1 NEWS RELEASE Shaw Announces First Quarter Results Broadband advantage helps drive solid Q1 performance Calgary, Alberta (January 12, 2017) – Shaw Communications Inc. announces consolidated financial and operating results for the quarter ended November 30, 2016. Consolidated revenue from continuing operations for the quarter of $1.3 billion increased by 14.9% over the comparable period. Operating income before restructuring costs and amortization 1 for the quarter of $539 million improved 6.1% over the comparable period. Excluding the results of the Wireless division, acquired on March 1, 2016, revenue for the quarter from the combined Consumer, Business Network Services and Business Infrastructure Services divisions was up 2.8% and operating income before restructuring costs and amortization for the quarter remained flat over the comparable period. Chief Executive Officer, Brad Shaw said, “We’ve entered fiscal 2017 with momentum and on track to deliver on our strategic initiatives. Shaw recently announced the completion of key milestones demonstrating our commitment to execute on our video and network technology roadmaps, most notably, the introduction of our next generation video product BlueSky TV and the launch of Freedom Mobile’s LTE-Advanced network. Our solid first quarter results reflect the broadband advantage we’ve created and our disciplined approach to long-term and sustainable growth.” Selected Financial Highlights Three months ended November 30, Change % (millions of Canadian dollars except per share amounts) 2016 2015 Revenue 1,313 1,143 14.9 Operating income before restructuring costs and amortization 1 539 508 6.1 Operating margin 1 41.1% 44.4% (3.3pts) Free cash flow 1 158 173 (8.7) Net income 89 218 (59.2) Basic and diluted earnings per share 0.18 0.43 Net income for the current quarter in the amount of $89 million decreased by $129 million relative to the first quarter of fiscal 2016 mainly due to a non-recurring provision in the amount of $107 million related to the wind down of our investment in shomi. Net income in the quarter also reflects a decrease in income from discontinued operations, net of tax, in the amount of $80 million due to the sale of the former Media division in the third quarter of the prior year which is offset partially by the equity income of $27 million in the quarter from our investment in Corus. Consolidated free cash flow 1 for the quarter of $158 million compared to $173 million in the prior year. The decrease for the quarter was largely due to the loss of free cash flow generated by the former Media division and higher planned capital expenditures from continuing operations driven by the addition of the Wireless division. In the quarter, we continued our momentum of improving subscriber trends. Consumer revenue generating units (“RGUs”) in the first quarter declined by 29,696, a meaningful improvement over the 43,750 loss in the first quarter of fiscal 2016. This year-over-year improvement was driven by a reduction in cable video and phone RGU losses in addition to strong Internet RGU net gains of 16,669 reflecting a full quarter impact of our WideOpen Internet 150 offering launched in August 2016. The

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

NEWS RELEASE

Shaw Announces First Quarter Results

Broadband advantage helps drive solid Q1 performance

Calgary, Alberta (January 12, 2017) – Shaw Communications Inc. announces consolidated financial

and operating results for the quarter ended November 30, 2016. Consolidated revenue from continuing

operations for the quarter of $1.3 billion increased by 14.9% over the comparable period. Operating

income before restructuring costs and amortization1 for the quarter of $539 million improved 6.1% over

the comparable period. Excluding the results of the Wireless division, acquired on March 1, 2016,

revenue for the quarter from the combined Consumer, Business Network Services and Business

Infrastructure Services divisions was up 2.8% and operating income before restructuring costs and

amortization for the quarter remained flat over the comparable period.

Chief Executive Officer, Brad Shaw said, “We’ve entered fiscal 2017 with momentum and on track to

deliver on our strategic initiatives. Shaw recently announced the completion of key milestones

demonstrating our commitment to execute on our video and network technology roadmaps, most notably,

the introduction of our next generation video product BlueSky TV and the launch of Freedom Mobile’s

LTE-Advanced network. Our solid first quarter results reflect the broadband advantage we’ve created

and our disciplined approach to long-term and sustainable growth.”

Selected Financial Highlights

Three months ended November 30, Change %

(millions of Canadian dollars except per share amounts)

2016

2015

Revenue 1,313 1,143 14.9

Operating income before restructuring costs and amortization 1 539 508 6.1 Operating margin 1 41.1% 44.4% (3.3pts)

Free cash flow 1 158 173 (8.7)

Net income 89 218 (59.2) Basic and diluted earnings per share 0.18 0.43

Net income for the current quarter in the amount of $89 million decreased by $129 million relative to the

first quarter of fiscal 2016 mainly due to a non-recurring provision in the amount of $107 million related

to the wind down of our investment in shomi. Net income in the quarter also reflects a decrease in

income from discontinued operations, net of tax, in the amount of $80 million due to the sale of the

former Media division in the third quarter of the prior year which is offset partially by the equity income

of $27 million in the quarter from our investment in Corus.

Consolidated free cash flow1 for the quarter of $158 million compared to $173 million in the prior year.

The decrease for the quarter was largely due to the loss of free cash flow generated by the former Media

division and higher planned capital expenditures from continuing operations driven by the addition of the

Wireless division.

In the quarter, we continued our momentum of improving subscriber trends. Consumer revenue

generating units (“RGUs”) in the first quarter declined by 29,696, a meaningful improvement over the

43,750 loss in the first quarter of fiscal 2016. This year-over-year improvement was driven by a

reduction in cable video and phone RGU losses in addition to strong Internet RGU net gains of 16,669

reflecting a full quarter impact of our WideOpen Internet 150 offering launched in August 2016. The

2

decline in Consumer RGUs was also largely impacted by the anticipated seasonal disconnections of

satellite Video subscribers in the amount of 15,704 RGUs.

“We are using our wireline broadband advantage to support WideOpen Internet 150 with the majority of

new Internet customers opting for our two-year value plan, underlining the value we are providing with

much faster speeds at affordable prices across 95% of our footprint,” said Mr. Shaw. “We continue to

enhance our wireline network and are on track to complete our DOCSIS 3.1 upgrade by the end of fiscal

2017.”

In Wireless, we added approximately 9,500 RGUs, a shortfall from the net gains achieved in the fourth

quarter of fiscal 2016. The wireless subscriber results reflect our focus on the launch of Freedom Mobile,

the rollout of our LTE-Advanced network and significantly heightened competitive activity in the period.

“We achieved three important milestones in our Wireless division this quarter. First, we launched the new

Freedom Mobile brand, anchored by a commitment of trust and transparency for our customers. Second,

the rollout of our LTE-Advanced network in the key markets of central Toronto and central Vancouver.

Third, the introduction of the Freedom Wi-Fi trial, allowing customers to connect to over 65,000 Shaw

Go WiFi hotspots across Alberta and British Columbia,” said Mr. Shaw.

Mr. Shaw added, “Today, we are excited to be the first in Canada to offer a best-in-class TV experience

powered by our strategic partnership with Comcast. This next chapter in our video technology roadmap

marks an important and exciting milestone in Shaw’s history. Our new X1 TV experience, named

BlueSky TV, provides ease-of-use and customization that is unprecedented in Canada. Its innovative

voice remote technology provides a whole new way for our customers to quickly and easily discover what

they want to watch. We are pleased to offer this leading technology experience to customers in Calgary,

with subsequent launches in major cities within our footprint planned throughout fiscal 2017.”

Shaw continues to be disciplined in driving efficiencies throughout the business. In the quarter, we shifted

our In-Home Technician team to a hybrid unit-based installation and service technician model, combining

a foundation of customer experience with technical skill that will deliver annualized operating cost

savings of approximately $16 million. This initiative resulted in a non-recurring restructuring charge of

$10 million in the quarter.

Brad Shaw concluded, “In fiscal 2017 we are focused on delivering exceptional customer experiences

through the launch of BlueSky TV, Freedom Mobile and continuously building our converged network.

We thank our 14,000 employees for their dedication to delivering on Shaw’s key strategic initiatives. This

is an exciting time for Shaw as we leverage our broadband advantage and strengthen our wireless network

delivering significant value to both our customers and our shareholders.”

Shaw Communications Inc. is an enhanced connectivity provider. Our Consumer division serves

consumers with broadband Internet, Shaw Go WiFi, video and digital phone. Our Wireless division

provides wireless voice and data services through an expanding and improving mobile wireless network

infrastructure. The Business Network Services division provides business customers with Internet, data,

WiFi, telephony, video and fleet tracking services. The Business Infrastructure Services division, through

ViaWest, provides hybrid IT solutions including colocation, cloud computing and security and

compliance for North American enterprises.

Shaw is traded on the Toronto and New York stock exchanges and is included in the S&P/TSX 60 Index

(Symbol: TSX - SJR.B, SJR.PR.A, SJR.PR.B, NYSE – SJR, and TSXV – SJR.A). For more information,

please visit www.shaw.ca

3

The accompanying Management’s Discussion and Analysis (“MD&A”) forms part of this news release

and the “Caution concerning forward-looking statements” applies to all the forward-looking statements

made in this news release.

For more information, please contact:

Shaw Investor Relations

[email protected] 1 See definitions and discussion under “Non-IFRS and additional GAAP measures” in the accompanying MD&A.

Shaw Communications Inc.

4

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the three months ended November 30, 2016

January 12, 2017

Contents

Introduction 7

Selected financial and operational highlights 8

Overview 9

Outlook 12

Non-IFRS and additional GAAP measures 12

Discussion of operations 15

Supplementary quarterly financial information 19

Other income and expense items 21

Financial position 22

Liquidity and capital resources 23

Accounting standards 24

Related party transactions 25

Financial instruments and other instruments 25

Risk and uncertainties 25

Advisories

The following Management’s Discussion and Analysis (“MD&A”), dated January 12, 2017, should be

read in conjunction with the unaudited interim Consolidated Financial Statements and Notes thereto for

the quarter ended November 30, 2016 and the 2016 Annual Consolidated Financial Statements, the Notes

thereto and related MD&A included in the Company’s 2016 Annual Report. The financial information

presented herein has been prepared on the basis of International Financial Reporting Standards (“IFRS”)

for interim financial statements and is expressed in Canadian dollars unless otherwise indicated.

References to “Shaw”, the “Company”, “we”, “us” or “our” mean Shaw Communications Inc. and its

subsidiaries and consolidated entities, unless the context otherwise requires.

Caution concerning forward-looking statements

Statements included in this MD&A that are not historic constitute “forward-looking statements” within

the meaning of applicable securities laws. Such statements include, but are not limited to:

• statements about future capital expenditures;

• asset acquisitions and dispositions;

• cost efficiencies;

• financial guidance for future performance;

• business and technology strategies and measures to implement strategies;

• statements about the Company’s equity investments, joint ventures and partnership arrangements

including any statements about write-downs, losses and liabilities;

• competitive strengths; and

• expansion and growth of the Company’s business and operations and other goals and plans.

Shaw Communications Inc.

5

They can generally be identified by words such as “anticipate”, “believe”, “expect”, “plan”, “intend”,

“target”, “goal” and similar expressions (although not all forward-looking statements contain such

words). All of the forward-looking statements made in this report are qualified by these cautionary

statements.

Forward-looking statements are based on assumptions and analyses made by the Company in light of its

experience and its perception of historical trends, current conditions and expected future developments as

well as other factors it believes are appropriate in the circumstances as of the current date. The

Company’s management believes that its assumptions and analysis in this MD&A are reasonable and

that the expectations reflected in the forward looking statements contained herein are also reasonable

based on the information available on the date such statements are made and the process used to prepare

the information. These assumptions, many of which are confidential, include, but are not limited to:

• general economic conditions;

• interest;

• income tax and exchange rates;

• technology deployment;

• content and equipment costs;

• industry structure;

• conditions and stability;

• government regulation; and

• the integration of recent acquisitions.

You should not place undue reliance on any forward-looking statements. Many factors, including those

not within the Company's control, may cause the Company's actual results to be materially different from

the views expressed or implied by such forward-looking statements, including, but not limited to:

• general economic, market and business conditions;

• changes in the competitive environment in the markets in which the Company operates and from

the development of new markets for emerging technologies;

• industry trends, technological developments, and other changing conditions in the entertainment,

information and communications industries;

• the Company’s ability to execute its strategic plans and capital projects;

• the Company’s ability to achieve cost efficiencies;

• technology, cyber security and reputational risks;

• opportunities that may be presented to and pursued by the Company;

• changes in laws, regulations and decisions by regulators that affect the Company or the markets

in which it operates;

• the Company’s status as a holding company with separate operating subsidiaries; and

• other factors described in this report under the heading “Known events, trends, risks and

uncertainties”.

The foregoing is not an exhaustive list of all possible factors.

Should one or more of these risks materialize, or should assumptions underlying the forward-looking

statements prove incorrect, actual results may vary materially from those described herein.

The Company provides certain financial guidance for future performance as the Company believes that

certain investors, analysts and others utilize this and other forward-looking information in order to assess

the Company's expected operational and financial performance and as an indicator of its ability to service

debt and pay dividends to shareholders. The Company's financial guidance may not be appropriate for

this or other purposes.

Shaw Communications Inc.

6

Any forward-looking statement speaks only as of the date on which it was originally made and, except as

required by law, the Company expressly disclaims any obligation or undertaking to disseminate any

updates or revisions to any forward-looking statement to reflect any change in related assumptions,

events, conditions or circumstances. All forward looking statements contained in this MD&A are

expressly qualified by this statement.

Non-IFRS and additional GAAP measures

Certain measures in this MD&A do not have standard meanings prescribed by IFRS and are therefore

considered non-IFRS measures. These measures are provided to enhance the reader’s overall

understanding of our financial performance or current financial condition. They are included to provide

investors and management with an alternative method for assessing our operating results in a manner that

is focused on the performance of our ongoing operations and to provide a more consistent basis for

comparison between periods. These measures are not in accordance with, or an alternative to, IFRS and

do not have standardized meanings. Therefore, they are unlikely to be comparable to similar measures

presented by other entities.

Please refer to “Non-IFRS and additional GAAP measures” in this MD&A for a discussion and

reconciliation of non-IFRS measures, including operating income before restructuring costs and

amortization and free cash flow.

Shaw Communications Inc.

7

Introduction

With the completion of two transformative transactions in 2016 and other significant strategic initiatives

and acquisitions in recent years, we have strengthened Shaw’s growth profile. The addition of the

Wireless division enables Shaw to combine the power of fibre, coax, Wi-Fi and wireless networks to

deliver a seamless experience of anytime and anywhere enhanced connectivity within our operating

footprint. We are focused on operational efficiency to ensure we execute on our strategic priorities and

build on delivering an exceptional customer experience that is centered on our world-class converged

network and strategic partnerships with best in-class providers.

We enter fiscal 2017 with a solid foundation in place to execute on the strategic initiatives we set out to

achieve. Our broadband advantage is supporting the continued momentum in the WideOpen Internet 150

offering with most new Internet customers opting for our two-year value plan, underlining the value we

are providing with much faster speeds at affordable prices across 95% of our footprint. We continue to

enhance our wireline network and are on track to complete our DOCSIS 3.1 upgrade by the end of fiscal

2017.

We are also excited to be the first in Canada to offer a best-in-class TV experience powered by our

strategic partnership with Comcast. This next chapter in our video technology roadmap marks an

important and exciting milestone in Shaw’s history. Our new X1 TV experience, named BlueSky TV,

provides ease-of-use and customization that is unprecedented in Canada. Its innovative voice remote

technology provides a whole new way for our customers to quickly and easily discover what they want

to watch. We are pleased to offer this leading technology experience to customers in Calgary, with

subsequent launches in the remaining major cities in our footprint planned throughout fiscal 2017.

In Wireless, we continued taking the necessary steps to becoming an enhanced connectivity provider and

in the quarter reached three important milestones. First, the launch of the new Freedom Mobile brand,

anchored by a commitment of trust and transparency for our customers. Second, the rollout of our LTE-

Advanced network in the key markets of central Toronto and central Vancouver. Third, the introduction

of the Freedom Wi-Fi trial, allowing customers to connect to over 65,000 Shaw Go WiFi hotspots across

Alberta and British Columbia.

Shaw continues to be disciplined in driving efficiencies throughout the business. In the quarter, we

shifted our In-Home Technician team to a hybrid unit-based installation and service technician model,

combining a foundation of customer experience with technical skill that will deliver annualized operating

cost savings of approximately $16 million. This initiative resulted in a non-recurring restructuring charge

of $10 million in the quarter.

In 2017, we are focused on delivering exceptional customer experiences through the launch of BlueSky

TV, Freedom Mobile and continuously building our converged network. In our Wireless division, we

will continue with the rollout of our LTE-Advanced upgrade which is expected to be complete in our

existing major markets by the end of fiscal 2017. The Business Network Services division continues to

strengthen our position as trusted advisors to small and medium sized businesses, applying a managed

services strategy developed in partnership with Broadsoft, Cisco and Meraki. We have made it easy for

businesses to harness seamless technology advances such as SmartVoice, SmartWiFi, and SmartSecurity

for all of their connectivity needs. Our Business Infrastructure Services division continues its industry

leadership in providing hybrid IT solutions, including colocation, cloud and managed services, by

leveraging ViaWest’s established track record.

This is an exciting time for Shaw as we capitalize on our broadband advantage and strengthen our

wireless network delivering significant value to both our customers and our shareholders.

Shaw Communications Inc.

8

Selected financial and operational highlights

Basis of presentation

On April 1, 2016, Shaw sold 100% of its wholly owned subsidiary Shaw Media Inc. to Corus

Entertainment Inc. (“Corus”), a related party subject to common voting control for $2.65 billion,

comprised of $1.85 billion in cash and 71,364,853 Corus Class B non-voting participating shares.

Accordingly, the operating results and operating cash flows for the previously reported Media division

are presented as discontinued operations separate from the Company’s continuing operations. Prior

period financial information has been reclassified to present the Media division as a discontinued

operation, and has therefore been excluded from both continuing operations and segmented results for all

periods presented in this MD&A and the accompanying interim financial statements. This MD&A

reflects the results of continuing operations, unless otherwise noted.

Financial Highlights Three months ended November 30,

(millions of Canadian dollars except per share amounts)

2016

2015 Change %

Operations: Revenue 1,313 1,143 14.9

Operating income before restructuring costs and

amortization (1) 539 508

6.1 Operating margin (1) 41.1% 44.4% (3.3pts)

Net income from continuing operations 89 138 (35.5)

Income from discontinued operations, net of tax - 80 (100.0) Net income 89 218 (59.2)

Per share data: Basic and diluted earnings per share

Continuing operations 0.18 0.28

Discontinued operations - 0.15

0.18 0.43

Weighted average participating shares outstanding during period (millions) 487 480

Funds flow from continuing operations (2) 414 347 19.3 Free cash flow(1) 158 173 (8.7)

(1) See definitions and discussion under “Non-IFRS and additional GAAP measures”. (2) Funds flow from operations is before changes in non-cash balances related to operations as presented in the unaudited

interim Consolidated Statements of Cash Flows.

Shaw Communications Inc.

9

Subscriber highlights Change

Three months ended November 30,

November 30, 2016 August 31, 2016 2016 2015

Consumer

Video – Cable 1,657,913 1,671,059 (13,146) (18,029)

Video – Satellite 774,905 790,574 (15,669) (12,927)

Internet 1,804,606 1,787,642 16,964 9,433

Phone 938,918 956,763 (17,845) (22,227)

Total Consumer 5,176,342 5,206,038 (29,696) (43,750)

Business Network

Services

Video – Cable 57,955 61,153 (3,198) (2,871)

Video – Satellite 30,959 30,994 (35) 299

Internet 177,000 179,867 (2,867) (1,015)

Phone 306,692 301,328 5,364 2,497

Total Business

Network Services 572,606 573,342 (736) (1,090)

Wireless

Postpaid 681,335 667,028 14,307 -

Prepaid 371,423 376,260 (4,837) -

Total Wireless 1,052,758 1,043,288 9,470 -

Total Subscribers 6,801,706 6,822,668 (20,962) (44,840)

Overview

Our fiscal 2017 first quarter financial results represent improvements in consolidated revenue and

operating income before restructuring costs and amortization over the first quarter of fiscal 2016.

Highlights of the first quarter financial results are as follows:

Revenue for the quarter of $1.31 billion, an increase of 14.9% from $1.14 billion for the first

quarter of 2016

First quarter operating income before restructuring costs and amortization of $539 million, an

increase of 6.1% from $508 million for the first quarter of 2016

Operating margin for the first quarter of 41.1%, down from 44.4% for the first quarter of 2016

Net income for the first quarter of $89 million, a decrease of 59.2% from $218 million for the

first quarter of 2016

Free cash flow for the first quarter of $158 million, a $15 million decrease from $173 million for

the first quarter of 2016

The period ended with 6,801,706 RGUs, inclusive of 1,052,758 Wireless subscribers. Wireless

subscribers increased by 9,470 in the first quarter. Consumer and Business Network Services had

a combined 30,432 RGU decline in the first quarter compared to a decline of 44,840 for the first

quarter of 2016.

Revenue increased 14.9% for the quarter, primarily due to the acquisition of Freedom Mobile (formerly,

WIND) on March 1, 2016, contributing Wireless revenues of $138 million. The Consumer, Business

Network Services and Business Infrastructure Services divisions also contributed to the consolidated

Shaw Communications Inc.

10

revenue increases for the quarter. In Consumer, the improvement was driven primarily by the August

2016 rate increases, growth in Internet RGUs and a year-over-year decrease in promotional costs.

Revenue increases in the Business Network Services and Business Infrastructure Services divisions were

driven by customer growth in the quarter and the year-over-year impact of the December 2015

acquisition of INetU.

Operating income before restructuring costs and amortization of $539 million for the quarter improved

6.1% compared to $508 million for fiscal 2016. The improvement in the first quarter reflects the added

contribution of $30 million from the Wireless division and increases in the Business Infrastructure

Services and Business Network Services divisions attributable to profitable customer growth and the

acquisition of INetU. These improvements were partially offset by lower operating income before

restructuring costs and amortization in the Consumer division where higher revenue was more than fully

offset by increased costs, primarily programming related.

As compared to the fourth quarter of fiscal 2016, consolidated revenue for the quarter increased 0.5% or

by $7 million to $1.31 billion and operating income before restructuring costs and amortization

decreased 1.8% or by $10 million to $539 million. The improvement in revenue was primarily due to the

August 2016 rate increases in the Consumer division and customer growth in each the Business Network

Services and Business Infrastructure Services divisions offset partially by decreased revenue in the

Wireless division due mostly to lower handset sales. The decrease in operating income before

restructuring costs and amortization was driven primarily by higher costs in the Consumer division

related to an increase in programming costs and the timing of sponsorship related marketing costs.

In the quarter, the Company continued its momentum of improving subscriber trends. Consumer

revenue generating units (“RGUs”) in the first quarter declined by 29,696, a meaningful improvement

over the declines of 37,104 RGUs in the fourth quarter of 2016 and 43,750 RGUs in the first quarter of

2016. The year-over-year improvement was driven by a reduction in cable video and phone RGU losses

in addition to strong Internet RGU net gains of 16,669 reflecting a full quarter impact of our WideOpen

Internet 150 offering launched in August 2016. The decline in Consumer RGUs was also impacted by

the anticipated seasonal disconnections of satellite Video subscribers in the amount of 15,704 RGUs.

The Wireless division added a net 9,470 RGUs, a shortfall from the net gains achieved in the fourth

quarter of fiscal 2016, finishing the period with a total 1,052,758 RGUs. The wireless subscriber results

reflect our focus on the launch of Freedom Mobile, the rollout of our LTE-Advanced network and

significantly heightened competitive activity

Shaw Communications Inc.

11

Net income for the current fiscal quarter of $89 million compared to $154 million in the prior quarter

(August 31, 2016) and $218 million in the comparable quarter of the prior year (November 30, 2015).

The changes in net income are outlined in the following table.

November 30, 2016 net income compared to:

Three months ended Three months ended

(millions of Canadian dollars) August 31, 2016 November 30, 2015

Increased (decreased) operating income before restructuring costs

and amortization (1) (10) 31

Increased restructuring costs (11) (12)

Increased amortization (2) (32)

Change in net other costs and revenue (2) (62) (60)

Decreased (increased) income taxes 30 24

Decreased income from discontinued operations, net of tax (10) (80)

(65) (129)

(1) See definitions and discussion under “Non-IFRS and additional GAAP measures”. (2) Net other costs and revenue includes business acquisition costs, accretion of long-term liabilities and provisions, debt

retirement costs, equity income and losses of an associate or joint venture and other losses as detailed in the unaudited

Consolidated Statements of Income.

First quarter net income decreased $65 million compared to the fourth quarter of fiscal 2016 primarily

due to a non-recurring provision in the amount of $107 million related to the wind down of shomi

operations included in net other costs and revenue for the current quarter offset partially by $27 million

in equity income from our investment in Corus. Also contributing to the decrease in net income was

lower operating income before restructuring costs, higher restructuring costs and lower income from

discontinued operations, partially offset by lower income taxes.

Net income for the current quarter in the amount of $89 million decreased by $129 million relative to the

first quarter of fiscal 2016 mainly due to the non-recurring provision in the amount of $107 million

related to the wind down of our investment in shomi. Net income in the quarter also reflects a decrease

in income from discontinued operations, net of tax, in the amount of $80 million due to the sale of the

former Media division in the third quarter of the prior year which is offset partially by the equity income

of $27 million in the quarter from our investment in Corus.

Free cash flow of $158 million for the quarter compared to $173 million for first quarter of fiscal 2016.

The free cash flow decrease was primarily the result of a reduction in free cash flow from discontinued

operations in the amount of $74 million following the sale of the Media division in 2016 and the addition

of the Wireless division, where capital expenditures of $64 million exceeded $30 million of operating

income before restructuring and amortization for the quarter. These decreases were partially offset by

lower capital investment by Consumer and Business Network Services and Business Infrastructure

Services, a reduction in cash taxes, increased dividends from equity accounted associates and lower

pension funding during the quarter.

Shaw Communications Inc.

12

Outlook

Shaw confirms at this time that there are no changes to our previously issued fiscal 2017 guidance.

Operating income before restructuring costs and amortization is expected to range between $2.125 and

$2.175 billion and free cash flow is expected to exceed $400 million. Consolidated capital investment

targets also remain unchanged from previously provided guidance at $1.3 billion for the year.

See “Caution concerning forward-looking statements”.

Non-IFRS and additional GAAP measures

The Company’s continuous disclosure documents may provide discussion and analysis of non-IFRS

financial measures. These financial measures do not have standard definitions prescribed by IFRS and

therefore may not be comparable to similar measures disclosed by other companies. The Company’s

continuous disclosure documents may also provide discussion and analysis of additional GAAP

measures. Additional GAAP measures include line items, headings, and sub-totals included in the

financial statements.

The Company utilizes these measures in making operating decisions and assessing its performance.

Certain investors, analysts and others utilize these measures in assessing the Company’s operational and

financial performance and as an indicator of its ability to service debt and return cash to shareholders.

The non-IFRS financial measures and additional GAAP measures have not been presented as an

alternative to net income or any other measure of performance required by IFRS.

Below is a discussion of the non-IFRS financial measures and additional GAAP measures used by the

Company and provides a reconciliation to the nearest IFRS measure or provides a reference to such

reconciliation.

Operating income before restructuring costs and amortization

Operating income before restructuring costs and amortization is calculated as revenue less operating,

general and administrative expenses. It is intended to indicate the Company’s ongoing ability to service

and/or incur debt, and is therefore calculated before one-time items such as restructuring costs,

amortization (a non-cash expense) and interest. Operating income before restructuring costs and

amortization is also one of the measures used by the investing community to value the business. Three months ended November 30,

(millions of Canadian dollars)

2016

2015

Operating income from continuing operations 272 285

Add back (deduct): Restructuring costs 12 -

Amortization:

Deferred equipment revenue (14) (19) Deferred equipment costs 34 40

Property, plant and equipment, intangibles and other 235 202

Operating income before restructuring costs and amortization 539 508

Shaw Communications Inc.

13

Operating margin

Operating margin is calculated by dividing operating income before restructuring costs and amortization

by revenue.

Three months ended November 30,

2016 2015 Change

Consumer 42.8% 44.4% (1.6pts)

Business Network Services 50.0% 47.1% 2.9pts Business Infrastructure Services 35.6% 34.2% 1.4pts

Wireless 21.7% - n/a

41.1% 44.4% (3.3pts)

Income from discontinued operations before restructuring costs, amortization, taxes and other

non-operating items

Income from discontinued operations before restructuring costs, amortization, taxes and other non-

operating items is calculated as revenue less operating, general and administrative expenses from

discontinued operations. This measure is used in the determination of free cash flow.

Three months ended November 30,

(millions of Canadian dollars) 2016 2015

Income from discontinued operations, net of tax - 80 Add back (deduct): -

Gain on divestiture, net of tax - -

Income taxes - 29 Restructuring costs - -

Amortization: -

Property, plant and equipment, intangibles and other - 7 Other non-operating items - 2

Income from discontinued operations before restructuring costs, amortization, taxes

and other non-operating items

-

118

Free cash flow

The Company utilizes this measure to assess the Company’s ability to repay debt and pay dividends to

shareholders. Free cash flow is calculated as free cash flow from continuing operations and free cash

flow from discontinued operations.

Free cash flow from continuing operations is comprised of operating income before restructuring costs

and amortization adding dividends from equity accounted associates, changes in receivable related

balances with respect to customer equipment financing transactions as a cash item and deducting capital

expenditures (on an accrual basis and net of proceeds on capital dispositions) and equipment costs (net),

interest, cash taxes paid or payable, dividends paid on the preferred shares, recurring cash funding of

pension amounts net of pension expense and adjusted to exclude share-based compensation expense.

Free cash flow from continuing operations has not been reported on a segmented basis. Certain

components of free cash flow from continuing operations, including operating income before

restructuring costs and amortization continue to be reported on a segmented basis. Capital expenditures

and equipment costs (net) are reported on a combined basis for Consumer and Business Network

Services due to the common infrastructure and separately for Business Infrastructure Services and

Wireless. Other items, including interest and cash taxes, are not generally directly attributable to a

segment, and are reported on a consolidated basis.

Free cash flow from discontinued operations is comprised of income from discontinued operations

before restructuring costs, amortization, taxes and other non-operating items after deducting capital

expenditures (on an accrual basis and net of proceeds on capital dispositions), cash taxes paid or payable,

Shaw Communications Inc.

14

program rights amortization on assets held for sale, cash amounts associated with funding CRTC benefit

obligations related to media acquisitions, recurring cash funding of pension amounts net of pension

expense and excludes non-controlling interest amounts that are included in the income from discontinued

operations before restructuring costs, amortization, taxes and other non-operating items.

Free cash flow is calculated as follows:

Three months ended November 30,

(millions of Canadian dollars)

2016

2015

Change

%

Revenue Consumer 947 943 0.4

Business Network Services 144 136 5.9

Business Infrastructure Services 90 73 23.3 Wireless 138 - n/a

1,319 1,152 14.5

Intersegment eliminations (6) (9) 33.3

1,313 1,143 14.9

Operating income before restructuring

costs and amortization (1)

Consumer 405 419 (3.3) Business Network Services 72 64 12.5

Business Infrastructure Services 32 25 28.0

Wireless 30 - n/a

539 508 6.1

Capital expenditures and equipment costs (net):(2)

Consumer and Business Network Services 205 215 (4.7) Business Infrastructure Services 21 30 (30.0)

Wireless 64 - n/a

290 245 18.4

Free cash flow before the following 249 263 (5.3) Less:

Interest (73) (73) -

Cash taxes (44) (68) (35.3)

Other adjustments:

Dividends from equity accounted

associates

21

-

n/a Non-cash share-based compensation 1 1 -

Pension adjustment 4 (23) (>100.0) Customer equipment financing 2 2 -

Preferred share dividends (2) (3) (33.3)

Free cash flow from continuing

operations

158 99

59.6

Income from discontinued operations

before restructuring costs, amortization,

taxes and other non-operating items

- 118

n/a Less:

Capital expenditures - (1) n/a

Cash taxes - (29) n/a CRTC benefit obligation funding - (4) n/a

Non-controlling interests - (9) n/a

Pension adjustment - (1) n/a

Free cash flow from discontinued

operations

- 74

n/a

Free cash flow 158 173 (8.7)

(1) See definitions and discussion under “Non-IFRS and additional GAAP measures”. (2) Per Note 4 to the unaudited interim Consolidated Financial Statements.

Shaw Communications Inc.

15

Discussion of operations

Consumer Three months ended November 30,

(millions of Canadian dollars)

2016

2015

Change %

Revenue 947 943 0.4

Operating income before restructuring costs and amortization (1) 405 419 (3.3)

Operating margin (1) 42.8% 44.4% (1.6pts)

(1) See definitions and discussion under “Non-IFRS and additional GAAP measures”.

In the quarter, net gains achieved in Internet RGUs of 16,964 were more than fully offset by phone and

Video RGU declines, including the anticipated seasonal disconnections of satellite Video subscribers in

the fall months. In aggregate, Consumer RGUs in the first quarter declined by 29,696 RGUs, a

meaningful improvement over the first quarter of fiscal 2016 where RGUs declined 43,750. The

improvement over the prior year was due primarily to the market launch of WideOpen Internet 150,

together with a reduction in phone unbundling activity from a year ago and lower cable video RGU

losses. Despite the continued improvements in RGU trends, the economic slowdown in parts of western

Canada, competitive pressures and wireline substitution continue to put downward pressure on

Consumer RGUs.

Consumer revenue for the current quarter of $947 million marginally improved by 0.4% or $4 million

compared to the prior year period. Improvements in revenue were driven by August 2016 rate increases,

growth in Internet RGUs and a year-over-year decrease in promotional costs.

Operating income before restructuring costs and amortization for the quarter of $405 million was lower

by 3.3% relative to the comparable quarter. The reduction in operating margin results in the quarter

primarily reflect higher expenses, most notably the impact of higher programming costs which more than

fully offset the revenue growth achieved in the period.

As compared to the fourth quarter of fiscal 2016, the current quarter revenue improved 1.0% or $9

million. Improvements were driven primarily by a full quarter of the August 2016 rate increase, lower

promotional costs and a full quarter of revenue from our reconnected customers in Fort McMurray.

These gains were partially offset by RGU declines and lower On Demand revenues. Operating income

before restructuring costs and amortization decreased 3.1% or by $13 million reflecting higher expenses

most notably programming costs and timing of various other administrative costs including sponsorship

related marketing costs.

On January 11, 2017, we announced a significant milestone in our video technology roadmap with the

market launch of BlueSky TV. BlueSky’s TV experience, powered by Comcast’s X1 technology,

provides ease-of-use and customization that is unprecedented in Canada. This leading technology

experience is now available to customers in Calgary, with subsequent launches in the remaining major

cities in our footprint planned throughout fiscal 2017. Also in the quarter, we shifted our In-Home

Technician team to a hybrid unit-based installation and service technician model, combining a

foundation of customer experience with technical skill that will deliver annualized operating cost savings

of approximately $16 million. This initiative resulted in a non-recurring restructuring charge of $10

million in the quarter.

Shaw Communications Inc.

16

Business Network Services

Three months ended November 30,

(millions of Canadian dollars)

2016

2015

Change

%

Revenue 144 136 5.9

Operating income before restructuring costs and amortization (1) 72 64 12.5

Operating margin (1) 50.0% 47.1% 2.9pts

(1) See definitions and discussion under “Non-IFRS and additional GAAP measures”.

Revenue of $144 million for the quarter was up 5.9% over the comparable period. The business,

excluding satellite services, increased revenues 7.7% in the current quarter primarily due to our

continued growth across the entire customer base as well as an August 2016 rate increase for video,

Internet and phone products.

Operating income before restructuring costs and amortization of $72 million for the quarter improved

12.5% over the comparable period. Consistent with the growth trends achieved in fiscal 2016, current

quarter improvements were due mainly to profitable customer growth partially offset by the incremental

costs associated with pursuing new customer opportunities including additional employee and marketing

related costs.

Revenue improved 2.9% or by $4 million over the fourth quarter of fiscal 2016, primarily due to

customer growth across our entire customer base as well as a full quarter of revenue after the August

2016 rate increases in our video, Internet and phone products. Operating income before restructuring

costs and amortization also improved by 2.9% or by $2 million over the fourth quarter due mainly to the

profitable customer growth.

Business Infrastructure Services

Three months ended November 30,

(millions of Canadian dollars)

2016

2015

Change %

Revenue 90 73 23.3 Operating income before restructuring costs and amortization (1) 32 25 28.0

Operating margin (1) 35.6% 34.2% 1.4pts

(1) See definitions and discussion under “Non-IFRS and additional GAAP measures”.

Revenue of $90 million for the current quarter increased 23.3% over the comparable period primarily

due to the December 2015 acquisition of INetU and continued customer growth. Excluding the effect of

foreign exchange, revenue for the U.S. based operations increased by 21.3% to US$67 million for the

three month period. Excluding the effect of INetU, revenue for the U.S. based operations increased by

5.6% to US$59 million for the three month period.

Operating income before restructuring costs and amortization improved over the comparable period by

28.0% for the current quarter. Excluding the effect of foreign exchange, operating income before

restructuring costs and amortization for the U.S. based operations increased by 22.9% to US$25 million

for the three month period. Year-over-year improvements were primarily due to the acquisition of INetU

and profitable customer growth.

Compared to the fourth quarter of 2016, revenue increased 4.7% or by $4 million and operating income

before restructuring costs and amortization was comparable as the incremental margin earned on

customer growth was offset by the timing of certain annual administrative costs and planned IT-related

enhancement costs incurred in the quarter. Excluding the impact of foreign exchange, revenue and

Shaw Communications Inc.

17

operating income before restructuring costs and amortization for U.S. based operations increased 1.5%

and flat respectively, compared to the fourth quarter of fiscal 2016.

Wireless

(millions of Canadian dollars) Three months ended November 30, 2016

Revenue 138

Operating income before restructuring costs and amortization (1) 30

Operating margin (1) 21.7%

(1) See definitions and discussion under “Non-IFRS and additional GAAP measures”.

The Company is reporting its third full quarter of results from its Wireless division that was acquired in

March 2016.

Revenue for the quarter decreased by $10 million over the fourth quarter of fiscal 2016 due mainly to a

reduction in handset revenue and a 1.5% decrease in average revenue per unit (“ARPU”) to $36.84,

partially offset by the impact of 9,470 added RGUs. Slower RGU growth and a decline in ARPU over

the prior quarter reflect our focus on the launch of Freedom Mobile, the rollout of our LTE-Advanced

network and significantly heightened competition in the market, particularly in the month of November.

Operating income before restructuring costs and amortization was comparable to the prior quarter as the

decrease in revenue and higher commercial costs associated with the branding transition from WIND to

Freedom Mobile were offset by a decrease in costs associated with handset sales, and lower dealer

commissions on fewer customer activations.

In the quarter, the Wireless division continued taking the necessary steps to becoming an enhanced

connectivity provider and achieved three important milestones. First, the launch of the new Freedom

Mobile brand, replacing WIND and signaling the Company’s renewed focus on making wireless service

more affordable while saving on trademark costs. Second, the rollout of our LTE-Advanced network in

the key markets of central Toronto and central Vancouver. Third, the introduction of the Freedom Wi-Fi

trial, allowing customers to connect to over 65,000 Shaw Go WiFi hotspots across western Canada.

Capital expenditures and equipment costs

Three months ended November 30,

(millions of Canadian dollars)

2016

2015

Change

%

Consumer and Business Network Services

New housing development 22 23 (4.3)

Success based 81 73 11.0 Upgrades and enhancements 71 93 (23.7)

Replacement 6 10 (40.0)

Building and other 25 16 56.3

Total as per Note 4 to the unaudited interim

consolidated financial statements 205 215 (4.7)

Business Infrastructure Services Total as per Note 4 to the unaudited interim

consolidated financial statements 21 30 (30.0)

Wireless Total as per Note 4 to the unaudited interim

consolidated financial statements 64 - n/a

Consolidated total as per Note 4 to the unaudited interim

consolidated financial statements 290 245 18.4

Shaw Communications Inc.

18

Capital investment was $290 million in the current quarter, an 18.4% increase over the comparable

period investment of $245 million driven primarily by the $64 million of added capital expenditures

from the Wireless division.

Consumer and Business Network Services

The combined Consumer and Business Network Services divisions investment in capital reduced 4.7%

or $10 million compared to the first quarter of fiscal 2016 primarily due to lower planned capital spend

on plant upgrades and enhancements offset partially by an increase in success based capital.

Success based capital for the quarter of $81 million was 11% higher than in the prior year. The higher

capital spend was driven primarily by advanced Internet WiFi modem purchases and installs offset

partially by lower phone installations.

For the quarter, investment in the combined upgrades and enhancement and replacement categories was

$77 million, a 25% decrease over the prior year due mostly to the timing of spend in network capacity

upgrades in support of enhanced broadband capacity and DOCSIS 3.1.

Investment in buildings and other of $25 million for the quarter was up $9 million over the comparable

period. The increase relates mostly to refurbishment expenditures in owned corporate facilities.

Business Infrastructure Services

Capital investment of $21 million for the quarter, decreased 30% or by $9 million primarily due to higher

spend in the prior year related to the investment in the Calgary, Alberta data centre. The current quarter

spend relates primarily to capital invested in core infrastructure and equipment to deploy customer

solutions.

Wireless

Capital investment of $64 million for the quarter represented investment for the continued improvement

in the network infrastructure primarily in the LTE-Advanced core and the radio network rollout readiness

project across the network as well as capital investments made on the upgrade of back office systems.

Shaw Communications Inc.

19

Discontinued operations – Shaw Media

On April 1, 2016, Shaw sold 100% of its wholly owned subsidiary Shaw Media Inc. to Corus, a related

party subject to common voting control for $2.65 billion, comprised of $1.85 billion in cash and

71,364,853 Corus Class B non-voting participating shares. Accordingly, the operating results and

operating cash flows for the previously reported Media division are presented as discontinued operations

separate from the Company’s continuing operations. Prior period financial information has been

reclassified to present the Media division as a discontinued operation. Three months ended November 30,

2016 2015

Revenue - 294 Eliminations(1) - (19)

- 275

Operating, general and administrative expenses

Employee salaries and benefits - 45 Purchases of goods and services - 131

- 176

Eliminations(1) - (19)

- 157

Amortization - 7

Accretion of long-term liabilities and provisions - 1 Other losses - 1

Income from discontinued operations before tax and gain on divestiture - 109

Income taxes - 29

Income (loss) from discontinued operations, net of tax - 80

(1) Eliminations relate to intercompany transactions between continuing and discontinued operations. The costs are

included in continuing operations as they are expected to continue to be incurred subsequent to the disposition.

Supplementary quarterly financial information

Quarter

Revenue

Operating

income before

restructuring

costs and

amortization (1)

Net income from

continuing

operations

attributable to

equity shareholders

Net income

attributable

to equity

shareholders

Net income (2)

Basic and

Diluted earnings

per share from

continuing

operations

Basic and

Diluted

earnings per

share

(millions of Canadian dollars except per share amounts)

2017

First 1,313 539 89 89 89 0.18 0.18

2016

Fourth 1,306 549 144 154 154 0.29 0.31

Third 1,283 555 58 700 704 0.11 1.44

Second 1,151 502 116 156 164 0.24 0.32

First 1,144 508 138 209 218 0.28 0.43

2015

Fourth 1,131 525 247 272 276 0.51 0.57

Third 1,135 527 136 202 209 0.28 0.42

Second 1,118 498 135 163 168 0.28 0.34

(1) See definition and discussion under “Non-IFRS and additional GAAP measures”. (2) Net income attributable to both equity shareholders and non-controlling interests

In the first quarter of fiscal 2017, net income decreased $65 million compared to the fourth quarter of

fiscal 2016 mainly due to a non-recurring provision related to the wind down of shomi operations

included in net other costs and revenue for the current quarter. Also contributing to the decreased net

income was lower operating income before restructuring costs and amortization, higher restructuring

charges and lower income from discontinued operations, partially offset by $27 equity income from our

Shaw Communications Inc.

20

investment in Corus and lower income taxes. See “Other income and expense items” for further detail

on non-operating items.

In the fourth quarter of fiscal 2016 net income decreased $550 million compared to the third quarter of

fiscal 2016 mainly due to lower income from discontinued operations relating primarily to the gain on

the divestiture of the former Media division recorded in the third quarter, decreased operating income

before restructuring costs and amortization, and higher income taxes. Partly offsetting the decrease in

net income were decreases in net other costs and revenues and restructuring costs. Net other costs and

revenue decreased primarily due to non-recurring charges recorded in the third quarter, including a $17

million impairment of goodwill relating to the Tracking business, a $51 million impairment of the

Company’s joint venture investment in shomi, a $20 million write-down of a private portfolio

investment, $12 million acquisition related costs and a $10 million loss from an equity accounted

associate.

Net income for the third quarter of fiscal 2016 increased $540 million compared to the second quarter of

fiscal 2016 mainly due to higher income from discontinued operations relating primarily to the gain on

the divestiture of the former Media division, increased operating income before restructuring costs and

amortization and lower income taxes. Partly offsetting the net income improvement in the quarter were:

i) decreased net other costs and revenue; ii) increased restructuring charges; and iii) increased

amortization. Net other costs and revenue decreased primarily due to $17 million impairment of

goodwill relating to the Tracking operations in the Business Networks Services division, a $51 million

impairment of the Company’s shomi joint venture investment, a $20 million write-down of a private

portfolio investment and a $10 loss from an equity accounted associate.

In the second quarter of fiscal 2016, net income decreased $54 million compared to the first quarter of

fiscal 2016 mainly due to decreased income from discontinued operations of $32 million, primarily due

to the seasonality of the Media business reflected in income from discontinued operations, net of tax, and

net other costs and revenue of $13 million. Net other costs and revenues decreased primarily due to $8

million of costs recorded in the quarter related to the acquisition of WIND and INetU.

In the first quarter of fiscal 2016, net income decreased $58 million compared to the fourth quarter of

2015 mainly due to a change in net other costs and revenues of $140 million and decrease in operating

income before restructuring costs and amortization of $17 million offset by an increase in income from

discontinued operations, net of tax, of $51 million and a decrease in income taxes of $50 million. Net

other costs and revenue decreased primarily due to a fourth quarter fiscal 2015 gain on the sale of

wireless spectrum of $158 million less the impact of a $27 million write-down of a private portfolio

investment in the same period offset by an increase in the equity loss of a joint venture interest in shomi

of $5 million in the first quarter of fiscal 2016.

In the fourth quarter of fiscal 2015, net income increased $67 million primarily due to improved net other

costs and revenue items of $191 million partially offset by lower income from discontinued operations,

net of tax, of $44 million and higher income tax expense of $70 million. The improvement in net other

costs and revenue items was due to the combined effect of the aforementioned sale of spectrum licenses

and write-down of a private portfolio investment during the fourth quarter and the $59 million net charge

arising in the third quarter related to an impairment of goodwill, write-down of IPTV assets and proceeds

received from the Shaw Court insurance claim.

In the third quarter of fiscal 2015, net income increased $41 million due to higher operating income

before restructuring costs and amortization of $29 million, an increase in income from discontinued

operations, net of tax, of $40 million, lower restructuring costs of $35 million and $11 million of

proceeds related to the Shaw Court insurance claim, partially offset by a charge for impairment of

goodwill of $15 million and write-down of IPTV assets of $55 million as well as the distributions

Shaw Communications Inc.

21

received from a venture capital fund in the second quarter. The impairment of goodwill was in respect of

the Tracking operations in the Business Network Services division and was a result of the Company’s

annual impairment test of goodwill and indefinite-life intangibles in the third quarter. The write-down of

IPTV assets was a result of the Company’s decision to work with Comcast to begin technical trials of

their cloud-based X1 platform.

In the second quarter of fiscal 2015, net income decreased $59 million due to lower income from

discontinued operations, net of tax, of $46 million and restructuring expenses of $36 million partially

offset by higher operating income before restructuring costs and amortization of $10 million, net other

costs and revenue items of $24 million due to the aforementioned venture capital fund distributions.

Other income and expense items

Amortization Three months ended November 30,

(millions of Canadian dollars)

2016

2015

Change %

Amortization revenue (expense)

Deferred equipment revenue 14 19 (26.3) Deferred equipment costs (34) (40) 15.0

Property, plant and equipment,

intangibles and other

(235)

(202)

16.3

Amortization of property, plant and equipment, intangibles and other increased 16.3% over the

comparable quarter due to amortization related to the new Wireless division and the amortization of new

expenditures exceeding the amortization of assets that became fully amortized during the periods.

Amortization of financing costs and Interest expense

Three months ended November 30,

(millions of Canadian dollars)

2016

2015

Change

%

Amortization of financing costs –

long-term debt

1

1

-

Interest expense 73 73 -

Interest expense for the quarter was comparable to the same period in the prior year.

Equity income (loss) of an associate or joint venture

For the quarter the Company recorded equity income of $27 million related to its interest in Corus. In

the comparable period, the Company recorded equity losses of $18 million related to its interest in

shomi.

Other losses

In the current quarter, the category is comprised primarily of a $107 million provision in respect of the

Company’s investment in shomi which announced a wind down of operations during the quarter. This

category also includes realized and unrealized foreign exchange gains and losses on U.S. dollar

denominated current assets and liabilities, gains and losses on disposal of property, plant and equipment

and minor investments, and the Company’s share of the operations of Burrard Landing Lot 2 Holdings

Partnership.

Shaw Communications Inc.

22

Income taxes

Income taxes are lower in the current quarter compared to the prior year mainly due to a reduction in net

income.

Financial position

Total assets were $15.4 billion at November 30, 2016 and August 31, 2016. Following is a discussion of

significant changes in the consolidated statement of financial position since August 31, 2016.

Current assets decreased $107 million due to decreases in cash of $116 million, partially offset by

increases in other current assets of $15 million. Cash decreased as the cash outlay for investing and

financing activities exceeded the funds provided by operations. Other current assets increased due to the

timing of payments related to prepaid expenses.

Investments and other assets increased $35 million primarily due to equity income and other

comprehensive income of associates related to the Company’s investment in Corus. Property, plant and

equipment increased $36 million due to capital investment in excess of amortization and the effect of

foreign exchange rates on the translation of ViaWest. Intangibles and goodwill increased $39 million

due to net software intangible additions and the ongoing effect of foreign exchange arising on translation

of ViaWest.

Current liabilities decreased $50 million during the quarter due to decreases in accounts payable and

accruals of $71 million and income taxes payable of $89 million, partially offset by increases of $115

million in current provisions. Accounts payable and accruals decreased due the timing of payment and

fluctuations in various payables including capital expenditures and interest. Income taxes payable

decreased due to tax installment payments, partially offset by the current period provision. Current

provisions increased primarily due to unpaid amounts relating to the current period provisions for the

wind down of the shomi investment and restructuring.

Long-term debt increased $47 million due to additional US dollar borrowings by ViaWest under its bank

credit facilities and the effect of foreign exchange rates on ViaWest’s debt and the Company’s US dollar

borrowings under its credit facility.

Other long-term liabilities decreased $18 million mainly due to actuarial gains on employee benefit plans

in the current quarter.

Shareholders’ equity increased $36 million primarily due to an increase in share capital of $54 million

and decrease in accumulated other comprehensive loss of $41 million, partly offset by a decrease in

retained earnings of $59 million. Share capital increased due to the issuance of 2,013,081 Class B non-

voting participating shares (“Class B Non-Voting Shares”) under the Company’s option plan and

Dividend Reinvestment Plan (“DRIP”). As at December 31, 2016, share capital is as reported at

November 30, 2016 with the exception of the issuance of a total of 1,073,922 Class B Non-Voting

Shares upon exercise of options under the Company’s option plan and the DRIP. Retained earnings

decreased due to dividends of $148 million, partially offset by current year earnings of $89 million.

Accumulated other comprehensive loss decreased due to the net effect of exchange differences arising on

the translation of ViaWest and U.S. dollar denominated debt designated as a hedge of the Company’s net

investment in those foreign operations as well as re-measurements recorded on employee benefit plans

and the Company’s share of other comprehensive income of associates.

Shaw Communications Inc.

23

Liquidity and capital resources

In the current quarter, the Company generated $158 million of free cash flow. Shaw used its free cash

flow along with cash of $116 million, borrowings of $20 million under ViaWest’s credit facility and

proceeds on issuance of Class B Non-Voting Shares of $3 million to fund the net working capital change

of $160 million, pay common share dividends of $96 million, make $31 million in financial investments,

pay $3 million in restructuring costs and pay $7 million in other net items.

The Company issues Class B Non-Voting Shares from treasury under its DRIP which resulted in cash

savings and incremental Class B Non-Voting Shares of $49 million during the three months ending

November 30, 2016. On December 16, 2016, the Company amended its DRIP to permit eligible

shareholders who are residents of the United States to enroll their Class A Participating Shares and Class

B Non-voting Participating Shares in the DRIP. Prior to this amendment, the DRIP was only available to

eligible shareholders who were residents of Canada.

As at November 30, 2016, the Company had $289 million of cash on hand, as well as approximately

$970 million of available credit under its $1.5 billion bank credit facility. On December 15, 2016, the

Company amended the terms of this bank credit facility to extend the maturity date from December 2019

to December 2021. The facility is used for working capital and general corporate purposes.

Shaw’s and ViaWest’s credit facilities are subject to customary covenants which include maintaining

minimum or maximum financial ratios.

Covenant Limit

Shaw Credit Facilities

Total Debt to Operating Cash Flow(1) Ratio < 5.00:1 Operating Cash Flow(1) to Fixed Charges(2) Ratio > 2.00:1

ViaWest Credit Facilities

Total Net Leverage Ratio(3) ≤ 6.50:1 (1) Operating Cash Flow, for the purposes of the covenants, is calculated as net earnings before interest expense, depreciation,

amortization and current and deferred income taxes, excluding profit or loss from investments accounted for on an equity basis, for

the most recently completed fiscal quarter multiplied by four, plus cash dividends and other cash distributions received in the most recently completed four fiscal quarters from investments accounted for on an equity basis.

(2) Fixed Charges are defined as the aggregate of interest expense for the most recently completed fiscal quarter multiplied by four and

dividends paid or accrued on shares (other than participating shares) during the most recently completed four fiscal quarters. (3) Total Net Leverage Ratio is calculated as the ratio of consolidated total debt under the facility as of the last day of the most recent

completed four fiscal quarters to Consolidated Adjusted EBITDA of ViaWest for the same period. Consolidated Adjusted EBITDA,

for the purposes of the covenants, is calculated similar to Operating income before restructuring and amortization with adjustments for certain items such as one-time expenses and extraordinary items.

At November 30, 2016 Shaw is in compliance with these covenants and based on current business plans,

the Company is not aware of any condition or event that would give rise to non-compliance with the

covenants over the life of the borrowings.

Based on the aforementioned financing activities, available credit facilities and forecasted free cash flow,

the Company expects to have sufficient liquidity to fund operations and obligations, including maturing

debt, during the upcoming fiscal year. On a longer-term basis, Shaw expects to generate free cash flow

and have borrowing capacity sufficient to finance foreseeable future business plans and refinance

maturing debt.

Shaw Communications Inc.

24

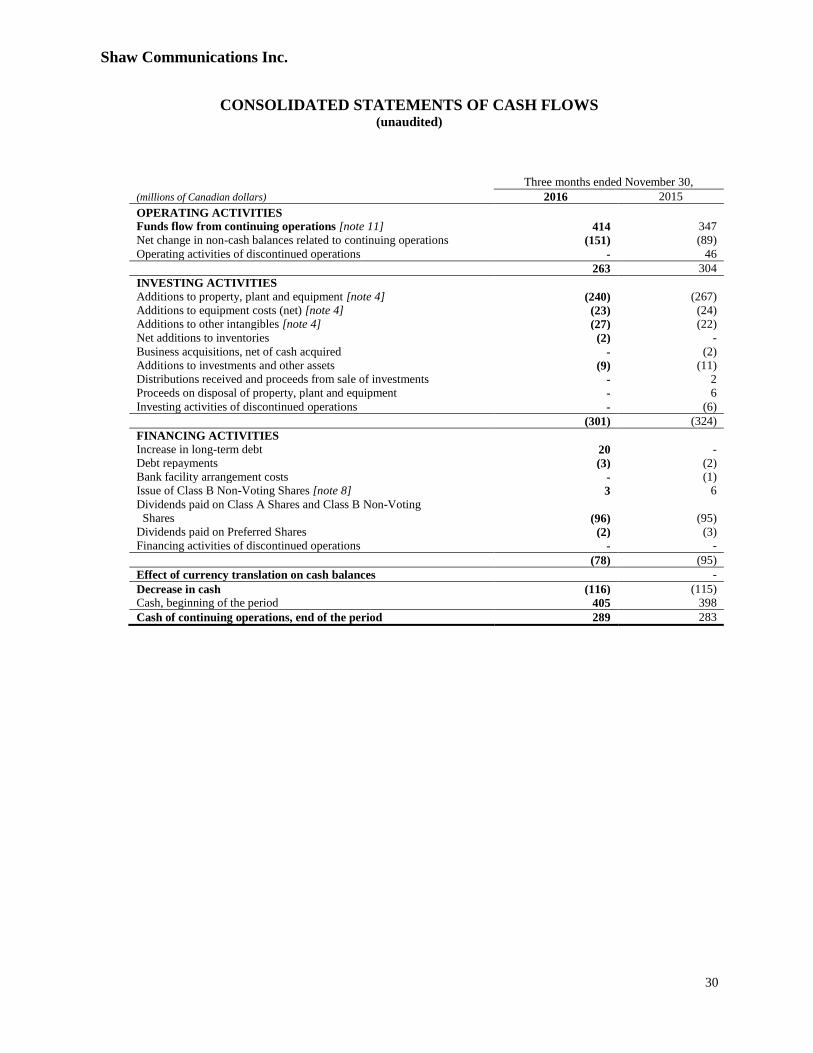

Cash Flow from Operations

Operating Activities Three months ended November 30,

(millions of Canadian dollars)

2016

2015

Change

%

Funds flow from operations 414 347 19.3

Net change in non-cash balances related to

operations

(151)

(89)

(69.7)

Operating activities of discontinued operations

-

46

(100.0)

263 304 (13.5)

For the three month period ended November 30, 2016, funds flow from operations increased over the

comparable period primarily due to higher operating income before restructuring costs and amortization,

lower income tax expense and lower pension funding, partially offset by higher restructuring costs

recorded during the quarter. The net change in non-cash working capital balances related to operations

fluctuated over the comparative periods due to changes in accounts receivable balances and the timing of

payment of current income taxes payable and accounts payable and accrued liabilities.

Investing Activities Three months ended November 30,

(millions of Canadian dollars) 2016 2015 Decrease

Cash flow used in investing activities (301) (324) 23

The cash used in investing activities decreased over the comparable quarter due primarily to reduced

cash outlays for capital expenditures in the current year.

Financing Activities

The changes in financing activities during the comparative periods were as follows:

Three months ended November 30,

(millions of Canadian dollars) 2016 2015

Bank loans – net borrowings - - ViaWest’s credit facility and finance lease obligations 18 (2)

WIND finance lease obligations (1) -

Bank facility arrangement costs - (1) Dividends (98) (98)

Issuance of Class B Non-Voting Shares 3 6

Financing activities of discontinued operations - -

(78) (95)

Accounting standards

The MD&A included in the Company’s August 31, 2016 Annual Report outlined critical accounting

policies, including key estimates and assumptions that management has made under these policies, and

how they affect the amounts reported in the Consolidated Financial Statements. The MD&A also

describes significant accounting policies where alternatives exist. The condensed interim consolidated

financial statements follow the same accounting policies and methods of application as the most recent

annual consolidated financial statements except as described below.

Shaw Communications Inc.

25

Change in accounting policy

In November 2016, the IFRS Interpretations Committee (“the Committee”) published a summary of its

meeting discussion regarding a request to clarify how an entity determines the expected manner of

recovery of an intangible asset with an indefinite useful life for the purposes of measuring deferred tax in

accordance with IAS 12 Income Taxes. Although the Committee decided not to add this issue to its

agenda, the Committee noted that an intangible asset with an indefinite useful life is not a non-

depreciable asset because a non-depreciable asset has an unlimited (or infinite) life, and that indefinite

does not mean infinite. Consequently, the fact that an entity does not amortize an intangible asset with an

indefinite useful life does not necessarily mean that the entity will recover the carrying amount of that

asset only through sale and not through use. As such, the Company changed retrospectively its

accounting policy for the accounting of deferred tax on intangible assets with indefinite useful lives to be

in line with the Committee discussions.

The following table summarizes the impact of this change of accounting policy on previously reported

consolidated statements of financial position. The change of accounting policy did not have an impact

on the previously reported consolidated statements of income or consolidated statements of cash flows.

Increase (decrease) to previously reported amounts: As at August 31,

(millions of Canadian dollars) 2016 2015

Goodwill 143 182

Deferred income tax liabilities 740 779

Retained earnings (1) (597) (597) (1) Included in Shareholders’ equity - Common and preferred shareholders

Related Party Transactions

The Company’s transactions with related parties are discussed in its Management’s Discussion and

Analysis for the year ended August 31, 2016 under “Related Party Transactions” and under Note 27 of

the Consolidated Financial Statements of the Company for the year ended August 31, 2016. There has

been no material change in the Company’s transactions with related parties between August 31, 2016 and

November 30, 2016.

Financial Instruments

There has been no material change in the Company’s risk management practices with respect to financial

instruments between August 31, 2016 and November 30, 2016. See “Known Events, Trends and

Uncertainties – Interest Rates, Foreign Exchange Rates and Capital Markets” in the Company’s

Management’s Discussion and Analysis for the year ended August 31, 2016 and the section entitled

“Risk Management” under Note 28 of the Consolidated Financial Statements of the Company for the

year ended August 31, 2016.

Risks and Uncertainties

The significant risks and uncertainties affecting the Company and its business are discussed in the

Company’s August 31, 2016 Annual Report under “Known events, trends, risks and uncertainties” in

Management’s Discussion and Analysis.

Shaw Communications Inc.

26

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION (unaudited)

[millions of Canadian dollars] November 30, 2016

August 31, 2016

August 31, 2015

(restated, note 2) (restated, note 2)

ASSETS

Current

Cash 289 405 398

Accounts receivable 259 268 468

Inventories 68 65 60

Other current assets 153 138 78

Asset held for sale - - 5

769 876 1,009

Investments and other assets [notes 12 and 13] 888 853 97

Property, plant and equipment 4,643 4,607 4,220

Other long-term assets 281 275 259

Deferred income tax assets 6 6 14

Intangibles 7,466 7,450 7,459

Goodwill 1,338 1,315 1,688

15,391 15,382 14,746

LIABILITIES AND SHAREHOLDERS’ EQUITY

Current

Accounts payable and accrued liabilities 873 944 887

Provisions 148 33 52