Vol.1 Issue-2 July – December 2013 Vidyaniketan Journal of Management and Research 57 AN EMPIRICAL STUDY ON NPA MANAGEMENT STRATEGIES BETWEEN PUBLIC AND PRIVATE BANKS – WITH SPECIAL REFERENCE TO BANKS IN BANGALORE CITY. Ranjini . M L. Research Scholar, Centre for Management Studies, Atria tower, Palace road, Jain University, Bangalore Abstract: This Study was undertaken to know the NPA Management Strategies between Public and Private Bank and also to know the recovery mechanism adopted for recovery mechanism adopted for recovery of NPA’s. Non- performing assets are one of the major concerns for banks in India. NPAs reflect the performance of banks. A high level of NPAs suggests high probability of a large number of credit defaults that affect the profitability and net-worth of banks and also erodes the value of the asset. The NPA growth involves the necessity of provisions, which reduces the overall profits and shareholders’ value. The issue of Non Performing Assets has been discussed at length for financial system all over the world. The problem of NPAs is not only affecting the banks but also the whole economy. In fact high level of NPAs in Indian banks is nothing but a reflection of the state of health of the industry and trade. This research deals with understanding the concept of NPAs, its magnitude and major causes for an account becoming non-performing, projection of NPAs over next years in banks and concluding remarks. Key Words : NPA, Public and Private Bank, Management Strategies ,Recovery Mechanism, Profits, Industry and Trade. Introduction: Banking sector plays an indispensable role in economic development of a country through mobilization of savings and deployment of funds to the productive sectors. Bank lending is very crucial for it makes it possible, the financing of agricultural, industrial and commercial activities of the country. It is an established fact that a fragile banking system can, not only hamper the development of a particular economy but also it can deepen the real economic crisis and impose heavy social costs. So the health of the banking system should be one of the primary concerns of the government of each country. Currently the Indian banking sector is not in a good health. The symptoms of the disease are vastly apparent viz. rising NPAs, high labor costs, competition from mutual funds, bureaucratic hurdle and red tapism to name a few. The existing weak banks only compound the problem. Most of these symptoms have been present in the Indian banking system since independence but it is only in the post reform era that they have became more ostensible. Indian Banking Sector: The banking sector in India is currently passing through an exciting and challenging phase. The reform measures have bought about sweeping changes in this vital sector of the country’s economy. The report provides an analysis of the banking sector in india. In the 1970’s and 1980’s the Indian banking industry

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research57

AN EMPIRICAL STUDY ON NPA MANAGEMENT STRATEGIES BETWEEN PUBLIC AND PRIVATE BANKS – WITH SPECIAL REFERENCE TO BANKS IN BANGALORE CITY.

Ranjini . M L.Research Scholar, Centre for Management Studies, Atria tower, Palace road, Jain University, Bangalore

Abstract: This Study was undertaken to know the NPA Management Strategies between Public and Private Bank and also to know the recovery mechanism adopted for recovery mechanism adopted for recovery of NPA’s. Non-performing assets are one of the major concerns for banks in India. NPAs reflect the performance of banks. A high level of NPAs suggests high probability of a large number of credit defaults that affect the profitability and net-worth of banks and also erodes the value of the asset. The NPA growth involves the necessity of provisions, which reduces the overall profits and shareholders’ value. The issue of Non Performing Assets has been discussed at length for financial system all over the world. The problem of NPAs is not only affecting the banks but also the whole economy. In fact high level of NPAs in Indian banks is nothing but a reflection of the state of health of the industry and trade. This research deals with understanding the concept of NPAs, its magnitude and major causes for an account becoming non-performing, projection of NPAs over next years in banks and concluding remarks.

Key Words : NPA, Public and Private Bank, Management Strategies ,Recovery Mechanism, Profits, Industry

and Trade.

Introduction: Banking sector plays an indispensable role in economic development of a country through mobilization of savings and deployment of funds to the productive sectors. Bank lending is very crucial for it makes it possible, the financing of agricultural, industrial and commercial activities of the country. It is an established fact that a fragile banking system can, not only hamper the development of a particular economy but also it can deepen the real economic crisis and impose heavy social costs. So the health of the banking system should be one of the primary concerns of the government of each country. Currently the Indian banking sector is not in a good health. The symptoms of the disease are vastly apparent viz. rising NPAs, high labor costs,

competition from mutual funds, bureaucratic hurdle and red tapism to name a few. The existing weak banks only compound the problem. Most of these symptoms have been present in the Indian banking system since independence but it is only in the post reform era that they have became more ostensible.

Indian Banking Sector: The banking sector in India is currently passing through an exciting and challenging phase. The reform measures have bought about sweeping changes in this vital sector of the country’s economy. The report provides an analysis of the banking sector in india. In the 1970’s and 1980’s the Indian banking industry

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research58

was marked by a high degree of regulation. Banking sector reforms were initiated in 1991 with the following objectives; improving the macro-economic policy framework within which banks operate, introducing prudent practices; improving the financial health and competitive condition of banks; building financial infrastructure relating to supervision, audit standards and legal framework; and strengthening the level of managerial competence and quality of personnel.

In the 1970’s and 1980’s the banking industry was marked by a high degree of regulation. The banks functioned in a heavily regulated and controlled environment, with an administered interest rate structure, quantitative restrictions on credit flows, high reserve requirements, and pre-emption of a significant proportion of lendable resource towards the “priority” sector etc.

In 1991 the government of India (GOI) established a nine-member committee on financial systems, under the chairmanship of Mr.N.Narsimha to evaluate the systemic banking problems. The Narsimham committee report published towards the end of 1991, containing far-reaching recommendations for the banking sector. This report formed the basis for the sector’s reforms, which were undertaken in parallel with the overall economic reforms of the 1990’s.

Non-Performing assets of the banking sector : A non-performing asset means an asset which does not yield any income/interest/installment on principal for a period of two quarter. Normally non-performing asset is an amount under any of the credit facilities viz., term loans, overdraft, cash credit accounts, bills purchased and discounted and other accounts in respect of which interest/installment of principle is an arrears for

two quarters during the accounting year. NPA’s are always a serious case of concern to the banks.

Reasons for Mounting NPA’s in the banking sector

1. Proceeding against the defaulters for recovery of our dues through legal action is the last resort among the various alternatives when persuasive efforts fail to produce any concrete results, legal action for recovery of loans has to be initiated against all defaulters.

2. A major portion of bad debts occurred due to the lending to the priority sector. At the pressure of politicians and bureaucrats, many big borrower defaulted only due to the recession in the economy. The absence of proper bankruptcy laws and the dilatory legal producer in schedule commercial banks in Indian has swollen from Rs. 47,300 crores to Rs. 70,904 crores during the five years from March 1997 to march 2002, as per the reserve bank’s annual report on trend and progress of banks in India.

3. A major portion of bank lending is to industries and trade; this segment accounted for over 53 percent of the gross bank credit excluding loans to these borrowers bankers have to relearn a lot. Till the early 1960s bankers lent only to traditional companies owned by respected business group and relied primarily on the credentials of the group. The emergence of small-scale industries and the gradual opening up of the economy changed the scenario with many news entrepreneurs on

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research59

the scene and bankers had to learn newer of assessment and appraisal.

4. An expert committee under the chairmanship of Prakash Tandon was formed in 1974 to rewrite the policies and producer of lending to industries by banks. All banks under the directions of RBI freed banks from the shackles of the norms, but banks are yet to get out of their reliance norms and arithmetic formula. Appraisal of credit needs of industrial units and business concern cannot be put in to relearn tricks of the trade.

5. Another factor that make contribute to the low level of expertise in many big public sector banks is the constant rotation of duties among officers and the apparent lack of training in the lending principle for loan officers. If the public sector banks have to stand in the fierce financial market they have to create and nurture good cadre of officers in various disciplines.

6. For a long time the country was turned to s policy of reviving or ‘rehabilitating’ every unit under financial trouble. Thus a separate judicial body called to Board for industrial and financial resonation (BIFR) was set up in the 1980’s to consider cases of sick unit to see if they can be rehabilitated. The banks were the main sufferers as they could not sell their security when required. The BIFR is being abolished and the new security law supersedes (BIFR). It is reported that CRISIL the rating agency had estimated that the new law would enable banks to reduce their gross NPA’s. The agency states that over 36.4 percent of the bad loans would be outside the ambit of the new act. However, it is understood the

main reasons for mounting NPA’s in the sector are

a. Diversion of funds by promoters b. Gestation period in starting on

enterprises/venture and c. Time as well as cost over time

Classification of loans In India bank loans are classified on the following basis:

Performing Assets:

Non-Performing assets:

Asset classification Assets can be categorized into Four categories namely

(1) Standard

(2) Sub –Standard

(3) Doubtful

(4) Loss the last three categories are classified as NPAs based on the period for which the asset has remained non-performing and the reliability of the dues.

NPA IDENTIFICATION NORMS With effect from 31st March’2004,

A loan or advance would become NPA where;

i) Interest and/ or installment of principal remain overdue for a period of more than 90 days in respect of a term loan,

ii) The account remains ‘out of order’ for a period of more than 90 days, in respect of an Overdraft/Cash Credit (OD/CC),

iii) The bill remains overdue for a period of more than 90 days in the case of bills purchased and discounted,

iv) With effect from September 2004, loansgranted for short duration crops will be

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research60

treated as NPA, if the installment of principal or interest thereon remains overdue for two crop seasons and loans granted for long duration crops will be treated as NPA, if installment of principal or interest thereon remains overdue for one crop season, and Any amount to be received remains overdue for a period of more than 90 days in respect of other accounts. Out of Order: An account should be treated as out of order if the outstanding balance remains continuously in excess of the sanctioned limit/drawing power.

Review of Literature: Bhattachraya (2001) has carried on a “Study on management of Non-performing advances in banks”, it reveals three important aspects

1. Scientific techniques in management of NPA’s

2. Causes of an account turning into an NPA’s and

3. General contribution factor for accounts turning into NPA’s

He has suggested sound risks assessment rating system for the prevention of NPA’s by banks. Sound risks agreement system involves a detailed scrutiny of the project to judge its continued viability looking to the condition of the economy, markets and industry as well as the strengthen and weakness of the borrower and promoter.

Vradi, Vijay, Mauluri, Nagarjuna (2006), in his study on ´Measurement of efficiency of bank in India concluded that in modern world performance of banking is more important to stable the economy .in order to see the efficiency of Indian banks we have see the fore indicators i.e. profitability, productivity, assets, quality and

financial management for all banks includes public sector, private sector banks in India for the period 2000 and 1999 to 2002-2003. For measuring efficiency of banks we have adopted development envelopment analysis and found that public sectors banks are more efficient then other banks in India.

Subbaroo (2007) concludes the Indian banking system has undergone transformation itself from domestic banking to international banking. However, the system requires a combination of new technologies, well regulated risk and credit appraisal, treasury management, product diversification, internal control, external regulations and professional as well as skilled human resource to achieve the heights of the international excellence to play its role critically in meeting the global challenge. This paper mainly concentrates on the major trends that change the banking industry world over, viz. consolidation of players through mergers and acquisitions globalization of players, development of new technology, universal banking and human resource in banking, profitability, rural banking and risk management. Banks will have to gear up to meet stringent prudential capital adequacy norms under Basel I and II, the free trade agreements. Banks will also have to cope with challenges posed by technological innovations in banking B.Satish Kumar (2008), in his article on an evaluation of the financial performance of Indian private sector banks wrote Private sector banks play an important role in development of Indian economy. After liberalization the banking industry underwent major changes. The economic reforms totally have changed the banking sector. RBI permitted new banks to be started in the private sector asper the recommendation of

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research61

Narashiman committee. The Indian banking industry was dominated by public sector banks. But now the situations have changed new generation banks with used of technology and professional management has gained a reasonable position in the banking industry.

Roma Mitra, Shankar Ravi (2008), A stable and efficient banking sector is an essential precondition to increase the economic level of a country. This paper tries to model and evaluate the efficiency of 50 Indian banks. The Inefficiency can be analyzed and quantified for every evaluated unit. The aim of this paper is to estimate and compare efficiency of the banking sector in India. The analysis is supposed to verify or reject the hypothesis whether the banking sector fulfils its intermediation function sufficiently to compete with the global players. The results are insightful to the financial policy planner as it identifies priority areas for different banks, which can improve the performance. This paper evaluates the performance of Banking Sectors in India.

Singla (2008) examines that how financial management plays a crucial role industrialists growth of banking. It is concerned with examining the profitability position of the selected sixteen banks of banker index for a period of six years (2001-06). The study reveals that the profitability position was reasonable during the period of study when compared with the previous years. Strong capital position and balance sheet place. Banks in better position to deal with and absorb the economic constant over a period of time.

Research Methodology

Statement of the problem: It is widely accepted fact that the quantity of NPA’s is often associated with bank failures and financial crises in both developing and developed countries. Though various reforms were introduced in India, banks are struggling to face the global challenges a head. Therefore the present study is undertaken to know the reason for NPA’s in public sector and private sector banks and also to know the recovery mechanism adopted for recovery of NPA’s

Scope of the study: The study has been conducted at Bangalore. The study encompasses all matters related to NPA’s including factors responsible for NPA’s. The outcome of the study would also help the banks to formulate suitable programs and use appropriate methods to improve the level of NPA’s in the public sector and private banks.

Objectives of the study:

1. To know the quantum of NPA’s in selected Public and Private sector banks in Bangalore city2. To know the reason and measures adopted for reducing NPA’s3. To know the recovery mechanism adopted

for NPA’s pre and post securitization act 4. To know the impact of central government

relief benefited the bank to reduce the NPA’s

5. To recommend some tentative suggestion based on findings

Working Hypotheses: The present study relied on the following tentative statements, which formed the hypotheses of the study.

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research62

Hypothesis 1: There is significant difference in the market share affected due to existence of NPA’s

Hypothesis 2: Securitization Act has empowered banks for reducing NPA’s

Hypothesis 3: Securitization Act has reduced the level of NPA’s in banks

Hypothesis 4: Government relief has benefited the banks to reduce NPA’s

Hypothesis 5:NPA’s affect the bank performance in terms of profit

Methodology and sources of data : The research study was exploratory in nature, therefore qualitative research was used for data gathering and analysis. The study is conducted through a survey method. To carryout the study, the structure questionnaire technique is used to get insight about the issue explored in the present study. For the purpose of the study, both primary

and secondary data is collected, to achieve the formulated objectives. The primary data is collected from employees of private and public banks having a minimum of five years of work experience. The secondary data is collected from journals, books and websites.

Sampling Design: This study is based on data collected from the banks based in Bangalore city, the study followed multi stage sampling design. In the first stage 4 private banks and seven public banks were selected, the selection was based on the following criteria

a. The bank should be located in Bangalore city

b. Banks should have operating profit of Rs. 4,000 crores or more

In the second stage one hundred and seventy five respondents having a minimum of five years of experience in this area were randomly approached to fill in the developed questionnaire.

Analysis and Interpretation

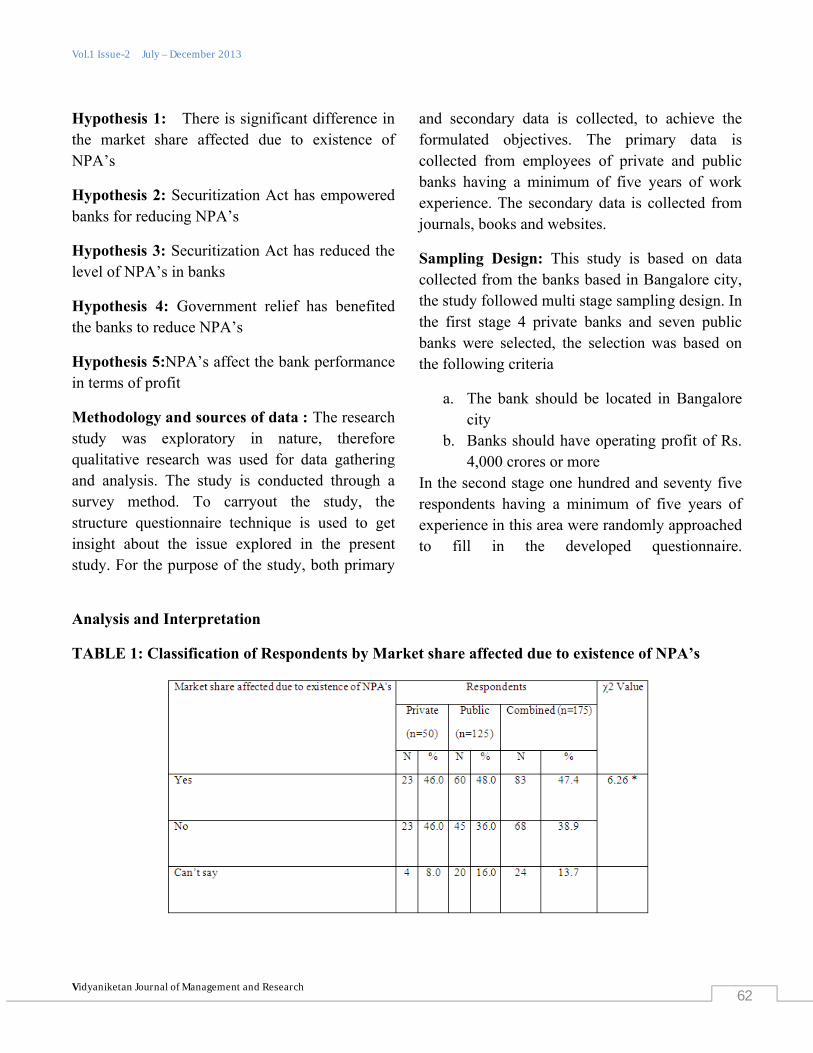

TABLE 1: Classification of Respondents by Market share affected due to existence of NPA’s

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research

NS : Non-Significant,

χ2 (0.05,2df) = 5.991

Analysis and interpretation : The above table shows the classification of respondents on market share affected due to existence of NPA’s. It is interesting to note that 46% of private and 48% of public banks respondents conveys that market share is affected by existence of NPA’s as coand 36% of public banks conveys market share is not affected by the existence of NPA’s.

The data was subjected for statistical test which indicate the response on market share affect due to existence of NPA’s between private and putherefore H1 is accepted

Hypothesis – 1 There is significant difference in the market share affected due to existence of NPA’s

Classification of Respondents by Market share affected

0.0

10.0

20.0

30.0

40.0

50.0

Res

pond

ents

(%

)

Significant,

The above table shows the classification of respondents on market share affected due to existence of NPA’s. It is interesting to note that 46% of private and 48% of public banks respondents conveys that market share is affected by existence of NPA’s as compared to 46% of private and 36% of public banks conveys market share is not affected by the existence of NPA’s.

The data was subjected for statistical test which indicate the response on market share affect due to existence of NPA’s between private and public banks found to be significant (X

There is significant difference in the market share affected due to existence of NPA’s

GRAPH - 1

Classification of Respondents by Market share affected due to existence of NPA’S

Yes No Can't say

48.0

36.0

16.0

Market share affected due to existence of NPA's

Private Nationalized

63

Significant,

The above table shows the classification of respondents on market share affected due to existence of NPA’s. It is interesting to note that 46% of private and 48% of public banks

mpared to 46% of private and 36% of public banks conveys market share is not affected by the existence of NPA’s.

The data was subjected for statistical test which indicate the response on market share affect due to blic banks found to be significant (X2 = 6.26*, P<0.05),

There is significant difference in the market share affected due to existence of NPA’s

due to existence of NPA’S

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research64

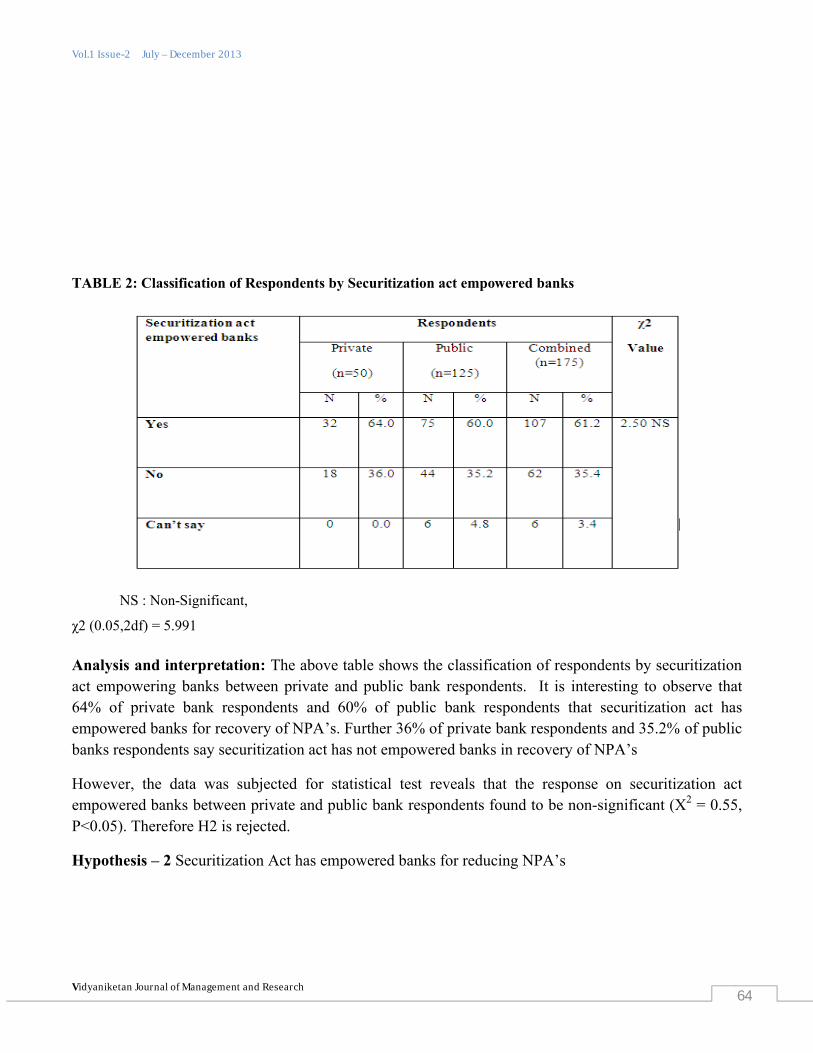

TABLE 2: Classification of Respondents by Securitization act empowered banks

NS : Non-Significant,

χ2 (0.05,2df) = 5.991

Analysis and interpretation: The above table shows the classification of respondents by securitization act empowering banks between private and public bank respondents. It is interesting to observe that 64% of private bank respondents and 60% of public bank respondents that securitization act has empowered banks for recovery of NPA’s. Further 36% of private bank respondents and 35.2% of public banks respondents say securitization act has not empowered banks in recovery of NPA’s

However, the data was subjected for statistical test reveals that the response on securitization act empowered banks between private and public bank respondents found to be non-significant (X2 = 0.55, P<0.05). Therefore H2 is rejected.

Hypothesis – 2 Securitization Act has empowered banks for reducing NPA’s

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research

Classification of Respondents by Securitization act empowered banks

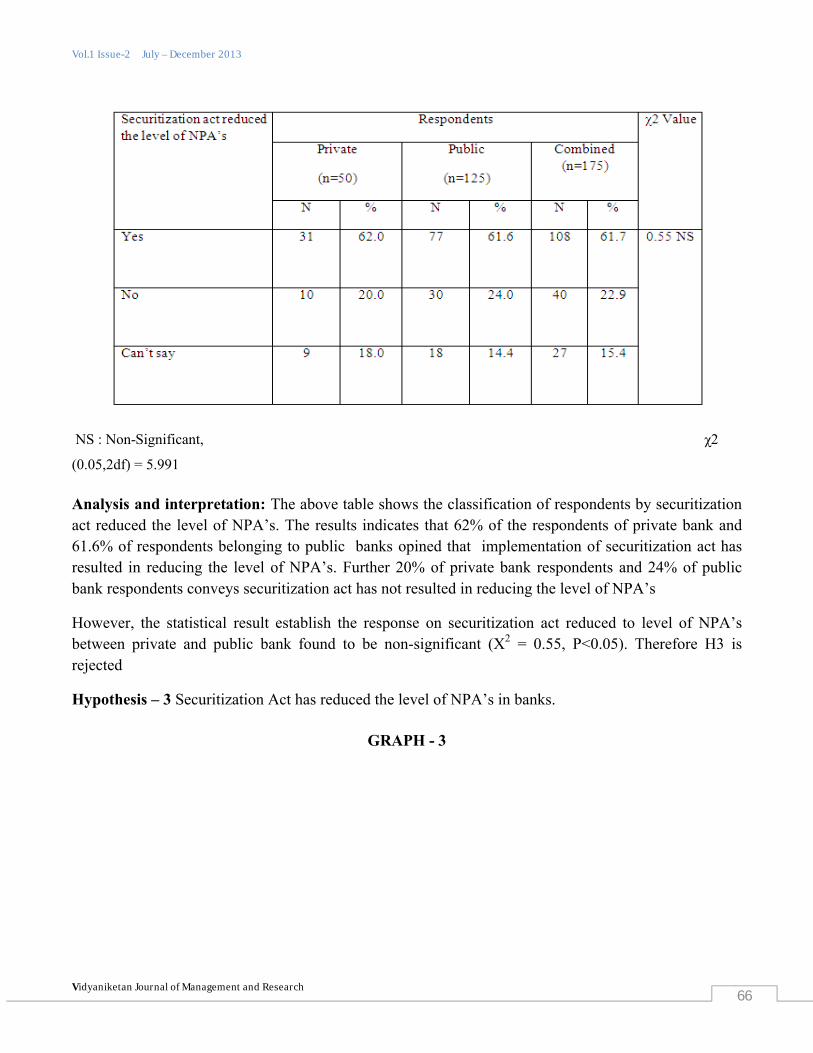

TABLE 3: Classification of Respondents by Securitization act reduced the level of NPA’s

0.010.020.030.040.050.060.070.080.090.0

100.0

Yes

64.0

Res

pond

ents

(%

)

GRAPH – 2

Classification of Respondents by Securitization act empowered banks

TABLE 3: Classification of Respondents by Securitization act reduced the level of NPA’s

Yes No Can't say

64.0

36.0

0.0

60.0

35.2

4.8

Securitization act empowerered banks

Private Nationalized

`̀

65

Classification of Respondents by Securitization act empowered banks

TABLE 3: Classification of Respondents by Securitization act reduced the level of NPA’s

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research66

NS : Non-Significant, χ2

(0.05,2df) = 5.991

Analysis and interpretation: The above table shows the classification of respondents by securitization act reduced the level of NPA’s. The results indicates that 62% of the respondents of private bank and 61.6% of respondents belonging to public banks opined that implementation of securitization act has resulted in reducing the level of NPA’s. Further 20% of private bank respondents and 24% of public bank respondents conveys securitization act has not resulted in reducing the level of NPA’s

However, the statistical result establish the response on securitization act reduced to level of NPA’s between private and public bank found to be non-significant (X2 = 0.55, P<0.05). Therefore H3 is rejected

Hypothesis – 3 Securitization Act has reduced the level of NPA’s in banks.

GRAPH - 3

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research

Classification of Respondents by Securitization

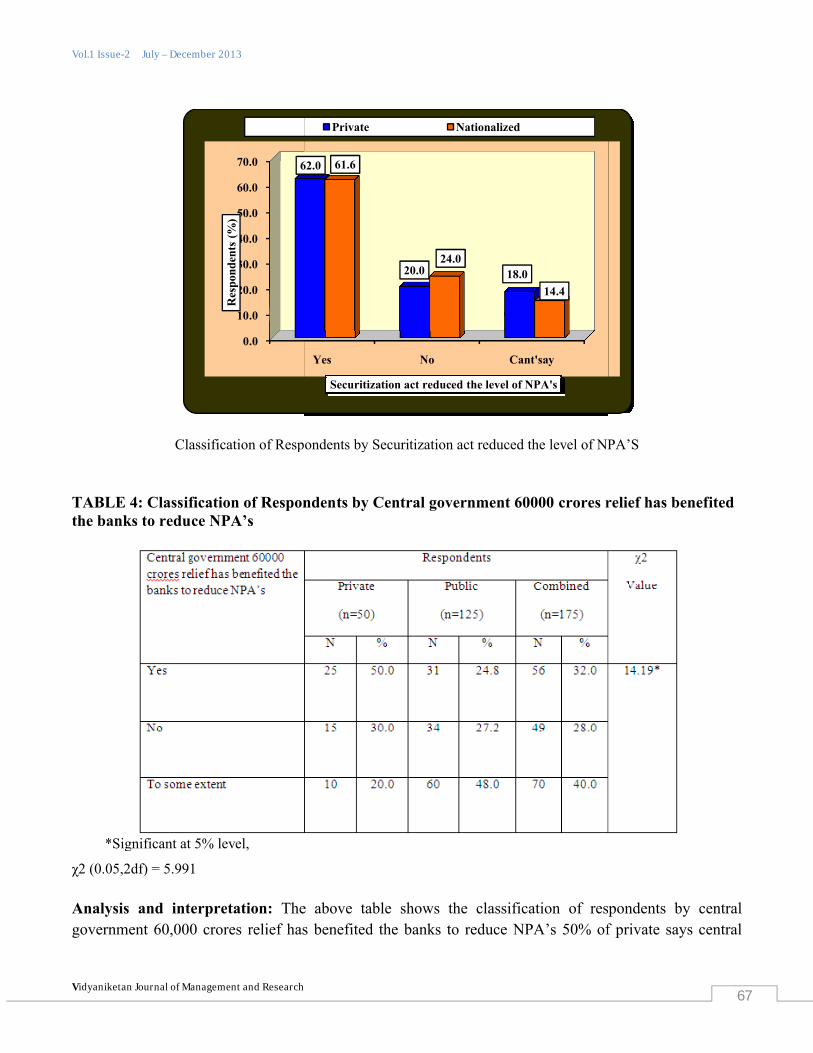

TABLE 4: Classification of Respondents by Central government 60000 crores relief has benefited the banks to reduce NPA’s

*Significant at 5% level,

χ2 (0.05,2df) = 5.991

Analysis and interpretation: The above table shows the classificatgovernment 60,000 crores relief has benefited the banks to reduce NPA’s 50% of private says central

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0 62.0

Res

pond

ents

(%

)

Classification of Respondents by Securitization act reduced the level of NPA’S

TABLE 4: Classification of Respondents by Central government 60000 crores relief has benefited

*Significant at 5% level,

The above table shows the classification of respondents by central government 60,000 crores relief has benefited the banks to reduce NPA’s 50% of private says central

Yes No Cant'say

62.0

20.0 18.0

61.6

24.0

14.4

Securitization act reduced the level of NPA's

Private Nationalized

67

act reduced the level of NPA’S

TABLE 4: Classification of Respondents by Central government 60000 crores relief has benefited

*Significant at 5% level,

ion of respondents by central government 60,000 crores relief has benefited the banks to reduce NPA’s 50% of private says central

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research

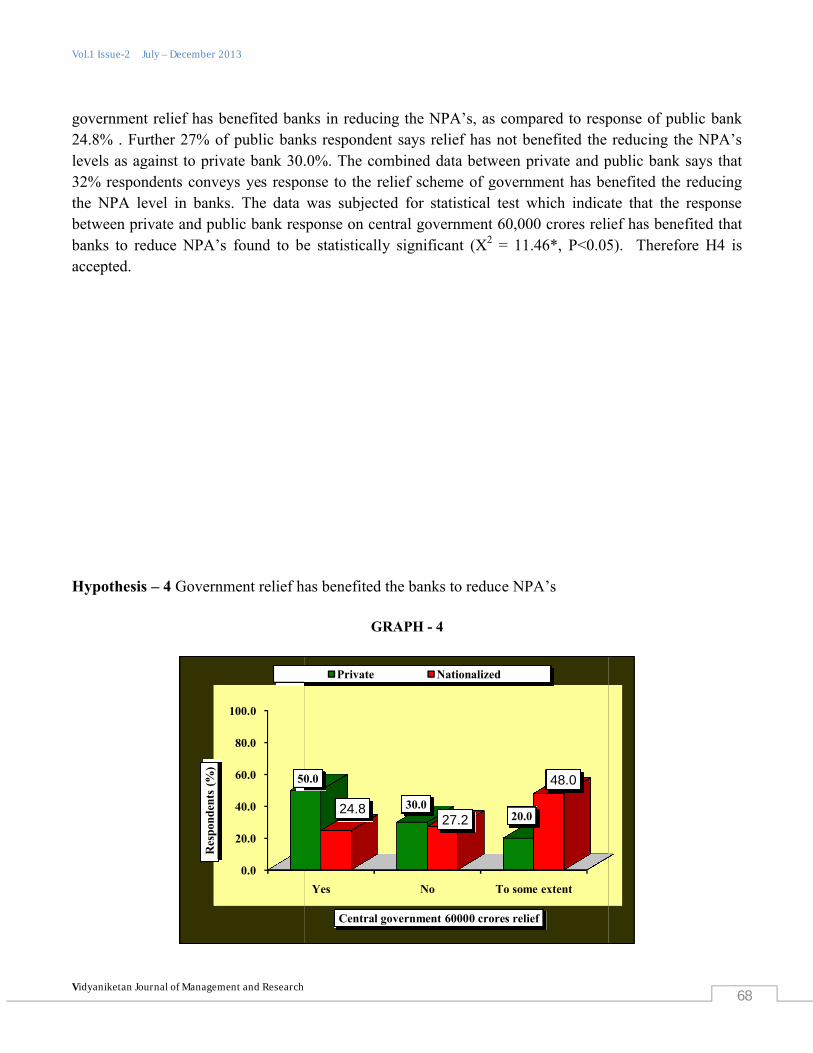

government relief has benefited banks in reducing the NPA’s, as compared to response of public bank 24.8% . Further 27% of public banks respondent says relief has not benefited the reducing the NPA’s levels as against to private bank 30.0%. The combined data between private and public bank says that 32% respondents conveys yes response to the relief scheme of government has benefthe NPA level in banks. The data was subjected for statistical test which indicate that the response between private and public bank response on central government 60,000 crores relief has benefited that banks to reduce NPA’s found to be accepted.

Hypothesis – 4 Government relief has benefited the banks to reduce NPA’s

0.0

20.0

40.0

60.0

80.0

100.0

50.0

Res

pond

ents

(%

)

government relief has benefited banks in reducing the NPA’s, as compared to response of public bank lic banks respondent says relief has not benefited the reducing the NPA’s

levels as against to private bank 30.0%. The combined data between private and public bank says that 32% respondents conveys yes response to the relief scheme of government has benefthe NPA level in banks. The data was subjected for statistical test which indicate that the response between private and public bank response on central government 60,000 crores relief has benefited that banks to reduce NPA’s found to be statistically significant (X2 = 11.46*, P<0.05). Therefore H4 is

Government relief has benefited the banks to reduce NPA’s

GRAPH - 4

Yes No To some extent

50.0

30.020.0

24.827.2

48.0

Central government 60000 crores relief

Private Nationalized

68

government relief has benefited banks in reducing the NPA’s, as compared to response of public bank lic banks respondent says relief has not benefited the reducing the NPA’s

levels as against to private bank 30.0%. The combined data between private and public bank says that 32% respondents conveys yes response to the relief scheme of government has benefited the reducing the NPA level in banks. The data was subjected for statistical test which indicate that the response between private and public bank response on central government 60,000 crores relief has benefited that

= 11.46*, P<0.05). Therefore H4 is

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research69

Classification of Respondents by Age Central government 60000crores relief has benefited the banks to reduce NPA’S

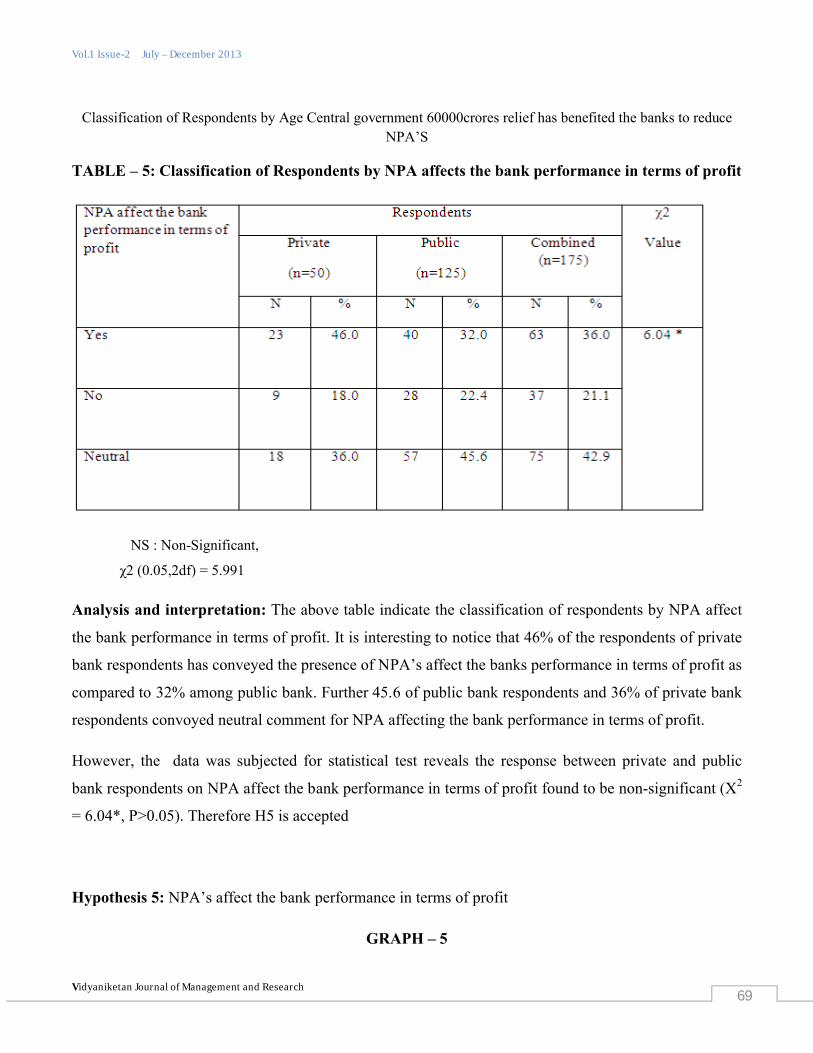

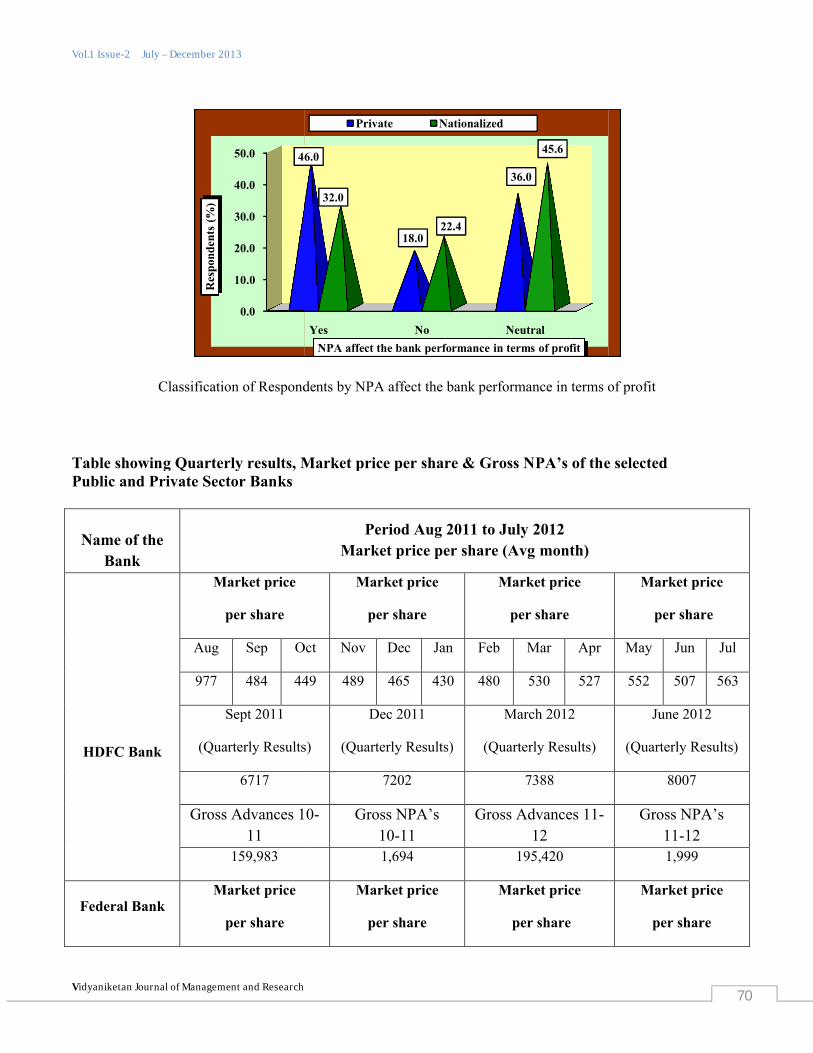

TABLE – 5: Classification of Respondents by NPA affects the bank performance in terms of profit

NS : Non-Significant,

χ2 (0.05,2df) = 5.991

Analysis and interpretation: The above table indicate the classification of respondents by NPA affect

the bank performance in terms of profit. It is interesting to notice that 46% of the respondents of private

bank respondents has conveyed the presence of NPA’s affect the banks performance in terms of profit as

compared to 32% among public bank. Further 45.6 of public bank respondents and 36% of private bank

respondents convoyed neutral comment for NPA affecting the bank performance in terms of profit.

However, the data was subjected for statistical test reveals the response between private and public

bank respondents on NPA affect the bank performance in terms of profit found to be non-significant (X2

= 6.04*, P>0.05). Therefore H5 is accepted

Hypothesis 5: NPA’s affect the bank performance in terms of profit

GRAPH – 5

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research

Classification of Respondents by NPA affect the bank performance in terms of profit

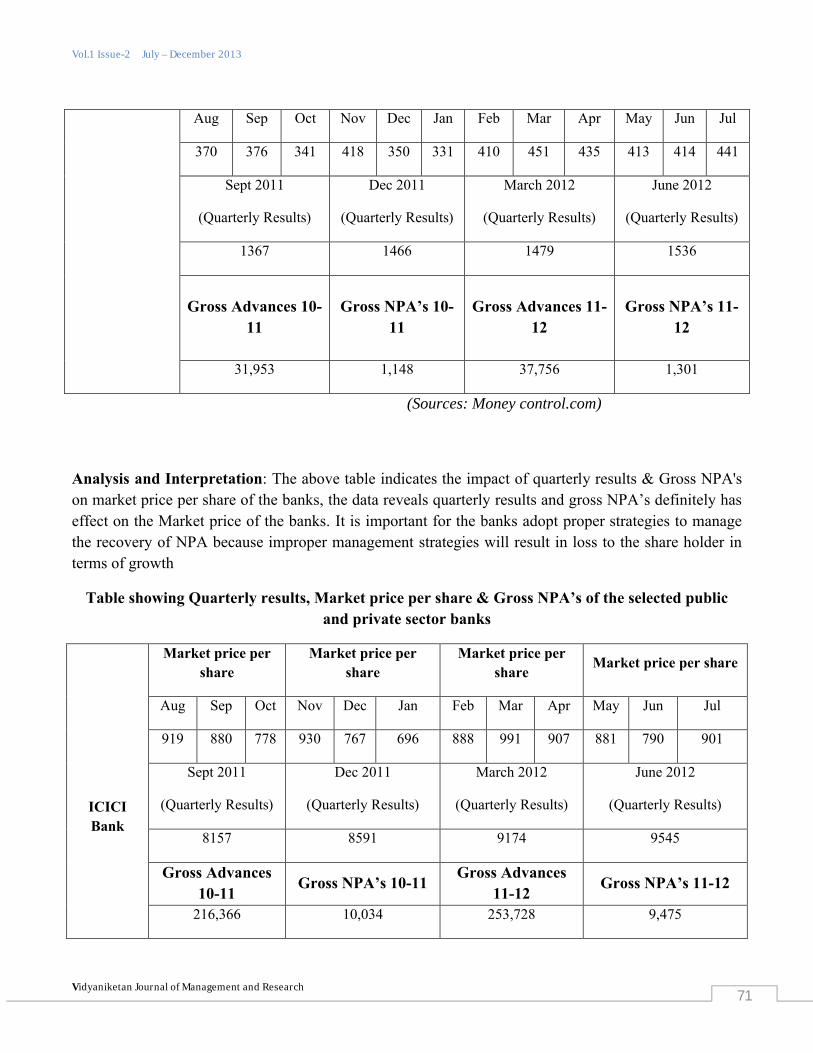

Table showing Quarterly results, Market price per share & Gross NPA’s of the selected Public and Private Sector Banks

Name of the Bank

HDFC Bank

Market price

per share

Aug Sep Oct

977 484 449

Sept 2011

(Quarterly Results)

6717

Gross Advances 1011

159,983

Federal BankMarket price

per share

0.0

10.0

20.0

30.0

40.0

50.0 46.0

Res

pond

ents

(%

)

ssification of Respondents by NPA affect the bank performance in terms of profit

Table showing Quarterly results, Market price per share & Gross NPA’s of the selected

Period Aug 2011 to July 2012Market price per share (Avg month)

Market price

per share

Market price

per share

Oct Nov Dec Jan Feb Mar Apr

449 489 465 430 480 530 527

(Quarterly Results)

Dec 2011

(Quarterly Results)

March 2012

(Quarterly Results)

7202 7388

Gross Advances 10- Gross NPA’s10-11

Gross Advances 11-12

1,694 195,420

Market price

per share

Market price

per share

Yes No Neutral

46.0

18.0

36.0

32.0

22.4

45.6

NPA affect the bank performance in terms of profit

Private Nationalized

70

ssification of Respondents by NPA affect the bank performance in terms of profit

Table showing Quarterly results, Market price per share & Gross NPA’s of the selected

Market price

per share

May Jun Jul

552 507 563

June 2012

(Quarterly Results)

8007

Gross NPA’s11-121,999

Market price

per share

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research71

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

370 376 341 418 350 331 410 451 435 413 414 441

Sept 2011

(Quarterly Results)

Dec 2011

(Quarterly Results)

March 2012

(Quarterly Results)

June 2012

(Quarterly Results)

1367 1466 1479 1536

Gross Advances 10-11

Gross NPA’s 10-11

Gross Advances 11-12

Gross NPA’s 11-12

31,953 1,148 37,756 1,301

(Sources: Money control.com)

Analysis and Interpretation: The above table indicates the impact of quarterly results & Gross NPA's on market price per share of the banks, the data reveals quarterly results and gross NPA’s definitely has effect on the Market price of the banks. It is important for the banks adopt proper strategies to manage the recovery of NPA because improper management strategies will result in loss to the share holder in terms of growth

Table showing Quarterly results, Market price per share & Gross NPA’s of the selected public and private sector banks

ICICI Bank

Market price per share

Market price per share

Market price per share

Market price per share

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

919 880 778 930 767 696 888 991 907 881 790 901

Sept 2011

(Quarterly Results)

Dec 2011

(Quarterly Results)

March 2012

(Quarterly Results)

June 2012

(Quarterly Results)

8157 8591 9174 9545

Gross Advances 10-11

Gross NPA’s 10-11Gross Advances

11-12Gross NPA’s 11-12

216,366 10,034 253,728 9,475

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research72

Axis Bank

Market price per share

Market price per share

Market price per share

Market price per share

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

1103 1116 952 1168 958 816 1059 1287 1210 992 1023 1066

Sept 2011

(Quarterly Results)

Dec 2011

(Quarterly Results)

March 2012

(Quarterly Results)

June 2012

(Quarterly Results)

5275 5776 6060 6482

Gross Advances 10-11

Gross NPA’s 10-11Gross Advances

11-12Gross NPA’s 11-12

142,408 1,599 169,760 1,806

(Sources: Money control.com)

Analysis and Interpretation: The above table indicates the impact of quarterly results & Gross NPA's on market price per share of the banks, the data reveals quarterly results and gross NPA’s definitely has effect on the Market price of the banks. It can be noticed that the ICICI and Axis bank market share are fluctuation because of increases in gross NPA’s. The data also reveals that as the quarterly results are increasing the market price share going up and better management of NPA’s will result in better market price per share

Table showing Quarterly results, Market price per share & Gross NPA’s of the selected public and private sector banks

Vijaya Bank

Market price per share

Market price per share

Market price per share

Market price per share

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

62 53 60 56 51 44 56 67 56 58 54 60

Sept 2011

(Quarterly Results)

Dec 2011

(Quarterly Results)

March 2012

(Quarterly Results)

June 2012

(Quarterly Results)

1992 2058 2152 2197

Gross Advances 10-11

Gross NPA’s 10-11Gross Advances

11-12Gross NPA’s 11-

12

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research73

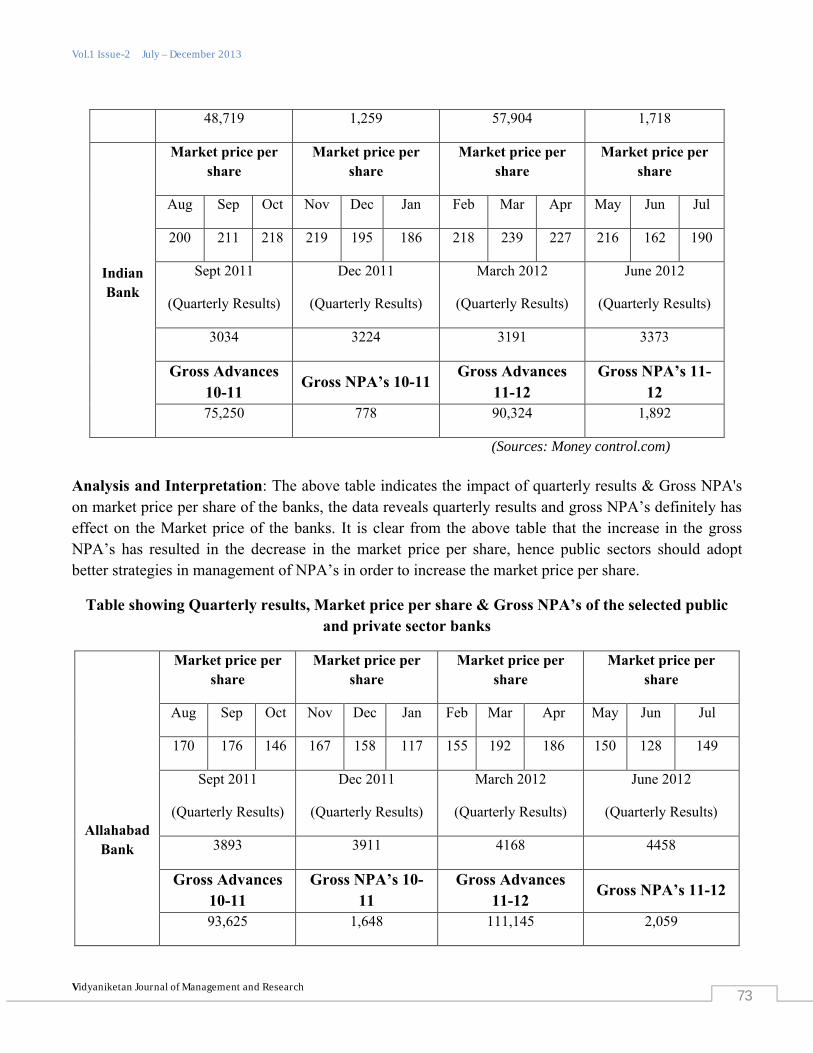

48,719 1,259 57,904 1,718

Indian Bank

Market price per share

Market price per share

Market price per share

Market price per share

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

200 211 218 219 195 186 218 239 227 216 162 190

Sept 2011

(Quarterly Results)

Dec 2011

(Quarterly Results)

March 2012

(Quarterly Results)

June 2012

(Quarterly Results)

3034 3224 3191 3373

Gross Advances 10-11

Gross NPA’s 10-11Gross Advances

11-12Gross NPA’s 11-

1275,250 778 90,324 1,892

(Sources: Money control.com)

Analysis and Interpretation: The above table indicates the impact of quarterly results & Gross NPA's on market price per share of the banks, the data reveals quarterly results and gross NPA’s definitely has effect on the Market price of the banks. It is clear from the above table that the increase in the gross NPA’s has resulted in the decrease in the market price per share, hence public sectors should adopt better strategies in management of NPA’s in order to increase the market price per share.

Table showing Quarterly results, Market price per share & Gross NPA’s of the selected public and private sector banks

Allahabad Bank

Market price per share

Market price per share

Market price per share

Market price per share

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

170 176 146 167 158 117 155 192 186 150 128 149

Sept 2011

(Quarterly Results)

Dec 2011

(Quarterly Results)

March 2012

(Quarterly Results)

June 2012

(Quarterly Results)

3893 3911 4168 4458

Gross Advances 10-11

Gross NPA’s 10-11

Gross Advances 11-12

Gross NPA’s 11-12

93,625 1,648 111,145 2,059

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research74

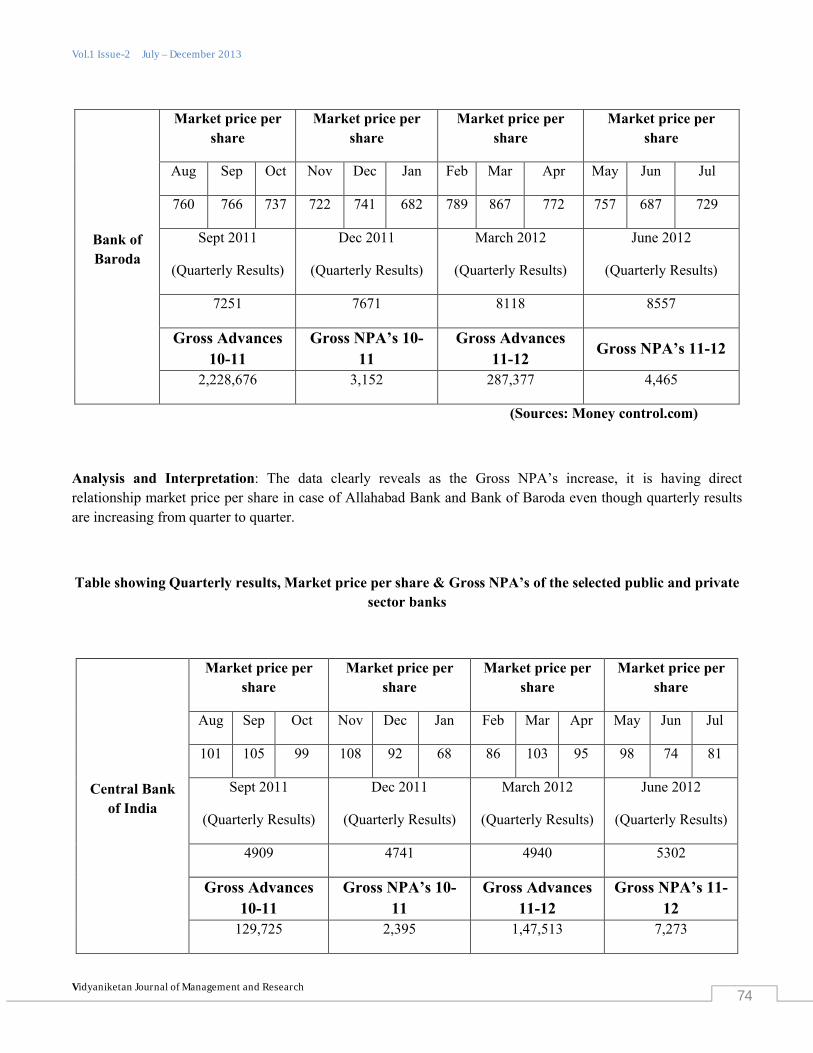

Bank of Baroda

Market price per share

Market price per share

Market price per share

Market price per share

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

760 766 737 722 741 682 789 867 772 757 687 729

Sept 2011

(Quarterly Results)

Dec 2011

(Quarterly Results)

March 2012

(Quarterly Results)

June 2012

(Quarterly Results)

7251 7671 8118 8557

Gross Advances 10-11

Gross NPA’s 10-11

Gross Advances 11-12

Gross NPA’s 11-12

2,228,676 3,152 287,377 4,465

(Sources: Money control.com)

Analysis and Interpretation: The data clearly reveals as the Gross NPA’s increase, it is having direct relationship market price per share in case of Allahabad Bank and Bank of Baroda even though quarterly results are increasing from quarter to quarter.

Table showing Quarterly results, Market price per share & Gross NPA’s of the selected public and private sector banks

Central Bank of India

Market price per share

Market price per share

Market price per share

Market price per share

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

101 105 99 108 92 68 86 103 95 98 74 81

Sept 2011

(Quarterly Results)

Dec 2011

(Quarterly Results)

March 2012

(Quarterly Results)

June 2012

(Quarterly Results)

4909 4741 4940 5302

Gross Advances 10-11

Gross NPA’s 10-11

Gross Advances 11-12

Gross NPA’s 11-12

129,725 2,395 1,47,513 7,273

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research75

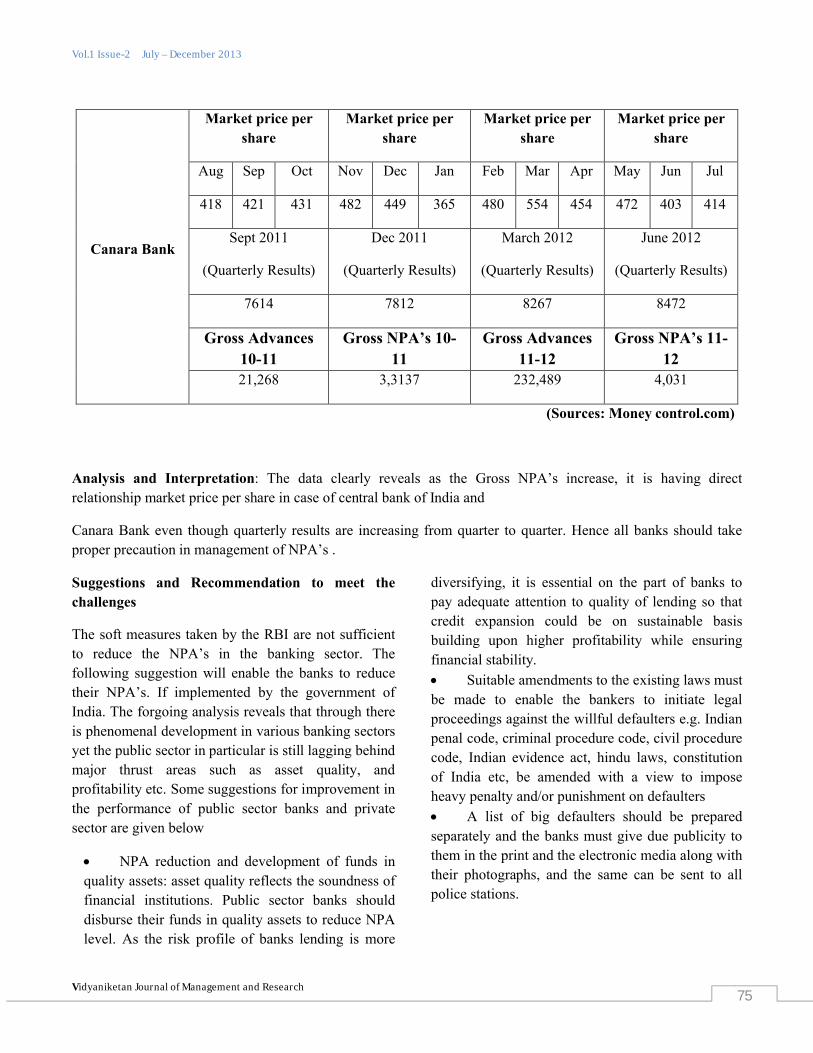

Canara Bank

Market price per share

Market price per share

Market price per share

Market price per share

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

418 421 431 482 449 365 480 554 454 472 403 414

Sept 2011

(Quarterly Results)

Dec 2011

(Quarterly Results)

March 2012

(Quarterly Results)

June 2012

(Quarterly Results)

7614 7812 8267 8472

Gross Advances 10-11

Gross NPA’s 10-11

Gross Advances 11-12

Gross NPA’s 11-12

21,268 3,3137 232,489 4,031

(Sources: Money control.com)

Analysis and Interpretation: The data clearly reveals as the Gross NPA’s increase, it is having direct relationship market price per share in case of central bank of India and

Canara Bank even though quarterly results are increasing from quarter to quarter. Hence all banks should take proper precaution in management of NPA’s .

Suggestions and Recommendation to meet the challenges

The soft measures taken by the RBI are not sufficient to reduce the NPA’s in the banking sector. The following suggestion will enable the banks to reduce their NPA’s. If implemented by the government of India. The forgoing analysis reveals that through there is phenomenal development in various banking sectors yet the public sector in particular is still lagging behind major thrust areas such as asset quality, and profitability etc. Some suggestions for improvement in the performance of public sector banks and private sector are given below

NPA reduction and development of funds in quality assets: asset quality reflects the soundness of financial institutions. Public sector banks should disburse their funds in quality assets to reduce NPA level. As the risk profile of banks lending is more

diversifying, it is essential on the part of banks to pay adequate attention to quality of lending so that credit expansion could be on sustainable basis building upon higher profitability while ensuring financial stability. Suitable amendments to the existing laws must be made to enable the bankers to initiate legal proceedings against the willful defaulters e.g. Indian penal code, criminal procedure code, civil procedure code, Indian evidence act, hindu laws, constitution of India etc, be amended with a view to impose heavy penalty and/or punishment on defaulters A list of big defaulters should be prepared separately and the banks must give due publicity to them in the print and the electronic media along with their photographs, and the same can be sent to all police stations.

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research76

Fast-track courts must be established to nab the corporate criminals especially institutional defaulters in the criminal courts Banks should obey the RBI norms and provide facilities as per the norms, which are not being followed by the banks. While the customer must be given prompt services and the bank officer should not have any fear on mind to provide the facilities as per RBI norms to the units going sick.

Conclusion

To conclude till the recent past, corporate borrowers even after defaulting continuously never had any real fear of banks taking any action to recover their dues despite the fact that their entire assets were hypothecated to the banks. This is because there was no legal act framed to safeguard the real interest of the banks. The introduction of SARFAESI ACT 2002 whereby banks can send notices to their defaulters to repay their dues else make to get rid of sticky loans there by improving their bottom line. The act has facilitated the investors to deploy their funds in the NPA’s portfolios of bank and financial institutions, asset reconstruction companies (ARC’s) were formed as an independent body corporate to expedite the process of resolving the bad loans portfolio. This has warranted the need to create some kind of standard to make the process transparent and consistent. Banks were also able to contain the growth of gross and net Non-performing asset both in absolute terms as also in percent of net advances. Recently, our finance minister said in the inauguration of a public sector bank that the net NPA level now was 1.3 percent, efforts were taken to bring it to one percent in one year. He expressed confidence that the public sector banks will be able to bring down the Net Non-performing assets (NPA) to below 0.5 percent in the future years.

References

1. Anantharam Iyer TN, former Executive Director, RBI, Bank Supervision and the management of NPA advances, the Journal of

Indian Institute of Bankers, Apr-Jun 99, vol.70, No.2, pp.7-9.

2. A.V. Aruna Kumari (2002), “Economic Reforms and Performance of Indian Banking: A Cross Structural Analysis”, Indian Economic Panorama, A Quarterly Journal of Agriculture, Industry, Trade and Commerce, Special Banking Issue, pp.19-21.

3. A.K. Trivedi (2002), “Economic Reforms and Banking Scenario: An Analysis”, Indian Economic Panorama, A Quarterly Journal of Agriculture, Industry, Trade and Commerce, Special Banking Issue, pp.6-8

4. Af-Tamini, H. A. H. and Iabnoun, N. (2006): Service Quality of Bank Performance: A Comparison of the UAE National Foreign Banks’, Finance India, 20(1):181-197.

5. Ballabh, J. (2001): The Indian Banking Industry: Challenges Ahead’, IBA Bulletin, 23 (4 & 5): 8-10.

6. Basu, C R, Central Banking in a planned economy; The Indian Experiment, Tata Mc Graw Hill Publishing co., New Delhi 1978

7. Bhattacharya KM, Management of Non-performing advances in Banks, Journal of Accounting and Finance, oct. 2001-Mar. 2002, vol.16, No.1

8. Chandrasekhar, C.P. 2009. How sound is Indian banking. The Economic & Political Weekly. May, pp. 8

9. Desai V, Banking and Financial system, Himilaya publishing House, Bombay, 1995

10. Dr. Vibha Jain: Non-Performing Assets in commercial Banks: Regal Publication, New Delhi,1st Edition 2007p p78-79

11. George Kutty VV, NPA in Agricultural and Rural Development Bank, Indian commerce Bulletin December 2000, Vol.14, No.1,2.

12. Hallinan, Joseph T. (2003), “Bigger Banks. Better Deals?”, Wall Street Journal - Eastern Edition, Vol. 242, Issue 84, pp.D1-D3

Vol.1 Issue-2 July – December 2013

Vidyaniketan Journal of Management and Research77

13. Kaveri, V. S. (2001): Prevention of NPAs-Suggested Strategies’, IBA Bulletin, 23(8):7-9.

14. Kumar, T. S. (2006): Leveraging Technology Foreign Banks Financial Inclusion, Bankers Conference Proceedings (Nov.): 44-152.

15. Mahajan VS, studies in Indian Banking and Finance, Vol.I,(1989) , Vol.2 (1989). Deep & Deep Publication Chandigarh. 1989

16. Ministry of finance, Government of India, Reports of the committee on banking sector reforms (under the Chairmanship of M.Narsimham), New Delhi, April 1998, pp.22-26

17. Madhavankutty, G. (2007): Indian Banking – Towards Global Best Practices, Bankers Conference Proceedings (Nov.): 84-86.

18. Muniappan, G. P. (2002): Indian Banking: Paradigm Shift –A Regular Point of View, IBA Bulletin, 24(3): 151-155.

19. Nair, K. N. C. (2006): Banking on Technology to Meet 21st Century Challenges, Contributions, II, Banknet India: 6-11.

20. RBI, Report on trend and progress of banking in India 1996-97 band 2003-04, Mumbai, 1997, p.13, 2004, p.35-37,80

21. Reserve Bank of India, master circular on prudential norms on income recognition. Asset classification and provisioning.

22. RBI, Report on currency and Finance 1998-99,RBI Mumbai, 1998, p.VIII-8.

23. Savaraj A H, Rural Banking in India An empirical study, Daya Publishing house Delhi 1988

24. Subramanium, K. 1997. Banking Reformsinindia. TMH Publishing Co. Ltd., New Delhi.

25. Shroff, F. T. (2007): Modern Banking Technology’, Contributors, Vol. 4, Banknet Publications.: 44-49.

26. Singh, R. (2003): Profitability Management in Banks under Deregulated Environment’, IBA Bulletin, 25(7): 19-26.

27. Singla, H. K. (2008): Financial Performance of Banks in India, The ICFAI Journal of Bank Management, 7 (1): 50-62.

28. Subbaroo, P. S. (2007): Changing Paradigm in Indian Banking, Gyan Management, 1(2):151-160.

29. Tandon ML, Banking Law and Practice in India, Orient Law House, New Delhi, 1989

30. Tiwari, S. (2005): Development Financial Institutions & Indian Banking: A Paradigm Shift, Punjab Journal of Business Studies, 1(1): 38-45.

31. Uppal, R. K. and Kaur, R. (2007): Indian Banking Industry: Comparative Performance Evaluation in the Liberalized and Globalized Era’, Gyan Management, 2 (2):3-24.

32. Vashisht, A. K. (2004): Commercial Banking in the Globalized Environment, Political Economy Journal of India, 13(1 & 2): 1-11.

33. Wahab, A. (2001): Commercial Banks Under Reforms: Performance and Issues Edited Book, Deep & Deep Publications, New Delhi.

34. WELLS Fargo & Co. (2003), “Big Banks Report Strong Gains, Led by Wells Fargo, Bank One”, Wall Street Journal - Eastern Edition, Vol. 242, Issue 80, p.C5

Related Documents