Carpenter & Company -- 2013 INDUSTRY VALUATION The number of bank merger announcements in 2013 was essentially unchanged from the number of mergers announced in 2012. There were a total of 244 merger announcements involving U.S. ϐinancial institutions made in 2012, according to SNL Financial. In 2013, the total number of ϐinancial institution merger announcements equaled 242. Of the 2012 merger announcements, 218 were completed by year‐end 2013, ϐive were still pending, and 21 had been terminated. Through the ϐirst 17 days of 2014, 143 of the mergers announced in 2013 had been completed, 85 were still pending, and 14 had been terminated. For the merger transactions with reported deal ratios, the average price to tangible book value (P/TBV) ratio for the 2013 announcements at 1.28x was slightly higher than the average P/TBV ratio of 1.20x for the 2012 merger announcements. Assets to be acquired under the 2012 non‐terminated merger announcements totaled $137.1 billion, compared with $111.6 billion for the non‐terminated merger announcements made in 2013. The largest merger by target size for the 2013 announcements was the pending acquisition by Umpqua of the $9.9 billion Sterling Financial. The largest merger from the 2012 announcements was M&T Bancorp’s planned acquisition of the $43.6 billion Hudson City Bancorp. The M&T deal, which was announced on August 27, 2012, is currently scheduled to close by the end of 2014. According to company ϐilings, regulatory approval had been held up by BSA issues at M&T. INDUSTRY VALUATIONS: BANK MERGER AND ACQUISITION ACTIVITY CONTENTS Bank Merger activity ..................................................... 1 National bank stock prices ......................................... 2 California bank stock prices ....................................... 3 CA banks under $125 million ..................................... 4 CA banks $125‐$250 million....................................... 6 CA banks $250‐$500 million....................................... 8 CA banks $500 million‐$1 billion.............................. 9 CA banks $1‐$5 billion ................................................ 11 CA banks $5‐$10 billion ............................................. 12 CA banks $10‐$100 billion........................................ 13 CA thrifts ........................................................................... 14 California mergers ........................................................ 16 LTM P/E ratios ............................................................... 18 Price/Book ratios.......................................................... 19 Ratio comparisons ........................................................ 20 Stock performance under $125 million .............. 21 Stock performance $125‐$250 million ............... 22 Stock performance $250‐$500 million ............... 23 Stock performance $500 mln‐$1 bln.................... 24 Stock performance $1‐$5 billion............................ 25 Stock performance $5‐$10 billion ......................... 25 Stock performance $10‐$100 billion.................... 26 Stock performance thrifts ......................................... 26 Return rankings ............................................................. 27 The number of banks continued to dwindle in 2013, yet bank stocks recorded an exceptional year. At the end of 2013, there were 6,813 FDIC‐insured ϐinancial institutions, a decline of 279 institutions over the year. That 3.9% drop essentially matched the percentage decline in 2012 and brought the number of banks to an historic low in the annuls of FDIC history. By the end of 2013, there were 17 fewer ϐinancial institutions headquartered in California than at the start of the year. The number of publicly‐traded California banks declined, with 2013 ending with seven fewer banks in the Carpenter & Company tracking report. Scarcity may be a contributing factor for the exceptional stock performance of the California banking industry. Over 83% of the companies tracked in the Carpenter & company stock report recorded higher stock prices, and more than 85% of the companies with rising stock prices experienced price gains well in excess of 10%. Largely due to the run‐up in stock prices, the market capitalization of California’s publicly‐traded banks and thrifts was 67% higher than at the end of 2012. NOTE: This analysis utilized data for bank assets, earnings, and share counts, as of September 30, 2013.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Carpenter & Company --

2013 INDUSTRY VALUATION

Thenumberofbankmergerannouncementsin2013wasessentially unchanged from the number of mergersannounced in 2012. There were a total of 244 mergerannouncementsinvolvingU.S. inancialinstitutionsmadein 2012, according to SNL Financial. In 2013, the totalnumber of inancial institution merger announcementsequaled 242. Of the 2012 merger announcements, 218were completed by year‐end 2013, ive were stillpending,and21hadbeen terminated.Throughthe irst17daysof2014,143ofthemergersannouncedin2013had been completed, 85were still pending, and 14 hadbeenterminated.For the merger transactions with reported deal ratios,the average price to tangible book value (P/TBV) ratioforthe2013announcementsat1.28xwasslightlyhigherthan the average P/TBV ratio of 1.20x for the 2012mergerannouncements.Assets to be acquired under the 2012 non‐terminatedmergerannouncementstotaled$137.1billion,comparedwith $111.6 billion for the non‐terminated mergerannouncements made in 2013. The largest merger bytargetsizeforthe2013announcementswasthependingacquisition by Umpqua of the $9.9 billion SterlingFinancial. The largest merger from the 2012announcementswasM&TBancorp’splannedacquisitionofthe$43.6billionHudsonCityBancorp.TheM&Tdeal,whichwas announced on August 27, 2012, is currentlyscheduled to close by the end of 2014. According tocompany ilings,regulatoryapprovalhadbeenheldupbyBSAissuesatM&T.

INDUSTRY VALUATIONS: BANK MERGER AND ACQUISITION ACTIVITY

CONTENTS BankMergeractivity.....................................................1Nationalbankstockprices.........................................2Californiabankstockprices.......................................3CAbanksunder$125million.....................................4CAbanks$125‐$250million.......................................6CAbanks$250‐$500million.......................................8CAbanks$500million‐$1billion..............................9CAbanks$1‐$5billion................................................11CAbanks$5‐$10billion.............................................12CAbanks$10‐$100billion........................................13CAthrifts...........................................................................14Californiamergers........................................................16LTMP/Eratios...............................................................18Price/Bookratios..........................................................19Ratiocomparisons........................................................20Stockperformanceunder$125million..............21Stockperformance$125‐$250million...............22Stockperformance$250‐$500million...............23Stockperformance$500mln‐$1bln....................24Stockperformance$1‐$5billion............................25Stockperformance$5‐$10billion.........................25Stockperformance$10‐$100billion....................26Stockperformancethrifts.........................................26Returnrankings.............................................................27

Thenumberofbankscontinuedtodwindlein2013,yetbankstocksrecordedanexceptionalyear.Attheendof2013, therewere6,813FDIC‐insured inancial institutions,adeclineof279 institutionsover theyear. That 3.9% drop essentially matched the percentage decline in 2012 and brought the number ofbankstoanhistoriclowintheannulsofFDIChistory.Bytheendof2013,therewere17fewer inancialinstitutions headquartered in California than at the start of the year. The number of publicly‐tradedCaliforniabanksdeclined,with2013endingwithsevenfewerbanksintheCarpenter&Companytrackingreport. Scarcity may be a contributing factor for the exceptional stock performance of the Californiabankingindustry.Over83%ofthecompaniestrackedintheCarpenter&companystockreportrecordedhigherstockprices,andmorethan85%ofthecompanieswithrisingstockpricesexperiencedpricegainswellinexcessof10%.Largelyduetotherun‐upinstockprices,themarketcapitalizationofCalifornia’spublicly‐tradedbanksandthriftswas67%higherthanattheendof2012.NOTE:Thisanalysisutilizeddataforbankassets,earnings,andsharecounts,asofSeptember30,2013.

Carpenter & Company --

Industry Valuations

Forthemergerannouncementsmadein2013,Texaswasthestatewiththemostmergertargetsat29.ThestateinthedistantsecondpositionformostmergerswasIllinoisat14,andCaliforniawasthirdwith13.Thetargetassetsizeforthe2013classofmergerannouncementsrangedfrom$4.2million(OakwoodStateBank)to $9.9 billion (Sterling Financial). The average asset size of the targets equaled $492 million, while themedian sizewas $168million. In 2012, the acquisition target size ranged between $7.4million and $43.6billion.Theaveragetargetsizeforthe2012mergerannouncementsequaled$615million,whilethemedianmergersizewas$126million.A total of 13 merger announcements in 2013 involved California institutions, compared with 14announcements in2012.All14of the2012Californiamergerannouncementswerecompletedbyyear‐end2013,while eight of the13announcements from2013were closed in2013.Of the ivependingCaliforniaacquisitions, two transactions involved the recapitalization of institutions by private investors, while theotherthreetransactionswillresultinthefurtherreductioninthenumberofbankingchartersinthestate.Forthe irst27daysof2014,therehadbeen15bankmergerannouncementsmadeandinvolved$9.1billionintargetassets.Threeoftheannouncedacquisitionstargetedinstitutionswithmorethan$1billioninassets.Reported deal ratios for the 2014 mergers announced through January 27 indicated a step‐up in pricingrelative totangiblebookvalue.Dealratioswerereported for13of the15mergerannouncements,withanaveragepricetotangiblebookvalueof1.45x.Twooftheearly2014announcementsinvolvedtheacquisitionsofpublicly‐tradedCaliforniabanks,speci icallyBankonIt,Inc.andNorthValleyBancorp.

INDUSTRY VALUATIONS: NATIONAL BANK STOCK PRICES Oneofthemostfeaturedeconomicnewsitemin2013wastheexceptionalperformanceofthestockmarket.TheDowJonesIndustrialAverageclimbed26.5%in2013forthebestmarketadvancesince1997.In2012,theincreasefromyear‐endtoyear‐endfortheDowequaled7.3%.In2011,thegainwas5.5%.At no time over the course of last year was the Dow ever below its start‐of‐the‐year level. Over the 252tradingdaysin2013,theDowwashigherin146ofthosedaysfora58%ratioofup‐days.Inaddition,for43ofthetradingdates,theDowincreasedbymorethan100points.The rise inequitymarketpriceswasbroadlybased.TheS&P500 index climbed29.6%over the courseof2013, comparedwith the 13.4% rise in 2012 and no change in 2011. The trends for theNASDAQwere adeclineof1.8%in2011,andgainsof15.9%in2012and34.0%in2013.Thebankingindustryexceededtheexceptionalstockperformanceofthebroadermarket,asre lectedintheresults of the Dow, S&P 500, and NASDAQ indices. The KBW Bank stock index increased 35.1% over thecourseof2013,besting therise in theDowbymorethan8.5percentagepoints.The35.1%advance in theKBWindexin2013followedthe30.2%advancethatoccurredin2012,thusproducingatwo‐yearincreaseintheKBWindexof76%.Thetwo‐yeargainintheDowwas36%.

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

J F M A M J J A S O N D

Annual Change in DJIA

2011

2012

2013

12/31= 1.0

1.00

1.05

1.10

1.15

1.20

1.25

1.30

1.35

1.40

J A J O

2013ChangeinStockIndices

KBWBank

DJIA

1/1/13=1.0

Carpenter & Company --

Industry Valuations

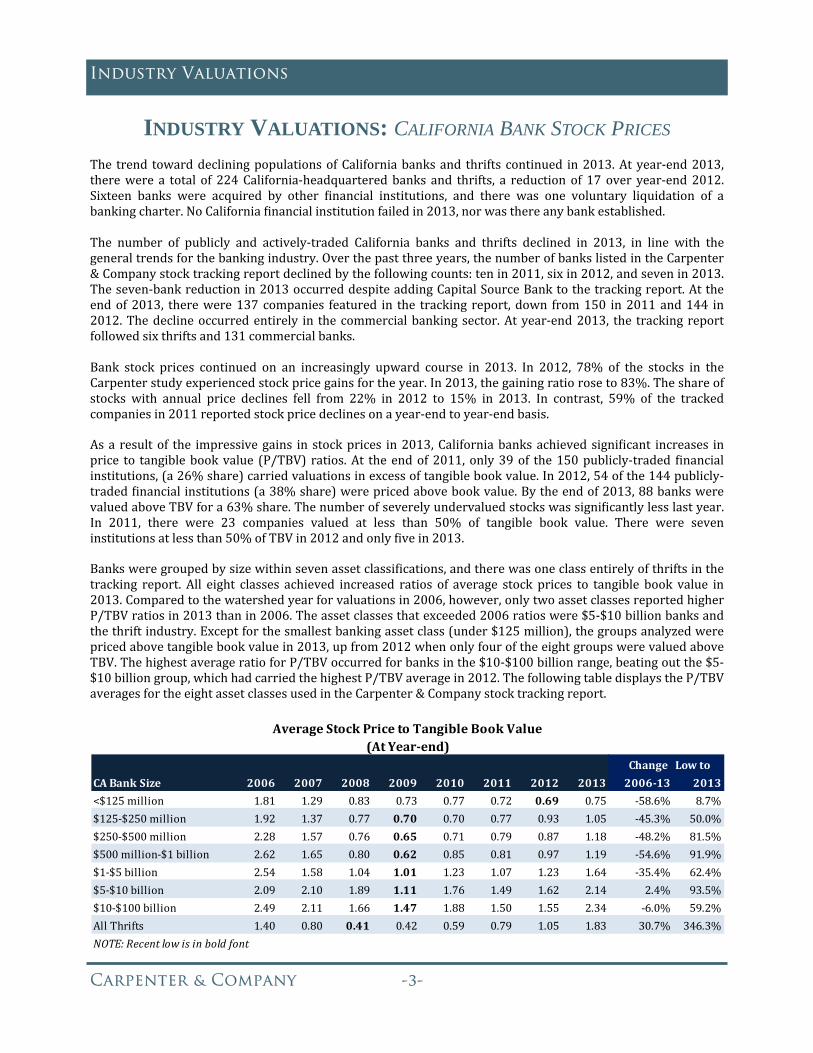

INDUSTRY VALUATIONS: CALIFORNIA BANK STOCK PRICES The trend towarddecliningpopulationsofCaliforniabanksand thrifts continued in2013.Atyear‐end2013,therewere a total of 224California‐headquarteredbanks and thrifts, a reductionof 17 over year‐end2012.Sixteen banks were acquired by other inancial institutions, and there was one voluntary liquidation of abankingcharter.NoCalifornia inancialinstitutionfailedin2013,norwasthereanybankestablished.The number of publicly and actively‐traded California banks and thrifts declined in 2013, in line with thegeneraltrendsforthebankingindustry.Overthepastthreeyears,thenumberofbankslistedintheCarpenter&Companystocktrackingreportdeclinedbythefollowingcounts:tenin2011,sixin2012,andsevenin2013.Theseven‐bankreductionin2013occurreddespiteaddingCapitalSourceBanktothetrackingreport.Attheendof2013, therewere137companies featured in the tracking report,down from150 in2011and144 in2012.Thedeclineoccurredentirely in thecommercialbankingsector.Atyear‐end2013, the tracking reportfollowedsixthriftsand131commercialbanks.Bank stock prices continued on an increasingly upward course in 2013. In 2012, 78% of the stocks in theCarpenterstudyexperiencedstockpricegainsfortheyear.In2013,thegainingratioroseto83%.Theshareofstocks with annual price declines fell from 22% in 2012 to 15% in 2013. In contrast, 59% of the trackedcompaniesin2011reportedstockpricedeclinesonayear‐endtoyear‐endbasis. Asa resultof the impressivegains in stockprices in2013,Californiabanksachievedsigni icant increases inprice to tangiblebookvalue (P/TBV) ratios.At theendof2011,only39of the150publicly‐traded inancialinstitutions,(a26%share)carriedvaluationsinexcessoftangiblebookvalue.In2012,54ofthe144publicly‐traded inancialinstitutions(a38%share)werepricedabovebookvalue.Bytheendof2013,88bankswerevaluedaboveTBVfora63%share.Thenumberofseverelyundervaluedstockswassigni icantlylesslastyear.In 2011, there were 23 companies valued at less than 50% of tangible book value. There were seveninstitutionsatlessthan50%ofTBVin2012andonly ivein2013. Banksweregroupedbysizewithinsevenassetclassi ications,andtherewasoneclassentirelyofthriftsinthetracking report. All eight classes achieved increased ratios of average stock prices to tangible book value in2013.Comparedtothewatershedyearforvaluationsin2006,however,onlytwoassetclassesreportedhigherP/TBVratiosin2013thanin2006.Theassetclassesthatexceeded2006ratioswere$5‐$10billionbanksandthethriftindustry.Exceptforthesmallestbankingassetclass(under$125million),thegroupsanalyzedwerepricedabovetangiblebookvaluein2013,upfrom2012whenonlyfouroftheeightgroupswerevaluedaboveTBV.ThehighestaverageratioforP/TBVoccurredforbanksinthe$10‐$100billionrange,beatingoutthe$5‐$10billiongroup,whichhadcarriedthehighestP/TBVaveragein2012.ThefollowingtabledisplaystheP/TBVaveragesfortheeightassetclassesusedintheCarpenter&Companystocktrackingreport.

Change Lowto

CABankSize 2006 2007 2008 2009 2010 2011 2012 2013 2006‐13 2013

<$125million 1.81 1.29 0.83 0.73 0.77 0.72 0.69 0.75 ‐58.6% 8.7%

$125‐$250million 1.92 1.37 0.77 0.70 0.70 0.77 0.93 1.05 ‐45.3% 50.0%

$250‐$500million 2.28 1.57 0.76 0.65 0.71 0.79 0.87 1.18 ‐48.2% 81.5%

$500million‐$1billion 2.62 1.65 0.80 0.62 0.85 0.81 0.97 1.19 ‐54.6% 91.9%

$1‐$5billion 2.54 1.58 1.04 1.01 1.23 1.07 1.23 1.64 ‐35.4% 62.4%

$5‐$10billion 2.09 2.10 1.89 1.11 1.76 1.49 1.62 2.14 2.4% 93.5%

$10‐$100billion 2.49 2.11 1.66 1.47 1.88 1.50 1.55 2.34 ‐6.0% 59.2%

AllThrifts 1.40 0.80 0.41 0.42 0.59 0.79 1.05 1.83 30.7% 346.3%

NOTE:Recentlowisinboldfont

AverageStockPricetoTangibleBookValue(AtYear‐end)

Carpenter & Company --

Industry Valuations

From2006through2010,thethriftclasshadbeenthelowestperforminggroupintermsofP/TBV.Thriftsweretiedforthethirdlowestinperformancein2011andclimbedtothirdbestoftheeightin2013.Thriftsrecordedin2013thelargestpercentageincreaseinP/TBVamongtheassetclasses,up74%.Thesmallestgainin2013P/TBVwasthe9%advanceforbanksunder$125million.ThemarketcapitalizationfortheCaliforniapublicly‐tradedbanksandthriftstrackedbyCarpenter&Companyincreased67%in2013toatotalof$43.2billion,comparedwith$26.8billionin2012.Thisgainintotalmarketcapitalization occurred despite the seven‐bank reduction in the number of banks. As a result, the per‐bankmarketcapitalizationin2013expanded75%overthepreviousyear.

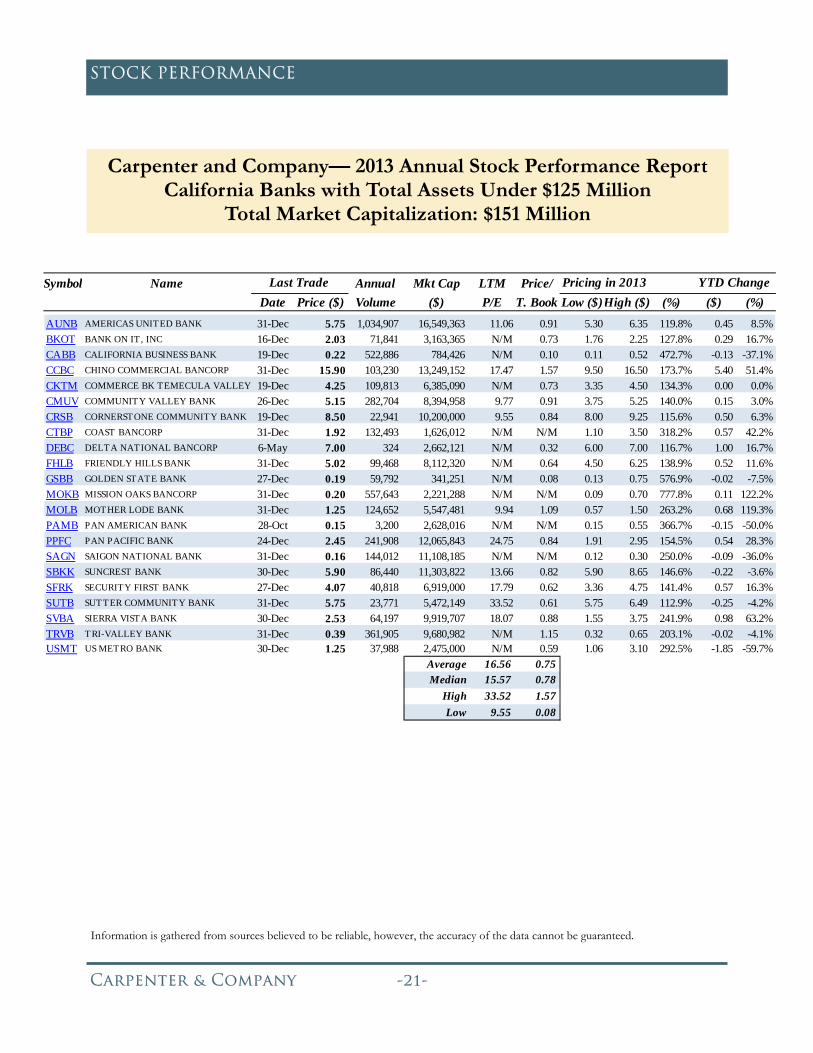

INDUSTRY VALUATIONS: BANKS UNDER $125 MILLION Bankswereanalyzedbyassetsize in theCarpenter&Companystockmarket report.Thesmallestassetsizestudiedwerebanksunder$125million.Attheendof2013,therewere22publicly‐tradedCaliforniabankswithassetslessthan$125million.Theassetsforthisgroupandforalloftheassetclassesinthisreportwerebasedupondataavailableatyear‐end2013,whichwereinformationfromtheSeptember30,2013CallReports.Thereported data for assets, share counts, tangible book value, and last twelve month (LTM) earnings utilizedinformationasofSeptember30,2013.Thereweretwofewerbankswithlessthan$125millioninassetsattheendof2013thanayearearlier.Themovementinthisassetclassincludedthreebanksthatgrewabove$125million,onebankthatwasacquired,andtwobanksthatdeclinedinassetstorejointhisclass.Twentybankscarriedoverinthisgroupfrom2012.MojaveDesertBank,N.A.wasacquired in January2013byMissionBancorp, theparentcompanyofMissionBank,whichisheadquarteredinBakers ield.The$7.1millionpurchaseofMojaveDesertBankwasacashandstock transaction, priced at 0.82x tangible book value. The price represented a 42% premium to the pre‐announcementtradingpriceofMOJA.Northern CaliforniaNational Bank, Paci ic Alliance Bank, andVibra Bank grew above $125million in assetsoverthecourseof2013tojointhenextlargerassetclass.BankonIt,Inc.andCoastBancorpdeclinedinsizetorejointhisgroup.Asthecostofcompilingwithbankingregulationsincreasedtorepresentarisingexpenseforbanksofallsizes,investorperceptionsoftenviewedthatacertainsizeofoperationswascriticalforpro itableandfuturegrowth.Asaresult,someinvestorsheldthatverysmallbanksmayfaceoperationalandearningschallenges.Theunder$125millionclasshadthelowestshareofrisingstockpricesamongtheeightassetclassesanalyzed.Only54%ofthe22stocksinthisgroupexperiencedstockpricegainsin2013.Thenextlowestshareofpricegainswasthe$125‐$250milliongroupwitha77%shareofstockpricegainers.In2013,stockpricesfor13ofthe22banksinthisgroupwerehigherovertheyear,whileeightstocksdeclinedinprice,andonebankreportednochange instockprice. In2012, thegroupof24banksunder$125millionreported13bankswithprice gains and11bankswithpricedeclines. The steepestpercentageprice gain in2013wasthe122%advanceinthepriceofMissionOaksBancorp,whereinitsstockpriceincreased$0.11overtheyearfrom$0.09/sharein2012to$0.20/shareattheendof2013.Intotal,tenofthebanksinthiscategoryexperienced signi icant percentage gains in stockprices. Signi icant price gainswere de ined as increases inexcessof10%.InadditiontoMissionOaks,othersigni icantpricegainswererecordedbyMotherLodeBank,SierraVistaBank,ChinoCommercialBancorp,CoastBancorp,PanPaci icBank,BankonIt,Inc.,DeltaNationalBancorp,SecurityFirstBank,andFriendlyHillsBank.Ofthe11bankswithdecliningstockpriceslastyear,fourstocksdroppedbymorethan35%.Thesteepeststockpricedeclinewas60%forU.S.MetroBank.

Carpenter & Company --

Industry Valuations

Theunder$125millionassetclasswastheonlygroupwithanaverageprice/tangiblebookvalueratiothatwasless than 1.0x, that is, valued under tangible book. Only three banks in this class traded above book value,notablyChinoCommercialBancorp,MotherLodeBank,andTri‐ValleyBank.ChinoCommercialBankhadthehighestP/TBVof1.57x.Therewerethreebanksthattradedatlessthan50%ofbookvalue.ThelowestP/TBVforthisgroupandforallpublicly‐tradedinstitutionswas0.08xforGoldenStateBank.Theotherbankspricedunder50%ofbookvaluewereCaliforniaBusinessBankandDeltaNationalBancorp.Four companies,CoastBancorp,MissionOaksBancorp,PanAmericanBank,andSaigonNationalBank,didnothavemeaningfulP/TBVratiosandwerenotincludedintheaverage.TheaverageP/TBVforthegroupwithmeaningfulP/TBVequaled0.75x,upfromthe0.69xin2012.Asarule,whenaP/Eratioexceeded50x,itwasdeterminedthatpro itsweretoolowrelativetopricingtoyieldameaningfulratio.Hence,P/Eratios inexcessof50xwerecitedasNMornotmeaningful. Inaddition, if thebank sustained losses, theP/E ratiowas shownasNM.Twelve of the22banks reportedpro its for the lasttwelve months (LTM) ending September 30, 2013. Of these 12 pro itable banks, ten of the banks hadmeaningfulpriceearningsratios,thatis,aratiobelow50x.ThemeaningfulpricetoLTMearningsratiosforthisasset class ranged from 9.55x for Cornerstone Community Bank to 33.52x for Sutter Community Bank. TheaverageP/Eforthisclassequaled16.6xin2013,upslightlyfromthe16.3xaveragefor2012.Thetradingvolumeforthesebankswasgenerallyquitesmall.Thevolumeofoutstandingshares,notablythosesharesnotheldby insiders,alsotendedbequite limitedforthisassetclass.Asaresult, theper‐banktradingvolumeforthisassetclasswasthesmallestofanyoftheclasses.Nonetheless,allofthebankstradedoverthecourseof theyear,andonlytwobanksdidnottradeduringDecember.Onebankhad its lastpostedtrade inMay.Thecombinedvolumeofsharestradedoverthecourseof theyearequaled4.1million,anapproximateannual volume of 187,500 shares per bank. This average trading volume in 2013was 23% lower than theaveragevolume for the$125‐$250millionassetclass.Thestockwith thehighestannualvolumeof trades in2013wasAmericas United Bankwith over 1million shares traded. The lowest volumewas the 324 sharestradedforDeltaNationalBancorp.Thebankwiththelargestmarketcapitalizationattheendof2013wasAmericasUnitedBankat$16.5million.Twobankscarriedmarketcapitalizationoflessthan$1million,notablyCaliforniaBusinessBankat$784,426andGoldenStateBankat$341,251.Thetotalmarketcapitalizationofthisgroupequaled$151million,downfromthe$172millionin2012marketcapitalization.Attheendof2013,thereweretwofewerbanksthanintheprioryear.Marketcapitalizationonaper‐bankbasis,however,edgedlowerin2013to$6.8millionfrom$7.1millionattheendof2012.Ofthe22companiesinthisgroup, ifteenreportedyear‐over‐year(YoY)increasesinmarketcapitalization,sixweredownovertheyear,andonewasessentiallyunchanged.Recapitalizationbyaprivate investorbrought$7.9millionofnewcapital toCaliforniaBusinessBank.SierraVistaBankgenerated$1.5millioninnewcapitaloverthelasttwelvemonthsendingSeptember30,2013.

LargestPriceGainsMissionOaksBancorp +122.2%MotherLodeBank +119.3%SierraVistaBank +63.2%SteepestPriceDeclineUSMetroBank ‐59.7%

BANKS UNDER $125 MILLION (continued)

0.0

0.5

1.0

1.5

2.0

2.5

02 03 04 05 06 07 08 09 10 11 12 13

1.51.7

2.1 2.01.8

1.3

0.80.7 0.8 0.7 0.7 0.8

PricetoBook‐‐CABanks<$125Million

Carpenter & Company --

Industry Valuations

INDUSTRY VALUATIONS: BANKS BETWEEN $125 AND $250 MILLION Theassetcategorywiththelargestnumberofbankswasintherangeof$125and$250millionbanksbaseduponSeptember30,2013data.AttheendofDecember2012,therewere47banksinthisclass.Overthecourseofthepastyear,thisgroupdeclinedbyeightto39banks.Within this class, 36banks remained in the groupover the year.Oneof these carry‐over banks changed itsnamefromOjaiCommunityBanktoOCBBancorp.Elevenbanksexitedthisclass.Twobanksdeclinedinsizetorejointhesmallestassetclass.Threebankswereacquiredbyotherbanks.Sixbanksgrewinassetstojointhe$250‐$500millionclass.Threebanksgrewintothisclassfromtheunder$125milliongroup.Threepublicly‐tradedbanksfromthe$125to$250milliongroupwereacquiredin2013.VisaliaCommunityBankwasacquiredon July1,2013byCentralValleyCommunityBancorp ina50/50cash/stocktransaction.The$21.3milliondeal forVisaliaCommunityBankwasvaluedat1.24x tangiblebookvalue.Paci icPremierBancorpclosedonitsacquisitionofSanDiegoTrustBankonJune24,2013.TheacquisitionofSanDiegoTrustBank was through a cash/stock transaction valued at $31.1 million or 1.21x tangible book value. SterlingFinancialCorporationacquiredCommerceNationalBankonOctober1,2013inacashpurchasevaluedat$42.9million or 1.43x tangible book value. Subsequently, Sterling Financial Corp. of Washington became theacquisitiontargetofUmpquaHoldingsCorp.ofOregon.Growing into this asset class from the under $125 million group were Northern California National Bank,Paci icAllianceBank,andVibraBank.Leavingthisassetclasstorejointheunder$125milliongroupwereBankon It, Inc.andCoastBancorp.Growing into the$250‐$500milliongroupwereFocusBusinessBank,MissionValley Bancorp, Open Bank, Redwood Capital Bancorp, and Seacoast Commerce Bank. Coronado First Bankacquired privately‐held SanDiego Private Bank onApril 2, 2013 in an all‐stock transaction valued at $13.6millionor1.04xtangiblebookvalue.CoronadoFirstBankchangeditsnametoSanDiegoPrivateBankanditstickersymbolSDPBandgrewintothe$250‐$500millionclass.In addition to the completed transactions involving banks in this group, Independence Bank announced onNovember 4, 2013 its intention to acquire Premier Service Bank. This pending 55% cash/45% stocktransactionwasvaluedat$8.6millionforapricetotangiblebookvalueratioof1.26x.Atthebeginningof2013,Premier Service Bank had been under a merger agreement with First California Financial Group, Inc.; thisagreementwasterminatedonJanuary30,2013.Ofthe39banksinthe$125‐$250milliongroupattheendofDecember2013,31banksreportedYoYgainsinstockprices. Sevenbanks reported lower stockprices, andonebankwasunchanged in stockpriceover theyear.Twenty‐threebanksreportedstockpricegainsinexcessof10%.Onlyoneofthepricedeclinesexceeded10%, notably OCB Bancorp at ‐14%. AltaPaci ic Bank ended 2013 with no change in stock price, despitereportingstocktradingactivity.Acquisition‐target Premier Service Bank experienced the steepest price increase last year, up 583%. Othertriple‐digitpricegainswererealizedforCalWestBancorp(278%),ValleyCommunityBank(221%),NorthernCalifornia Bancorp, Inc. (200%), and Uniti Financial Corp (149%). Other signi icant stock price gains wererecorded for American California Bank, American Riviera Bank, Bank of Napa, N.A., Bank of Santa Clarita,CommunityBusinessBank,CommunityBankoftheBay,Community1stBank,BankofSouthernCalifornia,N.A.,First Mountain Bank, Golden Valley Bancorp, Liberty Bancorp, Inc., MNB Holdings Corp., Orange CountyBusinessBank, PinnacleBank, Paci ic AllianceBank, Paci ic CommerceBank, ProAmericaBank,RiverValleyCommunityBank,andSummitBancshares,Inc.

Carpenter & Company --

Industry Valuations

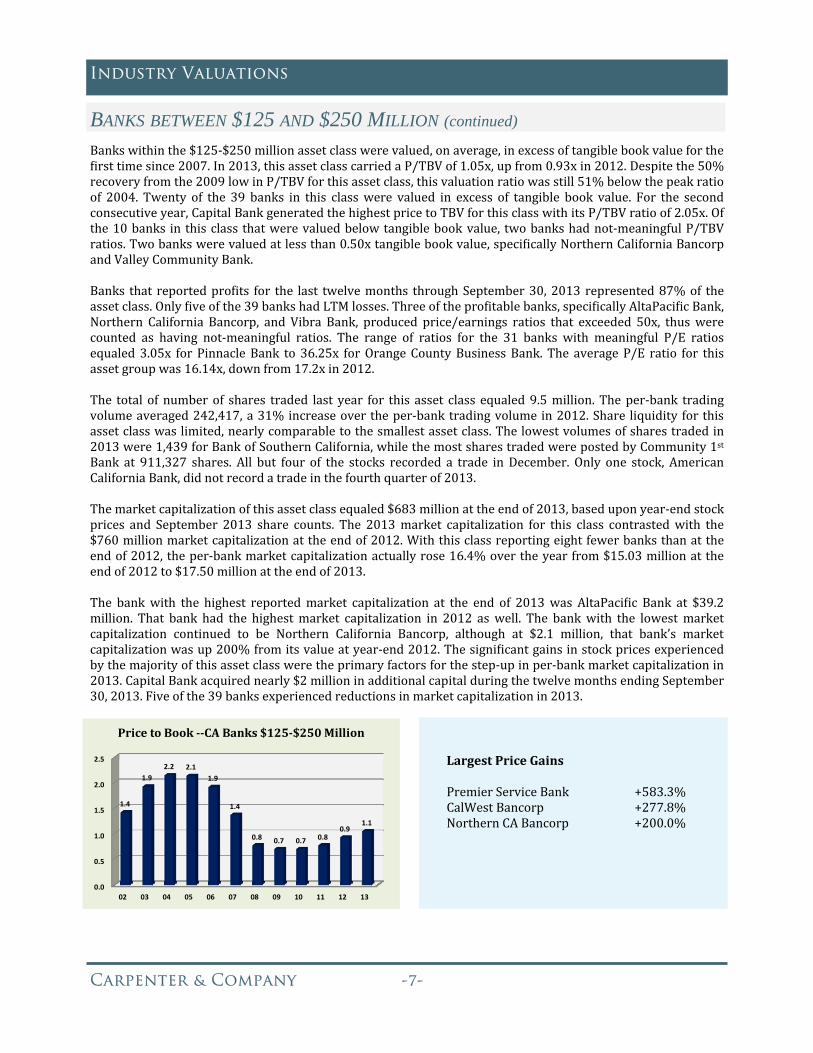

Bankswithinthe$125‐$250millionassetclasswerevalued,onaverage,inexcessoftangiblebookvaluefortheirsttimesince2007.In2013,thisassetclasscarriedaP/TBVof1.05x,upfrom0.93xin2012.Despitethe50%recoveryfromthe2009lowinP/TBVforthisassetclass,thisvaluationratiowasstill51%belowthepeakratioof 2004. Twenty of the 39 banks in this classwere valued in excess of tangible book value. For the secondconsecutiveyear,CapitalBankgeneratedthehighestpricetoTBVforthisclasswithitsP/TBVratioof2.05x.Ofthe10banks in thisclass thatwerevaluedbelowtangiblebookvalue, twobankshadnot‐meaningfulP/TBVratios.Twobankswerevaluedatlessthan0.50xtangiblebookvalue,speci icallyNorthernCaliforniaBancorpandValleyCommunityBank.Banks that reportedpro its for the last twelvemonths throughSeptember30,2013 represented87%of theassetclass.Only iveofthe39bankshadLTMlosses.Threeofthepro itablebanks,speci icallyAltaPaci icBank,Northern California Bancorp, and Vibra Bank, produced price/earnings ratios that exceeded 50x, thuswerecounted as having not‐meaningful ratios. The range of ratios for the 31 banks with meaningful P/E ratiosequaled3.05x forPinnacleBank to 36.25x forOrangeCountyBusinessBank. The averageP/E ratio for thisassetgroupwas16.14x,downfrom17.2xin2012.The total of numberof shares traded last year for this asset class equaled9.5million.Theper‐bank tradingvolumeaveraged242,417,a31%increaseovertheper‐banktradingvolumein2012.Share liquidity forthisassetclasswaslimited,nearlycomparabletothesmallestassetclass.Thelowestvolumesofsharestradedin2013were1,439forBankofSouthernCalifornia,whilethemostsharestradedwerepostedbyCommunity1stBank at 911,327 shares. All but four of the stocks recorded a trade inDecember. Only one stock, AmericanCaliforniaBank,didnotrecordatradeinthefourthquarterof2013.Themarketcapitalizationofthisassetclassequaled$683millionattheendof2013,baseduponyear‐endstockprices and September 2013 share counts. The 2013market capitalization for this class contrastedwith the$760millionmarketcapitalizationattheendof2012.Withthisclassreportingeightfewerbanksthanattheendof2012,theper‐bankmarketcapitalizationactuallyrose16.4%overtheyearfrom$15.03millionattheendof2012to$17.50millionattheendof2013.The bankwith the highest reportedmarket capitalization at the end of 2013was AltaPaci ic Bank at $39.2million. That bank had the highestmarket capitalization in 2012 aswell. The bankwith the lowestmarketcapitalization continued to be Northern California Bancorp, although at $2.1 million, that bank’s marketcapitalizationwasup200%fromitsvalueatyear‐end2012.Thesigni icantgainsinstockpricesexperiencedbythemajorityofthisassetclassweretheprimaryfactorsforthestep‐upinper‐bankmarketcapitalizationin2013.CapitalBankacquirednearly$2millioninadditionalcapitalduringthetwelvemonthsendingSeptember30,2013.Fiveofthe39banksexperiencedreductionsinmarketcapitalizationin2013.

LargestPriceGainsPremierServiceBank +583.3%CalWestBancorp +277.8%NorthernCABancorp +200.0%

BANKS BETWEEN $125 AND $250 MILLION (continued)

0.0

0.5

1.0

1.5

2.0

2.5

02 03 04 05 06 07 08 09 10 11 12 13

1.4

1.9

2.2 2.1

1.9

1.4

0.8 0.7 0.7 0.80.9

1.1

PricetoBook‐‐CABanks$125‐$250Million

Carpenter & Company --

Industry Valuations

INDUSTRY VALUATIONS: BANKS BETWEEN $250 AND $500 MILLION The number of banks in the $250‐$500 million asset class was unchanged in 2013 at 23 for the thirdconsecutiveyear.Despitetheconsistency inthenumberofbanks, thecompositionofbankswithinthisassetclassvariedovertheyear.Asin2012,therewere17carry‐overbanksfromthepreviousyear.Sixbanksjoinedthisclassfromthe$125‐$250milliongroup.Fivebanksgrewto jointhe$500millionto$1billionclass.Onebankwasacquiredbyalargerin‐statebank.Joining this class in 2013 from the smaller groupwere Focus Business Bank,Mission Valley Bancorp, OpenBank,RedwoodCapitalBancorp,SeacoastCommerceBank,andSanDiegoPrivateBank.Fiveofthesesixbanksexperiencedorganicassetgrowth,whilethegrowthinSanDiegoPrivateBankwasassistedbythemergerofequalsbetweenCoronadoFirstBankandin‐marketSanDiegoPrivateBank.Growingintothenextlargerassetclass were California First National Bancorp, Commonwealth Business Bank, 1st Century Bancshares, Inc.,PlumasBancorp,andSecurityCaliforniaBancorp.BankofAlameda,thesubsidiarybankofNorCalCommunityBancorp,wasacquiredonNovember29,2013byBankofMarinBancorp.BankofMarinpaid$32.5millionor1.23xTBVinacash/stocktransactionforBankofAlameda.The acquisition of NCAL Bancorp by privately‐held Grandpoint Capital, Inc. was terminated on January 28,2013.OnSeptember16,2013,anannouncementwasmadethataprivateinvestorwouldinfuse$23.5millioninnewcapital toobtainamajorityownershipofNCALBancorp,andexistingdirectorswill investanadditional$1.5millionintothecompany.Thistransactionwasanticipatedtocloseinthe irsthalfof2014.HeritageOaksBancorpannouncedonOctober21,2013itsintentiontoacquirein‐marketMissionCommunityBancorp.Thiscash‐stocktransactionincludedtheassumptionofdebtinadealvaluedat$56.0millionor1.63xtangiblebookvalue.Overthecourseof2013,nineteenbanksinthisclassexperiencedstockpricegains,whilefourstocksdeclinedin price. Following the termination of the announced acquisition by Grandpoint, the price of NCAL edgedsteadilylowerovertheyeartoproducethesteepestannualstockpricedeclineof72%.Seventeenofthe19stocksrecordedsigni icant,over10%,gainsinstockpricesin2013.Thesteepestpricegainwas recorded for Open Bank, up 257%. Other double‐digit rates of stock price gains were reported forAvidbank Holdings, Inc., Bay Commercial Bank, California Bank of Commerce, CommerceWest Bank, FocusBusinessBank,MissionCommunityBancorp,ManhattanBancorp,MissionValleyBancorp,PresidioBank,PlazaBank,RedwoodCapitalBancorp,SeacoastCommerceBank,SantaCruzCountyBank,SanDiegoPrivateBank,SummitStateBank,andValleyCommerceBancorp.

LargestPriceGainsOpenBank +257.1%MissionCommunityBancorp +92.9%SeacoastCommerceBank +77.8%SteepestPriceDeclineNCALBancorp ‐71.8%0.0

0.5

1.0

1.5

2.0

2.5

3.0

02 03 04 05 06 07 08 09 10 11 12 13

1.7

2.2

2.6 2.6

2.3

1.6

0.80.7 0.7 0.8 0.9

1.2

PricetoBook‐‐ CABanks$250‐$500Mln

Carpenter & Company --

Industry Valuations

Theaveragepricetotangiblebookvalueforthisassetclassequaled1.18xin2013,upsigni icantlyfromthe0.87xaveragein2012.Eighteenofthe23bankswerepricedabovetangiblebookvalue.Fouroftheremainingivebankswerevaluedwithin11basispointsoftangiblebookvalue.ThevaluationforUnitedAmericanBankwasdeemedtobenotmeaningful.ThehighestvaluationwascarriedbySeacoastCommerceBankat2.03x,while thebankswith the lowestmeaningful P/TBVwere tied at 0.89x forBayCommercialBankandNCALBancorp.TheP/TBVratioforthisassetclassralliedgreatlyfromits2009cyclicallow,increasing82%throughtheendof2013.Despitethisrecovery,theP/TBVratioattheendof2013wasstill55%belowthepeakratiothathadoccurredin2004.Onlytwobanksinthisgroupof23 inancial institutionssustainedlossesforthelasttwelvemonthsthroughSeptember30,2013,notablyNCALBancorpandUnitedAmericanBank.LTMpro itsat SeacoastCommerceBankproducedaP/Eratioinexcessof50xand,therefore,theratioforthatcompanywasdeemedtobenotmeaningful. The average P/E ratio for the remaining 30 companies averaged 17.88x at the end of 2013,compared to the 15.31x ratio in 2012. The P/E ratios ranged from 8.72x for Redwood Capital Bancorp to36.85xforPresidioBank.Trading activity for banks in the $250‐$500million class wasmore robust than for the two smaller assetclasses.All23bankstockstradedinDecember,andallbuttwobankspostedtradesduringthe inalweekoftheyear.Thesumofalltradesin2013forthisclassequaled11.1millionsharesforaper‐bankaveragetradingvolume of 480,884 shares or 156%more than the under $125 million bank group. The volume of tradesrangedfrom25,009sharesforValleyRepublicBankto1.47millionsharesforSummitStateBank.Themarketcapitalization for thisclassequaled$898million,upmarginally from$830million in2012.Theaverageper‐bankmarketcapitalizationequaled$39.0millioncomparedto$36.1millionin2012.Therelativestabilityoftheyear‐over‐yearmarketcapitalizationcomparisoncouldbeslightlymisleading.Thebanksthatgrewoutofthisgroupreportedaggregatemarketcapitalizationof$334million,whilethebankscomingintothisclasshadatotalmarketcapitalizationof$196million,or$138millionlessthantheexitinggroup.Therangeinmarketcapitalizationattheendof2013equaledalowof$1.3millionforNCALBancorptoahighof$60.3millionforCommerceWestBank.Withinthisassetgroup,increasesinmarketcapitalizationoccurredforallofthebanks,exceptGreaterSacramentoBancorp.Theannualriseinmarketcapitalizationresultedfromthesteepincreasesstockpricesthatwereexperiencedbythemajorityofthesecompanies.In addition to the price‐driven increase in market capitalization, two banks generated merger‐relatedincreasesinsharecountandcapital.SanDiegoPrivateBankrecognizedmerger‐relatedincreasesincapitalof$16.2million.MissionBank reported a $3.5million increase in capital as a result of itsmerger. Twootherbanksreportedstockofferingorconversionsthataddedmorethan$1millionincapital,speci icallythe$1.5millioncapitalincreasefor1stCapitalandthe$7.9millionofferingbyAvidbank.

INDUSTRY VALUATIONS: BANKS BETWEEN $500 MILLION AND $1 BILLION

ThenumberofCaliforniabankswithassets intherangeof$500millionand$1billiongrewbythree intheyearendingDecember2013.Thethree‐bankgainwasachievedthroughtheadditionofsixbankstothisclassandtheeliminationofthreebanks.Fivebanksjoinedthisclassfromthe$250to$500millionclass.Onebankdeclinedinassetstorejointhegroupfromtheover$1billionclass.Astheresultofanacquisition,onebankgrewabove$1billioninassets.Twobanksfromthisclasswereacquiredbylargerbanks.Therewasacarry‐overof13banksfromthepreviousyear.

BANKS BETWEEN $250 AND $500 MILLION (continued)

Carpenter & Company --

Industry Valuations

CaliforniaFirstNationalBancorp,CommonwealthBusinessBank,1stCenturyBancshares,PlumasBancorp,andSecurity California Bancorp exceeded $500million in assets by September 30, 2013 to join this asset class.Paci icMercantileBancorpdeclinedbelow$1billioninassetstorejointhisclass.CentralValleyCommunityBank,byvirtueofitsacquisitionofthe$200millionVisaliaCommunityBank,grewabove$1billionduring2013.BancofCaliforniacompleteditsacquisitionofThePrivateBankofCaliforniaonJuly1,2013.Thisstock/cashtransactionwasvaluedat$52.0millionor1.28xtangiblebookvalue.ThePrivateBankofCaliforniaacquisitionwasintwophases.First,BeachBusinessBankwasmergedintoThePrivateBankofCalifornia,andlaterThePrivateBankofCaliforniawasmergedintoBancofCalifornia.WilshireStateBankacquiredtheKorean‐American‐focusedSaehanBankinacash/stocktransactionvaluedat$105.0million.TheWilshire‐Saehandealwasvaluedat1.81xoftangiblebookvalueandclosedonNovember20,2013.Ofthe19banksinthe$500millionto$1billionassetclass,18experiencedstockpricegains,whileonebanksustained aminimal price decline over the year. Sixteen of the 18 stock price gainswere considered to besigni icant increases, that is in excess of 10%. The steepest stock price gain was the 139% advance forCommonwealth Business Bank. The price of Paci ic City Financial Corp. stock increased 122%. Double‐digitpercentage increases in stock prices occurred for American River Bancshares, Bank of Commerce Holdings,California Republic Bank, Community West Bancshares, 1st Century Bancshares, 1st Enterprise Bank, FNBBancorp, First Northern Community Bancorp, North Valley Bancorp, Oak Valley Bancorp, Plumas Bancorp,SecurityCaliforniaBancorp,SunwestBank,andUnitedSecurityBancshares.Thenumberofbankstradingabovetangiblebookvalueincreasedto13bytheendof2013.Ayearearlier,thenumberofbankswithinthisclasswithaprice/tangiblebookvalueratioover1.0xwas ive.Inadditiontothe13bankstradingabovetangiblebookvalue,therewerefourbankswithinstrikingdistanceof1.0x,withratiosrangingbetween0.96xand0.99x.ThehighestP/TBVwas carriedbyCaliforniaRepublicBankat2.13x.ThiswasthesecondconsecutiveyearthatCaliforniaRepublicBankhadthehighestP/TBVforthisassetclass.ThelowestP/TBVwasforthethinly‐tradedSunwestBankat0.78x.TheaverageP/TBVratioforthisassetcategoryequaled1.19xattheendof2013.Thatratiowasupfromthe0.97x average P/TBV at the endof 2012. Since the 2009 low in the ratio, theP/TBVaverage for this grouprecovered92%.Nonetheless,P/TBVforthisgroupwas57%belowthe2004peakratioof2.77x.OnlyonebankinthisgrouprecordedalossforthelasttwelvemonthsendingSeptember30,2013.Therefore,out of the 19 banks, there was only one not meaningful P/E ratio at the end of 2013. The average price/earnings ratio for this class equaled 14.74x, comparedwith the 14.19x P/E at the end of 2012. The lowestreportedP/Ewas5.31xforPaci icCityFinancialCorp.ThehighestP/Ewas40.23xforNorthValleyBancorp.

LargestPriceGainsCommonwealthBusinessBank +139.1%CommunityWestBancshares +95.8%PlumasBancorp +90.8%

BANKS BETWEEN $500 MILLION AND $1 BILLION (continued)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

02 03 04 05 06 07 08 09 10 11 12 13

1.8

2.7 2.82.6 2.6

1.7

0.80.6

0.8 0.81.0

1.2

PricetoBook‐‐CABanks$500Mln‐$1Bln

Carpenter & Company --

Industry Valuations

Thetotalnumberofsharestradedin2013forthe$500millionto$1billionassetgroupequaled33.3millionforanaveragevolumeperbankof1.75millionshares.Thisaveragetradingactivityrepresenteda35%increaseoverthevolumein2012.SunwestBank,withits$33,000averagesharepriceanditsclosely‐heldownership,reportedthefewestnumberofsharestradedat198sharesfortheentireyear.Incontrast,thelargestnumberofsharestradedoccurredforPaci icMercantileBancorpat9.0millionshares.Withinthisassetclass,eightofthe19bankshadtradingvolumesinexcessof1millionsharesin2013.Themarketcapitalizationof thisclass in2013 totaled$1.6billion,up from$988million in2012.Partof the63% increase in total market capitalization was the addition over the year of three banks to this group.Nonetheless, theper‐bankmarket capitalization increased37% to$84.6million from$61.7million in 2012.Thelowestmarketcapitalizationwas$29.7millionforPlumasBancorp.ThelargestmarketcapitalizationwasheldbyCaliforniaFirstNationalBancorpat$157.8million,whichwasmorethan4timesgreaterthanPlumasBancorp.OnlyOakValleyBancorpsustainedaYoYreductioninmarketcapitalization.

INDUSTRY VALUATIONS: BANKS BETWEEN $1 AND $5 BILLION Thenumberofbanksinthe$1‐$5billionassetclassdecreasedbytwoin2013to18.Thetwo‐bankreductionmatchedthereductioninthesizeofthisclassthathadoccurredin2012.Therewasconsiderablemovementinthisassetclass.CentralValleyCommunityBank,throughitsacquisitionofVisaliaCommunityBank,grewabove$1billion inassets.Farmers&MerchantsBankgrewabove$5billionto jointhenext largerassetclass.FirstCaliforniaFinancialGroupwasacquiredbyPacWestBancorp.Paci icMercantileBankdroppedbelow$1billioninassetstorejointhesmallerassetclass.Seventeenbankscarriedoverinthisclassfromtheprioryear.All18banksinthisclassreportedannualgainsinstockprices.Allbutonebankreporteddouble‐digitratesofincreaseinstockprices.TheFarmers&MerchantBancorpofLongBeachstockpriceincreaseof3.0%wasthesmallestgainofthegroup.WilshireBancorp,Inc.experiencedthesteepestincreaseof86%.Otherstockpricegainsinexcessof50%wererecordedbyHanmiFinancialCorp.,Paci icPremierBancorp,andTricoBancshares.Only three banks in this groupwere valued below 1.0x price/tangible book value, notablyMechanics Bank,ExchangeBank,andRiverCityBank.MechanicsBankwithits0.85xP/TBVcarriedthelowestratioofthegroup.WestamericaBancorpat3.75xP/TBVhadthehighestvaluationofthegroupandhadthesecondhighestratioofallthepublicly‐tradedcompaniesanalyzed.BridgeCapitalHoldingsandWilshireBancorp,Inc.tradedabove2.0xP/TBV.

LargestPriceGainsWilshireBancorp +86.2%TricoBancshares +69.4%HanmiFinancialCorp +61.1%

BANKS BETWEEN $500 MILLION AND $1 BILLION (continued)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

02 03 04 05 06 07 08 09 10 11 12 13

2.0

2.5

3.0

2.42.5

1.6

1.0 1.01.3

1.11.2

1.6

PricetoBook‐‐ CABanks$1‐$5Billion

Carpenter & Company --

Industry Valuations

Theaverageratioofpricetotangiblebookvaluefortheentireclassequaled1.64xin2013,upfrom1.23xin2012.Theaveragepricetotangiblebookvalueforthisclassrankedfourthhighestoftheeightassetclassesanalyzed.FromitslowinP/TBVin2009,theratioexpanded62%throughyear‐end2013.Allbanks inthisgroupreportedpro its forthetwelve‐monthsendingSeptember2013.Allof theP/Eratioswere meaningful statistics. The range in the price/earnings ratios for this class varied between 8.69x forExchangeBank to 25.80x for Paci ic Premier Bancorp. The average ratiowas 16.89x, a steep rise from the12.21xratioin2012.Thetotalvolumeofsharestradedforthisassetclassequaled254.6millionshares,representinganaverageper‐company trading volume of 14.1 million shares. The 14.1 million shares per‐company trading volumematched the comparable statistic for 2012. Three stocks in the class, speci ically Farmers & MerchantsBancorpofLongBeach,MechanicsBank,andRiverCityBank,werepricedatorabove$100pershare.Forthatreason,therewasconsiderablevariationintradingvolumesbetweenthecompaniesinthisgroup.MechanicsBank,whichclosed2013atapriceof$13,000pershare,hadthelowestannualtradingvolumeat269shares.Incontrast,WilshireBancorp,Inc.recorded93.5millionsharestradedduring2013.This classofbankswasactive in theacquisitionof inancial institutions.Sevenof the18banks in thisclassannounced and/or completed bank acquisitions, including the late January 2014 announcement by TricoBancsharesofitsintentiontoacquireNorthValleyBancorp.BankofMarinBancorpacquiredthe$243millionBankofAlamedaonNovember29,2013.CentralValleyCommunityBancorpacquiredthe$200millionVisaliaCommunityBankon July 1, 2013.Hanmi Financial Corp. announcedonDecember16, 2013 its intention toacquire the $1.6 billion Central Bank of Garland, Texas. Heritage Oaks Bancorp entered into a mergeragreement on October 21, 2013 with the $447million Mission Community Bank. Paci ic Premier Bancorpcompletedtwoacquisitionsin2013,speci icallytheacquisitionsofthe$375millionFirstAssociatesBankofDallas,Texas,andthe$242millionSanDiegoTrustBank.WilshireBancorp,Inc.closedonitsacquisitionofthe$542millionSaehanBancorponNovember20,2013.The market capitalization for the entire class equaled $6.5 billion, a 22% increase over 2012’s marketcapitalizationof$5.4billion.Withtwofewerbanksthanin2012,theper‐bankmarketcapitalizationexpanded36%to$362.9million,up from2012’saverageof$267.7million.Allof thebanks in thiscategory reportedincreasesinmarketcapitalizationlastyear.Marketcapitalizationforthisgrouprangedfromalowof$118.3millionforExchangeBankto$1.5billionforWestamericaBancorp.The following banks reported stock conversion and/or capital acquisition in lows in excess of $1 millionduringtheyearendingSeptember30,2013:AmericanBusinessBank,BridgeCapitalHoldings,BankofMarinBancorp, CU Bancorp, and Preferred Bank. In addition, Central Valley Community Bancorp realized a $24millionincreasetocapitalasaresultofitsacquisitionofVisaliaCommunityBank.

INDUSTRY VALUATIONS: BANKS BETWEEN $5 AND $10 BILLION At the end of 2013, the number of banks with assets, as of September 2013, between $5 and $10 billionequaled ive,atwo‐bankincreaseoveryear‐end2012.Farmers&MerchantsBankgrewintothisclassfromtheunder $5 billion group. The tracking report initiated coverage in 2013 of Capital Source, Inc. BBCN, CVBFinancialCorp.,andPacWestBancorpwerecarry‐oversfromthepreviousyear.On July 22, 2013, PacWestBancorp announced its intention to acquire $8.9 billion Capital Source, Inc. in amixed transaction valued at $2.4 billion or 1.71x tangible book value. Additionally, PacWest closed on itsacquisitionofFirstCaliforniaFinancialGrouponMay31,2013.

BANKS BETWEEN $1 AND $5 BILLION (continued)

Carpenter & Company --

Industry Valuations

LargestPriceGainsCapitalSource,Inc. +89.6%PacWestBancorp +70.4%CVBFinancialCorp +64.1%

Forthesecondconsecutiveyear,allofthebanksinthe$5to$10billionrangeexperiencedannualstockpricegains. In 2013, all ive banks reported stock price gains in excess of 20%. The steepest gain occurred formerger‐targetCapitalSource, Inc.,up90%.Thesecondlargestprice increasewasfortheacquirerofCapitalSource,notablyPacWestBancorp,whichregistereda70%stockpricegain.Fourof the ivebanks inthisclasstradedabovetangiblebookvalue.TheexceptionwasFarmersMerchantsBank at 0.91x tangible book value. The highest price/tangible book value ratio was carried by PacWestBancorpat3.35x.Thegroup’saveragepricetotangiblebookvalueequaled2.14x,thesecondhighestpricetotangiblebookvalueoftheeightclassesanalyzed,andwas94%abovetherecession’slowratioin2009.The ive banks all reported pro its for the twelve months ending September 2013, and each bank hadmeaningfulprice/earningsratios.TheP/Eratiosrangedfrom11.3xforFarmers&MerchantsBankto27.2xforPacWestBancorp.Theaverageprice/earningsratioforthisgroupequaled18.47x,thesecondhighestP/Eoftheeightclassesandwasupfromthe15.72xratioattheendof2012.Thecombinedannual tradingvolumefor the ivebanksequaled778.6millionshares in2013,producinganaveragesharevolumeperbankof155.7millionshares.Farmers&MerchantsBank,withits$5,226pricepershare, reported the fewest shares traded in 2013 at 4,417. In contrast, Capital Source, Inc. experienced anannualtradingvolumeof468.4millionshares.The totalmarket capitalization forbanksbetween$5 and410billion equaled$8.6billion, producing aper‐bank market capitalization of $1.7 billion, compared with $973 million in 2012,. The per‐bank marketcapitalizationincreased76%lastyear.Allofthebanksreportedastep‐upinmarketcapitalization.Thelowestmarketcapitalizationwas$684millionforFarmers&MerchantsBank,whileCapitalSourcehadthehighestmarket capitalization at $2.8 billion. Capital Source, BBCN Bancorp, and PacWest Bancorp experiencedadditionstocapitalthatexceeded$1millionduringtheyearendingSeptember30,2013.

INDUSTRY VALUATIONS: BANKS BETWEEN $10 AND $100 BILLION ThenumberandcompositionoftheCaliforniapublicly‐tradedbankswithassetsbetween$10and$100billionheldsteady,asofyear‐end2013.All ivebanksreportedsigni icantgainsinstockpricesduring2013,withtheprice advances ranging from 37% to 87%. The steepest increase occurred for SVB Financial Group, whileCathay General Bancorp had the lowest percentage gain in stock prices. The rise in stock prices for CityNationalCorp,EastWestBancorp,andFirstRepublicBankwereallaroundthenarrowrangeof60%to63%.

BANKS BETWEEN $5 AND $10 BILLION (continued)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

02 03 04 05 06 07 08 09 10 11 12 13

1.5

2.1

3.3

2.6

2.1 2.11.9

1.1

1.71.5

1.6

2.1

PricetoBook‐‐ CABanks$5‐$10Billion

Carpenter & Company --

Industry Valuations

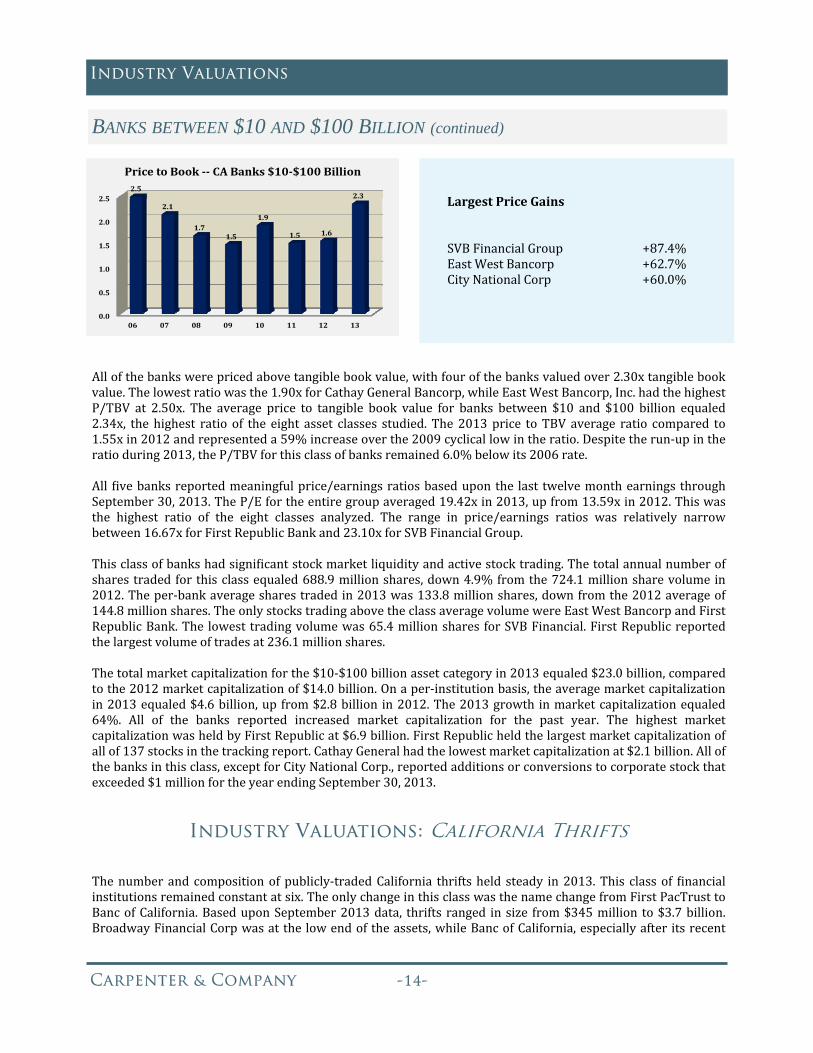

LargestPriceGainsSVBFinancialGroup +87.4%EastWestBancorp +62.7%CityNationalCorp +60.0%

BANKS BETWEEN $10 AND $100 BILLION (continued)

0.0

0.5

1.0

1.5

2.0

2.5

06 07 08 09 10 11 12 13

2.5

2.1

1.71.5

1.9

1.5 1.6

2.3

PricetoBook‐‐ CABanks$10‐$100Billion

Allofthebankswerepricedabovetangiblebookvalue,withfourofthebanksvaluedover2.30xtangiblebookvalue.Thelowestratiowasthe1.90xforCathayGeneralBancorp,whileEastWestBancorp,Inc.hadthehighestP/TBV at 2.50x. The average price to tangible book value for banks between $10 and $100 billion equaled2.34x, thehighest ratio of the eight asset classes studied. The2013price toTBV average ratio compared to1.55xin2012andrepresenteda59%increaseoverthe2009cyclicallowintheratio.Despitetherun‐upintheratioduring2013,theP/TBVforthisclassofbanksremained6.0%belowits2006rate.All ivebanksreportedmeaningfulprice/earningsratiosbaseduponthe last twelvemonthearningsthroughSeptember30,2013.TheP/Efortheentiregroupaveraged19.42xin2013,upfrom13.59xin2012.Thiswasthe highest ratio of the eight classes analyzed. The range in price/earnings ratios was relatively narrowbetween16.67xforFirstRepublicBankand23.10xforSVBFinancialGroup.Thisclassofbankshadsigni icantstockmarketliquidityandactivestocktrading.Thetotalannualnumberofsharestradedforthisclassequaled688.9millionshares,down4.9%fromthe724.1millionsharevolumein2012.Theper‐bankaveragesharestradedin2013was133.8millionshares,downfromthe2012averageof144.8millionshares.TheonlystockstradingabovetheclassaveragevolumewereEastWestBancorpandFirstRepublicBank.The lowesttradingvolumewas65.4millionshares forSVBFinancial.FirstRepublicreportedthelargestvolumeoftradesat236.1millionshares.Thetotalmarketcapitalizationforthe$10‐$100billionassetcategoryin2013equaled$23.0billion,comparedtothe2012marketcapitalizationof$14.0billion.Onaper‐institutionbasis,theaveragemarketcapitalizationin2013equaled$4.6billion,upfrom$2.8billion in2012.The2013growth inmarketcapitalizationequaled64%. All of the banks reported increased market capitalization for the past year. The highest marketcapitalizationwasheldbyFirstRepublicat$6.9billion.FirstRepublicheldthelargestmarketcapitalizationofallof137stocksinthetrackingreport.CathayGeneralhadthelowestmarketcapitalizationat$2.1billion.Allofthebanksinthisclass,exceptforCityNationalCorp.,reportedadditionsorconversionstocorporatestockthatexceeded$1millionfortheyearendingSeptember30,2013.

Industry Valuations: California Thrifts

Thenumberandcompositionofpublicly‐tradedCalifornia thriftsheld steady in2013.This classof inancialinstitutionsremainedconstantatsix.TheonlychangeinthisclasswasthenamechangefromFirstPacTrusttoBancofCalifornia.BaseduponSeptember2013data, thrifts ranged insize from$345million to$3.7billion.BroadwayFinancialCorpwasatthelowendoftheassets,whileBancofCalifornia,especiallyafter itsrecent

Carpenter & Company --

Industry Valuations

0.0

0.5

1.0

1.5

2.0

2.5

02 03 04 05 06 07 08 09 10 11 12 13

1.4

2.11.9

1.61.4

0.8

0.4 0.4

0.8 0.8

1.1

1.8

PricetoBook‐‐ CAThrifts LargestPriceGainsBOFIHoldingsInc. +182.0%BroadwayFinancial +40.8%

acquisitions of three commercial banks, ranked as the largest publicly‐traded thrift in California with $3.7billioninSeptember2013assets.BOFIHoldingsalsoexceeded$3.0billioninassets.Five of the six thrifts experienced YoY stock price gains in 2013. Only Provident Financial Holdings, Inc.reportedadeclineinstockpricefortheyear.Thelargestannualadvanceinstockpriceswasthe182%increaseinthestockpriceofBOFIHoldings,Inc.Othernotableincreaseswerethegainsof41%forBroadwayFinancialCorp.andthe14%riseinthestockpriceofMalagaFinancialCorp.BOFIHoldings,Inc.reportedthehighestpricetotangiblebookratioofallofthestocksanalyzedinthisreport.TheP/TBV forBOFIHoldings, Inc. climbedto3.90x in2013 from1.70x in2012.Also tradingabove tangiblebook value were Banc of California at 1.29x and Malaga Financial Corp at 1.19x. The ratios for BroadwayFinancial Corp. and Provident Financial Holdings were deemed to be not meaningful. The average price totangiblebookvalueratiofortheentireclassequaled1.83x,asteepincreasefromthe2008lowandbroughtthethriftP/TBVtoitshighestratiosince2004.Fiveofthesixthriftsreportedpro itsforthelasttwelvemonthsendingSeptember2013.TheP/EratioforBancofCaliforniaexceeded50x,causingtheratiobeconsiderednotmeaningful.BroadwayFinancialCorp.sustainedalossinLTMearnings.TheresultantfourmeaningfulP/Eratiosproduceda16.45xaverage,upfrom12.75xin2012.TheP/Eratiosrangedfrom8.72xforProvidentFinancialCorp.to25.55xforBOFIHoldings.AsaresultofthewidedifferentialintheassetsizeoftheCaliforniathrifts,therewasasigni icantvariationinthemarketcapitalizationwithinthegroup.BroadwayFinancialCorp.carriedamarketcapitalizationof$18.1million.BOFIHoldingsreportedthelargestmarketcapitalizationofanythriftat$1.1billion,whichwasa200%increaseoverits2012marketcapitalization.TotalmarketcapitalizationofCaliforniathriftsclimbedfrom$931millionin2012to$1.8billionattheendof2013.This89%increaseintotalmarketcapitalizationwasprimarilyduetothesteepincreasesinmarketcapitalizationatBOFIandBancofCalifornia.ProvidentFinancialHoldingsandSimplicityreportedreductionsinthelevelsoftheirmarketcapitalizationoverthepastyear.The total tradingvolume in2013 for thriftsequaled87.8millionshares foraper‐institutionaverageof14.6millionsharestraded.The2013tradingvolumewasup132%over2012.Thehighestannualtradingvolumewas for BOFI Holdings at 42.9 million shares, an 186% pick‐up from 2012. The lowest volumes were the276,342sharestradedforMalagaFinancial.

CALIFORNIA THRIFTS (continued)

Carpenter & Company --

Industry Valuations

InstitutionName CityInactiveDate

TotalAssets($000)

Traded* Outcome

FirstCaliforniaBank WestlakeVillage 1‐Jun‐13 1,741,192 yesAcquiredbyPacWestBancorpat1.709xTBV

ThePrivateBankofCalifornia LosAngeles 11‐Oct‐13 1,065,164 no MergedintoBancofCalifornia

ThePrivateBankofCalifornia LosAngeles 1‐Jul‐13 656,622 yes

AcquiredbyFirstPacTrustBancorpat1.279xTBVandmergedwithBeachBusinessBank

SaehanBank LosAngeles 21‐Nov‐13 591,998 yesAcquiredbyWilshireBancorpat1.805xTBV

RegentsBank,N.A. LaJolla 20‐Sep‐13 587,550 no MergedintoGrandpointCapital,Inc.

CentennialBank FountainValley 1‐May‐13 529,292 no

AcquiredoutofbankruptcybyWesternAllianceBancorpat0.66xTBV

BankofAlameda Alameda 30‐Nov‐13 271,640 yesAcquiredbyBankofMarinBancorpat1.233xTBV

CommerceNationalBank NewportBeach 1‐Oct‐13 244,834 yesAcquiredbySterlingFinancialCorp.at1.425xTBV

SanDiegoTrustBank SanDiego 26‐Jun‐13 210,898 yesAcquiredbyPacificPremierBancorpat1.210xTBV

VisaliaCommunityBank Visalia 1‐Jul‐13 197,465 yesAcquiredbyCentralValleyCommunityBancorpat1.236xTBV

LosAngelesNationalBank BuenaPark 17‐May‐13 192,793 no AcquiredbyRBBBancorp

GilmoreBank LosAngeles 26‐Sep‐13 171,102 no AcquiredbyGrandpointCapital,Inc.

BorregoSpringsBank,N.A. LaMesa 1‐Mar‐13 141,708 noAcquiredbySterlingFinancialCorp.at0.507xTBV

SanDiegoPrivateBank LaJolla 3‐Apr‐13 132,262 no MergedwithCoronadoFirstBank

MojaveDesertBank,N.A. Mojave 25‐Jan‐13 103,504 yesAcquiredbyMissionBancorpat0.824xTBV

EvergreenInternationalBank LongBeach 2‐Jan‐13 22,473 no Voluntarilyliquidatedcharter

*Traded:yesmeanspubliclytradedandnomeansprivatelyheld TBV=Tangiblebookvalue

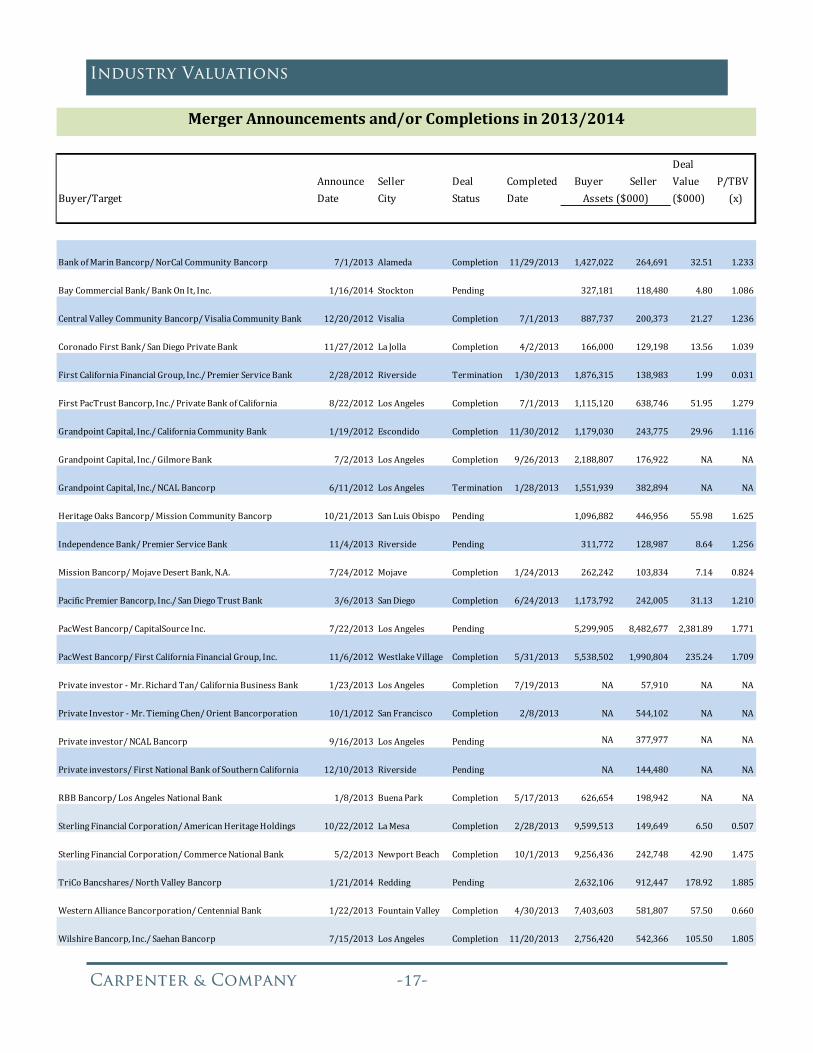

CALIFORNIAFINANCIALINSTITUTIONSCLOSEDIN2013(Sortedbyassetsizeofseller)

Carpenter & Company --

Industry Valuations

Deal

Announce Seller Deal Completed Buyer Seller Value P/TBV

Buyer/Target Date City Status Date ($000) (x)

BankofMarinBancorp/NorCalCommunityBancorp 7/1/2013 Alameda Completion 11/29/2013 1,427,022 264,691 32.51 1.233

BayCommercialBank/BankOnIt,Inc. 1/16/2014 Stockton Pending 327,181 118,480 4.80 1.086

CentralValleyCommunityBancorp/VisaliaCommunityBank 12/20/2012 Visalia Completion 7/1/2013 887,737 200,373 21.27 1.236

CoronadoFirstBank/SanDiegoPrivateBank 11/27/2012 LaJolla Completion 4/2/2013 166,000 129,198 13.56 1.039

FirstCaliforniaFinancialGroup,Inc./PremierServiceBank 2/28/2012 Riverside Termination 1/30/2013 1,876,315 138,983 1.99 0.031

FirstPacTrustBancorp,Inc./PrivateBankofCalifornia 8/22/2012 LosAngeles Completion 7/1/2013 1,115,120 638,746 51.95 1.279

GrandpointCapital,Inc./CaliforniaCommunityBank 1/19/2012 Escondido Completion 11/30/2012 1,179,030 243,775 29.96 1.116

GrandpointCapital,Inc./GilmoreBank 7/2/2013 LosAngeles Completion 9/26/2013 2,188,807 176,922 NA NA

GrandpointCapital,Inc./NCALBancorp 6/11/2012 LosAngeles Termination 1/28/2013 1,551,939 382,894 NA NA

HeritageOaksBancorp/MissionCommunityBancorp 10/21/2013 SanLuisObispo Pending 1,096,882 446,956 55.98 1.625

IndependenceBank/PremierServiceBank 11/4/2013 Riverside Pending 311,772 128,987 8.64 1.256

MissionBancorp/MojaveDesertBank,N.A. 7/24/2012 Mojave Completion 1/24/2013 262,242 103,834 7.14 0.824

PacificPremierBancorp,Inc./SanDiegoTrustBank 3/6/2013 SanDiego Completion 6/24/2013 1,173,792 242,005 31.13 1.210

PacWestBancorp/CapitalSourceInc. 7/22/2013 LosAngeles Pending 5,299,905 8,482,677 2,381.89 1.771

PacWestBancorp/FirstCaliforniaFinancialGroup,Inc. 11/6/2012 WestlakeVillage Completion 5/31/2013 5,538,502 1,990,804 235.24 1.709

Privateinvestor‐Mr.RichardTan/CaliforniaBusinessBank 1/23/2013 LosAngeles Completion 7/19/2013 NA 57,910 NA NA

PrivateInvestor‐Mr.TiemingChen/OrientBancorporation 10/1/2012 SanFrancisco Completion 2/8/2013 NA 544,102 NA NA

Privateinvestor/NCALBancorp 9/16/2013 LosAngeles Pending NA 377,977 NA NA

Privateinvestors/FirstNationalBankofSouthernCalifornia 12/10/2013 Riverside Pending NA 144,480 NA NA

RBBBancorp/LosAngelesNationalBank 1/8/2013 BuenaPark Completion 5/17/2013 626,654 198,942 NA NA

SterlingFinancialCorporation/AmericanHeritageHoldings 10/22/2012 LaMesa Completion 2/28/2013 9,599,513 149,649 6.50 0.507

SterlingFinancialCorporation/CommerceNationalBank 5/2/2013 NewportBeach Completion 10/1/2013 9,256,436 242,748 42.90 1.475

TriCoBancshares/NorthValleyBancorp 1/21/2014 Redding Pending 2,632,106 912,447 178.92 1.885

WesternAllianceBancorporation/CentennialBank 1/22/2013 FountainValley Completion 4/30/2013 7,403,603 581,807 57.50 0.660

WilshireBancorp,Inc./SaehanBancorp 7/15/2013 LosAngeles Completion 11/20/2013 2,756,420 542,366 105.50 1.805

Assets($000)

MergerAnnouncementsand/orCompletionsin2013/2014

Carpenter & Company --

STOCK PERFORMANCE: 2013 Annual Report

Carpenter and Company—Stock Performance Report Average LTM P/E Ratios by Asset Group

Information is gathered from sources believed to be reliable, however, the accuracy of the data cannot be guaranteed.

12/31/2013 revious Mon 12/31/2012 Change Mon % Change YTDTotal Assets:

Under $125M 16.56 16.83 16.27 -1.62% 1.74%$125M - $250M 16.14 15.59 17.19 3.55% -6.14%$250M - $500M 17.88 17.67 15.31 1.18% 16.75%$500M - $1Bn 14.74 14.63 14.19 0.71% 3.87%$1Bn - $5Bn 16.89 16.76 12.21 0.80% 38.35%$5Bn - $10Bn 18.47 18.06 15.72 2.28% 17.48%Over $10Bn 19.42 19.11 13.59 1.67% 42.96%CA Thrifts 16.45 16.51 12.75 -0.31% 29.06%

*LTM= Last Twelve Months. LTM P/E calculated based on last twelve months earnings through 9/30/2013.

Average LTM* P/E Ratio

02468

101214161820

Under$125M

$125M -$250M

$250M -$500M

$500M -$1Bn

$1Bn -$5Bn

$5Bn -$10Bn

Over$10Bn

CAThrifts

12/31/2012 12/31/2013

Carpenter & Company --

STOCK PERFORMANCE

Information is gathered from sources believed to be reliable, however, the accuracy of the data cannot be guaranteed.

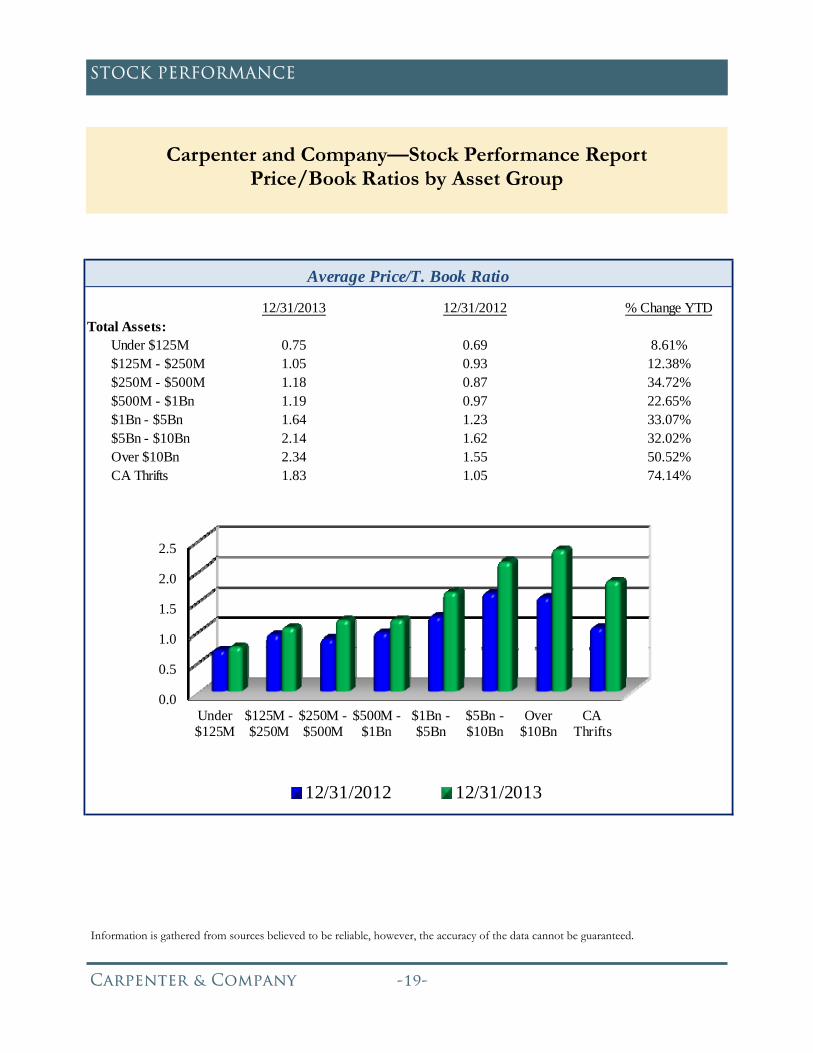

Carpenter and Company—Stock Performance Report Price/Book Ratios by Asset Group

12/31/2013 Previous Month 12/31/2012 Change Month % Change YTDTotal Assets:

Under $125M 0.75 0.75 0.69 -1.15% 8.61%$125M - $250M 1.05 1.05 0.93 -0.26% 12.38%$250M - $500M 1.18 1.16 0.87 1.32% 34.72%$500M - $1Bn 1.19 1.16 0.97 2.72% 22.65%$1Bn - $5Bn 1.64 1.59 1.23 3.25% 33.07%$5Bn - $10Bn 2.14 2.09 1.62 2.42% 32.02%Over $10Bn 2.34 2.29 1.55 1.88% 50.52%CA Thrifts 1.83 1.85 1.05 -1.26% 74.14%

Average Price/T. Book Ratio

0.0

0.5

1.0

1.5

2.0

2.5

Under$125M

$125M -$250M

$250M -$500M

$500M -$1Bn

$1Bn -$5Bn

$5Bn -$10Bn

Over$10Bn

CAThrifts

12/31/2012 12/31/2013

Carpenter & Company --

STOCK PERFORMANCE

Information is gathered from sources believed to be reliable, however, the accuracy of the data cannot be guaranteed.

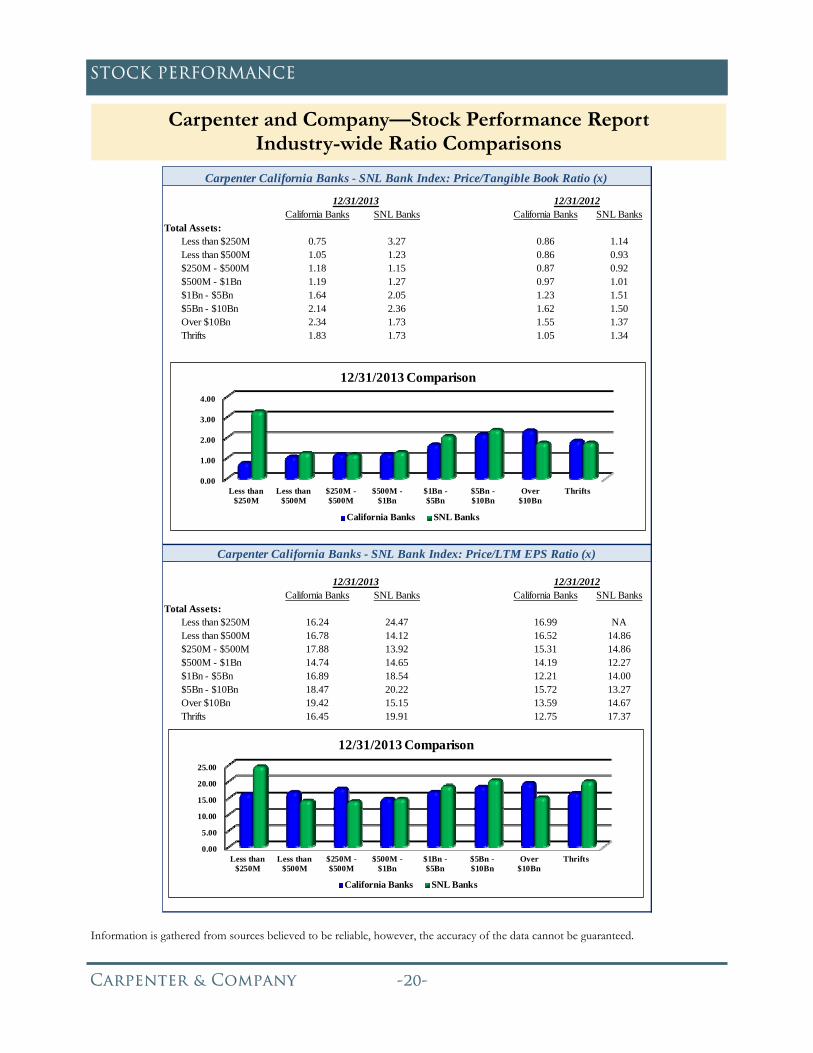

Carpenter and Company—Stock Performance Report Industry-wide Ratio Comparisons

California Banks SNL Banks ifornia BaNL Bank California Banks SNL BanksTotal Assets:

Less than $250M 0.75 3.27 0.75 3.26 0.86 1.14Less than $500M 1.05 1.23 1.05 1.20 0.86 0.93$250M - $500M 1.18 1.15 1.16 1.13 0.87 0.92$500M - $1Bn 1.19 1.27 1.16 1.27 0.97 1.01$1Bn - $5Bn 1.64 2.05 1.59 2.03 1.23 1.51$5Bn - $10Bn 2.14 2.36 2.09 2.34 1.62 1.50Over $10Bn 2.34 1.73 2.29 1.69 1.55 1.37Thrifts 1.83 1.73 1.85 1.70 1.05 1.34

California Banks SNL Banks ifornia BaNL Bank California Banks SNL BanksTotal Assets:

Less than $250M 16.24 24.47 15.90 25.35 16.99 NALess than $500M 16.78 14.12 16.51 14.01 16.52 14.86$250M - $500M 17.88 13.92 17.67 13.79 15.31 14.86$500M - $1Bn 14.74 14.65 14.63 14.60 14.19 12.27$1Bn - $5Bn 16.89 18.54 16.76 18.39 12.21 14.00$5Bn - $10Bn 18.47 20.22 18.06 20.06 15.72 13.27Over $10Bn 19.42 15.15 19.11 14.99 13.59 14.67Thrifts 16.45 19.91 16.51 19.66 12.75 17.37

Previous Month 12/31/201212/31/2013

Carpenter California Banks - SNL Bank Index: Price/Tangible Book Ratio (x)

12/31/2013 Previous Month 12/31/2012

Carpenter California Banks - SNL Bank Index: Price/LTM EPS Ratio (x)

0.00

1.00

2.00

3.00

4.00

Less than$250M

Less than$500M

$250M -$500M

$500M -$1Bn

$1Bn -$5Bn

$5Bn -$10Bn

Over$10Bn

Thrifts

12/31/2013 Comparison

California Banks SNL Banks

0.00

5.00

10.00

15.00

20.00

25.00

Less than$250M

Less than$500M

$250M -$500M

$500M -$1Bn

$1Bn -$5Bn

$5Bn -$10Bn

Over$10Bn

Thrifts

12/31/2013 Comparison

California Banks SNL Banks

Carpenter & Company --

STOCK PERFORMANCE

Information is gathered from sources believed to be reliable, however, the accuracy of the data cannot be guaranteed.

Carpenter and Company— 2013 Annual Stock Performance Report California Banks with Total Assets Under $125 Million

Total Market Capitalization: $151 Million

Symbol Name Annual Mkt Cap LTM Price/

Date Price ($) Volume ($) P/E T. Book Low ($)High ($) (%) ($) (%)

AUNB AMERICAS UNITED BANK 31-Dec 5.75 1,034,907 16,549,363 11.06 0.91 5.30 6.35 119.8% 0.45 8.5%BKOT BANK ON IT, INC 16-Dec 2.03 71,841 3,163,365 N/M 0.73 1.76 2.25 127.8% 0.29 16.7%CABB CALIFORNIA BUSINESS BANK 19-Dec 0.22 522,886 784,426 N/M 0.10 0.11 0.52 472.7% -0.13 -37.1%

CCBC CHINO COMMERCIAL BANCORP 31-Dec 15.90 103,230 13,249,152 17.47 1.57 9.50 16.50 173.7% 5.40 51.4%CKTM COMMERCE BK TEMECULA VALLEY 19-Dec 4.25 109,813 6,385,090 N/M 0.73 3.35 4.50 134.3% 0.00 0.0%CMUV COMMUNITY VALLEY BANK 26-Dec 5.15 282,704 8,394,958 9.77 0.91 3.75 5.25 140.0% 0.15 3.0%

CRSB CORNERSTONE COMMUNITY BANK 19-Dec 8.50 22,941 10,200,000 9.55 0.84 8.00 9.25 115.6% 0.50 6.3%CTBP COAST BANCORP 31-Dec 1.92 132,493 1,626,012 N/M N/M 1.10 3.50 318.2% 0.57 42.2%

DEBC DELTA NATIONAL BANCORP 6-May 7.00 324 2,662,121 N/M 0.32 6.00 7.00 116.7% 1.00 16.7%FHLB FRIENDLY HILLS BANK 31-Dec 5.02 99,468 8,112,320 N/M 0.64 4.50 6.25 138.9% 0.52 11.6%GSBB GOLDEN STATE BANK 27-Dec 0.19 59,792 341,251 N/M 0.08 0.13 0.75 576.9% -0.02 -7.5%

MOKB MISSION OAKS BANCORP 31-Dec 0.20 557,643 2,221,288 N/M N/M 0.09 0.70 777.8% 0.11 122.2%MOLB MOTHER LODE BANK 31-Dec 1.25 124,652 5,547,481 9.94 1.09 0.57 1.50 263.2% 0.68 119.3%PAMB PAN AMERICAN BANK 28-Oct 0.15 3,200 2,628,016 N/M N/M 0.15 0.55 366.7% -0.15 -50.0%

PPFC PAN PACIFIC BANK 24-Dec 2.45 241,908 12,065,843 24.75 0.84 1.91 2.95 154.5% 0.54 28.3%SAGN SAIGON NATIONAL BANK 31-Dec 0.16 144,012 11,108,185 N/M N/M 0.12 0.30 250.0% -0.09 -36.0%SBKK SUNCREST BANK 30-Dec 5.90 86,440 11,303,822 13.66 0.82 5.90 8.65 146.6% -0.22 -3.6%

SFRK SECURITY FIRST BANK 27-Dec 4.07 40,818 6,919,000 17.79 0.62 3.36 4.75 141.4% 0.57 16.3%SUTB SUTTER COMMUNITY BANK 31-Dec 5.75 23,771 5,472,149 33.52 0.61 5.75 6.49 112.9% -0.25 -4.2%

SVBA SIERRA VISTA BANK 30-Dec 2.53 64,197 9,919,707 18.07 0.88 1.55 3.75 241.9% 0.98 63.2%TRVB TRI-VALLEY BANK 31-Dec 0.39 361,905 9,680,982 N/M 1.15 0.32 0.65 203.1% -0.02 -4.1%USMT US METRO BANK 30-Dec 1.25 37,988 2,475,000 N/M 0.59 1.06 3.10 292.5% -1.85 -59.7%

Average 16.56 0.75Median 15.57 0.78

High 33.52 1.57

Low 9.55 0.08

Last Trade YTD ChangePricing in 2013

Carpenter & Company --

STOCK PERFORMANCE

Information is gathered from sources believed to be reliable, however, the accuracy of the data cannot be guaranteed.

Carpenter and Company— 2013 Annual Stock Performance Report California Banks with Total Assets Between $125 and $250 Million

Total Market Capitalization: $683 Million

Symbol Name Annual Mkt Cap LTM Price/

Date Price ($) Volume ($) P/E T. Book Low ($) High ($) ($) (%)

ABNK ALTAPACIFIC BANK 31-Dec 7.40 815,978 39,195,913 N/M 1.17 6.05 9.75 0.00 0.0%

ACAL AMERICAN CALIFORNIA BANK 7-Aug 4.56 114,400 6,553,691 4.35 0.57 3.50 4.56 1.06 30.3%ARBV AMERICAN RIVIERA BANK 31-Dec 10.50 433,697 26,837,055 16.94 1.20 7.50 11.00 3.00 40.0%

BNNP BANK OF NAPA NA 31-Dec 8.70 163,047 19,913,291 10.24 1.05 7.55 9.50 1.30 17.6%

BSCA BANK OF SANTA CLARITA 30-Dec 8.95 300,021 19,918,306 18.65 1.02 7.30 10.00 1.80 25.2%

CALW CALWEST BANCORP 27-Dec 1.70 643,943 4,286,530 N/M N/M 0.22 1.70 1.25 277.8%CBBC COMMUNITY BUSINESS BANK 11-Dec 8.90 170,411 19,165,242 18.19 1.15 6.12 10.00 2.78 45.4%

CBJC CAPITAL BANK 13-Dec 19.50 46,229 30,304,892 16.98 2.05 17.51 22.95 -1.50 -7.1%

CBYAA COMMUNITY BANK OF THE BAY 26-Dec 4.40 902,459 18,107,866 7.86 1.41 3.10 4.90 1.50 51.7%

CFBN COMMUNITY 1ST BANK 24-Dec 4.00 911,327 21,796,968 33.33 1.36 2.62 4.49 1.00 33.3%CNYB COUNTY COMMERCE BANK 20-Dec 16.10 131,679 23,076,919 15.33 1.29 14.05 16.99 0.10 0.6%

CYSM COMMUNITY BANK OF SANTA MARIA 31-Dec 6.90 670,142 16,436,807 21.91 0.97 6.53 7.47 -0.45 -6.1%

FBBN BANK OF SOUTHERN CALIFORNIA NA 18-Dec 7.00 1,439 22,844,738 23.03 1.29 5.65 8.00 1.35 23.9%

FBCP FOUNDERS BANCORP 31-Dec 10.30 101,698 11,656,510 11.97 1.02 10.00 11.99 0.30 3.0%

FMBP FIRST MOUNTAIN BANK 31-Dec 7.30 460,705 11,423,960 N/M N/M 3.75 7.75 1.50 25.9%FOLB FOLSOM LAKE BANK 31-Dec 7.10 66,072 11,311,088 12.68 0.96 6.06 8.50 0.29 4.3%

FSNF FRESNO FIRST BANK 31-Dec 10.00 371,105 19,515,880 N/M 1.42 8.71 10.95 0.31 3.2%

FTFS F&T FINANCIAL SERVICES, INC. 30-Dec 68.50 12,915 20,064,678 12.83 0.69 63.00 72.00 5.50 8.7%

GVYB GOLDEN VALLEY BANCORP 31-Dec 9.40 62,946 18,731,587 14.30 1.20 7.85 9.50 0.91 10.7%LGHT LIGHTHOUSE BANK 31-Dec 10.90 192,894 23,328,616 10.49 1.16 9.62 11.00 -0.10 -0.9%

LIBC LIBERTY BANCORP INC 20-Dec 12.00 6,600 10,639,344 18.75 0.99 10.03 12.00 1.97 19.6%

MNBO MNB HOLDINGS CORP 11-Dec 26.00 7,810 11,902,098 9.54 0.72 18.67 26.00 7.33 39.3%

NCNB NORTHERN CA NATIONAL BANK 18-Nov 8.75 33,406 11,898,828 14.52 0.89 7.60 35.00 0.60 7.4%NRLB NORTHERN CALIFORNIA BANCORP INC 30-Dec 1.20 113,525 2,143,069 N/M 0.24 0.28 1.90 0.80 200.0%

NWBN NEW RESOURCE BANK 31-Dec 3.95 476,885 22,112,961 18.69 0.87 3.65 4.95 -0.05 -1.3%

OCBB ORANGE COUNTY BUSINESS BANK NA 31-Dec 7.25 400,582 34,253,176 36.25 1.03 3.91 7.34 3.34 85.4%

OJCB OCB BANCORP 31-Dec 6.00 186,967 12,484,668 13.78 0.91 5.65 7.00 -1.00 -14.3%PBNK PINNACLE BANK 23-Dec 5.28 93,124 17,376,522 3.05 0.85 4.25 5.40 0.80 17.9%

PFBN PACIFIC ALLIANCE BANK 30-Dec 4.90 44,198 9,102,661 9.42 0.62 3.81 5.25 1.09 28.6%

PFCI PACIFIC COMMERCE BANK 27-Dec 4.25 256,471 18,960,334 3.48 0.95 2.40 5.20 1.85 77.1%

PMRA PROMERICA BANK 26-Dec 5.05 150,935 13,993,550 12.63 0.78 3.90 6.00 1.46 40.7%PSBK PREMIER SERVICE BANK 31-Dec 6.15 212,383 7,756,878 18.64 1.32 0.80 6.25 5.25 583.3%

PVBK PACIFIC VALLEY BANK 30-Dec 10.10 83,028 36,329,205 18.39 1.78 7.27 10.77 0.10 1.0%

RVVY RIVER VALLEY COMMUNITY BANK 31-Dec 17.00 36,536 29,312,981 24.14 1.67 14.50 21.00 2.00 13.3%

SCVE SANTA CLARA VALLEY BANK NA 31-Dec 5.60 105,336 10,741,735 N/M 1.08 5.52 6.00 -0.39 -6.5%

SMAL SUMMIT BANCSHARES INC 30-Dec 11.30 68,011 14,692,011 16.14 0.74 7.50 11.80 3.80 50.7%UIFC UNITI FINANCIAL CORP 10-Oct 1.37 55,131 16,961,637 33.82 0.86 0.55 1.37 0.82 149.1%

VBBK VIBRA BANK 14-Nov 18.00 28,644 13,299,570 N/M 1.10 17.30 21.00 -0.51 -2.8%

VCBC VALLEY COMMUNITY BANK 24-Dec 2.25 521,582 4,227,449 N/M 0.47 0.80 2.50 1.55 221.4%Average 16.14 1.05

Median 15.33 1.02High 36.25 2.05

Low 3.05 0.24

Last Trade YTD ChangePricing in 2013

Carpenter & Company --

STOCK PERFORMANCE

Information is gathered from sources believed to be reliable, however, the accuracy of the data cannot be guaranteed.

Carpenter and Company— 2013 Annual Stock Performance Report California Banks with Total Assets Between $250 and $500 Million

Total Market Capitalization: $898 Million

Symbol Name Annual Mkt Cap LTM Price/

Date Price ($) Volume ($) P/E T. Book Low ($) High ($) ($) (%)

AVBH AVIDBANK HOLDINGS INC 31-Dec 11.70 441,925 50,093,339 15.39 1.06 9.21 12.00 2.45 26.5%BCML BAY COMMERCIAL BANK 31-Dec 9.70 1,324,732 46,855,433 18.65 0.89 7.40 10.25 1.50 18.3%CABC CALIFORNIA BANK OF COMMERCE 31-Dec 10.90 470,813 30,075,749 12.96 1.10 7.90 12.00 3.27 42.9%CWBK COMMERCEWEST BANK 31-Dec 13.90 1,184,479 60,358,790 11.58 1.22 8.50 14.00 4.95 55.3%FCSB FOCUS BUSINESS BANK 23-Dec 8.90 126,890 26,035,953 27.98 0.99 7.24 9.45 1.20 15.6%FISB 1ST CAPITAL BANK 30-Dec 11.33 705,455 38,269,024 20.60 1.06 10.51 13.50 0.58 5.4%GSCB GREATER SACRAMENTO BANCORP 26-Dec 15.20 184,796 39,682,442 12.56 1.16 14.75 16.98 -0.70 -4.4%MISN MISSION COMMUNITY BANCORP 31-Dec 6.56 153,836 57,433,233 26.24 1.60 3.20 6.56 3.16 92.9%MNHN MANHATTAN BANCORP 26-Dec 4.16 151,848 52,135,973 27.76 1.05 3.51 5.20 0.41 11.1%MSBC MISSION BANCORP 31-Dec 24.05 83,951 33,864,613 17.70 1.01 22.25 28.55 -0.70 -2.8%MVLY MISSION VALLEY BANCORP 26-Dec 6.50 326,663 17,103,015 12.04 1.09 4.95 7.15 1.55 31.3%NCAL NCAL BANCORP 23-Dec 0.55 219,878 1,322,885 N/M 0.89 0.53 1.99 -1.40 -71.8%OPBK OPEN BANK 31-Dec 7.50 1,074,647 54,194,445 9.38 1.74 2.10 7.75 5.40 257.1%PDOB PRESIDIO BANK 31-Dec 9.95 472,778 41,491,500 36.85 1.14 7.30 9.95 2.45 32.7%PLZB PLAZA BANK 31-Dec 2.98 209,837 51,049,602 11.04 1.04 2.05 4.00 0.93 45.4%RWCB REDWOOD CAPITAL BANCORP 26-Dec 8.81 104,661 15,945,060 8.72 1.05 7.10 9.25 1.71 24.1%SCCB SEACOAST COMMERCE BANK 31-Dec 8.00 693,838 44,567,456 N/M 2.03 4.30 8.00 3.50 77.8%SCZC SANTA CRUZ COUNTY BANK 31-Dec 17.75 120,125 35,184,973 10.82 1.11 14.00 19.50 3.85 27.7%SDPB SAN DIEGO PRIVATE BANK 27-Dec 11.69 530,018 47,763,107 27.85 1.04 9.03 11.69 2.54 27.8%SSBI SUMMIT STATE BANK 31-Dec 10.50 1,472,972 50,144,535 12.80 1.15 6.81 10.53 3.75 55.6%UABK UNITED AMERICAN BANK 31-Dec 0.22 770,248 9,902,176 N/M N/M 0.18 0.40 -0.03 -12.0%VCBP VALLEY COMMERCE BANCORP 27-Dec 13.51 210,934 37,614,934 9.72 0.95 10.32 14.00 3.16 30.5%VLLX VALLEY REPUBLIC BANK 31-Dec 16.28 25,009 56,745,373 26.89 1.53 15.00 16.50 1.28 8.5%

Average 17.88 1.18Median 14.18 1.07

High 36.85 2.03

Low 8.72 0.89

Last Trade YTD ChangePricing in 2013

Carpenter & Company --

STOCK PERFORMANCE

Information is gathered from sources believed to be reliable, however, the accuracy of the data cannot be guaranteed.

Carpenter and Company— 2013 Annual Stock Performance Report California Banks with Total Assets Between

$500 Million and $1 Billion Total Market Capitalization: $1.6 Billion

Symbol Name Annual Mkt Cap LTM Price/

Date Price ($) Volume ($) P/E T. Book Low ($)High ($) ($) (%)

AMRB AMERICAN RIVER BANKSHARES 31-Dec 9.45 2,854,927 82,734,948 28.64 1.14 6.75 9.52 2.54 36.8%

BOCH BANK OF COMMERCE HLDG 31-Dec 5.71 5,754,167 81,504,266 12.41 1.00 4.59 5.90 1.11 24.1%

CFNB CALIFORNIA FIRST NATIONAL BANCORP 31-Dec 15.10 1,357,432 157,753,128 20.68 0.86 14.73 18.52 0.15 1.0%

CRPB CALIFORNIA REPUBLIC BANK 26-Dec 23.70 462,504 123,240,000 17.00 2.13 15.50 25.00 7.20 43.6%

CWBB COMMONWEALTH BUSINESS BANK 31-Dec 21.40 735,722 72,697,491 7.81 1.23 11.98 21.40 12.45 139.1%

CWBC COMMUNITY WEST BANCSHARES 31-Dec 6.56 1,607,536 51,606,096 7.37 1.05 2.87 6.59 3.21 95.8%

FCTY 1ST CENTURY BANCSHARES 31-Dec 7.15 2,441,156 66,340,581 8.51 1.22 4.65 7.93 2.54 55.1%

FENB 1ST ENTERPRISE BANK 30-Dec 19.30 263,660 73,772,108 16.08 1.42 15.40 19.80 4.00 26.1%

FNBG FNB BANCORP 31-Dec 28.00 410,879 110,660,536 18.49 1.36 17.67 28.00 9.45 50.9%

FNRN FIRST NORTHERN COMMUNITY BANCORP 27-Dec 7.20 529,087 68,243,760 15.14 0.96 5.10 7.40 2.00 38.5%

NOVB NORTH VALLEY BANCORP 31-Dec 18.91 2,891,543 129,280,711 40.23 1.36 14.50 19.90 4.67 32.8%

OVLY OAK VALLEY BANCORP 31-Dec 8.37 835,949 66,371,047 11.79 1.05 7.50 8.75 0.92 12.3%

PFCF PACIFIC CITY FINANCIAL CORP 13-Dec 4.00 526,260 100,476,012 5.31 1.54 1.65 4.75 2.20 122.2%

PLBC PLUMAS BANCORP 31-Dec 6.22 616,813 29,749,881 9.87 0.99 3.27 6.79 2.96 90.8%

PMBC PACIFIC MERCANTILE BANCORP 31-Dec 6.22 8,969,510 118,139,290 N/M 0.99 5.24 6.62 -0.07 -1.1%

PVLY PREMIER VALLEY BANK 31-Dec 5.82 827,256 74,891,760 11.64 1.42 5.65 6.95 0.52 9.8%

SCAF SECURITY CALIFORNIA BANCORP 31-Dec 9.61 482,900 54,483,088 15.48 0.99 8.07 10.70 1.60 20.0%

SWBC SUNWEST BANK 1-Aug 33,000 198 73,095,000 6.43 0.78 26,900 33,500 6,000 22.2%UBFO UNITED SECURITY BANCSHARES 31-Dec 4.92 1,695,315 72,094,413 12.37 1.05 2.41 5.47 2.36 92.2%

Average 14.74 1.19

Median 12.39 1.05

High 40.23 2.13

Low 5.31 0.78

Last Trade YTD ChangePricing in 2013

Carpenter & Company --

STOCK PERFORMANCE

Information is gathered from sources believed to be reliable, however, the accuracy of the data cannot be guaranteed.

Carpenter and Company— 2013 Annual Stock Performance Report California Banks with Total Assets Between $1 and $5 Billion

Total Market Capitalization: $6.5 Billion

Carpenter and Company— 2013 Annual Stock Performance Report California Banks with Total Assets Between $5 and $10 Billion

Total Market Capitalization: $8.6 Billion

Symbol Name Annual Mkt Cap LTM Price/

Date Price ($) Volume ($) P/E T. Book Low ($) High ($) ($) (%)

BBCN BBCN BANCORP 31-Dec 16.59 92,710,568 1,315,049,152 15.22 1.95 11.85 16.85 5.02 43.4%

CSE CAPITAL SOURCE, INC. 31-Dec 14.37 468,405,310 2,829,613,470 19.16 1.99 7.67 14.50 6.79 89.6%CVBF CVB FINANCIAL CORP 31-Dec 17.07 124,497,602 1,796,440,552 19.40 2.53 10.31 17.29 6.67 64.1%

FMBL FARMERS & MERCHANTS BK 31-Dec 5,226 4,417 684,229,728 11.32 0.91 4,310 5,300 916 21.3%PACW PACWEST BANCORP 31-Dec 42.22 92,966,134 1,945,419,577 27.24 3.35 25.79 42.78 17.45 70.4%

Average 18.47 2.14

Median 19.16 1.99

High 27.24 3.35

Low 11.32 0.91

Last Trade YTD ChangePricing in 2013

Symbol Name Annual Mkt Cap LTM Price/

Date Price ($) Volume ($) P/E T. Book Low ($) High ($) ($) (%)

AMBZ AMERICAN BUSINESS BANK 31-Dec 30.28 258,280 148,339,025 11.23 1.55 24.10 31.00 3.73 14.0%

BBNK BRIDGE CAPITAL HOLDINGS 31-Dec 20.54 5,654,764 323,784,200 23.61 2.07 13.65 21.22 4.98 32.0%

BMRC BANK OF MARIN BANCORP 31-Dec 43.39 3,975,873 254,883,187 14.37 1.47 37.40 45.99 5.93 15.8%

BSRR SIERRA BANCORP 31-Dec 16.09 4,888,258 228,424,243 19.86 1.32 11.74 19.38 4.66 40.8%

CUNB CU BANCORP 31-Dec 17.48 6,475,639 193,545,412 21.85 1.60 11.80 19.28 5.77 49.3%

CVCY CENTRAL VALLEY COMMUNITY BAN 31-Dec 11.25 2,058,355 122,790,150 15.63 1.39 7.76 12.69 3.49 45.0%

EXSR EXCHANGE BANK 31-Dec 69.00 49,635 118,289,736 8.69 0.87 53.75 69.94 15.25 28.4%

FMCB FARMERS & MERCHANTS BANCORP ( 31-Dec 417.00 8,837 324,376,794 13.61 1.54 384.00 500.00 12.00 3.0%

HAFC HANMI FINANCIAL CORP 31-Dec 21.89 58,433,548 695,152,302 15.86 1.75 14.10 22.40 8.30 61.1%

HEOP HERITAGE OAKS BANCORP 31-Dec 7.50 8,683,927 190,435,073 17.86 1.75 5.35 7.99 1.70 29.3%

HTBK HERITAGE COMMERCE CORP 31-Dec 8.24 7,169,369 217,085,511 24.24 1.45 6.36 8.33 1.26 18.1%

MCHB MECHANICS BANK 31-Dec 13,000 269 251,940,000 9.95 0.85 10,825 14,999 2,200 20.4%

PFBC PREFERRED BANK 31-Dec 20.05 5,512,695 265,982,719 14.74 1.33 14.47 21.05 5.85 41.2%

PPBI PACIFIC PREMIER BANCORP 31-Dec 15.74 17,965,442 262,039,378 25.80 1.78 10.44 16.18 5.50 53.7%

RCBC RIVER CITY BANK 30-Dec 100.00 12,339 122,192,100 12.18 0.93 70.50 102.00 29.50 41.8%

TCBK TRICO BANCSHARES 31-Dec 28.37 10,165,281 456,094,901 17.09 1.99 15.77 28.76 11.62 69.4%

WABC WESTAMERICA BANCORP 31-Dec 56.46 29,731,295 1,503,470,912 21.63 3.75 42.29 57.21 13.87 32.6%WIBC WILSHIRE BANCORP INC 31-Dec 10.93 93,530,959 852,464,408 15.84 2.17 5.87 11.13 5.06 86.2%

Average 16.89 1.64

Median 15.85 1.55

High 25.80 3.75

Low 8.69 0.85

12/31/2013Last Trade YTD ChangePricing in 2013

Carpenter & Company --

STOCK PERFORMANCE

Information is gathered from sources believed to be reliable, however, the accuracy of the data cannot be guaranteed.

Carpenter and Company— 2013 Annual Stock Performance Report California Banks with Total Assets Between $10 and $100 Billion

Total Market Capitalization: $23.0 Billion

Carpenter and Company— 2013 Annual Stock Performance Report California Thrifts

Total Market Capitalization: $1.8 Billion

Symbol Name Annual Mkt Cap LTM Price/

Date Price ($) Volume ($) P/E T. Book Low ($) High ($) ($) (%)

CATY CATHAY GENERAL BANCORP 31-Dec 26.73 67,866,142 2,125,127,219 19.95 1.90 18.37 27.63 7.20 36.9%

CYN CITY NATIONAL CORP 31-Dec 79.22 78,071,511 4,309,875,136 20.26 2.46 51.13 79.33 29.70 60.0%

EWBC EAST WEST BANCORP INC 31-Dec 34.97 221,522,884 4,816,694,013 17.14 2.50 22.29 35.15 13.48 62.7%