Companies Act 2013 IMPACT ON SMALL & MEDIUM COMPANIES CA DS VIVEK Partner, Suresh & Co., www. sureshandco.com

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Companies Act 2013

IMPACT ON SMALL & MEDIUM COMPANIES

CA DS VIVEKPartner, Suresh & Co.,

www. sureshandco.com

A company may be an OPC having a sole member.

NEW CONCEPT – ONE PERSON COMPANY

Formation of Company – Section 3

Subscriber of one person company (OPC) shall nominate another person

Nominated person’s consent is required at the time of incorporation

MOA of OPC to have a specific succession clause stating name of such person

Nominee may be changed – to be reported to ROC

Suresh & Co12 Dec 2013

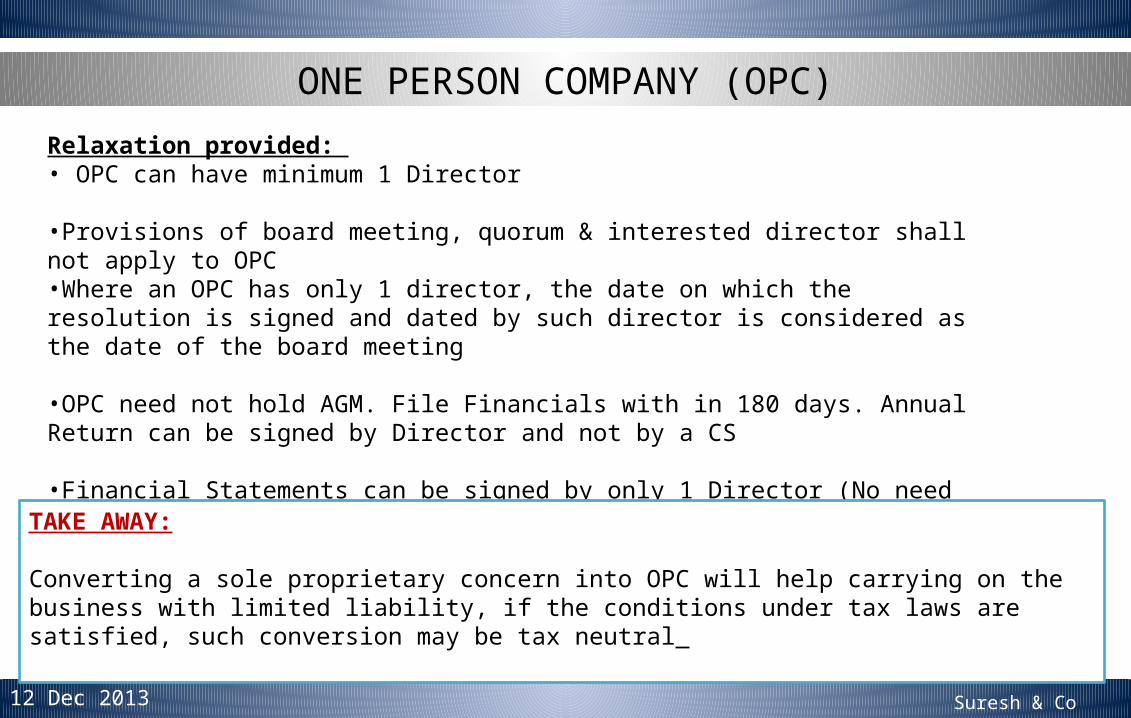

ONE PERSON COMPANY (OPC)

Relaxation provided: • OPC can have minimum 1 Director

•Provisions of board meeting, quorum & interested director shall not apply to OPC•Where an OPC has only 1 director, the date on which the resolution is signed and dated by such director is considered as the date of the board meeting

•OPC need not hold AGM. File Financials with in 180 days. Annual Return can be signed by Director and not by a CS

•Financial Statements can be signed by only 1 Director (No need for a Cash Flow)

•OPC can contract with the sole member who is DirectorTAKE AWAY:

Converting a sole proprietary concern into OPC will help carrying on the business with limited liability, if the conditions under tax laws are satisfied, such conversion may be tax neutral

Suresh & Co12 Dec 2013

ONE PERSON COMPANY (OPC)

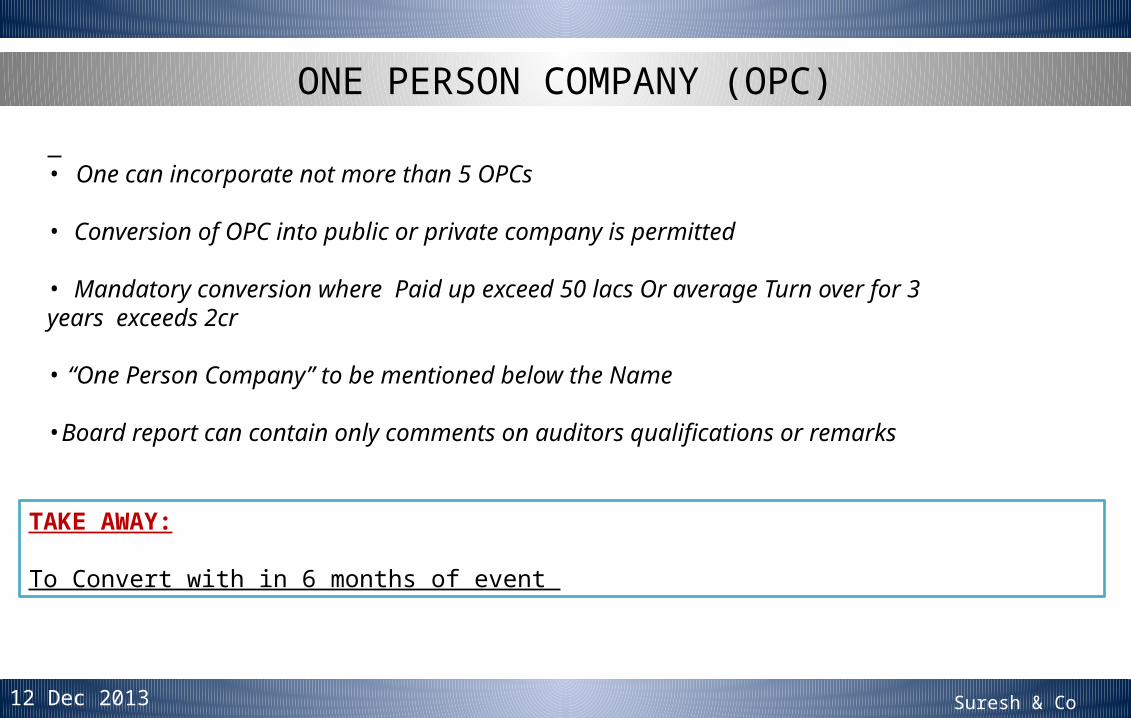

• One can incorporate not more than 5 OPCs

• Conversion of OPC into public or private company is permitted

• Mandatory conversion where Paid up exceed 50 lacs Or average Turn over for 3 years exceeds 2cr

• “One Person Company” to be mentioned below the Name

•Board report can contain only comments on auditors qualifications or remarks

TAKE AWAY:

To Convert with in 6 months of event

Suresh & Co12 Dec 2013

ONE PERSON COMPANY (OPC)Incorporation of OPC

Natural PersonIndian Citizen &

ResidentPrior Consent of Nominee

•

Board Meetings

1 per calendar half year If only 1 director

No Meeting is required, merely intimation to company by the Director

Suresh & Co12 Dec 2013

ONE PERSON COMPANY (OPC)Section 193 - Contracts by one person company

OPC either limited by capital or guarantee

Enters into a contract with sole members who is also the Director

The Terms of Contract

Contained in Memorandum Recorded in the Minutes of 1st Board Meeting held next after entering the contract

OR

• Sec 193 not applicable to the contracts entered by Co. in the ordinary course of business• Every such contract entered by Co. u/s 193 shall intimate ROC within 15 days of its approval by board

Suresh & Co12 Dec 2013

SMALL COMPANY

Not a Public Company

Paid up share capital less than 50 Lacs or higher amount as may be prescribed (not exceeding Rs.5 Crores)

Turn over not more than Rs.2 Crore or higher amount as may be prescribed(not exceeding Rs.20 Crore)

Not a holding or Subsidiary Company

Suresh & Co12 Dec 2013

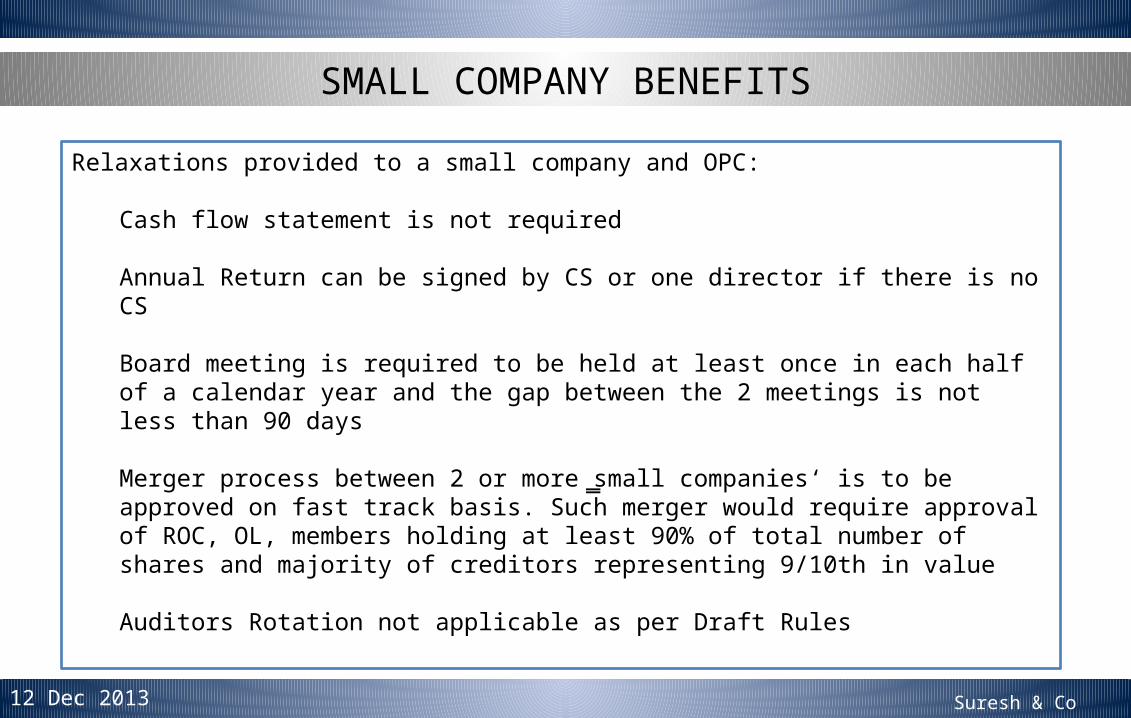

SMALL COMPANY BENEFITS

Relaxations provided to a small company and OPC:

Cash flow statement is not required

Annual Return can be signed by CS or one director if there is no CS

Board meeting is required to be held at least once in each half of a calendar year and the gap between the 2 meetings is not less than 90 days

Merger process between 2 or more @small companies‘ is to be approved on fast track basis. Such merger would require approval of ROC, OL, members holding at least 90% of total number of shares and majority of creditors representing 9/10th in value

Auditors Rotation not applicable as per Draft Rules

Suresh & Co12 Dec 2013

Benefits for Private Limited Company- New Act

Loan for Purchase of own Shares can continue to be given by Pvt Co ( sec 67 of new Act ) ( Sec 77 of Old Act)

Sec 164 ( 1) & (2) provides various scenarios for Directors Disqualification of Appointment . As per Sec 164 (3) a Pvt Co in its Article provides for Additional Clause for disqualification of directors. This can be beneficial to have business specific disqualifications.

Retirement of Directors by rotation – continues to be not applicable ( Sec 152(6) of New Act & Sec 255(1) of Old Act )

Restriction on Remuneration to MD & WTD– in case of inadequate profits applicable only to public co. ( Sec 197 of the New Act and Sec 309 of the Old Act)

Section 190 provides Inspection by Members Copies of employment contracts/details of employment contracts with Managing Director or WTD . This is exempted for a Pvt Co.

Suresh & Co12 Dec 2013

Benefits for Private Limited Company- New Act-2

Sec 149(1) prescribes at least 1 Women Director for prescribed class of companies. The prescribed class does not have Pvt Co ( Listed Co & Public Co with paid up capital 100cr or more OR Turnover 300cr or more)

Sec 149(4) specifies 1/3rd Independent Directors for listed Cos and prescribed no. for prescribed class of public company. Pvt Co need not have independent directors. ( Public Co with paid up capital 100cr or more OR Turnover 300cr or more OR aggregate loans or deposits outstanding more than 200 cr )

Only listed Co to have Small Share holders Director (optional ) and not for Pvt Co.

Suresh & Co12 Dec 2013

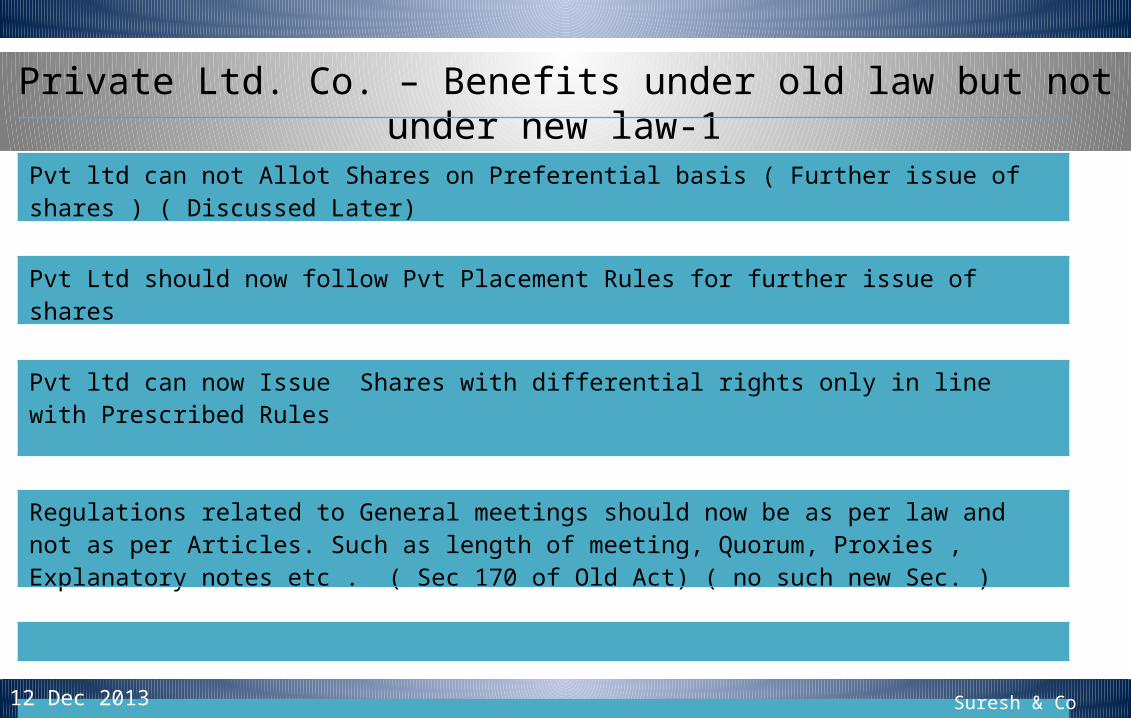

Private Ltd. Co. – Benefits under old law but not under new law-1

Pvt ltd can not Allot Shares on Preferential basis ( Further issue of shares ) ( Discussed Later)

Pvt Ltd should now follow Pvt Placement Rules for further issue of shares

Pvt ltd can now Issue Shares with differential rights only in line with Prescribed Rules

Regulations related to General meetings should now be as per law and not as per Articles. Such as length of meeting, Quorum, Proxies , Explanatory notes etc . ( Sec 170 of Old Act) ( no such new Sec. )

Suresh & Co12 Dec 2013

Private Ltd. Co. – Benefits under old law but not under new law-2

Directors appointment requires consent, earlier required only for Public Company. To be filed with ROC with in 30 days

Director now not eligible for appointment – if not filed Statements or Annual Returns even of Pvt Ltd

A Director who wants to be elected should file Statutoy notice not less than 14 days as per Sec 160 of new Act ( earlier exemption to Pvt Co as per Sec 257(2) of Old Act )

All Directors appointment can not be voted by a single resolution ( Earlier Sec 263(1) of Old act gave exemption to Pvt Co. Sec 162 of new act applicable for all companies.

Pvt Co also has to appoint Key Managerial Persons now ( discuused later) if certain conditions are met ( Sec 203 of New Act) ( Earlier Sec 269 exempted appointment of MD or Whole Time Director for Pvt. Co

Suresh & Co12 Dec 2013

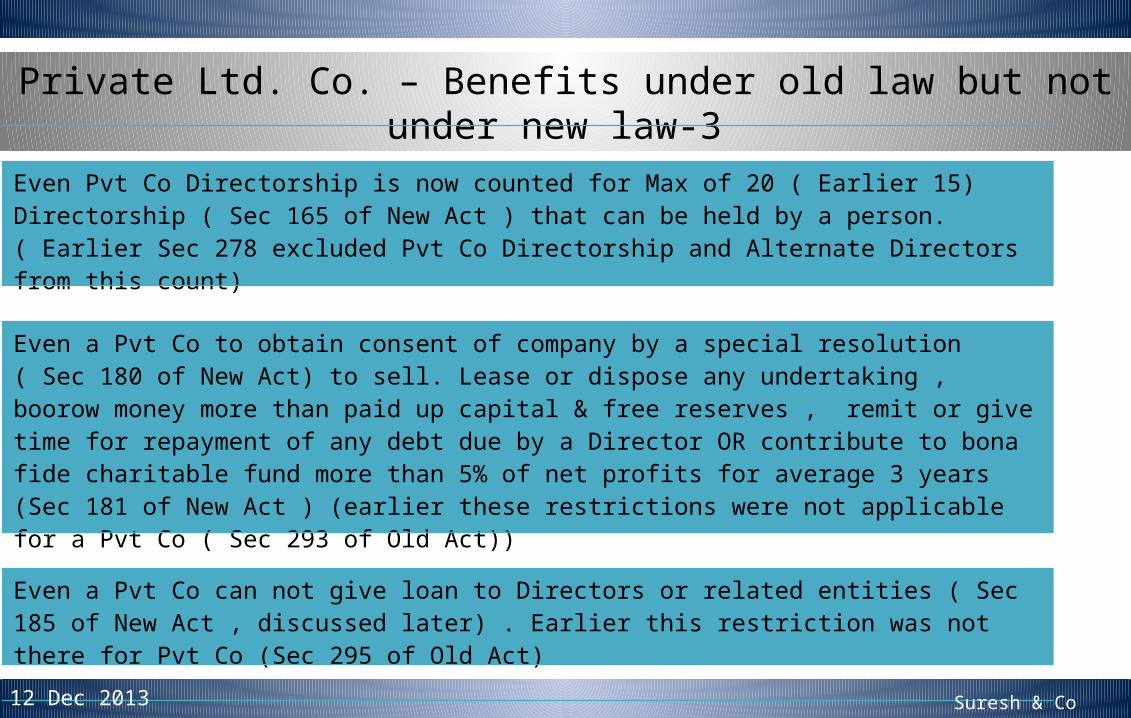

Private Ltd. Co. – Benefits under old law but not under new law-3

Even Pvt Co Directorship is now counted for Max of 20 ( Earlier 15) Directorship ( Sec 165 of New Act ) that can be held by a person. ( Earlier Sec 278 excluded Pvt Co Directorship and Alternate Directors from this count)

Even a Pvt Co to obtain consent of company by a special resolution ( Sec 180 of New Act) to sell. Lease or dispose any undertaking , boorow money more than paid up capital & free reserves , remit or give time for repayment of any debt due by a Director OR contribute to bona fide charitable fund more than 5% of net profits for average 3 years (Sec 181 of New Act ) (earlier these restrictions were not applicable for a Pvt Co ( Sec 293 of Old Act))

Even a Pvt Co can not give loan to Directors or related entities ( Sec 185 of New Act , discussed later) . Earlier this restriction was not there for Pvt Co (Sec 295 of Old Act)

Suresh & Co12 Dec 2013

Private Ltd. Co. – Benefits under old law but not under new law-4

Even in Pvt Co Interested Director cannot participate in a Board Meeting where a contract in which he is interest is discussed ( New Sec 184) Earlier Old Sec 300(2) exempted Pvt Co. from this. In case there are only 2 Directors and one is Interested, it can not be taken up in Board Meeting

Even Pvt Co now have restrictions on granting loans or investing in other companies subject to obtaining a special resolution ( Sec 186 of New Act). ( Earlier Sec 370(2) & 370(14) gave relaxation from these provisions to Pvt. Co.)

Even a Pvt Ltd should now file decleration for Commencement of Business ( Discussed later)

Suresh & Co12 Dec 2013

Preferential Allotment

• Preferential issue (Unlisted companies)– Issue of shares on preference basis to be authorized by Articles – Special resolution– Detailed disclosure to be made in the explanatory statement to notice – Pricing of a preferential issue of shares by a company shall be

determined by a Registered Valuer – Amounts received as share application money by private companies

also will not be available for use until allotment of shares

Suresh & Co12 Dec 2013

Private Ltd Co. - Private Placement

Issue of a Private Placement offer letter to not more than 50 persons

The above letter to be accompanied by an application form addressed specifically to that person

Approval by Special Resolution

Offer Shall not be made to more than 200 persons in a Financial Year (QIB’s & ESOP excluded for this Purpose), Max 4 with gap of 60 days

Allottee under private placement shall not transfer his securities to more than 20 persons during a quarter

Only 1 offer in a quarter and 4 in a year is permitted with a gap of 60days

Offer size per person shall be Rs. 50,000 or more .

Suresh & Co12 Dec 2013

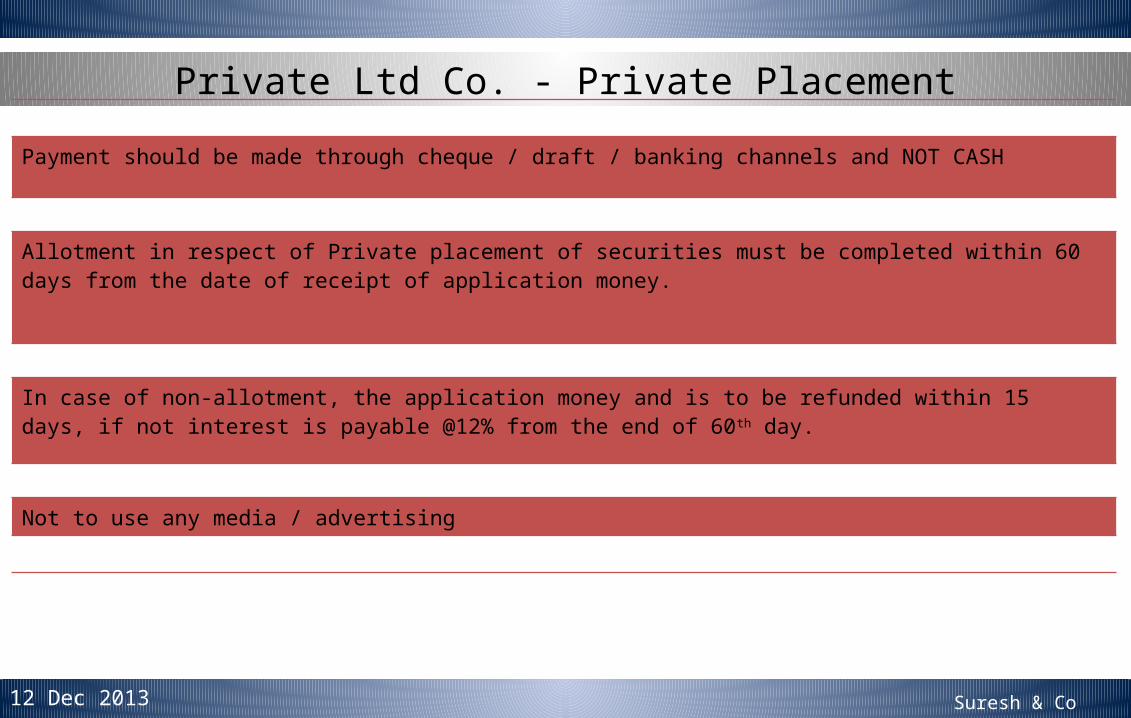

Private Ltd Co. - Private Placement

Payment should be made through cheque / draft / banking channels and NOT CASH

Allotment in respect of Private placement of securities must be completed within 60 days from the date of receipt of application money.

In case of non-allotment, the application money and is to be refunded within 15 days, if not interest is payable @12% from the end of 60th day.

Not to use any media / advertising

Suresh & Co12 Dec 2013

Conditions for issue of equity shares with differential rights. (As per draft Rules)-1

• issue of shares with differential rights to be authorized by articles of association • (b) special resolution passed at a general meeting (postal ballot in case of listed

companies)• (c) shares with differential rights shall not be more than 25% total post-issue paid

up equity share capital • (d) track record of dividend payment of at least 10% for last 3 years immediately

before issue • (e) no default in filing financial statements and annual returns for 5 years

immediately before issue; • (f) the company has not been convicted of any offence under

i) Reserve Bank of India Act, 1934 , ii) Securities and Exchange Board of India Act, 1992, iii) Securities Contract Regulation Act, 1956, iv) Foreign Exchange Management Act, 1999 etc.,

Suresh & Co12 Dec 2013

Conditions for issue of equity shares with differential rights. (As per draft Rules)

• no subsisting default in• i) payment of a declared dividend• ii) repayment of deposits• iii) redemption of shares or debentures • Iv) payment of interest on such deposits/ preference shares/ debentures• v) repayment of any term loan/ interest to scheduled banks or public financial

institution • vi) Statutory payments relating to its employees

Complete particulars to be given in the explanatory statement to notice calling general meeting

Conversion of existing share capital with voting rights to shares with differential rights and vice- versa is not permitted

Detailed disclosure to be made in Directors report

Suresh & Co12 Dec 2013

Commencement of Business & Borrowing Power

Incorporation (Private or Public)

Declaration filed within 180 days

- Subscription money Received- Verification of registered office

YES

Commence Business/ Exercise Borrowing powers

NOROC may strike

off the company’s

name

Subscribers to bring in subscription money within 180 days

Suresh & Co12 Dec 2013

Issue of Share CertificatesCertificate for Stipulated time for issuance of certificates

Shares – on subscription to the MOA and AOA i.e. on incorporation of a Company

within 2 months from the date of incorporation

Shares – allotted subsequent to incorporation within 2 months from the date of allotment if shares are issued in physical form;

Shares – on transfer within 1 month from the date of receipt of the instrument of transfer

Suresh & Co12 Dec 2013

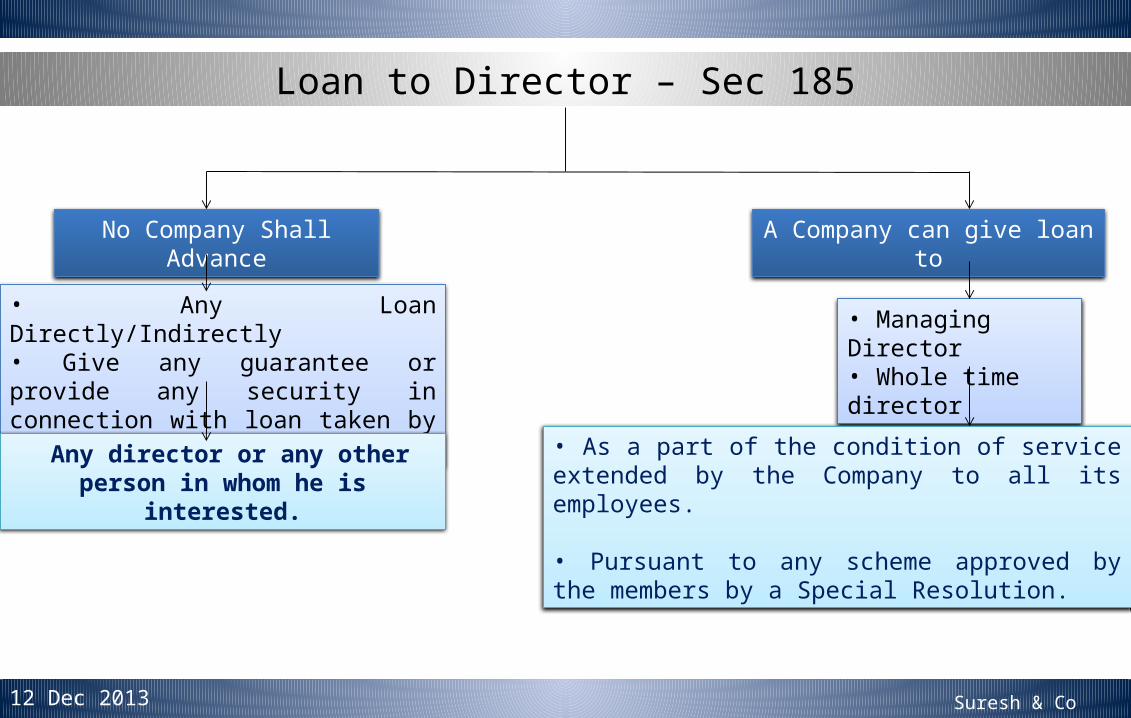

Loan to Director – Sec 185

• Any Loan Directly/Indirectly• Give any guarantee or provide any security in connection with loan taken by

No Company Shall Advance

Any director or any other person in whom he is interested.

A Company can give loan to

• Managing Director• Whole time director

• As a part of the condition of service extended by the Company to all its employees.

• Pursuant to any scheme approved by the members by a Special Resolution.

Suresh & Co12 Dec 2013

Loan to Directors

• A Company can however provide loan or give guarantee or provide security for the due repayment of any loan if it is in the ordinary course of its business.

• The rate of interest shall not be less than the rate of interest prescribed by RBI.

Penal consequences for contravention of Sec.185

• The Company shall be punishable with fine which shall not be less than Rs. 5 Lacs may extend to Rs. 25 Lacs

• The person to whom the loan etc is given shall be punishable with imprisonment which may extend to 6 months or with fine which shall not be less than Rs. 5 Lacs may extend to Rs. 25 Lacs or with both.

Suresh & Co12 Dec 2013

Acceptance of Deposits

Particulars Companies Act 1956 Companies Act 2013

Share Application Money To be refunded if shares not allotted within specified period (i.e. 180 days )

If the securities are not allotted within 60 days & failed to refund within 15 days, treated as Deposit

Amount Received from an employee

Any amount received from an employee by way of security deposit was not treated as deposit

Any amount received from employee exceeding his annual salary to be treated as Deposit.

Amount Received for Supply of Goods/Services

Was not a Deposit If the amount not appropriated against supply of goods /services within 180 days

Advance against sale of Property Was not a Deposit Consider as Deposit if the agreement not duly registered

The new deposit rules has narrowed acceptance of Deposits :

Suresh & Co12 Dec 2013

Annual Returns – Sec 92 The return to be prepared as on close of the financial year and NOT on AGM date

Content of the returns are

Details of Registered office, Principal Business Activities, Particulars of Holding-Subsidiary-Associate Companies

Particulars of Shares, Debenture and Securities and pattern of share holding.

Details of Members and Debenture holders and changes therein

Details of Promoters, Directors and KMP and changes therein

Attendance details and meeting details of members, Board and its various committees.

Remuneration of Directors and KMP

Suresh & Co12 Dec 2013

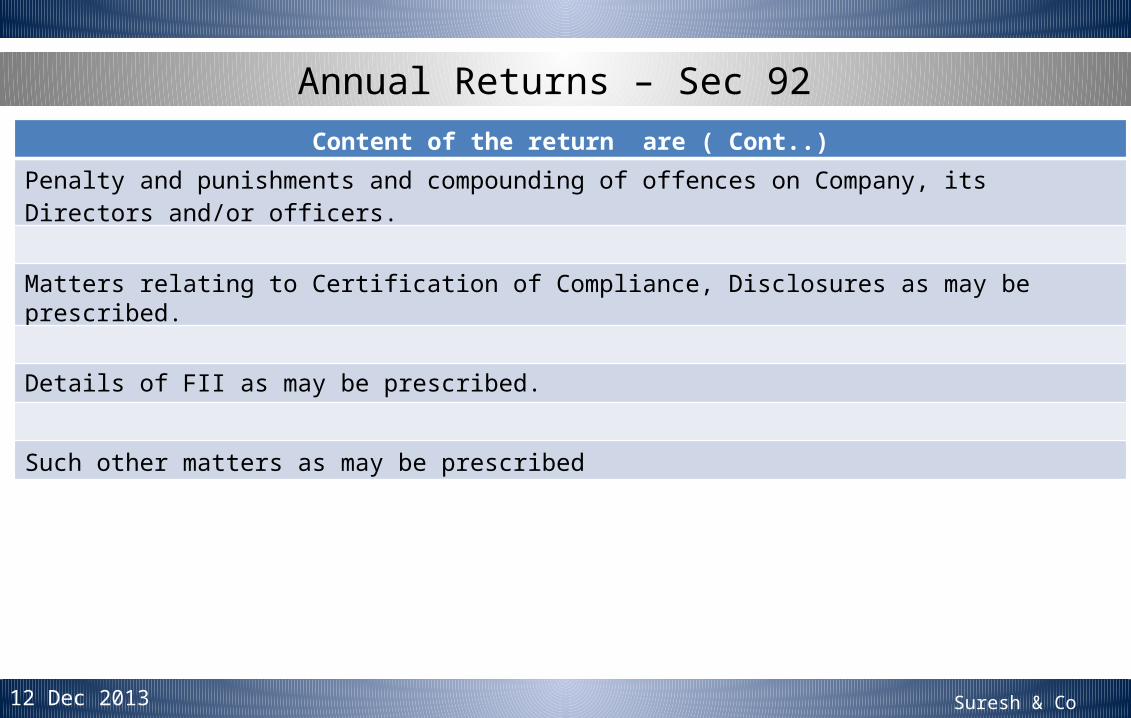

Annual Returns – Sec 92 Content of the return are ( Cont..)

Penalty and punishments and compounding of offences on Company, its Directors and/or officers.

Matters relating to Certification of Compliance, Disclosures as may be prescribed.

Details of FII as may be prescribed.

Such other matters as may be prescribed

Suresh & Co12 Dec 2013

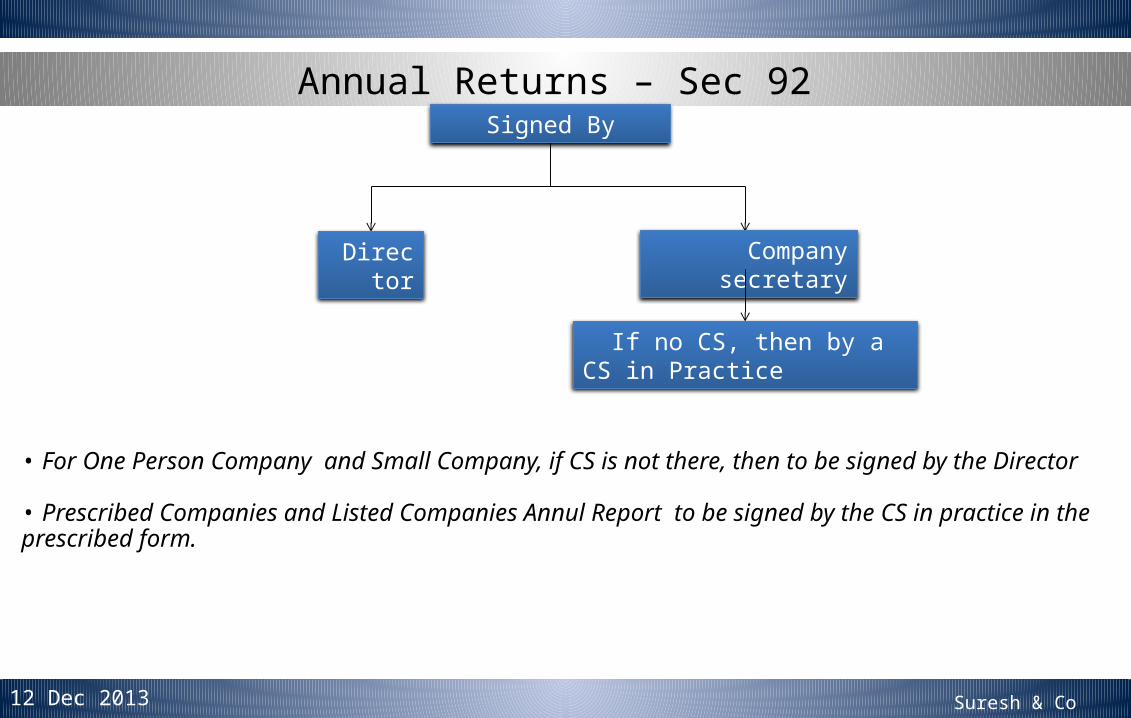

Annual Returns – Sec 92 Signed By

Director Company secretary

If no CS, then by a CS in Practice

• For One Person Company and Small Company, if CS is not there, then to be signed by the Director

• Prescribed Companies and Listed Companies Annul Report to be signed by the CS in practice in the prescribed form.

Suresh & Co12 Dec 2013

Annual Returns – Sec 92

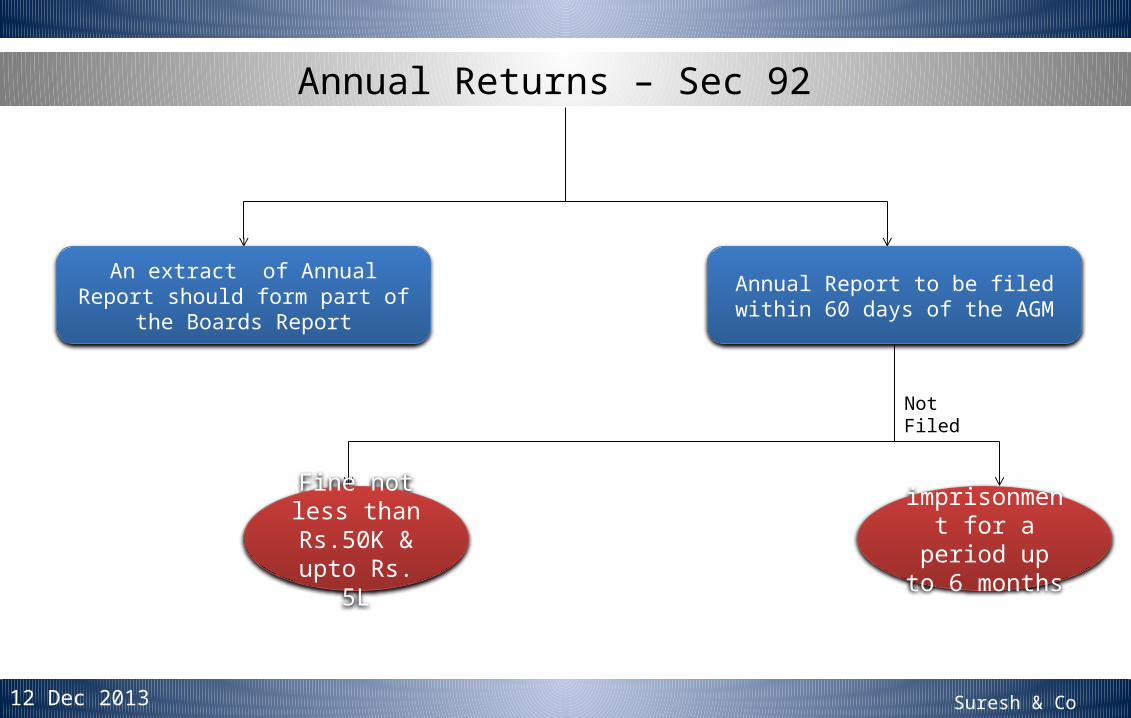

An extract of Annual Report should form part of the Boards Report

Annual Report to be filed within 60 days of the AGM

Not Filed

Fine not less than Rs.50K &

upto Rs. 5L

imprisonment for a period up

to 6 months

Suresh & Co12 Dec 2013

Accounts

Particulars Provisions under Companies Act 2013

Financial Statements FY is April to March . For Companies Incorporated after 1st Jan , it is next March . 2 years transition period

Signing of financial statements • Financial Statements to be signed at least by

Chairperson of the company, if authorized by BOD; or 2 directors including MD, where there is one; and CEO if he is a Director, CFO and CS, wherever they are appointed

Consolidated financial statements for all holding Co.

Suresh & Co12 Dec 2013

Accounts

Particulars Provisions under Companies Act 2013

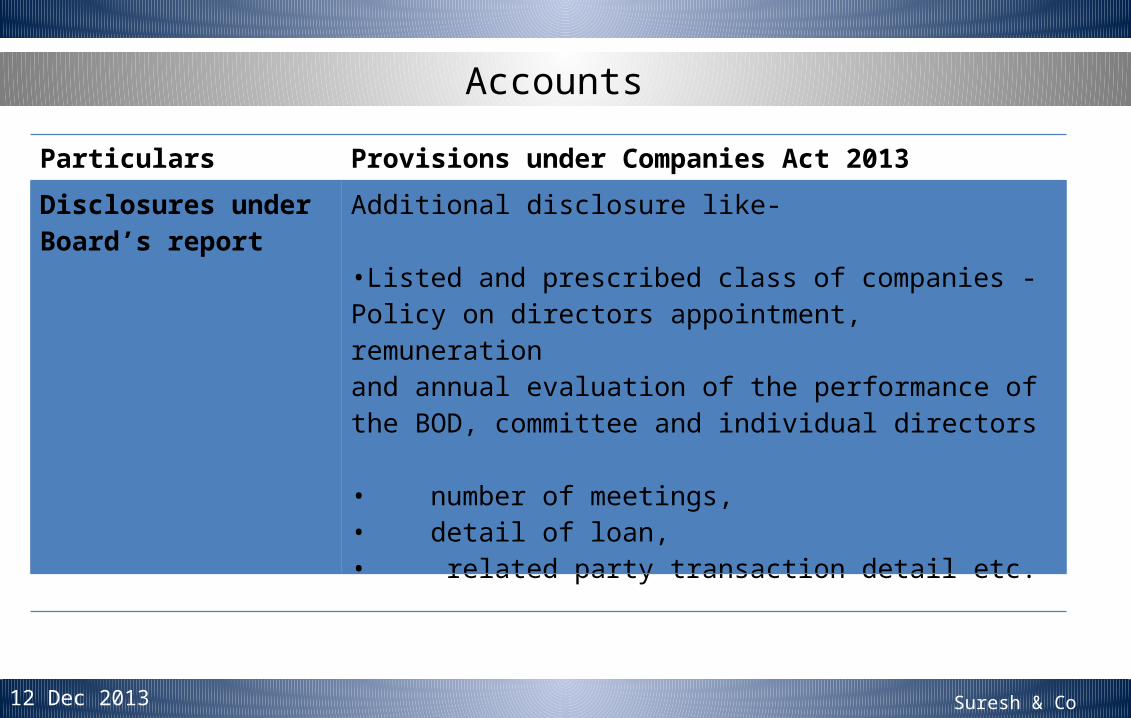

Disclosures under Board’s report

Additional disclosure like-

•Listed and prescribed class of companies - Policy on directors appointment, remuneration and annual evaluation of the performance of the BOD, committee and individual directors

• number of meetings, • detail of loan, • related party transaction detail etc.

Suresh & Co12 Dec 2013

Accounts Particulars Provisions under Companies Act 2013

Authority on Accounting and Auditing Standard

National Financial Reporting Authority (Role of auditing and accounting standard) to make recommendation to Central Government

Filing of Balance Sheet & Profit & Loss

Filing of Balance Sheet and P/L separately has been withdrawn . (major concern on sensitive information being available to competitors , customers etc)

Filing with ROC In case financials not adopted at AGM or AGM got adjourned, then un-adopted financial statement shall be filed to ROC within 30 days

Suresh & Co12 Dec 2013

Auditor AppointmentAppointment

Auditors Appointment and re-appointment

• To be appointed at first AGM • Who shall hold office till conclusion of 6th AGM• Gap of 5 years required for reappointment

Intimation to Registrar of Companies (ROC) and Duty of auditor’s when they resign

• Within 15 days of appointment in AGM• Onus on Company • Retiring auditor to file a statement with the ROC as well as the Company, within 30 days of resignation, indicating reasons .

AUDIT TERM Of an individual as an auditor 1 term of 5 consecutive years Of an audit firm as an auditor 2 terms of 5 consecutive years Cooling off period of 5 years before next appointment

Suresh & Co12 Dec 2013

Auditor Liabilities for Willful Default Liability

contravened the provisions of section 139, 143, 144 and 145 willfully with the intention to deceive the company or its shareholders or tax authorities,

Imprisonment for a term which may extend to 1 year

Fine not less than Rs.1L but may extend upto Rs.25L

The affected Person including the statutory authorities can claim damages

Penalty for professional misconduct – NFRA shall have power to investigate, either suo moto or on reference made by CG ( Rs.1,00,000/- may to extend 5 times of fee for Individuals / Rs. 10,00,000/- may extend to 10 times of fee received in case of firms.

Suresh & Co12 Dec 2013

Internal Auditor

• Appointment • Such class or classes of Companies as may prescribed need to compulsory appoint Internal Auditor to conduct the

internal audit of functions and activities of the company • Qualification • Internal Auditor shall either be a CA or a cost accountant, or such other professional as may be decided by the BOD

• CARO contained provisions requiring auditor‘s comments on existence and efficacy of internal audit system in case of listed companies and / or companies having net worth > ` 50 lakhs or average annual turnover > ` 5 crores for a period of 3 consecutive FY immediately preced-ing the FY concerned. 2013 Act contains specific provision of appointment of internal auditor • Draft Rules • Prescribed class of companies means: • listed companies ; and • public companies-

– with paid-up capital of ` 10 crores or more, – with outstanding loans or borrowings from banks or public financial institutions exceeding ` 25 – crores or which have accepted deposits of ` 25 crores or more at any point of time during the last FY

Suresh & Co12 Dec 2013

Appointment of KMP ( Sec 203)

• All Companies with paid up Capital above 5Cr should appoint KMP• KMPs are

- Managing Director or CEO or Manager, or in their absence a Whole Time Director- Chief Financial Officer- Company Secretary

• Chairperson can not be MD or CEO• KMP shall not hold office in more than 1 company other than

subsidiary ( KMP can be director in another company with approval of the Board )

Suresh & Co12 Dec 2013

Liability of Key Managerial PersonKey Managerial Personnel (KMP) includes

MD CEO or Manager Whole time Director Company Secretary CFO

Restrictions on forward dealing/insider trading by directors/ KMP

No director/ KMP can be involved in forward dealing or buying options in shares/debentures of company or its holding/ subsidiary/associate company.

No person (including director/ KMP) shall enter into insider trading.

Suresh & Co12 Dec 2013

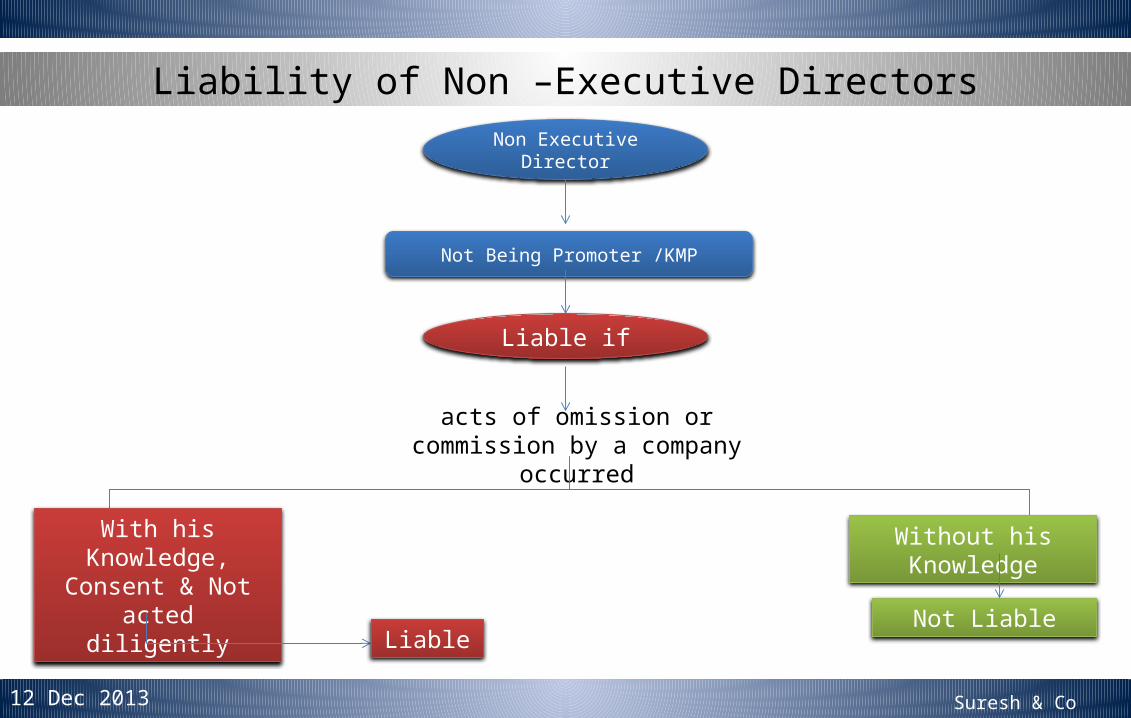

Liability of Non –Executive Directors

Non Executive Director

Not Being Promoter /KMP

Liable if

acts of omission or commission by a company occurred

With his Knowledge, Consent & Not acted

diligently

Without his Knowledge

LiableNot Liable

Suresh & Co12 Dec 2013

Powers of Directors at BM onlyPowers exercised only by means of resolution passed at a meeting of board (Contained in Act)

To make calls on shareholders in respect of money unpaid on their shares

To authorise buy-back of securities under section 68

To issue securities, including debentures, whether in India or outside

To borrow monies

To grant loans or give guarantee or provide security in respect of loans

To approve financial statement and the director’s report

To approve business restructuring decisions

Suresh & Co12 Dec 2013

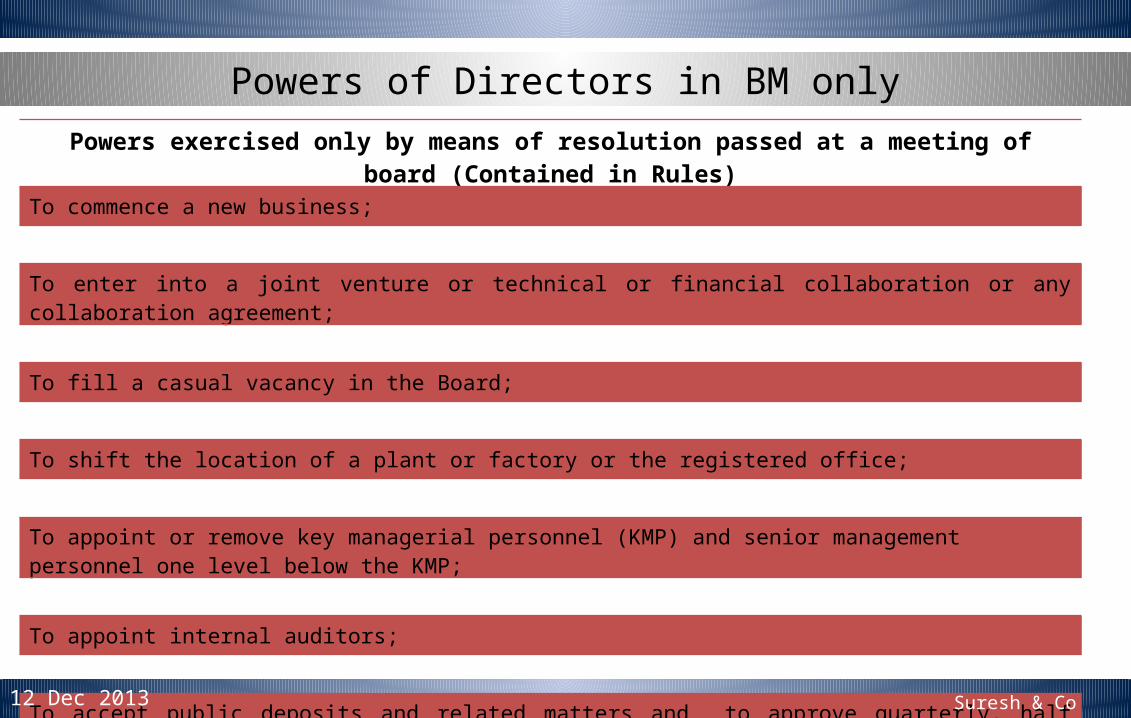

Powers of Directors in BM onlyPowers exercised only by means of resolution passed at a meeting of board (Contained in Rules)

To commence a new business;

To enter into a joint venture or technical or financial collaboration or any collaboration agreement;

To fill a casual vacancy in the Board;

To shift the location of a plant or factory or the registered office;

To appoint or remove key managerial personnel (KMP) and senior management personnel one level below the KMP;

To appoint internal auditors;

To accept public deposits and related matters and to approve quarterly, half yearly and annual financial statements.

Suresh & Co12 Dec 2013

Suresh & Co.Assurance – Tax – Advisory

Bangalore www.sureshandco.com

Thank You

+91-98453 78991

Related Documents