Lincoln University Digital Thesis Copyright Statement The digital copy of this thesis is protected by the Copyright Act 1994 (New Zealand). This thesis may be consulted by you, provided you comply with the provisions of the Act and the following conditions of use: you will use the copy only for the purposes of research or private study you will recognise the author's right to be identified as the author of the thesis and due acknowledgement will be made to the author where appropriate you will obtain the author's permission before publishing any material from the thesis.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Lincoln University Digital Thesis

Copyright Statement

The digital copy of this thesis is protected by the Copyright Act 1994 (New Zealand).

This thesis may be consulted by you, provided you comply with the provisions of the Act and the following conditions of use:

you will use the copy only for the purposes of research or private study you will recognise the author's right to be identified as the author of the thesis and

due acknowledgement will be made to the author where appropriate you will obtain the author's permission before publishing any material from the

thesis.

Non-Financial Information Disclosures and Firm Risk

A thesis

submitted in partial fulfilment

of the requirements for the Degree of

Doctor of Philosophy

at

Lincoln University

by

Muhammad Arif

Lincoln University

2020

I dedicate this work to my daughter Amsah, parents, wife, siblings,

friends, colleagues and all the teachers who supported and

encouraged me to reach this point in my life

i

Abstract of a thesis submitted in partial fulfilment of the requirements for the Degree of Doctor of Philosophy

Non-Financial Information Disclosures and Firm Risk

By

Muhammad Arif

Abstract

Recently, world leaders and organisations have realised the seriousness of unsustainable

production practices, ethical misconduct and governance failures by businesses that have

caused severe environmental hazards, employees’ and customers’ rights violations and

financial fraud. As a result, there have been increasing calls by regulators and stakeholders,

including firms’ shareholders, to improve the quantity and quality of information disclosures

vis-à-vis a firm’s business operations, financial transactions, governance structures, work

ethics, environmental and social ramifications. Besides, organisational theories such as the

agency, stakeholder and legitimacy theories highlight the importance of a transparent

information environment in mitigating concerns such as agency conflicts and legitimacy

issues.

Generally, firms use conventional financial statements and reports that offer limited

information about the firm’s activities. However, more recently, firms started to supplement

conventional financial statements with non-financial information (NFI) that encompasses

information related to their policies and activities for a sustainable environment, societal

well-being, work ethics and governance. This additional disclosure provides opportunities to

explore the impact of additional such information disclosure on a firm’s information

environment, future performance and risk.

Recognizing this opportunity and the knowledge gap in the literature, this study uses the S&P

1200 index firms’ environmental, social and governance (ESG) disclosures for 2008-2018 to

investigate their contribution to reducing the uncertainty surrounding firms’ future earnings.

The results show that ESG disclosures have a significant negative impact on earnings risk,

ii

signifying that the additional disclosures relating to ESG issues reduce the uncertainty

surrounding firms’ future earnings risk. The disaggregated analysis of ESG disclosure scores

shows a more pronounced effect of the social and environmental dimensions on earnings risk.

The results are robust to various sub-sample analyses and endogeneity controls.

This study also explores how sensitive industry status augments the extent of a firm’s NFI

disclosures as well as the association between NFI disclosures and earnings risk. The results

show that sensitive industry firms make higher NFI disclosures and, as a result, have a lower

earnings risk than non-sensitive industry firms. This study provides novel evidence concerning

the causal impact of the European Union’s NFI reporting regulations on the level of ESG

disclosures of regulated firms and the changes in NFI disclosures and earnings risk association

after the mandating NFI reporting. The results show that the mandatory NFI reporting regime

has not only increased the extent of NFI disclosures for European firms, but has also improved

the efficiency of NFI disclosures in alleviating the uncertainty surrounding the future earnings

of the sample firms.

Our findings provide important implications for corporate managers, stakeholders and

regulators. Specifically, the findings suggest that corporate managers can alleviate agency

conflicts and legitimacy issues by reporting information regarding firms’ policies and efforts

to manage ESG issues. Our finding regarding the efficiency of the EU directive to increase the

quantity of NFI disclosures further suggests that regulators from other parts of the world

should shift towards mandatory NFI reporting. We propose that mandatory NFI regimes

would improve the adoption of sustainable business practices that are necessary to achieve

long-term targets such as sustainable development and the Paris Agreement’s targets.

Keywords: Non-financial information disclosures, earnings risk, sensitive industries, non-

financial reporting regulations, directive 2014/95/EU

iii

Table of Contents

Abstract ……………………………………………………………………………………………………………………………….i

Table of Contents ...................................................................................................................... iii

List of Tables ............................................................................................................................. vi

List of Figure ............................................................................................................................. vii

Acknowledgements ................................................................................................................. viii

Chapter 1 Introduction………………………………………………………………………………………………………..1

1.1. Introduction ............................................................................................................................ 1

1.2. Knowledge Gaps...................................................................................................................... 5

1.3. Research Questions ................................................................................................................ 6

1.4. Purpose of the Research ......................................................................................................... 7

1.5. Significance of the Research ................................................................................................... 8

1.6. Research Findings ................................................................................................................. 10

1.7. Organisation of the Thesis .................................................................................................... 11

Chapter 2 Literature Review .................................................................................................. 13

2.1. Introduction .......................................................................................................................... 13

2.2. Theoretical Foundations ....................................................................................................... 14

2.2.1. Agency Theory ............................................................................................................... 15

2.2.2. Legitimacy Theory ......................................................................................................... 16

2.2.3. Stakeholder Theory ....................................................................................................... 18

2.3. Definition Evolution of Non-financial Information ............................................................... 19

2.3.1. Institutional contribution to the definition evolution of Non-financial Information ..... 20

2.4. Evolution of Non-financial Information Reporting Research ................................................ 22

2.4.1. Initial studies on the measurement of NFI information disclosures .............................. 22

2.4.2. The development of improved NFI disclosure databases .............................................. 23

2.5. Empirical Studies on the Impact of NFI Disclosures .............................................................. 24

2.5.1. NFI disclosures and the firm performance link .............................................................. 25

2.5.2. The NFI and information asymmetry link ...................................................................... 25

2.5.3. NFI disclosures and the firm risk link ............................................................................. 27

2.5.4. The linkage between NFI disclosures and firms’ earnings risk (the case of sensitive

industry firms) ............................................................................................................................... 30

2.6. NFI Disclosures Regulations .................................................................................................. 32

iv

2.6.1. NFI disclosures regulations in Europe Directive 2014/95/EU ........................................ 33

2.6.2. The consequences of the NFI disclosure regulations ..................................................... 34

2.7. Chapter Summary ................................................................................................................. 36

Chapter 3 Sample, Data and Methodology ............................................................................ 38

3.1. Introduction ......................................................................................................................... 38

3.2. Sample .................................................................................................................................. 38

3.3. Dependent and Independent Variables ................................................................................ 40

3.3.1. Analysts’ earnings forecasts dispersion – earnings risk relationship ............................ 40

3.3.2. Non-Financial Information disclosures .......................................................................... 41

3.3.3. Sensitive industries ........................................................................................................ 42

3.3.4. Non-Financial Information disclosure regulations ........................................................ 42

3.4. Control Variables ................................................................................................................... 43

3.4.1. Firm size ........................................................................................................................ 43

3.4.2. The number of analysts following a firm ...................................................................... 44

3.4.3. Financial leverage ......................................................................................................... 44

3.4.4. Loss ................................................................................................................................ 45

3.4.5. Earnings volatility .......................................................................................................... 45

3.4.6. Financial opaqueness .................................................................................................... 45

3.4.7. Firm growth ................................................................................................................... 46

3.4.8. Firm profitability ........................................................................................................... 46

3.4.9. Industry and index dummies ......................................................................................... 46

3.5. Basic Diagnostic Test ............................................................................................................. 47

3.5.1. Pairwise correlation ...................................................................................................... 48

3.6. Regression models ................................................................................................................ 48

3.7. Robustness and Endogeneity ................................................................................................ 52

3.8. Chapter Summary ................................................................................................................. 53

Chapter 4 Results and Discussion ........................................................................................... 54

4.1. Introduction .......................................................................................................................... 54

4.2. Descriptive Statistics ............................................................................................................. 54

4.3. Diagnostics Test .................................................................................................................... 57

4.3.1. Pairwise correlation analysis ............................................................................................... 57

4.4. The Impact of NFI Disclosures on Earnings Risk .................................................................... 61

4.4.1. Baseline results ................................................................................................................... 61

4.4.2. NFI quartile results .............................................................................................................. 64

4.4.3. Subsample analysis ............................................................................................................. 67

v

4.4.4. Robustness tests .................................................................................................................. 70

4.5. Sensitive Industries Analysis ................................................................................................ 77

4.5.1. Level of NFI disclosure: Sensitive v/s non-sensitive industry firms ...................................... 78

4.5.2 NFI disclosures and future earnings risk: Sensitive versus non-sensitive industry firms ...... 81

4.5.3 NFI disclosures and future earnings risk: Interaction approach........................................... 82

4.6. Chapter Summary ................................................................................................................. 85

Chapter 5 Mandatory NFI Disclosures and Firm Risk ......................................................... 87

5.1. Introduction ......................................................................................................................... 87

5.2. The European Union’s NFI Directive 2014/95/EU ................................................................ 87

5.3. The Impact of Directive 2014/95/EU on NFI Disclosures ...................................................... 88

5.4. The Impact of the EU Directive on Future Earnings Risk ...................................................... 93

5.5. Chapter Summary ................................................................................................................ 97

Chapter 6 Summary and Conclusions ................................................................................ 99

6.1. Introduction ......................................................................................................................... 99

6.2. Research Background and Objectives ................................................................................... 99

6.3. Study Sample, Data and Empirical Models ........................................................................ 100

6.4. Summary of Findings ........................................................................................................... 100

6.4.1. NFI disclosures and earnings risk ...................................................................................... 101

6.4.2. Sensitive industries and NFI disclosures ............................................................................ 102

6.4.3. NFI disclosures and earnings risk (sensitive vs non-sensitive industry firms) ................... 102

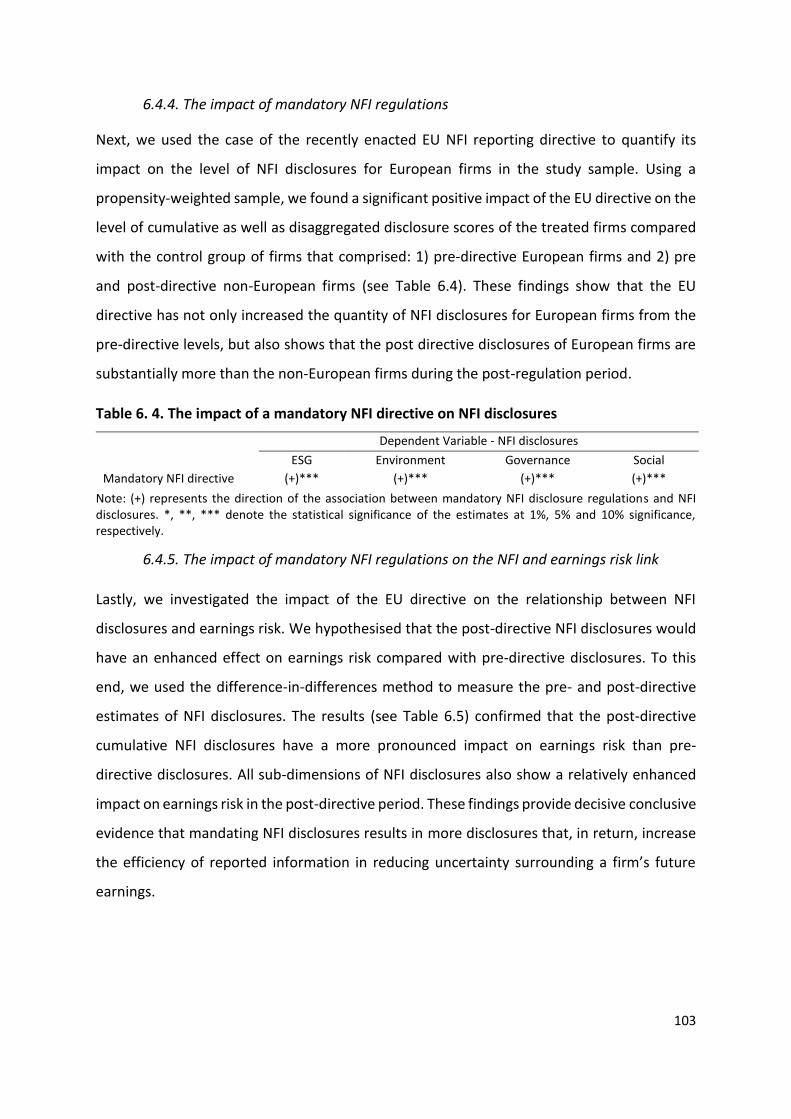

6.4.4. The impact of mandatory NFI regulations ........................................................................ 103

6.4.5. The impact of mandatory NFI regulations on the NFI and earnings risk link .................... 103

6.5. Practical and Policy implications ......................................................................................... 104

6.5.1. Implications for corporate managers................................................................................ 104

6.5.2. Implications for firm stakeholders .................................................................................... 104

6.5.3. Implications for regulators ................................................................................................ 105

6.6. Research Contribution ........................................................................................................ 106

6.7. Research Limitations ........................................................................................................... 107

6.8. Future Research ................................................................................................................. 108

Appendix A ............................................................................................................................. 109

Appendix B ............................................................................................................................. 115

Appendix C ............................................................................................................................. 117

References ………………………………………………………………………………………………………………………139

vi

List of Tables

Table 3. 1. Index and industry-wide companies that comprise the study sample ............................... 39

Table 3. 2. A summary of the study variables and expected signs ....................................................... 47

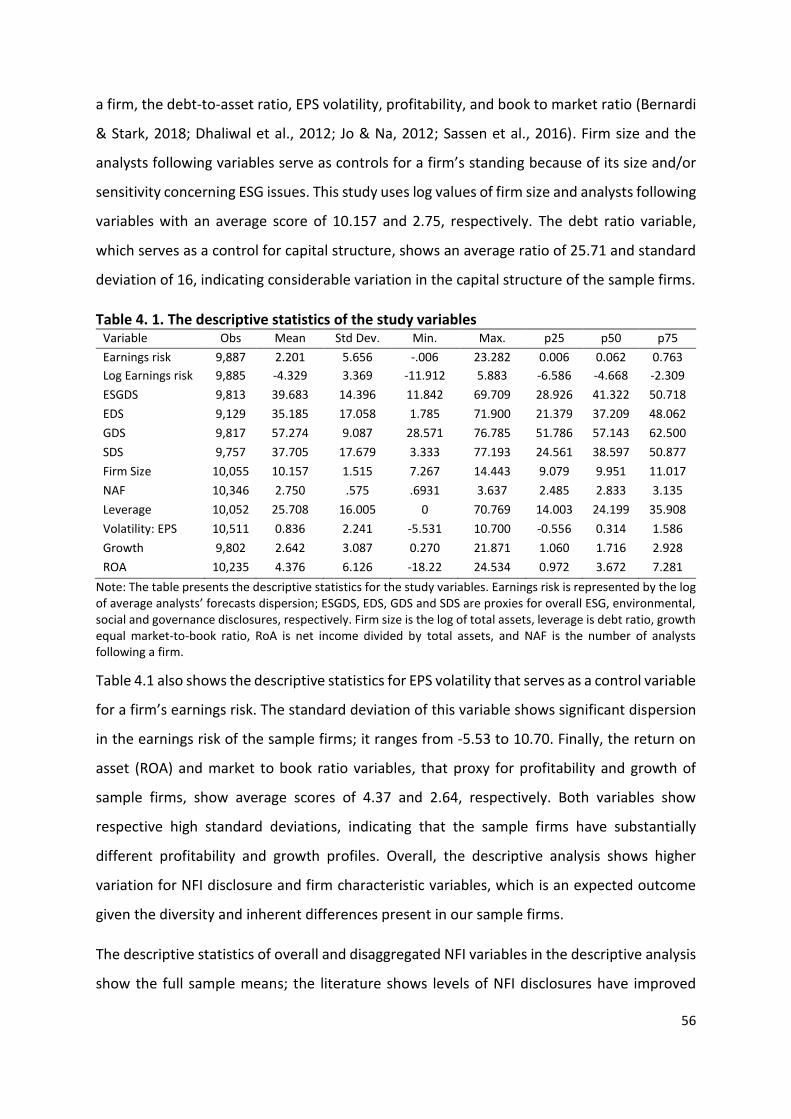

Table 4. 1. The descriptive statistics of the study variables ................................................................. 56

Table 4. 2. Pairwise correlation matrix of the study variables ............................................................. 60

Table 4. 3. The impact of NFI disclosures on firms’ earnings risk ......................................................... 62

Table 4. 4. The impact of NFI disclosure quartiles on firms’ earnings risk ........................................... 66

Table 4. 5. The impact of NFI disclosures on stock return volatility ..................................................... 70

Table 4. 6. The impact of NFI disclosures on firms’ earnings risk (Alternative proxies) ....................... 71

Table 4. 7. The impact of NFI disclosures on firms’ earnings risk (Alternative proxies) ....................... 72

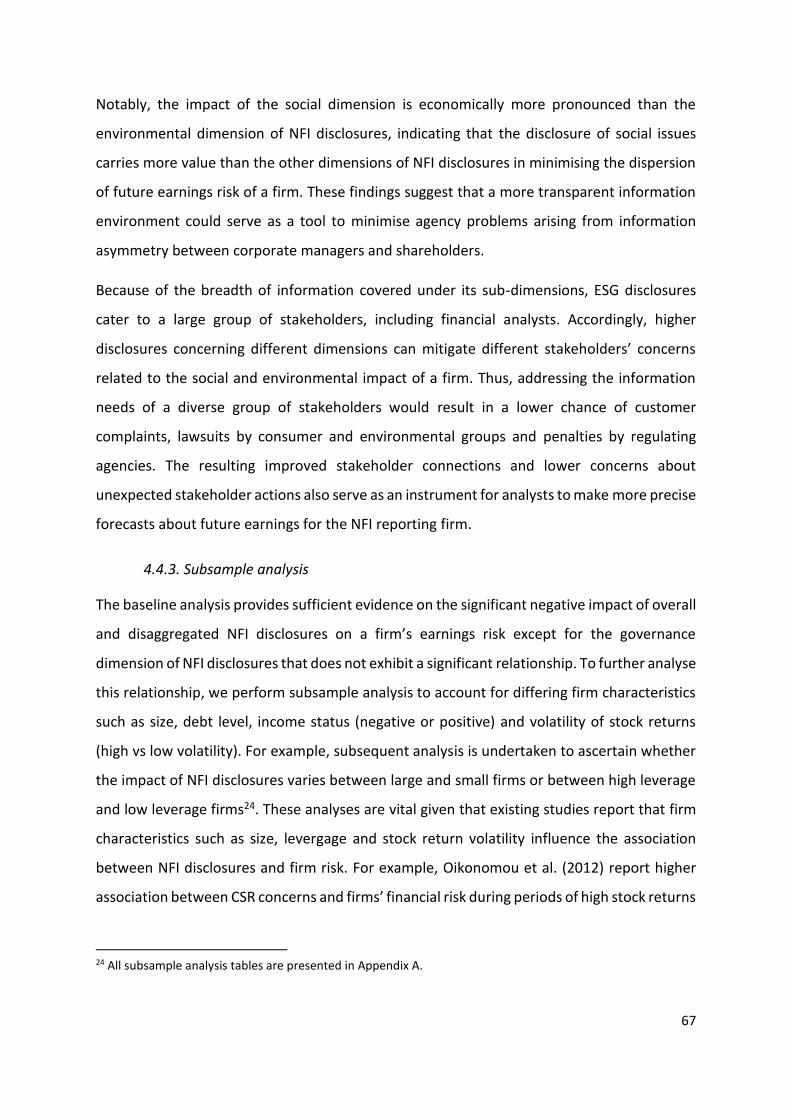

Table 4. 8. The impact of NFI disclosure on firms’ earnings risk (Lagged variables) ............................ 74

Table 4. 9. The impact of NFI disclosure on firms’ earnings risk (System GMM estimator) ................. 76

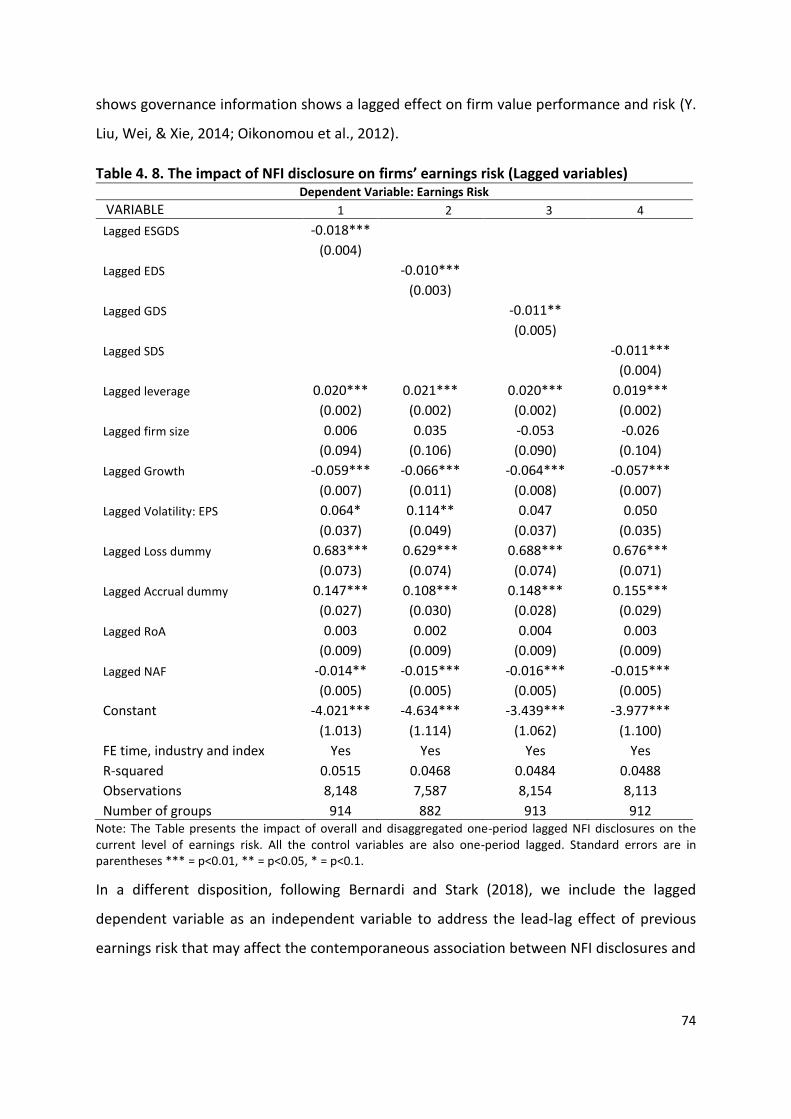

Table 4. 10. Balance table of ES statistic comparison ........................................................................... 80

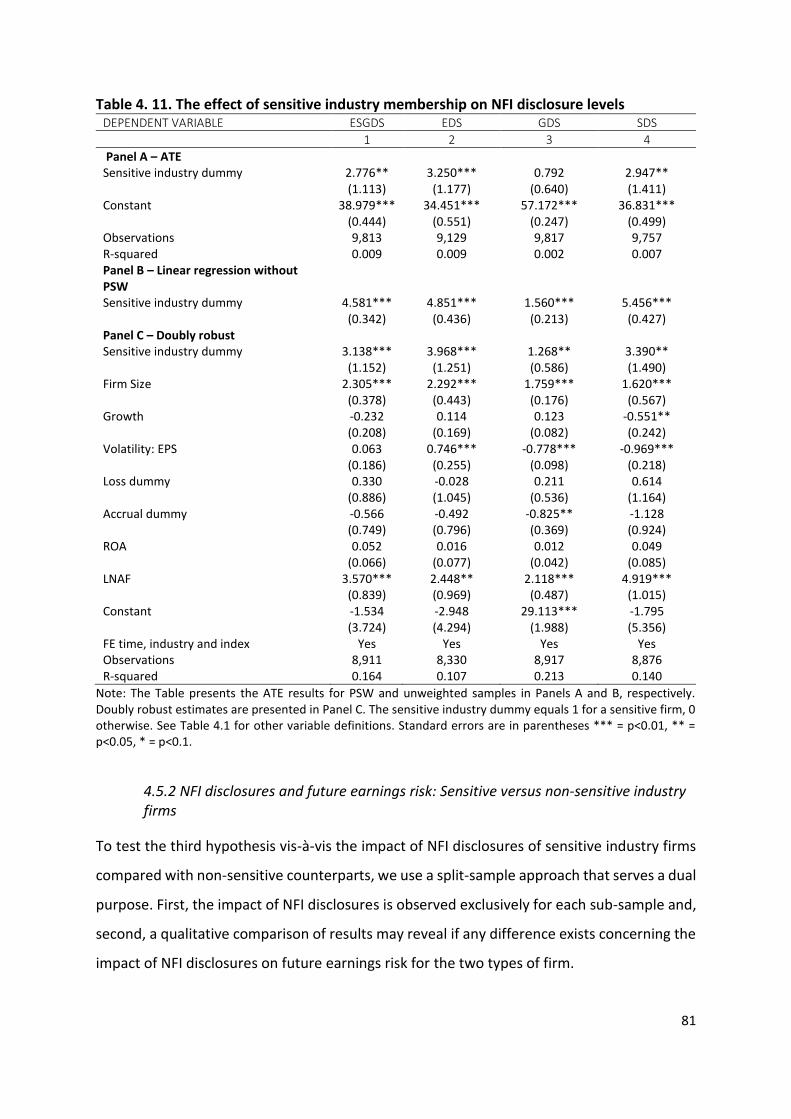

Table 4. 11. The effect of sensitive industry membership on NFI disclosure levels ............................. 81

Table 4. 12. The impact of NFI disclosures on firms’ earnings risk – Split sample approach ............... 83

Table 4. 13. The impact of NFI disclosures on firms’ earnings risk – Interaction approach ................. 84

Table 5. 1. The balance table of ES statistics ........................................................................................ 90

Table 5. 2. The impact of the EU directive on NFI disclosures .............................................................. 92

Table 5. 3. The impact of NFI disclosures on firms’ earnings risk (pre and post EU directive) ............. 95

Table 5. 4. The impact of NFI disclosures on firms’ earnings risk (Australian sample) ......................... 96

Table A.1. The Hausman test estimates of the study variables .......................................................... 109

Table A.2. The impact of NFI disclosures on firms’ earnings risk ....................................................... 110

Table A.3. The impact of NFI disclosures on firms’ earnings risk ....................................................... 111

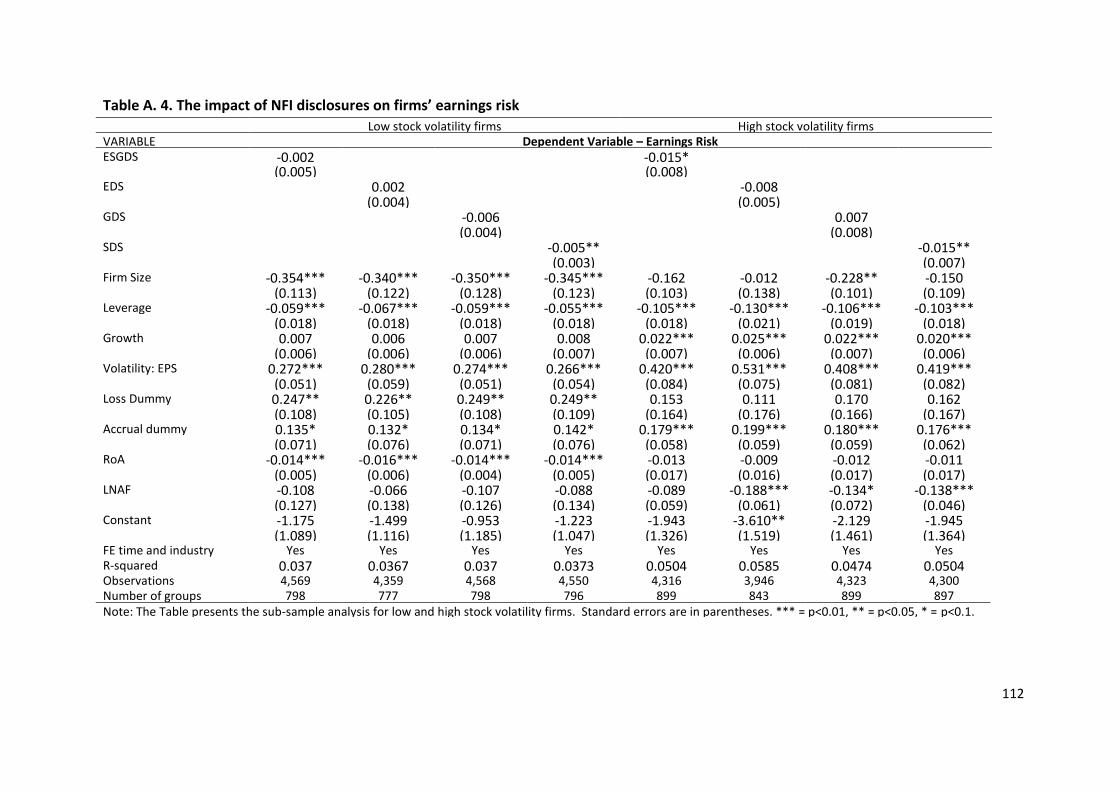

Table A. 4. The impact of NFI disclosures on firms’ earnings risk ....................................................... 112

Table A.5. The impact of NFI disclosures on firms’ earnings risk ....................................................... 113

Table A.6. The impact of NFI disclosures on firms’ earnings risk (non-financial firms) ..................... 114

vii

List of Figure

Figure 4.1. Evolution of NFI disclosures ................................................................................................ 57

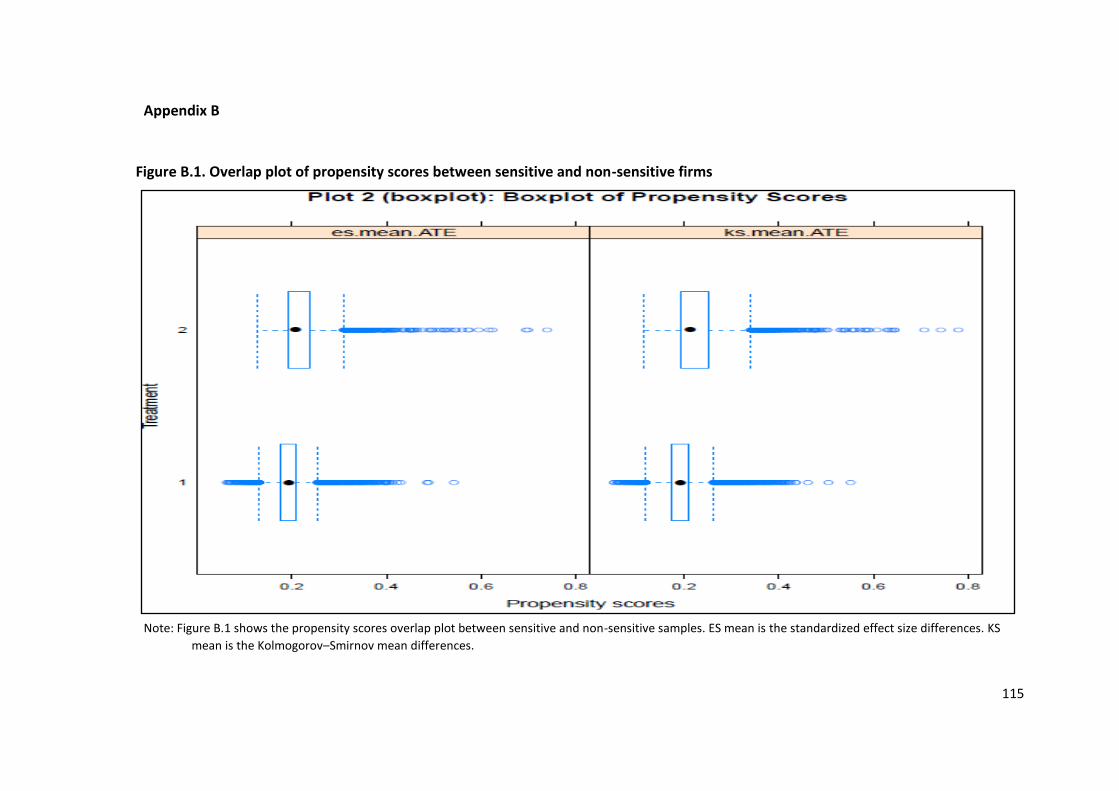

Figure B.1. Overlap plot of propensity scores between sensitive and non-sensitive firms ................ 115

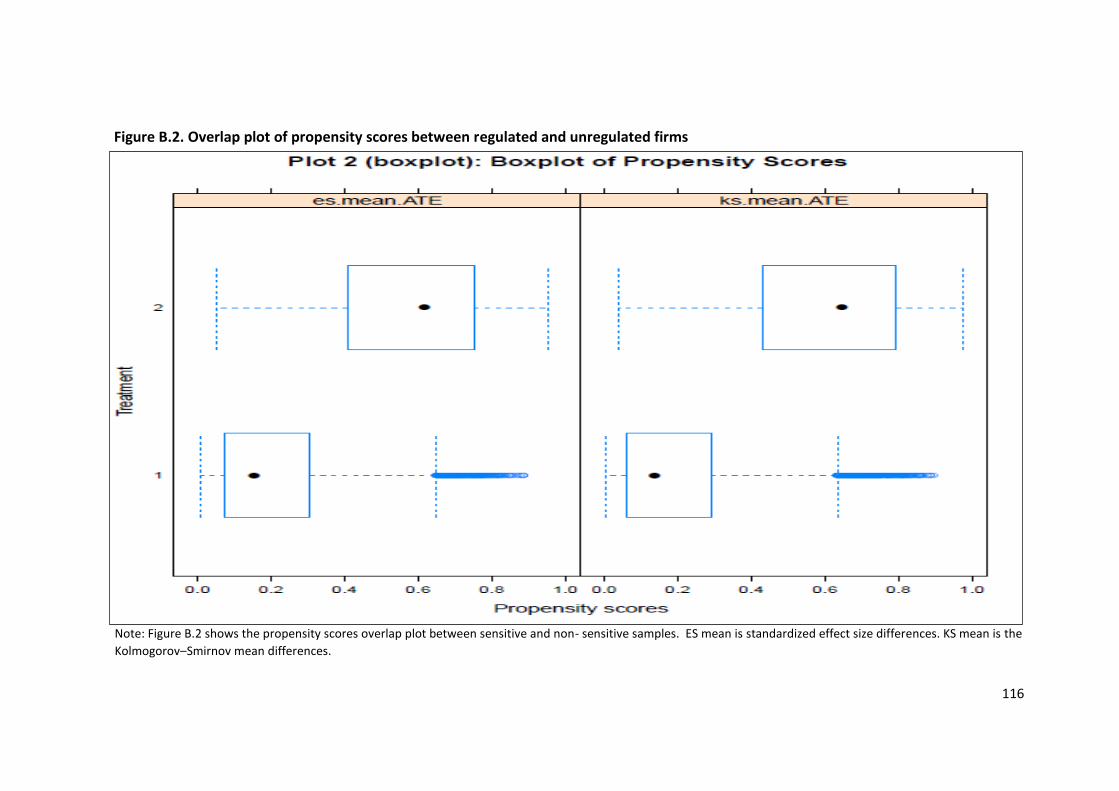

Figure B.2. Overlap plot of propensity scores between regulated and unregulated firms ................ 116

viii

Acknowledgements

All the praises and thanks be to Allah Almighty, Who guided me and gave me the strength to

complete my PhD studies. May the peace and blessing of Allah Almighty be upon Muhammad

(peace be upon him), who is the perfect mentor.

Firstl, I express my utmost gratitude to Prof. Christopher Gan for his guidance, support and

motivation throughout this journey. He did not only guide and support me to complete the

PhD thesis but also provided many opportunities to learn and grow in the academic field. He

has always been a source of motivation and inspiration throughout my time at Lincoln

University. I would also sincerely thank my asscociate supervisor, Dr Muhammad Nadeem

(Senior Lecture at Otago Business School, Otago University), for his valuable guidance and

contribution to my PhD research thesis.

I thank my employer Shaheed Benazir Bhutto University (SBBU), Shaheed Benazirabad,

Pakistan, and the Higher Education Commission, Pakistan, for the provision of funds for my

PhD studies without which this journey would not have been possible. Notably, I thank Mr

Najam Ud din Sohu, Akhtar Hussain Mangi and Qurban Farooqi for their continuous support

during my PhD tenure at Lincoln University. I would also like to thank Nicos Tescos who

ensured my employment at Lincoln University.

The completion of my PhD studies and my stay in New Zealand would not have been possible

without continuous support from my family, especially my parents, wife, siblings and in-laws.

They have always encouraged and supported me during this time. I pay special thanks to my

father and mentor, Muhammad Ramzan. He has always been a source of inspiration and

motivation to achieve higher standards of education throughout my life.

I also thank all my friends who supported me to this point in my life. Notably, my sincere

gratitude goes to Mudassar Hasan, Abu Bakr Naeem, Aon Waqas, Javed Ali, Rashid Waheed,

Sanaullah, Raheel Khan, Tauseef Khan Babar and Mabruk Billah for their support and guidance

throughout my life. Lastly but most importantly, I extend sincere gratitude to all my teachers

and alma maters. They nurtured my skills and abilities to achieve the ultimate goal in my

academic career, the completion of my PhD studies.

1

Chapter 1

Introduction

1.1. Introduction

Today’s world is overloaded with an abundance of information and there has never been

more demand for data. Similarly, businesses are increasingly required to report information

related to all aspects of their operations and activities. Requests for such information not only

come from the firms’ shareholders but also other stakeholders such as suppliers, regulators,

NGOs and creditors, who demand information about firms’ business processes, products,

policies and impacts on society (Camilleri, 2015).

Stakeholders, including the firms’ shareholders, seek information to make informed

decisions. For example, shareholders and creditors make investment decisions; suppliers

make decisions to conduct business with a firm and customers make purchase decisions. All

these stakeholders need information to make the best decisions and narrow the information

gap between themselves and corporate managers, better known as the information

asymmetry problem in the finance literature (Bhattacharya & Singh, 2018; Cui, Jo, & Na, 2018;

Easley & O'hara, 2004).

To satisfy their stakholders’ information needs, historically, firms have provided information

mainly on their financial matters using conventional financial statements such as the

statement of financial position, income statement and statement of stakeholders’ equity.

However, these statements mainly cater to the information needs of stakeholders with a

financial interest in the firm, i.e., shareholders and creditors. The information needs of

stakeholders seeking data about a firm’s policies and activities for a sustainable environment,

society well-being, work ethics and governance issues, remain unnswered (Bozzolan, Favotto,

& Ricceri, 2003; Manes-Rossi, Tiron-Tudor, Nicolò, & Zanellato, 2018).

As a result, corporate managers started to report more information in their business

communications to cater for the needs of the broad range of stakeholders. This information

is mainly non-financial and includes details of a firm’s policies and practices concerning

governance, environmental sustainability, society, and employees (Burgman, Roos, Boldt-

Christmas, & Pike, 2007; Cortesi & Vena, 2019; Felber, Campos, & Sanchis, 2019). Firms use

2

several reports and statements to make non-financial information (NFI) disclosures. The most

common statements are: corporate social responsibility (CSR) reports, statements of the code

of ethics and conduct, statements from the senior decision-maker (CEO, President),

statements of corporate intent, corporate governance reports, and, more recently, integrated

reports. Some of the NFI disclosure reports such as CSR and sustainability reports are used

interchangeably in this study.

Historically, NFI disclosures have had a long journey, starting with the concept of social

responsibility (Bowen, 1953) and stakeholder concerns (Davis, 1960). Sethi (1975)

emphasised the need to link social responsibility with corporate strategy and actions.

Progressively, Carroll (1979) provided a detailed framework of corporate social performance

consisting of four stages of customer social responsibility (CSR) development: economic, legal,

ethical, and philanthropic obligations. These ground-breaking studies laid the foundations for

issues that business managers should address in their corporate communications. There has

been a steady increase in NFI disclosures and many third party organisations have started to

develop NFI databases1 that measure the extent of corporate disclosures and performance in

the areas of environmental, social, economic and governance issues. Given the availability of

comprehensive NFI databases, NFI disclosures are also available in disaggregated components

as environmental, social and governance (ESG) disclosures.

Although there has been a recent noteworthy increase in the quantity and quality of NFI

reporting (Arvidsson, 2011; Coluccia, Fontana, & Solimene, 2016; Jain, Keneley, & Thomson,

2015; Sethi, Martell, & Demir, 2017) around the world, these disclosures have been largely

voluntary (Hoffmann, Dietsche, & Hobelsberger, 2018; Muslu, Mutlu, Radhakrishnan, &

Tsang, 2019). Because of their voluntary nature and a lack of accounting standards and

frameworks, the format and content of NFI disclosures have generally been unstandardized

and inconsistent (Demir & Min, 2019; Muslu et al., 2019; Sethi et al., 2017). Additionally, rapid

growth and changes in the content and methodology of sustainability reporting tools

complicate the use of NFI disclosures for organisational stakeholders (Siew, 2015).

Consequently, there has been a lack of interest from academics, analysts and practitioners

1 Kinder, Lydenberg and Domini (KLD), Thomson Reuters ESG, Refinitiv ESG, Bloomberg ESG database and others.

3

about using the information content of these statements and reports in their efforts to

comprehend organisations’ NFI disclosures and their quality.

Nevertheless, after the establishment of international standards and organisations such as

ISO 26000, the Global Reporting Initiative (GRI), Sustainability Accounting Standards Board

(SASB) and the International Integrated Reporting Council (IIRC), firms now have more

knowledge and better guidance available to develop their NFI disclosures. Therefore,

organisations adopting the improved reporting frameworks produce standardised, coherent

NFI disclosures that are useful to measure the quantity and quality of NFI reporting across a

large variety of organisations (Bhattacharyya & Yang, 2019; Crisóstomo, de Azevedo

Prudêncio, & Forte, 2017; Demir & Min, 2019). Additionally, countries and economic regions2

are enacting NFI disclosure regulations and developing reporting frameworks to provide

consistent, mandatory guidelines for firms’ NFI disclosures. These regulations3 mainly target

achieving sustainable, accountable, responsible and transparent business practice targets set

by relevant governments, the United Nations’ sustainable development goals (SDGs), and the

United Nations Paris Climate Change Agreement (Nations, 2015).

In this vein, (Directives, 2014) enacted by the European Parliament, provides a detailed

framework for mandatory NFI reporting by large4 organisations and required all member

states to adopt the framework by the end of 2016. This directive amends the non-mandatory

Directive 2013/34/EU and Regulation (EC) No 562/2006 that were in place in the EU for

disclosure of NFI. This recent directive requires firms to report information on six broad

topics: 1) environmental, 2) social, 3) employee matters, 4) respect for human rights, 5) anti-

corruption, and 6) bribery matters, as the minimum mandatory requirement of NFI

disclosures. Firms are also required to report how their business model, policies, policy

outcomes, potential risks and key performance indicators (KPIs) synchronise with the six

broad topics in NFI disclosures.

2 An economic region is a group of countries that have geographical proximity and share similar economic and

financial patterns and regulations e,g,. ASEAN, the EU, South Asian Association for Regional Cooperation

(SAARC). 3 NFI reporting is a stock exchange listing requirement in Malaysia and South Africa. China and Denmark made ESG

reporting mandatory for large organisations in 2008 and 2009, respectively. 4 Companies with a total balance sheet, net turnover and average number of employees over EUR 400,000, EUR

800,000 and 500, respectively.

4

Significant developments in the reporting and regulatory frameworks provide opportunities

to explore the impact of NFI disclosure regulations on the quantity and quality of corporate

NFI disclosures. Notably, the recent NFI reporting regulation by the EU is vital for two reasons.

First, it has to be adopted by all EU member countries, so it has considerable implications in

its scope. Secondly, it affects some of the largest corporations in the world.

The literature also reports the impact of NFI reporting regulations on the extent of NFI

disclosures and how such regulations affect firm risk and value. For example, Ioannou and

Serafeim (2017) report increased ESG disclosures following the enforcement of mandatory

NFI disclosure regulations in China, Denmark, Malaysia, and South Africa. They also report an

increase in firm value for reporting firms. Similarly, using South Africa’s integrated reporting

regulation, Bernardi and Stark (2018) report an increased level of ESG disclosures that, in turn,

results in increased analysts’ forecast accuracy. These findings show NFI regulations not only

increase the level of CSR disclosures, but also moderate the link between CSR disclosures and

information asymmetry and firm value. Given the recent NFI regulation enacted by the

European parliament in 2014, it is pertinent to investigate how the enforcement of this

regulation affects the disclosure practices of the regulated organisations.

Potential improvements in the quality of NFI disclosures under a mandatory reporting regime

can serve as a channel to reduce information asymmetry among a range of stakeholders. The

improved quality of disclosed information serves as a legitimacy enhancing tool and offers

potential benefits. For example, using South Africa’s mandated integrated reporting case, Lee

and Yeo (2016) suggest that integrated reporting mitigates the information asymmetry

among managers and creditors. It serves as a tool for enhancing firm value. Similarly, Bernardi

and Stark (2018) report an increase in analysts’ earnings forecast accuracy after the

mandating of integrated reporting in South Africa. Their results suggest that the mandated

disclosure regime prompted higher quality of information disclosures, resulting in reduced

information asymmetry among financial analysts. Therefore, it is important to explore

whether improved disclosure helps regulated organisations to reduce their risk.

In a broader context, the literature reports a significant negative relationship between NFI

disclosures and firm risk. Prior studies use standard measures of firm risk such as cost of

capital, bid-ask spread, idiosyncratic risk, systematic risk and analysts’ forecasts. Studies on

5

the relationship between NFI disclosure and analysts’ forecasts dispersion provide evidence

of a significant negative relationship (Bouslah, Kryzanowski, & M’Zali, 2013; Chien & Lu, 2015;

Dhaliwal, Li, Tsang, & Yang, 2011; Jo & Na, 2012; Kothari, Li, & Short, 2009). Some studies use

analysts’ forecasts dispersion as a measure of information asymmetry (Dhaliwal,

Radhakrishnan, Tsang, & Yang, 2012; Schulz, 2017) and others as a measure of risk (Chien &

Lu, 2015; Kothari et al., 2009) because of different underlying assumptions. Nevertheless,

Barron, Stanford, and Yu (2009) reconcile the contradictory evidence of analysts forecasts

dispersion as a measure of information asymmetry or uncertainty. They conclude that the

dispersion level of analysts’ forecasts represents uncertainty, which is negatively associated

with firms’ future stock returns. Consequently, we apply this explanation to use analysts’

forecasts dispersion as a measure a firm’s future earnings risk. We maintain that analysts’

forecasts dispersion is a better measure for analysing the complexity of a firm’s information

environment than traditional risk proxies such as systematic, idiosyncratic and total risk.

1.2. Knowledge Gaps

The availability of comprehensive NFI disclosure datasets and their division into

environmental, social and governance components provides promising avenues to

understand which dimensions of NFI disclosures are most valued by the market participants

such as financial analysts, investors and regulators. Therefore, it is worthwhile to investigate

how the total and different dimensions of NFI disclosures affect an organisation’s information

environment and influence its future earnings’ risk. This enquiry becomes more important for

firms operating in sensitive industries5. Given the environmental and social sensitivity of their

operations, firms in sensitive industries face stringent scrutiny from stakeholders to keep their

communications transparent and provide all the relevant information to stakeholders (Emma

& Jennifer, 2021; Sethi, Martell, & Demir, 2016; Yusoff, Yusoff, Abd Rahman, & Darus, 2019).

Previous empirical studies on NFI disclosure and the firm risk relationship report economically

valuable, statistically significant findings for a diverse collection of samples and periods. For

example, (see Benlemlih et al., 2018; Oikonomou, Brooks and Pavelin, 2012; Sassen, Hinze

and Hardeck, 2016). However, to the best of our knowledge, no previous study explores the

5 Following Baron et al. (2011) and Garcia et al. (2017), we treat a firm as a sensitive industry firm if it belongs to

the alcohol, tobacco, gambling, weapon production, adult entertainment, oil, gas, and consumable fuels, metals

and mining, paper and forest products, chemicals, construction materials, or energy businesses.

6

disaggregated6 effect of NFI disclosures on earnings risk. The literature is also silent on the

impact of NFI disclosures on earnings risk for sensitive industries, i.e., industries that need to

make higher NFI disclosures to maintain the legitimacy of their operations.

Because of increasing pressure from stakeholders and regulators, NFI disclosures are shifting

from voluntary to mandatory. This change in the status of NFI disclosures has significant

implications for corporate disclosure policies. Prior studies report the effect of NFI regulation

on the extent of a firm’s disclosures and its mediating impact on firm value (Ioannou &

Serafeim, 2017) and analysts’ forecasts accuracy (Bernardi & Stark, 2018) at country level.

Similarly, recent NFI regulations in the EU provide a unique opportunity to examine the effect

of mandatory NFI regulations on the magnitude of firms’ disclosures at a regional level. It is

also worthwhile investigating the mediating impact of mandatory NFI reporting regulations

on firms’ earnings risk and the NFI disclosure relationship.

1.3. Research Questions

Based on the research gaps identified from the literature review, this study aims to address

the following research questions:

i. What is the impact of cumulative and disaggregated NFI disclosure scores on the

earnings risk for S&P1200 index firms?

ii. What is the impact of sensitive industry status on the level of overall and

disaggregated NFI disclosures for S&P1200 index firms?

iii. Does the impact of total and disaggregated NFI disclosure scores on earning risk vary

between sensitive and non-sensitive industry firms included in the S&P 1200 index?

iv. How did the enforcement of mandatory NFI disclosure requirements change the

degree of NFI disclosures at the total and disaggregated levels for S&P 350 EU index

firms?

v. Did the enforcement of mandatory NFI disclosure requirements strengthen the

relationship between NFI disclosure and earnings risk for S&P 350 EU index firms?

6 NFI disclosures are commonly disaggregated into environmental, social and governance (ESG) components.

7

1.4. Purpose of the Research

As discussed earlier, organisations increasingly make NFI disclosures to provide much-needed

information to market participants so they can make informed decisions. Using NFI

disclosures, organisations aim to send positive signals to stakeholders and market participants

to enhance organisational legitimacy (Ochi, 2018). The purpose of these signals is two-fold;

first, these signals improve firms’ legitimacy. Secondly, they improve firms’ information

environment, which results in better forecasts of their future earnings.

To test this idea, this study first explores the nature and magnitude of NFI disclosures’ impact

on future earnings risk for S&P1200 index companies. The proxy for NFI disclosure is ESG

disclosure scores reported in the Bloomberg ESG database and the proposed proxy for

earnings risk is analysts’ earnings forecasts dispersion. We adopt Barron et al. (2009)

definition to measure the dispersion of analysts’ earnings forecast for a firm, which represents

a firm’s earnings risk. This study also explores the impact of individual components of ESG,

environmental, social and governance disclosures, on earnings risk. The disaggregated

analysis aims to ascertain whether different categories of ESG disclosure have varying

importance in improving a firm’s information environment.

Secondly, this study aims to measure the impact of sensitive industry status on firms NFI

disclosures and the resulting impact of NFI disclosure scores on firm risk for sensitive industry

firms. We aim to confirm and extend the evidence in the literature that sensitive industry

firms make higher NFI disclosures because of higher environmental and social risk exposure

(Du & Vieira, 2012; Garcia, Mendes-Da-Silva, & Orsato, 2017; Kilian & Hennigs, 2014; Vollero,

Conte, Siano, & Covucci, 2019). Following (Baron, Harjoto, & Jo, 2011; Garcia et al., 2017), we

treat a firm as a sensitive firm if it belongs to the alcohol, tobacco, gambling, weapon

production, adult entertainment, oil, gas, and consumable fuels, metal and mining, paper and

forest products, chemicals, construction materials, or energy businesses.

Thirdly, this study explores the impact of NFI reporting regulations on the quantity of firms’

NFI disclosures. To test this relationship, we use the recent NFI disclosure regulations enacted

by the European parliament as an exogenous shock for the disclosure practices of

organisations domiciled in the EU. Lastly, this study investigates the changes in the

relationship between earnings risk and NFI disclosures after the enforcement of mandatory

8

disclosure regulations. To that end, this study uses difference in differences (DID) analysis to

investigate the enforcement impact of NFI reporting regulations on the relationship between

NFI disclosures and earnings risk for European firms. For the DID method, the treatment group

includes constituents of the S&P Europe 350 Index, which is a sub-index of the S&P Global

1200 Index. We include S&P Europe 350 index companies in the treatment group as the

(Directives, 2014) applies only to companies domiciled in the EU. The other companies in the

S&P Global 1200 Index constitute the control group.

1.5. Significance of the Research

Recently, business organisations have not only faced increased pressure from legislators and

international standards organisations to include NFI disclosures in their corporate

communications, but investors and professional fund managers also assign a higher weight to

NFI disclosures in their investment decisions. A 2018 report7 documents professionally

managed investments of US$20 trillion are tied exclusively to socially responsible investment

(SRI) funds, which have increased from $7.6 trillion in 2010, a growth of 163% in just eight

years. Similarly, signatories to the United Nations-backed Principles of Responsible

Investments (UNPRI) have increased from 850 to 1600. McKinsey and Company (2002) reveal

that investors are willing to pay an average of a 25% premium for rightly governed company

shares. Additionally, consumers are willing to pay higher prices for eco-friendly products

(Fanasch & Frick, 2020; Mostafa, 2016). These findings suggest that socially responsible

investments are gaining momentum so investors and other stakeholders will assign a higher

weight to firms’ NFI disclosures in making investment decisions and assessing financial

performance and risk. Consequently, firms will improve their NFI disclosures to attract more

socially responsible investors and also avoid information the information asymmetry problem

between different stakeholder groups.

However, given the nature of the information and the lack of homogeneous reporting

frameworks, the use of broader NFI disclosure proxies such as stand-alone sustainability/CSR

reports is not a suitable approach. Thus, comprehensive, well-developed NFI disclosure

proxies are required to capture the real effect of NFI disclosures on firms’ earnings risk.

7 Report on US Sustainable, Responsible and Impact Investing Trends

https://www.ussif.org/files/Trends/Trends%202018%20executive%20summary%20FINAL.pdf

9

Consequently, this study uses the Bloomberg ESG disclosure score as a proxy of a firm’s NFI

disclosures. The Bloomberg ESG database provides data for over 11,500 companies across 70

countries. Bloomberg analysts construct ESG disclosure scores by using an over 900 data field

across a variety of NFI indicators, such as air quality, water and energy management, human

capital, waste management, compensation, diversity, shareholders rights. Bloomberg uses

company reported data from CSR reports, annual reports, company websites and other

company sources to maintain accuracy and consistency in their database8.

Given the depth and breadth of data used, Bloomberg ESG disclosure scores serve as a better

proxy than broader proxies of NFI disclosures such as stand-alone CSR reports, and inclusion

in sustainability indices. Additionally, the availability of individual scores for the ESG

dimensions is useful to measure the disaggregated impact of each component of ESG

disclosures on a firm’s risk. The disaggregated analysis will help to identify which aspects of

ESG disclosures drive the association between firm risk and NFI disclosures.

This study uses analysts’ earnings forecasts dispersion as a proxy for a firm’s earnings risk. We

use this proxy for two reasons. First, the accuracy of analysts’ earnings forecasts for a firm

mainly depends on the availability of public information. Secondly, this proxy better captures

the risk inherent in the information environment of a firm compared with conventional risk

proxies such as stock return volatility, systemic risk and idiosyncratic risk.

The arguments presented above suggest the use of precise, well developed NFI disclosures

and firm risk proxies to capture true nature and magnitude of the relationship between firm

risk and NFI disclosures. To the best of our knowledge, no prior study provides categorical

evidence of a relationship between firm risk and NFI disclosures at the international level.

Hence, this study’s results promise to add new insights to existing NFI disclosure literature.

Further, the use of analysts’ forecasts dispersion as an earnings risk proxy is a novel, valuable

contribution to the current knowledge concerning the effects of NFI disclosures on firms’ risk

profile. This study also presents evidence about sensitive industry firms that face stringent

scrutiny because of the nature of their business.

8 https://data.bloomberglp.com/professional/sites/10/1148330431.pdf

10

This study’s findings provide useful suggestions for corporate managers and decision makers

about reducing the uncertainty surrounding future earnings of a firm through the information

channel. This study’s results can potentially be used to mitigate agency problems and

legitimacy issues that are critical for modern firms, especially sensitive industry ones.

Addressing the agency and legitimacy issues have become essential because of ever-

increasing governance and sustainability issues, stakeholder pressures and shifting investors’

preferences towards socially responsible investment. Thus, this study is a timely enquiry to

answer pressing questions that corporate managers face regarding their efforts to minimise

the adverse environmental and social effects of business operations and practices.

Prior studies, e.g., (Schulz, 2017; Siew, Balatbat, & Carmichael, 2016), investigating the

relationship between information asymmetry and firm risk indicate the need for the

enactment and enforcement of mandatory NFI disclosure regulations to improve timeliness

and standardisation of NFI disclosures. Those studies also suggest standardisation and

timeliness of NFI disclosures would enhance analysts’ information processing efficiency.

Given the importance of NFI regulations, this study investigates the impact of mandatory NFI

regulations on the extent of NFI disclosures and determines the changes in the relationship

between firms’ earnings risk and NFI disclosures after the enforcement of such regulations.

Importantly, this study investigates the impact of the NFI regulations enacted by the EU. This

regulation provides the opportunity to investigate the impact of NFI reporting regulations at

a regional level. Exploring the impact of mandatory NFI regulations at a regional level is a

valuable contribution to the literature since current evidence is limited to country-level

(Bernardi & Stark, 2018; Ioannou & Serafeim, 2017) regulations. To the best of our knowledge,

this is the first study that attempts to ascertain the impact of a legislative change in this

research area at an international level.

1.6. Research Findings

This study’s results reveal important insights regarding the relationship between NFI

disclosures and firms’ earnings risk. First, this study shows that cumulative and disaggregated

NFI disclosures exhibit a strong negative impact on firms’ earnings risk. Notably, the social

and environmental dimensions of NFI disclosures exhibit negative impact on firms’ earnings

risk. However, governance disclosures do not reduce earnings risk for our sample firms. The

11

quartile-based analysis reveals that higher quartiles of overall and disaggregated NFI

disclosures have a more substantial negative impact than lower quartiles. These results are

robust for alternative measures of firm risk and firm characteristics, sub-sample analyses, and

endogeneity problems.

Second, using a propensity score weighted sample, this study shows that sensitive industry

firms report higher overall and disaggregated NFI disclosures than non-sensitive firms. This

difference is more pronounced for the environmental and social dimensions. Using the

interaction term and split-sample approaches, this study confirms that the disclosure of

environmental information provides more benefit to sensitive industry firms in reducing

earnings risk than for non-sensitive industry firms. Governance disclosures benefit non-

sensitive industry firms only with regard to reducing uncertainty surrounding future earnings.

This study offers significant evidence that sensitive industry firms may increase the legitimacy

of their operations and reduce earnings risk by improving their NFI disclosures, especially the

disclosure of environmental information.

Finally, this study uses a recently enacted EU NFI reporting directive to quantify its impact on

the NFI disclosures level and the resulting impact on the earnings risk of European firms in

the study sample. Using a propensity weighted sample, this study finds a significant positive

impact of the EU directive on the level of cumulative and disaggregated disclosure scores of

the treated firms compared with the control group firms. The difference-in-differences

analysis results confirm that the post-directive cumulative and disaggregated NFI disclosures

have a more pronounced impact on earnings risk than pre-directive disclosures. These

findings provide decisive evidence to conclude that mandating NFI disclosures results in

higher disclosures that in turn, increase the efficiency of reported information in reducing

uncertainty surrounding a firm’s future earnings.

1.7. Organisation of the Thesis

The rest of the thesis is as follows: Chapter 2 presents a literature review related to NFI

disclosures, the theoretical foundations of NFI disclosures, the relationship between NFI

disclosures and firm risk. The literature on the impact of NFI disclosure regulations on the

degree of disclosures and firm risk is discussed. Chapter 3 discusses the data collection,

measurement of data variables and the study’s research methodology. Chapter 4 separately

12

presents the descriptive and empirical results on the impact of NFI disclosures on firm risk for

the S&P 1200 companies and sensitive industries firms. Chapter 5 presents the evidence on

the impact of NFI disclosure regulations on the degree of NFI disclosures and the mediating

impact on the firm earnings risk and NFI disclosures relationship. Chapter 6 discusses the

policy and market implications of the findings and concludes the thesis. Finally, the study’s

limitations and future directions for NFI disclosures research are discussed.

13

Chapter 2

Literature Review

2.1. Introduction

Business organisations have long been recognised for their influential role in economic, social

and legal systems around the world. As a result, the activities and operations of business

entities come under scrutiny from different stakeholders such as shareholders, creditors,

government agencies and non-governmental organizations (NGOs). Additionally, because of

increasing stakeholder demands, media pressure and consumer awareness, firms now face

immense pressures to be more transparent, sustainable and ethical in their communications

regarding their business practices and operations. Therefore, to legitimise their actions and

meet the information needs of the stakeholders, businesses publish information related to

their policies, operations and business outcomes. Traditionally, the information content of

corporate communications has been investor and creditor centric; mostly financial. However,

because of increased awareness and concerns about social, environmental and governance

issues among stakeholders, firms have started to integrate NFI disclosures in their

communications. NFI disclosures contain information about business policies, processes,

work ethics, concern for employees, and contribution to environment and society, i.e., mostly

non-financial information.

Although businesses have started to make more NFI disclosures, these disclosures have been

mostly voluntary and unstandardized. Given the voluntary nature of non-financial

information and the lack of reporting standards, the content and presentation of such

information have been very diverse and inconsistent (Demir & Min, 2019; Muslu et al., 2019;

Sethi et al., 2017). However, there have been enormous developments such as establishment

NFI reporting frameworks, e.g., the global reporting initiative (GRI), the International

Integrated Reporting Council (IIRC), and the Sustainability Accounting Standards Board (SASB)

frameworks. The evolution of mandatory NFI reporting regulations in different countries has

changed and improved the quantity and quality of NFI disclosures over the years.

Given the broad nature of information covered under NFI disclosures, the literature on this

topic uses a variety of terms to characterize seemingly similar information. Therefore, terms

like corporate social responsibility (CSR), environmental, social and governance (ESG), and

14

sustainability disclosures are used interchangeably. Similarly, there are various reports that

firms use to report NFI disclosures such as CSR reports, sustainability reports, statement of

the code of ethics and conduct, the statement from senior decision-maker (CEO, President),

statement of corporate intent, corporate governance reports, and, more recently, integrated

reports. As NFI disclosures contain diverse information, more recently, data providers9,

practitioners and academics have started to divide NFI disclosures into three broad

categories: environmental, social and governance disclosures to empirically measure the

effect of NFI disclosures on the various factors of firm profitability and risk.

Although studies on NFI disclosures and their implications entail a very diverse, detailed

knowledge base in the finance and accounting literature, the following sections review the

literature that is most relevant to this study’s scope. The review starts from the theoretical

foundations that conceptualize the needs and consequences of NFI disclosures and follows

the historical development of definitional constructs and NFI reporting. The subsequent

sections present the literature regarding the impact of NFI disclosures on firm performance,

information asymmetry and firm risk. The last section discusses the literature on the

developments of NFI disclosure regulations and their impact and mediating effect on the

extent of disclosures, firm value and information asymmetry.

2.2. Theoretical Foundations

Given the far-reaching effect of NFI disclosures, there are several motivations for a firm to

disclose NFI in its corporate communications. Prior studies use several theories to address the

issue of the social responsibilities of firms and identify sources that require firms to be more

transparent in their business conduct and information disclosures. For example, using the

well-known agency cost framework (Borghei, Leung, & Guthrie, 2018; Garcia et al., 2017)

provides evidence of reduced information asymmetry for firms with improved ESG related

disclosures. These studies show NFI disclosures help firms resolve the information asymmetry

problem that has multiple adverse effects on the organization-stakeholder relationship. For

example, information asymmetry could result in lower investor confidence, mispricing of firm

value and higher cost of capital.

9 Bloomberg ESG database, MSCI ESG research, Refinitiv ESG score and others.

15

Studies also provide evidence of comparatively higher ESG related disclosures from

sensitive/controversial industry firms (Gamerschlag, Möller, & Verbeeten, 2011; Garcia et al.,

2017). These authors maintain that sensitive industry firms go through strict scrutiny by

stakeholders so they make higher ESG disclosures to maintain the legitimacy of their business

operation. The literature on NFI disclosures identifies three main theories that fundamentally

identify the motives and grounds for managers to disclose NFI. These theories are: 1) the

Agency Theory; 2) the Legitimacy Theory; and 3) the Stakeholder Theory.

2.2.1. Agency Theory

Jensen and Meckling (1976) define the agency relationship as “a contract under which one or

more persons (the principal(s)) engage another person (the agent) to perform some service

on their behalf which involves delegating some decision making authority to the agent. If both

parties to the relationship are utility maximisers there is a good reason to believe that the

agent will not always act in the best interests of the principal” (p. 5). They also introduce the

concept of agency cost as a combination of three elements: “1) the monitoring expenditures

by the principal; 2) the bonding expenditures by the agent; and 3) the residual loss” (p.5).

They define “residual loss” as the decrease in the market value of a firm arising from a poor

agency relationship between principals and agents. On the other hand, the conflict of interest

between principals and agents generates an information gap, because the agents, being in-

charge of the business, possess first-hand information about the firm and principals depend

on agents to get access to this information. Principals not only pay incentives to the agents to

align their objectives with them but also provide more incentives to keep the information gap

as small as possible (Shapiro, 2005). These foundational works on agency theory provide the

rationale for NFI disclosures by corporate managers to align principal-agent objectives and

reduce agency costs via a reduction in information asymmetry.

Many researchers have used agency theory to conceptualize the relationship between NFI

disclosures and information asymmetry, firm performance and risk. For example, Borghei et

al. (2018) maintain that corporate managers make extra efforts to disclose more NFI to

resolve agency problems arising from information asymmetry. They report a decrease in

information asymmetry following carbon disclosures for non-greenhouse gas registered

companies in Australia. Similarly, (Garcia et al., 2017; Ness & Mirza, 1991) find a reduction in

16

information asymmetry because of the adoption of integrated reporting. Jo and Harjoto

(2012) reject the “CSR over-investment” argument of agency theory since they find a positive

relationship between firms’ CSR and financial performance. They argue that disclosure of CSR

information plays an important role in increasing a firm’s financial performance. Further, ESG

disclosure transparency increases firm value through the information asymmetry and agency

cost reduction channel (Yu, Guo, & Luu, 2018). Looking from the lense of agency theory, Velte

(2020) report a two-way association between institutional shareholders and corporate ESG

disclosures.

Studies also report that NFI disclosures are more prevalent in economies that promote higher

levels of stakeholder protection. For example, Martínez‐Ferrero, Ruiz‐Cano, and García‐

Sánchez (2016) report that additional, voluntary NFI disclosures can help reduce agency

problems. They also suggest that environments with a higher social responsibility

commitment reduce agency conflict by increased voluntary disclosures. Conversely,

Kartadjumena and Rodgers (2019) report a negative impact of climate and environmental

reporting by managers on financial performance and market value of Indonesian banks. They

argue that banking firms in Indonesia are practising sustainability reporting as an altruistic

rather than a strategic motive. Recognizing the importance of NFI disclosures in risk

optimization for shareholders, this study uses agency theory concepts to ascertain a reduction

in the agency problem as a result of lower future earnings risk.

2.2.2. Legitimacy Theory

Legitimacy theory considers business organizations as part of a larger social system, hence

firms are required to abide by the social and ethical norms of the society where they operate.

A comprehensive, straightforward definition of legitimacy theory is given by (Kaplan &

Ruland, 1991) as “organizational legitimacy is a process, legitimation, by which an

organization seeks approval (or avoidance of sanction) from groups in society” (p. 370).

Legitimacy theory comprehends organizational efforts to be more transparent and provide

additional information as a way to legitimize firms’ existence in society and avoid adverse

outcomes of their operations and actions. Additionally, organizations pursue business

legitimacy objectives to abide by the social contract that they have with society. These social

contracts can be macro- or micro-social contracts as explained by the integrative social

17

contract theory. According to (Donaldson & Dunfee, 1999), macrosocial contracts are hyper

norms that are acceptable at the level of society as a whole like anti-bribery policies,

employees’ rights protection, and sustainable use of natural resources. Microsocial contracts

are specific to a particular society or culture like religious and cultural sensitivities. For

example, multinational organizations operating in Muslim countries cannot use an obscene

advertisement to promote their products. With macrosocial contracts, organizations make

more NFI disclosures as a result of regulations introduced by governments and international

standard organizations to maintain and enhance their legitimacy (Arena, Liong, & Vourvachis,

2018; Bernardi & Stark, 2018).

Similarly, firms operating in countries that promote higher levels of stakeholder protection,

make more environmental and social disclosures to meet the socially acceptable standards of

business conduct (Martínez‐Ferrero et al., 2016). Additionally, to establish legitimacy and

maintain a balance between corporate objectives, firms carefully trade-off between voluntary

and mandatory corporate disclosures. For instance, Fallan and Fallan (2019) maintain that

firms make a trade-off between corporate tax behaviour and environmental performance

disclosures. Although both are essential elements of NFI disclosures, they cater to the needs

of different stakeholders and have different reporting requirements. Hence, firms must

decide an optimum focus level on such elements to maintain legitimacy from the perspectives

of different stakeholders. These social contracts are influenced by organizational

characteristics. For example, large firms are considered more liable to practice socially

acceptable practices because of their more significant impact on society. Similarly, firms

working in the natural resources sector are considered more accountable to practice

sustainable business practices than other firms.

Prior studies report the influence of firms’ characteristics on their legitimacy seeking

behaviour. For example, Reverte (2009) reports firms’ media exposure, size and industry to

be the main determinants of their CSR disclosures. Hence, the author claims disclosures of

NFI as legitimacy seeking behaviour. Similarly, Khan, Muttakin, and Siddiqui (2013) find

corporate governance indicators, such as foreign ownership, board independence, and

presence of an audit committee, as major determinants of CSR disclosures that strengthen

the view of the corporate legitimacy theory. Firms operating in environmentally sensitive

18

and/or socially controversial industries face more scrutiny from society. Hence, they need to

make more significant NFI disclosures to maintain their legitimacy. Consequently, several

studies report evidence of higher NFI disclosures for sensitive industry firms compared with

other industry firms, e.g., (Gamerschlag et al., 2011; Garcia et al., 2017).

Overall, firms have to make careful choices when deciding the level of NFI disclosures because

the nature and importance of NFI disclosure elements differ significantly and proper

understanding of such differences is required to establish legitimacy. This study uses the

legitimacy concept to understand how firms use different dimensions of NFI disclosures to

address changing stakeholder information needs and regulatory pressures, which can

enhance organizational legitimacy measured by the transparency of the information

environment.

2.2.3. Stakeholder Theory

The seminal work Strategic Management: A Stakeholder Approach (Freeman, 1984) lays the

foundations of stakeholder theory. In more recent work, Freeman (2010) defines

stakeholders as: “any group or individual that can affect or be affected by the realization of

the organization’s purpose” (p. 26). According to his definition, stakeholders consist of a

variety of individuals and groups that might be internal to a firm like employees and

shareholders or external like suppliers, customers, competitors and governments. These

individuals and groups seek information related to firms’ processes and performance to make

informed decisions. Hence, firms disclose additional information to meet the informational

needs of their stakeholders and so reduce any potential information asymmetry between

different stakeholders (Garcia et al., 2017).

Though large amounts of NFI disclosures are voluntary; stakeholder theory provides the

perspecptive for firms’ voluntary disclosures. Mukherjee and Nuñez (2019) maintain that

firms make voluntary disclosures alongside mandatory disclosures to address the concerns of

the diverse group of stakeholders. Firms also make voluntary disclosures to meet the

demands of different pressure groups such as environmental and climate change

organizations. Stakeholder-oriented countries and regions increase stakeholder bargaining

power and force firms to make voluntary disclosures. As a result, studies report a higher level

19

of NFI in stakeholder-oriented countries than in their counterparts (García-Sánchez, Suárez-

Fernández, & Martínez-Ferrero, 2019; Landi & Sciarelli, 2019).

The stakeholder theory justifies increased information disclosures by corporation managers

(Ullmann, 1985). Ratnatunga & Jones (2012) describe the practicality of stakeholder theory

to justify the motivations of corporate managers to disclose additional information. Branco

and Rodrigues (2007) state that firms’ NFI (CSR) disclosures should be capable of addressing

firms’ contributions to satisfy the long-run needs of their stakeholders and convey the efforts

undertaken by a firm to minimise their social and environmental concerns. In other words, to

satisfy stakeholders’ information needs and address concerns about environmental and social

impacts of a firm, NFI disclosures are the most suitable approach that managers can use

(Huang & Kung, 2010).

A financial analyst is an important stakeholder of firms. Financial analysts use company

reported information with market information to forecast firms’ future earnings and market

price. Studies show NFI disclosures could improve (reduce) the accuracy (dispersion) of

analysts earnings forecasts (Bernardi & Stark, 2018; Dhaliwal, Radhakrishnan, Tsang, & Yang,

2012). Other studies also show analysts forecast accuracy is value relevant (Wei & Xue, 2015)

and cost-effective (Park & Park, 2019) for investors. This study uses stakeholder theory to test

whether higher NFI disclosures improve the accuracy of analysts’ earnings forecasts that

ultimately relate to lower earnings risk for firms. The precision of analysts earnings forecasts

for a firm may influence many other stakeholders such as investors, creditors and suppliers

since these stakeholders use analysts’ forecasts to make decisions about firms.

2.3. Definition Evolution of Non-financial Information

The idea of businesses being responsible towards society and the demands to include non-

financial information in corporate disclosures dates back more than a half-century when H. R.

Bowen (1953) introduced the concept of social responsibility (SR) in his book Social

Responsibilities of the Businessman. He proposed an initial definition of social responsibility

for businesses as: “It refers to the obligations of businessmen to pursue those policies, to

make those decisions, or to follow those lines of action which are desirable in terms of the

objectives and values of our society” (p. 6). Davis (1960) presents the managerial perspective

of socially responsible behaviour and argues that a socially responsible stance by a firm could

20

bear fruit in the long-run. Davis also argues that because of the possession of resources,

organizations have social power and, to avoid gradual erosion of this power, it should be

coupled with social responsibility (pp. 70-73).

Though the initial definition of CSR pointed towards the responsibility of businesses towards

society as a whole, Johnson (1971), for the first time, presented CSR from the stakeholder’s

perspective. He states that organizations should not only be concerned about the wealth

maximisation of their stockholders but also consider the interests of employees, suppliers,

dealers and the local community (p. 50). Sethi (1975) introduced the progressive concept of

corporate social performance (CSP) by linking CSR with a company’s strategy and actions. The

author argues that organizations must be socially responsive rather than just being merely

socially obliging. Taking things further, Carroll (1979) defines CSR as a process consisting of

four stages of CSR development: economic, legal, ethical, and philanthropic obligations.

In the early 1980s, Peter Drucker gave a new dimension to the CSR concept by emphasizing

the idea of compatibility between firms’ responsibilities and business opportunities (Drucker,

1984). Following Drucker’s work, several studies have focussed on the marketing aspect of

CSR, such as cause-related marketing, social sponsorship, environmental marketing,

communicating with consumers concerning CSR issues and corporate reputation (Barone,

Miyazaki, & Taylor, 2000; Brown & Dacin, 1997; Caruana & Crane, 2008; Crouch, 2006;

Handelman & Arnold, 1999; Varadarajan & Menon, 1988; Wagner, Lutz, & Weitz, 2009).

From the early 1980s onwards, there has been less focus on the development of a CSR

definition. Instead, researchers and practitioners started to focus more on the measurement

of CSR disclosures and how such disclosures can affect different aspects of firms’ business.

Wang (2015) describes the period 1980-1989 as the exploration stage of CSR development,

where researchers started to explore the content of CSR information reported in firms’

communications and ascertain the impact of such information on the financial performance

of the reporting firms.

2.3.1. Institutional contribution to the definition evolution of Non-financial

Information

Apart from individual researchers who contributed to the evolution of CSR definitions and

frameworks, various institutions have played a vital role in developing CSR frameworks for

21

the firms to understand their social responsibilities and understand how to incorporate such

information in their communications. In 1971, the Committee for Economic Development

(CED) presented a broader view of CSR based on the reasoning that the social contract

between business and society is changing very substantially. The CED framework for CSR

includes three circles of responsibility for business entities: the inner circle of responsibility

asks the firms to be responsible for their economics functions such as production, economic

growth, and shareholder wealth maximisation. The intermediate circle relates to social

responsibility towards the environment, employees’ relationships and the provision of

accurate information about products and processes to customers. Finally, the outer circle

covers the broader role of the firms, such as the well-being of society and improving the social

environment (CED, 1971). Manne and Wallich (1972) in a debate organized by the American

Enterprise Institute expressed the view that firms’ acts of responsibility should be considered

socially responsible only when it is done purely for the benefit of society or any stakeholder

group, and it is not bound by any legal obligations.

In the aftermath of Exxon Valdez oil spill10, environmental protection groups and socially

responsible investment (SRI) funds pushed for more NFI disclosures. Several social investment

professionals formed the Coalition for Environmentally Responsible Economies (CERES). In

1989, CERES put forth its “Valdez principles” for better management of environmental issues

and disclosure of information related to firms’ environmental and social impact. Continuing

their work, CERES and the Tellus Institute, with the support of United Nations Environment

Programme (UNEP), launched the Global Reporting Initiative (GRI) in 1997 to establish a

universal reporting framework that incorporates economic, governance and CSR information

in a single report framework (Gilbert, 2002). Major world organizations such as the United

Nations (UN) and the Organization for Economic Co-operation and Development (OECD)

extended their efforts to develop NFI disclosure frameworks to promote sustainable business