1 A PRODUCT PROJECT REPORT ON COFFEE PREPARED BY : KHADELA NIRUPA CLASS : T.Y. B.B.A. SEM-5 SHEET NO : 13100103066 COLLEGE : VIVEKANAND COLLAGE ACADEMIC YEAR : 2015-16 SABMITTED TO : SAURASTRA UNIVERSITY GUIDED BY : PRO. JATIN SHETH

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

A PRODUCT PROJECT REPORT ON COFFEE

PREPARED BY : KHADELA NIRUPA

CLASS : T.Y. B.B.A. SEM-5

SHEET NO : 13100103066

COLLEGE : VIVEKANAND COLLAGE

ACADEMIC YEAR : 2015-16

SABMITTED TO : SAURASTRA UNIVERSITY

GUIDED BY : PRO. JATIN SHETH

2

DDEECCLLAARRAATTIIOONN

I, the undersigned KHADELA NIRUPA student of

T.Y.B.B.A.SEM-5 here by declare that the project work presented

in this report is my own work and has been carried out under the

supervision of Pro. Jatin Sheth of VIVEKANAND COLLEGE

OF COMPUTER SCIENCE & MANAGMENT,RAJKOT

This work has not been previously submitted to any other

university for any examination.

Date : Student Signature

Place : RAJKOT KHADELA NIRUPA

3

PPRREEFFAACCEE

Small is beautiful, so also, small scale industry. It is

significant segment of the Indian economy & the objectives

underlying its development are increase in the supply of

manufactured goods, the development of indigenous entrepreneurial

talents and skills and the creation of employment opportunities.

Students with initiative, creativity and Indian orientation

have wonderful opportunities of becoming successful entrepreneurs

of small scale business unit which have attained a lot of protection

and encouragement from govt.

The subject “Entrepreneurship & Management of

small scale business” adds further to the vocational guidance

through the course of Bachelor of Business Administration

(B.B.A.).

4

AACCKKNNOOWWLLEEDDGGEEMMEENNTT

I feel great pleasure to present this report of

“Coffee”. I would like to heartily thanks to all the persons who have

helped me in this report and give me adequate guidance and

information for preparing this report.

I am thankful to Pro. Jatin Sheth who is guide of our

subject.

Date : Student signature

Place : RAJKOT KHADELA NIRUPA

5

Index

Particulars

Introduction

Introduction to Product

Project at a Glance

Bio-data of Partners

Justification of Location

Implementation of schedule

Raw-Material use in process

Manufacturing process

Supplier & Address of Machine Supply

Supplier & Address of Coffee Supply

Production Capacity Schedule

Quality Control

Wages and Salary Administration

Marketing Strategies

Channel of Distribution

Advertisement

Financial Details

Profitability

Trading Account for 3 years

Profit & Loss Account for 3 years

Balance Sheet for 3 years

B.E.P Analysis

Ratio Analysis

Risk Factors

Future Plan

Conclusion

6

INTRODUCTION TO SSI

Small scale industries has place of pride in

our economy. It is the base for medium & large scale

industries helps in earning foreign exchange, helps generating

employment opportunities and many more benefits are available

to the economy.

Hence, the government has introduced the

small and medium enterprise development bill – 2005 in the “

Lok – Sabha ”, seeking to enhance the investment cap for small

scale units from Rs. 1 corers to Rs. 5 corers. The bill aims to

consolidate the laws governing small and medium enterprises.

It also seeks to extend progressive credit facilities in line with

the guidelines laid out by the RBI. In a move to enable small

enterprise to grow the bill provides that more than 50

employees can be freed from the purview of labor laws

including the employer’s liability Act , 1938. This report is made

within the boundaries of SSI. With the intense to acquaint the

students with the functions of entrepreneur.

7

INTRODUCTION TO PRODUCT

According to a coffee history legend, an Arabian

shepherd named Kaldi found his goats dancing joyously around a

dark green leafed shrub with bright red cherries in the southern tip

of the Arabian Peninsula. Kaldi soon determined that it was the

bright red cherries on the shrub that were causing the peculiar

euphoria and after trying the cherries himself, he learned of their

powerful effect. The stimulating effect was then exploited by

monks at a local monastery to stay awake during extended hours of

prayer and distributed to other monasteriearound the world. Coffee

was born.

Despite the appeal of such a legend, recent botanical

evidence suggests a different coffee bean origin. This evidence

indicates that the history of the coffee bean began on the plateaus of

central Ethiopia and somehow must have been brought to Yemen

where it was cultivated since the 6th century. Upon introduction of

the first coffee houses in Cairo and Mecca coffee became a passion

rather than just a stimulant.

8

PROJECT AT A GLANCE

Name of the unit : Coke COFFEE

Office address : Nr. Panchanath mandir,

Star plaza,

Rajkot-360001.

Size of the organization : Small scale industry

Form of organization : Partnership Firm

Partners : Khadela Nirupa

Khushali Patel

Accountant : Mukund Gajera

Bankers : Bank of Baroda &

State Bank of Saurashtra

Weekly off : Sunday

Cost of project : 67,30,000

Owned capital : 60%

Borrowed capital : 40

9

BIO-DATA OF PARTNERS

PARTNER – 1

NAME : - Khadela Nirupa

ADDRESH : - 41-rajdeep society,

N/R rajeshvar mahadev temple,

150, feet ring road,

Rajkot.

AGE : - 24 years

QUALIFICATION : - M.B.A with Marketing

RESPONSIBILITY : - Production department &

Marketing department

CONTRIBUTION : - 50%

IN FINANCE

10

PARTNER - 2

NAME : - Khushali Patel

ADDRESH : - 4“Harsh”,

Illora duplex,

Opp. Ajanta Park,

University road,

Rajkot.

AGE : - 25 years

QUALIFICATION : - M.B.A.

RESPONSIBILITY : - Finance department &

H.R.department

CONTRIBUTION : - 50%

IN FINANCE

11

LOCATION OF THE INDUSTRY

Location is the place where the industry is located, means it is

the particular place where the promoters are thinking to establish

their working unit and its plays a vital role at the time of

establishment of the unit. Location has great importance because by

choosing location, one can decrease the cost of production and can

increase the cost of the profit. The selection of location of industry

is very difficult task, for this, requires great thinking perfect

planning taking into consideration future changes.

Location plays vital role in success of any industry once the

location is chosen it cannot be changed often. Frequent changes in

location leads to heavy loss to the firm. Several factors hold is kept

in mind while choosing location because the success of business

depends on the location. Factors, which are, affect the location as

below:

Availability of Raw Material:-

This is the most important factor that must be considered at the

time of selecting location in industry. The main raw material of

these industries available from Assam, tamilnadu & Karnataka

12

Government Policy:-

Government provides certain incentives to the industry,

located at rural areas for the purpose of development of such areas

and making balances regional growth, “Coke” is located at Gondal

so it can take certain benefits like subsidies, loans etc, from

government and also get loans from GIDS & ICICI.

Availability of Labor :-

Labor is the most important factors of production. In “Coke

coffee co.” skilled worker, semi-skilled worker, and unskilled

worker all are required. For the purpose of the production & making

a various products skilled workers are necessary the worker.

Semiskilled workers are necessary for the official work. Unskilled

workers are necessary for the other works in industry. All types of

labor are easily available from the city areas.

Transport Facility :-

Transport facility is the heart of any business for getting raw

material and for distribution of the final product transportation is

must. This industry has not developed its own transportation

because whenever, require the transport can easily available for

taking raw material and sending final products.

13

Power Supply :-

Power is the basic factor that affects the location of any

industry. The power is easily available where the “cc” located. But

sometimes, the problem of the electricity arises. Wednesday is the

day that is declares by the Gujarat Electricity Board that on that day

the supply will remain close

14

IMPLEMENTATION SCHEDULE

The major activities in the implementation of the project

have been listed and the average time for implementation is

estimated at 8-9 months.

No. Particulars Time Period

1. SSI Registration 1 Week

2. Acquisition of Land 1 Month

3. Preparation of Project Report 1 Month

4. Finance Assistance 3 Months

5. Building Construction 3 Months

6. Arrangement of Power 1 Month

7. Acquisition of Machinery 1 Month

8. Installation of Machinery 15 Days

9. Appointment of Staff & Labor 15 Days

10. Trial Production & Shooting Problem 2 Weeks

11. Commercial Production 1 Week After

Trial

Production

15

RAW MATERIAL USE IN PROCESS

Raw material is very useful for producing a final

product without Raw Materials Company cannot make its final

products. Raw materials are the basic requirement for any

production unit. It act as a fuel which is required to run a vehicle of

production. Raw materials are an inseparable part of any

manufacturing unit. for making of coffee green leaf is first raw-

material & from that leaf coffee bean is prepared.

16

MANUFACTURING PROCESS

1) Roasting of coffee beans

Coffee roasting is a chemical process. The green beans are

slowly dried to become a yellow color and the beans begin to smell

like popcorn after roasting coffee beans. The color changes from

light brown and medium brown.

2) Grinding

The second step is grinding. It is essential to grind coffee.

The roasted coffee beans are being grind in grinder machine. The

coffee should not be grinding more than 2 minutes.

3) Brewing

Brewing is as much of an art as it is a science. Coffee

should be brewed 4-5 minutes after coffee beans are grinding. In

this step timing is more important.

4) Cupping

Cupping is one of the coffee tasting techniques. The

condition of the cupping room is very important to the results

achieved during coffee cupping. The room should have a natural

light. The best time of cup is between late Mornings or late

afternoon at least six cups should prepare for each sample. They

should be arranged like triangle.

17

5) Sampling

To prepare the coffee samples, place 2 table spoons of

freshly roasted. After cupping by grinding of portion of each sample

and lining the coffee samples up next to each other on a black sheet

of a paper.

18

19

SUPPLIER & ADDRESS OF MACHINE SUPPLY

M/S Almech Fabs (p)Fabs (p) ltd ,

72, Industrial town

Ban lore 44.

M/S Steel & bras trading corporation

Nirman Nagar,

Kesar Baugh,

Karnataka

M/sLeoProducts,

83/3Said playa,

Henneries road,

Bangalore 44

20

SUPPLIER & ADDRESS OF COFFEE SUPPLY

1. Kiran Group Pvt Ltd.

81, New Avid Road,

KI Park,

Chennai 6000010

India.

2. Global Group Pvt Ltd.

W-11, Anna Nagar,

Chennai

India

21

PRODUCTION CAPACITY SCHEDULE

Production capacity & actual production plan are

planned after considering working time & period is as follow

Year. Installed

Capacity

(100%)

Utilized

Capacity

Production

Size

(gm)

(Packets)

Prices

1st 250000

76.67% 191666 500 120

2nd 250000

83.33% 208333 500 120

3rd 250000

98% 245000 500 120

22

QUALITY CONTROL

In common word, quality control means maintaining quality

but as far as materials is concerned, quality control is measure taken

by management for removing imperfection of a product by taking

various corrective measures. Various types of quality checks &

quality tests are conducted for determining the quality of the

product.

Quality control is a step through which properties, condition &

characteristics of product or process is measured. it is stated in terms

of grades, classes or specification & it is determined by application

involved.

So, in Coke there is also maintain the quality by management

well. In Coke quality is measured through sample method. So the

quality can be maintained through quality control.

23

WAGES AND SALARY ADMINISTRATION

Wages and salary administration is one of the important

functions of a professional personnel man and organization to

manage a business is to balance a variety of need and goals, which

required careful judgment. Every employee and workers are

working to get the reward in the form of salary and wage. Every

organization must give good salary and wages to reduce the

turnover of workers and employees that helps in increasing

efficiency of the organization.

Coke has good wage and salary structure. Coke provides

good salary to its employee. Coke also gives bonus to the employees

at the time of Diwali and other important festival.

The basic purpose of wage and salary administration is to

maintain equitable wage and salary structure. The employee is

working to get monetary returns, so it should be fair and enough

Proper and regular wage and salary helps to avoid

industrial disputes and decrease in productivity. It indirectly

motivates the worker and increases his efficiency. In “Coke” the

account department handles wage and salary affairs. The company

has adopted the method of monthly wage and salary. Every month

all the employees are paid salary in between 1st to 5th of every

month.

24

MARKETING STRATEGIES

Sales were built through advertising but now built brands

through a co-oriented integrated marketing strategy that involves all

point of contract between company & public.

1. Focus on profitable was short term. It is organized by

customer’s life time value.

2. Product unit organized marketing, now it is organized by

customer segment.

3. Marketing was focus on capturing new customer, now

emphasis is given to keeping existing customer.

4. Previously marketing department to do the marketing now

everyone in the company does some metrics.

5. It had individual & hierarchical work structures but now cross

functional teams.

6. Previously Developing & implementing a market plan took

years now it take months or weeks.

“Coke” planned to undertake marketing through sales agent in

different arties. They market them sales as per order

25

CHANNEL OF DISTRIBUTION

We can define formally the distribution channel as the

set of marketing instructions participating in the marketing activities

involve in the movement of the of goods or services form the

primary producer to the ultimate consumer.

Producer - Consumer

Producer - wholesaler - Retailer - Consumer

Producer - Agent - Wholesaler - Consumer

The channel of distribution is different to different

organization to organization. The channel of distribution followed

by the Coke is as under,

Company

Distributor

Dealers

Retailer

Consumers

26

ADVERTISMENT

Advertisement is a major promotion tool that a company

uses to target buyers and sellers.

In the competitive business world of transmission of

ideas, thought values development one cannot imagine a world

without advertising.

Advertisement is paid communication of goods services or

ideas by an identified sponsor. Moreover it can contact and

influence numbers people simultaneously quickly and at low cost

per prospect.

Thus “Coke” gives advertisement of their product in

directly magazine, radio, television and even in newspaper.

27

Financial Details

28

Details of land & building

No. Particulars Area Rate Total

1. Land 2300 sq mts 650 14,95,000

2. Building 7500 sq fts 300 22,50,000

TOTAL 37,45,000

Details of plant & machinery

No. Particulars Qty. Amount

1. Roasting 1 2,20,000

2. Grinder 1 1,80,000

3. Packing 1 1,00,000

4. Mixture 1 2,00,000

5. Sampling 1 3,00,000

TOTAL 10,00,000

29

OTHER FIXED ASSESTS

No. Particulars Amount(Rs.)

1. Delivery Van 4,00,000

2. Furniture 1,00,000

3. Electric Fitting 2,00,000

4. Computer 50,000

TOTAL 7,50,000

TOTAL FIXED ASSESTS

No. Particulars Amount(Rs.)

1. Land and Building 37,45,000

2. Plant and Machinery 10,00,000

3. Other Fixed Assets 7,50,000

4. Preliminary and Pre-operative Exps. 1,50,000

TOTAL 56,45,000

30

RAW MATERIAL REQUIREMENT

No Particular Rt. Per month Per annum

Qty Amt Qty. Amt.

1 Green leafs 8 35000 280000 42000 3,36,000

2 Green bean 60 10000 600000 120000 7,20,000

3

Cupping 6 250 1500 3000 18,000

4

Others 140 200 28000 2400 3,36,000

5

Packing 25000 3,00,000

6 Preservative 25000 3,00,000

TOTAL 959500 1151400

31

UTILITIES

No. Particulars Qty. Rate Monthly Annually

1. Electricity 3000KWH 10 30,000 3,60,000

2. Water 15,000 1,80,000

3. Fuel 9,000 1,08,000

TOTAL 54,000 6,48,000

OTHER CONTINGENT EXPENSES

No. Particulars Amount Per

Month

Amount Per

Year

1. Repairs & Maintenance 6,000 72,000

2. Legal Expenses 4,000 48,000

3. Miscellaneous Expenses 4,000 48,000

4. Printing Expense 8,000 96,000

5. Telephone Expense 2,500 30,000

6. Advertisement & Selling

Expenses

6,000 72,000

7. Postage & Stationary 750 9,000

TOTAL 31,250 3,75,000

32

MAN POWER REQUIREMENT

TOP LEVEL

No. Designation No. Of

Employees

Monthly

Salary

Yearly

Salary

1. Manager 1 6,000 72,000

2. Accountant 1 4,500 54,000

TOTAL 10,500 1,26,000

MIDDLE LEVEL

No. Designation No. Of

Employees

Monthly

Salary

Yearly

Salary

1. Clerk 1 3,000 36,000

2. Supervisor 2 6,000 72,000

TOTAL 9,000 1,08,000

LOWER LEVEL

No. Designation No. Of

Employees

Monthly

Salary

Yearly

Salary

1. Skilled 4 8,000 96,000

2. Unskilled 5 7,500 90,000

TOTAL 15,500 1,86,000

33

TOTAL WORKING CAPITAL

No. Particulars Amount Per

Month

Amount Per

Annum

1. Raw Material 9,59,500 1,151,4000

2. Utility 54,000 6,48,000

3. Wages & Salary 40,250 4,83000

4. Contingent Expenses 31,250 3,75,000

TOTAL 10,85,000 1,302,0000

TOTAL COST OF PROJECT

No. Particulars Amount

1. Total Fixed Capital 56,45,000

2. Total Working Capital 10,85,000

TOTAL 67,30,000

34

SOURCE OF FUND

No. Particulars Percentage Amount

1. Owned Capital 60% 26,92,000

2. Borrowed Capital 40% 40,38,000

TOTAL 67,30,000

INTEREST

No. Particulars Percentage Amount

1. Owned 8 % 2,15,360

2. Borrowed Loan (SBS) 11 % 4,44,180

TOTAL 6,59,540

35

DEPRECIATION

No. Particulars Value Rate 1st Year 2nd

Year

3rd

Year

1. Building 2250000 10 % 225000 202500 182250

2. Plant &

Machinery

1000000 25 % 250000 187500 140625

3. Computer 50000 40 % 20000 12000 7200

4. Furniture 100000 15 % 15000 12750 10838

5. Vehicle 400000 15 % 60000 51000 43350

TOTAL 5,70,000 4,65,750 3,84,263

ANNUAL COST OF PRODUCTION

No. Particulars Amount

1. Raw Materials 11514000

2. Wages & Salary 483000

3. Other Expenses 375000

4. Utilities 648000

5. Depreciation 570000

6. Interest On Capital (Owned) 215360

7. Interest On Capital (Borrowed) 444180

TOTAL 1,42,49,540

36

SALES FORECAST

TERM LOAN REPAYMENT

Year Utilized

Capacity

Production Sales Packets

Price(500gm)

Amount

1st 60 % 245000 245000 60 14700000

2nd 70 % 280000 280000 60 16800000

3rd 85 % 297500 297500 65 19337500

No. Particulars 1st Year 2ndYear 3rd Year

Opening

Balance of

Loan

4038000 3230400 2422800

A. Payment of

Principal

Amount

807600 807600 807600

B. Payment of

Interest @

11%

444180 355344 266508

Total

Installment (

A + B )

1251780 1162944 1074108

37

COST PER UINT

1. FIXED COST

No. Particulars Amount

1. Staff & Labor (60 %) 289800

2. Other Contingent Expenses (60%) 225000

3. Depreciation 570000

4. Interest on Capital 659540

5. Preliminary Expenses W/O 50000

TOTAL 1134800

1. FIXED COST

FCPU = Total Fixed Cost

Sold

= 1134800 = Rs. 4.63

245000

38

2. VARIABLE COST

No. Particulars Amount

1. Raw Materials 11514000

2. Other Contingent Expenses (40%) 150000

3. Utilities 648000

4. Staff & Labor (40%) 193200

TOTAL 12505200

VARIABLE COST

VCPU = Total Variable Cost

Sold

= 12505200 = Rs.51.04

245000

39

PROFITABILITY

Particulars Amount

Sales

14700000

Less:-

Cost Of Production 13640000

EBIT 1060000

Less:-

Interest on Bank Loan

444180

EBT 615820

Less:-

Tax @ 35%

215537

NET PROFIT 400283

40

Trading Account 1st Year

Particulars Amount Particulars Amount

To Opening Stock --- By Sales 11500000

To Labour Expense 180000

To Raw Material

Expenses

9225000

To Utilities 625000

To Gross Profit

(16%)

1470000

TOTAL 11500000 TOTAL 11500000

Trading Account 2nd Year

Particulars Amount Particulars Amount

To Opening Stock --- By Sales 12500000

To Labour Expense 186000

To Raw Material

Expenses

11014000

To Utilities 640000

To Gross Profit

(16%)

1874000

TOTAL 12500000 TOTAL 12500000

41

Trading Account 3rd Year

Particulars Amount Particulars Amount

To Opening Stock --- By Sales 14700000

To Labour Expense 186000

To Raw Material

Expenses

11514000

To Utilities 648000

To Gross Profit

(16%)

2352000

TOTAL 14700000 TOTAL 14700000

42

Profit & Loss Account 1st year

Particulars Amount Particulars Amount

To Advertising

Expense

58000 By Gross Profit

(16%)

1470000

To Depreciation 300000

To Salaries 250000

To Legal Expense 38000

To Repairs &

Maintenance

58000

To Post & Stationary 5500

To Printing 75000

To Telephone

Expense

30000

To Preliminary

Expense W/O

50000

To Miscellaneous

Expenses

40000

To Interest on

Borrowed Loan

278520

To Income Tax 189145

NET PROFIT

(2.72%)

177835

TOTAL 1470000

TOTAL 1470000

43

Profit & Loss Account 2nd year

Particulars Amount Particulars Amount

To Advertising

Expense

70000 By Gross Profit

(16%)

1874000

To Depreciation 400000

To Salaries 297000

To Legal Expense 45000

To Repairs &

Maintenance

69000

To Post & Stationary 7500

To Printing 85000

To Telephone

Expense

30000

To Preliminary

Expense W/O

50000

To Miscellaneous

Expenses

48000

To Interest on

Borrowed Loan

302180

To Income Tax 202537

NET PROFIT

(2.72%)

272783

TOTAL 1874000

TOTAL 1874000

44

Profit & Loss Account 3rd year

Particulars Amount Particulars Amount

To Advertising

Expense

72000 By Gross Profit

(16%)

2352000

To Depreciation 570000

To Salaries 297000

To Legal Expense 48000

To Repairs &

Maintenance

72000

To Post & Stationary 9000

To Printing 96000

To Telephone

Expense

30000

To Preliminary

Expense W/O

50000

To Miscellaneous

Expenses

48000

To Interest on

Borrowed Loan

444180

To Income Tax 215537

NET PROFIT

(2.72%)

400283

TOTAL 2352000 TOTAL 2352000

45

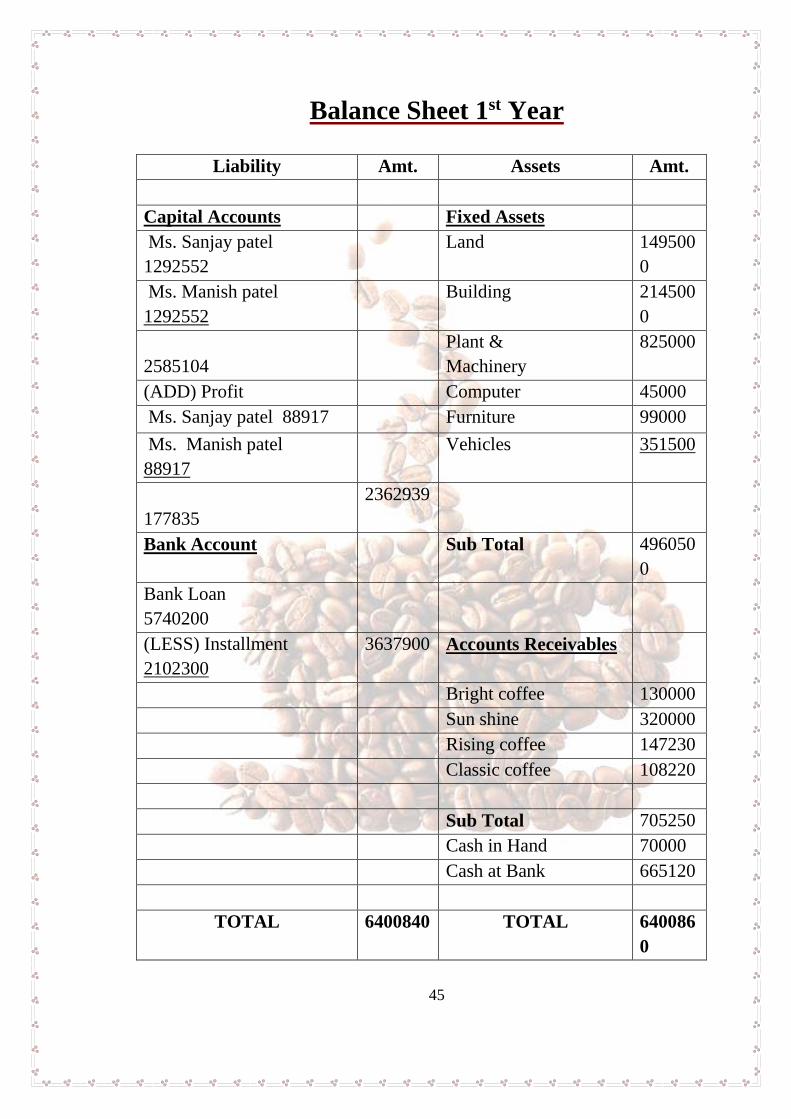

Balance Sheet 1st Year

Liability Amt. Assets Amt.

Capital Accounts Fixed Assets

Ms. Sanjay patel

1292552

Land 149500

0

Ms. Manish patel

1292552

Building 214500

0

2585104

Plant &

Machinery

825000

(ADD) Profit Computer 45000

Ms. Sanjay patel 88917 Furniture 99000

Ms. Manish patel

88917

Vehicles 351500

177835

2362939

Bank Account Sub Total 496050

0

Bank Loan

5740200

(LESS) Installment

2102300

3637900 Accounts Receivables

Bright coffee 130000

Sun shine 320000

Rising coffee 147230

Classic coffee 108220

Sub Total 705250

Cash in Hand 70000

Cash at Bank 665120

TOTAL 6400840 TOTAL 640086

0

46

Balance Sheet 2nd Year

Capital/Liability Amount. Property/Assets Amt.

Capital Accounts Fixed Assets

Ms.sanjay patel

1546141

Land 1495000

Ms. Manish patel

1546142

3099283

Building 1822500

Plant &

Machinery

562500

(ADD) Profit Computer 18000

Ms. Sanjay patel

375855

Furniture 72250

Ms. Manish patel

375856

751711

Vehicles 289000

3850994 4259250

Bank Account Sub Total

Bank Loan

3230400

(LESS) Installment

807600

2422800 Accounts Receivables

Bright coffee 147000

Sun shine 117544

Rising coffee 200000

Classic coffee 150000

Sub Total 614544

Cash in Hand 200000

Cash at Bank 1200000

TOTAL 6273794 TOTAL 6273794

47

Balance Sheet 3rd Year

-

Capital/Liability Amount. Property/Assets Amount

Capital Accounts Fixed Assets

Ms. Sanjay patel

1921996

Land 1495000

Ms. Manish patel

1921998

Building 1640250

3843994 Plant &

Machinery

421875

(ADD) Profit Computer 10800

Ms. Sanjay patel

738480

Furniture 61412

Ms. Manish patel

738480

Vehicles 245650

1476960

5320954

Bank Account Sub Total 3874897

Bank Loan

2422800

(LESS) Installment

807600

1615200 Accounts Receivables

Bright coffee 116257

Sun shine 345000

Rising coffee 275000

Classic coffee 200000

Sub Total 936257

Cash in Hand 325000

Cash at Bank 1800000

TOTAL 6936154 TOTAL 6936154

48

BREAK EVEN ANALYSIS

TR

TC BEP Profit

& TC

TR A

FC

C Loss

0 Production

Particulars Amount (UK ts.) Amount (Rs.)

Sales

(Less) Variable Cost

Contribution

Fixed Cost

60.00

51.04

8.96

4.63

14700000

12505200

2194800

1134800

49

Profit Volume Ratio = Contribution X 100

Sales

= 2194800 X 100 = 14.93 %

14700000

1. BEP = Fixed Cost

Contribution

= 1134800 = 126552 Uts.

8.96

2. BEP (in Rs.) = Fixed Cost X 100

PV Ratio

= 1134800 X 100 = 7600804 Rs.

14.93

3. BEP (in %) = Fixed Cost X utilized capacity

Contribution

= 1134800 X 70 = 36.19 %

2194800

50

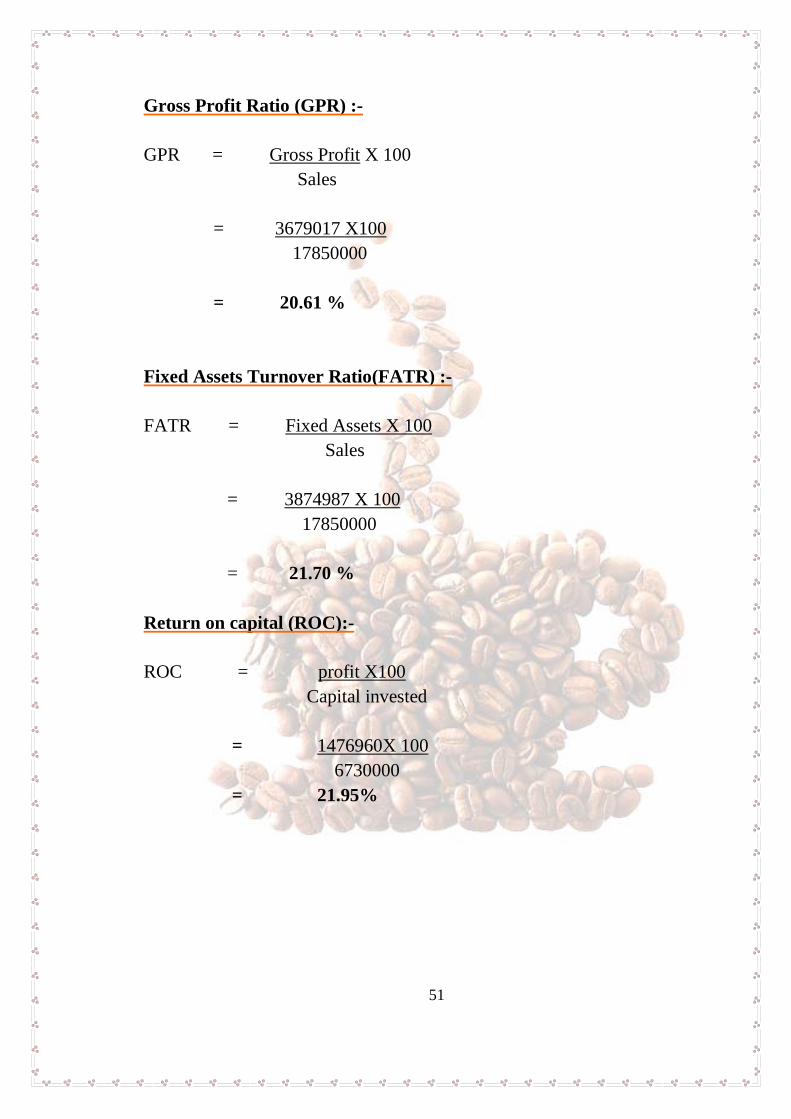

RATIO ANALYSIS

Rate Of Investment (ROI) :-

ROI = EBIT X 100

Project Fund

= 2538754 X 100

6730000

= 21.95 %

Net Profit Ratio (NPV) :-

NPR = Net Profit X 100

Sales

= 1476960 X100

14700000

= 8.27 %

51

Gross Profit Ratio (GPR) :-

GPR = Gross Profit X 100

Sales

= 3679017 X100

17850000

= 20.61 %

Fixed Assets Turnover Ratio(FATR) :-

FATR = Fixed Assets X 100

Sales

= 3874987 X 100

17850000

= 21.70 %

Return on capital (ROC):-

ROC = profit X100

Capital invested

= 1476960X 100

6730000

= 21.95%

52

RISK FACTORS

Every new business needs to determine its risk factors that the

business will face. It risk factors are carefully determined then the

entrepreneur can take better measures to see that they have limited

effect on the business following are some of the risks that the new

business will face:-

1. The risk of failure of Project.

2. The unit may face competition from existing & new units as it is

Common & prevalent for any unit.

3. Consumer wont get much well aware about the products

4. Negative attitude of customers

5. Change in government policy may affect the unit

53

FUTURE PLANS

The “Coke” has following future plans;

The company looks forward to enlarge its market both at

national and international level. To meet their production capacity

“Coke” constructed its new site on 1,90,000 sq. it area company

proposed expansion plans with help to increase the production to

reach the set target.

“Coke” desire to stand in a top five leading coffee companies

of India with in a short period of time.

Recognizing the imperative the company has been moving

firmly in recent years to enter in the selected new markets with

promise for significant growth in future.

54

CONCLUSION

“Coke” have a rapid development and having a bright

successful future in the production and marketing of coffee

Company has well established marketing and personnel

department and the financial condition is very strong.

A part form profit objective company has also social

responsibility objective. Company is doing much for the

development of human resources and provides various facilities to

its personnel.

Related Documents