NAVIGATING MID MAREKT GROUP SALES WE ARE HERE TO ASSIST YOU. MID MARKET GROUP: how to do it

NAVIGATING MID MAREKT GROUP SALES WE ARE HERE TO ASSIST YOU. MID MARKET GROUP: how to do it.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

NAVIGATING MID MAREKT GROUP SALES

WE ARE HERE TO ASSIST YOU.

MID MARKET GROUP:how to do it

MID MARKET GROUP SALES

Our goal is to make the Mid Market sale as easy as possible for You.

At Rogers Benefit Group we are experts in assisting brokers and their clients. We are your one stop for quotes from the Mid Market carriers. We even obtain quotes for you from carriers we don’t represent, saving you time and trouble.

Once quotes are received, we put them in a professional presentation format, and assist you in identifying the best fit for your client.

We are available to accompany you to the employer presentation; once the go- ahead is given we will help you implement the plan the employer has selected. We make it as simple and easy as possible for you.

We do all of this on your behalf. There is no charge or reduction in your compensation for our services.

Let us assist you with your Mid Market prospects. You’ll be glad you did.

Mid Market Group Sales

OBJECTIVE OF THIS POWER POINT:

Review some of the in’s and outs of writing and renewing Mid Market business

Familiarize you with all the help we give you with your Mid Market cases

Encourage you to be as comfortable writing Mid Market groups as your are with Small Groups .

Mid Market Group Sales

What is a Mid Market Group?Various definitions:

● 51-99● 51-125● 51-200● 51-299● 51-500

Mid Market Group Sales

Rogers Benefit Group represents: Aetna to 125 lives Blue Shield to 299 lives California Choice to 199 lives Healthnet to 250 lives HSA California to 100 lives Kaiser Permanente Choice Solution to 50 lives Principal (non medical only) any size group Sharp Health Plan to 200 lives Unitedhealthcare to 99 lives

*We will obtain quotes for you for all mid market medical carriers.

MID MARKET GROUP SALES

Determining if a group is Mid Market or Small Group

If at least 50% of the group’s working days during the preceding calendar quarter or preceding calendar year, a firm employed 50 or fewer eligible employees the group is considered a small group. (quarters need not be consecutive)

MID MARKET GROUP SALES

Advantages of keeping a group in a small group contract

1. The group may prefer age rates vs. composite rates

2.The group may prefer SGR renewal methodology due to concern of increases due to health issues

3. The group may fear leaving GI environment4. Small group rates are possibly lower than

Mid Market rates on a case by case basis.

MID MARKET GROUP SALES

Disadvantages of a Group remaining in a Small group contract.

1. The group may prefer composite rates 2. A group that has grown over 50 employees

may be required to stay in small group due to medical conditions

3. The small group rates could be higher than Mid Market rates

MID MARKET GROUP SALES

Important consideration once a group is over

50 lives:

Mid Market is not Guarantee Issue. Carriers may choose not to quote for a

variety of Underwriting reasons.For example, a group may not be able to

switch carriers if they develop serious medical conditions.

MID MARKET GROUP SALES

For Success with a Mid Market Sale:

MANAGE CLIENT EXPECTATIONS

Please let the employer know upfront what they might expect…

MID MARKET GROUP SALES

MANAGING EXPECTATIONS Examples:

1. Quote turnaround time ---7 -10 business days2. The Possibility of a decline to quote3. Underwriting is done upfront4. May need additional information to obtain

quotes5. Must set realistic expectations on group

getting into the system and ID cards received.

Mid Market Group Sales

Differences between Small and Mid Market

With Mid Market the Underwriting Is Done Upfront, at the Beginning of the Process

Small Group: A broker can obtain a quote for almost any small group.

Mid Market: The Carrier decides upfront, based on Underwriting criteria, if they want to quote on a group.

Mid Market Group Sales

Some differences between Small and Mid Market Underwriting non guarantee issue --- a group can be declined for:

A.HealthB.Industry/SIC CodeC.Participation with other carriers such as staff model HMOD.Persistence --- too many carriers in the last 5 yearsE.Percentage of COBRA is too highF.Too few participants, i.e., group size <50 livesG.Other

MID MARKET GROUP SALES

Some Groups Have Unusual or Special SituationsExamples: Group with under 50 employees; Under 50 employees enrolling; A large number of employees covered by staff HMO; A large number of valid waivers; 50% contribution; Difficult industry.

It may not be possible to get Mid Market quotes if the group has unusual Underwriting situations that do not meet Carrier requirements.

Please contact RBG, we will assist you with determining the Underwriting eligibility.

MID MARKET GROUP SALESThe Quote

Often, with small group, the process of quoting and enrolling begins the month prior to the effective date…

With Mid Market the process must begin sooner…

MID MARKET GROUP SALES

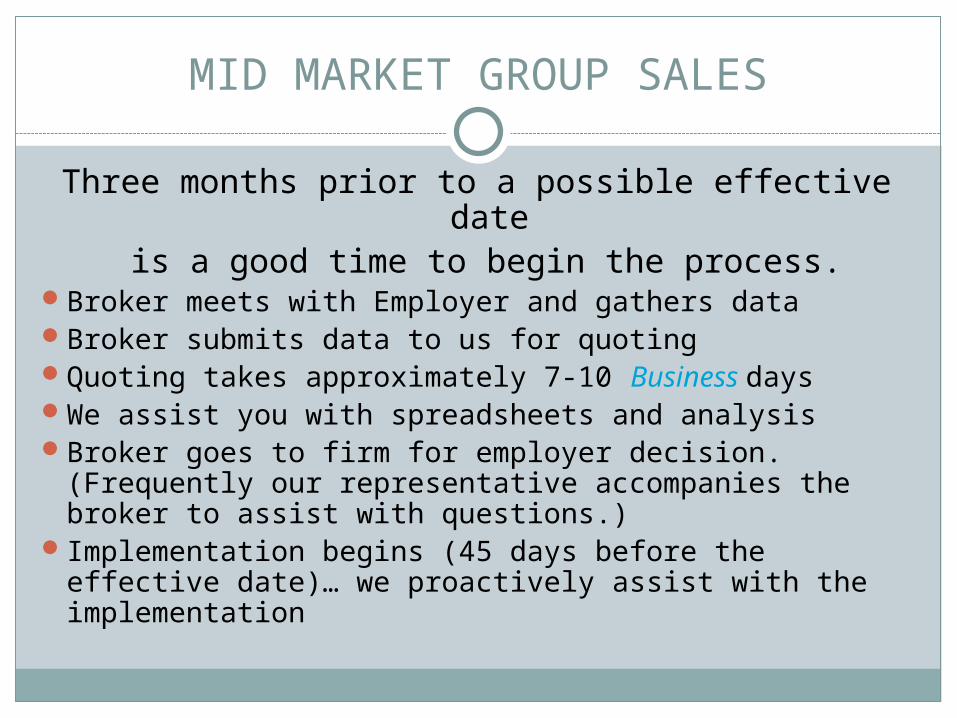

Three months prior to a possible effective date is a good time to begin the process.

Broker meets with Employer and gathers dataBroker submits data to us for quotingQuoting takes approximately 7-10 Business daysWe assist you with spreadsheets and analysisBroker goes to firm for employer decision. (Frequently

our representative accompanies the broker to assist with questions.)

Implementation begins (45 days before the effective date)… we proactively assist with the implementation

Mid Market Group Sales

Mid Market Underwriting is done upfront

How is Underwriting done for Mid Market?

MID MARKET GROUP SALES

Underwriting is done using the Request for Proposal (RFP)

The RFP consists of the:DataCensusQuestionnaire

Mid Market Group Sales

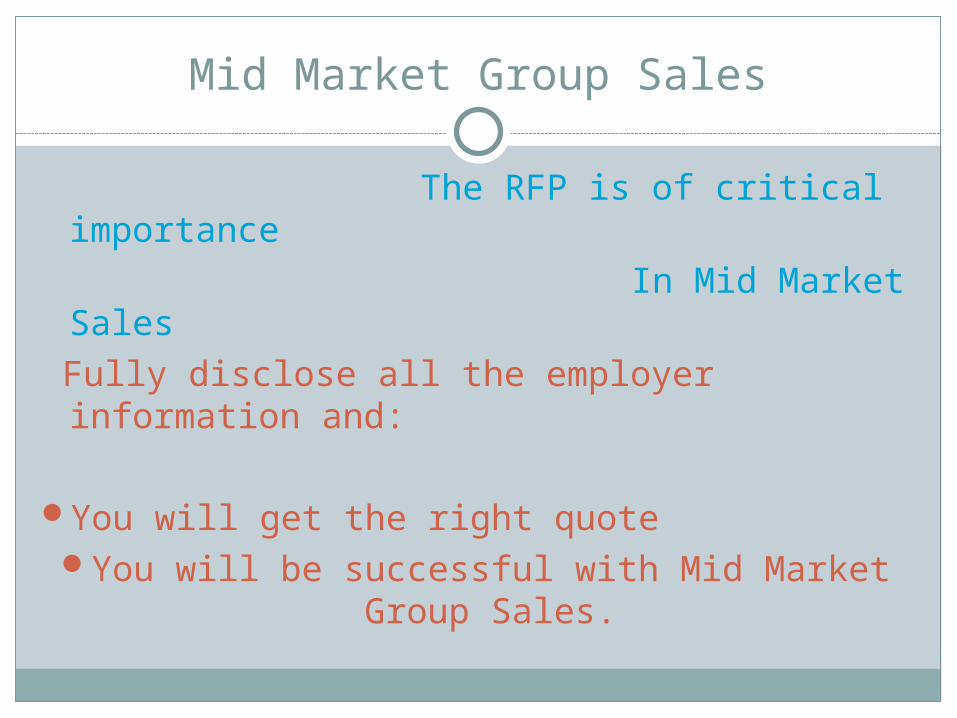

The RFP is of critical importance In Mid Market Sales Fully disclose all the employer information

and: You will get the right quote You will be successful with Mid Market Group

Sales.

MID MARKET GROUP SALES

THE RFPIt’s about gathering all the data,

all the information upfront.The RFP must be complete and thorough or…1. It increases the time it takes to get a quote2. The quote you get may not be correct3. It increases the chance for a re-rate upon

submission of the group

MID SIZE GROUP SALES

The RFP must be complete, thorough, correct

The CENSUS

Correct, accurate census data is a must.

MID MARKET GROUP SALES

Most frequently missed on the Census.Accurate breakdown of who is taking the

HMO, PPO, Staff model HMO, COBRAEligible ee’s who are waiving are not

includedZips missing or not accurateDeps missing or not accurateSalary (for life, STD and LTD)Job titles (for STD and LTD)

Mid Market Group Sales

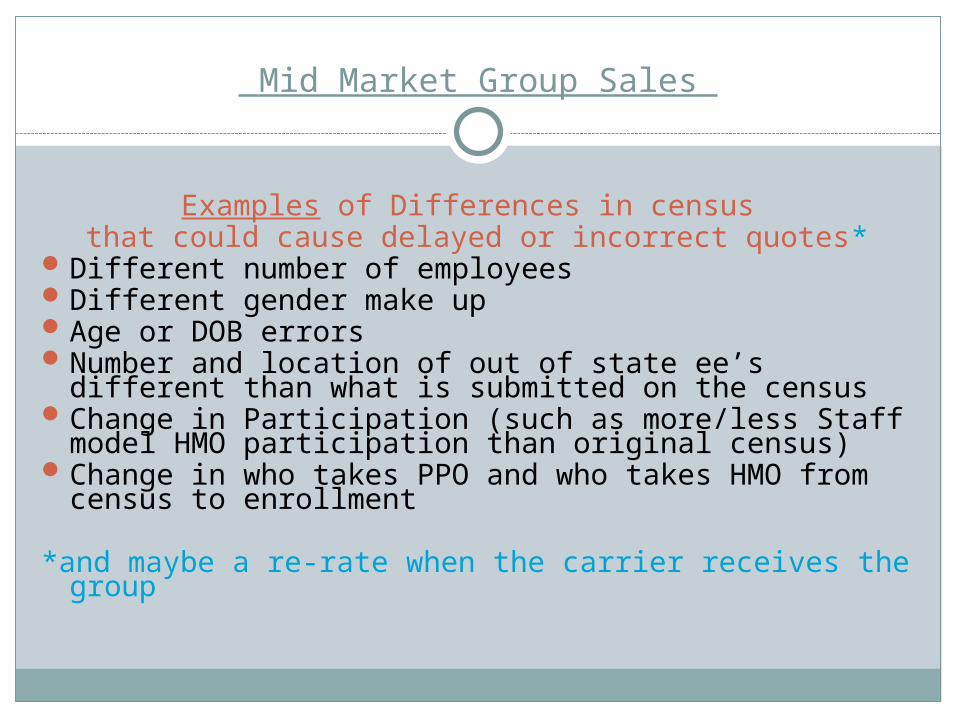

Examples of Differences in census

that could cause delayed or incorrect quotes*Different number of employeesDifferent gender make upAge or DOB errorsNumber and location of out of state ee’s different than

what is submitted on the censusChange in Participation (such as more/less Staff model

HMO participation than original census)Change in who takes PPO and who takes HMO from

census to enrollment

*and maybe a re-rate when the carrier receives the group

Mid Market Group Sales

Differences between Small and Midsize

A BIG QUOTING DIFFERENCE---

Small group: It’s often requested to quote: each employee in PPO and each employee in the

HMO or total replacement of a Staff Model HMO, or all employees in each plan as with a Carrier

that offers a menu of plans…

And then, the enrollment may differ from the quote with no consequences in small group.

Mid Market Group Sales

Differences between Small and Midsize

QUOTING DIFFERENCE---A BIG ONE With Mid Market, a carrier requests an

accurate census of who will enroll in each plan---if the enrollment is different by

more than a certain percent, usually 10%, the carrier can re-rate at time of submission of the group.

(Avoid Re-rates)

MID MARKET GROUP SALES

Please be sure to manage employer expectations if the census has any

guessing or estimating.

MID MARKET GROUP SALES

Submitting a Complete RFP

Employer Underwriting Questionnaire

Recommended1. Shows the carrier the group’s health2. Confirms other facts on the RFP3. Gathering complete, accurate information

upfront (with the RFP submission), avoids any surprises at enrollment.

MID MARKET GROUP SALES

Accurate information on the Employer questionnaire is essential.

Examples:ContributionHealth…within the bounds of the privacy

lawsCOBRA… ending up with unexpected excess

COBRA could cause re-rate or decline

Mid Market Group Sales

Differences between Small and Midsize

Ownership and other documentation generally not needed for Mid Market at time of submission --- However, the same rules apply (generally) but must be clarified upfront at time of submitting the RFP with mid market groups

DE 6 is not asked for by the carriers in Mid Market (although could be asked for if group size is questionable) –

Issues of employee eligibility and actual size of group are clarified upfront as part of the RFP submission in mid market.

Mid Market Group Sales

Differences between Small and Mid Market

Please remember the Gotchas1. Census Differences between quoted and

enrolled2. Enrollment doesn’t match RFP3. Enrollment does not match ER questionnaire4. Enrollment does not match Assumptions.

Be sure to closely review the ASSUMPTIONS PAGE ON THE QUOTES.

We will assist you with this.

MID MARKET GROUP SALES

…and please remember it will take approximately 7-10 business days to get quotes (more during peak times such as November and December)

Please Manage Employer Expectations

MID MARKET GROUP SALES

Renewals

Please remember to begin Three months before the renewal.

We assist you at Renewal as fully as we do at the sale.

We are there for you through the entire process.

Our Commitment to YOU.

At Rogers Benefit Group our Commitment is to assist you and your staff through the entire process of writing AND renewing Mid Market groups.

We will assist you in assembling needed Underwriting data, obtaining quotes, quote analysis, plan comparisons and materials. and the employer presentation.

If a group decides to switch carriers we are there to assist you and your group with the implementation and understanding of the new plan.

Let’s work together on a Mid Market prospect. You’ll see the difference it make for YOU.

Related Documents