Subramanya Bettadapura Industry Manager, Energy Practice, Frost & Sullivan Natural Gas Opportunities in Asia Presented by the Latest Gas Development Projects and Recent Exploration Finds April 10 th , 2007 © 2007 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost &

Natural Gas Opportunities in Asia Presented by the Latest Gas Development Projects and Recent Exploration Finds

Aug 20, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Subramanya BettadapuraIndustry Manager, Energy Practice, Frost & Sullivan

Natural Gas Opportunities in Asia Presented by the Latest Gas Development Projects and

Recent Exploration Finds

April 10th, 2007

© 2007 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

Natural Gas Reserves in Asia, 2005

Natural Gas Exploration and Development Activity in Asia

Discoveries and Major Gas Projects in Indonesia

Discoveries and Major Gas Projects in Malaysia

Discoveries and Major Gas Projects China

Discoveries and Major Gas Projects in Myanmar, Thailand and

Vietnam

Discoveries and Major Gas Projects in India, Pakistan and

Bangladesh

Other Countries

Table of Contents

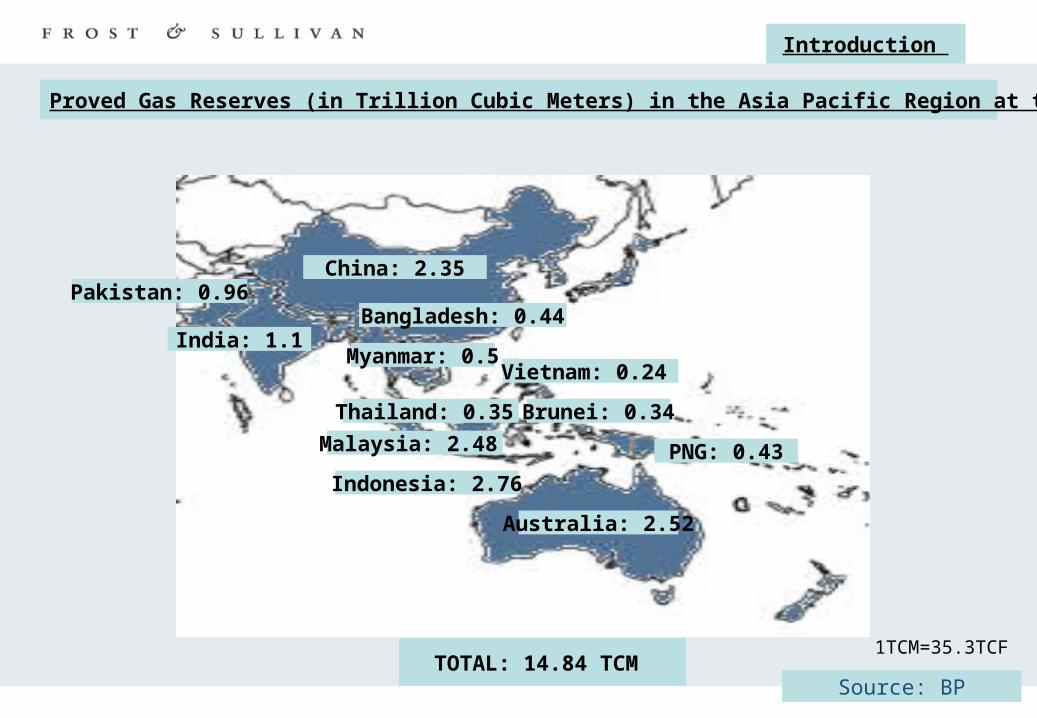

Proved Gas Reserves (in Trillion Cubic Meters) in the Asia Pacific Region at the end of 2005

Introduction

TOTAL: 14.84 TCM Source: BP

Malaysia: 2.48

Indonesia: 2.76

China: 2.35

Bangladesh: 0.44

Australia: 2.52

India: 1.1Myanmar: 0.5

Brunei: 0.34

PNG: 0.43

Pakistan: 0.96

Thailand: 0.35

Vietnam: 0.24

1TCM=35.3TCF

• Gas Production between 2001 and 2005

Production Growth of select countries in Asia (2001 – 2005)

ASIA

Source: Data from BP Statistical Review

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

Pro

du

ctio

n (

BC

M)

2001

2002

2003

2004

2005

• Gas Consumption between 2001 and 2005

Consumption Growth of select countries in Asia (2001 – 2005)

ASIA

Source: Data from BP Statistical Review

0.010.020.030.040.050.060.070.080.090.0

Co

nsu

mp

tio

n (

BC

M)

2001

2002

2003

2004

2005

• Widening gap between consumption and production in Asia. Production in the region not increasing in tune with consumption. Thus, gas importing countries in Asia will have to rely on imports from other regions – Australia, Iran, Qatar and other gas surplus countries

Consumption versus Production Gap - Asia

ASIA

Note: Production and Consumption figures are for Asia only (not including Australia, New Zealand and Papua New Guinea)

Source: Data from BP Statistical Review

Between 2001 and 2005, consumption increased 32% across Asia. Production increased 31% during this period

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

2001 2002 2003 2004 2005

Year

BC

M Production

Consumption

GAS EXPORTERS AND IMPORTERS - ASIA

Introduction

Source: Frost & Sullivan

INDIA – Potential major importer

INDONESIA

CHINA – Potential major importer

JAPAN – Largest Importer

S. KOREA – Major Importer

MYANMAR

BRUNEI

THAILAND

EXPORTER

IMPORTER

MALAYSIA

SINGAPORE

TAIWAN

• Strong Demand for LNG from Japan and South Korea

• Demand for LNG from China and India set to increase

• Proximity of Thailand to major gas exporters makes natural gas pipelines viable. Singapore connected to Malaysia and Indonesia through natural gas pipelines

• Increase in demand and new discoveries give a thrust for the completion of the other planned phases of the Trans-ASEAN Gas pipeline

• Both Thailand and Singapore exploring options to build LNG import terminals

• China, India, Pakistan, Philippines, Thailand and Vietnam – Domestic E&P programs to supplement imports and to meet increasing gas needs

Demand Side Trends

Exploration & Development

• Liquefaction costs are reducing making LNG more attractive. LNG emerges as a viable option for long distance transportation

• Australia, Russia, Iran, Qatar, Saudi Arabia, Oman and UAE – major global competitors for Asian Exporters

• Australia has supply contracts with Japan, South Korea and China.

GLOBAL COMPETITORS FOR ASIAN EXPORTERS

Global Competition

2008 to 2012 – Window of Opportunity to Lock-in Customers in the Asia-Pacific region?

Asia Pacific region is a sellers’ market at present and is expected to remain one till 2012 after which it is likely to transition to a buyers’ market. So, there is a window of opportunity for suppliers that opens in 2008 and closes four or five years later to lock in customers in the Asia-Pacific while there is a shortfall in supply

Development of new gas fields in Australia is being accelerated to start supply as early as 2008. Securing customers after 2012 is likely to be difficult because supply from plants in Qatar and Iran - which have reserves of 52.5 trillion cubic meters of gas, or 21 times the proven reserves in Australia – will start supplying to the market.

• Field Surveys

• Drilling equipment and services

• Well assessment

• Production Platforms supply

• Support and Maintenance services for Development projects

• Pipelines

• LNG plants (Liquefaction plants)

• LNG import terminals and Re-gasification plants

• Marine Vessels (FSOs, LNG Carriers, Pipe-laying vessels)

• Equipment supply (Turbo-machinery, etc)

• Gas to Power (Gas power plants)

Opportunities in exploration and development projects

ASIA

During the Period 2002 to 2006, US$28 to US $30 billion is estimated to have been spent on

offshore drilling in Asia

The Pipeline expenditure in Asia during the period 2002 to 2006 is estimated to be US$15 to

US $17 billion

Asian Shipyards report growing number of orders for offshore production units and rigs

Offshore Support Companies continue to display impressive growth

Exploration and Development Activity – Asia Snapshot

Exploration & Development

PhilippinesOffshore Palawan

VietnamNam Con Son

ChinaPanyu, Hui Zhui

IndiaKG Basin

IndiaRajasthan

PakistanZamazama

IndonesiaMaleo

IndonesiaBontangIndonesia

Natuna Sea Blocks

MalaysiaGuntong E

IndonesiaKakap Field

MalaysiaOffshore Sarawak

MyanmarShwe Field

Source: Frost & Sullivan

Discoveries and Major gas projects

INDONESIA

Source: Frost & Sullivan

Maleo Development

Proposed Pipeline

Tangguh

Jatirarangon field

Onshore Pondok Tengah field

Lukah IXNatuna Sea Block A

Tunu Field Development

Bontang

Kerendan

Kakap Field

Padang LNG

Discoveries and Major gas projects in Indonesia

Indonesia

Country Gas Discovery/Project

Kerendan area gas reserves, onshore Kalimantan

Tunu Field Development Project, Phase two

Maleo Gas Development project

Tangguh Project

Lukah IX

Kakap Field Development - Maintenace Contract

Onshore Pondok Tengah field, West Java.

Jatirarangon Field

Natuna Sea Block A

Padang LNG Project, Central Sulawesi

Samarinda to Surabaya Pipeline

INDONESIA

Discoveries and Major gas projects in Malaysia

Malaysia

2006 E&P Spending in Malaysia: RM16billion

Source: Frost & Sullivan

PM 302

Pisagan 1A

Oil & Gas Terminal at

Kimanis

Kanowit 1

E-11 Hub Integrated Gas Project

E-8, F13 West and F13 East satellite gas

fields

PC4-1 exploration well

F-38, F2 attic and B12 Guntong

Hub

Discoveries and Major gas projects in Malaysia

Malaysia

Country Gas Discovery/Project

Guntong Hub Development

PC4-1PM302

Pisagan-1AKanowit 1

E-11 Hub Integrated Gas ProjectSabah Oil & Gas Terminal at

Kimanis, Sabah

MALAYSIA

Discoveries and Major gas projects in China

China

Shanghai’s LNG receiving terminal

Fujian LNG Import terminal

Pearl River basin Husky Energy

Liwan 3-1-1, Block 29/26

Puguang Gas Field

Proposed West-East Pipeline -2

Hui Zhou Gas Field

Panyu Gas Field

Source: Frost & Sullivan

Discoveries and Major gas projects in China

China

Country Gas Discovery/Project

Shanghai’s LNG receiving terminal

Fujian LNG Import Terminal

Pearl River BasinPuguang Gas Field

Hui Zhou 21-1Panyu 30-1

Second West East Pipeline

CHINA

Discoveries and Major gas projects in Myanmar, Thailand and Vietnam

Myanmar, Thailand and Vietnam

Shwe & Shwepyu Block A-1,

Mya Block A-3

Proposed Myanmar – Bangladesh – India

Gas Pipeline

Proposed Arakan Kunming Pipeline

Chauk Field

Proposed LNG import facility

Phu Horn Project

Bongkot Phase IV

Arthit Field

Ban Yen 2A

Song Hong Basin

Ca Ngu Vang

Rong DoiNam Con Son

Source: Frost & Sullivan

Discoveries and Major gas projects in Myanmar, Thailand and Vietnam

Myanmar, Thailand and Vietnam

Country Gas Discovery/Project

Offshore Blocks A-1 (Shwe and Shwepyu) & A-3 (Mya Field)

Chauk oil field

Phu Horm Project

Bongkot Phase-4 development, Gulf of Thailand

Arthit Production

Ban Yen 2A

Proposed LNG Terminal

Song Hong Basin

Ca Ngu Vang (CNV)

Nam Con Son

Rong Doi

VIETNAM

MYANMAR

THAILAND

Discoveries and Major gas projects in India, Pakistan and Bangladesh

India, Pakistan and Bangladesh

Krishna Godavari BasinONGC

KG-DWN-A-1KG-DWN-E-1KG-DWN-U-1KG-DWN-W-1

RelianceDhirubhai 1 & 3

D6

RajasthanFocus Energy –

SGL1

Vasai-East

Bangora-1 WellZamZama Field

Mahanadi Basin

Source: Frost & Sullivan

Kochi LNG Terminal

Discoveries and Major gas projects in Other Countries in India, Pakistan and Bangladesh

India, Pakistan and Bangladesh

Country Gas Discovery/Project

D6, Krishna-Godavari basin

Dhirubhai gas field development project in the Krishna-Godavari

(KG) basin

ONGC Discoveries KG basin and Mahanadi basin

SGL-1, Rajasthan

Vasai East Development Project

Kochi LNG Terminal

PAKISTAN ZamZama Phase-2

BANGLADESH Bangora-1

INDIA

• The Korea National Oil Corporation (KNOC) has discovered a commercial natural gas deposit in

the Donghae 6-1 sector of the Sea of Japan

Discoveries and Major gas projects in Other Countries in Asia

South Korea

Singapore

Rest of Asia

• LNG terminal by 2012. Contract to be awarded in 2008. Project cost estimated to be $500million

Philippines

• Forum Energy has surveyed the Sampaguita gas discovery at offshore Palawan. Results show

in place gas reserves of 3.4 trillion cubic feet (tcf) with upside reserves of approximately 10 tcf

Related Documents