Lecture Lecture 2 Accounting Cycle (I) R di E i - Recording Economic Activities

NUS ACC1002X Lecture 2 Accounting Cycle (I) - Recording

Oct 28, 2015

The lecture notes by Dr. Vincent Chen for NUS module ACC1002X Financial Accounting.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

LectureLecture

2

Accounting Cycle (I)

R di E i- Recording Economic Activities

Steps in accounting cycle and basic concepts of

accounting records

by Vincent Chen 2

S f A ti C lSequence of Accounting Cycle

1. Analyze transactions2. Record the effects of transactions3. Summarize the effects of transactions

• Posting journal entries• Preparing a trial balance

4. Prepare financial reports (Lecture 3)• Adjusting entries• Preparing financial statements

Cl i th b kby Vincent Chen 3

• Closing the books

Basic Concepts

• Account and Ledger

Basic Concepts

Account and Ledger

CashAccounts are individual Cash

Accounts

records showing increasesand decreases.

The entire group of accounts is kept together

Accounts Payable

C it laccounts is kept together in an accounting record

called a ledger.

Capital Stock

by Vincent Chen 4

Basic Concepts

• The use of accounts

Basic Concepts

The use of accounts– Increases are recorded on one side of the T-account,

and decreases are recorded on the other side.

Title of the Account

Debit Credit

by Vincent Chen 5

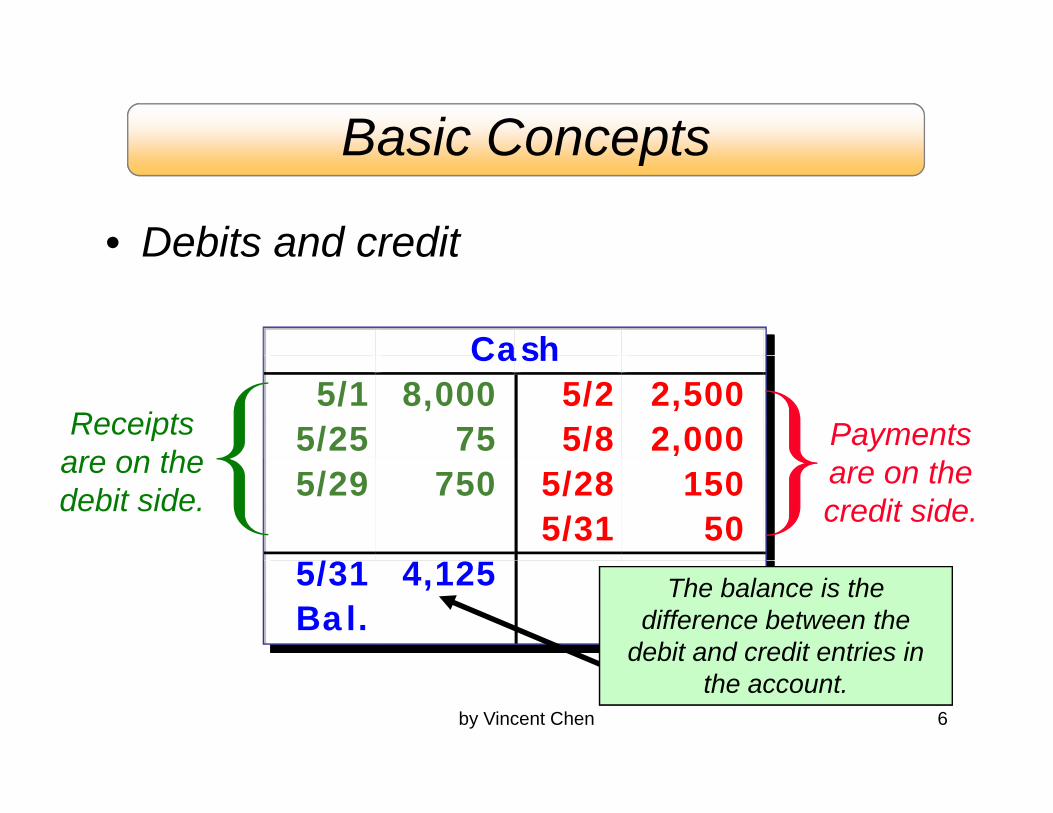

Basic Concepts

• Debits and credit

Basic Concepts

Cash

Debits and credit

Cash5/1 8,000 5/2 2,500

5/25 75 5/8 2,000Receipts are on the

Payments 5/29 750 5/28 150

5/31 50 /

are on the debit side.

are on the credit side.

5/31 4,125Ba l.

The balance is the difference between the

debit and credit entries in

by Vincent Chen 6

the account.

Basic Concepts

Debits and credits affect accounts as follows:

Basic Concepts

Debits and credits affect accounts as follows:

AA = LL + OEOEASSETSASSETS EQUITIESEQUITIESLIABILITIESLIABILITIES

Debit for Increase

Credit for Decrease

Debit for Decrease

Credit for Increase

Debit for Decrease

Credit for Increase

by Vincent Chen 7

Basic Concepts• Double entry system

Basic Concepts

– Each transaction is recorded with at least one debit and one credit

– For every transaction, total debits must be equal to total creditsf (– Total debits must be equal to total credits of all accounts (must

be balanced)

AA = LL + OEOEDebit Debit Credit Credit

by Vincent Chen 8

balancesbalances balancesbalances

Step 1 Analyzing TransactionsTransactions

by Vincent Chen 9

Step 1 Analyzing TransactionsStep 1 Analyzing Transactions

• Is this transaction related to the company?– Entity principle: only record economic

activities to a specific business entity

• How does this transaction affect the• How does this transaction affect the financial positions of the company

Use debit and credit and the equality– Use debit and credit and the equality

Assets = Liabilities + Owners’ Equityby Vincent Chen 10

q y

Example 1: May 1: Jack and his family investedExample 1: May 1: Jack and his family invested $8,000 in NUS Lawn Care Service and received 800 shares of stock.

Will Cash increase Will Capital Stock increase oror decrease? increase or decrease?

by Vincent Chen 11

Example 1: May 1: Jack and his family investedExample 1: May 1: Jack and his family invested $8,000 in NUS Lawn Care Service and received 800 shares of stock.

Cash increases $8,000 with a

Capital Stock increases $8,000

with a creditdebit. with a credit.

Capital Stock5/1 8,000

Cash5/1 8,000

by Vincent Chen 12

Example 2: May 2: NUS purchased a lawn mower forExample 2: May 2: NUS purchased a lawn mower for $2,500 in cash.

Will Cash increase Will Equipment increase oror decrease? increase or decrease?

by Vincent Chen 13

Example 2: May 2: NUS purchased a lawn mower forExample 2: May 2: NUS purchased a lawn mower for $2,500 in cash.

Cash decreases $2,500 with a

Equipment increases $2,500

with a debitcredit. with a debit.

Equipment5/2 2,500

Cash5/1 8,000 5/2 2,500

by Vincent Chen 14

Step 2 Record the Effects of TransactionsTransactions

by Vincent Chen 15

Step 2 Record the Effects of Transactions

• Journal: Similar to a financial diary, a chronological listing of all businesschronological listing of all business transactions throughout the year

• Journal entry: A recording of a transaction h d bit l t ditwhere debits equal to credits

by Vincent Chen 16

GENERAL JOURNAL (pp.12)

Date Account Titles and Explanation Debit Credit2010

May 1 Cash 8,000Capital Stock 8,000

Owners invest cash in the business.

GENERAL JOURNAL (pp.14)

Date Account Titles and Explanation Debit Credit20102010

May 2 Equipment 2,500Cash 2,500

by Vincent Chen 17

Purchased lawn mower.

Debits and Credits for Revenue and Expense (pp 7)(pp.7)

EQUITIESEQUITIESExpensesExpenses RevenuesRevenuesEQUITIESEQUITIES

Debit for Debit for DecreaseDecrease

Credit for Credit for IncreaseIncrease

Expenses Expenses decrease decrease owners’ owners’

Revenues Revenues increase increase owners’ owners’

equity.equity. equity.equity.

EXPENSESEXPENSES REVENUESREVENUES

Credit for Credit for DecreaseDecrease

Debit for Debit for IncreaseIncrease

Debit for Debit for DecreaseDecrease

Credit for Credit for IncreaseIncrease

by Vincent Chen 18

Investments by and Payments to Owners (pp 7)

EQUITIESEQUITIESPayments to Owners’

(pp.7)

EQUITIESEQUITIES

Debit for Debit for DecreaseDecrease

Credit for Credit for IncreaseIncrease

owners decrease

owners’ equity

investments increase

owners’ equityowners’ equity. owners’ equity.

DIVIDENDSDIVIDENDS CAPITAL STOCKCAPITAL STOCK

Credit for Credit for DecreaseDecrease

Debit for Debit for IncreaseIncrease

Debit for Debit for DecreaseDecrease

Credit for Credit for IncreaseIncrease

by Vincent Chen 19

Step 3 Summarize the effects of transactionseffects of transactions

by Vincent Chen 20

Step 3 Summarize the effects ofStep 3 Summarize the effects of transactions

• Posting (copying) journal entries to• Posting (copying) journal entries to accounts in ledgers

• Preparing a trial balance

by Vincent Chen 21

Step 3 Summarize the effects of transactions

GENERAL JOURNAL

Date Account Titles and Explanation Debit Credit20102010

May 1 Cash 8,000Capital Stock 8,000

Owners invest cash in the business.General LedgerCash

Date Debit Credit Balance2010

M 1 8 000 8 000by Vincent Chen 22

May 1 8,000 8,000

Step 3 Summarize the effects of transactions

GENERAL JOURNALGENERAL JOURNAL

Date Account Titles and Explanation Debit Credit20102010

May 1 Cash 8,000Capital Stock 8,000Capital Stock 8,000

Owners invest cash in the business.General LedgerCapital Stockp

Date Debit Credit Balance2010

by Vincent Chen 23May 1 8,000 8,000

St 3 S i th ff t f t tiStep 3 Summarize the effects of transactions

Leger acco nt after posting• Leger account after posting

General LedgerGeneral LedgerCash

Date Debit Credit Balance2010

May 1 8,000 8,000 2 2,500 5,500

by Vincent Chen 24

St 3 S i th ff t f t tiStep 3 Summarize the effects of transactions

General LedgerGeneral LedgerCash

Date Debit Credit Balance2010

May 1 8,000 8,000 2 2 500 5 5002 2,500 5,500

T accounts are simplified versions of the ledgerT accounts are simplified versions of the ledger account that only show the debit and credit

columns.by Vincent Chen 25

columns.

Step 3 Summarize the effects ofStep 3 Summarize the effects of transactions

• Posting (copying) journal entries to• Posting (copying) journal entries to accounts in ledgers

• Preparing a trial balance

by Vincent Chen 26

All balances are NUS Lawn Care Service

Unadjusted Trial BalanceMay 31, 2010

taken from the ledger accounts on May 31 afterMay 31, 2010

Cash 3,925$ Accounts receivable 75 T l & i t 2 650

on May 31 after considering all of

NUS’s transactions forTools & equipment 2,650

Truck 15,000 Notes payable 13,000$

transactions for the month.

Notes payable 13,000$ Accounts payable 150 Capital stock 8,000 Di id d 200 Proves equality ofDividends 200 Sales revenue 750 Gasoline expense 50

Proves equality of debits and credits.

by Vincent Chen 27

p Total 21,900$ 21,900$

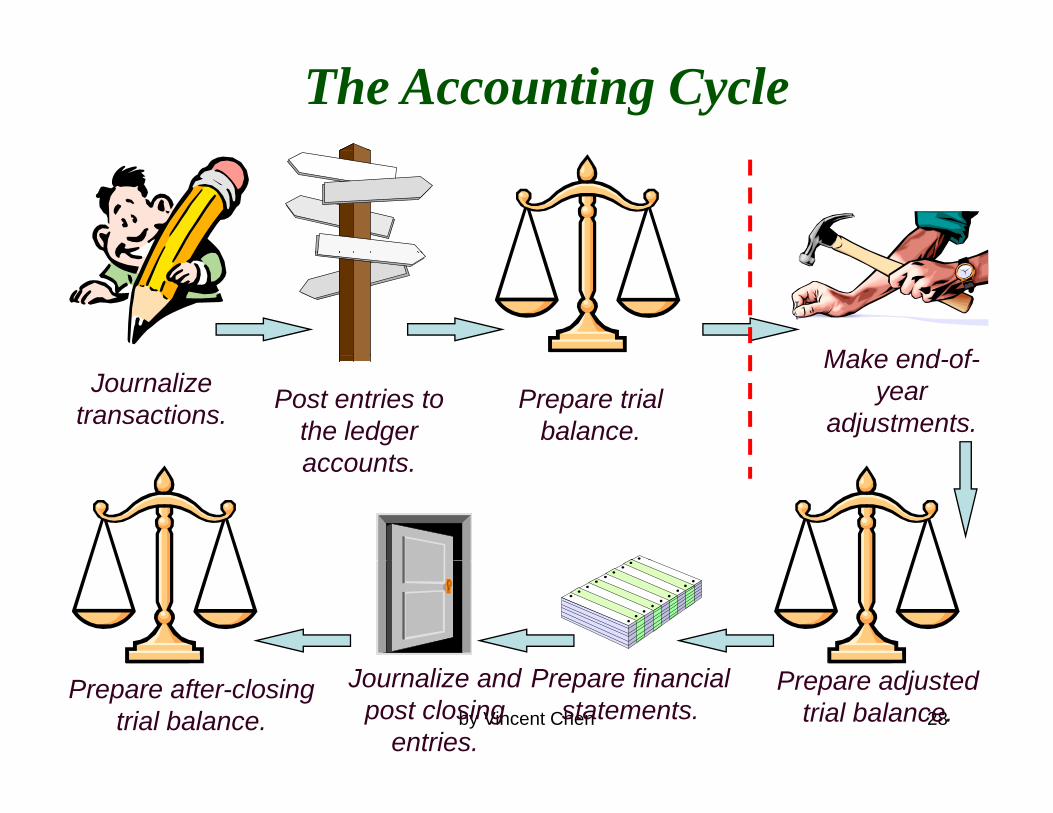

The Accounting Cycle

Make end ofJournalize

transactions. Post entries to the ledger accounts

Prepare trial balance.

Make end-of-year

adjustments.accounts.

by Vincent Chen 28

Prepare adjusted trial balance.

Prepare financial statements.

Prepare after-closing trial balance.

Journalize and post closing

entries.

SummarySummary

• The sequence of accounting cycle

Th f d bit/ dit d d bl t• The use of debit/credit and double entry system to record economic transactions

• Posting journal entries to ledgers

• Use ledgers to prepare a trial balance

by Vincent Chen 29

Related Documents