Gas Reference Case І Fall 2007 © Copyright 2007, Global Energy Decisions, LLC All rights reserved. No part of this report may be reproduced or transmitted in any form or means, electronic or mechanical, including photocopying, recording, or by any information storage or retrieval system without the permission of Global Energy Decisions, LLC. This report constitutes and contains valuable trade secret information of Global Energy Decisions. Disclosure of any information contained in this report by you and your Company to anyone other than the employees of your Company ("Unauthorized Persons") is prohibited unless authorized in writing by Global Energy Decisions. You will take all necessary precautions to prevent this report from being available to Unauthorized Persons, as defined above, and will instruct and make arrangements with employees of your Company to prevent any unauthorized use of this report. You will not lend, sell, or otherwise transfer this report (or information contained therein or parts thereof) to any Unauthorized Person without Global Energy Decisions’ prior written approval. PROPRIETARY AND CONFIDENTIAL Global Energy Advisors 2379 Gateway Oaks Drive, Suite 200 | Sacramento, CA 95833 tel 916-569-0985 | fax 916-569-0999 Global Energy Decisions

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Gas Reference Case І Fall 2007

© Copyright 2007, Global Energy Decisions, LLC

All rights reserved. No part of this report may be reproduced or transmitted in any form or means, electronic or mechanical, including photocopying, recording, or by any information storage or retrieval system without the permission of Global Energy Decisions, LLC. This report constitutes and contains valuable trade secret information of Global Energy Decisions. Disclosure of any information contained in this report by you and your Company to anyone other than the employees of your Company ("Unauthorized Persons") is prohibited unless authorized in writing by Global Energy Decisions. You will take all necessary precautions to prevent this report from being available to Unauthorized Persons, as defined above, and will instruct and make arrangements with employees of your Company to prevent any unauthorized use of this report. You will not lend, sell, or otherwise transfer this report (or information contained therein or parts thereof) to any Unauthorized Person without Global Energy Decisions’ prior written approval. PROPRIETARY AND CONFIDENTIAL Global Energy Advisors 2379 Gateway Oaks Drive, Suite 200 | Sacramento, CA 95833 tel 916-569-0985 | fax 916-569-0999

Global Energy Decisions

The opinions expressed in this report are based on Global Energy Decisions’ judgment and analysis of key factors expected to affect the outcomes of future power and gas markets. However, the actual operation and results of energy markets may differ from those projected herein. Global Energy Decisions makes no warranties, expressed or implied, including, but without limitation, any warranties of merchantability or fitness for a particular purpose, as to this report or other deliverables or associated services. Specifically, but without limitation, Global Energy Decisions makes no warranty or guarantee regarding the accuracy of any forecasts, estimates, or analyses, or that such work products will be accepted by any legal, financial, or regulatory body.

Executive Summary

Gas Reference Case, Fall 2007 ES-1

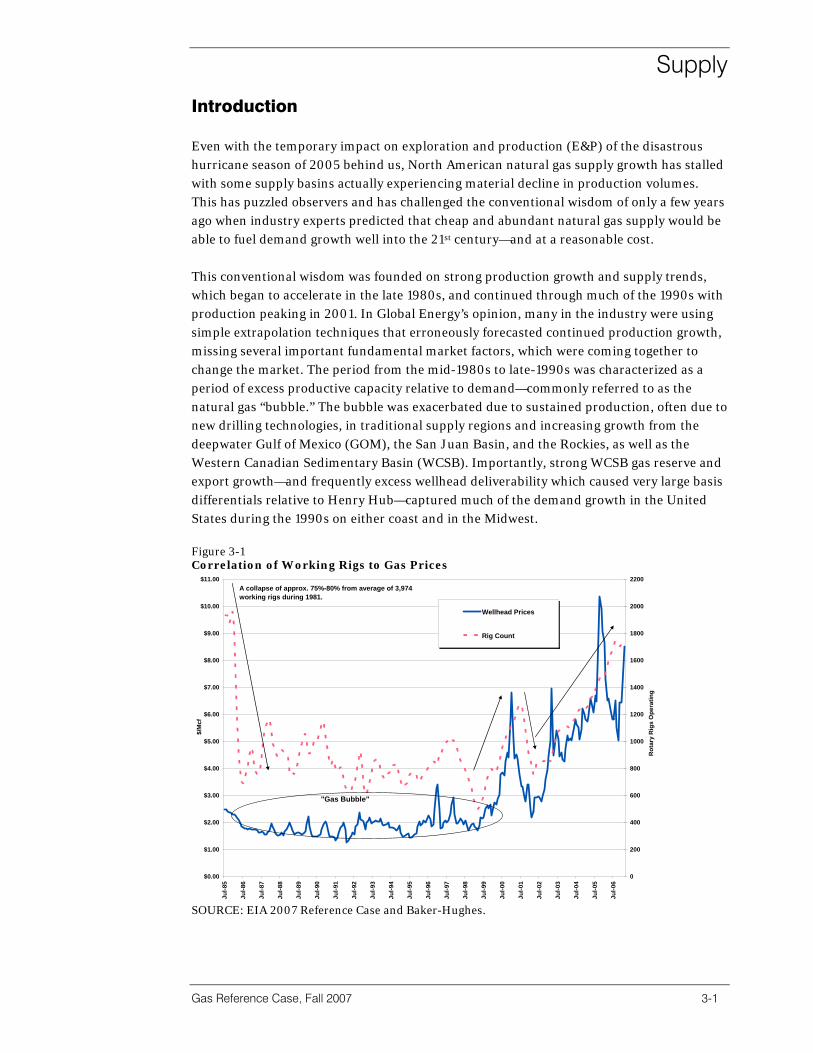

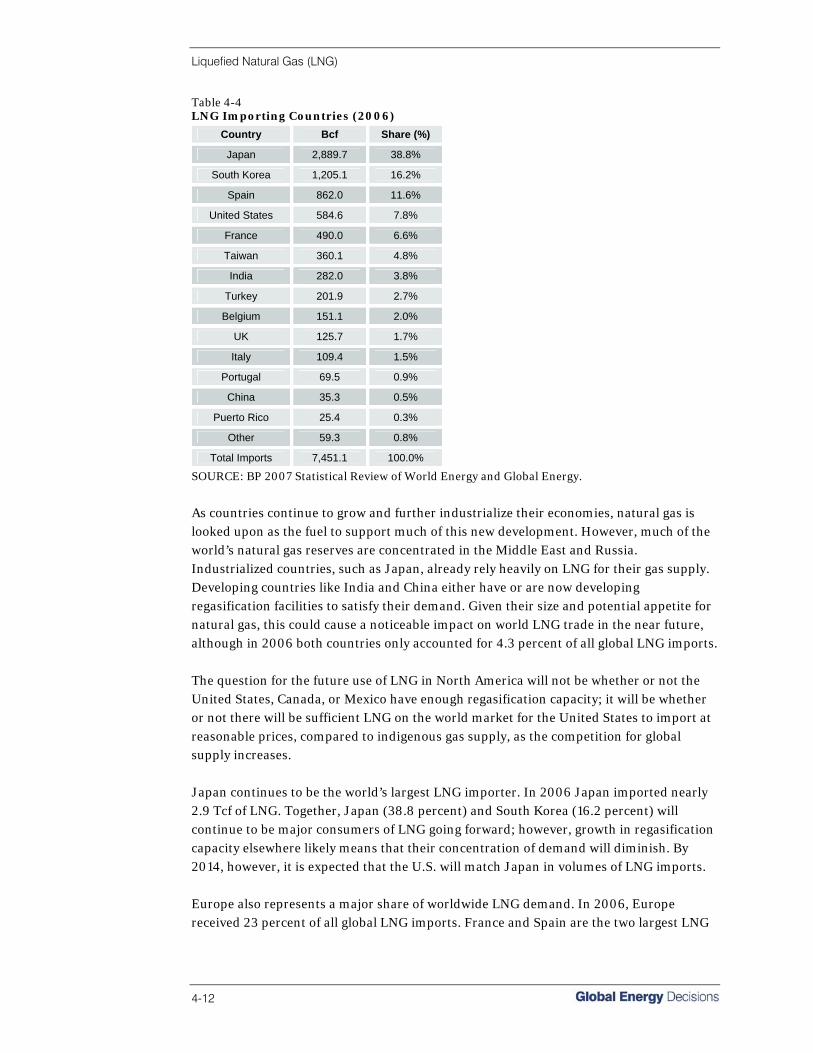

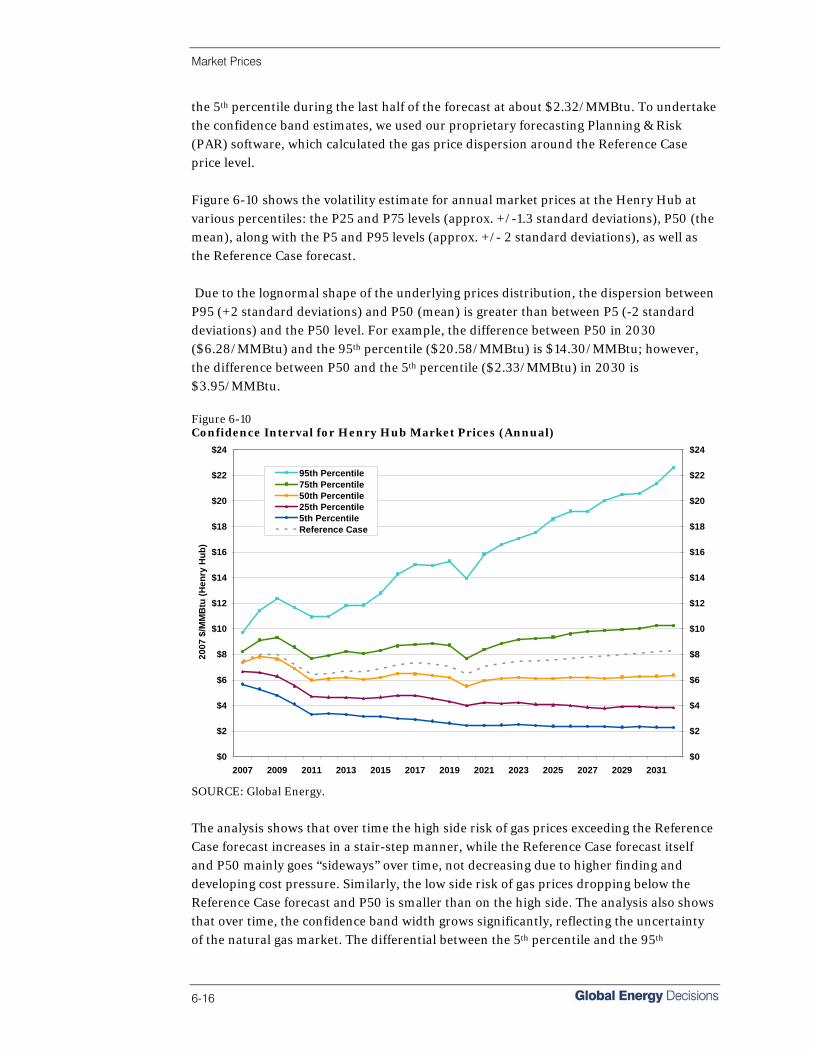

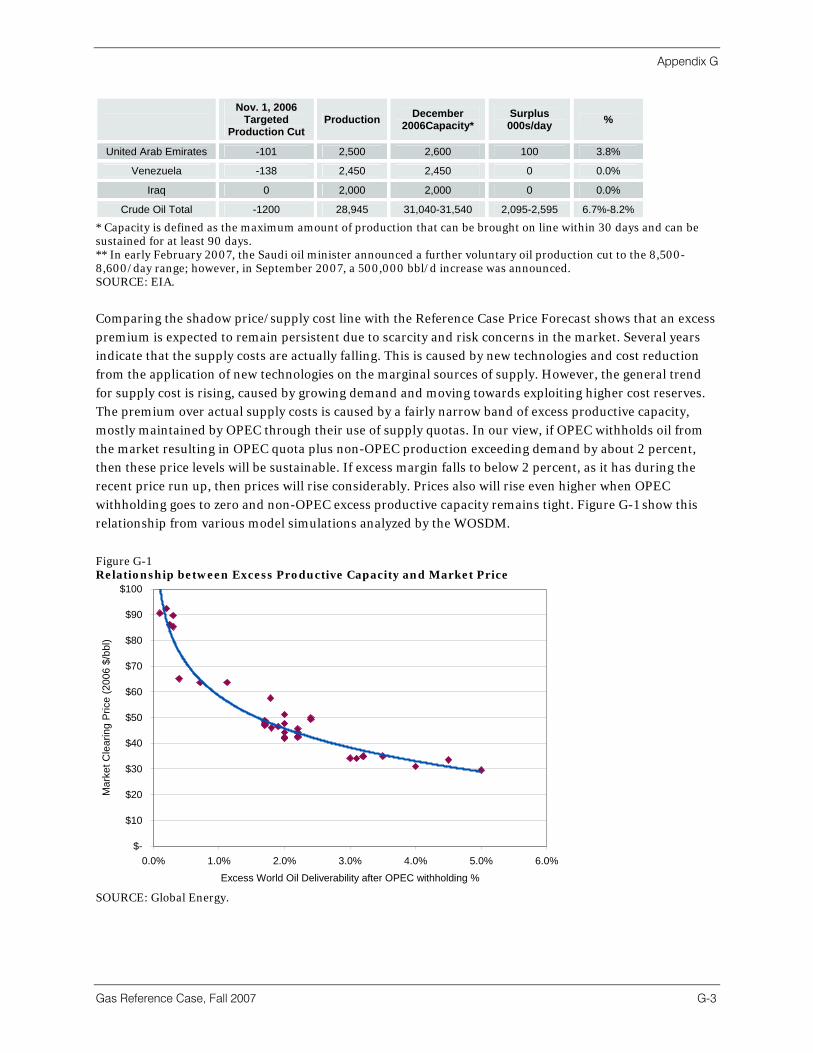

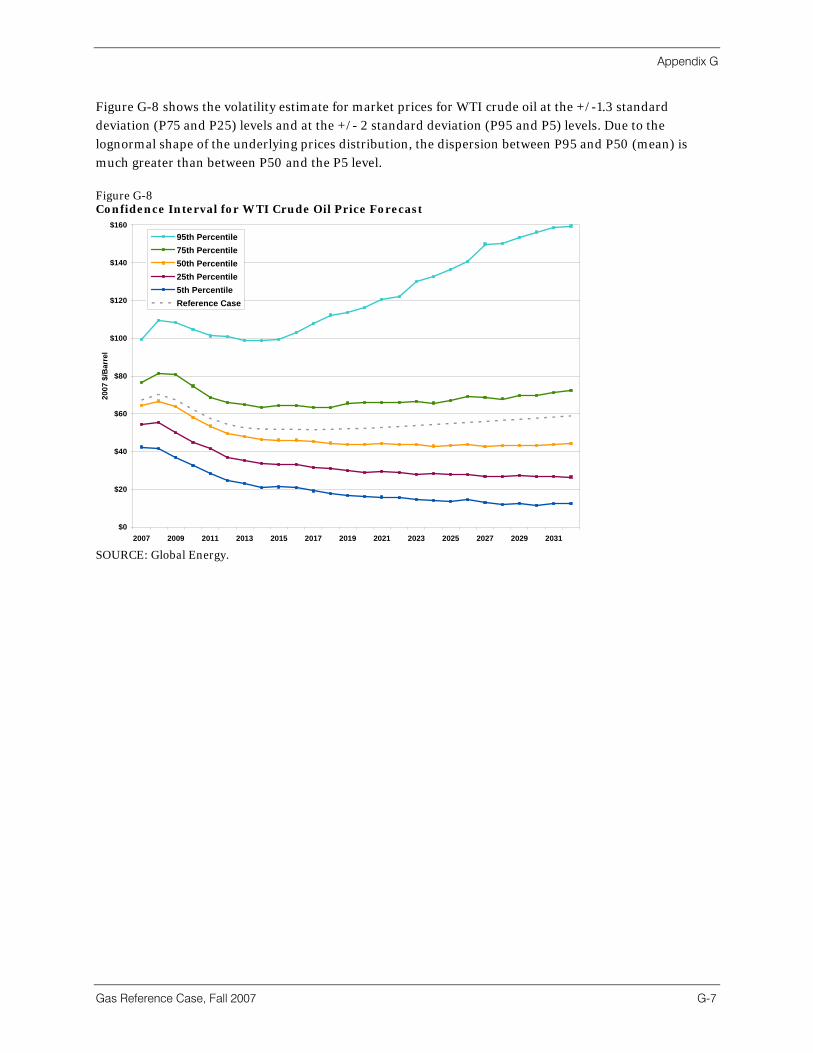

Market Commentary With natural gas supply and demand nearly in balance, gas prices and volatility levels have remained tenaciously steep by most historical measures since early 2003. The horrific hurricane damage sustained in autumn 2005 in the Gulf of Mexico added further stress to domestic natural gas and oil supply infrastructure that is not quite yet back to “normal.” For example, U.S. crude oil production in 2006 is currently estimated to have averaged 5.1 million bbl/day, down slightly from 2005 levels as a result of the hurricanes. And offshore gas production averaged 7.8 Bcf/day in 2006, down nearly 20 percent from mid-2005 levels, although some is undoubtedly due to gas deliverability depletion. Since that time gas prices have retreated but still remain well above long-run supply cost. Figure ES-1 Gulf of Mexico Monthly Natural Gas Production and Wellhead Price ($/Mcf)

0

50

100

150

200

250

300

350

400

450

500

Jan-

01

Apr

-01

Jul-0

1

Oct

-01

Jan-

02

Apr

-02

Jul-0

2

Oct

-02

Jan-

03

Apr

-03

Jul-0

3

Oct

-03

Jan-

04

Apr

-04

Jul-0

4

Oct

-04

Jan-

05

Apr

-05

Jul-0

5

Oct

-05

Jan-

06

Apr

-06

Jul-0

6

Oct

-06

Jan-

07

Apr

-07

Jul-0

7

Bcf

/ M

onth

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

$10

$ / M

cf

GOM Gas Production

EIA Avg. Wellhead Price

Hurricane Ivan (Category 3)

Hurricane Lili (Category 4)

Hurricane Katrina (Category 5)

SOURCE: EIA and Global Energy.

In Global Energy’s opinion, current high gas prices are reflective of several factors that have converged into the “perfect storm.” First, the high cost of replacing natural gas production across all basins has raised the price floor. This is exacerbated by the gradual reduction in supply from conventional gas basins and the steady increase from unconventional basins, coupled with increased LNG imports. Absent immediate alternative sources of supply, we expect to experience these price levels for some time. Second, persistently high crude prices (in part due to increased world turmoil in the Middle East) have strengthened the “crude sympathy” that exists between the two commodities. High oil prices “allow” gas prices to rise due to competitive fuel switching. Also, the petroleum supply industry tends to favor oil development over gas when prices rise since oil development costs and the lead time to first production are usually less. And recently, due to cold weather a record amount of natural gas was withdrawn from storage

Executive Summary

ES-2

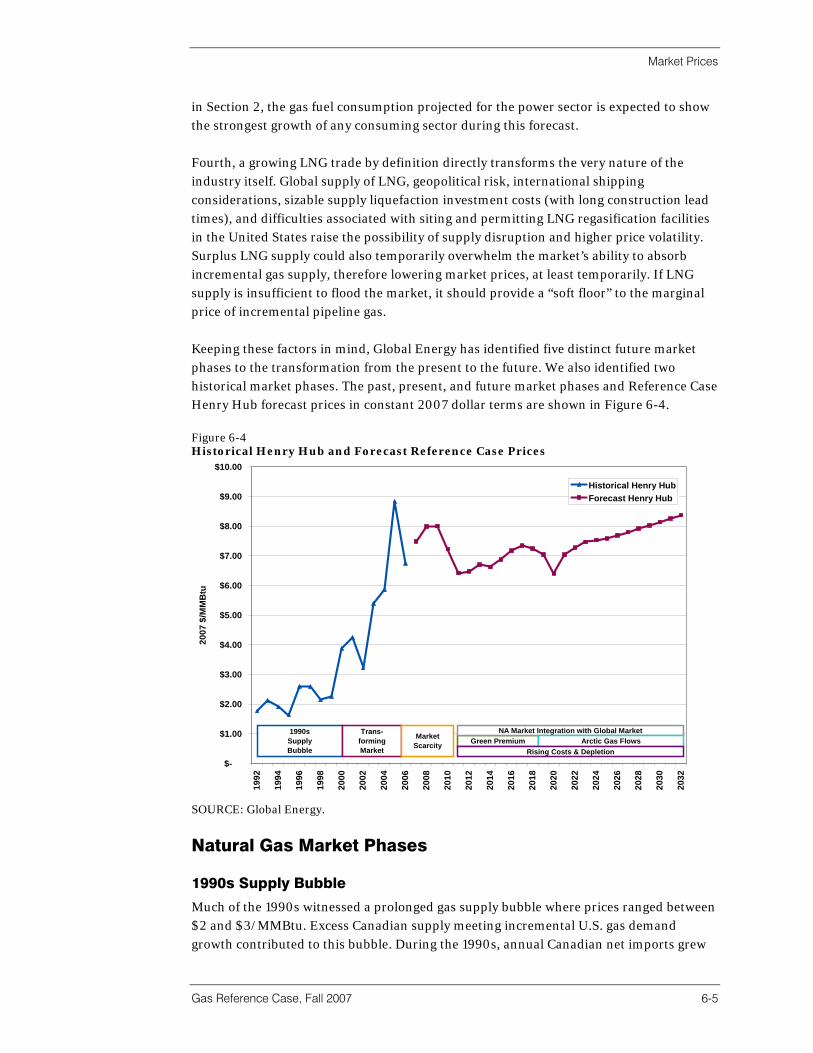

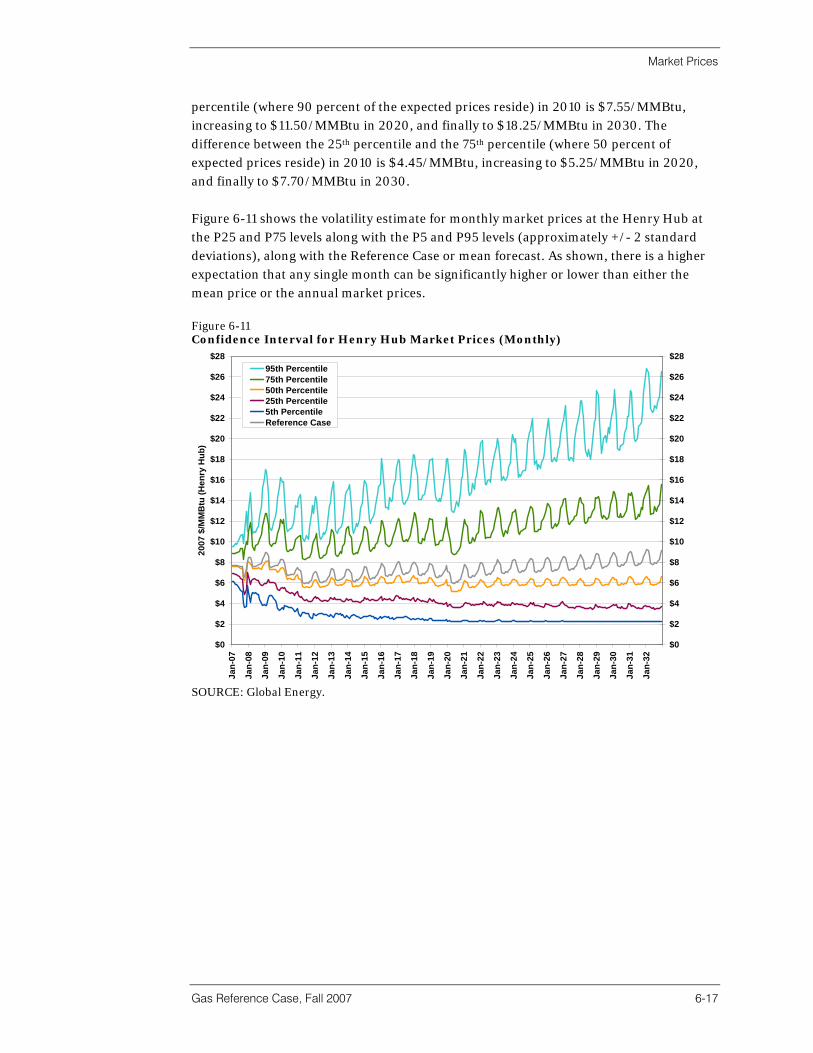

in February, dropping inventories below the five-year maximum for the first time in over a year. Global Energy projects that oil and gas price moderation will occur after several years, but the actual timing and extent are still subject to large amounts of uncertainty. In particular, price declines are not expected until significant new sources of supply materialize in North America. We previously cited the impending increase in LNG supply as one sign that moderation would eventually occur. Our opinion is now bolstered by the fact that the Gulf Gateway Energy Bridge and Altamira projects are operational and significant new liquefied natural gas (LNG) construction is presently under way (such as Canaport in New Brunswick) as is more drilling for “unconventional” gas. The timing of these projects is such that price moderation is forecast by the end of the decade. In addition, pipeline imports from Canada are expected to continue to decline due to their increased domestic demand and supply moderation of their own (i.e., disappointing production in the North Atlantic/Canada Basin). Therefore, the days of $2 or $3 gas as was seen during much of the 1990s when the market experienced a supply glut are long gone. Additionally, the 1.8 Bcf/day Rockies Express Pipeline is scheduled to go into service January 2008, relieving the congestion of relatively inexpensive Rocky Mountain gas thus allowing flows from Colorado and Wyoming eastward to Illinois, Ohio, and western Pennsylvania. Of course, basis differentials will change markedly. Following the NYMEX forward curve, Global Energy expects Henry Hub natural gas prices for 2008 to average $7.99/MMBtu, compared with $8.07 in the previous Reference Case (down $0.08 and 1 percent). For 2009, the Henry Hub price is expected to be $8.00/MMBtu (up $0.73 and 10 percent). However, overall the current Reference Case has just slight to moderately higher gas prices than forecasted last spring, about 4.5 percent for the 25-year strip from 2008-2032. In the current and last Reference Cases, forecasted gas prices do not sag as low following the high “prompt” years as in the previous reports, reflecting the impact of greater costs from increasing percentages of gas from unconventional sources, greater recognition of natural gas being “green” and a solution to global warming (see Appendix J for more information on Legislative Initiatives), and the reality of a continuing tight supply/demand situation in the United States. In the current Reference Case, the Henry Hub gas price perigee occurs in 2011 at $6.43/MMBtu, up $0.53 and 9 percent from the previous Reference Case, and a relative apogee is reached in 2030 at $8.08/MMBtu, up $0.19 and 2.4 percent. In the longer term, the landed price of LNG remains uncertain given the vagaries of the world market, available LNG supply, political unrest, and cartel formation, etcetera; however, its cost of production is well understood and very attractive at today’s market price. Other potential new supplies in North America (and the uncertainties associated with them) create additional uncertainty for the price of natural gas. Many of these factors are quantified through stochastic volatility analysis presented later in the report.

Executive Summary

Gas Reference Case, Fall 2007 ES-3

Figure ES-2 Monthly LNG Imports By Country; January 1997 through July 2007

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

Jan-

97

May

-97

Sep-

97

Jan-

98

May

-98

Sep-

98

Jan-

99

May

-99

Sep-

99

Jan-

00

May

-00

Sep-

00

Jan-

01

May

-01

Sep-

01

Jan-

02

May

-02

Sep-

02

Jan-

03

May

-03

Sep-

03

Jan-

04

May

-04

Sep-

04

Jan-

05

May

-05

Sep-

05

Jan-

06

May

-06

Sep-

06

Jan-

07

May

-07

MM

CF

Algeria

Trinidad&Tobago

Egypt

Australia

Qatar

Oman

Nigeria

Malaysia

Other (UAE, Brunei,Indonesia, etc.)

SOURCE: EIA and Global Energy.

One conclusion we draw from the analysis, which is possibly the most important point, is that our increasing reliance on LNG will transform the continental gas market into a global gas market over the next 10 years. This is expected to impact market prices, industry financial performance, and capital deployment. For example, although LNG imports totaled just over 0.5 Tcf in 2006, by 2030 Global Energy expects LNG to supply 8.4 Tcf of the total U.S. gas supply requirement of 32.7 Tcf, up over fifteen-fold. Another force already present is the massive build up of gas-fired electric generation capacity of recent years. Since the late 1990s, well over 200,000 MW of new combined cycle, gas-fired power plants have entered the North American markets. Thus far, the financial and operating performance of these plants has been disappointing as a result of the massive overbuild of capacity witnessed in many regions. Global Energy’s Electric Power Reference Case forecasts conclude that during the next 10 years capacity utilization of these plants is projected to grow by nearly 40 percent over present levels. Given that these combined cycle plants are already operating, and that long lead times and other financing and permitting hurdles exist for building alternative resources such as coal or nuclear, we characterize gas fuel demand growth as “predetermined”—at least through the 2012-2015 time frame. This will apply continuous pressure on gas markets and fuel suppliers. It will also further squeeze industrial gas consumers, who are relatively price sensitive, resulting in only flat industrial gas demand over the forecast period. The view presented above remains our base case view; however, in the past two years, utilities and independent power producers (IPPs) have been increasingly proposing alternative sources of generation. What was certainly our base case view one or two years ago, is now being viewed with diminished certainty: the record high gas fuel costs, strong industrial demand destruction, global and political uncertainty of supply, and the

Executive Summary

ES-4

development plans noted above will require close scrutiny in the coming years. High fuel prices have already begun to take their toll on the industry, and given the growth in proposals for alternative generation supply—especially coal, nuclear, and renewables—could leave natural gas suppliers, in particular LNG along with generators, holding large amounts of gas-fired capacity out of much of the market. Although we certainly live in “interesting times” when it comes to gas prices and volatility, gas prices have always been relatively volatile, driven primarily by unexpected weather events. From mid-1985 to mid-1993, the EIA’s survey of monthly average wellhead gas prices averaged $1.78/Mcf. Since Order 636 in 1993, which opened up the interstate gas price network and increased competition, gas prices, for the most part, remained in the $2.00 to $3.00/MMBtu range until the 2000s when the decade-long drilling recession ended and supply/demand was more or less balanced. Figure ES-3 illustrates the historical record of gas prices traded at the Henry Hub in Louisiana, North America’s main natural gas trading hub and delivery point of the NYMEX futures market. The figure is annotated with many of the key, primarily weather-driven events over the past 10 years. Most prominent was the effect of Hurricanes Katrina and Rita on market prices and the impact from the recent cold spell pushing Henry Hub prices into the $8-$9/MMBtu range. More recently, record cold in January/February caused a bump in prices, followed by a collapse due to high LNG imports and high storage levels. Figure ES-3 Historical Henry Hub Gas Prices

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

Jan-

97

May

-97

Sep-

97

Jan-

98

May

-98

Sep-

98

Jan-

99

May

-99

Sep-

99

Jan-

00

May

-00

Sep-

00

Jan-

01

May

-01

Sep-

01

Jan-

02

May

-02

Sep-

02

Jan-

03

May

-03

Sep-

03

Jan-

04

May

-04

Sep-

04

Jan-

05

May

-05

Sep-

05

Jan-

06

May

-06

Sep-

06

Jan-

07

May

-07

$/M

MB

tu

Thin Storage /Extreme Cold

Mild Weather

Energy Crisis/ Market Manipulation

Storage Fears

Hurricane Lili

Weather Event /High Demand

Perception of ShortSupply / Crude Sympathy

Hurricane Ivan

Hurricanes Katrina and Rita

Storage Glut /Cool Summer

Mid-Winter Cold Spell

Expectation of a Cold Winter, Low Storage, and Thin Supply

SOURCE: Global Energy.

Quantitative Gas Modeling In this report, Global Energy has applied fundamental supply and demand analysis of the competitive natural gas market to quantify natural gas market prices through 2032. The fundamental model used to prepare Global Energy’s forecast is the GPCM™ model, developed by RBAC Inc. In this specification, Global Energy forecasts natural gas production, interstate and intrastate transportation, storage, and consumption by sector. GPCM simulates regional interactions between supply, transportation, storage, and demand to determine market clearing prices and reserve additions. Prices and gas

Executive Summary

Gas Reference Case, Fall 2007 ES-5

demand for electric generation from GPCM are integrated with Global Energy’s North American Power Reference Case price forecast.1 The model creates a market clearing price centered on expected demand growth and it models endogenous supply and transportation capacity solutions. Short-term (48 month) price estimates are based on the NYMEX futures strip as of August 16, 17, and 20, 2007, combined with a mean reversion process during the latter one half of this period based on the GPCM model results. Beyond 48 months (October 2011), Global Energy has utilized GPCM fundamental results exclusively. The modeling also reflects natural gas consumption by power plants in North America over the 25-year planning horizon based on Global Energy’s forecast of new electricity needs over that time frame and Global Energy’s view of how much of that new demand will be met with new gas-fired resources. Monthly hub prices are produced by applying an appropriate shape for seasonality to the model projected annual basis values. We used monthly NYMEX prices and basis swap prices at various market hubs along with Global Energy’s seasonal price shape to produce these values. Input data used in Global Energy’s GPCM specification is prepared using Global Energy Intelligence’s Velocity Suite dataset along with the GPCM gas transportation network and supply assumptions as well as proprietary sector gas demand equations. Combining GPCM with Global Energy’s Power Reference Case forecast is only part of the integrated price forecasting solution Global Energy uses to prepare fundamental energy and fuel price forecasts. Figure ES-4 shows a graphical framework for the generalized equilibrium solution and integrated modeling framework employed. Figure ES-4 Generalized Equilibrium Solution Example

Demand

EmissionPrice

Forecast

Price

Oil Model

Coal Model

ReferenceCase

ForecastPrice Price

Price

Price

Demand

PricePrice

EmissionPrice

Forecast

Oil Model

CoalModel

GasModel

Demand

Demand

EmissionPrice

Forecast

Price

Oil Model

Coal Model

ReferenceCase

ForecastPrice Price

Price

Price

Demand

PricePrice

EmissionPrice

Forecast

Oil Model

CoalModel

GasModel

Demand

SOURCE: Global Energy.

1 The North American Reference Case is a 25-year price forecast of 76 competitive power markets across every North American Electric Reliability Council region. These forecasts are updated twice per year.

Executive Summary

ES-6

Combining the GPCM model with Global Energy’s Market Analytics power model and data platform, fundamentally based world oil, coal and emission models, and our multidisciplinary energy expertise, provides a bottom up fundamental forecast of supply, demand, and market price trends.

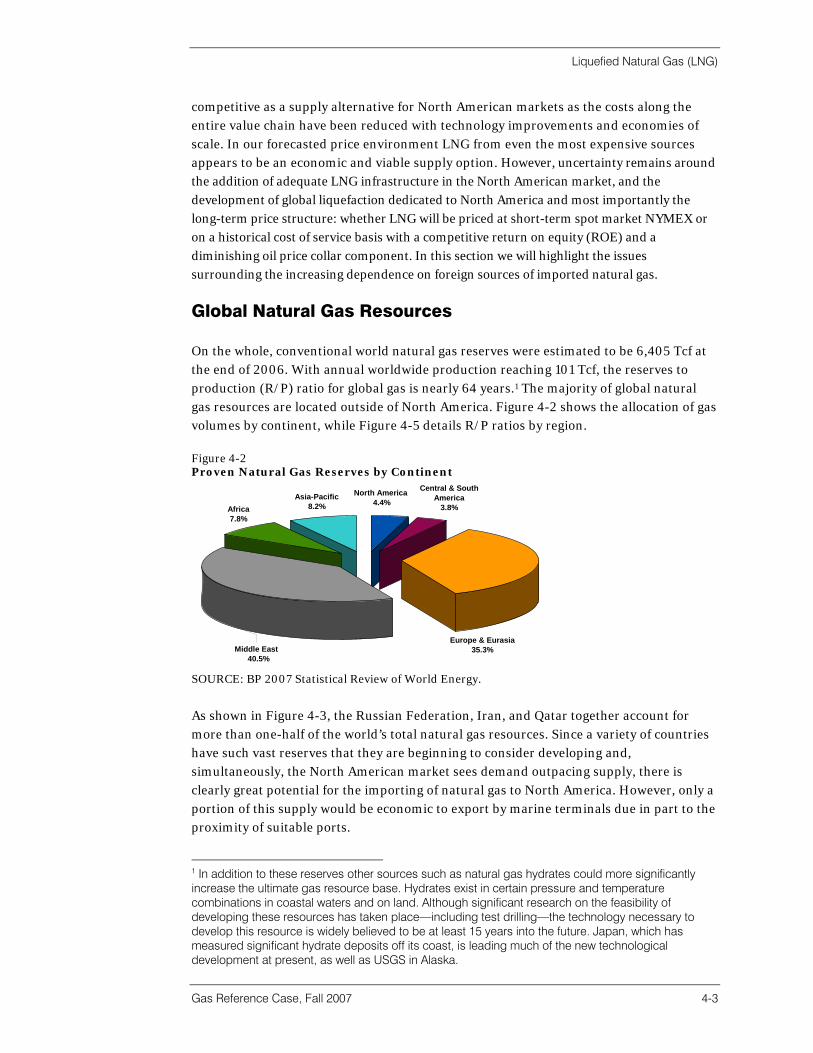

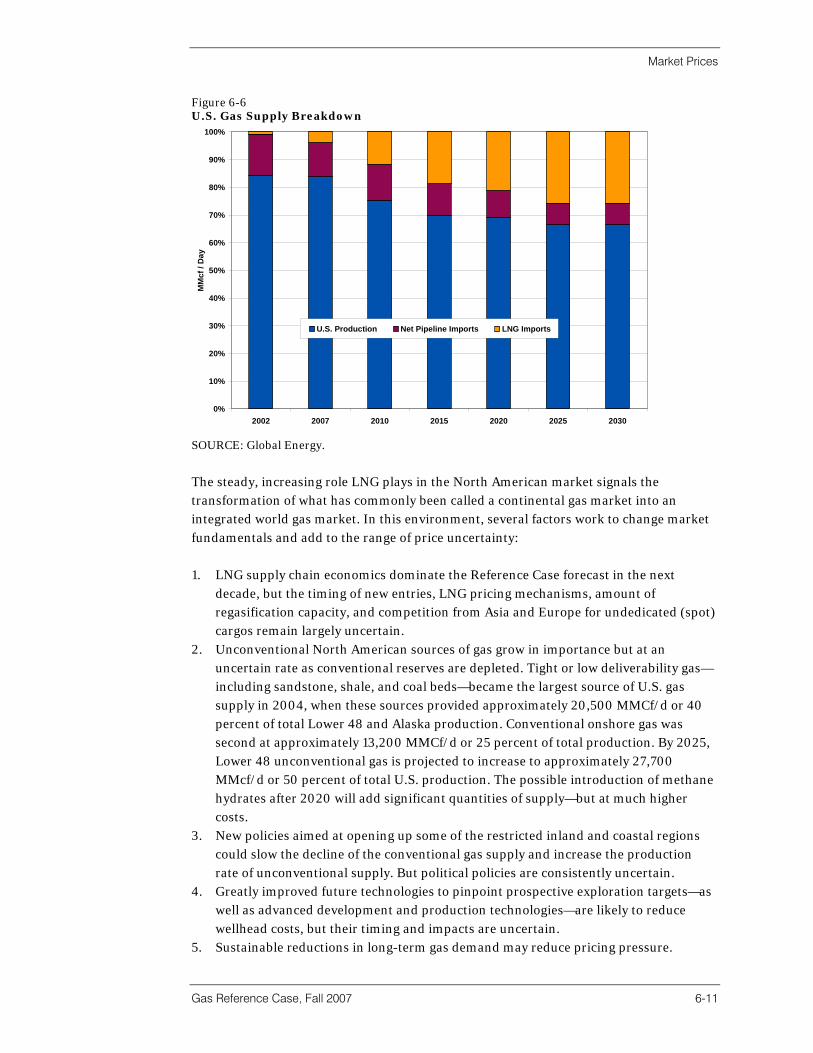

The Sources Of Natural Gas Will Change Much of the analysis presented in this report quantifies several market forces that have “upset” conventional views of the natural gas market in North America. In Global Energy’s opinion, the North American natural gas market is transforming from a continental gas market, mostly disconnected from world LNG trade, to a more integrated global gas market with increasing dependence on various global LNG suppliers. This transformation has begun, in part, due to rising supply cost options, conventional reserve depletion, and because of the impending growth in gas demand for electric power generation. From our analysis, by 2020 over 21 percent of U.S. gas supply will be sourced from LNG with less than 10 percent coming from pipeline imports. By 2030, LNG supply will increase to nearly 26 percent of total requirements while less than 8 percent will come from North American pipeline imports. Figure ES-5 shows the breakdown of the source of U.S. gas supply beginning in 2002 through 2030.

Figure ES-5 Source of Gas Consumed in the United States

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2002 2007 2010 2015 2020 2025 2030

MM

cf /

Day

U.S. Production Net Pipeline Imports LNG Imports

SOURCE: Global Energy.

By 2011, under Global Energy’s Reference Case, North America is expected to overtake Europe, currently the second largest global importer of LNG. In that year, we expect LNG imports to exceed 10.3 Bcf/d to the U.S., Mexico, and Canada. While delays in building

Executive Summary

Gas Reference Case, Fall 2007 ES-7

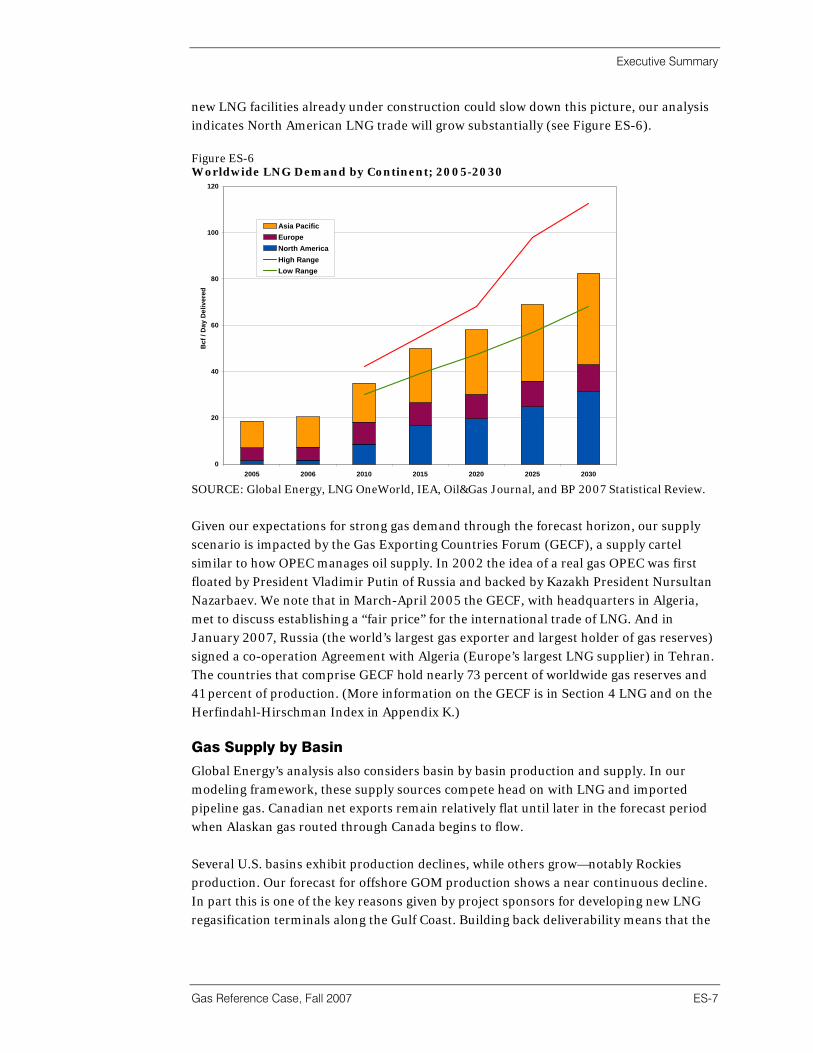

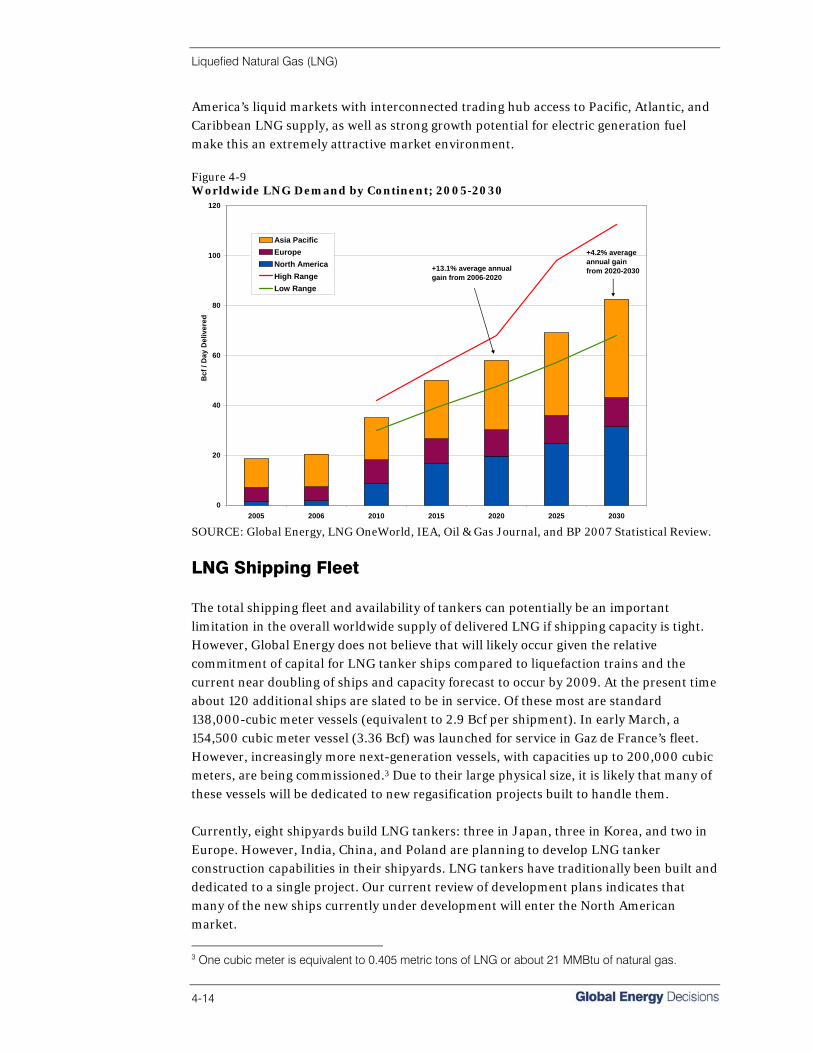

new LNG facilities already under construction could slow down this picture, our analysis indicates North American LNG trade will grow substantially (see Figure ES-6). Figure ES-6 Worldwide LNG Demand by Continent; 2005-2030

0

20

40

60

80

100

120

2005 2006 2010 2015 2020 2025 2030

Bcf

/ D

ay D

eliv

ered

Asia PacificEuropeNorth AmericaHigh RangeLow Range

SOURCE: Global Energy, LNG OneWorld, IEA, Oil&Gas Journal, and BP 2007 Statistical Review.

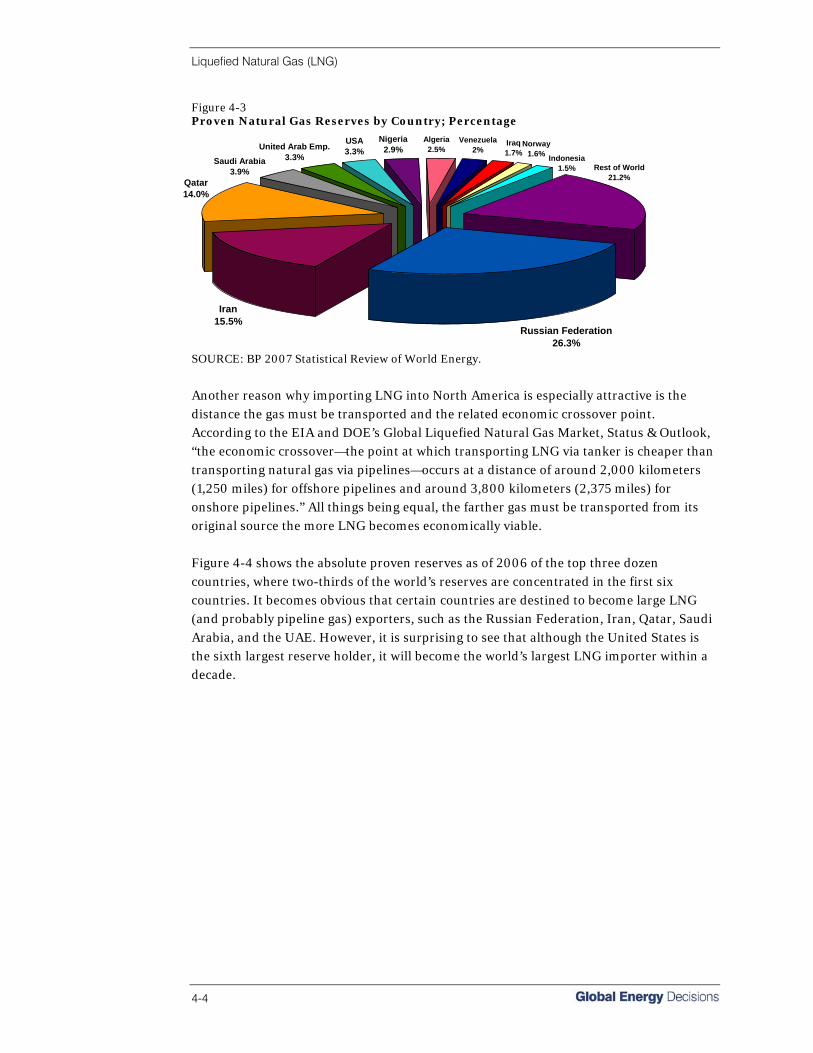

Given our expectations for strong gas demand through the forecast horizon, our supply scenario is impacted by the Gas Exporting Countries Forum (GECF), a supply cartel similar to how OPEC manages oil supply. In 2002 the idea of a real gas OPEC was first floated by President Vladimir Putin of Russia and backed by Kazakh President Nursultan Nazarbaev. We note that in March-April 2005 the GECF, with headquarters in Algeria, met to discuss establishing a “fair price” for the international trade of LNG. And in January 2007, Russia (the world’s largest gas exporter and largest holder of gas reserves) signed a co-operation Agreement with Algeria (Europe’s largest LNG supplier) in Tehran. The countries that comprise GECF hold nearly 73 percent of worldwide gas reserves and 41 percent of production. (More information on the GECF is in Section 4 LNG and on the Herfindahl-Hirschman Index in Appendix K.) Gas Supply by Basin

Global Energy’s analysis also considers basin by basin production and supply. In our modeling framework, these supply sources compete head on with LNG and imported pipeline gas. Canadian net exports remain relatively flat until later in the forecast period when Alaskan gas routed through Canada begins to flow. Several U.S. basins exhibit production declines, while others grow—notably Rockies production. Our forecast for offshore GOM production shows a near continuous decline. In part this is one of the key reasons given by project sponsors for developing new LNG regasification terminals along the Gulf Coast. Building back deliverability means that the

Executive Summary

ES-8

existing network of offshore, onshore, and interstate pipelines will remain well utilized in the future. Since onshore and offshore GOM production represents nearly 36 percent of current domestic production, replacing part of that decline from other sources will be challenging. Furthermore, many of the offshore GOM conventional wells lie in deep water and experience exponential decline rates, some with a first-year decline equaling 50 percent of the initial production rate. Thus, offshore GOM production is relatively expensive. Demand by Sector

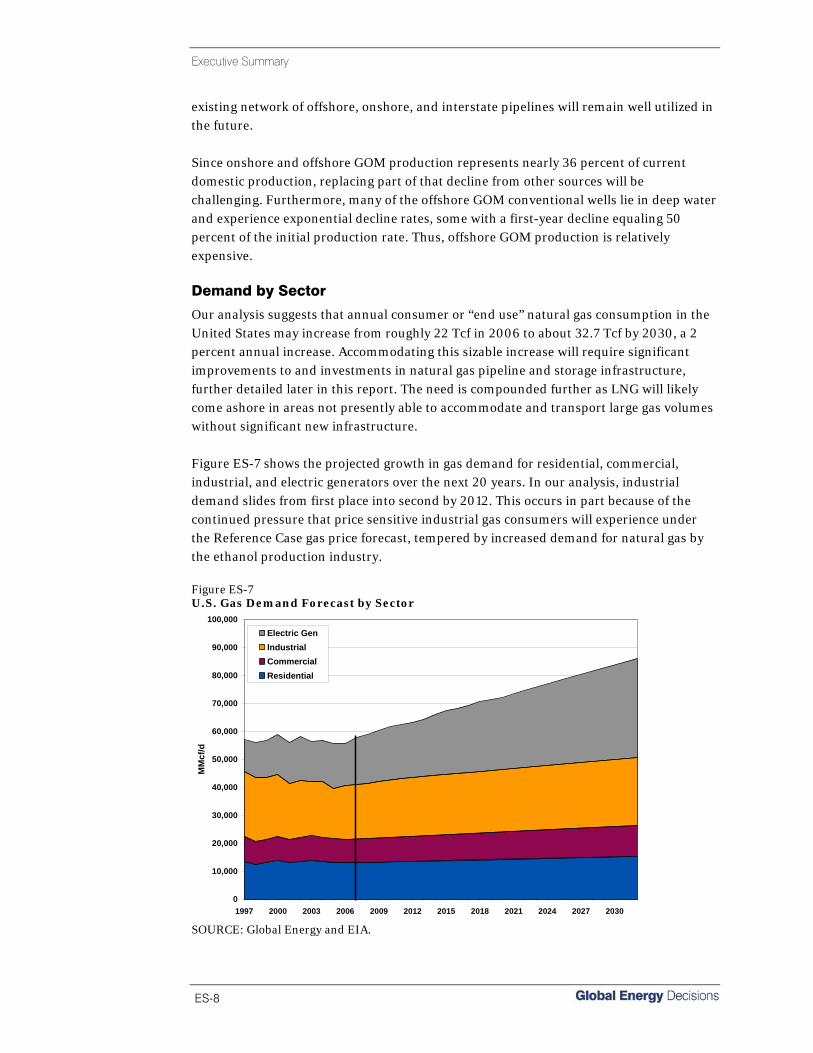

Our analysis suggests that annual consumer or “end use” natural gas consumption in the United States may increase from roughly 22 Tcf in 2006 to about 32.7 Tcf by 2030, a 2 percent annual increase. Accommodating this sizable increase will require significant improvements to and investments in natural gas pipeline and storage infrastructure, further detailed later in this report. The need is compounded further as LNG will likely come ashore in areas not presently able to accommodate and transport large gas volumes without significant new infrastructure. Figure ES-7 shows the projected growth in gas demand for residential, commercial, industrial, and electric generators over the next 20 years. In our analysis, industrial demand slides from first place into second by 2012. This occurs in part because of the continued pressure that price sensitive industrial gas consumers will experience under the Reference Case gas price forecast, tempered by increased demand for natural gas by the ethanol production industry. Figure ES-7 U.S. Gas Demand Forecast by Sector

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

1997 2000 2003 2006 2009 2012 2015 2018 2021 2024 2027 2030

MM

cf/d

Electric GenIndustrialCommercialResidential

SOURCE: Global Energy and EIA.

Executive Summary

Gas Reference Case, Fall 2007 ES-9

Continued demand growth for generation will place constant pressure on the supply industry’s ability to find and develop new sources of natural gas. In our analysis, electric generators tend to be far less price sensitive than many industrial consumers. Fuel is only one of several components to the price of delivered power so higher fuel prices will have a less than proportional impact on power prices. Much of the gas demand growth in this sector is due to the delayed impact of the electric power overbuild. Currently, many power markets are significantly overbuilt with combined cycle, gas-fired power plants. However, these plants will increasingly be used over the coming 5-10-year time frame due to continued electric load growth, retirements of older existing plants, and new environmental restrictions (e.g., NOX, SO2, CO2, Hg, etc.), which will increase the cost of generation for some solid fuel and oil-fired generators. As an example of this new paradigm where environmental factors must be taken into account, Figure ES-8 outlines the period from January 2005 through March 2007 when SO2 and NOX allowance prices were relatively very high. It indicates that the typical older vintage residual oil-fired ST was significantly penalized in relation to a gas-fired ST of similar vintage. As shown on the right-hand axis, the penalty (increased SO2/NOx adder in SIP call states and just SO2 in other states) during this period varied between $0.30/dth and nearly $1.00/dth, a hefty amount. The increased penalty for burning residual fuel oil during 2006 (not just 1 percent sulfur but for other qualities such as 0.3 percent, 0.5 percent, 0.7 percent and 2 percent as well) was one of the reasons for greatly increased natural gas usage for electric generation that year, taking over the #2 spot from nuclear power. In the future, it is anticipated that CO2 adders will similarly impact coal and well as oil plants, being at a proportional disadvantage as compared to natural gas units. Figure ES-8 SO2 and NOX Allowance Prices with Increased Adder for 1 percent Sulfur Residual Oil

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

Jan-

05

Feb-

05

Mar

-05

Apr

-05

May

-05

Jun-

05

Jul-0

5

Aug

-05

Sep-

05

Oct

-05

Nov

-05

Dec

-05

Jan-

06

Feb-

06

Mar

-06

Apr

-06

May

-06

Jun-

06

Jul-0

6

Aug

-06

Sep-

06

Oct

-06

Nov

-06

Dec

-06

Jan-

07

Feb-

07

Mar

-07

$ Pe

r Allo

wan

ce

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

$ Pe

r MM

Btu

Allo

wan

ce P

enal

tyAll Resid Penalty due to NOx

Resid 1% S Penalty due to SO2

NOx Allowances (left axis)

SO2 Allowances (left axis)

SOURCE: Global Energy and Cantor-Fitzgerald Brokerage L.P.

Table of Contents

Gas Reference Case, Fall 2007 i

Executive Summary ES-1

1 Introduction And Current Market Overview 1-1

Report Objectives .....................................................................................................1-1 Market Overview .......................................................................................................1-2 Changing U.S. Gas Demand....................................................................................1-4 The Changing Role Of LNG In North America ........................................................1-5 Greater FERC And CFTC Oversight Of Gas Markets ..............................................1-7 Land Access Restrictions For Drilling ......................................................................1-9 Rising Finding & Developing (F&D) Costs And Growth ........................................1-10 Gas-Fired Generation Demand Growth .................................................................1-11 Natural Gas And Crude Oil Price Relationship ......................................................1-12 Additional Market Forces........................................................................................1-14 Report Outline.........................................................................................................1-15

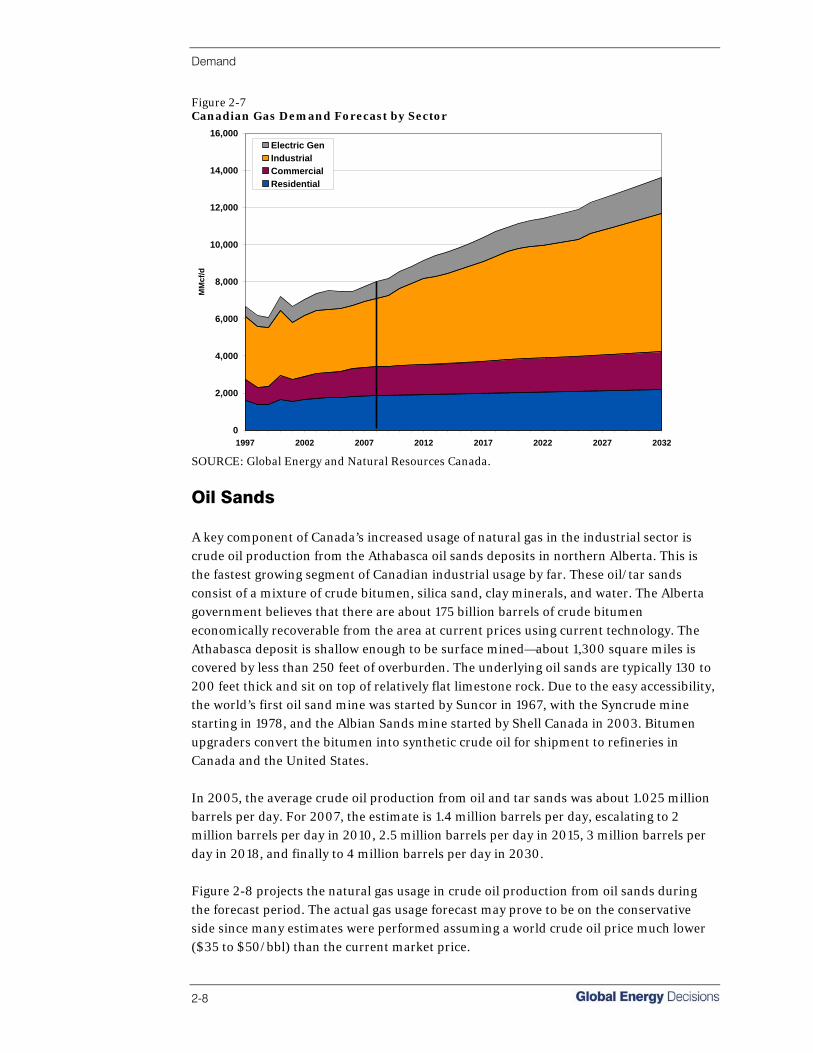

2 Demand 2-1

Introduction...............................................................................................................2-1 U.S. Demand Trends ................................................................................................2-1 Ethanol ......................................................................................................................2-2 Electric Generation ...................................................................................................2-4 Canadian Demand Trends .......................................................................................2-7 Oil Sands ..................................................................................................................2-8 South Atlantic Division ..............................................................................................2-9

• Core Demand...................................................................................................2-10

• Industrial Demand............................................................................................2-10

• Electric Generation Demand ...........................................................................2-11

Middle Atlantic Division...........................................................................................2-11

• Core Demand...................................................................................................2-12

• Industrial Demand............................................................................................2-12

• Electric Generation Demand ...........................................................................2-12

New England Division.............................................................................................2-13

• Core Demand...................................................................................................2-14

• Industrial Demand............................................................................................2-14

• Electric Generation Demand ...........................................................................2-14

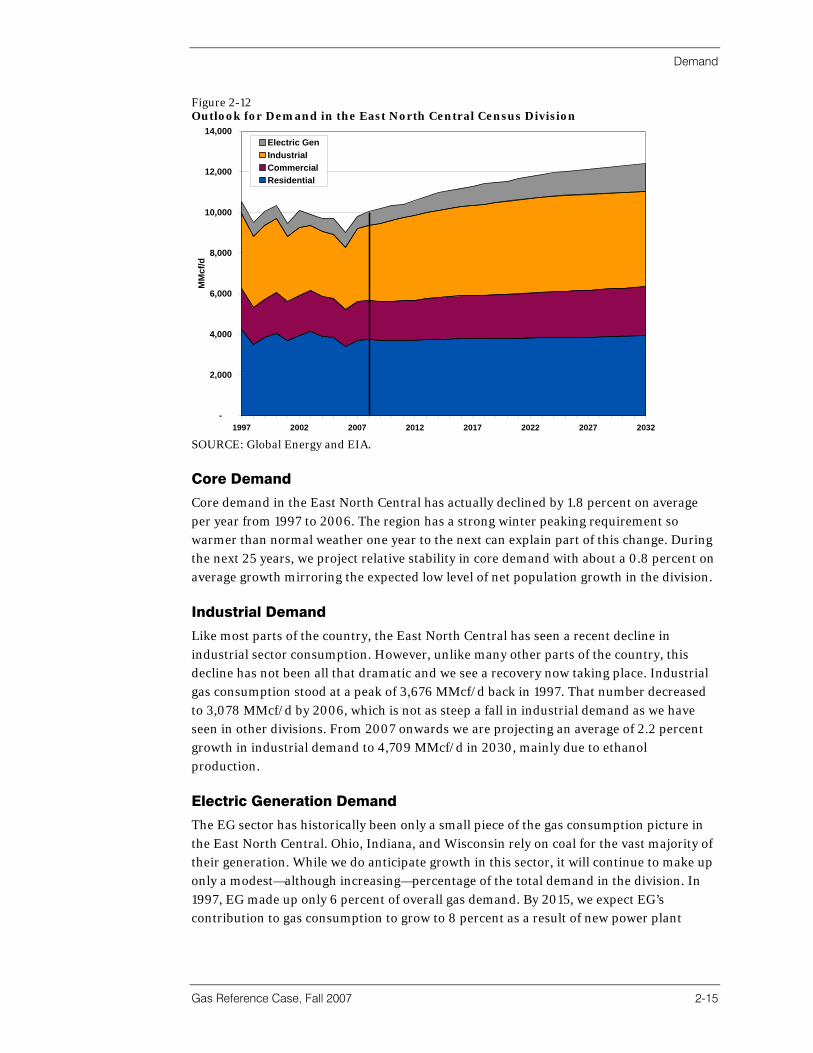

East North Central Division.....................................................................................2-14

• Core Demand...................................................................................................2-15

• Industrial Demand............................................................................................2-15

• Electric Generation Demand ...........................................................................2-15

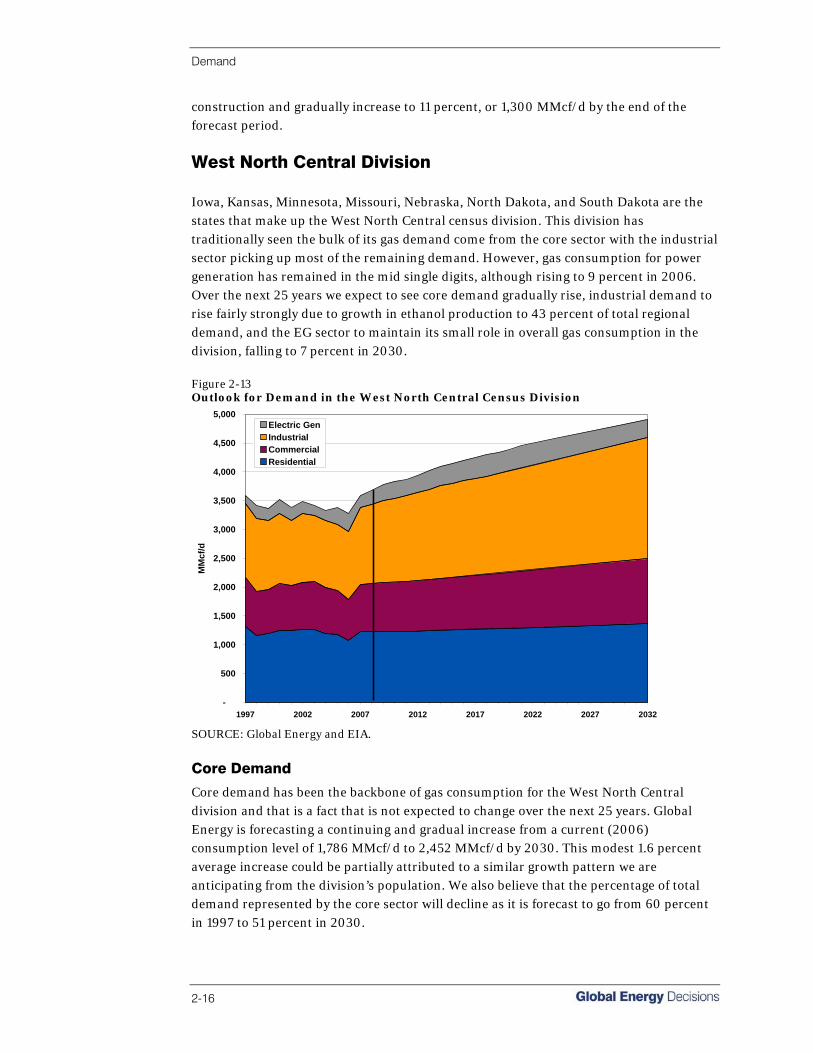

West North Central Division....................................................................................2-16

• Core Demand...................................................................................................2-16

Table of Contents

ii

• Industrial Demand............................................................................................2-17

• Electric Generation Demand ...........................................................................2-17

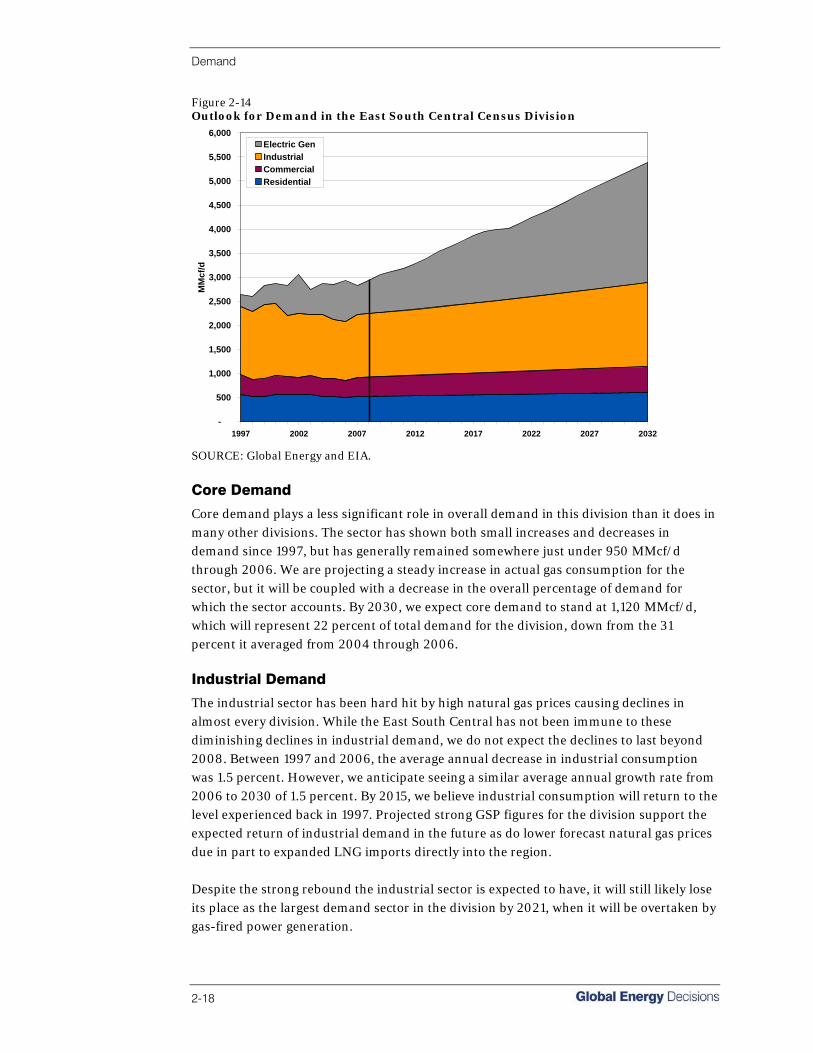

East South Central Division ....................................................................................2-17

• Core Demand...................................................................................................2-18

• Industrial Demand............................................................................................2-18

• Electric Generation Demand ...........................................................................2-19

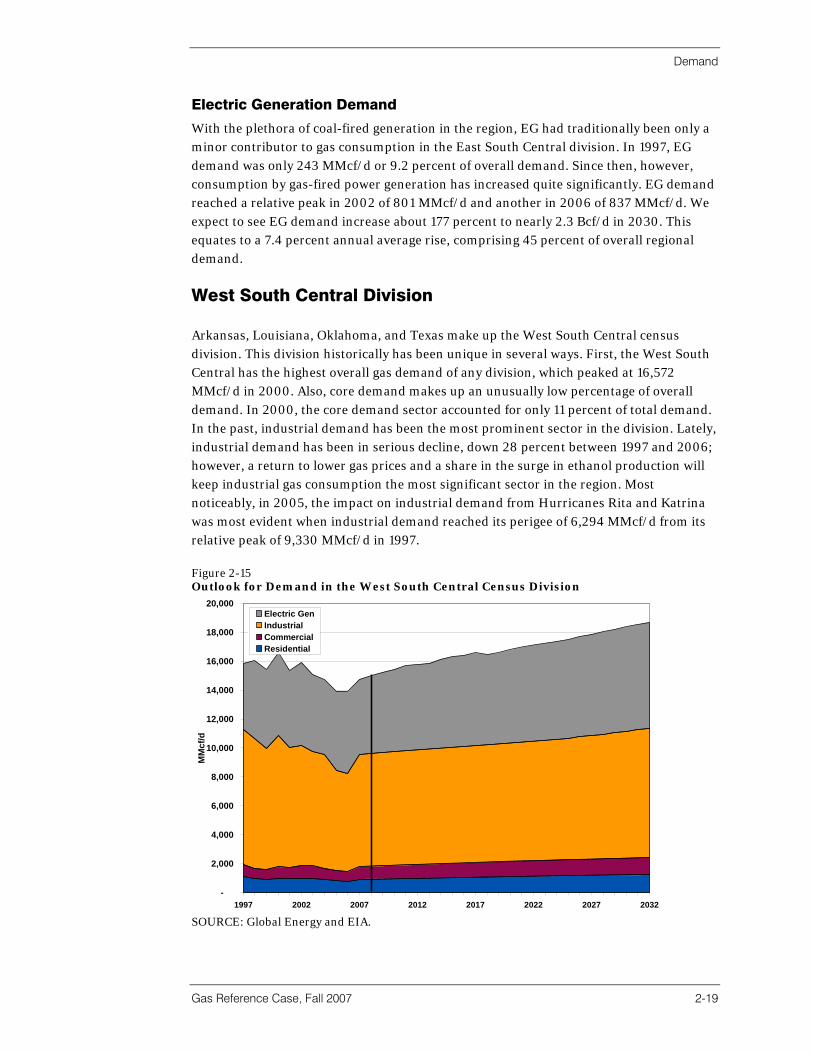

West South Central Division ...................................................................................2-19

• Core Demand...................................................................................................2-20

• Industrial Demand............................................................................................2-20

• Electric Generation Demand ...........................................................................2-20

Mountain Division ...................................................................................................2-20

• Core Demand...................................................................................................2-21

• Industrial Demand............................................................................................2-21

• Electric Generation Demand ...........................................................................2-22

Pacific Division........................................................................................................2-22

• Core Demand...................................................................................................2-22

• Industrial Demand............................................................................................2-23

• Electric Generation Demand ...........................................................................2-23

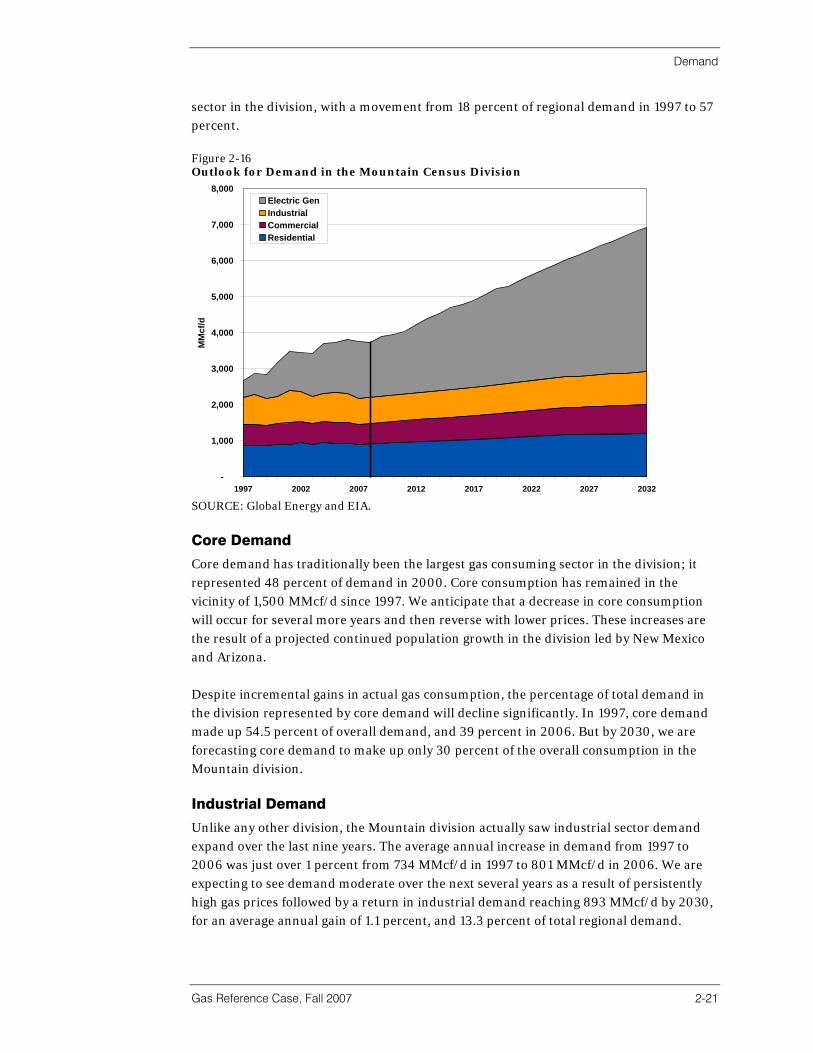

Conclusions ............................................................................................................2-23

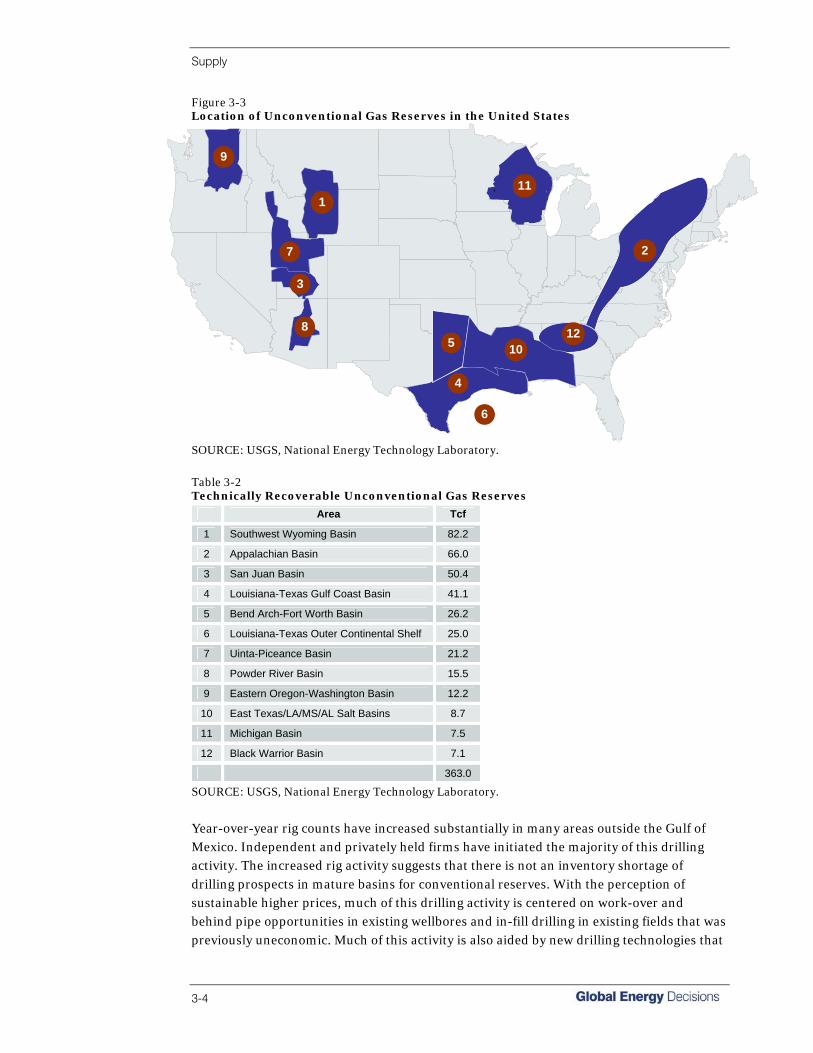

3 Supply 3-1

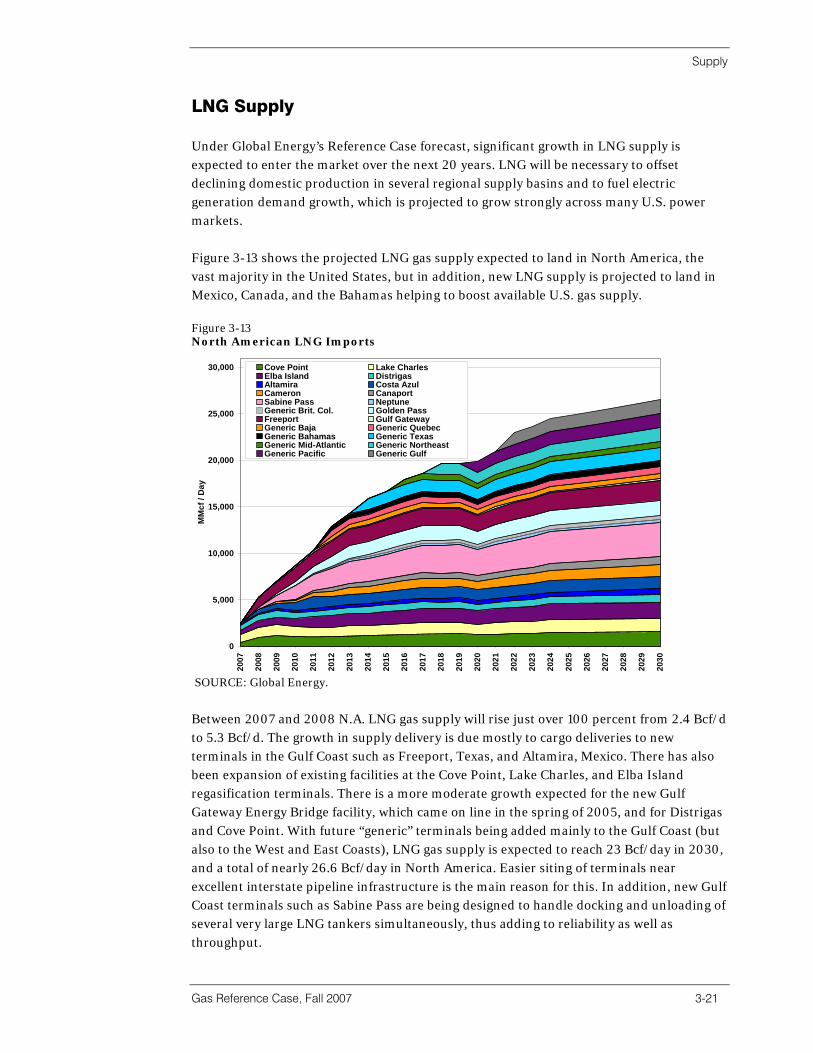

Introduction...............................................................................................................3-1 Supply Methodology.................................................................................................3-7 Supply Cost Curves ..................................................................................................3-8 North American Supply Picture ................................................................................3-9 Working Gas Storage .............................................................................................3-17 Market Hubs ...........................................................................................................3-18 LNG Supply.............................................................................................................3-21 Supply Uncertainty..................................................................................................3-23

4 Liquefied Natural Gas (LNG) 4-1

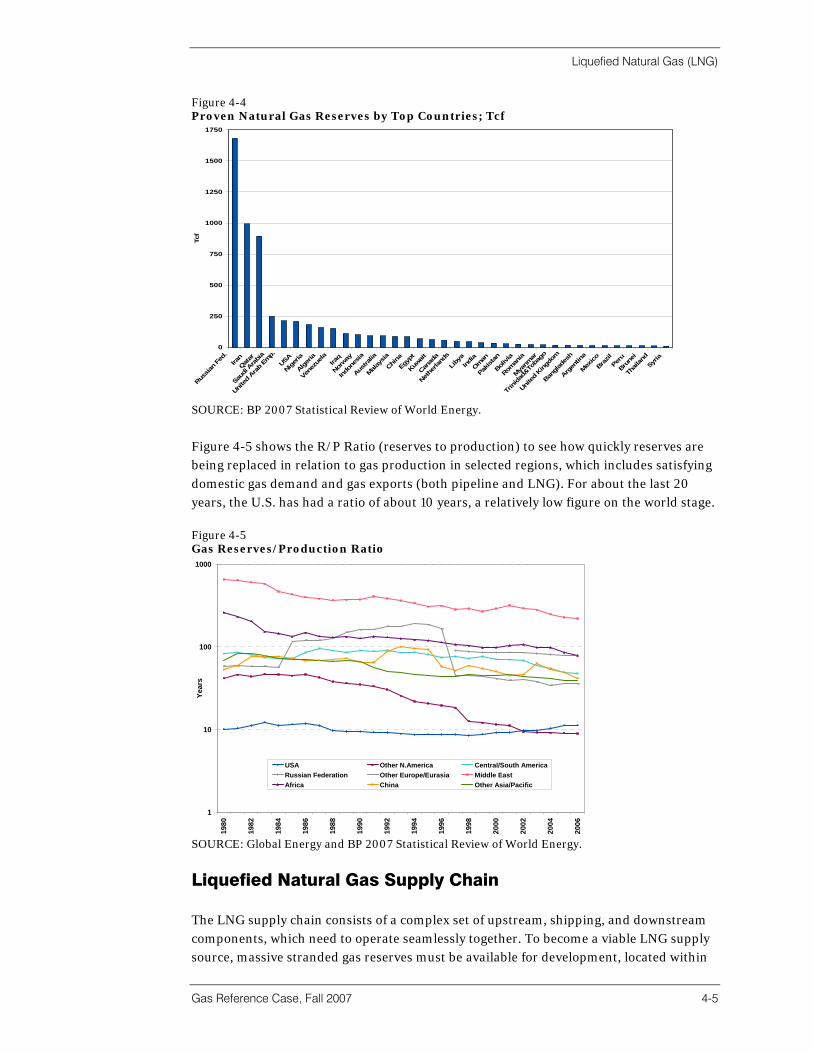

Introduction...............................................................................................................4-1 Global Natural Gas Resources.................................................................................4-3 Liquefied Natural Gas Supply Chain .......................................................................4-5

• LNG Liquefaction ...............................................................................................4-6

• LNG Transportation ...........................................................................................4-6

• LNG Regasification ............................................................................................4-7

• LNG Storage ......................................................................................................4-7

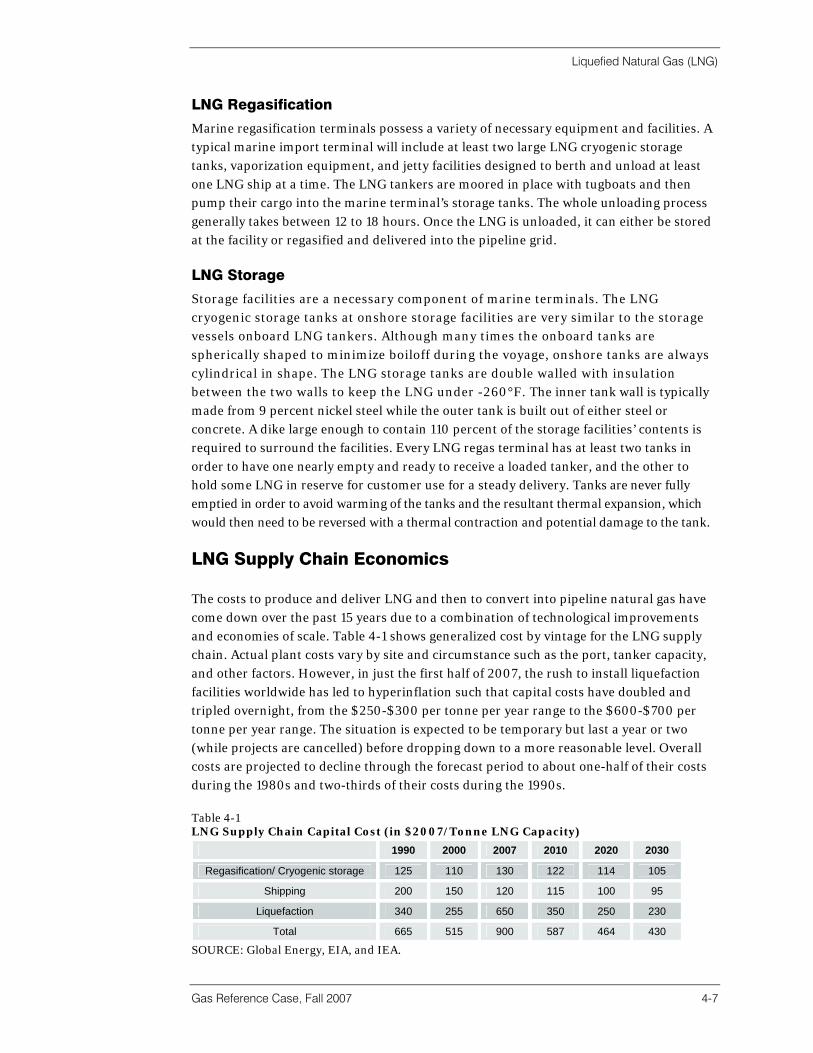

LNG Supply Chain Economics.................................................................................4-7 Global Liquefaction Trade ........................................................................................4-8

Table of Contents

Gas Reference Case, Fall 2007 iii

• Exporting Countries ...........................................................................................4-8

• Importing Countries ...........................................................................................4-9

Global Liquefaction Projections .............................................................................4-10

• Global LNG Supply ..........................................................................................4-10

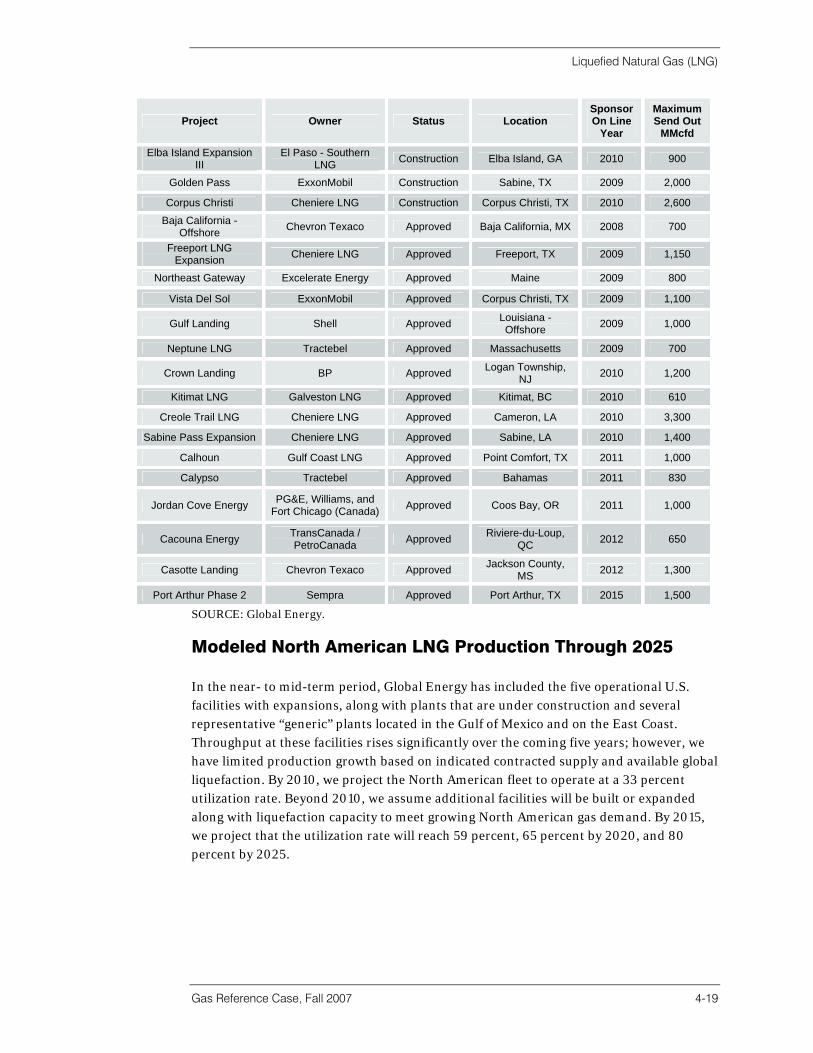

Global LNG Demand ..............................................................................................4-11 LNG Shipping Fleet ................................................................................................4-14 Overview Of LNG In North America........................................................................4-15 Outlook For Regasification in North America.........................................................4-16 Modeled North American LNG Production Through 2025.....................................4-19

• LNG Concerns .................................................................................................4-21

• LNG Siting and Permitting ...............................................................................4-23

Regasification Economics In North America..........................................................4-24 Implied Infrastructure Requirements ......................................................................4-25 Possible LNG Cartel ...............................................................................................4-26 Costs.......................................................................................................................4-28 Summary And Conclusions....................................................................................4-29

5 Infrastructure 5-1

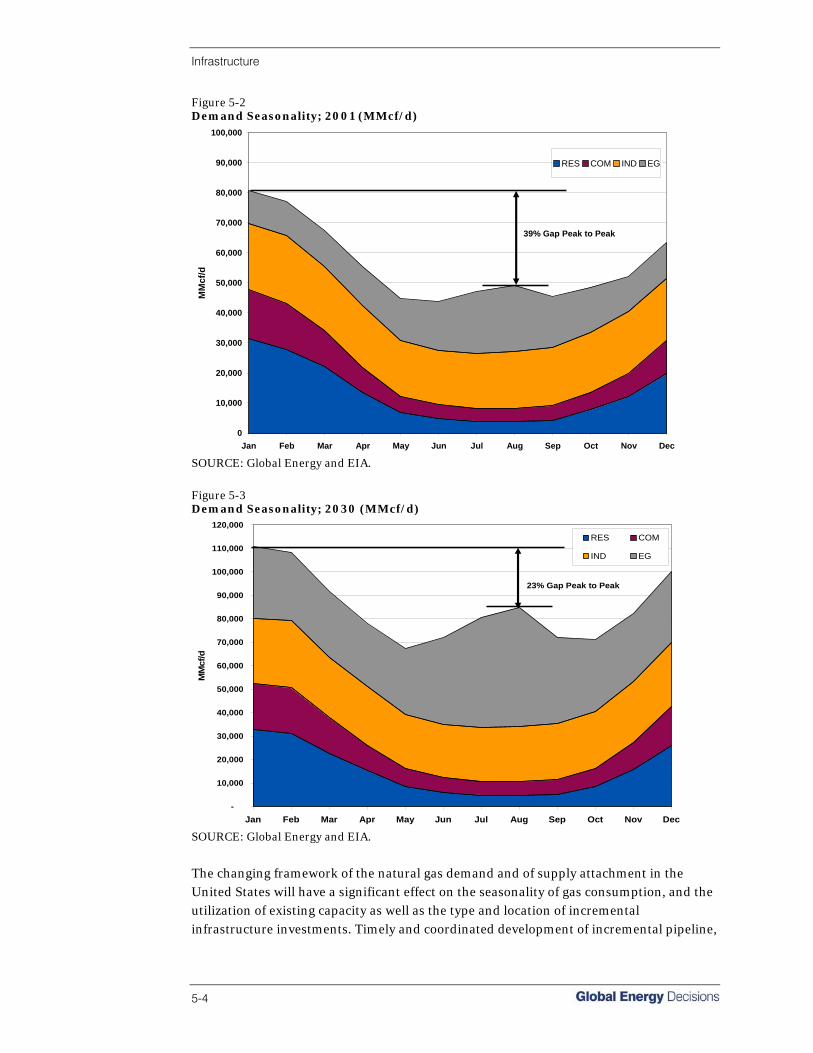

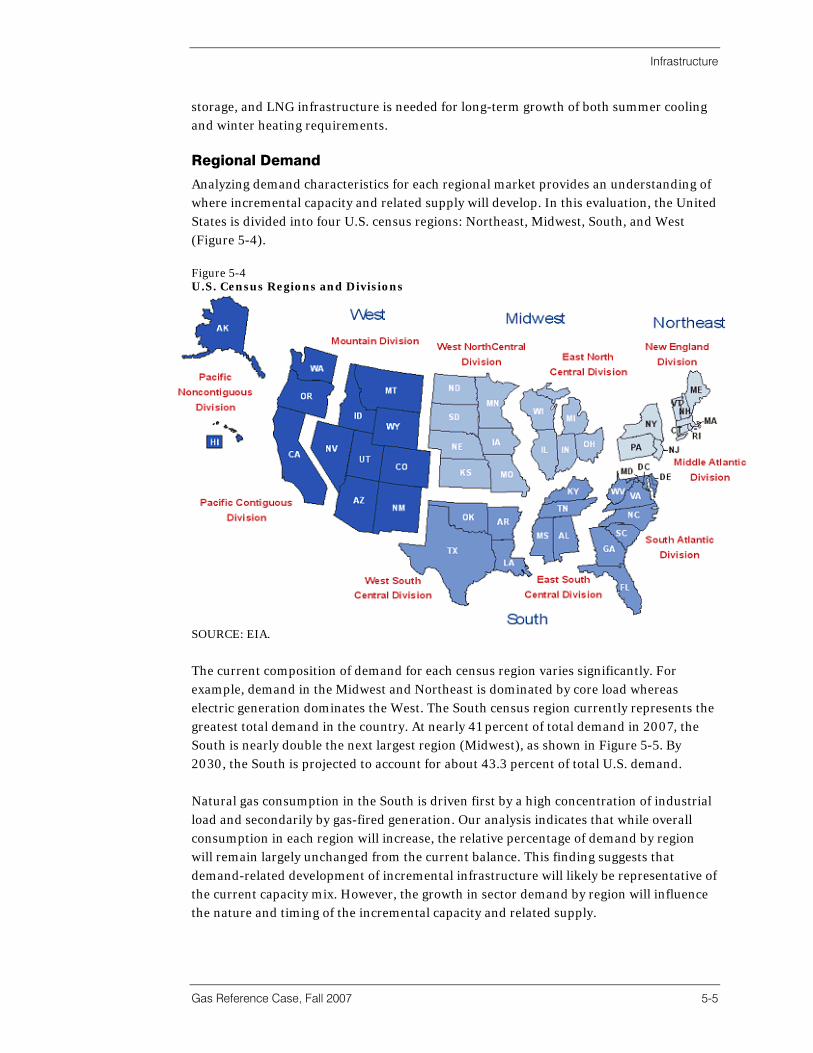

Introduction...............................................................................................................5-1 Demand Influences...................................................................................................5-1

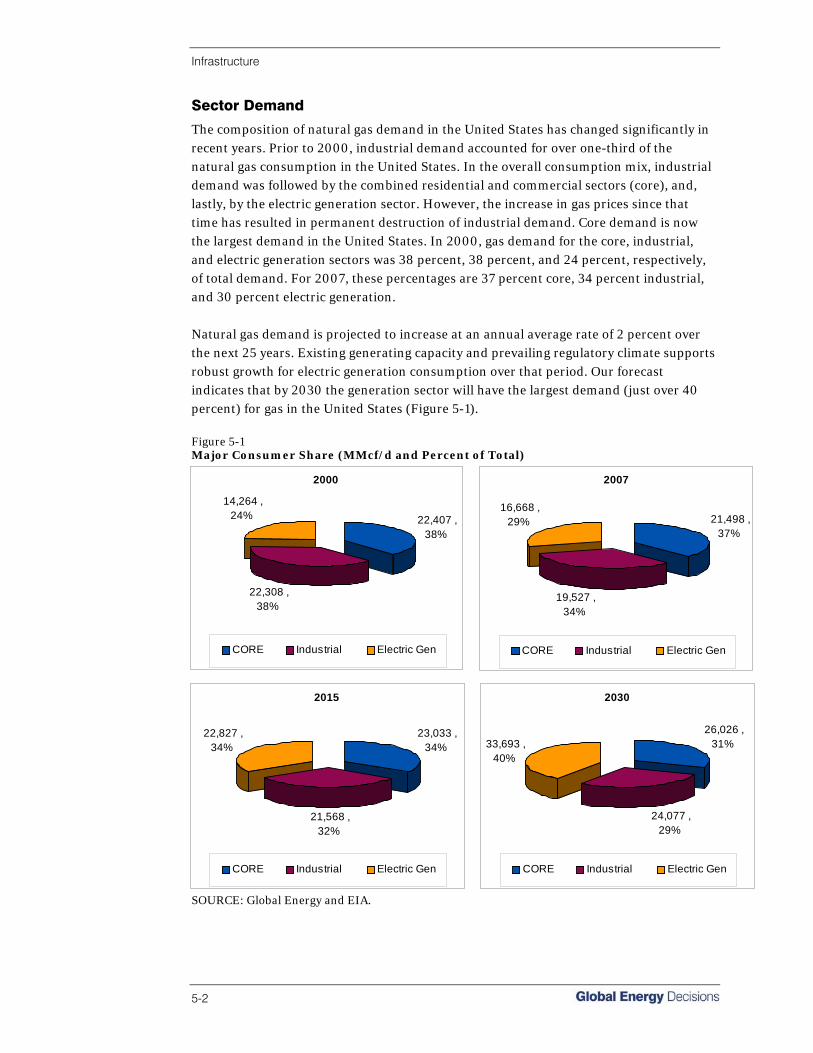

• Sector Demand..................................................................................................5-2

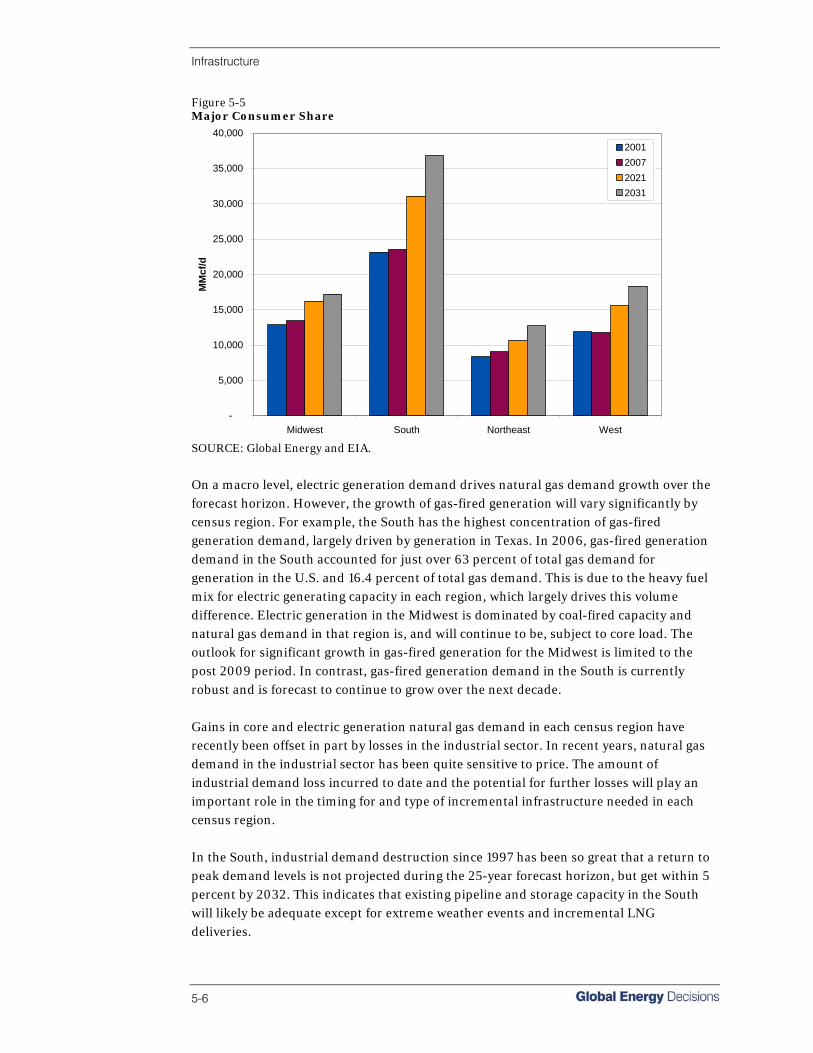

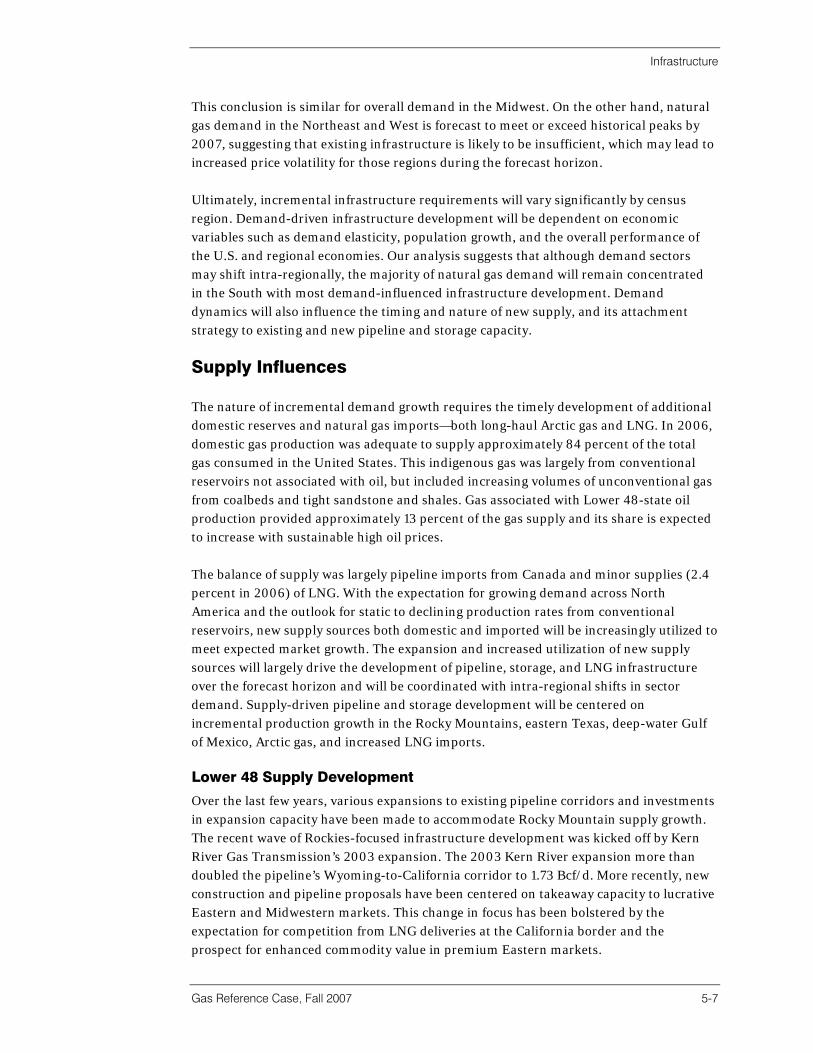

• Regional Demand ..............................................................................................5-5

Supply Influences .....................................................................................................5-7

• Lower 48 Supply Development..........................................................................5-7

• Arctic Gas...........................................................................................................5-9

• Imported Natural Gas and LNG ......................................................................5-13

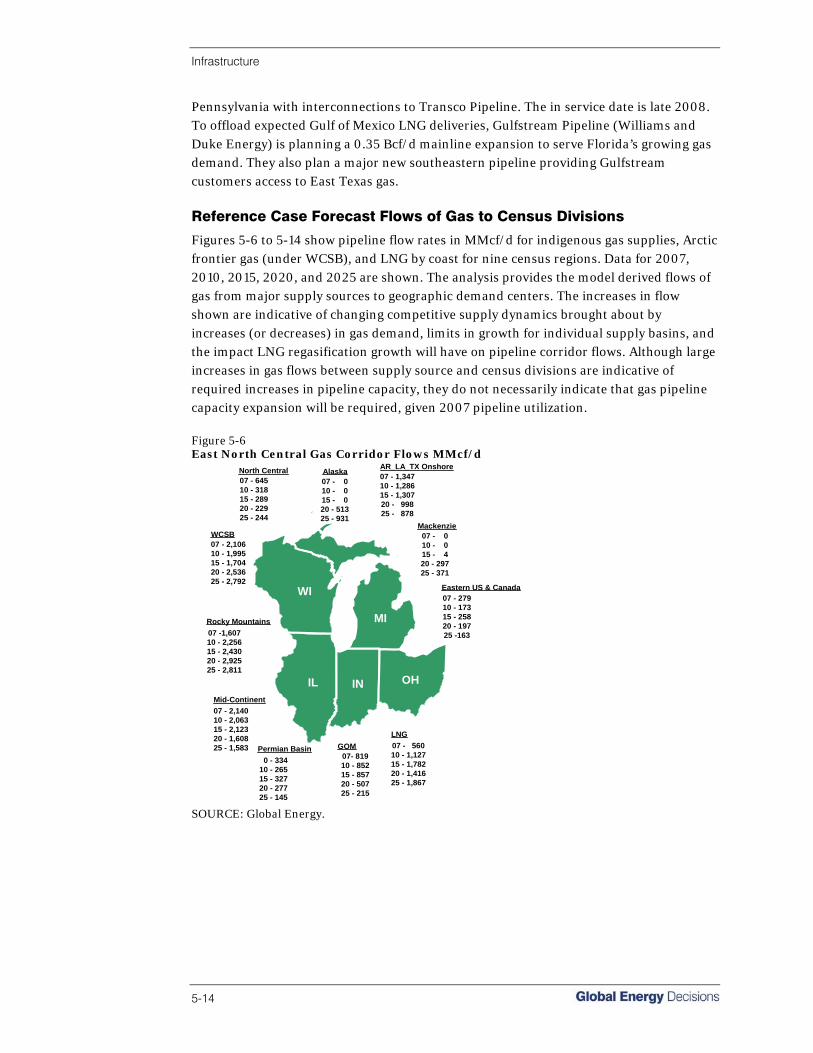

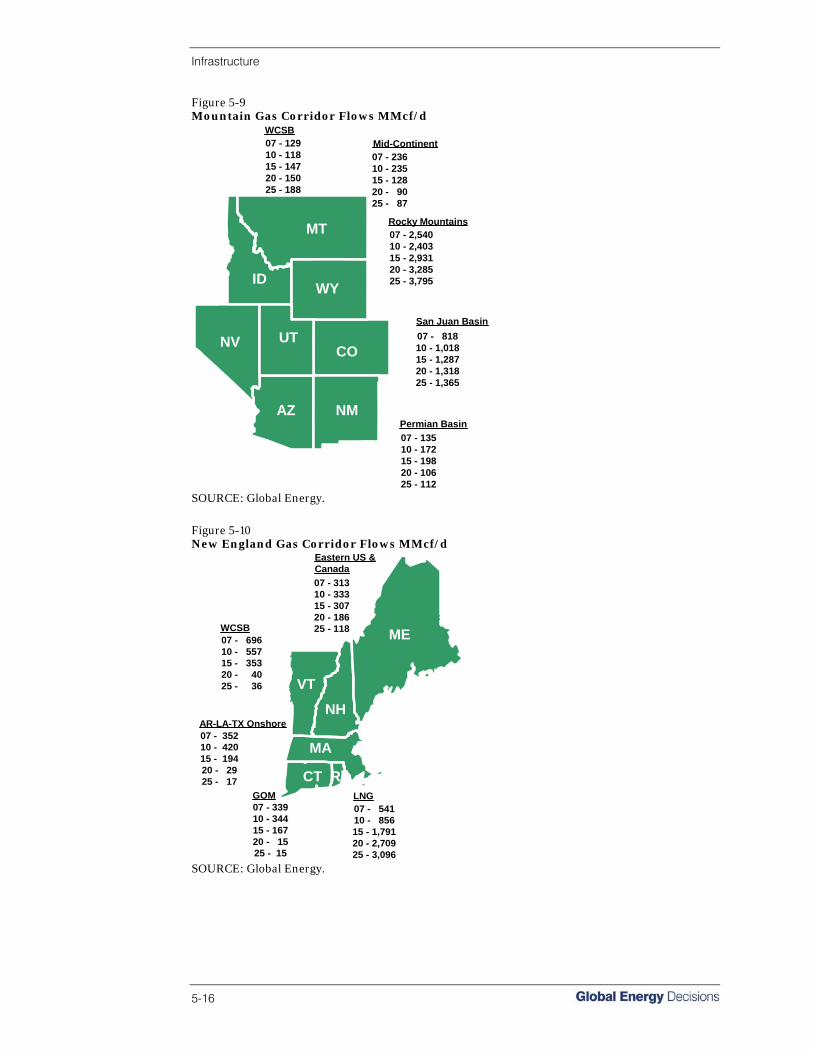

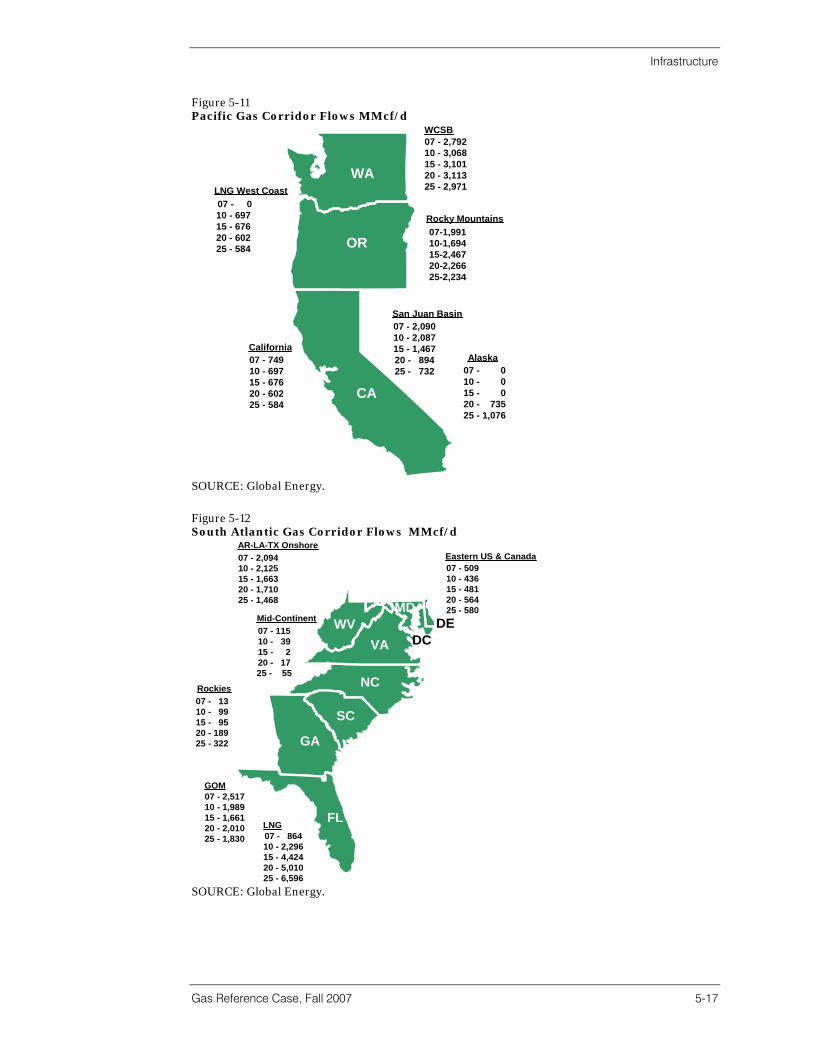

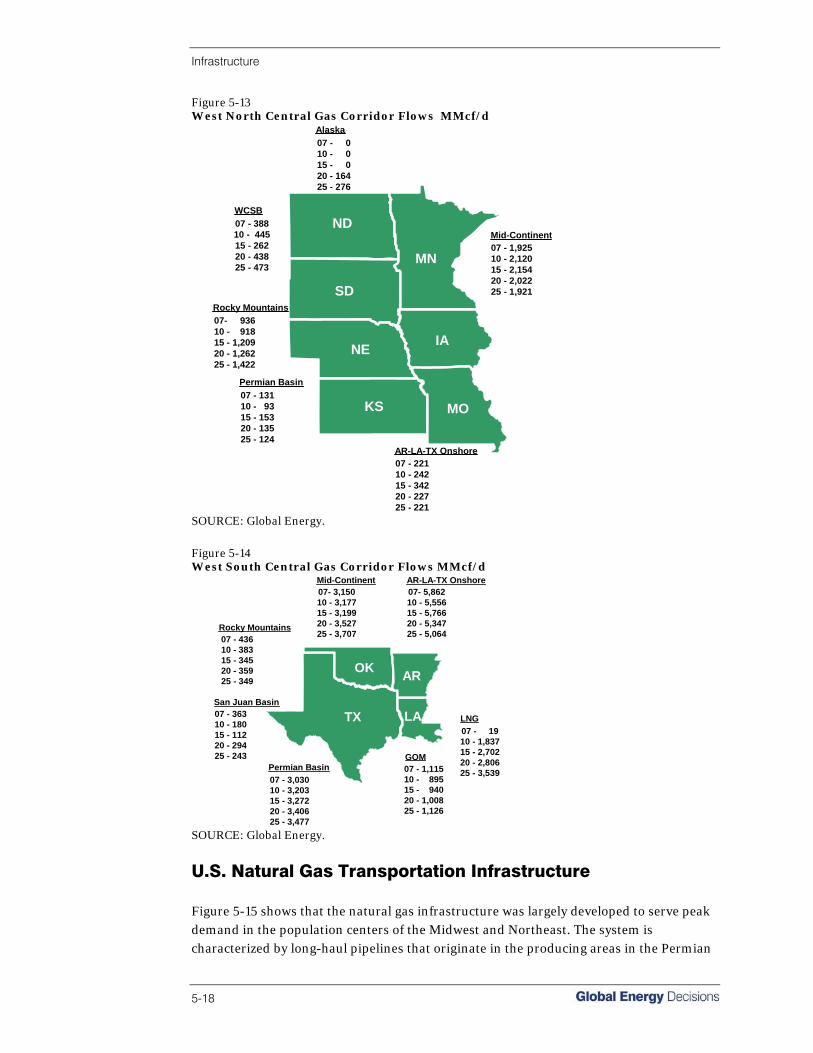

• Reference Case Forecast Flows of Gas to Census Divisions ........................5-14

U.S. Natural Gas Transportation Infrastructure......................................................5-18

• National Transportation Growth and Associated Costs..................................5-26

• Regional Transportation Growth......................................................................5-26

• Natural Gas Storage Infrastructure in the United States.................................5-27

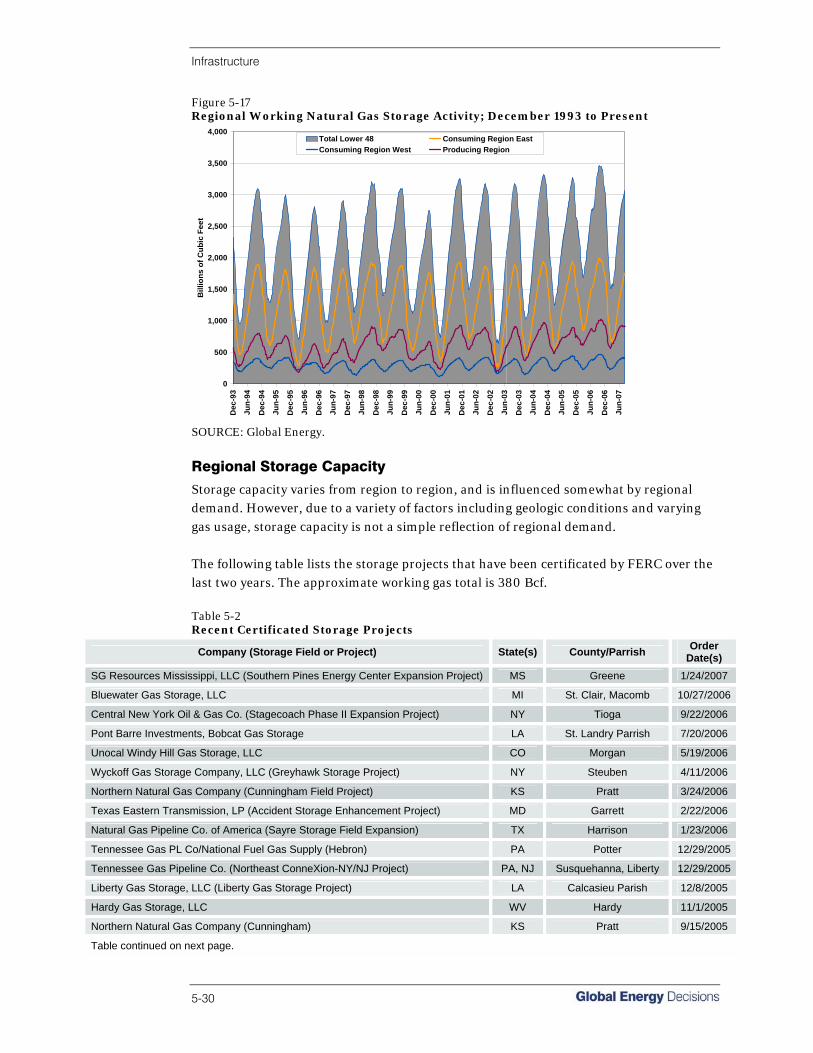

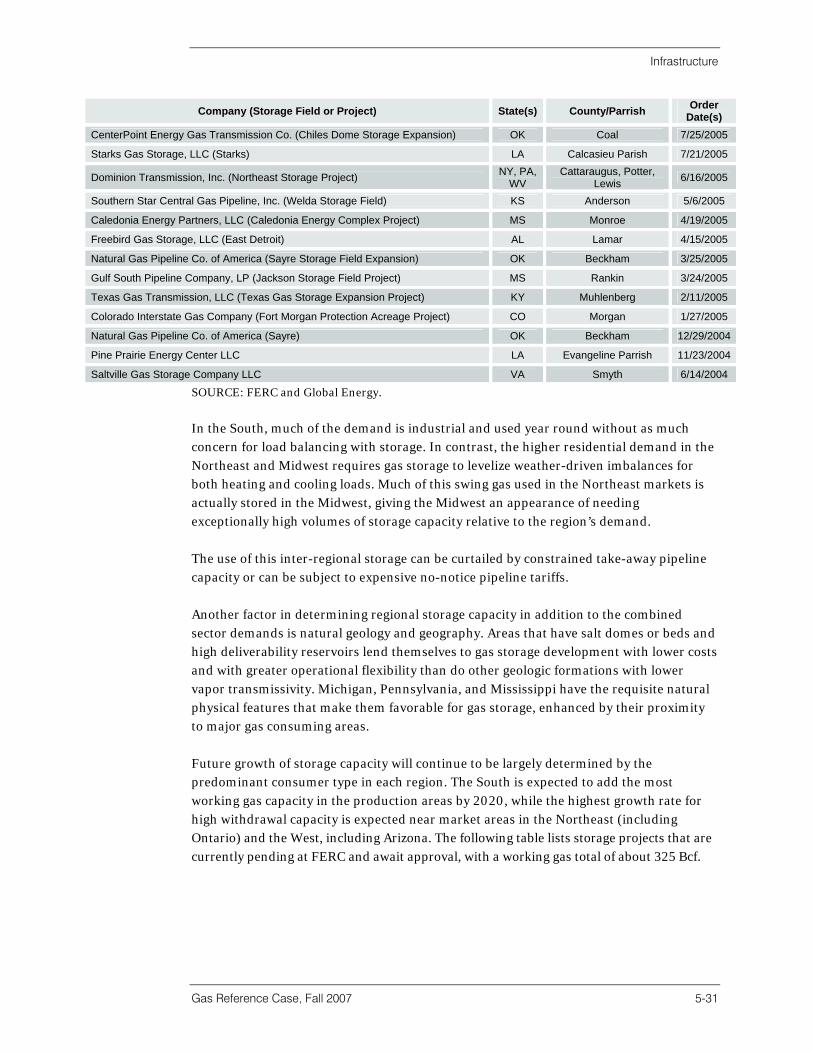

• Regional Storage Capacity..............................................................................5-30

Summary and Conclusions ....................................................................................5-32

6 Market Prices 6-1

Historical Market Perspective ...................................................................................6-1 Gas Market Evolution ...............................................................................................6-4 Natural Gas Market Phases......................................................................................6-5

• 1990s Supply Bubble.........................................................................................6-5

• Transforming Market: 2000-2004 ......................................................................6-6

Table of Contents

iv

• Market Scarcity: 2005-2008...............................................................................6-7

• LNG Renaissance: 2009-2015 ..........................................................................6-8

• Arctic Gas Flows: 2015-2025.............................................................................6-9

• Rising Costs and Depletion: 2009-2030..........................................................6-10

• Global Gas Market Integration: 2009 and Beyond..........................................6-10

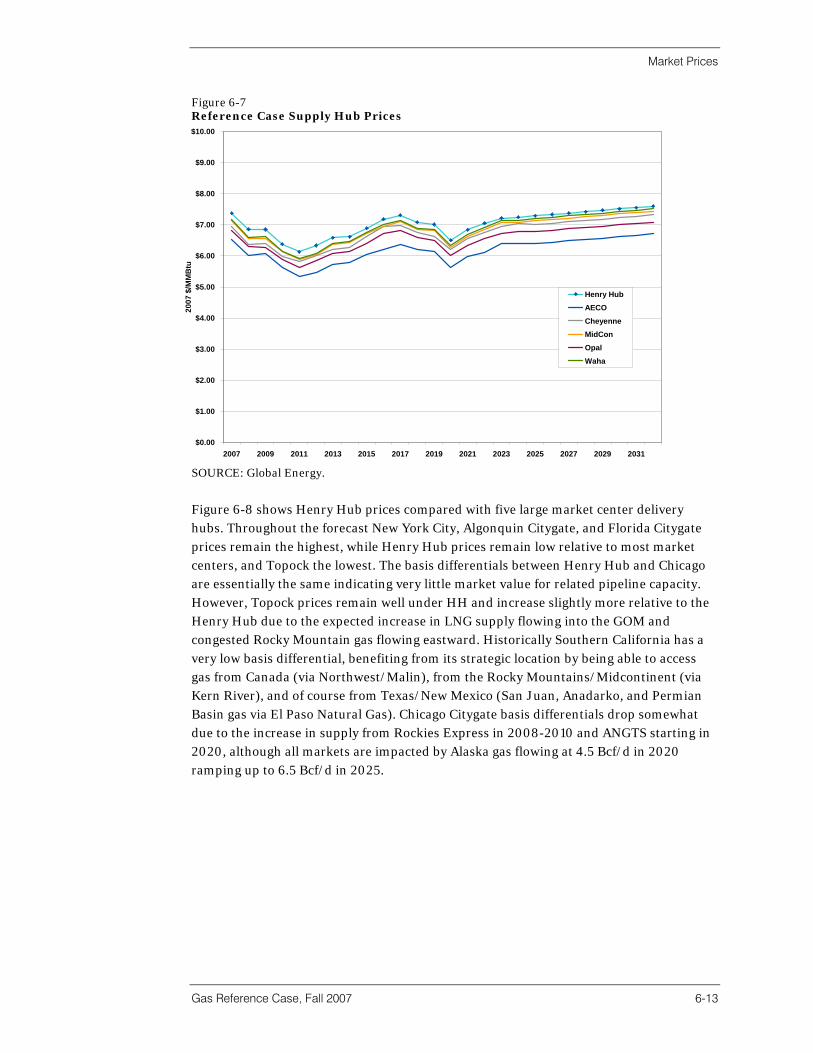

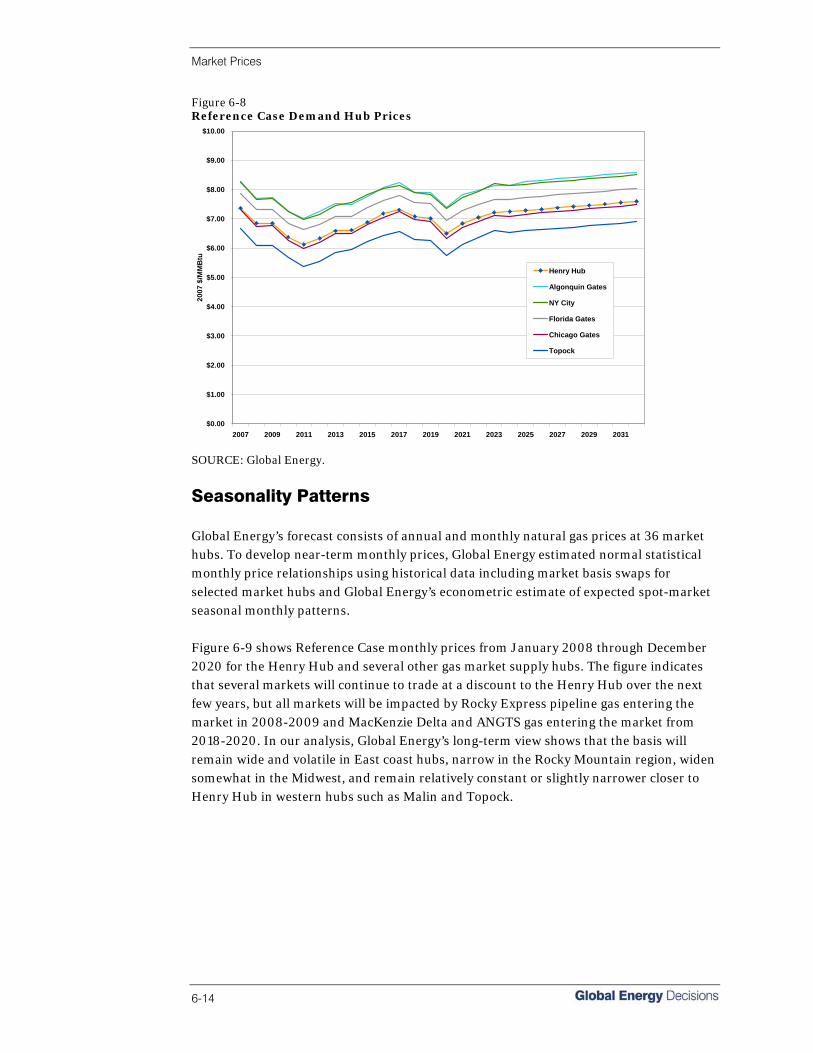

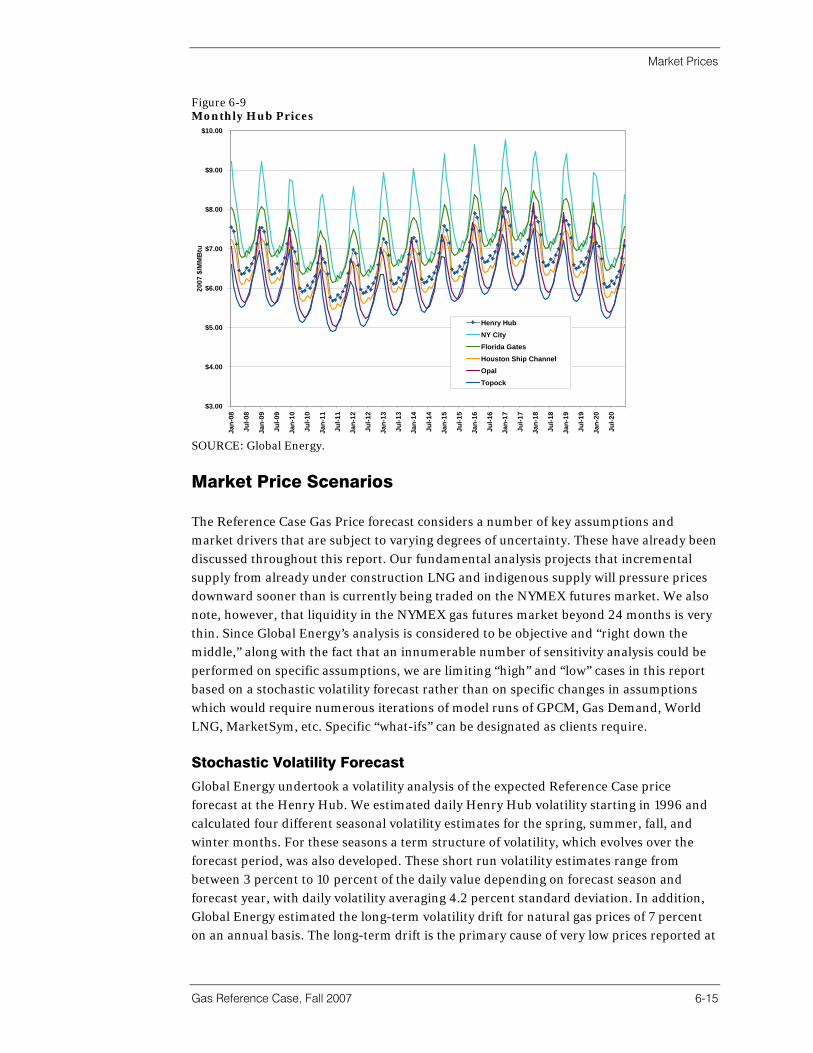

Key North American Market Prices ........................................................................6-12 Seasonality Patterns ...............................................................................................6-14 Market Price Scenarios...........................................................................................6-15

• Stochastic Volatility Forecast...........................................................................6-15

7 Methodology 7-1

Introduction...............................................................................................................7-1 Base Loaded Capacity .............................................................................................7-3 Data Sources ............................................................................................................7-4 Supply .......................................................................................................................7-5 Pipeline And Storage ................................................................................................7-5 Demand ....................................................................................................................7-5 GPCM™ Overview ....................................................................................................7-6

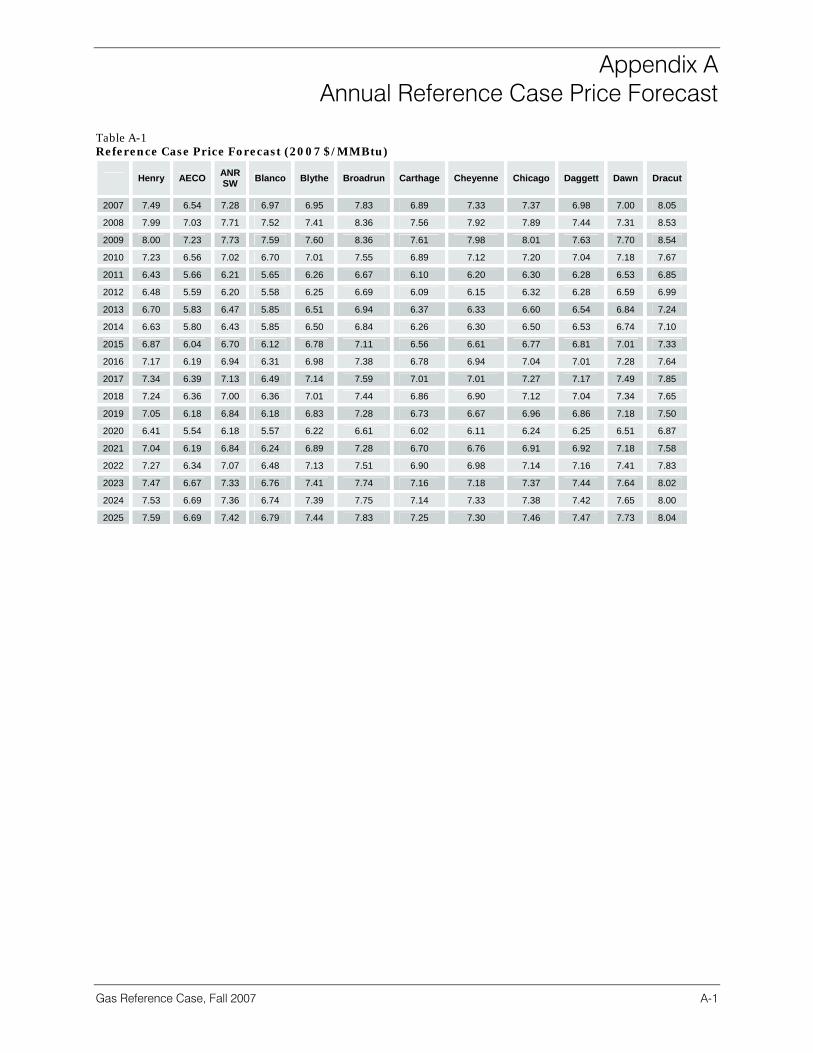

Appendix A Annual Reference Case Price Forecast

Appendix B Henry Hub Stochastic Price Forecast

Appendix C U.S. Supply And Disposition

Appendix D Demand Forecast (MMcf/d)

Appendix E Corridor Flow Forecast

Appendix F U.S. Dry Gas Production Forecast

Appendix G WTI Oil

Appendix H WTI Reference Case Price Forecast

Appendix I History And Evolution Of Natural Gas Deregulation

Appendix J Legislative Initiatives On Carbon Trading

Appendix K Herfindahl-Hirschman Index

List of Tables

Gas Reference Case, Fall 2007 v

2-1 U.S. Gas Demand; Bcf, 2000-2030..........................................................................2-6

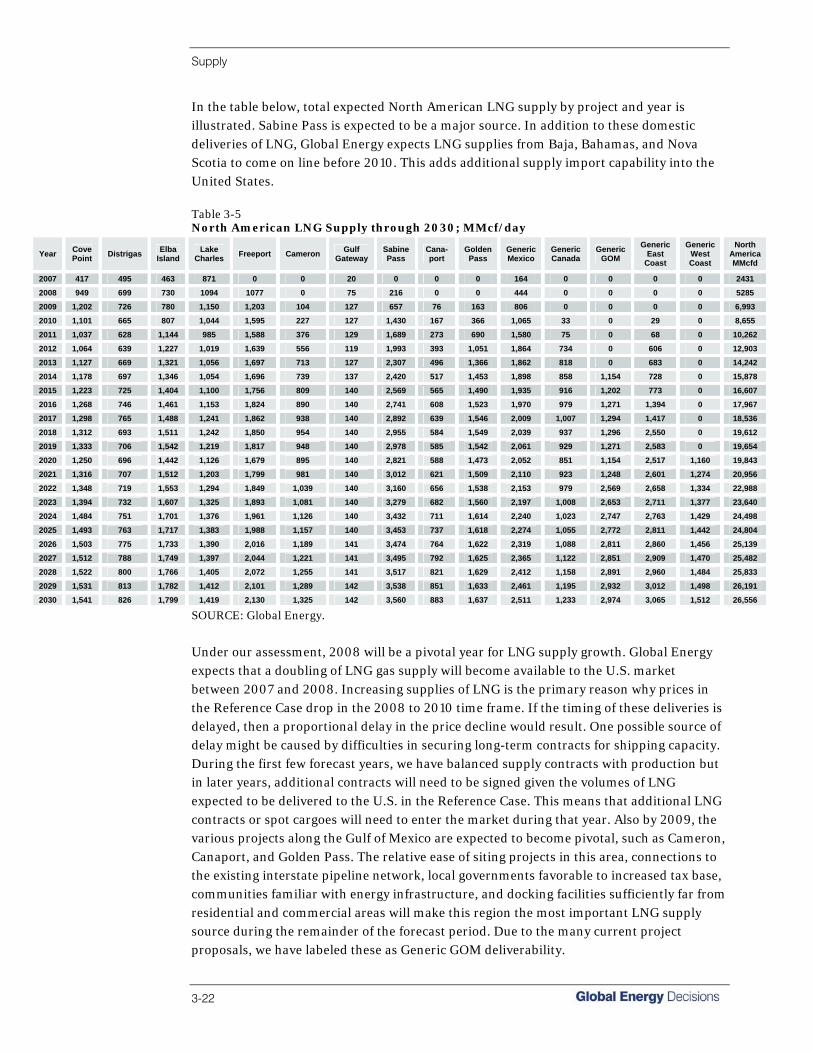

3-1 Domestic Gas Production (Tcf) ................................................................................3-3 3-2 Technically Recoverable Unconventional Gas Reserves ........................................3-4 3-3 U.S. Gas Supply Balance; Bcf, 2000-2030 ............................................................3-11 3-4 North American Gas Market Hubs .........................................................................3-19 3-5 North American LNG Supply through 2030; MMcf/day .........................................3-22

4-1 LNG Supply Chain Capital Cost (in $2007/Tonne LNG Capacity) ..........................4-7 4-2 Regasified LNG Supply Cost Range to the U.S. (in $2007/MMBtu)........................4-8 4-3 LNG Exporting Countries (2006) ..............................................................................4-9 4-4 LNG Importing Countries (2006) ............................................................................4-12 4-5 Approved North American Regasification Project Details .....................................4-18 4-6 Modeled Regasification Terminal Delivery through 2025 (Annual Average MMcf/d

and Utilization Rate)................................................................................................4-20 4-7 North American LNG Delivered Costs (In $2007) ..................................................4-25

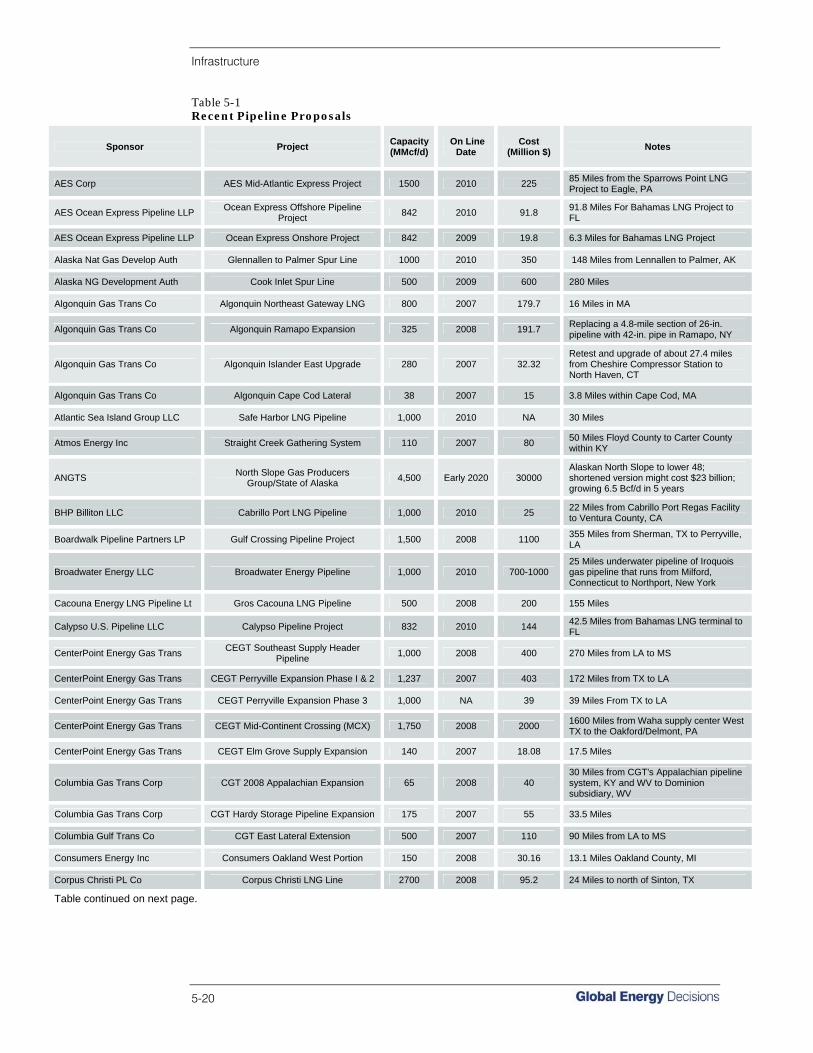

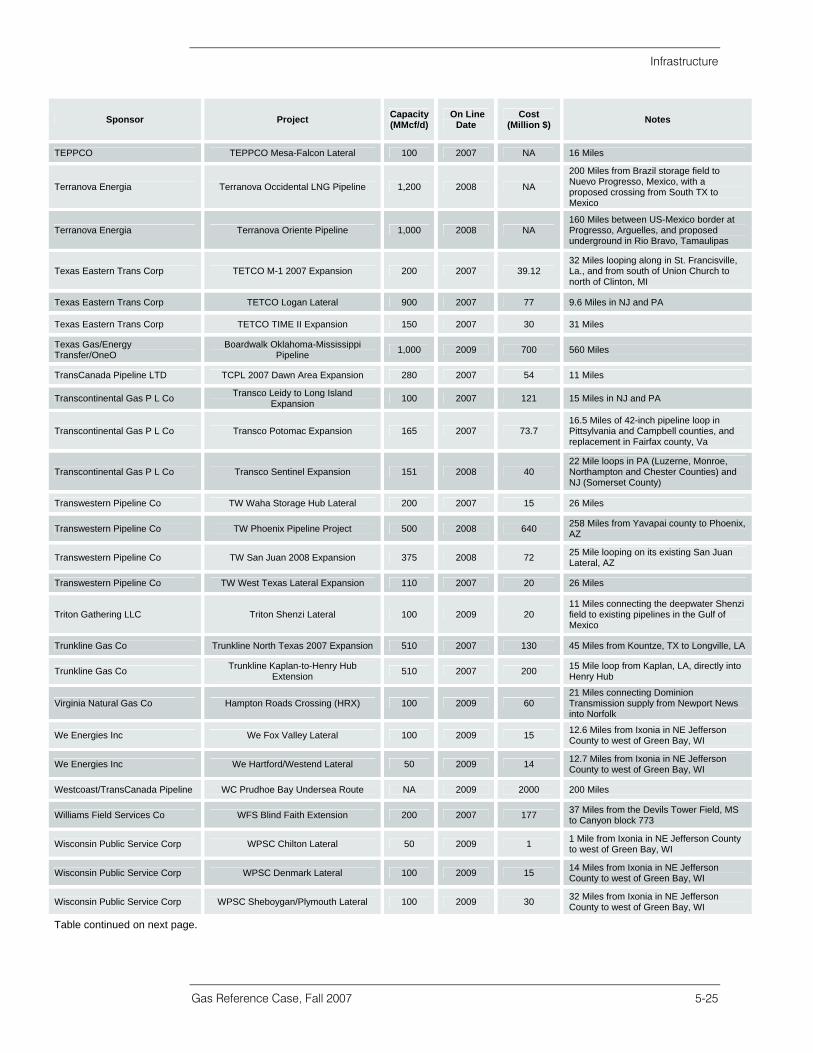

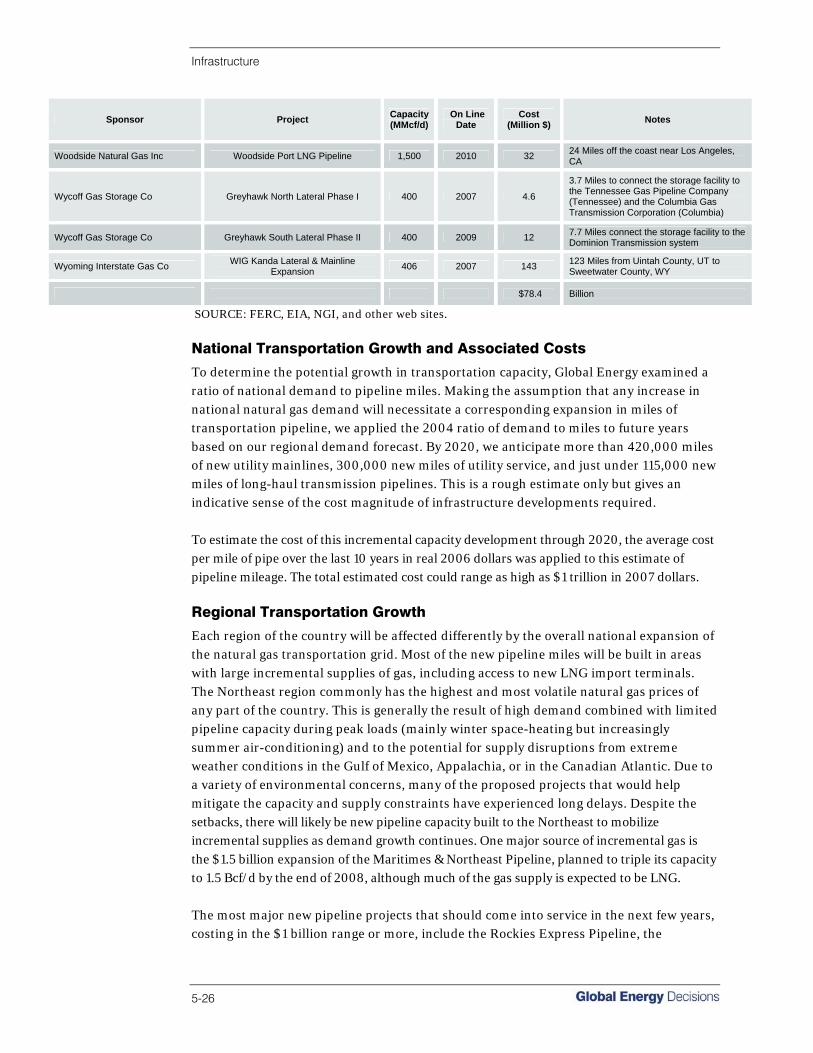

5-1 Recent Pipeline Proposals......................................................................................5-20 5-2 Recent Certificated Storage Projects .....................................................................5-30 5-3 Pending Storage Projects.......................................................................................5-32

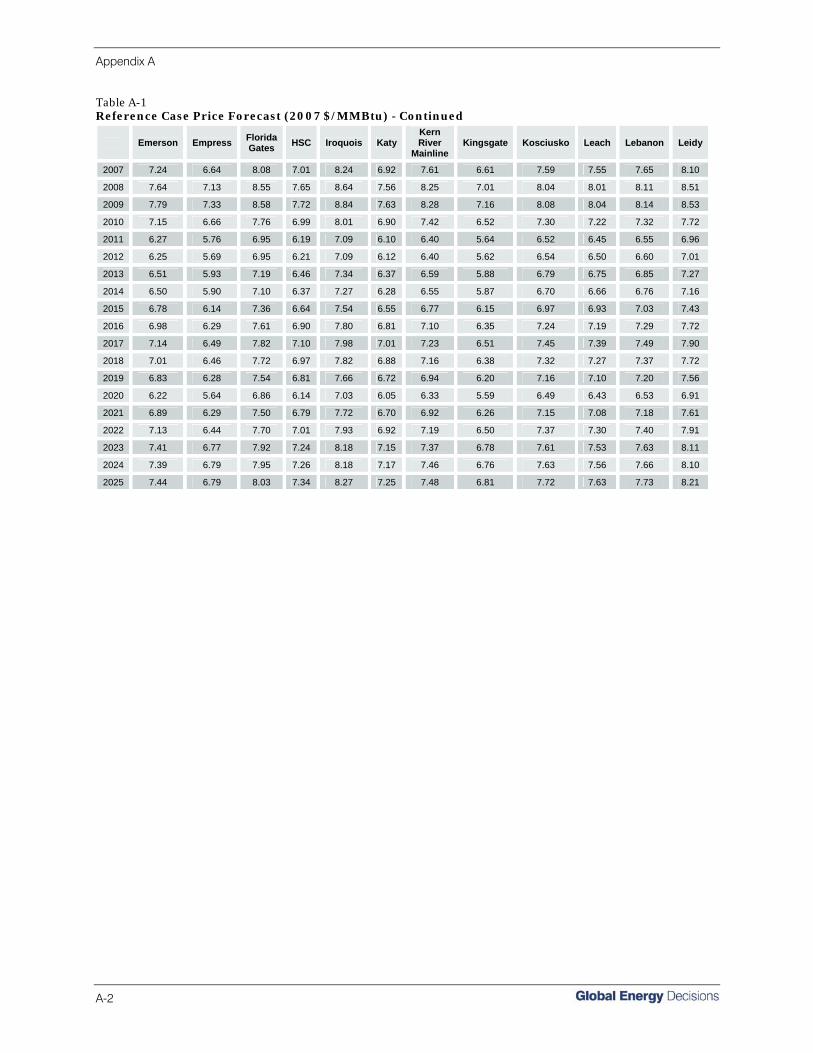

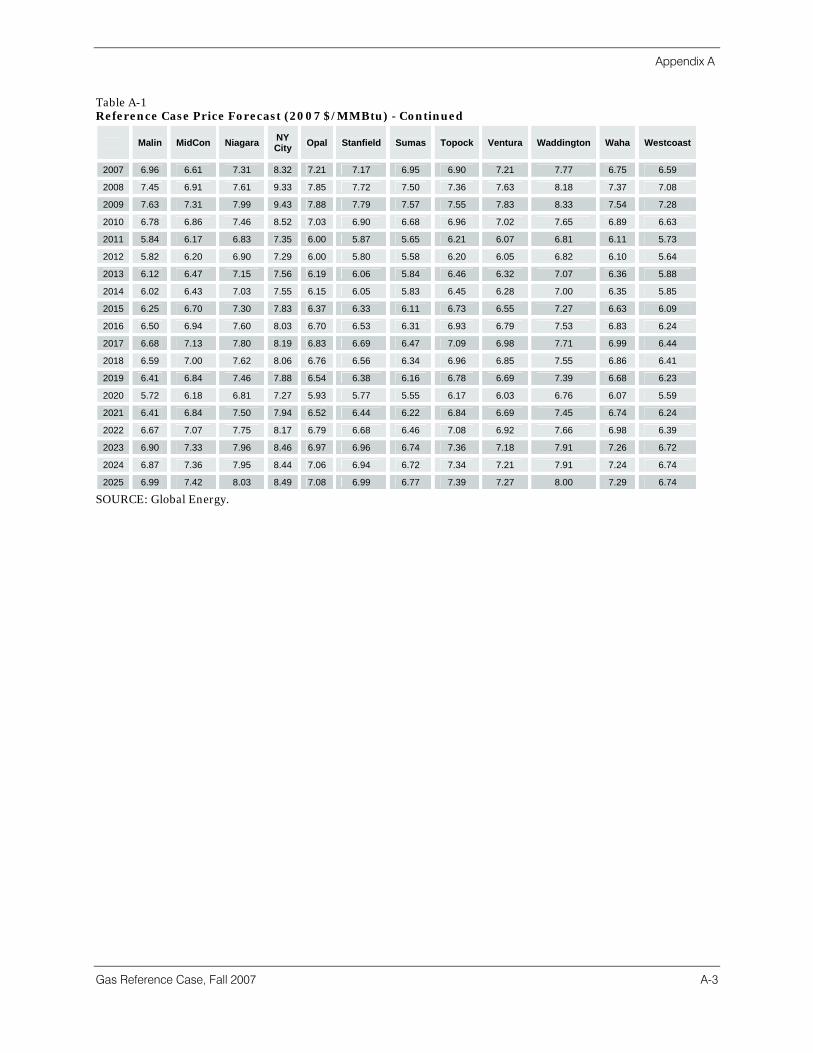

A-1 Reference Case Price Forecast (2007 $/MMBtu) ................................................... A-1

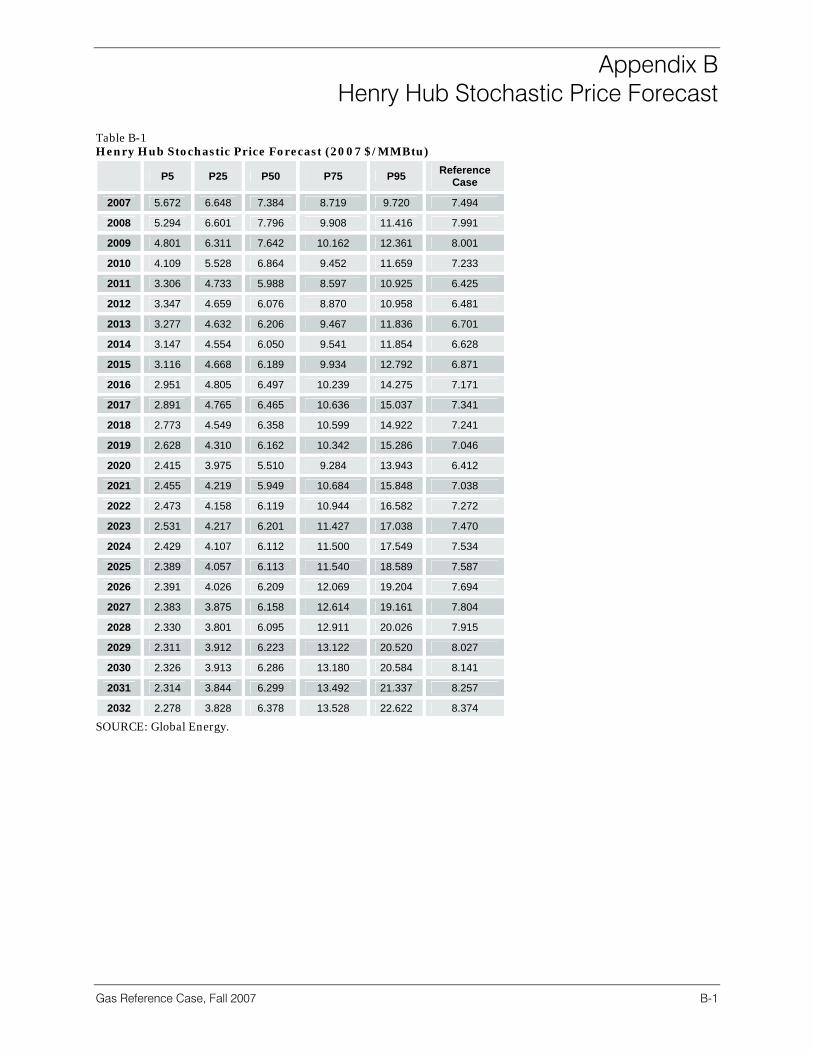

B-1 Henry Hub Stochastic Price Forecast (2007 $/MMBtu).......................................... B-1

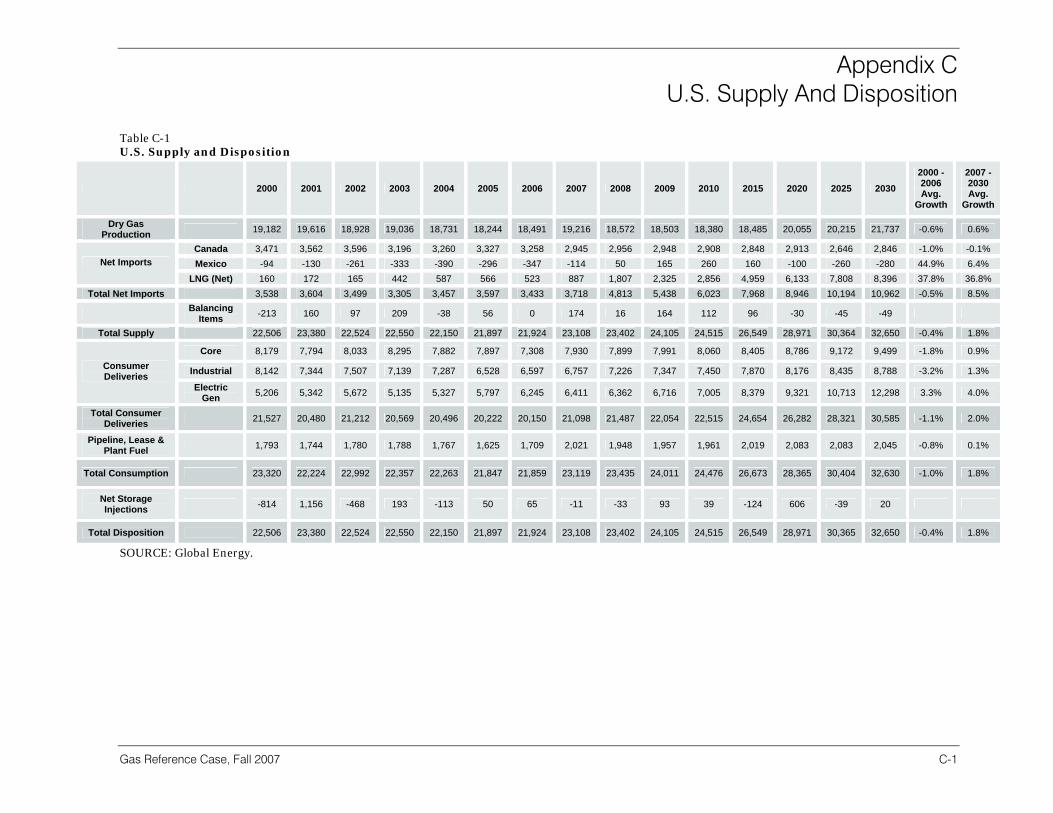

C-1 U.S. Supply and Disposition.................................................................................... C-1

D-1 Demand Forecast ................................................................................................... D-1

E-1 Corridor Flow Forecast (MMcf/d) 2007 ................................................................... E-1

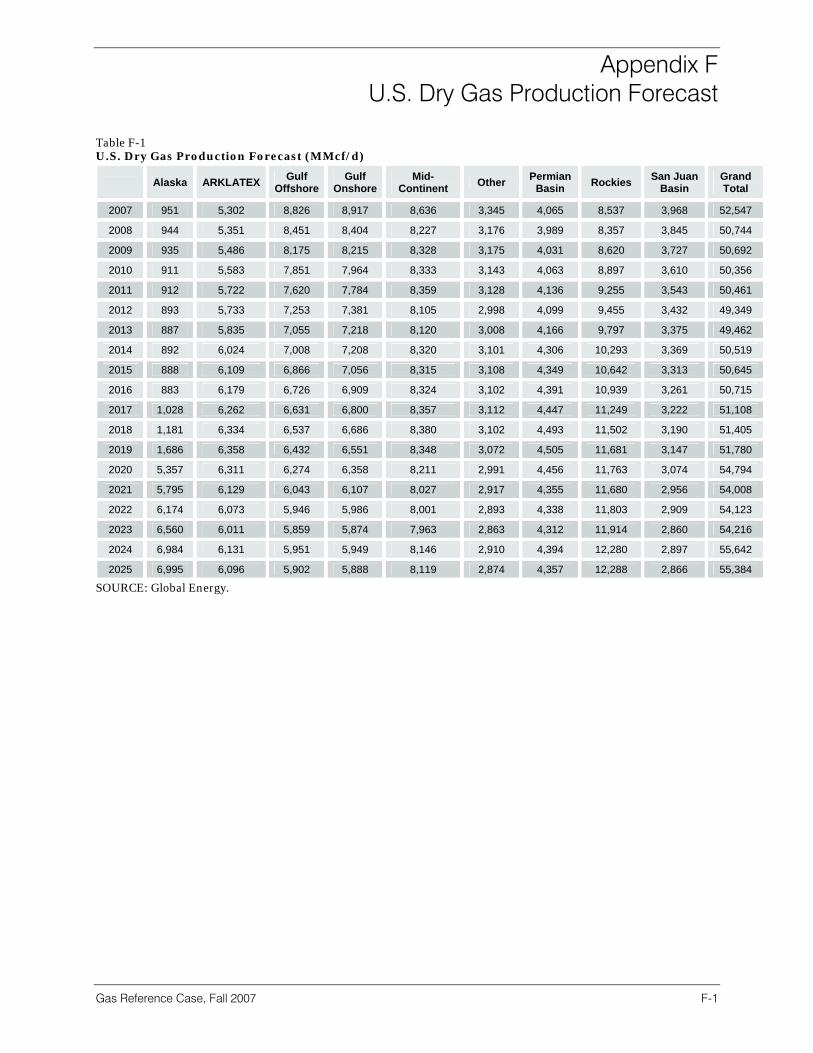

F-1 U.S. Dry Gas Production Forecast (MMcf/d) ...........................................................F-1

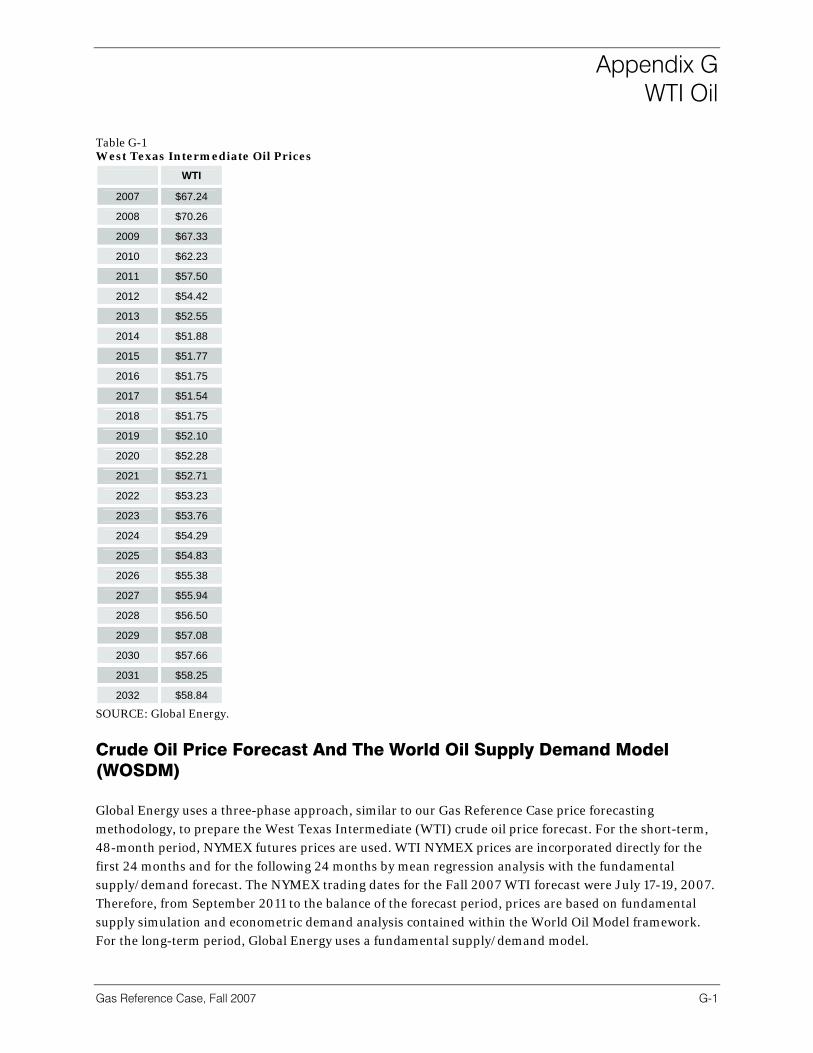

G-1 West Texas Intermediate Oil Prices.........................................................................G-1 G-2 Current OPEC Supply Quota...................................................................................G-2

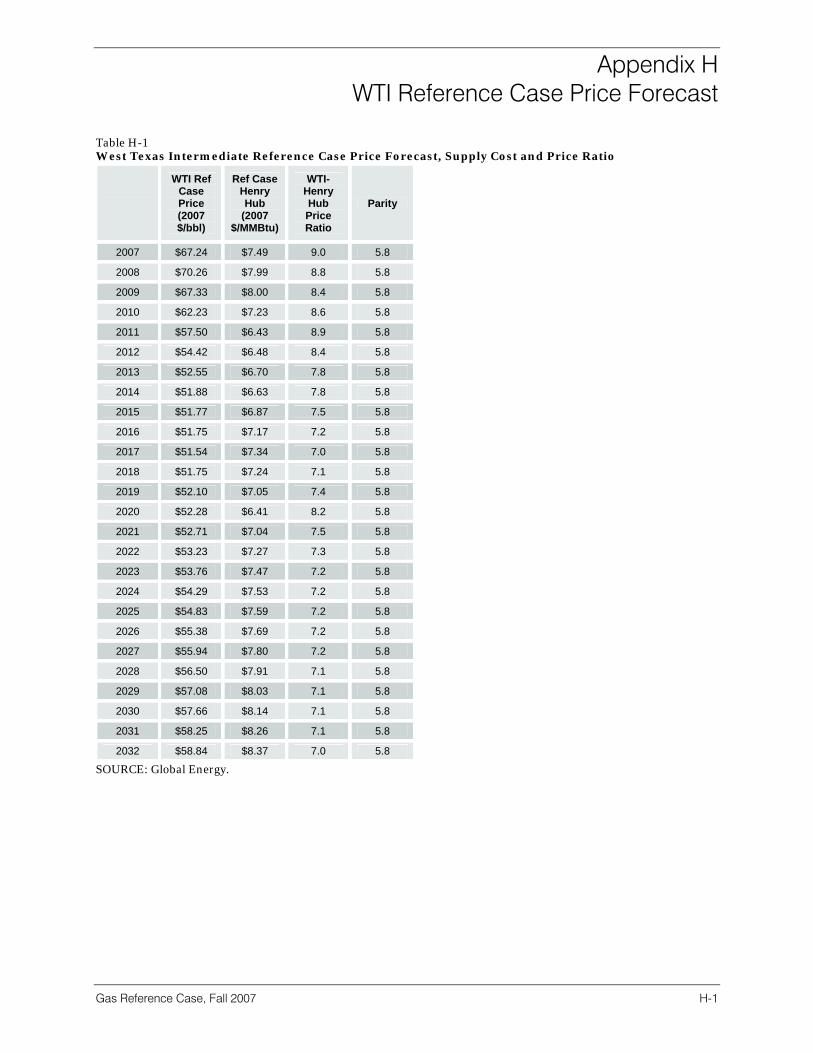

H-1 West Texas Intermediate Reference Case Price Forecast, Supply Cost and Price Ratio ........................................................................................................ H-1

vi

List of Figures

Gas Reference Case, Fall 2007 vii

ES-1 Gulf of Mexico Monthly Natural Gas Production and Wellhead Price .................. ES-1 ES-2 Monthly LNG Imports by Country, January 1997 through July 2007.................... ES-3 ES-3 Historical Henry Hub Gas Prices........................................................................... ES-4 ES-4 Generalized Equilibrium Solution Example ......................................................... ES-5 ES-5 Source of Gas Consumed in the United States.................................................... ES-6 ES-6 Worldwide LNG Demand by Continent; 2005-2030 ............................................. ES-7 ES-7 U.S. Gas Demand Forecast by Sector.................................................................. ES-8

ES-8 SO2 and NOx, Allowance Price with Increased Adder for 1 Percent Sulfur Residual Oil ................................................................................................. ES-9

1-1 Historical Henry Hub Gas Prices, Volatility and Trend Line; October 1993-May 2007...........................................................................................1-3 1-2 U.S. Natural Gas Consumption by End User...........................................................1-4 1-3 U.S. Industrial Gas Demand Destruction .................................................................1-5 1-4 Historical U.S. Net Gas Imports ...............................................................................1-6 1-5 Proposed LNG Regasification Capacity for North America.....................................1-6 1-6 Operating and Proposed Global LNG Liquefaction Capacity .................................1-7 1-7 Prominent Trading Losses in Various Commodities................................................1-8 1-8 U.S., Canadian and Mexican Natural Gas Reserves (1982-2006) ........................1-10 1-9 U.S. Power Plant Capacity by Installation Year......................................................1-11 1-10 Electric Generation Gas Fuel Demand Growth......................................................1-12 1-11 Historic Crude Oil and Natural Gas Price Ratios (Three-Month Rolling Averages)....................................................................................................1-13 1-12 Forecast of Crude Oil-to-Natural Gas Price Ratios (Annual) .................................1-14

2-1 U.S. Gas Demand Forecast by Sector.....................................................................2-2 2-2 Historic U.S. Gasoline and Motor Fuels Consumption............................................2-3 2-3 Projected U.S. Gasoline and Motor Fuels Consumption.........................................2-3 2-4 Projected U.S. Gas Demand in Ethanol Production ................................................2-4 2-5 U.S. Gas-Fired Generation Additions and Peak Gas Consumption .......................2-5 2-6 Monthly Gas Demand; 2001-2030 ...........................................................................2-7 2-7 Canadian Gas Demand Forecast by Sector............................................................2-8 2-8 Projected Canadian Gas Demand in Oil Sand Crude Production ..........................2-9 2-9 Outlook for Demand in the South Atlantic Census Division ..................................2-10 2-10 Outlook for Demand in the Middle Atlantic Census Division .................................2-12 2-11 Outlook for Demand in the New England Census Division ...................................2-13 2-12 Outlook for Demand in the East North Central Census Division ...........................2-15 2-13 Outlook for Demand in the West North Central Census Division ..........................2-16 2-14 Outlook for Demand in the East South Central Census Division...........................2-18 2-15 Outlook for Demand in the West South Central Census Division..........................2-19 2-16 Outlook for Demand in the Mountain Census Division..........................................2-21 2-17 Outlook for Demand in the Pacific Census Division ..............................................2-22

List of Figures

viii

3-1 Correlation of Working Rigs to Gas Prices...............................................................3-1 3-2 U.S. Gulf of Mexico Gas Production and Working Gas Rigs...................................3-2 3-3 Location of Unconventional Gas Reserves in the United States .............................3-4 3-4 Unconventional Gas Production: Volume and Share of Domestic Production.................................................................................................................3-6 3-5 Representative Gas Supply Cost Curve...................................................................3-8 3-6 Changing Source of U.S. Gas Supply....................................................................3-12 3-7 U.S. Production Forecast and Trends....................................................................3-13 3-8 Long-Term Decline in U.S. Gulf of Mexico Gas Production ..................................3-14 3-9 U.S. Gulf of Mexico Working Rigs ..........................................................................3-15 3-10 U.S. Gulf of Mexico Gas Production by Depth; Percentage of Gas Production >200 m ........................................................................................3-16 3-11 U.S. Coal Bed Methane Production; As Percentage of Gulf of Mexico Production ......................................................................................3-16 3-12 U.S. Annual Storage Activity for Year 2006 through September 1, 2007 ..............3-17 3-13 North American LNG Imports .................................................................................3-21

4-1 U.S. Supply Allocation in 2006 .................................................................................4-1 4-2 Proven Natural Gas Reserves by Continent.............................................................4-3 4-3 Proven Natural Gas Reserves by Country; Percentage...........................................4-4 4-4 Proven Natural Gas Reserves by Top Countries; Tcf ..............................................4-5 4-5 Gas Reserves/Production Ratio ...............................................................................4-5 4-6 LNG Importing Countries; 1990-2006 ....................................................................4-10 4-7 Global Liquefaction Capacity (Million Tonnes/Year) ..............................................4-11 4-8 Worldwide LNG Demand Range; 2005-2030 ........................................................4-13 4-9 Worldwide LNG Demand by Continent; 2005-2030 ..............................................4-14 4-10 Global LNG Fleet through 2012 .............................................................................4-15 4-11 Existing, Under Construction and Proposed Regasification Capacity ..................4-17 4-12 Cumulative Existing, Under Construction and Proposed

Regasification Capacity..........................................................................................4-17 4-13 Cumulative Exisiting, Under Construction and Permitted

Regasification Capacity..........................................................................................4-18 4-14 North American Regasification Capacity, Production and

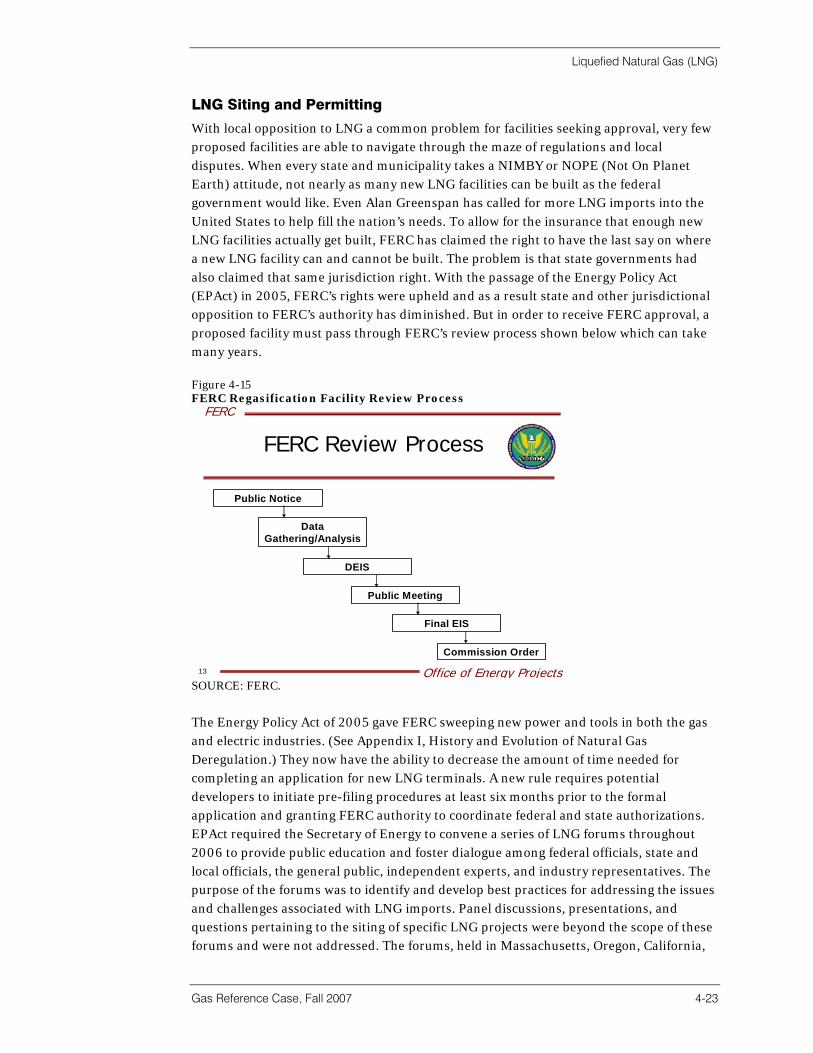

Utilization Percentage.............................................................................................4-21 4-15 FERC Regasification Facility Review Process........................................................4-23

5-1 Major Consumer Share (MMcf/d and Percent of Total)...........................................5-2 5-2 Demand Seasonality; 2001 (MMcf/d).......................................................................5-4 5-3 Demand Seasonality; 2030 (MMcf/d).......................................................................5-4 5-4 U.S. Census Regions and Divisions.........................................................................5-5 5-5 Major Consumer Share.............................................................................................5-6 5-6 East North Central Gas Corridor Flows MMcf/d ....................................................5-14 5-7 East South Central Gas Corridor Flows MMcf/d....................................................5-15 5-8 Middle Atlantic Gas Corridor Flows MMcf/d ..........................................................5-15

List of Figures

Gas Reference Case, Fall 2007 ix

5-9 Mountain Gas Corridor Flows MMcf/d ...................................................................5-16 5-10 New England Gas Corridor Flows MMcf/d ............................................................5-16 5-11 Pacific Gas Corridor Flows MMcf/d .......................................................................5-17 5-12 South Atlantic Gas Corridor Flows MMcf/d............................................................5-17 5-13 West North Central Gas Corridor Flows MMcf/d ...................................................5-18 5-14 West South Central Gas Corridor Flows MMcf/d...................................................5-18 5-15 Natural Gas Infrastructure in North America ..........................................................5-19 5-16 U.S. Underground Storage Capacity by Type of Reservoir ...................................5-28 5-17 Regional Working Natural Gas Storage Activity; December 1993 to Present .......5-30

6-1 Henry Hub Market Prices..........................................................................................6-1 6-2 Historical Natural Gas Price Volatility and Trend Line,

October 1993-May 2007...........................................................................................6-2 6-3 Net Annual Canadian and Mexican Imports ............................................................6-3 6-4 Historical Henry Hub and Forecast Reference Case Prices....................................6-5 6-5 Gulf of Mexico (GOM) Working Gas Rigs and Wellhead Price (Monthly Averages)...................................................................................................6-7 6-6 U.S. Gas Supply Breakdown..................................................................................6-11 6-7 Reference Case Supply Hub Prices.......................................................................6-13 6-8 Reference Case Demand Hub Prices ....................................................................6-14 6-9 Monthly Hub Prices.................................................................................................6-15 6-10 Confidence Interval for Henry Hub Market Prices (Annual) ...................................6-16 6-11 Confidence Interval for Henry Hub Market Prices (Monthly)..................................6-17

7-1 Generalized Equilibrium Solution Example ..............................................................7-1 7-2 Modeling Framework Inputs and Outputs ...............................................................7-4

7-3 Market Crossing Point ..............................................................................................7-7

G-1 Relationship between Excess Productive Capacity and Market Price ...................G-3 G-2 OPEC Production; 1st Quarter 2006 through 2nd Quarter 2007...............................G-4 G-3 World Oil Demand by Major Region; 1966-2006 ....................................................G-4 G-4 World Oil Production by Major Region; 1966-2006 ................................................G-5 G-5 Oil Production/Demand (P/D) Ratio by Region; 1996-2006 ...................................G-5 G-6 Oil Reserves/Production (R/P) Ratio by Region; 1986-2006 ..................................G-6 G-7 Reference Case Oil to Gas Price Ratio ...................................................................G-6 G-8 Confidence Interval for WTI Crude Oil Price Forecast ............................................G-7

J-1 Existing Non-Attainment Areas and Regional Cap-and-Trade Programs for NOX: .................................................................................................... J-2

J-2 Clean Air Interstate Rule (CAIR) Geographical Scope and Reduction Targets ...... J-2 J-3 States/Provinces with CO2 Initiatives in Process ..................................................... J-5

J-4 Coal Generation as a Percentage of Total Regional Generation ............................ J-6 J-5 Representative Environmental Adders to Electric Dispatch Cost (Under Specific Pricing Assumptions for NOx, SO2, and CO2) .......................... J-10

Section 1 | Introduction And Current Market Overview

Introduction And Current Market Overview

Gas Reference Case, Fall 2007 1-1

Report Objectives Global Energy’s Natural Gas Reference Case provides a comprehensive review of important natural gas market drivers and a forecast of projected gas market conditions. As of 2007, the natural gas market has entered its seventh year of unprecedented high prices, along with wide price swings. The last few years have caused many industry observers to rethink their conventional wisdom about current and future natural gas markets. Global Energy’s own analysis is no different in this regard. Others have assumed that futures prices are the best that one can do in forming market opinion and have therefore largely abandoned some aspects of fundamental research. Global Energy believes this is a risky approach to take for several reasons—not the least of which is the lack of trading liquidity beyond 18 months in the NYMEX natural gas futures market. This report’s objective is to provide an expected case analysis of current and future natural gas market conditions and drivers. Global Energy’s “down the middle” independent analysis is highly regarded in the industry and can serve as a solid base for alternative forecasts using alternative assumptions. To prepare the forecasts, Global Energy undertook a fundamental analysis of gas market supply and demand and price scenarios of the future. For this task we combine an integrated approach to energy modeling that considers competitive fuel economics, continental electric power, and coal markets along with RBAC’s GPCM natural gas market modeling platform.1 The forecasts presented for market prices for all cases are prepared to 2032. However, due to the inherent high degree of uncertainty in gas supply and demand and the current model configuration, including computer run time for LP optimization, we report the quantitative supply and demand values to 2027 only. Beyond 2027, Global Energy chose to produce an extrapolated forecast. Gas (and oil) market forecasting tends to be inherently more uncertain than other energy commodities such as power price forecasting, due to its inherent uncertainty about reserves and supply costs. In fact, most petroleum supply models are based on extrapolated statistical reserve pool plays based on highly incomplete information. In addition, the ultimate extraction cost and the role technology plays in reducing those costs are highly uncertain. No one knows with a high degree of accuracy exactly how much extractable gas resources will be available in the future and at what cost. Furthermore, the history of the petroleum extraction is punctuated with periods of intense technological innovation where new methodologies and processes have revolutionized finding, developing, and extraction methods. Some of these include 3 and 4D-seismic and micro-seismology, which have greatly improved seismic imaging and reduced dry holes; logging while drilling, which has improved operator target accuracy;

1 GPCM originally stood for Gas Pipeline Competition Model, but has been expanded to account for the entire natural gas industry.

Introduction And Current Market Overview

1-2

horizontal drilling used to produce petroleum where economic recovery was not possible with conventional methods; coil tube drill pipe, which reduces the cost to drill certain formations; deep offshore drilling and production platforms, which have extended the range of drillers and increased the area of “land” available for exploration; and finally, greatly improved computer imaging and seismic processes which enable geologists and geophysicists to better understand pools. But technological innovation tends to be lumpy in its introduction and difficult to accurately predict more than a few years forward. The introduction and innovation of each of the aforementioned technologies has greatly contributed to improving the success rate of drillers, increased the deliverability of pools, optimized the total reserves to be produced, and reduced the finding and developing costs per Mcf of natural gas. Until recently, the combination of these innovations has kept pace with the naturally decreasing gas reserve quality in many North American gas basins. At the same time, rapid expansion of the upstream industry along with rising materials costs, have created a bonanza for drillers, seismic crews, and land bonus sales, raising day rates and costs for all. The current manic pace has greatly inflated industry finding and developing costs, at least temporarily. Given all the uncertainties combined with demand uncertainty, Global Energy has also chosen to produce a stochastic volatility forecast based on Reference Case price results, historical volatility, and correlation with other market drivers. These results are presented in Section 6.

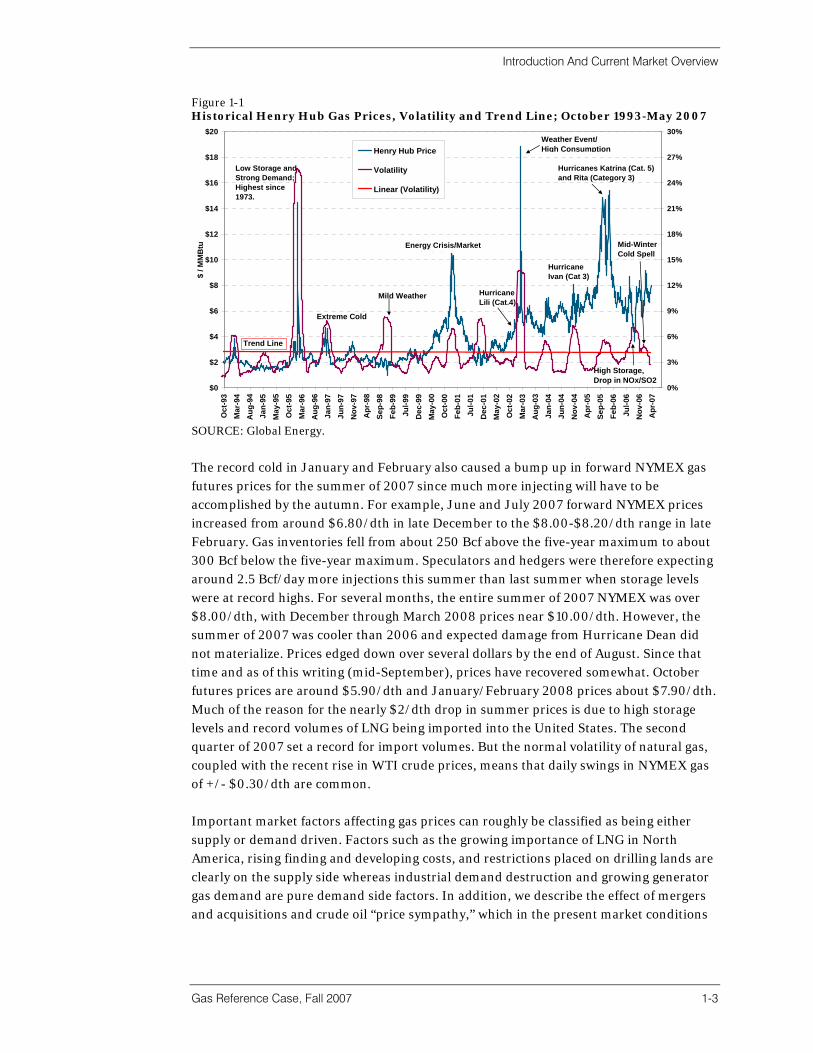

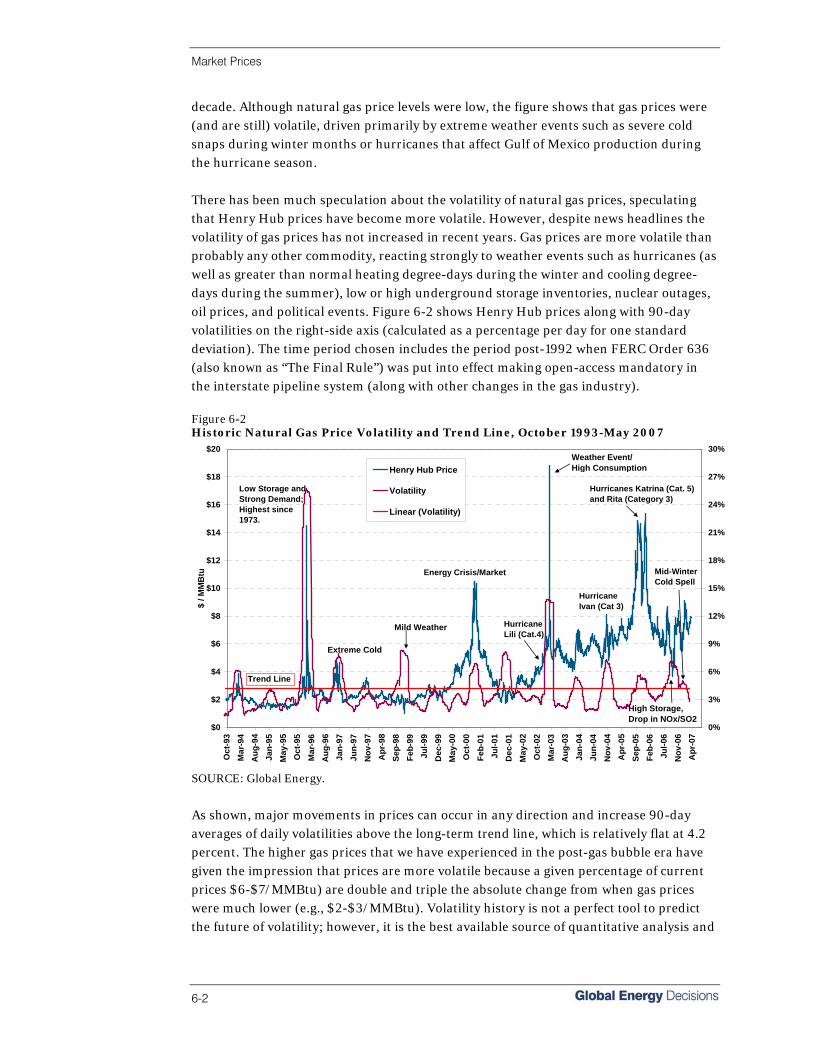

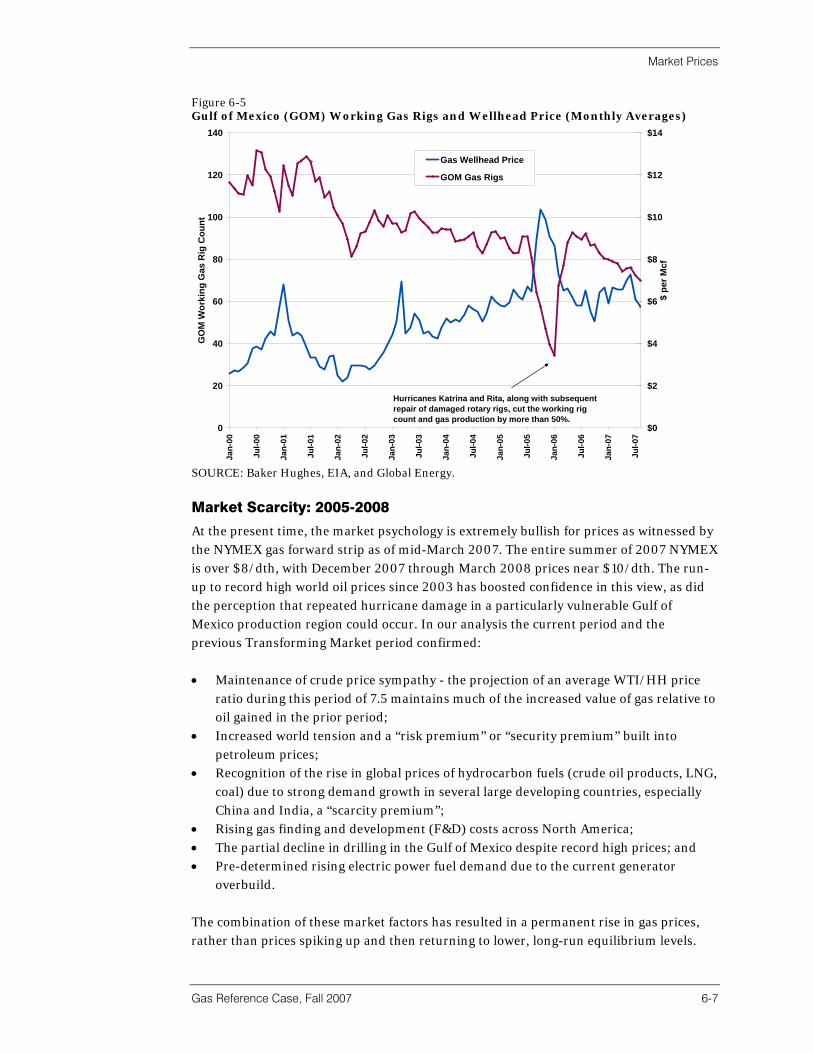

Market Overview Since Order 636 in 1993, which opened up the interstate gas price network and eliminated the merchant role enjoyed by pipeline companies, gas prices have, for the most part, remained in the $2.00 to $3.00/MMBtu range until late 2000. Figure 1-1 starts in January 1993, about half way through the infamous “gas bubble” years and includes the period post-1992 when FERC Order 636 (also known as “The Final Rule”) was put into effect making open-access mandatory in the interstate pipeline system (along with other changes in the gas industry). Henry Hub prices are shown along with 90-day rolling averages of daily volatilities on the right-side axis (calculated as a percentage per day for one standard deviation). It illustrates the historical record (including wild swings) of gas prices traded at the Henry Hub in Louisiana, North America’s main natural gas trading hub and delivery point of the NYMEX futures market. The figure shows that market prices have always been volatile, driven primarily by unexpected weather events, such as extreme cold (or warm) winters and Hurricanes Katrina and Rita in 2005. Also, there are more recent events like the price drop in 2006 due to high storage inventories and high emissions allowance prices, the mid-winter 2007 cold spell pushing Henry Hub prices into the $8-$10/MMBtu range, and the late-summer 2007 price collapse following many months of record LNG imports and high storage inventories.

Introduction And Current Market Overview

Gas Reference Case, Fall 2007 1-3

Figure 1-1 Historical Henry Hub Gas Prices, Volatility and Trend Line; October 1993-May 2007

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

Oct

-93

Mar

-94

Aug

-94

Jan-

95M

ay-9

5O

ct-9

5M

ar-9

6A

ug-9

6Ja

n-97

Jun-

97N

ov-9

7A

pr-9

8Se

p-98

Feb-

99Ju

l-99

Dec

-99

May

-00

Oct

-00

Feb-

01Ju

l-01

Dec

-01

May

-02

Oct

-02

Mar

-03

Aug

-03

Jan-

04Ju

n-04

Nov

-04

Apr

-05

Sep-

05Fe

b-06

Jul-0

6N

ov-0

6A

pr-0

7

$ / M

MB

tu

0%

3%

6%

9%

12%

15%

18%

21%

24%

27%

30%

Henry Hub Price

Volatility

Linear (Volatility)

Trend Line

Weather Event/High Consumption

Energy Crisis/Market M i l i

Mild Weather

Hurricanes Katrina (Cat. 5) and Rita (Category 3)

Mid-WinterCold Spell

Hurricane Lili (Cat.4)

Hurricane Ivan (Cat 3)

Extreme Cold

Low Storage and Strong Demand;Highest since 1973.

High Storage,Drop in NOx/SO2

SOURCE: Global Energy.

The record cold in January and February also caused a bump up in forward NYMEX gas futures prices for the summer of 2007 since much more injecting will have to be accomplished by the autumn. For example, June and July 2007 forward NYMEX prices increased from around $6.80/dth in late December to the $8.00-$8.20/dth range in late February. Gas inventories fell from about 250 Bcf above the five-year maximum to about 300 Bcf below the five-year maximum. Speculators and hedgers were therefore expecting around 2.5 Bcf/day more injections this summer than last summer when storage levels were at record highs. For several months, the entire summer of 2007 NYMEX was over $8.00/dth, with December through March 2008 prices near $10.00/dth. However, the summer of 2007 was cooler than 2006 and expected damage from Hurricane Dean did not materialize. Prices edged down over several dollars by the end of August. Since that time and as of this writing (mid-September), prices have recovered somewhat. October futures prices are around $5.90/dth and January/February 2008 prices about $7.90/dth. Much of the reason for the nearly $2/dth drop in summer prices is due to high storage levels and record volumes of LNG being imported into the United States. The second quarter of 2007 set a record for import volumes. But the normal volatility of natural gas, coupled with the recent rise in WTI crude prices, means that daily swings in NYMEX gas of +/- $0.30/dth are common. Important market factors affecting gas prices can roughly be classified as being either supply or demand driven. Factors such as the growing importance of LNG in North America, rising finding and developing costs, and restrictions placed on drilling lands are clearly on the supply side whereas industrial demand destruction and growing generator gas demand are pure demand side factors. In addition, we describe the effect of mergers and acquisitions and crude oil “price sympathy,” which in the present market conditions

Introduction And Current Market Overview

1-4

where a risk premium of as much as $10-25/ barrel is “built into the price” has permitted natural gas to trade at higher prices. In the following sections Global Energy discusses several pivotal market factors that drive the natural gas market throughout the forecast horizon.

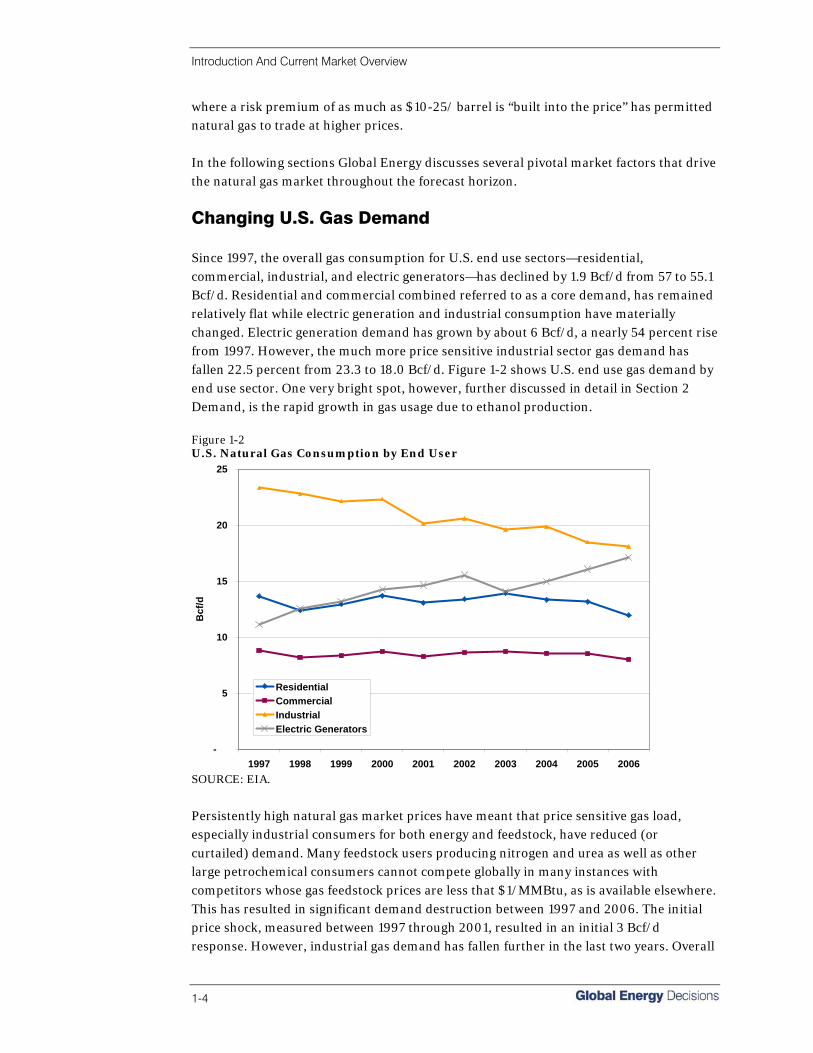

Changing U.S. Gas Demand Since 1997, the overall gas consumption for U.S. end use sectors—residential, commercial, industrial, and electric generators—has declined by 1.9 Bcf/d from 57 to 55.1 Bcf/d. Residential and commercial combined referred to as a core demand, has remained relatively flat while electric generation and industrial consumption have materially changed. Electric generation demand has grown by about 6 Bcf/d, a nearly 54 percent rise from 1997. However, the much more price sensitive industrial sector gas demand has fallen 22.5 percent from 23.3 to 18.0 Bcf/d. Figure 1-2 shows U.S. end use gas demand by end use sector. One very bright spot, however, further discussed in detail in Section 2 Demand, is the rapid growth in gas usage due to ethanol production. Figure 1-2 U.S. Natural Gas Consumption by End User

-

5

10

15

20

25

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Bcf

/d

ResidentialCommercialIndustrialElectric Generators

SOURCE: EIA.

Persistently high natural gas market prices have meant that price sensitive gas load, especially industrial consumers for both energy and feedstock, have reduced (or curtailed) demand. Many feedstock users producing nitrogen and urea as well as other large petrochemical consumers cannot compete globally in many instances with competitors whose gas feedstock prices are less that $1/MMBtu, as is available elsewhere. This has resulted in significant demand destruction between 1997 and 2006. The initial price shock, measured between 1997 through 2001, resulted in an initial 3 Bcf/d response. However, industrial gas demand has fallen further in the last two years. Overall

Introduction And Current Market Overview

Gas Reference Case, Fall 2007 1-5

industrial demand destruction now approaches 5.25 Bcf/d as hedges unwind and belief in the permanence of higher prices works its way through industrial users and industries move overseas. Figure 1-3 shows historical U.S. industrial gas demand destruction. Figure 1-3 U.S. Industrial Gas Demand Destruction

16

17

18

19

20

21

22

23

24

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Bcf

/d

Over 5 Bcf/d reduction

in industrialdemand

SOURCE: Global Energy and EIA.

The Changing Role Of LNG In North America Traditionally, North American gas markets have been described as a continental gas marketplace. Extensive north-south trade between Canada and the United States—as well as growing trade between Mexico and the United States—highlights this. In particular, during the 1990s, growth in U.S. imports from Canada grew substantially. Indigenous gas production from several supply basins dominates U.S. domestic trade. This level of integration has resulted in very little need for global LNG imports—until recently. Figure 1-4 shows this trend has stalled and expected to decline with LNG making up much of the shortfall in supply in recent years. Since 1995, U.S. marine LNG imports have grown from 18 Bcf to reach their all time high of 652 Bcf in 2004. However, in 2005, LNG imports declined by 93 Bcf due in part to higher natural gas prices in Europe relative to the United States. This caused some redirection of LNG cargos originally intended for the United States. Finally, net pipeline imports increased slightly over 2004. The contribution from LNG shown in the figure was provided by four LNG onshore and one offshore regasification terminals operating at about one-third of their design rating capacity. Even the higher gas prices of 2006 only caused LNG imports to recover to 623 Bcf.

Introduction And Current Market Overview

1-6

Figure 1-4 Historic U.S. Net Gas Imports

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005

Bcf

/Yea

rNet LNG Imports

Net Pipeline Imports

SOURCE: Global Energy.

In light of today’s relatively high gas prices, many new LNG terminals have been proposed for the United States, Canada, and Mexico. Project developers, some of whom are integrated producers with stranded gas, see increased LNG trade serving their own corporate interests as well as their nation’s desire for an economic, clean, and uninterrupted supply of energy. Presently, there is a development boom for LNG projects as developers vie for the first mover advantage in an attempt to monetize their stranded gas reserves worldwide. Figure 1-5 shows the announced level of LNG regasification capacity in bcf/d for North America by on line year. Figure 1-5 Proposed LNG Regasification Capacity for North America

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2007 2008 2009 2010 2011

mm

cf/d

ProposedApprovedConstructionOperational

SOURCE: Global Energy.

Introduction And Current Market Overview

Gas Reference Case, Fall 2007 1-7

Although this level of building could not possibly materialize as proposed by the project sponsors due to environmental, construction, NIMBY, harbor, and other factors, the availability of liquefaction capacity over the next several years will likely represent the most critical constraint affecting LNG developer plans—at least prior to 2010. Even if most of these regasification projects were to proceed as planned, limits on LNG supply would act to constrain the volumes of natural gas delivered from these terminals. We believe that in order to obtain financing, most projects (but not all, as the recently completed Energy Bridge project has shown) will need to secure long-term LNG supply contracts for at least some of their capacity. Figure 1-6 shows current and projected future global liquefaction capacity through 2010 by on line year. Given the very long lead times and the high capital costs of building these facilities, we believe it is unlikely that significantly higher amounts of capacity can be completed during this time frame. In our opinion, this will either severely limit North American (and global) regasification building or constrain the capacity factors on existing and future LNG regasification facilities. We discuss these developments further in Section 4. Figure 1-6 Operating and Proposed Global LNG Liquefaction Capacity

0

50

100

150

200

250

300

350

400

450

2007 2008 2009 2010 2011 2012 2013 2014 2015

Mill

ion

Tonn

es p

er Y

ear

PlanningEngineeringConstructionExisting

SOURCE: Global Energy.

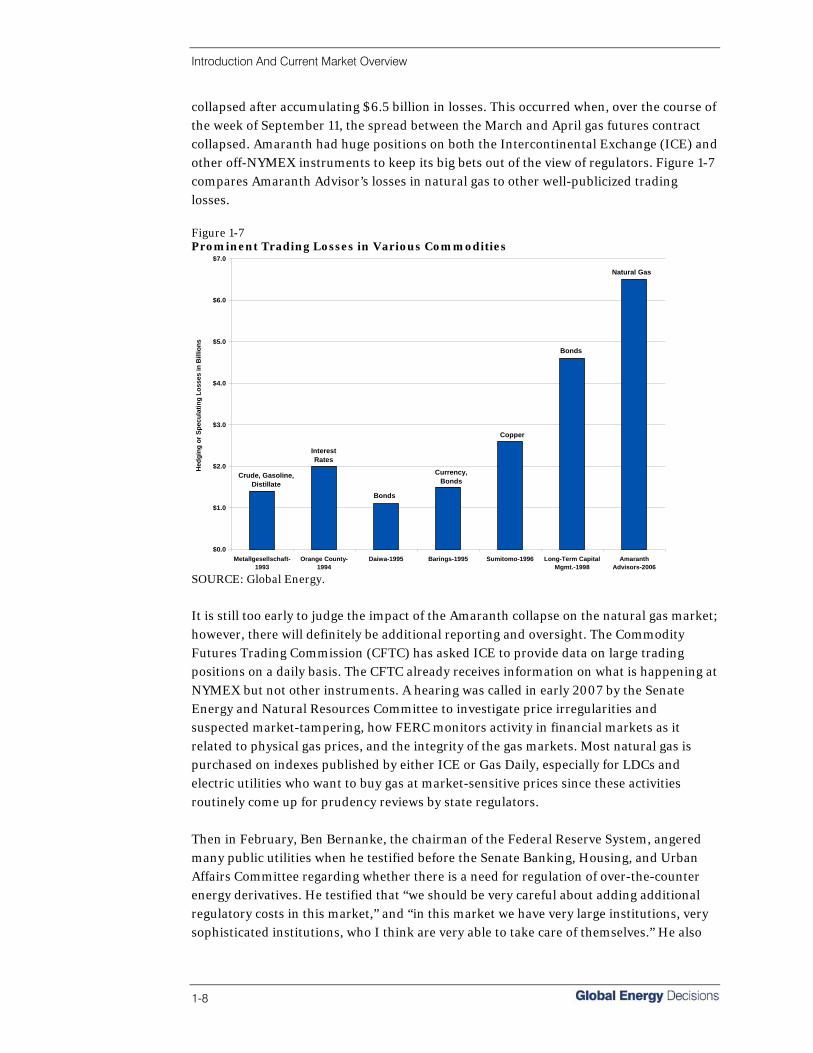

Greater FERC And CFTC Oversight Of Gas Markets In 2005 the Energy Policy Act was passed, the first substantial piece of energy legislation since 1992. The policy addresses a wide range of energy production, transportation, and regulatory issues. Among other duties, the EPAct of 2005 gives sweeping new tools to FERC, including civil penalty authority to prevent market manipulation (in response to an assortment of gas trading scandals and the resulting reduction in confidence in market indices). Since the passage of the Act, the world’s largest trading loss occurred in September 2006 when the Greenwich, Connecticut, “hedge” fund Amaranth Advisors

Introduction And Current Market Overview

1-8

collapsed after accumulating $6.5 billion in losses. This occurred when, over the course of the week of September 11, the spread between the March and April gas futures contract collapsed. Amaranth had huge positions on both the Intercontinental Exchange (ICE) and other off-NYMEX instruments to keep its big bets out of the view of regulators. Figure 1-7 compares Amaranth Advisor’s losses in natural gas to other well-publicized trading losses. Figure 1-7 Prominent Trading Losses in Various Commodities

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

Metallgesellschaft-1993

Orange County-1994

Daiwa-1995 Barings-1995 Sumitomo-1996 Long-Term CapitalMgmt.-1998

AmaranthAdvisors-2006

Hed

ging

or S

pecu

latin

g Lo

sses

in B

illio

ns

Natural Gas

Crude, Gasoline,Distillate

InterestRates

Bonds

Currency,Bonds

Copper

Bonds

SOURCE: Global Energy.