NATIONAL POLICE CONTACT MANAGEMENT BENCHMARKING REPORT 2008

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

NATIONAL POLICE CONTACT MANAGEMENT

BENCHMARKING REPORT 2008

2

National Police Contact Management Benchmarking Report 2008

Contents

Foreword ......................................................................................................................................................4

Introduction ..................................................................................................................................................5

Merchants and the Global Contact Centre Benchmarking Report ...................................................................6

Research Methodology..................................................................................................................................7

Executive Summary .......................................................................................................................................9

Fundamental KPI Scorecard .........................................................................................................................25

Chapter 1: Background Information.............................................................................................................29

Introduction ......................................................................................................................................................................... 29 Findings ................................................................................................................................................................................ 29

Organisation Details................................................................................................................................................................................ 29 Contact Centre Details ............................................................................................................................................................................ 30

Observations and Recommendations .................................................................................................................................. 30 Chapter 2: Strategy and Development .........................................................................................................33

Introduction ......................................................................................................................................................................... 33 Global Perspective................................................................................................................................................................ 33 Findings ................................................................................................................................................................................ 38

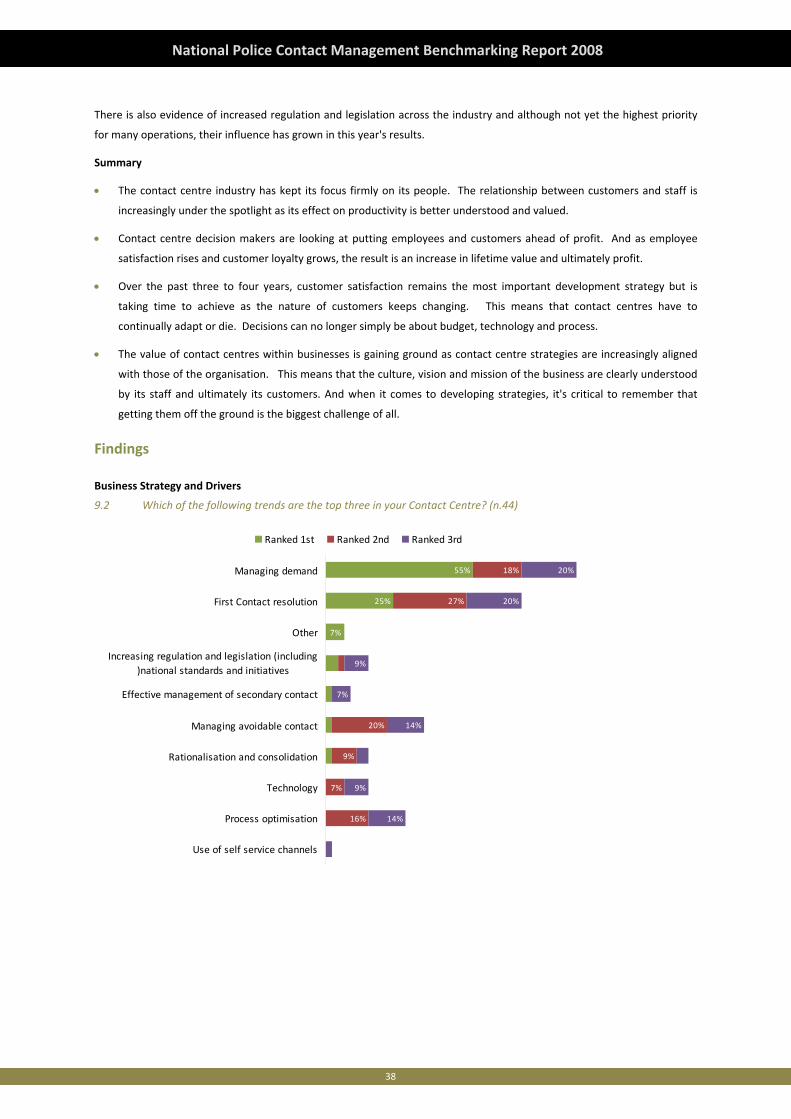

Business Strategy and Drivers ................................................................................................................................................................. 38 Location Strategy .................................................................................................................................................................................... 40 Organisational Strategy, Maturity and Development ............................................................................................................................. 41 Channel Use and Strategy ....................................................................................................................................................................... 43

Observations and Recommendations .................................................................................................................................. 44 Chapter 3: Financial Rationale and Management .........................................................................................47

Introduction ......................................................................................................................................................................... 47 Global Perspective................................................................................................................................................................ 47 Findings ................................................................................................................................................................................ 52

Financial Rationale and Objectives.......................................................................................................................................................... 52 Financial Management and Procedures.................................................................................................................................................. 53

Observations and Recommendations .................................................................................................................................. 54 Chapter 4: Customer Knowledge and Management .....................................................................................57

Introduction ......................................................................................................................................................................... 57 Global Perspective................................................................................................................................................................ 57 Findings ................................................................................................................................................................................ 64

Segmentation.......................................................................................................................................................................................... 64 Service Offering Per Segment.................................................................................................................................................................. 66 Customer Knowledge .............................................................................................................................................................................. 66 Impact of Service Changes on Customers................................................................................................................................................ 68

Observations and Recommendations .................................................................................................................................. 70

3

National Police Contact Management Benchmarking Report 2008

Chapter 5: Performance Measurement and Metrics.....................................................................................73

Introduction ......................................................................................................................................................................... 73 Global Perspective................................................................................................................................................................ 73 Findings ................................................................................................................................................................................ 78

Telephone Interactions Statistics............................................................................................................................................................. 78 Resolution and Response Times .............................................................................................................................................................. 84 Key Performance Indicators and Targets................................................................................................................................................. 88 Statistical Analysis and Reporting ........................................................................................................................................................... 90

Observations and Recommendations .................................................................................................................................. 92 Chapter 6: Processes and Procedures...........................................................................................................95

Introduction ......................................................................................................................................................................... 95 Global Perspective................................................................................................................................................................ 95 Findings ................................................................................................................................................................................ 98

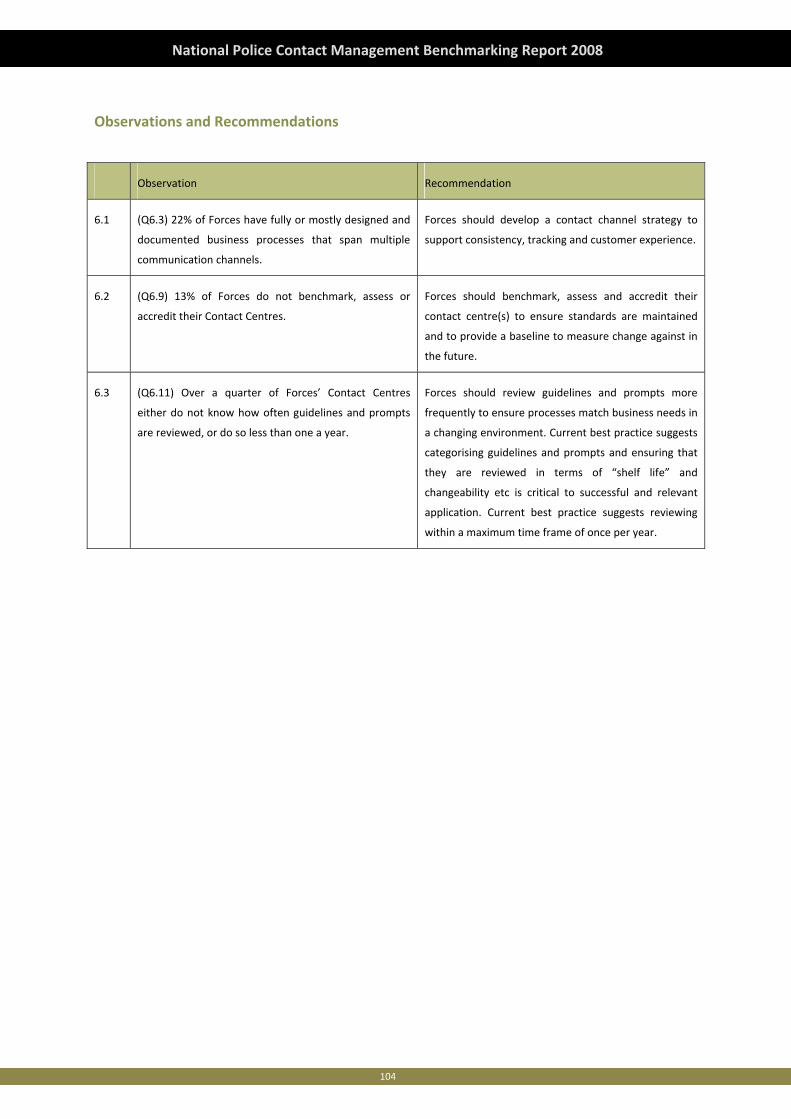

Process Design and Documentation ........................................................................................................................................................ 98 Organisation Process Management ........................................................................................................................................................ 99 Assessment and Quality .......................................................................................................................................................................... 99 Facilities ................................................................................................................................................................................................ 102 Premises and Environment.................................................................................................................................................................... 103

Observations and Recommendations ................................................................................................................................ 104 Chapter 7: Structure and Resource Management .......................................................................................107

Introduction ....................................................................................................................................................................... 107 Global Perspective.............................................................................................................................................................. 107 Findings .............................................................................................................................................................................. 111

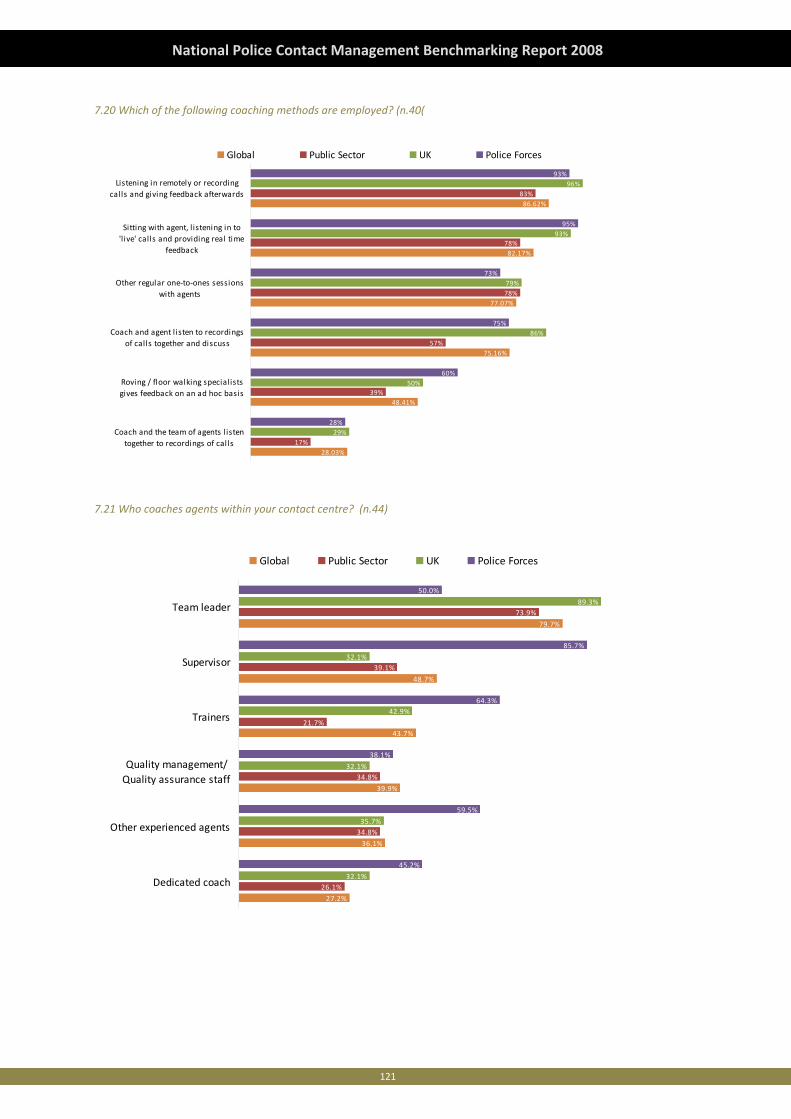

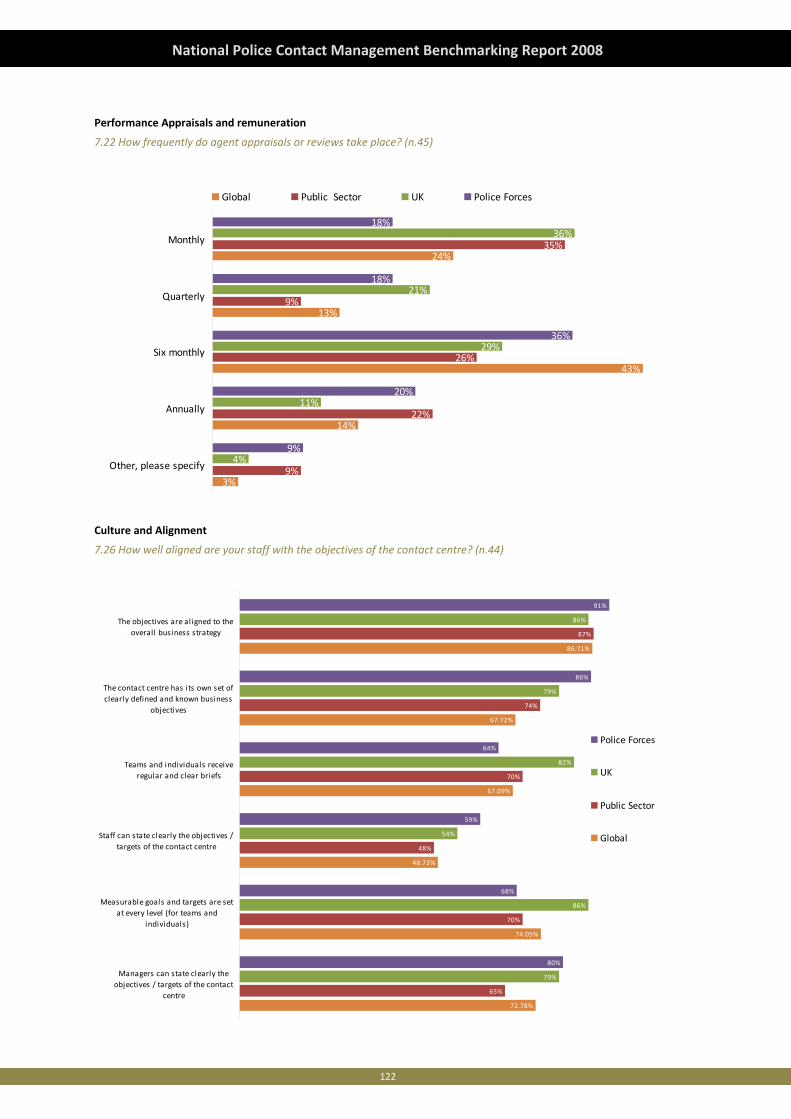

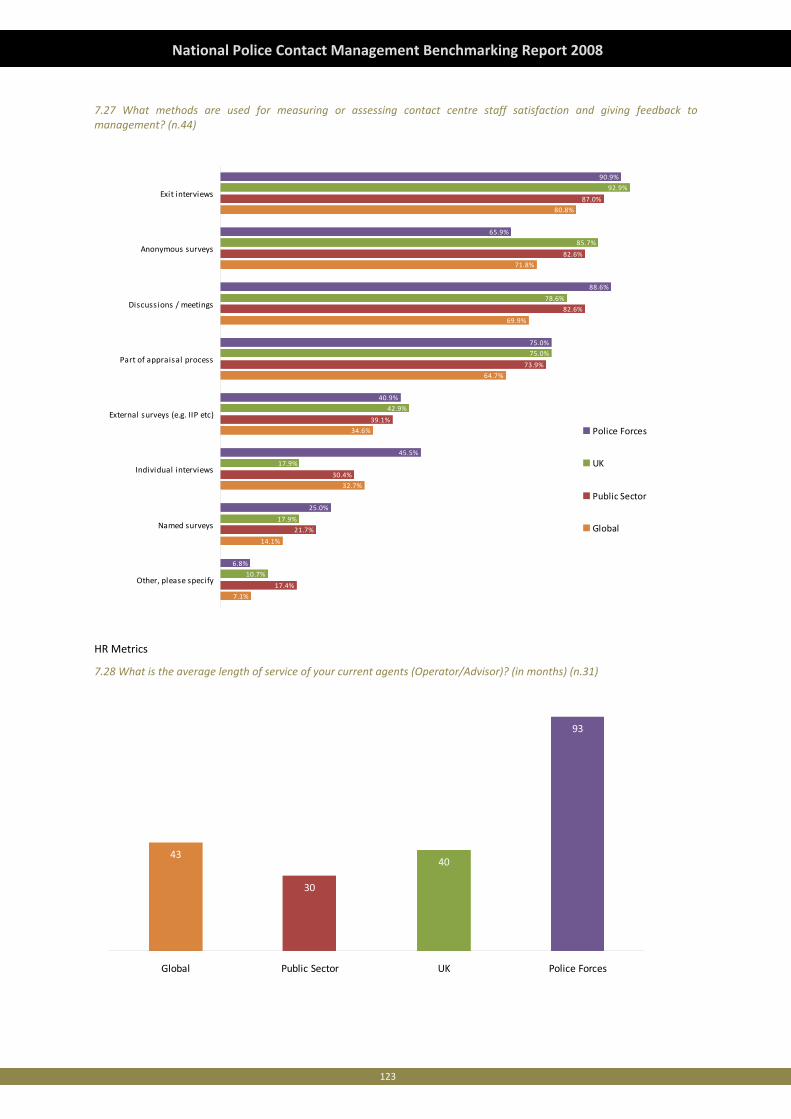

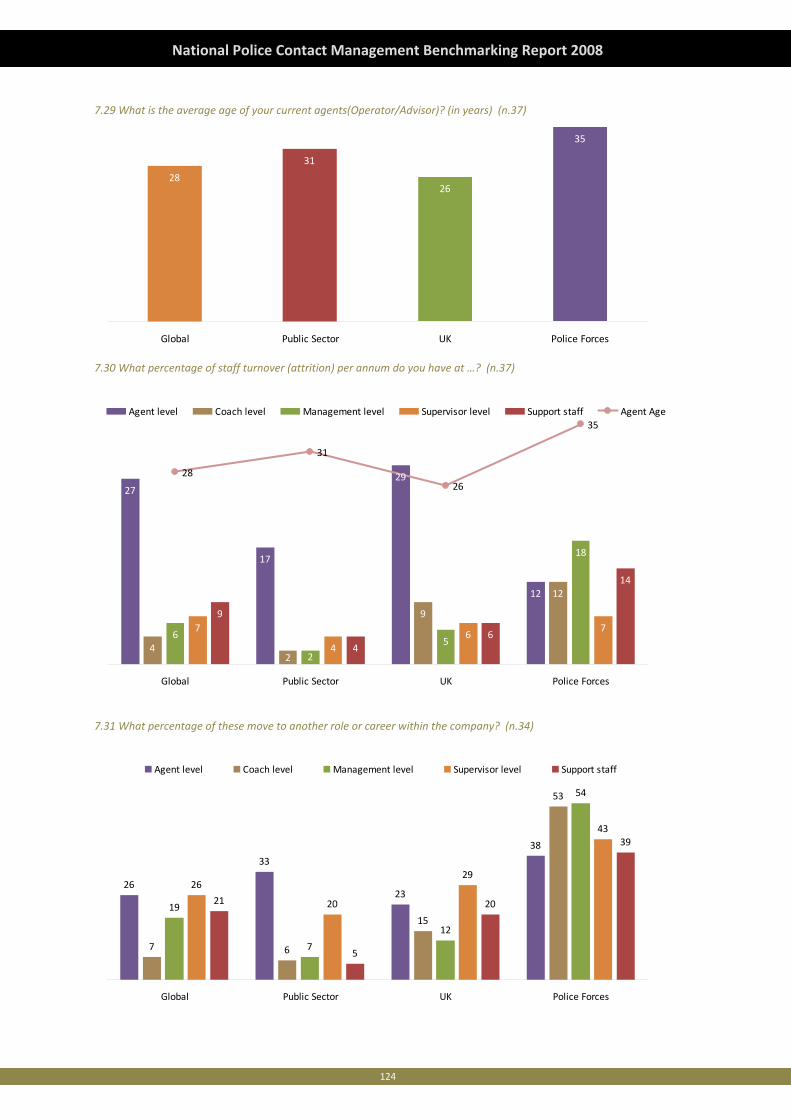

Strategy and Positioning ....................................................................................................................................................................... 111 Structure and Resources........................................................................................................................................................................ 112 Recruitment .......................................................................................................................................................................................... 116 Training, Coaching and Support ............................................................................................................................................................ 117 Performance Appraisals and remuneration .......................................................................................................................................... 122 Culture and Alignment .......................................................................................................................................................................... 122

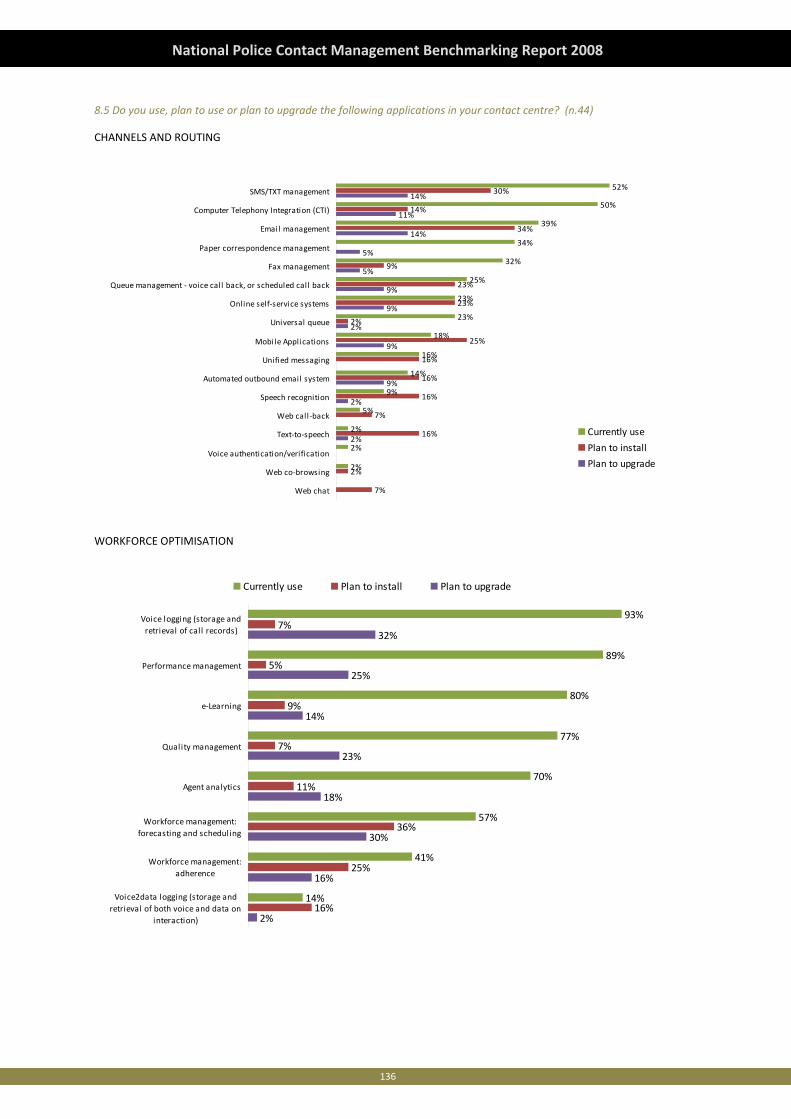

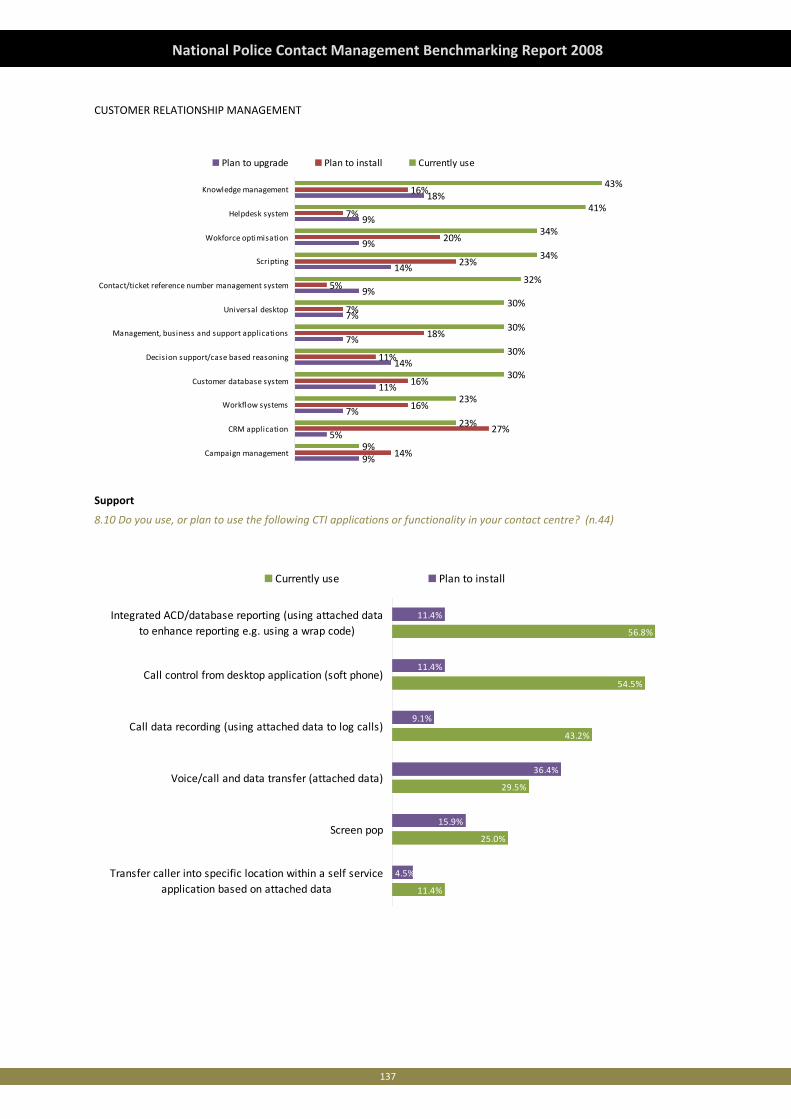

Observations and Recommendations ................................................................................................................................ 126 Chapter 8: Technology Environment ..........................................................................................................129

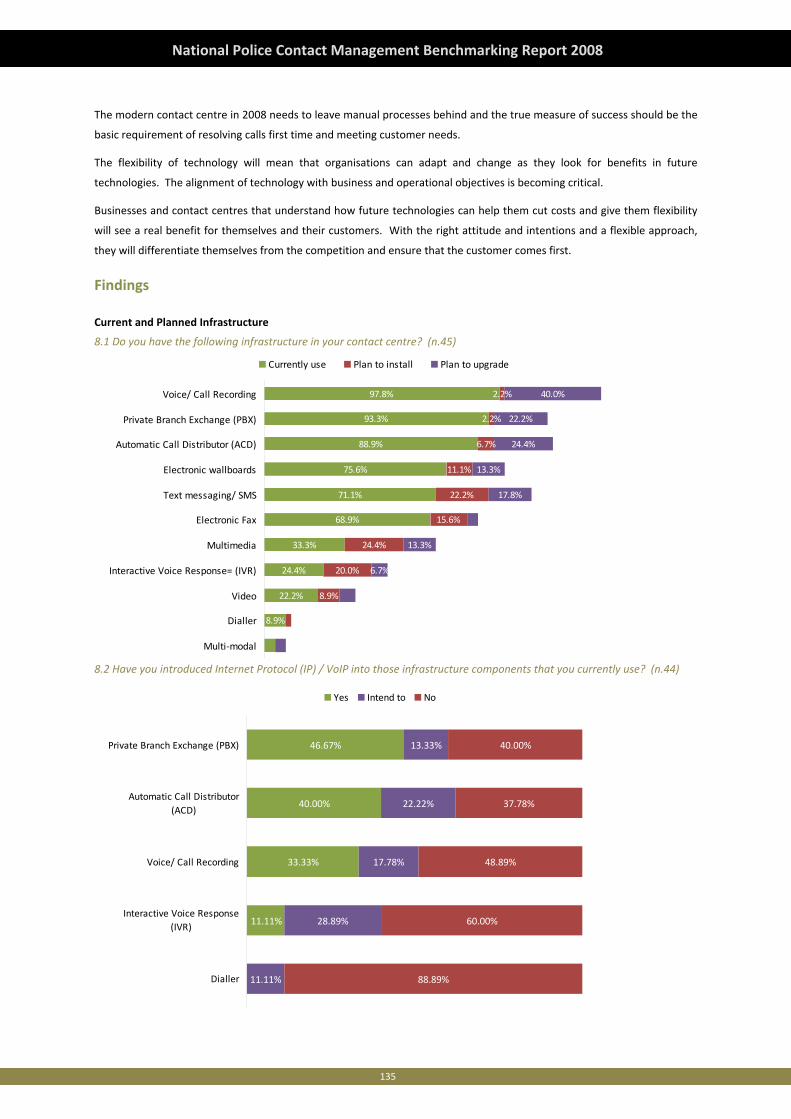

Introduction ....................................................................................................................................................................... 129 Global Perspective.............................................................................................................................................................. 129 Findings .............................................................................................................................................................................. 135

Current and Planned Infrastructure....................................................................................................................................................... 135 Support ................................................................................................................................................................................................. 137 Strategy and Infrastructure................................................................................................................................................................... 138

Observations and Recommendations ................................................................................................................................ 140 Glossary of Terms......................................................................................................................................141

4

National Police Contact Management Benchmarking Report 2008

Foreword

The HMIC thematic on call handling, ‘First Contact’ (2005) recommended that an independent and externally led contact

management benchmarking exercise be carried out. In the summer of 2007 we contacted all forces to establish the level of

willingness to take part in such an event. There was clear support for this work to be undertaken.

The importance of this work has increased in line with the raised profile of the Citizen Focus Agenda (CFA) and the

understanding that effective contact management lies at the heart of strategic and citizen focussed service delivery.

I am grateful to all the Forces who took part in this exercise and to Merchants for the production of this excellent report.

For the first time the Police Service has an opportunity to establish a true baseline position around contact management.

Forces will now be able to benchmark against one another and to make effective comparisons against the public and

private sector, both within the UK and globally.

Benchmarking activity will help the Service to identify where there are similarities of approach as well to determine areas

where we differ, (or are perhaps unique), from other organisations, in our approach to the management of public contact.

Better understanding of trends and variations in performance will allow the Police Service to identify those factors that are

critical in terms of improving public service delivery. Benchmarking not only focuses on the strengths and good practice of

others but it also provides an opportunity to identify and validate that, which works well in Policing. This report shows that

there are areas in which the Service is already at the leading edge.

This benchmarking exercise is a significant event in the drive to develop a truly citizen focused approach to policing. The

outputs of this exercise will also inform ongoing work around a Review of National Call Handling Standards (NCHS), and the

creation of a National Contact Management Standard (NCMS). The NCMS will exist to ensure that contact management in

the police service is truly citizen focused, reflects advances in technology and appropriately meets needs of the public in the

21st century.

It is important to stress that the aim of this exercise is to support performance improvement in the round and not to create

a system of leagues and tables. Should this exercise prove as productive to the police service as it has to other public and

private sector organisations, then funding permitting, a programme of annual or bi‐annual benchmarking will be

introduced. This will allow individual Forces and the Service, as a whole, to understand what improvements, over time,

have been achieved.

I hope sincerely that this work will prove a valuable source of information to colleagues and which will help us deliver a

continuously improving service to the public

Commander Simon Foy

National Contact Management Programme, ACPO Lead

5

National Police Contact Management Benchmarking Report 2008

Introduction

The Police Service has always recognised its responsibilities in relation to customer care and the importance of its

relationship with the public. This responsibility has been identified within a number of national reports, including ‘Policing

Bureaucracy Taskforce’, ‘Open All Hours’,’ The National Policing Plan 2005 – 2008’, ‘The Police Reform Agenda’, ‘Building

Communities, Beating Crime’, ‘The Quality of Service Commitment’ and ‘Citizen Focus Policing Guide’.

The Police Service acknowledges that prior to the introduction of the National Call Handling Standards (NCHS) in 2005, the

public’s expectations in respect of call handling and primary contact with the police had not been sufficiently well met.

There was and remains a requirement for consistency and harmonisation between forces in contact management

methodology. This point was reinforced by HMIC in the thematic inspections of police contact management ‐ ‘First Contact’

and ‘Beyond the Call’. These reports recommended that an independent and externally led benchmarking exercise be

carried out.

Contact Management is much wider than call handling and sits at the heart of Citizen Focused service delivery. The

National Contact Management Programme is currently developing NCHS into a National Contact Management Standard

(NCMS) that will meet the needs of the public in the 21st century. The findings of the National Police Contact Management

Benchmarking Report 2008 will inform this process and set a baseline for contact management in the Police Service.

Additionally, it will allow identification and celebration of existing areas of world class performance and/or good practice

that is evident within Police contact management.

The national police contact management benchmarking exercise will provide the Service with the opportunity to compare

itself internally and with other public and private sector organisations from across the globe. The report also considers the

uniqueness of the Police Service, whilst acknowledging that the vast bulk of police contact with the public is similar to other

public or private sector service providers and therefore open to productive benchmark. To address the unique aspects of

police contact, potential international police benchmarking partners will in the near future, be identified and appropriate

comparison activity commissioned.

Delivery of the National Police Contact Management Benchmarking Report 2008 has been co‐ordinated by the National

Contact Management Programme (NCMP), which is located within the National Policing Improvement Agency (NPIA). This

work has the full support and involvement of Her Majesty’s Inspectorate of Constabulary (HMIC), the Association of Chief

Police Officers (ACPO) and the Police Service of England and Wales. All Forces accept the need to improve contact

management and the responsibility they have to manage such activity efficiently and to the satisfaction of the Police

Authorities and the communities they serve. This work is both aligned to and supportive of Sir David Varney’s report on

‘Service Transformation’ (2006).

This is the first time within policing (globally it is believed) that at a national level benchmarking of contact management

has been undertaken. This is an important factor, because as with all ‘path finding’ activity there will always be a period of

learning and reflection. We will overtime identify how best to use the information that results from this activity to help the

Police Service provide a truly world class citizen focused service.

Acknowledgements

The Association of Chief Police Officers (ACPO), the National Policing Improvement Agency (NPIA) and Her Majesty’s

Inspectorate of Constabulary (HMIC) would like to acknowledge the support and commitment of all staff who contributed

to the production of this report.. Thank you to all forces for taking part and specifically Mike Horne (Her Majesty’s

Inspectorate of Constabulary), Pauline Smith (Staffordshire Police), Kay Southall, Peter Major, Mike Rawsthorn and other

members of the National Contact Management Programme Team (National Policing Improvement Agency ‐ Assisted

Implementation).

6

National Police Contact Management Benchmarking Report 2008

Merchants and the Global Contact Centre Benchmarking Report

Merchants – a division of Dimension Data – is a

leading customer management firm, providing a

full range of innovative managed services and

contact centre consultancy expertise.

Internationally recognised for providing best

practice consulting and managed service

solutions for over 25 years, they have gained

over 70 awards of recognition in the industry

that testify the premium nature of their

customer contact solutions and industry

knowledge.

Their in‐depth understanding and specialised

skills enable them to provide organisations with

a range of services from creating customer

management strategy solutions, developing

people including training of frontline managers

and agents and providing business solutions for process and technology issues. They provide industry innovation and

thought leadership by combining strategic understanding with practitioner’s knowledge and experience, Performance

Improvement is at the core of both their own operations and work with other organisations around the globe.

With increasing pressures being placed on customer contact professionals to contain the costs of, improve efficiencies in

and improve the performance of their centre, the need to know what is happening and to understand the reasons for it are

essential. As a key player in the global contact centre industry, Merchants are firmly committed to the ongoing growth of

this vibrant sector. They demonstrate their dedication by providing the industry with an extremely valuable tool for

customer contact and contact centre review: The Global Contact Centre Benchmarking report.

The Global Contact Centre Benchmarking Report was first published by Merchants in 1997 and to draw on their operational

and commercial expertise. It is a rich and comprehensive information source on the day‐to‐day realities faced by contact

centres and the trends occurring in the industry.

The report is an industry‐renowned study of contact centres around the world and has a proud history of comprehensively

investigating and reporting the performance levels achieved and operational realities experienced by global contact

centres. The Benchmarking Report aims to add value to you and your contact centre: providing information and analysis of

operational daily productivity benchmarks through to helping you articulate the true purpose and value of your centres.

The report is concerned with the current status of the global contact centre market. Its content encompasses the entire

sphere of today’s contact centre environment. It includes all aspects of contact centre operations and performance from

strategy, customer management and financial management, through processes and procedures, human resources and

training, to technology environment and overall performance management. The Global Contact Centre Benchmarking

Report provides you with global contact centre information of an unparalleled depth and scale.

Customer Management

•Contact Centre set up•Shoring & Sourcing•Customer Contact

Strategy•Channel Management•Customer Experience•Customer Lifecycle and

Journey•Benchmarking

•Recruitment•Training

• Interim/Project Management

•Performance Management

•Culture Change

•Workforce Optimisation

•Quality Assurance•Technology intercept

•Process review/engineering

•Self Service•Operational Improvement

Customer Strategy______

Customer Customer StrategyStrategy____________

People Development

______

People People DevelopmentDevelopment

____________

Business Solutions______

Business Business SolutionsSolutions____________

Performance ImprovementPerformance Improvement

7

National Police Contact Management Benchmarking Report 2008

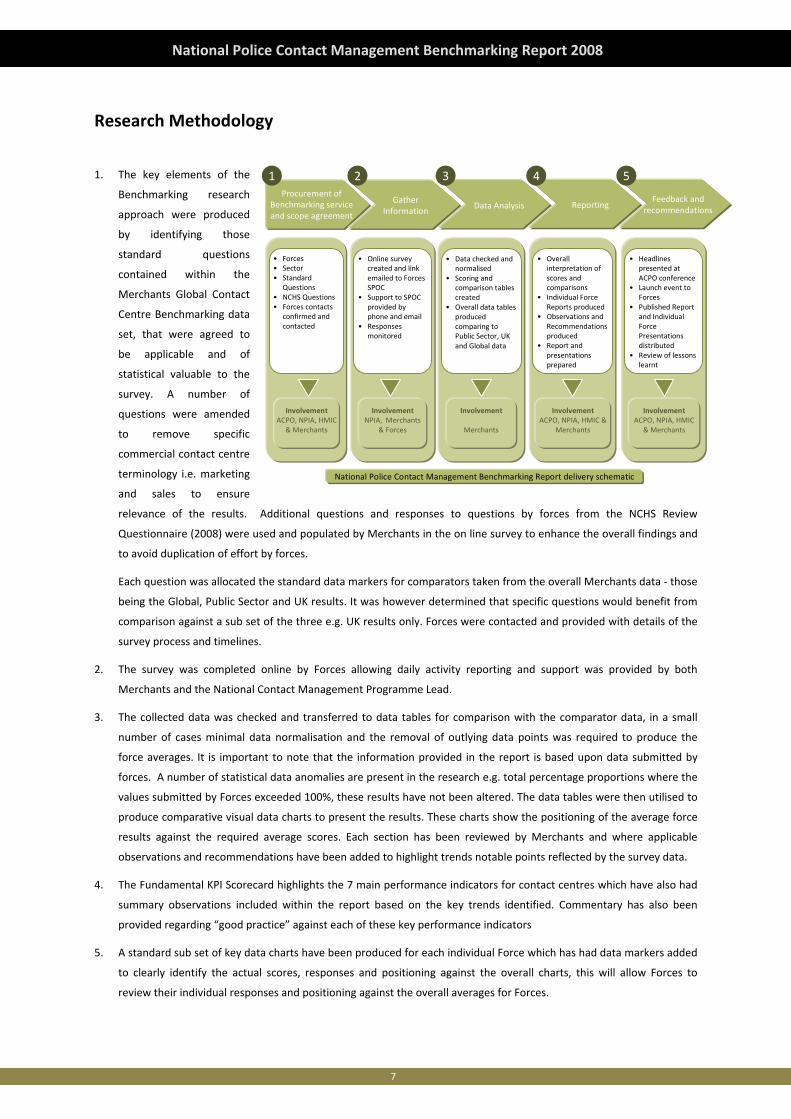

Research Methodology

1. The key elements of the

Benchmarking research

approach were produced

by identifying those

standard questions

contained within the

Merchants Global Contact

Centre Benchmarking data

set, that were agreed to

be applicable and of

statistical valuable to the

survey. A number of

questions were amended

to remove specific

commercial contact centre

terminology i.e. marketing

and sales to ensure

relevance of the results. Additional questions and responses to questions by forces from the NCHS Review

Questionnaire (2008) were used and populated by Merchants in the on line survey to enhance the overall findings and

to avoid duplication of effort by forces.

Each question was allocated the standard data markers for comparators taken from the overall Merchants data ‐ those

being the Global, Public Sector and UK results. It was however determined that specific questions would benefit from

comparison against a sub set of the three e.g. UK results only. Forces were contacted and provided with details of the

survey process and timelines.

2. The survey was completed online by Forces allowing daily activity reporting and support was provided by both

Merchants and the National Contact Management Programme Lead.

3. The collected data was checked and transferred to data tables for comparison with the comparator data, in a small

number of cases minimal data normalisation and the removal of outlying data points was required to produce the

force averages. It is important to note that the information provided in the report is based upon data submitted by

forces. A number of statistical data anomalies are present in the research e.g. total percentage proportions where the

values submitted by Forces exceeded 100%, these results have not been altered. The data tables were then utilised to

produce comparative visual data charts to present the results. These charts show the positioning of the average force

results against the required average scores. Each section has been reviewed by Merchants and where applicable

observations and recommendations have been added to highlight trends notable points reflected by the survey data.

4. The Fundamental KPI Scorecard highlights the 7 main performance indicators for contact centres which have also had

summary observations included within the report based on the key trends identified. Commentary has also been

provided regarding “good practice” against each of these key performance indicators

5. A standard sub set of key data charts have been produced for each individual Force which has had data markers added

to clearly identify the actual scores, responses and positioning against the overall charts, this will allow Forces to

review their individual responses and positioning against the overall averages for Forces.

Procurement of Benchmarking service and scope agreement

1 2 3 4 5

• Forces• Sector• Standard

Questions• NCHS Questions• Forces contacts

confirmed and contacted

• Online survey created and link emailed to Forces SPOC

• Support to SPOC provided by phone and email

• Responses monitored

• Data checked and normalised

• Scoring and comparison tables created

• Overall data tables produced comparing to Public Sector, UK and Global data

• Overall interpretation of scores and comparisons

• Individual Force Reports produced

• Observations and Recommendations produced

• Report and presentations prepared

• Headlines presented at ACPO conference

• Launch event to Forces

• Published Report and Individual Force Presentations distributed

• Review of lessons learnt

InvolvementACPO, NPIA, HMIC

& Merchants

Gather Information

Data Analysis ReportingFeedback and

recommendations

InvolvementNPIA, Merchants

& Forces

Involvement

Merchants

InvolvementACPO, NPIA, HMIC &

Merchants

InvolvementACPO, NPIA, HMIC

& Merchants

National Police Contact Management Benchmarking Report delivery schematic

8

National Police Contact Management Benchmarking Report 2008

6. The final outputs of the Benchmarking survey include a presentation to the Forces and the production and distribution

of a printed report. In addition a Force specific CD containing copies of this report, the Overall presentation including

all of the survey charts and a copy of the Forces individual presentation (each force receiving a personalised CD

containing their own presentation).

7. Each Chapter within this report contains an introductory section which provides a commentary around the chapter

subject matter based on the results of the 2008 Global Contact Centre Benchmarking report and Merchants industry

experience.

8. All charts shown within this report display the question asked of the survey respondents followed by the number of

responses to the question eg (n.45). The Report also includes nine questions that have been taken from the NCHS

questionnaire previously responded to by forces and these questions have been highlighted by the inclusion of the

following indicator, (NCHS).

9

National Police Contact Management Benchmarking Report 2008

Executive Summary

Introduction

This report is the result of the initial National Police Contact Management Benchmarking exercise, co‐ordinated by the

National Policing Improvement Agency (NPIA) with the support of Association of Police Officers (ACPO) and Her Majesty’s

Inspectorate of Constabulary (HMIC), and delivered by Merchants. The findings of the report will serve as a baseline for

contact management, enabling progress to be tracked and improvements measured.

Merchants produce the industry standard Global Contact Benchmark Report annually, and have subsequently created a

specific survey for Police Contact Management Benchmarking. Each of the 43 Forces from England & Wales plus British

Transport Police (BTP) and Civil Nuclear Constabulary (CNC) were invited to participate in the survey, and all 45 of these

Forces responded with high quality submissions.

During the Benchmarking exercise, 23,500 police‐specific pieces of data have been collated and analysed, in addition to

existing data gained from the recent National Call handling Standards (NCHS) Review Questionnaire. The Police‐specific

data has been compared with Merchants’ 2008 Global Contact Centre Benchmark Report data, providing direct

comparisons with Global, UK Commercial, and Public Sector data.

Selected Findings

This report comprises 8 chapters which contain charts and graphs of the data collected during the Benchmarking exercise,

together with high‐level observations and recommendations. The report chapters are:

• Background Information

• Strategy and Development

• Financial Management and Rationale

• Customer Knowledge and Management

• Performance Measurement and Metrics

• Processes and Procedures

• Structure and Resource Management

• Technology Environment

Whilst the individual chapters comprise the detail of the collated and analysed data, there follow some selected findings

and interpretations of the results.

10

National Police Contact Management Benchmarking Report 2008

Chapter 1 – Background

This chapter evaluates the scale and size of the forces contact centre operations providing an overall view of the average

number of sites and seats across all forces. The sections include organisational details and contact centre details.

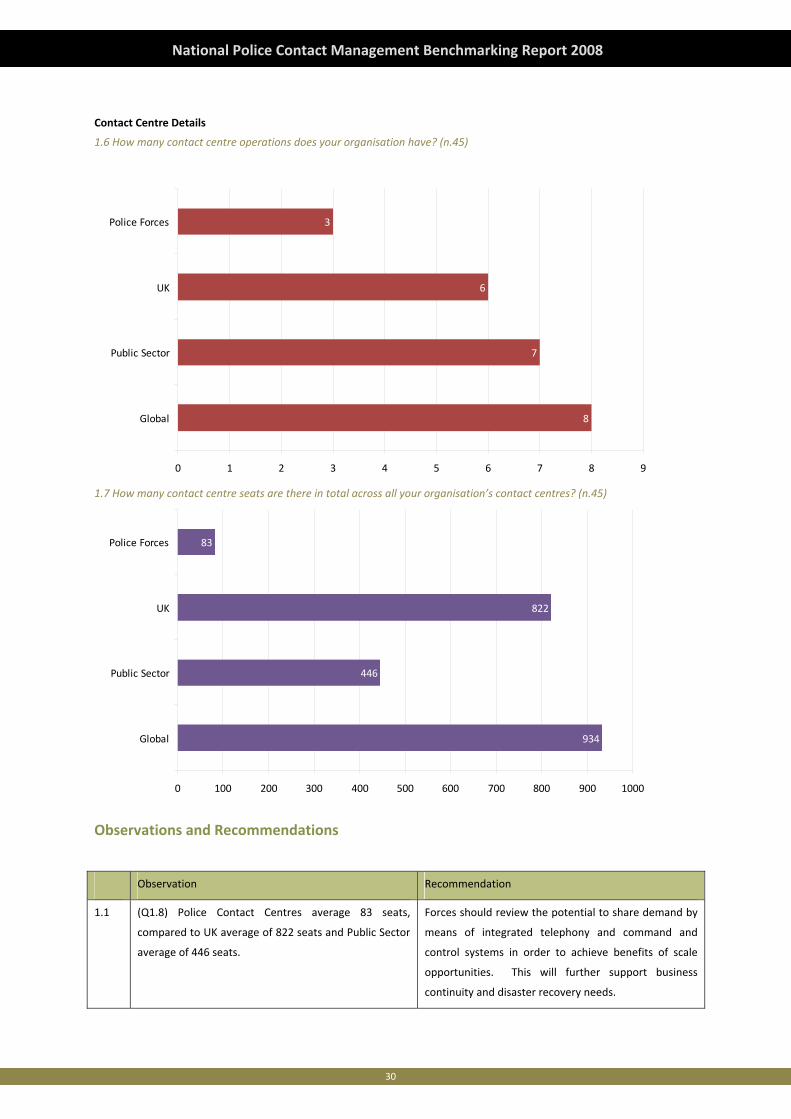

1.7 How many contact centre seats are there in total across all your organisation’s contact centres? (n.45)

934

446

822

83

0 100 200 300 400 500 600 700 800 900 1000

Global

Public Sector

UK

Police Forces

This graph shows that there are on average 83 seats per contact centre within the Police Service compared to the 446

within the public sector and over 900 globally. The impact of this is discussed in Recommendation 1.1.

Chapter 2 – Strategy and Development

In this chapter, we review the research regarding customer management strategy, its people and processes. The results of

the Global Benchmarking Report give us a clear insight into industry and regional trends and will help in evaluating the

performance of your contact centre.

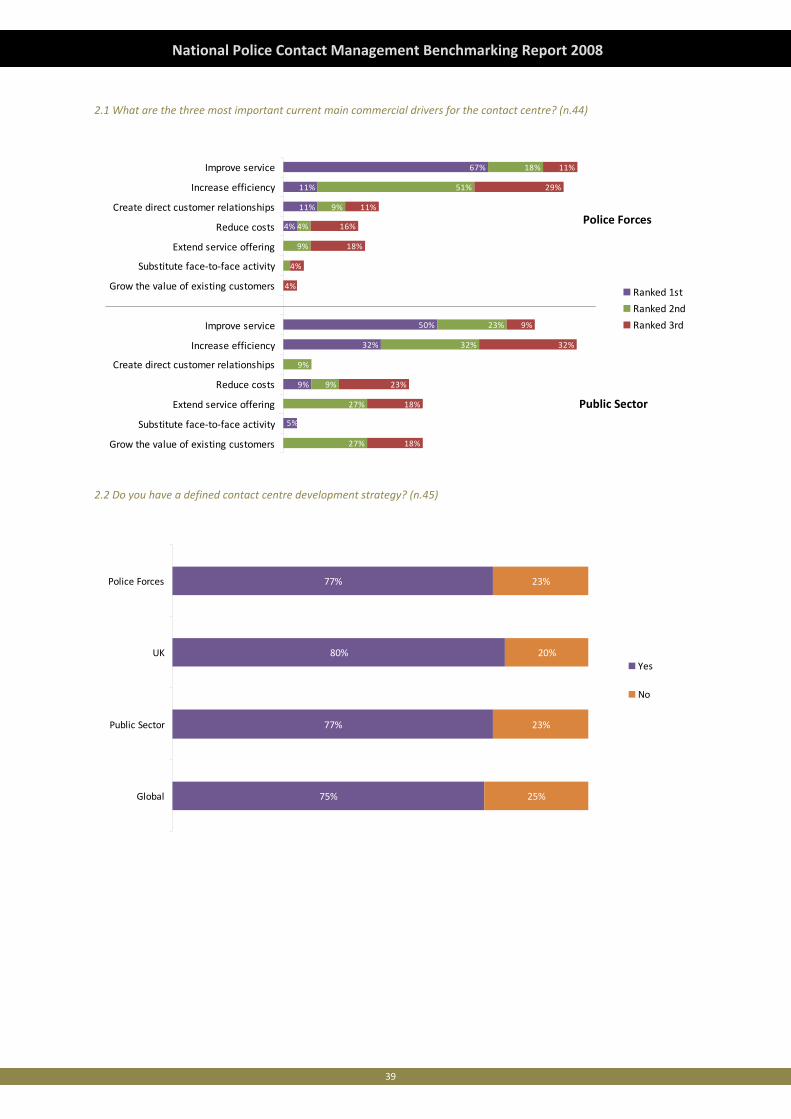

2.1 What are the three most important current main commercial drivers for the contact centre? (n.44)

0%

9%

32%

50%

11%

11%

67%

27%

27%

9%

32%

23%

4%

9%

51%

18%

18%

18%

32%

9%

4%

18%

16%

11%

29%

11%

5%

4%

9%

9%

0%

23%

4%

Grow the value of existing customers

Substitute face‐to‐face activity

Extend service offering

Reduce costs

Create direct customer relationships

Increase efficiency

Improve service

Grow the value of existing customers

Substitute face‐to‐face activity

Extend service offering

Reduce costs

Create direct customer relationships

Increase efficiency

Improve service

Ranked 1st

Ranked 2nd

Ranked 3rd

Police Forces

Public Sector

11

National Police Contact Management Benchmarking Report 2008

In this case, the Police data is compared with Public Sector generally, and it is interesting to note that 96% of Police Forces

rank Improve Service in their top 3, compared with 82% in Public Sector generally, whilst 96% of Public Sector rank Increase

Efficiency in their top 3, with 32% ranking this first compared with 11% in Police Forces. Reduce Costs is also a key driver for

41% of Public Sector Contact Centres, compared with 25% in Police.

This clearly demonstrates that the main driver for Police Contact Centres is in Improving Service, compared with other

Public Sector bodies that place Efficiency and Cost Reduction higher.

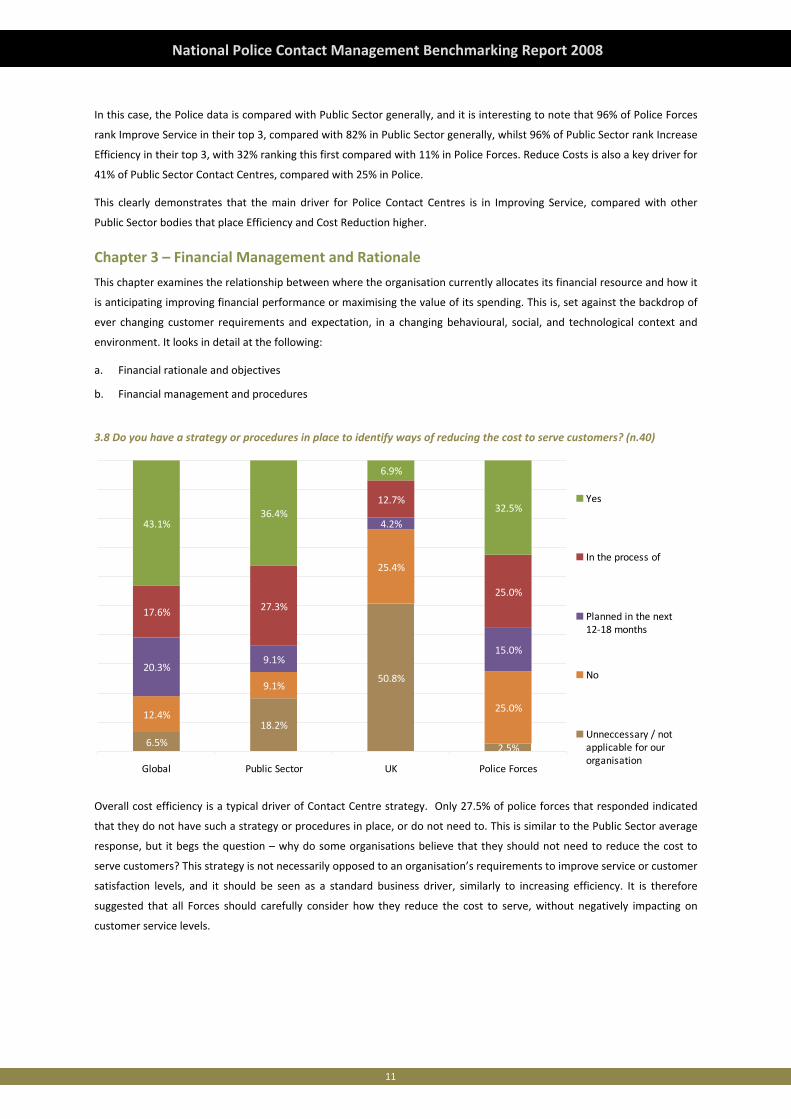

Chapter 3 – Financial Management and Rationale

This chapter examines the relationship between where the organisation currently allocates its financial resource and how it

is anticipating improving financial performance or maximising the value of its spending. This is, set against the backdrop of

ever changing customer requirements and expectation, in a changing behavioural, social, and technological context and

environment. It looks in detail at the following:

a. Financial rationale and objectives

b. Financial management and procedures

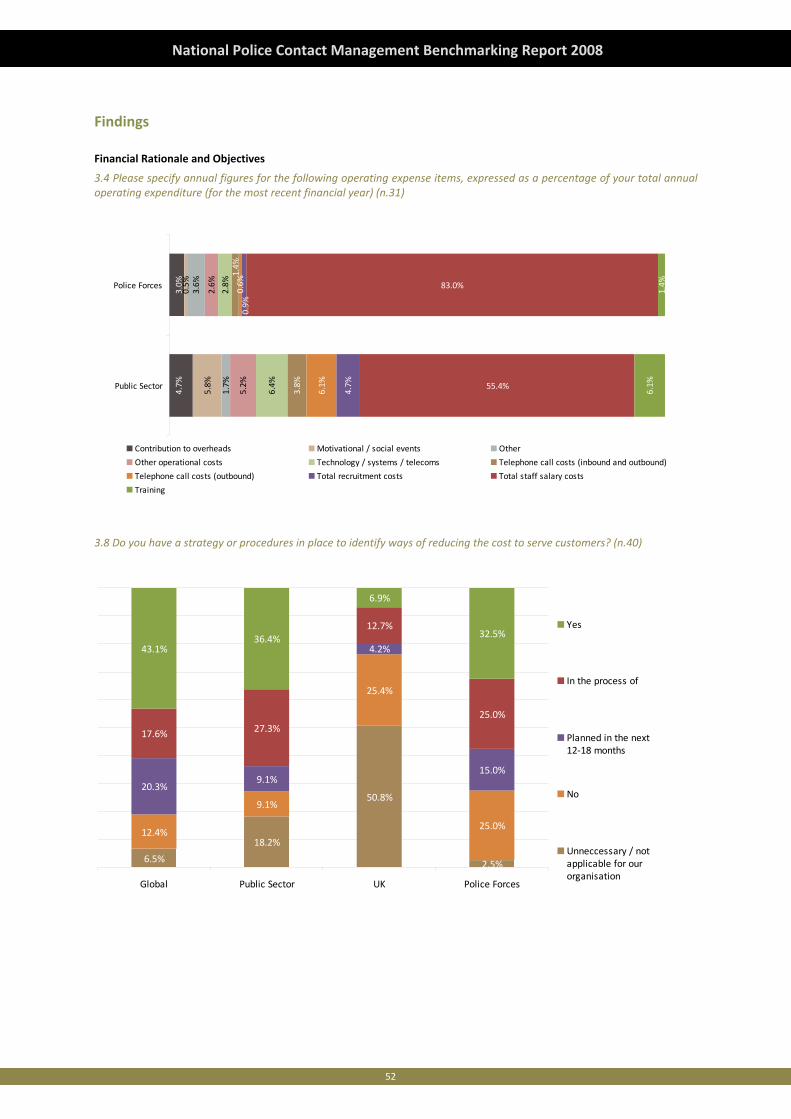

3.8 Do you have a strategy or procedures in place to identify ways of reducing the cost to serve customers? (n.40)

6.5%

18.2%

50.8%

2.5%

12.4%

9.1%

25.4%

25.0%

20.3%9.1%

4.2%

15.0%

17.6% 27.3%

12.7%

25.0%

43.1%36.4%

6.9%

32.5%

Global Public Sector UK Police Forces

Yes

In the process of

Planned in the next12‐18 months

No

Unneccessary / notapplicable for ourorganisation

Overall cost efficiency is a typical driver of Contact Centre strategy. Only 27.5% of police forces that responded indicated

that they do not have such a strategy or procedures in place, or do not need to. This is similar to the Public Sector average

response, but it begs the question – why do some organisations believe that they should not need to reduce the cost to

serve customers? This strategy is not necessarily opposed to an organisation’s requirements to improve service or customer

satisfaction levels, and it should be seen as a standard business driver, similarly to increasing efficiency. It is therefore

suggested that all Forces should carefully consider how they reduce the cost to serve, without negatively impacting on

customer service levels.

12

National Police Contact Management Benchmarking Report 2008

Chapter 4 – Customer Knowledge and Management

This chapter looks at how organisations are broadening their service portfolios and offering more variations in an effort to

maximise customer loyalty and satisfaction. This in turn creates major challenges in working out how to effectively,

efficiently and appropriately support their customers with multiple services. To do this it is vitally important to maximise

the use of Customer Management strategies through informed customer insight and knowledge.

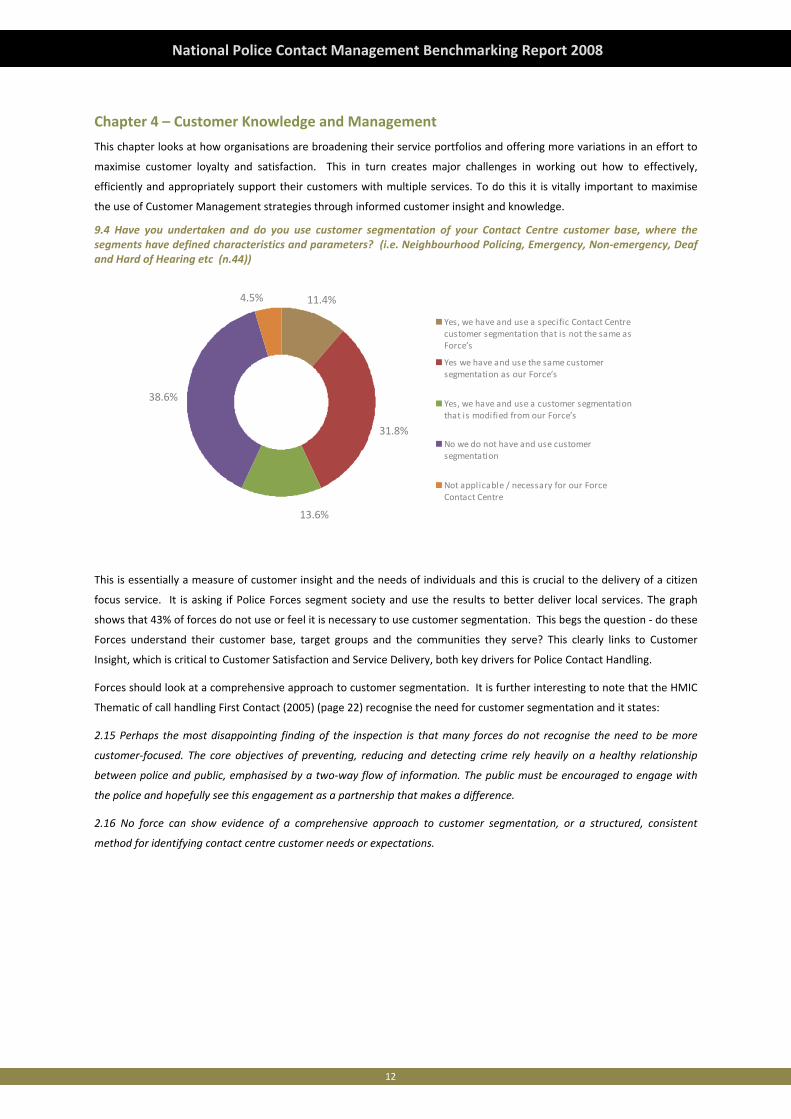

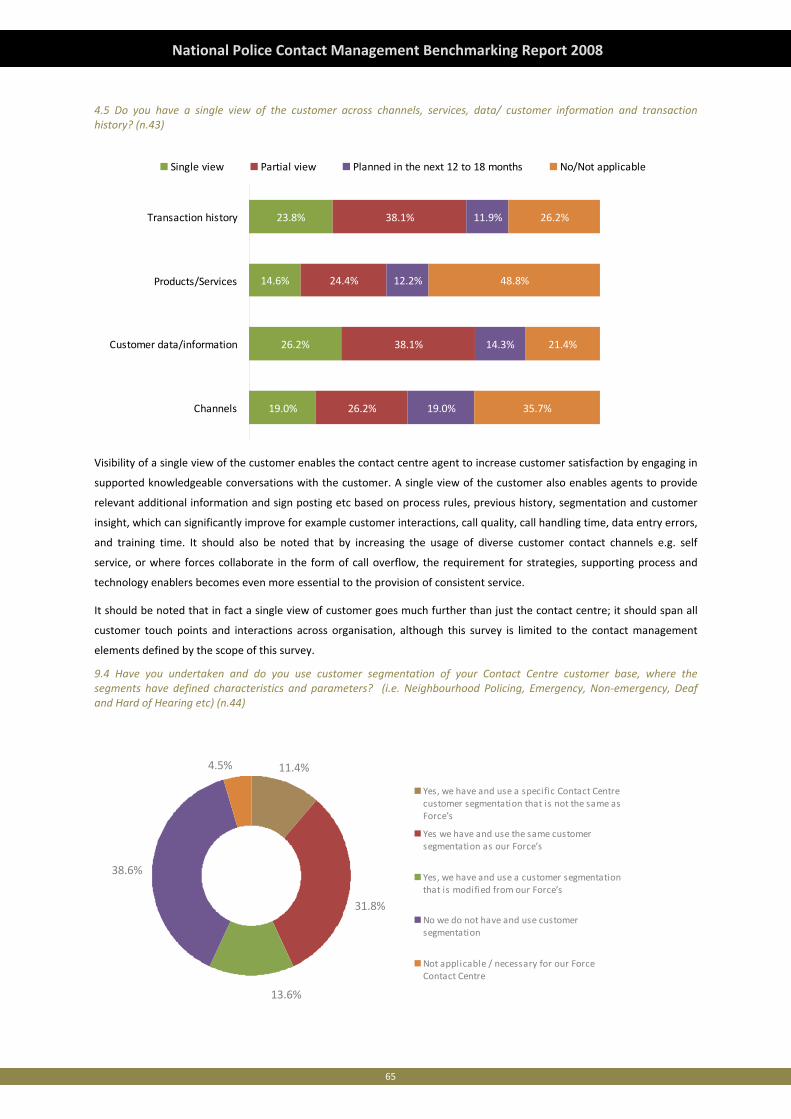

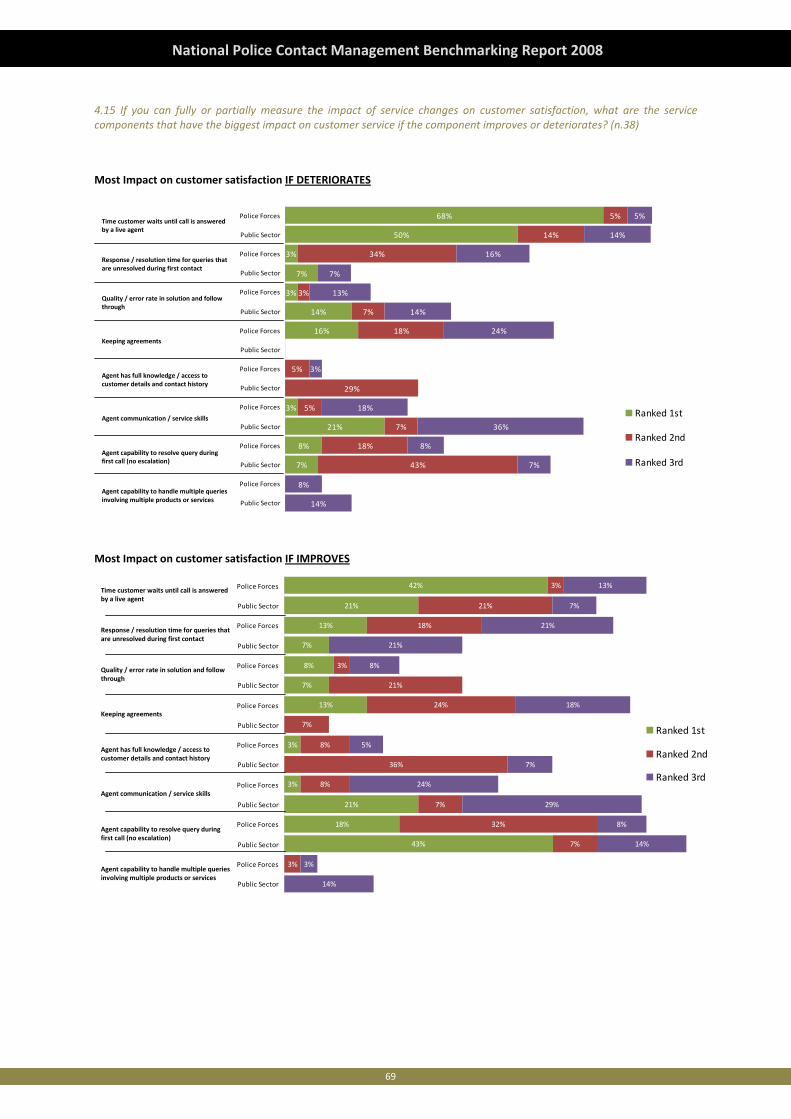

9.4 Have you undertaken and do you use customer segmentation of your Contact Centre customer base, where the segments have defined characteristics and parameters? (i.e. Neighbourhood Policing, Emergency, Non‐emergency, Deaf and Hard of Hearing etc (n.44))

38.6%

13.6%

4.5% 11.4%

31.8%

Yes, we have and use a specific Contact Centrecustomer segmentation that is not the same asForce’s

Yes we have and use the same customersegmentation as our Force’s

Yes, we have and use a customer segmentationthat is modified from our Force’s

No we do not have and use customersegmentation

Not applicable / necessary for our ForceContact Centre

This is essentially a measure of customer insight and the needs of individuals and this is crucial to the delivery of a citizen

focus service. It is asking if Police Forces segment society and use the results to better deliver local services. The graph

shows that 43% of forces do not use or feel it is necessary to use customer segmentation. This begs the question ‐ do these

Forces understand their customer base, target groups and the communities they serve? This clearly links to Customer

Insight, which is critical to Customer Satisfaction and Service Delivery, both key drivers for Police Contact Handling.

Forces should look at a comprehensive approach to customer segmentation. It is further interesting to note that the HMIC

Thematic of call handling First Contact (2005) (page 22) recognise the need for customer segmentation and it states:

2.15 Perhaps the most disappointing finding of the inspection is that many forces do not recognise the need to be more

customer‐focused. The core objectives of preventing, reducing and detecting crime rely heavily on a healthy relationship

between police and public, emphasised by a two‐way flow of information. The public must be encouraged to engage with

the police and hopefully see this engagement as a partnership that makes a difference.

2.16 No force can show evidence of a comprehensive approach to customer segmentation, or a structured, consistent

method for identifying contact centre customer needs or expectations.

13

National Police Contact Management Benchmarking Report 2008

Chapter 5 – Performance Measurement and Metrics

In this chapter we deal with the key performance measures and metrics surrounding the contact management and contact

centre operations of the organisation. The contact centre industry generally is one of the most highly performance

managed areas in most organisations due to the importance of real time and historic statistical information and data. It is

vital therefore to have availability and understanding of the relationships between key measures and metrics, ensuring that

this is utilised to manage and improve service efficiency and effectiveness.

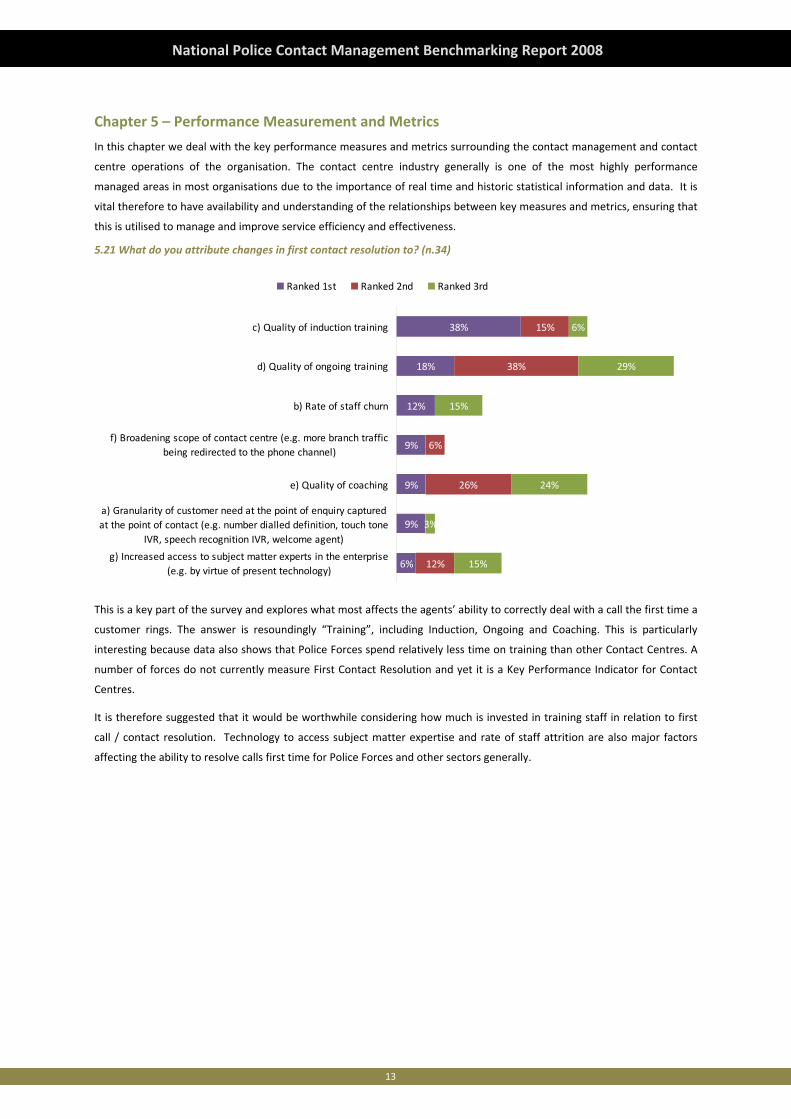

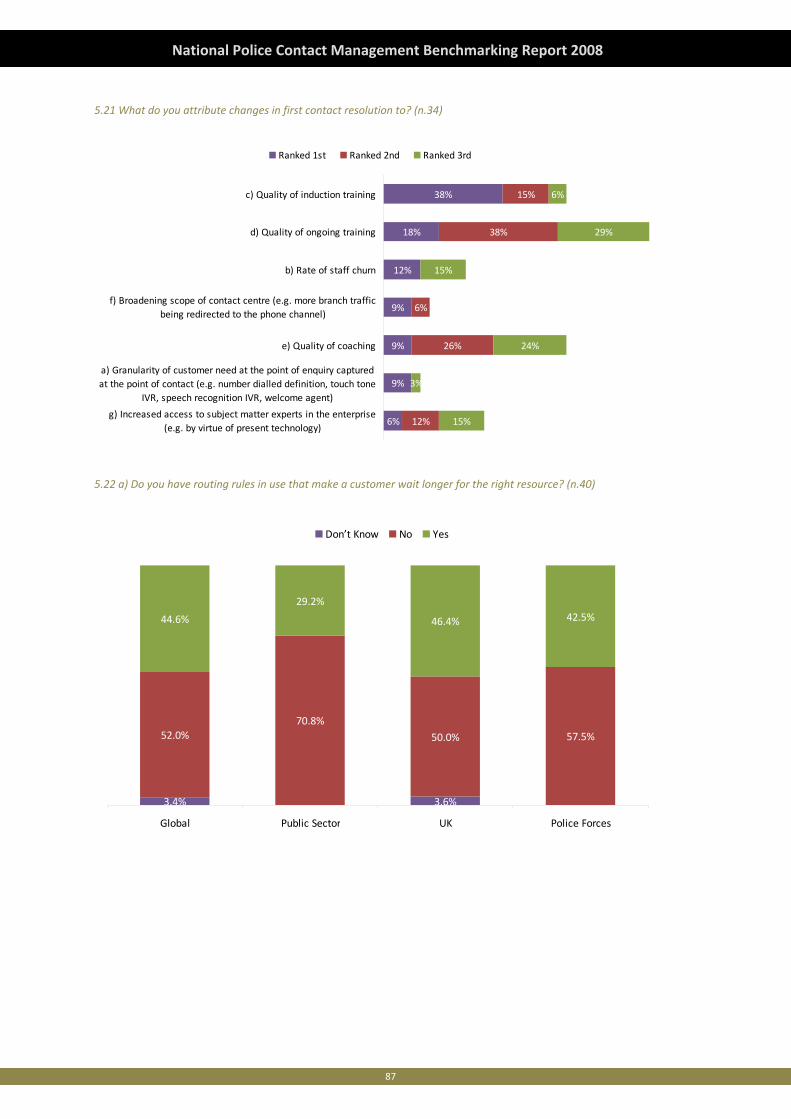

5.21 What do you attribute changes in first contact resolution to? (n.34)

6%

9%

9%

9%

12%

18%

38%

12%

26%

6%

38%

15%

15%

3%

24%

15%

29%

6%

g) Increased access to subject matter experts in the enterprise(e.g. by virtue of present technology)

a) Granularity of customer need at the point of enquiry capturedat the point of contact (e.g. number dialled definition, touch tone

IVR, speech recognition IVR, welcome agent)

e) Quality of coaching

f) Broadening scope of contact centre (e.g. more branch trafficbeing redirected to the phone channel)

b) Rate of staff churn

d) Quality of ongoing training

c) Quality of induction training

Ranked 1st Ranked 2nd Ranked 3rd

This is a key part of the survey and explores what most affects the agents’ ability to correctly deal with a call the first time a

customer rings. The answer is resoundingly “Training”, including Induction, Ongoing and Coaching. This is particularly

interesting because data also shows that Police Forces spend relatively less time on training than other Contact Centres. A

number of forces do not currently measure First Contact Resolution and yet it is a Key Performance Indicator for Contact

Centres.

It is therefore suggested that it would be worthwhile considering how much is invested in training staff in relation to first

call / contact resolution. Technology to access subject matter expertise and rate of staff attrition are also major factors

affecting the ability to resolve calls first time for Police Forces and other sectors generally.

14

National Police Contact Management Benchmarking Report 2008

Chapter 6 – Processes and Procedures

This chapter concentrates on the process element of the contact centre industry which underpins technology and people to

deliver against the organisations needs and that of its customers and stakeholders. Process management is an essential

component in ensuring that the contact centre remains aligned to changing and developing requirements for managing

customer contact.

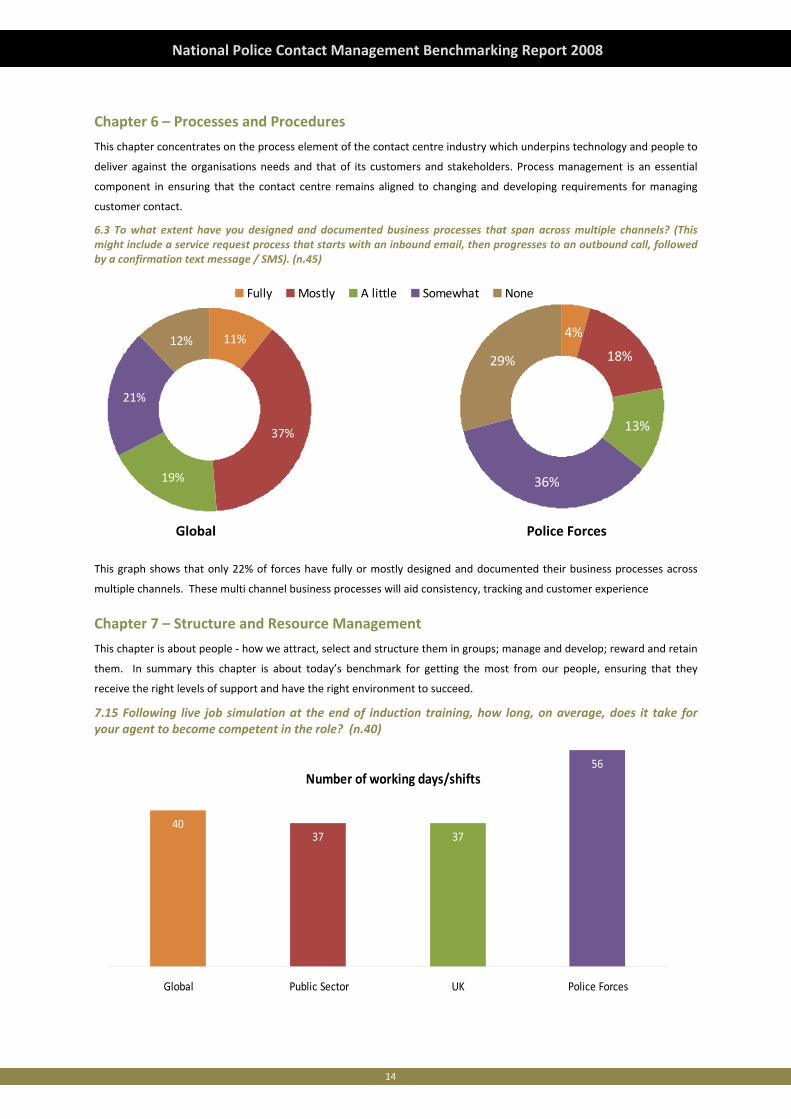

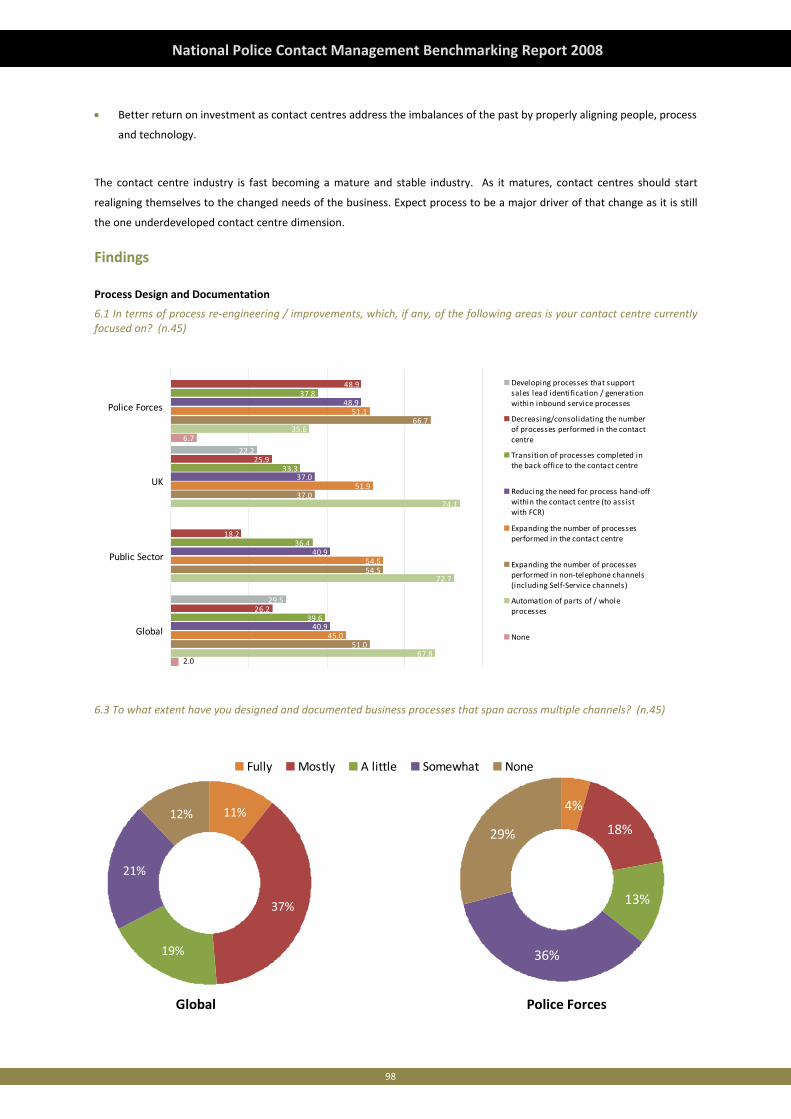

6.3 To what extent have you designed and documented business processes that span across multiple channels? (This might include a service request process that starts with an inbound email, then progresses to an outbound call, followed by a confirmation text message / SMS). (n.45)

11%

37%

19%

21%

12%

Fully Mostly A little Somewhat None

4%

18%

13%

36%

29%

Police ForcesGlobal

This graph shows that only 22% of forces have fully or mostly designed and documented their business processes across

multiple channels. These multi channel business processes will aid consistency, tracking and customer experience

Chapter 7 – Structure and Resource Management

This chapter is about people ‐ how we attract, select and structure them in groups; manage and develop; reward and retain

them. In summary this chapter is about today’s benchmark for getting the most from our people, ensuring that they

receive the right levels of support and have the right environment to succeed.

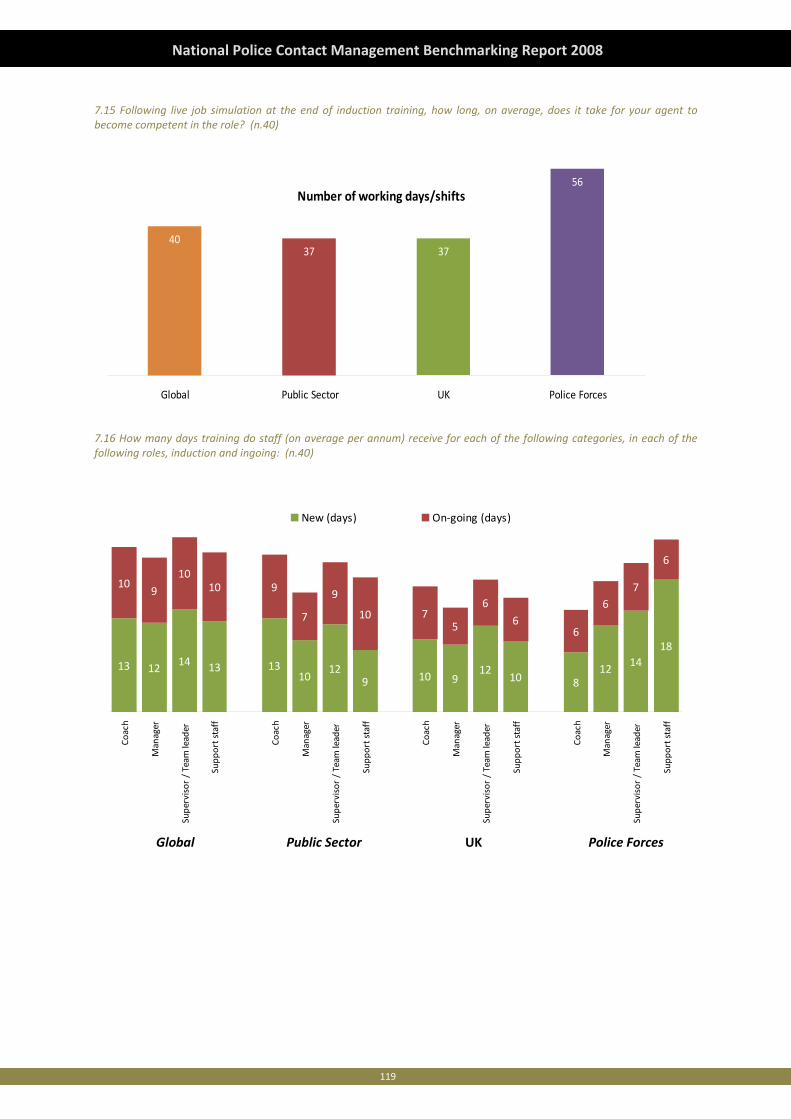

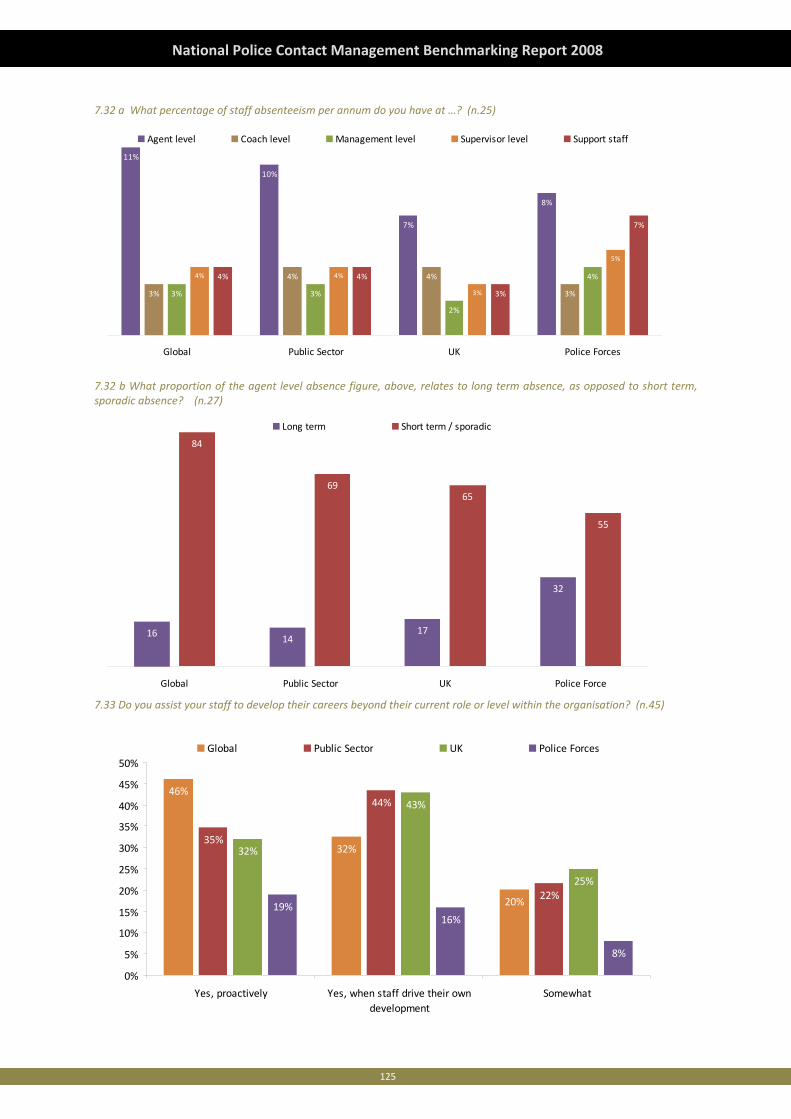

7.15 Following live job simulation at the end of induction training, how long, on average, does it take for your agent to become competent in the role? (n.40)

Number of working days/shifts

4037 37

56

Global Public Sector UK Police Forces

15

National Police Contact Management Benchmarking Report 2008

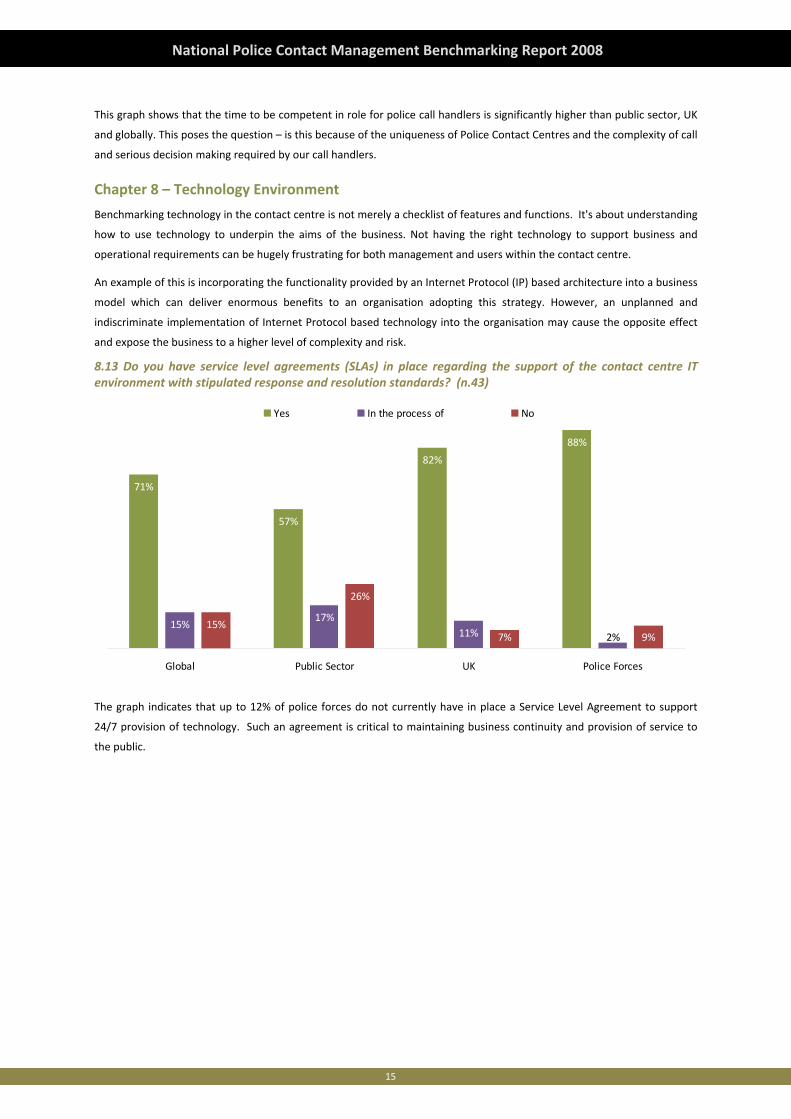

This graph shows that the time to be competent in role for police call handlers is significantly higher than public sector, UK

and globally. This poses the question – is this because of the uniqueness of Police Contact Centres and the complexity of call

and serious decision making required by our call handlers.

Chapter 8 – Technology Environment

Benchmarking technology in the contact centre is not merely a checklist of features and functions. It's about understanding

how to use technology to underpin the aims of the business. Not having the right technology to support business and

operational requirements can be hugely frustrating for both management and users within the contact centre.

An example of this is incorporating the functionality provided by an Internet Protocol (IP) based architecture into a business

model which can deliver enormous benefits to an organisation adopting this strategy. However, an unplanned and

indiscriminate implementation of Internet Protocol based technology into the organisation may cause the opposite effect

and expose the business to a higher level of complexity and risk.

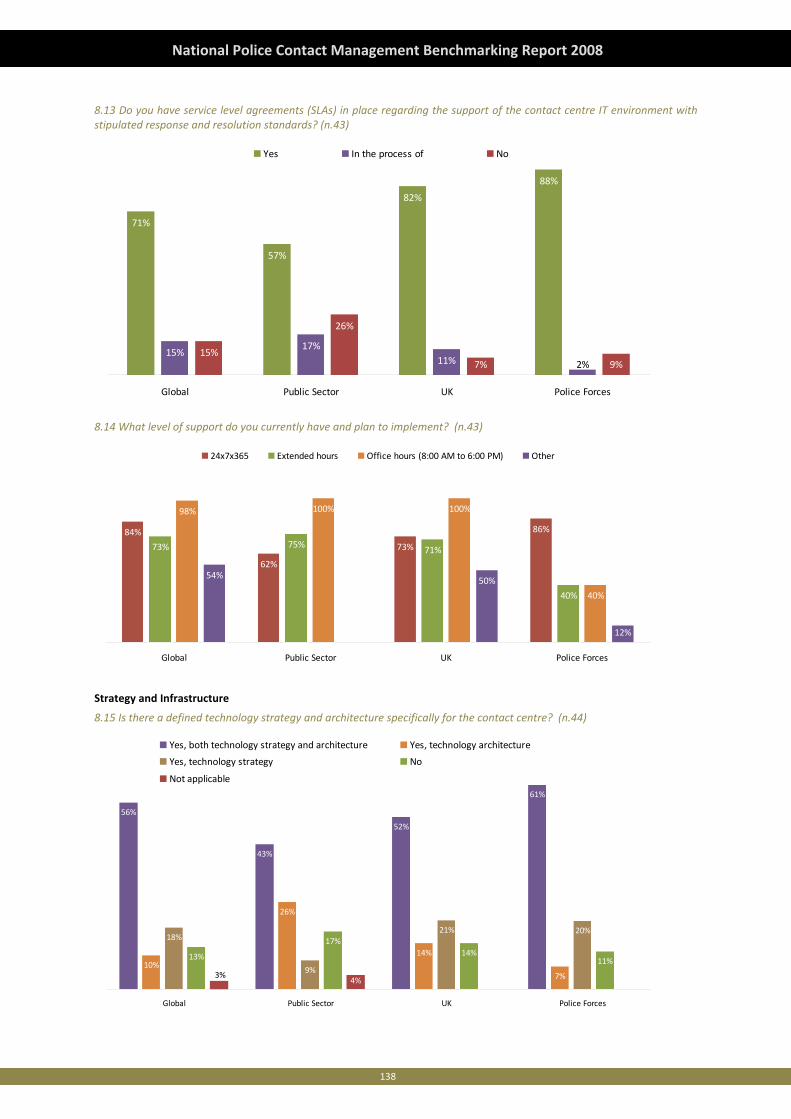

8.13 Do you have service level agreements (SLAs) in place regarding the support of the contact centre IT environment with stipulated response and resolution standards? (n.43)

71%

57%

82%

88%

15%17%

11%15%

26%

7% 9%2%

Global Public Sector UK Police Forces

Yes In the process of No

The graph indicates that up to 12% of police forces do not currently have in place a Service Level Agreement to support

24/7 provision of technology. Such an agreement is critical to maintaining business continuity and provision of service to

the public.

16

National Police Contact Management Benchmarking Report 2008

Fundamental KPI Scorecard for Contact Centres

Within the Contact Centre industry there are numerous performance criteria and metrics surrounding both qualitative and

quantitative measurements. Merchants has been tracking a set of KPI’s for the last 10 years. As mentioned these are not

the only KPI’s that Contact Centres track, however they are generally recognised as the most powerful generic Contact

Centre KPI’s providing a good snapshot of performance. Merchants has a wealth of data comparing different sectors’

performance and year‐on‐year changes. Police Forces’ performance has therefore been compared to Global, Public Sector

and UK geographic results from the 2008 Global Contact Centre Survey KPI Scorecard results.

Customer Satisfaction

This measures how satisfied callers are with the service received on a call to the Contact Centre. Different organisations

measure customer satisfaction in different ways and it can be affected by perception of “brand” if not done correctly.

The UK generally performs better than the Global average since organisations place high emphasis on customer

satisfaction, and many Contact Centres overseas are targeted more on cost reduction, which inevitably adversely affects

customer satisfaction. Compared to last year, it is encouraging to see UK increase from 83% to 86%, reflecting the

improvements many organisations have made in response to customers’ demands for better service.

The Public Sector generally out‐performs most other sectors in customer satisfaction, and represents Best Practice across

all sectors in the 2008 Global Contact Centre Report, partly because there is often no competition, partly due to lower

customer expectations, but also due to the fact that Public Sector understands service. Most Public Sector employees see

themselves as Public Servants and strive to do just that – serve the public.

It is extremely encouraging to note that all 45 Police Forces surveyed measure customer satisfaction, and it is good to see

that the average Police Force score is a percentage point in advance of Public Sector generally. This is based on customer

satisfaction measured by Police Forces themselves, and it will be interesting to see how this changes over the next year.

This is a very difficult KPI to improve year‐on‐year due to the ever‐increasing expectations from customers.

First Contact / Call Resolution

This KPI measures the percentage of calls to a Contact Centre that are resolved the first time, without the need for a

customer to call again or for a follow‐up action.

Last year’s Global score was 81%, which is consistent with this year’s score.

The UK score shows a marked increase compared with the Global average, and is an improvement on last year’s score.

Most customers call to access information or to get an issue resolved as quickly as possible, and this is a key driver of

Customer Satisfaction; there is a direct link between First Contact Resolution (FCR) and customer satisfaction,

demonstrated by the UK’s higher performance compared to the Global average.

Public Sector is generally behind the average on FCR, since the nature of the calls tend to be more complex and wide‐

ranging in scope. Many commercial organisations deal with relatively straight‐forward transactions, such as order‐taking,

balance enquiries and delivery schedules. The range of calls to a Local Authority can be very broad, including Housing,

Parking, Refuse Collection, Revenues and Benefits, and many more. It is not always possible to route a caller to someone

who can deal with this range of enquiries first time.

The Police Service FCR score is significantly lower than the Public Sector average, but this question was only answered by

68% of Forces. This suggests three points:

1. Not all Police Forces can measure FCR, which is a real concern, since FCR drives customer satisfaction, and also

because it drives efficiency; if a call is resolved first time, there is no repeat call from a customer, or follow‐up action

required.

17

National Police Contact Management Benchmarking Report 2008

2. The nature of calls to Police Forces is such that some calls cannot be resolved whilst the caller is on the telephone,

meaning that further investigation or follow‐up actions are often required, such as the deployment of an officer.

3. It is possible that systems are not in place to assist Contact Centre agents to adequately deal with customers’ issues

when they call.

4. It is possible that current culture within the Police Service, which is driven by existing measures has led to a focus

more on answering the Non‐emergency calls than meeting the needs of the customer.

Forces should conduct a contact observation review of activities to ascertain if time management and more unified

technology could support a reduction in wrap time.

Best practice is represented by the Manufacturing and Products sector with a score of 88% in the latest published Global

Contact Centre Benchmark Report.

Agent Utilisation

This measures the amount of time that a Contact Centre Agent is actually talking with customers. It therefore excludes

waiting time and wrap‐up time after a call.

The Global average has been around 55%‐60% for a number of years and it is typically agreed that this is a good target

figure, with best practice being around 60‐65% for commercial organisations. Any higher and agents get burned out; any

lower and they get bored and leave.

Public Sector and UK average is close to ideal and it is good to see, particularly in relation to the Public Sector’s long average

wrap‐up time. The UK number is from last year’s report because we have not extracted this piece of geographic data at

present.

Police Forces’ Agent Utilisation score looks poor on first sight at 34%. However, when we note that wrap‐up time for each

call is typically the same length as talk time, we soon see that the maximum score achievable would be around 50%.

Globally, wrap‐up time represents 28% of call handle time. When we also take into account the unique nature of policing

and the fact that there must be idle time built in to enable citizens to get through for Emergency calls, this figure looks

surprisingly realistic.

Again, it is suggested that it would be good to conduct a contact observation exercise to determine if wrap‐time could be

reduced.

Best practice is represented by the Service Providers and Telecommunications sector with a score of 64% in the 2008 Global

Contact Centre Benchmark Report.

Staff Attrition (% annual agent turnover)

This measures the percentage of Contact Centre agents that leave their role in a year.

Contact centres tend to be high‐turnover environments for staff, with 27% attrition globally. There is often no career path

for agents, and many agents are employed on temporary contracts. In some areas there is huge competition for staff, so

agents regularly move from one Contact Centre to another as a new Centre opens offering a slight increase in hourly pay.

The UK fares worse at 29% which is a major concern for the UK Contact Centre industry. The costs associated with staff

turnover are huge, such as training, recruitment and time taken to become effective. These are all large cost drivers in

Contact Centres, where typically 70% of costs are directly in agent salaries, training and recruitment.

Public Sector is generally better at 17% representing Best practice across all sectors in the 2008 Global Contact Centre

Report, and it is pleasing to see Police Forces with attrition down at 12%. It is always good to have some movement, with

people flowing between different parts of the organisation, and some people leaving and new blood joining. This is

18

National Police Contact Management Benchmarking Report 2008

sustainable at the 12% indicated by Police Forces and represents good practice in the UK contact centre industry. It tends to

indicate that Police Contact Centres are viewed as attractive places to work.

Effective resource planning and forecasting of attrition play a key role in having the right people at the right time to deal

with demands for service. This will result in lower abandoned call rates and decreased agent idle time which in turn can

have a positive impact upon both staff moral and cost.

Staff Absenteeism (% annual agent absenteeism)

This measures the amount of time that agents are absent when they are scheduled for a shift. This includes short‐term

unplanned sickness, but excludes long‐term planned absences.

Absenteeism varies significantly by country with UK better than the global average, although 7% means that agents are

absent for 15 days a year, which is poor compared to other industries.

It is interesting to think about illness and absenteeism on a global basis. Perhaps one should expect much higher numbers

in 3rd world countries, where agents are often affected by social issues (such as AIDS, gang masters and basic transportation

issues). A 2 hour commute each way in the middle of the night to match US or European time zones is not unusual in some

parts of the world.

Police Contact Centre absenteeism is similar to the Public Sector average of 8%. This could be improved and it is suggested

that absenteeism should be investigated to determine if there are reasons for Police Forces to be higher than their

commercial counterparts. Absenteeism represents a large direct and indirect cost to the Contact Centre leading to

unnecessarily increased staffing levels, and needs focus on motivation and satisfaction initiatives to resolve.

Best practice is represented by the Utilities and Energy sector with a score of 6% in the 2008 Global Contact Centre

Benchmark Report.

Abandoned Call Rate (% calls abandoned)

This measures the number of calls abandoned when they have been put through to an agent queue and where one typically

listens to music or “please wait” messages.

Globally, 14% of calls are abandoned whilst waiting to speak to an agent. The abandon rate gives a clear indication of an

organisation’s service levels in response to customers’ calls and their ability to effectively apply routing and channel

strategies to meet volume demands.

UK tends to provide a better service, but it is clear that Contact Centres still have some way to go to meet customers’

expectations; well over one in ten customers give up. This is last year’s number since the 2008 data has not been calculated

at the time of publishing.

Public Sector’s service ethos shows through clearly, with abandon rate down at 9% and Financial Services at 4%. Police

Forces show a very good, low score of 3.6%, which is likely caused by three factors:

• Emergency callers are answered very quickly and are extremely unlikely to hang up.

• Callers are prepared to wait to speak to someone in a Police Contact Centre, whether for Emergency on Non‐

emergency calls.

• There is a lower expectation of how quickly a call is answered in Public Sector compared to many commercial

organisations, such as banks.

Best practice across all sectors is represented by Police Service with a score of 3.6%.

19

National Police Contact Management Benchmarking Report 2008

Speed‐to‐answer (% calls answered in 20 seconds)

This measures the number of calls answered within 20 seconds of reaching the agent queue. This metric, together with

Abandoned Call Rate and First Contact Resolution are the key drivers of Customer Satisfaction. Speed to Answer is often is

impacted by Agent Utilisation; the more free time for agents, the more likely someone is available to answer a call when it

arrives.

The Global average across all sectors is 69%, meaning that almost one third of customers’ calls are kept waiting longer that

20 seconds.

UK does very well at 81% with Public sector a little behind at 74%.

In the police forces, this is 79%, made up of a combination of Emergency calls, of which 95% are answered in 20 seconds

and Non‐emergency calls at 76%. It should be noted that police forces currently measure their speed to answer in 10

seconds (Emergency calls), 30 seconds (Non‐emergency calls) and 40 seconds (one stop shop). Best practice is represented

by the Travel and Transportation sector with a score of 83% in the latest published Global Contact Centre Benchmark

Report.

Overall Conclusion

The results of this survey paint a good picture for Police Force Contact Centres, with a number of observations and

recommendations for improvement being made. This represents a good baseline of the as is position for contact

management, enabling progress to be tracked and improvements measured.

20

National Police Contact Management Benchmarking Report 2008

Recommendations

Chapter 1 – Background

Recommendation 1.1

Forces should review the potential to share demand by means of integrated telephony and command and control systems

in order to achieve benefits of scale opportunities. This will further support business continuity and disaster recovery

needs.

Chapter 2 – Strategy and Development

Recommendation 2.1

Forces should review processes to improve First Contact Resolution and explore the use of self‐service mechanisms such as

Interactive Voice Response (IVR) and web self‐help to move Frequently Asked Questions (FAQs) and transactional processes

away from contact centre staff activity.

Recommendation 2.2

Forces should review commercial drivers to determine if service improvement and efficiency can be balanced within the

bounds of business objectives and regulations.

Recommendation 2.3

Forces should ensure that their contact centres apply National Intelligence Model (NIM) discipline and use a flow of

intelligence to develop and meet individual and corporate strategies.

Recommendation 2.4

Forces should integrate the customer experience into strategic objectives to support understanding of customers and their

behaviours.

Recommendation 2.5

The NPIA should, through the National Contact Management Programme, further explore the reasons why 14% of forces

have not implemented the national call grades and definitions as part of the ongoing NCHS review.

Chapter 3 – Financial Management and Rationale

Recommendation 3.1

Forces should review the use of technology to reduce call volumes into the Contact Centre and additionally review the use

of training to improve efficiency of call handling and First Contact Resolution. Technology changes should realise customer

benefits and or support staff in the delivery of customer service.

Recommendation 3.2

Forces should have a strategy in place to identify ways to reduce cost to serve or provide improved service at the same cost.

Recommendation 3.3

Forces should review (or in the absence of, develop) a channel strategy to explore the potential areas for self service. (Also

see Recommendation 6.1).

21

National Police Contact Management Benchmarking Report 2008

Chapter 4 – Customer Knowledge and Management

Recommendation 4.1

Forces should use call recording analysis and Contact Centre agent review sessions to improve knowledge and

understanding of customers. Agents have direct contact with the customer and will therefore have insight into their needs.

Recommendation 4.2

Forces should focus on continuing to improve satisfaction through the increased use of segmentation. Once segmented

groups have been identified, a range of different consultation methods may be used (surveys, focus groups, in‐depth

interviews with users etc) to gain Customer Insight regarding customer views of the services being provided and then an

appropriate strategy based on those demands can be formed.

Recommendation 4.3

Forces should ensure that they have a single view of the customer across channels, services, data / customer information

and transaction history to maximise customer satisfaction.

Chapter 5 – Performance Measurement and Metrics

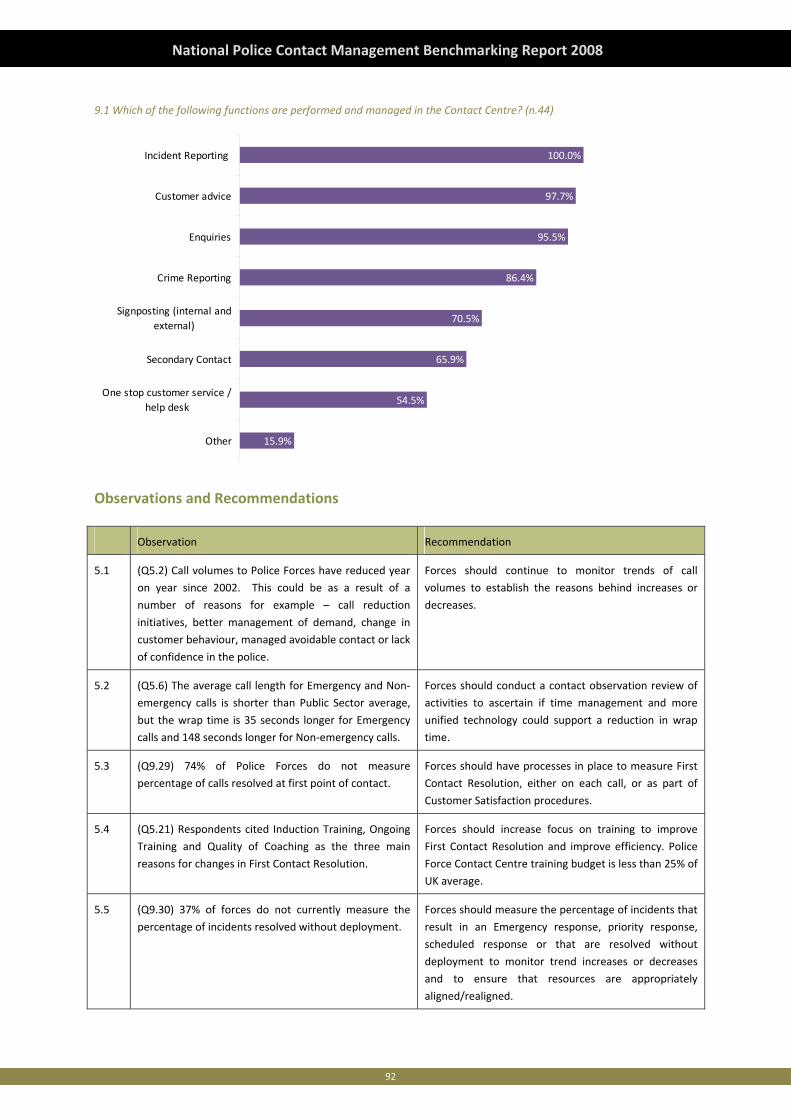

Recommendation 5.1

Forces should continue to monitor trends of call volumes to establish the reasons behind increases or decreases.

Recommendation 5.2

Forces should conduct a contact observation review of activities to ascertain if time management and more unified

technology could support a reduction in wrap time.

Recommendation 5.3

Forces should have processes in place to measure First Contact Resolution, either on each call, or as part of Customer

Satisfaction procedures.

Recommendation 5.4

Forces should increase focus on training to improve First Contact Resolution and improve efficiency. Police Force Contact

Centre training budget is less than 25% of UK average.

Recommendation 5.5

Forces should measure the percentage of incidents that result in an emergency response, priority response, scheduled

response or that are resolved without deployment to monitor trend increases or decreases and to ensure that resources

are appropriately aligned / realigned.

Chapter 6 – Processes and Procedures

Recommendation 6.1

Forces should develop a contact channel strategy to support consistency, tracking and customer experience.

Recommendation 6.2

Forces should benchmark, assess and accredit their contact centre(s) to ensure standards are maintained and to provide a

baseline to measure change against in the future.

22

National Police Contact Management Benchmarking Report 2008

Recommendation 6.3

Forces should review guidelines and prompts more frequently to ensure processes match business needs in a changing

environment. Current best practice suggests categorising guidelines and prompts and ensuring that they are reviewed in

terms of “shelf life” and changeability etc is critical to successful and relevant application. Current best practice suggests

reviewing within a maximum time frame of once per year.

Chapter 7 – Structure and Resource Management

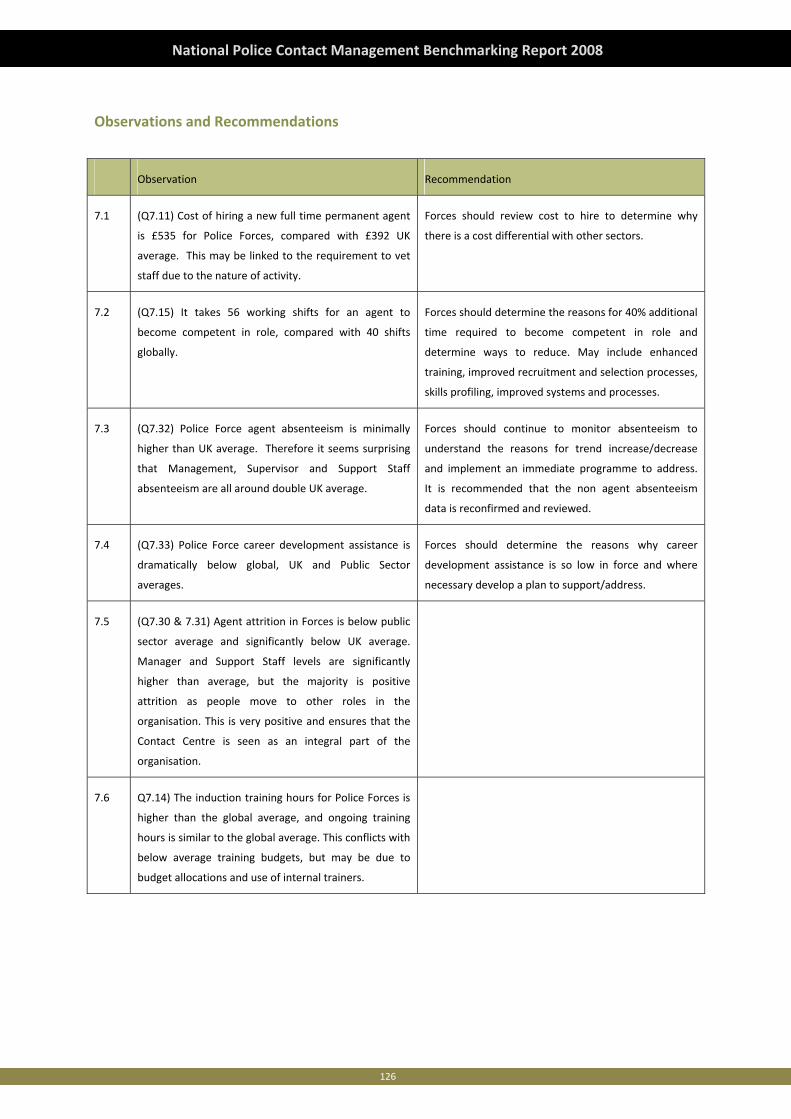

Recommendation 7.1

Forces should review cost to hire to determine why there is a cost differential with other sectors.

Recommendation 7.2

Forces should determine the reasons for 40% additional time required to become competent in role and determine ways to

reduce. May include enhanced training, improved recruitment and selection processes, skills profiling, improved systems

and processes.

Recommendation 7.3

Forces should continue to monitor absenteeism to understand the reasons for trend increase / decrease and implement an

immediate programme to address.

Recommendation 7.4

Forces should determine the reasons why career development assistance is so low in force and where necessary develop a

plan to support / address.

Chapter 8 – Technology Environment

Recommendation 8.1

Forces should ensure that Contact Centre IT is business critical and that they have robust Service Level Agreements in place

to maintain business continuity 24/7.

Recommendation 8.2

Forces should consider renting or hosting technology as it is typically better supported, more cost‐effective and future

proofed.

Recommendation 8.3

The NPIA should work with ACPO (IT & Communications) to revisit the potential for a national contact management

technology solution. In the absence of such a solution, ACPO and NPIA should ensure that a set of agreed system capability

standards are developed to help assist in force procurement decisions.

23

National Police Contact Management Benchmarking Report 2008

24

National Police Contact Management Benchmarking Report 2008

25

National Police Contact Management Benchmarking Report 2008

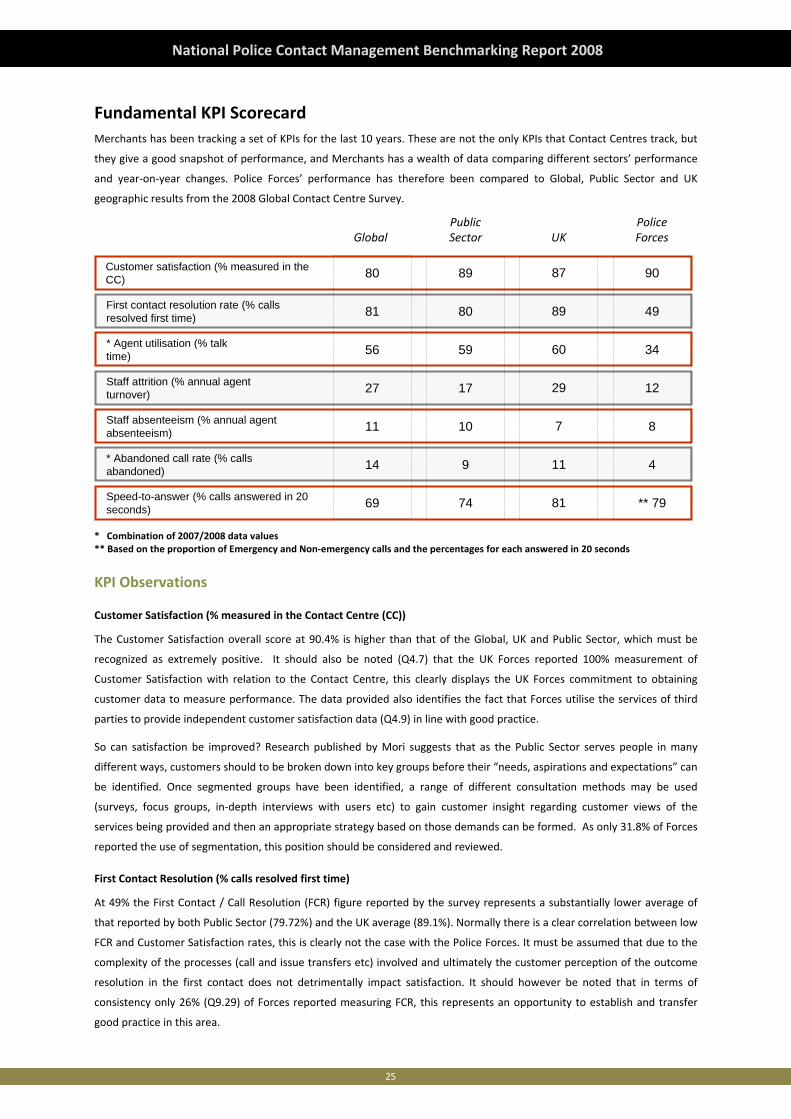

Fundamental KPI Scorecard Merchants has been tracking a set of KPIs for the last 10 years. These are not the only KPIs that Contact Centres track, but

they give a good snapshot of performance, and Merchants has a wealth of data comparing different sectors’ performance

and year‐on‐year changes. Police Forces’ performance has therefore been compared to Global, Public Sector and UK

geographic results from the 2008 Global Contact Centre Survey.

Customer satisfaction (% measured in the CC)

First contact resolution rate (% calls resolved first time)

* Agent utilisation (% talk time)

Staff attrition (% annual agent turnover)

Staff absenteeism (% annual agent absenteeism)

* Abandoned call rate (% calls abandoned)

Speed-to-answer (% calls answered in 20 seconds)

Public Sector

89

80

59

17

10

9

74

Global

80

81

56

27

11

14

69

UK

87

89

60

29

7

11

81

Police Forces

90

49

34

12

8

4

** 79

* Combination of 2007/2008 data values ** Based on the proportion of Emergency and Non‐emergency calls and the percentages for each answered in 20 seconds

KPI Observations

Customer Satisfaction (% measured in the Contact Centre (CC))

The Customer Satisfaction overall score at 90.4% is higher than that of the Global, UK and Public Sector, which must be

recognized as extremely positive. It should also be noted (Q4.7) that the UK Forces reported 100% measurement of

Customer Satisfaction with relation to the Contact Centre, this clearly displays the UK Forces commitment to obtaining

customer data to measure performance. The data provided also identifies the fact that Forces utilise the services of third

parties to provide independent customer satisfaction data (Q4.9) in line with good practice.

So can satisfaction be improved? Research published by Mori suggests that as the Public Sector serves people in many

different ways, customers should to be broken down into key groups before their “needs, aspirations and expectations” can

be identified. Once segmented groups have been identified, a range of different consultation methods may be used

(surveys, focus groups, in‐depth interviews with users etc) to gain customer insight regarding customer views of the

services being provided and then an appropriate strategy based on those demands can be formed. As only 31.8% of Forces

reported the use of segmentation, this position should be considered and reviewed.

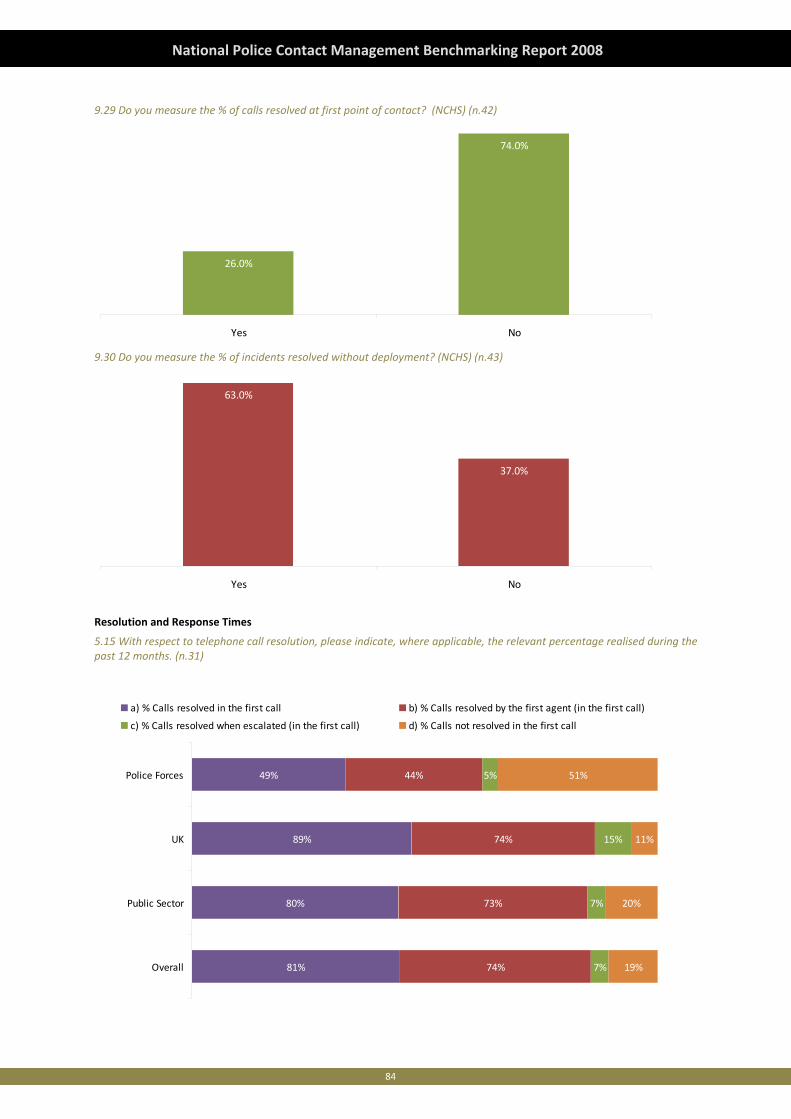

First Contact Resolution (% calls resolved first time)

At 49% the First Contact / Call Resolution (FCR) figure reported by the survey represents a substantially lower average of

that reported by both Public Sector (79.72%) and the UK average (89.1%). Normally there is a clear correlation between low

FCR and Customer Satisfaction rates, this is clearly not the case with the Police Forces. It must be assumed that due to the

complexity of the processes (call and issue transfers etc) involved and ultimately the customer perception of the outcome

resolution in the first contact does not detrimentally impact satisfaction. It should however be noted that in terms of

consistency only 26% (Q9.29) of Forces reported measuring FCR, this represents an opportunity to establish and transfer

good practice in this area.

26

National Police Contact Management Benchmarking Report 2008

Agent Utilisation (% talk time)

Agent utilised talk time is substantially lower at 34.45% than the National UK average of 49.1%, in isolation this would

normally be expected to represent a negative impact on both service realisation and cost. However, when reviewed

alongside the average after call work or “wrap” time, which is high at 3 minutes 10 seconds compared to the UK average of

50 seconds (Q9.21), it becomes clearer that post call activity is complex or hampered by technology / process constraints.

The provided data also identified greatly varying times in terms of individual Forces “wrap” times. It would seem prudent to

identify those Forces where lower after call handling is being experienced and look to leverage the enablers of this in terms

of process or technology good practice.

Staff Attrition (% annual agent turnover)

The Survey has identified that the Forces overall report an average attrition rate in the Contact Centre area of only 12%

verses a UK average of 29%. This is extremely positive, as it presumes that the environment, working conditions and career

prospects within the Contact Centre are producing a stable platform for staff retention. This is supported for example by

the fact that for although Management attrition is higher at 18% than the 5% UK average for this role (Q7.30), over 54% of

this is as a result of internal promotion, as opposed to only 12% as the UK average (Q7.31).

Staff Absenteeism (% annual agent absenteeism)

Staff absenteeism is 8%, which is in line with the Public Sector generally but minimally higher than the UK average at 7%. It

should however be noted that the proportion of long term absenteeism is much higher at 32% than the UK 17%, this may

be due to the way Forces report intervals of absenteeism. Conversely the Short Term figure is 55% as opposed to 65% UK

average, which would indicate that investigation into the reporting mechanisms needs consideration.

Abandoned Call (% calls abandoned)

The overall percentage of calls abandoned has been calculated based on Combination of 2007/2008 data values. At 4% this

is dramatically lower than the UK average at 11% and the Public Sector average at 9%. It would be expected for this overall

figure to be substantially lower due to the number of Emergency calls received and the SLA’s required for the handling of

these calls. It should also be noted however that on average calls are abandoning in 16 seconds (Q5.5) as opposed to longer

hold times before a caller abandons as the UK average of 27 seconds and 26 in the Public Sector once connected to an

agent queue. This again probably linked to the nature of the call types and may be a driver of repeat calls which will drive

up both the abandon rate and call volumes. It would possibly be worth further investigating in more detail the types of call

that abandon and finding the correlation between these and repeat calls. In summary the Forces are however maintaining

excellent call abandon rates.

Speed‐to‐answer (% calls answered in 20 seconds)

The overall percentage of speed to answer has been calculated based on the proportion of Emergency and Non‐emergency

calls and the percentages for each answered in 20 seconds. For Emergency calls it is 12 seconds against a UK average of 21

seconds (Q5.6) and for Non‐emergency it is 26 seconds as opposed to 21 UK average (Q9.21). It should however be noted

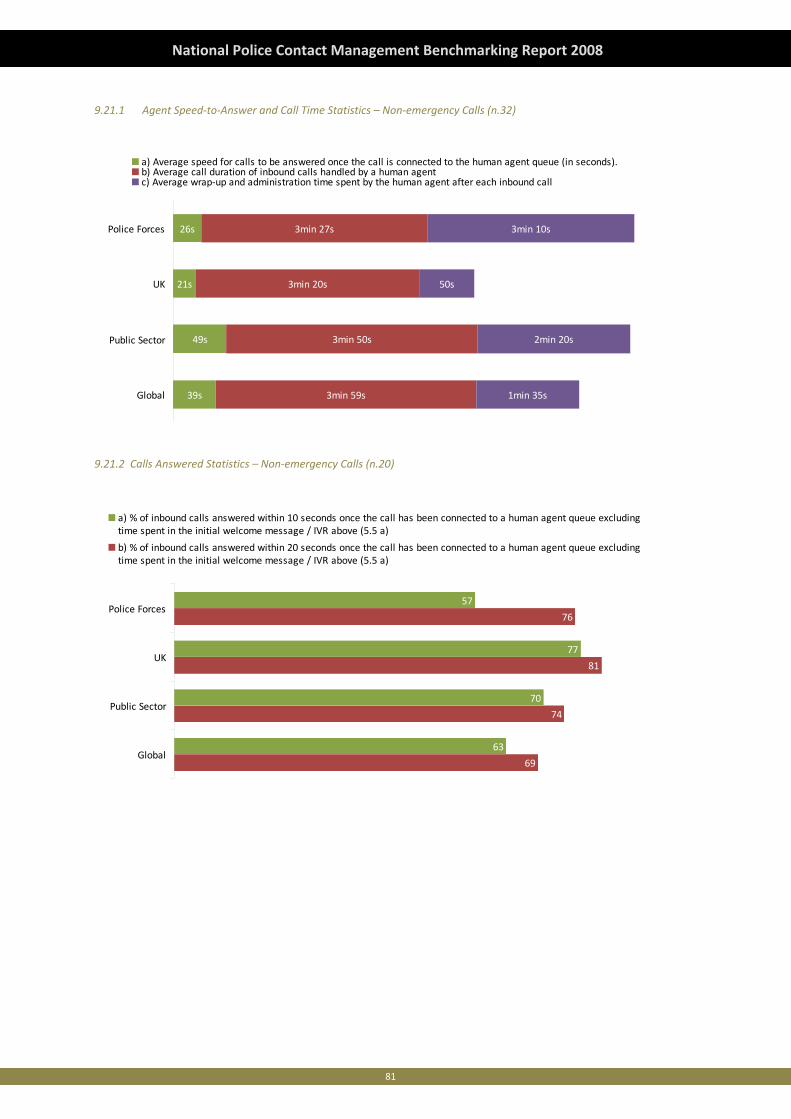

that when looking specifically at Non‐emergency calls answered in 10 and 20 seconds the averages are 57 and 76 seconds

respectively (Q9.21). The UK average for these time frames are 77 and 81 seconds respectively. As Non‐emergency calls

represent a large percentage of the call volumes it would seem prudent to review this area in more detail within the

context of balancing Emergency and Non‐emergency call types and weighting. One observation regarding a possible area

for increasing agent availability therefore impacting service levels is that of average “wrap time” (post call handling) which

for Non‐emergency calls is 3 minutes 10 seconds opposed to the UK average of 50 seconds for similar call talk time

durations (Q9.21) as previously discussed under Agent Utilisation.

27

National Police Contact Management Benchmarking Report 2008

28

National Police Contact Management Benchmarking Report 2008

29

National Police Contact Management Benchmarking Report 2008

Chapter 1: Background Information

Introduction

Chapter 1 evaluates the scale and size of the forces contact centre operations, providing an overall view of the average

number of sites and seats across all forces. The section includes:

1. Organisational Details

2. Contact Centre Details

Findings

Organisation Details

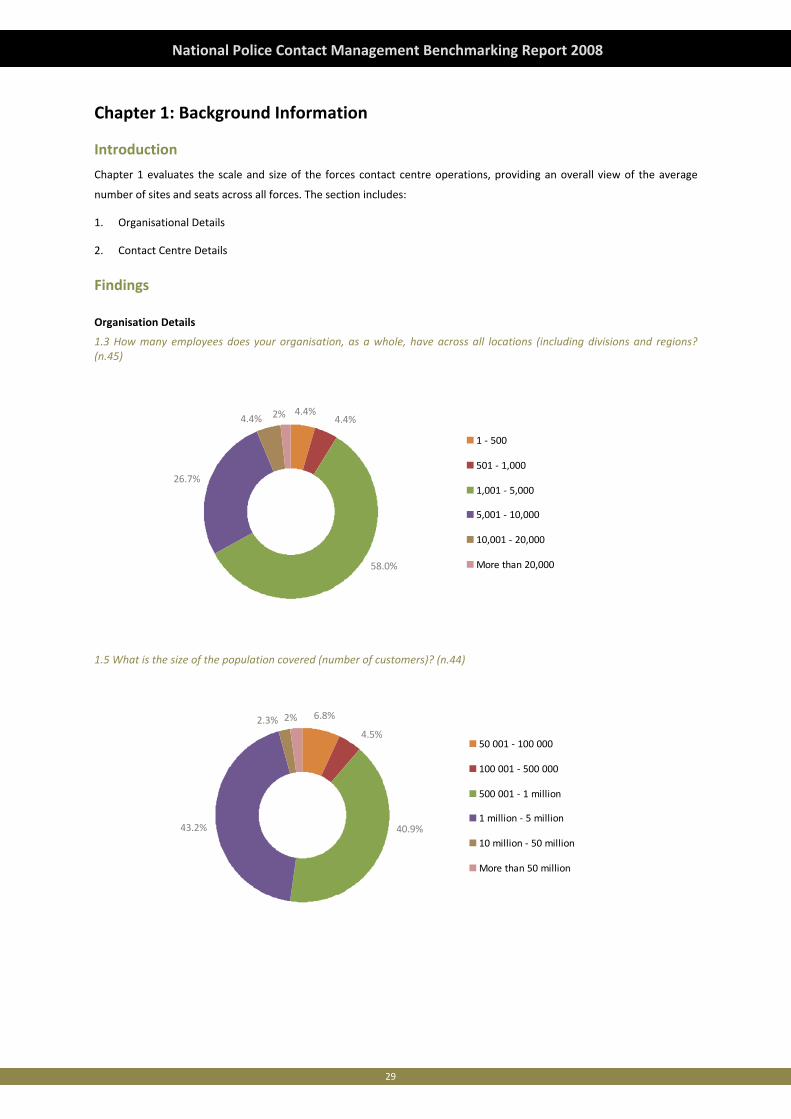

1.3 How many employees does your organisation, as a whole, have across all locations (including divisions and regions? (n.45)

4.4%4.4%

4.4% 2%

58.0%

26.7%

1 ‐ 500

501 ‐ 1,000

1,001 ‐ 5,000

5,001 ‐ 10,000

10,001 ‐ 20,000

More than 20,000

1.5 What is the size of the population covered (number of customers)? (n.44)

4.5%

6.8%2.3% 2%

40.9%43.2%

50 001 ‐ 100 000

100 001 ‐ 500 000

500 001 ‐ 1 million

1 million ‐ 5 million

10 million ‐ 50 million

More than 50 million

30

National Police Contact Management Benchmarking Report 2008

Contact Centre Details

1.6 How many contact centre operations does your organisation have? (n.45)

8

7

6

3

0 1 2 3 4 5 6 7 8 9

Global

Public Sector

UK

Police Forces

1.7 How many contact centre seats are there in total across all your organisation’s contact centres? (n.45)

934

446

822

83

0 100 200 300 400 500 600 700 800 900 1000

Global

Public Sector

UK

Police Forces

Observations and Recommendations

Observation Recommendation

1.1 (Q1.8) Police Contact Centres average 83 seats,

compared to UK average of 822 seats and Public Sector

average of 446 seats.

Forces should review the potential to share demand by

means of integrated telephony and command and

control systems in order to achieve benefits of scale

opportunities. This will further support business

continuity and disaster recovery needs.

31

National Police Contact Management Benchmarking Report 2008

32

National Police Contact Management Benchmarking Report 2008

33

National Police Contact Management Benchmarking Report 2008

Chapter 2: Strategy and Development

Introduction

In this chapter, we review the research regarding customer management strategy, its people and processes. The results of

the Global Benchmarking Report give us a clear insight into industry and regional trends and will help in evaluating the

performance of your contact centre. We look at the evolving patterns and industry trends for:

a. Business strategy and drivers

b. Location strategy

c. Operating models and implementation options

d. Organisational strategy, maturity and development

e. Channel use and strategy

Global Perspective

Putting the centre at the centre

Contact centres continue to gain strategic ground within organisations. They are now finding themselves increasingly

integrated into core business objectives and not simply as standalone functions. Driving business outcomes is mission

critical for contact centres which are growing in value and importance to businesses.

In light of fast‐paced technology and the electronic communications age we find ourselves in, operations are continuing to