© 2013 Research Academy of Social Sciences http://www.rassweb.com 376 International Journal of Management Sciences Vol. 1, No. 10, 2013, 376-385 Non-Governmental Organization’s Agricultural Micro Credit Facilities and Farmer’s household Income in Benue State, Nigeria C. V. O. Eneji 1 , E. Obim 2 , J. E. Otu 3 , S. O. Ogli 4 Abstract The study was undertaken to investigate the Non- Governmental Organization’s Agricultural Micro-Credit Facilities on farmers’ income output in Benue State. Stage wise random sampling was adopted to select 220 respondents for the study. Information on respondents’ socio-economic characteristics as well as their income before and after the loan was sourced using questionnaire and Focus Group Discussion (FGD). A null hypothesis which stated that there is no significant difference between income of farmers before and after the loan facility, the hypothesis was tested using dependent t-test analysis while percentages were calculated in order to analyze other data. Socio-economic characteristics of the respondents revealed that majority (59.3%) were males and mostly youth of less than 50 years of age. Result of T-test analysis revealed a significant difference in beneficiaries’ income before and after the scheme at 0.05 significance level. This led to the rejection of the null hypothesis which stated that there is no significant difference in the income of beneficiaries before and after the scheme. The findings shows farmers’ income improved considerably after the loan, this has also contributed in improving the farmer’s livelihoods and quality of lives within these agrarian communities. Recommendations were made on the basis of the findings of the study, to encourage the provision of more loans to rural farmers and also to use middle men like the NGOs in the mobilization, disbursement and monitoring of the utilization of such facilities to improve farmer’s output in terms of income and productivities. Keywords: non- governmental organization, micro-credit facilities, farmer’s income, livelihoods and productivities. 1. Introduction Rural dwellers need agricultural credit at reasonable terms to invest in their various businesses. This will increase their earning capacity and consequently their standard of living. In Benue State, most of the rural dwellers are poor farmers with small farm holdings and thus require agricultural micro-credit to invest in farm business. Agriculture is one of the major economic activities in Benue State. Agricultural activities provide employment for a sizeable population of the State. The State is endowed with favorable climatic and soil conditions for the production of different types of crops like yams, cassava, rice, cocoa, maize, guinea corn, palms among others. Imodu (2000) observed that financial outlay is an integral part of any business and as a result, adequate capital is important in agricultural production. Oruonye and Musa, (2012), however observed that about 80% of the present farm populations in Nigeria are small scale farmers or producers with fragmented farm holdings who can only utilize small resources. Hence for farmers to meet their agricultural input demands, they need additional inputs in terms of both financial and other forms of agricultural inputs. The only way 1 Department of Curriculum and Teaching, Environmental Education Unit, University of Calabar, Nigeria 2 Department of Banking and Finance, University of Calabar, Nigeria 3 Department of sociology, University of Calabar, Nigeria 4 International Organization of the Red Cross Abuja, Nigeria

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© 2013 Research Academy of Social Sciences http://www.rassweb.com 376

International Journal of Management Sciences

Vol. 1, No. 10, 2013, 376-385

Non-Governmental Organization’s Agricultural Micro Credit

Facilities and Farmer’s household Income in Benue State, Nigeria

C. V. O. Eneji1, E. Obim

2, J. E. Otu

3, S. O. Ogli

4

Abstract

The study was undertaken to investigate the Non- Governmental Organization’s Agricultural Micro-Credit

Facilities on farmers’ income output in Benue State. Stage wise random sampling was adopted to select 220 respondents for the study. Information on respondents’ socio-economic characteristics as well as their

income before and after the loan was sourced using questionnaire and Focus Group Discussion (FGD). A

null hypothesis which stated that there is no significant difference between income of farmers before and

after the loan facility, the hypothesis was tested using dependent t-test analysis while percentages were calculated in order to analyze other data. Socio-economic characteristics of the respondents revealed that

majority (59.3%) were males and mostly youth of less than 50 years of age. Result of T-test analysis revealed

a significant difference in beneficiaries’ income before and after the scheme at 0.05 significance level. This led to the rejection of the null hypothesis which stated that there is no significant difference in the income of

beneficiaries before and after the scheme. The findings shows farmers’ income improved considerably after

the loan, this has also contributed in improving the farmer’s livelihoods and quality of lives within these

agrarian communities. Recommendations were made on the basis of the findings of the study, to encourage the provision of more loans to rural farmers and also to use middle men like the NGOs in the mobilization,

disbursement and monitoring of the utilization of such facilities to improve farmer’s output in terms of

income and productivities.

Keywords: non- governmental organization, micro-credit facilities, farmer’s income, livelihoods and

productivities.

1. Introduction

Rural dwellers need agricultural credit at reasonable terms to invest in their various businesses. This will increase their earning capacity and consequently their standard of living. In Benue State, most of the rural

dwellers are poor farmers with small farm holdings and thus require agricultural micro-credit to invest in

farm business. Agriculture is one of the major economic activities in Benue State. Agricultural activities provide employment for a sizeable population of the State. The State is endowed with favorable climatic and

soil conditions for the production of different types of crops like yams, cassava, rice, cocoa, maize, guinea

corn, palms among others.

Imodu (2000) observed that financial outlay is an integral part of any business and as a result, adequate

capital is important in agricultural production. Oruonye and Musa, (2012), however observed that about 80%

of the present farm populations in Nigeria are small scale farmers or producers with fragmented farm holdings who can only utilize small resources. Hence for farmers to meet their agricultural input demands,

they need additional inputs in terms of both financial and other forms of agricultural inputs. The only way

1 Department of Curriculum and Teaching, Environmental Education Unit, University of Calabar, Nigeria 2 Department of Banking and Finance, University of Calabar, Nigeria 3 Department of sociology, University of Calabar, Nigeria 4 International Organization of the Red Cross Abuja, Nigeria

International Journal of Management Sciences

377

this can be achieved is through sourcing of credit facilities. The importance of micro-credit as a strategy for increasing agricultural productivity and market has also been stressed.

Ayinde, et al. (2004) observed that most farmers have not been able to accumulate capital because they

have been trapped in the vicious circle of low level of output as a result of poor inputs, low income, low savings and investments. This problem is particularly applicable to rural farmers. To help them, there is the

urgent need to inject small loans from outside the farm sector. The real essence of agricultural micro-credit is

that, it enables farmers to take advantage of new technologies in the form of machines, improved seeds, fertilizers, insecticides, herbicides, storage facilities and effective and efficient labor. Some author like

Partners for Development (2002), Ayinde et al. (2005) and Ayinde and Ayinde, (2006), often mentioned the

importance of micro-credit in agricultural development which generally enabled idle resources to be tapped

and to be adequately utilized provided that the attitude of rural people and their consumption patterns actually encourage the use of resources. Ayinde, (2008) however observed that there is no doubt that

improving the lot of rural farmers is a sure way to improving the socio-economic life, including their quality

of lives, their health and living standard. The surest way of doing this is by extending micro-credit to needy farmers to establish or expand already existing agricultural businesses. Credit to rural farmers could be

another way in which the marketing system could be made to operate efficiently. With adequate credit, post-

harvest prices depressions could be avoided and the rural people could be placed in a better bargaining

position.

Micro-credit inadequacy is seen as a major constraint in agricultural production for small-scale farmers

who are expected to grow to become medium and eventually large-scale farmers. They must have among other incentives an assured supply of credit. The credit helps to improve the economic well being of the rural

farmers, increase agricultural output and promote development generally (NACRDB, 2001, Mundi and

Tenere, 2007 and Johnson, 2007). Economic Commission for Africa (2001) was of the opinion that the bulk

of such loan funds should be provided in kind. According to this commission, the ingredients necessary for capital productivity were complementary. It stressed that it is counter-productive to give credit to farmers

when certain farm inputs such as fertilizers, improved seeds, insecticides, herbicides etc are not physically

available.

Agricultural credit policy aims at making adequate investment funds available to the agricultural sector

at the right time and at such rate as will make returns from agriculture more attractive (Imoudu, 2002). To

achieve this, government has persued structural adjustment in fiscal and monetary policies as they affect agricultural loans. For example, the sectoral allocation of loans and advances from 15 percent to 25 percent is

envisaged by the policy adjustment, in addition to the grace period granted on agricultural loans in line with

the gestation period of the project that is 1-2 years for seasonal crops, poultry, piggery and cattle fattening; while 4-7 years for tree crops, cattle breeding and ranching (FAO and World, 2007). These Authors affirm

that the implementation of the credit policy has been successfully carried out through the Nigeria

Agricultural and Co-operative Bank (NACB) now known as Nigeria Agricultural Co-operative and Rural

Development Bank (NACRDB), Agricultural Credit Guarantee Scheme Fund (ACGSF) operated by various Commercial Banks, State Ministries of Agriculture and Natural Resources and Agricultural Development

Projects (ADPs).

Ezihe, et al. (2007) observed that capital shortages significantly constrained the economic development of farmers in developing countries. For this reason, there is need for suitable agricultural credit policy and

loan-able funds to enable farmers adopt modern methods of agricultural production and marketing. The

purpose of the agricultural credit policy is importantly aimed at increasing the volume of formal credit in rural areas. This is to enable small-scale farmers have access to loan in order to finance agricultural

production and to test new technologies (Community Development Foundation, 2006).

Akramov, (2009) affirmed that vicious circle of low output, low income, low savings and little or no investment are characteristics of most developing economies and particularly the problems of farming

communities. Breaking this vicious circle of poverty is a key goal of governments the world over. According

to these writers, small-scale farmers are poor because they cultivate small hectares of land, produce low

C.V.O. Eneji et al.

378

output and as such their income is low which in turn constrains farm expansion and the acquisition of new technologies. As a result of this, government intervention in credit starts with policy. Bassey and Coate

(1995), also see agricultural credit policy as an important instrument of economic policy in most market

oriented developing countries.

The involvement of government in agricultural credit policy in Nigeria started in the former Northern Region in the 1930s. For active participation of farmers in agricultural financing in Nigeria, the government

established these financial institutions- the Native Advance System which encouraged mixed farming and stimulated the adoption of technology in the region (Ejiofor,1996); Co-operative Credit Union League in the

Western region in 1940s which became Co-operative Bank Plc in 1953. Later, others like Agricultural

Credit Guarantee Scheme Fund (ACGSF), the Rural Banking Programme now Community Bank (CB) in the

1990s and the Central Bank of Nigeria (CBN) Department of Agricultural Financing for active participation in agricultural credit financing in Nigeria and Rural Banking Scheme by same CBN in 1977 while

Commercial Banks were forced to open rural branches to meet the credit needs of the people at the sub-urban

and rural areas of Nigeria (Ajakaiye, 1984 and Chlorida, 1984).

On the whole, government agricultural credit policy in Nigeria has been implemented through the

NACRDB, ACGSF and the state Federal Ministries of Agriculture and Natural Resources (Okorie, 1987).

Many developing regions of the world including West Africa have high population of the poor. ADB and FAO, (2003) pointed out that there are several countries including Burkina Faso, the Gambia, Guinea Bissau,

Niger and Nigeria where per capital income is less than 1 USD per day. In several West African countries,

the per capita income declined between 1990 and 2000 (FAO/World Bank, 2007). This would imply an overall decline in purchasing power and continued deprivation of a sizeable section of the population if

current low income growth persists.

In Nigeria, Benue state is reputed to be a major producer of a diverse agricultural produce which include yam, rice, beans, cassava, potatoes, maize, soya beans, sorghum, millet and coco-yam and major cash crops

like oil palm, cotton bean among others. It also boasts of one of the longest stretches of river systems in the

country with potentials for a viable fishing industry and dry season farming through irrigation and as a source

of transportation. Since the state is an Agrarian state; most farmers use their land for agricultural purposes. Thus majority of the population make their living by farming. The types of crops to be produced, when and

where to produce the crops is largely controlled by the size and land tenure system, the distance of the farm

from the house and the individual’s ability to mechanize or commercialize his farm operation.

The rural small-scale farmers are actually poor, especially those that cultivate small hectare of land.

They produce low output and have low income which hinders expansion of their farms from the current

subsistence level. To reverse this trend, small-scale farmers need agricultural credit to purchase modern agricultural tools, input, technology, labor and other shared facilities for overall increase in production and

output (Olutayo, 2009). According to them, the role of credit in agriculture is to enable the farmers move on

to a higher level of technology that would create an increased and sustainable agricultural output. For this reason, Nigeria, Non-governmental Organizations and many other West African countries have recognized

the positive role micro-credits can play in agricultural production and marketing and have established a

number of special agencies to provide agricultural credit and inputs to farmers. For example, in Nigeria the NACRDB, rural branches of commercial banks as well as NGOs and CBOs are established mainly to provide

credit for rural development, particularly agricultural productions. In Ghana for instance, the Agricultural

Development Bank as well as Government owned rural banks perform similar roles like that of NACRDB

Limited (Olutayo, 2009).

In 1999, Partners for Development (PFD) conducted a research in several rural communities in North

central and Northeast Nigeria. Two primary constraints emerged; lack of credit opportunities for the poor

farmers and poor infrastructure. In April 2000, it expanded geographically into Nasarawa and Bauchi States and sectorally into public health and agriculture. The agricultural marketing support programme which is

funded by the United States Department of Agriculture (USDA) is being implemented in Benue State

through PFD programs that are increasing the income of farming households through the provision of micro-

International Journal of Management Sciences

379

credit (small loans) for various agricultural enterprises and feeder road improvement for easy transportation of agricultural output to markets seem to be gaining more grounds (PFD, 2002)..

There is serious problem in the repayment of loans or credit given to small-scale farmers if given to

wrong people (Ijere, 1990). In explaining this fact, the author cited the Operation Feed the Nation (OFN) in 1976 where government subsidized agricultural inputs such as improved seeds, fertilizer, cleared sites and

provided finances to wrong people. According to him, instead of concentrating on the real rural farmers, the

government paid more attention to absentee farmers and urban dwellers that in most cases had no farms and so diverted the loans to other unprofitable ventures. The factors that will enhance proper use of agricultural

credit include information on agricultural matters, such as availability of new technology, agro-chemicals,

irrigation pumps, tractors hiring services at the right time, improved seeds and fertilizer and the assurance of

good prices for the products. For instance, in Philippines the income raising activities of the small-scale farmers and peasant production groups were held back by long delays in obtaining credit and services

(Oruonye and Musa, 2012).

2. Agricultural Micro-Credit Lending Institutions in Nigeria

According to Nigeria Agricultural Co-operative and Rural Development Bank Limited (NACRDB, 2002), agricultural micro-credit lending institutions in Nigeria include:

NACRDB - Nigeria Agricultural Co-operative and Rural Development Bank;

C.B - Community Bank Limited;

P.B.N – Peoples Bank of Nigeria Limited;

A.C.G.S – Agricultural Credit Guarantee Scheme by Federal Government of Nigeria the Central

Bank through Commercial Banks;

Co-operative Bank throughout Nigeria;

Co-operative societies and informal financial institutions (Local Bam);

FEAP – Family Economic Advancement Programme;

N.T.C – Nigerian Tobacco Company Limited on targeted lending.

At present, most agricultural micro-credit lending institutions that have a firmer or stronger presence at

the rural areas of Benue State are NACRDB, PFD with Agricultural Marketing Support Programme.

According to Akramov (2009) the role of credit in agricultural enterprise development and sustainability has prompted the Federal Government of Nigeria (FGN) to establish credit schemes such as the Agricultural

Credit Guarantee Scheme (ACGS) and the Agricultural Credit Support Scheme (ACSS) to ensure farmers’

access to agricultural credit. Mundi and Tenere (2007) reported that the need for providing agricultural credit to farmers is universal.

PFD is a private American non-profit organization currently managing self-help overseas projects in

Cambodia, Bosnia and Nigeria. The mission of the PFD is to work within local community’s often in remote or conflict prone locations in activities that develop skills and improve standards of living and in such a

manner that local partners help design implement and assess programs to the greatest degree possible. The

basic criterion used to achieve the above mission has no restriction to race, religion and ethnicity. Apart from the agricultural sector, PFD works also in the public health, clean water supply, household economy and food

security sectors. PFD’s approach is to operate from a community base and to collaborate with local

counterparts. To ensure local ownership of programs and sustainability, local partners are involved in the

design, implementation and assessment of programs. This in turn leads to skill development in key areas. Providing technical assistance and micro-credit loans for the start up and support of small farm enterprises;

Training local technicians in communities for water supply and structure maintenance; Training local health

care providers to provide and treat primary health care problems; In April 2002, PFD started working closely

C.V.O. Eneji et al.

380

with local NGOs and local communities to assess problems, plan, implement and monitor progress. PDF Focus Sectors include health, water supply and food security. Key impacts by sector include: capacity

building, small agricultural enterprise development, reproductive health and HIV/AIDs.

3. Materials and Methodology

In order to realize the aim of this study, both qualitative and quantitative data were collected. Well structured questionnaire and focus group discussions were used for data collection to assess the income of

farmers before and after the loan scheme. The study population was made up of five (5) NGOs based in

Makurdi, Gboko, Katsina Ala and Oturkpo, zones of Benue State with a total number of 2200 farmers

(members) who were beneficiaries of the Partners for Development (PFD)-assisted micro-credit scheme in the State. Each of the NGOs has 440 beneficiaries. To give a geographical spread to the study, the

researchers randomly selected 4 zones out of the 6 zones participating in the micro credit loan scheme given

to farmers by PFD to assist in their agricultural productivity. The stage-wise sampling procedure was done in three stages and using tie and draw where the names of the 6 zones were all written on a piece of paper,

shuffle together and put in a bag, four children were randomly selected to draw from the bag without

replacement, these was done to make sure no zone was selected twice. A total of four zones were then selected to include Makurdi, Oturkpo, Gboko and Katsina Ala. A total of five NGOs with a sample of 220

respondents (10%) were randomly sampled for the study. These NGOs are Health and Development

organization, (HADO) Oturkpo, Widows Foundation Association, (WFA) Katsina Ala, OSA Foundation,

Gboko and women in Nigeria, Benue chapter, Makurdi. The researchers personally administered the instruments to the respondents and collected same from the respondents. A total of 220 questionnaires were

given out, but only 182 respondents returned their questionnaire, so there was a shortage of 38 questionnaires

recorded. The dependent t-test statistics and simple percentage was then used to analyze the data.

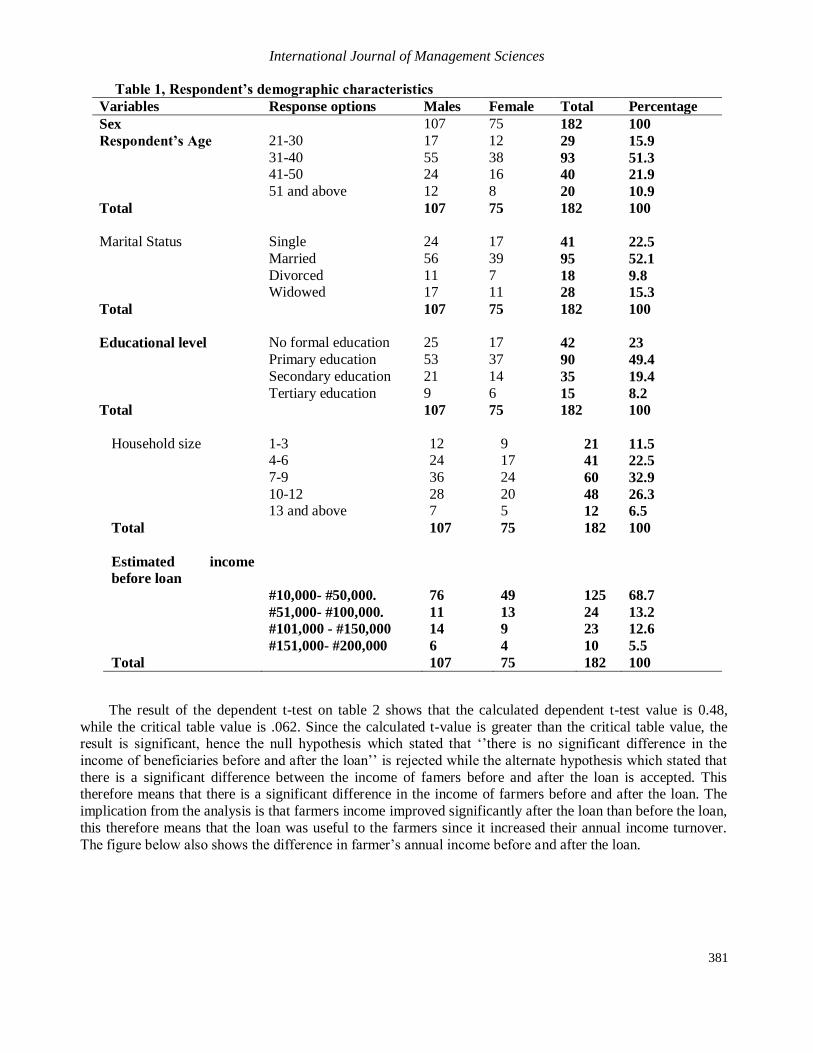

4. Result and discussion

From Table 1, respondent’s marital status, 41 respondents (22.5%) said there are single and never

married, 95 respondents (52.1%) were married, 18 respondents, (9.8%) were divorced, separated or single

parents, while 28 respondents (15.3%) were either widows or widowers. Respondent’s educational status shows that 42 respondent’s (23%) had never received any formal education, 90 respondents (49.4%) had

primary education as the highest educational qualification attained, 35 respondents (19.4%) had secondary

education, while 15 respondents representing 8.2% had tertiary education. In terms of household sizes of

respondents, 21 respondents (11.5%) had a household size of between 1-3 persons, 41 respondents (22.5%) had household sizes of between 4-6 persons, 60 respondents (32.9%) had a household size of between 7-9

persons, while about 48 respondents (26.3%) have a household size of 10-12 persons and 12 respondents

(6.6%) had a household size of 13 and above persons.

On the estimated household income before getting the loan, it was gathered that about 125

respondents representing 68.7% of the population said their annual income at that time was between #10,000

to #50,000, 24 respondents (13.2%) said their estimated annual income before the loan was between #51,000- #100,000, 23 respondents (12.6%) said their annual income before the loan was between #101,000-

#150,000, 10 respondent representing 6.5% said their annual income before the loan was between #151,000

and above., on the same assessment after the loan, 46 respondents said their income after the loan was between #10,000-#50,000, 52 respondents representing 28.6% said their income after the loan now is

between #51-#100,000, 57 respondent (31.3%) said their income now after the loan is falls between

#101,000- #150,000 and 27 respondents said their annual income after the loan is about #151,000 and above

(see table 1).

International Journal of Management Sciences

381

Table 1, Respondent’s demographic characteristics

Variables Response options Males Female Total Percentage

Sex 107 75 182 100

Respondent’s Age 21-30 17 12 29 15.9

31-40 55 38 93 51.3 41-50 24 16 40 21.9

51 and above 12 8 20 10.9

Total

107 75 182 100

Marital Status Single 24 17 41 22.5

Married 56 39 95 52.1

Divorced 11 7 18 9.8 Widowed 17 11 28 15.3

Total

107 75 182 100

Educational level No formal education 25 17 42 23

Primary education 53 37 90 49.4

Secondary education 21 14 35 19.4

Tertiary education 9 6 15 8.2

Total

107 75 182 100

Household size 1-3 12 9 21 11.5 4-6 24 17 41 22.5

7-9 36 24 60 32.9

10-12 28 20 48 26.3 13 and above 7 5 12 6.5

Total 107 75 182 100

Estimated income

before loan

#10,000- #50,000. 76 49 125 68.7

#51,000- #100,000. 11 13 24 13.2

#101,000 - #150,000 14 9 23 12.6

#151,000- #200,000 6 4 10 5.5

Total 107 75 182 100

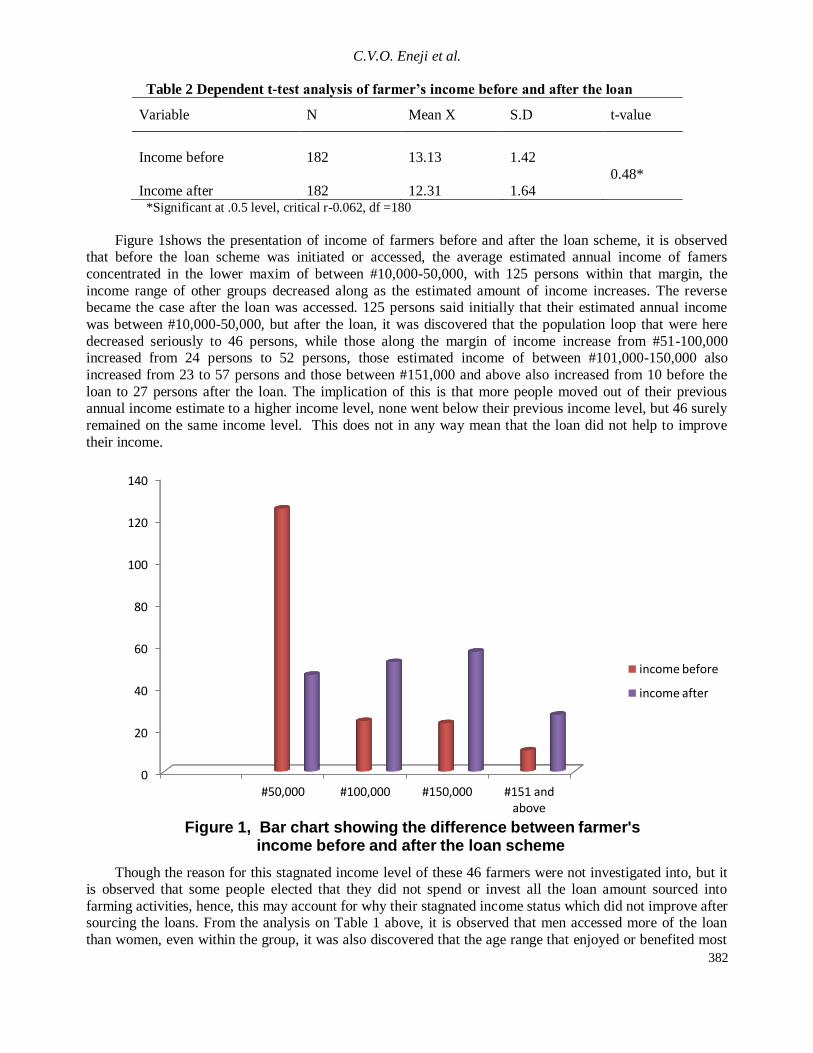

The result of the dependent t-test on table 2 shows that the calculated dependent t-test value is 0.48,

while the critical table value is .062. Since the calculated t-value is greater than the critical table value, the result is significant, hence the null hypothesis which stated that ‘’there is no significant difference in the

income of beneficiaries before and after the loan’’ is rejected while the alternate hypothesis which stated that

there is a significant difference between the income of famers before and after the loan is accepted. This therefore means that there is a significant difference in the income of farmers before and after the loan. The

implication from the analysis is that farmers income improved significantly after the loan than before the loan,

this therefore means that the loan was useful to the farmers since it increased their annual income turnover.

The figure below also shows the difference in farmer’s annual income before and after the loan.

C.V.O. Eneji et al.

382

Table 2 Dependent t-test analysis of farmer’s income before and after the loan

Variable N Mean X S.D t-value

Income before

182

13.13

1.42

0.48* Income after 182 12.31 1.64

*Significant at .0.5 level, critical r-0.062, df =180

Figure 1shows the presentation of income of farmers before and after the loan scheme, it is observed that before the loan scheme was initiated or accessed, the average estimated annual income of famers

concentrated in the lower maxim of between #10,000-50,000, with 125 persons within that margin, the

income range of other groups decreased along as the estimated amount of income increases. The reverse became the case after the loan was accessed. 125 persons said initially that their estimated annual income

was between #10,000-50,000, but after the loan, it was discovered that the population loop that were here

decreased seriously to 46 persons, while those along the margin of income increase from #51-100,000 increased from 24 persons to 52 persons, those estimated income of between #101,000-150,000 also

increased from 23 to 57 persons and those between #151,000 and above also increased from 10 before the

loan to 27 persons after the loan. The implication of this is that more people moved out of their previous annual income estimate to a higher income level, none went below their previous income level, but 46 surely

remained on the same income level. This does not in any way mean that the loan did not help to improve

their income.

Though the reason for this stagnated income level of these 46 farmers were not investigated into, but it is observed that some people elected that they did not spend or invest all the loan amount sourced into

farming activities, hence, this may account for why their stagnated income status which did not improve after sourcing the loans. From the analysis on Table 1 above, it is observed that men accessed more of the loan

than women, even within the group, it was also discovered that the age range that enjoyed or benefited most

0

20

40

60

80

100

120

140

#50,000 #100,000 #150,000 #151 and above

Figure 1, Bar chart showing the difference between farmer's income before and after the loan scheme

income before

income after

International Journal of Management Sciences

383

from the loan was the age bracket between 31-40 years of age with a population of about 93 respondents representing 51.3%. Though the loan was also accessed by people within other age brackets but the

implication is that those who benefited most are the youths. Hence the observation that their income improve

considerably within the period under study could be attributed to the extent of benefits derived from the loan

seen through an improvement on their annual household income.

In the distribution of the loans along marital status, married men and women accessed most of the loans,

about 95 respondents, (52.1%), followed by single 41, 22.5%. This also shows that the more the family type and the willingness of the heads or family head to feed his family, the more he pursues larger and increased

farming activities and the end product is improving the income of the farmers may be because these family

members use their children and wives as labor to do most of the farming activities in these farms. From the

analysis and discussion so far, there was a redistribution of income along the line of recipients with more having moved from lower income status to improved income status.

5. Conclusion

It is therefore concluded that there was an improvement in the income of farmers after the loan;

meaning the loan was useful to the farmers in this study, hence the loan was very beneficial to the farmers under study. Since the loan has contributed in improving the income of these farmers, it is advisable that the

volume, scope and frequency of the loan should be increased; this will enable these farmers access more of

the loan, thereby increasing the number of the loan recipients and the size of farm holdings thereby boasting an expanded food productivities and food security in Nigeria.

6. Recommendations

Micro-credit financing to small-scale farmers is a sure way of improving the lot of rural dwellers and

also the socio-economic life of the people. Financial institutions that lend funds should promote lending through viable cooperative groups offering repayment terms that are very convenient to the local farmers.

Agricultural micro-credit should be directed toward the rural, poor income groups since it has been

found to improve the capacity of poor rural farmers to manage, sustain their resources and increase the annual income of farmers. This loan granting system of giving to the farmers themselves

directly in the field has proven useful, since the system here marked a deviation from situations

whereby influential absentee farmers divert agricultural micro-credit facilities meant for the rural poor into non-agricultural uses.

Despite the findings that the loan amount was adequate, the volume of agricultural micro-credit to

these farmers was inadequate. It is thus, recommended that volumes of loan to farmers should be increased to be commensurate with the size of farms and household sizes too.

Loan administration by PFD through NGOs to cooperative groups has proved successful as the

study has shown. It is recommended that other lending institutions should focus on cooperative groups and if possible have intermediaries like the NGOs used by PFD to assist in monitoring and

supervision of benefiting farmers.

Although some modest achievements have been seen in agricultural micro-credit delivery to rural farmers of Benue State through the NGOs, much progress may not be made without a policy

backup to support, enforce and expand agricultural micro-credit. It is therefore recommended that

proper policies should be formulated in the state with a view to implementing favorable micro-finance delivery system to the rural-poor farmers.

Other organizations like the World Bank, Food and Agricultural Organization, UNICEF/UNESCO,

etc should also adopt the loan granting systems to enable rural small farmers improve their food security and income. It is believed that this will improve the socio-economic life of the farmers,

C.V.O. Eneji et al.

384

maintain infrastructure, improve projects and enhance establishment of small enterprise development programs. More agencies (national and international) should assist in providing loan

or credit to rural farmers in the state.

Financial institutions such as agricultural and community banks should be established in the rural areas. The procedures for securing loans should be reviewed in order to make it simple for the

farmers. The relevant government agencies should mobilize the rural farmers to form themselves

into formidable groups so that they can derive maximum benefit of collective Investment of group savings.

References

African Development Bank Food and Agricultural Organ (2003) Forestry Outlook Study for African Sub-

regional Reports West Africa, United Nation Publications.

Agburu, J. I (2001) Modern Research Methodology, Solid Paper Company, Makurdi pp 62.

Ajakaiye, M.B (1984) The Role of Bank in Financing Private Sector Investment in Nigeria Agricultural

Development. ARMTI Publication, Illorin, Nigeria pp 68.

Akramov, K.T (2009) Decentralization, agricultural services, and determinants of input use in Nigeria.

Discussion paper 941, Washington D.C International Food policy research Institute

Ayinde, O.E. and K. Ayinde, (2006) Analysis of risk in Cowpea Production in Kwara State, Nigeria: A Target-MOTAD Approach. Global J. Agric. Sci., 5 (1): 27-32.

Ayinde, O.E., (2008) Effect of Socio-Economic Factors on Risk Behaviour of Farming Households: An Empirical Evidence of Small-Scale Crop Producers in Kwara State, Nigeria, Agricultural Journal 3

(6): 447-453, 2008

Ayinde, O.E., M.O. Adewumi and O.A. Omotesho, (2004) Trade-off between expected returns and risk among farming household in Kwara State. Advanced Modeling Stimulation Enterprise Journal, 25

(4): 31-42.

Ayinde, O.E., O.A. Omotesho and K. Ayinde, (2005) Farm planning under risk and uncertainty: An application of TARGET-MOTAD Model. Centre Point. Sci. Edn., University of Ilorin, 13 (1): 11-23.

Bassey T. and O.S Coate (1995) Group Lending Repayment Incentives and Social Collateral in India. Australia J. Development & Economics 46(1): 30-32.

Chlorida, N.M. (1984). Focus on Financing of Small Farmers in the Nigerian Economy of Indo Nigeria

Merchant Bank, Nigeria Journal of financial management pg 106-117.

Community Development Foundation (2006) Manual of Financial and Credit Management, GRA Lagos.

Economic Commission for Africa (2001) Transforming Africa’s Economy. Economic Report on Africa 2000 Addis Ababa E.C.A 27-29.

Ezihe, J.A.C; Oboh, V.U and F.O. Ogebe (2007) The role of Nigerian Agricultural Cooperative and Rural

Development Bank in Financing of Poultry farming in Makurdi Metropolis, Benue State. In: U. Ibrahim, S.A Jibril, Y.P Mancha and N. Nasiru (Eds) Consolidation ofGrowth and Development of

Agricultural Sector. Proceedings of the 9th Annual National Conference of Nigerian Association of

Agricultural Economics (NAAE), 5th -8

th November, 2001, ATBU Bauchi, Nigeria. Pp 346-351

FAO and World Bank (2007) Farming Systems and Improving Farmers Livelihood. Rome and Washington

D.C: FAO and World Bank Report.

Ijere M.O. (1990) The Place of Co-operative in Nigeria Economy. Optimal Computer Solutions Enugu. Pp 45-54.

International Journal of Management Sciences

385

Imoudu, P.B. (2002) Agricultural Development Strategy-Institutional Framework. Workshop Paper, Ibadan NCEMA pp 16.

Johnson, D.T. (2007) The Business of Farming: A guide to Farm Business Management in the Tropics.

Macmillan Education Publishers London. Johnson, S. and Ben Rogaly (1997). Micro Finance and Poverty Reduction. Oxford Publication pp 134.

Mundi N.E and Tenere, V.A (2007) Identification of major sources of credit available to small-scale farmers

in Kogi State, Nigeria. In: U. Ibrahim, S.A Jibril, Y.P Mancha and N. Nasiru (Eds) Consolidation of Growth and Development of Agricultural Sector. Proceedings of the 9

th Annual National Conference

of Nigerian Association of Agricultural Economics (NAAE), 5th -8

th November, 2001, ATBU

Bauchi, Nigeria. Pp 283-287

NACRDB (2001) Situation Report: Holder of Small-scale Loan Scheme. Alphabet Publishers Ltd, Kaduna.

Pp 6.

NPC (2006) National Population Commission. Abuja, Nigeria

Okorie, A. (1987) The Agricultural Credit Guarantee Scheme Fund Credit Administration in Nigeria:

Problems and Prospects. In Okorie A. and M.O Ijere (eds) Readings in Agricultural Finance. A production of Faculty of Agriculture, University of Nigeria Nsukka. Pp 159-160.

Olutayo, I.B (2009) Poverty and income diversification among households in rural Nigeria: A Gender

Analysis of livelihood. A paper presented at the 2nd

Instituto de Estudos Sociais e Economics (IESE) Conference on “Dynamics of poverty and patterns of Economic Accumulation in Mozambique.” 22-

23 April, 2009

Oruonye, E.D and Musa, Y.N (2012) Challenges of small scale farmers access to micro-credit (Bada Kaka) in Gassol LGA, Taraba State, Nigeria. Journal of Agricultural Economics and Development. Vol

1(3) pp 62-68

Partners for Development (2002) Improving the Effectiveness of Micro Finance Operation Workshop Manual, PFD Makurdi.

Related Documents