NFM-2121AO.8 (11/11)

NFM-2121AO.8 (11/11). Some things you need to know Neither Nationwide ® nor any of its representatives may provide legal or tax advice; please consult.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

NFM-2121AO.8 (11/11)

NFM-2121AO.8 (11/11)

Some things you need to know

• Neither Nationwide® nor any of its representatives may provide legal or tax advice; please consult a legal or tax advisor for answers to your specific questions

• Life insurance is issued by Nationwide Life Insurance Company or Nationwide Life and Annuity Insurance Company, Columbus, Ohio, members of Nationwide Financial®

• Guarantees and coverage are based on the claims paying ability of the issuing company

• Nationwide, Nationwide Financial, the Nationwide framemark and On Your Side are registered service marks of Nationwide Mutual Insurance Company

©2010, Nationwide Financial Services. All rights reserved.

• Not a deposit • Not FDIC or NCUSIF insured

• Not guaranteed by the institution • Not insured by any federal government agency

• May lose value

NFM-2121AO.8 (11/11)

Some things you need to know

• Investing involves risk, including the possible loss of principal

• As your personal situations change (i.e., marriage, birth of a child or job promotion), so will your life insurance needs. Care should be taken to ensure this product is suitable for your long-term life insurance needs. You should weigh any associated costs before making a purchase. Life insurance has fees and charges associated with it that include costs of insurance that vary with such characteristics of the insured as gender, health and age, and has additional charges for riders that customize a policy to fit your individual needs.

• Keep in mind that as an acceleration of the death benefit, the LTC rider payout will reduce both the death benefit and cash values. Care should be taken to make sure that your clients' life insurance needs continue to be met even if the rider pays out in full. There is no guarantee that the rider will cover the entire cost for all of the insured's long-term care as these vary with the needs of each insured.

NFM-2121AO.8 (11/11)

Some things you need to know

• This information assumes that the life insurance is not a modified endowment contract, or MEC; as long as the contract meets the non-MEC definitions of IRC Section 7702A, most distributions are taxed on a first-in/first-out basis; surrender charges may apply to partial surrenders; loans and partial surrenders from a MEC will generally be taxable and, if taken prior to age 59½, may be subject to a 10% tax penalty; loans and partial surrenders will reduce the cash value and the death benefits payable to your beneficiaries, and withdrawals above the available free amount will incur surrender charges; if your contract were to lapse with a loan outstanding, the loan amount in excess of basis will be treated as a distribution and all or a portion will be subject to income tax

NFM-2121AO.8 (11/11)

Agenda

• The need for life insurance• The need for long-term care coverage• The long-term care dilemma• Medicare vs. Medicaid• Skilled care vs. chronic care• An alternative solution: Nationwide’s long-term care

rider

NFM-2121AO.8 (11/11)

The need for life insurance

• Life insurance provides some financial protection for those you care about

• Your personal life insurance needs should be considered in planning

• Customizations to life insurance policies are optional and typically available at an additional cost– Nationwide® long-term care rider

NFM-2121AO.8 (11/11)

The need for long-term care coverage

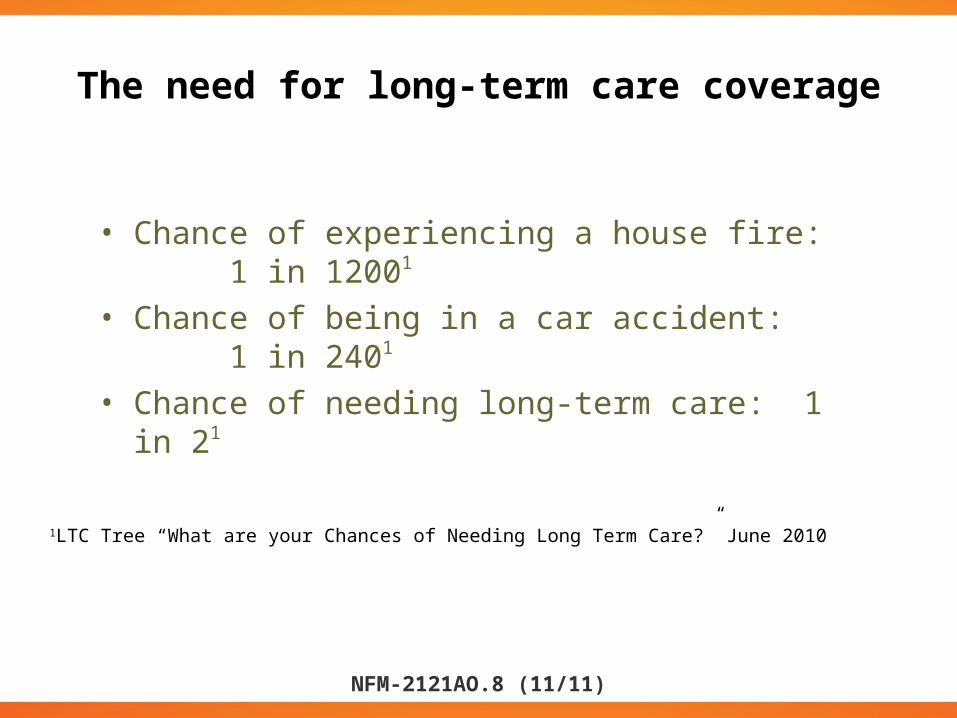

• Chance of experiencing a house fire: 1 in 12001

• Chance of being in a car accident: 1 in 2401

• Chance of needing long-term care: 1 in 21

1LTC Tree “What are your Chances of Needing Long Term Care?” June 2010

NFM-2121AO.8 (11/11)

Preparing for long-term care coverage

• Only 17% of baby boomers have planned for long-term care needs1

• Only 10% of adults over age 65 own a long-term care insurance policy2

1 Sources: LTC Insurance Tree – “What are the Chances of Needing Long Term Care?” June 20102 Sources: “Do You Need Long Term Care?” – The Money Alert, Set. 2010

Have you thought about long-term care?

NFM-2121AO.8 (11/11)

The need for long-term care coverage

• Sources estimate 50% of Americans will need some type of long-term care during their lifetime1

• For couples over age 65, there is a 70% chance one partner will need long-term care2 – 73% of people who need long-term care receive care at home or from

services such as assisted living or adult day care3

– 27% will need care in a nursing home3

• Average stay in a nursing home: 2.5 years4

– About 10% of people in nursing homes will stay 5 years or more5

• Average length of care outside a nursing home is 4.5 years4

1 Mature Market Institute, Market Survey of Long Term Care Costs, October 20102 U.S. Department of Health and Human Services, National Clearinghouse for Long-Term Care Information, Jan. 31, 20113 American Association for Long-term Care Insurance, 2011 LTCi Sourcebook4 ”What is Long Term Care? The Misunderstood Health Care”, Guide to Long Term Care.com, 20105“Insurance for Women and What They Need to Know” – 2010, LTC News, completelongtermcare.com

NFM-2121AO.8 (11/11)

The need for long-term care coverage

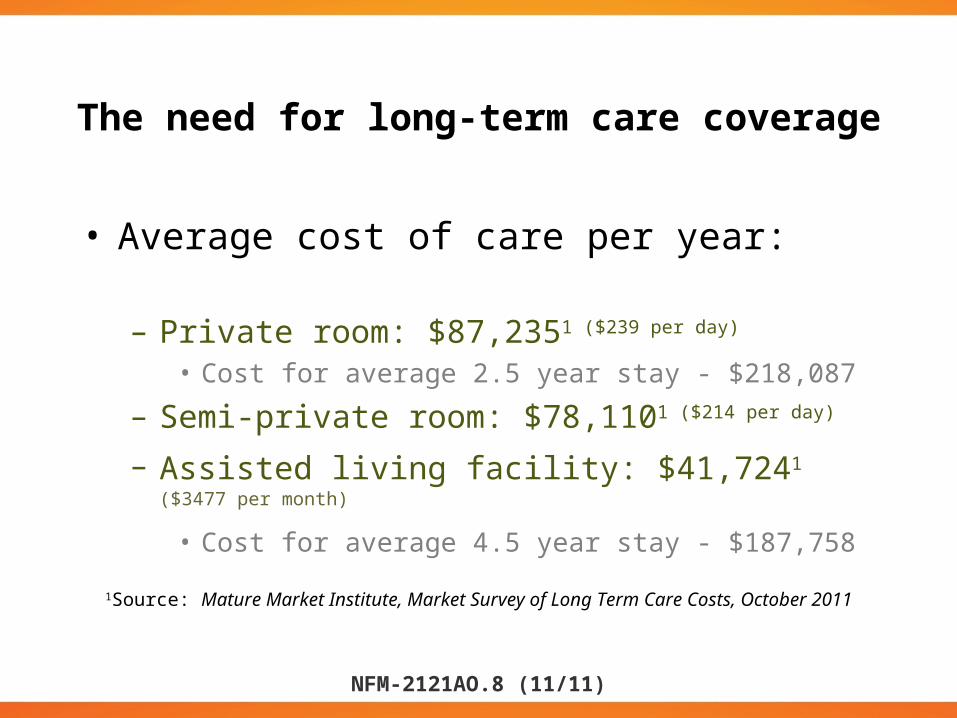

• Average cost of care per year:

– Private room: $87,2351 ($239 per day)

• Cost for average 2.5 year stay - $218,087

– Semi-private room: $78,1101 ($214 per day)

– Assisted living facility: $41,7241 ($3477 per month)

• Cost for average 4.5 year stay - $187,758

1Source: Mature Market Institute, Market Survey of Long Term Care Costs, October 2011

NFM-2121AO.8 (11/11)

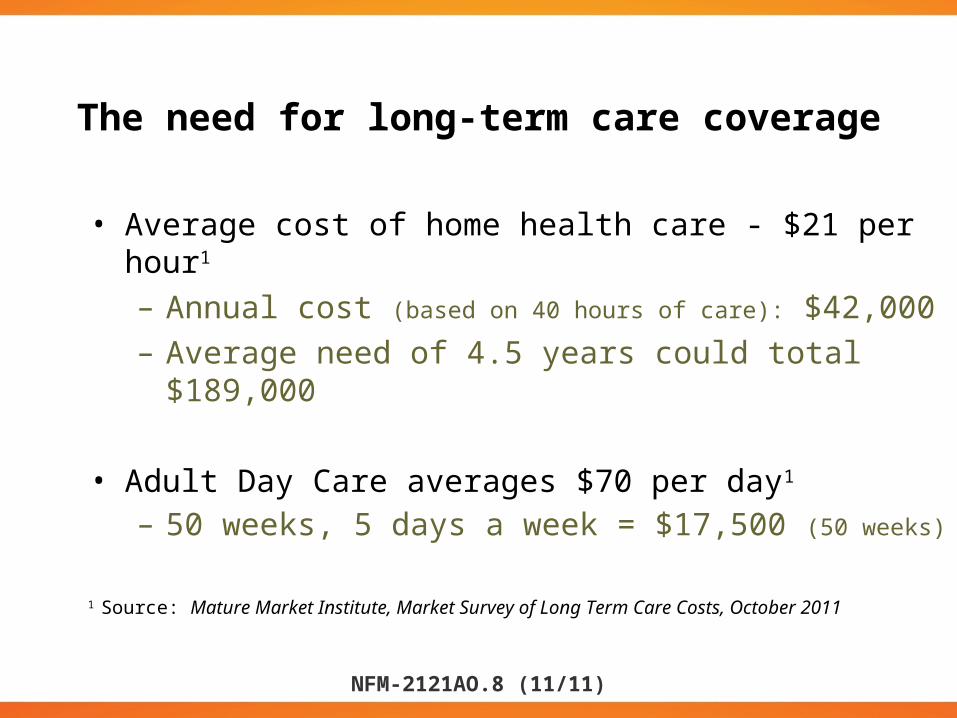

The need for long-term care coverage

• Average cost of home health care - $21 per hour1 – Annual cost (based on 40 hours of care): $42,000– Average need of 4.5 years could total $189,000

• Adult Day Care averages $70 per day1

– 50 weeks, 5 days a week = $17,500 (50 weeks)

1 Source: Mature Market Institute, Market Survey of Long Term Care Costs, October 2011

NFM-2121AO.8 (11/11)

The need for long-term care coverage

• Costs keep rising• Long-term care costs are expected to quadruple

2008’s averages by the year 20301

• By 2030, the cost for a semi-private room is expected to be $265,000 per year1

1 Life and Health Advisor, Sept. 17, 2010, “Don’t Let Clients Get Blindsided by Unexpected LTC Costs”

NFM-2121AO.8 (11/11)

Why haven’t more Americans prepared for their long-term care need?

• Cost1

• Other financial responsibilities1

• Loss of premium1

– Some policies guarantee return of premium, subject to the claims-paying ability of the issuing insurance company

• Simply don’t see the need, or do not wish to discuss1

1 “Why People Don’t Buy Long-Term Care Insurance”, Howard Gleckman, Forbes, Sept. 12, 2011

NFM-2121AO.8 (11/11)

Who is preparing for long-term care?

• What age group is actively looking to purchase long-term care?– Currently, 81% of people purchasing LTC are under the

age of 651

– No longer just for the elderly• 56% of sales were to people age 55-64

• 20.9% of sales were to people age 45-54

14 American Association for Long-term Care Insurance, 2011 LTCi Sourcebook

NFM-2121AO.8 (11/11)

Who should plan for long-term care?

• Who should be purchasing long-term care coverage?– Anyone with assets to protect

• What about the wealthy?– Self insuring possible but not cost efficient

• Middle Class concerns?– Preserving a legacy– Protecting healthy spouse from impoverishment

NFM-2121AO.8 (11/11)

Understanding real solutions to long-term care needs

• Self-insure – Only possible for the affluent, though not cost efficient

• Medicaid – For the impoverished

• Long-term Care coverage– Practical choice for the middle class?– Are there other options?

NFM-2121AO.8 (11/11)

Long-term care costs

How do you think long-term care costs are being paid?

• According to studies, Americans erroneously believe the following1

– 54% believe Medicare will pay– 46% believe Medicaid will pay– 44% believe health insurance will pay

1Source: AAHSA, American Association of Homes and Services for the Ageing, June, 2010

NFM-2121AO.8 (11/11)

Long-term care costs

• Where does the money actually come from for

paid care?– 24% out of pocket or from family members16

– 49% Medicaid16

– 20% Medicare (temporary)16

– 7% private long-term care insurance16

• What about informal unpaid care? – Comprises 50% of care in the U.S17

– Usually provided by spouse or daughters17

16National Clearinghouse for Long-term Care Information (2010).17Long-Term Care Financing Reform: Lessons from U.S. and Abroad, Howard Gleckman, 2010

NFM-2121AO.8 (11/11)

Medicaid vs. Medicare

• Medicaid is for the impoverished18

– Welfare program that pays for skilled or chronic care – Assets must be $2,000 or less (amount varies by state)– With new five-year look-back period, giving away assets is

complicated– Lose control over options for care– Medicaid uses nursing homes first, not as a last resort

18National Clearinghouse for Long-term Care Information, U.S. Department of Health and Human Services, http://www.longtermcare.gov (2010).

NFM-2121AO.8 (11/11)

Medicaid vs. Medicare

• Medicare pays a maximum of 100 days19

– Requires a three-consecutive-day hospital stay– Limited to 100 days– First 20 days are provided at no cost– Next 80 days require a substantial daily co-pay ($144.50 per

day in 2012)– Covers skilled care, not chronic care

http://www.medicare.gov (Nov 2011).

NFM-2121AO.8 (11/11)

Skilled care vs. Chronic Care

Skilled care: • Patient shows sign of improvement

– Has nothing to do with severity of illness or injury– Is determined by the services received– Is short-term to help recover from something

• Health Insurance and Medicare will pay• Possible qualified treatment

– Short-term IVs or tube feeding– Physical therapy – with improvement– Speech therapy – with improvement

NFM-2121AO.8 (11/11)

Skilled care vs. chronic care, continued

Chronic care: • Patient does not show progress

– Respiratory therapy for emphysema– Catheter maintenance – Colostomy drain – Chronic care can include care for strokes, paralysis and comas– Help with bathing, dressing, other activities of daily living

• Long-term care– Is considered chronic care– Neither chronic care nor maintenance care are covered by

private insurance or Medicare

• What about Alzheimer’s or the frail?

NFM-2121AO.8 (11/11)

Impact of Lack of Planning

• Choice in care requires planning and resources– Planning should include the adult children

• Can your family really take care of you?– Do you have the physical ability to care for your spouse?– Do you or your children have the ability to give quality care?– Can your child afford to quit work or reduce hours?– Do you want to move where your child lives?

• What asset would you sell first to cover bills?– How long would your assets last?– Risk to spouse’s financial security?

• Dissention among siblings– One child often carries the load– Powers of Attorney – which child? Will all children agree on plan?– How to children fairly split the parent’s care expenses?

NFM-2121AO.8 (11/11)

What to Look for in LTC Coverage

• LTC coverage helps a family plan • Make sure you understand your coverage

– A full service policy will cover all qualified LTC services including:

• Nursing home• Home health care• Assisted living• Adult day care, etc.

– Make sure temporary claims will be covered• Not all LTC products pay for temporary claims

– Make sure your understand cost structure• Check whether policy is subject to increase in cost

NFM-2121AO.8 (11/11)

An alternative solution: Nationwide® life insurance with the optional long-term care rider

• Evaluate the need for life insurance and purchase an appropriate policy

• Long-term care coverage can be added at an additional cost– Provides a beginning to long-term care planning for younger people

– Long-term care benefit is paid tax-free as an accelerated death benefit

– If long-term care benefit is used, it is important to ensure that sufficient life insurance coverage remains

NFM-2121AO.8 (11/11)

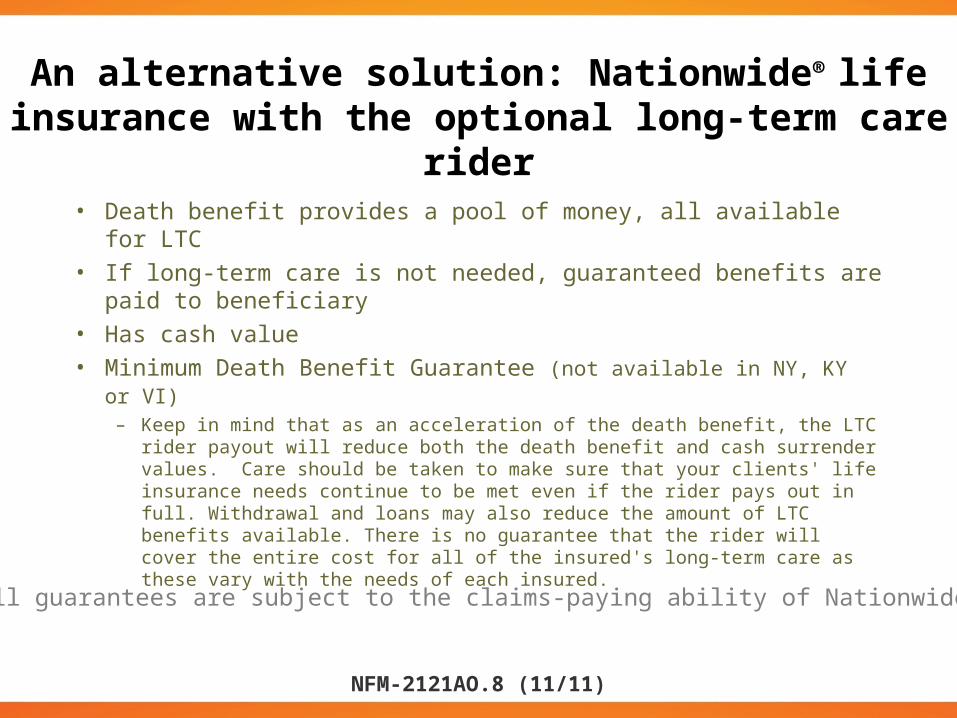

An alternative solution: Nationwide® life insurance with the optional long-term care rider

• Death benefit provides a pool of money, all available for LTC• If long-term care is not needed, guaranteed benefits are paid to

beneficiary • Has cash value• Minimum Death Benefit Guarantee (not available in NY, KY or VI)

– Keep in mind that as an acceleration of the death benefit, the LTC rider payout will reduce both the death benefit and cash surrender values. Care should be taken to make sure that your clients' life insurance needs continue to be met even if the rider pays out in full. Withdrawal and loans may also reduce the amount of LTC benefits available. There is no guarantee that the rider will cover the entire cost for all of the insured's long-term care as these vary with the needs of each insured.

All guarantees are subject to the claims-paying ability of Nationwide®

NFM-2121AO.8 (11/11)

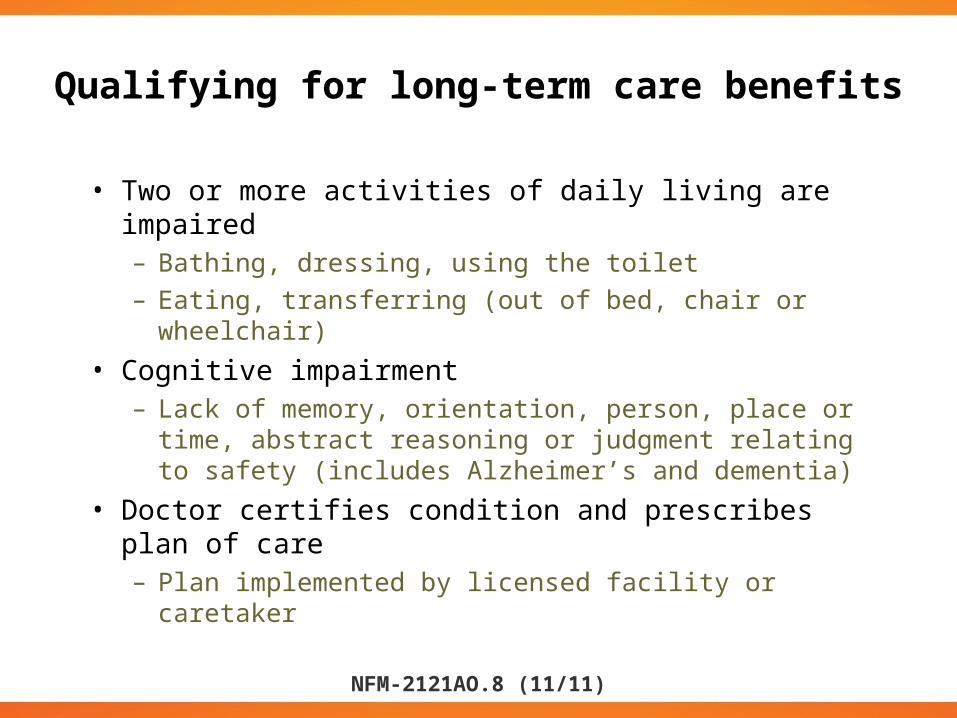

Qualifying for long-term care benefits

• Two or more activities of daily living are impaired – Bathing, dressing, using the toilet

– Eating, transferring (out of bed, chair or wheelchair)

• Cognitive impairment – Lack of memory, orientation, person, place or time,

abstract reasoning or judgment relating to safety (includes Alzheimer’s and dementia)

• Doctor certifies condition and prescribes plan of care– Plan implemented by licensed facility or caretaker

NFM-2121AO.8 (11/11)

Long-term care benefits elimination period

• One-time 90-day elimination period– Any combination of days in a long-term care facility or

days requiring services of home health care or adult day care

– Days don’t need to be consecutive, but must be accumulated within a continuous period of 730 days

NFM-2121AO.8 (11/11)

What benefit will the client receive?

• The long-term care benefit is the lesser of:– 2% per month of the death benefit OR– Daily HIPAA rate (in 2012, $310/day) multiplied by the number

of days in the month – For example:Long-term care rider: $500,000 X 2% = $10,000 per month ORHIPAA: $310 X 30 days = $9,300 per month– In this example the initial long term care benefit is $9,300 monthly

• In this example, how long will the long-term care benefit last?– At least four years and two months or until the full long-term

care benefit of $500,000 is paid*

* Assuming no loans or withdrawals have been taken prior to collecting long-term care benefit

NFM-2121AO.8 (11/11)

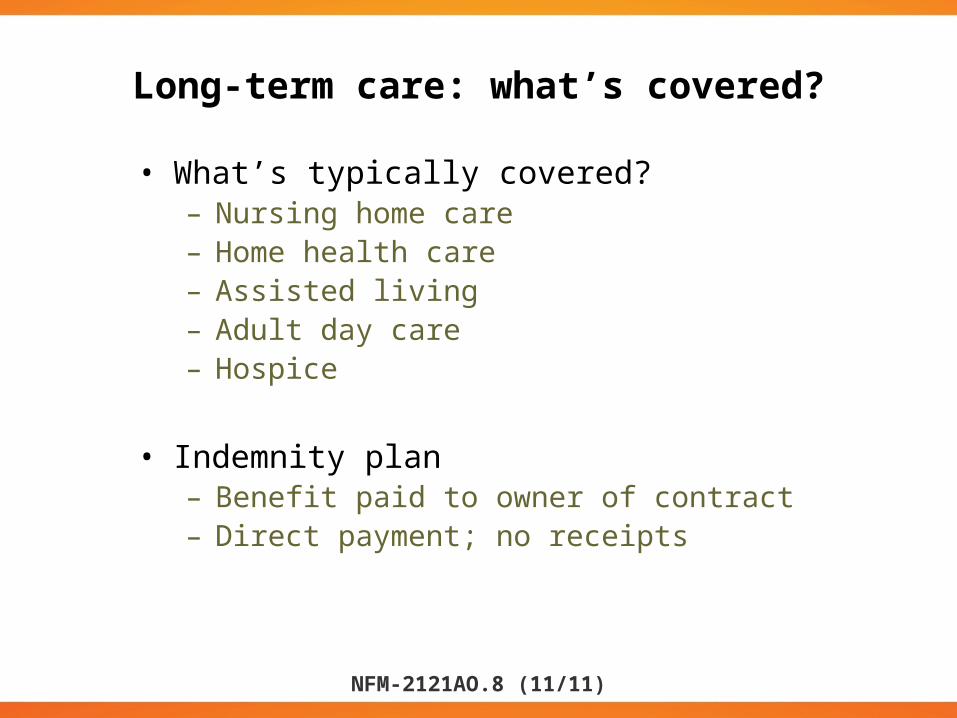

Long-term care: what’s covered?

• What’s typically covered?– Nursing home care– Home health care– Assisted living– Adult day care– Hospice

• Indemnity plan– Benefit paid to owner of contract– Direct payment; no receipts

NFM-2121AO.8 (11/11)

Other features

• Issue ages are 21 through 80 in most states• No-lapse provision• Guaranteed minimum death benefit (except NY, KY, and VI)

– Example (this hypothetical does not represent any actual client or client situation):

• $500,000 death benefit

• $500,000 long-term care rider

• Use all $500,000 for long-term care

• Beneficiaries still receive $50,000

• Available on most Nationwide® permanent individual life insurance contracts

• Contracts available with guaranteed premiums

NFM-2121AO.8 (11/11)

There are four kinds of people in the world:

those who have been caregivers

those who are currently caregivers

those who will be caregivers

and those who will need caregivers

------- Rosalynn Carter

NFM-2121AO.8 (11/11)

Summary

• The likelihood of needing long-term care is significant• The cost of such care can be financially devastating

– Not covered by health insurance

– Not covered by Medicare after 100 days

• Long-term care coverage is another piece in financial and retirement considerations

• Purchasing long-term care coverage may help preserve financial and family well-being

NFM-2121AO.8 (11/11)

Thank you!

What questions do you have?

Related Documents