N O R T H E R N T R U S T Jeff Porta, Senior Vice President [email protected] (312) 557-0474 City of Fresno Fire and Police Retirement System & City of Fresno Employees Retirement System Northern Trust Update Robert Ernst, Senior Vice President [email protected] (312) 444-5498 Don Anderson, Vice President [email protected] (312) 444-5386 Patrick Fitzgibbons [email protected] (312) 557-1819

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

N O R T H E R N T R U S T

Jeff Porta, Senior Vice President

(312) 557-0474

City of Fresno Fire and Police Retirement System &

City of Fresno Employees Retirement System

Northern Trust Update

Robert Ernst, Senior Vice President

(312) 444-5498

Don Anderson, Vice President

(312) 444-5386

Patrick Fitzgibbons

(312) 557-1819

pattiel

Text Box

Agenda Item: 1:00 pm Joint Meeting of the Retirement Boards Meeting Date: 8/26/2014

2

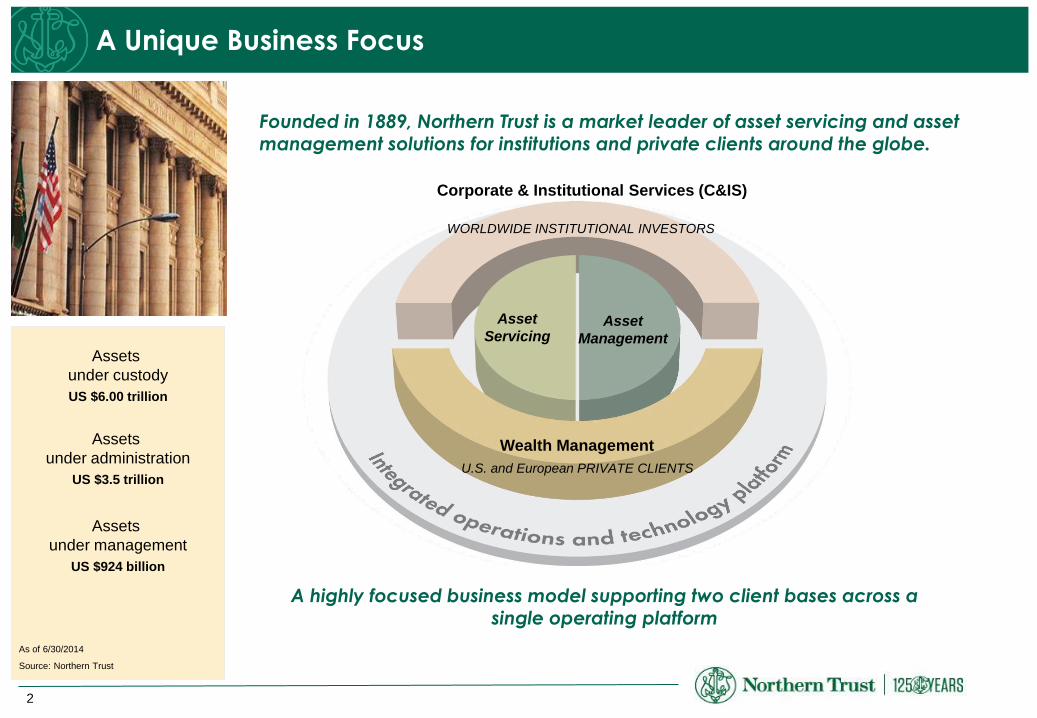

A Unique Business Focus

Founded in 1889, Northern Trust is a market leader of asset servicing and asset management solutions for institutions and private clients around the globe.

A highly focused business model supporting two client bases across a single operating platform

Wealth Management

Corporate & Institutional Services (C&IS)

Asset

Servicing Asset

Management

WORLDWIDE INSTITUTIONAL INVESTORS

U.S. and European PRIVATE CLIENTS

Assets

under custody

US $6.00 trillion

Assets

under administration

US $3.5 trillion

Assets

under management

US $924 billion

As of 6/30/2014

Source: Northern Trust

3

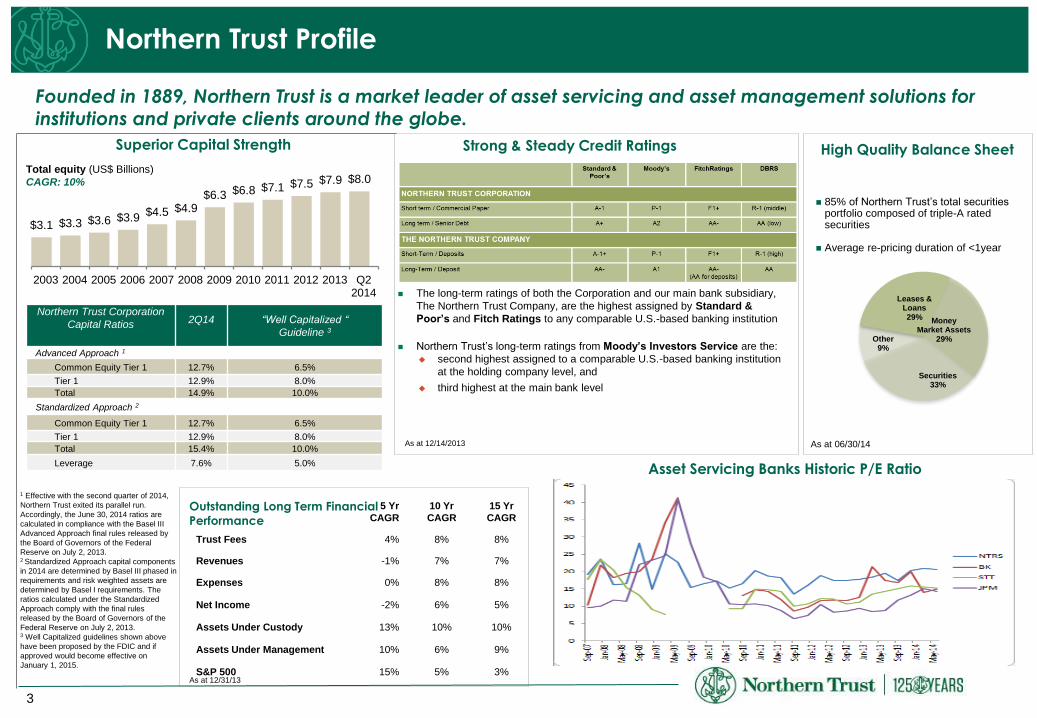

Northern Trust Profile

Founded in 1889, Northern Trust is a market leader of asset servicing and asset management solutions for institutions and private clients around the globe.

Outstanding Long Term Financial

Performance

5 Yr

CAGR

10 Yr

CAGR

15 Yr

CAGR

Trust Fees 4% 8% 8%

Revenues -1% 7% 7%

Expenses 0% 8% 8%

Net Income -2% 6% 5%

Assets Under Custody 13% 10% 10%

Assets Under Management 10% 6% 9%

S&P 500 15% 5% 3% As at 12/31/13

Asset Servicing Banks Historic P/E Ratio

Superior Capital Strength Strong & Steady Credit Ratings

85% of Northern Trust’s total securities portfolio composed of triple-A rated securities

Average re-pricing duration of <1year

High Quality Balance Sheet

As at 06/30/14

The long-term ratings of both the Corporation and our main bank subsidiary,

The Northern Trust Company, are the highest assigned by Standard &

Poor’s and Fitch Ratings to any comparable U.S.-based banking institution

Northern Trust’s long-term ratings from Moody’s Investors Service are the:

second highest assigned to a comparable U.S.-based banking institution

at the holding company level, and

third highest at the main bank level

Total equity (US$ Billions)

CAGR: 10%

Leases & Loans 29% Money

Market Assets 29%

Securities 33%

Other 9%

As at 12/14/2013

$3.1 $3.3 $3.6 $3.9 $4.5 $4.9

$6.3 $6.8 $7.1 $7.5 $7.9 $8.0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Q22014

Northern Trust Corporation

Capital Ratios 2Q14 “Well Capitalized “

Guideline 3

Advanced Approach 1

Common Equity Tier 1 12.7% 6.5%

Tier 1 12.9% 8.0%

Total 14.9% 10.0%

Standardized Approach 2

Common Equity Tier 1 12.7% 6.5%

Tier 1 12.9% 8.0%

Total 15.4% 10.0%

Leverage 7.6% 5.0%

1 Effective with the second quarter of 2014,

Northern Trust exited its parallel run.

Accordingly, the June 30, 2014 ratios are

calculated in compliance with the Basel III

Advanced Approach final rules released by

the Board of Governors of the Federal

Reserve on July 2, 2013. 2 Standardized Approach capital components

in 2014 are determined by Basel III phased in

requirements and risk weighted assets are

determined by Basel I requirements. The

ratios calculated under the Standardized

Approach comply with the final rules

released by the Board of Governors of the

Federal Reserve on July 2, 2013. 3 Well Capitalized guidelines shown above

have been proposed by the FDIC and if

approved would become effective on

January 1, 2015.

4

California Locations

10 Offices

Illinois Ohio

Michigan

Florida

Colorado

Washington

Missouri

Nevada

Wisconsin

Georgia

Arizona

New York

Connecticut

Delaware

Minnesota

Texas

Massachusetts

California

Santa Barbara

Montecito 1485 East Valley Road

Santa Barbara 206 East Anapamu

Menlo Park 2500 Sand Hill Road, Suite 150

San Francisco 580 California Street, Suite 1800

Mill Valley 575 Redwood Highway

Pasadena 201 South Lake Ave, Suite 600

Los Angeles 2049 Century Park East, Suite 3600

Newport Beach 16 Corporate Plaza Drive

San Diego 4370 La Jolla Village Drive, Suite 1000

La Jolla 1125 Wall Street

Marin County

Montecito

Pasadena

San Diego

Santa Barbara

La Jolla

San Francisco

Silicon Valley

Orange County

5

Public Funds Clients in California

City of Fresno – Fresno, CA Kern County Employees’ Retirement Association – Bakersfield,

CA

City of Oakland – Oakland, CA Los Angeles City Employees' Retirement System – Los Angeles,

CA

East Bay Municipal – Oakland, CA Los Angeles Fire & Police – Los Angeles, CA

Fresno County – Fresno, CA Orange County Treasurer – Santa Ana, CA

Golden Gate Transit Amalgamated Ret Board – San Rafael, CA San Francisco City and County Employees' Retirement System –

San Francisco

San Joaquin County – Stockton, CA Los Angeles Water & Power Employees Retirement Plan – Los

Angeles, CA

San Mateo County Employees Retirement Association –

Redwood City, CA

Alameda-Contra Costa Transit District – Oakland, CA

Stanislaus County Employees’ Retirement Association - Modesto, CA

Representative California Public Funds Clients:

6

Delivering A Broad Range of Solutions

Full array of capabilities to meet needs of sophisticated institutional investors.

Fund accounting

Transfer agency

Corporate secretarial

Trustee

Investment operations outsourcing

Safekeeping

Settlement

Derivatives processing

Banking/Integrated Disbursements

Income collection

Corporate actions

Tax reclamation

Global index management

Quantitative active

Fundamental active

Target date

Multi manager

Exchange traded funds

Hedge funds

Private equity

Investment outsourcing

Liability driven investing

Investment accounting

Reporting and valuation

Performance analytics

Risk monitoring and reporting

Trade execution analysis

Data warehouse

Cross-border pooling (patent pending)

Trade execution

Cash management

Transition management

Securities lending

Foreign exchange

Commission management

Passive currency overlay

Asset Administration

Asset Processing

Asset Reporting

Asset Enhancement

Asset Management

N O R T H E R N T R U S T

Don Anderson, Vice President

(312) 444-5386

City of Fresno Fire and Police Retirement System &

City of Fresno Employees Retirement System

Northern Trust Global Securities Lending

8

Background of the Lending Process

It promotes market efficiency and liquidity

Integral component of developed securities market for both domestic and international investors

Allows price discovery and the arbitrage of pricing inefficiencies

Supports the development of the capital markets by facilitating various investment strategies

Important part of risk management

Used for fail coverage to ensure smooth settlement cycles

Who lends securities and why?

Long-Term, Institutional Investors

An investment tool to enhance portfolio returns

To offset or eliminate costs of custody and administration

Does not interfere with portfolio strategy – investment manager should continue regardless of

securities lending

Who borrows securities and why?

Investment banks (Prime Brokers), investment funds, prop traders, market makers and other intermediaries

Hedging

Short sell

Arbitrage strategies

Settlement obligations

Why do borrowers borrow

and lenders lend?

9

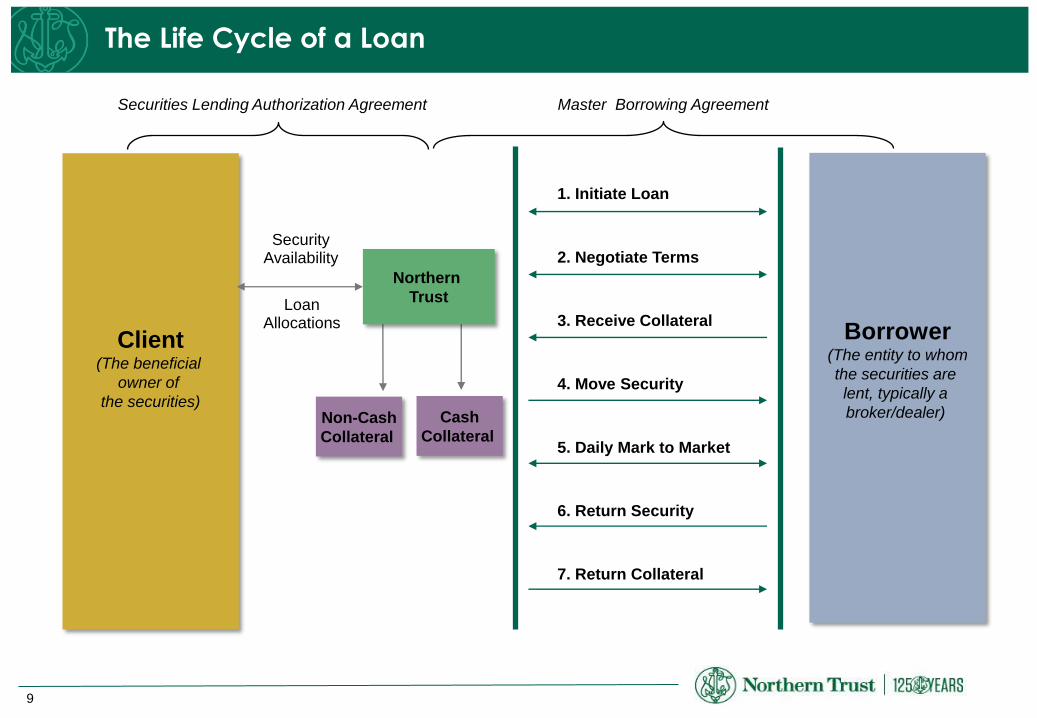

The Life Cycle of a Loan

Client (The beneficial

owner of

the securities)

Borrower (The entity to whom

the securities are

lent, typically a

broker/dealer)

Security Availability

Loan Allocations

1. Initiate Loan

2. Negotiate Terms

3. Receive Collateral

4. Move Security

5. Daily Mark to Market

6. Return Security

7. Return Collateral

Master Borrowing Agreement Securities Lending Authorization Agreement

Cash

Collateral Non-Cash

Collateral

Northern

Trust

10

Understanding the Components of Securities Lending Income

Yield on

Cash Collateral

Investment

Federal Funds

(or benchmark) Rate

Rebate Rate (Positive, above 0%, is paid

to borrower. Negative, below

0%, is paid by borrower)

Reinvestment Spread + Intrinsic Value Spread = Total Securities Lending Spread

Total Securities Lending Spread x Loan Volume = Total Gross Securities Lending Income

Reinvestment Spread:

Basis points earned from

reinvestment of cash collateral

(Yield on Cash Collateral

Investment – Fed Funds Rate)

Total

Securities

Lending

Spread

Intrinsic Value Spread:

Basis points earned

from lending security

to borrower, based on

intensity of borrower

demand

(Fed Funds Rate –

Rebate Rate)

11

How Revenue is Generated: Cash Collateral Loan

Gross Spread = Lending Spread + Investment Spread

Lending Spread = Fed Funds – Rebate Rate

Investment Spread = Reinvestment Yield – Fed Funds

Example: Northern Trust lends $25 million of US Treasuries at par

The $25 million market value loan is for 30 days collateralized with cash (fed

funds at 0.15%)

1 Receive cash collateral valued at $25,500,000 (102%)

2 Cash collateral invested in a collateral pool at yield of 0.20% $ 4,250.00

3 Rebate paid to borrower at rate of 0.05% $ (1,062.50)

4 Gross Revenue (gross spread 15 bps) $ 3,187.50

6 Net client earnings $ 1,912.50

5 Monthly lender’s fee (@ 40%) $ 1,275.00

12

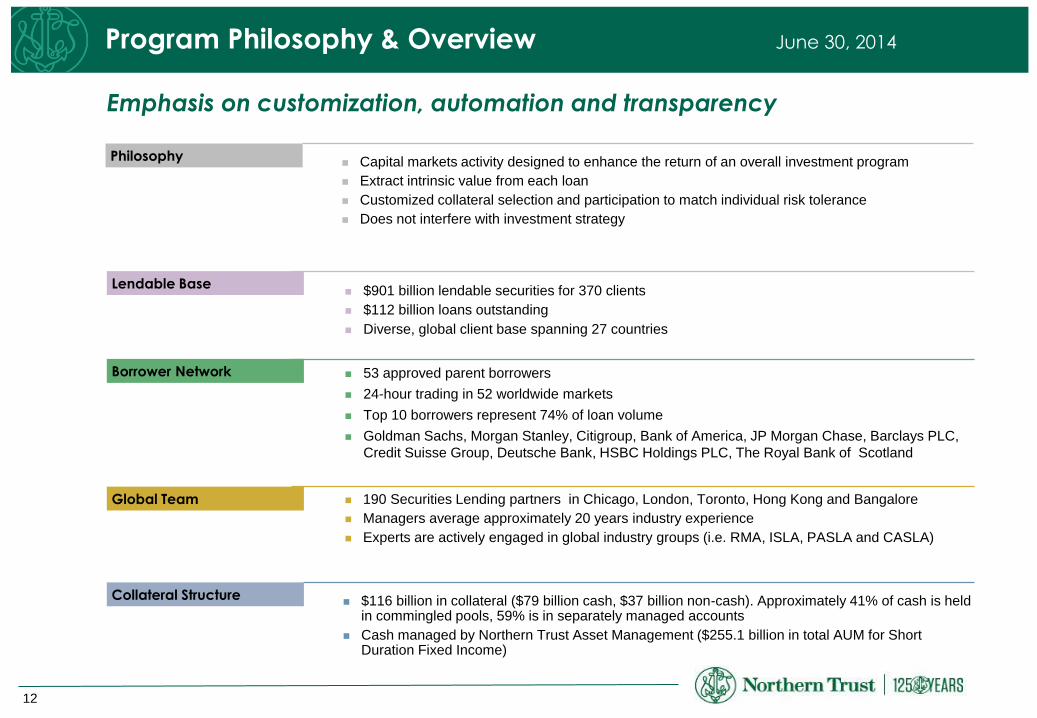

Emphasis on customization, automation and transparency

Borrower Network 53 approved parent borrowers

24-hour trading in 52 worldwide markets

Top 10 borrowers represent 74% of loan volume

Goldman Sachs, Morgan Stanley, Citigroup, Bank of America, JP Morgan Chase, Barclays PLC,

Credit Suisse Group, Deutsche Bank, HSBC Holdings PLC, The Royal Bank of Scotland

Collateral Structure $116 billion in collateral ($79 billion cash, $37 billion non-cash). Approximately 41% of cash is held

in commingled pools, 59% is in separately managed accounts

Cash managed by Northern Trust Asset Management ($255.1 billion in total AUM for Short Duration Fixed Income)

Global Team 190 Securities Lending partners in Chicago, London, Toronto, Hong Kong and Bangalore

Managers average approximately 20 years industry experience

Experts are actively engaged in global industry groups (i.e. RMA, ISLA, PASLA and CASLA)

Lendable Base $901 billion lendable securities for 370 clients

$112 billion loans outstanding

Diverse, global client base spanning 27 countries

Program Philosophy & Overview June 30, 2014

Philosophy Capital markets activity designed to enhance the return of an overall investment program

Extract intrinsic value from each loan

Customized collateral selection and participation to match individual risk tolerance

Does not interfere with investment strategy

13

Managing Risk

Risk Definition Mitigating Factors

Borrower Risk Borrower default combined with

insufficient collateral

Rigorous credit committee review

of borrowers and exposure limits

Daily marking of loans/collateral

Borrower default indemnification

Risk analysis tools (MSCI Barra)

to measure and calibrate exposure

Trade Settlement

Risk

Investment manager sells loaned

security and borrower fails to return in

time to settle the trade

Timely trade notification

Robust automated reallocations

Trade settlement protection

Additional Risks with Taking Cash as Collateral

Cash Collateral

Reinvestment Risk

Cash collateral investment becomes

impaired or decreases in value

Client approved investment guidelines

Robust independent oversight of cash pools

and investments

Dedicated team of fixed income research analysts

Daily automated monitoring of portfolio guidelines

and compliance

Interest Rate Risk Loan rebate rate exceeds earnings on

cash collateral investments

Close daily communication between lending and

cash management teams

Shared risk between Northern Trust

and client

Weekly “gap analysis” and periodic

stress testing of portfolio

Risk Management

is the cornerstone

of our program

14

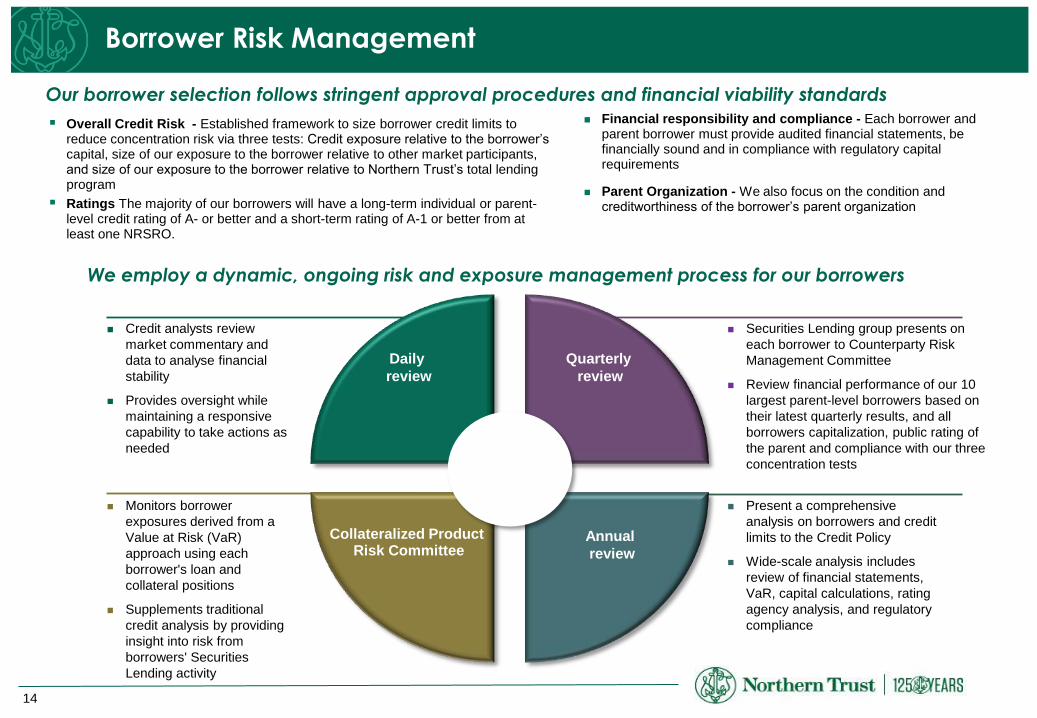

Borrower Risk Management

We employ a dynamic, ongoing risk and exposure management process for our borrowers

Credit analysts review

market commentary and

data to analyse financial

stability

Provides oversight while

maintaining a responsive

capability to take actions as

needed

Monitors borrower

exposures derived from a

Value at Risk (VaR)

approach using each

borrower's loan and

collateral positions

Supplements traditional

credit analysis by providing

insight into risk from

borrowers' Securities

Lending activity

Securities Lending group presents on

each borrower to Counterparty Risk

Management Committee

Review financial performance of our 10

largest parent-level borrowers based on

their latest quarterly results, and all

borrowers capitalization, public rating of

the parent and compliance with our three

concentration tests

Present a comprehensive

analysis on borrowers and credit

limits to the Credit Policy

Wide-scale analysis includes

review of financial statements,

VaR, capital calculations, rating

agency analysis, and regulatory

compliance

Quarterly

review

Annual

review

Collateralized Product Risk Committee

Daily

review

Our borrower selection follows stringent approval procedures and financial viability standards

Overall Credit Risk - Established framework to size borrower credit limits to reduce concentration risk via three tests: Credit exposure relative to the borrower’s capital, size of our exposure to the borrower relative to other market participants, and size of our exposure to the borrower relative to Northern Trust’s total lending program

Ratings The majority of our borrowers will have a long-term individual or parent-level credit rating of A- or better and a short-term rating of A-1 or better from at least one NRSRO.

Financial responsibility and compliance - Each borrower and parent borrower must provide audited financial statements, be financially sound and in compliance with regulatory capital requirements

Parent Organization - We also focus on the condition and creditworthiness of the borrower’s parent organization

15

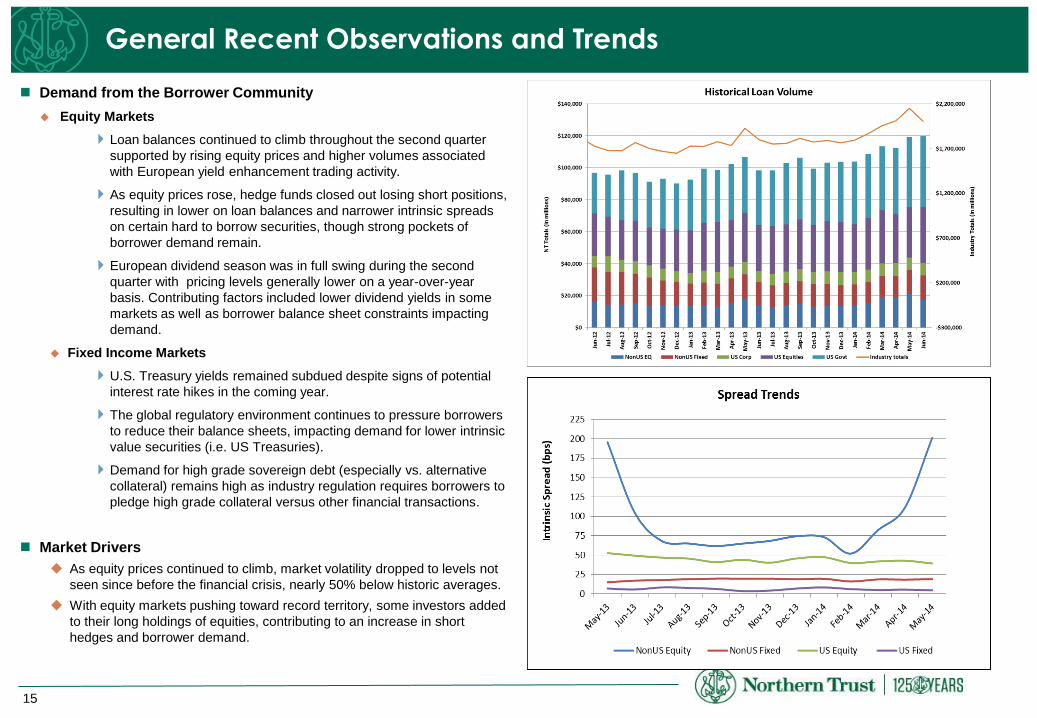

Demand from the Borrower Community

Equity Markets

Loan balances continued to climb throughout the second quarter

supported by rising equity prices and higher volumes associated

with European yield enhancement trading activity.

As equity prices rose, hedge funds closed out losing short positions,

resulting in lower on loan balances and narrower intrinsic spreads

on certain hard to borrow securities, though strong pockets of

borrower demand remain.

European dividend season was in full swing during the second

quarter with pricing levels generally lower on a year-over-year

basis. Contributing factors included lower dividend yields in some

markets as well as borrower balance sheet constraints impacting

demand.

Fixed Income Markets

U.S. Treasury yields remained subdued despite signs of potential

interest rate hikes in the coming year.

The global regulatory environment continues to pressure borrowers

to reduce their balance sheets, impacting demand for lower intrinsic

value securities (i.e. US Treasuries).

Demand for high grade sovereign debt (especially vs. alternative

collateral) remains high as industry regulation requires borrowers to

pledge high grade collateral versus other financial transactions.

Market Drivers

As equity prices continued to climb, market volatility dropped to levels not

seen since before the financial crisis, nearly 50% below historic averages.

With equity markets pushing toward record territory, some investors added

to their long holdings of equities, contributing to an increase in short

hedges and borrower demand.

General Recent Observations and Trends

16

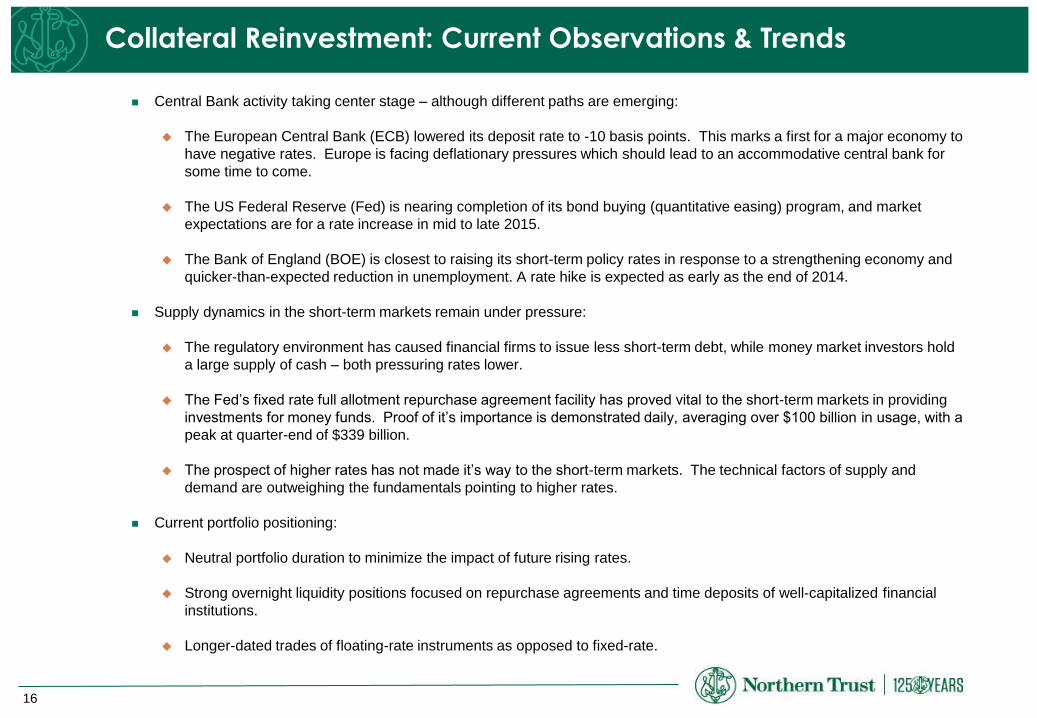

Collateral Reinvestment: Current Observations & Trends

Central Bank activity taking center stage – although different paths are emerging:

The European Central Bank (ECB) lowered its deposit rate to -10 basis points. This marks a first for a major economy to

have negative rates. Europe is facing deflationary pressures which should lead to an accommodative central bank for

some time to come.

The US Federal Reserve (Fed) is nearing completion of its bond buying (quantitative easing) program, and market

expectations are for a rate increase in mid to late 2015.

The Bank of England (BOE) is closest to raising its short-term policy rates in response to a strengthening economy and

quicker-than-expected reduction in unemployment. A rate hike is expected as early as the end of 2014.

Supply dynamics in the short-term markets remain under pressure:

The regulatory environment has caused financial firms to issue less short-term debt, while money market investors hold

a large supply of cash – both pressuring rates lower.

The Fed’s fixed rate full allotment repurchase agreement facility has proved vital to the short-term markets in providing

investments for money funds. Proof of it’s importance is demonstrated daily, averaging over $100 billion in usage, with a

peak at quarter-end of $339 billion.

The prospect of higher rates has not made it’s way to the short-term markets. The technical factors of supply and

demand are outweighing the fundamentals pointing to higher rates.

Current portfolio positioning:

Neutral portfolio duration to minimize the impact of future rising rates.

Strong overnight liquidity positions focused on repurchase agreements and time deposits of well-capitalized financial

institutions.

Longer-dated trades of floating-rate instruments as opposed to fixed-rate.

17

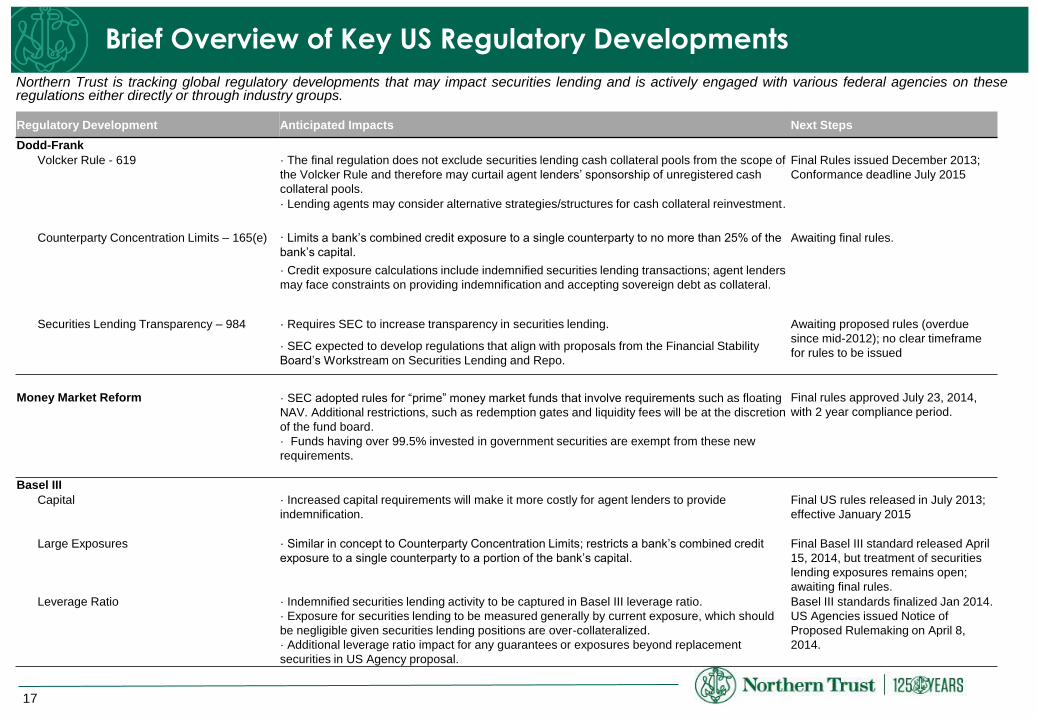

Brief Overview of Key US Regulatory Developments

Northern Trust is tracking global regulatory developments that may impact securities lending and is actively engaged with various federal agencies on these regulations either directly or through industry groups.

Regulatory Development Anticipated Impacts Next Steps

Dodd-Frank

Volcker Rule - 619 · The final regulation does not exclude securities lending cash collateral pools from the scope of

the Volcker Rule and therefore may curtail agent lenders’ sponsorship of unregistered cash

collateral pools.

Final Rules issued December 2013;

Conformance deadline July 2015

· Lending agents may consider alternative strategies/structures for cash collateral reinvestment.

Counterparty Concentration Limits – 165(e) · Limits a bank’s combined credit exposure to a single counterparty to no more than 25% of the

bank’s capital.

Awaiting final rules.

· Credit exposure calculations include indemnified securities lending transactions; agent lenders

may face constraints on providing indemnification and accepting sovereign debt as collateral.

Securities Lending Transparency – 984 · Requires SEC to increase transparency in securities lending. Awaiting proposed rules (overdue

since mid-2012); no clear timeframe

for rules to be issued · SEC expected to develop regulations that align with proposals from the Financial Stability

Board’s Workstream on Securities Lending and Repo.

Money Market Reform · SEC adopted rules for “prime” money market funds that involve requirements such as floating

NAV. Additional restrictions, such as redemption gates and liquidity fees will be at the discretion

of the fund board.

Final rules approved July 23, 2014,

with 2 year compliance period.

· Funds having over 99.5% invested in government securities are exempt from these new

requirements.

Basel III

Capital · Increased capital requirements will make it more costly for agent lenders to provide

indemnification.

Final US rules released in July 2013;

effective January 2015

Large Exposures · Similar in concept to Counterparty Concentration Limits; restricts a bank’s combined credit

exposure to a single counterparty to a portion of the bank’s capital.

Final Basel III standard released April

15, 2014, but treatment of securities

lending exposures remains open;

awaiting final rules.

Leverage Ratio · Indemnified securities lending activity to be captured in Basel III leverage ratio.

· Exposure for securities lending to be measured generally by current exposure, which should

be negligible given securities lending positions are over-collateralized.

· Additional leverage ratio impact for any guarantees or exposures beyond replacement

securities in US Agency proposal.

Basel III standards finalized Jan 2014.

US Agencies issued Notice of

Proposed Rulemaking on April 8,

2014.

18

Investment Profile: Core USA Cash Collateral Fund June 30, 2014

* Based upon traded basis from holdings reports

NOTE: This information was created using the best unaudited data available to us and may not be completely reliable, accurate, or timely. Data is prepared on a

settled basis, which may differ from traded basis data on the Cash Collateral Holdings report. “Traded Basis” reflects pending trades.

Core USA 6/30/13 Fresno

Average Yield Market to Book Avg Loan Duration

0.24% 0.99999 65 Days

19

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

2007 2008 2009 2010 2011 2012 2013 2014

Int'l Equity

Int'l Fixed

US Equities

US Corp Bds

US Agencies

US Treasuries

Historical Net Earnings Fiscal Years Ended June 30

CITY OF FRESNO

$2,154,273

$1,153,376

$1,015,208

$1,723,512

$823,419

$1,025,408 $1,105,631

$1,237,025

20

Earnings Scorecard Year Ended 06/30/14

21

Earnings Performance Comparison Year Ended 06/30/14 versus Year Ended 06/30/13

22

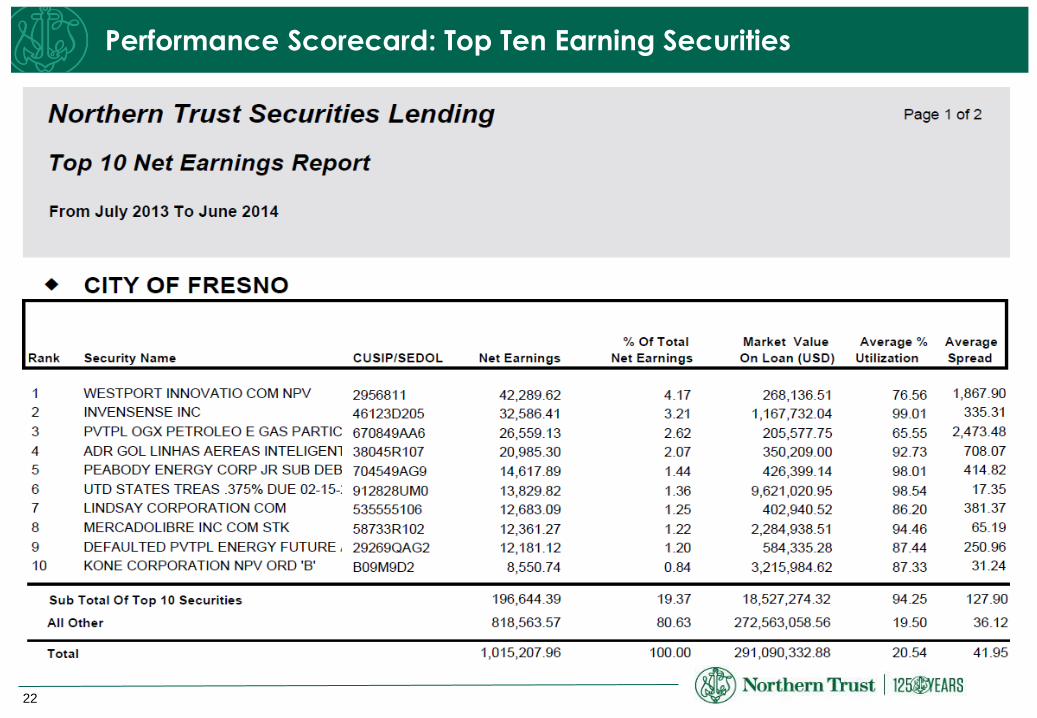

Performance Scorecard: Top Ten Earning Securities

23

Transparency and Information Delivery

Monthly reporting

Performance scorecard:

Account earnings and performance

Security level detail

Client by asset type and account earnings

Date range comparison

Historical statistics graph

Earnings statement - summary and detail

Daily reporting

Securities loaned – detail

Borrower utilization – summary by borrower

Account utilization – loan detail, summary by

account

Collateral – by security type, country and detail

holdings

Executive Summary

Flexible, electronic reporting: Northern Trust provides you with customized reports to help monitor

your Securities Lending activity

Helping to keep you

informed about your

Securities Lending

performance.

Securities Lending

Data Block on

Passport®

Facilitates the online

distribution of vital,

tailored information on

each client’s portfolio

holdings, characteristics,

investment performance

and commentary

24

Fully committed to

Securities Lending

Capitalize on Northern Trust’s

Asset Servicing

and Asset Management

strengths

Stable and experienced team

dedicated to

Securities Lending

Northern Trust

Global

Securities

Lending

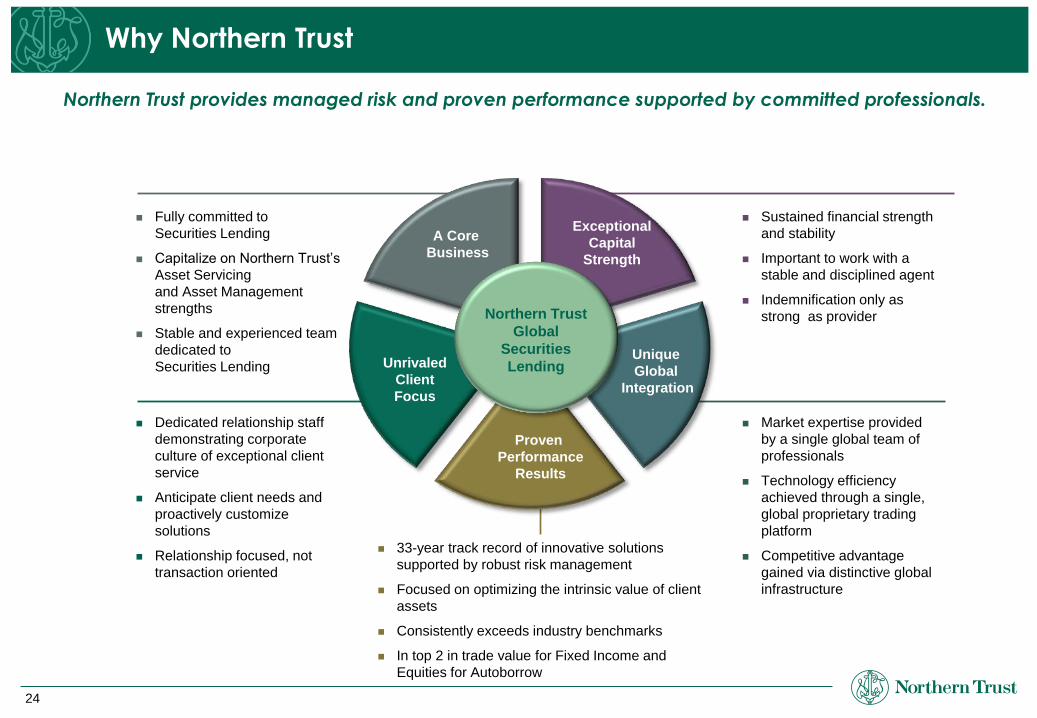

Northern Trust provides managed risk and proven performance supported by committed professionals.

Why Northern Trust

Exceptional

Capital

Strength

A Core

Business

Unique

Global

Integration

Proven

Performance

Results

Unrivaled

Client

Focus

Sustained financial strength

and stability

Important to work with a

stable and disciplined agent

Indemnification only as

strong as provider

Market expertise provided

by a single global team of

professionals

Technology efficiency

achieved through a single,

global proprietary trading

platform

Competitive advantage

gained via distinctive global

infrastructure

33-year track record of innovative solutions

supported by robust risk management

Focused on optimizing the intrinsic value of client

assets

Consistently exceeds industry benchmarks

In top 2 in trade value for Fixed Income and

Equities for Autoborrow

Dedicated relationship staff

demonstrating corporate

culture of exceptional client

service

Anticipate client needs and

proactively customize

solutions

Relationship focused, not

transaction oriented

northerntrust.com © 2013 Northern Trust Corporation

N O R T H E R N T R U S T

Antwon McGruder, Vice President

(312) 557-3545

City of Fresno Fire and Police Retirement System &

City of Fresno Employees Retirement System

Northern Trust Commission Management

26

Commission Management Review – 2013

January 1, 2013 through December 31, 2013

Program Commission $ 994,130.62

Rebate basis $ 49,762.81

Rebate $ 38,036.34

Rebate % 80 – Domestic

70 – International

% CM trades of total 9.75 %

Effective commission rate

Before rebate 1.31 cps (cents per share)

After rebate 1.26 cps

27

Effective Commission Rates – 2013

28

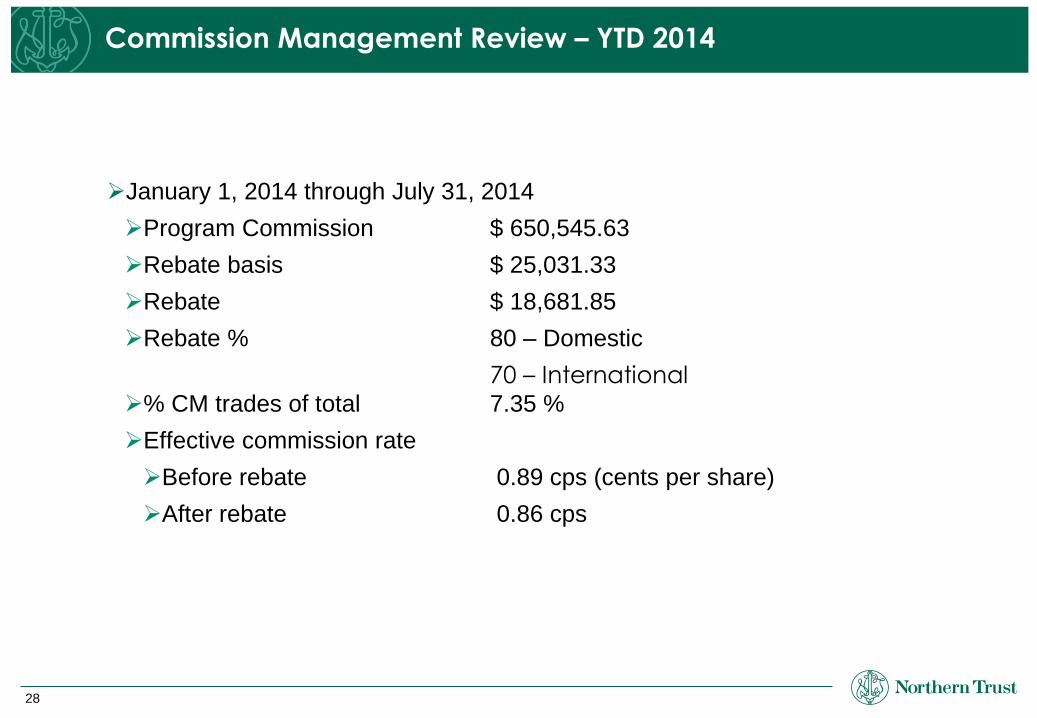

Commission Management Review – YTD 2014

January 1, 2014 through July 31, 2014

Program Commission $ 650,545.63

Rebate basis $ 25,031.33

Rebate $ 18,681.85

Rebate % 80 – Domestic

70 – International % CM trades of total 7.35 %

Effective commission rate

Before rebate 0.89 cps (cents per share)

After rebate 0.86 cps

29

Effective Commission Rates – YTD 2014

30

Current Environment

Commissions have been falling for the last few years

Providers excluding trades having commissions under a specified level, usually 3cps

Many CM providers and participating brokers left the space

Program economics tough in the lower commission environment

Northern’s Commission Management, a smarter approach

Northern Trust Securities restructured its Commission Management program

Economics work for all parties

All trades are eligible

Rebate basis is 80% commission in excess of the executing brokers cost of trade processing

Economics work for City of Fresno Retirement Systems

Recaptured amount lowers effective commission

Benefit to plan until there is no rebate available

No rebate available means plan is trading at broker’s cost.

Commission Management Summary

31

Disclosures

Please note that the reports have been created using the best available preliminary data. Please also note that the information

contained in the reports is preliminary (and therefore may not be completely reliable) and it is provided to you for your own internal

informative purposes only. Reports may also contain information provided by third parties, derived by third parties or derived from third

party data and/or data that may have been categorized or otherwise reported based upon client direction - Northern Trust assumes no

responsibility for the accuracy, timeliness or completeness of any such information. If you have questions regarding third party data or

direction as it relates to any reports, please contact your Northern Trust relationship team.

Evaluations are based on the asset allocation, actual historical spread and on-loan figures provided to Northern Trust. Consequently,

as changes in these factors occur and as trading patterns of the portfolio managers’ shift, actual earnings generated in Securities

Lending may be impacted.

CONFIDENTIALITY NOTICE: This communication is confidential, may be privileged and is meant only for the intended recipient. If

you are not the intended recipient, please notify the sender ASAP and delete this message from your system.

IRS CIRCULAR 230 NOTICE: To the extent that this message or any attachment concerns tax matters, it is not intended to be used

and cannot be used by a taxpayer for the purpose of avoiding penalties that may be imposed by law. For more information about this

notice, see http://www.northerntrust.com/circular230.

32

Disclosures

FOR INSTITUTIONAL INVESTORS ONLY: This material is directed to eligible counterparties and professional clients only and should not be

relied upon by retail investors.

CONFIDENTIALITY NOTICE: This communication is confidential, may be privileged and is meant only for the intended recipient. If you are

not the intended recipient, please notify the sender ASAP and delete this message from your system.

IRS CIRCULAR 230 NOTICE: To the extent that this message or any attachment concerns tax matters, it is not intended to be used and

cannot be used by a taxpayer for the purpose of avoiding penalties that may be imposed by law. For more information about this notice, see

http://www.northerntrust.com/circular230.

The content of this material is provided for informational purposes only. This material is not intended to be relied upon as a forecast,

research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment

strategy. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed to be

reliable, but are not necessarily all inclusive and are not guaranteed as to accuracy. Any opinions expressed herein are subject to changed

at any time without notice; any person relying upon this information shall be solely responsible for the consequences of such reliance. Past

performance is no guarantee of future results.

The foregoing discussion is general in nature, is intended for informational purposes only and is not intended to provide specific advice or

recommendations for any individual or organization.

Products offered through Northern Trust Securities, Inc. are not FDIC insured, not guaranteed by any bank, and are subject to investment

risk including loss of principal amount invested. Northern Trust Securities, Inc. is a member of FINRA and the SIPC and a wholly owned

subsidiary of Northern Trust Corporation.

Additional information available upon request.

Related Documents