1 Report by Sharon Obuobi New approaches to financing Africa’s SMEs

New Approaches to Financing Africa's SMEs2

Oct 27, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Report by Sharon Obuobi

New approaches to financing Africa’s SMEs

2

Contents

Contact Us

Sub-Saharan Consulting Group 7200 The Quorum Oxford business Park Oxford, Ox4 2JZ, UK T: + (44) 01865 589022 F: + (44) 01865 481482 E: [email protected] W: www.s-scg.com

3

Contents I. Financial services outlook 4

a. The Economic Scene b. Economic Forecast: Two Scenarios c. Institutional Growth restraints d. Expanding Financial Firms

II. Revolutionising banking services: credit-based economy 5

a. Private Equity Investment: The formal sector b. Private Equity Investment: Structural development of SMEs c. SMEs with information asymmetry

III. Mobile banking in Sub-Saharan Africa 7

a. Opportunities b. Challenges c. Impact on corporate banks

IV. Financing SMEs in Africa 8

a. Higher Reinvestment Rates b. Agile Asset reallocation c. Developing the “Missing Middle”

V. Managing lending financial risk 10

a. Developing SME capacity of clients b. Engaging in the management of federal financial policies c. Pursue innovative financing tools d. Minimize operating costs to maximize efficiency

VI. Appendix 12

VII. References 15

4

The Economic Scene Sub-Saharan Africa is predicted to experience a boom in the financial sector from 2010 to 2020. Real GDP growth in sub-Saharan Africa averaged 6.8% from 2005 – 2008.1 Despite the global recession, real GDP growth was forecasted to fall only slightly to 5.5% from 2011-2012.2

This has caused high expectations for the doubling of banking assets and deposits, as well as a continued expansion in the industry.

Economic Forecast: Two scenarios In one economic scenario, the Economist Intelligence Unit (EIU) anticipates that total bank claims for sub-Saharan countries will expand by 178% to US$980 billion. In another scenario, the EIU predicts that assets

1 The Economist Intelligence Unit: Banking in Sub-‐Saharan Africa to 2020 2 Ibid.

will grow by 248% to US$1.37 trillion. This is attributed to the expectation that more households and businesses will be saving, borrowing, and transferring money through banks with greater frequency. The high growth is expected to be strongest in countries such as Tanzania, Uganda, Ghana, and Angola that are currently experiencing a wave of new resource booms.

Institutional Growth restraints Sub-Saharan countries still face growth restraints due to the poor quality of financial institutions responsible for providing services, which include bankruptcy programs and legal support.

Expanding Financial Firms There is a growing interest in banking opportunities for expansion. Ecobank Transnational has spread its reach from West Africa across the continent. Meanwhile, South African bank Standard Bank has been noted for its recent landmark deal with the Industrial and Commercial Bank of China. On the other hand, French and English banks continue to operate in their respective ex-colonial countries.

Financial services outlook

5

Private Equity Investment: The formal sector In order to experience the benefits of a credit-based economy, SMEs must join the formal sector. However SMEs are discouraged from entering the formal sector due to high taxation and the requirement to comply with accounting regulations. Tax inspectors often implement costly unethical practices, while accounting obligations are generally perceived negatively by SME managers. To alleviate this problem, it is recommended that formal legal and accounting frameworks be implemented to support the access of SMEs to formal financing.3

3 Proparco. pp 22-‐23

Structural development of SMEs

To supplement the support of SMEs through legal and accounting frameworks, SMEs must also further develop their management structure. One recommendation is the development of parties to establish partnerships with SMEs. Lenders may provide equity, while remaining minority shareholders. Separate parties may become responsible for implementing accounting procedures and legal structures within SMEs. Partnerships like these make SMEs more attractive within the formal financial sector.4

SMEs with information asymmetry Information asymmetry between SMEs and banks is a prevalent hindrance to lending programs. SMEs are unable to provide the required information for the facilitation of formal financing. Furthermore, supporting institutions such as credit bureaus are either non-existent or ineffective. To mitigate the high risk of default, a theoretical option for banks is to rely on financial guarantees or collateral. However with the lack of mortgage structures, and the scarcity of collateral among SME managers, the use of loan securitization is an unlikely solution. For this reason, 4 Proparco. pp 22-‐23

Revolutionising banking services: Credit-based economy

6

some SMEs are depending on the use of guarantee funds. Notable funds include the Fonds de Garantie Malgache (Malagasy Guarantee Fund), the Small Business Credit Guarantee in Namibia (national funds), the African Solidarity Fund, the African Fund for Guarantee and Economic Cooperation (pan-African funds), the Guarantee Fund for Private Investments in West Africa (GARI Fund, managed by the BOAD), the ARIZ Fund (managed by AFD), as well as USAID and IFC funds.5

5 Proparco, pp 13-‐15

7

Opportunities A 2010 report by African Development Bank on mobile banking cites four key opportunities from the successful adoption of mobile banking service providers. These are:

• A boost in domestic savings through the expansion of financial services to the poor and rural populations.

• Increased money transfers from the diaspora at low costs.

• Reduction in financial transaction costs, leading the to lowering of the cost of doing business for the benefit of SMEs and overall private sector development

• Increased government revenues as a result of increased corporate revenues from the booming mobile

banking, and improved corporate earnings.6

Challenges With the surge in mobile banking, service providers and banks face some challenges in ensuring continued successful adoption. Critical challenges include the development of capacity to support users and the strengthening of mobile-banking security.

Impact on corporate banks The biggest advantageous impact that mobile banking has on corporate banks is the surging new source of revenue. As a result, a key costly impact is the requirement for stronger and secure infrastructure to support the increase in mobile banking users. Banks may also be required to redesign their service offerings to suit the needs of new consumer segments.

6 Ondiege

Mobile banking in sub-Saharan Africa

8

According to a report by McKinsey, successful well-established companies headquartered in emerging markets grow approximately twice as fast as their counterparts in developed economies.7 Two key factors emerged as contributing components to this significant difference in growth.

7 Atsmon, Kloss, and Smit

Higher reinvestment rates Emerging market companies generally offered lower dividend payouts, and reinvested excess cash to develop fixed assets at a higher rate. Thus, SMEs are encouraged to reinvest profits into fixed assets to strengthen future business developments and expansions.

Agile asset reallocation Another key component in the rapid development of emerging market companies has been the reallocating of capital toward new business opportunities. 8 SMEs must acquire assets that are easily transferable, and develop a governance model which best for the facilitation of rapid decisions.

Developing the “Missing Middle” Emerging-market companies require better financing to boost their capacity and market competitiveness. The OECD offers a four-pronged approach9 to increasing SME access to finance:

1. Improve business conditions 2. Help SMEs meet the requirements

for formal financing

8 Ibid. 9 Kauffmann

0

10

20

30

40

50

60

70

80

90

Average dividend payout rate %

Average cash as % of sales

Fixed assets, compound

annual rate, %

Developed Economies

Emerging Economies

Financing

SMEs in Africa

9

3. Make the financial system more accessible to SMEs

4. Expand the supply of finance through the non-financial private sector

Despite the significant range in the level of institutional financial development, there this still much room to improve for the average emerging market SME.

One key characteristic of emerging markets is the existence of high financial risk. Despite the challenge, implementing a well-designed management strategy will help to ensure that a company is financially sustainable and able to withstand market changes.

There are four ways that companies can manage lending financial risk in emerging marks with SMEs:

1. Developing SME capacity of clients 2. Engaging in the management of

federal financial policies 3. Pursue innovative financing tools 4. Minimize operating costs to

maximize efficiency

10

Developing SME capacity of clients As discussed in the report entitled, Africa Entrepreneurship Outlook 2012 by Sub-Saharan Consulting Group, there is much financial promise from the development of entrepreneurship in emerging markets.

Simply defined as the development of skills and institutions, capacity building is critical for the achievement of sustainable economic growth. The quality of economy’s human skills and institutions is a critical determinant in the quality of output generated. As a result, investors and entrepreneurs alike have stakes in the building of capacity in their regions. The availability of effective government institutions, financial programs, and a highly skilled human resource pool are important factors in the management of lending financial risk.

Engaging in the management of federal financial policies By playing an active role in the development and management of financial policies, companies can minimize the risk and weight of unexpected financial policies on their investments. According to the IMF’s Regional Economic Outlook report on sub-Saharan Africa, many countries in the region are approaching their peak in growth.10 As a result, the risks involved in maintaining the current macroeconomic environment are highly asymmetric. For this reason, it is in the interest of lending financial institutions to engage in the management of federal financial policies. This can take place through the provision of direct feedback to the institutions responsible for implementing fiscal and monetary policies. Through direct partnership, the achievement of common economic goals will be more likely, and the risk of unexpected financial events will be minimized.

Pursue innovative financing tools The financial environment of emerging markets is very different from the financial environment of developed

10 Sub-‐Saharan African: Sustaining the Expansion

Managing lending financial risk

11

markets. Emerging markets require a new set of innovative financing tools, which are adapted for the conditions of the market.

Minimize operating costs to maximize efficiency

Due the existing characteristics of rapid change in emerging markets, financial lenders should be prepared to adapt to sudden new opportunities or unexpected costly events. Minimizing the company’s operating costs will increase its profitability and make it more financially equipped to be competitive in the market.

12

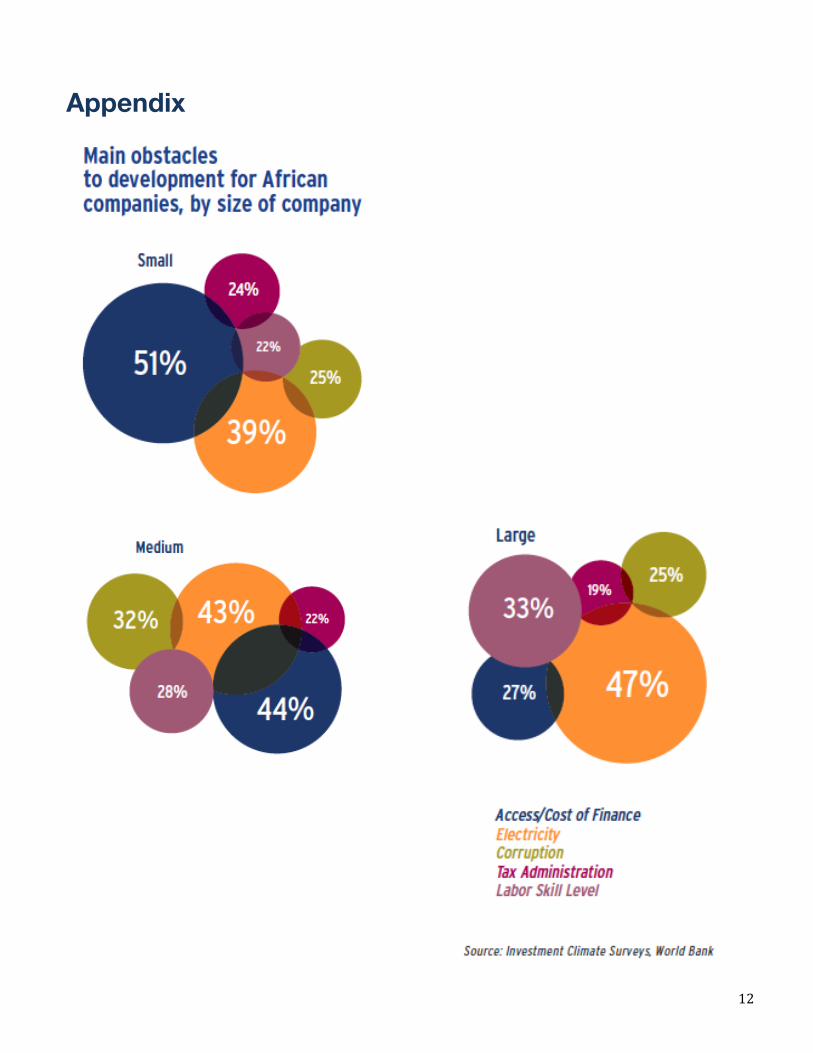

Appendix

13

14

References

Atsmon, Yuval, Michael Kloss, and Sven Smit. "Parsing the growth advantage of emerging-market companies." Strategy Practice. (2012): n. page. Print. Kauffmann, Céline. "Financing SMEs in Africa." OECD DEVELOPMENT CENTRE:Policy Insights. 7 (2005): n. page. Web. 25 May. 2012. <http://www.oecd.org/dataoecd/57/59/34908457.pdf>. Ondiege, Peter. "Mobile Banking in Africa: Taking the Bank to the People ." Africa Economic Brief. (2010): n. page. Print. "Banking in Sub-Saharan Africa to 2020: Promising frontiers." Economist Intelligence Unit. (2011): n. page. Print. "Press 1 for modernity." Economist. 28 05 2012: n. page. Web. 25 May. 2012. <http://www.economist.com/node/21553510>. "SME Financing In Sub-Saharan Africa." Proparco's Magazine: Private Sector Development. 1 (2009): n. page. Print. "World Economic and Financial Surveys: Regional Economic Outlook." Sub-Saharan African: Sustaining the Expansion. Oct (2011): n. page. Print.

15

Disclaimer

This publication contains general information only, and Sub-‐Saharan Consulting Group is by no means of this publication, rendering professional advice or services. Consult a qualified professional before making any decisions or taking actions that may affect your finances or business.

© Sub-‐Saharan Consulting Group 2012

Designed and written by Sharon Obuobi

Related Documents