Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

This brochure is provided for information purposes only and does not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, interests in Oaktree European Principal Fund III, L.P. (the “Fund”) or its related feeder fund(s) and parallel fund(s). Any such offer may only be made pursuant to the Fund’s confidential private placement memorandum and related supplements (the “PPM”), subscription documents and constituent documents in their final form.

This brochure does not constitute and should not be construed as investment, legal, or tax advice, or a recommendation or opinion regarding the merits of investing in the Fund or its related feeder fund(s) and parallel fund(s). Each potential investor should consult its own counsel, accountant, and/or investment adviser as to the legal, tax, and related matters concerning its investment. A potential investor considering an investment in the Fund or its related feeder fund(s) and parallel fund(s) should read this brochure in conjunction with the PPM. The PPM contains a more complete description of the Fund’s investment practices, terms and conditions, restrictions, and other factors relevant to a decision to invest, and also contains tax information and risk disclosures that are important to any investment decision. All information herein is subject to and qualified in its entirety by the PPM. No person has been authorized to make any statement concerning the Fund or its related feeder fund(s) and parallel fund(s) other than as set forth in the PPM and any such statements, if made, may not be relied upon. Terms used but not defined herein shall have the meanings set forth in the PPM.

Responses to any inquiry that may involve the rendering of personalized investment advice or effecting or attempting to effect transactions inResponses to any inquiry that may involve the rendering of personalized investment advice or effecting or attempting to effect transactions in securities will not be made absent compliance with applicable laws or regulations (including broker dealer, investment adviser, or applicable agent or representative registration requirements), or applicable exemptions or exclusions therefrom.

See the Appendix on page 37 for relevant marketing disclosures.

The term “Oaktree®” used herein refers to Oaktree Capital Management, L.P.™ and, where applicable, its affiliates.

None of the information contained herein has been filed with the U.S. Securities and Exchange Commission, any securities administrator under any state securities laws, or any other U.S. or non-U.S. governmental or self-regulatory authority. No governmental authority has passed on the merits of , y g g y y g y pthis offering or the adequacy of the information contained herein. Any representation to the contrary is unlawful.

This brochure is being provided on a confidential basis solely for the information of those persons to whom it is given. The materials, including the information contained herein, may not be copied, reproduced, republished, posted, transmitted, distributed, disseminated, or disclosed, in whole or in part, to any other person in any way without our prior written consent. By accepting this brochure, you agree that you will comply with these confidentiality restrictions and acknowledge that your compliance is a material inducement to our providing this brochure to you.

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

oaktree european principal fund iii, l.p.

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

Table of Contents

Tab Section Title Page

1 | Overview of Oaktree and the Principal Group 1

2 | The European Opportunity 6

3 | European Investment Approach 13

4 | In estment Performance Histor 234 | Investment Performance History 23

5 | Case Study: Countrywide 24

6 | Information, Disclosures and Disclaimers 31

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

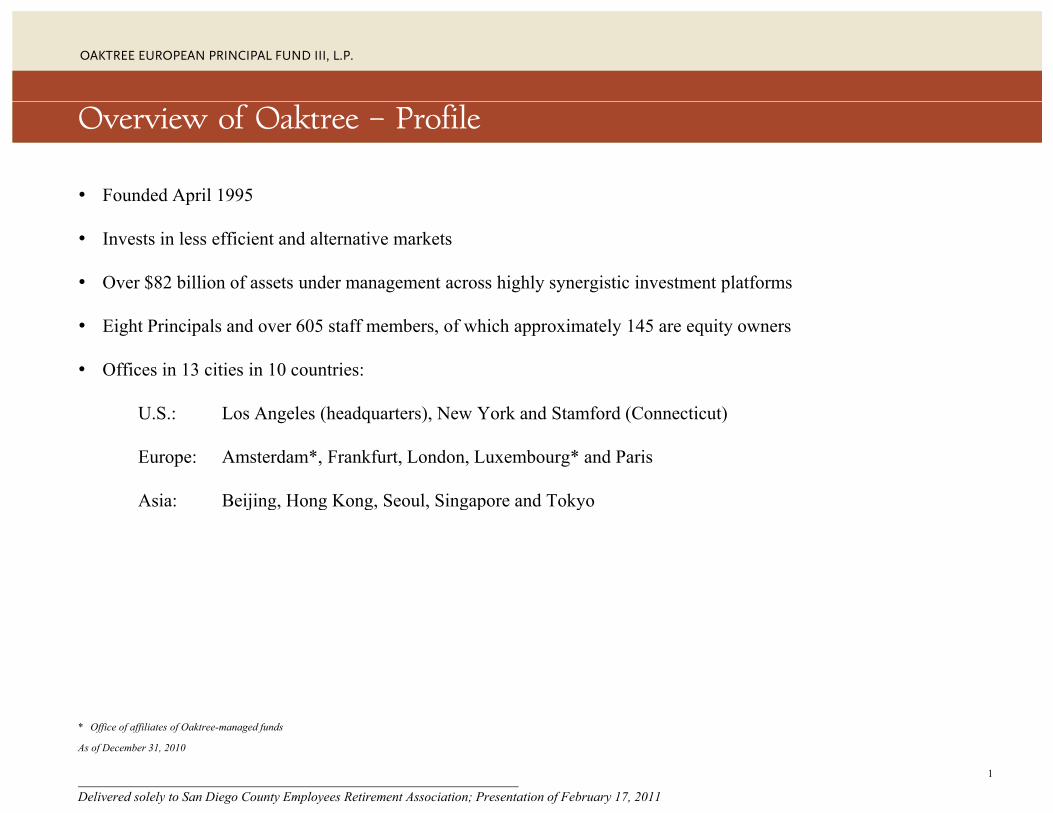

Overview of Oaktree – Profile

• Founded April 1995p

• Invests in less efficient and alternative markets

• Over $82 billion of assets under management across highly synergistic investment platforms

• Eight Principals and over 605 staff members, of which approximately 145 are equity owners

• Offices in 13 cities in 10 countries:

U S L A l (h d ) N Y k d S f d (C i )U.S.: Los Angeles (headquarters), New York and Stamford (Connecticut)

Europe: Amsterdam*, Frankfurt, London, Luxembourg* and Paris

Asia: Beijing, Hong Kong, Seoul, Singapore and Tokyoj g, g g, , g p y

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

1

* Office of affiliates of Oaktree-managed funds

As of December 31, 2010

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

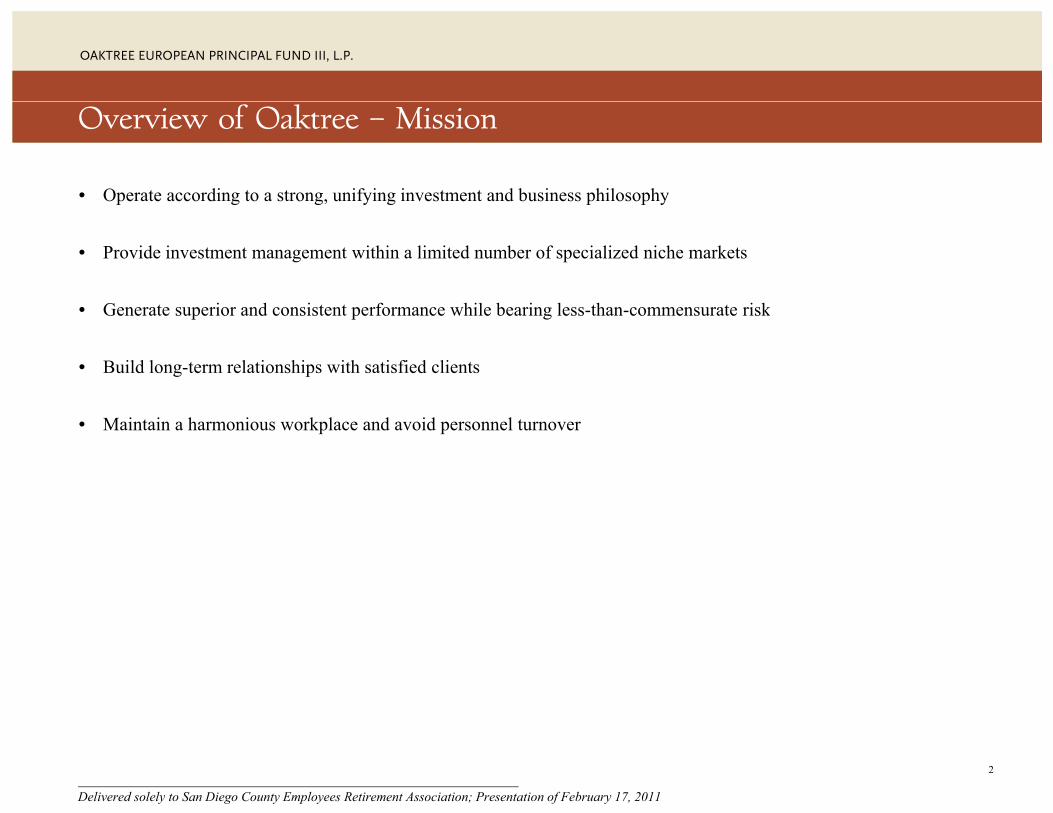

Overview of Oaktree – Mission

• Operate according to a strong, unifying investment and business philosophyp g g, y g p p y

• Provide investment management within a limited number of specialized niche markets

G t i d i t t f hil b i l th t i k• Generate superior and consistent performance while bearing less-than-commensurate risk

• Build long-term relationships with satisfied clients

• Maintain a harmonious workplace and avoid personnel turnover

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

2

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

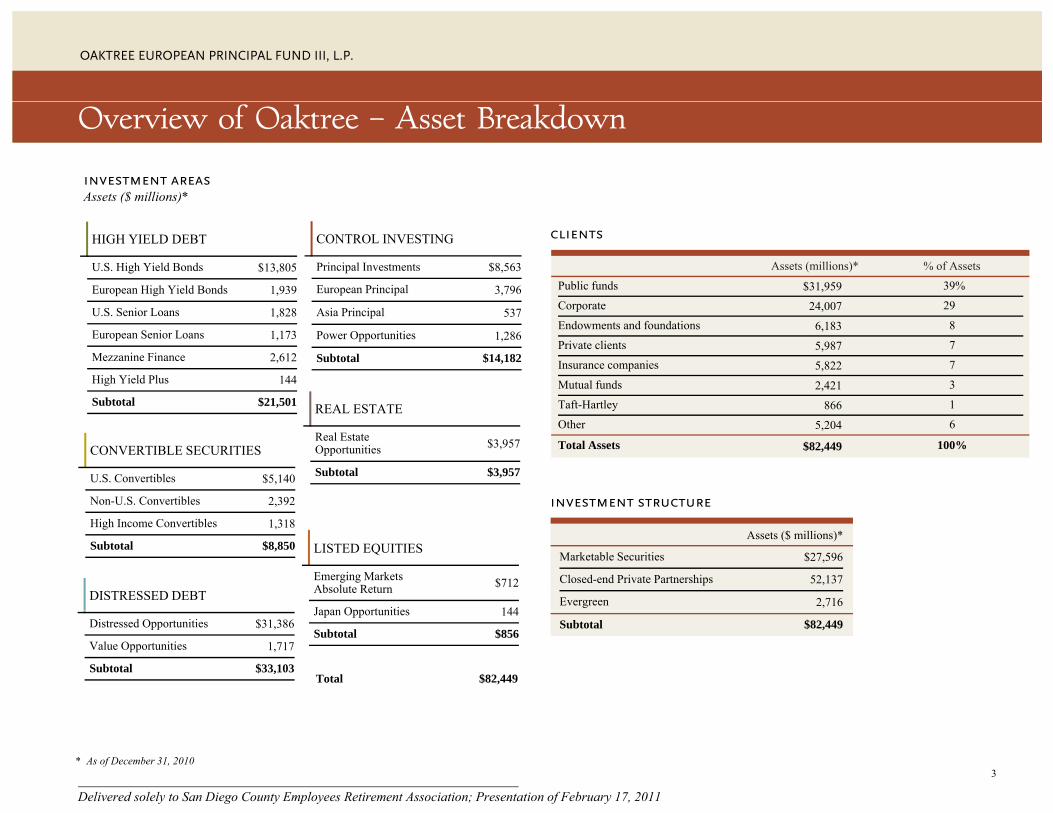

Overview of Oaktree – Asset Breakdown

investment areasAssets ($ millions)*

Assets (millions)* % of Assets

Public funds $31,959 39%

Corporate 24 007 29

HIGH YIELD DEBT

U.S. High Yield Bonds $13,805

European High Yield Bonds 1,939

CONTROL INVESTING

Principal Investments $8,563

European Principal 3,796

( )

clients

Corporate 24,007 29

Endowments and foundations 6,183 8

Private clients 5,987 7

Insurance companies 5,822 7

Mutual funds 2,421 3

Taft-Hartley 866 1

U.S. Senior Loans 1,828

European Senior Loans 1,173

Mezzanine Finance 2,612

High Yield Plus 144

Subtotal $21,501

Asia Principal 537

Power Opportunities 1,286

Subtotal $14,182

REAL ESTATE Taft Hartley 866 1

Other 5,204 6

Total Assets $82,449 100%

,

CONVERTIBLE SECURITIES

U.S. Convertibles $5,140

Non-U.S. Convertibles 2,392

REAL ESTATE

Real Estate Opportunities $3,957

Subtotal $3,957

investment structureHigh Income Convertibles 1,318

Subtotal $8,850

DISTRESSED DEBT

LISTED EQUITIES

Emerging Markets Absolute Return $712

Japan Opportunities 144

Assets ($ millions)*

Marketable Securities $27,596

Closed-end Private Partnerships 52,137

Evergreen 2,716

Distressed Opportunities $31,386

Value Opportunities 1,717

Subtotal $33,103

Japan Opportunities 144

Subtotal $856

Total $82,449

Subtotal $82,449

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

3* As of December 31, 2010

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

The U.S. Principal Group – Overview

• U.S. strategy founded in 1994 to focus on “control” investing

− $10.3 billion of committed capital raised and $9.1 billion invested via 7 funds/accounts

− Investments in approximately 172 companies worldwide

bli h d k d i i h h l i l i l• Established track record investing through multiple economic cycles

• Integrated international presence and cross-border capabilities

− Focused on middle market

• Cohesive, talented and experienced team

− 28 investment professionals, including 8 managing directors, and over a dozen industry partners or groups

− The two senior managers have approximately 30 years of combined tenure in the Principal Group

− Minimal turnover since inception

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

As of September 30, 20104

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

The European Principal Group – Overview

• In 2005, Oaktree created a specialized team for the unique European opportunity

− Control investments in twelve companies and debt investments in more than twenty others

− From 2004 – 2007, unprecedented European debt issuance and financial complexity from a ‘standing start’

− EPOF I – $495 million fund raised in 2006 and invested pre-crisis (93% of fund invested in 2006/2007)

− EPOF II – €1.759 billion fund raised in 2007/2008 and invested during and after the crisis

di f d i i h k l di i i• Largest distress-focused team in Europe, with a market-leading position

− Completed deals in all major European countries

• EPG track record has established that distressed private equity/distress-for-control is an attractive method of investing in Europe

− Investments have been made at all points in the cycle

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

5

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

The European Opportunity

• We believe Europe will see a “wave of restructurings” in the next five years− Estimated €1 trillion of leveraged loans outstanding − Significant need for both debt-for-equity conversions and new money − The most attractive situations (at the biggest discounts) will require both operational and balance sheet restructuring

• Restructurings expected to be driven by numerous factors working in concert, many of which have been building for a long time− Low-cost Asian manufacturing sophistication and capacity is increasing− Changes in retail landscape (pre-crisis) and consumer behavior (post-crisis) is shifting retailers’ influence − Volatility of input prices and exchange rates− Global nature of markets and suppliers

• As Europe is not cost-competitive on a global basis, significant business model changes are required to respond to globalization

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

6

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

The European Opportunity (continued)

• Company-level strategic and operational changes must be executed in the face of unprecedented levels of leverage and a coming wave of amortization

− Decade-long period of easy access to capital and low borrowing costs deferred the need to restructure

− Companies currently unable to implement strategic decisions given leverage and high cost of restructuring in Europe

• We believe the best opportunities for distress-for-control and new money restructurings are yet to come

− In contrast to U S banks European banks still hold the majority of leveraged loans as they lack selling mentality andIn contrast to U.S. banks, European banks still hold the majority of leveraged loans as they lack selling mentality and infrastructure

− Banks often did not sell syndicated leveraged loans and cannot sell bilateral loan exposures

− Leveraged capital structures used more senior debt than in U.S.Leveraged capital structures used more senior debt than in U.S.

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

7

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

The European Opportunity (continued)

€800 billion - €1 trillion of senior leveraged loans

Bilateral Loans

• Traditional financing for middle market companies

Syndicated Leveraged Loans

• Traditional financing for middle-market companies

• Direct relationship between borrower and lender

• Documentation resembles a corporate loan

• Typically, banks cannot sell without borrower consent

• €450 - €500 billion in total size

• Underwriting bank disintermediates relationship between borrower and lender(s)

• Developed in London from 2004 to 2008yp ca y, ba s ca ot se w t out bo owe co se t

• Development of syndicated loan market pushed bilateral market to underwrite increased risk

• Traditional banks own 100% of the debt in the bilateral market

• Limited protection offered to unsecured creditors in Europe means there is significantly more senior debt in a typical capital structure compared to U.S.

• Banks own 60% - 80% of syndicated leveraged loans

• Limited selling by banks in fourth quarter 2008 and in 2009

cannot access this opportunity set through u.s. distress approachcannot access european opportunity through traditional u.s. distress-for-control approach

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

8

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

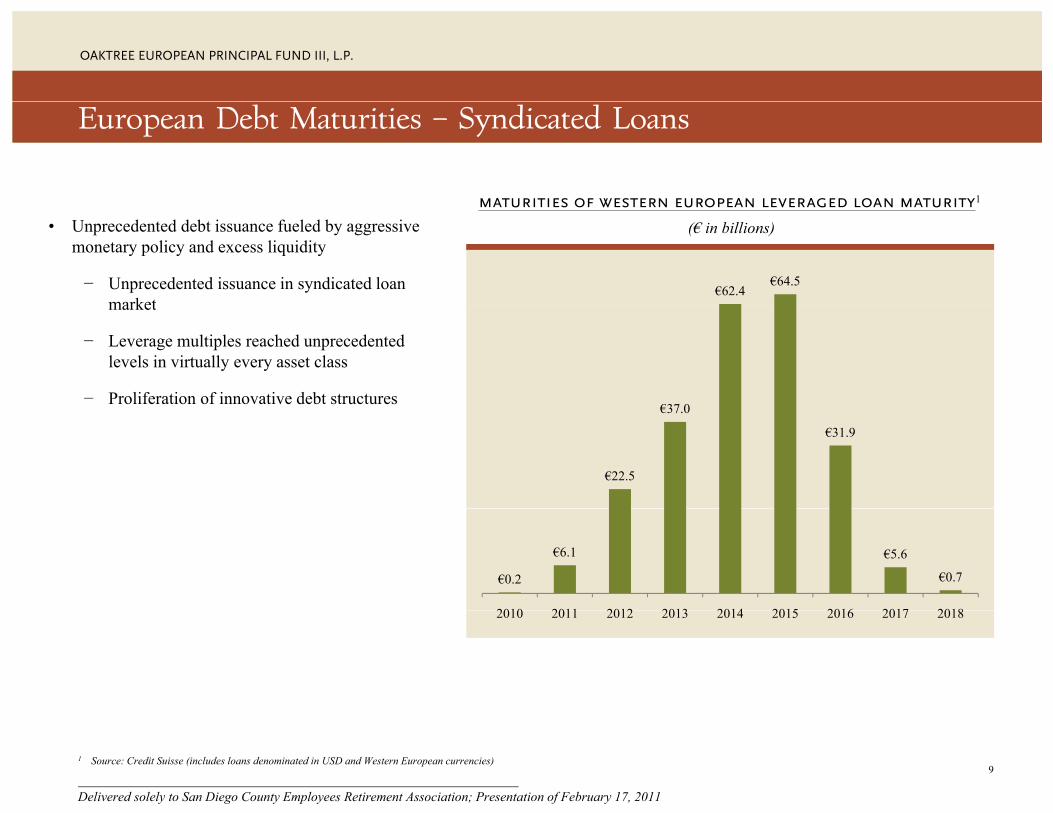

European Debt Maturities – Syndicated Loans

maturities of western european leveraged loan maturity1

• Unprecedented debt issuance fueled by aggressive monetary policy and excess liquidity

− Unprecedented issuance in syndicated loan market

€62.4€64.5

maturities of western european leveraged loan maturity(€ in billions)

market

− Leverage multiples reached unprecedented levels in virtually every asset class

− Proliferation of innovative debt structures €37 0

€22.5

€37.0

€31.9

€0.2

€6.1 €5.6

€0.7

2010 2011 2012 2013 2014 2015 2016 2017 20182010 2011 2012 2013 2014 2015 2016 2017 2018

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

1 Source: Credit Suisse (includes loans denominated in USD and Western European currencies)9

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

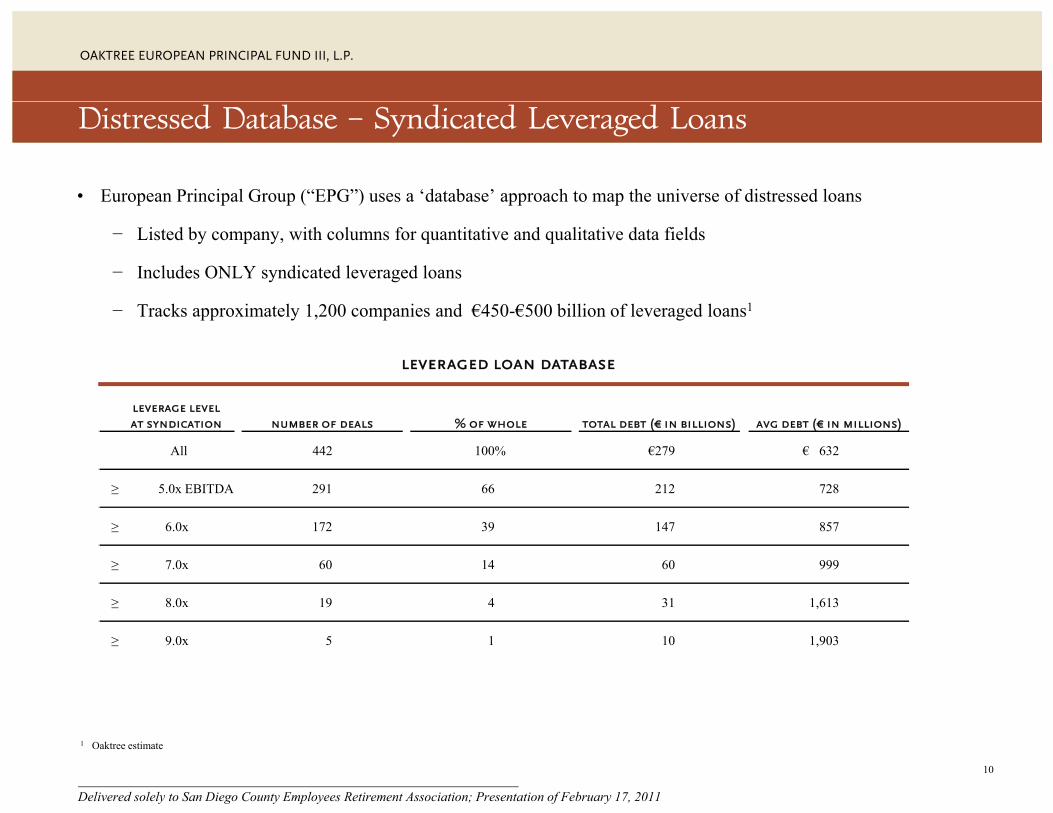

Distressed Database – Syndicated Leveraged Loans

• European Principal Group (“EPG”) uses a ‘database’ approach to map the universe of distressed loansp p p ( ) pp p

− Listed by company, with columns for quantitative and qualitative data fields

− Includes ONLY syndicated leveraged loans

T k i l 1 200 i d €450 €500 billi f l d l 1− Tracks approximately 1,200 companies and €450-€500 billion of leveraged loans1

leverage level

leveraged loan database

leverage levelat syndication number of deals % of whole total debt (€ in billions) avg debt (€ in millions)

All 442 100% €279 € 632

≥ 5.0x EBITDA 291 66 212 728

≥ 6.0x 172 39 147 857

≥ 7.0x 60 14 60 999

≥ 8.0x 19 4 31 1,613

≥ 9.0x 5 1 10 1,903

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

1 Oaktree estimate

10

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

Bilateral Loan Market

• Bilateral leveraged loan market is likely to be similar in size to syndicated leveraged loan market− Traditional channel with very little transparency; cannot apply database approach− Dominated by family-controlled companies or subsidiaries of larger corporations− Difficult to access

• As banks have the ability to defer losses on bilateral loans, situations only materialize after several years of under performance− Catalyst is the need for liquidity or belief that there is permanent impairment

• Frequently banks cannot sell loans without borrower’s consent

S d th h l ti hi ith b k d i t t ti• Sourced through our relationships with banks and proprietary transactions

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

11

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

European Banks

• Pressure on banks to address troubled credits will continue to increase− Troubled leveraged loans and bilateral loans restrict bank’s ability to deploy new capital− Increasing regulation and requirement of transparency

M b i i d b i i di li• Many borrowers are not amortizing debt or improving credit quality− Demand remains below 2007 peak levels− Interest costs were swapped at the time of borrowing− Capital expenditures and working capital need to be fundedCapital expenditures and working capital need to be funded− Borrowers unable to restructure low-margin operations due to high cash cost and significant amount of leverage− End of government subsidy programs

• Precedent suggests that banks will resist the need to restructure debt and to crystallize losses for as long as possible− Stress tests and Basel III have been watered down

• Banks in Europe are liquidity constrained p q y− A significant amount of debt issued by major European banks is due in the next three years

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

12

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

European Investment Approach

• EPG pursues several types of control investing• EPG pursues several types of control investing− Distress-for-control− New-money restructurings− Hybrid transactions − Special situation private equity

• For most transactions, the unifying theme is a significant element of distress and/or industry dislocation− Forced sellers of debt or equity; distressed process; liquidity crisis; covenant or payment default; bankruptcy orForced sellers of debt or equity; distressed process; liquidity crisis; covenant or payment default; bankruptcy or

insolvency; failed capital raising or failed sale− Private equity in industries where longer-term trends have ‘structurally’ altered profitability

• Cause of distress can vary significantlyy g y− Capital markets- or liquidity-driven− Cyclical industry or an industry subject to raw material price fluctuations− Structural industry-level trends− Company-specific underperformance − Instability among equity or debt holders

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

13

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

Flexible Approach

EPG i d d b k lli h i d b l di• EPG strategy is not dependent on banks selling their debt at large discounts− Positioned to take advantage of inevitable de-leveraging in response to either broad-based capital

market pressure or a more gradual company-by-company approach− New money offers a lower creation value (versus debt purchases)y ( p )

• Focus on situations in which restructuring is driven by the need for liquidity/new money− Liquidity is the primary catalyst for stakeholders to pursue a permanent solution

Gi en recent press res banks generall do not ha e the abilit to contrib te ne mone (especiall eq it ) to− Given recent pressures, banks generally do not have the ability to contribute new money (especially equity) to finance operational restructurings

− Banks do not have the resources required to manage restructurings or to own businesses

Oth t l t f t t i i l d• Other catalysts for restructuring include:− Distrust or disinterest from existing owner− Management’s frustration with excessive leverage and inability to influence restructuring process− CLOs own a significant portion of syndicated leveraged loans and are leveraged on average at over 10x1CLOs own a significant portion of syndicated leveraged loans and are leveraged on average at over 10x1

50% of CLOs show little or no commitment to the business1

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

1 Source: Fitch European CLO Management Update (June 10, 2010 )14

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

Flexible Approach (continued)

• EPG positioned as the complete solution provider with the ability to:

− Buy debt from banks that want to sell AND/OR to invest new money (as debt or equity) to support banks that remain in the credit

D l i / i l l i d b b l h / l l i− Develop a strategic/operational solution supported by a balance sheet/structural solution

− Augment/replace the management team and/or equity owner (frequently the parties responsible for the distress)

• First companies within an industry to de-leverage have significant advantagesp y g g g

− Liquidity needed to implement strategic decisions

− Complexity of European restructurings becomes an advantage for companies which are first to restructure

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

15

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

European Principal Group Advantages

EPG i i d id h b d f l i di d l d i i• EPG positioned to provide the broadest set of solutions to distressed related situations

− Positioned as new money provider and sponsor of the restructuring

− Existing stakeholders do not have the resources to provide both new funds for balance sheet restructuring and to l d th ti l/ t t i t t i f th d l i b ilead the operational/strategic restructuring for the underlying business

− Negotiations must involve multiple stakeholders including many who are not invested in the capital structure

− Industrial plan, which optimizes value of company, is often the key to achieve credibility with all parties

− From bank’s perspective, proposed transaction should (i) minimize write-down, (ii) preserve upside and (iii) protect reputation

− EPG will often invest in multiple parts of the capital structure

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

16

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

‘Six Pillars’ of EPG Strategy

• Local-country deal teams supported by strong senior advisor(s)

• Unique distress-focused sourcing model

• Expertise in buying debt and structuring a solution; capable of investing in multiple debt and equity instruments

F hi h lit k t l di i i i d t i ith f bl l t t d• Focus on high-quality, market-leading companies in industries with favorable long-term trends

• Portfolio Enhancement Team assists in both diligence and the operational restructuring of distressed companies

• In-house legal team to lead restructurings

limited competition due to the resource-intensive nature of the strategy

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

17

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

European Investment TeamCaleb Kramer

Managing Director and Portfolio Manager

london

Karim KhairallahManaging Director

Oren PelegManaging Director

Mathieu GuilleminManaging Director

paris milan1

Giovanni VolonteManaging Partner

Francesco ManciniManaging Partner

Roberto QuagliuoloAssociate

deal execution team portfolio enhancement team

Nicolas MoutéSenior Vice PresidentManaging Director Managing Director

Jim Van SteenkisteSenior Vice President

Guillaume BayolA i

Nael KhatounSenior Vice President

Mario AdarioVice President

Constantin von Bülow S i Vi P id

Roger IliffeSenior Vice President

Marc SchmidA i Vi P id

Baptiste VaissiéVice President

Nicolas DucarreAssistant Vice President

Associate

Rick KrensSenior Vice President

Donald BrydenS i Ad i

Senior Vice President

Stefano MazzoliAssistant Vice President

Augusto LippiSenior Vice President

Jean RollierSenior Vice President

madrid

Carlos GilaSenior Advisor

Hermann DambachManaging Director

frankfurt

Associate Senior Vice President Assistant Vice President

Samuele CappellettiAssociate

Szymon DecDirector

luxembourg2

Carl Johan KaskAssociate

Jack KeenanSenior Advisor

Dan MacFarlanSenior Advisor

Laurence CooklinSenior Advisor

Rob Davison

pf sarls

Eyal MalingerAssociate

Muriel Zingraff

Senior Advisor

Gina McDonaldSenior Advisor

Brian Eastwood

Justin BickleManaging Director

Martin GrahamVice President

Jean-Pierre BaccusCFO, Luxembourg

Krisztina BollaSenior Accountant

Sebastian EiselerAssistant Vice President

Program Manager g

Senior Advisor

Jabir ChakibGeneral Accountant

Jil KelhetterSenior Accountant

Advisor

Dedicated Legal Team

Heiko KepplerAssistant Vice President

Andreas KrämerVice President

Vice President

Wojciech Janczyk

Uwe FlachSenior Advisor

Tom JaggersAssistant Vice President

warsaw

General Accountant

Stephanie CeliTrade Specialist

Figen ErenStaff Attorney

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

1 Office of R72, the Principal Group’s exclusive advisor for the Italian market.2 Office of affiliates of Oaktree-managed funds.

18

Wojciech JanczykSenior Advisor

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

I N - H O U S E T E A M

Portfolio Enhancement Team – Resources

Portfolio Enhancement Executives Finance Director Operating Partners Functional Experts

profile and team

– Consulting and operational background REQUIRED

– CFO with extensive governance and operational experience

– Ex-senior executives with significant experience in business

– Experts in functional areas that are key in executing business

– Must have completed significant business transformation

p p– Team: Rick Krens, supported by

Jean Pierre Baccus and Jabir Chakib

g ptransformation

– Team: Laurence Cooklin, Jack Keenan, Dan MacFarlan, and Muriel Zingraff

y gimprovement

– Team: Gina McDonald (HR) and Rob Davison (Programme Management)

role

– Due diligence– Taking control– First 200 days– Governance

– Establishing and monitoring financial/key performance indicators

– Capital expenditure trackingT ki t l

– Providing leverage to team by taking over leadership of transformation post taking control

– Governance leadershipD dili t

– Providing leverage and improved execution in key process areas

– Task oriented

– Taking control– Governance

– Due diligence support – Interim management

E X T E R N A L P A R T N E R S

Analytical Support Primary Data Gathering Industry Expertise Human CapitalAnalytical Support Primary Data Gathering Industry Expertise Human Capital

– Offshore dedicated resource (~ FTE 20) providing analytical support

– Supports due diligence and portfolio company strategy work

– Offshore and onshore partners to support intense interviews in multiple languages to gather primary information during due diligence

– Three partners facilitating access to industry subject matter experts

– Industry specialist consulting firms which evaluate industry dynamics

– Two leading executive search firms which assist in the delivery of an integrated end-to-end HR process, including; early management evaluation, search, assessment recruitment

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

assessment, recruitment, development, and succession

19

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

Legal Resources and Strategy

• Internal legal team leads restructuring process in partnership with deal teamg g p p p− Supports EPG’s flexible mandate in terms of structure and types of securities (e.g., investment can be in the form of

super senior debt, convertible debt/equity, etc.)− Strategic/operational plan provides ‘blue print’ for financial restructuring

S l t d b t i l l fi− Supplemented by strong regional law firms

• After closing, legal team provides portfolio companies with support for strategic legal and tax projects, acquisitions, divestures, refinancings and exits as appropriate

• Advantages of in-house legal team− Crafts consensual legal solutions/processes to avoid use of court or bankruptcy processes where possible− Leverages network of preferred external legal service providers across Europe and holds them accountable − Utilizes support/leverage provided by Luxembourg team

• The only dedicated in-house legal team in European distressed debt or distress-for-control investing

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

20

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

Targeted Companies

• Market-leading companies in terms of share, product offering and/or innovationMarket leading companies in terms of share, product offering and/or innovation

− Companies large enough to access multiple exits (e.g., sale, IPO or refinancing)

− Potential to capture strategic premiums

C li l i d i i h f bl l h i d d hi• Cyclical industries with favorable long-term growth, economics and demographics

• Changing industry dynamics capable of creating strong organic and external growth

• Low cost and flexible production footprints (existing or potential)• Low-cost and flexible production footprints (existing or potential)

• Products with global/pan-European appeal and manufacturing/design expertise that can be leveraged across regions

• Strong conversion of EBITDA to cash flow (due to low capital expenditure and working capital requirements)g ( p p g p q )

• Platforms capable of being used for consolidation

• Post-restructuring balance sheet that permits the company to maximize its strategic value

− Ability to finance both organic and external growth

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

21

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

Discounts Versus Private Equity

selected equity/and “blocking” positions obtained($/₤/€ in millions)

original buyout european principal group transaction

TEV at Net

Leverage TEV at Net

Leverage

Discountto

Sponsor

• in order for equity owners to recover a single dollar, we must receive private equity-type returns

($/₤/€ in millions)

Company Year Creation Multiple1 Creation2 Multiple3 TEV

Countrywide 2007 £ 914 5.4x £184 0.0x (80)%

Bavaria Yachts 2007 €1,056 9.5 €291 0.0 (72)

SGD 2007 € 697 5.1 €202 0.0 (71)

equity type returns (17 – 30%) from debt holdings

• if equity owners do not recover

Panrico 2005 € 880 7.1 €344 0.4 (61)

Building Products Company 2007 £ 238 7.9 £ 46 0.0 (81)

Almatis 2007 $1,278 6.4 $401 0.0 (69)

P k i C I 2007 € 866 6 0 €310 0 0 (64)

anything, we expect to own the businesses at a reduced cost, creating upside potential

Packaging Company I 2007 € 866 6.0 €310 0.0 (64)

Niche UK Homebuilder 2006 £1,168 6.1 £350 0.0 (66)

Packaging Company II 2007 €1,324 6.9 €403 0.0 (70)

Note: Includes only those companies that completed a sponsor-backed LBO or IPO prior to the incidence of financial distress. EPOF II investment position information is the latest available as of July 16, 2010. Balance sheet information is as of May 31, 2010 unless otherwise indicated.

1 Net leverage that sits ahead of the sponsor’s equity investment.2 For investments that have not undergone restructuring, the analysis excludes any interest and principal payments that have subsequently reduced EPOF II's basis and, thus, total enterprise value.

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

For investments that have not undergone restructuring, the analysis excludes any interest and principal payments that have subsequently reduced EPOF II s basis and, thus, total enterprise value. 3 Net leverage that sits ahead of Oaktree’s senior-most investment.

22

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

($/€ i illi )1

European Principal Funds – Investment Performance Summary

($/€ in millions)1

Committed Period of

Weighted Average Holding Invested

ValueInternal

Rate of Return5Total Value as Multiple of Invested

Fund Capital Investment3g

Period4 Capital Profit/Loss Capital6Realized Unrealized Total Gross Net

EPOF I $ 495.0 2006-2010 3.7 $ 461.9 $115.8 $ 730.2 $ 846.0 $384.1 18.0% 13.0% 1.8xEPOF II €1,759.02 2007-Present 1.2 €1,236.3 €549.7 €1,111.7 €1,661.4 €425.1 29.0% 15.0% 1.3x

1 Because EPOF I and EPOF II are denominated in different currencies, totals have been excluded.2 Based on the euro/U.S. dollar exchange rate at the final closing. 3 Includes the period in which follow-on investments are made. 4 The weighted average holding period is defined as the number of years required to equate the gross IRR of the investment cash flows to the multiple of invested capital.5 The internal rate of return (“IRR”) represents the since inception annualized implied discount rate calculated from a series of investment cash flows. The investment-level IRR is the return that

equates the present value of all capital invested in an investment to the present value of all returns of capital, or the discount rate that will provide a net present value of all cash flows equal to zero. Gross investment-level IRRs reflect returns on an investment-by-investment basis before allocation of the management fee general fund expenses income earned on cash and cash equivalents andGross investment-level IRRs reflect returns on an investment-by-investment basis before allocation of the management fee, general fund expenses, income earned on cash and cash equivalents, and any carried interest to the general partners, but after any direct investment expenses and profit allocations to third parties. Because the carried interest allocated to the general partners is not calculated on an investment-by-investment basis, but on an aggregate fund-by-fund basis only, comparable after-fee IRRs on an investment-by-investment basis are not available. The net IRR is presented on a fund-level basis and reflects the actual timing of cash contributions from and distributions to the limited partners and the net asset value of the limited partners’ capital accounts, derived using a valuation methodology at the end of the period, after allocation of management fees, general fund expenses and any carried interest to the general partners.

6 Total Value as Multiple of Invested Capital represents total profit generated at the investment level as a multiple of invested capital. While this metric is similar to Total Value as Multiple of Cost, it is based on investment-level performance (as opposed to fund-level performance), is calculated before fees, expenses and any incentive allocation or carried interest and includes recycled capital. It is typically used for private equity funds that have a smaller number of core investments, which is why it is being provided for the European Principal Funds.

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

23

As of September 30, 2010.Refer to additional performance disclosures beginning on page 31.

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

Case Study: Countrywide

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 201124

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

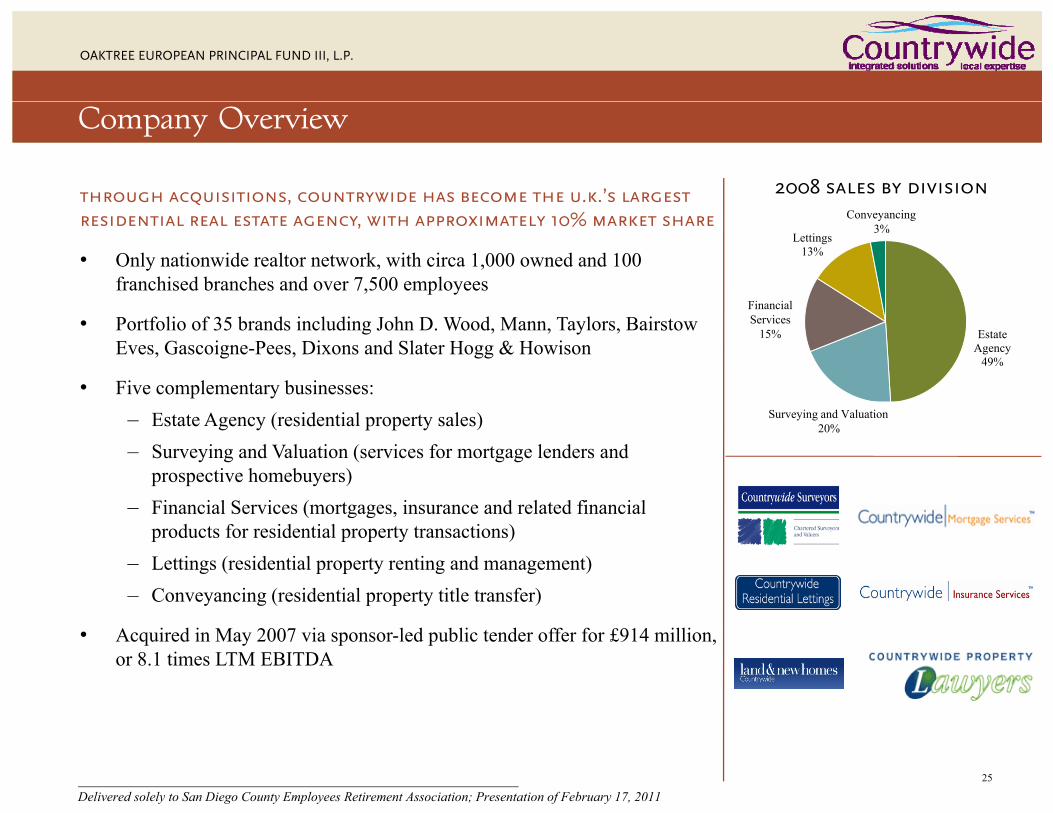

through acquisitions, countrywide has become the u.k.’s largest

Company Overview

2008 sales by divisionq ,residential real estate agency, with approximately 10% market share

• Only nationwide realtor network, with circa 1,000 owned and 100 franchised branches and over 7,500 employees

Lettings13%

Financial

Conveyancing 3%

• Portfolio of 35 brands including John D. Wood, Mann, Taylors, Bairstow Eves, Gascoigne-Pees, Dixons and Slater Hogg & Howison

• Five complementary businesses:

Estate Agency

49%

Financial Services

15%

– Estate Agency (residential property sales)– Surveying and Valuation (services for mortgage lenders and

prospective homebuyers)– Financial Services (mortgages insurance and related financial

Surveying and Valuation 20%

– Financial Services (mortgages, insurance and related financial products for residential property transactions)

– Lettings (residential property renting and management)– Conveyancing (residential property title transfer)

• Acquired in May 2007 via sponsor-led public tender offer for £914 million, or 8.1 times LTM EBITDA

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 201125

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

Transaction Overview

• In early 2008, the collapse of Northern Rock adversely impacted the U.K. mortgage market and, consequently, the number and value of housing transactions, resulting in a precipitous decline in Countrywide’s earnings

– From August 2007 to August 2008, transaction volume fell by 72% and average prices fell by 13%– Countrywide’s run-rate EBITDA was negative by year-end

• Beginning in 3Q08 EPOF II began accumulating a significant position in the company’s super senior revolver and• Beginning in 3Q08, EPOF II began accumulating a significant position in the company s super-senior revolver and secured floating rate notes (“FRNs”) at discounted prices, ultimately becoming the largest debt holder

• Subsequently, we negotiated a restructuring with the sponsor in which EPOF II would become Countrywide’s largest shareholder, and the company’s debt would be reduced significantly

• Simultaneous with the closing of the restructuring, the company completed an equity offering at the same valuation, 87.5% of which was offered to FRN holders with the remainder offered to unsecured note holders

• As a result of the foregoing, EPOF II became the company’s largest shareholder, with a 32% equity stake, and remained the largest debt holder with 31% of the new notesthe largest debt holder, with 31% of the new notes

based on this ownership, creation value (i.e. the enterprise value required in order for epof ii to recover its invested cost) is only one-fifth of the

former sponsor’s purchase price and 1 6 times countrywide’s peak ebitda

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

26

former sponsor s purchase price, and 1.6 times countrywide s peak ebitda

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

Investment Thesis

strengths risks• Leading share and brands offer attractive cyclical

play on the recovery of the U.K.’s residential property market

• Longer-than-expected downturn in the U.K. housing market (mitigated by post-restructuring capital structure)

• Broad and synergistic services capture multiple revenue streams

• Lettings division under-managed historically, with

• Potential loss of material contracts in the conveyancing division

• Highly competitive market with low barriers to g g yopportunity for growth and operational improvement

• Expectation of taking share during downturn and recovery due to quality of management and scale

g y pentry

• Evolution toward internet-based, virtual-agent model

• Significant cost savings from integrating prior acquisitions

• Meaningful potential for further consolidation• Meaningful potential for further consolidation

• Historically high cash flow conversion due to low capex and working capital requirements

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

27

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

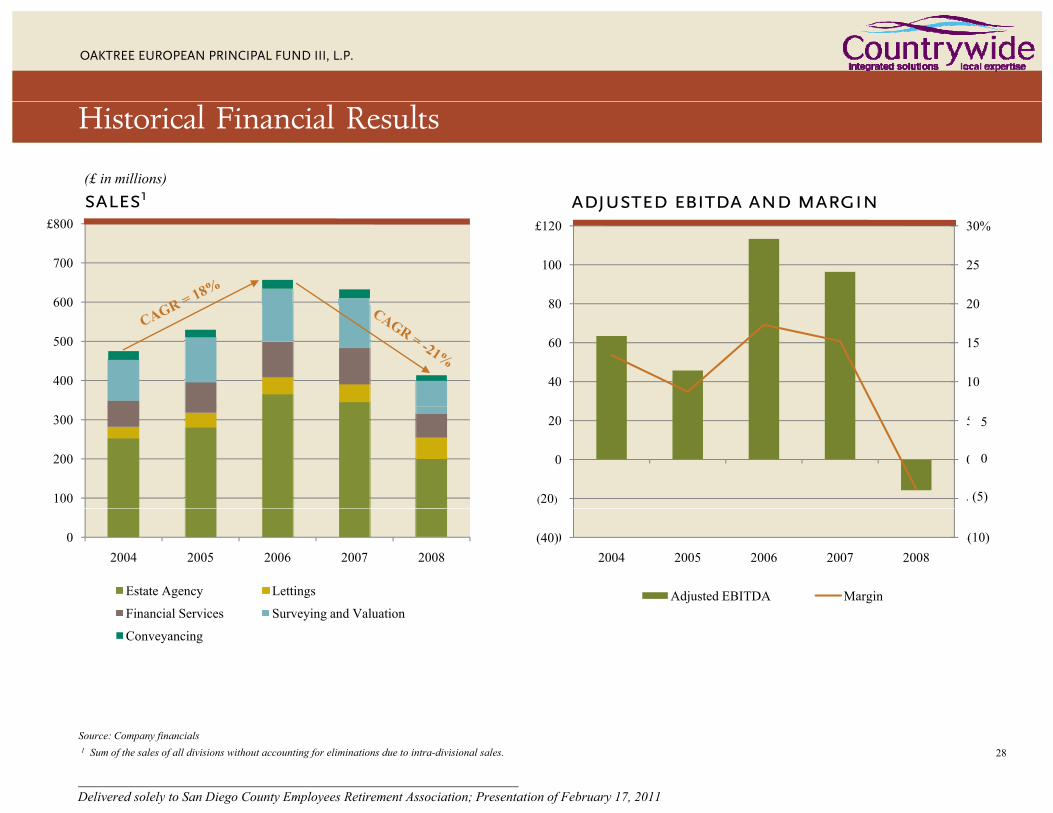

(£ in millions)

Historical Financial Results

sales1 adjusted ebitda and margin

20

25

30%

80

100

£120

sales adjusted ebitda and margin

600

700

£800

10

15

20

40

60

80

400

500

600

-5

0

5

-20

0

20

100

200

300

(20) (5)

5

0

-10 -402004 2005 2006 2007 2008

Adjusted EBITDA Margin

02004 2005 2006 2007 2008

Estate Agency Lettings

Fi i l S i S i d V l ti

(40) (10)

Financial Services Surveying and Valuation

Conveyancing

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

Source: Company financials 1 Sum of the sales of all divisions without accounting for eliminations due to intra-divisional sales. 28

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

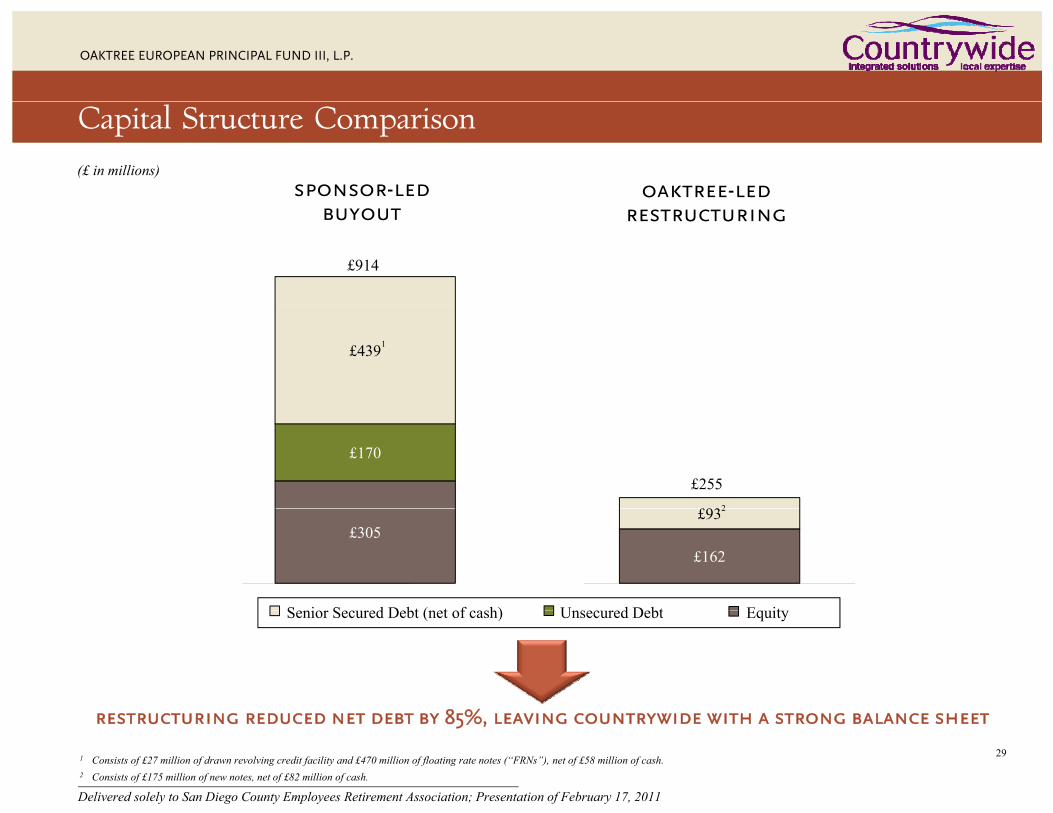

Capital Structure Comparison

sponsor-led oaktree-led(£ in millions)

buyout restructuring

£914

£4391

£170

£93

£2552

£305£162

£93

S i S d D bt ( t f h) U d D bt E it

2

8 %

Senior Secured Debt (net of cash) Unsecured Debt Equity

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

restructuring reduced net debt by 85%, leaving countrywide with a strong balance sheet

1 Consists of £27 million of drawn revolving credit facility and £470 million of floating rate notes (“FRNs”), net of £58 million of cash. 2 Consists of £175 million of new notes, net of £82 million of cash.

29

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

Action Plan and Outlook

• Detailed action plan includes:– Optimize branch network– Rationalize inefficient and redundant back-office infrastructure– Develop lettings division– Streamline organizational structure– Enhance IT and web-based offering – Exit small but distracting non-core activities

• We believe we have acquired, on a low-cost, limited-risk basis, an excellent platform to benefit from any eventual improvement in the U.K. residential real estate market

– Countrywide’s capital structure is significantly deleveraged, providing the company with meaningful staying power in the event the housing market’s recovery is drawn outpowe e eve e ous g e s ecove y s d w ou

– The company has the ability to pay interest on its debt in kind, and EPOF II is the largest holder of this debt, creating significant flexibility

– The 300,000 annualized housing transactions at the end of February 2009 are just one-fourth of the lowest b f l h i t ti i th l t 25number of annual housing transactions in the last 25 years

– At their current depressed level, any surprises with respect to the number of housing transactions are likely to be to the upside

– If home sales recover even moderately, we manage Countrywide skillfully, and the company’s value returns

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

y g y y p yto even half the old buyout price, our profits should be substantial

30

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

Prospective investors and their representatives may contact representatives of the Fund to ask questions about the procedures and methodologies used to calculate the investment

Corporate and government bonds and other marketable securities that are not listed or admitted to trading on any securities exchange are valued at the average mean of the last bid and ask

Performance Information and Disclosures

q p greturns and other information provided herein and to discuss any other questions they may have. The information set forth herein is intended solely to provide potential investors with information about prior transactions consummated by similar funds and entities managed by Oaktree or its principals. Neither the investment performance summary information contained herein nor information otherwise provided to potential investors in the Fund should be construed or relied upon as indications of the future performance of the Fund. Past performance is not indicative of future results.

prices on the valuation date based on quotations supplied by recognized quotation services or by reputable broker dealers.

Non-publicly traded securities, other securities or instruments for which reliable market quotations are not available, securities or instruments for which the General Partner determines in its discretion that the foregoing valuation methods do not represent the fair value of such securities or instruments and other private investments may be initially valued at the acquisition price as the best indicator of fair value. Valuations will depend on facts andp p

There can be no assurance that investment returns similar to any Oaktree fund, or any combination of Oaktree funds, will be achieved. Moreover, wherever there is the potential for profit, there is also the possibility of loss.

In reviewing the performance tables included herein, please note the following:

valuation methodology

acquisition price as the best indicator of fair value. Valuations will depend on facts and circumstances known as of the valuation date and the application of certain valuation methodologies, pursuant to which the General Partner will generally seek to establish the market value of the portfolio investment using one or a combination of income capitalization and sales comparison approaches. These approaches take into account specific financial measures (such as EBITDA, adjusted EBITDA, free cash flow, net income, book value or net asset value) believed to be most relevant for the given investment. Consideration may also be given to such factors as the acquisition price of the security, discounted cash flow valuations, historical and projected operational and financial results for the portfolio company the

For purposes of all performance data set forth in this presentation, securities or instruments for which reliable market quotations were not available (including securities or instruments having a public market price that Oaktree determined did not fairly represent the fair value of such securities or instruments), were valued at their “fair value” as determined in the sole discretion of Oaktree, taking into account all factors, information, and data deemed to be pertinent, in accordance with U.S. GAAP. GAAP requires that a “fair value” be assigned to all assets and establishes a single authoritative

historical and projected operational and financial results for the portfolio company, the strengths and weaknesses of the portfolio company relative to market comparables, valuations of comparable companies, industry trends, general economic and market conditions and other factors deemed relevant.

The valuation of a portfolio company’s securities may be impacted by expectations of investors’ receptiveness to a public offering of the portfolio company’s securities, the size of the holding of the portfolio company’s securities and any associated control, information with requires that a fair value be assigned to all assets and establishes a single authoritative

definition of fair value that includes a framework for measuring fair value and enhanced disclosures about fair value that includes measurements. The hierarchal disclosure framework prioritizes the inputs used in measuring investments at fair value into three levels based on their market price observability. Market price observability is affected by a number of factors, including the type of investment and the characteristics specific to the investment. Investments with readily available quoted prices from an active market or for which fair value can be measured based on actively quoted prices generally will have

hi h d f k t i b bilit d l d f j d t i h t i

respect to transactions or offers for the portfolio company’s securities (including the transaction pursuant to which the investment was made and the period of time elapsed from the date of the investment to the valuation date) and applicable restrictions on the transferability of the portfolio company’s securities.

These valuation methodologies involve a significant degree of management judgment. Accordingly, valuations by the General Partner do not necessarily represent the amounts which may eventually be realized from sales or other dispositions of investments. Estimated fair a higher degree of market price observability and a lesser degree of judgment inherent in

measuring fair value.

Securities listed on one or more national securities exchanges are valued at their last reported sales price on the date of valuation. If no sale occurred on the valuation date, the security is valued at the mean of the last “bid” and “ask” prices on the valuation date. Securities that are not listed on a national securities exchange are valued at a price equal to either (a) in the case of any security designated as a National Market System Security

y y pvalues may differ from the values that would have been used had a ready market for the investment existed, and the differences could be material to the financial statements.

Investments measured and reported at fair value are classified and disclosed in one of the following categories:

• Level I – Quoted unadjusted prices for identical instruments in active markets to which the General Partner has access at the date of measurement.

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

and traded on NASDAQ, its last sales price on the date of determination on NASDAQ or (b) in the case of other securities, the mean of the last bid and ask prices on the valuation date as reported by NASDAQ. Securities that are not marketable due to legal restrictions that may limit or restrict transferability are generally valued at a discount from quoted market prices, as determined by the General Partner.

the General Partner has access at the date of measurement.

31

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

• Level II – Quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model derived

no benchmark

Performance Information and Disclosures (continued)

identical or similar instruments in markets that are not active; and model derived valuations in which all significant inputs are directly or indirectly observable. Level II inputs include prices in markets for which there are few transactions, the prices are not current, little public information exists or instances where prices vary substantially over time or among brokered market makers, as well as interest rates, yield curves, volatilities, prepayment speeds, loss severities, credit risks and default rates.

No benchmarks are presented in this presentation, as Oaktree is not aware of any benchmarks that, in Oaktree’s opinion, provide a basis for measuring the performance of the relevant funds, particularly in light of the managers’ investment philosophy, strategy and implementation.

• Level III – Model derived valuations in which one or more significant inputs or significant value drivers are unobservable. Unobservable inputs are those inputs that reflect the General Partner’s own assumptions about the assumptions market participants would use to price the investment based on the best available information.

In some instances, inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such instances, the investment’s level within the fair value y ,hierarchy is based on the lowest level of input that is significant to the value measurement. The General Partner’s assessment of the significance of an input requires judgment and considers factors specific to the investment.

past performance is not indicative of future results

There can be no assurance that the Fund will be able to earn the rates of return indicated in this presentation. Moreover, wherever there is the potential for profit, there is also thein this presentation. Moreover, wherever there is the potential for profit, there is also the possibility of loss. Prospective investors should note that the internal rates of return (“IRRs”) set forth in this presentation are based on valuations of investments in companies that have not been fully realized as of September 30, 2010. There can be no assurance that any of these valuations will be attained as actual realized returns will depend upon, among other factors, future operating results, the value of the assets and market conditions at the time of disposition, any related transaction costs and the timing and manner of sale, all of which may differ from the assumptions upon which the valuations contained herein are based Consequently the actual realized returns mayvaluations contained herein are based. Consequently, the actual realized returns may differ materially from the current returns indicated in this presentation. Nothing contained herein should be deemed to be a prediction or projection of future performance of the Fund.

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

32

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

use of case studies

Performance Information and Disclosures (continued)

The case study presented in this brochure relates to an investment made by OCM European Principal Opportunities Fund II, L.P. (“EPOF II”). The EPOF II investment that is the subject of the case study was selected because it is an illustrative example of a recent restructuring transaction in one of the core markets for the strategy. In addition, this particular investment is one which illustrates the full range of capabilities of the European Principal Group and how it approaches a complex opportunity. The investment presented in the case study, however, may be more favorable than other investments made by EPOF II and OCM European Principal Opportunities Fund, L.P. (together the “European Principal Funds”). Additionally, the investment presented in the case study may be more favorable than, and not representative of, all the investments that may be made by the Fund. If you would like additional information regarding any other investment of the European Principal Funds not presented here, please contact Oaktree. The purpose of the case study is intended to give the recipient of this brochure a general understanding of the range of Oaktree’s European Principal Group strategy, as well as an understanding of the amounts invested in the selected investment. As a result, the caseunderstanding of the amounts invested in the selected investment. As a result, the case study is not intended to be, and should not be read as, a full and complete description of the investment transaction underlying the case study. If the recipient would like additional details regarding the case study, please contact Oaktree. Further, for a listing of all control investments made by the European Principal Funds and the related returns as of September 30, 2010, see page 20 of this brochure.

The case study is provided for informational purposes only. Neither Oaktree nor its affiliates make any representation and it should not be assumed that past investmentaffiliates make any representation, and it should not be assumed, that past investment performance is an indication of future returns, and there can be no assurance that the Fund will be able to earn the rates of return indicated in the case study. Wherever there is the potential for profit there is also the possibility of loss.

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

33

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

An investment in the Fund is speculative and involves a high degree of risk. An i t t h ld l b d ft lt ti ith i d d t lifi d

investment environment

Legal Information and Disclosures

investment should only be made after consultation with independent qualified sources of investment and tax advice. Such risks include, but are not limited to, the following:

investments

The Fund will invest in securities and obligations that entail substantial risk, including investments in private or public equity interests and debt securities, options, short sales,

Many factors affect the appeal and availability of investments in companies that are the focus of the Fund. Although Oaktree sees changes in these factors indicating a trend towards increased opportunities and value creation, there can be no assurance that such changes will continue. In addition, legal and regulatory changes could occur during the term of the Fund that may adversely affect the Fund.

risks in effecting operating improvementshigh yield and preferred securities, and other obligations such as bank loans and participations. There can be no assurance that the Fund’s investments will increase in value, that the Fund will not incur significant losses or that the objectives of the Fund will be achieved. In addition, the Fund’s investments may result in the Fund incurring significant costs, fees and expenses, including legal, advisory and consulting fees and expenses, costs of regulatory compliance and costs of defending third-party litigation.

unspecified use of proceeds

In some cases, the success of the Fund’s investment strategy will depend, in part, on the ability of the Fund to restructure and effect improvements in the operations of a portfolio company. The activity of identifying and implementing restructuring programs and operating improvements at portfolio companies entails a high degree of uncertainty. There can be no assurance that the Fund will be able to successfully identify and implement such restructuring programs and improvements.

illiquidity u u

Investors in the Fund will not have an opportunity to evaluate for themselves the relevant economic, financial and other information regarding the investments by the Fund. No assurance can be given that the Fund will be successful in obtaining suitable investments or that, if the investments are made, the objectives of the Fund will be achieved.

lack of diversification

The F nd ma in est p to the greater of €600 million or 20% of Capital Commitments

illiquidity

Participation in the Fund will generally be an illiquid investment. Investors will not be permitted to withdraw from the Fund and may only in limited circumstances transfer their interests in the Fund. Furthermore, a significant portion of the Fund’s assets may consist of illiquid securities or securities which are restricted as to their transferability. This factor may limit the ability of the Fund to sell such securities at their fair market value.

options and short salesThe Fund may invest up to the greater of €600 million or 20% of Capital Commitments based on cost in any one portfolio company and will be under no other obligation to further diversify its investments. Accordingly, the investment portfolio of the Fund may be subject to more rapid changes in value than would be the case if the Fund were required to maintain a wide diversification among companies, industries, and types of securities.

foreign investments

options and short sales

The Fund may purchase and sell covered and uncovered put and call options. There can be no assurance that the price movements of the securities underlying such options will not result in significant losses to the Fund. Further, the Fund may sell securities short for the purpose of hedging an existing investment of the Fund. A short sale involves the risk of a theoretically unlimited loss from a theoretically unlimited gain in the market price of the security sold short. Furthermore, there can be no assurance that the Fund will be able to purchase the securities necessary to cover a short position.

The Fund may invest in entities operating and/or organized in a variety of countries. Such investments will involve special risks including the risk of nationalization of assets, currency exchange rate fluctuations, higher rates of inflation, controls on foreign investment, limitations on repatriation of capital, differences in auditing and financial reporting standards and limited due diligence review. Additionally, there may be economic risks associated with such investments as well as the risk of potential political, social and diplomatic changes within such countries. These risks may increase expenses of the Fund, adversely affect the value of the Fund’s investments and adversely impact the

no right to control the fund’s operations

Limited Partners will have no opportunity to control the day-to-day operations of the Fund, including investment and disposition decisions. In order to safeguard their limited liability for the liabilities and obligations of the Fund, Limited Partners must rely entirely on the General Partner to conduct and manage the affairs of the Fund.

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

, y y pFund’s investment program and strategy.

34

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

currency and foreign exchange

Distributions by the Fund will generally be made in euros. However, Oaktree anticipates

through foreign or domestic corporations subject to corporate income tax or otherwise utilize structures that are less efficient than structures that would have been used in the absence of the need to comply with the qualifying income requirement Oaktree also has long-term

Legal Information and Disclosures (continued)

y g y pthat some of the Fund’s investments will be denominated in currencies other than the Euro. Changes in the rates of exchange between the Euro and other currencies may have an adverse effect on the performance of the Fund.

tax matters

Some countries in which the Fund may invest impose taxes on certain types of income, such as dividends, interest and in some instances capital gains. Although such taxes may

need to comply with the qualifying income requirement. Oaktree also has long term relationships with companies, individuals and investors that may influence the decisions made by it on behalf of the Fund.

additional capital

Certain of the Fund’s investments may require additional financing to satisfy working capital needs or acquisition strategies and may have to raise capital at a price unfavorable to the Fund.

p g g ybe subject to reduction to the extent that Limited Partners are entitled to the benefits of an income tax treaty between their home jurisdiction and the other jurisdictions in which the Fund invests, there can be no assurance that treaty benefits will be available in any particular case, as this will be dependent on the terms of the treaty and the timely provision of certifications and other documentation. Furthermore, even if Limited Partners are entitled to treaty benefits, withholding taxes may still be deducted by the payers of income, with a material time delay before refunds of such withholding taxes can be obtained from the relevant taxing authority. In addition, changes in the tax laws or tax t ti ( th i i t t ti ) f th t i i hi h th F d i t l

bridge financing

The Fund may provide bridge financing in connection with one or more of its equity investments. The Fund will bear the risk of any changes in capital markets, which may adversely affect the ability of a portfolio company to refinance any bridge investments. If the portfolio company were unable to complete a refinancing, the Fund could have a long-term investment in a junior security or that junior security might be converted to equity.

treaties (or their interpretation) of the countries in which the Fund invests may severely and adversely affect the Fund’s ability to efficiently realize income or capital gains and may subject the Fund and/or the Limited Partners to tax and return filing obligations in such countries. Also, there can be no assurance that the Fund’s distributions will be sufficient to satisfy any U.S. federal, state, local or foreign income taxes imposed on the Limited Partners in respect of their distributive shares of the Fund’s taxable income.

nature of bankruptcy proceedings

strategic and other investors

The General Partner may in its sole discretion offer strategic and other investors (including one or more Limited Partners) the opportunity to participate in one or more Fund investments.

material, non-public information

In connection with the operation of the Fund or other activities, personnel of Oaktree may i t i l bli i f ti b t i t d f i iti ti t ti i t i

The Fund may make investments that could require substantial workout negotiations or restructuring in the event of a default or bankruptcy, which could entail significant risks, time commitments and costs.

leverage

The Fund’s investments are expected to include companies whose capital structures may have significant leverage Such investments are inherently more sensitive than others to

acquire material, non-public information or be restricted from initiating transactions in certain securities. The Fund will not be free to act upon any such information and may not be able to initiate transactions that it otherwise might have initiated.

control person liability

The Fund’s exercise of control of, or significant influence in, a company in which it invests may impose additional risks of liability, such as liability for environmental damage or product d f t th t f li bilit i hi h th li it d li bilit ll h t i ti fhave significant leverage. Such investments are inherently more sensitive than others to

declines in revenues and to increases in expenses and interest rates.

potential conflicts of interest

Oaktree and its affiliates manage other investments, funds, and accounts which present the possibility of overlapping investments, and thus the potential for conflicts of interest with the Fund. In addition, in May 2007, the indirect parent of the General Partner, Oaktree Capital Group, LLC (“OCG”), became a “publicly traded partnership” within the meaning

defects or other types of liability in which the limited liability generally characteristic of business ownership may be ignored.

contingent liabilities on disposition of investments

The Fund may be required to indemnify the purchasers of the investments it sells. In that regard, Limited Partners may be required to return amounts distributed to them to fund the Fund’s indemnity obligations.

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

Capital Group, LLC ( OCG ), became a publicly traded partnership within the meaning of section 7704(b) of the Code. As a result, at least 90% of OCG’s gross income for every taxable year must consist of “qualifying income” as defined in section 7704 of the Code in order for OCG to avoid being treated as a corporation for U.S. federal income tax purposes. It is possible that the General Partner may cause the Fund to make investments

35

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

investment company act

The Fund will not be registered under the Investment Company Act, and therefore,

Legal Information and Disclosures (continued)

g p yinvestors in the Fund will not be accorded the protections of the Investment Company Act.

regulatory risks

In recent years, market disruptions and the dramatic increase in the capital allocated to alternative investment strategies have led to increased governmental as well as self-regulatory scrutiny of the alternative investment fund industry in general, and certain l i l i i l i f h i d i di ll i id d b hlegislation proposing greater regulation of the industry periodically is considered by the U.S. Congress and the U.S. Securities and Exchange Commission, as well as the governing bodies of non-U.S. jurisdictions. It is impossible to predict what, if any, changes in the regulations applicable to the Fund, the general partner, Oaktree, the markets in which they trade and invest or the counterparties with which they do business may be instituted in the future. The effect of any future regulatory change could be substantial and adverse.

institutional risk

The institutions, including brokerage firms and banks, with which the Fund directly or indirectly will do business (including swap counterparties), or to which securities will be entrusted for custodial and prime brokerage purposes, may encounter financial difficulties, fail or otherwise become unable to meet their obligations. In light of recent market turmoil and overall weakening of the financial services industry, the Fund, its prime broker(s) and other financial institutions' financial condition may be adversely affected and they may become subject to legal, regulatory, reputational or other unforeseen risks that could have a material adverse effect on the business and operations of the Fund.

Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. The Fund, Oaktree Capital Management, L.P. and their affiliates believe that such information is accurate and that the sources from which it has been obtained are reliable; however, they cannot guarantee the accuracy of such information and have not independently verified the accuracy or completeness of such information or the assumptions on which such information is based. Moreover, independent third-party sources cited in this brochure are not making any representations or warranties regarding any information attributed to them and shall have no liability in connection with the

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

information attributed to them and shall have no liability in connection with the use of such information in this brochure.

36

OAKTREE U.S. HIGH YIELD BOND MANAGEMENTOAKTREE EUROPEAN PRINCIPAL FUND III, L.P.

Marketing DisclosuresAUSTRALIA, BERMUDA, CANADA, AND UNITED STATES

This brochure is being provided to persons in these countries by OCM® Investments, LLC (Member FINRA) a subsidiary of Oaktree Persons in these countries should direct all

JAPAN, SINGAPORE, AND SOUTH KOREA

This brochure is being provided to persons in these countries by Oaktree European Principal Fund III GP L P the general partner of the Fund with respect to information relating to the(Member FINRA), a subsidiary of Oaktree. Persons in these countries should direct all

inquiries regarding the Fund to a marketing representative of OCM Investments, LLC.Fund III GP, L.P., the general partner of the Fund, with respect to information relating to the Fund and its related feeder funds. Persons in these countries should direct all inquiries regarding the Fund and its related feeder funds to a representative of Oaktree European Principal Fund III GP, L.P.ocm investments, llc

333 S. Grand Avenue, 28th FloorLos Angeles, CA 90071Tel: +1 213 830 6300

1301 Avenue of the Americas, 34th FloorNew York, NY 10019Tel: +1 212 284 1900

oaktree european principal fund iii gp, l.p.

c/o Oaktree Capital Management, L.P.

AUSTRIA, BELGIUM, DENMARK, FINLAND, FRANCE, GERMANY, ICELAND, IRELAND, ISRAEL, ITALY, KUWAIT, LIECHTENSTEIN, LUXEMBOURG, NETHERLANDS, NORWAY, OMAN, QATAR, SPAIN, SWEDEN, SWITZERLAND, UNITED ARAB EMIRATES, AND UNITED KINGDOM

BRUNEI DARUSSALAM, HONG KONG, NEW ZEALAND, PEOPLE’S REPUBLIC OF CHINA TAIWAN AND THAILAND

333 S. Grand Avenue, 28th FloorLos Angeles, CA 90071Tel: +1 213 830 6300

This brochure is being provided to persons in these countries by Oaktree Capital Management Limited, an affiliate of Oaktree. Persons in these countries should direct all inquiries regarding the Fund to a marketing representative of Oaktree Capital Management Limited.

Oaktree Capital Management Limited and other affiliated entities manage various funds that are unregulated collective investment schemes and that cannot be promoted to the general public in the U K or dealt in by any person in the U K other than by persons authorised or

OF CHINA, TAIWAN, AND THAILAND

This brochure is being provided to persons in these countries by Oaktree Capital (Hong Kong) Ltd., an affiliate of Oaktree. Persons in these countries should direct all inquiries regarding the Fund to a marketing representative of Oaktree Capital (Hong Kong) Ltd.

Oaktree Capital (Hong Kong) Ltd. is a corporation licensed by the Hong Kong Securities and Futures Commission to conduct Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities on the basis that eachpublic in the U.K. or dealt in by any person in the U.K. other than by persons authorised or

exempt under the Financial Services and Markets Act 2000 (“FSMA”). This presentation is issued in the U.K. only to restricted categories of recipients, namely persons falling within article 14 (Investment Professionals) and article 22 (High Net Worth Companies etc.) of the Financial Services and Markets Act 2000 (Promotion of Collective Investment Schemes) (Exemptions) Order 2001 and to other categories of investors to whom unregulated collective investment schemes can be marketed without contravening Section 238 of the FSMA. Transmission of this presentation to any other person in the U.K. is unauthorised

securities), and Type 9 (asset management) regulated activities, on the basis that each recipient of this brochure in these countries is a Professional Investor as defined in the Hong Kong Securities and Futures Ordinance (the “Ordinance”). By accepting this brochure, each recipient of this brochure in these countries acknowledges and agrees that this brochure is provided for its use only and it will not distribute or otherwise make this brochure available to a person who is not a Professional Investor as defined in the Ordinance.

oaktree capital (hong kong) ltd. FSMA. Transmission of this presentation to any other person in the U.K. is unauthorisedand may contravene the FSMA.

Oaktree Capital Management Limited is authorised and regulated by the Financial Services Authority of the United Kingdom (the “FSA”). It is entered in the FSA’s register with register number 3592405. Its registered office is at 27 Knightsbridge London SW1X 7LY.

oaktree capital management limited

( )

Suite 2001, AIA Central1 Connaught Road CentralHong KongTel: +852 3655 6800

Delivered solely to San Diego County Employees Retirement Association; Presentation of February 17, 2011

27 Knightsbridge, 4th FloorLondon, SW1X 7LY, United KingdomTel: +44 207 201 4600

37

Related Documents