Bank Indonesia enlisted banks that operated in Jakarta to become

participants of the BI-RTGS system. In the next stage, the BI-RTGS system

was implemented in regions that already had a Bank Indonesia branch

office. The account balances of banks held at BI branch offices were moved

and amalgamated into one account in the BI-RTGS system (one-bank-one-

account policy).

Currently, the BI-RTGS system is implemented throughout Indonesia

with 152 participating members, including 150 bank members (including

Sharia Business Units) and 2 non-bank participants.

The characteristics of the BI-RTGS system are as follows:

A. V-SHAPED STRUCTURE

As applied by the majority of RTGS systems worldwide, the BI-RTGS

system also uses a V-shaped structure in the process of message

transmission, from sender participant to recipient participant through Bank

Indonesia as operator of the BI-RTGS system (please refer to below figure).

Using such a structured approach, all information contained in a

transaction is transmitted by the sender participant to the RTGS Central

V-shaped

SENDER RECIPIENT

massage massage RCC 2. Full payment 3. Full payment

1. SETTLEMENT

Computer (RCC), which is subsequently forwarded to the recipient member

when the transfer is settled by RCC at Bank Indonesia.

B. PARTICIPANTS OF BI-RTGS

Participating members of the BI-RTGS system comprise of banks and

non-bank financial institutions. Participants are grouped into two categories,

namely direct members and indirect members. Direct members can perform

transactions directly using a RTGS Terminal owned by the Member. Indirect

members can perform BI-RTGS transactions indirectly with assistance from

Bank Indonesia officers using a RTGS Terminal owned by Bank Indonesia.

Indirect members are obliged to become direct members within one year

from their date of registration as an indirect member. The status of BI-RTGS

participants is classified as:

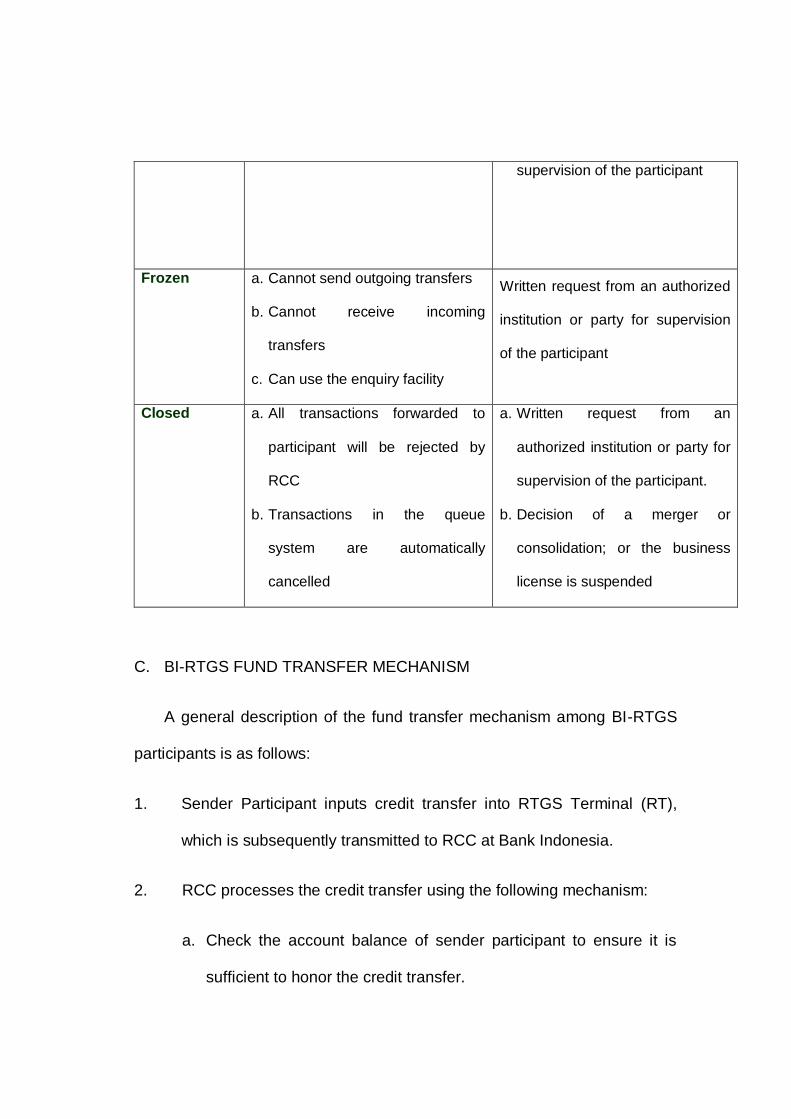

STATUS ACTIVITY REASON

Active a. Can send outgoing transfers

b. Can receive incoming transfers

c. Can perform all other functions at

RTGS Terminal

Suspended a. Can receive incoming transfers

b. Can perform all other functions at

RTGS Terminal

c. Cannot send outgoing transfers

a. Negative account balance at cut-

off time

b. Written request from an

authorized institution or party for

Elu supervision of the participant

Frozen a. Cannot send outgoing transfers

b. Cannot receive incoming

transfers

c. Can use the enquiry facility

Written request from an authorized

institution or party for supervision

of the participant

Closed a. All transactions forwarded to

participant will be rejected by

RCC

b. Transactions in the queue

system are automatically

cancelled

a. Written request from an

authorized institution or party for

supervision of the participant.

b. Decision of a merger or

consolidation; or the business

license is suspended

C. BI-RTGS FUND TRANSFER MECHANISM

A general description of the fund transfer mechanism among BI-RTGS

participants is as follows:

1. Sender Participant inputs credit transfer into RTGS Terminal (RT),

which is subsequently transmitted to RCC at Bank Indonesia.

2. RCC processes the credit transfer using the following mechanism:

a. Check the account balance of sender participant to ensure it is

sufficient to honor the credit transfer.

b. If the account balance of sender participant is sufficient, posting is

simultaneous from the sender participant (debited) account to the

recipient participant (credited) account.

c. If the account balance of sender participant is insufficient, the

credit transfer is queued in the BI-RTGS system.

3. Information on the settled credit transfer is automatically transferred

by RCC to the RT of the recipient participant.

D. WINDOW TIME FRAME

The operational time frame for fund transfers among members in the

interest of their customers is currently set between 06.30 and 16.30 (West

Indonesia Time). This window is expected to provide generous flexibility for

business players throughout Indonesia, which consists of three time zones,

enabling them to transact smoothly.

However, if in certain cases a longer window is required, Bank Indonesia

can extend the time to accommodate such needs.

E. RTGS TRANSACTION CHARGES

BI-RTGS transaction charges are set by Bank Indonesia as follows: (All

times quoted in WIB (West Indonesia Time)

1. Single credit transaction charges:

a. For transactions sent from 06:30 to 15:00 the fee is Rp7,000

per transaction.

b. For transactions sent after 15:00 to the cut-off time the fee is

Rp15,000 per transaction.

2. Multiple credit transaction charges:

a. For transactions sent from 06:30 to 15:00 the fee is Rp35,000

per transaction.

b. For transactions sent after 15:00 until the cut-off time, the fee

is Rp50,000 per transaction.

3. The charge for sending an Administrative Message is Rp2,500 per

Administrative Message.

F. NO MONEY NO GAME

The BI-RTGS system only allows its participants to credit the accounts

of other BI-RTGS members. In other words, BI-RTGS participants are not

authorized to debit the account of other BI-RTGS participants. This is to

create a new paradigm in the payment system in Indonesia, where member

banks are wiser and more disciplined in terms of managing their liquidity.

More specifically, if the account balance of a participating member is

insufficient, transactions cannot be settled and are queued. Queued

transactions are only settled once the respective participants receive

sufficient incoming transfers.

G. CAPPING

To minimize payment risks due to the application of net settlement in

the clearing process, Bank Indonesia has set a maximum cap on credit

transfer transactions processed through clearing (clearing capping). Initially,

the clearing cap was set at Rp1 billion but on 1st October 2002 it was

amended to Rp100 million.

H. QUEUE MANAGEMENT AND GRIDLOCK RESOLUTION

If the account balance of the participant to be debited is less than the

payment transaction sent, the transaction is automatically queued using the

following procedure:

1. Queue in the BI-RTGS system is based on priority level and First-In-First-

Out (FIFO).

2. Priority levels in the queue module of BI-RTGS system are:

a. First priority :clearing settlement

b. Second priority :transactions of BI-RTGS members with

BI/Government.

c. Third priority :credit transfers among members of BI-RTGS

3. If BI-RTGS detects gridlock, the gridlock resolution facility is applied,

either automatically or manually based on balance sufficiency criteria or

using the First–Available-First-Out (FAFO) method.

I. INTRADAY LIQUIDITY FACILITY and SHORT-TERM FUNDING

FACILITY

As described previously, transactions settled in the BI-RTGS system

use gross settlement, therefore, they are settled individually and

continuously during the specified window. This is different to the clearing

mechanism, which currently applies net settlement. Under the net settlement

system, banks are not required to maintain relatively high liquidity on a daily

basis, whereas under the RTGS system, participants are obliged to maintain

high liquidity all day. Such a precondition precipitated the need for an

intraday liquidity facility to boost the efficiency of interbank payments during

the day.

Under a gross settlement system, such conditions can occur at a

certain period of time, for instance in the morning, when the balance of

member accounts is less than the total transactions to be settled, which

leads to a queue. This does not imply that the respective participant is

suffering chronic liquidity problems; the participant is merely expecting

incoming transfers from other participants. Therefore, the situation is simply

an intraday gap between outgoing and incoming transactions at certain

periods of the day.

To overcome the intraday gap, most RTGS systems around the world

require a support facility like an Intraday Liquidity Facility, which is designed

to improve the efficiency of real-time transactions. The terms and conditions

of the Intraday Liquidity Facility for BI-RTGS include:

1. To qualify for the Intraday Liquidity Facility, BI-RTGS members must

submit a proposal to Bank Indonesia.

2. Participants must pledge BI Certificates and/or other government bonds

as collateral with a minimum value equaling the proposed Intraday

Liquidity Facility in order to fully secure the facility.

3. The Intraday Liquidity Facility is automatically applied when the account

balance is insufficient for outgoing transactions, providing the shortage

does not exceed the value of the Intraday Liquidity Facility (provided

when necessary).

4. When a bank receives an incoming transfer, the incoming transfer is

automatically applied to reduce the balance of the Intraday Liquidity

Facility used.

5. The Intraday Liquidity Facility can only be utilized from 06:30 to 17:00

(West Indonesia Time), and settlement of Intraday Liquidity Facility

should be completed by 18:00 (West Indonesia Time). If the participating

member fails to settle on time, the Intraday Liquidity Facility will

automatically change to an overnight Short-Term Funding Facility.

6. During T+1 up to 16:00 (West Indonesia Time), Bank Indonesia will

request payments from members using “Super Priority” transactions, for

which settlement is prioritized over other transactions.

7. In the case where the account balance is insufficient to settle the Short-

Term Funding Facility before 17:00 (West Indonesia Time) and the

respective participant does not request a new Short-Term Funding

Facility before 18:15, the payment is settled by executing the collateral.

J. BI-SCRIPTLESS SECURITIES SETTLEMENT SYSTEM (BI-SSSS)

To integrate the final settlement of funds in the BI-RTGS system with

the final settlement of BI Certificates (SBI) and Government Bonds (SUN), or

in other words DVP for SBI and SUN settlements, Bank Indonesia

developed a securities settlement system known as BI-SSSS. BI-SSSS

merges the transaction system of Bank Indonesia that covers the application

of Open Market Operations with the Bank Indonesia fund facility for banks

and Government Bonds transactions for and on behalf of the Government

into one integrated, online system for Bank Indonesia and market players. In

addition, BI-SSSS also covers the information system for Members and the

Operator of BI-SSSS, the securities settlement system and the securities

administration system.

BI-SSSS was implemented on 16th February 2004 to replace the BER

system and then on 17th March 2004 the BI-SSSS system was officially

launched by the Governor of Bank Indonesia.

K. BYLAWS

In addition to the BI-RTGS regulations promulgated by Bank Indonesia,

a number of Bylaws are also applicable to BI-RTGS participants in order to

achieve standardized interbank payment operations among BI-RTGS

members. Bylaws are valid for all payment activities conducted by each

participating member in a payment series, commencing from the

originator/initiator and concluding with the ultimate beneficiary. the Bylaws

legislate the following:

1. Cut-off time for payment and settlement

Funds for intraday interbank money market payment transactions must be

received in the borrower participant’s account no later than 30 minutes

after transactions are closed. Whereas intraday interbank money market

settlements should be made no later than 16.30 on the same day.

Same day value Money Market/Foreign Exchange deals performed prior

to 16:00 must be settled no later than 16:30 (WIB). Settlement must be

made no later than 16:30 (WIB) on the due date.

End of day funding transactions must be received in the borrower account

no later than 18:00 (WIB) on the same day.

2. Compensation for interbank payment default

If interbank payment default occurs, the related parties can request

compensation due to the payment default. Payment default can be in the

form of late payments, early payments, overpayment, underpayment and

incorrect transfers.

Compensation is calculated based on the different corrections, for

instance currency date adjustment, payment return of incorrect transfer,

late payment or settlement and beneficiary change. The interest rate

applied for compensation is 120% of the average overnight JIBOR

interest rate.

3. Compensation agreement to avoid unfair profit seeking

The payment of compensation is to ensure that BI-RTGS participants

provide reparations to the aggrieved party should such conditions occur.

Compensation is set up in a way that no member can unjustly be

penalized or falsely enriched.

4. Dispute settlement by Arbitration Committee

To resolve disputes among BI-RTGS participants in relation with RTGS

transactions, and/or to deal with participant noncompliance in the BI-

RTGS system, the Bylaws Committee was established. Decisions taken

by the BI-RTGS Arbitration Committee are final and legally binding for all

BI-RTGS members.

L. INFORMATION TECHNOLOGY SECURITY AND DISASTER

RECOVERY PLAN (DRP)

The BI-RTGS system is heavily reliant on information technology (IT).

The use of hardware, software and sophisticated telecommunication tools

require additional efforts to ensure that all aspects of the BI-RTGS system

are secure. Various security layers are applied to the system; thus, the BI-

RTGS system is expected to operate in a secure manner. To this end, Bank

Indonesia employs independent IT auditors to examine all applications and

networks associated with BI-RTGS. To testing the reliability of the BI-RTGS

system, independent IT auditors also apply penetration testing to analyze

any potential loopholes that could be exploited by hackers to break BI-RTGS

security system. The current opinion of the independent IT auditors

regarding the overall performance and security of the BI-RTGS system is

very satisfactory, however, additional IT audits will be applied periodically in

the future to maintain the security of the BI-RTGS system.

Moreover, the heavy reliance and dependence on IT ensures that IT-

using institutions apply reliable backup policy and procedures. Bank

Indonesia as the administrator of the BI-RTGS system prepared a Disaster

Recovery Plan (DRP) and established a Disaster Recovery Center (DRC) to

ensure that the payment system in Indonesia is buttressed by reliable

infrastructure. Participating members are also expected to use sufficient

backup systems in separate locations from the main system that can be

activated promptly if the main system fails. Consequently, payment system

efficiency in the banking industry is not jeopardized. Periodically, all BI-

RTGS participants are required to test their backup systems and DRP to

ensure that all aspects are active.

M. IMPLEMENTATION OF BI-RTGS SYSTEM AT BI BRANCH OFFICES

After the successful initial phase of BI-RTGS implementation, the

system was gradually introduced to BI branch offices from 2001. The

integration of BI-RTGS at head office and the branch offices allowed for the

member checking accounts held at BI branch offices to be moved and

amalgamated at head office (Centralized Settlement Account or CSA).

The benefits of CSA implementation to participants of BI-RTGS are as

follows:

1. To assist members control their liquidity position;

2. Money in transit is eliminated, therefore member cost of funds can be

minimized; and

3. To assist members manage their funds effectively and efficiently.

Whereas for Bank Indonesia, CSA implementation yielded the following

benefits:

1. To assist Bank Indonesia monitor member compliance to the Minimum

Reserve Requirement;

2. To assist Bank Indonesia monitor liquidity because member accounts

are consolidated nationally and can be monitored in real-time; and

3. To provide more accurate information for an early warning system of

members suffering liquidity problems.

HISTORICAL REVIEW OF RTGS DEVELOPMENT IN INDONESIA

Year Activity

1995-

97

Blueprint of the National Payment System (NPS) and establishment of the

NPS Reform Committee

Implementation of BI-Line as an electronic fund transfer transition project

to RTGS implementation

Analysis of RTGS development in Indonesia

1997 More detailed analysis on several policies related to RTGS

1998 Pyusunan Request For Proposal (RFP)

1999 Explanation of User Requirements

Communicate the RTGS plan to all banks in Jakarta

Detailed explanation of User Requirement

Appoint security auditor for RTGS application

Commence System design

Discuss the possibility of an Intraday Liquidity Facility

Year Activity

2000 Establish the Internal Committee of RTGS for all RTGS member banks in

Jakarta

COO Conference (Jakarta, Surabaya & Bandung) to acquaint banks with

RTGS and its implications

System Development and Testing

Purchase of RTGS support equipment

Installation of RTGS for all RTGS member banks

RTGS training for all banks and internal BI

User Acceptance Test on 17 pilot banks

Network installation at 124 banks + Cilangkap DRC site

Development of Cilangkap DRC site

Discussion on DRC scenario internally and with all RTGS participants

Bank & industry testing

Development of fund transfer regulations (BI Regulation)

Development of 17 pilot banks

Preparation of account relations legislation

Preparation of Intraday Liquidity Facility regulations

Review all accounting/operations of BI

Development of interbank bylaws on good practice for interbank payments

with HIMBARA, Joint-Venture Bank Association and other Bank

Year Activity

Associations

Preparation of contract documents with all RTGS participating banks

Formation of Rupiah Transaction Settlement Unit as operator of BI-RTGS

system

Simulation Test for 2 months to ensure all systems run effectively and

efficiently

RTGS system went live on 17th November 2000 in Jakarta

BI-RTGS system launching on 23rd November 2000 in Jakarta

2001

BI-RTGS system implementation at BI branch office in Bandung on 1/6/01

BI-RTGS system implementation at BI branch office in Surabaya on 6 /7/01

BI-RTGS system implementation at BI branch offices in Yogyakarta and

Manado on 3/8/01

BI-RTGS system implementation at BI branch office in Samarinda and

Balikpapan on 24/8/01

BI-RTGS system implementation at BI branch office in Semarang on

28/9/01

BI-RTGS system implementation at BI branch office in Denpasar on

2/10/01

BI-RTGS system implementation at BI branch office in Medan and Padang

on 26/10/01

Year Activity

BI-RTGS system implementation at BI branch office in Batam and

Pekanbaru on 23/11/01

2002

BI-RTGS system implementation at BI branch office in Banjarmasin and

Makasar on 25/2/02

BI-RTGS system implementation at BI branch office in Pontianak and

Palangkaraya on 22/3/02

BI-RTGS system implementation at BI branch office in Jayapura and

Ambon on 26/4/02

BI-RTGS system implementation at BI branch office in Kendari and Palu

on 24/5/02

BI-RTGS system implementation at BI branch office in Bandar Lampung

on 21/6/02

BI-RTGS system implementation at BI branch office in Kupang and

Mataram on 26/7/02

BI-RTGS system implementation at BI branch office in Jambi and

Bengkulu on 23/8/02

BI-RTGS system implementation at BI branch office in Palembang and

Banda Aceh on 27/9/02

2003 BI-RTGS system implementation at BI branch office in Solo and Malang on

Year Activity

28/2/03

BI-RTGS system implementation at BI branch office in Purwokerto and

Tasikmalaya on 28/3/03

BI-RTGS system implementation at BI branch office in Jember and

Cirebon on 25/4/03

BI-RTGS system implementation at BI branch office in Kediri and Sibolga

on 29/5/03

BI-RTGS system implementation at BI branch office in in Ternate on

27/6/03

BI-RTGS system implementation at BI branch office of Lhokseumawe on

16/10/03

For further information, kindly contact: HELP DESK BI-RTGS Settlement Division Bank Indonesia, Ged. D Lt. 3 Jl. MH. Thamrin No.2, Jakarta 10350 Telp.3818888, 3817575 Email : [email protected] Fax: 021-2310485

Related Documents