NATIONAL OVERVIEW 2014 ENERGY MARKET PERSPECTIVE Neil Copeland Management Consulting Division

NATIONAL OVERVIEW 2014 ENERGY MARKET PERSPECTIVE Neil CopelandManagement Consulting Division.

Dec 26, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

NATIONAL OVERVIEW 2014ENERGY MARKET PERSPECTIVE

Neil Copeland Management Consulting Division

2

BLAC

K &

VEA

TCH

CO

NFI

DEN

TIAL

—FO

R CL

IEN

T’S

INTE

RNAL

USE

ON

LY—

SECO

NDA

RY D

ISTR

IBU

TIO

N P

ROH

IBIT

ED

About the Black & Veatch Energy Market Perspective

.

The EMP is available as a National Service or as one or more regional services: Western, Texas (ERCOT), Northeast, Midwest and Southeast.

EMP North American Market Coverage

Black & Veatch EMP: 2014 Outlook

3

BLAC

K &

VEA

TCH

CO

NFI

DEN

TIAL

—FO

R CL

IEN

T’S

INTE

RNAL

USE

ON

LY—

SECO

NDA

RY D

ISTR

IBU

TIO

N P

ROH

IBIT

EDBlack & Veatch EMP: 2014 Outlook

Top 7 Electric Industry Issues

20

12

ST

RA

TE

GIC

DIR

EC

TIO

NS

SU

RV

EY

3Reliability, environmental regulation, and economic regulation are the top issues industry-wide

4

BLAC

K &

VEA

TCH

CO

NFI

DEN

TIAL

—FO

R CL

IEN

T’S

INTE

RNAL

USE

ON

LY—

SECO

NDA

RY D

ISTR

IBU

TIO

N P

ROH

IBIT

ED

Black & Veatch Outlook on U.S. Power Demand

• Growth of 1.6% annually from 2014-2016, before reverting to a long-term growth trend of about 1.0% per year

Source: EIA, Black & Veatch Energy Market Perspective Analysis

20082009

20102011

20122013

20142015

20162017

20182019

20202021

20222023

20242025

-

100

200

300

400

500

600

700

800

900

1,000

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

Peak Demand - United StatesCoincident Peak Demand (GW) Annual Growth Rate (%)

Coin

ciden

t Pea

k De

man

d (G

W)

Annu

al G

row

th ra

te (%

)

Black & Veatch EMP: 2014 Outlook

5

BLAC

K &

VEA

TCH

CO

NFI

DEN

TIAL

—FO

R CL

IEN

T’S

INTE

RNAL

USE

ON

LY—

SECO

NDA

RY D

ISTR

IBU

TIO

N P

ROH

IBIT

ED

5

Black & Veatch EMP: 2014 Outlook

Natural Gas; 352,226

Nuclear; 97,393 Coal; 293,597

Hydro & Other Re-

newables; 112,175

Wind; 67,681 Solar; 12,815

Coal (IGCC); 1,709

Other Steam Turbine; 86,246

34%

10%29%

11%

7%1%0%

8%

Natural Gas; 717,028

Nuclear; 61,137

Coal; 162,885

Hydro & Other Re-

newables; 113,324

Wind; 133,321

Solar; 39,227

Coal (IGCC); 5,166 Other Steam Turbine; 50,126

56%

5%

13%

9%

10%

3%0%4%

CAPACITY MIX (MW) IN 2014 CAPACITY MIX (MW) IN 2038

Capacity represents the total amount of electricity that can be produced.

The Changing Capacity Mix: Where U.S. energy will come from

6

BLAC

K &

VEA

TCH

CO

NFI

DEN

TIAL

—FO

R CL

IEN

T’S

INTE

RNAL

USE

ON

LY—

SECO

NDA

RY D

ISTR

IBU

TIO

N P

ROH

IBIT

ED

6

Black & Veatch EMP: 2014 Outlook

ENERGY MIX (GWh) IN 2014 ENERGY MIX (GWh) IN 2038

Energy mix refers to total electricity consumed and where that electricity came from.

Natural Gas;

1,048,284

Nuclear; 773,764

Coal; 1,596,070

Other Steam

Turbine; 63,899

Wind; 185,157

Solar; 23,982

Hydro & Other Re-newables; 356,139 Coal (IGCC); 10,519

26%

19%39%

2%5%

1%9% 0%

Natural Gas; 2,705,297

Nuclear; 486,210

Coal; 1,079,001

Other Steam

Turbine; 39,076

Wind; 416,767

Solar; 123,609

Hydro & Other Re-newables; 371,286 Coal (IGCC); 40,879

51%

9%

21%

1%

8%

2%7%1%

The Changing U.S. Energy Mix

7

BLAC

K &

VEA

TCH

CO

NFI

DEN

TIAL

—FO

R CL

IEN

T’S

INTE

RNAL

USE

ON

LY—

SECO

NDA

RY D

ISTR

IBU

TIO

N P

ROH

IBIT

ED

Black & Veatch forecasts additional 86.2 GW of coal-fueled generator retirements by 2038

• Continuing trend in retirement of smaller, older coal-fired assets through 2020

• Forecasted retirements driven primarily by low-cost natural gas prices and EPA hazardous air pollutant requirements

• Future Green House Gas emission regulations could materially alter projections

Coal Unit Retirements Forecasted at 60.1 GW by 2020

Source: Black & Veatch

Black & Veatch EMP: 2014 Outlook

7

8

BLAC

K &

VEA

TCH

CO

NFI

DEN

TIAL

—FO

R CL

IEN

T’S

INTE

RNAL

USE

ON

LY—

SECO

NDA

RY D

ISTR

IBU

TIO

N P

ROH

IBIT

ED

West County Energy Center, Fla.

Coal retirements and decline in regional reserve margins will drive continued capacity growth

• Power sector demand for gas expected to grow 3.1% annually

• More than 364,000 MW of new gas capacity is expected before 2038

• Technology advances, clean air initiatives drive growth

Natural Gas-Fueled Generation Will Continue to Grow

Source: Black & Veatch

Black & Veatch EMP: 2014 Outlook

8

9

BLAC

K &

VEA

TCH

CO

NFI

DEN

TIAL

—FO

R CL

IEN

T’S

INTE

RNAL

USE

ON

LY—

SECO

NDA

RY D

ISTR

IBU

TIO

N P

ROH

IBIT

ED

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 $-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

Henry Hub Natural Gas Spot PriceHistorical (Nominal) B&V Projection (Mid-Year 2013) B&V Projection (Year End 2013) EIA AEO 2013

2013

$/M

MBt

uNatural Gas Price Forecast

2013-2017Growth in low-cost supplies

dampens price growth

2017-2022Price growth is driven by LNG exports, coal capacity retirements, and GHG legislation

Black & Veatch EMP: 2014 Outlook

10

BLAC

K &

VEA

TCH

CO

NFI

DEN

TIAL

—FO

R CL

IEN

T’S

INTE

RNAL

USE

ON

LY—

SECO

NDA

RY D

ISTR

IBU

TIO

N P

ROH

IBIT

ED

New England price spikes in winter signal infrastructure constraints

Black & Veatch EMP: 2014 Outlook

11

BLAC

K &

VEA

TCH

CO

NFI

DEN

TIAL

—FO

R CL

IEN

T’S

INTE

RNAL

USE

ON

LY—

SECO

NDA

RY D

ISTR

IBU

TIO

N P

ROH

IBIT

ED

Major Pipeline Constraint Points During Peak Winter in New England

Iroquois Gas TransmissionMaritimes & Northeast

Portland Natural GasTennessee Gas Pipeline

Algonquin Gas Transmission

Tennessee 300 Line

Algonquin G System/J Loop

Tennessee 200 Line

M&NE and TGP Dracut

Pipeline Constraint Points

• Winter pipeline constraints exist due to a lack of market area storage and growing peak residential, commercial, and power generation demand

• During last week’s winter storm, regional natural gas prices reached above $40.00/MMBtu while Gulf Coast prices remained at $4.00/MMBtu

Black & Veatch EMP: 2014 Outlook

12

BLAC

K &

VEA

TCH

CO

NFI

DEN

TIAL

—FO

R CL

IEN

T’S

INTE

RNAL

USE

ON

LY—

SECO

NDA

RY D

ISTR

IBU

TIO

N P

ROH

IBIT

ED

Planned U.S. Pipeline Projects Highlight Constraints on the System

Source: EIA, March, 2013

Over 50% of 2012 projects are in theNortheast U.S.

13

BLAC

K &

VEA

TCH

CO

NFI

DEN

TIAL

—FO

R CL

IEN

T’S

INTE

RNAL

USE

ON

LY—

SECO

NDA

RY D

ISTR

IBU

TIO

N P

ROH

IBIT

ED

Lopburi 55 MW Solar Farm - Thailand

Renewable capacity additions are driven by state Renewable Portfolio Standards requirements

• In the short term, the status of tax incentives for wind looms in the political arena

• ~93,200 MW of new capacity additions anticipated by 2038

• Wind will make up majority of new capacity additions

• Solar capacity expected to grow as a result of technology advances

Renewable Energy Growth Will Continue

Source: Black & Veatch

Black & Veatch EMP: 2014 Outlook

13

14

BLAC

K &

VEA

TCH

CO

NFI

DEN

TIAL

—FO

R CL

IEN

T’S

INTE

RNAL

USE

ON

LY—

SECO

NDA

RY D

ISTR

IBU

TIO

N P

ROH

IBIT

ED

Trajectory of Renewables Growth

Source: Black & Veatch Energy Market Perspective Analysis

15

BLAC

K &

VEA

TCH

CO

NFI

DEN

TIAL

—FO

R CL

IEN

T’S

INTE

RNAL

USE

ON

LY—

SECO

NDA

RY D

ISTR

IBU

TIO

N P

ROH

IBIT

EDBlack & Veatch EMP: 2013 Outlook

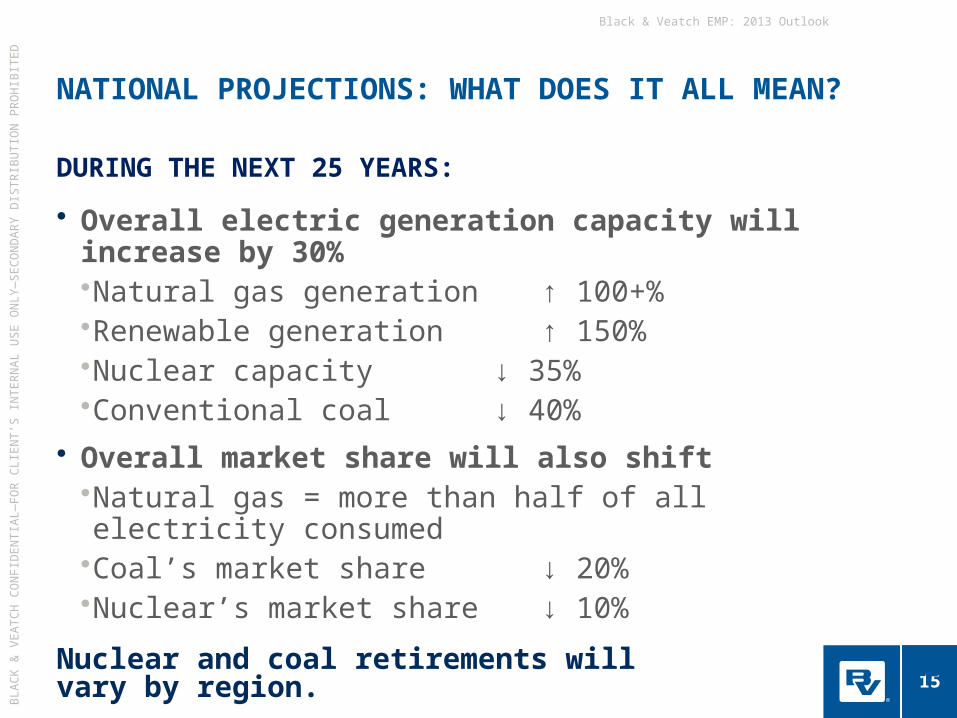

• Overall electric generation capacity will increase by 30%•Natural gas generation ↑ 100+%•Renewable generation ↑ 150%•Nuclear capacity ↓ 35%•Conventional coal ↓ 40%

• Overall market share will also shift•Natural gas = more than half of all electricity consumed•Coal’s market share ↓ 20%•Nuclear’s market share ↓ 10%

Nuclear and coal retirements will vary by region.

NATIONAL PROJECTIONS: WHAT DOES IT ALL MEAN?

DURING THE NEXT 25 YEARS:

15

Related Documents